Embed Size (px)

Citation preview

1

Swedish firms' untimely financial reporting - A study of goodwill impairment as a tool used to mislead financial users.

Master's Thesis 30 credits

Department of Business Studies

Uppsala University

Spring Semester of 2019

Date of Submission: 2019-05-29

Viktor Axelsson

Ludvig Eriksson

Supervisor: Leon Caesarius

Abstract

Title Swedish firms' untimely financial reporting

- A study of goodwill impairment as a tool used to

mislead financial users.

Date of submission 2019-05-29

Authors Viktor Axelsson, Ludvig Eriksson

Supervisor Leon Caesarius

Course 2FE840, Master Thesis, Advanced course, 30 ECTS

Five key words Earnings management, Real acitivites management,

Cash flow manipulation, Untimely reporting,

Goodwill impairment.

Purpose The purpose of the study is to investigate how

postponement of goodwill impairment is conducted

and if managers thereby contribute to a distortion of

the underlying qualitative characteristics in financial

reporting.

Methodology Proxies for earnings management activities, through

cash flow manipulation, are computed cross-

sectionally by sector-year with at least ten

observations. Suspect firms are then matched with

control firms within the same sector and operating

year to control for these effects.

Theoretical perspective The transition to the IFRS framework has contributed

to changes in the handling of goodwill. The yearly

impairment test has contributed with subjectivity in

the measurements resulting in fewer but larger

impairments.

Empirical foundation The study consists of quantitative secondary data

collected from Thomson Reuters Eikon. The data

consists of 1090 observations covering seven years of

Swedish listed firms with goodwill in their balance

sheet.

Conclusion The study concludes that suspect firms experience

abnormal current free cash flows compared to control

firms, which indicate managers manipulating cash

flows in order to postpone goodwill impairment. Also,

growth opportunities and analysts' coverage have a

significant impact on earnings management activities.

Acknowledgment

We would like to acknowledge everyone who contributed to our academic accomplishments.

First of all, we would like to thank our supervisor Leon Caesarius and fellow students who have

provided insightful comments and guidance. Secondly, we would like to thank David Randahl

from the Department of Statistics for the time and help with statistical guidance throughout this

writing process.

Table of content

1. Introduction .......................................................................................................................... 1

1.1 Background ..................................................................................................................... 1

1.2 Problem statement .......................................................................................................... 2

1.3 Purpose ............................................................................................................................ 4

1.4 Research question ........................................................................................................... 4

1.5 Delimitation ..................................................................................................................... 4

2. The theoretical framework of IFRS.................................................................................... 5

2.1 The objective of financial reporting.............................................................................. 5

2.2 Business combination framework ................................................................................. 5

2.3 Impairment of goodwill.................................................................................................. 6

3. Literature review .................................................................................................................. 7

3.1 Earnings management ................................................................................................... 7

3.1.1 Goodwill impairment ................................................................................................ 8

3.2 Abnormal cash flows ...................................................................................................... 9

3.3 Incentives to manipulate earnings .............................................................................. 12

3.3.1 Analysts and earnings thresholds ............................................................................ 13

3.3.2 Growth opportunities ............................................................................................... 14

3.4 Asymmetric information .............................................................................................. 14

3.5 Summary and hypotheses development ..................................................................... 16

3.6 Criticism to precedent literature................................................................................. 18

4. Method ................................................................................................................................. 19

4.1 Research Design ............................................................................................................ 19

4.2 Sample method ............................................................................................................. 19

4.3 Test of earnings management ...................................................................................... 21

4.3.1 Real activities management (RAM) ........................................................................ 21

4.3.2 Operating cash flow management (OCFM) ............................................................ 22

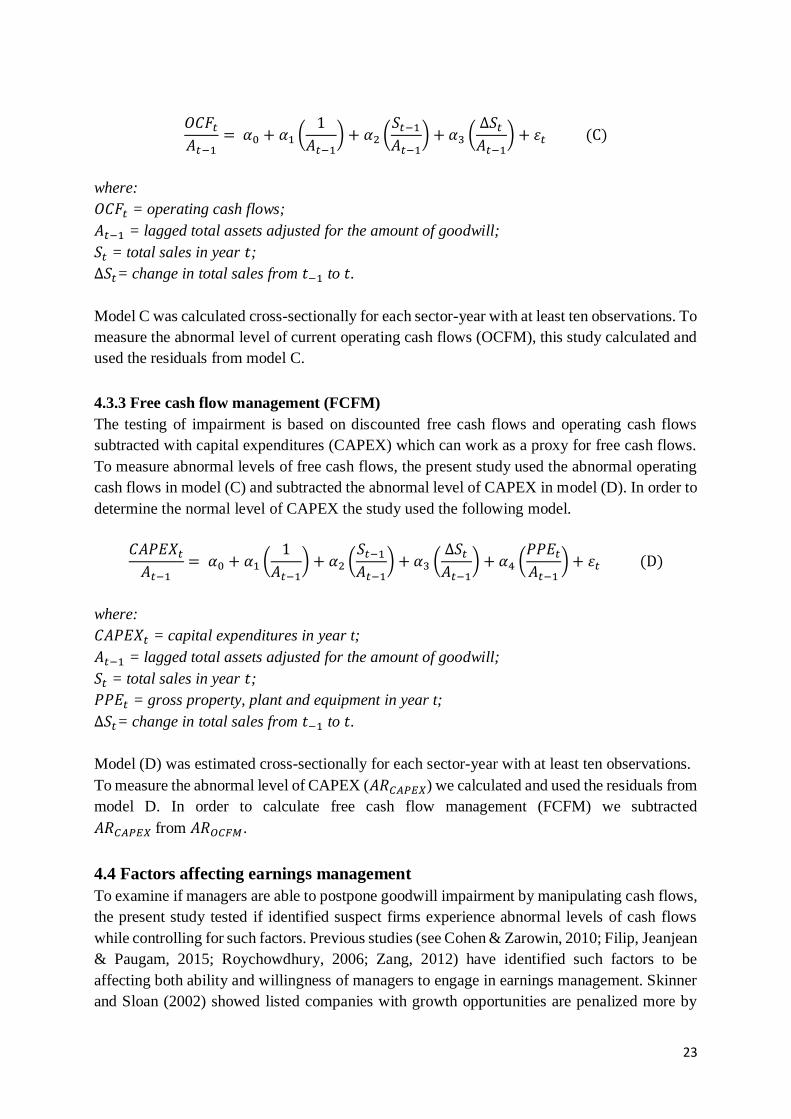

4.3.3 Free cash flow management (FCFM) ...................................................................... 23

4.4 Factors affecting earnings management..................................................................... 23

4.5 Method discussion ........................................................................................................ 24

4.5.1 Reliability & replicability ........................................................................................ 24

4.5.2 Validity and ethical considerations ......................................................................... 25

4.5.3 Criticism of research design and method ................................................................ 25

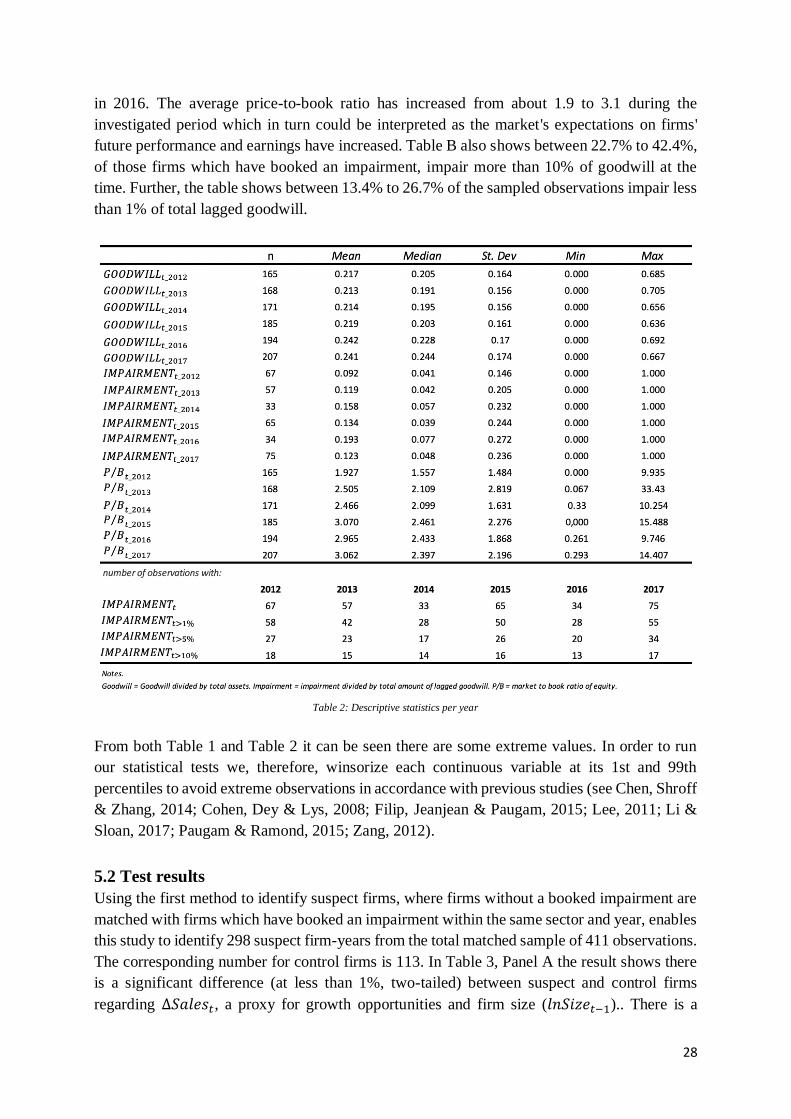

5. Sample and result ............................................................................................................... 27

