Embed Size (px)

Citation preview

INDUSTRY REPORT | Consumer Electronics | December 7, 2010

TabletsTabletsTabletsTablets EpicenterEpicenterEpicenterEpicenter for for for for tttthe Convergence of he Convergence of he Convergence of he Convergence of Smartphones and PCsSmartphones and PCsSmartphones and PCsSmartphones and PCs

Report Author

William Kidd

Director,

Financial Services

© 2010 iSuppli Corporation. All Worldwide Rights Reserved. Confidential. Patents Pending | 1700 E. Walnut Avenue, El Segundo CA 90245 | Telephone: 310.524.4007 | Email: [email protected]

El Segundo, USA (HQ) Santa Clara, USA Scottsdale, USA Minnetonka, USA Hong Kong, China

Shanghai, China Shenzhen, China Hsin-Chu, Taiwan Tokyo, Japan Kyoto, Japan

Seoul, Korea Bracknell, United Kingdom Munich, Germany Herblay, France

Industry Report | Financial Services

`

� Although many devices have been labeled as convergent from a consumer perspective, tablets are unique in that they truly have brought once disparate industries together and as direct competitors. Tablets represent a significant challenge for many consumer electronics OEMs, since not all possess the tools to be successful, leaving many scrambling to develop a competent mobile O/S, as well as device, commerce and content ecosystems. In contrast with a smartphone O/S, a mobile O/S is capable of handling a broader set of CE devices (e.g., tablets, TVs, automobiles, etc) and range of uses, supported by more tailored/media-intensive UIs.

� We’ll soon see O/S and UIs developed specifically for tablets, highlighting an opportunity to out-innovate Apple. Although Apple has taken its smartphone O/S very far and impresses with interconnectivity, we believe the tablet user interface (UI) could undergo significant improvements. Thus, ample opportunities exist to innovate further with MeeGo and possibly later by Microsoft. Android’s tablet O/S is a wild card in terms of features.

� We don’t think many smartphone players are as ready for tablets as they imagine due to their lack of competitive commerce/content ecosystems. iTunes has taken years to built up its content/commerce portal, whereas most other smartphone players just have app stores. What may be acceptable to smartphone users isn’t likely to be the same for tablets, since the uses (e.g., watch movies, read newspapers) are so different.

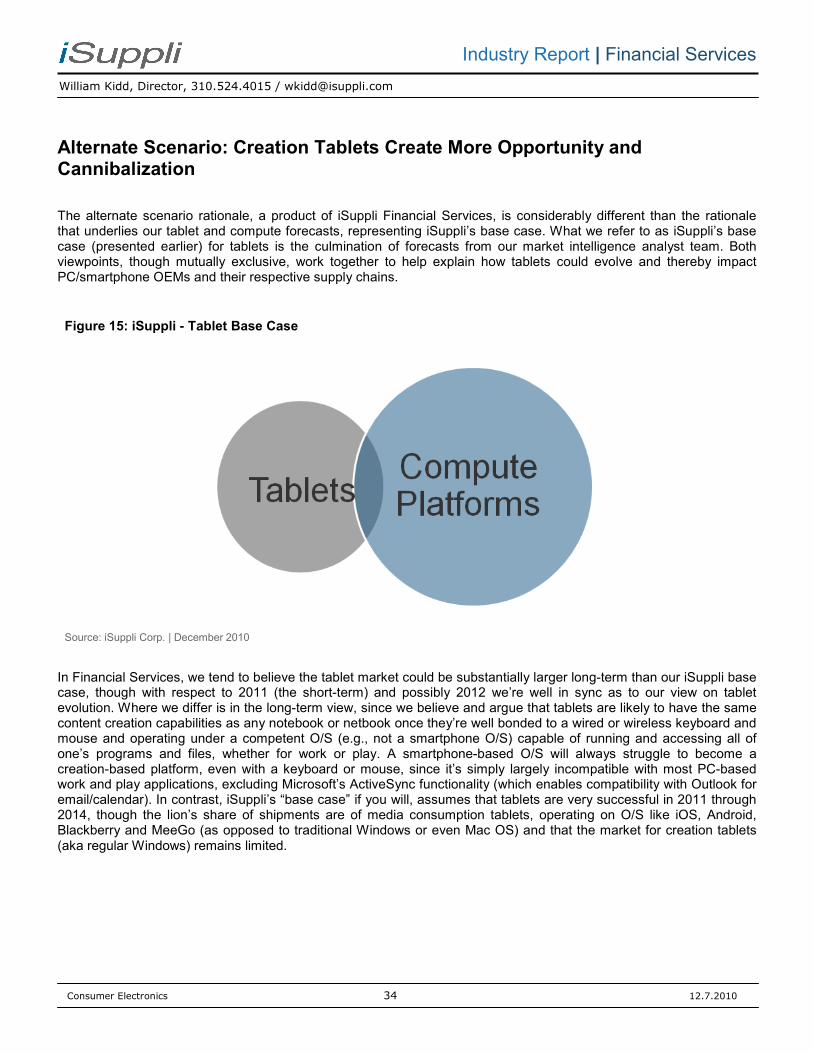

� We believe creation tablets will create both a larger market opportunity and more PC cannibalization than others forecast today. Our departure from conventional thinking stems from our belief that tablets (2-4 years out) will not only be able to retain their form factor advantages, but also possess notebook-like content creation capabilities when equipped with a competent O/S and a wireless keyboard/mouse. A smartphone-based O/S will always struggle to become a creation-based platform. Our creation position bolsters Microsoft’s competitive footing, believing that it still has a large role to play in tablets, whereas a consumption-centric view favors Apple and Android. With our creation tablet view, the overall market by definition has to be substantially larger than forecasts that assume largely consumption tablets, which represents an iPad-centric market evolution. Based on our view, PC makers should be able to improve their competitive position in tablets over time, since consumers would be purchasing a hardware solution that is essentially a new notebook form factor.

� We see the supply chain as a sound way of capturing broader technology themes, such as the growth in smart devices, mobility or even connectivity. However, for a tablet specific investment play, we prefer tablet OEMs, given the value of the O/S and ecosystem. Suppliers as a group tend to be more device diversified, lessening their reliance on tablet components. DRAM is a good example of this, though mobile DRAM has more tablet relevance (potentially 25% of demand in 2014). That said, tablets are likely important in spurring broader adoption of flash and SSD in other devices. Similarly, processor makers could leverage progress in tablets into other smart devices, whereas for Intel specifically, mobile competition make tablets more of a threat than an opportunity. For a few smaller players with narrow but strong product offerings, tablets alone can be meaningful. Atmel, a supplier of touch controllers to Android smartphones, may be one such example.

� Tablets are an early step in a larger CE revolution, where devices increasingly get smarter and possess greater commonality, empowered by a unifying O/S and more shared chipsets. Thus, hardware and software similarity will exist in devices that previously had none. Homes, even faster than lifestyles, have always evolved with technology, from coffee makers to microwaves to Wi-Fi, and we expect the near future to be no different. We believe TVs (by bringing them under a converged mobile O/S with relevant and new apps) are probably the next important catalyst in this evolution. We believe consumers will be drawn to a platform solution for their lives, adding TVs/cars initially and later exercise equipment, lighting/home security and other devices, beyond tablets and smartphones. Interconnected and integrated solutions will create new compelling functionality, which once in existence, will become a requisite. Android is surely an early favorite here.

Consumer Electronics

Tablets: Epicenter for the Convergence of Smartphones and PCs

William Kidd

Director 310.524.4015

December 7, 2010

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 2 12.7.2010

Industry Report | Financial Services

Table of Contents

I. Convergence and the Mobile O/S ............................................................................................................ 8

The Converged Mobile O/S ...................................................................................................................................... 8

O/S Framework Makes CE Devices More Compelling ......................................................................................... 10

The Dizzying Rate of Change ............................................................................................................................... 11

O/S Competitive Landscape ................................................................................................................................... 13

Nokia ..................................................................................................................................................................... 14

Microsoft and Windows Phone 7 .......................................................................................................................... 15

HP, Palm and WebOS .......................................................................................................................................... 17

Blackberry OS ....................................................................................................................................................... 17

Software vs. Hardware ............................................................................................................................................ 18

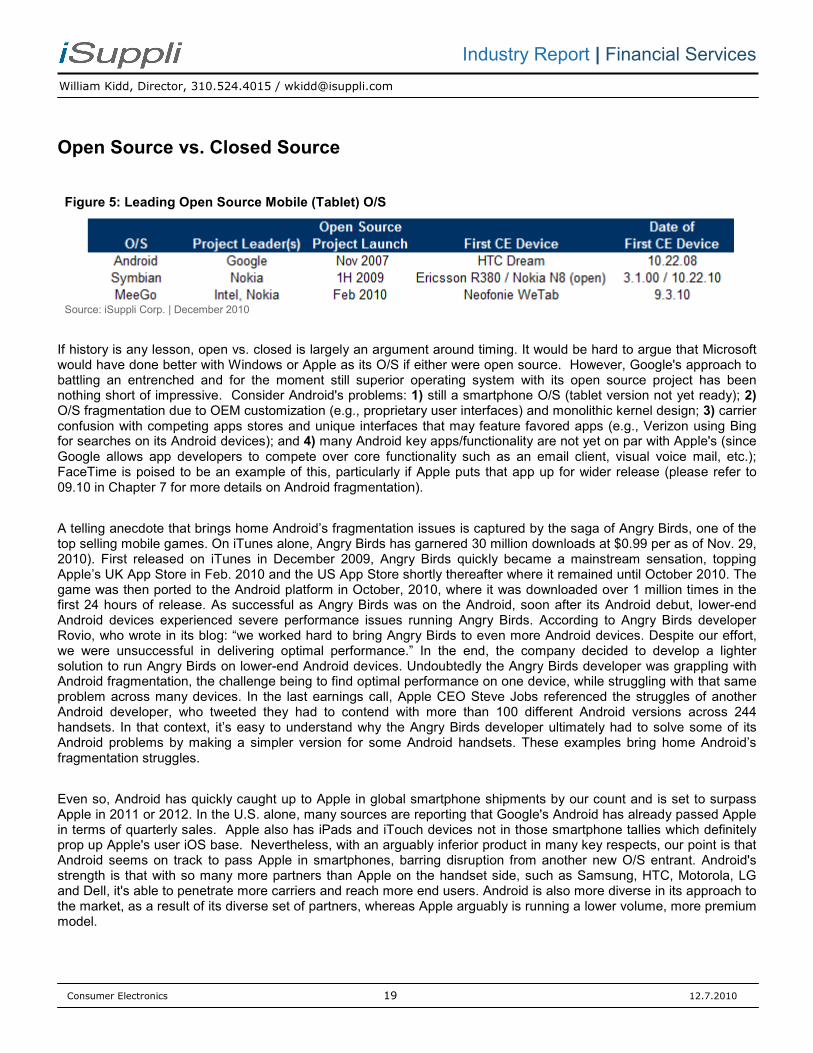

Open Source vs. Closed Source............................................................................................................................. 19

Interconnectivity ...................................................................................................................................................... 21

II. Ecosystems ........................................................................................................................................... 22

Commerce/Content Portals ..................................................................................................................................... 22

Smartphone ≠ Tablet .............................................................................................................................................. 24

III. Tablet Device Forecast ........................................................................................................................ 25

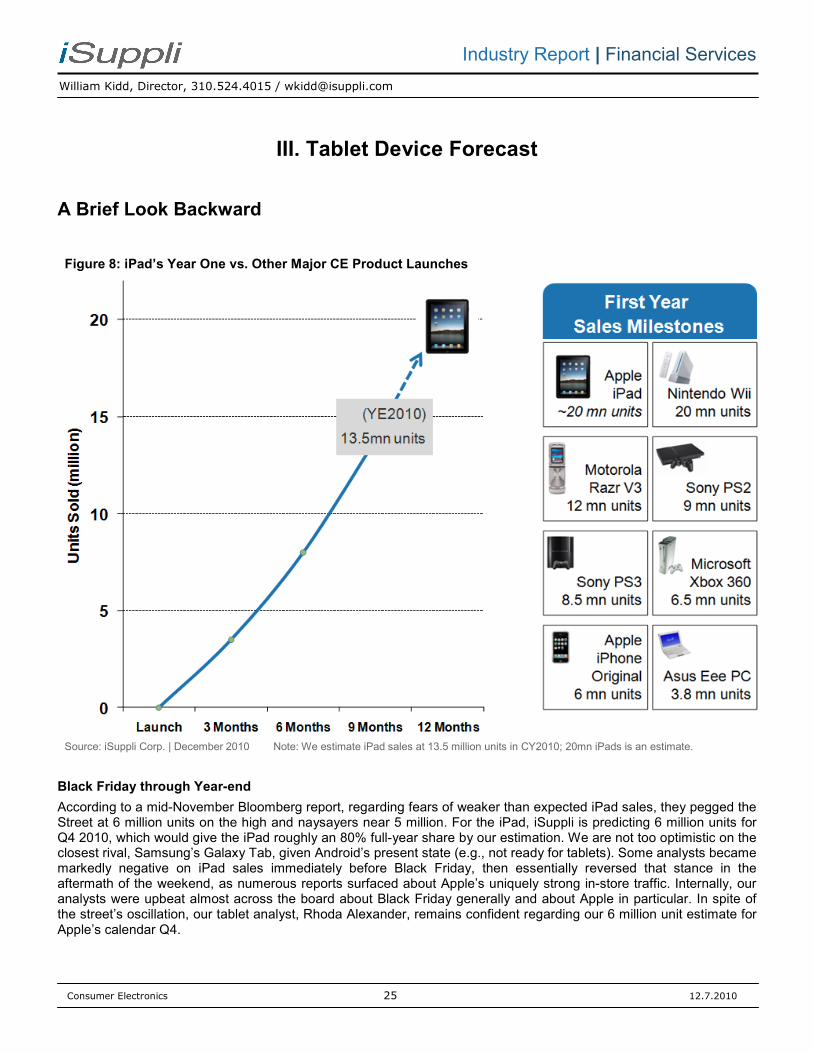

A Brief Look Backward ............................................................................................................................................ 25

Black Friday through Year-end ............................................................................................................................. 25

A Great iPad Start = Higher Expectations ............................................................................................................ 26

Forecast Rationale (Base Case): Media Tablets Are Very Successful, Modest PC Overlap ................................. 27

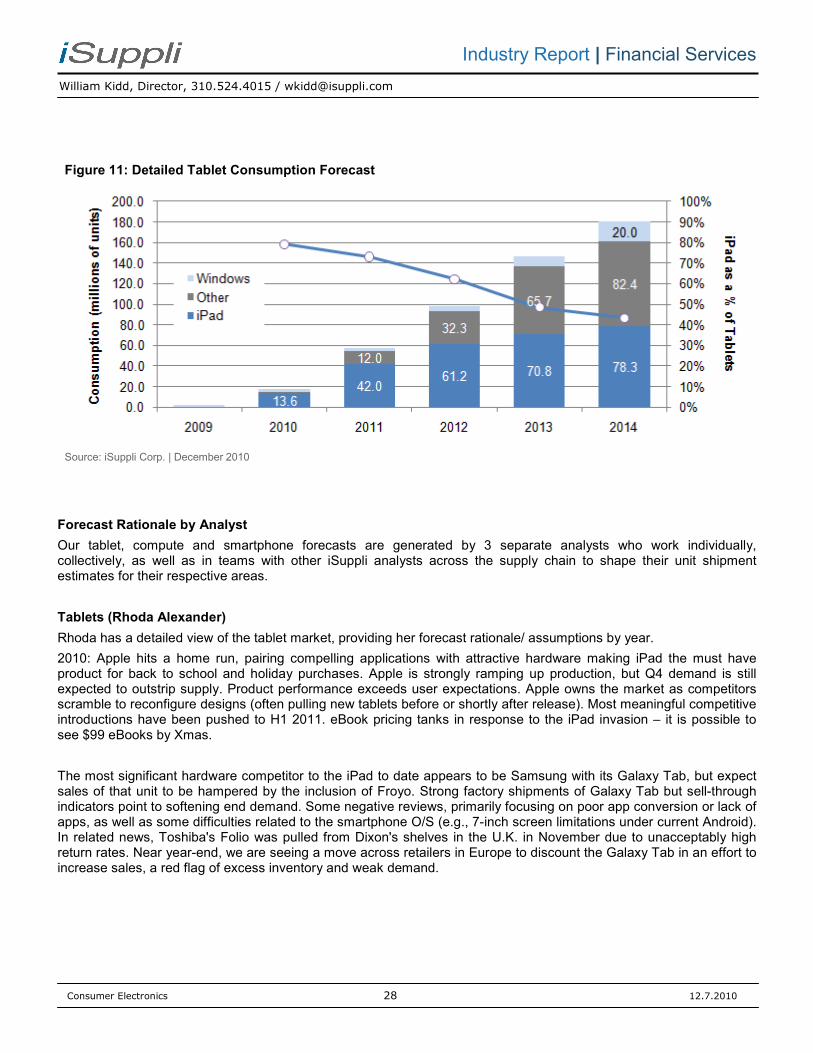

Tablets (Rhoda Alexander) ................................................................................................................................... 28

Compute Platforms (Matthew Wilkins) .................................................................................................................. 30

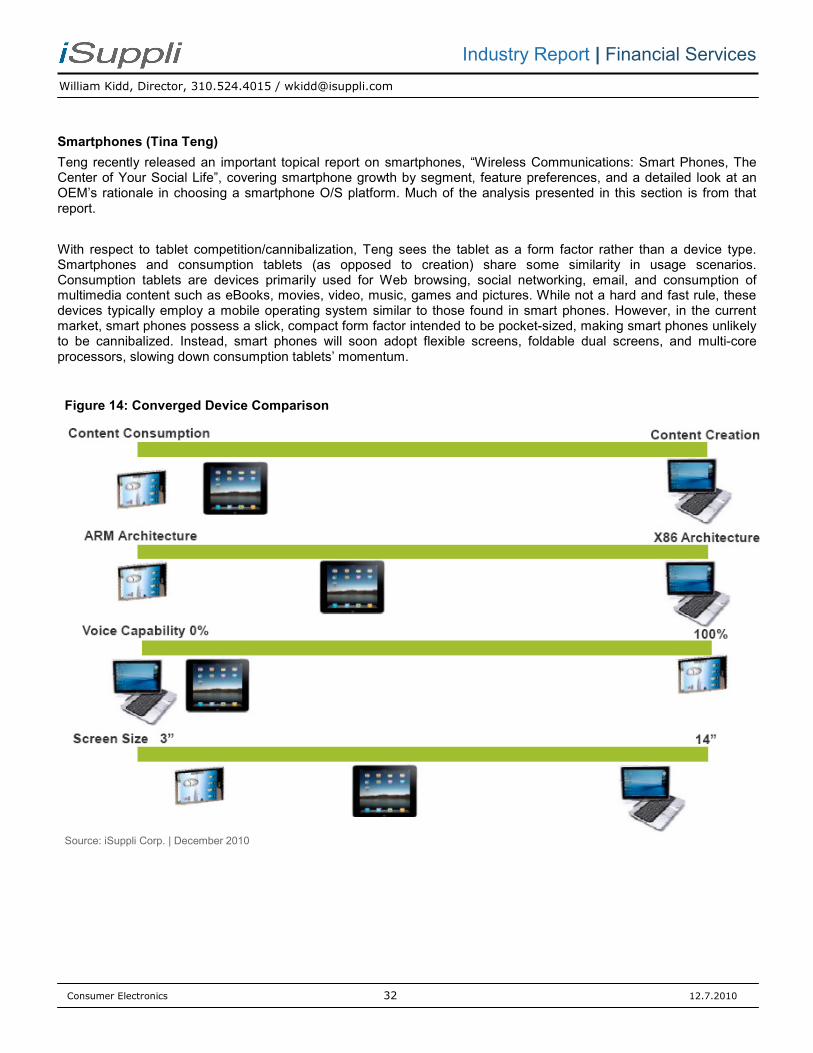

Smartphones (Tina Teng) ..................................................................................................................................... 32

