Embed Size (px)

Citation preview

By Dr Peter Harrop, Franco Gonzalez, Jess Armstrong and Kathryn

Greaves

IDTechEx

www.IDTechEx.com

Supercapacitor/

Ultracapacitor Strategies

and Emerging

Applications

2013-2025 Electrochemical Double Layer Capacitors &

Supercabatteries AEDLC: Supplier & User

Interviews/Appraisal: Advances Creating Extra

Markets – Map to 2023

© IDTechEx Ltd

except company literature which remains the

copyright of the companies in question.

IDTechEx Ltd

Downing Park

Swaffham Bulbeck

Cambridge, CB25 0NW

United Kingdom

IDTechEx, Inc.

222 Third Street

Suite 0222

Cambridge MA 02142

United States

IDTechEx GmbH

Berlin

Germany

The rights of Dr Peter Harrop, Franco Gonzalez, Jessica Armstrong and Kathryn Greaves to be identified as

the authors of this work

have been asserted in accordance with sections 77 and 78 of the

Copyright, Designs and Patents Act 1988.

DISCLAIMER

The facts set out in this publication are obtained from sources which we believe to be reliable. However, we

accept no legal liability of any kind for the publication contents, nor any information contained therein nor

conclusions drawn from it by any party. IDTechEx accept no responsibility for the consequences of any actions

resulting from the information in this report.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted

in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior

permission of the publishers.

Designed, produced, and typeset by IDTechEx Ltd. www.IDTechEx.com/research

1304A

Supercapacitor/ Ultracapacitor Strategies 2013-2025

Free consultancy from IDTechEx Thank you for buying this IDTechEx publication, which includes up to 30 minutes telephone time

with an expert analyst who will help you link key findings in the report to the business issues you

are addressing. For more details please contact the primary author (details below). Please give the

name of the report purchased and when.

The publisher IDTechEx is a knowledge-based consultancy company providing research and analysis on printed

and thin film electronics, RFID, energy harvesting, photovoltaics and smart packaging. The

company gives strictly independent marketing, technical and business advice and services on these

subjects in three forms - consulting, publications and events. Learn more at www.IDTechEx.com

Raghu Das, CEO

+ 44 1223 813703

Dr Peter Harrop, Chairman

+ 44 1256 862163

Glyn Holland, Senior Editor

+ 44 1223 813703

The authors

Dr Peter Harrop, PhD, FIEE is founder, controlling shareholder and

Chairman of IDTechEx Ltd. He was previously Chief Executive of Mars

Electronics, the $260 million .electronics company and Chairman of

Pinacl plc, the $100m fibre optic company. He has been chairman of

over 15 high tech companies. [email protected]

Franco Gonzalez is technology analyst at IDTechEx. Franco obtained an

MPhil in Engineering for Sustainable Development from the University

of Cambridge, where he focused on Sustainable Energy Systems. He

has a degree in Chemical Engineering from National Autonomous

University of Mexico. At IDTechEx, he is mainly involved with analysis

and research of the electric vehicles and energy harvesting industries.

Jess Armstrong and Kathryn Greaves are technical researchers for

IDTechEx and are based in the UK.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

