Embed Size (px)

Citation preview

SUPPLY AND DEMAND: AN INTRODUCTION

Chapter 3 in Frank and Bernanke

Purpose of Lecture

• Review price formation in markets and market equilibrium through interaction of supply and demand curves

• Central Planning vs. Markets• Demand Curve• Supply Curve• Market Equilibrium• 3 Steps to Analyzing Changes in

Equilibrium

Central Planning vs. Markets

• How to organize economic activities in societies?

• Two basic options: 1. Central planning 2. Markets

• Central Planning Major economic decisions made centrally, by

individual or small group of individuals, on behalf of a larger group

The case for most of history with clans, tribes, extended families, empires

Centralized Economic Organizations• Agrarian society• Former Soviet Union• Cuba, North Korea• China• Bureaucracy

• Markets Production and distribution decisions left to

individuals interacting in private markets Market or capitalist economies

• Mixed economies• Social control over markets

Decentralized decision-making by individuals Coordination of decisions through markets Prices from the different markets signal

information and the individual choices to coordinate this decentralized behavior

• Market A market consists of all buyers and sellers of

a good or service Buyers as a group determine demand for the

product Sellers as a group determine the supply of the

product

• Competitive Market Market in which there are many buyers and

many sellers, so that each has a negligible impact on the market price

• Conservation and Management of Resources and Environment by Principle of Central Planning or Markets Command-and-control regulations vs. market-based Analogous to central planning vs. markets Market-Based

Give decentralized decision-making by economic agents involved

Economic agents more likely to face full social costs of their decisions

Give positive economic incentives

Command-and-Control Sometimes necessary

Demand

• Quantity demanded The amount of a good that buyers are willing

and able to purchase

• Law of Demand Quantity demanded is inversely related to

price, all other things equal (held constant)• As price rises, quantity demanded falls• As price falls, quantity demanded rises

• Demand Schedule Table showing the quantity of a good that

buyers wish to buy at each price

Price of Good ($/kg) Quantity of Good (kg)

---------------------------- --------------------------------

0 10

1 9

2 8

3 7

Demand CurveGraph of the relationship between the price of a good and

the quantity demanded

Figure 3.1

Demand CurveFigure 3.1

8 12 16

The buyers reservation price: The highest price the buyer would be willing to pay for a good4

2

3

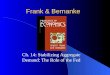

Demand

Horizontal Interpretation

Price determines quantity demanded

Price($ per slice)

4

2

3

8 12 16

Demand

Price($/unit)

Quantity(# units per time period)

Price determines quantity demanded

Price determines quantity demanded

Demand

Vertical Interpretation

Quantity measures the marginal buyer’s reservation price

Price($ per slice)

4

2

3

8 12 16

Demand

Quantity measures the marginal buyer’s reservation price

Quantity measures the marginalbuyer’s reservation price

Price($/unit)

Quantity(# units per time period)