5.1 Sample selection and descriptive statistics ................................................................. 27

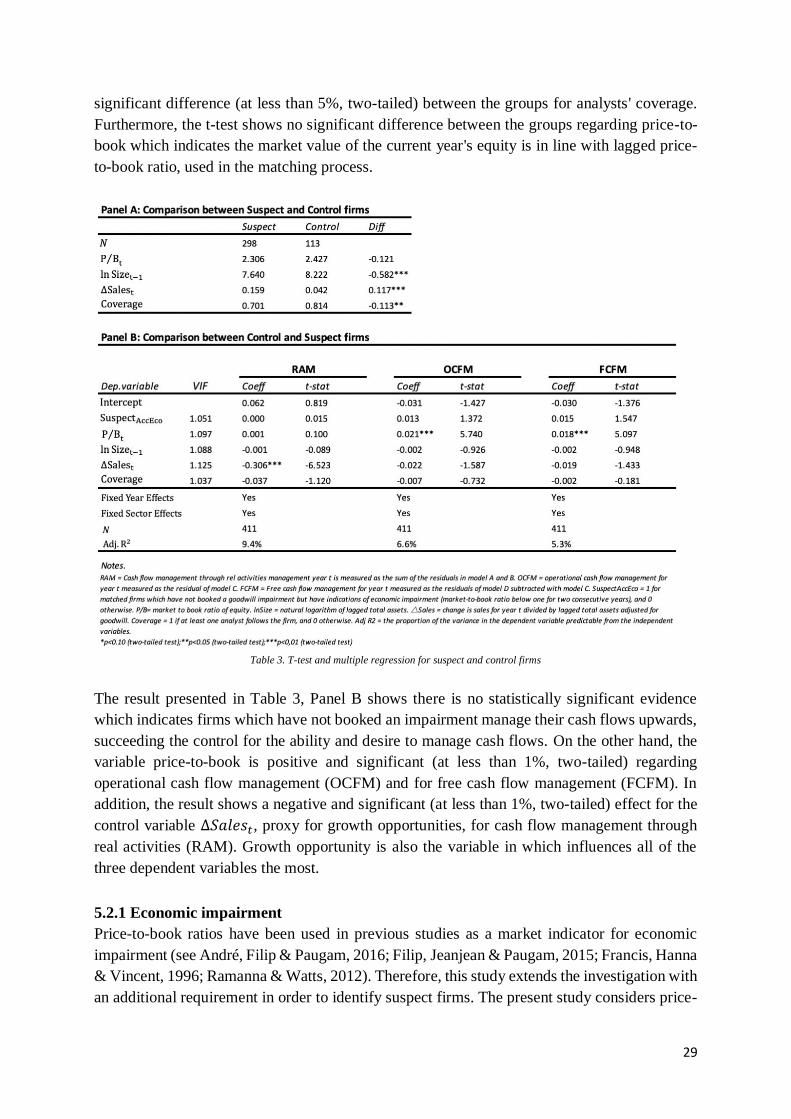

5.2 Test results .................................................................................................................... 28

5.2.1 Economic impairment ............................................................................................. 29

5.2.2 Summary hypotheses result ..................................................................................... 31

6. Discussion ............................................................................................................................ 32

6.1 Dispersion of the sample .............................................................................................. 32

6.2 Earnings management through cash flow manipulation .......................................... 33

6.2.1 Analysts coverage and growth opportunities .......................................................... 34

6.2.2 Timeliness of goodwill impairment ........................................................................ 35

7. Conclusion ........................................................................................................................... 38

7.1 Contribution.................................................................................................................. 38

7.2 Limitations and future research ................................................................................. 39

8. References ........................................................................................................................... 40

9. Appendix ............................................................................................................................. 48

1

1. Introduction

In the following chapter, a background of the study's subject is presented and problematized,

which leads to the formulation of a question and a purpose. The chapter ends with a

delimitation.

1.1 Background

During takeovers, firms are paying premiums to acquire other businesses. Takeover premiums

can be defined as the difference between the purchase price and the fair value of the acquired

firm's identifiable net assets (Gore & Zimmerman, 2010). Previous studies have shown the

average paid premium in takeovers between 1990 and 2002 is 45% (Betton, Eckbo & Thorburn,

2008) and the past deals made in the U.S. have shown acquiring firms tend to pay an average

43% takeover premium (Woo, Cho, Park & Byun, 2018). The reason why takeover premium

exists is due to the belief the entire business is greater than the individual sum of all the assets

(Gore & Zimmerman, 2010) and absence of a premium would result in shareholders refusing

to sell (Eccles, Lanes & Wilson, 1999). This belief originates from synergy effects and the

premium can, therefore, be explained by the future additional value generated from the

combination of business units, a value that would not be available if the businesses were

operating independently (ibid). This premium is then categorized as goodwill (Gore &

Zimmerman, 2010; Marton, Sandell & Stockenstrand, 2016) and is visualized as an intangible

asset on the acquiring firm's balance sheet.

The accounting of goodwill has been a frequently discussed subject over the past century by

standard setters and producers of financial reports all over the world (Chalmers, Godfrey &

Webster, 2011; Garcia, Katsuo & van Mourik, 2018). The debate has regarded questions such

as the recognition and measurement process of goodwill in financial reports and whether it is

an asset under depletion or permanent one (Chalmers, Godfrey & Webster, 2011). Throughout

history, the answers to the questions have differed depending on which country and legislative

framework that has been used at the time (Garcia, Katsuo & van Mourik, 2018). The definition

of goodwill has differed the last century but the general perception of what is considered as

goodwill in modern times is that goodwill is inseparable from the entity and cannot exist by

itself (Ma & Hopkins, 1988). This definition corresponds to International Financial Reporting

Standards (IFRS) where it is stated goodwill are future economic benefits pertaining to assets

which are incapable of being individually identified and recognized separately (IFRS 3, 2009).

The differences in definition and practice between countries inspired a movement toward

harmonization of standards in the 1970s which has inspired new rules and regulations along the

way (Garcia, Katsuo & van Mourik, 2018). The practice for goodwill throughout this period

was to use a conservative approach and amortize the goodwill which impacted the company's

profit. However, the year 2005 contributed with conversions and changes for both companies

and investors regarding the value handling of goodwill due to the transition to the legislative

framework IFRS (Hellman, Andersson, Fröberg & Cahan, 2016; Johansson, Hjelström &

Hellman, 2016). In the application of IFRS the amortization of goodwill is not sanctioned and

2

a yearly impairment test should be conducted to determine the fair value of an asset (Hamberg,

Paananen & Novak, 2011; IAS 36.96; Marton Sandell & Stockenstrand, 2016). The reason

behind this change was the argument from International Accounting Standards Board (IASB)

where impairment of goodwill better reflects the underlying economic value compared to the

previous practice of amortization (Chalmers, Godfrey & Webster, 2011).

Previous research has identified the valuation process of impairment as problematic due to its

subjective nature and that miscalculations might result in a future need for impairment which

can have a negative impact on shareholders (Hirschey & Richardson, 2003; Li, Shroff,

Venkataraman & Zhang, 2011). The existence of real-world examples of goodwill impairments

is not absent, and some recent examples constitute of Ericsson, Nordea, and Kraft Heinz. In

2018 the telecom manufacturer Ericsson was forced to make a goodwill impairment of 12.7

billion SEK which had a negative impact on the operating profit for the quarter (Privataaffärer,

2019). Another example is the bank Nordea, due to a change of investment strategy, who

performed a goodwill impairment in the Russian market of 1.4 billion SEK (Nordea, 2019).

The impairment for Kraft Heinz amounted to 15.4 billion dollars which is one of the largest

impairments in history (Gara, 2019). This impairment was triggered by short term financial

developments which surprised the market and caused a rapid decline in the company's stock

price, thus destroying value for both investors and the company. The impaired goodwill in

Ericsson pertained to investments made in 2008 and the timing of the impairment raises

questions about credibility and if the impairment had been delayed. Thus, the transition to IFRS

has provided greater flexibility and subjectivity in the accounting choices (Capkun, Collins &

Jeanjean, 2016) which can impact the market's credibility and the value of the company.

