Embed Size (px)

Citation preview

Surety:

the alternative for

the bank

guarantee!

Paul Becue

General Manager EHSB

February 28, 2013

Ambos NBGO

2

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Agenda

1 Credit insurance and surety

2 Bonding: definition + terms

3 No shadow banking: legal regulations

4 Bonding market: world + USA + Europe + Belgium

5 Basel III: capital becomes more rare for banks

3

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

1 1 Credit insurance and surety

2 Bonding: definition + terms

3 No shadow banking: legal regulations

4 Bonding market: world + USA + Europe + Belgium

5 Basel III: capital becomes more rare for banks

4

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

INSURED

= SUPPLIER

= CREDITOR

CREDIT INSURER BUYER

= DEBTOR

PREVENTION

MONITORING

RECUPERATION

DE

LIV

ER

Y

PA

YM

EN

T

What is credit insurance?

Offered services

5

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

No commercial relationship CI with the debtor (buyer)

Surety/bonding is sometimes called the reverse of credit insurance:

- credit insurance: supplier is PH on his own behalf

- bonding: buyer/debtor is PH on behalf of the supplier/creditor =

contractual relationship with insurer

Legally credit insurance and bonding have in the case of reversed credit

insurance the same insured interest = the payment of the receivable on

behalf of the supplier

Reason why on the legal plan both are treated together in Belgian

and European law (CI: branch 14; surety: branch 15).

But nevertheless big differences: cf. contractual guarantees

Longer tenor, bigger amounts, risk of fraud, …

Credit insurance and surety/bonding

6

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

2 1 Credit insurance: the invisible bank

2 Bonding: definition + terms

3 No shadow banking: legal regulations

4 Bonding market: world + USA + Europe + Belgium

5 Basel III: capital becomes more rare for banks

7

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Bonds: definition

A written commitment by a financial institution (bank or insurance company) that covers the beneficiary (a client or a supplier) if the bonded company should be in default or not able to meet its obligations.

A written commitment by a financial institution (bank or insurance company) that covers the beneficiary (a client or a supplier) if the bonded company should be in default or not able to meet its obligations.

A three-way relationship

SellerContractor or bonded

party (or ‘debtor’)

BuyerBeneficiary

(or ‘creditor’)

IssuerEuler Hermes

Main contract

Bond

contract

Recourse

(if bond is

paid)

