Embed Size (px)

Citation preview

SUSTAINABLE WATER INFRASTRUCTURE

MARCH 2017 |

COLUMBIA UNIVERSITY

SOURCE: FOOD AND AGRICULTURE ORGANIZATION OF THE UNITED NATIONS, 2011

Global distribution of physical water scarcity by major basin (2011)

Note: The map shows the global distribution of water scarcity by major river basin based on consumptive use of water in irrigation.

Worldwide Water Scarcity

Objectives

Water Infrastructure

Emerging Water Technologies

Water Markets

International Case Studies

Objectives

Examine freshwater infrastructure and energy related technologies to forecast potential areas for investment.

Objectives

Water Infrastructure

Emerging Water Technologies

Water Markets

Case Studies

Water Infrastructure Current Condition

Most of the drinking water infrastructure in the U.S. was built in the post-World

War II era, over 50 years ago, with some of it having been in the ground for

more than a century. Northeast and Midwest Large Water Systems are the

oldest.

Large:

> 50,000 ppl

Medium:

10,000-49,999 ppl

Small:

3,300 – 9,999 ppl

Very Small:

< 3,300 ppl

DATA SOURCE: AMERICAN WATER WORKS ASSOCIATION

Aging Water Infrastructure Reasons

Economic Reasons

- Lacking of capital: 30%-35% water infrastructure projects do not have enough

working capital to complete construction after engineers design them.1

- Large scale projects interrupt residents’ lives and generate extra costs,

especially in big cities.

Political Reasons

- New technologies for water infrastructure have been in existence for 15-20

years, but some municipalities don’t want to use them. E.g. New York City and

Los Angeles city do not allow the use of plastic pipes in water applications.1

a) Engineers have old mentality and do not have experience using new materials

b) People do not pay attention to underground pipes until some incident occurs and are not

promoting change

c) Some unions, e.g. iron and steel unions, very strong political organizations with

extensive lobbying budgets to maintain high levels of employment for members.

- Each state has 2-7 water agencies and they function autonomously.2

1. INTERVIEW WITH JMEAGLE’S CEO & CHAIRMAN MR. WALTER WANG2. WATER WEBSTER STATE WATER AGENCIES

Water Infrastructure Capital Need

Estimated total replacement costs for water pipes in the U.S. add up to over $2.1

trillion and investment in water mains added up to over $1.7 trillion through

2050. The system that needs the most capital are Medium & Small pipes in the

South.

0

100

200

300

400

500

600

NortheastLarge

NortheastMedium &

Small

NortheastVerySmall

MidwestLarge

MidwestMedium &

Small

MidwestVerySmall

SouthLarge

SouthMedium &

Small

SouthVerySmall

WestLarge

WestMedium &

Small

WestVerySmall

AggregateReplacementValue of Water Pipes(billions)

Water Utility Location and Size

Aggregate Replacement Value of Water Pipes in the U.S.

DATA SOURCE: AMERICAN WATER WORKS ASSOCIATION

Water Infrastructure Finance – National• Federal Level – “Water Infrastructure Finance and Innovation Act of

2014”(WIFIA)

• Issued by Environmental Protection Agency (EPA)

• > $1.0 billion in credit assistance & may finance > $2.0 billion in water

infrastructure1

• The new EPA Chief Scott Pruitt includes water structures in plans for

national infrastructure renewal2

1. UNITED STATES ENVIRONMENTAL PROTECTION

AGENCY (EPA)

2. BLOOMBERG BNA

Water Infrastructure Finance – Partnerships

• Federal-State Partnerships (EPA & States)

• The self-perpetuating loan assistance Clean Water State Revolving Fund (CWSRF) &

The Drinking Water State Revolving Fund (DWSRF) were established in 1987

• The nation's largest water quality financing source has provided $133 billion in low-

cost funding over the last 25 years, using a combination of federal and state funds1

• Public-Private Partnerships (P3s)

• Long-term contractual agreements between a public and private entities to provide

high quality services in a cost effective way, can leverage both the WIFIA and SRFs

• Water Finance Center under EPA performs research in water P3s and provides

technical assistance for projects2

It is hard to carry out P3s projects in the U.S. like in China because of different

political systems3

IdeasChina

• Selling a Package (Treatment Plant + Pipes)

U.S.