Alternate Scenario: Creation Tablets Create More Opportunity and Cannibalization ............................................ 34

Where is the real opportunity? The Connected Life. .............................................................................................. 38

Compelling Data Points .......................................................................................................................................... 41

Supporting Data and Forecasts .............................................................................................................................. 43

Connected Devices ............................................................................................................................................... 43

Mobile Handsets ................................................................................................................................................... 44

Smartphones ......................................................................................................................................................... 44

Mobile Landscape ................................................................................................................................................. 46

IV. Insight from Teardowns ...................................................................................................................... 48

What separates a tablet from other devices? ......................................................................................................... 48

Apple’s New Design Paradigm: The User Experience Comes First ..................................................................... 48

The HMI Cost ........................................................................................................................................................ 50

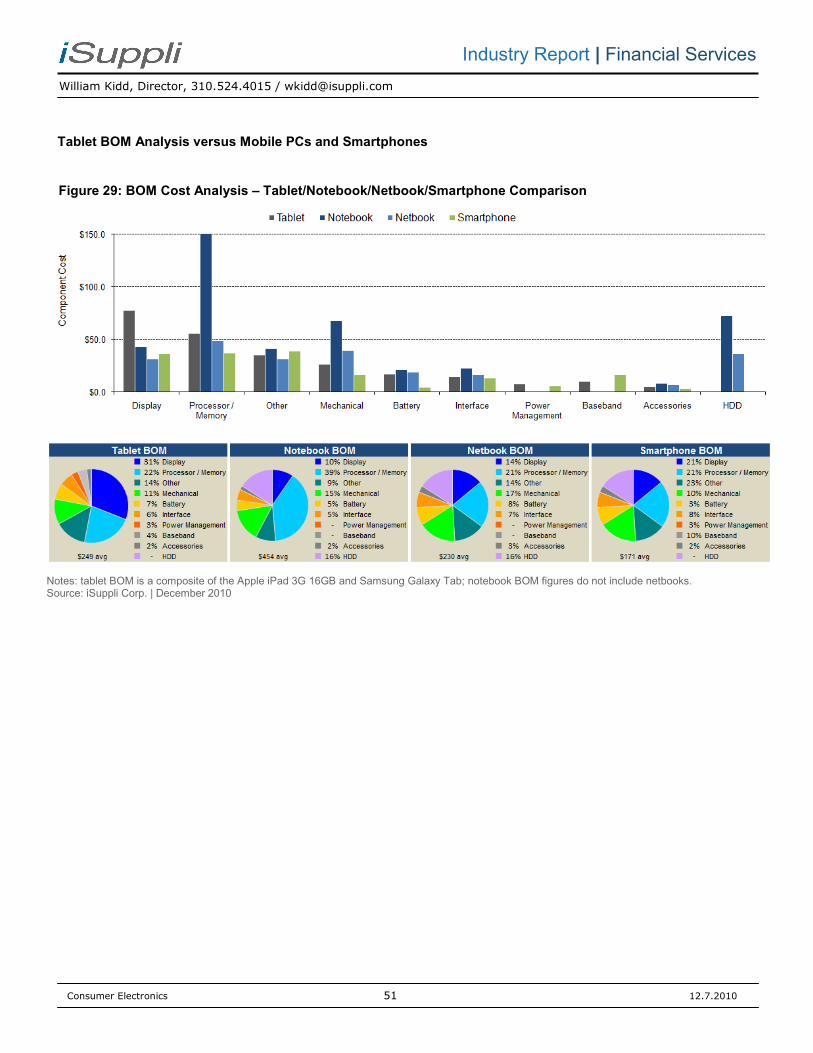

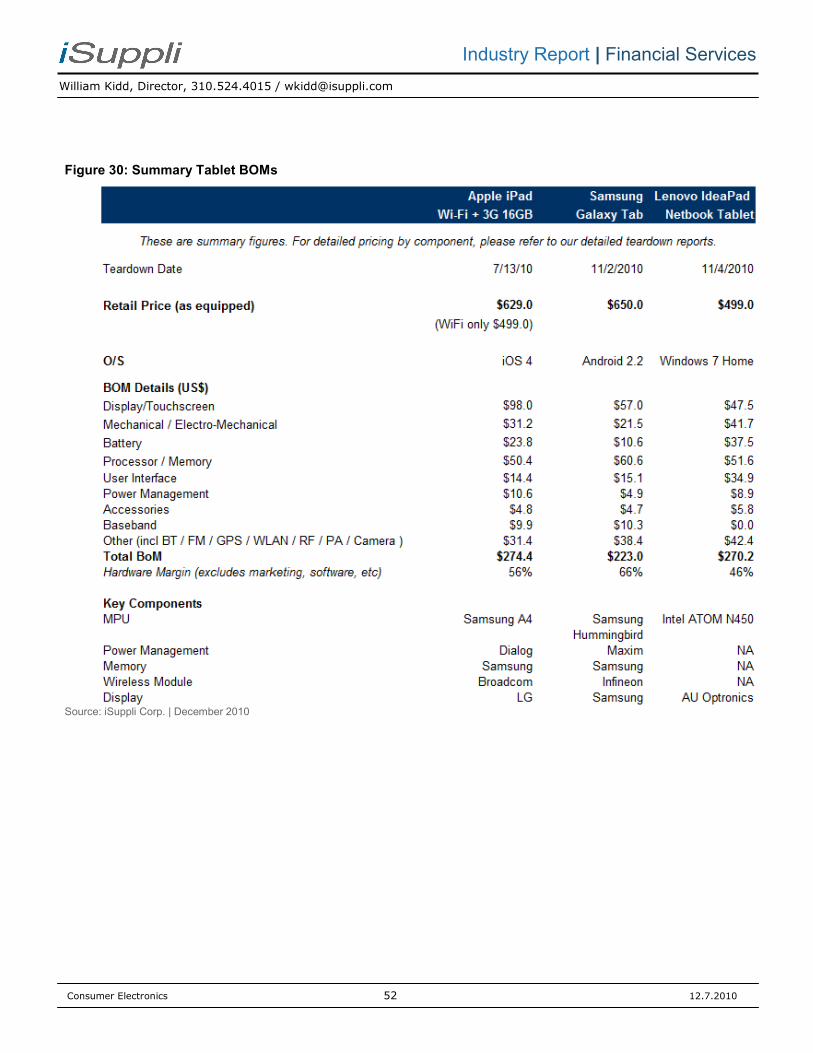

Tablet BOM Analysis versus Mobile PCs and Smartphones................................................................................ 51

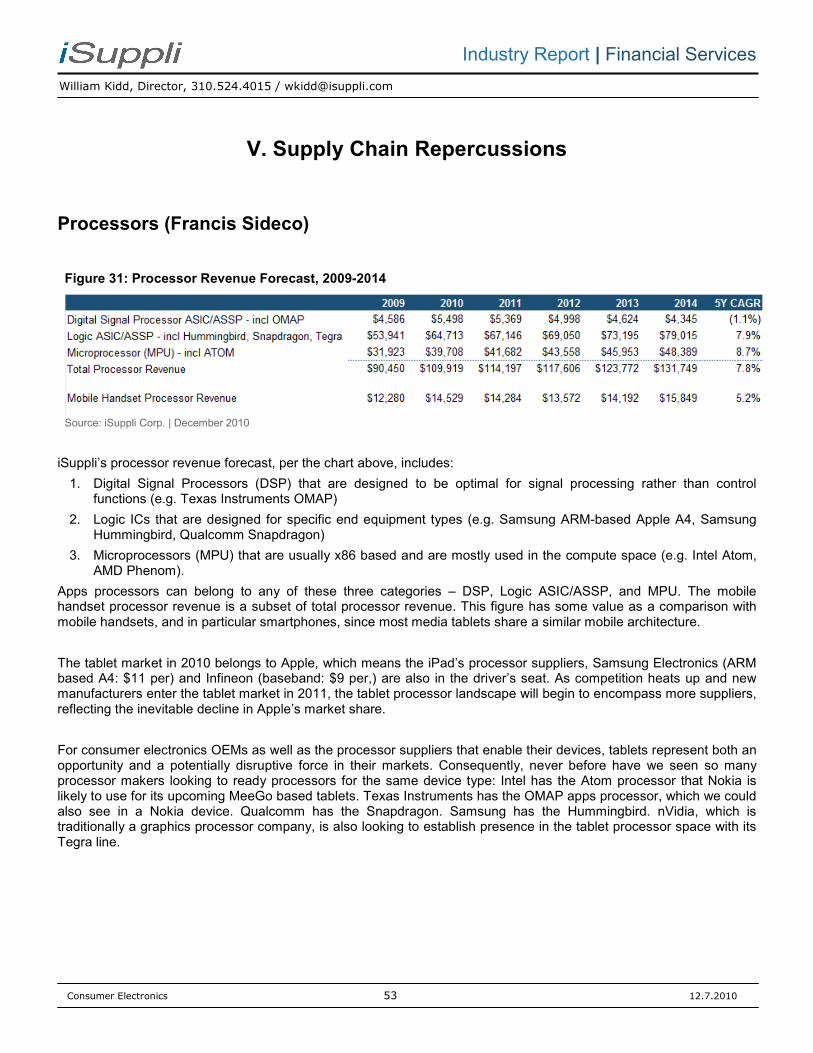

V. Supply Chain Repercussions ............................................................................................................... 53

Processors (Francis Sideco) ................................................................................................................................... 53

Flash (Michael Yang) .............................................................................................................................................. 55

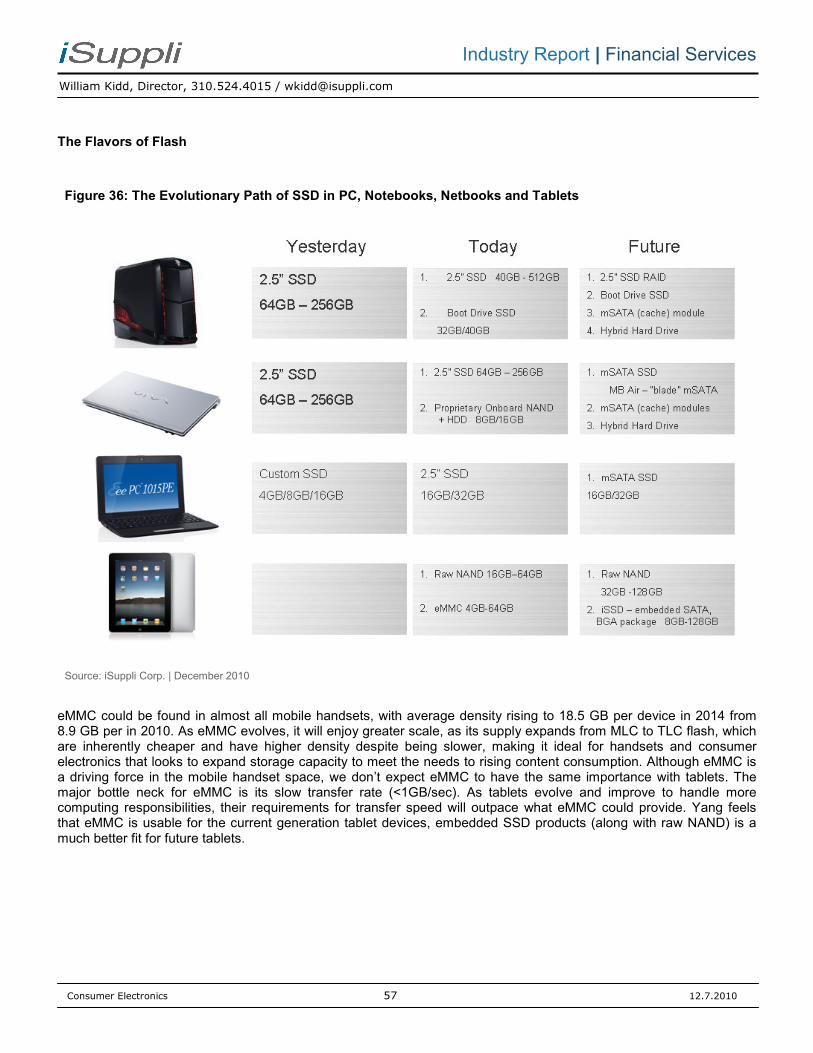

The Flavors of Flash ............................................................................................................................................. 57

DRAM (Mike Howard) ............................................................................................................................................. 59

Display Systems (Vinita Jakhanwal, Joe Abelson) ................................................................................................. 61

Other Tablet Component Suppliers ........................................................................................................................ 62

VI. Tablet-Related Valuation Comps ........................................................................................................ 63

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 3 12.7.2010

Industry Report | Financial Services

VII. Key Developments .............................................................................................................................. 66

11.12 - Android’s Tablet O/S version delayed; iPad continues to lack real competition ...................................... 66

10.15 - Intel sees path to tablets through new atom-based “Oak Trail” processor. ............................................. 67

10.15 - PC market growth remains strong, but not as strong as previously forecast. .......................................... 67

10.01 - RIM announces that it intends to launch its new BlackBerry PlayBook 7” tablet in early 2011 ............... 68

09.17 - Are Tablets the Next NAND Pillar?........................................................................................................... 68

09.10 - Android: Our thoughts on tablet screen-size challenges and O/S fragmentation. ................................... 70

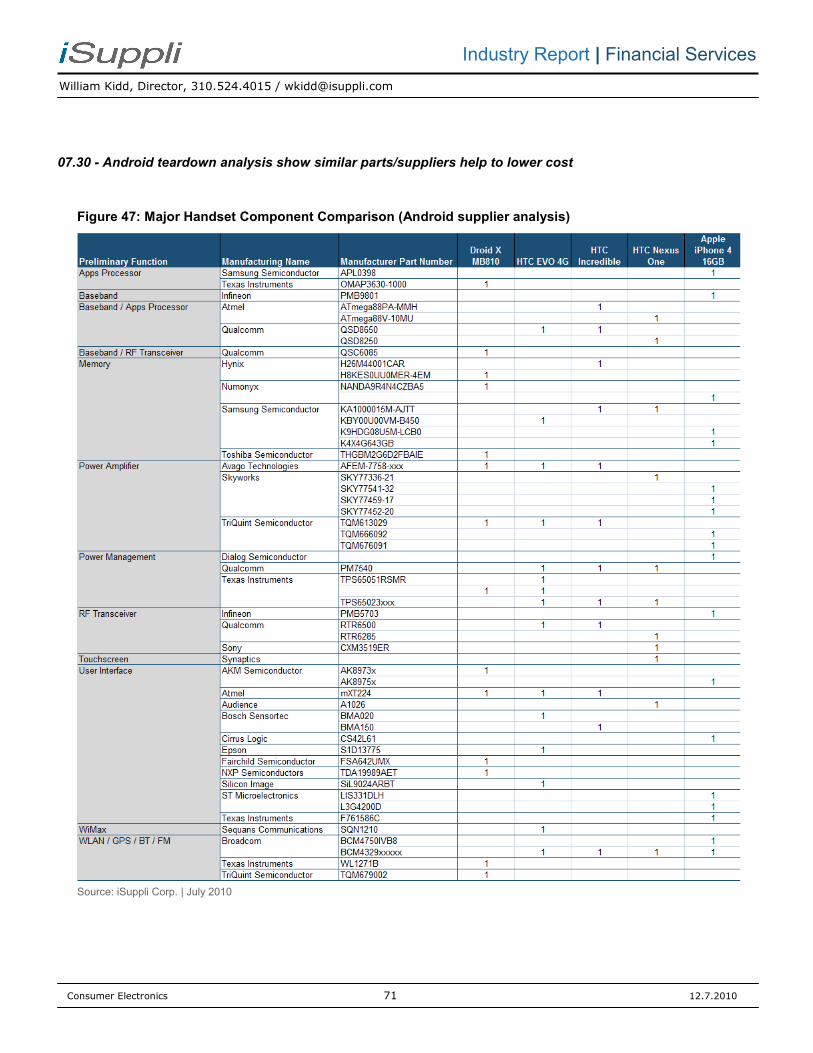

07.30 - Android teardown analysis show similar parts/suppliers help to lower cost ............................................. 71

