Embed Size (px)

Citation preview

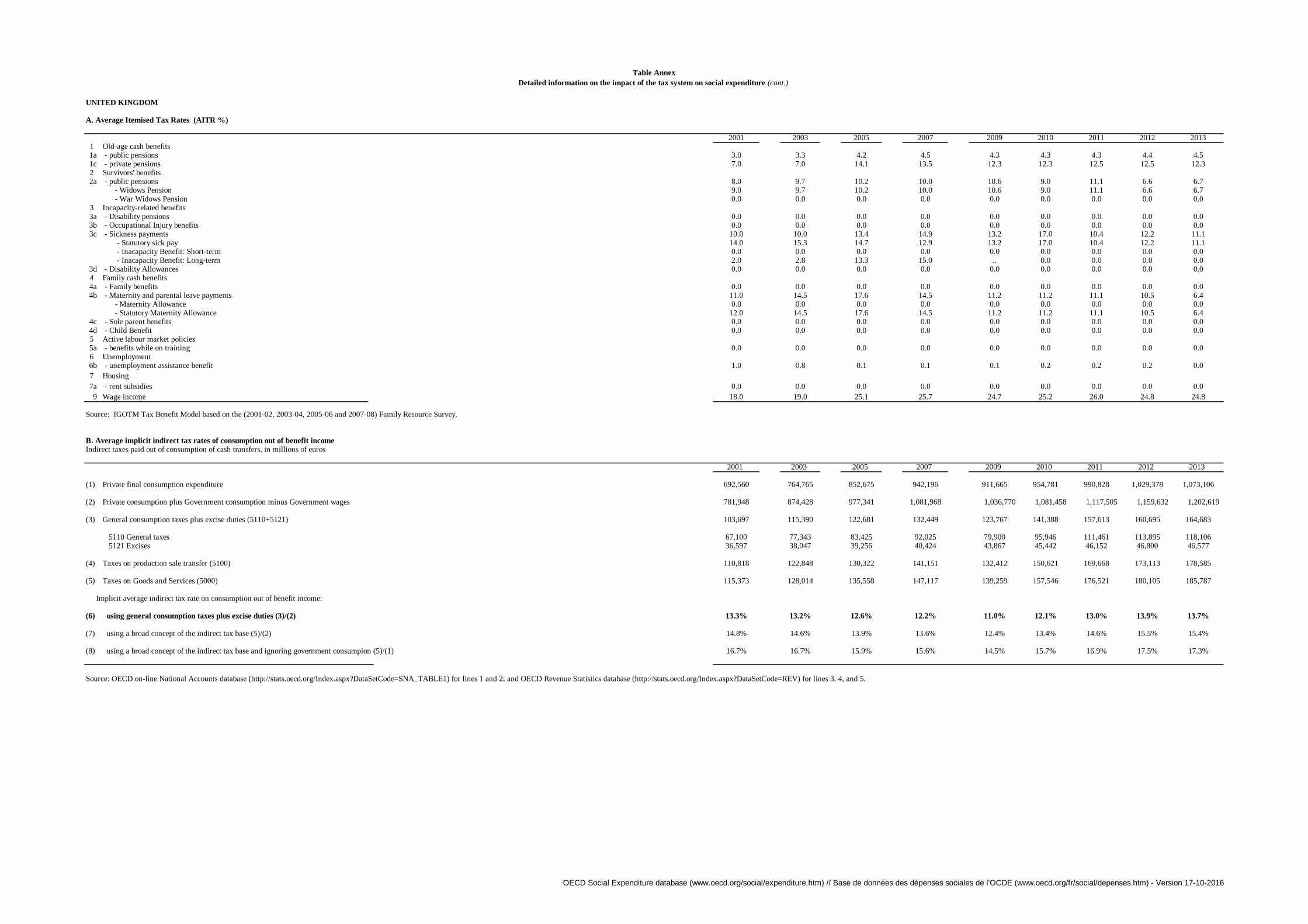

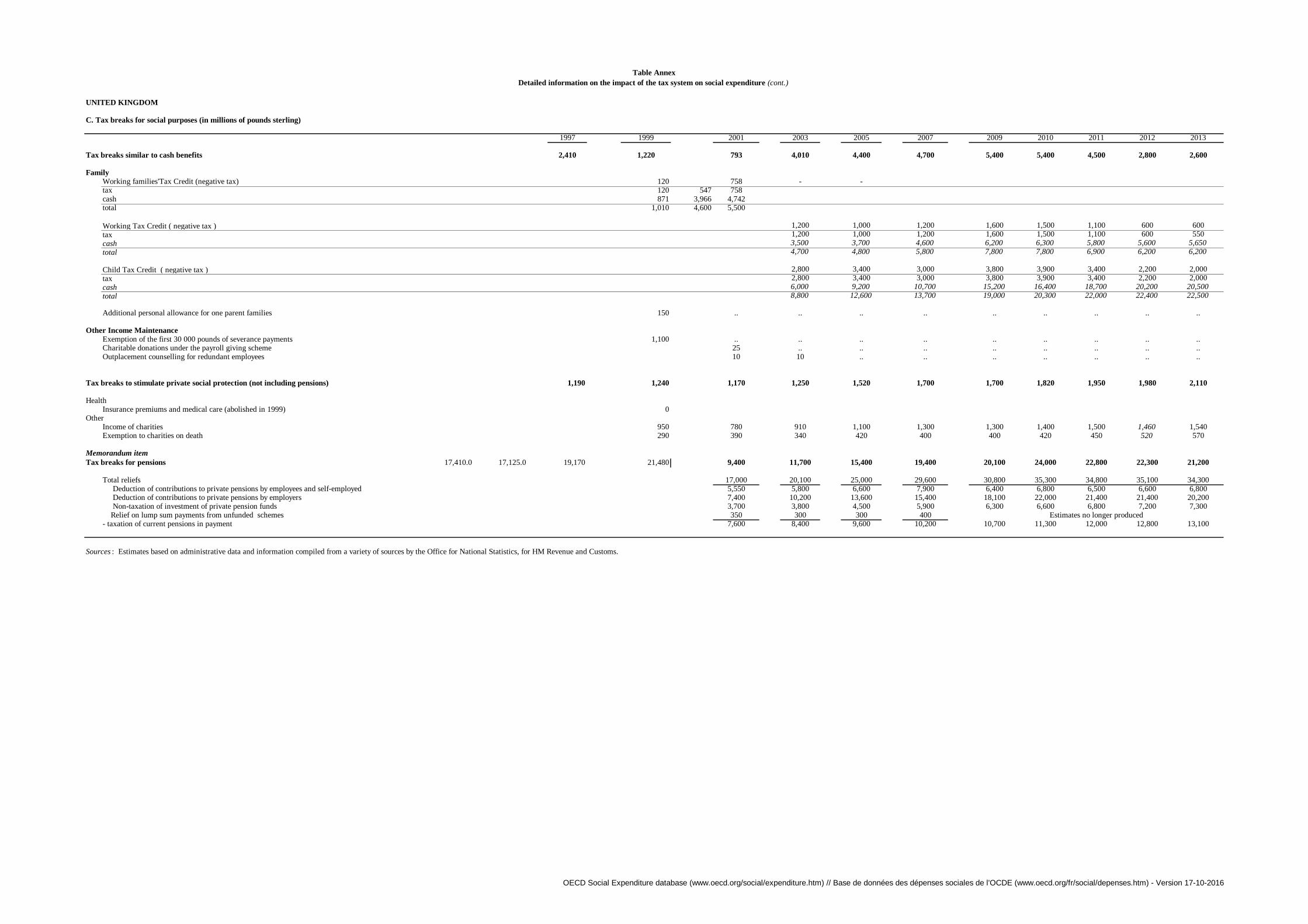

Table Annex: Detailed information on the impact of the tax system on social expenditure

A. Average Itemised Tax Rates (AITR %)

B. Average implicit indirect tax rates of consumption out of benefit income

C. Tax breaks for social purposes

Missing values are presented as follows:

m data not available;

a data do not exist;

x data included in another category.

SOCX Manual/MethodologySee Part II. (p.88) OECD Social, Employment and Migration Working Papers No. 124, October 2011: “Is the European welfare state really more

expensive? Indicators on social spending, 1980-2012 and a manual to the OECD Social Expenditure database (SOCX)"

II.4. Net (after tax) social expenditure ................................................................................................. 103

www.oecd.org/social/expenditure.htm

AUSTRALIA

A. Average Itemised Tax Rates (AITR %)

2001(a)

2003(a)

2005(b)

2007(b)

2009(b)

2010 2011(d)

2012 2013 2014

1 Old-age cash benefits

1a - public pensions

Age Pension 0.38 0.03 0.84 0.12 0.03 0.05 0.07 0.05 0.08

Wife's Pension 0.38 1.25 0.14 0.07 0.06 na na na na

Widow's B Pension 0.26 0.77 0.67 0.67 na na na na na

1b - early retirement benefits

1c - private pensions

Superannuation pension 16.83 15.07 13.58 1.87 1.38 1.80 1.84 1.70 1.29 1.18

Superannuation Lump Sums 2.66 10.45 9.50 0.31 0.23 0.34 0.34 0.43 0.24 0.19

2 Survivors' benefits

2a - public pensions

Veteran's Service Pensions 0.68 0.00 0.54 0.21 0.08 0.10 0.12 0.05 0.07

3 Incapacity-related benefits

Disability Support Pension 0.02 0.00 na na 0.36 0.36

3c - Sickness payments

Sickness Allowance (c) 0.45 0.09 0.05 0.00 0.01 0.10 0.12 na na

4 Family cash benefits

4a - Family benefits

Parenting Allowance 1.03 1.49 1.44 0.24 0.06 0.10 0.12 0.11 0.11

Partner Allowance 0.17 1.02 0.61 0.14 0.13 na na na na

Carer's Payment 0.00 0.19 0.31 0.00 0.01 0.14 0.20 0.16 0.23

4c - Sole parent benefits

Sole Parent 0.64 0.92 1.43 0.72 0.41 0.42 0.50 0.42 0.52

Widow Allowance 0.00 0.05 0.05 na na

6 Unemployment

6b - unemployment assistance benefit

Unemployment Benefits 1.10 0.81 1.11 0.33 0.13 0.55 0.67 0.14 0.19

9 Wage income 23.59 24.63 23.78 22.48 20.88 20.49 21.15 22.79 23.54

(e) Data is reported for the financial year commencing on 1 July of the year indicated and finishing on 30 June of the following year.

(f) Data is unavailable for 2012 as the current micro-simulation model does not provide information for 2012-13.

Sources: CAPITA distributional model. Revenue Group of The Treasury, NZLtralian Government.B. Average implicit indirect tax rates of consumption out of benefit income

Indirect taxes paid out of consumption of cash transfers, in millions of NZLtralian dollars

2001 2003 2005 2007 2009 2010 2011 2012 2013

(1) 437,841 502,035 566,955 663,844 719,001 761,638 801,183 835,826 878,289

Private final consumption expenditure

(2) 492,080 563,115 638,585 754,264 822,710 872,123 919,502 951,493 998,305

Private consumption plus Government consumption minus Government wages

(3) 48,674 57,019 62,882 69,843 73,172 76,018 76,329 77,887 83,291

General consumption taxes plus excise duties (5110+5121)

28,180 35,123 40,086 45,486 47,800 49,329 50,004 51,462 56,819

5110 General taxes 20,494 21,896 22,796 24,357 25,372 26,689 26,325 26,425 26,472

5121 Excises

(4) 60,440 69,938 75,988 85,022 88,585 92,038 94,210 97,072 103,678

Taxes on production sale transfer (5100)

(5) 66,219 76,724 83,441 93,645 98,188 103,425 105,931 116,712 123,516

Taxes on Goods and Services (5000)

Implicit average indirect tax rate on consumption out of benefit income:

(d) 2011 figures have been updated using revised estimates published in the 2015 Tax Expenditure Statement.

Table Annex

Detailed information on the impact of the tax system on social expenditure

The AITRs for wage income, superannuation pensions and superannuation lump sums were calculated using a sample file of NZLtralian tax returns in 2001. All other AITRs were calculated using the STINMOD model, a static microsimulation model developed by the National Center for

Social and Economic Modelling (NATSEM).

(a) The AITRs were obtained by calculating the amount of tax paid in aggregate with and without the income streams. The difference between the taxes paid was then divided by the value of the income stream to reveal the value of the AITR.

(b) Tax paid on an income stream was calculated by dividing income from stream by total tax liability and then multiplying it by total tax paid. This amount was then divided by the total income from stream to calculate the AITR. This methodology has been adopted to align with the

instructions provided by the OECD.(c) Figure is derived from a small sample of observations and caution should be taken with interpretation.