• Wastewater Trade

• Public – Infrastructure & Private – Equipment

1. UNITED STATES ENVIRONMENTAL PROTECTION AGENCY (EPA)

2. EPA P3S

3. INTERVIEW WITH JMEAGLE CEO&CHAIRMAN MR. WALTER WANG

U.S. Water System Violations

Lead and Copper Rule Violations1

• Safe Drinking Water Act passed in 1974

• 49 States have primacy, EPA retains

enforcement authority

• Lead and Copper Rule established in

1991 by EPA

• Regulates lead levels and testing of

high risk homes -15 ppb cutoff

• ~5,360 community water systems were in

violation in 2015

• Incorrect testing methods, failure to

report and treat contamination

• Over 18 million Americans live in these

communities

• EPA took formal enforcement measures in

only 11.2% of the 8,000 violations

• Only ~5% of violations were compliant

by 12/31/15

Community Water Systems in Violation of Lead and Copper Rule (2015)1

1. NRDC WATER REPORT 2016

Lead Action Level Exceedance

• 1,110 community water systems

exceeded 15 ppb1

• ~3,950,000 people

• Communities above 15 ppb are

underrepresented on this map due to

poor state monitoring and testing methods

• 33 cities have been accused of using

water testing cheats in determining lead

levels (Jun. 2016)2

• Major cities include Chicago, Boston,

Buffalo, and Philadelphia, which is

accused of having the worst water testing

in the U.S.2

• Testing methods such as pre-flushing

and running water slowly contributed to

the Flint, Michigan crisis

Community Water Systems that Exceed 15 ppb (2015)1Testing Methods

1. NRDC WATER REPORT 20162. THE GUARDIAN

Other Major Cities Requiring Investment

• PWSA (Pittsburgh Water and Sewer Authority) is investing $60.0 million in Pittsburgh’s water system in 20171

• In June 2016, top 10% of tested Pittsburgh homes had lead levels of 22 ppb, Flint was 20 ppb1

• December 2016, Top 10% was 18 ppb

• The city of Pittsburgh is planning to invest $1.0 million in facet filters to distribute to the city’s residents

• Pittsburgh Mayor Bill Peduto is searching for private investors to form a public private partnership with PWSA in

hopes of reducing debt levels and overhauling the city’s water infrastructure

Requirement for Infrastructure Investment

4. BOSTON GLOBE

5. BALTIMORE SUN

Pittsburgh Water Infrastructure

• New York: 14% of water school outlets outside of NYC showed lead levels of more than 15 ppb (Jan. 2017)2

• Governor Cuomo recently announced the Clean Water Infrastructure Act of 2017, invest $2.0 billion in

water infrastructure

• Estimates say that New York requires $80.0 billion over the next 20 years

• Wisconsin: ~176,000 lead service pipes and the cost of replacing them is between $511 and $756 million3

• Milwaukee plans to spend $6.8 million in 2017 to replace lead pipes (Jan. 2017)

• Massachusetts: 164 schools had at least one sample that was above the 15 ppb. (Nov. 2016)4

• Baltimore: 4% of all samples taken from a Baltimore water survey in 2016 were above 15 ppb (Apr. 2016)5

1. PGH2O.COM

2. SYRACUSE NEWTIMES

3. WISCONSINWATCH.ORG

“Nothing is more useful than water: but it will purchase scarce anything; scarce anything can be had in exchange for it. A diamond, on

the contrary, has scarce any use-value; but a very great quantity of other goods may frequently be had in exchange for it.”

— Adam Smith, Chapter 4, Book I, Wealth of Nations (1776)

Pricing of Water1

• Key difference between water and other commodities is the lack of sufficiently accurate price signals

determined by the forces of supply and demand

• Regulators require that monopolistic suppliers charge prices that cover the cost of delivery – cost does

not include scarcity price. This results in administrative cost far lower than value of water or cost of a

shortage

• Survey of 30 metropolitan regions in the United States found that cities in rain-scarce regions have the

lowest residential water rates and the highest level of water use

The Economics of Water Scarcity

1. DAVID ZETLAND – INTERVIEW, MARCH 2017

2. TABLE DATA: USGS

Transaction Overview

• The plant produces approximately 50 million US gallons (190,000 m3) of fresh water per day

• Operating cost of $49 million to $59 million a year. It will provide about 7% of the potable water needs

for the San Diego metropolitan area

• The cost of water from the plant is roughly $.03-$.06 more per gallon than recycled water, $.31-$.34

more than reservoir water, but $.03 to $.06 less than importing water from outside the county

• However, San Diego still imports roughly 90% of its water, leaving potential opportunities for

further water infrastructure investment in an area not without significant demand

Efficacy of the Project

Bayonne, NJ – P3 Concession

• December 21, 2012 – Bayonne Municipal Utilities Authority (“BMUA”) took part in Public-

Private Partnership with United Water (dba Suez) and KKR for a 40-year concession

• In 2012, BMUA increased rates 27%, resulting in decreased revenue due to conservation

efforts on the part of customers

• A major barrier for proceeding with the P3 concession approach was BMUA’s double-digit

debt burden coupled with the significant necessary capital and maintenance needed to

update infrastructure

• Under the deal terms of the 40-year contract, United Water (dba Suez) formed a joint venture

with KKR to form the Bayonne Water Joint Venture

• The transaction was structured with a $150 million upfront concession payment coupled with

annual $500,000 concession fees

• BMUA issued roughly $110 million in privately placed taxable bonds with a November 2037

maturity and a 5.07% coupon

• KKR-Suez provided $63.8 million in equity in order to finance BMUA’s upfront payment and

initial capital obligations, with KKR accounting for 90% of the total position

Transaction Overview

• Customers would be forced to absorb the bulk of the price increase over the first year

• Deal structure designed to lock in fixed rate increases over the 40-year life

• Structure included a 2-year rate increase freeze as well as a 4th year 3.5% fixed rate

