Embed Size (px)

Citation preview

1

Sustainability Accounting: A Critical Review of the Literature

Authors:

Larry O’Connor*

Lecturer - Accounting La Trobe University

Carol A. Adams Professor of Accounting

La Trobe University

*Corresponding author

2

Sustainability Accounting: A Critical Review of the Literature

ABSTRACT

The purpose of this paper is to critically examine published sustainability accounting

(SA) studies in the light of ‘change’ being a key theme and to determine the extent to

which concerns about the quality of research in the field and the lack of engagement

(Parker 2005; Adams and Larringa-Gonzalez 2007; Owen 2008) are valid.

An evaluation of 252 sustainability accounting studies spanning the period 1973-2007

was undertaken. The evaluation covered six areas: (i) The degree to which change – a

key theme in the sustainability accounting literature – is discussed in the sustainability

accounting studies reviewed; (ii) Theoretical rigor; (iii) Methodology employed; (iv) The

explication of structures and tensions at societal and organizational levels of analysis; (v)

The exploration of new imaginings; and (vi) The examination of SA within specific

organizational contexts.

The review found that the sustainability accounting academe’s desire for ‘change’, as

reflected in the sustainability accounting theoretical / philosophical literature, has not

been reflected in the sustainability accounting empirical literature. This is also reflected

in a minimal effort to seriously engage with questions about structure and tensions at

societal and organizational levels of analysis, a lack of new imaginings about what

sustainability accounting could be, and a fundamental lack of engagement with

practitioners on the ground. The author proposes a number of reasons as to why this has

been the case, and makes a number of suggestions for future research endeavours in the

sustainability accounting field, principally centred on an engagement-based action

research agenda.

3

Appropriate research methods and avenues are recommended…How the field might

develop in order to facilitate change in practice; How the field might develop in order to

facilitate policy development to facilitate change.

1. Introduction

The purpose of this review of the sustainability accounting (SA) literature is to assess the

progress that has been made by the SA academe in the light of the core theme of SA –

change, and to determine the extent to which concerns about the quality of research in the

field with regard to theoretical underpinnings and the lack of engagement raised by

Parker (2005), Adams and Larrinaga-Gonzalez (2007) and Owen (2008) are valid.

Certainly, given recent suggestions that the SA project may have been a ‘failure’ (Gray et

al. 2007, pp.3-4)1, the time appears to be appropriate to re-assess the achievements of SA

empirical research in the light of this assessment, and to highlight factors that may have

contributed to such an assessment being made.

The following review is broken into six sections. In the first section, the roots of SA are

considered in order to highlight the fact that ‘change’ is the key theme in the SA

literature. In the second section a review of 252 SA studies was conducted with the view

to assessing the degree to which published SA research has reflected this emphasis upon

change, and in doing so provide insight into the concerns about the quality of SA research

in the light of recent concerns (Parker 2005; Adams & Larringa-Gonzalez 2007; Owen

2008). The results of this review are then discussed in the third section. The fourth

section considers some reasons as to why the SA research agenda has been somewhat

unsuccessful in the light of SA’s change agenda. Finally, the last two sections consider

policy implications of the preceding analysis and provide some suggestions as to how the

SA research agenda might move forward in the future.

1 It is important to note that this view has been documented by, although not endorsed by Gray et al. (2007).

4

2. A review of the roots of SA: Identifying ‘change’ as the key theme in SA

There are at least three reasons why ‘change’ can be viewed as the key theme in the SA

literature2: (i) the emergence of SA from the business and society debate in the late-1960s

and early-1970s was symptomatic of a growing view of a need for change in the

business-society relationship and how business activity is accounted for; (ii) SA being

labelled, amongst other things, as a ‘project’ with an ‘agenda for action’; and (iii) SA is a

significantly broader accounting that extends beyond the narrow confines of the

conventional accounting paradigm and the desire to extend accounting beyond the

financial to incorporate the social and environmental is reflected in the writings of a

number of leading SA academics. Each of these will be considered in turn.

To begin with, SA emerged out of the broader business and society debate in the 1960s

and early-1970s (AAA 1975a; Epstein et al. 1976; Estes 1976; Spicer 1978; Ullmann

1979; Parker 1986; Gray 1994; Mathews 1997; Gray 2002) in which the twin concerns

about the seeming lack of accountability of modern business organizations

(corporations), and externalities3 associated with capitalistic enterprise were prominent

(Votaw & Sethi 1969; Meyer 1971; Davis 1973; Chastan 1973; Hay & Gray 1974; Vogel

1975; Davis 1976; Buehler & Shetty 1976). Indeed, a number of authors have noted that

during this period there was a fundamental shift in societal expectations about the nature

of the business-society relationship and the need for business organizations to change

they way in which they went about their activities (Committee on Economic

Development (U.S.) 1971; Chastain 1973; Churchill 1974; Hay & Gray 1974; AAA

1975b; Epstein et al. 1976; Davis 1976; Dierkes 1979; Heard & Bolce 1981).

2 Although ‘accountability’ and ‘transparency’ have also been key themes in the SA literature, it is the author’s position that ‘accountability’ and ‘transparency’ are simply vehicles through which greater change can be promoted. 3 The term ‘externalities’ is used here under sufferance and refers to both environmental and social costs associated with capitalistic activities that are bourn by society at large with no compensation from the producer.

5

It was out of this broader business and society debate that the SA paradigm emerged4.

Indeed, a review of the accounting literature during the late-1960s and early-to-mid-

1970s reveals the first attempts by the accounting profession / academe to grapple with

the challenge of accounting for the social and environmental impact of an organization’s

activities (Beyer 1969; Von Berg 1972; Linowes 1972; Dilley & Weygandt 1973; Marlin

1973; Ward & Dubos 1973; Elliott & Rosenthal 1973; Estes 1976; Ullman 1976; Dierkes

& Preston 1977; Grojer & Stark 1977). The single unifying theme underlying all of the

early attempts to theorise what SA might be was the need to extend the conventional

accounting paradigm, so as to incorporate the social and environmental impacts of

economic activity into any accounting for such activity5, thereby leading to different

‘accountings’ and, ultimately, changed behaviour.

Although a number of authors have proffered a variety of definitions for SA (for

example, Ramanathan 1976; Epstein et al. 1976; Anderson et al. 1978; Gray et al. 1987;

Mathews 1993; Mathews & Perera 1995)6, the essential difference between the SA and

the conventional accounting paradigm is that the conventional accounting paradigm, with

its philosophical underpinnings grounded in neo-classical economics, privileges the

interests of financial stakeholders (Gray et al. 1988; Dillard 1991; Maunders & Burritt

1991; Gray 1992; Gray et al. 1997; Gray 2002b; Tinker & Gray 2003), whereas SA is

more focussed upon bringing about a more egalitarian worldview (Tinker et al. 1991;

Gray 1992; Tinker & Gray 2003; O’Dwyer et al. 2005) and necessarily adopts a more

expansive view of accounting which incorporates the social and environmental in

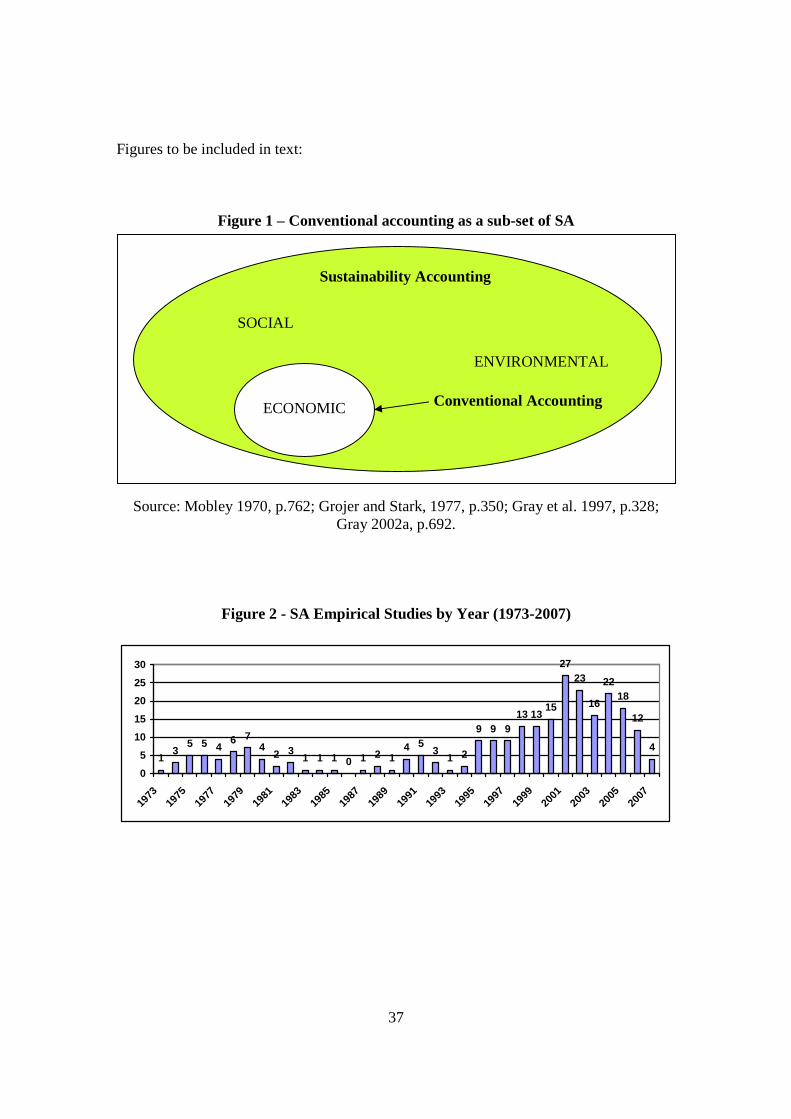

addition to the economic (Mobley 1970; Grojer & Stark 1977). In the words of Gray et

al. (1997, p.328) and Gray (2002a, p.692; 2002b, p.364), SA can be conceptualised as

‘…the universe of all possible accountings…’ of which conventional accounting is a part

4 Although there is evidence that companies have been engaging in social and/or environmental reporting – which has become a major focus of SA – for many years prior to the 1960s (Guthrie & Parker 1989; Unerman 2003; Tilling 2003), it was only in the late-1960s and early 1970s that a more formalized SA paradigm began to emerge. 5 Although the simple ‘extension’ of the conventional accounting paradigm so as to capture the social and environmental may be viewed as being somewhat managerialist and, ultimately, of limited effect. 6 Many of these early attempts to define SA were subsequently criticized for trying to ‘fit’ the social and environmental within the confines of the conventional accounting paradigm (Gray et al. 1988, pp.7, 10-11; Gray 2002b, p.363).