1.2 Problem statement

The increased use of accounting estimates in financial reporting have faced major criticism and

concerns due to misstatements of earnings and equity, inappropriate fair value measurements

originating from management bias (Beatty & Weber, 2006) and its unethical approach

(Smieliauskas, Bewley, Gronewold & Menzefricke, 2018). In addition, impairment losses from

goodwill are perceived to lack verifiability and contain significant measurement uncertainty

and the possibility of being opportunistically reported (Francis, Hanna & Vincent, 1996;

Ramanna & Watts, 2012; Riedl, 2004). This will, therefore, conflict the objectives of the

financial reporting which state financial information should be useful for decision making

(IFRS, 2018a) and thereby represent what it intends to disclose (Nobes & Stadler, 2015). Under

the framework of IFRS, impairment tests allow managers to imply a wide level of discretion

(Filip, Jeanjean & Paugam, 2015; Lhaopadchan, 2010). Estimates of the fair value of goodwill

reflect management's assumption regarding the firm's future actions, strategy (Filip, Jeanjean

& Paugam, 2015), productivity and profitability (Roychowdhury & Martin, 2013). Subjective

views and assumption of future performance might reduce transparency and reliability of

reported financial information which might cause an information gap between shareholders and

management (Caruso, Ferrari & Pisano, 2016), defined as information asymmetry. Standard

setters, on the other hand, expect managers to mediate private information, which is the basis

of the estimates of future cash flows, to the market (Filip, Jeanjean & Paugam, 2015) and

therefore mitigate the asymmetric information distribution. Also, the difficulties arising from

3

impairment processes forces standard setters to regulate an increment of impairment disclosure

as a method of reducing information asymmetry and thereby increase the level of transparency

and reliability (Caruso, Ferrari & Pisano, 2016).

Despite these regulations of increased disclosure, there are some problems arising from

discretionary methods and assumptions in impairment tests of goodwill. Impairments are

considered faithfully reported when impairment losses reflect economic impairment (Ramanna

& Watts, 2012; Riedl, 2004). When they are not, goodwill impairment can be seen as a tool

used in earnings management (Caruso, Ferrari & Pisano, 2016; Ramanna & Watts, 2012).

Francis, Hanna and Vincent (1996) argue managers perform impairments out of two reasons.

The first reason is that managers want to reflect changes in future economic conditions,

strategies, competitive situations or previous and current poor firm performance. The

alternative reason is that managers take advantage of the discretion and only recognize

impairments when it is advantageous to do so, without investors being able to undo these

manipulations which impact them unfavorably.

A growing body of empirical evidence shows that managers do not recognize economic

impairments of goodwill in accounting books in a timely manner and tend to manipulate

impairment tests (Filip, Jeanjean & Paugam, 2015; Paugam & Ramond, 2015; Ramanna &

Watts, 2012). Consequently, when assets with indications of impairment are not impaired

delayed goodwill impairments contain lack of timeliness (André, Filip & Paugam, 2016) with

the result in overvalued firms due to overstated booked values (Li & Sloan, 2017). Ramanna &

Watts (2012) find evidence of managers manipulating earnings by selectively delaying

goodwill impairment in circumstances where they have agency-based motives to do so. This is

in line with the prediction of the agency theory which predicts the average manager tends to

take advantage of the unsecured elements of goodwill accounting rules to alter the financial

reports opportunistically (Filip, Jeanjean & Paugam, 2015). In applying previous study results

with the definition of earnings management that managers using judgment in financial reporting

to mislead some stakeholders about the company's underlying economic performance (Healy

& Wahlen, 1999), one could argue goodwill impairment tests could be a useful tool for

managers to manipulate financial reporting.

Previous studies of firms which have market indications of goodwill impairment show a 69%

frequency of non-impairment of goodwill (Ramanna & Watts, 2012) and that only 53% actually

impairs when they have an indication (Verriest & Gaeremynck, 2009). The evidence presented

in Ramanna and Watts (2012) is consistent with predictions from the agency theory regarding

a positive association between non-impairment and CEO compensation, debt covenant

violation, and CEO reputation concerns. On the contrary, the study finds no explanation of the

predictions that non-impairment is related to the flexibility of managers and the possession of

private information about the firm. Previous research by Filip, Jeanjean and Paugam (2015)

focused on the managerial postponement of goodwill impairment recognition through

manipulation of the cash flows and the future consequence on performance due to this strategy.

The conclusion from their study is that real activities manipulation is detrimental to future

4

performance and firms which were suspected of postponing their goodwill impairment losses

were exhibiting an increased discretionary cash flow compared to other control groups.

The empirical evidence indicates managers in firms, with market indications of goodwill

impairment, engage in manipulation of cash flows to avoid impairment losses. The reason for

goodwill manipulation can be grounded in managements unwillingness to admit that the firm

overpaid for previous acquisitions and to uphold a facade of adequate stewardship of company

assets (Li & Sloan, 2017; Roychowdhury & Martin, 2013). Such manipulations would,

therefore, be unethical and in conflict with IFRS fundamental qualitative characteristics of

useful financial information. For financial information to be useful, it must possess relevance

and be faithfully represented (IFRS, 2018). With other words, it must be relevant and represent

the substance of an economic phenomenon instead of exclusively representing its legal form

(ibid.). In addition to prior research, a study by Duff and Phelps (2018) showed goodwill

impairments for US firms increased with 23% and reached a total value of 35.1 billion dollars

in 2017, despite a strengthening global economy. The study also showed a marginally

increasing number of impairment, which indicates the magnitude of goodwill impairment has

become larger and therefore more important for investors to understand.

Previous studies have shown that earnings management is used by managers for their own

utility maximization and to disclose higher financial earnings for the firm. The present study

assumes this phenomenon occurs in different geographic and demographic contexts and the

investigation of the phenomenon can contribute with further knowledge to academic literature,

standard setters and users of financial information. Consequently, the present study investigates

goodwill to determine if, and thus how, managers engage in earnings management through

manipulating current cash flows in order to delay goodwill impairment.

1.3 Purpose

The purpose of the study is to investigate how postponement of goodwill impairment is

conducted and if managers thereby contribute to a distortion of the underlying qualitative

characteristics in financial reporting.

1.4 Research question

How do managers separate accounting and economic impairment of goodwill and thereby

disrupt timeliness of financial reporting?

1.5 Delimitation

An investigation by Gauffin and Nilsson (2018) on listed firms on the Stockholm Stock

Exchange shows approximately 56% of the purchase price is allocated to goodwill during

acquisitions in 2016. In addition, the result showed only 0.9% of total goodwill was impaired

during the same period. Due to these results of low impairment and a large amount of distributed

goodwill to acquiring firms' balance sheet this study will focus on how managers can disrupt

timeliness of financial reporting by separate accounting and economic impairment of goodwill

by delimiting the investigation of the phenomenon within a Swedish context.

5

2. The theoretical framework of IFRS

Chapter two narrates parts of the IFRS framework since it constitutes of a fundamental basis

for complying with the purpose of the study.

2.1 The objective of financial reporting

IFRS is an international accounting standard which is mandatory to use in the consolidated

financial statements for listed companies on regulated markets (IFRS, 2018). The theoretical

framework of IFRS presents foundational concepts for financial reporting and is applied by the

International Accounting Standards Board (IASB) when developing new standards (ibid.) IFRS

has a principle-based view which gives companies the ability to tailor the financial reporting to

fit their specific organization (ibid.). The intention of IFRS is to achieve transparency,

accountability and efficiency to financial markets all over the world (ibid.). The framework of

IFRS currently contains 17 principles and the additional framework IAS (International

Accounting Standards) contains 28 principles (ibid.). To support the purpose of the study the

objective of financial reporting and IFRS principles are presented.

The objective of financial reporting is to provide financial information that is useful to users in

making decisions relating to providing resources to the entity” (IFRS, 2018a). The users of

financial information are firms', both existing and potential, investors, lenders and other

creditors (ibid.). The decisions, made by the users based on this information, regard for example

buying, selling or holding equity or debt instruments and influence management actions (ibid.).

In order to make these decisions, the users of financial information evaluate the firm's prospects

for future net inflows and management's stewardship of the firm's financial resources (ibid.).

Also, a majority of information is obtained by the users from financial reports. Therefore, to

make these assessments users need useful financial information to make their decisions as good

as possible.

For financial information to be perceived as useful, it requires to be relevant and faithfully

represent what it intends to disclose (Nobes & Stadler, 2015). Faithful representation and

relevance are deemed as elementary qualitative characteristics for financial information to be

useful (IFRS, 2018a). When financial information is verifiable, timely, understandable and

comparable the usefulness can be enhanced (ibid.). For information to be considered as relevant,

it needs to be capable of making a difference in decision-making and possess confirmatory or

predictive value (Beaver, 1968; Nobes & Stadler, 2015). For information to be considered

faithfully it should be, to the highest possible extent, neutral, free from error and complete

(Nobes & Stadler 2015).