Revenue Path Model

Initial based year 2011 revenue has

been set at $20,639,000 as per the

BMAU Agreement

$20.6 mm

2011 Revenue

2013-2014

Rate Freeze Period

For the period covering 2013-2014 rates

will be fixed

Rates increase by 8.5% initially and then

remain flat in 2013 and 2014, increasing

3.5% in 2015

$26.3 mm

2015 Revenue

$19.4 mm

$6.9 mm

2015 Fixed

Revenue

2015 Inflation

Linked Revenue

2015-2052

2015-2052

~3.5% from 2015-2021

3.75% thereafter

20% at the Labor Adjustment Index plus

(i) 1.0% per year during 2015 to 2021 and

(ii) 1.25% per year thereafter

10% at the Standard Adjustment Index

plus (i) 1.0% per year during 2015 to

2021 and (ii) 1.25% per year thereafter

Objectives & Deliverables

Water Infrastructure

Emerging Water Technologies

Water Markets

Case Studies

Permian Basin

• Total wells: 14,662

• Total water usage: 63.6 billon gallons

Eagle Ford Shale

• Total wells: 14,687

• Total water usage: 82.1 billions gallons

DJ Basin

• Total wells: 7,376

• Total water usage: 17.0 billons gallons

California Basin

• Total Wells: 2,649

• Total water usage: 0.3 billons gallons

Approximate % of wells in high and

extreme water stress:

• Permian Basin ~69%

• California Basin 99%

• Eagle Ford 89%

• DJ Basin 100%

Shale Basins & Water Scarcity

Basin Statistics1

The average shale well in the United States requires roughly 71 - 119 thousands barrels of water to hydraulically fracture depending on location1

1. CERES2. U.S. GEOLOGICAL SURVEY

1. Where will operators in water scarce areas continue to get their freshwater for fracking operations?• Majority of shale producers are highly dependent on ground water resources for their fracking operations

2. What will operators do with their produced water from their exploration and production operations?

• The national weighted average is 9.2 barrels of produced water for every barrel of crude and 97 barrels of produced water for every million cubic feet of natural gas1

O&G Water Problems & Plays

Two Water Problems

Marcellus, Eagle Ford, and Permian

Marcellus

• Surface water accounts for 63% of water used, municipalities & recycled water account for 20% & 18% respectively2

• Companies operating in the Marcellus play typically recycle 80-90% of their waster water3

• Factors include seven state permitted disposal wells and high trucking costs of waste water to Ohio

Eagle Ford

• Approximately 90% of water used in fracking is sourced from fresh groundwater,, in some counties consumption

exceeds recharge rates by a 2.5x factor4

• Majority of operators use disposal wells due to their abundance and low cost

Permian

• Operators source roughly 100% of their water from fresh and brackish aquifers due to low cost5

• Majority of operators use disposal wells due to low costs and abundance

4. BUSH SCHOOL OF GOVERNMENT

REPORT

5. TEXAS UNIVERSITY REPORT

1. GROUND WATER PROTECTION COUNCIL 2015

2. STATE IMPACT NPR

3. PENN STATE REPORT

Fracking Water Economics

Costs Of Recycle Technology

• Halliburton electrocoagulation procedures have been cited at costing roughly between $1.68 to $1.89 per barrel3

• Ecosphere Energy Services provides on-site treatment for roughly $0.3- $0.5 per barrel, trucking and disposal fee costs $1 per barrel3

• Basic Energy Services estimates cost of recycling produced water at roughly $0.1 - $1.5 per barrel4

• Veolia: building Antero a $275 million treatment plant, $150,000 expected savings per well5

• Halliburton: saved Permian basin operator more than $500,000 using Cleanwave6

4. INTERVIEW WITH BASIC

5. WATER ONLINE

6. HALLIBURTON CASE STUDY

Produced Water Industry

• The current market for treating produced water is estimated to exceed $4.3 billon for the next five years and is

expected to grow at a 6.8% CAGR annually. The is expected to reach $8.56 billion by 2025.2

Water Costs

• Water treatment and disposal is extremely costly to E&P companies; typically produced water management

technology is categorized as minimization, recycle reuse, or disposal.

• Purchasing freshwater is expensive and total costs can range between $0.75 and $9.75 per barrel.1

• Disposal of produced water is expensive and can cost between $1.00 and $17.00 per barrel, this includes trucking

costs.1

1. EP MAG

2. GLOBAL PRODUCED WATER TREATMENT REPORT

3. BREAKING ENERGY

Pressure

• Due to the increasing water scarcity, desalination

has become an important source of fresh water,

especially for human consumption and

agriculture.

• Global desalinated water production amounts to

90 million m3, equivalent to 1% of global water

supply.

• Reverse Osmosis is the dominant technology for

desalination accounting for 63% of the installed

capacity around the world3.

