Embed Size (px)

Citation preview

T+2 shortened settlement cycle

February 2016

T+2 shortened settlement cycle 2

Shortened settlement (T+2) overview

• There are parallel industry initiatives in the US and Canadian markets to shorten the time frame between trade execution and

settlement from three days (T+3) to two days (T+2).

• This initiative covers all Depository Trust Company (DTC) settling products (equities, corporate bonds, municipal bonds and

unit investment trusts) and products traded on the Canadian exchanges (e.g., the Toronto Stock Exchange). It is expected to

have a significant impact on the middle- and back-office operations and technology supporting the trade life cycle.

• The Industry Steering Committee (ISC), composed of the DTCC, the Association of Global Custodians (AGC), the Association of

Institutional Investors (AII), the Investment Company Institute (ICI), the Securities Transfer Association (STA), and the

Securities Industry and Financial Markets Association (SIFMA) released a white paper in June 2015 proposing a target

migration to a T+2 settlement cycle in Q3 2017.

• The Canadian Depository for Securities (CDS) released a white paper in September 2015 calling for Canada to go live with T+2

on the same date as the US.

• Individual organizations need to make the necessary changes by Q1 2017 in order to be ready for industry-wide testing, which

is planned for Q2 2017.

• Industry-level requirements need to be understood and translated into impact for individual firms.• Organizations need to plan, build and iterate while the regulations are being drafted and published.• Adequate preparation for industry-level testing will be critical for each organization.

US settlement cycle for DTCC-settling securities

T+2 shortened settlement cycle 3

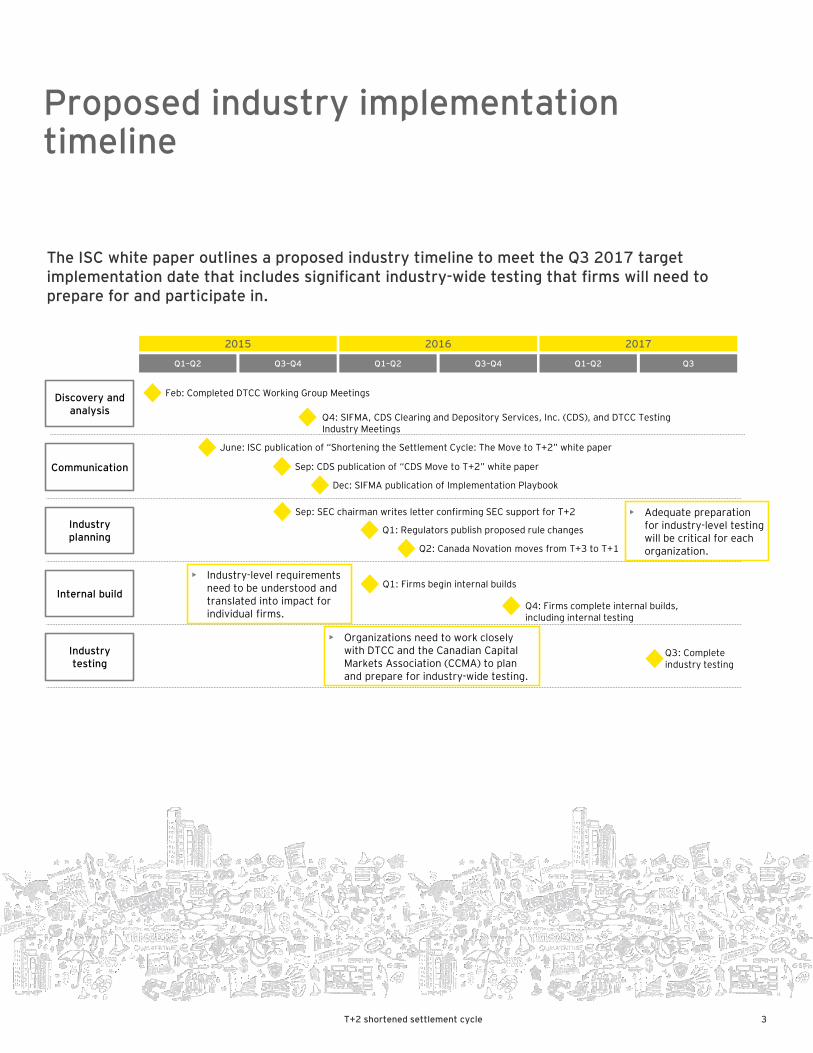

Proposed industry implementation timeline

The ISC white paper outlines a proposed industry timeline to meet the Q3 2017 target implementation date that includes significant industry-wide testing that firms will need to prepare for and participate in.