2.2 Business combination framework

The IFRS 3 principle regards business combination framework, and presents an outline of the

accounting treatments to consider when an acquirer obtains control over another business (IFRS

3, 2009). The standard is intended to enhance the reliability, relevance and comparability of

information disclosed pertaining to acquisitions and the effect on financial disclosures. In an

acquiring situation, the business unit should use the acquisition method to identify the acquirer,

6

acquisition date, recognition and fair value measurement of the transferred assets and liabilities

and the recognition of goodwill or gains pertaining to the acquisition (ibid.). Goodwill is

considered as an intangible asset and constitutes of the difference between the transferred

amount and the acquired company's net assets (Hamberg, Paananen & Novak 2011; Marton,

Sandell & Stockenstrand, 2016). Goodwill is recorded on the balance sheet and gains pertaining

to the acquisition is recorded in the profit and loss statement (Gore & Zimmerman, 2010, IFRS

3, 2009).

2.3 Impairment of goodwill

According to the IAS 36.96 principle an entity is required, annually, to test whether goodwill

indicates a loss in value which therefore needs to be impaired (IFRS, 2018). To perform an

impairment test the goodwill is allocated to all the acquirer's cash generating units which are

deemed to benefit from the synergies of the combination (IAS 36.80). A cash-generating unit

is an identifiable asset or group of assets generating cash inflows which are separable from cash

inflows from other assets. When a cash-generating unit has been allocated with goodwill the

impairment test is performed by a comparison of the carrying amount and the recoverable

amount of the unit (IAS 36.90). The carrying amount is the value in which an asset is recognized

in the balance sheet after accumulated depreciation and accumulated impairment losses (ibid.).

The recoverable amount is the highest of an asset's fair value less cost to sell and it's value in

use (ibid.) If the carrying amount is higher than the recoverable amount the value of the unit is

overstated unless the unit is impaired to equal the recoverable amount (ibid.). The value of the

asset is decreased on the balance sheet and the loss pertaining to the decrease in value is

accounted for as a loss in the profit and loss statement (ibid.). When an impairment is

recognized the entity must disclose detailed information to the financial users with estimates

and assumptions used to measure recoverable amounts of cash generating units (IAS 36.134-

135).

Impairment tests are usually based on the discounted cash flow model when estimating the

present value of future cash flows, normally forward-looking three to five years, generated from

a cash-generating unit (Filip, Jeanjean & Paugam, 2015; Nie, 2018). It is mostly used due to its

direct link with Modigliani and Miller's finance theories (Lander & Reinstein, 2003). This

model is an absolute valuation method which obtains the current value of an assets future free

cash flow based on an appropriate discount rate (Nie, 2018). The model is affected by several

parameters, such as the weighted average cost of capital, discount rate, growth assumption,

profitability margins and terminal growth rate (Filip, Jeanjean & Paugam, 2015). The use of a

discounted cash flow (DCF) model requires to first estimate the free cash flow (FCF), which is

the remaining and distributable cash flow after the firms operating and financing needs have

been covered (Lander & Reinstein, 2003). The DCF model estimates the sum of the firm's

equity and debt, the market value of the firm's debt netted for excess cash then determines the

value of the entity (ibid.).

7

3. Literature review

Chapter three narrates the relevant theories and literature given the research question and

purpose of the study. The literature review was conducted with a narrative approach. To build

the studies theoretical foundation literature were identified within the field of earnings

management, goodwill impairment and information asymmetry. The chapter concludes with a

formulation of hypotheses and critique against the presented literature.

3.1 Earnings management

Even though the earnings management theory has been researched since the 1960s (Beaver,

1968), and is a widely researched and relevant topic within accounting studies (Caruso, Ferrari

& Pisano, 2016) the theory lacks a clear definition (Ronen & Yaari, 2008). The consensus of

the literature is however that earnings management is manipulation of an entity's economic

performance made by insiders to mislead external stakeholders, influence contractual outcomes

(Leaz, Nanda & Wysocki, 2003; Ronen & Yaari, 2008) and most importantly avoid earnings

decline and reporting losses in order to meet certain earnings thresholds (Graham, Harvey &

Rajgopal, 2005; Roychowdhury, 2006).

Earnings management can be perceived as something unethical rather than illegal. The reason

behind the allowance of managerial discretionary actions is the argument that standard setters

must allow managers to exercise judgment in financial reporting in order to make financial

reports more informative for users through an extension of managers' knowledge and

information about their entity's future performance (Healy & Wahlen, 1999). This allows

managers, through judgment, to create opportunities for earnings management and the

allowance of preferring methods which do not accurately reflect the entity's underlying

economic situation (ibid.). Managers can use the opportunities given and their expert

knowledge about the business to select methods of reporting, altering estimates and disclosures

to match the business economics of the firm, which might increase the value of accounting as

a communication tool (Healy & Wahlen, 1999).

The literature highlights different fields of earnings management constituting of earnings

smoothing, minimization, maximization, accrual management and real activities manipulation

(Ronen & Yaari, 2008; Filip, Jeanjean & Paugam, 2015). The real activities manipulation is

argued to be more attractive for managers to use compared to other forms of earnings

management, due to difficulties for auditors and gatekeepers to detect such manipulations

(Cohen & Zarowin, 2010; Cohen, Dey & Lyz, 2008; Huang & Sun, 2017). The real activities

management literature indicates companies use overproduction to reduce the cost of goods sold

(COGS), use price discounts to temporarily boost cash flows and decreases discretionary

expenditure to meet certain earnings thresholds (Graham, Harvey & Rajgopal, 2005; Huang &

Sun, 2017; Roychowdhury, 2006). The body of literature indicates real activities manipulation

can have negative effects on the future performance of a firm due to the measures taken to

increase the profit of the current period (Caruso, Ferrari & Pisano, 2016; Huang & Sun, 2017;

Roychowdhury, 2006). Further, it is argued that reductions in investments could be potentially

harmful to companies due to the lack of investments will not support the future growth of the

8

company. The methods used for real activities manipulation mentioned in the literature regards

the reduction of research and development (R&D) expenses, advertising and selling, general

and administrative (SG&A) expenses (Cohen & Zarowin, 2010; Filip, Jeanjean & Paugam,

2015).

Previous research found a positive effect on companies' earnings due to the removal of

mandatory goodwill amortization in the transition to IFRS 3 (Hamberg, Paananen & Novak,

2009). The literature shows a growing acquisition rate after the adoption to IFRS 3 which

resulted in increased levels of goodwill being recorded on firms' balance sheets (Caruso, Ferrari

& Pisano, 2016; Hamberg, Paananen & Novak, 2009; Ramana & Watts, 2012). On the other

hand the literature also highlights the absence of goodwill impairments during the later period

(Hamberg, Paananen & Novak, 2009). The result in the study by Hamberg, Paananen and

Novak (2009) indicates goodwill-intensive firms were revalued upwards by the stock market

which implies that subjective methods have made financial reporting less useful to investors.

Previous studies have found evidence of managerial incentives being influential for the choice

of accounting method and for altering expenses such as debt contracts, bonuses and current

turnover in an opportunistic way (Beatty & Weber, 2006; Francis, Hanna & Vincent, 1996). In

contradiction, Capkun, Collins and Jeanjean (2003) found no link between changes in

incentives which could explain increased earnings management behavior. The study by Leuz,

Nanda and Wysocki (2003) found earnings management to be less occurring in countries which

had strong investor protection with an explanation that the risk of detection is a limiting factor

for earnings management due to high detection costs. The literature highlights detection cost as

a motivator for using real activities manipulation due to difficulties for auditors to find the

manipulation which present a low risk of scrutinization (Roychowdhury, 2006). The literature

indicates that managers use their discretion and subjectivity to postpone recognition of losses

and thus opportunistically inflate company performance (Dinh, Kang & Schultze, 2016; Filip,

Jeanjean & Paugam, 2017; Jarva, 2009; Ramanna & Watts, 2012).

3.1.1 Goodwill impairment

The literature points out the legislative transition to IFRS 3 facilitates earnings management

activities through goodwill impairment. The literature regards two perspectives of research

pertaining to goodwill impairment where the first focuses on the determinants for timeliness of

goodwill impairments and the latter focuses on the stock market consequences from non-

impairment of goodwill (Chen, Schroff & Zhang, 2014). A study by André, Filip and Paugam

(2016) found goodwill impairments to lack timeliness, defined as the consequences when

accounting impairment is separated from economic impairment. The sample from Ramanna

and Watts' (2012) study showed a frequency of 69% for goodwill non-impairment, which

means firms with lower price-to-book ratio than one do not write down goodwill during the

second year. The findings are corroborated by the findings by Roychowdhury and Martin

(2013) that firms, with price-to-book ratios below one, exhibit between 22-26% probability of

goodwill impairment. The study found evidence of managers avoiding timely goodwill

impairment when they have agency-based incentives to do so, even though the market indicates

for impairment. The literature stream indicates that subjectivity of impairment tests has caused

9

financial reports to not reflect the underlying economic reality in relation to goodwill (Ramanna

& Martin, 2013; Roychowdhury & Martin, 2013). In contrast to these studies, Jarva (2009)

investigates non-impairment firms and finds no supporting evidence of opportunistically

evasion of impairments by managers in firms with market indications of impairment.

