Embed Size (px)

Citation preview

Systemic Risk in ASEAN-6: A New

Empirical Investigation∗

Trung H. Le

Banking Faculty, Banking Academy of Vietnam

Current version: April 15, 2020

Abstract

We provide the first study on systemic risk of banking sector in the

ASEAN-6 countries. In particular, we investigate the systemic risk dynamics

and determinants of 49 listed banks in the region using the SRISK measure

of Brownlees and Engle (2017) over the 2000-18 period. We document

significant variations of systemic risk in each country, which are currently

at par or higher level than the recent global financial crisis. Our empirical

evidence advocates capital surcharges on the systemically important financial

institutions. We also encourage the regional regulators to account for the

idiosyncratic characteristics of their banking sector in designing effective

macroprudential policy to contain the systemic risk.

JEL classification:

Keywords: Systemic Risk, SRISK, Banking, ASEAN-6

∗Corresponding author is Trung H. Le: [email protected]

1

1 INTRODUCTION

One of the main reasons for the outbreak of the recent global financial crisis was the

widespread failures and losses of undercapitalized financial institutions. When financial

institutions face a negative shock to their capital, a typical response is selling assets or

raising capital in the market (Engle and Ruan, 2019). However, if the whole system is

also undercapitalized, the shocks may not be absorbed by other strong competitors and

aggravated to an aggregate capital shortage of the financial sector (Acharya et al., 2012,

2017). When this shortage is extreme, it could significantly reduce the aggregate supply

of credit and consequently hit the real economy (Brownlees and Engle, 2017). Thus, the

focus of post-crisis regulation has changed from keeping individual institutions sound to

containing the systemic risk, which is the risk of correlated failures in the financial sector

(Meuleman and Vander Vennet, 2020). In this context, measuring and monitoring systemic

risk are fundamental tasks for the banking supervisors to design relevant macroprudential

policy aiming at maintaining the stability of the financial market.

This paper provides the first study on the systemic risk of ASEAN-6 countries,

including Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam. This area

has been one of the most dynamic regions with rapid economic growth and increasing

financial integration.1 In particular, the financial system of these countries is bank-based

with the banks holding the predominant source of financing (Ha et al., 2019). Bats

and Houben (2020) find that the bank-based financial structure is associated with

higher systemic risk, compared to that of a market-based economy, due to the risky

nature of banks with high leverage, large asset-liability mismatches and high level of

interconnectedness. Thus, a detrimental shock to the bank stability could easily exacerbate

significant distress to the region’s economy. Against this background, we address two

questions. First, what are the levels and rankings of the bank’s systemic risk in the

ASEAN-6 countries? Second, what are the drivers of the bank’s exposure to systemic

risk in each country? The answers to these two questions are of particular interest to

the regional policymakers in designing macroprudential tools aiming at regulating and

reducing the systemic risk in the banking industry.

Measures of systemic risk have been widely developed in the aftermath of the global

financial crisis of 2007-2009.2 One approach is the scoring methodology developed by

the Basel Committee on Banking Supervision (BCBS). It starts with the requirement of

identifying the systemically important financial institutions (SIFIs), which are subjected

to higher capital requirements. Intuitively, this measure combines information about

the systemic importance of an institution with regards to four categories: size,

1According to the 2019 ASEAN Economic Integration Brief (ASEAN Secretariat, 2019) , theaverage real GDP growth of the ASEAN-6 countries in 2018 is 5.1%, compared to 3.6% of theglobal GDP growth

2Detailed surveys on the development of systemic risk measurements can be found in Bisiaset al. (2012) and Benoit et al. (2017).

1

cross-jurisdiction activity, complexity and substitutability.3 While this approach can be

useful in ranking banks at a given point in time, the use of accounting data limits its

usages to monitor systemic risk over time. Thus, growing measures of system risk exploit

the publicly market data to measure the systemic risk. This approach draws on the idea

that, if the market is efficient, the level and contribution of an institution to systemic risk

can be captured by the correlation between its stock price and the whole market. The

main advantage of these market-based measures is its ability to estimate systemic risk in

real-time and detect potential shifts in the systemic risk regimes.

In this study, we employ the market-based SRISK measure of Acharya et al. (2012)

and Brownlees and Engle (2017) to investigate the systemic risk of the ASEAN-6’s banking

sector. SRISK corresponds to the expected capital shortfall of a financial institution

conditional on a prolonged market stress. Thus, a bank with high SRISK imposes

pressure on the undercapitalization of the financial sector during the stressed period,

which subsequently produces negative externalities to the real economy. The idea is that

the undercapitalisation of financial institutions is a signal of excessive credit growth in the

financial sector (Engle and Ruan, 2019). When “credit boom goes bust”, the risky credit

that is typically issued at the end of the credit cycle would result to significant losses

to the financial sector and likely to initiate a financial crisis (Reinhart and Rogoff, 2011;

Schularick and Taylor, 2012). Brownlees and Engle (2017) finds that the aggregate SRISK

can also serve as an early warning signal of distress in the U.S., whereas Engle et al. (2015)

provide a similar result for European countries. The use of SRISK to measure systemic

risk has been widely applied in many recent empirical studies (see, amongst other Buch

et al., 2019; Bostandzic and Weiß, 2018; Colletaz et al., 2018; Brownlees et al., 2020; Bats

and Houben, 2020).

Another popular market-based systemic risk measure is the so-called ∆CoVaR of

Adrian and Brunnermeier (2016). ∆CoVaR considers the sensitivity of the overall market

to a particular institution by examining the risk of system losses conditional on that

institution being under financial distress.4 We prefer SRISK over ∆CoVaR because of two

main reasons. First, SRISK combines information from the market and balance sheet of

the financial firm, rather than purely rely on the market price. In particular, SRISK is

a function of a financial firm’s size, degree of leverage and level of dependence with the

market return. Thus, this specification can also capture the evidence that size is typically

an important determinant of systemic risk (see, for example, DeJonghe, 2010; Laeven

et al., 2016; Varotto and Zhao, 2018) and the high leverage nature of banking business

increases its risk exposure when the economy is weak (Acharya and Thakor, 2016; Bats and

Houben, 2020). Second, while SRISK focuses on the shortage of capital shortfall facing

3This methodology is currently implemented by the Financial Stability Board to classify a setof financial institutions as the Global Systemic Important Financial Institutions (G-SIFIs)

4Girardi and Tolga Ergun (2013) generalise the original ∆CoVaR to several more extremeevents, whereas Bonaccolto et al. (2019) extend the estimation process to include the state atwhich the financial system and the conditional firm are jointly in distress

2

financial institution conditional on the systemic distress, ∆CoVaR takes an opposite view

and determine the risk of financial system due to the effect of distress in one particular

firm. Engle (2018) argues that this approach is only valid when the health of other firms

is holding constant. In other words, it ignores the high interdependence between financial

institutions and could lead to the inference of many systemic firms even if only one is.

We investigate the SRISK on 49 listed banks in the ASEAN-6 from January, 2000

to December, 2018. Not surprisingly, Singapore has the highest systemic risk exposure

on average, as well as at the end of the study period, given the relatively large size of

their banking sector. Importantly, the systemic risk of ASEAN-6 countries, except for

only Philippines, has been increasing significantly and currently at par or even higher

level than the exposure during the global financial crisis. We then follow Engle and Ruan

(2019) to examine the severity of potential crisis caused by systemic risk. The systemic

risk severity is based on the cost of alternative strategies that banks may need to compel

to strengthen their balance sheet, which are appealing for a bailout, selling existing assets

and raising capital by selling new shares. The loss of GDP to bailout banks under stress

is highest in Singapore as expected, at 17% of GDP. If the banks choose to sell assets or

shares to reduce their capital shortfall, however, Vietnamese banks would have suffered the

most severity, followed by Thailand. Economically, Vietnamese banks would need to sell

62.5% of their total asset or approximately 45% worth of the current market capitalisation

to reduce the SRISK to zero. Such large sale of asset and equity could trigger the “fire

sale externality”, that could further dampen the undercapitalisation of the banking sector

and leads to a financial crisis (Engle and Ruan, 2019). Finally, we identify the most

systemically risky banks for each country as of December 2018. This list can be useful for

the regulators to monitor and apply capital surcharge on these so-called SIFIs to reduce

their risk exposures to the financial system.

Last, we analyse the determinants of systemic risk of banks in the region. We

find strong evidence of the too-big-to-fail paradigm, with which bank size is positively

related to the systemic risk (see, e.g., Laeven et al., 2016; Buch et al., 2019; Silva-Buston,

2019, for similar results). Moreover, banks with a more traditional business model,

lower quality loan portfolios, less profitable and lower market-to-book values are generally

associated with higher systemic risk. Notably, we do not find consistency in the empirical

results across ASEAN-6 countries. This finding implies that the regional supervisors

need to account for the fundamental differences in economic development, institutional

environment in designing relevant regulatory frameworks for the systemic risk.

The rest of the paper is organized as follows. Section 2 presents our measure

of systemic risk. In section 3, we present our data and examine the properties and

determinants of systemic risk in ASEAN countries. Section 4 discusses the implications

of our results to the policy makers while the last section concludes the paper.

3

2 SYSTEMIC RISK MEASURE

We employ the SRISK measure developed by Acharya et al. (2012) and Brownlees

and Engle (2017) to measure the systemic risk of a bank based on its capital shortfall

conditional on a systemic event. In particular, the SRISK measure how much capital

would a bank need to raise on a prolonged market decline. Thus, the calculation of SRISK

shares the same spirit of the stress test that is typically employed by the regulators but

it has the advantage of being more responsive to changes in the market and involves only

publicly available information.