RO Membrane Separation Mechanism

Reverse Osmosis (RO)1

Normal Osmosis

Reverse Osmosis

High salinity water

Membrane and water movement

1. ECONOMIC EVALUATION OF SEAWATER DESALINATION, SAUD MOHAMMED H BIN MARSHAD, HERIOT WATT UNIVERSITY, EDINBURGH, UNITED KINGDOM, AUGUST 20142. NITTO HYDRANAUTICS COMPANY, CRAIG R. BARTELS, PHD3. IEA-ETSAP AND IRENA© TECHNOLOGY BRIEF I12 – MARCH 2012

Desalination Technology: Reverse Osmosis

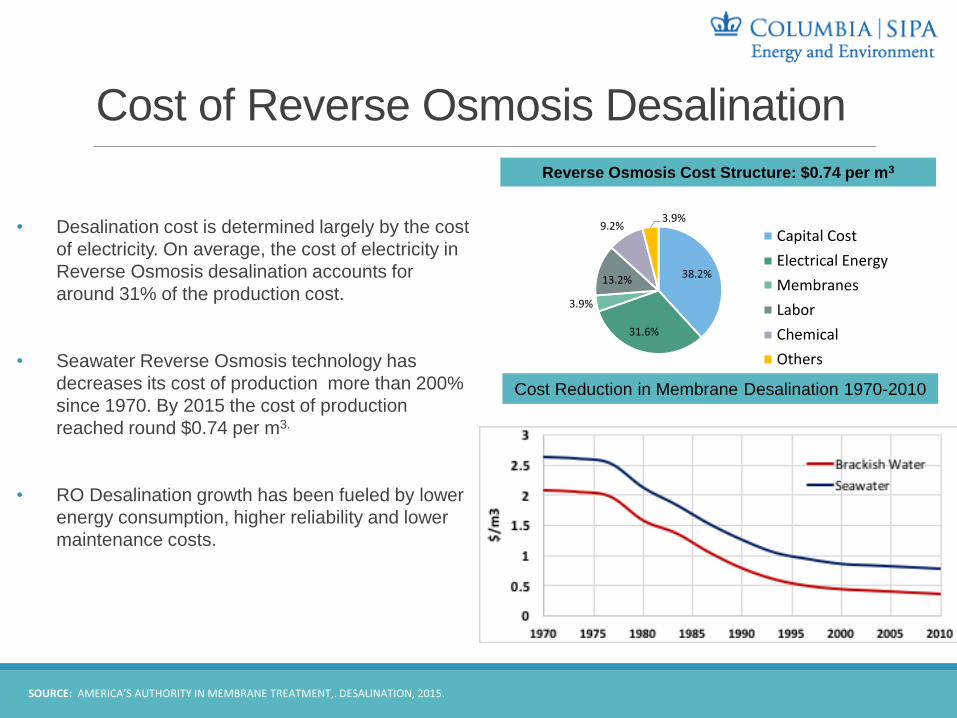

• Desalination cost is determined largely by the cost

of electricity. On average, the cost of electricity in

Reverse Osmosis desalination accounts for

around 31% of the production cost.

• Seawater Reverse Osmosis technology has

decreases its cost of production more than 200%

since 1970. By 2015 the cost of production

reached round $0.74 per m3.

• RO Desalination growth has been fueled by lower

energy consumption, higher reliability and lower

maintenance costs.

Cost Reduction in Membrane Desalination 1970-2010

Reverse Osmosis Cost Structure: $0.74 per m3

SOURCE: AMERICA’S AUTHORITY IN MEMBRANE TREATMENT,. DESALINATION, 2015.

38.2%

31.6%

3.9%

13.2%

9.2%3.9%

Capital Cost

Electrical Energy

Membranes

Labor

Chemical

Others

Cost of Reverse Osmosis Desalination

Florida, California, and Texas are the largest players

• Approximately, 2,000

desalination facilities larger

than 0.3 million gallons per

day (MGD) operate in the

U.S. This represents 2% of

U.S. municipal and industrial

freshwater use.

• Florida, California, and Texas

have the greatest installed

desalination capacity and

account for 68% of municipal

desalination facilities.

California:Orange County(Waste water)

100 MGD, 2015

California:Carlsbad

(Sea water)50 MGD, 2015

Texas:El Paso

(Brackish)27.5 MGD, 2004 Florida:

Tampa(Sea water)

25 MGD, 2006

Major Desalination Plants in U.S.

SOURCE: DESALINATION - INTERNATIONAL JOURNAL, 2014.

RO process in Wastewater

Seawater desalination

Brackish desalination

Desalination in U.S.

• Improvements in membrane technology leads to:

Reduction of energy consumption.

Reduction O&M cost.

Higher permeability.

Increases water recoveries.

• Material science promises important advances in

membrane development for reverse osmosis

technology:

Nanocomposite

Chlorine resistant membranes

Nanotube

Graphene based membrane

Scheme of graphene membrane for desalination1

1. WANG , Y. CARBON , 20172. AMY, G.,MEMBRANE-BASED SEAWATER DESALINATION: PRESENT AND FUTURE PROSPECTS, DESALINATION, 2016.

• Costs associated with desalination are expected to decrease is by 20% by 2021.

