Embed Size (px)

Citation preview

Synergy

Identification and

Valuation

Presented by Andy Sheats

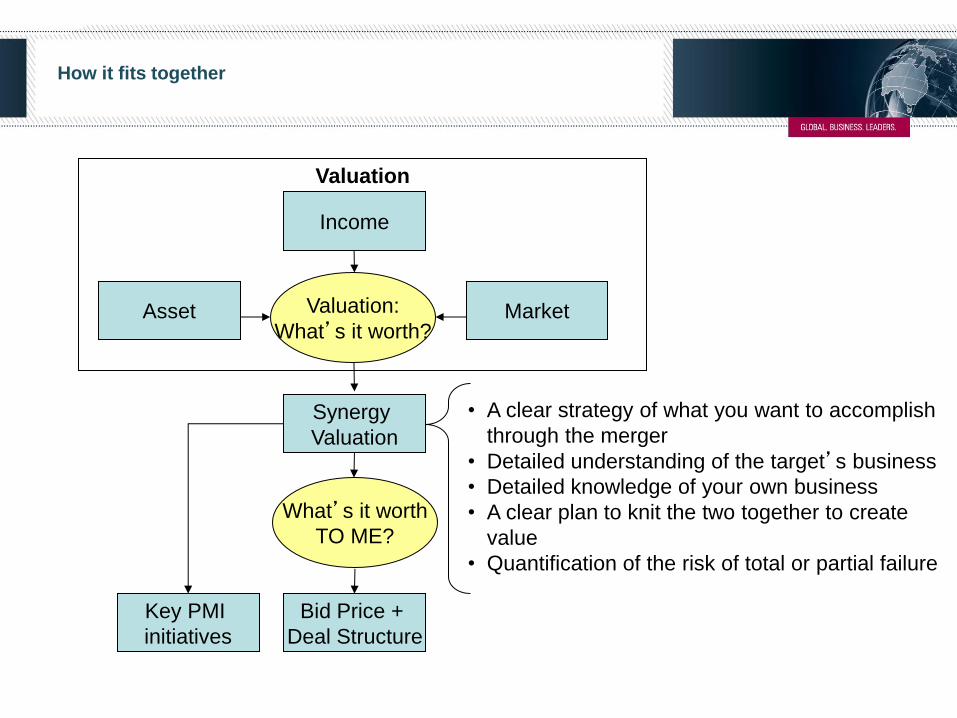

How it fits together

Valuation

Income

Asset Market Valuation:

What’s it worth?

Synergy

Valuation

What’s it worth

TO ME?

• A clear strategy of what you want to accomplish

through the merger

• Detailed understanding of the target’s business

• Detailed knowledge of your own business

• A clear plan to knit the two together to create

value

• Quantification of the risk of total or partial failure

Bid Price +

Deal Structure

Key PMI

initiatives

Agenda

• What are Synergies?

• Corporate Strategy Example: homesite.com.au

• Business Strategy Example: Airline merger

• Tools of the Trade: Strategic DD = Value of Information

Three Motivations to Acquire

Business Strategy Corporate Strategy Investment Strategy

Improve the competitive

position of an existing

business

• Scale

• Assets

• Capabilities

• …

TPG/iiNet

“Link” multiple

businesses to create

synergies between them

• Scope

ATT/DirectTV

Buy Low, Sell High

Buying cheap

(ie. “undervalued”)

PE/Qantas?

Seeking Synergy

“Worth more to us than to the Seller”

Synergy -- Management links two or more

businesses together such that:

Revenue

Increases

Cost

Decreases

Every other synergy is a figment of your imagination

(“organizational synergy”, “knowledge synergy”, etc.)

Simplistic Example

Cost Synergy through Scale

Bob’s

Bakery

Pat’s

Patisserie

Merger

Synergy “NewCo”

# Customers 10 10 20

Rev/Customer $10 $10 $10

Revenue $100 $100 $200

Trucks 1 1

Scale benefit:

1 truck 1

Cost/Truck $110 $125

Lowest cost

in group $110

Opex $110 $125 $110

“Profit” ($10) ($25) $90

Assumption

• Excess capacity allows consolidation

• Bob’s is “good enough”

Simplistic Example

Revenue through Pricing Power

Bob’s

Bakery

Pat’s

Patisserie

Merger

Synergy “NewCo”

# Customers 10 10 20

Rev/Customer $10 $10 +10% $11

Revenue $100 $100 $220

Trucks 1 1 1

Cost/Truck $110 $125 $110

Opex $110 $125 $110

“Profit” ($10) ($25) $110

Assumption

• No other bakeries in the area

• Cost advantage of 20% over more distant players (petrol cost)

• Customer has 200% profit margin (WTP)

• Note: Be careful of ACCC issues

10

A structured “value driver model” is helpful in identifying

detailed synergy opportunities (every consulting firm has one)

Get a copy from D&T at : http://tinyurl.com/4q69ym

Deloitte Consulting Enterprise Value Map (EVM)

Agenda

• What are Synergies?