Contents Page 1. EXECUTIVE SUMMARY AND CONCLUSIONS 1

1.1. Supercapacitors and batteries converge 1

1.2. Success by application and territory 3

1.3. Most are chasing area improvement 9

1.4. Even lower temperature 10

1.5. Price and functional issues 11

1.6. Supercapacitors in vehicles 13

1.6.1. Conventional vehicles 13

1.6.2. Electric vehicles 14

1.7. Incidence of the different technologies 17

1.7.1. Incidence of manufacturers by operating principle 17

1.7.2. Incidence of current collector and active electrode types 17

1.7.3. Electrolytes 18

1.7.4. Solid electrolytes 19

1.8. Achieving the impossible 20

1.9. Manufacturers and putative manufacturers 29

1.10. New entrants 33

1.11. Supercapacitors and lithium-ion batteries are now one business 33

1.12. Change of leadership of the global value market? 36

2. INTRODUCTION 39

3. ADVANCES REQUIRED AND PROGRESS IDENTIFIED 45

3.1. Supercapacitors in vehicles 48

3.2. Ensuring that supercapacitors will replace more batteries 60

4. APPLICATIONS NOW AND IN THE FUTURE 61

4.1. Pulse Power 62

4.2. Bridge Power 62

4.3. Main Power 62

4.4. Memory Backup 62

4.4.1. Evolution of commercially successful functions 64

4.4.2. Composite structural and smart skin supercapacitors for power storage 64

4.5. Manufacturer successes and strategies by application 66

Supercapacitor/ Ultracapacitor Strategies 2013-2025

© ID

Te

ch

Ex L

td

5. SURVEY OF 80 MANUFACTURERS 69

6. ACHIEVEMENTS AND OBJECTIVES BY MANUFACTURER 77

7. EXAMPLES OF NON-COMMERCIAL DEVELOPMENT PROGRAMS 105

8. ELECTROLYTES BY MANUFACTURER 109

9. INTERVIEWS AND COMMENTARY ON COMPANY STRATEGY FOR SUPERCAPACITORS 117

9.1. Interviews with suppliers 117

9.1.1. Cap-XX Australia 117

9.1.2. Cellergy Israel 118

9.1.3. East Penn Manufacturing USA 118

9.1.4. Elton Super Capacitor Russian Federation 119

9.1.5. Inmatech USA 123

9.1.6. Ioxus USA 127

9.1.7. JR Micro Japan 127

9.1.8. Maxwell Technologies USA 128

9.1.9. Nanotune Technologies USA 150

9.1.10. Nesscap Energy Inc Canada/Korea 150

9.1.11. Nichicon Japan 152

9.1.12. Nippon ChemiCon/ United ChemiCon Japan 155

9.1.13. Yo-Engineering Russian Federation 159

9.1.14. Yunasko Russian Federation 160

9.2. User interviews and inputs 164

9.2.1. Bombardier Canada 164

9.2.2. Hydrogenics Corporation USA 164

9.2.3. Honda Japan 164

10. DEVELOPER, MATERIALS SUPPLIER AND ACADEMIC INPUTS 165

10.1. Daikin Industries Japan 165

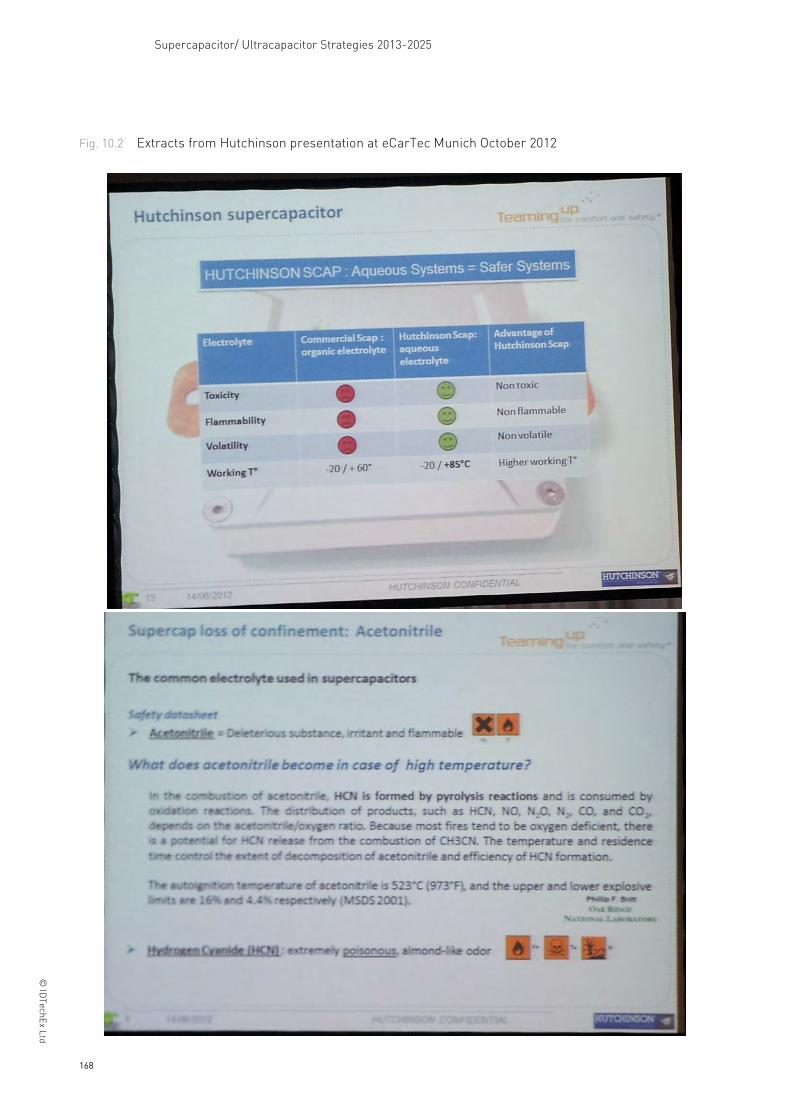

10.2. Hutchinson (TOTAL) France 167

10.3. IFEVS Italy 171

10.4. Northeastern University USA 172

10.5. NYSERDA grants reveal trends of research 173

10.6. Tecate Group USA 175

10.7. Yuri Gogotski 175

APPENDIX 1: IDTECHEX PUBLICATIONS AND CONSULTANCY 179

Supercapacitor/ Ultracapacitor Strategies 2013-2025

Tables Page Table 1.1 Main achievements and objectives with supercapacitors and their derivatives by number of

manufacturers and putative manufacturers involved 5

Table 1.2 The ten advances that will create the largest add-on markets for supercapacitors and their

derivatives in order of importance in creating market value with examples of organisations

leading the advance 8

Table 1.3 15 examples of component displacement by supercapacitors in 2012-3 21

Table 1.4 Supercapacitor functions reaching major market acceptance 2013-2023 with some of the

companies leading the success by sector 28

Table 1.5 80 manufacturers, putative manufacturers and commercial companies developing

supercapacitors, supercabatteries and carbon-enhanced lead batteries for

commercialisation with country, website and device technology. 29

Table 2.2 Some of the pros and cons of supercapacitors 41

Table 3.1 Advances that will create the largest add-on markets for supercapacitors and their

derivatives by value in order of importance with examples of organisations leading the

advance. 45

Table 3.2 Examples of component displacement by supercapacitors. 53

Table 4.1 Supercapacitor functions reaching major market acceptance 2013-2023 with some of the

companies leading the success by sector 64

Table 5.1 80 manufacturers, putative manufacturers and commercial companies developing