Developments in desalination

Objectives

Water Infrastructure

Emerging Water Technologies

Water Markets

Case Studies

Water MarketsWater Trading Schemes Around the World

1. Australia:

- Since 1994

- Largest system

- $3.1 billion market

- Electronic Exchanges

2. US:

- Since the 1980s

- Markets in AZ, CA, CO, NM

3. South Africa:

- Since 1997

- Early stage, small

volumes, local areas

4. Chile:

- Since 1981

- Only water entitlement

- Weak regulation

3. UK

- Since 2001

- Only water entitlement

6. Oman:

- Since 2500 BC

- Aflaj irrigation system

7. Canary Islands:

- Since 1975

- Informal

SOURCE: THE NATURE CONSERVANCY “WATER SHARE REPORT”,; REUTERS “WATER TRADING SCHEMES AROUND THE WORLD”

• Pre-conditions:

• Second dryest continent

• Uncertainty about rainfall

• Variation in river flow

• The Murray-Darling Basin:

• 65% of all irrigated farmland in Australia

• 55% of all farm revenue in Australia

• 90% of the consumptive use of Murray-

Darling water goes to irrigating cotton,

rice, cereals, pasture, etc.

Trading Water in Australia

Water Markets

SOURCE: AUSTRALIAN GOVERNMENT NATIONAL WATER COMMISSION “WATER MARKETS IN AUSTRALIA”; THE NATURE CONSERVANCY “WATER SHARE REPORT

Water Markets

Water Trading Types• Temporary Water Trade

• A transfer of water specifically for the irrigation season

• In some regions, temporary transfers are solely transfers of allocation

• In other regions, an entitlement can be transferred on a temporary basis

• Permanent Water Trade

• A transfer of the water entitlement to the purchaser on a permanent basis

• The purchaser will retain the parcel and receive any allocation granted upon it from

the date of the transfer indefinitely or until the time at which they sell the entitlement

• Forward Water Market

• Enables the contracting of temporary or permanent water parcels at a set price to be

delivered at a future date, to be determined by the seller and purchaser

SOURCE: WATERFIND; : AUSTRALIAN GOVERNMENT NATIONAL WATER COMMISSION “WATER MARKETS IN AUSTRALIA”

• Water Access Entitlement

• The perpetual or ongoing entitlement to exclusive access to a share of water from a

specified consumptive pool

• Water Allocation

• The specific volume of water allocated to a water access entitlement in a given

season

Water Right Types

• 1994 Water Reforms:

• Separation of water rights from land

• Allow inter-state trading

• 2004 National Water Initiative: Further unbundling of water rights into:

• Water access entitlement

• Water allocation

• Delivery share

• Water use license

Building up the Water Market

Water Markets

SOURCE: AUSTRALIAN GOVERNMENT NATIONAL WATER COMMISSION “WATER MARKETS IN AUSTRALIA”; THE NATURE CONSERVANCY “WATER SHARE

REPORT

• Millennium Drought (worst during 2007-09): water trading reduced losses in the

regional from $11.3 billion to $7 billion over 5 years

• Investment Partnerships:

• e.g. Nature Conservancy’s Water Sharing Investment Partnership

• e.g. Waterfind’s involvement with the On-Farm Irrigation Efficiency Program

Economic Results and Future Opportunities

Water Markets

SOURCE: AUSTRALIAN GOVERNMENT NATIONAL WATER COMMISSION “WATER MARKETS IN AUSTRALIA”; THE NATURE CONSERVANCY “WATER SHARE

REPORT

Water MarketsDevelopment of California’s Water Market

• In the mid 1990’s, water

regulation reforms began

allowing the transfer of water

from water rich areas to areas

of water scarcity through state-

owned water banks.

• Amidst large scale drought

allocation problems became

worse beginning in 2011, with

2011 and 2014 the State’s

driest years on record.

• As the State now enters a

phase of recovery, water

scarcity will remain a problem

as population growth

projected from 38 million today

to 44 million by 2030.

SOURCES: PERC 2016, HTTP://GRIST.ORG/ARTICLE/THE-CALIFORNIA-DROUGHT-IS-ON-ITS-WAY-OUT-BUT-DEEPER-DROUGHTS-LIE-AHEAD/

How can you sell water in California?

IDENTIFY & APPLY FOR RELEVANT PERMITS FOR TRANSFER

Prospective sellers should consult with relevant state and federal

regulatory bodies (i.e. Bureau of Reclamation, Department of Water

Resources, etc) to determine the permits required to execute a sale of

a quantity of water or the transfer of title to water rights in the specific

context.

FIND A BUYER EITHER PRIVATELY OR WATER BANK

Prospective sellers may either sell their water to a water

bank or locate prospective buyers through professional

networks or advertisements.

COMPLETE SALE THROUGH CONTRACT

The finalization of the sale of the rights typically occurs through

private contract (either executed by two private parties or

between a water bank and a seller).

12

3

?

Once the transfer is complete, the buyer is

generally responsible for the transportation of

water resources.