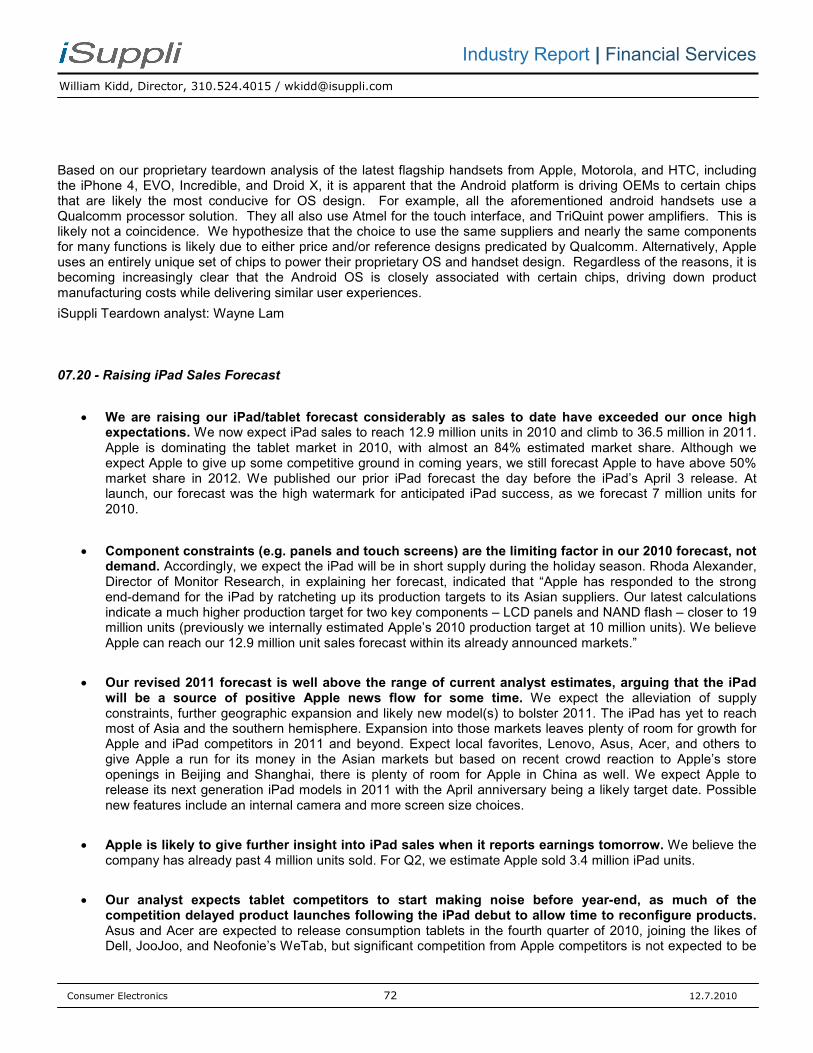

07.20 - Raising iPad Sales Forecast .................................................................................................................... 72

06.25 - As Apple improves its iOS for enterprise customers, RIM’s last bastion could crumble .......................... 74

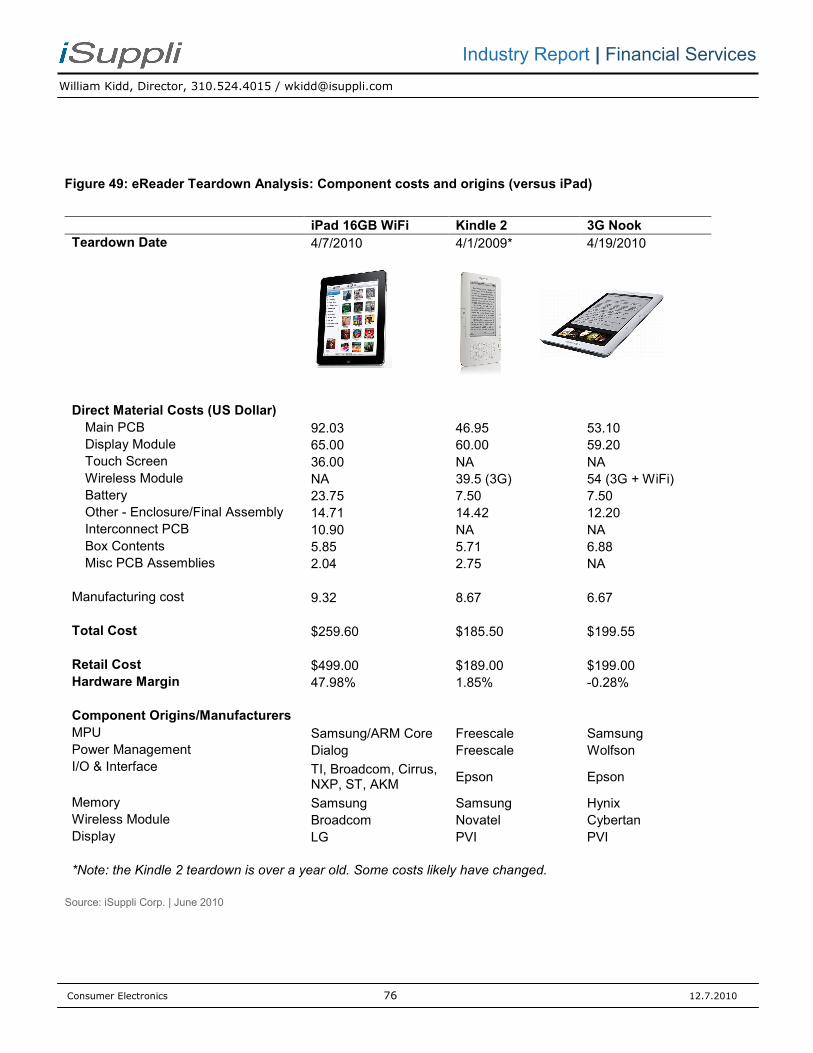

06.25 - New eReader Prices Reflect iPad Effect .................................................................................................. 75

06.25 - We are positive on PCs in Q2, though panel suppliers are concerned by iPad and Europe. .................. 77

06.18 - New PC systems touch-screen forecast .................................................................................................. 77

05.21 - Google Brings the O/S Wars to the Television ......................................................................................... 81

05.21 - Dell Streak wants to be your almost wallet-size virtual PC ...................................................................... 81

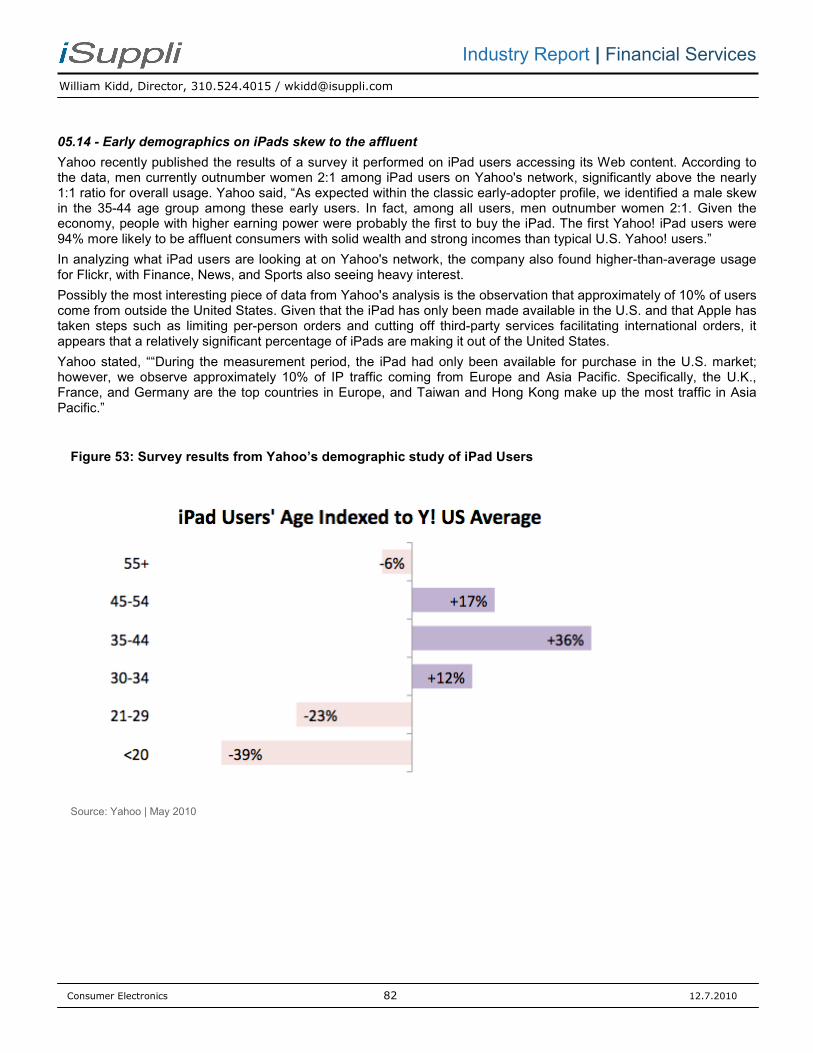

05.14 - Early demographics on iPads skew to the affluent................................................................................... 82

04.30 - Google is succeeding with Android, but apparently failing with its own handsets ................................... 83

04.30 - HP enters mobile O/S race, buying Palm ................................................................................................. 83

04.30 - Apple buys Intrinsity ................................................................................................................................. 84

04.16 - Intel executives not so optimistic on tablet pc category ........................................................................... 84

The following members of iSuppli Financial Services authored this industry report:

William Kidd Director

310.524.4015 [email protected]

Wenlie Ye Senior Researcher

310.524.4064 [email protected]

Sharon Stiefel Researcher

310.524.4048 [email protected]

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 4 12.7.2010

Industry Report | Financial Services

Table of Figures

Figure 1: Tablets Are at the Forefront of the Converge in Consumer Electronics ............................................................ 9

Figure 2: The Evolution in Consumer Electronics Devices to Networked from Digital .................................................... 11

Figure 3: Converging Connected Device Landscape ...................................................................................................... 12

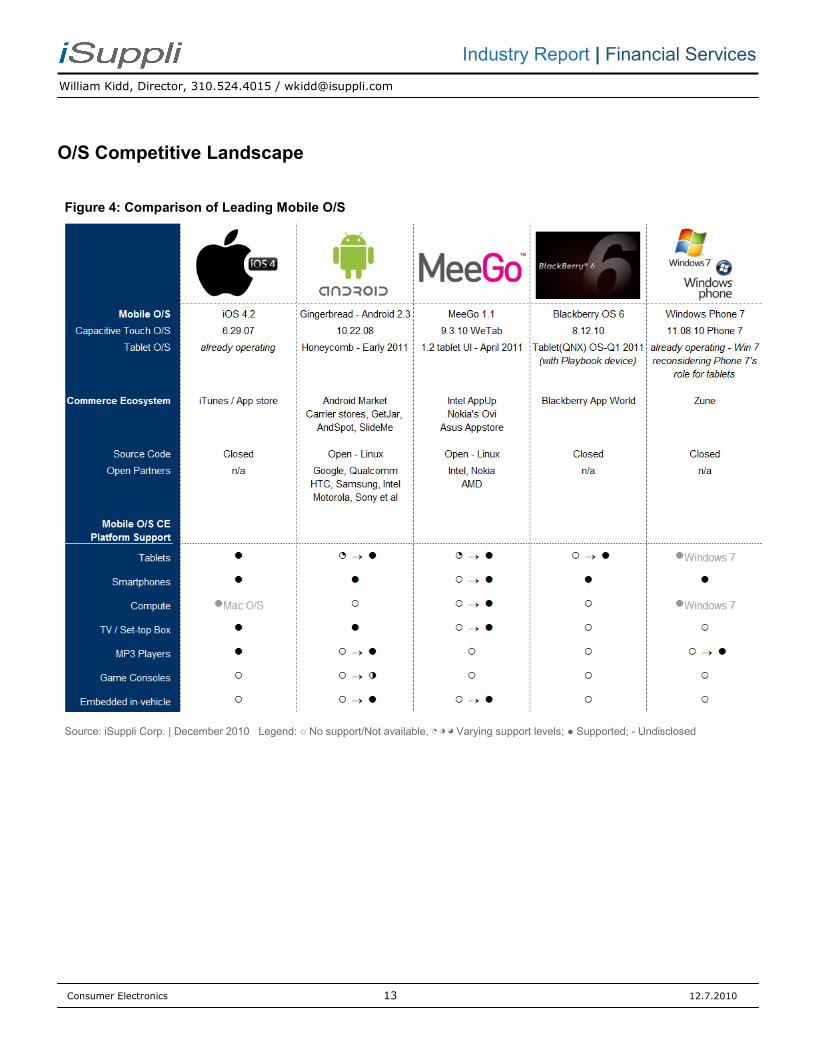

Figure 4: Comparison of Leading Mobile O/S ................................................................................................................. 13

Figure 5: Leading Open Source Mobile (Tablet) O/S ...................................................................................................... 19

Figure 6: Some Famous Open Source Success Stories ................................................................................................. 20

Figure 7: Comparison of Leading Mobile Commerce/Content Ecosystems ................................................................... 22

Figure 8: iPad’s Year One vs. Other Major CE Product Launches ................................................................................. 25

Figure 9: iSuppli iPad/Mobile PC Forecast Evolutions (thousands*) .............................................................................. 26

Figure 10: iSuppli’s “Base Case”: Media Tablets Excel but Don’t Replace Mobile PCs ................................................. 27

Figure 11: Detailed Tablet Consumption Forecast .......................................................................................................... 28

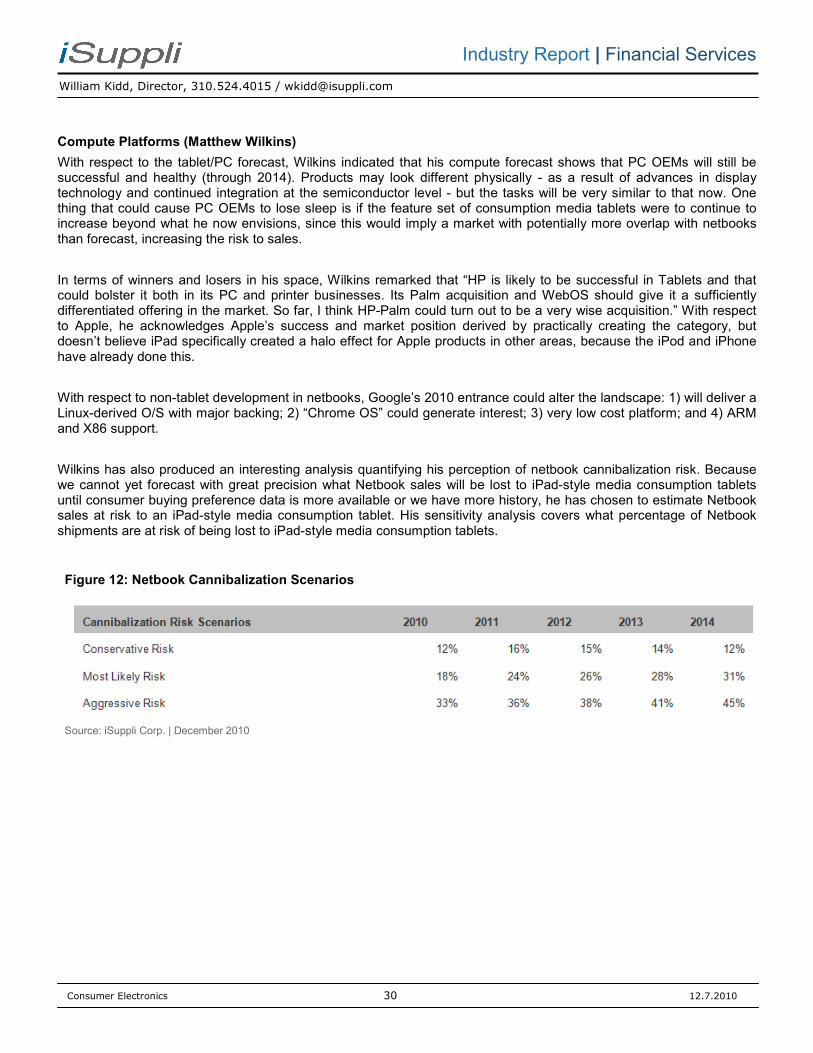

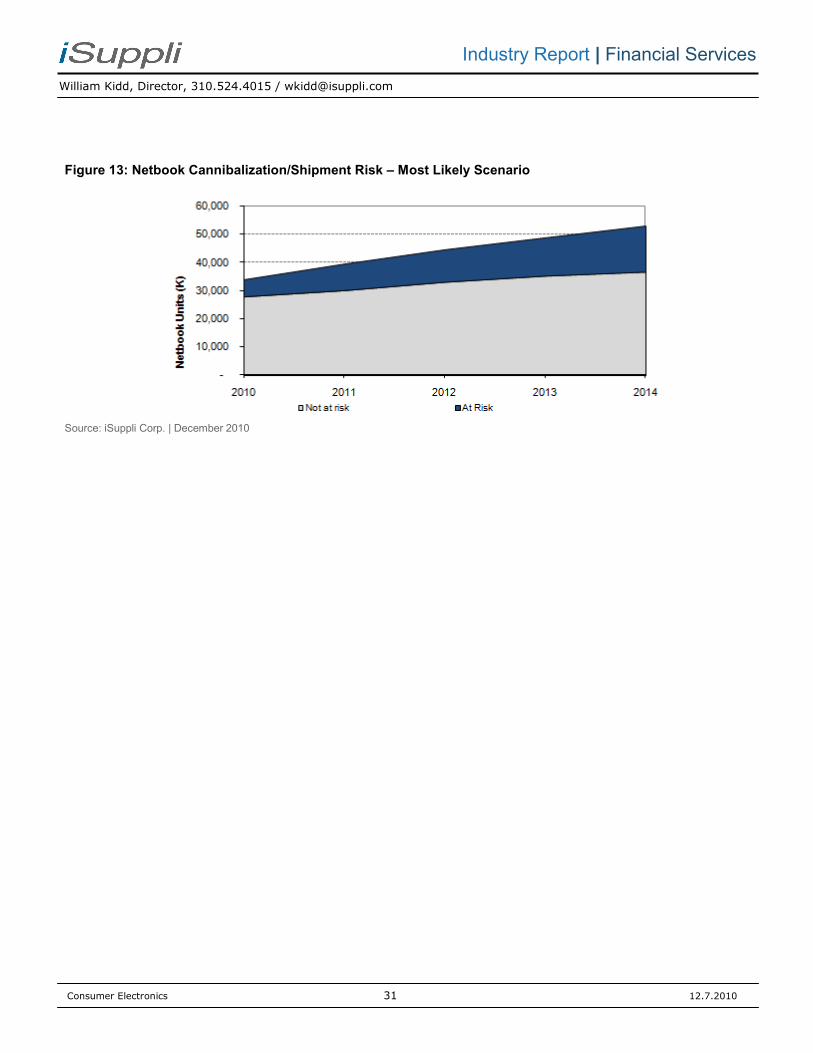

Figure 12: Netbook Cannibalization Scenarios ............................................................................................................... 30

Figure 13: Netbook Cannibalization/Shipment Risk – Most Likely Scenario .................................................................. 31

Figure 14: Converged Device Comparison ..................................................................................................................... 32

Figure 15: iSuppli - Tablet Base Case ............................................................................................................................. 34

Figure 16: iSuppli Financial Services – Tablet Alternate Case ....................................................................................... 35

Figure 17: Our Unified Consumer Electronics Future: The Connected Life .................................................................... 39