6

– see Figure 1. From the perspective of both internal decision-making and an external

user, the SA paradigm, in theory at least, represents a fundamental re-alignment of core

values.

Insert Figure 1 here.

Secondly, that change is a key theme in the SA literature is also highlighted by SA being

labelled as a ‘project’ (Gray 1992, p.401; 2002, p.687; Tinker & Gray 2003, p.747; Gray

et al. 2007, p.3) having an ‘agenda’ for action (Mathews 1997, p.503; Bebbington et al.

2001; Parker 2005, p.844; Adams & Larrinaga-Gonzalez 2007, p.338) which is intended

to be ‘radical’ (Gray et al. 2007, p.9), enabling (Bebbington 1997, p.365), emancipatory

(Gray et al. 1997, pp.328-29; Bebbington 1997, p.365; Gray 2002, p.692; Dillard et al.

2005, p.78) and result in ‘changed practice’ (Grojer & Stark 1977, p.354; Gray 1998,

p.213; Gray 2002, p.698; Dillard 2007, p.37) - terms which convey imagery of social

and/or political action7. Given the constitutive function of the conventional accounting

paradigm (Hines 1991; Ansari & Euske 1987; Boland 1989; Boland and Pondy 1983;

Burchell et al. 1980; Burrell 1987; Lehman & Tinker 1987; Miller and O’Leary 1987;

Neimark and Tinker 1986), advocates of SA view it as a means of articulating a

worldview that is more consistent with an egalitarian worldview that is better able to

capture both the financial and non-financial impacts of economic activity (Gray 2002;

Tinker & Gray 2003; Gray 2007).

Thirdly, given that SA is a broader accounting than the narrow conventional accounting

paradigm, the mere fact that accounting academics choose to work in the SA field implies

a sense of dissatisfaction with the conventional accounting paradigm and a desire to at

least contribute to bringing about change in society through the vehicle of accounting

(Bebbington 1997; Gray 2002; Adams & Larrinaga-Gonzalez 2007). This sense of

frustration / disillusionment is certainly evidenced in the writings of a number of leading

authors in the SA field (Maunders & Burritt 1991; Gray 1992; Bebbington et al. 1999;

7 Although it is acknowledged that both the conventional accounting and SA paradigms are political in the sense that they either support or challenge the status quo (Tinker et al. 1991).

7

Tinker & Gray 2003; Gray et al. 2007), even though the mechanisms for bringing about

such change may not have been clearly explicated (Gray 1992; Adams & Larrinaga-

Gonzalez 2007).

The desire to at least play a role in bringing about change is clearly evidenced in the

writings of leading authors in the SA literature who have enunciated change as one of the

core purposes of SA. For example, Gray et al. (1988, p.7), in speaking about CSR

(Corporate Social Reporting), notes that ‘…the subject struggles for legitimacy; it clearly

questions the unique dominance of investors as the primary (or at least the only)

participants in the organization; it is clearly non-passive in that it must always imply

some assumption about the desirability and direction of social change; and, in exposing

the fundamental beliefs of the protagonists (about society, politics and even the human

species itself), CSR naturally increases the opportunity for basic and profound

disagreement.’

Similarly, Bebbington (1997, p.365) has noted that one of the core concerns of SA

research activity has been ‘…with exploring and developing new forms of accounting

which are more socially and environmentally benign and which have the potential to

create a fairer more just society.’

In a similar vein, Tinker and Gray (2003, pp.728-29), in commenting on the need for SA

to have a political philosophy adequate for effecting change, noted that:

‘Our purpose in this paper is to try to engage colleagues in a series of arguments about

how best we might address social injustice and environmental degradation in our

activities as scholars. Doing this may well beg many questions, but whilst, on a personal

morality basis…we must act with respect for those beliefs which are both informed and

deeply held by colleagues, we, ourselves, cannot do other than directly address our

remarks to those means by which the worst exigencies of international financial

capitalism can be ameliorated or, preferably, excoriated. Our starting point is that the

negative consequences of modern accounting, finance and economics are self-evident

8

and, just because to “go with the flow” is easier – intellectually and spiritually – that is no

argument for passivity’.

Finally, Adams and Larrinaga-Gonzalez (2007, pp.333-34) state that the case for

conducting research in the SA field has already been made (citing Gray 1992) and that

the case for such research is ‘overwhelming’. They note that ‘(W)hat is in doubt is the

extent to which the research to date can effect changes which address the concerns of

those conducting it’ (emphasis added by author). Thus, it is clear that change is a key

intention of many authors in the SA field8. As such, any assessment of SA research to

date needs to be conducted in the light of this intention, and certainly any notion that the

SA project may have ‘failed’ (Gray et al. 2007, p.3) needs to be tested against this same

intention.

3. A review of SA studies in the light of ‘change’ being a key aim of SA researchers

a. Methodology employed for conducting the literature review

This literature review focuses upon SA, which has been defined for the purposes of this

review as any attempt to account for the social and/or environmental impacts of an

organization’s activities beyond the conventional accounting paradigm. Three basic

search strategies were employed in order to compile a database of SA empirical studies:

(i) A literature search was conducted of peer reviewed accounting journals using

electronic journal databases (Emerald Full Text; Expanded Academic ASAP; Science

Direct; Wiley Interscience Journals; Swets Wise (Blackwell Publishing); APAIS Full

Text);

(ii) In order to capture SA empirical studies that may not have been published in

accounting journals, a literature search was conducted of non-accounting electronic

8 The questions as to how much change is needed (ie: ‘marginal’ versus ‘radical’ change), and how this change can or should be brought about, are beyond the scope of this review.

9

journal databases Once again, only peer reviewed scholarly journals were selected when

searching the various databases9; and,

(iii) A literature search was conducted by tracing studies through the

bibliographies of published SA studies captured by the first two search strategies. Once

again, only SA empirical studies published in peer reviewed scholarly journals were

included in this search.

In addition to the above, a number of stand-alone research reports on social and

environmental accounting practice, including the annual Corporate Social Reporting

(CSR) studies conducted by accounting firm Ernst and Ernst during the period 1973-78;

the three reviews of CSR by the American Accounting Association in 1975; the tri-

annual Environmental / Sustainability Reporting studies conducted by KPMG during the

period 1993-2005; studies investigating environmental management accounting practice

conducted by the United States Environmental Protection Authority, the Association of

Certified Chartered Accountants, and the Victorian Environmental Protection Authority;

and the review of Environmental / Sustainability Reporting in Australia conducted by

CPA Australia during 2004-05, were included in the database due to the broadly

acknowledged significance of their contribution to the SA empirical literature10 and the

active involvement of leading members of the SA academe in many of these studies.

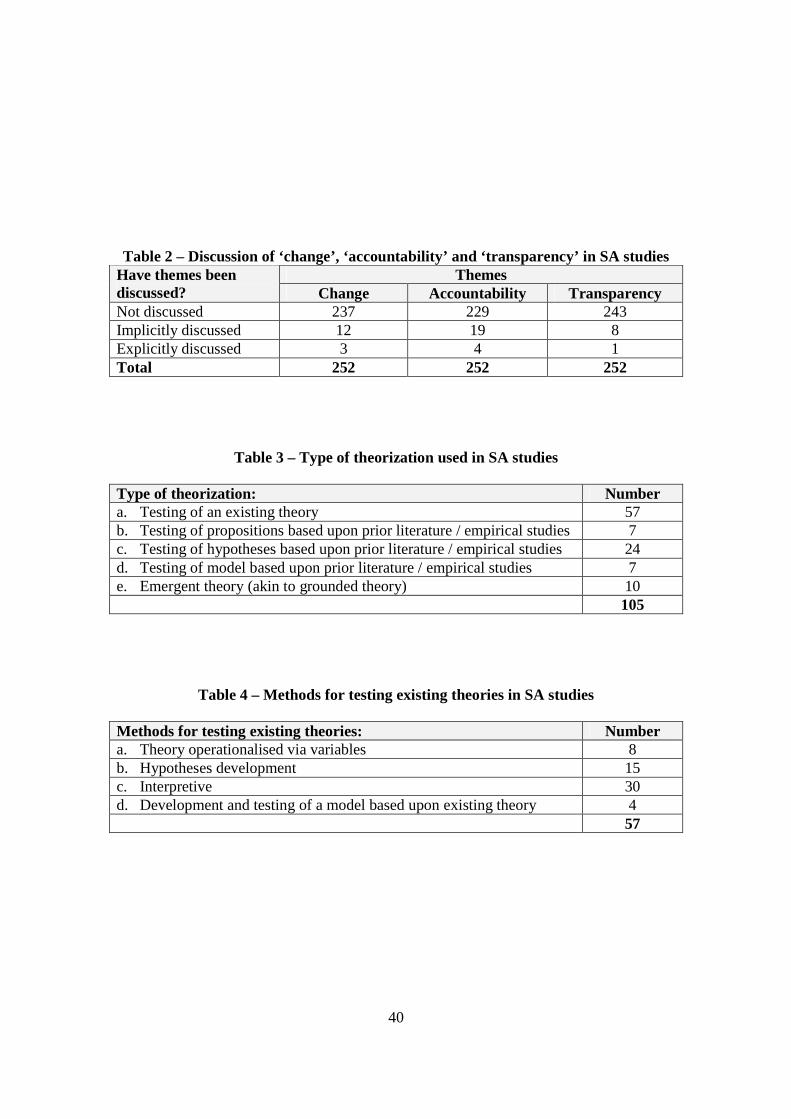

As a result, a database was compiled consisting of 252 SA empirical studies11 spanning