Reimbursement

Bond

Calling

of

guarantee

Payment

Bonds: definition

8

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

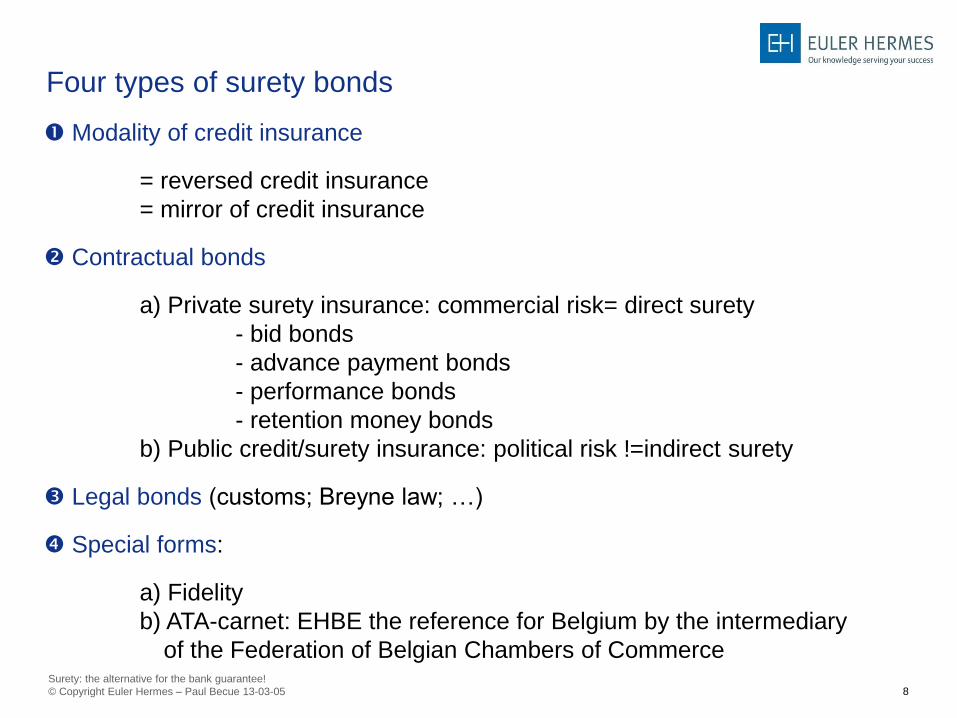

Modality of credit insurance

= reversed credit insurance

= mirror of credit insurance

Contractual bonds

a) Private surety insurance: commercial risk= direct surety

- bid bonds

- advance payment bonds

- performance bonds

- retention money bonds

b) Public credit/surety insurance: political risk !=indirect surety

Legal bonds (customs; Breyne law; …)

Special forms:

a) Fidelity

b) ATA-carnet: EHBE the reference for Belgium by the intermediary

of the Federation of Belgian Chambers of Commerce

Four types of surety bonds

9

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Bonding/bond is the general term in insurance and banking business

Bond: not to be confused with long term debt paper

A/ Insurance: surety

Insurance: surety is reflected in the ICC Uniform rules of contract

bonds (1993-2000):

- exceptions are possible based on the principal contract

- accessory nature

In practice evolution towards abstract nature

Two kinds of surety:

- direct (‘assurance cautionnement’) : private insurance (EHBE)

- indirect (‘assurance caution’) = kind of counter guarantee for thirds

who issued bonds: public insurance (ONDD)

B/ Banking: guarantees

Conditional guarantees (more exceptional)

Unconditional abstract guarantees (= on first demand) reflected in the

ICC Uniform Rules for Demand Guarantees (2010)

Confusion of terms

10

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

3 1 Credit insurance: the invisible bank

2 Bonding: definition + terms

3 No shadow banking: legal regulations

4 Bonding market: world + Europe + Belgium

5 Basel III: capital becomes more rare for banks

11

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Bonding: there’s reglementation

Linked to the real economy = no danger of bubbles

Surety:

-Europe: several directives + Solvency II (branch 15)

-Belgium: insurance legislation (art. 70-76 law 1992) +

prudential supervisor is NBB

-but not conform to Bonding practice

-more lined to practice credit insurance (art. 73-

74-75)

Banking:

-Prudential supervisor is NBB

-Legislation

-ICC Uniform Rules

Bonding is no shadow banking

12

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

4 1 Credit insurance and surety

2 Bonding: definition + terms

3 No shadow banking: legal regulations

4 Bonding market: world + USA + Europe +

Belgium

5 Basel III: capital becomes more rare for banks

13

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Selected markets In ‘000 USD

Selected surety markets

0

200.000

400.000

600.000

800.000

1.000.000

1.200.000

1.400.000

1.600.000

1.800.000

2004 2005 2006 2007 2008 2009

0

1.000.000

2.000.000

3.000.000

4.000.000

5.000.000

6.000.000

Germany Italy Latin America UK North America

14

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

The Global Surety Market

(1) Own estimation derived from Sigma Study No. 6 of Swiss Re 2006; Aon Re EMEA Feb. 2007

(2) Africa can be neglected except South Africa

In 2010 there is a total premium income of more than US-$ 11bn produced by

Bonding Insurance Companies. (1)

Break Down related to available market information:

Europe 18 % 14 %

North America 61 % 48 %

Latin- and South America 8 % 16 %

Asia / Australia (2) 13 % 22 %

Except in the Americas banks play an important or even dominating role in bond

providing for corporate companies.

Bank driven markets are proof of sustainable demands for bonds in numerous

sectors.