2.1 Conditional Capital Shortfall

Brownlees and Engle (2017) defines the capital shortfall of bank i in day t (CSi,t) as the

difference between the regulatory capital that the bank needs to hold and its market value

of equity.

CSi,t = kAi,t −Wi,t = k (Di,t +Wi,t)−Wi,t (1)

where k is the prudential capital ratio, which is set at 8% as similar to the international

standards and current practices of countries under consideration in this study. Ai,t is the

value of quasi assets, which comprises of the book value of debt, Di,t, and the market value

of equity, Wi,t. The formulation of Eq. (1) implies that the bank faces a capital shortfall

when its market value of equity falls below the required capital reserves, i.e. CSi,t < 0.

The SRISK measures the level of capital shortfall for the bank in case of a system-wise

crisis defined as a prolonged decline of the stock market:

SRISKi,t = Et (CSi,t+h|Rm,t+1:t+h < C) ,

= kEt (Di,t+h|Rm,t+1:t+h < C)− (1− k)Et (Wi,t+h|Rm,t+1:t+h < C)(2)

where Rm,t+1:t+h is the multiperiod arithmetic market returns of h−horizon from day t+1

to day t+h and (Rm,t+1:t+h < C) is the systemic event in which the market declines below

a threshold C. To compute the expectation, we assume the bank can not negotiate its

debt in the systemic event, i.e. Et (Di,t+h|Rm,t+1:t+h < C) = Di,t. Thus, Eq. (2) can be

rewritten as:

SRISKi,t = kDi,t − (1− k)Wi,t(1− LRMESi,t),

= Wi,t [kLV Gi,t + (1− k)LRMESi,t − 1] .(3)

where LV Gi,t is the quasi leverage ratio, (Di,t+Wi,t)/Wi,t and LRMESi,t denotes the long-

run marginal expected shortfall, which estimates the expectation of the bank multiperiod

4

returns conditional on the systemic event:

LRMESi,t = −Et(Ri,t+1:t+h|Rm,t+1:t+h < C) (4)

where Ri,t+1:t+h is the multiperiod arithmetic returns of bank i from day t+1 to day t+h.

Eq. (3) signifies that the systemic risk of a bank will increase when the bank has higher

leverage ratio, more sensitivity to the crisis in the stock market and has a bigger size.

2.2 Long-run Marginal Expected Shortfall

To estimate SRISK as in Eq. (3), it is necessary to estimate the time-series dependence

between the domestic stock market and bank equity returns. In this article, we follow

Brownlees and Engle (2017) and Engle et al. (2015) to rely on the standard DCC-GARCH

model of Engle (2002) to obtain estimators of LRMES.

Let ri,t = log(1 + Ri,t) and rm,t = log(1 + Rm,t) are the logarithmic returns of the

bank i and the market m at day t, where Ri,t and Rm,t are their corresponding arithmetic

returns. The return pair has conditional joint distribution D on the information set Ft−1

with zero mean and time-varying covariance as follows:[ri,t

rm,t

]∣∣∣∣Ft−1 ∼ D

(0,

[σ2i,t ρi,tσi,tσm,t

ρi,tσi,tσm,t σ2m,t

]). (5)

in which the dynamic of returns volatility is captured by the GJR-GARCH volatility model

of Glosten et al. (1993) as follows:

σi,t = ωi + αir2i,t−1 + γiri,t−1I(ri,t−1<0) + βiσ

2i,t−1, (6)

σm,t = ωm + αmr2m,t−1 + γmrm,t−1I(rm,t−1<0) + βmσ

2m,t−1, (7)

where I(.) is the indicator function. The time-varying correlation between the bank equity

returns and market index is estimated by the DCC correlation model of Engle (2002)

through the standardized innovations εi,t = ri,t/σi,t and εm,t = rm,t/σm,t:

Cor

(εi,t

εm,t

)=

[1 ρim,t

ρim,t 1

]= diag(Qi,t)

−1/2Qi,tdiag(Qi,t)−1/2, (8)

with Qi,t is the pseudo correlation matrix, with which the dynamics is specified as an

autoregressive process:

Qi,t = (1− αC,i − βC,i)Si + αC,i

[εi,t−1

εm,t−1

][εi,t−1

εm,t−1

]′+ βCiQi,t−1, (9)

where Si is the unconditional correlation matrix between the bank equity and market

5

index. To estimate LRMES, we adopt the simulation approach of Brownlees and Engle

(2017) to reflect the possibility of time-varying market risk of the bank equity. In

particular, we simulate S = 10, 000 random sample of h−period bank and market

arithmetic bank returns based on information available at day t and estimated parameters

of the GARCH-DCC models described above:5[Rs

i,t+1:t+h = exp(∑h

k=1 rsi,t+k

)− 1

Rsm,t+1:t+h = exp

(∑hk=1 r

sm,t+k

)− 1

]∣∣∣∣Ft−1 s = 1, .., S (10)

where rsi,t+k and rsm,t+k are the simulated bank and market logarithmic returns. The

LRMES of bank i for day t are then computed as follows:

LRMESi,t =

∑Ss=1R

si,t+1:t+hI(Rs

m,t+1:t+h<C)∑Ss=1 I(Rs

m,t+1:t+h<C)

(11)

where I(.) is the indicator function. We follow Engle (2018) and Engle et al. (2015)

to consider the systemic event as the worst 6-month of stock market when the market

capitalization lost 40% of the value, i.e h = 125 days and C = 40%. Similar to Engle

et al. (2015), we adjust the threshold level by its relative volatility with a World portfolio

to account for the difference in the volatility of the markets under consideration. In

particular, we set Cj = −0.4 × σj/σw, where σj and σw are the annualised volatility of

the domestic index in country j and the MSCI World portfolio. Finally, we plug the

LRMES measure to Eq. (3) together with the market capitalization, Wi,t, and the most

recent information the quarterly book debt, Di,t to estimate the systemic risk of bank i

at day t, SRISKi,t. A positive value of SRISK indicates that the bank would suffer an

undercapitalisation if a systemic risk event is triggered over the next 6 months.

3 EMPIRICAL STUDY

3.1 Data

Our empirical analysis comprises of banks listed on the stock markets of the ASEAN-6

countries. To estimate SRISK, we obtain the quarterly book value of equity and debt,

daily stock prices and market capitalization from S&P CapitalIQ database. We focus on

large banks with market capitalization greater than 200 million USD as of the end of

December 2018. The sample period spans from January 3, 2000 to December 31, 2018.

We also require the bank to start listing on the stock markets before January 1, 2010

to ensure relatively long historical data for the DCC-GARCH model estimation, which

results to an unbalanced panel data of 60 banks. We further drop 11 banks with which

5The simulation algorithm is described in details in Appendix A of Brownlees and Engle (2017)

6

the GARCH-DCC model can not converge due to the low level of liquidity. The final list

of 49 banks is reported in Table 1. Finally, we use the major stock index in each country

as the market index in the GARCH-DCC model estimation.6

Figure 1 presents the cumulative performance for the stock index and the aggregate

of bank returns in each country. All stock markets have experienced notable downturns

during the recent financial crisis 2007-2009 with the most severe drawdowns recorded in

Singapore and Vietnam. Banks are significant underperformed the aggregate market over

the sample period in most of the markets, except only for Malaysia where bank stocks

significantly outperform the index after the crisis. Between countries, Indonesia stock

market generates the highest returns, whereas Vietnam investors have suffered dramatic

falls during the crisis and only gradually regaining their losses until recently.

Table 2 confirms the cumulative performance. Only Vietnam has negative average

annualised returns over the sample period in both index and bank levels (-0.005 and -0.051,

respectively). Banks outperform the aggregate index in Malaysia (0.066 vs. 0.035) and

Singapore (0.022 vs. 0.014). Banks have higher volatility than the aggregate index in

all markets, except only for Philippines. Almost all series are characterised with negative

skewness and excess kurtosis, except only the bank stocks in Indonesia and the market

index of Philippines with positive skewness. In all countries, the dynamics of bank stocks

are highly correlated with the aggregate market.

3.2 SRISK computation

We estimate the GARCH-DCC model for each bank in the sample with the country index

in a recursive manner similar to Brownlees and Engle (2017). Since we compute LRMES

using simulation approach, the recursive approach ensures enough historical data to draw

sufficient number of scenarios for market crashes. In particular, we calculate SRISK for all

banks in the panel at the end of each month using all data available up to that date. For

each bank, the first estimation window consists of 5 years of available data to guarantee

the model convergence.