the period 1973-2007 – see Figure 2. In each case a physical copy of each study was

obtained and personally read by at least one of the authors. Although the 252 empirical

studies collated for this review does not constitute an exhaustive listing12, the time span

covered (1973-2007) and the breadth of accounting and non-accounting journals

9 Appendix 1 and Appendix 2 contains a full list of the journals searched via the electronic data bases. 10 As indicated by the numerous citations of these studies throughout the SA literature. 11 A list of the journals and other sources from which the 252 empirical studies have been drawn appears in Appendix 1. 12 For example, a number of SA studies which have been published in two information and research news orientated journals dedicated to SA research – the Social and Environmental Accounting Journal and the Journal of the Asia Pacific Centre For Environmental Accountability – were not included on the basis that both these journals have only become peer-reviewed in recent years.

10

represented in the 252 studies was deemed to be a sufficient sample from which a number

of general and specific observations could be made.

Insert Figure 2 here.

b. Determining the basis upon which the SA empirical studies were analysed

The analysis of the SA empirical studies was driven by one central question: Is the desire

for change that has been clearly enunciated in the SA philosophical/theoretical literature

reflected in the SA research literature? In order to conduct an ordered analysis of the SA

studies collated, six specific criteria were identified, based upon the work of Puxty (1986,

1991); Gray (1988, 1992); Bebbington (1997); Larrinaga-Gonzalez and Bebbington

(2001); O’Dwyer (2003); Parker (2005); and Adams and Larrinaga-Gonzalez (2007),

from which a number of specific questions were developed. The six criteria and

associated questions have been listed in Table 1.

Insert Table 1 here.

c. An overview of the basis upon which the six criteria summarised in Table 1 were

developed

The first criterion – discussion of ‘change’, ‘accountability’ and/or ‘transparancy’ – was

based upon the following premise: If ‘change’ and the related themes of ‘accountability’

or ‘transparency’ are important themes in the SA literature, then this should be reflected

in the discourse of the SA studies reviewed. It is evident from the SA literature that the

terms ‘change’, ‘accountability’ and ‘transparancy’ are used in conjunction with each

other, and it is acknowledged that the meanings given to the terms ‘accountability’ and

‘transparancy’ by various authors may not be consistent. As such, the authors have not

11

attempted to ‘define’ these terms, but rather to simply test for their presence in the

discourse of the SA studies reviewed. It is also important to note that there may be an

implicit motivation to see change on the part of those conducting research in the SA field,

but this cannot be assumed as it is conceivable that a researcher may engage in SA

research with a purely descriptive agenda. Hence the need to examine SA studies for the

presence of the above terms.

The second criterion - rigorous development of the proposals from a scholastic

framework – has been drawn from Gray’s (1992, p.401) observation that ‘(P)rojects for

social change through accounting change of one sort or another are generally coupled

with theoretical flaccidity resulting from (1) an implicit, or at least underspecified value

and belief base; (2) a lack of rigorous development of the proposals from some scholastic

framework; and (3) a failure to fully explicate social structures and tensions and thus, as a

result, a failure to articulate (or at least hypothesise) the mechanisms of social change’

(emphasis mine). The four questions listed alongside this second criteria were deemed to

be logical ‘applications’ of Gray’s observation.

The third criteria - structures and tensions – was drawn directly from the third point of

Gray’s observation in the previous paragraph. A failure to fully explicate social

structures and tensions and thus, as a result, a failure to articulate (or at least hypothesise)

the mechanisms of social change – is essentially a recognition that SA does not happen

within a vacuum. If one is going to investigate ‘change’ at either a societal or

organizational level, one must at least identify the structures and tensions that may be at

play which may hinder the potential success of any SA intervention. As Gray (2002,

p.701) has noted, ‘…how can we seek change without a complete understanding of the

present plus a complete specification of how change does and can take place?’ The four

questions listed against this third criterion were deemed to be logical ‘applications’ of

Gray’s observation.

The fourth criteria – methodology – has been drawn from the on-going debate in the SA

literature with regard to whether SA researchers should engage with the field of practice

12

and risk capture by the corporate and institutional world (Bebbington 1997; O’Dwyer

2003; Parker 2005). The questions relating to the methodology criterion were aimed at

answering one fundamental question: To what extent has the SA academe engaged with

practice? This is a particularly pertinent point given that engagement-based research has

the potential to affect change through critical engagement (Sikka et al. 1985; Bebbington

1997; Adams & Larrinaga-Gonzalez 2007), and a number of leading authors in the SA

field have argued that engagement is a core part of the SA project (Bebbington 1997;

Gray 2002; Adams & Larrinaga-Gonzalez 2007).

The fifth criteria – new imaginings – has been drawn from the work of Gray (1988, 2002)

and Bebbington (1997) in which the exploration and development of ‘new imaginings’ or

‘new accountings’ is described as being at the core of SA. It is the author’s contention

that if change is the key theme in SA, then there should be evidence of attempts to either

develop or implement new accountings in real life settings. As such, the key question to

ask here was: ‘Have there been attempts to develop, refine or implement ‘new

imaginings’ in the SA empirical work?’

The final criteria – interaction of SA with internal organizational processes - has been

drawn directly from Larrinaga-Gonzalez and Bebbington (2001) and Adams and

Larrinaga-Gonzalez (2007). Organization-based engagement research can provide

insights into organizational operations and the role of accounting within organizations.

Given that SA is about change, then it seems logical to inquire as to whether particular

SA research studies have provided insight into the interaction of SA with other internal

organizational dynamics which in turn can provide insight into factors which may help

drive or prevent change towards greater sustainability and/or accountability.

a. Overview of how the analysis was conducted

The analysis was conducted using a combination of content analysis and interpretive

judgement based upon the criteria and associated questions identified in Table 1. For

example, in order to answer the question ‘is change discussed in the study?’ each study

was reviewed with the purpose of identifying the word ‘change’ in the discourse – apart

13

from any mention of the word ‘change’ as a part of normal descriptive discourse clearly

unrelated to a change agenda13. With regard to the question ‘have social structures and

tensions been explicated?’ each study was reviewed with the purpose of identifying if the

authors had acknowledged or discussed the significance of social structures or tensions at

any point in the study, including as a broader context within which the findings could be

viewed. It is acknowledged that, as with all interpretive research, this approach to

analysis was subjective. However, care was taken to ensure that the specific criteria and

questions identified in Table 1 were applied uniformly to all studies included in this

review, resulting in an analysis that was consistent, so as to improve the validity of the

findings.

4. Results of the analysis

(i) Discussion of ‘change’, ‘accountability’ and/or ‘transparancy’

A summary of the results of the discourse analysis of the SA studies reviewed has been

provided in Table 2. Given the discussion in Section 2 of this paper in which the case for

‘change’ as the key theme in the SA literature was made, the results presented in Table 2

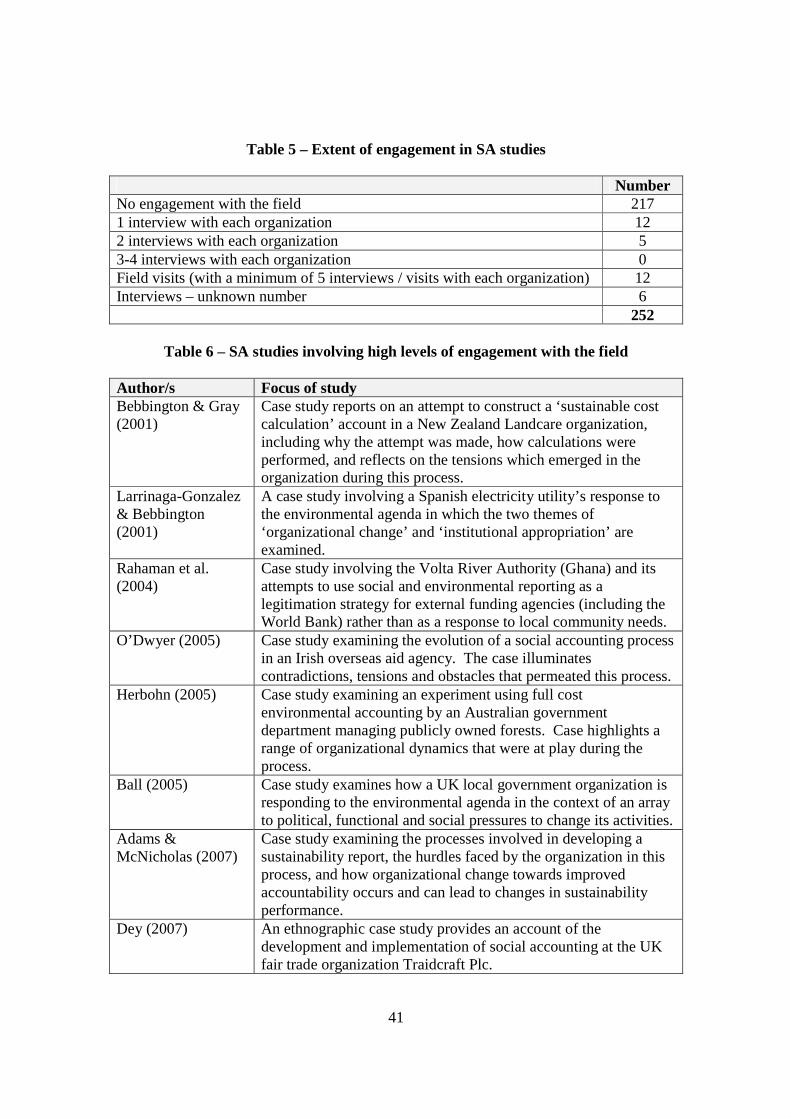

are quite revealing. In 237 of the 252 studies reviewed (94 per cent), change was not

discussed, and the results are not too dissimilar for the themes of ‘accountability’ (229 –