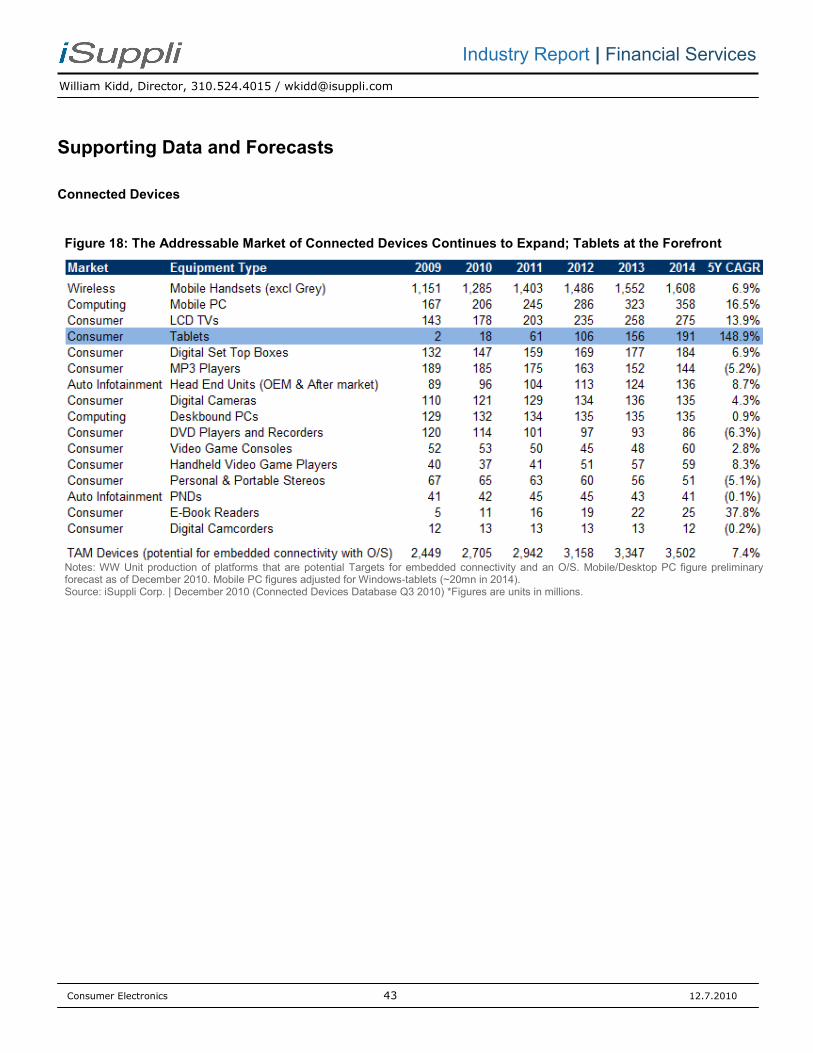

Figure 18: The Addressable Market of Connected Devices Continues to Expand; Tablets at the Forefront ................. 43

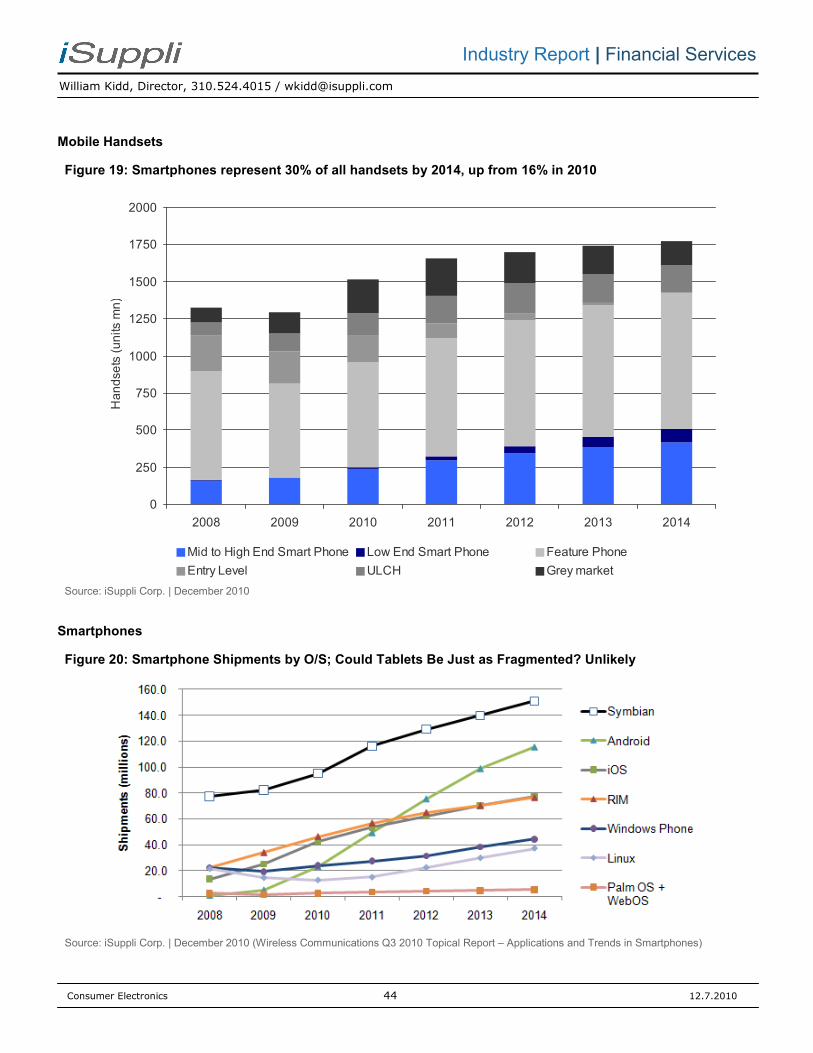

Figure 19: Smartphones represent 30% of all handsets by 2014, up from 16% in 2010 ................................................ 44

Figure 20: Smartphone Shipments by O/S; Could Tablets Be Just as Fragmented? Unlikely ....................................... 44

Figure 21: Smartphone Shipments by O/S (millions) ...................................................................................................... 45

Figure 22: Smartphone Shipments by Handset OEM (millions) ...................................................................................... 45

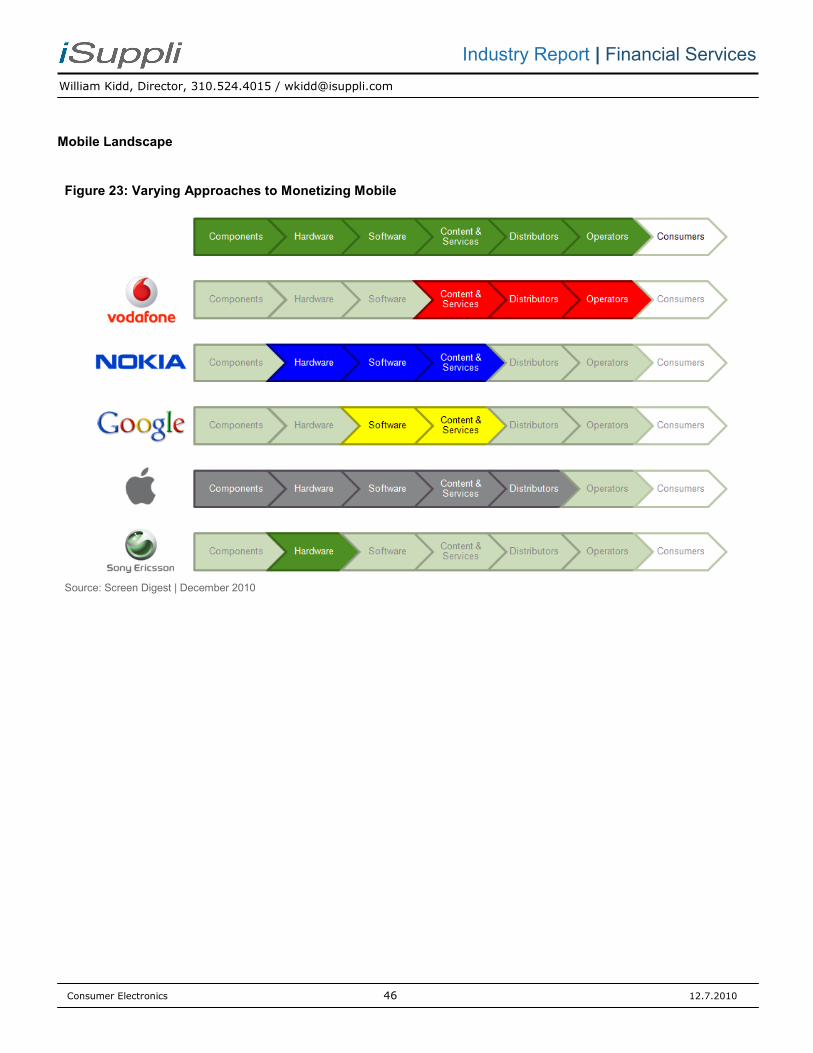

Figure 23: Varying Approaches to Monetizing Mobile ..................................................................................................... 46

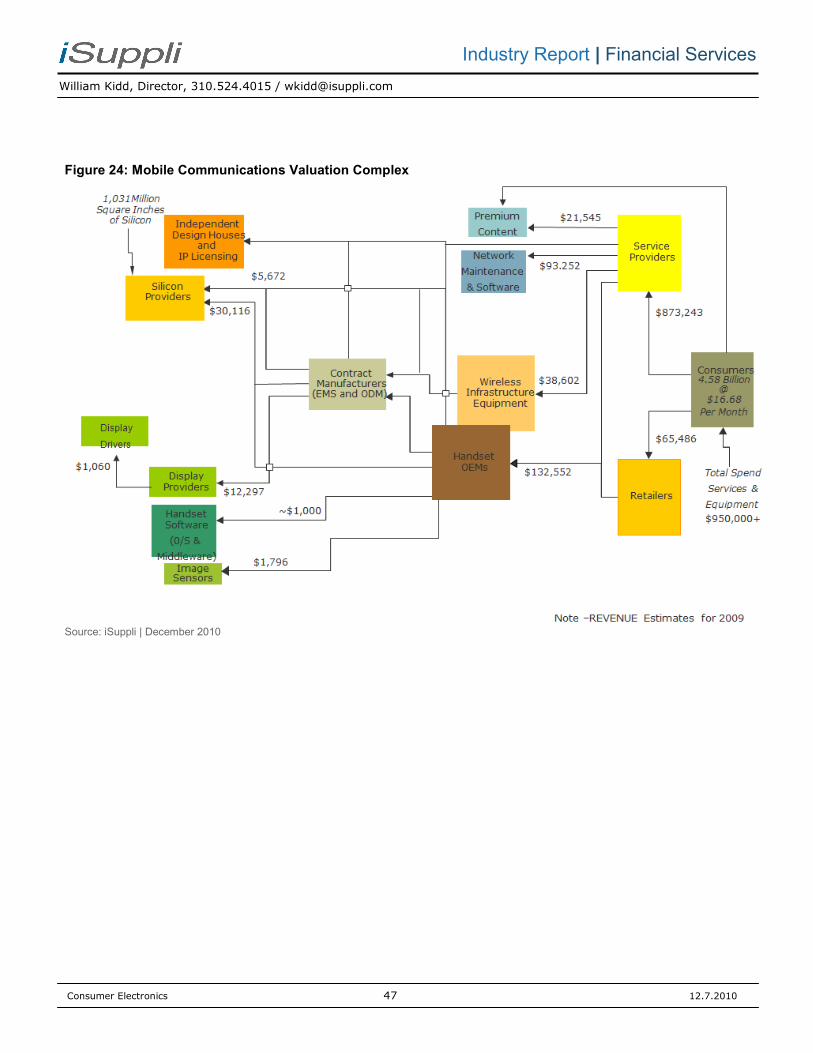

Figure 24: Mobile Communications Valuation Complex ................................................................................................. 47

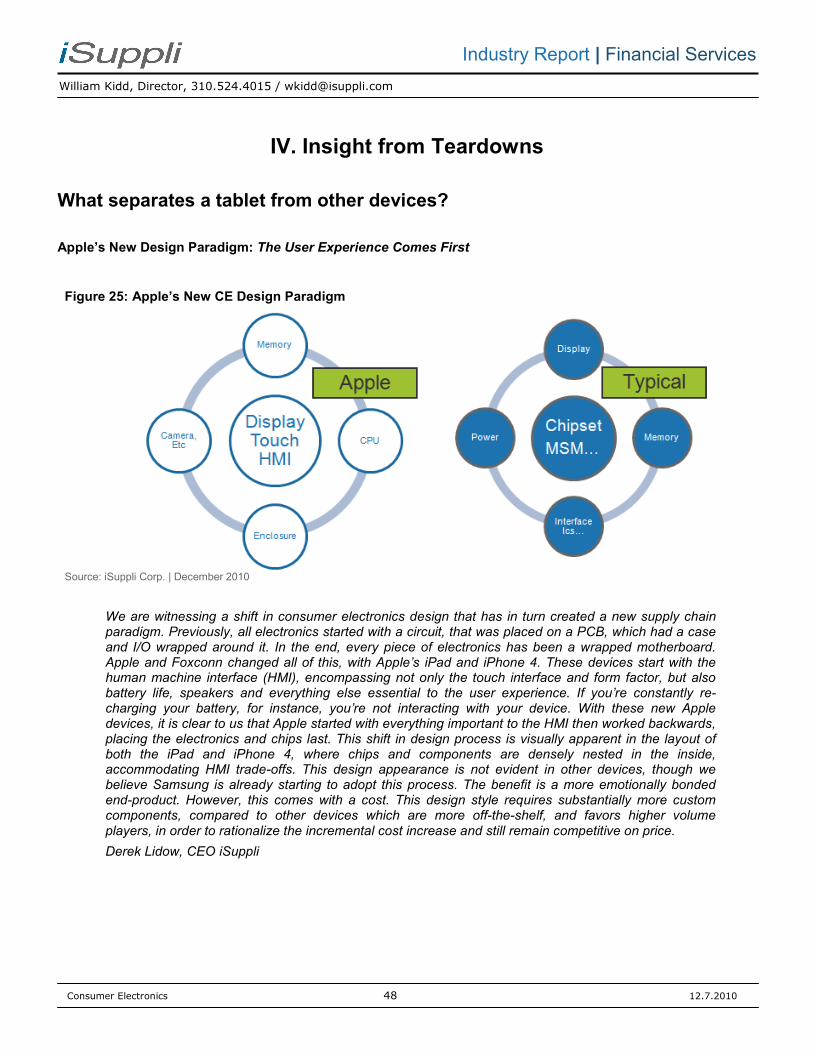

Figure 25: Apple’s New CE Design Paradigm ................................................................................................................. 48

Figure 26: The HMI First, “Nested” iPhone 4 .................................................................................................................. 49

Figure 27: Lenovo IdeaPad Exploded BOM View ........................................................................................................... 49

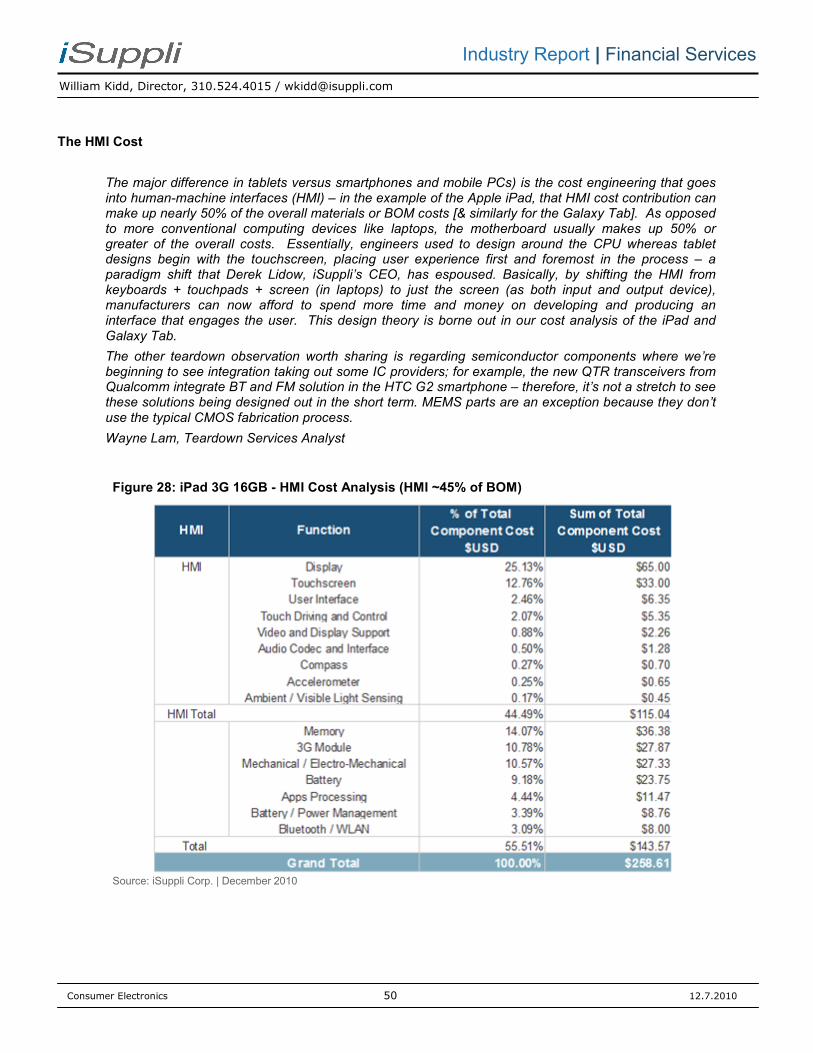

Figure 28: iPad 3G 16GB - HMI Cost Analysis (HMI ~45% of BOM) .............................................................................. 50

Figure 29: BOM Cost Analysis – Tablet/Notebook/Netbook/Smartphone Comparison .................................................. 51

Figure 30: Summary Tablet BOMs .................................................................................................................................. 52

Figure 31: Processor Revenue Forecast, 2009-2014 ..................................................................................................... 53

Figure 32: Tablet Apps Processor Revenue Forecast (millions) ..................................................................................... 54

Figure 33: Flash Memory Revenue by Category, 2009-2014 ......................................................................................... 55

Figure 34: The Insatiable Appetite for NAND Flash ........................................................................................................ 55

Figure 35: Tablets Produce Incremental Growth And Help Make NAND Affordable Elsewhere .................................... 56

Figure 36: The Evolutionary Path of SSD in PC, Notebooks, Netbooks and Tablets ..................................................... 57