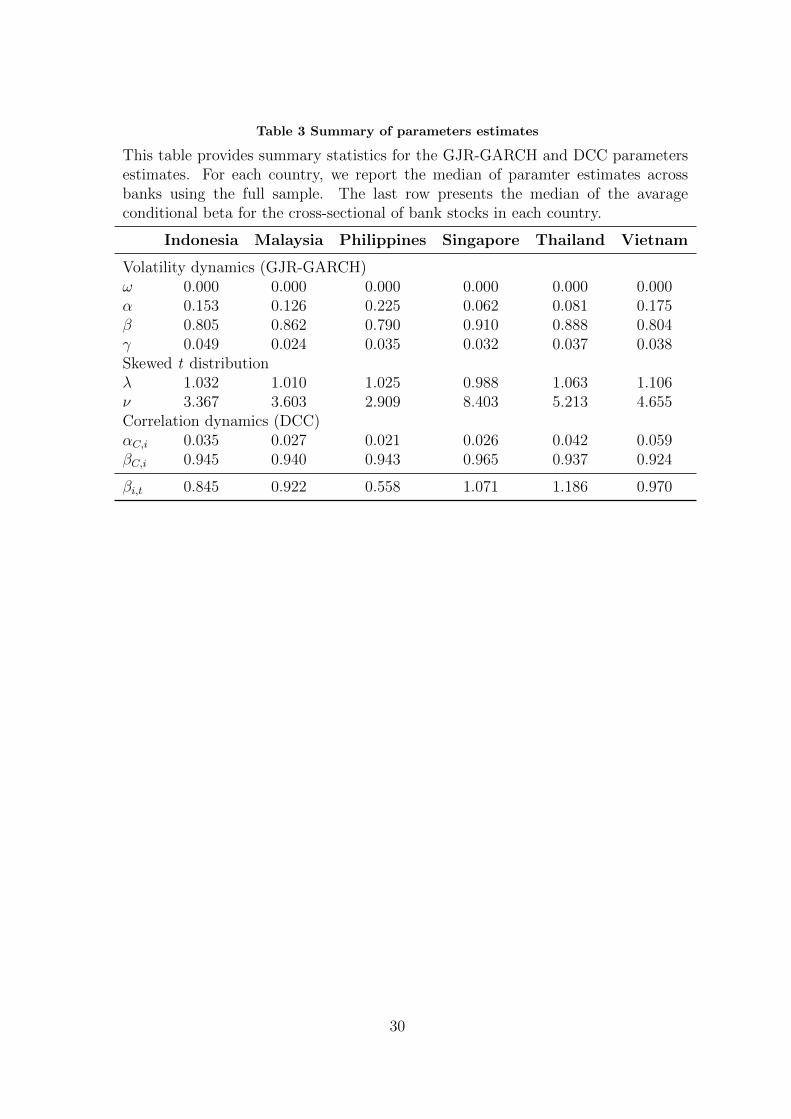

Table 3 reports the median of parameter estimates across banks for the GJR-GARCH

and DCC dynamics in each country using the full sample. The GJR-GARCH parameters

are similar across countries with highly persistent individual volatility dynamics. The

asymmetric coefficients (γ) are positive with a slightly higher sensitivity of the conditional

volatility to lagged negative returns in Indonesia. The skew parameters (λ) are higher than

unity in all but only Singapore, signaling positive conditional skewness in the univariate

conditional distribution. The degree of freedom (ν) ranges from 3.367 to 8.403, indicating

fat tails in the bank stock returns. The time-varying sensitivity of the bank stock returns

6For country with more than one stock index, we employ the index with greater marketcapitalization. We also repeat our analysis with the MSCI representative index for each countryas a robustness check. The result is relatively similar to the use of domestic index and availablefrom the authors upon request.

7

to the market index is highly persistent in all markets as the autoregressive coefficient βC,i

are ranging from 0.924 to 0.965. The median of the average conditional beta reported

the last row confirms this finding. Except for only Philippines (βi,t = 0.558), banks are

notably sensitive to the aggregate market dynamics with highest level being Thailand

(βi,t = 1.186).

3.3 SRISK dynamics and rankings

In this section, we analyse the dynamics and rankings of systemic risks between countries

and across banks within each market. Table 4 summarises the statistics of the main

ingredients in the SRISK measures as in (3), including the market capitalization, financial

leverage, LRMES and SRISK estimates. Panel A reports the median of the mean over time

of the systemic risk measures and its components across banks, while Panel B presents

the statistics as of December 2018. The listed banks in Singapore are the largest firms

on average, whereas Vietnamese banks have the smallest market capitalization. Figure

2 displays the evolution of the total market capitalization of the banking sector in all

countries over the sample period. While the bank stocks have plummeted to the lowest

level during the financial crisis in all countries, there is a significant upward trend in the

post-crisis period.

Two key ingredients in the SRISK measures as in Eq. (3) is the financial leverage and

LRMES estimates. The leverage of Vietnamese banks is highest on average, at 11.386,

whereas the lowest average leverage is at 6.670 in Philippines banking sector. The level of

leverage in the most recent period is higher than the average in all countries. Vietnamese

banks continue to have the highest financial leverage, at 15.950, while the leverages of

banks in Thailand and Malaysia are relatively moderate, at 8.862 and 8.819, respectively.

Figure 3 displays the dynamic of average financial leverage across banks in each country

over the full sample. Except only for Vietnam because of shorter historical data, the

financial leverage in the banking industry raised dramatically and peaked in mid-2009.

Since we define the financial leverage as the ratio of the quasi-market value of the bank

over its market value of equity, this observation is largely driven by severe drawdowns of

the market price of bank stocks. The dynamics of leverage post-crisis between countries

are not identical after the crisis. Leverage decreased substantially in all countries after the

crisis and remains at a relatively low level in Malaysia, Philippines and Thailand to the

current levels. In Indonesia, Singapore and Vietnam, in contrast, leverage gradually built

up after 2010 and reached the second highest point around 2017.

The LRMES estimates indicate higher average sensitivity to a shock in the aggregate

market in Thailand and Vietnam than other countries in the sample. A market decline of

relative 40% in the market index implies an average expected losses of 64.7% and 54.7%

in Thailand and Vietnam, respectively. Banks in Malaysia and Philippines have the least

sensitivity to a shock in the aggregate market. In particular, the expected losses of banks

8

in Malaysia to a 40% semiannual decline in the market index is only 22.9% on average and

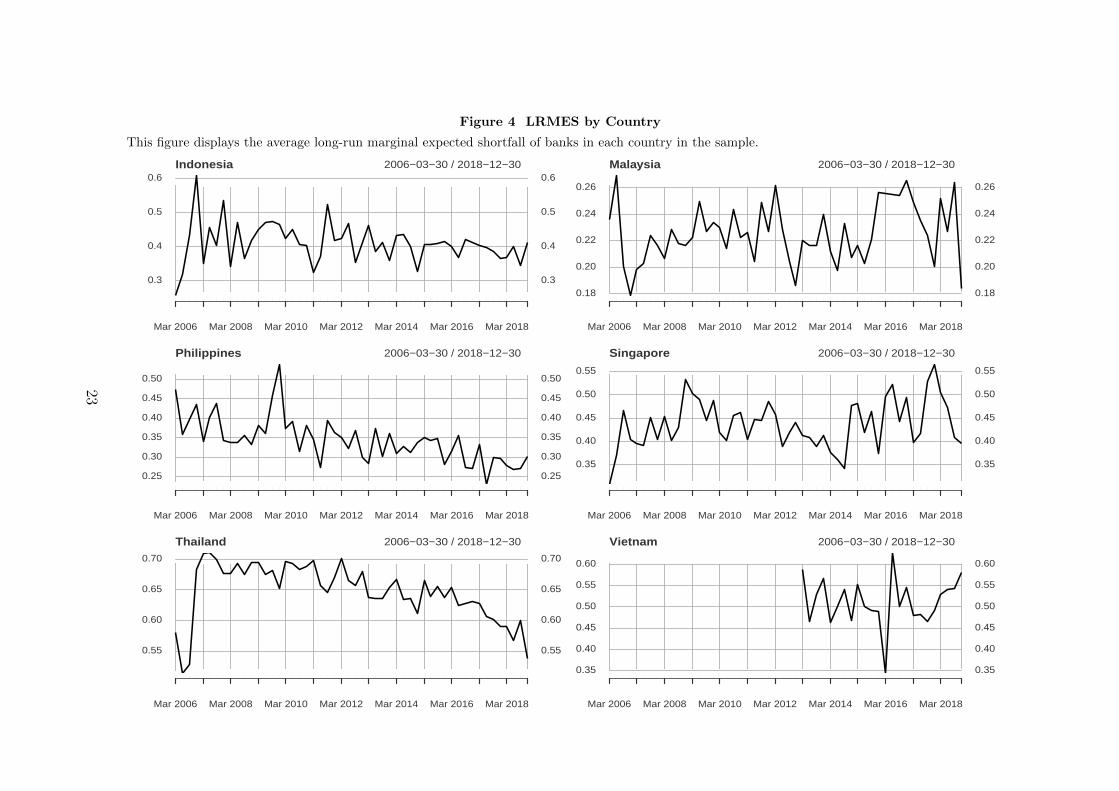

18.4% as of December 2018. Figure 4 shows significant variations in the average LRMES

of the banking sector in all countries. As shown in Table 4, the sensitivity of bank stocks

to the market index is highest in Thailand, reaching as high as an average expected loss

of 70% in 2007 before gradually decreasing to the current level of 53.7%. In contrast, the

LRMES of the banking sector in Malaysia ranges from only 17% to 27% over the sample

period. We also observe a significant increase in the sensitivity of banking stocks to the

market index in Vietnam in the most recent period. By the end of 2018, their LRMES is

even higher than that of Thailand, at 58.2%, implying notable risks to the banking sectors

in case of a shock hitting the equity market.

The SRISK measures for each country are reported in the last row of each panel. In

absolute term, Singapore has the largest systemic risk both on average over the sample

period and as of December 2018, mainly due to the relatively bigger size of their listed

banks compared to other countries in the sample. The combined effects of financial leverage

and LRMES to systemic risks can be clearly illustrated in the cases of Thailand and

Malaysia. Both countries have similar level of market capitalization and fragility (reflected

by the financial leverage). However, Thailand has the second largest systemic risk on

average, at 847.011 million $, whereas Malaysia would have suffered to the capital shortfall

of only 134.862 million $ in the case of aggregate market decline due to their relatively

low level of sensitivity to the equity market trends. Figure 5 shows the SRISK dynamics

in each country. The systemic risk of banking sectors increased significantly in the recent

financial crisis. However, except only for Philippines, the current level of expected capital

shortfalls are at par or even higher. In particular, the systemic risk of Vietnamese banks is

peaking at their highest level, at 6620.717 million $ as of December 2018. We notice that

while the exposure of banks to the aggregate markets during the crisis is mainly driven

by the high leverage, the current systemic risk is fuelled by a rapid growth of market

capitalization.