91 per cent) and ‘transparency’ (243 – 96 per cent).

Insert Table 2 here.

The relative absence of the terms ‘change’, ‘accountability’ and ‘transparency’ in the

discourse of the SA studies reviewed reveals a lack of discussion of these themes in the

studies reviewed.

13 For example, if a study contained a sentence such as ‘…and then in 2004 there was a change in the company’s ownership structure…’ – this was interpreted as being a part of normal descriptive discourse which is clearly unrelated to any change agenda.

14

(ii) Rigorous development of the proposals from a scholastic framework

The most significant finding in this part of the review was that only 105 of the 252 SA

empirical studies (42 per cent) used theory either as a means for aiding in study design, or

as a lens through which results were interpreted – see Table 3. Of the 57 studies that

used an existing theory, Table 4 summarises the ways in which these existing theories

were tested. Interestingly, the most commonly used existing theory was legitimacy

theory, which was employed in 28 studies.

Insert Table 3 and Table 4 here.

An important point to note at this point was that out of the 105 studies employing theory,

96 (91 per cent) could be described as deductive theorising, with only nine studies

employing inductive theorisation. This observation is in line with Parker’s (2005)

observation that inductive theorising in SA research has been quite scarce. These

findings are also consistent with a more general critique regarding the under-theorization

in the SA literature (Preston 1983; Ullman 1985; Puxty 1986, 1991; Gray 2002).

(iii) Methodology

The most significant finding with regard to the methodology criterion was that in only 35

of the 252 SA studies (14 per cent), did the researcher/s actually engage with the field –

see Table 5. Of these, only 12 studies (5 per cent) could be classified as field studies

involving a minimum of five interviews / visits to each organization represented in the

study. There were six studies that involved interviews with the field but the number of

interviews / visits to the organizations represented in the study was unable to be

determined from a reading of the study as published.

Insert Table 5 here.

15

It is important to note that the lack of engagement which has been characteristic of SA

research does appear to be changing. Of the 18 studies listed as either field visits or

which have an unspecified number of interviews, 12 of these have been published since

2003. A summary of the studies which exemplified this move toward more engagement-

based research has been provided in Table 6.

Insert Table 6 here.

In terms of research methodology employed, Figure 3 reveals that content analysis has

been by far the primary research methodology employed, followed by laboratory / model

testing – two research methodologies that require no engagement with the field. The

most revealing point in Figure 3 is the relatively few field studies that have been

conducted in the SA field14.

Insert Figure 3 here.

In terms of research focus, SA research has been dominated by inquiries into social

and/or environmental and/or sustainability reporting practice, which account for 237 of

the 252 studies reviewed (94 per cent) – see Table 7. It is not surprising to find therefore,

that documents such as Annual Reports, and Environmental/Social/Sustainability reports

have been the primary data source for a majority of the studies reviewed – see Table 8.

Insert Table 7 and Table 8 here.

14 Although the terms ‘case-study’ and ‘field-study’ have, at times, been used inter-changeably in the research literature more generally (Babbie 1989; Ferreira & Merchant 1992; Sheilds 1997; Atkinson & Shaffir 1998; Radcliffe et al. 2001; Burgess 2005; Merchant & Van der Stede 2006). For the purposes of this review, case-studies were differentiated from field-studies on the basis that a field-study necessarily involved personal contact between the researcher and the organization which is the object of the research. A case-study therefore implies no personal contact between the researcher and the object of the research.

16

SA studies have been dominated by a research methodology of non-engagement with the

field – an observation that has also been made by Larrinaga-Gonzalez and Bebbington

(2001), Gray (2002), Parker (2005), and Adams and Larrinaga-Gonzalez (2007). As a

result, the SA academe has, in the words of Parker (2005, p.856), run the real risk of their

discourse being confined ‘...to the halls of academe...’, thereby distancing themselves

from any significant influence over whatever institutionalization of SA may occur.

(iv) Structures and tensions

Even though it was noted at the beginning of this section that if one is going to

investigate ‘change’ at either a societal or organizational level, one must at least identify

the structures and tensions that may be at play which may hinder the potential success of

any SA intervention, the data presented in Table 9 clearly demonstrate that the vast

majority of SA empirical studies have failed to explicate structures and tensions at either

a societal or organizational level of analysis.

Insert Table 9 here.

(i) New imaginings

In answer to the question ‘have there been attempts to develop, refine or implement ‘new

imaginings’ in the SA empirical work?’, there have been only eight SA studies which

have focussed upon the development and implementation of ‘new’ accountings in real-

world organizational settings – the studies have been summarised in Table 10.

Insert Table 10 here

17

This observation is consistent with Gray’s (2002, p.698) observation that ‘...it is difficult

not to be struck by the relative paucity of kite-flying, of speculation, of imagination...if

social accounting it anything, it is the opening up of new spaces, of new accountings, not

simply reacting to old ones.’

(ii) Identification of factors that may drive or prevent change

The data presented in Table 11 demonstrate once again that although a number of studies

have identified potential factors that may drive or prevent change, the vast majority of SA

empirical studies have failed to identify the interaction of SA with other organizational

processes / dynamics.

Insert Table 11 here.

5. Evaluation of findings

The analysis described and presented in Sections Three and Four was based upon the

premise that if ‘change’ is one of the key themes in the SA philosophical/theoretical

literature, then this should be reflected in the SA research literature. Based upon the

ensuing analysis of each of the six criteria used to assess SA research in the previous

section, it can be concluded that the desire for change is not clearly reflected in the SA

research literature. The basis for this conclusion is elaborated upon in the remainder of

this section.

Firstly, a discourse analysis of the SA studies revealed that the themes of ‘change’,

‘accountability’ and ‘transparency’ have not been discussed in an overwhelming majority

of the studies reviewed – 94 per cent, 91 per cent, and 96 per cent respectively. Although

18

it could be argued that the notion of change is an implicit agenda in any SA research on

the basis that SA represents a ‘challenge’ or ‘alternative’ to the conventional accounting

paradigm, the fact that these themes have not been mentioned in the discourse of most of

the SA studies reviewed in this paper prima facie indicates that they have not been

prominent themes in most of the studies reviewed.

Secondly, the theoretical development of SA studies has generally lacked rigor, with only

42 per cent of studies using some form of theoretical framework – although this situation

has significantly improved in more recent years. This may indeed be a sign of a natural

maturation process taking place in the SA field given the voluminous amount of

descriptive empirical work that has been undertaken during the 1973-2007 period. It is

important to note that the under-theorization in SA has been a long-standing criticism of

the SA literature (Preston 1983; Ullman 1985; Puxty 1986, 1991; Gray 2002, p.699).

Thirdly, most SA studies have not sought to explicate social structures and tensions at

both societal (98 per cent) and organizational (96 per cent) levels of analysis and, as a

result, have failed to articulate the mechanisms of social and/or organizational change.

This is a significant finding given that ‘change’ has been clearly identified as a key theme

in the SA literature.

Fourthly, SA studies have been dominated by a research methodology characterised by

non-engagement with the field – an observation that has also been made by Larrinaga-

Gonzalez and Bebbington (2001), Gray (2002), Parker (2005), Adams and Larrinaga-

Gonzalez (2007) and Owen (2008). As a result, the SA academe has, in the words of

Parker (2005, p.856), run the real risk of their discourse being confined ‘…to the halls of

academe…’, thereby distancing themselves from any significant influence over whatever

institutionalization of SA may occur. Although there are signs that this is beginning to

change, the current study confirms that these observations have indeed been correct.

Fifthly, new imaginings – a review of SA research reveals that there have only been eight

studies focussing upon the development and implementation of ‘new’ accountings in

19

real-world organizations. This finding only serves to underline the lack of engagement of

the SA academe with the field as noted in the previous point, and is consistent with

Gray’s (2002, p.698) observation after reviewing the SA literature published in

Accounting, Organizations, and Society, that ‘…it is difficult not to be struck by the

relative paucity of kite-flying, of speculation, of imagination…if social accounting is

anything, it is the opening up of new spaces, of new accountings, not simply reacting to

old ones.’ If we accept that change is a key agenda for SA research, then a key challenge

facing the SA academe is the development of new imaginings. It is not enough to

continue critiquing the conventional accounting paradigm and the system (market

capitalism) of which it is a part. The SA academe must lead from the front in proposing

new imaginings of what could be giving the necessarily different value base upon which

SA is grounded.