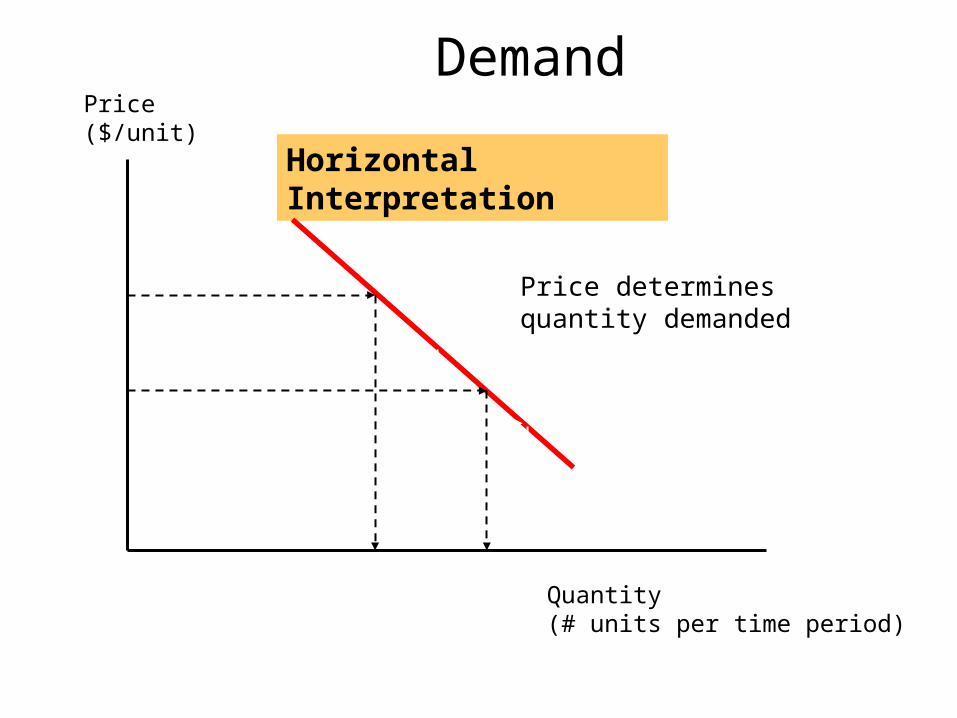

• Distinguish Between A change in the quantity demanded

• A movement along the demand curve that occurs in response to a change in price

A change in demand• A shift of the entire demand curve• Caused by change in factors of demand that are

otherwise held constant when examine price-quantity demanded relationship

• Movements Along The Demand Curve Changes in the price of the good or service lead to movements

along the demand curvePrice ($/kg)

P0

P1

Q0 Q1 Quantity demanded (kg per time period)

• Shifts in the Demand Curve

Price ($/kg)

D1

D0

D2

Quantity demanded ($/kg)

Increase in demand

Decrease in demand

An Increase in the Quantity Demanded versus an Increase in

Demand

Figure 3.10

• Variables That Can Shift Demand Curve Income

• Normal good A good for which, other things equal, an increase in

income leads to an increase in demand

• Inferior good A good for which, other things equal, an increase in

income leads to a decrease in demand

• The Income Effect The change in the quantity demanded of a good that

results because a change in the price of a good changes the buyer’s purchasing power

• Variables That Shift Demand, Cont’d. Prices of Related Goods

• Substitutes Two goods for which an increase in the price of one

leads to an increase in the demand for the other. Substitutes are often pairs of goods that are used in

place of each other, such as coffee and tea.

• Complements Two goods for which an increase in the price of one

leads to a decrease in the demand for the other. Complements are often pairs of goods that are used

together, such as gasoline and automobiles.

Variables That Shift Demand, Cont’d.

• Variables That Shift Demand, Cont’d. Prices of Related Goods, Cont’d.

• The Substitution Effect The change in the quantity demanded of a good that

results because buyers switch to substitutes when the price of the good changes

Variables That Shift Demand, Cont’d.

• Tastes and Preferences Most obvious determinant of consumer

demand

• Expectations Expectations about future may affect

consumer demand for a good or service today

• Number of Buyers The more buyers of a good or service, the

greater the market demand.

Variables That Influence Buyers

Variable A Change in This Variable …

Price Represents a movement along the demand curve

Income Shifts the demand curve

Prices of related goods Shifts the demand curve

Tastes and preferences

Shifts the demand curve

Expectations Shifts the demand curve

Number of buyers (Population)

Shifts the demand curve

Supply

• Quantity supplied The amount of a good or service that sellers

are willing and able to sell

• Law of Supply Quantity demanded is positively related to

price, all other things equal (held constant)• As price rises, quantity supplied rises• As price falls, quantity supplied rises

• Supply Schedule A table that shows the relationship between

the price of a good and the quantity supplied

Price of Good ($/kg) Quantity of Good (kg)

---------------------------- --------------------------------

1 7

2 8

3 9

4 10

5 11

Supply CurveA graph of the relationship between the price of a good and

the quantity supplied

Figure 3.2

• Seller’s Reservation Price The smallest dollar amount for which a seller

would be willing to sell an additional unit Generally equal to marginal cost

Quantity

Price Supply

Reservation price for 10th unit

105

Reservation price for 5th unit

Supply

Price($ per slice)

4

2

3

8 12 16

Supply

Horizontal Interpretation

Shows the quantity produced

for each price

Price($/unit)

Quantity(# units per time period)

Supply

Price($ per slice)

Quantity(1000s of slices per day)

4

2

3

8 12 16

Supply

Vertical Interpretation

Shows the marginal cost (reservation

price) for producing each additional unit

Quantity(# units per time period)

Price($/unit)