supercapacitors, supercabatteries and carbon-enhanced lead batteries for

commercialisation with country, website and device technology. 71

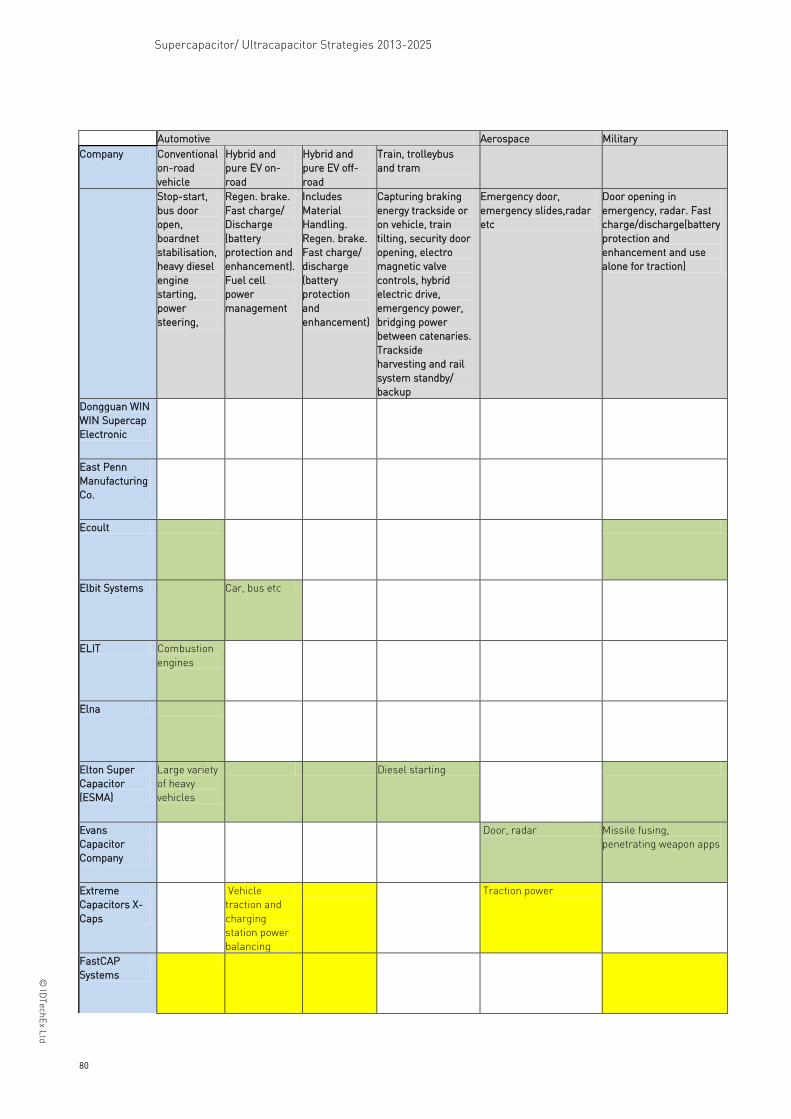

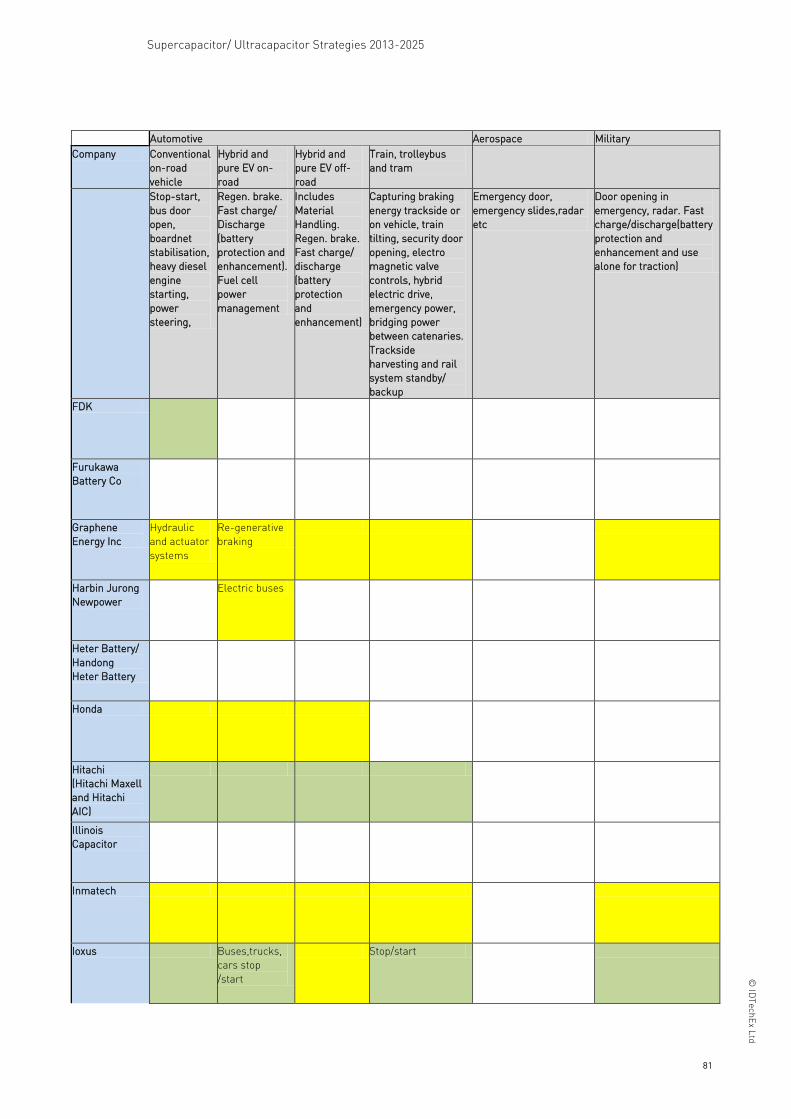

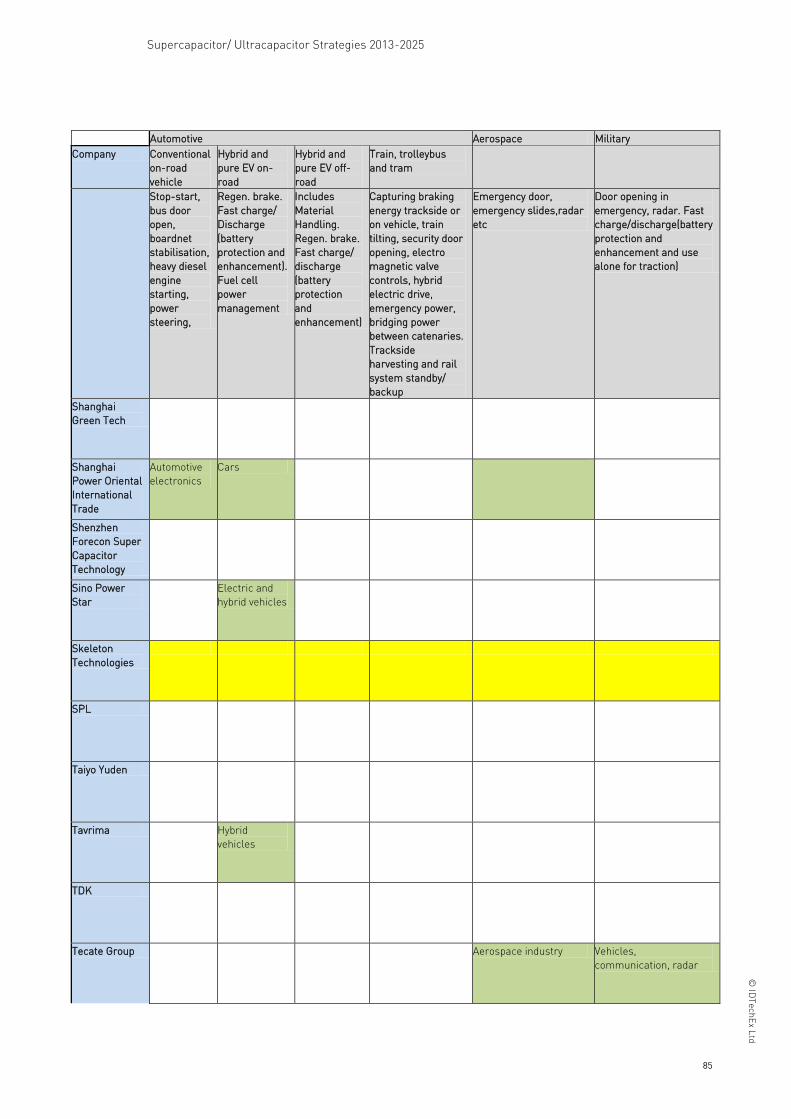

Table 6.1 By application, for Automotive, Aerospace, Military and Oil & Gas, the successes by 78

supercapacitor/supercabattery manufacturers in grey green and their targets for extra