Finally, the vast majority of SA studies – as many as 240 out of 252 (95 per cent) - have

failed to explicate, at an organization level, the interaction of SA with other internal

organizational dynamics, thereby limiting the insight into factors that may drive or

prevent change at an organizational level. Once again, if change is a key agenda in SA

research, then a key challenge for the SA academe is to explicate the complexities of

change within different organizational and broader societal contexts, and to delineate the

role that SA can play in effecting change within these contexts.

In summary, the preceding evaluation of the SA empirical literature based upon the six

criteria specified in Table 1 is consistent with the view that the desire for change, as

reflected in the SA philosophical / theoretical literature, has not been reflected in much of

the SA research to date, but there are indications that this is changing. The preceding

analysis also confirms the concerns of Parker (2005), Adams and Larringa-Gonzalez

(2007) and Owen (2008) about the quality of research in the SA field and the lack of

engagement which has been so characteristic of much of this research.

20

6. Suggestions as to why the SA agenda has largely ignored the issue of ‘change’

It is proposed that five factors may have contributed to the conclusion reached in the

previous section: ‘change’ is not a key theme in the hearts of many SA researchers; the

‘difficulties’ associated with pursuing an engagement-based research agenda; an over-

emphasis upon the ‘accountability’ perspective; a relatively young SA academe; and an

overly influential critical perspective. The reasonableness or otherwise of each of these

propositions will be considered in turn.

To begin with, the first proposition is that ‘change’ is not a key theme in the hearts of

many SA researchers. Even though the case for ‘change’ being the key theme in SA has

been made at the beginning of this paper, the fact that academic interest in SA did not

gain significant momentum until the 1990s (see Figure 2) has meant that, unlike in

mainstream accounting research, there has been a lot of relatively easily obtainable low

hanging academic research fruit in the SA field. This has made SA an attractive area for

both young and more senior academics looking for some quick research spoils. The basis

of this proposition rests in the fact that many SA empirical studies have only made what

can best be described as marginal or shallow (some would argue negligible) contributions

to the SA literature, evidenced by a dominance of disclosure-based studies that have

lacked theoretical rigor and engagement with the field. Even Mathews (1997, p.503), in

his seminal review of the SA literature during the 1970-95 period, noted that ‘(T)he

emphasis on environmental accounting in SEAL [read SA] is frequently at the “very light

green” end of the range of possible involvement.’

Gray (2002, p.689), in commenting upon the mountains of disclosure research in the SA

field, notes that ‘…these teach us much about the phenomena and raise the profile of the

new(er) accountings, but do not, directly, advance those accountings – and nor is it

obvious that the primary motivation behind such research is to do so. That is, these

research projects are largely passive, even conservative, in relying upon the phenomena

produced by international capitalistic enterprise.’

21

The second proposition is that the ‘difficulties’ associated with pursuing an engagement-

based research agenda have provided a disincentive to pursue more rigorous and

meaningful contributions to the SA literature. In short, engagement-based research is

more difficult to organize, takes significantly longer periods of time to implement,

evaluate and write-up, and is generally more ‘messy’ than much of the non-engaged

disclosure-based research that has been conducted in the SA field and even much of the

capital markets-based research that is published in the mainstream accounting literature.

In an academic environment where there is pressure to ‘publish or perish…and quickly if

you can’, the incentive to pursue in-depth engagement-based research, particularly for

young academics pursuing a PhD, is not very attractive.

The third proposition is that the conclusion reached in the previous section could have

been due to an over-emphasis upon the ‘accountability’ perspective. Although it is

acknowledged that ‘accountability’ is a key theme in the SA literature, is was noted at the

beginning of this paper that this theme is really a subsidiary theme to ‘change’. This

third proposition was based upon the fact that disclosure-based studies have dominated

the SA empirical literature – 237 out of 252 studies – thus, it was reasonable to assume

that ‘accountability’ may have been on the minds of those researchers conducting such

studies. However, the lack of discussion of ‘accountability’ as a theme in all but 23 of

the 252 studies reviewed in this paper indicates that ‘accountability’ has not been at the

forefront of the minds of most SA researchers.

The fourth proposition is that the relative youthfulness15 of the SA academe has also been

a contributor to the conclusion drawn in the previous section. The relative youthfulness

of the SA academe is clearly evident in the attendance at the annual Centre for Social and

Environmental Accounting Research (CSEAR) summer schools in the U.K., Australasia

and other places. These summer schools have traditionally been limited to 50-60

participants, but a cursory review of the papers presented at many of the summer schools

reveals that many of the papers are being written by researchers who are in the process of

15 Here, youthfulness is used to refer to a researcher’s stage in their academic career, rather than their biological age.

22

commencing and/or completing their PhD studies, or who are recent PhD graduates. As

such, it is difficult to expect too much ground-breaking research at this level. Whether or

not these young researchers continue to pursue a SA research agenda remains to be seen,

but there are positive signs that the transient behaviour of academics in the SA field,

which has been noted by Gray (2002) as a factor that has mitigated against the substantial

development of the SEA project, is changing16.

The final proposition contributing to the conclusion reached in the previous section is that

the SA empirical research project has been dominated by an overly influential critical or

conflict-based perspective that emerged during the 1980s. In essence, the critical

perspective was a critique of the middle-range SA perspective advocated by scholars such

as Parker (1986; 1991), Gray et al. (1988) and Gray (1992) and argued that any attempts

to engage or bring SA into the mainstream would inevitably result in the implicit

championing (legitimation) of the status quo (Puxty 1986, 1991; Tinker et al. 1991;

Maunders and Burritt 1991) and ultimately devoid SA of any of its potential to effect

change in any tangible way. In the words of Tinker et al. (1991, p.29), the middle-range

perspective will simply counsel ‘…moderation, consensus and compliance, middle-of-

the-road thinking implicitly champions the status quo…’. It is the position of the author

that although the critical perspective has provided a powerful lens through which to view

accounting (Gray 1998, p.205) and can therefore add significantly to the philosophical

underpinnings of SA, it has proved to be an overly influential perspective that has stifled

the development of both the theoretical and empirical literatures in SA due to the fact that

the critical perspective, by implication, advocates a position which discourages the

development of theoretical and empirical endeavours – an observation that has previously

been made by Mathews (1997), Parker (2005) and Adams and Larrinaga-Gonzalez

(2007). Further to this, it is the position of the author that the relative youthfulness of the

SA academe potentially exacerbates the influence of the critical perspective.

16 There are at least eight academics involved in the SA research field who have published at least five SA empirical studies during the post-1995 period.

23

It is pertinent to note that Gray (2002) also observed that one of the key reasons for there

being a lack of prior systematic social accounting was due to the rise of the critical

perspective – Gray (2002, p.697) – ‘…a better explanation of the lack of prior systematic

social accounting – especially in AOS – was that only in recent years has the social

accounting phenomenon attracted the systematic attention of the alternate/critical

theorists.’

7. Policy implications of non-engagement

The key policy implication of non-engagement which has been characteristic of much of

the SA research to date is the abdication of the SA academe from what the authors view

as a clear role that SA has to play in effecting change in a manner consistent with the

underlying values upon which SA is grounded. The leads directly to the SA academe

being left out in the dark with regard to the development of new accountings (for

example, the Global Reporting Initiative), with a very real risk of the SA academe’s

agenda being limited to the critiquing the subsequent implementation of these new

accountings. It is acknowledged that members of the SA academe are engaged in real

and tangible ways in the development of new accountings, but this involvement is limited

to those members of the academy who have seen the need for and importance of

engagement with the field.

This abdication was hinted as by Tinker and Gray (2003, p.748) when they claimed that

when corporations moved from social reporting to “sustainability reporting” during the

1990s, the corporate sector effectively moved attention away from simple and understood

ideas to an idea (that is, sustainability) which was not well understood, ‘…but on which

they have a ten-year head-start in controlling the agenda…’ and that the (SA) academe let

them do it! All arguments about the contestability of the premise of this claim aside (and

there are a few), it is the position of the authors that the SA academe has never had

‘control’ of the SA agenda at any time during its existence. Indeed, at best the SA

academe has been reactive rather than pro-active, with the possible exceptions of the

24

policy developments by Bebbington and Thomson (1996) and Bebbington et al. (2001).

The problem with all this is that no matter how justified one’s sense of moral outrage at

the inadequacies and/or injustices of the status quo (conventional accounting paradigm

and market capitalism) may be (or at least appear to be) with regard to social and

environmental impacts of economic activity – and there are plenty of examples of this in

the SA literature17 - such outrage combined with non-engagement will never contribute to

bringing about change (Parker 2005). What is needed is solutions to the problems we are

facing and which escape the capture of the conventional accounting paradigm.

8. Where to from here? Charting a way forward for SA research

Given the findings and discussion in the preceding sections of this review, it is not

surprising that the key exhortation of this review is that ‘change’ must be re-asserted as

one of the key agendas of the SA academe. This change agenda can be re-invigorated

through the adoption of the following recommendations:

Firstly, greater attention needs to be paid to improving the rigor of SA studies, which

includes either developing new frameworks within which change can be examined, or

employing many of the change frameworks that have been used successfully in other

fields of academic research such as the management literature. Such frameworks need to

carefully explicate the social structures and tensions at both the societal and

organizational levels of analysis so that the mechanisms of social or organizational

change can be clearly articulated.