Water Markets

Water MarketsCalifornia’s Water Market Today: 5% of Water Use or 2,000,000 acre-feet/year, representing a $500,000,000 market

Environment

Municipal & Industrial

San Joaquin Valley Farmers

Sacramento Valley Farmers

Other

Mixed Use

42% Municipal &

Industrial

Market Participants

Short-term

Long-term

Permanent Flow

Additional Long-term Commitment

Additional Permanent Commitment

33% Long-term

Same County

Same Region

Different Region

Unspecified

50% Same County

Type of Transfer Location of Transfer

SOURCES: HANAK, ELLEN, AND ELIZABETH STRYJEWSKI. "CALIFORNIA’S WATER MARKET, BY THE NUMBERS: UPDATE 2012." PUBLIC POLICY INSTITUTE

OF CALIFORNIA (2012). HTTP://WATERINTHEWEST.STANFORD.EDU/GROUNDWATER/CHARTS/COST-COMPARISON/INDEX.HTML

Water Markets Who’s Buying Water: Key Market Participants

Agriculture Industrial Municipal

Growers of high yield perennial crops.

• e.g. almond producers, pistachio

producers.

• Paramount Farming

• South Value Farms

‒ Two of the largest producers of

nuts globally by acres of crops

managed

Industries engaged in water intensive

processes.

• e.g. concrete contractors, data

center owners/operators (water

required for cooling)

• Muse Concrete Contractors (San

Francisco)

• Digital Realty Trust (San Francisco)

‒ Digital currently has 20.5% of

global data management market

share

Utilities responsible for provision of

residential and public use water sources.

• e.g. City Water Utilities

• Los Angeles Department of Water &

Power

• City of Sacramento Department of

Utilities

‒ Debt guaranteed by city

Largest potential private buyers are established companies with strong balance

sheets. Among public buyers, city water utilities are the largest market segment

and their credit is guaranteed by municipal authorities.

SOURCES: PERC 2016, DIGITAL REALTY 2016, WWW.GROWINGPRODUCE.COM

Water MarketsGrowth in California’s Water Markets: Current Growth Prospects & Potential Catalysts

Volume Traded

• In 2011, 687 billion gallons of water were traded

• Assuming levelized growth, this would grow to over 1.3 trillion

gallons by 2040

• Other catalysts that might further increase the volume of water

traded include:

• Currently discussion in state legislature to streamline

regulatory process for transfer approval that would lower

transaction costs

• Anticipated infrastructure investment will lower transportation

costs

Water Pricing

• The average price of a water transfer per gallon in 2011 was $.08.

Assuming an annualized increase in prices of 10%, water prices

would reach $1.21 by 2040

• Other catalysts that might further increase water prices might

include:

• Project higher demand for water in the industrial and

agricultural sector

• Significant population growth in the short to medium term will

stimulate residential demand

-1,000,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

1982 1991 2000 2011 2040

(Ac

re-f

ee

t)

Year

Volume of Water Traded

Assuming annualized growth in water prices of 10% per year, this will be a $15 billion market by 2040

SOURCES: PERC 2016 & DATA APPENDIX

Objectives

Water Infrastructure

Emerging Water Technologies

Water Markets

Case Studies

International Case Studies--China

• Challenges and issues in Chinese water sector

• Unequal access to water resources

• Infrastructure lags behind

• Poor water quality

• State Council, the highest level of government, supports water related projects

• Law enforcement on promoting and supervising urban drainage and wastewater

treatment

• Support of PPP through legislations and administrative orders

• Promotes Sponge Cities ideal

• Enable buildings, streets and wetlands in cities to absorb, store and release

rainwater like a sponge to better serve the cities’ urban development

• Cities will collect and utilize 70% of rainwater, with 20% of urban areas meeting the

target by 2020. The proportion will increase to 80% by 20301

1. THE STATE COUNCIL OF THE PEOPLE'S REPUBLIC OF CHINA

Popularity in PPP

• By September 2016, of the total 10,471 PPP projects, 33.5% are water-related1

• Key players—State Owned Enterprises (SOEs) and their satellite companies

• Foreign firms’ role tend to be limited -- advanced technology provider

• Hard access to local decision makers

• Hard access to financing

1. CHINA PRIVATE PUBLIC PARTNERSHIP CENTER

Foreign Corporation in PPP -- Veolia Environment in Shanghai

• Largest market share in sewage treatment facilities in China (13% in 20171)

• 60 projects in China, covering about 40 cities

• 1st PPP for full water service, including drinking water production, distribution and customer service

• Veolia Environment listed in Europe. But no data provided for this project

Municipal (local) investmentForeign Investment

Veolia Environment Group

Veolia Water

Shanghai Municipal Investment (Group)

Shanghai Water Assets Operation & Development

Shanghai Pudong Veolia Water Corporation Ltd(50-year joint venture)

Drinking Water Production Water Distribution Customer Services

ControlControl

50% shareholding 50% shareholding

1. IBIS, INDUSTRY REPORT

Foreign Corporation in PPP -- Veolia Environment in Shanghai

• Reason for Success

• Early entrance in 1980s

• Advanced technology and good reputation as a leading water resource management conglomerate