When SRISK is high, there is possibility of distress in the real economy since the

availability of credit is constrained. As a result, both the regulator and the risk manager

would be willing to strengthen the bank balance sheet to reduce their systemic risk

exposure. Engle and Ruan (2019) discuss several ways in which we can measure the

severity of systemic risk, depending on how the bank wants to reduce their exposure. One

possibility is that the bank can simply wait for the stock market upwards to increase their

market value, otherwise they appeal for a bailout. In this case, a systemic risk event

would lead to a loss to the government in order to rescue the stressed banks and a natural

measure of severity is SRISK/GDP , where GDP is the country gross domestic product

estimate. Another strategy is that the bank could sell existing assets to reduce their debt

and leverage. This scenario would lead to the so-called ’leverage spiral’, which results to

assets sales at price blow their fundamental values and a capital loss to the banks. The

severity of the sales depends on the level of regulatory capital ratio at which the bank

9

needs to maintain. Engle and Ruan (2019) shows that the corresponding measure if the

bank follows this strategy is SRISK/(k × TA), where TA is the total asset and k is the

capital requirement ratio. Finally, the bank could raise their capital by selling new stocks,

which in turn leads to a loss to the bank shareholders by lowering the values of existing

shares. Thus, the severity measure is simply SRISK/MV .

Figure 6 shows that Singapore has the highest level of SRISK/GDP , followed by

Vietnam. These numbers mean the amount of taxpayer money to bail out the banks

of Singapore and Vietnam are significant, at about 17% and 11% of GDP in another

financial crisis, respectively. Figures 7 and 8 indicate that Vietnamese banks would have

been suffered the most severity if there were a shock to the equity market, followed by

Thailand. The ratio of SRISK to total assets is approximately 5% in Vietnam, significantly

higher than that of other countries. Since we apply the capital ratio k = 8%, the

Vietnamese banks would need to sell 5/8 (62.5%) of their total asset to reduce the SRISK

to zero. Such large asset sales would likely to trigger a “fire sale externality”, when a

large volume of asset is sold to an insufficient number of buyers, further depress asset

prices to well-below its fundamental values. If Vietnamese banks choose to raise capital

by selling new shares to the equity market, they would need to sell approximately 45% of

the current market capitalization to reduce the capital shortfalls. Selling this volume of

shares when the market is undertaking a shock would dramatically dampen the market

prices. Furthermore, it would produce a signaling effect to the market participants that

the bank is in trouble and escalate the negative impact on stock price.

Table 5 shows the ranking of the most systematically risky banks at the end of

our estimation sample.7 In each country, we report the share of individual banks to

the aggregate country SRISK (SRISK %) and the two measures of SRISK severity,

namely SRISK/(k×TA) and SRISK/MV . In Indonesia, Malaysia and Philippines, the

aggregate SRISK is mainly driven by one particular risky institution in the sector. For

example, the Metropolitan Bank and Trust Company contributes to 93% of the capital

shortfall of banking sector in Philippines as of December 2018. In Singapore, Thailand and

Vietnam, the contribution to the aggregate country SRISKs is roughly shared between the

top 5 banks (top 3 in Singapore) in the sector. Except only for Malaysia and Philippines,

the most systemically risky bank is not necessary the bank that is affected the most when

they need to sell assets or new shares to eliminate SRISK. For example, Saigon-Hanoi

Commercial Joint Stock Bank contributes only 14.9% to the aggregate SRISK in Vietnam.

However, this bank would not be able to reduce their SRISK to zero, even after selling all

of their asset or three times of their current market capitalization worth of shares to the

equity market.

7We report the top 5 banks with highest systemic risks as of December 2018, except only forSingapore, where we only have 3 banks in our sample.

10

3.4 SRISK determinants in ASEAN countries

We now identify the factors that determine the severity of bank systemic risks on the

ASEAN level and in each individual country. In particular, we follow Bostandzic and

Weiß (2018) and Buch et al. (2019) to regress proxies for the severity in bank systemic

risks on several bank and country-specific variables.

SRISKsi,j,t = αi + γt + βiXi,t−1 + βcMj,t + εi,j,t (12)

where SRISKsi,j,t is measure of the severity of bank systemic risk, SRISK/MV and

SRISK/TA, respectively. Xi,t−1 are the banks-specific variables, which are lagged by

one period to mitigate the potential problem of endogeneity with the dependent variables.

Mj,t are the country-specific variables, which account for the effects of macroeconomic

conditions in each country on the systemic risks of the banking sector. To account

for potential unobserved heterogeneity between banks and over time due to common

macroeconomic developments, we estimate the panel regression with bank-fixed (αi) and

time-fixed (γt) effects. Standard errors are clustered at the bank-level, similar to Buch

et al. (2019). Our base model consists of all 49 banks in 6 ASEAN countries, while we

also explore the determinants of systemic risk severity in each country separately.

3.4.1 Main independent variables

For the bank-specific variables, we first consider the bank’s size, which equals to the natural

logarithm of the bank’s asset ((Size). Large banks have more complex and interconnected

business models (Laeven et al. (2016)), thus they tend to respond more aggressively than

those of smaller banks in a prolonged market decline. Moreover, the “too-big-to-fail”

hypothesis suggests that the managers of large banks would be more willing to take on

more risk in the presence of higher probability of government bailout in case of default

(Gandhi and Lustig (2015)). Consequently, we expect a positive relationship between

bank size and systemic risk, which implies that larger banks are more subject to systemic

risk.

The next potential driver of systemic risk is the difference in the bank’s business

models. To this end, we consider two proxies, which are the contribution of non-interest

income to the bank’s total income (Non − interest/Inc.) and the ratio of bank loans to

the total bank asset (Loan/TA). Lower contribution of non-interest income and a higher

percentage of loans in the bank’s total asset is indicatives of a more traditional banking

model. Previous studies have not yet reach a consensus on the effect of bank business

models to their systemic risk. One the one hand, DeYoung and Torna (2013) finds

that banks engage in risky non-traditional activities tend to take additional risks on the

traditional activities, which increase their probability of default. Likewise, Brunnermeier

et al. (2019) show that non-interest income positively relates to the bank’s tail risk and

11

interconnectedness risk. On the other hand, a higher share of non-interest income can

reduce the bank’s exposure to the systemic risk in the traditional market, thanks to a

more diversified portfolio. Furthermore, banks that supply higher credit to the market

are more exposed to the credit contagion (Jorion and Zhang, 2007). Buch et al. (2019)

recently explore that the relationship between non-interest income and bank’s systemic

risk is reversed between small and large banks. We further consider the quality of bank

loan’s portfolio as an indicator of the bank risk in their main business as proxied by the

ratio of loan loss provision to the net income (Loan prov./NI ). Allen et al. (2012) explore

that banks with lower quality in their loan portfolios are more exposed to the potential

spillover from interconnected banks. Therefore, we expect a positive impact of higher loan

loss provision to the bank’s systemic risks, similar to the recent findings of Buch et al.

(2019) and Brunnermeier et al. (2019).

We also explore the impacts of bank profitability, proxied by bank return on asset

(ROA), to the systemic risk, similar to Bostandzic and Weiß (2018) and Silva-Buston

(2019). The relationship between bank profitability to the bank systemic risk remains

inconclusive. While more profitable banks would be more resilient to the shocks in the

market, high profitability would also be a result of higher risk-taking behaviour and more

market power (DeJonghe, 2010). Finally, we employ the bank charter value, proxied by

the ratio of market price to book value of bank stock (Market− to− Book). We expect

this proxy to be negatively related to the bank’s systemic risk since banks with greater

charter value have incentives to limit their risk-taking and increase their diversification to

insure against potential losses (Bostandzic and Weiß, 2018).

In addition to the bank-specific characteristics, we also control for several country

variables to capture the potential effects of the financial development, banking sector

environment and macroeconomic condition on the bank’s systemic risk. For example,

banks operating in a more developed financial system may have a higher level of

interconnectedness, which could increase their systemic risks. In contrast, a more

developed financial markets would also provide better opportunities for banks to diversify

their portfolio and assess to liquidity and funding. To proxy for the financial development

and equity market condition, we consider the stock market capitalization to GDP

(Stockcap./GDP ) and the annualized volatility of the stock market (V ol(Stock)). For

the banking environment, we employ the market concentration in the banking sector

(Bankconcentration) and the banking system’s z-score (Bankz − score). Silva-Buston

(2019) argues that banking competition would increase the stability in banking system by

reducing the excess commonality between banks. Moreover, banks may be willing to take

excessive risks when they are facing a higher probability of insolvency (Laeven and Levine,

2009). Finally, we use the GDP growth (GDPgrowth) as a standard macroeconomic

control variable. All of these variables are sourced from World Bank’s World Development

Indicator and Global Financial Development Database.