(6) 9.9% 10.1% 9.8% 9.3% 8.9% 8.7% 8.3% 8.2% 8.3%

using general consumption taxes plus excise duties (3)/(2)

(7) 13.5% 13.6% 13.1% 12.4% 11.9% 11.9% 11.5% 12.3% 12.4%

using a broad concept of the indirect tax base (5)/(2)

(8) 15.1% 15.3% 14.7% 14.1% 13.7% 13.6% 13.2% 14.0% 14.1%

using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1)

C. Tax breaks for social purposes (in millions of NZLtralian dollars)

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

Tax breaks similar to cash benefits (f) 2,389 1,728 3,306 3,896 4,510 4,533 4,877 4,941 4,759 4,748

Family: 376 385 430 470 585 560 500 370 140 120

Tax offsets for taxpayers with dependants 16 15 20 - - - - - - -

Tax offset for housekeeper who cares for a prescribed dependant 360 370 390 - - - - - - -

Tax offset for dependant spouse, child-housekeeper and housekeeper who cares for prescribed dependent (d) - - - 430 585 560 500 370 140 120

Tax offsets for taxpayers supporting a parent, parent-in-law, or invalid relative - - 20 40 - - - - - -

Other areas: 2,013 1,343 2,876 3,426 3,925 3,973 4,377 4,571 4,619 4,628

Medical expenses tax offset 150 220 305 390 460 530 510 540 390 230

Exemption of certain income support benefits, pensions or allowances - - 820 690 590 770 880 500 550 570

Exemption of Utilities Allowance and Seniors’ Concession Allowance (g) - - 14 38 114 19 1 - - -

Exemption of payments made under the First Home Owners Grant Scheme - - 285 325 685 730 260 290 275 185

Income averaging for authors, inventors, performing artists, production associates and sportspersons - - 7 8 14 16 18 23 26 29

Exemption of post-judgment injury awards in personal injury compensation cases - - 2 2 2 3 3 3 3 4

Capped taxation rates for lump sum payments for unused recreation and long service leave 210 190 150 105 105 105 145 200 220 240

Concessional treatment of non-superannuation termination benefits 990 320 310 1,200 1,450 1,300 2,000 2450 2550 2700

Taxation of five per cent of unused long service leave accumulated by 15 August 1978 135 85 85 75 55 55 60 60 55 50

Capital gains tax exemption on the sale of a small business at retirement 55 100 190 490 360 350 370 370 400 420

Small business capital gains tax exemption for assets held for more than 15 years - 15 35 100 90 95 130 135 150 200

Exemption of rent subsidy payments under the Commonwealth/State mortgage and rent relief schemes 13 13 3 3 - - - - - -

Tax offset for low income earners 460 400 670 - - - - - - -

For informaton only: these items are not included in the sum of TBSPs as that constitute a double counting with the calculations on Average Direct Tax Rates over benefit incomeExemption of the Child Care Assistance Payments (Revenue foregone) (h) - - - - 485 360 735 815 1010 1225

Tax offset for child care (Revenue foregone) - - - 365 - - - - - -

Exemption of Child Care Benefit (Revenue foregone) (i) - - 410 455 270 290 - - - -

Exemption of the Baby Bonus (Revenue foregone) (j) - - 140 165 165 135 115 100 45 -

Exemption of the first child tax offset (Baby Bonus) (Revenue foregone) (k) - - 31 22 8 4 1 - - -Exemption of Family Tax Benefit, Parts A and B (Revenue foregone) - - 1,880 2,230 1,960 1,900 1950 1990 2090 2180Exemption of certain veterans' pensions, allowances or benefits, compensations, and particular WWII-related

payments for persecutions (Revenue foregone) - - 290 430 430 490 450 400 440 430

(g)

A range of dependency tax offsets, including the dependent spouse tax offset and the invalid relative, parent, parent-in-law, housekeeper, housekeeper (with child), child--housekeeper and child-housekeeper (with child) tax offsets, were abolished from 1 July 2014.

(h) From 20 September 2009, the Utilities and Seniors' Concession Allowance was incorporated into Pension Supplement.

(i)

(j) This tax expenditure is now incorporated into A24 - Exemption of Child Care Assistance payments

(k) The Baby Bonus was discontinued from 1 March 2014 and replaced by changes to Family Tax Benefit Part A. This change from 2014-15 onwards is reflected in A35. Source: 2013 TES.

(l) The first child tax offset expired on 30 June 2009.

Source: NZLtralian Government (2015, 2013, 2011, 2009, 2007,2005, 2003), Tax Expenditure Statement, The Treasury, Canberra.

For information only : Exemptions from Goods and Services Tax for social products and services (excluded from total) (l) 2005 2007 2009 2010 2011 2012 2013 2014

GST exemption for education supplies (e.g. education sources, student accommodation) 1,850 2,100 2,550 2,800 3,050 3,350 3,650 3,850

GST exemption for drugs and medicinal preparations 270 320 310 330 420 470 490 520

GST exemption for medical aids and applicances 30 35 80 85 95 100 110 115

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2, except Government wages from NZLtralian National Accounts (table 40); and OECD Revenue Statistics database

Reporting Modification. This tax expenditure modifies 'Exemption of the Child Care Rebate' (A26 in 2014 TES) and incorporates 'Exemption of Child Care Benefit' (A37 in the 2014 TES). From 2017-18 this tax expenditure incorporates the Child Care Subsidy, subject to passage

of legislation.

GST exemption for medical and health services 1,850 2,200 2,500 2,700 2,900 3,100 3,250 3,450

GST exemption for private health insurance 160 190 210 240 250 250 260 290

GST exemption for residential care, community care and other care services (e.g. publicly funded aged care, disability care) 70 90 780 830 870 910 970 1,030

GST exemption for child care services 360 480 600 670 770 880 1,020 1,150

(m)

Source: NZLtralian Government (2015, 2013, 2011), Tax Expenditure Statement, The Treasury, Canberra.

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

Tax breaks to stimulate private social protection (not including pensions) 1,170 1,510 1,992 2,800 3,140 3,240 3,625 3,955 4,030 4,135

Tax offset for expenditure on private health insurance (m) 590 740 900 1,020 1,140 1,220 1,330 1,600 1,470 1,450

Deduction for gifts to deductible gift recipients - - - 790 960 870 1,030 1,010 1,080 1,020

Deduction for gifts to approved donees 300 540 730 - - - -

Deduction for contributions with an associated minor benefit - - 3 - - - -

Partial rebate for certain non-profit, non-government bodies 40 20 19 30 30 30 30 40 50 55

Capped exemption for public benevolent institutions (excluding public hospitals) 240 210 250 720 890 980 1,100 1,150 1,300 1,400

Deduction for donations to prescribed private funds - - 90 240 120 140 135 155 130 210

(n) The rebate for private health insurance has been moved from the category 'Tax breaks similar to cash benefits' to 'Tax breaks to stimulate private social protection' to be consistent with other countries.Source: NZLtralian Government (2015, 2013, 2011, 2009, 2007,2005, 2003), Tax Expenditure Statement, The Treasury, Canberra.

Memorandum Items 2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

Tax breaks for pensions 9,215 13,540 19,525 38,868 25,336 29,110 28,770 26,870 26,590 29,470

Superannuation - capital gains tax discount for funds .. .. 1,090 1,030 80 100 90 80 170 350

Concessional taxation of employer contributions - - - 13,150 12,700 12,600 14,250 13,850 14,400 15,500

Concessional taxation of superannuation entity earnings - - - 22,050 10,650 15,050 13,100 11,600 11,100 12,500

Concessional taxation of funded superannuation 9,215 13,400 17,930 - - - - - - -

Concessional taxation of unfunded superannuation lump sums - 140 150 308 360 410 450 470 500 530

Superannuation - deduction and concessional taxation of certain personal contributions .. .. 410 2,000 1,500 870 960 1,000 620 750

Superannuation - measures for low-income earners .. .. 90 500 230 300 170 140 120 200

Superannuation - spouse contribution offset .. .. 15 10 6 - -

Superannuation - tax on funded lump sums relating to post-June 1983 service .. .. -160 -180 -190 -220 -250 -270 -320 -360

Source: NZLtralian Government (2015, 2013, 2011, 2009, 2007,2005, 2003), Tax Expenditure Statement, The Treasury, Canberra.

The GST is an indirect, broad based consumption tax charged at a rate of 10 per cent. Several goods and services that fall within the OECD's definition of a social product are exempt from this tax. The value of these exemptions are listed above. If this type of tax expenditure in

included in the calculation of net social expenditure for other countries, it may be appropriate to similarly incorporate this information in the calculation of net social expenditure in NZLtralia. Estimates of tax expenditure on these concessions is not available for 2003 or 2001. Note

that tax expenditures relating to GST exemptions was introduced into the Tax Expenditures Statement in 2008. For this reason, tax breaks relating to GST exemptions are not available for prior years.

AUSTRIA

A. Average Itemised Tax Rates (AITR %)

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

Old-age cash benefits (1 +3) 17.7% - public pensions 17.0% 16.6% 15.9% 15.0% 15.4% 15.8% 16.4% 16.8% 17.3% - private pensions 13.0% 16.6% 15.9% 15.0% 15.4% 15.8% 16.4% 16.8% 17.3%Incapacity-related benefits - Disability pensions 17.7% 17.0% 16.6% 15.9% 15.0% 15.4% 15.8% 16.4% 16.8% 17.3% - Occupational Injury benefits 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

- Sickness payments 30.0% 30.0% 29.3% 22.0% 22.0% 22.0% 22.0% 22.0% 22.0% 22.0%

Source: Ministry of Finance (Bundesministerium fur Finanzen), Wage Tax Statistics (2001, 2003, 2005, 2007, 2009, 2010, 2011).

B. Average implicit indirect tax rates of consumption out of benefit income

Indirect taxes paid out of consumption of cash transfers, in millions of euros

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

(1) Private final consumption expenditure 119,386 125,494 136,880 147,809 153,891 158,041 165,191 170,058 173,714 177,344

(2) Private consumption plus Government consumption minus Government wages 136,965 144,100 158,009 171,091 180,717 185,453 193,224 198,916 203,371 208,026

(3) General consumption taxes plus excise duties (5110+5121) 23,029 24,164 26,052 27,748 28,945 29,685 30,970 32,163 32,566 33,048

5110 General taxes 17,301 17,944 19,466 20,988 22,231 22,764 23,498 24,601 24,978 25,467 5121 Excises 5,728 6,220 6,586 6,760 6,714 6,921 7,472 7,562 7,588 7,581

(4) Taxes on production sale transfer (5100) 24,925 26,154 27,980 29,830 31,141 31,827 33,771 35,056 35,442 35,995

(5) Taxes on Goods and Services (5000) 26,550 27,924 29,732 31,688 33,088 33,818 35,881 37,263 37,745 38,671

Implicit average indirect tax rate on consumption out of benefit income:

(6) using general consumption taxes plus excise duties (3)/(2) 16.8% 16.8% 16.5% 16.2% 16.0% 16.0% 16.0% 16.2% 16.0% 15.9%

(7) using a broad concept of the indirect tax base (5)/(2) 19.4% 19.4% 18.8% 18.5% 18.3% 18.2% 18.6% 18.7% 18.6% 18.6%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 22.2% 22.3% 21.7% 21.4% 21.5% 21.4% 21.7% 21.9% 21.7% 21.8%

C. Tax breaks for social purposes (in millions of euros)

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

Tax breaks similar to cash benefits 55 95 165 175 175 175 175 180 180 180

Family:

Tax credits for one-parent families ("Alleinerzieherabsetzbetrag") 40 110 120 120 120 120 120 120 120

Other areas:

Appliances for the disabled (Steuerbefreiung für Kfz für Körperbehinderte) § 2 (1) Z 12 KfzStG und § 4 (3) Z 9 VersStG 15 15 15 15 15 15 15 15 15 15Special tax relief (Außergewöhnliche Belastungen) § 35 40 40 40 40 40 40 40 45 45 45

Tax measures to stimulate private social protection (including pensions) 270 280 280 280 280

Contributions to health, accident and pension insurance (Versicherungsbeiträge) § 18 Abs. 1 Z 2 270 280 280 280 280

Memorandum Items

Tax breaks for pensions 130 130 180 205 230 83 84 83 36 21

- Deduction of contributions to private pension insurances or funds as "special expenses" 130 130 150 150 150

- Premium (payable tax credit) for contributions to pension funds 30 55 80 83 84 83 36 21

Source: Budget Accounts, Foerderungsbericht (2001, 2003, 2005, 2007, 2009, 2010, 2011), Ministry of Finance, Austria.

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue Statistics database (http://stats.oecd.org/Index.aspx?DataSetCode=REV) for lines 3, 4, and 5.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

BELGIUM

A. Amount of direct tax paid on benefit income (in millions of euros)

2001 2003 2005 2007 2009 2010 2011 2012 2013

A.Taxes paid on transfer income (A1 minus A2 , then adding local tax rate *) 4,093.5 4,370.1 4,079.4 4,003.9 4,884.3 5,084.9 5,386.8 5,713.7 5,722.2

Pensions: PIT 5,060 5,458 5,972 5,974 7,030 7,315 7,778 8,243 8,371Sickness: PIT 449 496 485 483 597 651 700 735 794Early retirement: PIT 2 1Unemployment benefits: PIT 525 581 536 484 754 706 636 674 731Total PIT (A1) 6,036 6,535 6,993 6,941 8,381 8,672 9,114 9,652 9,896

- Pensions: tax credit 1,722 1,924 2,525 2,562 2,937 3,001 3,132 3,324 3,489 - Sickness: tax credit 177 213 304 308 384 413 449 477 519 - Early retirement: tax credit 1 0 - - - Unemployment benefits: tax credit 215 302 323 319 454 457 440 448 477 - Others 98 26 32 24 54 62 82 78 88Total tax credits (A2) 2,213 2,465 3,184 3,213 3,829 3,933 4,103 4,327 4,573

Local tax rate 0 0 0 0 0 0 0 0 0

B. Social security contributions 885 ## 984 ## 1,109 ## 1,187 ## 1,338 1,295 1,309 1,324 1,363

Total (A + B) 4,979 5,354 5,189 5,191 6,222 6,380 6,695 7,038 7,086

B. Average implicit indirect tax rates of consumption out of benefit income

Indirect taxes paid out of consumption of cash transfers, in millions of euros

2001 2003 2005 2007 2009 2010 2011 2012 2013

(1) Private final consumption expenditure 140,291 145,800 157,661 172,866 181,546 189,693 196,069 201,182 205,167

(2) Private consumption plus Government consumption minus Government wages 166,787 175,370 190,105 207,646 221,580 230,783 239,426 246,554 250,762

(3) General consumption taxes plus excise duties (5110+5121) 23,535 25,129 28,865 31,523 31,118 33,265 34,147 35,069 35,536

5110 General taxes 17,902 18,880 21,735 24,179 23,832 25,483 26,297 27,122 27,499 5121 Excises 5,632 6,249 7,130 7,344 7,287 7,783 7,850 7,947 8,036

(4) Taxes on production sale transfer (5100) 25,660 27,564 31,381 34,453 34,574 36,975 38,025 40,437 40,183

(5) Taxes on Goods and Services (5000) 27,928 29,714 33,678 36,823 36,898 39,364 40,571 42,876 42,678

Implicit average indirect tax rate on consumption out of benefit income:

(6) using general consumption taxes plus excise duties (3)/(2) 14.1% 14.3% 15.2% 15.2% 14.0% 14.4% 14.3% 14.2% 14.2%

(7) using a broad concept of the indirect tax base (5)/(2) 16.7% 16.9% 17.7% 17.7% 16.7% 17.1% 16.9% 17.4% 17.0%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 19.9% 20.4% 21.4% 21.3% 20.3% 20.8% 20.7% 21.3% 20.8%

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue Statistics database

(http://stats.oecd.org/Index.aspx?DataSetCode=REV) for lines 3, 4, and 5.