A theme within the goodwill impairment literature is the postponement of goodwill impairment,

referred to as timeliness of goodwill impairment (Chen, Schroff & Zhang, 2014; André, Filip

& Paugam, 2016). Both study results in Hayn and Hughes (2006) and Jarva (2009) indicate a

significant delay in the booking of goodwill impairments, the lag pertains to the recognition of

impairment loss when assets are economically impaired. Previous studies have found firms tend

to delay recognition of asset impairment even in the presence of economic impairment (Hayn

& Hughes, 2006; Jarva, 2009), such firms are referred to as suspect firms (Ramanna & Watts,

2012; André, Filip & Paugam, 2016). Prior studies show goodwill impairment to lag behind the

entity's operating performance and negative stock returns from two years (Li & Sloan, 2017)

up to three to four years (Hayn & Hughes, 2006), which indicates managers could selectively

delay accounting impairments.

Li and Sloan (2017) argue managers delay impairment tests due to the fear of negative stock

market reactions and managerial pride. The argument is corroborated by Roychowdhury and

Martin (2013) who argue that negative effects on firm value and managers' unwillingness to

admit to overpaying for prior acquisitions cause postponement of impairments. Therefore,

impairment of goodwill is portrayed as the least favorable action for managers and impairments

are strictly performed when it is clear that the benefits have expired from non-impaired goodwill

(Li & Sloan, 2017). The study by Chen, Shroff and Zhang (2014) gives other explanations for

non-impairment and argue that investors do not understand the intentions of goodwill

impairments and the signals of future performance. Further, it is argued that investors do not

learn the effects of goodwill impairment until the publication of the following annual report.

The postponement and untimeliness of goodwill impairment are argued to possibly be

detrimental for both investors and companies due to that investors systematically overvalue

firms with overstated goodwill values in their balance sheet (Li & Sloan, 2017). To sum up, the

literature highlights that the underlying economic value of goodwill was better reflected prior

to the legislative change and before the annual impairment tests were implemented (Hamberg,

Paananen & Novak, 2009; Li & Sloan, 2017).

3.2 Abnormal cash flows

One of the reasons for the postponement of impairments could be the unfavorable effect on firm

value because it sends signals to the market about reduced expectations of future performance.

To delay these impairments firms engage in earnings management, through real activities, such

as manipulating cash flows (Filip, Jeanjean & Paugam, 2015) because of its importance when

calculating the fair value of goodwill. Managers manipulate real activities to avoid reporting

losses (Roychowdhury, 2006) and use their discretion and subjectivity to postpone recognition

of losses and thus inflate the performance of the company (Filip, Jeanjean & Paugam, 2017;

Jarva, 2009; Ramanna & Watts, 2012). Filip, Jeanjean and Paugam (2015) extend the research

10

of firms carrying impaired goodwill and find a relation between upward cash flow manipulation

relative to firms not carrying impaired goodwill.

Similar as Filip, Jeanjean and Paugam (2015), a study by Greiner (2017) found aggressive cuts

in R&D, discretionary expenses, to be associated with changes and higher levels of cash

holdings for companies. A finding corroborated by the study of Graham, Harvey and Rajgopal

(2005) who found that 80% of executives are prepared to reduce R&D costs in order to meet

earnings thresholds. Roychowdhury (2006) argue that earnings can be increased by selling off

inventories to meet demand or reducing COGS by overproducing inventory. In line with this

argument Cohen and Zarowin (2010) highlight that overproduction gives managers the

opportunity to spread fixed overhead costs over a larger number of units, thus lowering fixed

costs per unit. The total cost per unit is argued to decline as long as any increase in marginal

costs does not offset the reduction in fixed cost per unit (Roychowdhury, 2006), a procedure

argued to decrease reported COGS in favor for increased reported earnings. Cohen and Zarowin

(2010) highlight that firms still incur alternative production and holding costs that lead to

increased production costs compared to sales, which lead to reduced cash flows from operations

given the relative sales level. However, cutting discretionary expenditures will lead to increased

cash flows, due to the fact that such expenses will increase current periods earnings (Cohen &

Zarowin, 2010). The study by Roychowdhury (2006) shows that firms can increase earnings by

reducing discretionary expenses, especially the reduction of reported expenses. Further,

Roychowdhury (2006) argue if the reduction in discretionary expenses are conducted to meet

earnings targets the firms should exhibit uncustomary low discretionary expenses.

Kothari, Wysocki and Shu (2009) argue goodwill impairment is subject to a magnitude of

manipulations due to the permitted subjectivity in the accounting standards. Further, it is argued

managers use their given discretion to withhold bad news from outsiders and that auditors

accept a certain degree of optimism in the estimations from managers if the forecasts are

consistent with the current level of cash flows. Pertaining to goodwill, a survey from KPMG

(2014) showed goodwill to be relevant for outsiders to assess the financial outcome of

managerial decisions and to be able to hold management accountable for their capital allocation

decisions.

It is highlighted by Penman (2006) the preferred method to use when preparing an impairment

test is the DCF model. The factors affecting the outcome of the test constitutes of growth

assumptions, the used discount rate, short term growth, estimated profit margins, if the model

extrapolates data and the assumption used for terminal growth. As a consequence, auditors may

challenge the initial forecast for the current years' operating cash flows used in the DCF model

due to the material impact it has at the end of the time horizon for the forecast (ibid.). Since the

DCF model is used to test for impairment indication the present study considers the model to

have a direct link to operating activities and the final impairment decision.

A theme in the literature regards the postponement of impairments which are showed to be

detrimental for investors due to a loss of critical informative signals (Chen, Shroff & Zhang,

2014; Filip, Jeanjean & Paugam, 2015; Schatt, Doukakis, Bessieux-Ollier & Walliser, 2016).

11

It is argued when companies perform an impairment it sends signals that the benefits from those

assets has expired and thus indicates a decline in revenue from those assets (Li & Sloan, 2017).

However, it is argued by Rockness, Rockness and Ivancevich (2001) the effects on financial

results from goodwill impairment is significant in years of impairment and the impairment

charges are prone to be shifted between periods to achieve desired targets. The study by Jarva

(2009) investigates a sample of non-impairing companies with indications that the assets are

impaired but fails to find evidence of opportunistic postponement of impairment. In contrast,

the study by Ramana and Watts (2012) finds evidence that non-impairment is increasing in the

presence of managerial incentives such as for example CEO compensation, CEO reputation and

debt covenants tied to financial performance.

In order to avoid a goodwill impairment despite impairment indication the current cash flows

need to support the non-impairment which is argued to be a motivator for managers to

artificially inflate the current cash flows according to the agency theory (Cohen & Zarrowin,

2010; Graham, Harvey, & Rajgopal, 2005; Jensen & Meckling, 1976; Ramanna & Watts, 2012;

Zang, 2012). As a consequence, the present study examines abnormal cash flows because

current cash flows can be increased by a faster collection of account receivables, inventory

reduction, stretching payables to suppliers and by reducing operational expenses (Cohen &

Zarovin, 2010; Zang, 2012).

Previous studies have shown managers' ability to decrease R&D expenditure increases when

firms have earnings considerations (Dechow & Sloan, 1991; Graham, Harvey & Rajgopal,

2005). The article by Canace, Jackson and Ma (2018) highlight R&D-intensive firms also

account significant amounts of capital expenditure, which is argued to present managers with

the opportunity of shifting expenses between the two categories in case of an earnings shortfall.

A theme in prior studies has regarded the usage of R&D reductions to increase earnings in the

short term, which can decrease the firm value in the long run (Canace, Jackson & Ma, 2018;

Graham, Harvey & Rajgopal, 2005). Canace, Jackson and Ma (2018) argue that unspent R&D

resources are spent on capital expenditure to offset the long-term negative effects. The

managerial incentives toward meeting the current year's earnings threshold, and the fact that

their job security and reputation depends on the long-term financial performance, affects

managers willingness to shift expenses (Fama, 1980).

The effect of shifting R&D expenses to capital expenditures is that instead of being recorded

as an expense in the income statement the capital expenditure is expensed as an asset in the

balance sheet (IFRS, 2018). Kothari, Languerre and Leone (2002) argue the shifting of R&D

expenses to be subjective due to the difficulties in determining the future benefits pertaining to

the assets, which is not helpful for outsiders' investment decisions. Further, it is argued that

capital expenditures are associated with higher future stock returns and lower variability in

earnings (ibid.). Since the shifting of R&D expenses to capital expenditure has a direct impact

on a firm's earnings, the present study assume managers are prone to alter these expenses in

line with the predicted utility maximization of the agency theory (Filip, Jeanjean & Paugam,

2015; Jensen & Meckling, 1976; Ramanna & Watts, 2012). The idea is corroborated and

extended by Filip, Jeanjean and Paugam (2015) who highlight that investments in capital

12

expenditures could be affected by the managerial willingness to avoid recording the economic

impairment. Thus, capital expenditure can be exposed to earnings management due to that

reduction in capital expenditures improves the free cash flows that are used in the valuation

models to determine impairment indications.