This will necessarily entail a move away from what Parker (2005) describes as the

augmentation theories, which include the positivist (economic agency and decision-

usefulness) and political economy (stakeholder and legitimacy) theories. Although these

theoretical perspectives have contributed to the burgeoning SA empirical literature, they

tend to be symptomatic of a much deeper concern that the author has with the SA

17 For example, Bebbington et al. 1997; Tinker and Gray 2003; Gray et al. 2007.

25

empirical research agenda – that is, a preoccupation with managerialist research on the

one hand, and a preoccupation with macro-social research on the other, with neither

talking the core question of how can change be brought about.

Secondly, the SA academe needs to engage with the field through organization-based

research which examines the interaction of SA with internal organizational and external

societal dynamics, thereby providing insight into factors that may drive or prevent change

at both an organizational and societal level of analysis. As such, it is the view of the

authors that the SA academe needs to seriously embrace an engagement-based action

research agenda which must also involve the development of new imaginings as

alternatives to the status quo. The authors are in agreement with Adams and Larrinaga-

Gonzalez (2007, p.337) who, in commenting upon the lack of engagement between the

SA academe and the field, contended that ‘…social and environmental accounting and

reporting scholars will not realise their desire to see organizational change towards

greater social and environmental accountability and responsibility unless this gap in the

research is filled’. The engagement-based action-research approach adopted by Adams

and McNicholas (2007) in their work with a public sector water utility company is, in this

sense, a watershed in the SA research agenda.

Such calls for an engagement-based action research agenda will inevitably lead to

criticisms from the critical school that such an agenda necessarily involves a ‘selling of

one’s soul’ to the interests of market capitalism and all that that entails, and will

ultimately lead to the legitimation of the status quo. But in the words of Gray (2002,

p.701), ‘(T)o bleat about engagement and the purity of the alternative / critical soul is

fiddling while Rome burns, and ‘Rome’ is certainly burning. Social (SA) accounting

may be naïve, under-theorised and in constant jeopardy of corporate capture – but what

other alternative is on offer?’

26

APPENDIX 1 – Journals from which SA studies have been sourced

Journal 1970s 1980s 1990s 2000+ Total Accountability & Performance 2 1 3 Contemporary Accounting Research 1 1 Business Strategy and the Environment 1 16 17 Sloan Management Review 1 1 California Management Review 2 2 Academy of Management Review 1 1 Stand-alone report 2 6 23 31 Journal of Accounting Audit & Finance 3 3 British Accounting Review 4 8 12 The Accounting Review 5 3 1 9 International Journal of Commerce & Management 1 1 Accounting Organizations and Society 10 5 6 6 27 Eco-Management & Auditing 2 2 Journal of Accounting Research 1 1 2 Accounting & Business Research 1 2 3 Journal of Business Finance & Accounting 1 1 1 3 Journal of Accounting & Public Policy 5 7 12 Cost & Management 1 1 Interdisciplinary Environment Review 1 1 Financial Management 1 1 European Accounting Review 1 1 Accountancy 1 1 Chartered Accountant in Australia 1 1 2 Pacific Accounting Review 1 1 2 Advances in Public Interest Accounting 4 4 Accounting Forum 4 11 15 Critical Perspectives on Accounting 1 6 7 Journal of Business Ethics 1 3 4 Accounting Auditing & Accountability Journal 2 13 20 35 Abacus 1 1 Accounting Horizons 1 1 International Journal of Accounting 6 2 8 Edited Volume 1 1 Accounting Research Journal 2 2 Business Ethics: A European Review 1 1 International Journal of Environmental Technology & Mgt

1 1

Journal of Business Strategies 1 1 Managerial Auditing Journal 1 1 Organization & Environment 1 1 Corporate Communications 1 1 Corporate Social Responsibility & Environmental Mgt

7 7

Management Communications Quarterly 1 1 Journal of International Business Studies 1 1 Australian Journal of Social Issues 1 1

27

Management of Environmental Quality: An Int’l Journal

2 2

International Journal of Commerce & Management 1 1 Australian Journal of Natural Resources Law & Policy

1 1

The TQM Magazine 1 1 Total 26 16 66 130 238

APPENDIX 1 – Accounting Journals from which SA studies have been sourced

Journal 1970s 1980s 1990s 2000+ Total Contemporary Accounting Research 1 1 Journal of Accounting Audit & Finance 3 3 British Accounting Review 4 8 12 The Accounting Review 5 3 1 9 Accounting Organizations and Society 10 5 6 6 27 Journal of Accounting Research 1 1 2 Accounting & Business Research 1 2 3 Journal of Business Finance & Accounting 1 1 1 3 Journal of Accounting & Public Policy 5 7 12 Cost & Management 1 1 European Accounting Review 1 1 Accountancy 1 1 Chartered Accountant in Australia 1 1 2 Pacific Accounting Review 1 1 2 Advances in Public Interest Accounting 4 4 Accounting Forum 4 11 15 Critical Perspectives on Accounting 1 6 7 Accounting Auditing & Accountability Journal 2 13 20 35 Abacus 1 1 Accounting Horizons 1 1 International Journal of Accounting 6 2 8 Accounting Research Journal 2 2 Managerial Auditing Journal 1 1 Total 26 16 66 130 238

28

APPENDIX 2 – Non-Accounting Journals from which SA studies have been sourced Journal 1970s 1980s 1990s 2000+ Total Accountability & Performance 2 1 3 Business Strategy and the Environment 1 16 17 Sloan Management Review 1 1 California Management Review 2 2 Academy of Management Review 1 1 Stand-alone report 2 6 23 31 International Journal of Commerce & Management 1 1 Eco-Management & Auditing 2 2 Interdisciplinary Environment Review 1 1 Financial Management 1 1 Journal of Business Ethics 1 3 4 Edited Volume 1 1 Business Ethics: A European Review 1 1 International Journal of Environmental Technology & Mgt

1 1

Journal of Business Strategies 1 1 Organization & Environment 1 1 Corporate Communications 1 1 Corporate Social Responsibility & Environmental Mgt

7 7

Management Communications Quarterly 1 1 Journal of International Business Studies 1 1 Australian Journal of Social Issues 1 1 Management of Environmental Quality: An Int’l Journal

2 2

International Journal of Commerce & Management 1 1 Australian Journal of Natural Resources Law & Policy

1 1

The TQM Magazine 1 1 Total 26 16 66 130 238

29

References Adams, C.A. 2002, ‘Internal organisational factors influencing corporate social and ethical reporting: Beyond current theorising,’ Accounting, Auditing & Accountability Journal, Vol.15, No.2, pp.223-50. Adams, C.A. and Larrinaga-Gonzalez, C. 2007, ‘Engaging with organizations in pursuit of improved sustainability accounting and performance,’ Accounting, Auditing & Accountability Journal, Vol.20, No.3, pp.333-55. Adams, C.A. and McNicholas, P. 2007, ‘Making a difference: Sustainability reporting, accountability and organisational change,’ Accounting, Auditing & Accountability Journal, Vol.20, No.3, pp.382-402. American Accounting Association (AAA) 1973, Proceedings on the Committee on Environmental Effects of Organization Behavior, The Accounting Review Supplement. American Accounting Association (AAA) 1974, Report of the Committee on the Measurement of Social Costs, The Accounting Review Supplement. American Accounting Association (AAA) 1975a, Proceedings on the Committee on Social Costs, The Accounting Review Supplement. American Accounting Association (AAA) 1975b, Report of the Committee on Accounting for Social Performance, The Accounting Review, pp.38-69. Ansari, S. & Euske, K.J. 1987, ‘Rational, rationalizing, and reifying uses of accounting data in organizations,’ Accounting, Organizations and Society, Vol.12, No.6, pp.549-70. Atkinson, A.A. and Shaffir, W. 1998, ‘Standards for field research in Management Accounting,’ Journal of Management Accounting Research, Vol.10, pp.41-68. Babbie, E. 1989, The Practice of Social Research, 5th Ed., Wadsworth Publishing Company: Belmont, CA. Beams, F.A. and Fertyg, P.E. 1971, ‘Pollution control through social cost conversion,’ Journal of Accountancy, Vol.132, No.5, November, pp.37-42. Bebbington, J. 1997, ‘Engagement, education and sustainability: A review essay on environmental accounting,’ Accounting, Auditing & Accountability Journal, Vol.10, No.3, pp.365-81. Bebbington, J., Gray, R., and Owen, D. 1999, ‘Seeing the wood for the trees: Taking the pulse of social and environmental accounting,’ Accounting, Auditing & Accountability Journal, Vol.12, No.1, pp.47-51.