Development

2004 - 2009

15

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

World: market share of banks and surety writers in

selected countries (2003)

16

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

On a total premium income of 7,9 bn USD in the world (2005):

- 4,3 bn USD comes from the USA (= 56 %)

- Fidelity is responsible for ca. 930 mln USD of this amount

In 2009 5.2 bn USD in USA: since then stabilisation due to

crisis

Legal reason: Llewyn Commentary of 1946:

- Bonding/guarantees forbidden for the banks, and can only

be exercised by the insurance companies

- Reason why Standby L/C is so popular in US = kind of

deviation of this rule

Bonding is risky business!

- Beginning years 2000 thorough restructuring US market

- 6 of the top 10 players went bankrupt, or merged

World: USA is market leader

17

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

USA: top 5 controls more than 50 % of the US market

Company Direct Premium Written in

2009 (Millions USD)

Market share USA

(in %)

Travelers Bond 924.2 17.8

Liberty Mutual Ins. Group 723.2 13.9

Zurich Insurance Group 486.8 9.4

CNA Insurance Group 406.1 7.8

Chubb & Son Inc. Group 277.0 5.3

The rest 2,373.8 45.7

TOTAL

5,191.0 100.0

Source: The Surety & Fidelity Association of America (SFAA)

18

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

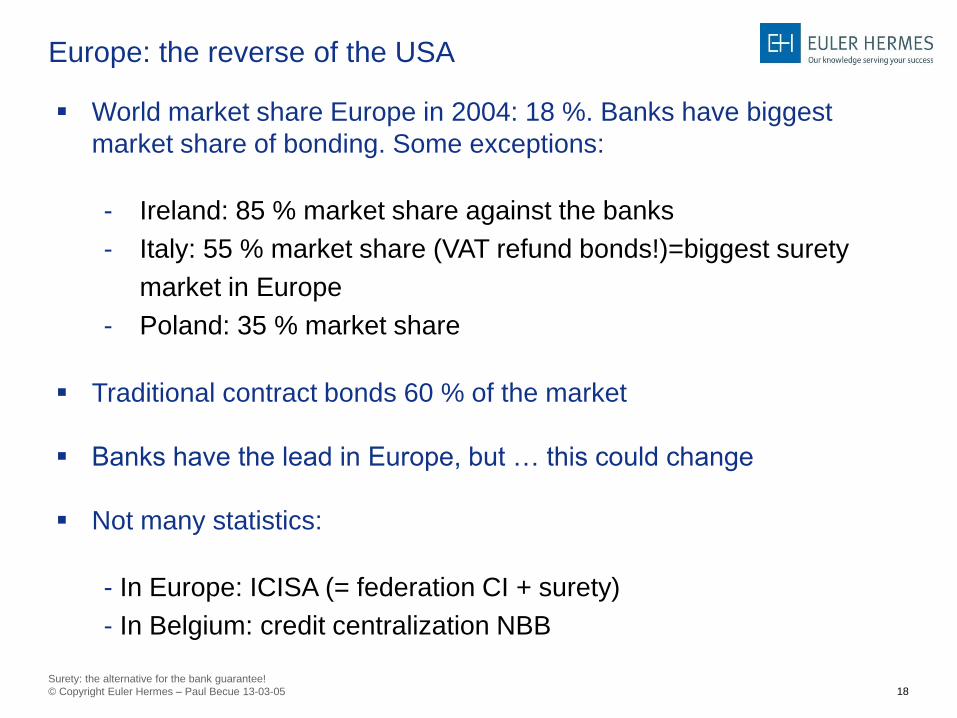

World market share Europe in 2004: 18 %. Banks have biggest

market share of bonding. Some exceptions:

- Ireland: 85 % market share against the banks

- Italy: 55 % market share (VAT refund bonds!)=biggest surety

market in Europe

- Poland: 35 % market share

Traditional contract bonds 60 % of the market

Banks have the lead in Europe, but … this could change

Not many statistics:

- In Europe: ICISA (= federation CI + surety)

- In Belgium: credit centralization NBB

Europe: the reverse of the USA

19

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

European Surety: premium & claims

2012: bad year with a lot of claims (cf. weak construction sector in several countries)

20

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Cf. Belgium: only 1,1 bn euro exposure (NBB CKO 1), but in reality higher

at 1,4 bn euro (reporting issues; without federations).