• Actively build relationship with municipal governments

• Prospects

• Weaker presence, compared with local major players

1. IBIS, INDUSTRY REPORT

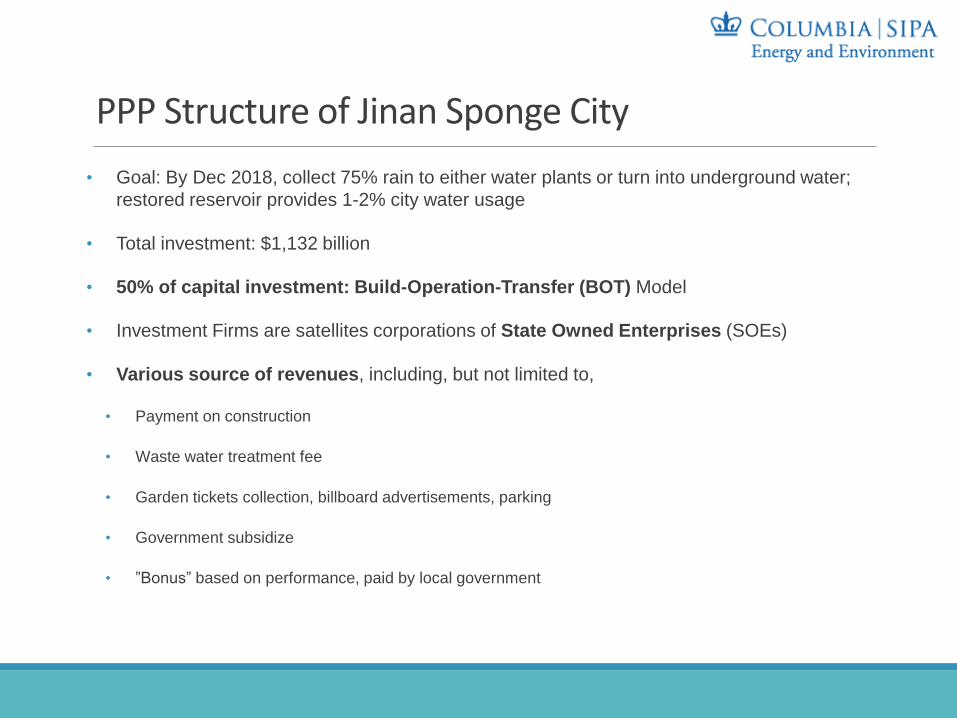

PPP Structure of Jinan Sponge City

• Goal: By Dec 2018, collect 75% rain to either water plants or turn into underground water;

restored reservoir provides 1-2% city water usage

• Total investment: $1,132 billion

• 50% of capital investment: Build-Operation-Transfer (BOT) Model

• Investment Firms are satellites corporations of State Owned Enterprises (SOEs)

• Various source of revenues, including, but not limited to,

• Payment on construction

• Waste water treatment fee

• Garden tickets collection, billboard advertisements, parking

• Government subsidize

• ”Bonus” based on performance, paid by local government

PPP Structure of Jinan Sponge City –Capital Contribution

• Investment firm (private partner) has controlling interests -- holds 90% shares and capital

investment

• Asset management company (public partner on behalf of the local government)

Construction Package

Project Company (Special Purpose

Vehicle)

Local Bureau of Finance

Government Subsidize

Annual Payment Based on Performance

Local Government

Bureau of Municipal Utility

Asset Management Company (Public

Partner)

Investment Firm (Private Partner)

Drainage, sewage

Wastewater treatment

Water pipelines

Gardens, rivers, lawns

Shareholding Agreement

Authorize

Supervise

Authorize

Public Tender

Franchise

Transfer Ownership upon Full Ferm

Operate, Maintain, collect

revenue

10% Shares

90% Shares(controlling interest)

Case Study 2 – Heerlen, Netherlands

Minewater Project – Heerlen

Minewater 1.0(2007-2013)

Minewater 2.0(2012-Present)

Minewater 3.0(Near Future)

A straightforward pilot system for turning an abandoned coal mine into

a geothermal energy source for the sustainable low-energy heating and

cooling of buildings

Demand and Supply

Controlled System

Full-scale hybrid sustainable energy

infrastructure

Deeper Layer:

• Depth: 2,300 ft

• Temperature: 82.4°F

Upper Layer:

• Depth: 820 ft

• Temperature: 60.8°F

Middle Section: Intermediate well

for injecting of the cooled hot and

warmed cold mine water

• Depth: 1,148 ft

• Temperature: 64.4-71.6°F

Minewater Project 1.0, Heerlen

Minewater Project – Heerlen

Minewater 1.0(2007-2013)

Minewater 2.0(2012-Present)

Minewater 3.0(Near Future)