30

Bebbington, J., Gray, R., Hibbitt, C. and Kirk, E. 2001, Full Cost Accounting: An Agenda for Action, Certified Accountants Educational Trust, London. Bebbington, J. and Gray, R. 2001, ‘An account of sustainability: Failure, success and a reconceptualization,’ Critical Perspectives on Accounting, Vol.12, No., pp.557-87. Bebbington, K.J. and Thomson, I. 1996, Business Conceptions of Sustainability and the Implications for Accountancy, ACCA, London. Bebbington, K.J., Gray, R.H., Hibbitt, C. and Kirk, E. 2001, Full Cost Accounting: An Agenda for Action, ACCA, London. Beyer, R. 1969, ‘The modern management approach to a program of social improvement,’ Journal of Accountancy, Vol.127, No.3, March, pp.37-46. Boland, R.J. 1989, ‘Beyond the objectivist and the subjectivist: Learning to read accounting as text,’ Accounting, Organizations and Society, Vol.14, No.5-6, pp.591-604. Boland, R.J. and Pondy, L.R. 1983, ‘Accounting in organizations: A union of natural and rational perspectives,’ Accounting, Organizations and Society, Vol.8, No.2-3 , pp.223-34. Broadbent, J., Ciancanelli, P., Gallhofer, S. and Haslam, J. 1997, ‘Enabling accounting: The way forward?’ Accounting, Auditing & Accountability Journal, Vol. , No. , pp.265-75. Buehler, V.M. and Shetty, Y.K. 1976, ‘Managerial response to social responsibility challenge,’ Academy of Management Journal, Vol.19, No.1, March, pp.66-78. Burchell, S., Chubb, C., Hopwood, A., Hughes, J. and Nahapiet, J. 1980, ‘The role of accounting in organizations and society,’ Accounting, Organizations and Society, Vol.5, No.1, pp.5-27. Burgess, R.G. 2005, ‘Approaches to Field Research,’ Chapter 2 (pp.13-32) in C. Pole (Ed.), Fieldwork: Sage Benchmarks in Social Science Research Methods, Sage Publications: London. Burrell, G. 1987, ‘No accounting for sexuality,’ Accounting, Organizations and Society, Vol.12, No.1, pp.89-102. Chastain, C.E. 1973, ‘A new role for accountants: Accounting for environmental expenditures,’ Business and Society, Vol.14, No.1, Fall, pp.5-12. Chua, W.F. 1986, ‘Theoretical constructions of and by the real,’ Accounting, Organizations and Society, Vol.11, No.6, pp.583-98.

31

Churchman, C.W. 1971, ‘On the facility, felicity, and morality of measuring social change,’ The Accounting Review, January, pp.30-35. Churchill, N.C. 1973, ‘The accountant’s role in social responsibility,’ in The Accountant in a Changing Business Environment, papers presented for discussion in the University of Florida Distinguished Accountants Seminar Series 1970-71 (University of Florida Accounting Series No.8), The University of Florida, pp.14-27. Churchill, N.C. 1974, ‘Toward a theory for social accounting,’ Sloan Management Review, Vol.15, No.3, pp.1-17. Committee on Economic Development (U.S.) 1971, Social Responsibilities of Business Corporations, New York. Cooper, C., Taylor, P., Smith, N. and Catchpowle, L. 2005, ‘A discussion of the political potential of social accounting,’ Critical Perspectives on Accounting, Vol.16, pp.951-74. Davis, K. 1960, ‘Can business afford to ignore social responsibilities?’ California Management Review, Vol.2, No.3, Spring, pp.70-76. Davis, K. 1973, ‘The case for and against business assumption of social responsibilities,’ Academy of Management Journal, Vol.16, No.2, June, pp.312-22. Davis, K. 1976, ‘Social responsibility is inevitable,’ California Management Review, Vol.19, No.1, Fall, pp.14-20. Deegan, C. 2003, Environmental Management Accounting: An Introduction and Case Studies for Australia, Environment Protection Authority of Victoria (EPA Victoria). Dierkes, M. 1979, ‘Corporate social reporting in Germany: Conceptual developments and practical experience,’ Accounting, Organizations and Society, Vol.4, No.1-2, pp.87-107. Dillard, J.F. 1991, ‘Accounting as a critical social science,’ Accounting, Auditing & Accountability Journal, Vol.4, No.1, pp.8-28. Dillard, J.F. 2007, Legitimating the social accounting project: An ethic of accountability, Chapter 2 in Bebbington et al. , pp.37-53. Dillard, J.F., Brown, D. and Marshall, R.S. 2005, ‘An environmentally enlightened accounting,’ Accounting Forum, Vol.29, pp.77-101. Dilley, S.C. and Weygandt, J.J. 1973, ‘Measuring social responsibility: An empirical test,’ Journal of Accountancy, Vol.136, No.3, September, pp.62-70. Elliott, R.K. 1972, ‘Accounting in the technological age,’ Journal of Accountancy, Vol.134, No.1, July, pp.70-73.

32

Elliot, R.K. and Rosenthal, S.I. 1973, ‘Social Accounting – An Annotated Biography,’ in Journal of Accountancy, Vol.136, No.1, July, pp.75-78. Epstein, M., Flamholtz, E. and McDonough, J.J. 1976, ‘Corporate social accounting in the United States of America: State of the art and future prospects,’ Accounting, Organizations and Society, Vol.1, No.1, pp.23-42. Estes, R.W. 1970, ‘The accountant’s social responsibility,’ Journal of Accountancy, Vol.129, No.1, January, pp.40-43. Estes, R.W. 1972, ‘Socio-economic accounting and external diseconomies,’ The Accounting Review, April, pp.284-90. Ferreira, L.D. and Merchant, K.A. 1992, ‘Field research in Management Accounting and Control: A review and evaluation,’ Accounting, Auditing & Accountability Journal, Vol.5, No.4, pp.3-34. Flannery, T. 2005, The Weather Makers – The History and Future Impact of Climate Change, The Text Publishing Company, Melbourne, Australia. Gaede, W.G. 1974, ‘Environmental management opportunities for the CPA,’ Journal of Accountancy, Vol.137, No.5, May, pp.50-54. Gallhofer, S. and Haslam, J. 1997, ‘Beyond accounting: The possibilities of accounting and ‘critical’ accounting research,’ Critical Perspectives on Accounting, Vol.8, No.1-2. pp.71-95. Gray, R. 1992, ‘Accounting and environmentalism: An exploration of the challenge of gently accounting for accountability, transparency and sustainability,’ Accounting, Organizations and Society, Vol.17, No.5, pp.399-425. Gray, R. 1998, ‘Imagination, a bowl of petunias and social accounting,’ Critical Perspectives on Accounting, Vol.9, pp.205-16. Gray, R. 2002a, ‘The social accounting project and Accounting Organizations and Society: Privileging engagement, imaginings, new accountings and pragmatism over critique?’ Accounting, Organizations and Society, Vol.27, pp.687-708. Gray, R. 2002b, ‘Of messiness, systems and sustainability: Towards a more social and environmental finance and accounting,’ British Accounting Review, Vol.34, pp.357-86. Gray, R., Owen, D. and Maunders, K. 1988, ‘Corporate social reporting: Emerging trends in accountability and the social contract,’ Accounting, Auditing & Accountability Journal, Vol.1, No.1, pp.6-20.

33

Gray, R., Kouhy, R. and Lavers, S. 1995, ‘Corporate social and environmental reporting: A review of the literature and a longitudinal study of UK disclosure,’ Accounting, Auditing & Accountability Journal, Vol.8, No.2, pp.47-77. Gray, R., Dey, C., Owen, D., Evans, R. and Zadek, S. 1997, ‘Struggling with the praxis of social accounting: stakeholders, accountability, audits and procedures,’ Accounting, Auditing & Accountability Journal, Vol.10, No.3, pp.325-64. Gray, R., Dillard, J. and Spence, C. 2007, ‘(Social) Accounting (Research) as if the World Matters: Postalgia and the new absurdism,’ paper presented at the 4th Asia Pacific Inter-disciplinary Research in Accounting (APIRA) conference, Auckland, New Zealand. Grojer, J. and Stark, A. 1977, ‘Social accounting: A Swedish attempt,’ Accounting, Organizations and Society, Vol.2, No.4, pp.349-86. Hackston, D. and Milne, M.J. 1996, ‘Some determinants of social and environmental disclosures in New Zealand companies,’ Accounting, Auditing & Accountability Journal, Vol.9, No.1, pp.77-108. Hay, R. and Gray, E., 1974, ‘Social responsibilities of business managers,’ Academy of Management Journal, Vol.17, No.1, March, pp.135-43. Heard, J.E. and Bolce, W.J. 1981, ‘The political significance of corporate social reporting in the United States of America,’ Accounting, Organizations and Society, Vol.6, No.3, pp.247-54. Herbohn, K. 2005, ‘A full cost environmental accounting experiment,’ Accounting, Organizations and Society, Vol.30, No., pp.519-36. Hines, R.D. 1991, ‘The FASB’s conceptual framework, financial accounting and the maintenance of the social world,’ Accounting, Organizations and Society, Vol.16, No.4, pp.313-31. Hogner, R.H. 1982, ‘Corporate social reporting: Eight decades of development,’ Research in Corporate Social Performance and Policy, Vol.4, pp.243-50. Larrinaga-Gonzalez, C. and Bebbington, J. 2001, ‘Accounting change or institutional appropriation? A case study of the implementation of environmental accounting,’ Critical Perspectives on Accounting, Vol.12, No. , pp.269-92. Lehman, C. and Tinker, T. 1987, ‘The “real” cultural significance of accounts,’ Accounting, Organizations and Society, Vol.12, No.5, pp.503-22. Linowes, D.F. 1968, ‘Socio-economic accounting,’ Journal of Accountancy, Vol.126, No.5, November, pp.37-42.