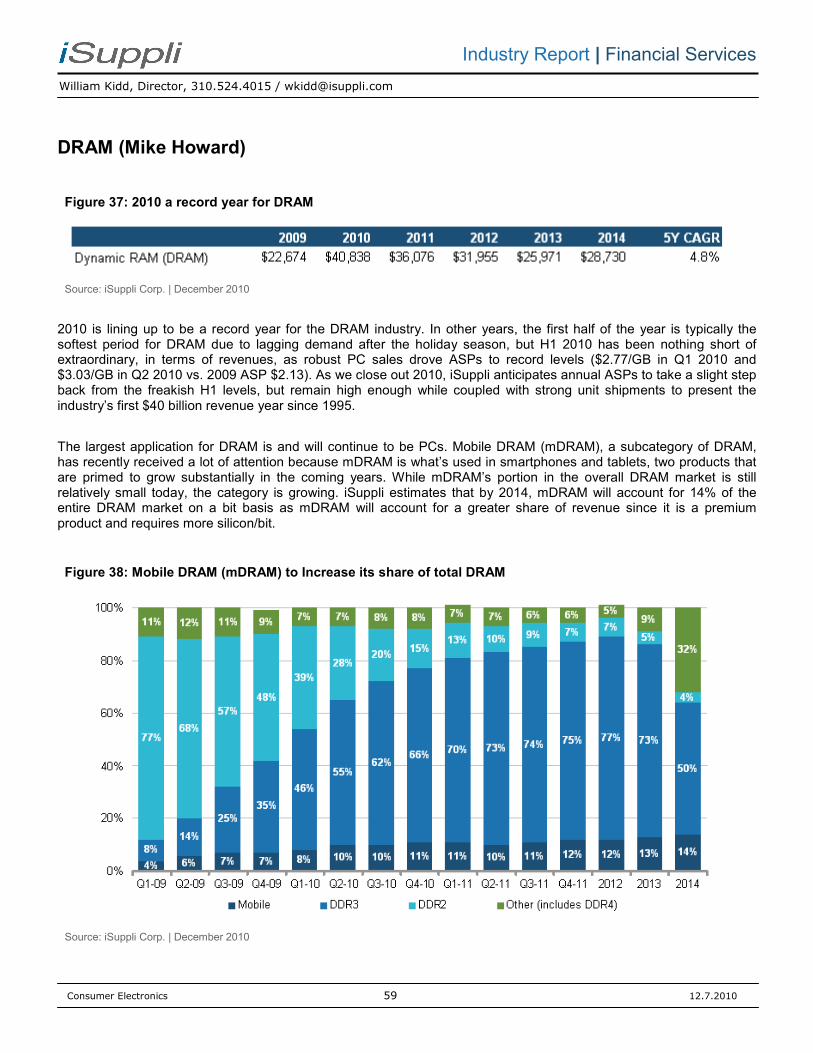

Figure 37: 2010 a record year for DRAM ........................................................................................................................ 59

Figure 38: Mobile DRAM (mDRAM) to Increase its share of total DRAM ....................................................................... 59

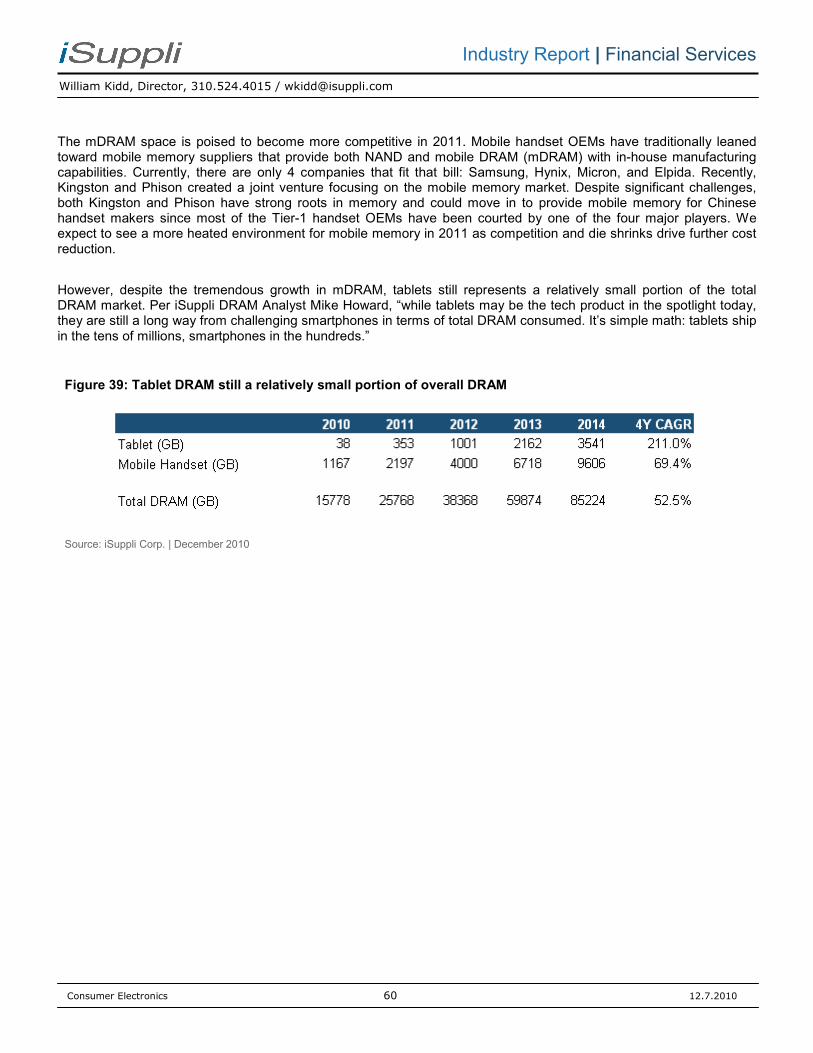

Figure 39: Tablet DRAM still a relatively small portion of overall DRAM ........................................................................ 60

Figure 40: Internet Access Device Display Revenue 2009-2014 (Millions) .................................................................... 61

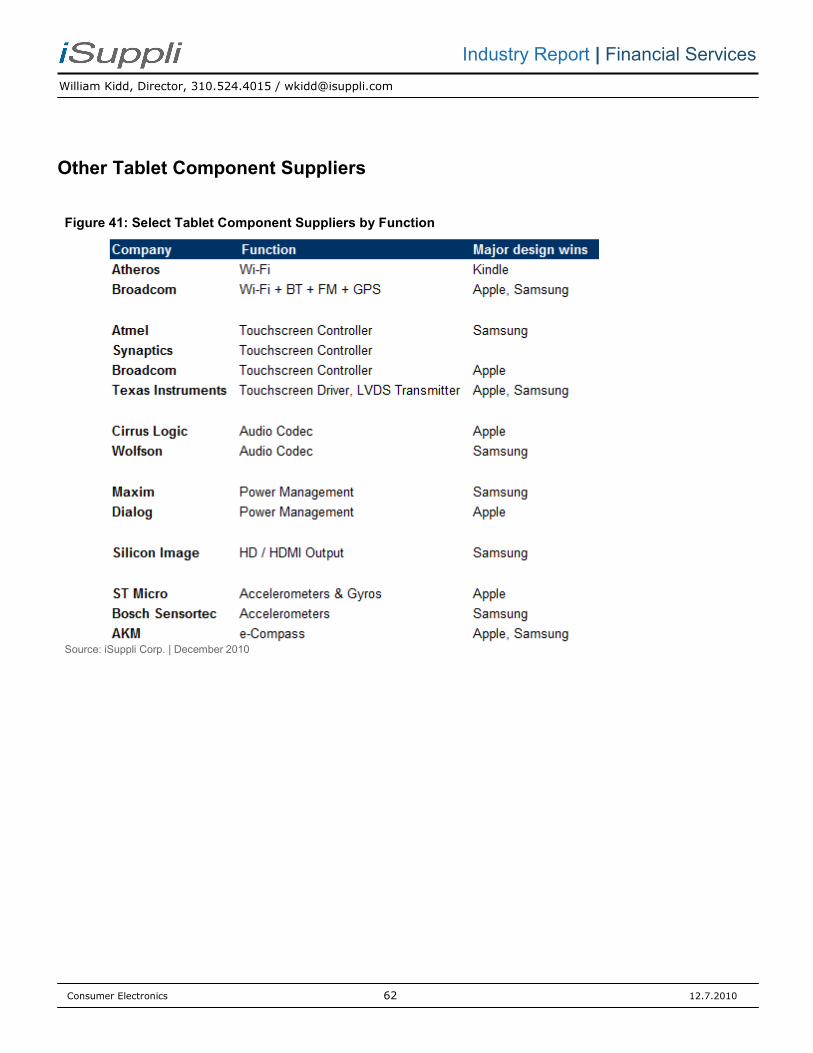

Figure 41: Select Tablet Component Suppliers by Function ........................................................................................... 62

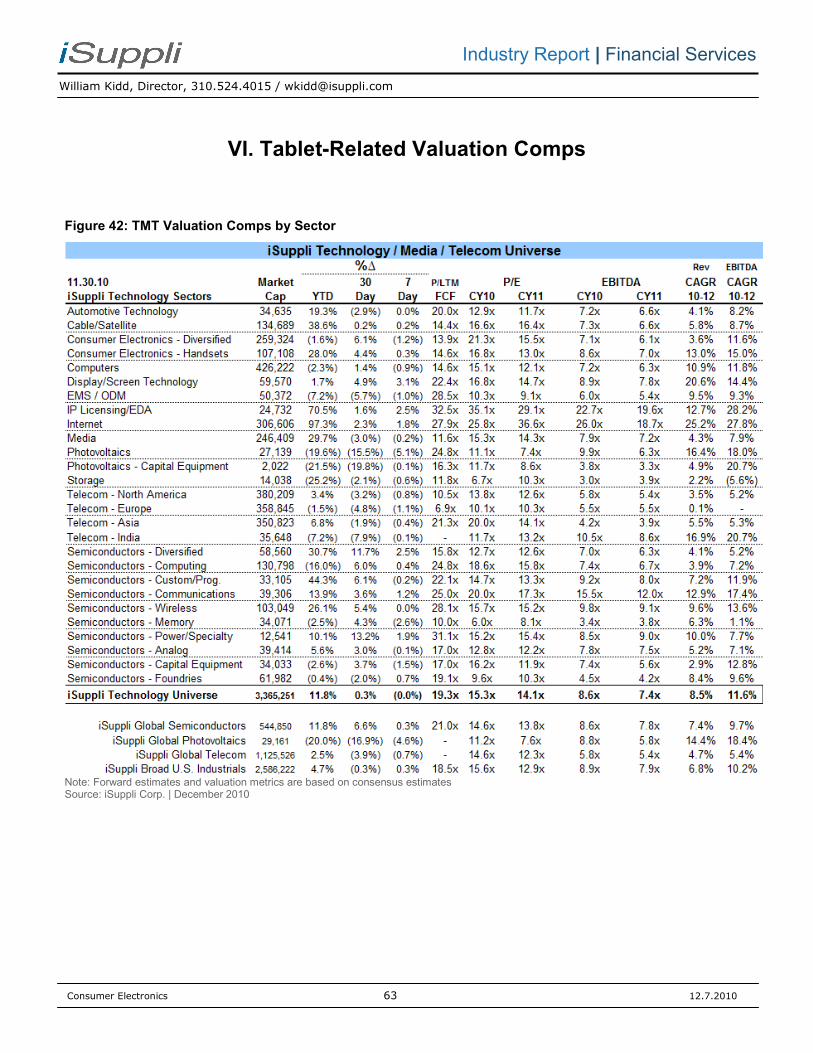

Figure 42: TMT Valuation Comps by Sector ................................................................................................................... 63

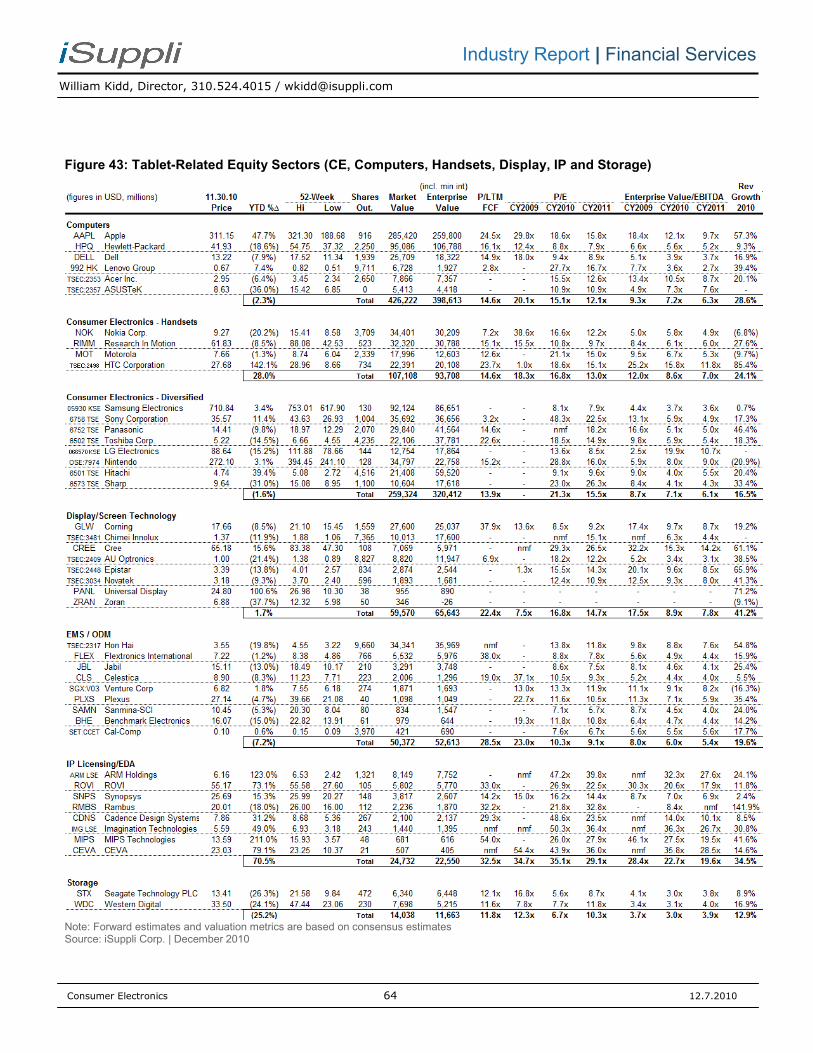

Figure 43: Tablet-Related Equity Sectors (CE, Computers, Handsets, Display, IP and Storage) .................................. 64

Figure 44: Tablet-Related Equity Sectors (Semiconductors) .......................................................................................... 65

Figure 45: Side-by-side comparison Playbook, Galaxy Tab, iPad .................................................................................. 68

Figure 46: Tablet NAND density and total GB shipped, 2010-2014................................................................................ 69

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 5 12.7.2010

Industry Report | Financial Services

Figure 47: Major Handset Component Comparison (Android supplier analysis) ............................................................ 71

Figure 48: iPad Sales Forecast 2010-2012 (July 2010) .................................................................................................. 73

Figure 49: eReader Teardown Analysis: Component costs and origins (versus iPad) ................................................... 76

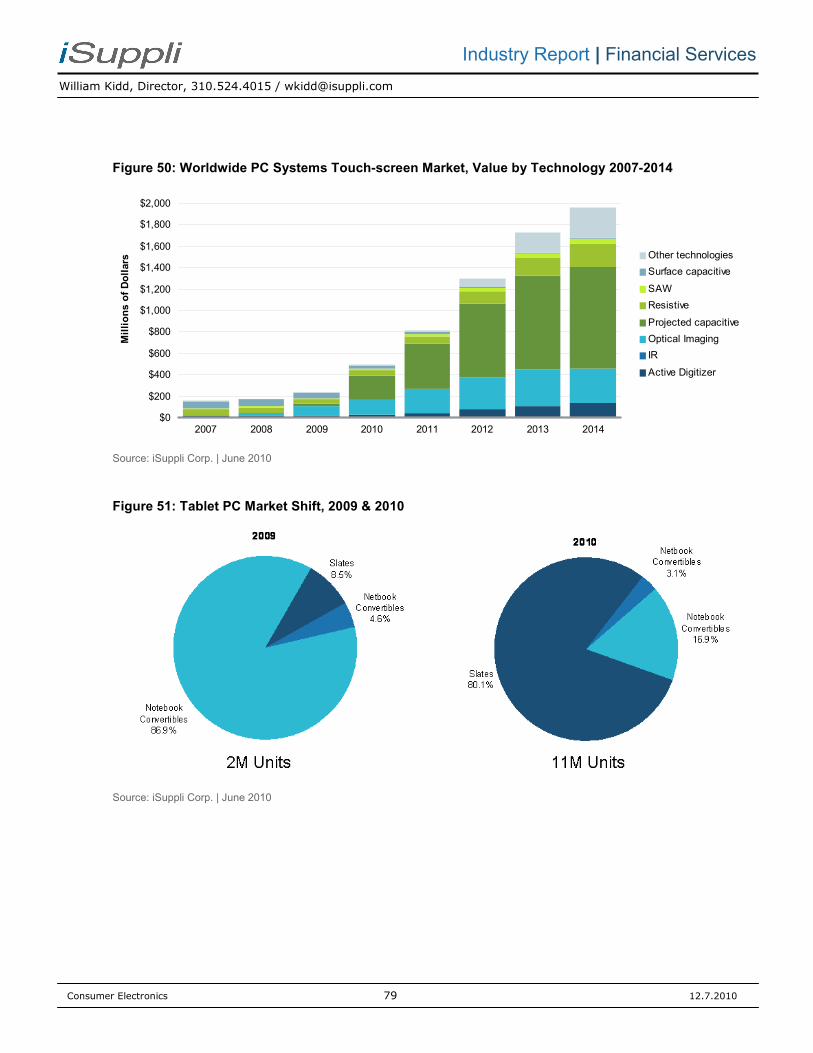

Figure 50: Worldwide PC Systems Touch-screen Market, Value by Technology 2007-2014 ........................................ 79

Figure 51: Tablet PC Market Shift, 2009 & 2010 ............................................................................................................. 79