• Corporate Strategy Example: homesite.com.au

• Business Strategy Example

• Strategic DD = Value of Information

Corporate Strategy in one slide

AU

Core

Business

Technology Link

“We will only have to use

one data center to serve both

markets”

New

Country

Product Link

“We can sell our existing products into a new market with low incremental cost”

New

Product

Business

Market Link:

“We get 4 million people to our

website each month, and can

sell this to them with no

incremental cost”

Your Corporate Strategy Answers These Two Questions:

1) What businesses are you in?

2) How you build links between them to create synergies?

Porter 1985

13

Corporate Strategy Example:

Acquisition of Homesite.com.au

58% owned by News Corp Australia’s #1 Real Estate website

(4M UVs)

Advertisers

include RE

Agents,

Developers,

Mortgage

lenders, etc.

Refresher on realestate.com.au

Corporate Strategy Example:

Acquisition of Homesite.com.au

A JV between News Corp and

Home Industry Association

Australia’s #1 Home Renovation

Webite (400K UVs) Advertisers

that REA

does not

currently

serve

What We Knew

Corporate Strategy Example:

Acquisition of Homesite.com.au

What We Found Out

A JV between News Corp and

Home Industry Association

• News Corp driving the business

with little input from HIA

• News Corp funding losses, and

unhappy to continue without JV

partner stepping up

Advertisers that REA does not

currently serve

• Advertisers unhappy due to low

advertising conversion

• Many on free trials

Australia’s #1 Home

Renovation Webite (400K UVs)

• Losing money hand-over-fist

• No clear way to improve financials

• News Corp funding losses, and

unhappy to continue without JV

partner stepping up

$M

Advertisers 1.9$

Display Ads 0.1$

Revenue 2.0$

SEM 1.5$

Staffing 1.0$

Rent 0.4$

IT 0.4$

EBITDA 1.3 )($

Note: P&L is not actual company data, but is illustrative of case issues

So how do we find the synergies???

REA

Technology Link

“We will only have to use

one data center to serve both

markets”

HomeSite

Market Link

“4M people come to the site every month. We can use this traffic

to “feed” homesite, saving $2M pa in SEM”

Thomas 1986

18

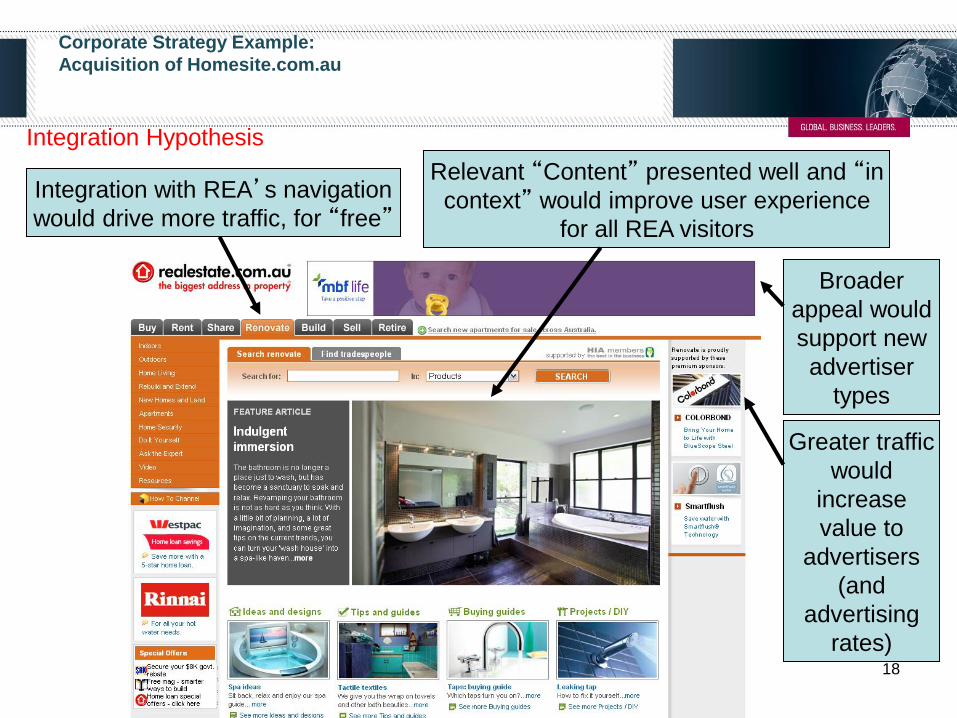

Corporate Strategy Example:

Acquisition of Homesite.com.au

Integration with REA’s navigation

would drive more traffic, for “free”

Relevant “Content” presented well and “in

context” would improve user experience

for all REA visitors

Greater traffic

would

increase

value to

advertisers

(and

advertising

rates)

Integration Hypothesis

Broader

appeal would

support new

advertiser

types

I recommend using a structured review of a business’s key value

drivers to identify potential synergies

REVENUE SYNERGIES

Free

Cash

Flow

20% Listings Revenue Uplift as we

reach scale to “define the

marketplace for commercial

property in Australia”

• Pricing power with lift to traffic

• More advertisers

Cost of Inputs

• Cost of Traffic / Google SEM

Remove duplication

• G&A

• R&D

• Facilities

Rationalization of PP&E

• IT infrastructure (over time)

Homesite Illustrative P&L Synergies

$M Before Synergy After

Synergy

"DCF" Comment

Advertisers 1.9$ 20% 2.3$ 1.0$ Uplift with traffic increase

Display Ads 0.1$ 0.5$ 0.6$ 1.3$ New advertisers, more inventory

Revenue 2.0$ 2.9$

SEM 1.5$ 1.5 )($ -$ 3.9$ Cut SEM to nil

Staffing 1.0$ 0.1 )($ 0.9$ 0.3$ One Managent Role

Rent 0.4$ -$ 0.4$ Move to our office with no net savings

IT 0.4$ 0.1 )($ 0.3$ 0.3$ We can supply for less

EBITDA 1.3 )($ 1.3$

6.7$

BASE CASE SYNERGY P&L and VALUATION ($) Illustrative Example

Note: P&L is not actual company data, but is illustrative of case issues

P&L Impact

Basic Synergy Model

Optimistic Synergy Valuation

Stand Alone

Valuation

(“Value to Them”)

Potential Value

“Value to Us”

Potential

Value

Creation

BASE CASE DCF VALUATION ($)

Increase

Advertising

Rates

$1M

Display

Ads

$1.3M

SEM

Reduction

$3.9M

IT+Staffing

$0.6M

Note: P&L is not actual company data, but is illustrative of case issues

But how sure are we?

Isn’t this the “optimistic” case?

How do we deal with uncertainty in

whether we get them, and what they are

worth?