34

Marlin, J.T. 1973, ‘Accounting for pollution,’ Journal of Accountancy, Vol.135, No.2, February, pp.41-46. Mathews, M.R. 1997, ‘Twenty-five years of social and environmental accounting research: Is there a silver jubilee to celebrate?’ Accounting, Auditing & Accountability Journal, Vol.10, No.4, pp.481-531. Maunders, K.T. and Burritt, R.L. 1991, ‘Accounting and ecological crisis,’ Accounting, Auditing & Accountability Journal, Vol.4, No.3, pp.9-26. Merchant, K.A. and Van der Stede, W.A. 2006, ‘Field-based research in Accounting: Accomplishments and prospects,’ Behavioural Research in Accounting, Vol.18, pp.117-34. Meyer, G.D. 1971, ‘Management and the environment,’ Academy of Management Journal, Vol.14, No.1, March, pp.119-128. Miller, P. and O’Leary, T. 1987, ‘Accounting and the construction of the governable person,’ Accounting, Organizations and Society, Vol., No., pp.235-66. Mobley, S.C. 1970, ‘The challenges of socio-economic accounting,’ The Accounting Review, October, pp.762-68. Neimark, M. and Tinker, T. 1986, ‘The social construction of management control systems,’ Accounting, Organizations and Society, Vol.11, No.4-5, pp.369-96. O’Dwyer, B. 2003, ‘Conceptions of corporate social responsibility: the nature of managerial capture,’ Accounting, Auditing & Accountability Journal, Vol.16, No.4, pp.523-57. O’Dwyer, B. 2005, ‘The construction of a social account: A case study in an overseas aid agency,’ Accounting, Organizations and Society, Vol.30, No., pp.279-96. O’Dwyer, B., Unerman, J. and Bradley, J. 2005, ‘Perceptions on the emergence and future development of corporate social disclosure in Ireland,’ Accounting, Auditing & Accountability Journal, Vol.18, No.1, pp.14-43. Owen, D. 2008, ‘Chronicles of wasted time? A personal reflection on the current state of, and future prospects for, social and environmental accounting research,’ Accounting, Auditing & Accountability Journal, Vol.21, No.2, pp.240-67. Parker, J.E. 1971, ‘Accounting and ecology: a perspective,’ Journal of Accountancy, Vol.132, No.4, October, pp.41-46. Parker, L.D. 1986, ‘Polemical themes in social accounting: A scenario for standard setting,’ Advances in Public Interest Accounting, Vol.1, pp.67-93.

35

Parker, L.D. 1991, ‘External social accountability: Adventures in a maleficent world,’ Advances in Public Interest Accounting, Vol.4, pp.23-34. Parker, L.D. 2005, ‘Social and environmental accountability research: A view from the commentary box,’ Accounting, Auditing & Accountability Journal, Vol.18, No.6, pp.842-60. Patten, D.M. 1992, ‘Intra-industry environmental disclosures in response to the Alaskin oil spill: A note on legitimacy theory,’ Accounting, Organizations and Society, Vol.17, No.5, pp.471-75. Patten, D.M. 1995, ‘Variability in social disclosure: A legitimacy-based analysis,’ Advances in Public Interest Accounting, Vol.6, pp.273-85. Puxty, A.G. 1986, ‘Social accounting as immanent legitimation: A critique of a technicist ideology,’ Advances in Public Interest Accounting, Vol.1, pp.95-111. Puxty, A.G. 1991, ‘Social accountability and universal pragmatics,’ Advances in Public Interest Accounting, Vol.4, pp.35-45. Ratcliffe, T.A. and Munter, P. 1980, ‘The development of social accounting models: A comparative analysis,’ Business and Society, Vol.19/20, No.1/2, Winter, pp.56-66. Radcliffe, V.S., Campbell, D.R. and Fogarty, T.J. 2001, ‘Exploring downsizing: A case study on the use of accounting information,’ Journal of Management Accounting Research, Vol.13, pp.131-57. Roberts, R.W. 1992, ‘Determinants of corporate social responsibility disclosure: An application of stakeholder theory,’ Accounting, Organizations and Society, Vol.17, No.6, pp.595-612. Shields, M.D. 1997, ‘Research in Management Accounting by North Americans in the 1990s,’ Journal of Management Accounting Research, Vol.9, pp.3-61. Sikka, P., Willmott, H. and Puxty, T. 1995, ‘The mountains are still there: accounting academics and the bearings of intellectuals,’ Accounting, Auditing & Accountability Journal, Vol.8, No.3, pp.113-40. Singer, S.F. and Avery, D.T. 2007, Unstoppable Global Warming, Rowman & Littlefield Publishers Inc., Lanham, USA. Solomon, A. and Lewis, L. 2002, ‘Incentives and disincentives for corporate environmental disclosure,’ Business Strategy and the Environment, Vol.11, No.3, pp.154-69.

36

Tinker, T., Lehman, C. and Neimark, M. 1991, ‘Falling down the hole in the middle of the road: Political quietism in corporate social reporting,’ Accounting, Auditing & Accountability Journal, Vol.4, No.2, pp.28-54. Tinker, T. and Gray, R. 2003, ‘Beyond a critique of pure reason: From policy to policies to praxis in environmental and social research,’ Accounting, Auditing & Accountability Journal, Vol.16, No.5, pp.727-61. Ullmann, A.A. 1979, ‘Corporate social reporting: Political interests and conflicts in Germany,’ Accounting, Organizations and Society, Vol.4, No.1-2, pp.123-33. Ullmann, A.A. 1985, ‘Data in search of a theory: A critical examination of the relationships among social performance, social disclosure and economic performance of US firms,’ Academy of Management Review, Vol.10, No.3, pp.540-57. Unerman, J. 2003, ‘Enhancing organizational global hegemony with narrative accounting disclosures: An early example,’ Accounting Forum, Vol.27, No.4, pp.425-48. Vogel D., 1975, ‘The political and economic impact of current criticisms of business,’ California Management Review, Vol.18, No.2, Winter, pp.86-92. VonBerg, W.G. 1972, ‘Accounting for responsibility,’ Journal of Accountancy, Vol.134, No.5, November, pp.71-74. Votaw, D. and Sethi, S.P. 1969, ‘Do we need a new corporate response to a changing social environment,’ California Management Review, Vol.12, No.1, Fall, pp.3-16. Ward, B. and Dubos, R. 1973, ‘The price of pollution – Excepts from Chapter 7 of the book Only One Earth’ as cited in Journal of Accountancy, Vol.136, No.1, July, pp.62-68.

37

Figures to be included in text:

Figure 1 – Conventional accounting as a sub-set of SA

Source: Mobley 1970, p.762; Grojer and Stark, 1977, p.350; Gray et al. 1997, p.328; Gray 2002a, p.692.

Figure 2 - SA Empirical Studies by Year (1973-2007)

13

5 5 46 7

42 3

1 1 1 0 1 2 14 5

31 2

9 9 913 13

15

2723

16

2218

12

4

0

5

10

15

20

25

30

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

ECONOMIC

SOCIAL

ENVIRONMENTAL

Sustainability Accounting

Conventional Accounting

38

Figure 3 – Methodology employed

5

35 2717

124

40

9

020406080

100120140

Event

Case s

tudy /

field

study

Surve

y

Inter

views

Conten

t analy

sis

Labo

rato

ry /

Model

testin

g

Other

39

Tables to be included in text:

Table 1 – Criteria for evaluation of SA empirical studies

Criteria Specific questions asked 1. Discussion of ‘change’, ‘accountability’ and/or ‘transparency’

a. Is ‘change’ discussed in the study? b. Is ‘accountability’ discussed in the study? c. Is ‘transparency’ discussed in the study?

2. Rigorous development of proposals from a scholastic framework

a. Has theory been used in the study? b. What type of theorization has been used? c. How was the theorization developed? d. What theories have been used? e. Was theorization deductive or inductive?

3. Methodology a. Has the researcher engaged with the field? b. What has been the extent of the engagement? c. What primary research method has been used? d. What has been the focus of the study? e. What have been the primary data sources used?

4. Structures and tensions a. Have social structures and tensions been explicated?

b. Have organizational structures and tensions been explicated?

c. Have the mechanisms of social change been articulated / hypothesised?

d. Have the mechanisms of organizational change been articulated / hypothesised?

5. New imaginings a. Have there been attempts to develop, refine or implement ‘new imaginings’ in the SEA empirical work?

6. Interaction of SEA with internal organizational processes

b. Has the research identified the interaction of SEA with other organizational processes and/or dynamics?

c. Has the research enabled the identification of factors that might drive or prevent change?

d. Does the research provide insight into how SEA is being used re ‘capture’ debate?

40

Table 2 – Discussion of ‘change’, ‘accountability’ and ‘transparency’ in SA studies

Themes Have themes been discussed? Change Accountability Transparency Not discussed 237 229 243 Implicitly discussed 12 19 8 Explicitly discussed 3 4 1 Total 252 252 252

Table 3 – Type of theorization used in SA studies Type of theorization: Number a. Testing of an existing theory 57 b. Testing of propositions based upon prior literature / empirical studies 7 c. Testing of hypotheses based upon prior literature / empirical studies 24 d. Testing of model based upon prior literature / empirical studies 7 e. Emergent theory (akin to grounded theory) 10 105

Table 4 – Methods for testing existing theories in SA studies

Methods for testing existing theories: Number a. Theory operationalised via variables 8 b. Hypotheses development 15 c. Interpretive 30 d. Development and testing of a model based upon existing theory 4 57

41

Table 5 – Extent of engagement in SA studies

Number No engagement with the field 217 1 interview with each organization 12 2 interviews with each organization 5 3-4 interviews with each organization 0 Field visits (with a minimum of 5 interviews / visits with each organization) 12 Interviews – unknown number 6 252

Table 6 – SA studies involving high levels of engagement with the field

Author/s Focus of study Bebbington & Gray (2001)

Case study reports on an attempt to construct a ‘sustainable cost calculation’ account in a New Zealand Landcare organization, including why the attempt was made, how calculations were performed, and reflects on the tensions which emerged in the organization during this process.

Larrinaga-Gonzalez & Bebbington (2001)

A case study involving a Spanish electricity utility’s response to the environmental agenda in which the two themes of ‘organizational change’ and ‘institutional appropriation’ are examined.

Rahaman et al. (2004)