applications in the near term in yellow. Six sub categories are analysed 78

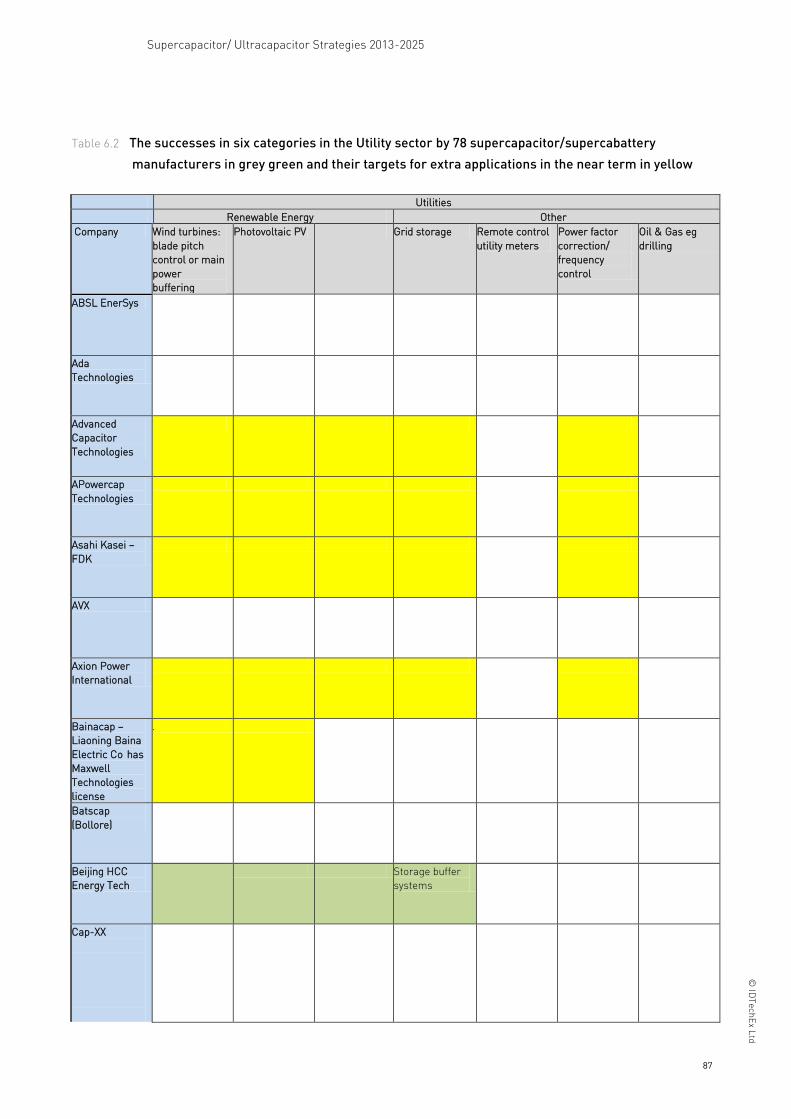

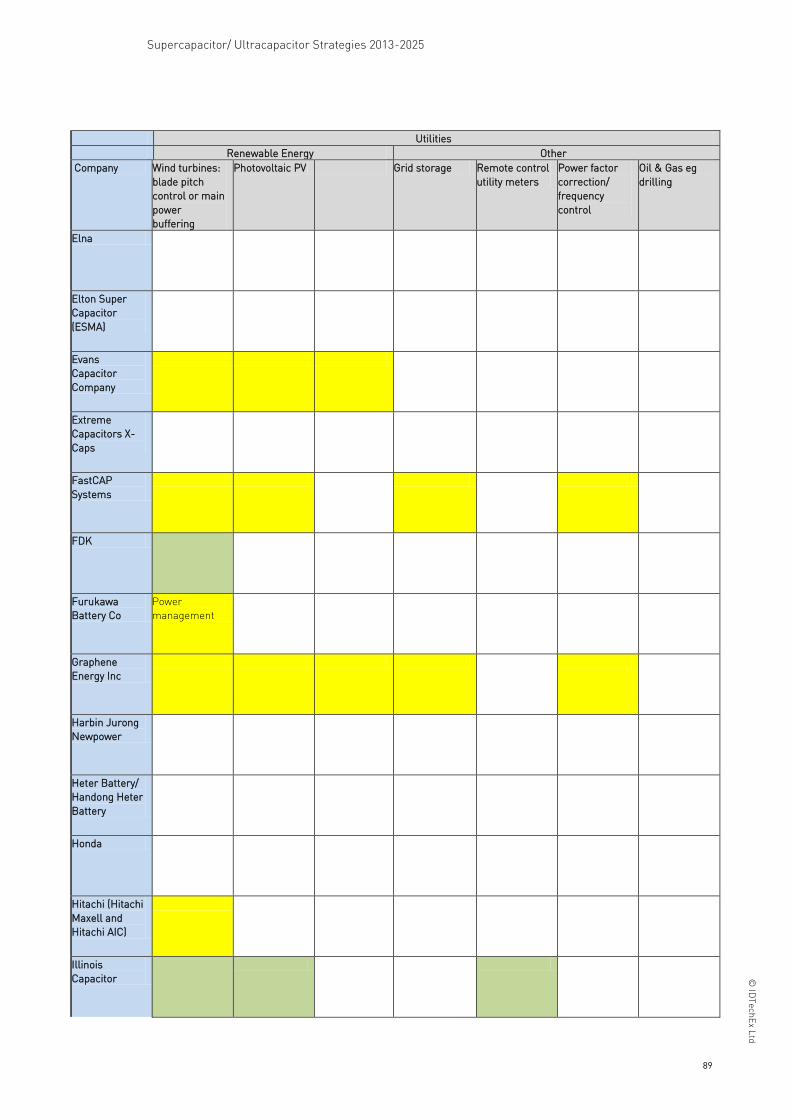

Table 6.2 The successes in six categories in the Utility sector by 78 supercapacitor/supercabattery

manufacturers in grey green and their targets for extra applications in the near term in

yellow 87

Table 6.3 The successes by 78 supercapacitor/supercabattery manufacturers in the Consumer and

Industrial & Commercial sectors in grey green and their targets for extra applications in the

near term in yellow. Eight sub-categories are analysed. 94

Table 7.1 Non-commercial supercapacitor developers with their country, website, industrial partner,

applications targeted 105

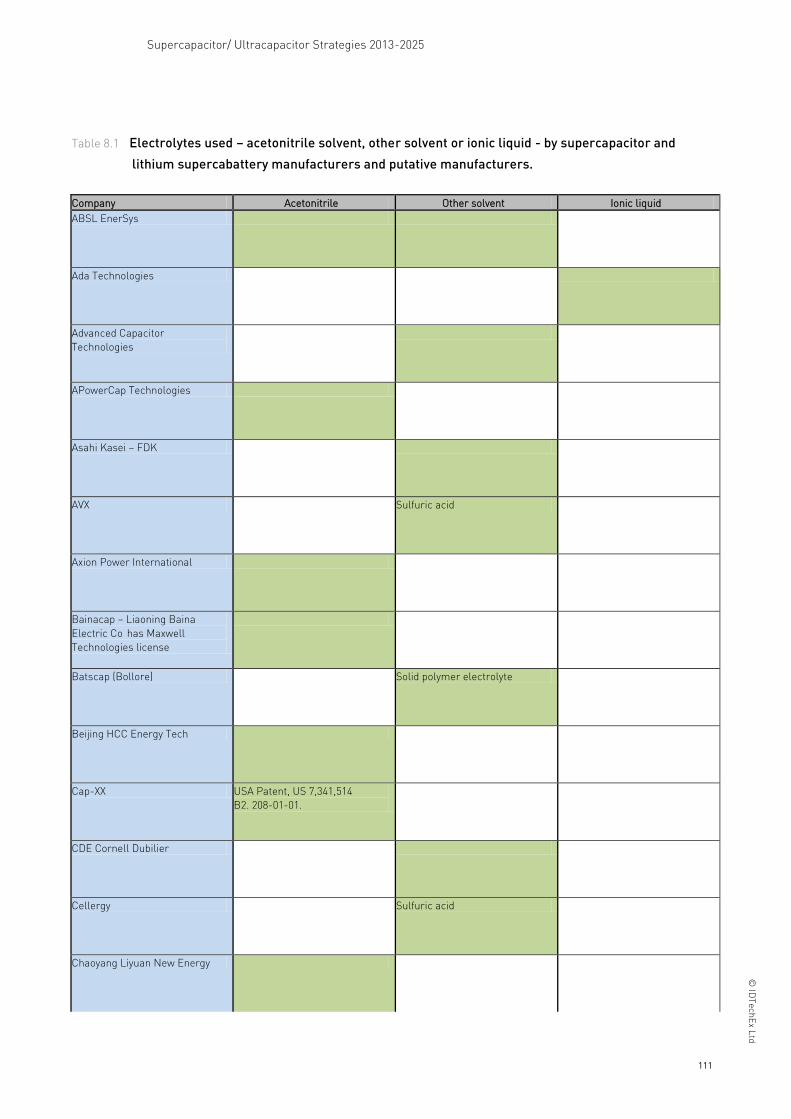

Table 8.1 Electrolytes used – acetonitrile solvent, other solvent or ionic liquid - by supercapacitor and

lithium supercabattery manufacturers and putative manufacturers. 111

Supercapacitor/ Ultracapacitor Strategies 2013-2025

Figures Page Fig. 1.1 Some of the options and some of the suppliers in the spectrum between conventional capacitors

and rechargeable batteries with primary markets shown in yellow 2

Fig. 1.2 Examination of achievement and strategy in the most important applicational sectors. Number

of manufacturers of supercapacitors and their variants that have that have supplied given

sectors vs number that target them for future expansion without having achieved significant

sales so far 4

Fig. 1.3 Probable timeline for market adoption by sector and technical achievements driving the growth

of the market for supercapacitors and their derivatives 2013-2025 with market value projections

for supercapacitors, cost and performance parameter improvements by year and, for

comparison, lithium-based batteries and pure/hybrid electric vehicles value market by year