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

* Local tax rate is applied to income tax, which overestimates local tax amount as local taxes are only paid when the amount of the credit does not exhaust income tax. So for 2011,

Taxes paid to on tranfers income refer to Total PIT - Total tax credits * local tax (A1 minus A2 , then adding local tax rate *) (9114-4103)* (1+0.075)= 5386.8

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

BELGIUM

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

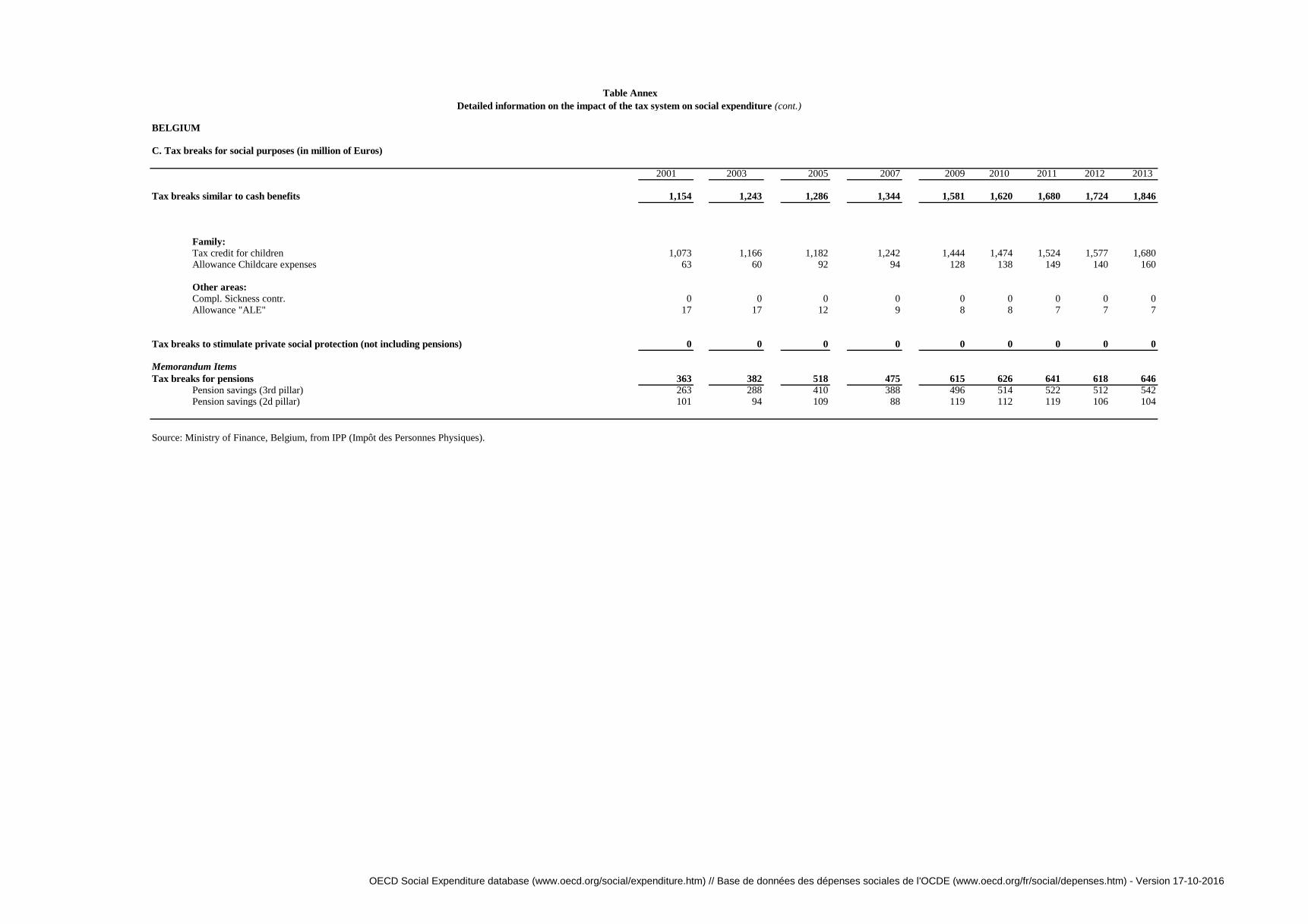

C. Tax breaks for social purposes (in million of Euros)

2001 2003 2005 2007 2009 2010 2011 2012 2013

Tax breaks similar to cash benefits 1,154 1,243 1,286 1,344 1,581 1,620 1,680 1,724 1,846

Family:

Tax credit for children 1,073 1,166 1,182 1,242 1,444 1,474 1,524 1,577 1,680Allowance Childcare expenses 63 60 92 94 128 138 149 140 160

Other areas:

Compl. Sickness contr. 0 0 0 0 0 0 0 0 0Allowance "ALE" 17 17 12 9 8 8 7 7 7

Tax breaks to stimulate private social protection (not including pensions) 0 0 0 0 0 0 0 0 0

Memorandum Items

Tax breaks for pensions 363 382 518 475 615 626 641 618 646

Pension savings (3rd pillar) 263 288 410 388 496 514 522 512 542Pension savings (2d pillar) 101 94 109 88 119 112 119 106 104

Source: Ministry of Finance, Belgium, from IPP (Impôt des Personnes Physiques).

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

CANADA

A. Average Itemised Tax Rates (AITR %)

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

1 Old-age Cash Benefits 14.8 14.2 14.5 12.7 11.7 11.9 12.4 12.0 12.0 12.11a - Public Pensions (OAS) 7.0 6.7 6.7 5.9 5.5 5.7 5.9 6.1 6.0 6.01b - Private Pensions 17.8 17.1 17.2 15.0 14.0 14.2 14.7 14.1 14.1 14.4

2 Canadian Pension Plan (Retirement) 9.7 9.3 9.4 8.3 7.8 8.0 8.2 8.3 8.3 8.4

3 Canadian Pension Plan (Disability) 5.6 5.0 5.1 4.5 4.2 4.1 3.8 4.3 4.4 4.4

4 Employment Insurance 11.2 10.9 10.1 9.2 9.1 9.1 9.4 9.6 9.7 9.94a - Regular Employment Insurance - 11.3 10.6 9.6 9.4 9.3 9.8 10.0 10.0 10.24b - Parental Leave Payments - n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a4c - Active Labour Market Programs - 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

5 Worker's Compensation 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

6 Guaranteed Income Supplement 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

7 Social Assistance 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

8 Universal Child Care Benefits (UCCB) - - - 4.3 4.2 4.1 4.4 4.0 4.1 4.2

9 Wage Income * 19.5 19.2 19.1 18.4 17.8 18.0 18.2 18.2 18.3 18.5

B. Average implicit indirect tax rates of consumption out of benefit incomeIndirect taxes paid out of consumption of cash transfers, in millions of Canadian dollars

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

(1) Private final consumption expenditure 627,551 695,313 768,649 860,349 901,170 946,350 988,577 1,020,599 1,059,398 1,106,703

(2) Private consumption plus Government consumption minus Government wages 722,722 799,940 882,619 985,356 1,044,858 1,097,518 1,147,908 1,183,633 1,227,423 1,278,816

(3) General consumption taxes plus excise duties (5110+5121) 75,516 85,008 91,462 94,002 90,067 96,447 101,870 106,467 109,280 114,778

5110 General taxes 56,297 62,348 68,510 71,242 66,843 72,104 76,663 81,098 82,978 86,988 5121 Excises 19,219 22,659 22,952 22,759 23,224 24,343 25,208 25,368 26,302 27,791

(4) Taxes on production sale transfer (5100) 90,699 101,791 109,926 114,701 110,439 116,994 123,068 128,292 131,473 137,458

(5) Taxes on Goods and Services (5000) 96,448 107,782 116,921 122,855 118,583 125,417 132,542 137,900 141,097 147,239

Implicit average indirect tax rate on consumption out of benefit income:

(6) using general consumption taxes plus excise duties (3)/(2) 10.4% 10.6% 10.4% 9.5% 8.6% 8.8% 8.9% 9.0% 8.9% 9.0%

(7) using a broad concept of the indirect tax base (5)/(2) 13.3% 13.5% 13.2% 12.5% 11.3% 11.4% 11.5% 11.7% 11.5% 11.5%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 15.4% 15.5% 15.2% 14.3% 13.2% 13.3% 13.4% 13.5% 13.3% 13.3%

C. Tax breaks for social purposes (in millions of Canadian dollars)1

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

Tax breaks similar to cash benefits (total without 5, 8 and 17 below) 5,328 5,621 6,079 8,129 8,547 8,811 9,122 9,607 9,850 12,085

Family: 2 Infirm Dependant Credit/ Caregiver Credit 69 85 89 94 102 105 115 125 130 135

10 Child care expense deduction 530 535 570 750 810 850 900 960 960 98511 Adoption Expense Tax Credit - - 3 3 3 3 3 3 2 212 Eligible Dependant Credit 610 660 665 755 785 770 770 775 770 79018 Children's Fitness Tax Credit - - - 90 110 110 110 115 120 18020 Child Tax Credit - - - 1,445 1,470 1,480 1,510 1,560 1,590 1,61521 Investment Tax Credit for Child Care Spaces - - - s s s s s s s

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

The sample used for the microdataset simulation was a stratified sample, consisting of approximately 690 000 records for the 2013 tax year, weighted to represent all taxfilers in Canada. The sample is provided by the Canada Revenue Agency.

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue Statistics database (http://stats.oecd.org/Index.aspx?DataSetCode=REV) for lines 3, 4, and

5.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

CANADA

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

Children's Arts Tax Credit - - - - - - 30 35 40 40Family Caregiver Tax Credit - - - - - - - 55 65 65Family Tax Cut - - - - - - - - - 1,900Inclusion of the Universal Child Care Benefit in the income of an eligible dependant 2 2 2 2 2

Other areas:1 Disability Tax Credit 419 460 496 585 620 650 675 720 770 8253 Infirm Dependant Credit

Disability supports deduction 0 1 1 2 2 1 2 2 1 19 Medical Expense Tax Credit 570 700 805 915 1,000 1,080 1,135 1,260 1,310 1,370

Goods and Services Tax/Harmonized Sales Tax Credit 3,130 3,180 3,450 3,490 3,645 3,760 3,870 3,995 4,090 4,175

For information only: not included in total TBSP

8 Age Credit (amount not included in total TBSP, as already taken into account when calculating AITRs) 1,916 2,036 2,010 2,496 2,295 2,410 2,530 2,700 2,885 3,010

Tax breaks to stimulate private social protection (not including pensions)1 2,165 2,245 2,826 3,245 4,753 5,165 5,290 5,310 5,510 5,965

Non-taxation of employer paid health and dental benefits .. .. .. .. 2,105 2,225 2,315 2,420 2,520 2,590Deductibility of charitable donations from corporate income tax 490 245 430 455 325 385 395 385 305 500Charitable Donation Tax Credit (excluding donations of cultural property and ecologically sensitive land) 1,490 1,825 2,233 2,510 2,118 2,320 2,330 2,315 2,450 2,575Non-taxation of capital gains on donations of publicly-listed securities (reduced inclusion rate for capital gains) - - 28 105 65 100 110 95 115 170First-Time Donor's Super Credit - - - - - - - - 5 5Non-taxation of non-profit organizations 185 175 135 175 140 125 125 70 90 90Registered Disability Savings Plan - - - - s 10 15 25 25 35

For information only: these items are not included in the sum of TBSPs, as that would constitute a double counting with the calculationis on Average Direct Tax Rates over benefit incomeExemption for certain supplies made by charities and non-profit organizations n.a. n.a. 810 845 895 865 955 865 890 945Rebate for qualifying non-profit organizations 60 70 75 70 70 75 70 65 65 65Rebate for registered charities 240 270 295 295 265 270 285 290 285 295Exemption for child care 130 135 155 135 135 120 120 130 135 140Exemption for health care services 325 495 665 585 515 585 585 610 640 680Rebate for specially equipped motor vehicles n.a. n.a. n.a. n.a. s s s s s sZero-rating of medical and assistive devices 120 160 185 190 290 310 320 325 335 350Zero-rating of prescription drugs 430 600 710 720 665 695 720 730 750 785Exemption and rebate for legal aid services 25 25 25 25 20 30 30 30 30 35

Memorandum item

Tax breaks for pensions (1+2+3+4) 5,390 13,980 22,535 30,765 21,030 27,885 28,050 34,525 37,595 40,360

Revenue foregone method:1 Pension Income Credit 405 430 420 975 965 1,010 1,035 1,065 1,100 1,1352 Registered retirement savings plans (RRSPs)

Deduction for contributions 6,225 6,000 6,820 7,405 7,005 7,330 7,480 7,705 8,050 8,090

Non-taxation of investment income 1,280 3,655 6,920 9,110 4,085 7,560 7,805 10,130 11,290 12,220

Taxation of withdrawals -3,465 -3,670 -4,280 -5,030 -4,375 -4,895 -5,330 -5,095 -5,440 -5,610

Net tax expenditure 4,040 5,985 9,460 11,485 6,715 9,995 9,955 12,740 13,900 14,700

3 Registered pension plans (RPPs)

Deduction for contributions 4,575 6,615 8,355 9,430 11,945 12,235 12,465 13,530 14,185 15,115

Non-taxation of investment income 2,785 7,525 11,580 14,825 7,145 11,035 11,290 13,875 15,840 17,260

Taxation of withdrawals -6,415 -6,575 -7,280 -6,790 -6,605 -7,285 -7,670 -7,725 -8,505 -8,960

Net tax expenditure 945 7,565 12,655 17,465 12,485 15,985 16,085 19,680 21,520 23,415

4 Pension Income Splitting - - - 840 865 895 975 1,040 1,075 1,110

Supplementary information:

Data supplied by Finance Canada, from Department of Finance Canada (2015, 2014, 2012, 2010, 2009, 2008, 2006, 2004, 2002), Tax Expenditures and Evaluations, Ottawa.1. Since 2001 Tax expenditures are for federal measures only cannot be considered complete, therefore cannot be compared to some other countries’ estimates, given that sub-national expenditures are not included. 1. The totals may overestimate total expenditure, as interactions between measures are not taken into account.