• Movements Along The Supply Curve Changes in the price of the good or service lead to movements

along the supply curvePrice ($/kg)

P1

P0

Q0 Q1 Quantity supplied ($/kg)

• Shifts in the Supply CurvePrice ($/kg) S1

S0

S2

Quantity supplied (kg)

Increase in supply

Decrease in supply

• Variables That Can Shift The Supply Curve Input Prices

• Increase in price of an input raises costs and makes production less profitable, thereby lowering supply (and shifting supply curve in)

• Decrease in price of an input lowers costs and makes production more profitable, thereby increasing supply (and shifting supply curve out)

Technology• Technical progress lowers costs and makes production more

profitable, thereby increasing supply (and shifting supply curve out)

Expectations Number of Sellers

Variables That Influence Sellers

Variable A Change in This Variable …

Price Represents a movement along the supply curve

Input prices Shifts the supply curve

Technology Shifts the supply curve

Expectations Shifts the supply curve

Number of buyers Shifts the supply curve

Market Equilibrium: Supply and Demand Together

Price ($/kg)

S

D

Quantity (kg/time period)

Equilibrium price

Equilibrium quantity

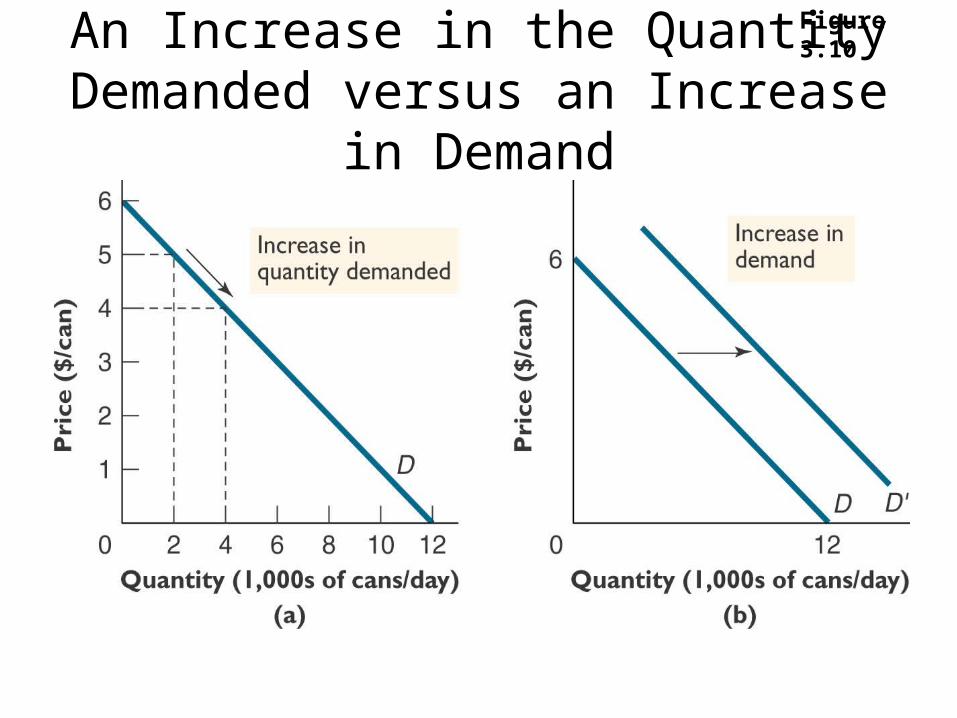

Equilibrium: Quantity Demand = Quantity Supplied

Market Equilibrium• Point where supply and demand curves intersect• Situation in which the price has reached the level

where quantity supplied equals quantity demanded Market Equilibrium Price

• Price at intersection called market equilibrium priceo Sometimes called market clearing price

• Price that balances quantity supplied and quantity demanded

• Supply price equals demand price Market Equilibrium Quantity

• Quantity supplied and quantity demanded at the equilibrium price

• Surplus or Excess Supply Excess quantity supplied at given price Suppliers unable to sell all they want at the

going price Sellers respond by cutting their prices Falling prices, in turn, increase quantity

demanded and decrease quantity supplied Prices continue to fall until the market reaches

equilibrium

• Excess Supply or Surplus Situation in which quantity supplied is greater than the

quantity demanded at given price

Price ($/kg) Supply

Demand

Quantity (kg/time period)