2013-2025 7

Fig. 1.4 Some of the main ways in which greater supercapacitor energy density is being sought by the

route of increasing useful carbon area per unit volume or weight 10

Fig. 1.5 The main functions that supercapacitors will perform over the coming decade 12

Fig. 1.6 Examples of the main functions performed by supercapacitors 13

Fig. 1.7 The evolution from conventional to various types of electric vehicle related to supercapacitor

applications in them today, where hybrids and pure electric versions are a primary target 15

Fig. 1.8 Possible timeframe and technology for reaching the tipping point for sales of pure electric on-

road cars 16

Fig. 1.9 The number of manufacturers and putative manufacturers of supercapacitors/supercabatteries

by six sub-categories of technology 17

Fig. 1.10 Incidence of manufacturers of various types of supercapacitor and variant by operating principle 18

Fig. 1.11 Component displacement mapped as a function of benefits relative to batteries conferred by

supercapacitors 20

Fig. 1.12 Estimate of the number of trading manufacturers of supercapacitors and supercabatteries

globally 1993-2025 including timing of industry shakeout. 33

Fig. 2.1 Types of capacitor 39

Fig. 2.2 Symmetric supercapacitor EDLC left compared with asymmetric AEDLC ie supercabattery with

battery-like cathode (ie part electrochemical in action) shown right. During charge and

discharge, the voltage is nearly constant resulting in higher maximum voltage and twice the

capacitance of anordinary supercapacitor/ ultracapacitor 40

Fig. 2.3 Symmetric supercapacitor EDLC compared with asymmetric AEDLC ie supercabattery with

lithiated carbon anode (ie entirely electrostatic in action) shown right 40

Fig. 2.4 Eight families of option and some of the suppliers in the spectrum between conventional

capacitors and rechargeable batteries with primary markets shown in yellow 42

Fig. 3.1 The main functions that supercapacitors will perform over the coming decade 47

Fig. 3.2 Examples of the main functions performed by supercapacitors. Those in black are currently only

achieved with a flammable, carcinogenic electrolyte – acrylonitrile – but this will change 48

Supercapacitor/ Ultracapacitor Strategies 2013-2025

© ID

Te

ch

Ex L

td

Fig. 3.3 The evolution from conventional to various types of electric vehicle related to supercapacitor

applications in them today, where hybrids and pure electric versions are a primary target. 49

Fig. 3.4 Possible timeframe and technology for reaching the tipping point for sales of pure electric on-

road cars 50

Fig. 3.5 Component displacement mapped as a function of benefits relative to batteries conferred by

supercapacitors 51

Fig. 3.6 Siemens view in 2012 of the elements of Electrical Bus Rapid Transit eBRT, for example,

mentioning U-Caps meaning supercapacitors 52

Fig. 4.1 Examples of applications of the ULTIMO Cell 63

Fig. 4.2 Structural supercapacitor as flexible film. 65

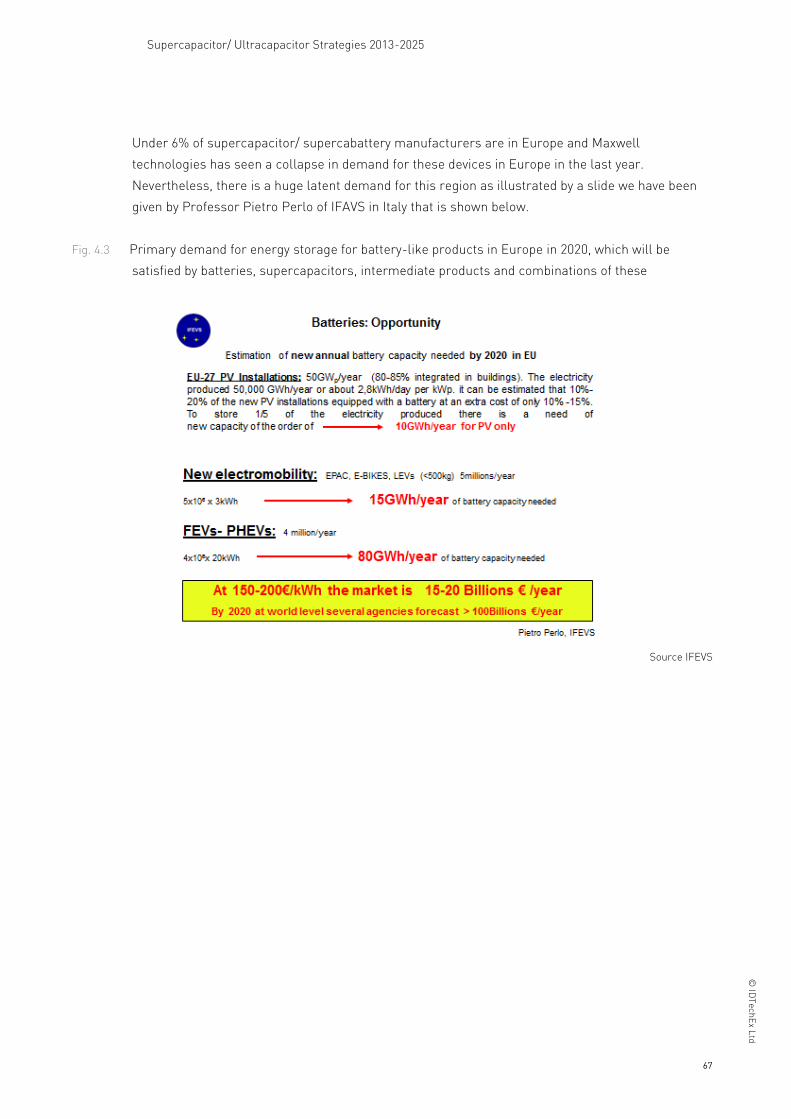

Fig. 4.3 Primary demand for energy storage for battery-like products in Europe in 2020, which will be

satisfied by batteries, supercapacitors, intermediate products and combinations of these 67