European Surety: insured exposure

21

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

The bonding market in Belgium (2007-2011)

In Thousand euro 2007 2008 2009 2010 2011 2011

Authorized Authorized Authorized Authorized Authorized

Share

(%)

Manufacturing industry 4 356 080 4 457 089 4 184 769 3 834 052 4 205 470 20.0%

Construction 5 096 449 5 843 879 6 117 897 5 815 903 5 859 272 27.9%

Wholesale and retail trade;

reparation autom vehicles and

motocycles 2 159 613 2 169 522 2 223 600 2 389 656 2 285 356 10.9%

Transports and warehousing 1 129 853 1 165 841 1 266 933 1 203 194 1 151 396 5.5%

Real estate activities 1 424 380 1 534 330 1 494 307 1 588 762 1 540 357 7.3%

Other sectors 4 641 683 9 065 094 8 026 562 8 423 870 5 953 893 28.4%

Total authorized lines 18 808 058 24 235 755 23 314 068 23 255 437 20 995 744 100.0%

Part insurance 237 620 343 443 1 348 667 1 211 874 1 116 465 5.3%

Part credit substitute 936 566 1 454 429 611 758 550 292 230 297 1.1%

Utilized lines 16 552 219 19 532 944 18 890 788 18 979 665 16 067 169 76.5%

In Thousand euro 2007 2008 2009 2010 2011 2011

Authorized Authorized Authorized Authorized Authorized

Share

(%)

Manufacturing industry 4 356 080 4 457 089 4 184 769 3 834 052 4 205 470 20.0%

Construction 5 096 449 5 843 879 6 117 897 5 815 903 5 859 272 27.9%

Wholesale and retail trade;

reparation autom vehicles and

motocycles 2 159 613 2 169 522 2 223 600 2 389 656 2 285 356 10.9%

Transports and warehousing 1 129 853 1 165 841 1 266 933 1 203 194 1 151 396 5.5%

Real estate activities 1 424 380 1 534 330 1 494 307 1 588 762 1 540 357 7.3%

Other sectors 4 641 683 9 065 094 8 026 562 8 423 870 5 953 893 28.4%

Total authorized lines 18 808 058 24 235 755 23 314 068 23 255 437 20 995 744 100.0%

Part insurance 237 620 343 443 1 348 667 1 211 874 1 116 465 5.3%

Part credit substitute 936 566 1 454 429 611 758 550 292 230 297 1.1%

Utilized lines 16 552 219 19 532 944 18 890 788 18 979 665 16 067 169 76.5%

Source: Credit Centralization National Bank of Belgium (CKO 1; CKO 2 starting May 1st, 2012)

22

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Market

- Highly dominated by banks (95 %)

- Only 1 specialized insurer and only 2 credit insurers active in

bonding

- Decrease in insured exposure due to the crisis (less activity)

- Surety institutions linked to professional federations (e.g.

construction) not in table

- NDD guarantees credit lines bank guarantees with banks=unfair

competition towards private surety insurers

Context

- Economic situation increases the need for bonding (cf. economic

uncertainty)

- Possible impacts of Basel III on banks capital allocation

Bonding in Belgium: an opportunity!