12

3.4.2 Empirical results

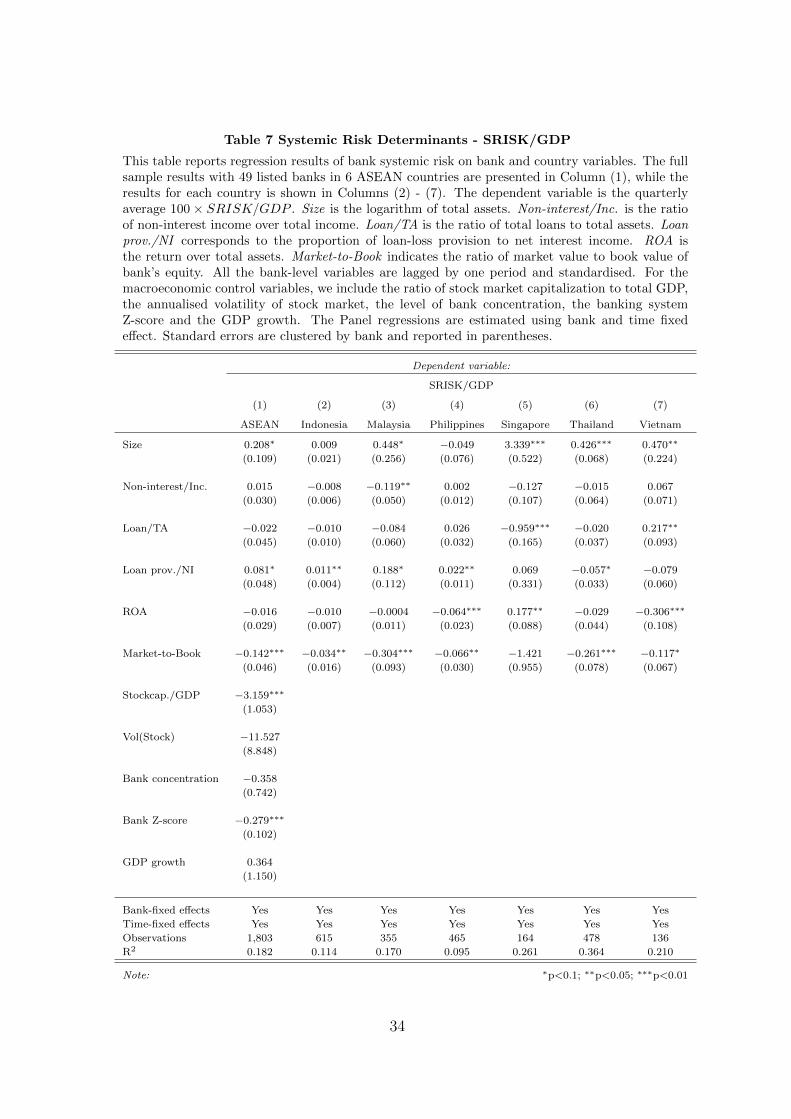

Table 6 reports the results of our panel regression for the determinants of bank’s SRISK.

The full sample results with 49 listed banks in 6 ASEAN countries are presented in Column

(1), while the results for each country are shown in Columns (2) - (7). Similar to Laeven

et al. (2016), we find that bank size has a positive and significant effect to the bank’s

systemic risk. This finding indicates that larger banks in ASEAN countries, on average,

have higher exposure to the financial distress since one standard deviation increase in the

bank size increases the SRISK by 0.125 billion $. For individual countries, however, we

do not find consistent effect as only the coefficients of bank size in Singapore, Thailand

and Vietnam are statistically significant.

Next, we find that the relationship between bank’s business models and systemic

risk varies considerably between countries. The coefficients of non-interest income on the

bank’s systemic risk is positive but not statistically significant in the full-sample regression.

The regression results in columns (2)-(7) reveal that the relationship is actually reversed

in Indonesia and Malaysia and signify that a higher share of income from non-traditional

activities would reduce the bank’s SRISK in these countries. The ratio of loans to total

assets enters the full-sample regression with negative sign. However, the coefficient is not

statistically significant and this effect varies considerably between countries. While banks

with a higher share of loans in their total assets have lower systemic risk in Singapore,

the corresponding effect is reversed in Vietnam. Not surprisingly, the level of loan loss

provision has negative impacts on the bank’s SRISK, even though the coefficient is not

statistically significant. The results in Columns (2) - (7) signify that this effect is mainly

driven by banks in Indonesian and Philippines.

We explore evidence that the profitability of ASEAN banks generally reduces the

bank’s systemic risk. This effect is statistically significant in Indonesia, Philippines

and Vietnam, implying that profitability helps to shield banks in these countries from

adverse effects in the period of financial distress. In Singapore, however, we find a

significant relationship between ROA and bank’s SRISK, similar to the results of Buch

et al. (2019). Since the sample of Singapore includes three banks of approximately

similar size, this observation might indicate that higher profitability in Singapore is a

sign of higher risk-taking activities as claimed in DeJonghe (2010). The coefficients of

the Market − to − Book variable are consistently negative and significant in the full

sample and across countries, similar to the finding of Lin et al. (2018) for Taiwanese

financial institutions. This finding indicates that indicate that banks with greater charter

value would reduce the incentives of their managers to take additional risks and be less

exposed to the financial instability. Finally, the systemic risk of banks is also related to the

financial market development and the condition of banking system. We find that countries

with higher development in the stock market, as proxied by the ratio of stock market

capitalisation to GDP, would economically and significantly reduce the bank’s systemic

13

risk. This evidence may be result of higher diversification opportunities in funding and

liquidity for both banks and the overall economy. Moreover, as a higher Z-score indicates

lower default risk, the bank’s systemic risk would be reduced when the overall default risk

of the banking sector decreases.

We also explore the determinants of the severity of the bank’s systemic risk in tables

7 and 8. In this article, we focus on the two measures of the severity of systemic risks,

namely SRISK/GDP and SRISK/TA, respectively. While raising capital by selling new

shares is feasible in developed markets, it is relatively more challenging in the case of

emerging stock markets due to higher market frictions. Moreover, this strategy depends

significantly on the regulatory requirements between countries. In contrast, the use of

GDP provides a natural comparison of banking systemic risks between countries under

consideration and selling assets to reduce required capital is the most common approach,

particularly during stressed periods (Engle and Ruan, 2019).8

The regression results exhibit similar findings to the main analysis. On average, the

economy faces higher losses when the systemic risk is originated from bigger banks and

banks with lower quality in the loan portfolio, whereas increasing the bank’s profitability

or market-to-book ratio reduces the loss of GDP for a potential bailout. Similarly, bank

size would significantly increase the severity of asset sales to reduce the bank’s systemic

risk, whereas higher ROA and bank’s charter value would produce the reversed effect.

Again, we do not find consistent relations between the bank’s specific variables to the

severity of systemic risk across ASEAN countries. For example, while banks in Singapore

with higher shares of loans to total assets significantly contribute to the lower severity

of systemic risk, the opposite relationship is found in the Vietnamese banks. Moreover,

a higher level of loan loss provisions in Thailand and Vietnam leads to the lower loss to

GDP, although the coefficient is only negatively significant in Thailand.

4 DISCUSSIONS

Our analysis provides relevant information on the systemic risk for the supervisors in

the ASEAN banking sectors. First, we explore significant dynamics in the systemic

risk in banking sector of the six ASEAN countries. In particular, we find that, except

for Philippines, the level of systemic risk is currently higher than that at the global

financial crisis during 2007-2008. This trend is mainly driven by the combined effect of

increasing level of bank’s market values and sensitivity to the market index as measured

by the LRMES. Higher capital shortfalls of financial institutions would lead to adverse

fundamental shocks in the economy (Giglio et al., 2016), provides early warning signals of

distress in real activity (Brownlees and Engle, 2017) and increase the probability of future

8The panel regression for SRISK/MV yields similar results and is available from the authorsupon request.

14

crisis (Engle and Ruan, 2019). Thus, this finding would provide warnings to the regulators

to strengthen their macroprudential policy on the banking sector.

Second, the structure of the systemic risk is considerably different between the six

countries. In Indonesia, Malaysia and Philippines, the aggregate systemic risk is mainly

driven by one particular bank, while the contributions are approximately similar between

top risky banks in the remaining countries. Most importantly, we note that the rankings

of banks regarding the severity of systemic risk as scaled by their total asset and market

capitalisation are generally different to the level of SRISK. This observation indicates that

the supervisors should not only pay higher attention to the banks with the highest SRISK,

but also the banks which would likely be suffered the most losses during financial distress.

Third, we observe strong evidence that bank size is positively related to the systemic

risk. This is in line previous studies (see, e.g., Laeven et al., 2016; Buch et al., 2019; Silva-

Buston, 2019) and supports the too-big-to-fail paradigm. Thus, this finding advocates

the incentive to impose a capital surcharge on large banks as documented in the Basel

III regulations. We also find that bank’s systemic risks are generally associated with

banks that have more traditional business models, lower quality in their loan portfolios,

less profitable and with lower market-to-book values. However, except for the market-to-

book ratio, these effects are not consistent between ASEAN countries. This observation

reveals the heterogeneity between ASEAN countries and their banking sectors due to

their fundamental differences in economic development, institutional environment and

regulatory framework (Ha et al., 2019; Wu, 2019). Although the region has been pushing

to higher financial integration in recent years, our empirical results imply that, at least

to the systemic risk, the banking supervisors would still need to account for idiosyncratic

characteristics of their banking sector in designing relevant regulatory frameworks.

5 CONCLUSION

We provide the first study on the systemic risk of the banking sectors in ASEAN-6

countries. It is important for the regional regulators since the bank-based financial

structures of these countries are associated with higher systemic risk and potentially more

severe distress to the real economy. In particular, we employ the popular SRISK measure

of Brownlees and Engle (2017) to investigate the dynamics, rankings and determinants

of systemic risk for 49 listed banks in the region. The main advantage of SRISK is

the use of both market data and balance sheet information to construct a market-based

measurement. This approach allows SRISK to provide a timely estimate of systemic risk

and explicitly capture the effect of size and leverage on the expected capital shortfall of a

financial firm, given the market is in long-run distress.