Fig. 5.1 Incidence of the different technologies 74

Fig. 5.2 Number of manufacturers offering the various supercapacitor technologies including

derivatives, some companies having several options 75

Fig. 5.3 Estimate of the number of trading manufacturers of supercapacitors and supercabatteries

globally 1993-2025 including timing of industry shakeout. 76

Fig. 9.1 UltrabatteryTM for medium hybrid vehicles 118

Fig. 9.2 Inmatech Innovations 124

Fig. 9.3 Supercapacitor market and Inmatech 124

Fig. 9.4 Maxwell Technologies flat supercapacitor for mobile phones etc. exhibited at EVS26 Los

Angeles 128

Fig. 9.5 Nichicon supercapacitor emphasis at EVS26 Los Angeles 2012 153

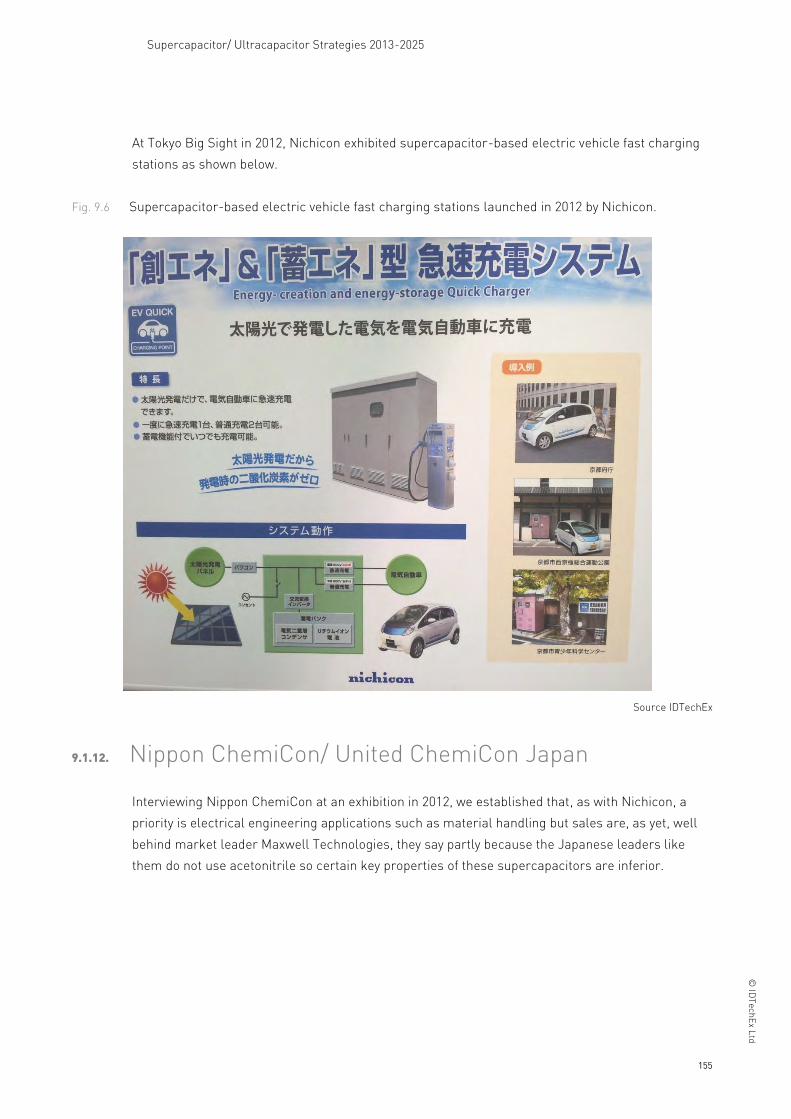

Fig. 9.6 Supercapacitor-based electric vehicle fast charging stations launched in 2012 by Nichicon. 155

Fig. 9.7 Mazda car supercapacitor exhibited at EVS26 Los Angeles 2012 156

Fig. 9.8 Nippon Chemi-Con low resistance DXE Series priority shown in 2012 157

Fig. 9.9 Exhibit by United ChemiCon at EVS26 Los Angeles 158

Fig. 10.1 Daikin Industries display on fluorination of supercapacitor electrolytes 166

Fig. 10.2 Extracts from Hutchinson presentation at eCarTec Munich October 2012 168

Supercapacitor/ Ultracapacitor Strategies 2013-2025

1

© ID

Te

ch

Ex L

td

1. Executive summary and

conclusions Our report, “Electrochemical Double Layer Capacitors: Supercapacitors 2013-2023” introduced the

subject, gave overall market forecasts, examples of research trends, analysis of patents and

achievements and it briefly profiled the manufacturers and putative manufacturers. By popular

request, we now look much more closely at the applications and technology today and in future and

company strategy in matching the two as they rapidly evolve. We address when certain new

applications will be identified and taken seriously plus when currently-impracticable applications

will become viable. Yes, the market is limited by unimaginative copy-cat marketing as well as

technological advance. This new report is based on extensive interviews and searches to reveal the

trends and lessons. Mainly, it consists of detailed tables of new analysis and roadmaps to 2025.