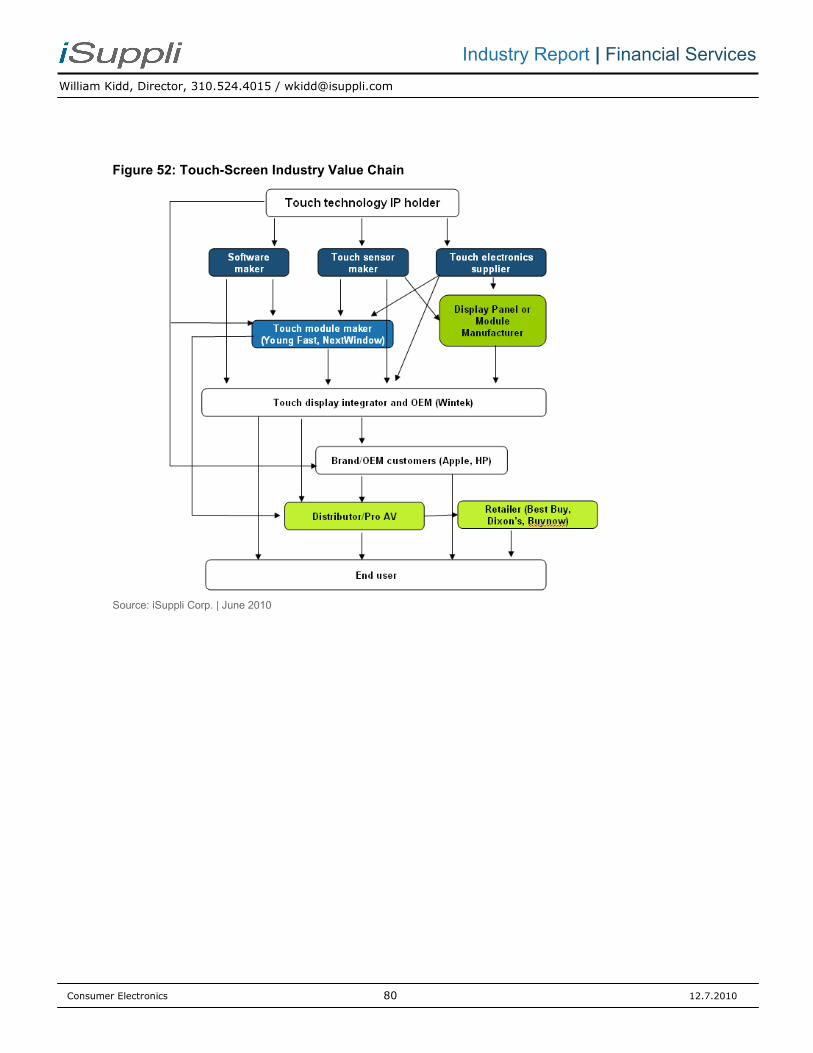

Figure 52: Touch-Screen Industry Value Chain .............................................................................................................. 80

Figure 53: Survey results from Yahoo’s demographic study of iPad Users .................................................................... 82

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 6 12.7.2010

Industry Report | Financial Services

iSuppli / Screen Digest

Tablet Market Intelligence Team

CONSUMER ELECTRONICS

� Tablets, Rhoda Alexander Tablets - U.S. Consumer Preferences Survey (pending Q1 release) U.S. Tablet Market Tracker (pending Q1 release) Portable and Desktop Computing Systems are Ready to Feel the Touch. 06.10.10

� Compute Platforms, Matthew Wilkins Compute Platforms Q3 2010 Market Tracker. 09.21.10 PC Technology Penetration. 07.30.10

� Wireless Handsets/Smartphones, Tina Teng Wireless Communications: Smart Phones, The Center of Your Social Life. 10.26.10 Smart Phones Become Multifunctional with Preloaded Software. 06.30.10

� Connected Devices, Jagdish Rebello, PhD Connected Devices Database - Q3 2010. 09.03.10

� Consumer Electronics (Macro), Jordan Selburn Consumer Platforms: Consumer OEMs Fight for Slice of $300 Billion Pie. 11.22.10

SUPPLY CHAIN

� Small & Medium Displays, Vinita Jakhanwal Small & Medium Displays PriceTrak. 11.19.10 Small Medium Displays Supply and Demand - Q2 2010 Database. 11.02.10

� Flash Memory & SSDs, Michael Yang Mobile and Embedded Memory - Mobile Fueling Next Generation Growth. 09.24.10 NAND Dynamics - Are Tablets the Next NAND Pillar? 09.10.10

� DRAM, Michael Howard DRAM Dynamics - The Logical Future of DRAM. 11.23.10 DRAM Q3 2010 Market Tracker Database. 09.28.10

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 7 12.7.2010

Industry Report | Financial Services

Wireless Processors/Baseband, Francis Sideco Touch and Go: Mobilized Tablets Spark Wireless Growth in CE Devices, 07.29.10 LTE, Tablets and Earthquakes: What Do They Have In Common For Wireless Systems? 06.29.10

� Teardowns, Andrew Rassweiler Teardown Analysis - Lenovo S10-3t Netbook Tablet. 11.04.10 Teardown Analysis - Samsung Galaxy Tab GT-P1000 Mobile Tablet. 11.02.10 Teardown Analysis - Apple iPad 3G 16GB. 07.13.10

MEDIA (Screen Digest)

� Mobile Media, Julien Theys Mobile Funding and M&A Trends - Q3 2010. 10.01.10 Mobile Hardware Market Monitor - Q2 2010. 09.23.10

� Mobile Media, Jack Kent Android Market Slow to Deliver. 09.29.10 Mobile Market Monitor: Games Q1 2010. 06.03.10

� Mobile Media, Ronan de Renesse Euro Mobile Operators Still Grow. 11.27.10 Mobile Video-New Apps Give TV Operators a Way to Make Video Pay. 09.27.10

� Internet Advertising, Vincent Létang Microsoft-Yahoo Search Alliance Completed in North America. 11.30.10 Internet Advertising Round-up Q3. 11.26.10

To request a meeting with our analyst team, please contact either

iSuppli – Kayle Watson at 914-437-7783 or [email protected]

Screen Digest – Ben Colbeck at 44 (0)20 7424 2832 or [email protected]

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 8 12.7.2010

Industry Report | Financial Services

I. Convergence and the Mobile O/S

Although there are countless examples of open and closed source software projects, even other related open models such as free and open source software (FOSS), we are going to ignore most of that history and debate in order to focus this report on the distinctions of a converged mobile O/S for tablets, smartphones and other like devices.

The Converged Mobile O/S

We would like to argue that the driving force for a converged mobile O/S has been devices like the iPod Touch and later iPad (announced January 2010). Clearly, the iPad's O/S traces its routes directly to the iPhone's smartphone O/S. However, Apple's iOS cannot be labeled merely a smartphone O/S as the Android presently is today, since it's powering a range of connected devices beyond the iPhone: iPod Touch/Nano, Apple TV and iPad. Hence, we consider Apple's iOS as the best working example today of a Converged Mobile O/S or "Mobile O/S" for short. The key distinction between a Mobile O/S and a smartphone O/S is its ability to work with a diverse set of converging consumer electronics platforms and also handle the more media-intensive applications expected from form factors like tablets. Android is a close but distant second as a Mobile O/S, having really only made the transition beyond smartphones with Google TV, where it's still rolling out the platform (the Android Market won't be available until early 2011 on Google TV). Android is presently struggling with the tablet form factor, as its current smartphone O/S incarnation is still struggling to handle the larger screen sizes of tablets (please refer to 11.12 in Chapter 7 for more details on Android’s O/S delays).

In our estimation, the current litmus test for a Mobile O/S is its ability to handle tablet devices, since a typical media use case can be almost as demanding as a traditional compute device, at least as it pertains to watching HD video (sans more intensive games), while its form factor, processor, connectivity options, and power constraints make tablets a cross between a notebook/netbook and smartphone. We surmise that for a mobile O/S developer, once their tablet-capable O/S is truly in place, other consumer electronics form factors (TV, MP3, automotive) should be easier to come by if Apple's iOS development history is any measure. Apple has already been able to port its iOS to multiple device types. As Android nears its O/S tablet release in early 2011, it is already being mentioned for portable game devices, (embedded in) cars, and MP3 players. Thus, Apple's iOS and Android both show that the role of a mobile O/S is quickly evolving to and from converged devices like tablets to support further evolution in connected devices (e.g. WiFi through representative devices such as MP3 players, TVs, set-top boxes and soon cars and possibly refrigerators) as well as mobilized devices (3g/4g).

While Apple is the de facto leader in Mobile O/S, Apple is neither the industry driver nor the guaranteed victor. Apple's just the first car on the road and there is a long, long journey ahead. The underlying technology evolution (e.g. semiconductors and connectivity) that powers such devices has really been the enabling factor for a Mobile O/S. However, Apple has been an important agent of change and its iOS is showing consumers new possibilities with seemingly old device types. Technology has been the driver and it's the same technological evolution that is now enabling once dissimilar devices (e.g., PDAs vs. notebooks, MP3 players vs. mobile handsets) to become increasingly similar in function and capability. The similarity that exists today between Apple's tablet, smartphone and MP3 player are prime examples of how consumer electronics are blurring together. And it's just not externally - from a teardown point of view, Apple's devices are internally similar, plus or minus a screen and touch interface. The same convergence trend that we are now discussing at a product level is also visible at a company and industry level, where hereto the implications are staggering, as once distinctly different industries are being forced to compete with one another.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 9 12.7.2010

Industry Report | Financial Services

Nokia's 20-F, dated March 2010, highlights this confluence of devices and industries:

Traditional mobile voice communications, the Internet, various means of messaging, media, music, entertainment, navigation, location-based and other services, personal computing and other consumer electronics are converging in many areas into one broader industry. Increasingly, people are using mobile devices to access digital content and web services and share their experiences. Converged mobile devices are based on programmable software platforms, can run applications such as email, web browsing, navigation and enterprise software, and can also have built-in music players, video recorders, mobile TV and other multimedia features. Increasingly, such devices are becoming more affordable for a wider population. The software that powers converged mobile devices has also become increasingly sophisticated, providing greater opportunities for the development of services, including applications and content, that enrich the experiences people have with their mobile device. A consumer’s choice of device is increasingly influenced by the quality and compatibility of the software and/or services and the resulting user experience, in addition to the quality of the hardware. During the past several years, the converged mobile device market has been characterized by growing volumes, high average selling prices and attractive profitability, as well as intense competition particularly from new entrants, and heightened media and consumer attention.

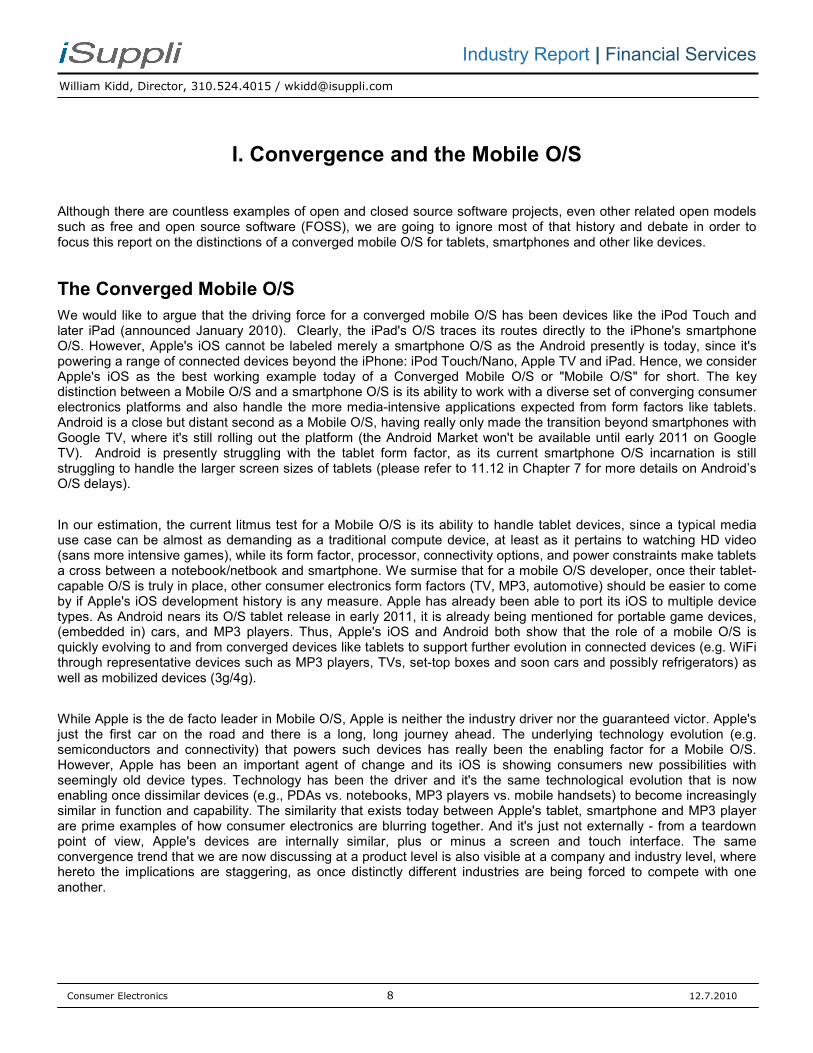

The capability and affordability of mobile processors are probably the most important aspects in this technological convergence, as mobile processors evolved and enabled more computing functionality. This evolution has created new competitive overlaps (see figure below). Affordable flash memory for storage is also important in this evolution along with a whole host of other low cost, low power semiconductor solutions.

Figure 1: Tablets Are at the Forefront of the Converge in Consumer Electronics

Source: iSuppli Corp. | December 2010

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 10 12.7.2010

Industry Report | Financial Services

Convergence at one time described voice, video and data services being delivered to the home vis-à-vis broadband networks and the new services that would result from the confluence. While that trend still exists, the convergence of consumer electronics devices and industries are now coming together at a fast pace, with the tablet form factor being a tangible representation of that convergence, since it is part smartphone and part netbook/notebook. However, the implications of the convergence in consumer electronics go well beyond tablets, as the trend could lead to the growing importance of Mobile O/S in a large number of consumer electronics devices where previously the O/S didn't exist or wasn't a factor before. Thus, it's a time of great risk and opportunity for all the players across the impacted consumer electronics food chain, which is why so many of them seem to be rushing to deliver (or be a key supplier to) a next generation tablet, smartphone or both, like the iPad/iPhone, while also attempting to keep their design options somewhat open, as it is still so early in this product's life cycle.

O/S Framework Makes CE Devices More Compelling

The mobile O/S provides a framework for (1) consumers to cheaply and effortlessly create custom use cases for a device through apps which greatly exceed the utility of an internet browser alone, (2) developers to create and monetize apps, (3) content providers to distribute content and adds another convenient option for consumers to access content; and (4) interconnectivity between connected devices (and thus, even more new use cases). Imagine an eReader with this type of O/S bundled with a competent processor, the use cases increase dramatically from simply reading books and surfing the web (assuming WiFi+browser). Without the structure of the O/S, a connected device is simply an Internet browser and a mobile handset is merely a phone or at most a PDA. For many consumer electronics devices, the O/S by itself, if added to an e-reader, gaming console, or TV set-top box means a significant increase in capability (e.g. increased consumption options, apps).

One has only to look at the demos of MeeGo's tablet UI now circulating to see how a mobile O/S can improve upon Windows 7, a well developed operating system, with tablets specifically. And undoubtedly the role of tablets and other converged devices will expand the opportunity set beyond what we now can foresee. The evolution in tablet uses/roles isn't limited to the traditional consumer. Examples are already cropping up of the wide range of applicability of the iPad, from uses for as young as toddlers to applications in retail sales where new apps have created new use cases, beyond just media consumption. These new tablet roles, powered by the mobile O/S, exceed what was previously possible from compute devices and smartphones. Many are waiting to see if RIM and HP will be able to deliver new compelling enterprise solutions when their next generation tablets come out in 2011.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 11 12.7.2010

Industry Report | Financial Services

The Dizzying Rate of Change

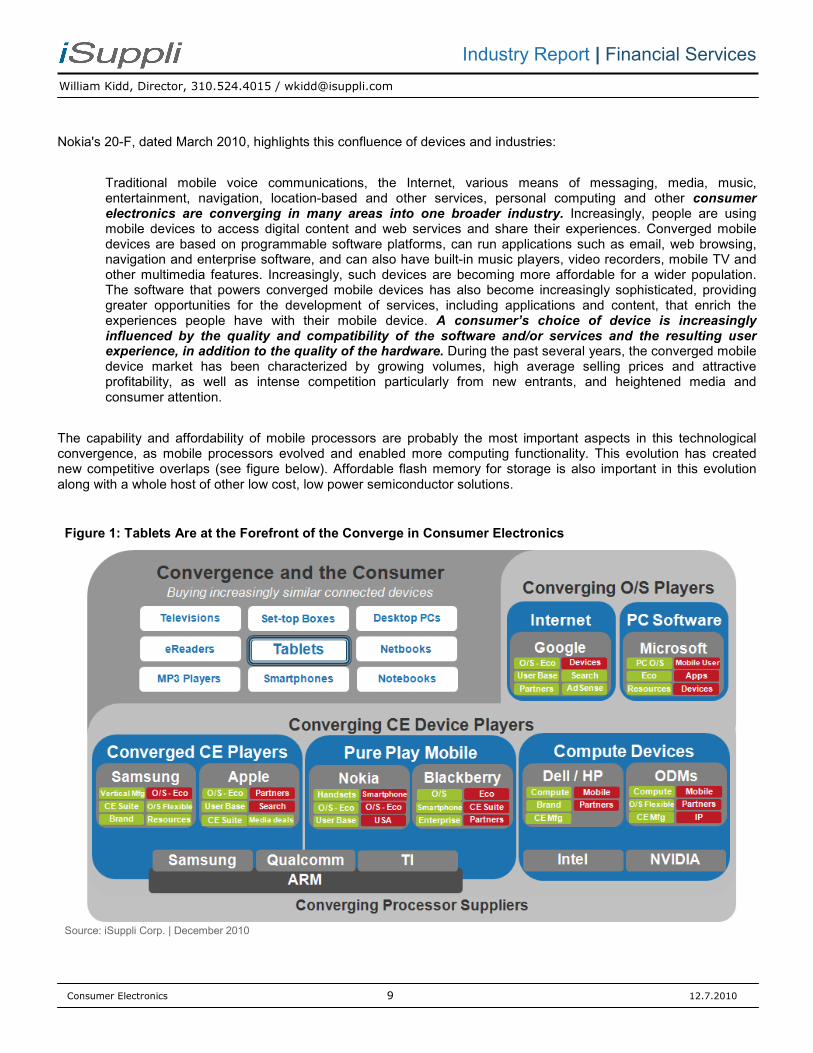

As I was researching this report, I was drawn to recent presentations on the connected home, which have seen rapid change as a result of the ubiquity and low-cost nature of WiFi. Consumer electronics have undergone a revolution from analog to digital to now to networked devices.

Figure 2: The Evolution in Consumer Electronics Devices to Networked from Digital

Source: iSuppli Corp. | December 2010

Although the battle for which broadband standard will ultimately serve most in-home networks will undoubtedly be waged for a long time to come, the consumer electronics battle has already taken another quick step forward in its evolution from the chart above as a result of the mobile O/S. As of year-end 2009, there wasn't one converged mobile O/S in the marketplace by our definition and even more precisely, in homes.