Transformation of the straight forward

geothermal minewater pilot system into full-scale

hybrid sustainable energy infrastructure

Demand and Supply

Controlled System

Straightforward Pilot System

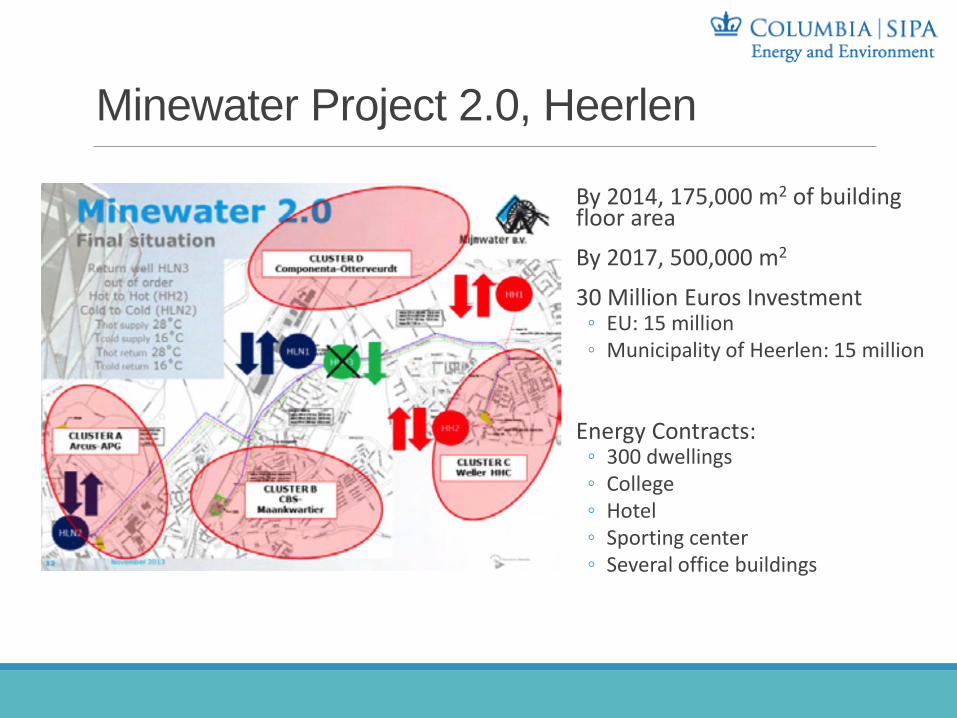

Minewater Project 2.0, Heerlen

By 2014, 175,000 m2 of building floor area

By 2017, 500,000 m2

30 Million Euros Investment◦ EU: 15 million◦ Municipality of Heerlen: 15 million

Energy Contracts:◦ 300 dwellings◦ College◦ Hotel◦ Sporting center ◦ Several office buildings

Privatization: Minewater Corporation (2013)

70%

30%

TRADITIONAL ENERGY

Fixed cost

Variable Cost(Energy Service)

70%

30%

MINEWATER SYSTEM

Fixed cost

Variable Cost(Energy Service)

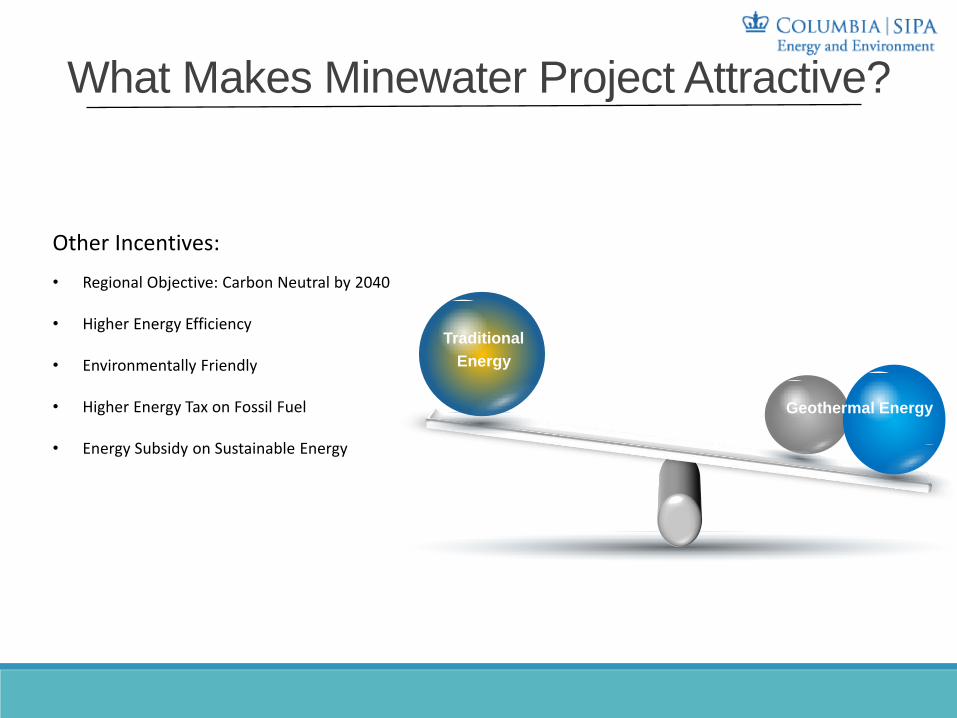

Traditional gas boiler Minewater heat pump Difference

Cost of energy 22 Euros/GJ 6 Euros/GJ 16 Euros

What Makes Minewater Project Attractive?

Traditional

Energy

Geothermal Energy

Other Incentives:

• Regional Objective: Carbon Neutral by 2040

• Higher Energy Efficiency

• Environmentally Friendly

• Higher Energy Tax on Fossil Fuel

• Energy Subsidy on Sustainable Energy

Minewater Project 3.0, Heerlen (nearfuture)

2 Key Elements:• Time• Intelligence

SUSTAINABLE WATER INFRASTRUCTURE

MARCH 2017 |

COLUMBIA UNIVERSITY