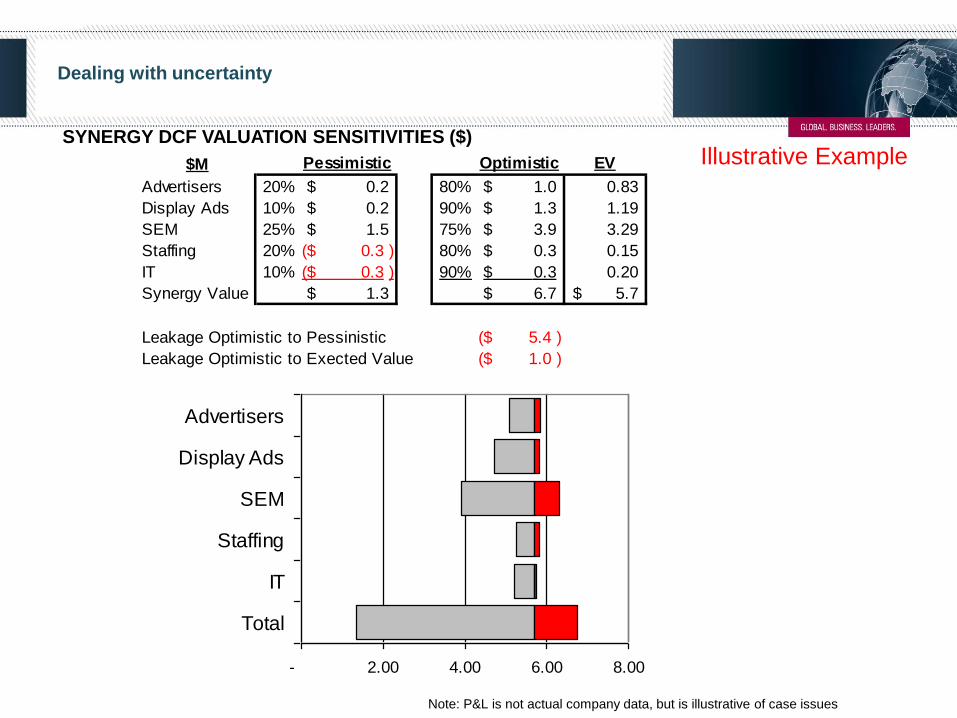

Dealing with uncertainty

Illustrative Example

Note: P&L is not actual company data, but is illustrative of case issues

$M Pessimistic Optimistic EV

Advertisers 20% 0.2$ 80% 1.0$ 0.83

Display Ads 10% 0.2$ 90% 1.3$ 1.19

SEM 25% 1.5$ 75% 3.9$ 3.29

Staffing 20% 0.3 )($ 80% 0.3$ 0.15

IT 10% 0.3 )($ 90% 0.3$ 0.20

Synergy Value 1.3$ 6.7$ 5.7$

Leakage Optimistic to Pessinistic 5.4 )($

Leakage Optimistic to Exected Value 1.0 )($

- 2.00 4.00 6.00 8.00

Advertisers

Display Ads

SEM

Staffing

IT

Total

SYNERGY DCF VALUATION SENSITIVITIES ($)

Basic Synergy Model

DCF VALUATION ($)

Potential Value Destruction

(“Leakage”)

(1.0M)

$5.7m

Negotiation

Range

“Value to Them” “Value to Us”

Optimistic Synergy Valuation

Agenda

• What are Synergies?

• Why Acquire Anyway

• Corporate Strategy Example: homesite.com.au

• Business Strategy Example

– Business Strategy on one slide

– Example: Commercial Property Sector

• Strategic DD = Value of Information

• Synergy Capture

A practical example of linking businesses

AU

Residential

Website in Australia

with real estate

classifieds

c. $100M in revenue

Mortgage Broking

Company in London with

c. GBP10M in revenue

A good move?

UK

Mortgage

Broking

A long time ago (1991) Geoffrey A. Moore made a bowling pin analogy for expanding into related

businesses

Moore 1991

This drives a path-dependent expansion into related businesses and markets that minimizes

risk at each step

AU

Residential

IR

Resi

UAE

Resi

NZ

Display

AU

Comm

UK

Display

UK

Mortgage

Broking

UK

Resi

NZ

Resi AU

Commercial

AU

Display

AU

Mortgage

Broking

AU

Renovate

Agenda

• What are Synergies?

• Why Acquire Anyway

• Corporate Strategy Example

• Business Strategy Example: Airline merger

• Strategic DD = Value of Information

Business Strategy Example:

Merger of Two Large Airlines

• Clients:

– Jointly engaged by the Boards of two large competing airlines

– Airline industry under extreme pressure (macro, competitive, … )

– Secretly considering a full merger

– Very contentious political and labour environment

• The Project:

– How would merger improve competitive position of the merged

business?

– Identify potential merger synergies

– Develop post-merger operating model

– Develop PMI plan to implement

• The Team:

– 10 consultants for 10 months

Business Strategy on One Slide

Market Selection Competitive Position

• What you can do?

(resource view of the firm)

• What you should do?

(value maximization)

• How you do it to beat competitors

How will this acquisition improve our competitive

position?

Airline Industry Challenges circa 2003

1. World events

2. Cost structure

3. Industry profitability

4. Asia-Pac industry changes

1. World Events

9-11

2. Cost structure : Dominated by Fuel + CapEx

Representative Airline Cost Structure – as of 2000

Oil prices have continued to have a massive

impact on industry profitability

3. Industry Profitability: Sage Advice

“The worst sort of business is

one that grows rapidly, requires

significant capital…, and then

earns little or no money. Think

airlines.

…

If a farsighted capitalist had

been present at Kitty Hawk, he

would have done his successors

a huge favor by shooting Orville

down.”

— Warren Buffett, annual letter to

Berkshire Hathaway shareholders,

February 2008.

Investment in Airlines

“People who invest in aviation

are the biggest suckers in the

world.”

David G. Neeleman, after raising a

record $128 million to JetBlue Airways,

quoted in Business Week, 3 May 1999.