Excess Supply

Quantity demandedQuantity supplied

EquilibriumQuantity

EquilibriumPrice

• Excess Demand or Shortage Situation in which quantity demanded is greater than

the quantity supplied at given price

Price ($/kg) Supply

Demand

Quantity (kg/time period)

Excess Demand

Quantity demandedQuantity supplied

Equilibrium Price

Equilibrium Quantity

• Shortage or Excess Demand Excess quantity demanded at given price Buyers unable to purchase all they want at

the going price• Too many buyers chasing too few goods

Buyers respond by bidding up their prices Sellers respond to shortage by raising their

prices As price rises, quantity demanded falls,

quantity supplied rises Prices continue to rise until the market

reaches equilibrium

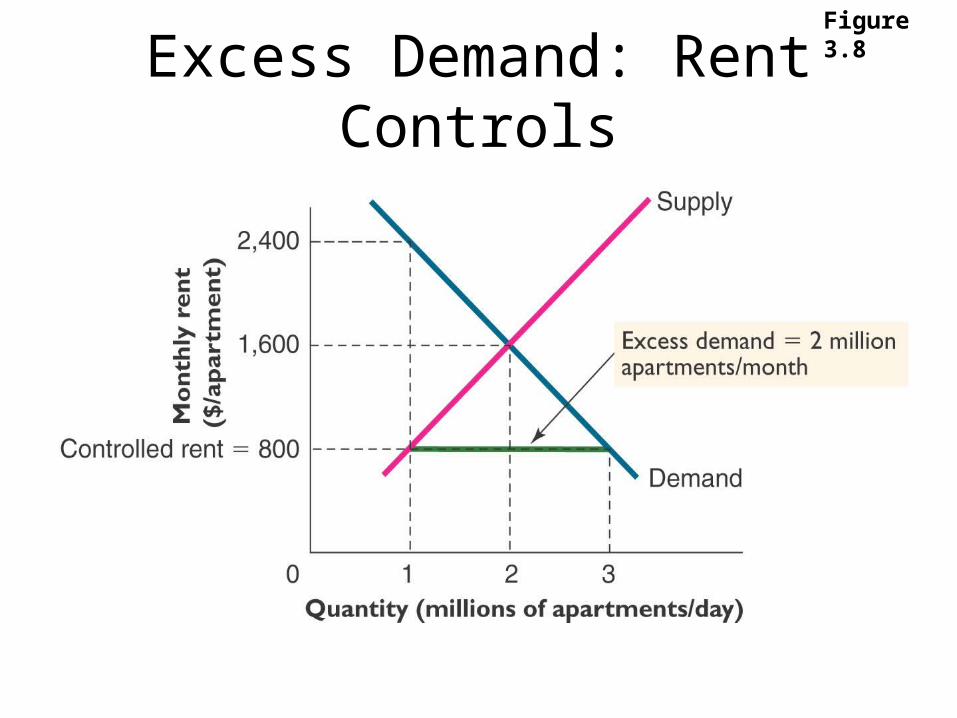

• Rent Controls Example of excess demand in market

An Unregulated Housing Market

Figure 3.7

Excess Demand: Rent Controls

Figure 3.8

Example: The Effect of Minimum Wage Legislation on Employment

The Effect of Minimum Wage Legislation on Employment

Figure 13.5

• Law of Supply and Demand Price of any good adjusts to bring the quantity

supplied and quantity demanded for that good into balance

Three Steps to Analyzing Changes in Equilibrium

• 1. Decide whether the event changes supply or demand (or perhaps both)

• 2. Decide in which direction the supply or demand curve shifts

• 3. Use the supply-and-demand diagram to see how the shift changes the equilibrium price and quantity

• Increase in DemandPrice ($/kg) Supply

D1

D0

Quantity (kg)

1. Increase in demand …

2…result in a higher price…

3…and a higher quantity sold.