Communication

2015

Discovery and analysis

Feb: Completed DTCC Working Group Meetings

June: ISC publication of “Shortening the Settlement Cycle: The Move to T+2” white paper

Sep: CDS publication of “CDS Move to T+2” white paper

Industry planning

Sep: SEC chairman writes letter confirming SEC support for T+2

Q1: Regulators publish proposed rule changes

Internal build

Industry testing

2016

Q1–Q2 Q3–Q4

2017

Q1–Q2 Q3Q1–Q2 Q3–Q4

Q3: Complete industry testing

• Industry-level requirements need to be understood and translated into impact for individual firms.

• Organizations need to work closely with DTCC and the Canadian Capital Markets Association (CCMA) to plan and prepare for industry-wide testing.

• Adequate preparation for industry-level testing will be critical for each organization.

Q1: Firms begin internal builds

Q4: Firms complete internal builds, including internal testing

Q4: SIFMA, CDS Clearing and Depository Services, Inc. (CDS), and DTCC Testing Industry Meetings

Dec: SIFMA publication of Implementation Playbook

Q2: Canada Novation moves from T+3 to T+1

T+2 shortened settlement cycle 4

How EY can help in the journey

EY can support organizations impacted by T+2 settlement across the multiple phases of the journey plan, leveraging tools, accelerators, leading practices and experienced practitioners.

T+2 shortened settlement cycle 5

Illustrative impact heat map

Securities operations and technology functions will be impacted by the move to T+2 in varying degrees. The following are examples of key changes that may be required across functions:

Trade support

Syndicate operations

Trade captureTrader

reconciliations

Streetside reconciliation

Middle office

AllocationsAffirmations/confirmations

Trade affirmations

Settlement

Clearing Settlement

Physical securities

Fails management

Securities lending

Mark-to-market

Inventory management Billing

Recalls andbuy-ins

Funding and treasury

Firm funding and financing

Cash management

Projections from financing

Tax/regulatory reporting

Tax reporting

Operational management

reporting

Financial reporting

Trade and position

reporting

Client onboarding

Document management

Anti-money laundering

(AML)/know your customer (KYC)

Account opening

Settlement instruction

management

Asset servicing

Announcement creation

Entitlement capture Payments

Election/instruction

Collateral management

Agreements documentation

Segregation

Margin calculation

Margin calls

Enterprise functions

Position keeping

Books and records

Reference data

► Updates to security reference data to reflect settlement calendar correctly

► Updates to stock record and accounting systems to reflect change in settlement date

► Thorough end-to-end testing of all reference data will be required to make sure all updates are captured correctly

► Update triggers and aging logic to enable accurate reporting for management of settlement risk

► Counterparty credit exposure reports may need to be updated and tested to enable accuracy within the shortened settlement cycle

► Potential change in projection process to incorporate activities completed on TD

► Updates to systems used to generate projections in order to produce earlier estimates

► FX deadlines for cross-border activity

► Leverage electronic fund transfers vs. physical checks

► Updates to systems supporting the margin calculation and processing of margin calls

► Increased resources may be required to handle the documentation changes to support the move to T+2

► Negotiate service-level arrangements with counterparties regarding the timeline for providing settlement instructions for new or existing accounts

► Update the notification triggers for new subaccounts received over Oasys or other automated allocation platforms to reduce lag time

► Improve coordination with upstream teams prior to key event dates to reduce risk of unintended elections

► Update corporate action and dividend processing systems for ex-dates and cover/protect expiration dates

► Proactive matching and inventory management to reduce/manage fails and enable compliance with the US Securities and Exchange Commission’s Rule 204 (SEC 204)

► Increase focus on processing of dual listed securities, American depository receipts, exchange-traded funds, “when issued,” and 144a/Reg S products

► Negotiate arrangements with counterparties for providing allocations on Trade Date (TD)

► Enable TD matching and affirmation and maximize affirmation/settlement rates

► Frequent communication with clients

► Update the notification triggers and modify controls to identify and escalate aged breaks earlier in settlement cycle

► Potential for system process changes depending on existing automation (e.g., batch timing and break aging logic)

► Expedite recall process to take place on TD in order to minimize settlement risk

► Revise and test billing calculations to maintain accuracy within the shortened settlement cycle

► Eliminate manual activities impeding efficient inventory management

Impact key: High impact

Medium impact

Lowimpact

Prospectus fulfillment

Foreign exchange (FX)

T+2 shortened settlement cycle 6

Key considerations

When implementing an accelerated settlement cycle, firms should consider several factors across the program life cycle. Each step should take into account impacts to people, process and technology, as well as the capacity to manage a complex change initiative.