The sample used for the microdataset simulation was a stratified sample of approximately 450,000 records, weighted to represent all taxfilers in Canada. The sample is provided by the Canada Revenue Agency.2. "s" denotes a very small number that has been suppressed.

* The present-value estimates reflect the lifetime cost of a given year’s contributions. This definition is different from that used for the cash-flow estimates, and thus the two sets of estimates are not directly comparable.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

CHILE

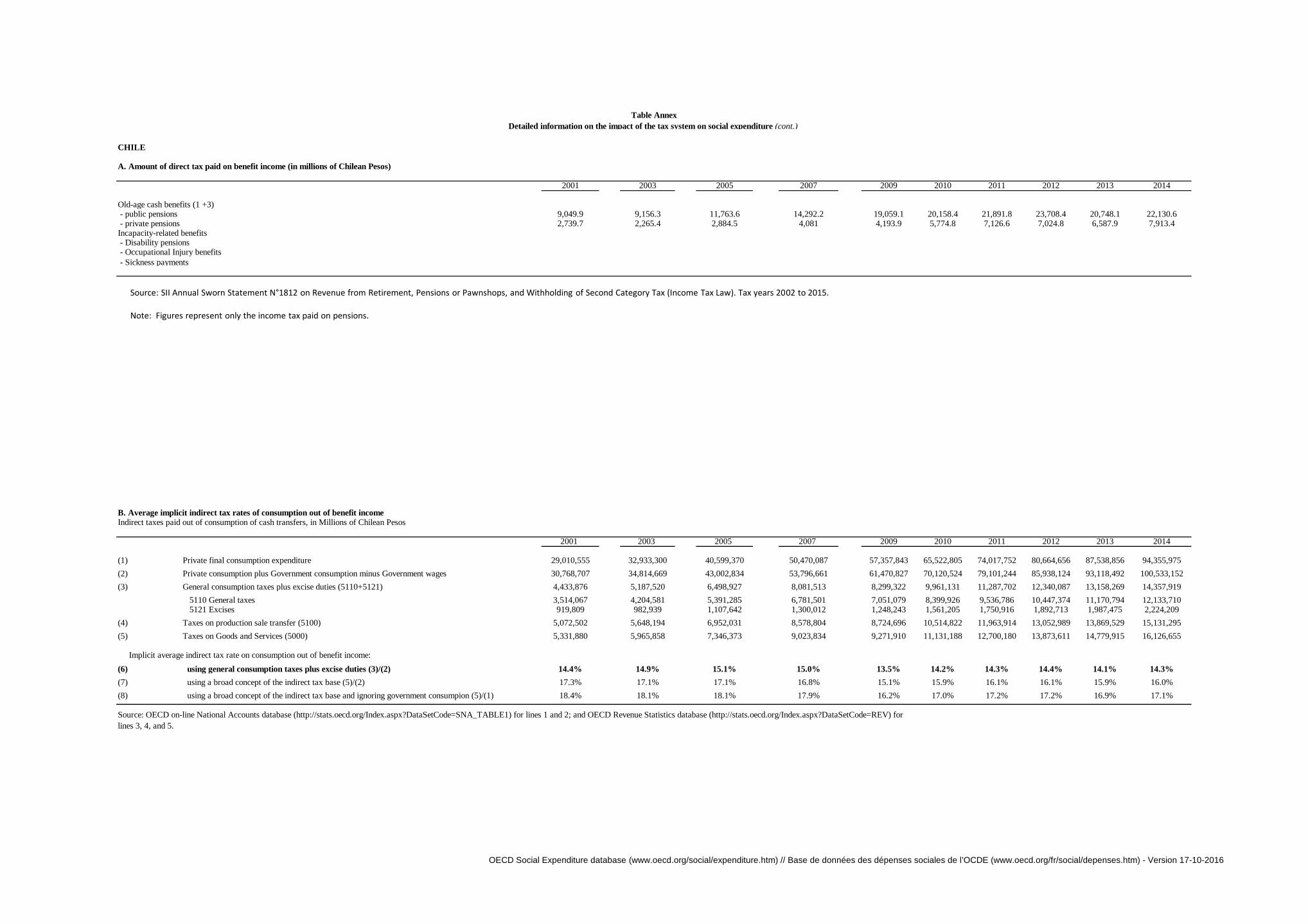

A. Amount of direct tax paid on benefit income (in millions of Chilean Pesos)

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

Old-age cash benefits (1 +3) - public pensions 9,049.9 9,156.3 11,763.6 14,292.2 19,059.1 20,158.4 21,891.8 23,708.4 20,748.1 22,130.6 - private pensions 2,739.7 2,265.4 2,884.5 4,081 4,193.9 5,774.8 7,126.6 7,024.8 6,587.9 7,913.4Incapacity-related benefits - Disability pensions - Occupational Injury benefits

- Sickness payments

B. Average implicit indirect tax rates of consumption out of benefit incomeIndirect taxes paid out of consumption of cash transfers, in Millions of Chilean Pesos

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

(1) Private final consumption expenditure 29,010,555 32,933,300 40,599,370 50,470,087 57,357,843 65,522,805 74,017,752 80,664,656 87,538,856 94,355,975

(2) Private consumption plus Government consumption minus Government wages 30,768,707 34,814,669 43,002,834 53,796,661 61,470,827 70,120,524 79,101,244 85,938,124 93,118,492 100,533,152

(3) General consumption taxes plus excise duties (5110+5121) 4,433,876 5,187,520 6,498,927 8,081,513 8,299,322 9,961,131 11,287,702 12,340,087 13,158,269 14,357,919

5110 General taxes 3,514,067 4,204,581 5,391,285 6,781,501 7,051,079 8,399,926 9,536,786 10,447,374 11,170,794 12,133,710 5121 Excises 919,809 982,939 1,107,642 1,300,012 1,248,243 1,561,205 1,750,916 1,892,713 1,987,475 2,224,209

(4) Taxes on production sale transfer (5100) 5,072,502 5,648,194 6,952,031 8,578,804 8,724,696 10,514,822 11,963,914 13,052,989 13,869,529 15,131,295

(5) Taxes on Goods and Services (5000) 5,331,880 5,965,858 7,346,373 9,023,834 9,271,910 11,131,188 12,700,180 13,873,611 14,779,915 16,126,655

Implicit average indirect tax rate on consumption out of benefit income:

(6) using general consumption taxes plus excise duties (3)/(2) 14.4% 14.9% 15.1% 15.0% 13.5% 14.2% 14.3% 14.4% 14.1% 14.3%

(7) using a broad concept of the indirect tax base (5)/(2) 17.3% 17.1% 17.1% 16.8% 15.1% 15.9% 16.1% 16.1% 15.9% 16.0%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 18.4% 18.1% 18.1% 17.9% 16.2% 17.0% 17.2% 17.2% 16.9% 17.1%

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue Statistics database (http://stats.oecd.org/Index.aspx?DataSetCode=REV) for

lines 3, 4, and 5.

Source: SII Annual Sworn Statement N°1812 on Revenue from Retirement, Pensions or Pawnshops, and Withholding of Second Category Tax (Income Tax Law). Tax years 2002 to 2015. Note: Figures represent only the income tax paid on pensions.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

CHILE

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

C. Tax breaks for social purposes (in Millions of Chilean Pesos)

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014

Tax breaks similar to cash benefits 0 0 0 0 0 0 0 0 0 0

FamilyOther areas

Tax breaks to stimulate private social protection (not including pensions) a), b), c)

0.0 236,640 296,973 373,905 426,814 476,355 419,142 459,717 529,924 501,325

Item 1 Health insurance (Income tax - deduction) n.a 37,418 53,507 74,970 95,840 112,199 104,851 122,975 147,518 146,339Item 2 Unemploment insurance ( Income tax - deduction) n.a. 14,593 27,750 39,376 47,007 59,051 65,738 81,075 103,059Item 3 Donations for social purposes (Income tax - credit and deduction) 756 174 616 1,228 2,246 49 21 4Item 4 Income from renting DFL 2 housing (Income tax exempt) n.a. 108,141 108,207 116,643 134,815 136,580 142,696 148,003 152,819 83,389Item 5 Health services (VAT exempt) n.a. 81,016 106,659 137,309 138,909 159,523 94,408 103,960 120,993 144,797Item 6 Contributions to Private Health System (VAT exempt) n.a. 10,065 13,251 17,059 17,258 19,819 15,890 18,993 27,498 23,737Item 7 Refund of customs duties when importing equipment for disabled people n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Item 8 Lower customs duties for disabled people that import vehicles with special features n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Memorandum Items

Tax breaks for pensions d), e)

n.a. 127,843 356,289 800,612 129,090 1,431,687 792,756 199,270 540,501 610,395

n.a. 54,466 71,985 100,980 129,090 151,125 171,078 199,270 201,768 226,326

- Non-taxation of investment of private pension funds n.a. 73,377 284,304 699,632 0 1,280,562 621,677 0 338,733 384,069

- Deduction of contributions to private pensions (e.g occupational pension plans, individual retirement accounts, RRSPs,

Superannuation, etc)

Source: Tax Expenditure Reports, elaborated by Servicio de Impuestos Internos (Chilean Internal Revenue Service). Note: a) Tax expenditure measurement began in 2002 and is made on a cash basis. b) Tax breaks concerning pensions (compulsory or voluntary) were excluded.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

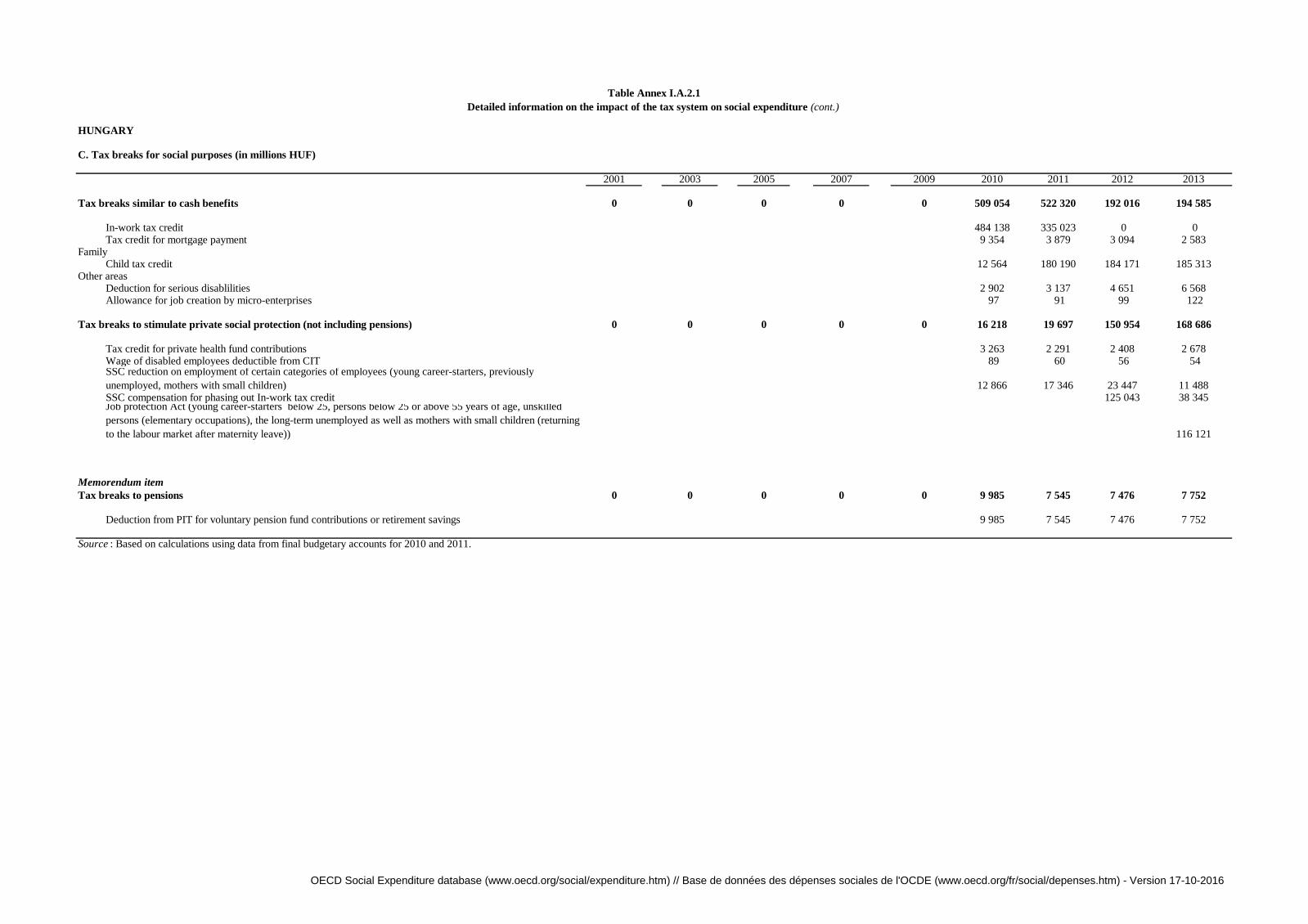

CZECH REPUBLIC

A. Amount of direct tax paid on benefit income (in millions of Czech koruny)

2001 2003 2005 2007 2009 2010 2011 2012 2013Total tax paid on transfer income old-age pensions 1.0 3.0 14.6 11.0 3.7 5.3 8.6 12.5 16.1

Source: Ministry of Finance, Tax Policy Unit; Czech Social Security Administation.