23

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

5 1 Credit insurance and surety

2 Bonding: definition + terms

3 No shadow banking: legal regulations

4 Bonding market: world + USA + Europe + Belgium

5 Basel III: capital becomes more rare for banks

24

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

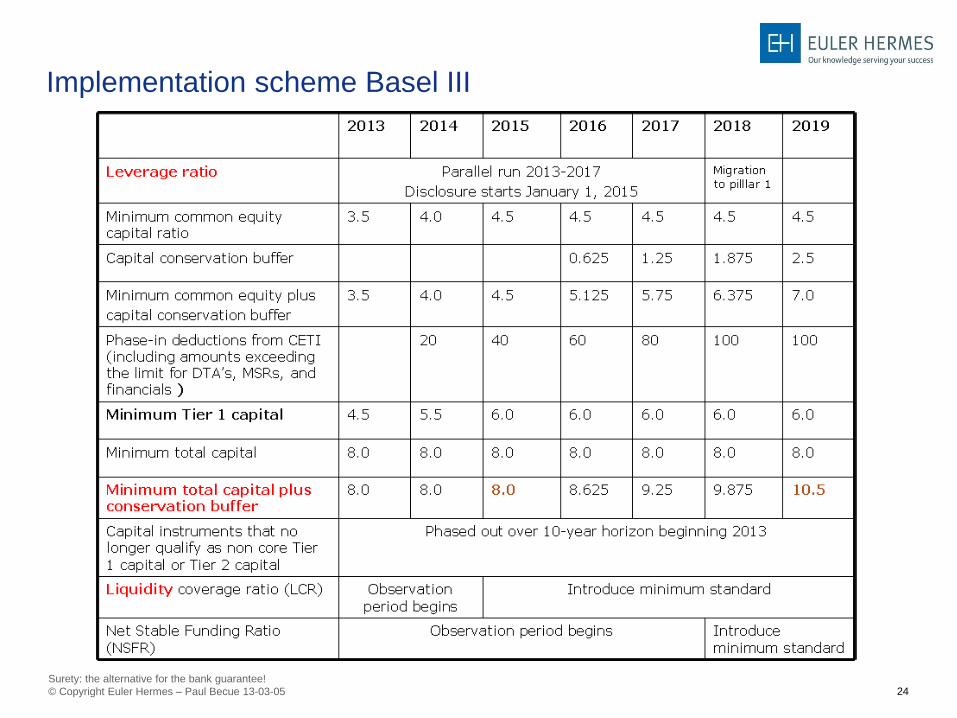

Implementation scheme Basel III

25

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Basel II: solvency

- Standardised approach allows weighting of 50 % for the bonds which

don’t substitute credit

- IRB approach allows even lower weightings

Reason why banks were in the past so keen on this product

Basel III: solvency + liquidity

- In principle no change of the weightings for bonds

- Solvency: from 8 % (Cooke ratio) towards 10,5 %

- Liquidity:

-LCR: cash out trade finance: 0-5 %=OK (ST: bank run 30 days)

-NSFR: ? (LT: avoid mismatch; cf. Dexia)

- But the leverage ratio (in principle > 3 %; 2018) doesn’t take into

consideration the philosophy of the (lower) weightings or off balance

products

Everything is in principle considered at 100 % for the

calculation of the leverage ratio (also Trade Finance products)

From Basel II towards Basel III

26

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

In Basel II L/C (20 %) and bonds (50 %) have an interesting weighting

for the bank sector.

This will change with Basel III due to the leverage ratio

Trade Finance products are nevertheless for the banks a relative low

risk:

- the self-liquidating nature

- fast turning and linked to trade: if the bills are not paid, the buyer

won’t get the necessary supplies

- recuperations are in general at 60 %

- ICC/ADB/WTO research: PD is at 0,022 % for Trade Finance in

2005-2010

Watch out:

- banks first do prevention (credit analysis)

- banks obtain sureties (credit insurance and surety don’t)

Basel III and Trade Finance

27

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Consequence Basel III:

- Capital will become more rare and expensive, which will lead to a

more selective attitude in credit granting and choice of credit

products: e.g. which products are less labour intensive, require

less capital, …

- Trade Finance will become relatively more expensive

This should create opportunities for surety:

- With reinsurance:

-there’s less need of capital (cf. context Solvency II

starting 2016?)

-there’s more capacity to commit risks

-Companies have interest in sourcing the available credit lines at as

many market participants as possible = diversification.

CONSEQUENCE Basel III for the banks

28

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Paul Becue: author of …

29

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Simplified version:

first in Dutch (ed. Lannoo), later in French (ed. Racine)

If you don’t have it yet, you can order it for free by

sending an e-mail to the following address:

Paul Becue: author of …

30

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Bonding article

Paul Becue: author of …

31

Surety: the alternative for the bank guarantee!

© Copyright Euler Hermes – Paul Becue 13-03-05

Thank you

for your attention.