• All relevant stakeholders identified with clear ownership, responsibility and engagement

• Lessons from European changes are understood and applied effectively

• Alignment with industry, including clients, counterparties, vendors and utilities

• Systematic identification of all key in-scope systems, processes and reference data that will be impacted by accelerated settlement

• Analysis and prioritization of risk areas that hinder acceleration of settlement across technology (e.g., batch updates), processes (e.g., manual processes to conduct reconciliations) and external parties (e.g., clients with highest risk of non-compliance)

• In-flight and planned strategic and tactical changes incorporated as part of the overall plan

• Need to consider implications on both process and technology change while developing business requirements

• Balance the opportunity to enhance operational efficiency across the trade life cycle with the need to make expeditious changes to comply with accelerated settlement

• Testing strategy decisions (e.g., dedicated T+2 environments vs. use of existing environments) on how the changes will be implemented and need to be finalized early

• Prioritization and sequencing of testing based on risks and complexity to minimize regression-testing impacts

• End-to-end testing to cover from pre-execution to settlement, including all corporate actions

• Management decisions are required on the extent and degree of industry testing (e.g., trading venues for participation, criteria for certification of readiness, specific areas where industry testing may be omitted vs required).

• Banks are required to sign-off or certify readiness for T+2 post-testing.

• Environments would need to be set up and synchronized with copy of production data.

• Contingency planning must be developed for the migration weekend to make sure technology platforms are up and running and support is on hand.

• Management of the double-settlement date will be critical for a smooth transition

Program management

Readiness assessment

Testing

Go-live/post-implementation

Key considerations

Design and development

T+2 shortened settlement cycle 7

Why EY?

EY is highly qualified to assist sell-side firms, buy-side firms and custodians with the T+2 shortened settlement cycle initiative, bringing a dedicated Capital Markets practice, a deep pool of advisors with extensive operations experience, a strong record of working on industry initiatives, and world-class program management accelerators and tools.

• EY has a dedicated Capital Markets practice with a deep pool of over 500 advisors across the globe.

• We are currently assisting over 15 global systemically important banks (G-SIBS) with a range of operations and technology initiatives related to the trade life cycle.

• EY has a depth of advisory experience in process, technology and operational risk management allows our clients to optimize their operating capabilities.

Accelerate results by leveraging EY understanding of securities operations and sharing industry leading practices

• EY has a deep pool of knowledgeable advisors with decades of industry experience leading front-, middle- and back-office trade processing operations.

• We have respected technologists with proven architecture, infrastructure, integration and data management skills.

• EY has deep experience in securities operations processing, including client onboarding, trade support, settlements and asset servicing. EY has leveraged these capabilities to help clients identify areas of improvement and implement large-scale global transformational initiatives.

Leverage a deep bench of subject-matter resources tosupport seamless execution of all phases of the initiative

• EY has extensive experience running complex global program management offices (PMO). These programs touched on all components of the trade life cycle and leveraged world-class accelerators and tools.

• EY has served as a key partner to global trading firms in developing operations and technology strategies, including large-scale transformations with industry organizations.

• EY as a firm and its individuals have held key roles in industry consortiums and utilities.

Increase confidence that deliverables will be met and deliver value with proven track record on complex engagements

• EY was selected as program management office for various industry groups and consortia to help clients with: • Implementation of the final margin policy

framework for over-the-counter derivatives• Drafting of recovery and resolution

planning playbooks for banks with financial market utilities

• EY has a program management team with capital markets knowledge and the seniority and relevant experience to coordinate, govern and report on this complex initiative.

Provide end-to-end PMO support for all phases of the initiative across operations and technology

Dedicated Capital Markets practice

Deep pool of advisors with

extensive operations experience

Strong track record of working on

industry initiatives

World-class PMOaccelerators and

tools

Value propositionEY differentiators and experience

T+2 shortened settlement cycle 8

Key Ernst & Young LLP contacts

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

© 2016 Ernst & Young LLP.All Rights Reserved.SCORE No. CK10501602-1822183 NY

Roy ChoudhuryPrincipal, Ernst & Young LLP Office: +1 212 773 [email protected]

Nagaraj SwaminathanExecutive Director, Ernst & Young LLP Office: +1 212 773 [email protected]

Matthew FischerSenior ManagerOffice: +1 212 773 [email protected]