B. Average implicit indirect tax rates of consumption out of benefit incomeIndirect taxes paid out of consumption of cash transfers, in millions of Czech koruny

2001 2003 2005 2007 2009 2010 2011 2012 2013

(1) Private final consumption expenditure 1,284,892 1,406,227 1,566,462 1,775,163 1,917,902 1,947,082 1,984,240 1,997,914 2,029,819

(2) Private consumption plus Government consumption minus Government wages 1,611,646 1,803,635 1,992,942 2,238,113 2,436,570 2,470,926 2,426,419 2,421,183 2,464,584

(3) General consumption taxes plus excise duties (5110+5121) 226,686 251,925 325,652 365,780 395,831 401,858 426,291 437,834 453,582

5110 General taxes 149,893 164,250 215,118 232,288 258,627 263,457 276,533 286,116 303,822 5121 Excises 76,793 87,675 110,534 133,492 137,203 138,401 149,757 151,719 149,760

(4) Taxes on production sale transfer (5100) 236,864 262,453 325,861 365,998 396,042 402,072 426,528 438,090 453,863

(5) Taxes on Goods and Services (5000) 255,029 285,108 350,949 393,041 421,958 427,813 452,578 463,459 478,386

Implicit average indirect tax rate on consumption out of benefit income:

(6) using general consumption taxes plus excise duties (3)/(2) 14.1% 14.0% 16.3% 16.3% 16.2% 16.3% 17.6% 18.1% 18.4%

(7) using a broad concept of the indirect tax base (5)/(2) 15.8% 15.8% 17.6% 17.6% 17.3% 17.3% 18.7% 19.1% 19.4%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 19.8% 20.3% 22.4% 22.1% 22.0% 22.0% 22.8% 23.2% 23.6%

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue Statistics database

(http://stats.oecd.org/Index.aspx?DataSetCode=REV) for lines 3, 4, and 5.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

CZECH REPUBLIC

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

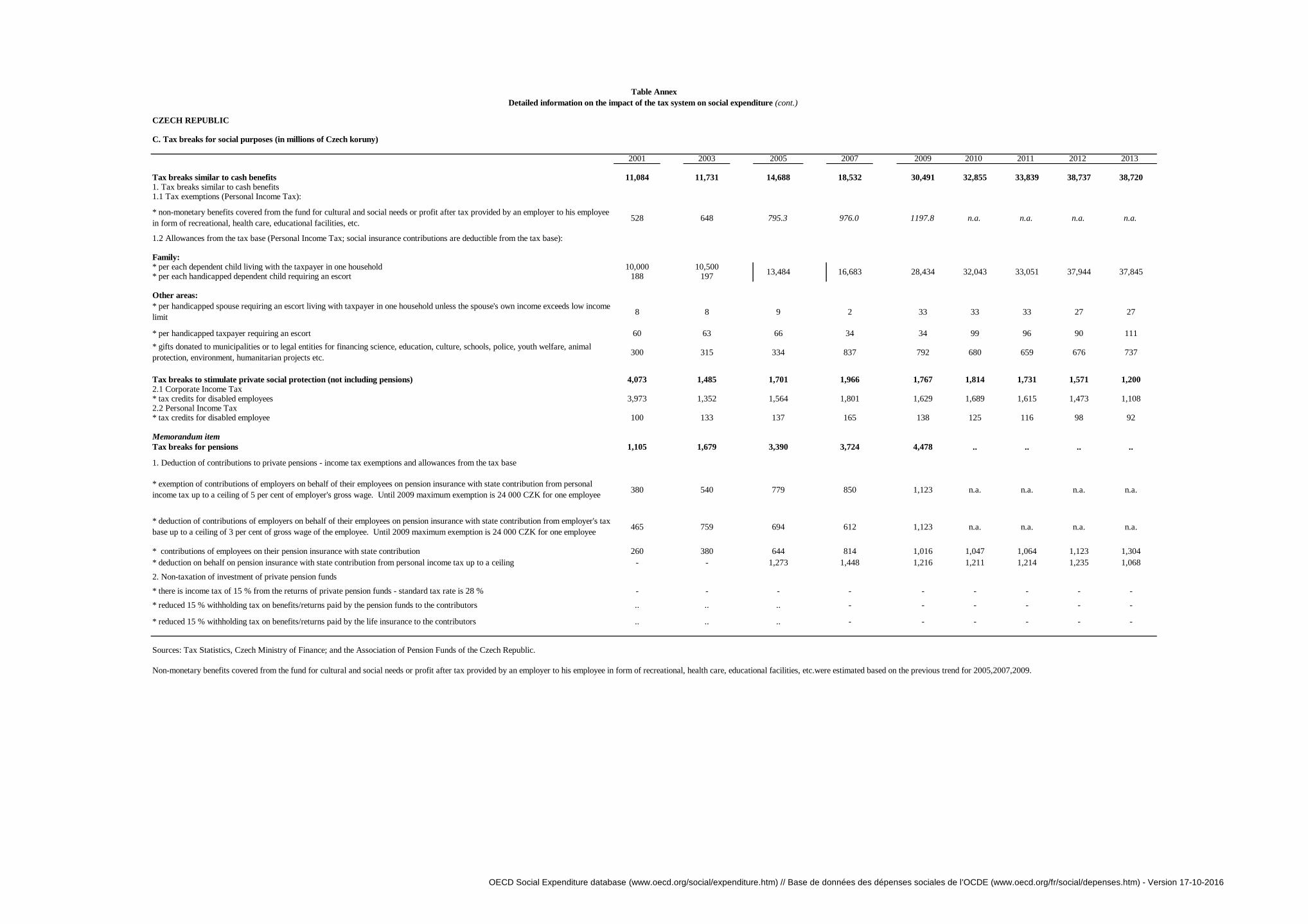

C. Tax breaks for social purposes (in millions of Czech koruny)

2001 2003 2005 2007 2009 2010 2011 2012 2013

Tax breaks similar to cash benefits 11,084 11,731 14,688 18,532 30,491 32,855 33,839 38,737 38,7201. Tax breaks similar to cash benefits1.1 Tax exemptions (Personal Income Tax):

528 648 795.3 976.0 1197.8 n.a. n.a. n.a. n.a.

1.2 Allowances from the tax base (Personal Income Tax; social insurance contributions are deductible from the tax base):

Family: * per each dependent child living with the taxpayer in one household 10,000 10,500* per each handicapped dependent child requiring an escort 188 197

Other areas:

8 8 9 2 33 33 33 27 27

* per handicapped taxpayer requiring an escort 60 63 66 34 34 99 96 90 111

300 315 334 837 792 680 659 676 737

Tax breaks to stimulate private social protection (not including pensions) 4,073 1,485 1,701 1,966 1,767 1,814 1,731 1,571 1,2002.1 Corporate Income Tax* tax credits for disabled employees 3,973 1,352 1,564 1,801 1,629 1,689 1,615 1,473 1,1082.2 Personal Income Tax* tax credits for disabled employee 100 133 137 165 138 125 116 98 92

Memorandum item

Tax breaks for pensions 1,105 1,679 3,390 3,724 4,478 .. .. .. ..

1. Deduction of contributions to private pensions - income tax exemptions and allowances from the tax base

380 540 779 850 1,123 n.a. n.a. n.a. n.a.

465 759 694 612 1,123 n.a. n.a. n.a. n.a.

* contributions of employees on their pension insurance with state contribution 260 380 644 814 1,016 1,047 1,064 1,123 1,304

* deduction on behalf on pension insurance with state contribution from personal income tax up to a ceiling - - 1,273 1,448 1,216 1,211 1,214 1,235 1,068

2. Non-taxation of investment of private pension funds

* there is income tax of 15 % from the returns of private pension funds - standard tax rate is 28 % - - - - - - - - -

* reduced 15 % withholding tax on benefits/returns paid by the pension funds to the contributors .. .. .. - - - - - -

* reduced 15 % withholding tax on benefits/returns paid by the life insurance to the contributors .. .. .. - - - - - -

Sources: Tax Statistics, Czech Ministry of Finance; and the Association of Pension Funds of the Czech Republic.

Non-monetary benefits covered from the fund for cultural and social needs or profit after tax provided by an employer to his employee in form of recreational, health care, educational facilities, etc.were estimated based on the previous trend for 2005,2007,2009.

* non-monetary benefits covered from the fund for cultural and social needs or profit after tax provided by an employer to his employee

in form of recreational, health care, educational facilities, etc.

13,484 16,683 28,434 32,043 33,051 37,944 37,845

* per handicapped spouse requiring an escort living with taxpayer in one household unless the spouse's own income exceeds low income

limit

* gifts donated to municipalities or to legal entities for financing science, education, culture, schools, police, youth welfare, animal

protection, environment, humanitarian projects etc.

* exemption of contributions of employers on behalf of their employees on pension insurance with state contribution from personal

income tax up to a ceiling of 5 per cent of employer's gross wage. Until 2009 maximum exemption is 24 000 CZK for one employee

* deduction of contributions of employers on behalf of their employees on pension insurance with state contribution from employer's tax

base up to a ceiling of 3 per cent of gross wage of the employee. Until 2009 maximum exemption is 24 000 CZK for one employee

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

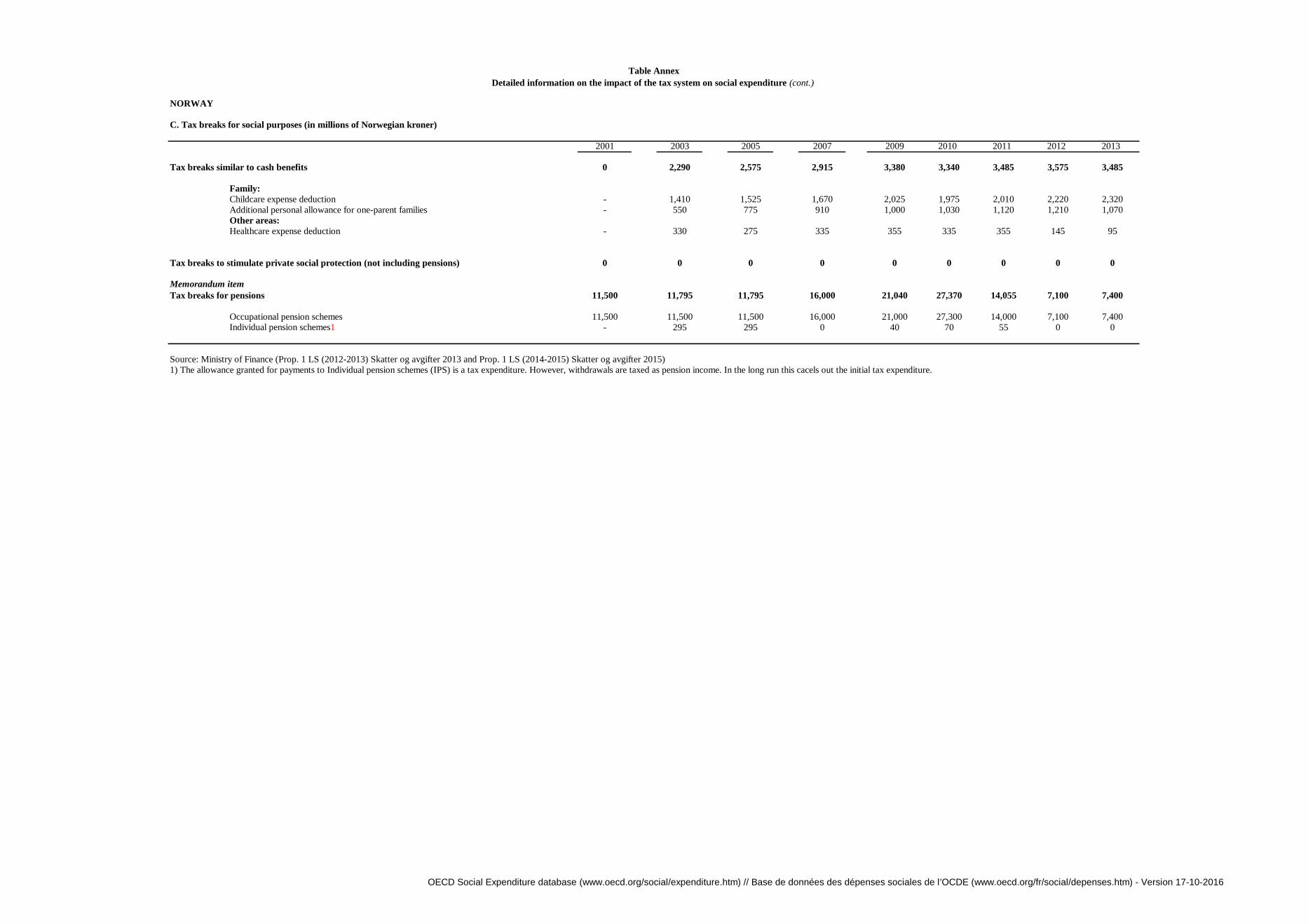

DENMARK No Social security <2012 and onwards>

A. Average Itemised Tax Rates - AITR %

2001 2003 2005 2007 2009 2010 2011 2012 2013

Tax and

Social security

Tax and

Social

security

Tax and

Social

security

Tax and

Social

security

Tax and

Social

security

Tax and

Social

security

Tax and

Social

security

Tax and

Social

security

Tax and

Social

security

1 Social pension

- state old age pension 27.68 (98%) 27.20 (98%) 27.25 (98%) 27.13 (98%) 26.54 (98%) 26.40 ('98%') 26.52 ('98%') 26.27 0.99 27.00 0.99

- disability pension 26.92 (75%) 26.22 (75%) 26.38 (77%) 27.16 (85%) 27.08 (88%) 27.05 ('89 %') 27.30 ('90 %') 27.21 0.91 27.89 0.92