4: Industry Change

Family Breakups

A New Neighbour

Death of a Friend New Kids on the Block

40

QF + SQ Merger

Generic Strategy for Airlines:

• Differentiation strategies: quality of service (seats, food, lounges);

routes, alliance programs, FF programs

• Cost: utilization (SWA), Scale, hedging strategies, low-cost labour pools,

outsourcing (variabilizing fixed costs)

• Focus: Geography (QF=AU), Leisure/Business, full service/LCC

How will this acquisition improve

competitive position?

(Hint: $Rev Up or $Cost Down Relatives to Competitors)

Sources of Value: Routes

Improved Aircraft Utilization

through on-flying

destinations

(cost down)

Combine latent capacity in

both Companies to enter

new markets ($ up)

Rationalize overlapping

routes to increase utilization

(cost down)

Sell onward flights to

“Newco” rather than

alliance partners – interline

leakage ($ up)

Sources of Value: OpEx Reduction

Flying

Baggage

Cargo

Holidays

Catering

Engineering/

Maintenance

Airline A

Flying

Baggage

Cargo

Holidays

Catering

Engineering/

Maintenance

Airline B

Corporate Corporate

SMASH!

1) Remove Duplication

2) Realize Scale

3) Lvg Best in Group

cost structure)

Flying

Baggage

Cargo

Holidays

Catering

Engineering/

Maintenance

Airline C

Corporate

Brand A Brand B

Corporate

Sources of Value: CapEx Reduction

Airline A Airline B

747 Jumbos 737 A320 747

A380’s

A380’s

SMASH! 1) Remove Duplication

2) Realize Scale

3) Lvg Best in Group

cost structure)

Sources of Value: CapEx Reduction

• Common Engineering

– Low-cost engineering units (location)

– Common spare parts (massive – engines

cost heaps)

– Scale in parts/service suppliers

• Common Facilities

– $500M to $1B per model

– Many of these currently under construction

(A380)

• Leverage with Boeing/Airbus

– Current orders/options

– Ongoing

– future

Airline C

A320 A380’s

Billions of dollars in CAPEX reduction

In the case of Airline mergers, synergies typically result from a

richer network that unlocks new revenue sources, and cost

reduction of overlapping and duplicate functions

Synergy

value

(NPV)

Cash

synergy

(run rate)

Sources of

merger

synergy

Airline value

drivers

Revenue

growth

Capture interline “leakage”

Combining passenger volume to increase frequencies in key markets

Open new destinations and increase routing possibilities

Operating

margin

improvement

Reduce duplication

Leverage scale benefits where appropriate

Migrate to best-in-group productivity where appropriate

Leverage best-in-group pricing for engineering, ground services, IT and

in other sourcing

Increase fleet commonality to decrease engineering

Reduced

tax rate (Potential corp tax rate changes)

Reduced

working capital Create scale benefits in spares/inventory pool

Reduced

CapEx

requirement

Increase fleet commonality to the extent possible:

Coordinate future CapEx for engineering

Create purchasing scale in aircraft purchase

Move to best-in-group aircraft purchase cost

Centralise and share engineering, simulation and training

Rationalise lounge CapEx

Reduced

cost of capital (Potential dual listing / migrated listing

NPAT

Improveme

nt

(run rate)

~50%

increase

Reduced

use of cash

to fund

operations

~2%

reduction

Outcomes Value

Billions of $

in value creation

Agenda

• What are Synergies?

• Why Acquire Anyway

• Corporate Strategy Example: homesite.com.au

• Business Strategy Example

• Tools of the Trade: Strategic DD = Value of Information

Value of Strategic DD = Value of information

• What’s it worth to know more about the target than anyone else?:

– Hidden value

– Turnaround action plan

– Company Risks & Turnaround Risks

• How it is typically done…

– Personal contacts at targets (developed over a long time)

– Conference hallways/starbucks

– Specialist firms (LEK is one, there are others)

X% earnings

growth from a

smaller

revenue base

Outcome of Strategic Due Diligence

• Highly informed “Go/No-go” decision

• Informed valuation : Public + non-public + industry knowledge

• Valuation checklist : Key deal attributed

• 100-day plan

The keys to capturing synergy value in an acquisition

1. Sound strategy

2. Sound rationale for acquisition

3. Sound synergy assumptions

– Tested against “the facts”

– Risk adjusted valuation

– Execution ownership (us/them)

4. Key elements of valuation maintained in deal execution

– The right price

– The right terms

5. Key synergy assumptions “baked into” post-merger integration

(PMI) plan

6. Governance in place through value capture