3.3 Incentives to manipulate earnings

The literature highlights managerial incentives to be a contributing factor of managing goodwill

impairment disclosures (Cohen & Zarowin, 2010; Filip, Jeanjean & Paugam, 2015; Ramanna

& Watts, 2012; Roychowdhury, 2006; Zang, 2012). Ramanna and Watts (2012) found evidence

which indicated if managers compensation is based on the profit and loss of the company the

incentives inspire to postpone goodwill impairment. Bergstresser and Philippon (2006) argue

managers can be encouraged to exploit their discretion in reported earnings if their incentives

are tied to the company stock price. Their study shows incentivized managers to be a

contributing factor for earnings management and years of high accruals are found to be

correlated with significant option exercises by managers. In addition to this, a theme in the

literature highlights CEO tenure as an influencing factor for opportunistically reported earnings

(Ali & Zhang, 2015; Cheng, 2004; Dechow & Sloan, 1991). The study by Ali and Zhang (2015)

finds that earnings overstatement is greater at the beginning of the service period of a CEO

compared to the later years of service, due to the willingness of CEOs to convince outsiders of

their capabilities. Further, the results are robust when controlling for other earnings

management measures, such as abnormal discretionary expenditures, namely R&D.

Within the framework, developed by standard setters, it is expected managers will, on average,

use judgment and assumptions while estimating the fair value of goodwill in order to transfer

private information associated to future cash flows (Filip, Jeanjean & Paugam, 2015). On the

other hand, the agency theory challenge this view by predicting managers, on average, will

utilize goodwill accounting rules, due to its unverifiable nature, to opportunistically tamper the

financial reports to fit their private incentives (Filip, Jeanjean & Paugam, 2015; Jensen &

Meckling, 1976; Ramanna & Watts, 2012). In addition, the real activities management behavior

has gained traction as an agency problem due to that managers modify the underlying operations

to disguise the true performance (Cohen & Zarowin, 2010; Graham, Harvey, & Rajgopal, 2005;

Zang, 2012). Because the value of goodwill is estimated with discounted projected cash flows

managers may have incentives to manipulate cash flows to delay goodwill impairments (Filip,

Jeanjean & Paugam, 2015). One of the reasons behind postponing impairments is the audit

process of impairment testing (Filip, Jeanjean & Paugam, 2015). Both auditors and financial

analysts can be seen as financial gatekeepers between users of financial information and the

reporting entity (ibid.). The gatekeepers will review the information disclosed by firms' by

evaluating the feasibility of estimated future cash flows based on current cash flows. Thereby,

managers will have incentives to manage cash flows in different ways to make their estimate

more reliable because if current cash flows are high auditors will perceive large future cash

flows as more reasonable (ibid.). Also, Roychowdhury (2006) argues managers have incentives

to manipulate real activities, e.g. R&D expenditures, which affects cash flows in order to meet

certain earnings targets.

13

3.3.1 Analysts and earnings thresholds

As earnings management can be used to govern earnings (Graham, Harvey & Rajgopal, 2005;

Roychowdhury, 2006) it could be used as a tool to beat analysts' forecasts. Analysts can be

considered as gatekeepers (Filip, Jeanjean & Paugam, 2015) and external monitors of managers

(Jensen & Meckling, 1976) because they have the task of providing the market with

information, containing public forecast with future earnings and cash flows, which also are

reflected in their recommendation and target prices (Bonini, Zanetti, Bianchini & Salvi, 2010;

Simon & Curtis, 2011). If these analyst recommendations or ratings are unfavorable Abarbanell

and Lehavy (2003) show managers have weak incentives to manipulate earnings in order to

meet earnings expectations. Consequently, favorable analyst recommendation or ratings tend

to encourage more earnings management activities to meet these expectations (Madhogarhia,

Sutton & Kohers, 2009).

Graham, Harvey and Rajgopal (2005) argue analysts influence on stock share prices is

perceived by managers as an important factor. As a result of this, their coverage can be

considered responsible for creating immoderate pressure on managers to engage in earnings

management activities (Yu, 2008), called the pressure hypothesis (Hong, Huseynov & Zhang,

2014). Those firms who miss analyst forecasts usually suffer significant declines in their stock

price (ibid.), where firms with growth opportunities are penalized more by the market when

these earnings thresholds are not fulfilled (Skinner & Sloan, 2002). Accordingly, managers are

sometimes willing to sacrifice economic value in order to meet a short run earnings target

because of the market's severe reactions (Graham, Harvey and Rajgopal, 2005). On the

contrary, analysts' incentives and governance role could be affected by the pressure from a

variety of sources (Yu, 2008). These pressures include the need to pursue investment banking

business (ibid.) and to please management and thus obtain greater access to managers' private

information (Lin & McNichols, 1998). Hence, managers seeking to increase the number of

analysts covering the firm could, therefore, choose to disclose more inside information and put

greater emphasis on management communication (Graham, Harvey & Rajgopal, 2005).

Even though Hughes and Ricks (1987) conclude analysts' earnings forecasts can be a poor proxy

for market expectations, researchers often use analysts' earnings forecasts in accounting and

finance literature (Eames & Kim, 2012). Burgstahler and Eames (2003) are unable to present

evidence suspect firms manipulate earnings in order to avoid minor losses, but the result show

analysts have the ability to predict earnings management activities. Further, Yu (2008) found

firms with lower analyst coverage exhibit higher incoherence around earnings targets in

comparison with firms with high coverage, which suggests that firms followed by more analysts

manage their earnings to a lesser extent. The finding is corroborated by Ali and Zhang (2015)

who found earnings overstatement to be less frequent in firms with stronger monitoring and

analyst coverage. Also, the existing literature has shown analysts tend to cover firms with better

information environment (Yu, 2008) which could be interpreted as analysts choose to cover

firms with fewer earnings management activities. On the other hand, analysts following firms

can have a dampening effect because they can see through such unethical activities and thereby

reduce their opportunity to manipulate earnings (Graham, Harvey and Rajgopal, 2005).

14

3.3.2 Growth opportunities

A firm's total value is composed of the sum of the total value of assets in place and growth

opportunities or expected future investments (AlNajjar & Riahi-Belkaoui, 2001).

Consequently, the lower the proportion of assets in place representing the firm's total value, the

higher are the growth opportunities for a given level of firm value (ibid.). That is also why

growth opportunities constitute a significant part of the market value of equity (Pindyck, 1988).

When firms have free cash flow surplus investors expect managers to invest these and in order

to maximize firm value (Jensen, 1986). With fewer growth opportunities, managers are more

likely to invest these cash flows in unprofitable projects (Chung, Firth & Kim, 2005). Thus,

when firms have high free cash flows in combination with low growth opportunities agency

problems can arise because they can be used in a way that not maximize shareholders' wealth.

Also, Chung, Firth and Kim (2005) show that firms with high free cash flow and low growth

opportunities tend to manipulate earnings in order to report better financial information.

Inconsistent with the agency view, Li and Kuo (2017) show that, on average, managers with

equity pay engage in earnings management activities. The result indicates growth opportunities

can mitigate the positive relationship between earnings management and equity pay at the same

time equity pay align managers' incentive more effectively for firms with greater growth

opportunities. In these firms with high growth Watts and Zimmerman (1986) argue managers

are more likely to have opportunistic behavior. In addition, Smith and Watts (1992) highlight

that the literature indicates managers' incentives increase in firms with greater growth

opportunities because such firms often have more convex executive pay contracts which will

result in more benefits when the opportunities are utilized. This means the economic benefit of

maximizing firm value by motivating managers outweighs other alternatives and firms with

growth opportunities are less likely to manipulate earnings (Li & Kuo, 2017). This argument is

in accordance with previous result (see Madhogarhia, Sutton & Kohers, 2009), which shows

managers in growth firms manipulate earnings upward and downward more aggressively in

comparison with managers in value firms.

A study by Avallone and Quagli (2015) finds that the variable growth rate manipulation has a

significant explanatory value for managers' postponement of goodwill impairment. The study

presents evidence that higher growth rates are used to manage impairment tests and thereby

avoid or postpone goodwill impairment. Furthermore, even though Roychowdhury (2006) finds

evidence that growth opportunities are positively associated with real activities manipulation,

such activities can have negative effects on future performance of a firm due to the measures

taken to increase the profit of the current period (Caruso, Ferrari & Pisano, 2016; Filip, Jeanjean

& Paugam, 2015; Huang & Sun, 2017; Roychowdhury, 2006).