Our empirical evidence provides several policy implications to the regional policy-

makers. The increasing trend of systemic risk in the region calls for advancements in

the macroprudential policy to maintain the stability of the regional financial system. In

15

particular, we find evidence supporting the too-big-to-fail paradigm, thus, we advocate

the use of a capital surcharge on the systemically important financial institutions as

documented in the Basel III regulations. However, we note that the local banking

supervisors should account for idiosyncratic characteristics of their banking sector in

designing the relevant macroprudential policy given the fundamental difference in economic

development and institutional environment between the ASEAN-6 countries.

16

References

Acharya, V. V., Engle, R. F., and Richardson, M. (2012). Capital Shortfall: A New

Approach to Ranking and Regulating Systemic Risks. American Economic Review,

102(3):59–64.

Acharya, V. V., Pedersen, L. H., Philippon, T., and Richardson, M. (2017). Measuring

systemic risk. Review of Financial Studies, 30(1):2–47.

Acharya, V. V. and Thakor, A. V. (2016). The dark side of liquidity creation: Leverage

and systemic risk. Journal of Financial Intermediation, 28:4–21.

Adrian, T. and Brunnermeier, M. K. (2016). CoVaR. American Economic Review,

106(7):1705–1741.

Allen, F., Babus, A., and Carletti, E. (2012). Asset commonality, debt maturity and

systemic risk. Journal of Financial Economics, 104(3):519–534.

Bats, J. V. and Houben, A. C. (2020). Bank-based versus market-based financ-

ing:Implications for systemic risk. Journal of Banking & Finance, 114:105776.

Benoit, S., Colliard, J. E., Hurlin, C., and Perignon, C. (2017). Where the risks lie: A

survey on systemic risk. Review of Finance, 21(1):109–152.

Bisias, D., Flood, M., Lo, A. W., and Valavanis, S. (2012). A Survey of Systemic Risk

Analytics. Annual Review of Financial Economics, 4(1):255–296.

Bonaccolto, G., Caporin, M., and Paterlini, S. (2019). Decomposing and backtesting a

flexible specification for CoVaR. Journal of Banking & Finance, 108:105659.

Bostandzic, D. and Weiß, G. N. (2018). Why do some banks contribute more to global

systemic risk? Journal of Financial Intermediation, 35(March):17–40.

Brownlees, C., Chabot, B., Ghysels, E., and Kurz, C. (2020). Back to the Future:

Backtesting Systemic Risk Measures during Historical Bank Runs and the Great

Depression. Journal of Banking and Finance, page 105736.

Brownlees, C. and Engle, R. F. (2017). SRISK: A conditional capital shortfall measure of

systemic risk. Review of Financial Studies, 30(1):48–79.

Brunnermeier, M. K., Dong, G., and Palia, D. (2019). Banks ’ Non-Interest Income and

Systemic Risk. (January).

Buch, C. M., Krause, T., and Tonzer, L. (2019). Drivers of systemic risk: Do national and

European perspectives differ? Journal of International Money and Finance, 91:160–176.

17

Colletaz, G., Levieuge, G., and Popescu, A. (2018). Monetary policy and long-run systemic

risk-taking. Journal of Economic Dynamics and Control, 86:165–184.

DeJonghe, O. (2010). Back to the basics in banking? A micro-analysis of banking system

stability. Journal of Financial Intermediation, 19(3):387–417.

DeYoung, R. and Torna, G. (2013). Nontraditional banking activities and bank failures

during the financial crisis. Journal of Financial Intermediation, 22(3):397–421.

Engle, R. F. (2002). Dynamic Conditional Correlation: A Simple Class of Multivariate

Generalized Autoregressive Conditional Heteroskedasticity Models. Journal of Business

and Economic Statistics, 20(3):339–350.

Engle, R. F. (2018). Systemic Risk 10 Years Later. Annual Review of Financial Economics,

10(1):125–152.

Engle, R. F., Jondeau, E., and Rockinger, M. (2015). Systemic risk in Europe. Review of

Finance, 19(1):145–190.

Engle, R. F. and Ruan, T. (2019). How Much SRISK Is Too Much?

Gandhi, P. and Lustig, H. (2015). Size anomalies in US bank stock returns. Journal of

Finance, 70(2):733–768.

Giglio, S., Kelly, B., and Pruitt, S. (2016). Systemic risk and the macroeconomy: An

empirical evaluation. Journal of Financial Economics, 119(3):457–471.

Girardi, G. and Tolga Ergun, A. (2013). Systemic risk measurement: Multivariate GARCH

estimation of CoVaR. Journal of Banking and Finance, 37(8):3169–3180.

Glosten, L. R., Jagannathan, R., and Runkle, D. E. (1993). On the relation between the

expected value and the volatility of the nominal excess return on stocks. Journal of

Finance, 48(5):1779–1801.

Ha, D., Gillet, P., Le, P., and Vo, D.-T. (2019). Banking integration in ASEAN-6: An

empirical investigation. Economic Modelling, (September).

Jorion, P. and Zhang, G. (2007). Good and bad credit contagion: Evidence from credit

default swaps. Journal of Financial Economics, 84(3):860–883.

Laeven, L. and Levine, R. (2009). Bank governance, regulation and risk taking. Journal

of Financial Economics, 93(2):259–275.

Laeven, L., Ratnovski, L., and Tong, H. (2016). Bank size, capital, and systemic risk:

Some international evidence. Journal of Banking and Finance, 69:S25–S34.

18

Lin, E. M., Sun, E. W., and Yu, M. T. (2018). Systemic risk, financial markets, and

performance of financial institutions. Annals of Operations Research, 262(2):579–603.

Meuleman, E. and Vander Vennet, R. (2020). Macroprudential policy and bank systemic

risk. Journal of Financial Stability, 47:100724.

Reinhart, C. M. and Rogoff, K. S. (2011). From financial crash to debt crisis. American

Economic Review, 101(5):1676–1706.

Schularick, M. and Taylor, A. M. (2012). Credit booms gone bust: Monetary

policy, leverage cycles, and financial crises, 1870-2008. American Economic Review,

102(2):1029–1061.

Silva-Buston, C. (2019). Systemic risk and competition revisited. Journal of Banking and

Finance, 101:188–205.

Varotto, S. and Zhao, L. (2018). Systemic risk and bank size. Journal of International

Money and Finance, 82:45–70.

Wu, F. (2019). Stock market integration in East and Southeast Asia: The role of global

factors. International Review of Financial Analysis.

19

Figure 1 Cumulative Returns by Country

This figure displays the cumulative performances of the stock index (solid line) and the aggregate bank returns (dashed line) for each country in thesample.

Jan 02 2001 Jan 03 2005 Jan 01 2009 Jan 01 2013 Jan 02 2017

Indonesia 2001−01−02 / 2019−04−09

5

10

15

5

10

15

Jan 03 2000 Jan 01 2004 Jan 01 2008 Jan 02 2012 Jan 01 2016

Malaysia 2000−01−03 / 2019−04−09

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan 03 2000 Jan 01 2004 Jan 01 2008 Jan 02 2012 Jan 01 2016

Philippines 2000−01−03 / 2019−04−10

1

2

3

4

1

2

3

4

Jan 03 2000 Jan 01 2004 Jan 01 2008 Jan 02 2012 Jan 01 2016

Singapore 2000−01−03 / 2019−04−09

0.6

0.8

1.0

1.2

1.4

1.6

0.6

0.8

1.0

1.2

1.4

1.6

Jan 03 2000 Jan 01 2004 Jan 01 2008 Jan 02 2012 Jan 01 2016

Thailand 2000−01−03 / 2019−04−10

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Apr 03 2007 Jan 01 2010 Jan 01 2013 Jan 01 2016 Jan 01 2019

Vietnam 2007−04−03 / 2019−04−09

0.4

0.6

0.8

1.0

0.4

0.6

0.8

1.0

20

Figure 2 Market Capitalization

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Indonesia 2006−03−30 / 2018−12−30

20

40

60

80

100

120

20

40

60

80

100

120

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Malaysia 2006−03−30 / 2018−12−30

30

40

50

60

70

80

90

30

40

50

60

70

80

90

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Philippines 2006−03−30 / 2018−12−30

10

15

20

25

30

35

10

15

20

25

30

35

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Singapore 2006−03−30 / 2018−12−30

40

60

80

100

120

40

60

80

100

120

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Thailand 2006−03−30 / 2018−12−30

20

30

40

50

60

70

80

20

30

40

50

60

70

80

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Vietnam 2006−03−30 / 2018−12−30

10

12

14

16

18

20

10

12

14

16

18

20

21

Figure 3 Financial Leverage by Country

This figure displays the average financial leverage of banks in each country in the sample.

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Indonesia 2006−03−30 / 2018−12−30

6

8

10

12

6

8

10

12

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Malaysia 2006−03−30 / 2018−12−30

8

10

12

14

16

8

10

12

14

16

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Philippines 2006−03−30 / 2018−12−30

6

8

10

12

14

6

8

10

12

14

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Singapore 2006−03−30 / 2018−12−30

8

10

12

8

10

12

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Thailand 2006−03−30 / 2018−12−30

8

10

12

14

16

18

20

8

10

12

14

16

18

20

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Vietnam 2006−03−30 / 2018−12−30

10

12

14

16

18

10

12

14

16

18

22

Figure 4 LRMES by Country

This figure displays the average long-run marginal expected shortfall of banks in each country in the sample.