- anticipated old age pension 23.78 (84%) 23.69 (84%) 26.57 (90%) 23.37 (76%) 23.06 (76%) 22.78 ('76%') 23.07 ('76 %') 23.06 0.78 23.99 0.78

2 Supplementary pensions (ATP) 30.68 29.79 29.83 29.56 28.95 28.57 28.45 28.13 28.71

3 Civil servants pension 34.77 34.00 33.66 33.81 33.31 31.98 31.97 31.44 31.70

4 Early retirement pensions (Delpension) 32.30 31.48 30.19 30.00 30.00 30 30 30 30

5 Sickness benefit 36.36 36.49 36.75 35.16 33.43 32.84 32.67 29.97 29.92

6 Parental leave 28.85 28.56 28.69 29.47 29.78 28.32 -'

7 Unemployment benefits 32.78 32.66 32.58 30.80 30.22 29.69 29.96 26.11 26.64

8 Early retirement benefits 29.38 28.16 28.09 30.29 29.78 29.59 29.7 26.95 27.68

9 Occupational accidents - except: 36.07 32.05 36.29 32.70 32.70 36.20 32.82 31.13 31.93

Occupational accidents and decease (10.3.1.3.1) 35.34 (22%) 35.09 (23%) 33.89 (26%) 32.12 32.29 31.95 32.18

War victims, accidents, sailors (10.3.1.5.5) (60%) 32.70 (40%) 32.70 (39%) 36.20 32.82 32.82 31.21

Handicapped children and adults (10.3.1.5.4) (47%) 39.85 (41%) 38.04 (47%) 36.99 37.03 35.02 34.22

10 Survivors 10.00 10.00 10.00 10.00 10.00 10 10 10 10

11 Childbirth benefit (barsel) 39.71 37.21 37.59 35.44 34.35 33.94 34.09 31.57 31.25

12 Items under active labour market policy

- Measures by regional labour market councils 26.89 26.42 26.02 25.37 23.75 23.24 23.70 25.05 24.21

- Employment measures for disabled 31.30 30.72 30.87 30.21 28.50 29.31 29.55 27.08 28.49

13 Other, war victims 35.30 (90%) 33.95 (90%) 33.50 (84%) 33.46 (88%) 32.78 (89%) 31.55 ('87%') 31.41 ('87%') 27.20 100 25.39 100

14 Other, wage earn. Guar. Fond. 44.10 39.31 35.40 37.48 37.73 37.46 37.87 34.45 35.02

15 Cash payments to refugees (10.9.1.2.1) 5.70 3.18 5.17 4.73 6.12 9.31 9.2

16 Low income 26.73 26.04 25.80 24.97 23.75 23.24 23.70 25.05 24.21

17 Transfers taxed as wages 43.54 42.07 41.21 39.85 38.04 36.99 37.03 35.02 34.22

In parentheses: proportion of spending subject to taxation if not 100%.

B. Average implicit indirect tax rates of consumption out of benefit income

Indirect taxes paid out of consumption of cash transfers, in millions Danish kroner

2001 2003 2005 2007 2009 2010 2011 2012 2013

(1) Private final consumption expenditure 640,633 678,795 757,919 825,592 834,603 861,835 884,301 908,702 914,493

(2) Private consumption plus Government consumption minus Government wages 758,248 804,509 898,246 982,010 1,014,139 1,044,224 1,064,712 1,095,698 1,101,377

(3) General consumption taxes plus excise duties (5110+5121) 196,031 204,715 232,644 256,629 235,329 244,568 250,659 259,209 262,479

5110 General taxes 125,829 132,588 154,111 174,049 166,871 170,852 175,620 180,778 180,947

5121 Excises 70,202 72,127 78,533 82,581 68,457 73,717 75,039 78,431 81,532

(4) Taxes on production sale transfer (5100) 200,850 210,529 239,350 263,151 241,093 249,992 256,085 263,821 266,857

(5) Taxes on Goods and Services (5000) 212,411 222,696 252,703 281,899 259,994 269,587 276,477 284,565 289,722

Implicit average indirect tax rate on consumption out of benefit income:

(6) using general consumption taxes plus excise duties (3)/(2) 25.9% 25.4% 25.9% 26.1% 23.2% 23.4% 23.5% 23.7% 23.8%

(7) using a broad concept of the indirect tax base (5)/(2) 28.0% 27.7% 28.1% 28.7% 25.6% 25.8% 26.0% 26.0% 26.3%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 33.2% 32.8% 33.3% 34.1% 31.2% 31.3% 31.3% 31.3% 31.7%

C. Tax breaks for social purposes (in millions of Danish kroner)

2001 2003 2005 2007 2009 2010 2011 2012 2013

Tax breaks similar to cash benefits 182 189 201 0 0 0 0 0 0

Family:

Other areas:

Supplement for older people "Engangsbelob" (67+) 135 140 147 .. .. .. .. .. ..

Capital tax reduction for older people (67+) 0 0

Housing for older people "Plejehjem" 47 49 54 .. .. .. .. .. ..

Tax breaks to stimulate private social protection (not including pensions) 0 0 0 0 0 0 0 0 0

Memorandum item

Tax breaks for pensions 0 0 0 0 0 0 0 0 0

Source: Ministry of Finance, Denmark.

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue Statistics database (http://stats.oecd.org/Index.aspx?DataSetCode=REV)

for lines 3, 4, and 5.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

ESTONIA

A. Average Itemised Tax Rates (AITR %)

2007 2009 2010 2011 2012 2013

Total tax paid (including soc. sec. cont.) over transfer income .. 2.2 2.0 3.5 4.4

- pensions 2.7 2.6 2.7 3.1 old age pensions 7.5 7.4 7.5 7.7 disability pension 0.4 0.3 0.4 0.5 survivor's pension 0.1 0.1 0.1 1.1

- benefits for temporary incapacity for work 16.1 15.8 16.2 17.0

- unemployment benefits 17.1 16.8 17.1 17.0 income tax: unemployment insurance benefit 9.5 8.9 9.7 9.7 insurance benefit upon lay-off 20.9 20.8 20.8 20.7 benefit upon insolvency of employer 20.9 20.8 20.7 20.7 social security contributions: insurance benefit upon lay-off benefit upon insolvency of employer

- family benefits 18.8 18.7 18.8 18.8 maternity benefit 18.8 18.7 18.8 18.8 parental benefit

B. Average implicit indirect tax rates of consumption out of benefit income

Indirect taxes paid out of consumption of cash transfers, in Millions of Estonian kroon (EEK).

2007 2009 2010 2011 2012 2013

(1) Private final consumption expenditure 8,670 7,551 7,689 8,427 9,104 9,738

(2) Private consumption plus Government consumption minus Government wages 9,739 8,753 8,937 9,752 10,570 11,293

(3) General consumption taxes plus excise duties (5110+5121) 2,000 1,922 1,881 2,091 2,304 2,354

5110 General taxes 1,423 1,224 1,263 1,380 1,513 1,558 5121 Excises 577 697 619 711 791 796

(4) Taxes on production sale transfer (5100) 2,033 1,942 1,905 2,113 2,328 2,380

(5) Taxes on Goods and Services (5000) 2,101 2,004 1,959 2,173 2,387 2,445

Implicit average indirect tax rate on consumption out of benefit income:

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) -

Version 17-10-2016

ESTONIA

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

(6) using general consumption taxes plus excise duties (3)/(2) 20.5% 22.0% 21.0% 21.4% 21.8% 20.8%

(7) using a broad concept of the indirect tax base (5)/(2) 21.6% 22.9% 21.9% 22.3% 22.6% 21.7%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 24.2% 26.5% 25.5% 25.8% 26.2% 25.1%

C. Tax breaks for social purposes (in Millions of EUR).

2007 2009 2010 2011 2012 2013

Tax breaks similar to cash benefits 38.6 41.0 38.1 38.9 39.5 40.4

Family: 38.6 41.0 38.1 38.9 39.5 40.4

Increased basic exemption upon provision of maintenance to child Additional allowance for 2nd+ children, accrual 22.6 24.8 24.2 24.7 25.2 25.8Deduction from tax base: educational expenses, accrual 14.3 14.5 14.0 14.1 14.3 14.6Deduction from tax base: education loan interests, accrual 1.6 1.7 0.0 0.0 0.0 0.0

Not included in the totalAdditional allowance for couple, accrual 32.7 34.9 35.2 34.2 34.2 32.8

Other areas: 30.6 27.9 17.9 20.2 17.3 12.2

Deduction from tax base: mortgage interest payments, accrual 30.6 27.9 17.9 20.2 17.3 12.2

Tax breaks to stimulate private social protection (not including pensions) 10.3 6.8 6.3 6.1 5.9 6.4

Deduction from tax base: contributions to voluntary pension funds, accrual 10.3 6.8 6.3 6.1 5.9 6.4

Memorandum Items

Tax breaks for pensions 76.8 110.6 113.9 114.2 119.1 125.8

Additional allowance for pensioners, this is not cash benefit but tax expenditure 76.8 110.6 113.9 114.2 119.1 125.8

Source: Estonian Tax and Customs Board

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue

Statistics database (http://stats.oecd.org/Index.aspx?DataSetCode=REV) for lines 3, 4, and 5.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) -

Version 17-10-2016

FINLAND

A. Average Itemised Tax Rates (%)

2001 2003 2005 2007 2009 2010 2011 2012 20131 Old-age cash benefits1a - public pensions 19.7 19.4 19.9 20.0 17.9 17.9 18.2 18.2 18.61c - private pensions 28.6 28.9 28.7 28.4 25.5 26.0 25.6 25.2 27.82 Survivors' benefits2a - public pensions 19.1 19.8 19.9 18.6 16.9 17.0 15.8 16.5 16.43 Incapacity-related benefits3a - Disability pensions 17.5 17.6 16.5 15.5 12.9 11.9 12.5 12.6 12.63b - Occupational Injury benefits 26.2 23.5 24.3 23.0 21.9 21.7 23.1 21.4 22.83c - Sickness payments 26.8 24.4 24.5 22.4 21.9 21.7 21.5 21.4 21.54 Family cash benefits 4a - Family benefits 15.8 15.4 14.6 15.14b - Maternity and parental leave payments 21.7 21.5 21.6 19.7 20.1 20.0 20.6 19.7 21.65 Active labour market policies5a - benefits while on training 19.4 19.9 20.0 18.5 19.1 20.5 21.2 19.7 24.46 Unemployment6a - unemployment insurance benefit 20.5 20.5 20.5 18.9 18.4 19.3 18.9 19.5 20.56b - unemployment assistance benefit 18.6 18.1 18.2 17.8 15.9 14.7 14.9 14.4 15.3

Source : Ministry of Finance.

B. Average implicit indirect tax rates of consumption out of benefit income

Indirect taxes paid out of consumption of cash transfers, in millions of euros

2001 2003 2005 2007 2009 2010 2011 2012 2013

(1) Private final consumption expenditure 68,771 75,526 81,876 91,052 95,212 99,553 105,771 109,108 111,277

(2) Private consumption plus Government consumption minus Government wages 79,461 87,551 95,370 106,532 113,252 117,820 124,813 129,229 132,460

(3) General consumption taxes plus excise duties (5110+5121) 16,789 18,689 19,713 21,220 21,064 21,819 24,634 25,501 26,399

5110 General taxes 11,118 12,487 13,748 15,207 15,176 15,533 17,315 17,987 18,888 5121 Excises 5,671 6,202 5,965 6,013 5,888 6,286 7,319 7,514 7,511

(4) Taxes on production sale transfer (5100) 18,004 20,043 21,188 22,754 22,700 23,491 26,407 27,355 28,496

(5) Taxes on Goods and Services (5000) 18,482 20,570 21,782 23,425 23,419 24,256 27,240 28,186 29,430

Implicit average indirect tax rate on consumption out of benefit income:

(6) using general consumption taxes plus excise duties (3)/(2) 21.1% 21.3% 20.7% 19.9% 18.6% 18.5% 19.7% 19.7% 19.9%

(7) using a broad concept of the indirect tax base (5)/(2) 23.3% 23.5% 22.8% 22.0% 20.7% 20.6% 21.8% 21.8% 22.2%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 26.9% 27.2% 26.6% 25.7% 24.6% 24.4% 25.8% 25.8% 26.4%

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

The micro-simulation model used in the Ministry of Finance is based on a representative sample of some 25 000 individual taxpayers. The model is used for the planning of national tax policies and for estimating the effect of tax policy alterations on tax

revenues and on the income tax liabilities of taxpayers at different income levels. The information is in principle collected for the Income Distribution Survey from Statistics Finland. The sample covers about 0,5% of the total taxpayer population, but the

model has been made representative for the total taxpayer population. The dataset is updated annually.There is a break in series in 2009 for unemployment average itemised tax rates resulting from a change in definition.

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue Statistics database

(http://stats.oecd.org/Index.aspx?DataSetCode=REV) for lines 3, 4, and 5.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

FINLAND

Table Annex

Detailed information on the impact of the tax system on social expenditure (cont.)

C. Tax breaks for social purposes (in millions of euros)

2001 2003 2005 2007 2009 2010 2011 2012 2013

Tax breaks similar to cash benefits 0 0 0 0 0 0 0 0 0

Family:

Other areas:

Tax breaks to stimulate private social protection (not including pensions) 0 0 0 0 0 0 0 0 0

Cash donations to Charities

Memorandum Items

Tax breaks for pension 170 205 220 125 130 125 125 120 105

- Deduction of contributions to private pensions 170 205 220 125 130 125 125 120 105

Source: Ministry of Finance, Finland.