3.4 Asymmetric information

The literature indicates subjectivity in financial accounting has increased after the transition to

IFRS, especially regarding the rules for impairment tests (Caruso, Ferrari & Pisano, 2016). Li

and Sloan (2017) argue increased subjectivity can decrease reliability and transparency of

financial statements and work as a catalyst for information asymmetry between outsiders and

insiders. The research applies the information asymmetry aspect to goodwill where it is argued

15

opportunistic postponement of impairments can increase the information asymmetry due to the

loss of critical signals about the future performance of the firm (Filip, Jeanjean & Paugam,

2015). Public information is information known by investors which are used to alter their

assumptions about future cash flows and earnings (Schatt, Doukakis, Bessieux-Ollier &

Walliser, 2016). Consequently, investors are considered to be in a position of information

disadvantage in relation to managers about the economic value of goodwill (Filip, Jeanjean &

Paugam, 2015).

Schatt, Doukakis, Bessieux-Ollier and Walliser (2016) argue impairment disclosures send

signals to investors that future cash flows or earnings will come in short compared to the

expectations at the initial goodwill activation. However, it is argued in the literature increased

level of disclosures may contribute with benefits in terms of a more stable stock and a decreased

bid-ask spread of the company stock (Leuz & Verrecchia, 2000). A study by Richardson (2000)

found that earnings management increases in the presence of information asymmetry, especially

significant are income increasing activities. This is in line with the study by Leuz and

Verrecchia (2000) which showed increased disclosures limits the extent of earnings

management.

The literature indicates asymmetric information is higher in R&D intensive firms (Aboody &

Lev, 2000). Aboody and Lev (1998) argue increased disclosure about R&D operations might

mitigate the possibilities for opportunistic actions since it is a part of real activities earnings

management. Schatt, Doukakis, Bessieux-Ollier and Walliser (2016) argue impairment of

goodwill is not always deemed as reliable information to change investors perception and may,

therefore, be seen as useless information. Furthermore, Vanza, Wells and Wright (2018) show

no evidence of information asymmetry being the motivator for the recognition of asset

impairments. However, the consensus of the literature highlights managerial incentives are

influential for financial disclosures, which are influential for information asymmetry (Chen &

Liu, 2013; Schatt, Doukakis, Bessieux-Ollier & Walliser, 2016). Increased level of information

in financial disclosure can, therefore, reduce the information gap between insiders and outsiders

of the company resulting in a transparent capital market (Jo & Kim, 2008).

Further, impairment of goodwill can provide useful information for investors if they are not

able to independently formulate expectations about future earnings and when reliable numbers

are provided by management (Schatt, Doukakis, Bessieux-Ollier & Walliser, 2016). Also,

unlike amortization, impairment of goodwill should provide financial statements users with

more and greater inside information if implemented correctly (Seetharaman, Sreenivasan,

Sudha & Yee, 2006). In this context, the information content from goodwill impairment can

result in a distribution shift from managers private information to public information (ibid.).

Under the assumption managers have incentives not to disclose reliable information to

investors, goodwill impairment could convey useful information to investors if a mechanism

which forces reliable information is present (ibid.). The impairment of goodwill can, therefore,

be helpful to investors, in some cases, as a tool to revise their expectations about the future

performance of a company. In other cases, impairments may be useless due to investors ability

16

to revise their expectations in line with public information or due to mistrust of accounting

numbers provided by dishonest managers (ibid.).

3.5 Summary and hypotheses development

The reasons for postponing goodwill impairments could pertain to unfavorable effects on

company value, due to reduced expectations of future performance. To delay the unfavorable

effects firms engage in earnings management, through real activities, such as cash flow

manipulation (Filip, Jeanjean & Paugam, 2015) because of its importance when calculating the

fair value of goodwill which is used in the impairment test (Roychowdhury, 2006). Managers

have been found to use their given discretion and subjectivity to avoid reporting losses, thus

inflating the performance of the company (Filip, Jeanjean & Paugam, 2015; Jarva, 2009;

Ramanna & Watts, 2012). Real activities manipulation such as R&D can be reduced to meet

earnings thresholds and overproduction can reduce the fixed costs per unit thus lowering the

COGS (Cohen & Zarowin, 2010; Roychowdhury, 2006). The hypothesis H1 builds on the idea

that firms carrying impaired goodwill in their balance sheet, manipulates cash flows from real

activities upwards compared to firms not carrying impaired goodwill in their balance sheet. The

hypothesis is stated as follows:

H1: Firms with an indication of economic impairment manage current cash flows from real

activities upwards in order to avoid goodwill impairment.

Apart from real activities, cash flows can also be managed in the operating activities of the firm.

The accounting standards permit subjectivity in goodwill calculations which present managers

with an opportunity to manipulate impairment tests (Kothari, Wysocki & Shu, 2009). The

preferred method for preparing impairment tests is to use the DCF model where estimations of

growth, discount rate and profit margins are used (Penman, 2006). Further, auditors accept a

certain degree of optimism in the estimations from managers if the forecasts are consistent with

the current level of cash flows (Kothari, Wysocki & Shu, 2009), which is argued to be a

motivator for managers to artificially inflate the current cash flows (Cohen & Zarrowin, 2010;

Graham, Harvey & Rajgopal, 2005; Jensen & Meckling, 1976; Ramanna & Watts, 2012; Zang,

2012). The hypothesis H2 builds on the idea that current cash flows are manipulated by a faster

collection of account receivables, inventory reduction and reduction of operational expenses.

The hypothesis is stated as follows:

H2: Firms with an indication of economic impairment manage current cash flows from

operating activities upwards in order to avoid goodwill impairment.

Building on hypotheses H1 and H2, managers can shift expenses between R&D and capital

expenditures (CAPEX) which has a direct impact on a firm's earnings due to the recognition of

assets rather than expenses in the income statement (IFRS, 2018). The willingness of managers

to decrease R&D expenditure increases when firms have earnings considerations (Dechow &

Sloan, 1991; Graham Harvey & Rajgopal, 2005). Investments in CAPEX can be affected by

the managerial willingness to avoid recognition of economic impairment due to that CAPEX is

used in the valuation models to determine impairment indications (Filip, Jeanjean & Paugam,

17

2015). The hypothesis H3 builds on the idea that CAPEX can be exposed to earnings

management due to that reduction in CAPEX improves the free cash flows. The hypothesis is

stated as follows:

H3: Firms with an indication of economic impairment manage current free cash flows upwards

in order to avoid goodwill impairment.

Analysts can be considered as gatekeepers and external monitors of managers (Filip, Jeanjean

& Paugam, 2015; Jensen & Meckling, 1976) because they provide the market with information

containing public forecasts with future earnings and target prices (Bonini, Zanetti, Bianchini &

Salvi, 2010; Simon & Curtis, 2011). As depicted in hypotheses H1, H2 and H3, earnings

management can be used to govern earnings and be used as a tool to beat analysts' forecasts

(Graham, Harvey & Rajgopal, 2005; Roychowdhury, 2006). Further, favorable analyst

recommendations tend to encourage earnings management through current cash flow

manipulation to meet these expectations (Madhogarhia, Sutton & Kohers, 2009) and

unfavorable recommendations give managers weak incentives to manipulate earnings

(Abarbanell & Lehavy, 2003). Firms with lower analyst coverage are found to exhibit higher

incoherence around earnings targets in comparison with firms with high coverage, which

suggests that firms followed by more analysts manage their earnings to a lesser extent. Also,

the existing literature has shown analysts tend to cover firms with better information

environment (Yu, 2008) which could be interpreted as analysts choose to cover firms with fewer

earnings management activities. The hypothesis H4 builds on the idea that analyst coverage has

an impact on earnings management. The hypothesis is stated as follows:

H4: Analyst coverage has a significant impact on earnings management through current cash

flow manipulation.

The total value of a firm is composed of both the value of total assets, future growth

opportunities and investment needs (AlNajjar & Riahi-Belkaoui, 2001). Consequently, when a

lower proportion of assets are representing the firm's total value, a higher proportion of growth

opportunities constitutes the firm value (ibid.). The managerial incentives can increase in firms

with greater growth opportunities because such firms often have more convex executive pay

contracts, thus giving the manager fewer motives to manipulate earnings (Li & Kuo, 2017).

Connecting to all the previous mentioned hypotheses cash flow manipulations are conducted to

e.g. inflate firm value. Firms' growth rates are found to be used in order to manage impairment

tests and to avoid or postpone impairment recognition. We interpret such a result as an

indication that firms with high growth don't have incentives to manipulate impairment tests

because current high growth will function as a good enough basis to support future growth. The

hypotheses H5 builds on the idea that growth opportunities have an impact on cash flow

manipulation. Thus, the hypothesis is stated as follows:

H5: Growth has a significant impact on earnings management through current cash flow

manipulation.

18

3.6 Criticism to precedent literature

Consensus exists among the presented literature about the difficulties in capturing earnings

management, especially real activities earnings management (Cohen, Dey & Lys, 2008; Huang

& Sun, 2017). The literature presents several methods for the measuring of real activities

manipulation (see Cohen, Dey & Lys, 2008; Filip, Jeanjean & Paugam, 2015; Ramanna &

Watts, 2012) where it is argued Roychowdhury's (2006) model captures both income increasing

and decreasing activities. A majority of the studies presented have been conducted in a different

geographic setting compared to the present study which can limit the possibilities to draw

conclusions regarding the alignment with other geographical jurisdictions. A critique could be

raised towards the presented literature which includes studies predating the IFRS transition.