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Indonesia 2006−03−30 / 2018−12−30

0.3

0.4

0.5

0.6

0.3

0.4

0.5

0.6

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Malaysia 2006−03−30 / 2018−12−30

0.18

0.20

0.22

0.24

0.26

0.18

0.20

0.22

0.24

0.26

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Philippines 2006−03−30 / 2018−12−30

0.25

0.30

0.35

0.40

0.45

0.50

0.25

0.30

0.35

0.40

0.45

0.50

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Singapore 2006−03−30 / 2018−12−30

0.35

0.40

0.45

0.50

0.55

0.35

0.40

0.45

0.50

0.55

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Thailand 2006−03−30 / 2018−12−30

0.55

0.60

0.65

0.70

0.55

0.60

0.65

0.70

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Vietnam 2006−03−30 / 2018−12−30

0.35

0.40

0.45

0.50

0.55

0.60

0.35

0.40

0.45

0.50

0.55

0.60

23

Figure 5 Systemic Risk by Country (billion $)

This figure displays the aggregate SRISK in billion $ for each country in the sample

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Indonesia 2006−03−30 / 2018−12−30

1

2

3

4

1

2

3

4

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Malaysia 2006−03−30 / 2018−12−30

1

2

3

4

1

2

3

4

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Philippines 2006−03−30 / 2018−12−30

0.5

1.0

1.5

2.0

0.5

1.0

1.5

2.0

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Singapore 2006−03−30 / 2018−12−30

5

10

15

20

25

5

10

15

20

25

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Thailand 2006−03−30 / 2018−12−30

4

6

8

10

12

4

6

8

10

12

Mar 2006 Mar 2008 Mar 2010 Mar 2012 Mar 2014 Mar 2016 Mar 2018

Vietnam 2006−03−30 / 2018−12−30

2

3

4

5

6

2

3

4

5

6

24

Figure 6 SRISK/GDP rankings

0.00 0.05 0.10 0.15

Indonesia

Philippines

Malaysia

Thailand

Vietnam

Singapore

Cou

ntry

SRISK / GDP

25

Figure 7 SRISK/TA rankings

0.00 0.01 0.02 0.03 0.04

Malaysia

Philippines

Indonesia

Singapore

Thailand

Vietnam

Cou

ntry

SRISK / Total Assets

26

Figure 8 SRISK/MV rankings

0.0 0.1 0.2 0.3 0.4

Indonesia

Malaysia

Philippines

Singapore

Thailand

Vietnam

Cou

ntry

SRISK / Market Cap

27

Table 1 List of tickers and banks grouped by country

This table reports the list of tickers and name of banks grouped by country used in the SRISK analysis

Tickers Indonesia Tickers Philippines

BNBA Bank Bumi Arta BPI Bank of the Philippine IslandsPNBN Bank Pan Indonesia BDO BDO Unibank, Inc.INPC Bank Artha Graha Internasional CHIB China Banking CorporationBBKP Bank Bukopin MBT Metropolitan Bank & Trust CompanyBACA Bank Capital Indonesia PBC Philippine Bank of CommunicationsBDMN Bank Danamon Indonesia RCB Rizal Commercial Banking CorporationBBNI Bank Negara Indonesia (Persero) SECB Security Bank CorporationBNLI Bank Permata UBP Union Bank of the PhilippinesBBTN Bank Tabungan Negara (Persero) PNB Philippine National BankBVIC Bank Victoria InternationalBBRI Bank Rakyat Indonesia (Persero) Tickers Thailand

BMRI Bank Mandiri (Persero) TMB TMB BankBBCA Bank Central Asia TISCO TISCO Financial GroupBNGA Bank CIMB Niaga SCB The Siam Commercial BankBNII Bank Maybank Indonesia TCAP Thanachart Capital

KTB Krung Thai BankTickers Malaysia KKP Kiatnakin Bank

AMBANK AMMB Holding Berhad KBANK KasikornbankCIMB CIMB Group Holdings Berhad BBL Bangkok BankMAYBANK Malayan Banking Berhad BAY Bank of AyudhyaPBBANK Public Bank BerhadHLBANK Hong Leong Bank Tickers Vietnam

BIMB BIMB Holdings Berhad ACB Asia Commercial Joint Stock BankHLFG Hong Leong Financial Group CTG VietinBank

SHB Saigon-Hanoi Commercial Joint Stock BankTickers Singapore STB Saigon Thuong Tin Commercial Joint Stock Bank

D05 DBS Group Holdings Ltd EIB EximBankO39 Oversea-Chinese Banking Corporation VCB VietcombankU11 United Overseas Bank Limited

28

Table 2 Summary statistics of bank stock returns and country index returns

This table provides summary statistics of the bank stock returns and country index returns over the sample period.Column (1) presents the average statistics for the bank stock returns, whereas column (2) presents statistics for thecountry index returns. For each catergory, we report the average annualized return, annualized volatility, skewness,kurtosis and the average correlation between the aggregate index and bank stocks.

Indonesia Malaysia Philippines Singapore Thailand Vietnam(1) (2) (1) (2) (1) (2) (1) (2) (1) (2) (1) (2)

Ann. Return 0.084 0.145 0.066 0.035 0.028 0.066 0.022 0.014 0.036 0.062 -0.051 -0.005Ann. Volatility 0.285 0.207 0.148 0.127 0.176 0.202 0.219 0.179 0.281 0.204 0.294 0.223Skewness 0.116 -0.687 -0.244 -0.847 0.158 0.276 -0.050 -0.268 -0.243 -0.753 -0.039 -0.284Kurtosis 12.023 10.918 10.795 14.354 16.727 18.873 8.528 8.916 12.740 14.322 5.891 4.768Correlation 0.641 0.811 0.706 0.886 0.880 0.810

29

Table 3 Summary of parameters estimates

This table provides summary statistics for the GJR-GARCH and DCC parametersestimates. For each country, we report the median of paramter estimates acrossbanks using the full sample. The last row presents the median of the avarageconditional beta for the cross-sectional of bank stocks in each country.

Indonesia Malaysia Philippines Singapore Thailand Vietnam

Volatility dynamics (GJR-GARCH)ω 0.000 0.000 0.000 0.000 0.000 0.000α 0.153 0.126 0.225 0.062 0.081 0.175β 0.805 0.862 0.790 0.910 0.888 0.804γ 0.049 0.024 0.035 0.032 0.037 0.038Skewed t distributionλ 1.032 1.010 1.025 0.988 1.063 1.106ν 3.367 3.603 2.909 8.403 5.213 4.655Correlation dynamics (DCC)αC,i 0.035 0.027 0.021 0.026 0.042 0.059βC,i 0.945 0.940 0.943 0.965 0.937 0.924

βi,t 0.845 0.922 0.558 1.071 1.186 0.970

30

Table 4 Systemic Risk and its components

This table reports the median of the mean over time of the systemic risk measure and its componentsacross firms in each country. In each panel, I report the market capitalization, leverage ratio (definedas Li,t = Ai,t/Wi,t), the LRMES and the SRISK measure. Panel A presents the results computed overthe entire sample, whereas Panel B shows the statistics as of December 30, 2018. Market capitalizationand SRISK are reported in million USD.

Indonesia Malaysia Philippines Singapore Thailand Vietnam

Panel A: Entire sample

Market capitalization 1672.59 5363.60 1287.14 23276.76 5359.65 983.34934Leverage 8.480 7.538 6.670 8.786 7.667 11.386LRMES 0.408 0.229 0.326 0.430 0.647 0.547SRISK 72.801 134.862 59.590 3277.547 847.011 489.753

Panel B: As of December 2018

Market capitalization 8267.33 11668.26 3608.02 36229.22 7240.34 2505.35Leverage 10.733 8.819 9.454 9.529 8.682 15.950LRMES 0.412 0.184 0.302 0.421 0.537 0.582SRISK 3410.512 2644.923 1348.345 15761.215 9533.334 6620.717

31

Table 5 Systemic Risk rankings by country

This table reports the ranking of Top 5 banks with the highest systemic risk ineach country as of December 30, 2018. For each country, we report the SRISKcontribution in percentage (%) and the two measures of SRISK severity, namelySRISK/(TA*k) and SRISK/MV.

Rank SRISK (%) SRISK/TA SRISK/MV

Indonesia

1 BBNI 0.470 BVIC 0.621 BVIC 1.5312 BBTN 0.155 BBKP 0.619 BBKP 0.8753 BNGA 0.096 BBNI 0.548 INPC 0.8444 BBKP 0.091 BBTN 0.509 BBTN 0.4745 BNLI 0.059 INPC 0.459 BNBA 0.306

Malaysia

1 CIMB 0.596 CIMB 0.267 CIMB 0.2592 MAYBANK 0.263 AMBANK 0.200 AMBANK 0.1593 AMBANK 0.119 MAYBANK 0.078 MAYBANK 0.0554 HLFG 0.022 HLFG 0.022 HLFG 0.0235 PBBANK 0 PBBANK 0.000 PBBANK 0.000

Philippines

1 MBT 0.930 MBT 0.210 MBT 0.1372 PNB 0.070 PNB 0.040 PNB 0.0353 UBP 0.000 UBP 0.000 UBP 0.0004 SECB 0.000 SECB 0.000 SECB 0.0005 RCB 0.000 RCB 0.000 RCB 0.000

Singapore

1 D05 0.399 O39 0.398 O39 0.3502 O39 0.388 D05 0.348 D05 0.3053 U11 0.213 U11 0.263 U11 0.214

Thailand

1 KTB 0.256 TCAP 0.621 TCAP 0.9372 BBL 0.215 TMB 0.512 KTB 0.4133 BAY 0.167 KTB 0.475 TMB 0.3554 KBANK 0.147 BAY 0.442 BBL 0.2815 TCAP 0.120 BBL 0.364 BAY 0.226

Vietnam

1 CTG 0.305 SHB 0.859 SHB 3.5302 VCB 0.244 STB 0.755 STB 1.1773 STB 0.180 ACB 0.551 CTG 0.6054 SHB 0.149 CTG 0.447 ACB 0.5935 ACB 0.093 VCB 0.431 EIB 0.291

32

Table 6 Systemic Risk Determinants - SRISK

This table reports regression results of bank systemic risk on bank and country variables. The fullsample results with 49 listed banks in 6 ASEAN countries are presented in Column (1), while theresults for each country is shown in Columns (2) - (7). The dependent variable is the quarterlyaverage SRISK in billion $. Size is the logarithm of bank total assets. Non-interest/Inc. isthe ratio of non-interest income over total income. Loan/TA is the ratio of total loans to totalassets. Loan prov./NI corresponds to the proportion of loan-loss provision to net interest income.ROA is the return over total assets. Market-to-Book indicates the ratio of market value to bookvalue of bank’s equity. All the bank-level variables are lagged by one period and standardised.For the macroeconomic control variables, we include the ratio of stock market capitalization tototal GDP, the annualised volatility of stock market, the level of bank concentration, the bankingsystem Z-score and the GDP growth. The Panel regressions are estimated using bank and timefixed effect. Standard errors are clustered by bank and reported in parentheses.