Today, Google and Apple both have products with a converged mobile O/S running on home networks, which would not be a great leap to say they may someday impact IETV-specific O/S design choices made by companies like Samsung and Vizio. Sony is already experimenting with an Android TV and Samsung has already publicly stated that it’s pondering it too. Television is just one example, but a great example of how devices that didn't previously require a Mobile O/S may soon require one, as a result of convergence.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 12 12.7.2010

Industry Report | Financial Services

The Mobile O/S can enable a greater set of uses/features as compared to a device-specific O/S built around a more narrowly defined use case, particularly if the mobile O/S comes up with an ecosystem that has hundreds of thousands of applications. As consumers quickly assimilate that a connected device with a mobile O/S is more functional than a connected device with a more limited O/S or simply a browser, we suspect it could quickly become difficult to sell feature rich connected devices without a mainstream converged mobile O/S, depending on the significance of the new alternative/secondary roles.

On this basis, TVs specifically may hold out longer than other simpler consumer electronics given how much more important the primary experience, watching TV, is over today's secondary experience, IETV. If that traditional use case were to evolve as a result of new apps and functionality, undoubtedly, a mobile O/S would become more compelling. In our minds, IETV hasn’t come as far as it needs to in order to bring about real consumer interest.

That said, we believe TVs (by bringing them under a converged mobile O/S with relevant and new apps) are probably the next important catalyst in this evolution toward a broader and more unifying CE platform that encompasses significantly more devices (discussed in more detail later); however, TVs have historically been very hard to crack with such interactive/internet functionality. Little has stuck beyond the EPG/IPG and DVR in the TV world. Numerous interactive TV ventures have tried and never really taken off as well as second set-top ventures. The next year or two will likely have more failures than successes in this area. However, in the end, we expect one of these mobile O/S players to get the formula right and transition TVs into a new paradigm, well beyond simple Facebook and Netflix widgets.

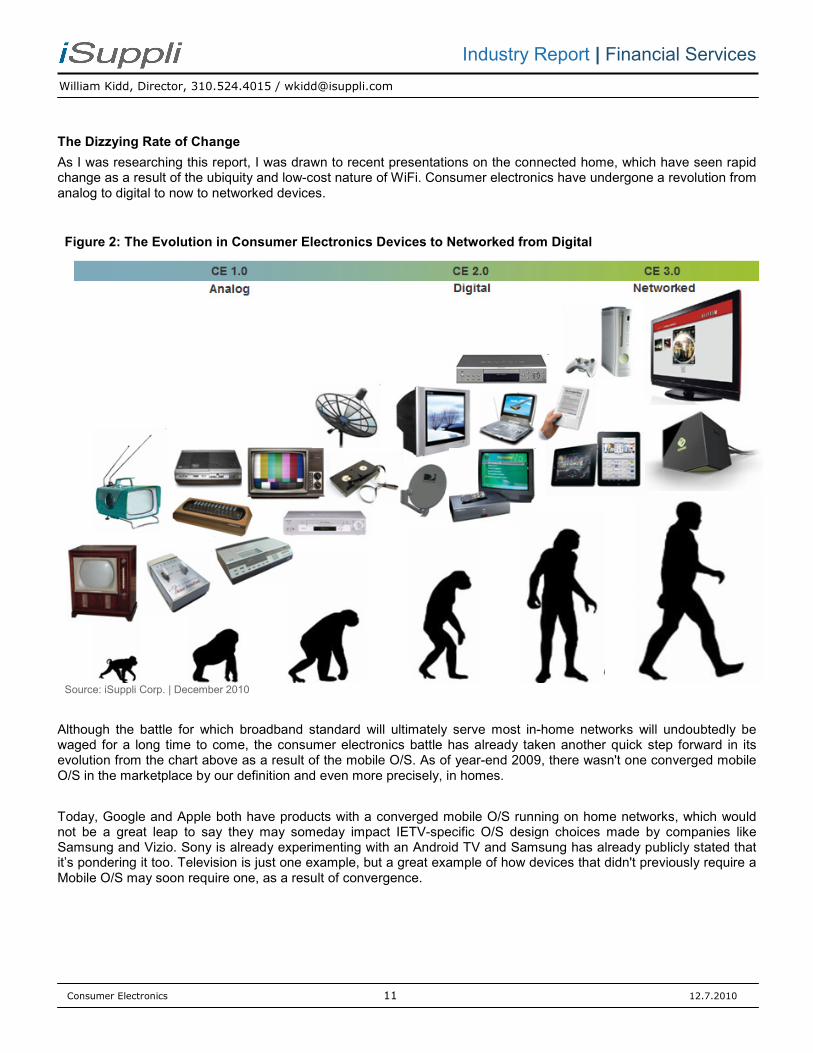

Figure 3: Converging Connected Device Landscape

Source: iSuppli | December 2010

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 13 12.7.2010

Industry Report | Financial Services

O/S Competitive Landscape

Figure 4: Comparison of Leading Mobile O/S

Source: iSuppli Corp. | December 2010 Legend: ○ No support/Not available, ◔ ◑ ◕ Varying support levels; ● Supported; - Undisclosed

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 14 12.7.2010

Industry Report | Financial Services

Nokia

Nokia's Symbian O/S and its latest incarnation, Symbian^3, are the most notable exclusions from our earlier O/S landscape chart. Symbian is the largest smartphone O/S when measured by handset shipments. However, most of the Symbian smartphones in circulation are more akin to the Palm PDA of old than to the user experience represented by the iPhone and Android smartphones. Symbian^3, released in 2010, came a long way in terms of bridging the distance between Nokia and its higher-end smartphone competitors. However, Symbian^3 does not yet seem ready for tablets, the focus of this report.

In the case of tablets specifically, Nokia has had "tablets" for years, but none like the current iPad or what we and others presently mean by the term tablet (meaning a converged mobile consumer electronics device). On those terms and deciphering recent press reports, the general consensus seems to be that Nokia recently tried to launch a "Z500" MeeGo tablet but met with carrier resistance to support it. However, rumors are abundant and facts are scant about the Z500, so it's hard to have any solid takeaways other than Nokia does not yet have a dominant smartphone O/S with Symbian^3 or tablet version of any sort, whether on Symbian^3 or Meego.

Nokia did say in its November 2010 earnings call, however, that it will launch its first MeeGo device in 2011 and indicated they plan to update the market on their strategy in February 2011. We suspect that the device is likely to be a tablet rather than a smartphone, although Nokia has yet to clarify. We base our reasoning on how compelling MeeGo tablet demos have appeared to date. Nokia does have a MeeGo smartphone in the works, according to numerous press reports, with most of that speculation centering around a June 2011 release date, near the next expected iPhone installment.

MeeGo, on top of two capable partners (Nokia-Smartphones; Intel-Processors), does seem to have some real potential as a tablet O/S, but it's hard to say much at this point with the O/S still essentially vaporware; however, videos demoing the alpha version are impressive. For background, MeeGo was made commercially available on the WeTab earlier this year, although the 1.0 version wasn't really commercially viable and lacked the tablet UI, which is now being developed and refined for launch early next year. The one advantage MeeGo may have over the smartphone O/S is that it was essentially designed for tablets from the onset, adding smartphone support along the way. That design difference seems to shine through in its early peeks at its yet to be released tablet UI, which seems very tablet centric.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 15 12.7.2010

Industry Report | Financial Services

Microsoft and Windows Phone 7

Windows Phone 7

With Apple's iOS and Android more the known quantities, Windows Phone 7 got off to a slow start in October 2010 and partly as a result, it has the most room for a positive 2011 surprise, at least in smartphones. That said, Tina Teng, our smart phone analyst is forecasting Windows Phone 7 to lose ground in 2011 relative to other smartphone O/S, forecasting the smartphone category to increase shipments by 30% to 322 million units, ahead of Windows 7's 14% gain. Windows 7 does not yet have a lot of handset OEM backing. Roughly two months after launch, though in the middle of the holiday selling season, there are only 4 Windows Phone 7 smartphones available in the U.S., per Microsoft's site: Samsung Focus (AT&T); LG Quantum (AT&T); HTC Surround (AT&T); HTC HD 7 (T-Mobile). The Dell Venue Pro (not yet available), is expected on T-Mobile sometime during the holiday season. The four available handsets are all priced at $199 including two-year carrier commitments. Samsung is expected to devote more of its smartphone line-up to Windows Phone 7 in 2011, which should help.

The market is still somewhat confused as to what Microsoft will do with Windows Phone 7 as it pertains to tablets. Initially, the impression given from Microsoft was that Windows 7 (not Phone 7) would be used successfully across a wide variety of form factors. At present, most of the compute ODMs seem to be designing tablets around traditional Windows with few if any plans out there for a real competitive Windows Phone 7-based tablet.

(Tina Teng): Microsoft reinvented the smartphone platform and leveraged Microsoft’s other businesses—including Windows Live, Office, Zune HD, and Xbox Live. What truly differentiates Windows Phone 7 from other products is Windows’ tight integration with Microsoft products across different user bases. One base is the enormous pool of Office-product users, and the other is users of game-console hardware for Xbox 360, which has a 24% share in the gaming console market. Before any Windows Phone 7 products become available on the market, Microsoft has announced 63 Xbox LIVE games on Windows 7. What puts the Windows Phone 7 at a disadvantage is the lack of backwards compatibility with Windows Mobile 6 and 6.5. Applications purchased for Windows Mobile cannot run on Windows Phone 7, and consumers will naturally not want to buy the same application or software twice. To provide a uniform WP7 experience, Microsoft is reportedly putting restrictions on UI design, which OEMs use for differentiation. iSuppli expects that Microsoft will eventually become more flexible if such restriction is the main roadblock to WP7 adoption, and Microsoft will gradually incorporate some UI native features into WP7.

Traditional Windows and Tablets

Anyone can see that Microsoft's advantages in tablets would come from its dominance of the PC O/S market. In January 2010 at CES, Microsoft CEO's Steve Ballmer highlighted a few Windows-driven slate PCs in development for 2010, highlighting an HP prototype tablet running Windows 7. Almost a year later, neither a dominant-Windows tablet product and/or tablet tailored O/S exist. Windows Phone 7 clearly isn't yet a tablet O/S, much in the same way Symbian^3 may power Nokia's N8 but isn't a tablet O/S. Ultimately, it turns out that the HP prototype touted at CES was also another tablet device that never really made it to market.

In October 2010, Microsoft CEO Ballmer publicly talked about the need for tablets to feature Intel's next generation Oak Trail processor for longer battery life as well as the possibility of using Windows Phone 7's touch UI in tablets, which many view as a departure from the company's strategy to rely on regular Windows for tablets. As an aside, a quick look at the Windows tablets now in the market place reveals battery life as an issue, with most possessing a range of 3-5 hours of battery life (vs. ~10 hours for the iPad). Intel's smartphone-based processor competitors had a jump on battery efficiency. Battery life should improve for Microsoft tablets in 2011, considering Intel is now reportedly in production of its Oak Trail platform Atom-based processors (Electronista, Nov. 24, 2010). New Oak Trail-based tablets are expected to be released in January 2011 and they are likely to be running the MeeGo O/S (and Windows too). Please refer to 10.15 in Chapter 7 for more details on Intel’s Oak Trail processor.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 16 12.7.2010

Industry Report | Financial Services

In a world where the tablets are a relatively small sliver of the combined smartphone and PC markets, the implication is that tablets play a unique role, such as media consumption. Surely, this view is largely based on the iPad, which makes it easy to envision how tablets will play an important role as a third or fourth device in a home. Thus, the device's use case almost by default is more specialized. In this type of market, Windows could struggle, as it’s really not well suited to do anything new in a tablet form factor; consumption-only is not Windows’ strength. This scenario also fairly reflects what most imagine 2011 will be for tablets in general and the rationale behind Microsoft’s struggles specifically. Our iSuppli “base case” assumes roughly 20mn shipments of Windows O/S tablets in 2014, discounted because our analysts do not believe they have the basis to forecast more Microsoft success without Microsoft having a fully evolved converged mobile O/S.

However, we don’t think 2011 is a good portrayal of the future of tablets and especially Microsoft’s competitive footing in tablets. If the demand for tablets continues to be strong, as most expect, tablets, when bundled with a keyboard and mouse, may quickly move from a new device category to being an evolutionary transition for notebook and netbook form factors. In this way, tablets could start to significantly cannibalize older form factors, more so than we or others presently forecast. In this scenario, Windows might do extremely well as an operating system for tablets, given that the role of the tablet wouldn't simply be for a specialized use case (as media consumption), rather all the traditional creation (vs. consumption) uses we associate with notebooks and netbooks. Thus, purchasers would want and be able to network the tablet device with their desktop (giving Microsoft a device ecosystem in tablets to leverage) and use the tablet more heavily for work, study and play than tablets running smartphone O/S, bringing Microsoft's advantage in PC applications software more into play.

We support our view with the following additional considerations. nVidia CEO Huang is on the record saying that “if you connect a wireless keyboard and mouse to a tablet, the difference between a tablet and notebook is pretty marginal, arguing that tablets will be quite disruptive to notebooks and entry-level desktops.” Another aspect to consider is that Microsoft didn't really write Windows Phone 7 for tablets (despite releasing the O/S well after the iPad’s launch). It easily could have called it a tablet UI if it wanted to use a smartphone UI to address tablets. Obviously, Microsoft is signaling that it does not want to follow Apple and Android down this path. Thus, Microsoft wants to address tablets directly through a future release of Windows (or Tablet version, but our bet is on traditional windows). While most simply see Microsoft as behind in its approach to tablets and undoubtedly in many respects it is, it does suggest Microsoft’s approach is very measured. Case in point, Microsoft was likely thoughtful when it chose not to take its newly released smartphone O/S and call it a mobile O/S as the prior version was labeled. It also refrained from announcing to the world that it has a tablet solution ready, despite having a smartphone O/S like many of the companies now attempting tablets. In fact, Microsoft changed the name from “Windows Mobile” to something more restrictive, “Windows Phone”. Given the power of its installed base and the need for content creation to be part of an extremely large tablet opportunity, we see promise in Microsoft’s approach. We surmise that Microsoft sees a very large future for tablets and doesn’t want a marginal and incompatible (to Windows) smartphone O/S as its tablet offering. In iSuppli Financial Services, we give this scenario (tablets to exceed expectations, cannibalize more form factors and Microsoft to be ultimately better positioned than now perceived) a far greater likelihood than most industry analysts, whether internal or external. On this basis, we believe the likelihood of Microsoft being able to do quite well with tablets is high, particularly if it’s able to deliver a future iteration of traditional Windows that also is capable of powering a full tablet UI. A tablet UI coupled with full Windows compatibility, running the same or at least a fully compatible version with desktops and notebooks would be a game changer in the tablets space. And when our software future is coupled with nVidia CEO’s hardware argument (that a tablet will essentially be a notebook), you end up with a device capable of content and creation with an improved touch interface that is 100% compatible to your existing work and play applications. On this basis, we can easily buy into lofty tablet projects and even wonder if perhaps they are too conservative. However, in this scenario, much of this growth would also simply come from cannibalization of the existing mobile PC form factors, allowing traditional PC OEMs and ODMs to be well positioned to continue their roles and retain share.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 17 12.7.2010

Industry Report | Financial Services

HP, Palm and WebOS

Although Microsoft Ballmer started 2010 by hyping an HP prototype slate running windows (that was never released), we're now ending 2010 with the expectation that HP will release both a WebOS-driven tablet and Windows tablet in 2011. It's hard to say what to expect when very little has been leaked about the planned WebOS tablet. Given that we've already seen what's possible with both Windows 7 and Windows Phone 7 as operating systems (sans the battery efficient Oak Trail processor), our excitement around HP delivering a Windows-based tablet in 2011 has definitely lessened. Like RIM, another tablet hopefully with a proprietary O/S, small user base and a comparatively small ecosystem, HP has the challenge of creating an exciting mobile O/S for a new tablet, motivating consumers and enterprises to buy it, while convincing apps developers that the aforementioned steps will come together without fail. It’s not an easy roadmap to follow, let alone with a relatively new proprietary O/S, even if full featured.

(Tina Teng) The market was impressed with the transformation that Palm made from Palm OS to WebOS 1.0 in 2009. After Apple brought out its iPhone in 2007, Palm introduced the Palm Pre—the first WebOS-based device. The Palm Pre was the first to introduce some new features: multi-touch support, aggregated views of all social information, a sleek user interface, universal search, and a wireless charging station. However, Palm had a difficult time expanding partnerships with carriers, and its limited variety of apps is a drawback to consumers. Launched in 2009, by July 2010 Palm’s app store (Palm App Catalog) offered only 3,000 official available applications. Even with the launch of a well-developed WebOS, Palm was still unable to secure its position and profitability. Hewlett-Packard (HP) came to rescue Palm by acquiring its advanced WebOS. With the $1.2 billion deal, HP intended to leverage WebOS’s capability to penetrate into other cloud-based devices and services, including medical equipment. HP brings improved multitasking, Node.js, and the HTML5 to WebOS 2.0, which will be available in late 2010. Developers can now write WebOS applications and also service in JavaScript through the built-in Node.js runtime environment. However, it is still questionable whether WebOS in smart phones can gain any market share under HP’s leadership.

Please refer to 04.30 in Chapter 7 for more details on HP’s acquisition of Palm.

As an aside, HP released the HP Slate 500 Tablet PC in the fall of this year, operating on an Intel Atom processor using Windows 7 Professional. It features an 8.9-inch display, weighs 1.5 lbs, 64GB flash storage and reportedly has 5 hours of battery life. Price $799 (no 3G connectivity). The device is a good representation of what a high-end Windows tablet looks like at this point in time.

Blackberry OS

(Tina Teng) PlayBook, RIM’s recent answer to the tablet market, is based on QNX Neutrino architecture, and prompts the industry to wonder whether RIM will gradually migrate smart phones to its BlackBerry Tablet O/S in the near future. The company already offers a new application development platform that broadens HTML5, CSS3, and JavaScript support; the developed applications can run on both the Tablet and BlackBerry O/S.