The fact is acknowledged by the authors and used to form the theoretical knowledge of the

study.

A general criticism lifted in several studies (see Hamberg, Paananen, Novak, 2009; Hirschey &

Richardson, 2003; Li, Shroff, Venkataraman & Zhang, 2011; Li & Sloan, 2017) is the increased

subjectivity that the transition to the IFRS framework has contributed with, especially the fair

value estimations and DCF calculations. The ongoing drive for harmonization of accounting

standards is critiqued due to the possibility for managers to exercise their given discretion and

use their expert knowledge about the firm, which macerates the accounting quality (Ewert &

Wagenhofer, 2005; Healy & Wahlen, 1999). A critique lifted in the literature is that earnings

management is a product of managerial discretion and that less interference of managerial

judgment would increase the accounting quality (Callao & Jarne, 2010). Finally, the presented

literature consists of several studies highlighting different forms of earnings management and

impairment than the investigated forms in the present study. In line with the approach of pre-

IFRS studies, the literature has been used to build a foundation of earnings management through

goodwill impairment.

19

4. Method

Chapter four gives a description of how the study approached the collection of data and the

matching process of firms. The formulas used for measuring earnings management are

disclosed and a regression model is presented. Finally, the chapter gives a critical discussion

of the chosen method and the qualitative consequences of the study's methodological choices.

4.1 Research Design

The focus of this study is on how managers in firms, under IFRS, use real activities to avoid or

postpone goodwill impairments. In order to fulfill the purpose of the study, the study measures

if, and how, managers engage in earnings management through manipulation of cash flows,

which have a direct impact on the valuation process of goodwill in impairment tests and the

qualitative characteristics of financial reporting. To enable the investigation of such activities

the study identified firms carrying impaired goodwill in their balance sheet. In the identification

of such firms', the study focused on firms with market indications of goodwill impairment, an

operationalization validated by previous studies (Beatty & Weber, 2006; Chen, Shroff & Zhang,

2014; Filip, Jeanjean & Paugam, 2015; Li & Sloan, 2017; Ramanna & Watts, 2012;

Roychowdhury & Martin, 2013) where firms' price-to-book ratio exceeds one. Roychowdhury

and Martin (2013) argue managers are likely to manipulate, especially boost earnings, when

there are indications of economic impairment, e.g. price-to-book ratio below one, in order to

postpone goodwill impairments. In addition, shorter periods of price-to-book ratios below one

could be a reflection of managers possession of private information, regarding goodwill's true

economic value, and therefore market inefficiency (Filip, Jeanjean & Paugam, 2015).

The present study used the price-to-book ratio as a measurement of economic impairment and

reported firm-level data were used due to that outsiders rely on firm-level market value as an

indicator to determine if book values are overstated (Filip, Jeanjean & Paugam, 2015; Ramanna

& Watts, 2012). At the firm-level, a price-to-book ratio below one for two successive years

indicates the market perceives that goodwill is economically impaired due to that the book value

is higher than the market value (ibid.). When impairment indications are present but not reduced

to equal the market value, the value of the assets are overstated in the balance sheet. To control

for impairment indications and to gather all data, the study used the financial database Thomson

Reuters Eikon, through the excel-function. The functions used to collect the study's variables

can be seen in appendix A.

4.2 Sample method

All of the sampled firms are still or have been, listed on the Stockholm Stock Exchange during

the period 2011 to 2017. Due to the timing of the study, all of the investigated firms' annual

reports for 2018 had not yet been published, which limited the study to the latest fiscal year as

2017. To avoid noise from the financial crisis, where the median level of impairment was larger

(André, Filip & Paugam, 2016), this thesis excluded the period prior 2011 and collected data to

the last fiscal year of available and published data. To enable comparison between sectors

companies were assigned with sector identifiers through the Global Industry Classification

Standards (GICS), where firms were given a specific sector code between 10-60. Banks and

20

financial institutions were excluded in accordance with prior studies (see André, Filip &

Paugam, 2016; Filip, Jeanjean & Paugam, 2015; Ramanna & Watts, 2012; Roychowdhury,

2006; Zang, 2012) due to different business models and additional regulations by the financial

supervisory authority. The reasons for dividing the observations by sector, and not industry as

used in prior studies (see André, Filip & Paugam, 2016; Filip, Jeanjean & Paugam, 2015;

Ramanna & Watts, 2012; Roychowdhury, 2006; Zang, 2012), was because of the statistical

requirement of having at least ten observations per sector. The statistical requirement enabled

the study to apply cross-sectional calculations for each sector-year, whereas the dividing of

observations by industry code would have resulted in too few groups, thus obstructing the study

to achieve statistical results. To be able to test this study's hypotheses we required data regarding

goodwill for at least two consecutive years, during the whole period, and firms without booked

goodwill were sorted out from the sample. An additional requirement was that all sampled firms

should have data regarding price-to-book ratios for at least two consecutive years. Thus, firms

with missing values for price-to-book ratios or firms lacking booked goodwill in their balance

sheets were excluded.

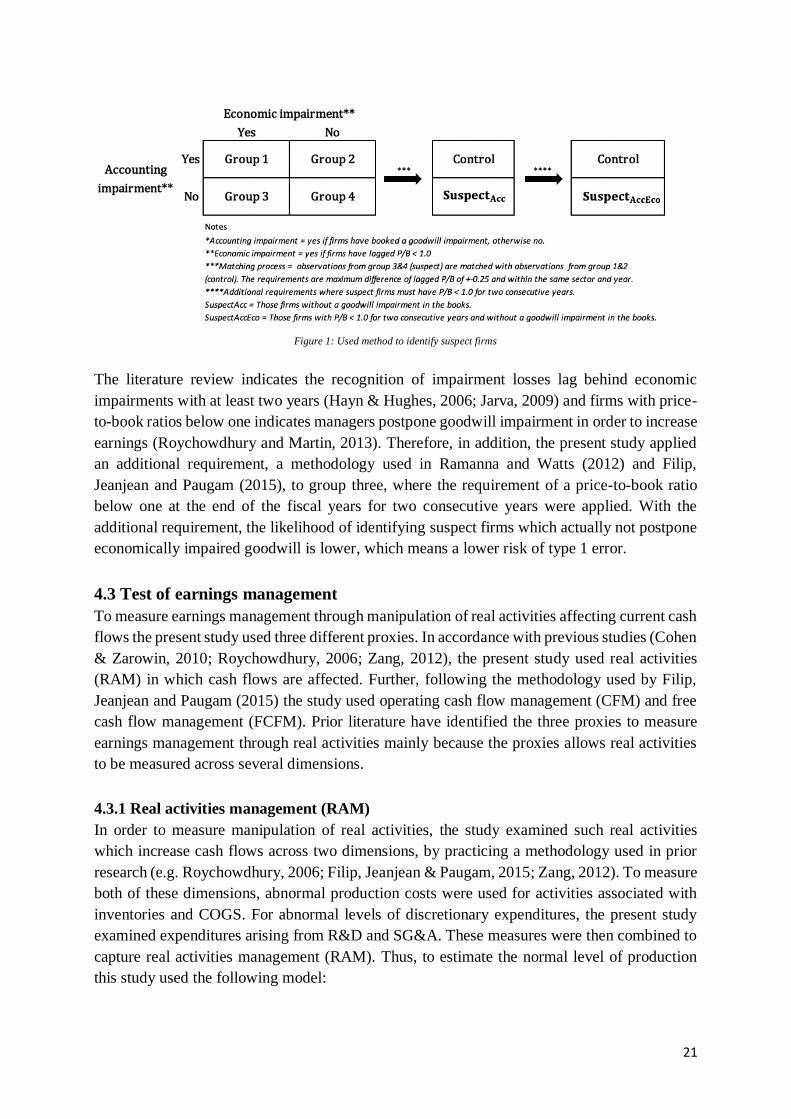

In order to identify suspect firms, the ones carrying impaired goodwill forward and have not

yet recognized an impairment, we used price-to-book ratios because investors, analysts and

researchers often use this measurement as a proxy at firm-level when they evaluate if booked

values are overstated (Chen, Schroff & Zhang, 2014; Ramanna & Watts, 2012; Roychowdhury

& Martin, 2013). First, we divided our sample into two groups, based upon whether or not they

have booked an impairment or not. Then we applied the requirement of indications of economic

impairment to separate these two groups into four (see figure 1). As an indicator of firms that

should impair goodwill, the present study used previous fiscal year (lagged) price-to-book ratios

below one in (see Beatty & Weber, 2006; Ramanna & Watts, 2012) which have found price-

to-book ratios to be an important indicator of potential goodwill impairment. The present study

followed the methodology presented by Filip, Jeanjean and Paugam (2015), where firms which