Dependent variable:

SRISK

(1) (2) (3) (4) (5) (6) (7)

ASEAN Indonesia Malaysia Philippines Singapore Thailand Vietnam

Size 0.125∗∗ 0.021 0.329 0.007 1.083∗ 0.272∗∗∗ 0.292∗∗

(0.057) (0.037) (0.203) (0.025) (0.635) (0.065) (0.146)

Non-interest/Inc. 0.053 −0.016∗∗ −0.079∗∗ −0.004 −0.050 −0.011 0.033

(0.035) (0.007) (0.037) (0.005) (0.094) (0.055) (0.038)

Loan/TA −0.036 −0.013 −0.075 −0.003 −0.657∗∗∗ −0.056 0.157∗∗

(0.036) (0.011) (0.049) (0.013) (0.079) (0.043) (0.066)

Loan prov./Inc 0.034 0.022∗∗∗ 0.142 0.011∗∗ 0.128 −0.036 −0.047

(0.028) (0.008) (0.088) (0.005) (0.219) (0.034) (0.031)

ROA −0.027 −0.012∗∗ 0.001 −0.014∗ 0.224∗∗ −0.015 −0.199∗∗∗

(0.020) (0.006) (0.007) (0.008) (0.098) (0.044) (0.060)

Market-to-Book −0.110∗∗∗ −0.049∗∗∗ −0.198∗∗∗ −0.026∗∗∗ −0.670 −0.307∗∗∗ −0.064∗

(0.038) (0.016) (0.068) (0.009) (0.729) (0.045) (0.038)

Stock cap./GDP −2.517∗∗∗

(0.920)

Vol(Stock) −7.030

(5.730)

Bank concentration −0.083

(0.584)

Bank Z-score −0.252∗∗∗

(0.097)

GDP growth 1.096

(0.742)

Bank-fixed effects Yes Yes Yes Yes Yes Yes Yes

Time-fixed effects Yes Yes Yes Yes Yes Yes Yes

Observations 1,803 615 355 465 164 478 136

R2 0.235 0.115 0.169 0.061 0.157 0.396 0.269

Note: ∗p<0.1; ∗∗p<0.05; ∗∗∗p<0.01

33

Table 7 Systemic Risk Determinants - SRISK/GDP

This table reports regression results of bank systemic risk on bank and country variables. The fullsample results with 49 listed banks in 6 ASEAN countries are presented in Column (1), while theresults for each country is shown in Columns (2) - (7). The dependent variable is the quarterlyaverage 100× SRISK/GDP . Size is the logarithm of total assets. Non-interest/Inc. is the ratioof non-interest income over total income. Loan/TA is the ratio of total loans to total assets. Loanprov./NI corresponds to the proportion of loan-loss provision to net interest income. ROA isthe return over total assets. Market-to-Book indicates the ratio of market value to book value ofbank’s equity. All the bank-level variables are lagged by one period and standardised. For themacroeconomic control variables, we include the ratio of stock market capitalization to total GDP,the annualised volatility of stock market, the level of bank concentration, the banking systemZ-score and the GDP growth. The Panel regressions are estimated using bank and time fixedeffect. Standard errors are clustered by bank and reported in parentheses.

Dependent variable:

SRISK/GDP

(1) (2) (3) (4) (5) (6) (7)

ASEAN Indonesia Malaysia Philippines Singapore Thailand Vietnam

Size 0.208∗ 0.009 0.448∗ −0.049 3.339∗∗∗ 0.426∗∗∗ 0.470∗∗

(0.109) (0.021) (0.256) (0.076) (0.522) (0.068) (0.224)

Non-interest/Inc. 0.015 −0.008 −0.119∗∗ 0.002 −0.127 −0.015 0.067

(0.030) (0.006) (0.050) (0.012) (0.107) (0.064) (0.071)

Loan/TA −0.022 −0.010 −0.084 0.026 −0.959∗∗∗ −0.020 0.217∗∗

(0.045) (0.010) (0.060) (0.032) (0.165) (0.037) (0.093)

Loan prov./NI 0.081∗ 0.011∗∗ 0.188∗ 0.022∗∗ 0.069 −0.057∗ −0.079

(0.048) (0.004) (0.112) (0.011) (0.331) (0.033) (0.060)

ROA −0.016 −0.010 −0.0004 −0.064∗∗∗ 0.177∗∗ −0.029 −0.306∗∗∗

(0.029) (0.007) (0.011) (0.023) (0.088) (0.044) (0.108)

Market-to-Book −0.142∗∗∗ −0.034∗∗ −0.304∗∗∗ −0.066∗∗ −1.421 −0.261∗∗∗ −0.117∗

(0.046) (0.016) (0.093) (0.030) (0.955) (0.078) (0.067)

Stockcap./GDP −3.159∗∗∗

(1.053)

Vol(Stock) −11.527

(8.848)

Bank concentration −0.358

(0.742)

Bank Z-score −0.279∗∗∗

(0.102)

GDP growth 0.364

(1.150)

Bank-fixed effects Yes Yes Yes Yes Yes Yes Yes

Time-fixed effects Yes Yes Yes Yes Yes Yes Yes

Observations 1,803 615 355 465 164 478 136

R2 0.182 0.114 0.170 0.095 0.261 0.364 0.210

Note: ∗p<0.1; ∗∗p<0.05; ∗∗∗p<0.01

34

Table 8 Systemic Risk Determinants - SRISK/(k × TAThis table reports regression results of bank systemic risk on bank and country variables. The fullsample results with 49 listed banks in 6 ASEAN countries are presented in Column (1), while theresults for each country is shown in Columns (2) - (7). The dependent variable is the quarterlyaverage SRISK/TA. Size is the logarithm of total assets. Non-interest/Inc. is the ratio ofnon-interest income over total income. Loan/TA is the ratio of total loans to total assets. Loanprov./NI corresponds to the proportion of loan-loss provision to net interest income. ROA isthe return over total assets. Market-to-Book indicates the ratio of market value to book value ofbank’s equity. All the bank-level variables are lagged by one period and standardised. For themacroeconomic control variables, we include the ratio of stock market capitalization to total GDP,the annualised volatility of stock market, the level of bank concentration, the banking systemZ-score and the GDP growth. The Panel regressions are estimated using bank and time fixedeffect. Standard errors are clustered by bank and reported in parentheses.

Dependent variable:

SRISK/(k × TA

(1) (2) (3) (4) (5) (6) (7)

ASEAN Indonesia Malaysia Philippines Singapore Thailand Vietnam

Size 0.050∗∗ 0.027 0.023 −0.041 0.094∗∗∗ 0.079∗∗∗ 0.070∗∗

(0.021) (0.037) (0.029) (0.034) (0.023) (0.024) (0.033)

Non-interest/Inc. 0.002 −0.006 −0.006 0.013∗ −0.004 −0.003 0.014

(0.005) (0.006) (0.004) (0.008) (0.005) (0.011) (0.017)

Loan/TA 0.0003 0.002 −0.012∗ 0.018 −0.019∗∗∗ −0.014∗∗∗ −0.003

(0.005) (0.011) (0.007) (0.018) (0.005) (0.005) (0.019)

Loan prov./NI 0.003 0.009 0.007 0.004 0.003 −0.011 −0.013

(0.003) (0.006) (0.012) (0.005) (0.009) (0.007) (0.012)

ROA −0.018∗∗∗ −0.018∗∗ −0.006 −0.034∗∗∗ −0.001 −0.024∗∗ −0.067∗∗∗

(0.004) (0.007) (0.005) (0.005) (0.003) (0.011) (0.024)

Market-to-Book −0.058∗∗∗ −0.055∗∗∗ −0.052∗∗∗ −0.038∗∗∗ −0.057∗∗ −0.097∗∗∗ −0.057∗∗∗

(0.008) (0.014) (0.014) (0.012) (0.029) (0.013) (0.015)

Stock cap./GDP −0.188∗∗∗

(0.072)

Vol(Stock) −0.435

(0.772)

Bank concentration −0.068

(0.080)

Bank Z-score −0.011∗

(0.007)

GDP growth −0.065

(0.156)

Bank-fixed effects Yes Yes Yes Yes Yes Yes Yes

Time-fixed effects Yes Yes Yes Yes Yes Yes Yes

Observations 1,803 615 355 465 164 478 136

R2 0.286 0.163 0.212 0.119 0.282 0.572 0.303

Note: ∗p<0.1; ∗∗p<0.05; ∗∗∗p<0.01

35

![ASEAN + ME [ASEAN object traveler]](https://img.dokumen.tips/doc/110x75/568c534f1a28ab4916ba3e5d/asean-me-asean-object-traveler.jpg)