Initial equilibrium

New equilibrium

• Example of Shift in Demand and Complement Goods Complements Decrease in price of one

causes a rightward shift in demand curve for other

Tennis courts and tennis balls are complements

Decline in court-rental fees shifts demand curve for tennis balls rightward from D to D’

The Effect on the Market for Tennis Balls of a Decline in Court Rentals

Fees

Figure 3.11

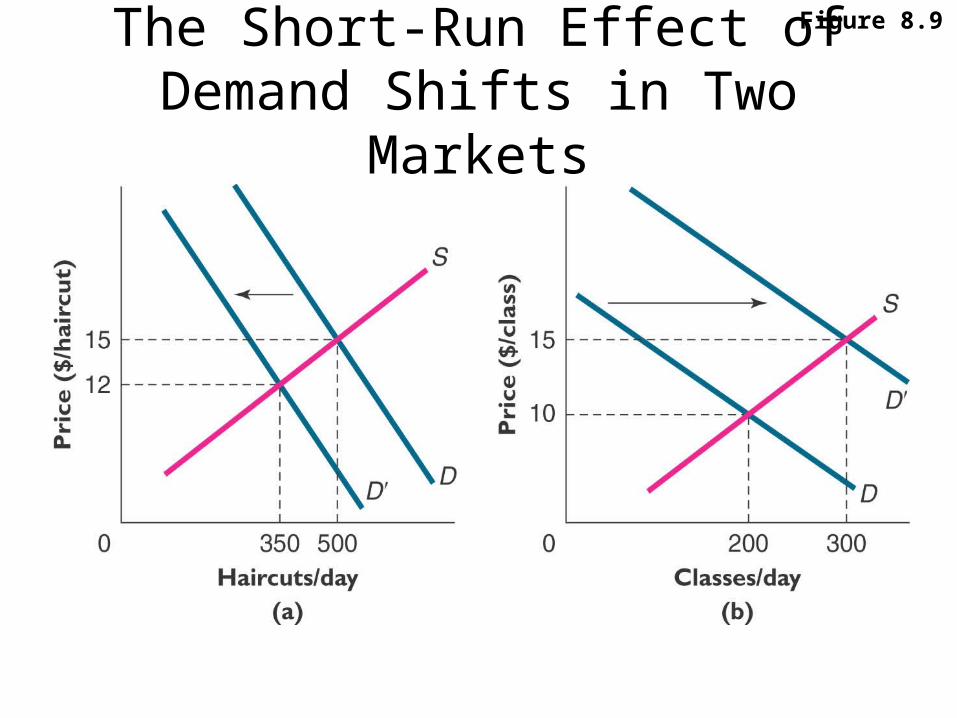

The Short-Run Effect of Demand Shifts in Two Markets

Figure 8.9

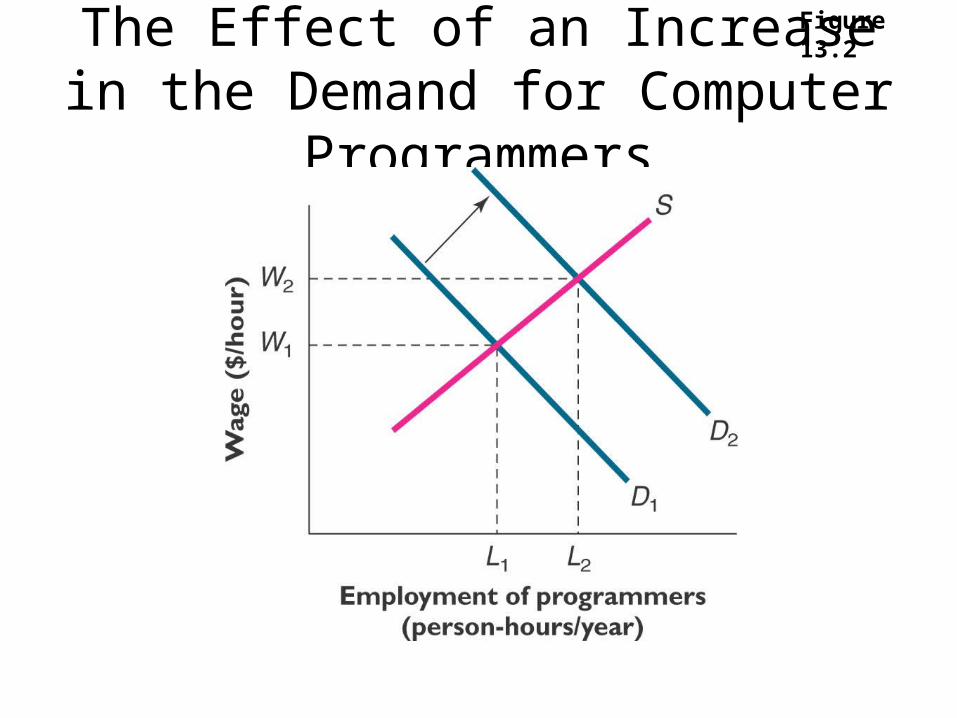

The Effect of an Increase in the Demand for Computer

Programmers

Figure 13.2

• Decrease in SupplyPrice ($/kg) S1

S0

Demand

Quantity (kg)