RIM launched its first touch-screen enabled smart phone with multi-touch capability based on the BlackBerry OS 4.7 in 2008; the company’s innovative approach, SurePress, included clickable touch screens, but reception was resentful rather than favorable. Although the next release, Storm2, offered a significantly improved SurePress (based on OS 5) in late 2009, the company was unable to make big splash, because it failed to recognize core features desirable in the smart phone market. Recently, RIM invested R&D in a major UI makeover of the OS 6.0 release, and intends to draw in consumers by offering more gesture capabilities, social media integration, and support for all IMs. The new OS also provides universal search, implemented widely in other OS platform.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 18 12.7.2010

Industry Report | Financial Services

Software vs. Hardware

While we could attempt to quantitatively prove using our teardown data that the hardware capabilities/features and overall bill of materials (BoM) value is not a major determinant in the success or failure of a smartphone and by extension, a tablet, the point is so obvious that we hope we can skip the exercise. Most high-end smartphone BoMs come in at near $180 today and have little substantive difference in features, particularly to the consumer. As we doubt consumers are motivated, given the large number of features on any one smartphone, by a slightly larger screen, more efficient battery, processor brand or megapixel count. Surely, if one smartphone is excellent on many of those elements, it would be compelling from hardware alone. However, that really isn't typically the case since the handset makers and compute OEMs rely on essentially the same set of semiconductor component and display suppliers as well as the same handful of EMS players. Thus, it's hard to differentiate on hardware, when hardware is the least proprietary element of the puzzle. Two exceptions:

Samsung, the most vertically integrated player (memory, AMOLED screens, hummingbird processor), is able to have more in-house control of its BoM compared to any other OEM. And for the moment, Samsung has access to AMOLED screens, when most others do not. However, we believe it's a stretch to argue that Samsung's Galaxy line is successful as a result of its hardware advantage/vertical integration, though the Galaxy smartphones do have nice screens. Even Samsung's success to date with smartphones and tablets, at least as it pertains to the consumer purchase decision, isn't driven by a hardware hard advantage. If you compare an HTC EVO to a Samsung Galaxy smartphone, it's difficult to derive a meaningful hardware advantage for Samsung. However, if you look at the Galaxy Tab, the relative advantage is obvious. Samsung was the first to truly mimic Apple’s approach to the iPad. Samsung did this by simply replicating its smartphone O/S experience on its tablet, unifying the experience. Unfortunately, Android isn't quite ready for tablets, but that's another matter.

Apple has its A4 processor and knack for product design. While Apple was first to this iteration of mobile processors with the A4 in the iPad, it may have a somewhat proprietary ARM processor (that is still earning high marks on battery life), but it's hard to argue that it maintains a proprietary edge. There are numerous examples of non-Apple smartphones and even tablets now running and rendering websites faster than Apple devices. That said, Apple does have a scale-driven cost advantage as it leverages the same processor across so many different devices; however, many Android devices should see similar scale benefits. Product design is just too subjective to assess in this context but surely Apple gets high marks.

To date, Apple is highly differentiated by its 4:3 screen choice. Many questioned the wisdom of this selection when the iPad was first introduced. Au contraire. While 16:9, the preferred format of most of the competitors to date, is ideal for movies, it is a far less desirable configuration for eBooks, eMagazines, web surfing, and a host of other multi-media applications. Hold it up next to a book and it’s a natural match with the printed page, providing a degree of instant familiarity to the end-user. With respect to the competition's 10-inch screens due out relative early in 2011, we are expecting most to be 16:9.

Rhoda Alexander, Tablet Analyst

While the A4 contributes to the iPad's solid battery life (10 hours vs. the Samsung Tab's 7 hours), iPad consumers have a good idea of what they're purchasing before they buy it because many likely come with familiarity to Apple's iPhone O/S and iTunes, its commerce and content management ecosystem. As a result, there are significantly more apps and content available on the iPad than any other like tablet device, none of which are due to hardware. Our point is that consumers know this going in before purchase. They also know if they already own an Apple device, the new device purchase can be managed from the same software that they already use, allowing the new Apple device to leverage content, purchases and organization from an existing device with no incremental effort. Hence, the O/S and ecosystem are big draws, since the software more than unique hardware differences translate into tangible applications and uses.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 19 12.7.2010

Industry Report | Financial Services

Open Source vs. Closed Source

Figure 5: Leading Open Source Mobile (Tablet) O/S

Source: iSuppli Corp. | December 2010

If history is any lesson, open vs. closed is largely an argument around timing. It would be hard to argue that Microsoft would have done better with Windows or Apple as its O/S if either were open source. However, Google's approach to battling an entrenched and for the moment still superior operating system with its open source project has been nothing short of impressive. Consider Android's problems: 1) still a smartphone O/S (tablet version not yet ready); 2) O/S fragmentation due to OEM customization (e.g., proprietary user interfaces) and monolithic kernel design; 3) carrier confusion with competing apps stores and unique interfaces that may feature favored apps (e.g., Verizon using Bing for searches on its Android devices); and 4) many Android key apps/functionality are not yet on par with Apple's (since Google allows app developers to compete over core functionality such as an email client, visual voice mail, etc.); FaceTime is poised to be an example of this, particularly if Apple puts that app up for wider release (please refer to 09.10 in Chapter 7 for more details on Android fragmentation).

A telling anecdote that brings home Android’s fragmentation issues is captured by the saga of Angry Birds, one of the top selling mobile games. On iTunes alone, Angry Birds has garnered 30 million downloads at $0.99 per as of Nov. 29, 2010). First released on iTunes in December 2009, Angry Birds quickly became a mainstream sensation, topping Apple’s UK App Store in Feb. 2010 and the US App Store shortly thereafter where it remained until October 2010. The game was then ported to the Android platform in October, 2010, where it was downloaded over 1 million times in the first 24 hours of release. As successful as Angry Birds was on the Android, soon after its Android debut, lower-end Android devices experienced severe performance issues running Angry Birds. According to Angry Birds developer Rovio, who wrote in its blog: “we worked hard to bring Angry Birds to even more Android devices. Despite our effort, we were unsuccessful in delivering optimal performance.” In the end, the company decided to develop a lighter solution to run Angry Birds on lower-end Android devices. Undoubtedly the Angry Birds developer was grappling with Android fragmentation, the challenge being to find optimal performance on one device, while struggling with that same problem across many devices. In the last earnings call, Apple CEO Steve Jobs referenced the struggles of another Android developer, who tweeted they had to contend with more than 100 different Android versions across 244 handsets. In that context, it’s easy to understand why the Angry Birds developer ultimately had to solve some of its Android problems by making a simpler version for some Android handsets. These examples bring home Android’s fragmentation struggles.

Even so, Android has quickly caught up to Apple in global smartphone shipments by our count and is set to surpass Apple in 2011 or 2012. In the U.S. alone, many sources are reporting that Google's Android has already passed Apple in terms of quarterly sales. Apple also has iPads and iTouch devices not in those smartphone tallies which definitely prop up Apple's user iOS base. Nevertheless, with an arguably inferior product in many key respects, our point is that Android seems on track to pass Apple in smartphones, barring disruption from another new O/S entrant. Android's strength is that with so many more partners than Apple on the handset side, such as Samsung, HTC, Motorola, LG and Dell, it's able to penetrate more carriers and reach more end users. Android is also more diverse in its approach to the market, as a result of its diverse set of partners, whereas Apple arguably is running a lower volume, more premium model.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 20 12.7.2010

Industry Report | Financial Services

Therefore, if Google didn't start, fund and drive Android as an open-source project, it would likely never have received the handset OEM support to become successful. It was also that simultaneous belief in a collective effort by Google and its partners that a combined approach was the only one likely to catch Apple, and that their proprietary approaches, if attempted on their own, may have worked against one another. Intel and Nokia were obviously taking notes, as MeeGo is open source, as well as the Nokia-led, Symbian O/S.

However, Google's ability to profit from its O/S is somewhat different than Nokia's with Symbian by nature of it being Google:

Google is somewhat unique in that it profits from growth in search in general as well as mobile search from essentially any handset and O/S given Google Search, YouTube and other properties. Android phones serve to increase the odds that the traffic goes to Google. Another benefit of having more Android devices is smaller payments to Apple to keep Google as the exclusive search. Google's display network, which serves non-Google properties, also benefits from increases in general internet traffic.

It doesn't end there, Google dominates targeted advertising with AdSense, which Apple is trying to take on with iAds. Android's success only helps. AdSense is a market leader in both web-based advertising and in-app advertising. Thus, although Google AdSense can make money off any smartphone O/S, it helps reduce the risks of competing O/S-born advertising competitors, like iAds, if Android is more successful.

Both PC and Smartphone OEMs see the potential in selling more units as converged CE devices grow and evolve their respective markets. Smartphone players, which have historically avoided software/platform competition, are now wary of their industry going the way of the PC industry, where Microsoft and Intel made a killing while PC OEMs were increasingly commoditized. It wasn't that long ago where a mobile handset maker could sell a feature phone almost irrespective of the O/S. Nokia's reluctance now to give up control of its O/S and join Android is undoubtedly based at least somewhat on the history of PC OEMs. Of smartphone OEMs, Nokia also has the most to lose given its dominant market position in mobile handsets. Handset OEMs like HTC have everything to gain, which is why it’s not surprising to the upstarts looking to ride the early O/S leader, Android.

HP's O/S perspective has to be somewhat similar to Nokia's, though HP has more to gain than lose. However, the primary difference is that Apple has a very refined smartphone O/S, maximizing the capabilities of the platform, a platform based on taking a PDA to another level. With smartphones, Android has succeeded by merely trying to replicate Apple's achievements. Tablet O/S entrants face many of the same competitive challenges that a smartphone O/S rival would beyond the O/S itself, such as building an ecosystem with content and apps. The opportunity to innovate is clearly greater with tablets than smartphones, if only because Apple never really tailored its smartphone O/S for the iPad. As we have already said, citing MeeGo, the ability to impress and wow with a new tablet O/S is surely greater than trying to exceed what Apple has already accomplished in smartphones.

Figure 6: Some Famous Open Source Success Stories

Source: iSuppli Corp. | December 2010

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 21 12.7.2010

Industry Report | Financial Services

Interconnectivity

It's hard to discuss interconnectivity without bringing up the ecosystem, which is our next chapter. However, it's an important topic particularly as more consumer devices, such as TVs and automobiles, take on O/S originally born from smartphones and tablets. And since the O/S typically runs on disparate consumer electronics devices, some discussion is warranted in our O/S chapter.

Originally, Apple's iPhone was launched with a new smartphone O/S. However, at launch, Apple was able to leverage its iPod user base by offering new iPhone users 1) content sharing, through the same iTunes control point, between Apple devices; and 2) an ecosystem, vis-a-vis iTunes, already rich in music and video content. However, Apple's devices really never communicated with one another. It was iTunes that made the process of adding additional Apple devices easy and advantageous.

However, Apple's devices still weren't interconnected. Apple is just starting to show the advantages of its device ecosystem (e.g. interconnectivity of Apple devices) through features like AirPlay and its Remote app, and could take this advantage to another level if it expands FaceTime to its entire device ecosystem beyond its iPod Touch and iPhone. An early first step in the process of promoting interconnectivity was Apple's Remote app, which allows the iPhone to control iTunes running on a PC, enabling you to control audio and video, assuming someone wants that content originating from a PC, irrespective of where one outputs it. However, that's the downfall, as most iPhone/iPad users probably aren't equipped to have iTunes as their media entertainment center, limiting Remote's appeal. With that first step, Apple has taken a very large step forward with Airplay and Apple TV. Airplay is an O/S feature, which has been upgraded across the iOS platform, enabling Apple devices such as the iPhone, iPad and iTouch to instantly take any content (such as movies or pictures) or apps (such as an action games) on their device and easily display it on their television, assuming Apple TV is also equipped. With iOS 4.2, Apple added AirPrint, the ability to wirelessly send print jobs. It's obvious that interconnectivity promotes stickiness, similar to how some of Apple's early iPhone subs may have been pre-sold on the platform as a result of already being wed to iTunes’ device interface as a result of their iPod.

So far, Microsoft hasn't really been able to use Windows to leverage its smartphone success, as Apple has been able to do with its suite of CE devices, since its phone operating system does not truly interconnect with PC devices in a way that's materially different from other incompatible smartphones, though the latest Windows Phone 7 does have an Office app. Today, for Microsoft, the leverage from PC to Smartphone is still largely branding and only marginally in the way of increased functionality from the association with Windows. Microsoft does have its Zune ecosystem, which is interesting (and provides leverage) for smartphones and tablets; unfortunately, Zune never had much of a user base, leaving Microsoft without the customers to leverage, but with a relatively strong commerce/content ecosystem.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 22 12.7.2010

Industry Report | Financial Services

II. Ecosystems

Commerce/Content Portals

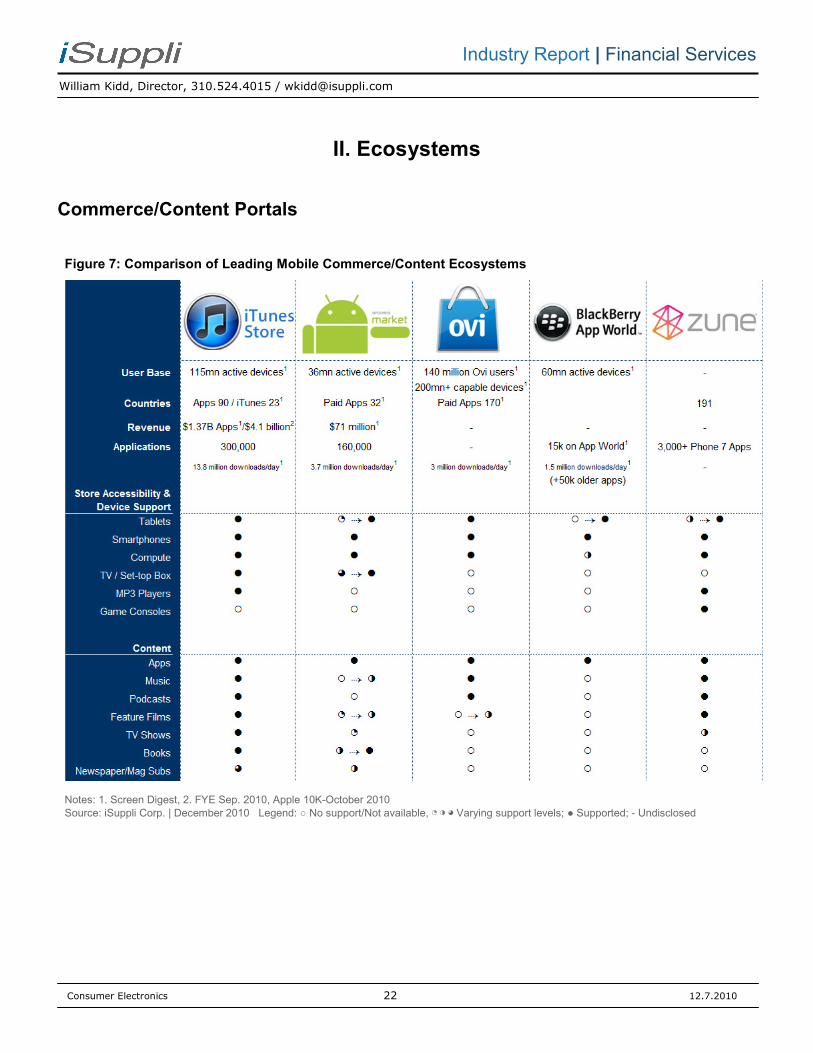

Figure 7: Comparison of Leading Mobile Commerce/Content Ecosystems

Notes: 1. Screen Digest, 2. FYE Sep. 2010, Apple 10K-October 2010

Source: iSuppli Corp. | December 2010 Legend: ○ No support/Not available, ◔ ◑ ◕ Varying support levels; ● Supported; - Undisclosed

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 23 12.7.2010

Industry Report | Financial Services

The term ecosystem is used so much in technology today that in some ways the term has evolved into an over- generalization, particularly since the term means something different to each and every one of the major tablet players.

To Google, ecosystem describes its internet presence and how its search, YouTube, AdSense, DoubleClick, Android and other properties work together to drive traffic across the various internet platforms. When talking about the Android ecosystem, this presumably means its commerce/app store, though we should point out that Android Market has little in the way of media content (sans Amazon music); content in the case of Android Market means apps for smartphones. Android is trying to address these weaknesses with recent reports saying that it’s working on adding books.

For Apple, ecosystem could mean its device ecosystem, and how iTunes (the software program, not the commerce portal) can manage those separate devices. Apple’s ecosystem could also describe its App Store, when being compared to Android, or its iTunes software client and commerce portal, which includes the App Store but has movies, TV shows, books and other content. “Among tablet manufacturers, Apple’s ability to serve customers through its own vertically integrated content store and billing platform also makes it unique,” Jack Kent, Mobile Media Analyst – Screen Digest.

The goal of this exercise is to point out that all of the companies vying to capture some of the tablet market have some sort of ecosystem, but the term can be used so nebulously that it loses almost all meaning, at least in an analytical context. In this chapter, we want to differentiate ecosystems by their content and commerce capabilities. Other relevant metrics such as installed base (which is different from unit sales) as well as the commerce/content portal’s device reach are also meaningful factors, which we assessed in the prior chart for some of the major ecosystems.

The (connected) device ecosystem like AirPlay on iOS, enabled largely by the O/S was addressed in the prior section, so this chapter does not cover interconnectivity and the power of a CE product suite. The type of vertical and horizontal web-property collection which describes Google is not really the focus of this section either, as we’re focused keenly on the mobile ecosystem, as it pertains to differentiating the tablet at/before sale and increasing customer utility thereafter.

William Kidd, Director, 310.524.4015 / [email protected]

Consumer Electronics 24 12.7.2010

Industry Report | Financial Services

Smartphone ≠ Tablet

Apple’s iPad has a very mature ecosystem in iTunes, which was launched in April 2003 (Windows – October 2003). iTunes also hosts Apple’s App Store. iTunes features a very robust Hollywood catalog and music library, most of which was built before the iPhone, in support of iPods. iTunes is supported by Mac and Windows-based software clients, which provides (1) improved accessibility to the store versus the limitations of a web or smartphone app interface; (2) PC-based access (expanding the use potential substantially beyond iPhone, iPads, etc.) to media content (which most Smartphone ecosystems don’t offer, even if they possess a limited PC client, since they only have smartphone apps to sell); and (3) a unified platform for other CE devices to interface with and access content. From an evolution standpoint, with the iPhone, iTunes picked up its App Store building on the music/film library with the iPod as a foundation. Jack Kent, Mobile Media Analyst Screen Digest adds, “Apple’s ability to build a market for paid mobile applications from an audience that already used and trusted its iTunes billing system (which provided a wealth of customer credit card details) has been vital.” When the iPad rolled out in April 2010, Apple focused on adding magazines and newspapers specifically for the iPad. And when Apple TV was launched, iTunes got cheaper TV shows ($0.99) and social networking. Our point being that iTunes was designed to serve a large number of devices, picking up content along the way. Didn’t they say Rome wasn’t built in a day? Apparently, iTunes wasn’t either.

Why Google Lost the Beatles to Apple, ZDNet November 2010

Amazon and Google didn’t stand a chance. This says a lot, actually, about the market position of the iPhone (and the iPod and Apple TV, although these are a bit less important to Google). If all of your music lives in iTunes because Apple so thoroughly dominates this market and you bought an iPod 3 years ago, what sort of phone are you going to buy? Maybe an Android if you have some compelling reason to do so, but the iPhone starts looking awfully attractive when you’d like to manage all of your digital content in one place.