Ministry of Finance (2001), Hallituksen kertomus Valtiovarain Hoidosta Ja Tilasta Vuonna 2000, helsinki

The micro-simulation model used in the Ministry of Finance is based on a representative sample of some 25.000 individual taxpayers. The model is used for the planning of national tax policies and for estimating the effect of tax policy alterations on tax revenues and on the

income tax liabilities of taxpayers at different income levels. The information is in principle collected for the Income Distribution Survey from Statistics Finland. The sample covers about 0,5% of the total taxpayer population, but the model has been made representative for

the total taxpayer population. The data set is updated annually.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

FRANCE

A. Amount of direct tax paid on benefit income (in millions of euros)

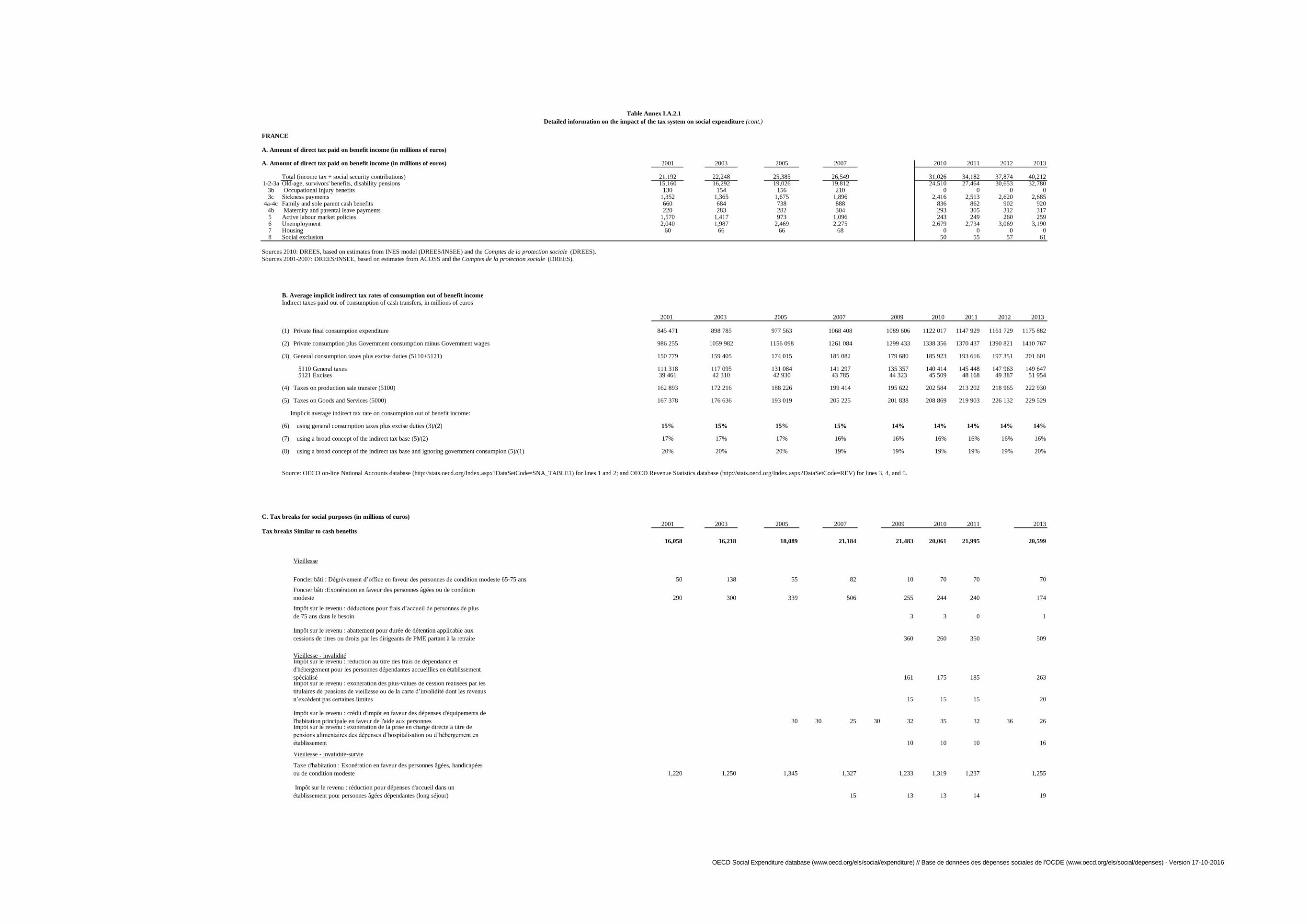

A. Amount of direct tax paid on benefit income (in millions of euros) 2001 2003 2005 2007 2010 2011 2012 2013

Total (income tax + social security contributions) 21,192 22,248 25,385 26,549 31,026 34,182 37,874 40,2121-2-3a Old-age, survivors' benefits, disability pensions 15,160 16,292 19,026 19,812 24,510 27,464 30,653 32,780

3b Occupational Injury benefits 130 154 156 210 0 0 0 03c Sickness payments 1,352 1,365 1,675 1,896 2,416 2,513 2,620 2,685

4a-4c Family and sole parent cash benefits 660 684 738 888 836 862 902 9204b Maternity and parental leave payments 220 283 282 304 293 305 312 3175 Active labour market policies 1,570 1,417 973 1,096 243 249 260 2596 Unemployment 2,040 1,987 2,469 2,275 2,679 2,734 3,069 3,1907 Housing 60 66 66 68 0 0 0 08 Social exclusion 50 55 57 61

Sources 2010: DREES, based on estimates from INES model (DREES/INSEE) and the Comptes de la protection sociale (DREES).

Sources 2001-2007: DREES/INSEE, based on estimates from ACOSS and the Comptes de la protection sociale (DREES).

B. Average implicit indirect tax rates of consumption out of benefit income

Indirect taxes paid out of consumption of cash transfers, in millions of euros

2001 2003 2005 2007 2009 2010 2011 2012 2013

(1) Private final consumption expenditure 845 471 898 785 977 563 1068 408 1089 606 1122 017 1147 929 1161 729 1175 882

(2) Private consumption plus Government consumption minus Government wages 986 255 1059 982 1156 098 1261 084 1299 433 1338 356 1370 437 1390 821 1410 767

(3) General consumption taxes plus excise duties (5110+5121) 150 779 159 405 174 015 185 082 179 680 185 923 193 616 197 351 201 601

5110 General taxes 111 318 117 095 131 084 141 297 135 357 140 414 145 448 147 963 149 647 5121 Excises 39 461 42 310 42 930 43 785 44 323 45 509 48 168 49 387 51 954

(4) Taxes on production sale transfer (5100) 162 893 172 216 188 226 199 414 195 622 202 584 213 202 218 965 222 930

(5) Taxes on Goods and Services (5000) 167 378 176 636 193 019 205 225 201 838 208 869 219 903 226 132 229 529

Implicit average indirect tax rate on consumption out of benefit income:

(6) using general consumption taxes plus excise duties (3)/(2) 15% 15% 15% 15% 14% 14% 14% 14% 14%

(7) using a broad concept of the indirect tax base (5)/(2) 17% 17% 17% 16% 16% 16% 16% 16% 16%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 20% 20% 20% 19% 19% 19% 19% 19% 20%

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue Statistics database (http://stats.oecd.org/Index.aspx?DataSetCode=REV) for lines 3, 4, and 5.

C. Tax breaks for social purposes (in millions of euros)

2001 2003 2005 2007 2009 2010 2011 2013

Tax breaks Similar to cash benefits

16,058 16,218 18,089 21,184 21,483 20,061 21,995 20,599

Vieillesse

Foncier bâti : Dégrèvement d’office en faveur des personnes de condition modeste 65-75 ans 50 138 55 82 10 70 70 70

Foncier bâti :Exonération en faveur des personnes âgées ou de condition

modeste 290 300 339 506 255 244 240 174

Impôt sur le revenu : déductions pour frais d’accueil de personnes de plus

de 75 ans dans le besoin 3 3 0 1

Impôt sur le revenu : abattement pour durée de détention applicable aux

cessions de titres ou droits par les dirigeants de PME partant à la retraite 360 260 350 509

Vieillesse - invaliditéImpôt sur le revenu : réduction au titre des frais de dépendance et

d'hébergement pour les personnes dépendantes accueillies en établissement

spécialisé 161 175 185 263Impôt sur le revenu : exonération des plus-values de cession réalisées par les

titulaires de pensions de vieillesse ou de la carte d’invalidité dont les revenus

n’excèdent pas certaines limites 15 15 15 20

Impôt sur le revenu : crédit d'impôt en faveur des dépenses d'équipements de

l'habitation principale en faveur de l'aide aux personnes 30 30 25 30 32 35 32 36 26Impôt sur le revenu : exonération de la prise en charge directe à titre de

pensions alimentaires des dépenses d’hospitalisation ou d’hébergement en

établissement 10 10 10 16

Vieillesse - invalidité-survie

Taxe d'habitation : Exonération en faveur des personnes âgées, handicapées

ou de condition modeste 1,220 1,250 1,345 1,327 1,233 1,319 1,237 1,255

Impôt sur le revenu : réduction pour dépenses d'accueil dans un

établissement pour personnes âgées dépendantes (long séjour) 15 13 13 14 19

Table Annex I.A.2.1

Detailed information on the impact of the tax system on social expenditure (cont.)

OECD Social Expenditure database (www.oecd.org/els/social/expenditure) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/els/social/depenses) - Version 17-10-2016

Impôt sur le revenu : abattement en faveur des personnes âgées ou invalides 23 24 22 25

Invalidité - survie

Mutations à titre gratuit : abattement effectué sur l’actif taxable aux droits de

mutation revenant à tout héritier, légataire ou donataire handicapé physique

ou mental 85 70 80 60

Famille - survie

Impôt sur le revenu : mantien du quotien conjugal des veufs pour enfants à

charge 80 85 80 110

Famille-invalidité

Impôt sur le revenu : quotient familial 9,700 9,866 10,987 11,528 10,098 10,249 12,428 11,036

Taxe d'habitation : abattement pour charge de famille 1,070 1,130 1,300 1,283 1,283 1,283 1,283 1,283 1,283

Taxe d'habitation : effet du quotient familial sur les dégrèvements partiels 100 100 120 118 118 118 118 118 118

FamilleImpôt sur le revenu: déduction des pensions pour enfants majeurs étudiants

(et mineurs et ascendants à partir de 2009) 280 290 333 265 1,110 1,126 1,201 1,344

Impôt sur le revenu : réduction d'impôt pour enfants scolarisés 400 399 372 216 366 372 360 377Impôt sur le revenu : crédit/réduction d'impôt pour frais de garde d'enfants

de moins de 7 ans 190 200 131 350 780 840 878 920 940 1,025 1,145Impôt sur le revenu : abattement en faveur des contribuables ayant des

enfants mariés à charge 10 10 12 2

Impôt sur le revenu : régime spécial d'imposition des assistantes maternelles 140 140 140 200Impôt de solidarité sur la fortune : réduction d'impôt en raison du nombre

d'enfants 22 22 12 -

Autres domaines de politique sociale

Impôt sur le revenu : Prime Pour l'Emploi 2,518 2,145 2,210 2,450 2,700 3,240 4,520 4,480 3,917 3,311 3,000 2,900 2,353

Impôt sur le revenu : crédit d'impôt exceptionnel aux contribuables modestes 1,004

Taxe d'habitation : dégrèvement total pour les titulaires du RMI 200 285 295 291 96 26 3 -

Impôt sur le revenu : réduction pour dons aux personnes en difficulté 40 50 82 133 127 128 118 124

Politiques actives du marché du travail

Impôt sur le revenu : crédit d'impôt en cas de déménagement pour reprise

d'une activité salariée 60 72 15 4

Crédit d’impôt en faveur des jeunes de moins de vingt-six ans s’orientant

vers un emploi qui connaît des difficultés de recrutement 15 22 40 26Logement

Foncier bâti : exonération des immeubles à caractère social 4 8 18 37

Taxe d'habitation : dégrèvement en faveur des personnes de condition

modeste relogées dans le cadre du programme ANRU 0 25 27 32

Tax breaks to stimulate private social protection (not including pensions)0 0 0 8 2,105 2,205 5 5

Invalidité - survie

Impôt sur le revenu : réduction au titre des primes des contrats de rente

survie et contrats d'épargne handicap 8 5 5 5 5

Santé

Taxe sur les conventions d'assurance : exonération en faveur de certains

contrats d'assurance maladie complémentaire 2,100 2,200 - -

Memorendum items

0 0 0 430 1,074 1,179 1,452 1,739

Vieillesse

Impôt sur le revenu : déduction des cotisations versées au titre de l'épargne

individuelle et facultative 360 339 344 365 504

Impôt sur le revenu : déduction du revenu imposable des cotisations de

retraite ou de prévoyance complémentaire versées à titre facultatif 700 800 1,050 1,200

par les non-salariés et leurs conjoints collaborateurs

Impôt sur le revenu: déduction des versements effectués en vue de la retraite

mutualiste du combattant 70 35 35 37 35

*2007 estimates

Sources 2009-2013: DREES, based on estimates from INES model (DREES-INSEE), the Projets de loi des finances (Direction Générale des Impôts) and the Comptes de la protection sociale (DREES).Sources 2001-2007: Direction Générale des Impôts, INES model (DREES/INSEE).