Initial equilibrium

New equilibrium

1. An increase in an input price reduces

the supply…

2…resulting in a higher price…

3…and a lower quantity sold

Technical Change Shifts Supply Curve

• Example of Technical Change Vessel electronics on fishing boats Effect on short-run supply of fish and price of

fish Short-run because take resource stock as

given Not long-run supply curve that is in steady-

state equilibrium in resource stock

Technical Change: Vessel Electronics

S0 Initial Supply of Fish

S1 Subsequent Supply of Fish

D

P0

P1

Q0

Price ($/unit)

Q1Quantity/time period

• Increase in Demand and Increase in Supply

Price ($/unit) S1

S0

D1

D0

Quantity (# units/time period)

Initial equilibrium

New equilibrium

P0

P1

Q0 Q1

Large increase in

demandSmall

increase in supply

• Increase in Demand and Decrease in Supply

Price ($/kg) S1

S0

D0

D1

Quantity (kg/time period)

Q0 Q1

P0

P1

New equilibrium

Initial equilibrium

Increase in demand

Decrease in supply

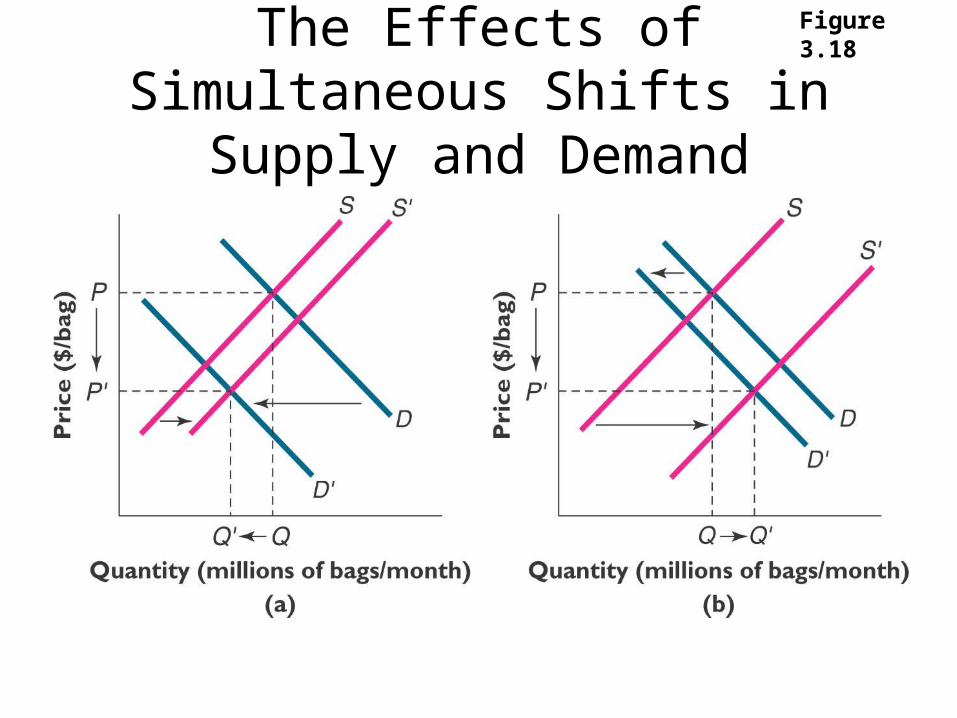

The Effects of Simultaneous Shifts in Supply and Demand

Figure 3.18

Four Rules Governing the Effects of Supply and Demand Shifts

Figure 3.17

What Happens to Price and Quantity When Supply or Demand Shifts?

No Change in Supply

An Increase in Supply

A Decrease in Supply

No Change in Demand

P same P down P up

Q same Q up Q down

An Increase in Demand

P up P ambiguous P up

Q up Q up Q ambiguous

A Decrease in Demand

P down P down P ambiguous

Q down Q ambiguous Q down