OECD Social Expenditure database (www.oecd.org/els/social/expenditure) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/els/social/depenses) - Version 17-10-2016

GERMANY

A. Amount of direct tax paid on benefit income (in millions of euros)

2001 2003 2005 2007 2009 2010 2011 2012 2013

Direct taxes and social contributions paid on public cash benefits 25,845 27,074 33,014 34,712 41,812 41,871 43,949 45,817 47,650

Social contributions paid by recipients of benefits (unemployment , disability, etc.) 16,534 17,949 21,092 22,024 27,351 27,454 28,594 29,237 30,057

Income tax on pensions 5,134 4,749 6,900 8,050 9,460 9,380 10,020 11,040 11,830

Social security contributions 1,094 1,219 1,920 2,087 2,287 2,296 2,409 2,470 2,542 Soc. Sec. Cont. on old-age security for farmers 253 268 266 274 283 275 278 275 275 Soc Sec Cont on pension schemes of liberal professions 165 204 244 299 359 376 404 429 463 Supplementary Pensions by public employers 677 747 1,410 1,515 1,645 1,645 1,727 1,765 1,804

Progressionsvorbehalt 1,600 1,670 1,895 2,070 1,980 2,030 2,190 2,300 2,430

Tax and social contributions on family allowances for public servants 1,483 1,488 1,207 481 734 712 736 770 791

Direct taxes and social contributions paid on mandatory private cash benefits 9,619 9,079 7,704 8,399 9,965 9,899 11,062 12,513 13,650Continued wage payments in case of sickness (Entgeltfortzahlung) 9,619 9,079 7,704 8,399 9,965 9,899 11,062 12,513 13,650Continued Wage Payments: Maternity and parental leave

Direct taxes and social contributions paid on voluntary private cash benefits 3,028 3,222 5,037 5,514 5,998 5,484 5,883 6,020 6,199

Tax over BAV (company pension) 1,189 1,306 1,775 1,935 2,190 1,640 1,790 1,795 1,815

Soc. Sec. cont over BAV (company pension) 1,527 1,597 3,028 3,500 3,808 3,844 4,093 4,225 4,384Tax and soc.sec. cont over other benefits by employers 312 319 234 79

B. Average implicit indirect tax rates of consumption out of benefit incomeIndirect taxes paid out of consumption of cash transfers, in millions of euros

2001 2003 2005 2007 2009 2010 2011 2012 2013

(1) Private final consumption expenditure 1,250,347 1,280,872 1,328,551 1,384,900 1,413,041 1,446,274 1,495,533 1,533,829 1,562,704

(2) Private consumption plus Government consumption minus Government wages 1,478,355 1,519,581 1,569,314 1,640,465 1,696,436 1,736,082 1,792,579 1,843,650 1,885,995

(3) General consumption taxes plus excise duties (5110+5121) 200,521 206,353 205,306 234,198 241,704 243,985 256,572 259,221 261,950

5110 General taxes 138,935 137,568 140,121 170,387 178,020 180,533 190,229 194,353 197,326 5121 Excises 61,586 68,785 65,185 63,811 63,684 63,452 66,343 64,868 64,624

(4) Taxes on production sale transfer (5100) 210,641 217,610 217,709 247,547 254,971 256,859 271,046 274,219 277,659

(5) Taxes on Goods and Services (5000) 219,252 225,190 226,641 256,708 264,523 266,014 281,180 285,221 288,064

Implicit average indirect tax rate on consumption out of benefit income:

(6) using general consumption taxes plus excise duties (3)/(2) 13.6% 13.6% 13.1% 14.3% 14.2% 14.1% 14.3% 14.1% 13.89%

(7) using a broad concept of the indirect tax base (5)/(2) 14.8% 14.8% 14.4% 15.6% 15.6% 15.3% 15.7% 15.5% 15.27%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 17.5% 17.6% 17.1% 18.5% 18.7% 18.4% 18.8% 18.6% 18.43%

Table Annex I.A.2.1

Detailed information on the impact of the tax system on social expenditure (cont.)

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue Statistics database

(http://stats.oecd.org/Index.aspx?DataSetCode=REV) for lines 3, 4, and 5.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

GERMANY

Table Annex I.A.2.1

Detailed information on the impact of the tax system on social expenditure (cont.)

C. Tax breaks for social purposes (in millions of euros)

2001 2003 2005 2007 2009 2010 2011 2012 2013

Tax breaks similar to cash benefits 33,327 36,473 32,743 30,283 28,174 29,373 28,668 28,481 28,277

Special expenses for owner-occupied homes 1,733 430 30Child component in conjunction with sec.10 e EStG (sec. 34 f EStG) 460 65 30Owner-occupied Homes Premium Law, total 8,050 10,536 10,247 7,722 4,972 3,616 2,378 1,366 542

Employee savings premiums for productive investment (sec. 19 a EStG) 41 41 36 80 97 122 150 150 150

Deduction of occupational training expenses 79 85 90 90 100 95 95 100 105Motor vehicle tax exemption for physically disabled persons 135 130 140 146 135 130 125 120 120Household allowance 1,100 1,000 340 350 360 355 350 355 365Deduction for extraordinary financial burdens 465 475 650 675 970 1,035 1,060 1,105 1,165Deduction for extraordinary financial burdens in special instances 1,094 659 845 845 805 815 810 840 885Lump sum allowances for the physically disabled and others 798 810 805 740 955 960 950 990 1,040Lump sum care allowance 72 72 60 60 65 65 70 75 75Childcare expenses (Kinderbetreuungskosten) 170 160 245 345 420 430 440 490Family benefits (child tax credit ) 19,300 22,000 19,310 19,330 19,370 21,760 22,250 22,940 23,340 For information: Family benefits (Familienlastenausgleich: tax credit + cash benefits) (32 021) (36 080) (36 600) (36 240) (38 570) (41 200) (40 960) (41 180) (41 140)

Tax breaks to stimulate private social protection (not including pensions) 9,480 9,485 9,480 10,580 9,970 18,510 19,800 20,330 21,550

Exclusion of contributions to health and accident insurance 8,400 8,400 8,400 9,300 8,820 17,020 18,150 18,700 19,850

Donations to (approved) NGOs and political parties 1,080 1,085 1,080 1,280 1,150 1,490 1,650 1,630 1,700

Memorandum Item

Tax breaks to pensions 17,520 18,280 19,585 20,270 20,730 19,610 26,470 30,270 31,880

- Deduction of contributions to public pensions 14,300 15,100 16,500 17,400 18,110 19,150 26,040 29,870 31,500

- Deduction of private life insurances 2,300 2,200 2,100 2,000 1,800

- Lump sump taxation of contributions to occupational pension plans 920 980 985 870 820 460 430 400 380

Sources : Bundesministerium fur Arbeit und Soziales (BMAS) = Federal Ministry of Labour and Social Affairs, Germany = red text

Bundesministerium der Finanzen (BMF) = Federal Ministry of Finance, Germany = blue figures

a) Donation to political parties are not in the social domain. However, the value of these donations cannot be separately identified, but is considered smaller that the donations to NGOs, and therefore this item is included in the list here.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

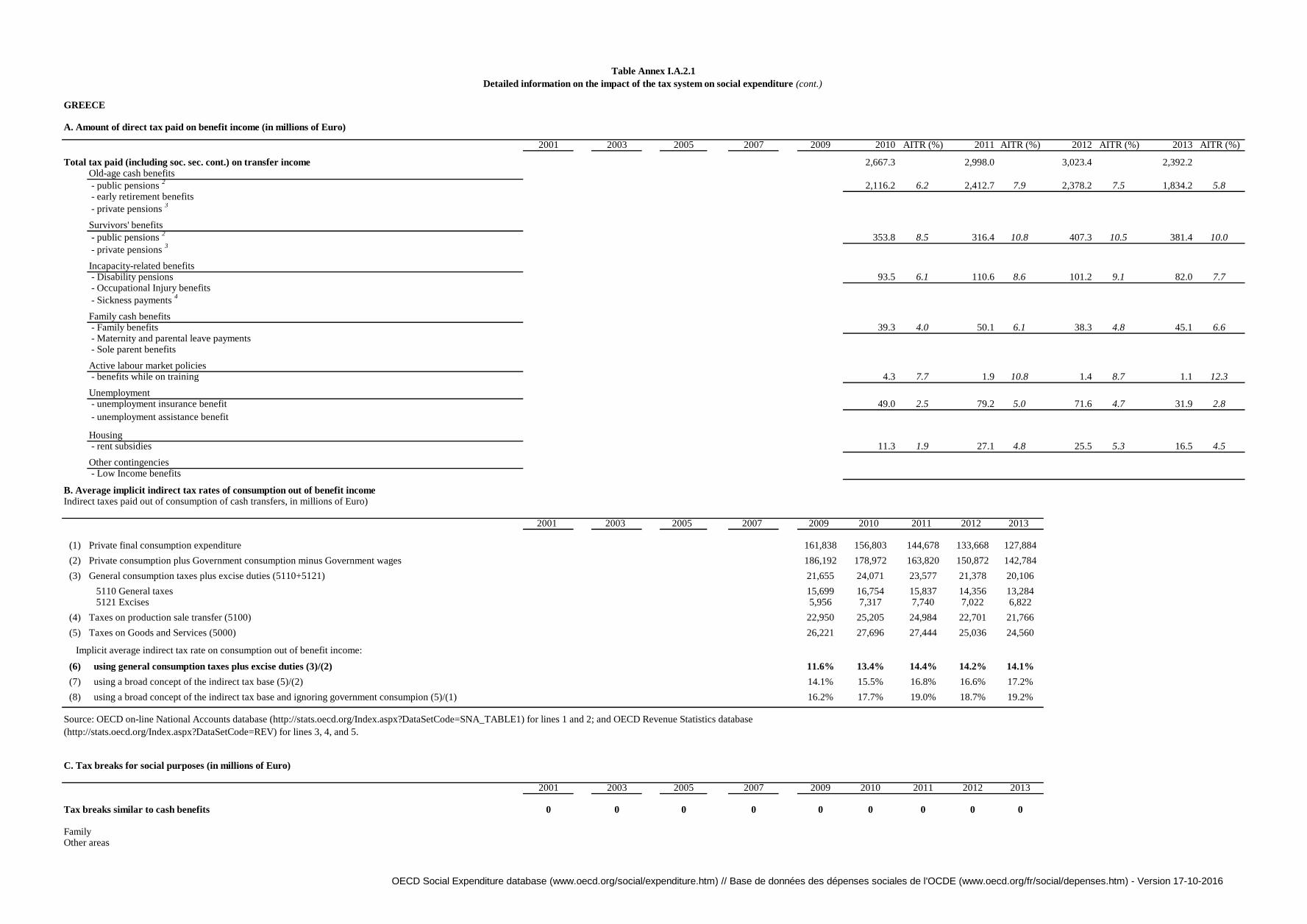

GREECE

A. Amount of direct tax paid on benefit income (in millions of Euro)

2001 2003 2005 2007 2009 2010 AITR (%) 2011 AITR (%) 2012 AITR (%) 2013 AITR (%)

Total tax paid (including soc. sec. cont.) on transfer income 2,667.3 2,998.0 3,023.4 2,392.2Old-age cash benefits

- public pensions 2

2,116.2 6.2 2,412.7 7.9 2,378.2 7.5 1,834.2 5.8 - early retirement benefits

- private pensions 3

Survivors' benefits

- public pensions 2

353.8 8.5 316.4 10.8 407.3 10.5 381.4 10.0

- private pensions 3

Incapacity-related benefits - Disability pensions 93.5 6.1 110.6 8.6 101.2 9.1 82.0 7.7 - Occupational Injury benefits

- Sickness payments 4

Family cash benefits - Family benefits 39.3 4.0 50.1 6.1 38.3 4.8 45.1 6.6 - Maternity and parental leave payments - Sole parent benefits

Active labour market policies - benefits while on training 4.3 7.7 1.9 10.8 1.4 8.7 1.1 12.3

Unemployment - unemployment insurance benefit 49.0 2.5 79.2 5.0 71.6 4.7 31.9 2.8

- unemployment assistance benefit

Housing - rent subsidies 11.3 1.9 27.1 4.8 25.5 5.3 16.5 4.5

Other contingencies - Low Income benefits

B. Average implicit indirect tax rates of consumption out of benefit incomeIndirect taxes paid out of consumption of cash transfers, in millions of Euro)

2001 2003 2005 2007 2009 2010 2011 2012 2013

(1) Private final consumption expenditure 161,838 156,803 144,678 133,668 127,884

(2) Private consumption plus Government consumption minus Government wages 186,192 178,972 163,820 150,872 142,784

(3) General consumption taxes plus excise duties (5110+5121) 21,655 24,071 23,577 21,378 20,106

5110 General taxes 15,699 16,754 15,837 14,356 13,284 5121 Excises 5,956 7,317 7,740 7,022 6,822

(4) Taxes on production sale transfer (5100) 22,950 25,205 24,984 22,701 21,766

(5) Taxes on Goods and Services (5000) 26,221 27,696 27,444 25,036 24,560

Implicit average indirect tax rate on consumption out of benefit income:

(6) using general consumption taxes plus excise duties (3)/(2) 11.6% 13.4% 14.4% 14.2% 14.1%

(7) using a broad concept of the indirect tax base (5)/(2) 14.1% 15.5% 16.8% 16.6% 17.2%

(8) using a broad concept of the indirect tax base and ignoring government consumpion (5)/(1) 16.2% 17.7% 19.0% 18.7% 19.2%

C. Tax breaks for social purposes (in millions of Euro)

2001 2003 2005 2007 2009 2010 2011 2012 2013

Tax breaks similar to cash benefits 0 0 0 0 0 0 0 0 0

FamilyOther areas

Table Annex I.A.2.1

Detailed information on the impact of the tax system on social expenditure (cont.)

Source: OECD on-line National Accounts database (http://stats.oecd.org/Index.aspx?DataSetCode=SNA_TABLE1) for lines 1 and 2; and OECD Revenue Statistics database

(http://stats.oecd.org/Index.aspx?DataSetCode=REV) for lines 3, 4, and 5.

OECD Social Expenditure database (www.oecd.org/social/expenditure.htm) // Base de données des dépenses sociales de l'OCDE (www.oecd.org/fr/social/depenses.htm) - Version 17-10-2016

GREECE

Table Annex I.A.2.1

Detailed information on the impact of the tax system on social expenditure (cont.)

Tax breaks to stimulate private social protection (not including pensions) 0 0 0 0 0 0 0 0 0

Memorendum item

Tax breaks to pensions 0 0 0 0 0 0 0 0 0

Source : International Economic Relations Directorate, Tax Affairs Section.

Note : AITRs and amounts of taxes (including Social Security Contributions) paid by recipients, is based on the annual EU SILC survey conducted by ELSTAT for the relevant years.

The survey’s average sample size is about 7.200 beneficiaries for the last two reference years.

The weights of the survey’s cases that have been used are associated with the number of individual’s that took advantage of a benefit, not with the amount of the benefit itself.

Also estimations for the taxes imposed to the individual’s benefit income have been evaluated according to his/her yearly overall gross income, employing properly escalating tax coefficients in valid for the related year.