1.1. Supercapacitors and batteries converge

Traditionally, rechargeable batteries have been used as energy dense products and the other

devices based on capacitors have been used as power dense products. There are more-power-

dense versions of the favourite rechargeable batteries – lithium-ion with 70% or so of the

rechargeable battery market in 2023. Unfortunately, power dense rechargeable batteries surrender

a lot of energy density. It is therefore helpful that more and more energy dense supercapacitors

and variants are becoming available, some even matching lead acid batteries and yet retaining

excellent power density. This convergence of properties has led to the widespread combination of

the two in parallel, particularly in power applications. Battery/ supercapacitor combinations

approach the performance of an ideal battery – something that can never be achieved with a battery

alone because its chemical reactions cause movement, swelling and eventually irreversability. In

some cases, things have gone further. For example, hybrid buses using supercapacitors now rarely

use them across the traction battery – the supercapacitor replaces the battery, the only battery

remaining in the vehicle being a small lead-acid starter battery.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

2

© ID

Te

ch

Ex L

td

Many more variants are now available, so there is now almost a continuum of devices between

conventional electrolytic capacitors and rechargeable batteries as we show below. The examples of

manufacturers, that are given below, illustrate how battery manufacturers and conventional

capacitor manufacturers are entering the business of devices intermediate between the two.

However, rather surprisingly, most of the intermediate devices are developed and manufactured by

companies not in either conventional capacitors or batteries. Although we use the term

intermediate devices, some have some properties superior to both conventional capacitors and

rechargeable batteries.

Fig. 1.1 Some of the options and some of the suppliers in the spectrum between conventional capacitors

and rechargeable batteries with primary markets shown in yellow

Conventional

symmetrical

(bipolar) solid

capacitor

Conventional

electrolytic

capacitor

Etched

aluminium foil

oxidised Al2O3

or sintered

tantalum

oxidised Ta2O5

“Hybrid

capacitor”

Super

Capacitor

electrode

plus sintered

tantalum

oxide Ta2O5

electrode

Symmetric

Super-

Capacitor ie

Electrochemical

Double Layer

Cpacitor

Asymmetric intermediate devices Rechargeable

battery

Supercabattery ie

Asymmetric

Electrochemical Double

Layer Capacitor AEDLC

Pseudo-

Capacitor eg

RuO2

Nippon

Chemi-con

Nichicon

AVX

Nippon

Chemi-con

Nichicon

Evans Maxwell

Technologies

Nippon Chemi-

con

Nichicon

AVX

Panasonic

Batscap

With battery

anode and

supercap.

cathode

JRMicro

With battery

cathode and

supercap

anode

East Penn

Furukawa

Evans

Capacitor

Panasonic

Batscap

Electrostatic

Partly electrostatic and

partly electrochemical

(faradaic)

Electro-

chemical

Source IDTechEx

Let us define the pseudocapacitance. There are two types of charge storage that can occur at the

interface: pseudocapacitance and electrochemical double layer capacitance. For example, if the

electrode is a carbon nanotube with some functional groups on it or nanoparticles that allow

intercalation of Li ions, then electron transfer reaction (Faradaic reaction) occurs at the surface of

the electrode, and this type of capacitance is called ‘pseudocapacitance’. Currently it gives a more

expensive capacitor because of use of ruthenium with higher capacitance and certain performance

limits so Evans capacitor sells them to the military for instance. Faradaic phenomena usually limit

INCREASING ENERGY DENSITY

INCREASING POWER DENSITY

Supercapacitor/ Ultracapacitor Strategies 2013-2025

3

© ID

Te

ch

Ex L

td

the life to electrostatic devices, something also seen in the hybrid devices with one battery-like

electrode and one battery-like (faradaic) one. Currently the market for faradaic variants of

supercapacitors, notably pseudocapacitors and supercabatteries is about one hundredth of that for

fully electrostatic supercapacitors and they are unlikely to ever dominate because most

applications need fit and forget and fastest charge-discharge (power density) and greatest safety

and reliability. Where highest energy density is needed, that may be provided by any of the three

options in years to come – opinion is divided. IDTechEx sees the biggest market value being

supercapacitors then supercabatteries in ten years from now.

If no Faradaic reaction is allowed, charges can only be physically absorbed in to the double layer

without any electron transfers. In this case we only have purely electrostatic double-layer

capacitance the primary topic of this report. As MIT reports, “When we view the

electrode/electrolyte interface as a black box, we only see that ions and electrons enter and are

stored at a given voltage, and it is difficult to distinguish whether charge is stored capacitively or

Faradaically. The time scales and nonlinear response of each process is very different, however, so

it is possible to separate these processes from experimental data using suitable mathematical

models.”

1.2. Success by application and territory

A multi-billion dollar market for supercapacitors and their variants is emerging within the decade,

so creation of a one billion dollar manufacturer will be feasible, certainly by 2025. Put at its

simplest, the lesson of the extensive interviews and investigations carried out for this report show

that, if you want to create such a billion dollar supercapacitor company, whatever else you do, you

sell into the automotive sector, land, water and airborne but particularly land – off and on-road -

for the next decade and secondarily the utility sector . You must work to increase energy density

and reduce cost, if necessary by making the variant called the lithium-ion capacitor, though several

participants believe that symmetric supercapacitors are all you need to make these gains. You

must make acquisitions and creatively market, opening up new applications with customised

products such as drop-in battery replacements. Large companies will have an advantage in taking

the ever bigger orders available from a relatively small number of large automotive companies and

utilities. Our study reveals that, although the early supercapacitor orders were for small devices in

electronics such as CMOS backup, we have passed through a period where electrical engineering

applications have become more important. Indeed, they will now be by far the most important. Let

us look at the evidence.

Our study of 78 manufacturers and putative manufacturers shows the following achievements and

intentions to enter a sector to be pre-eminent. The minor differences in numbers are not of

significance. However, on these criteria, this is an industry that has sharply changed direction and

this is reinforced by other evidence we present.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

4

© ID

Te

ch

Ex L

td

Fig. 1.2 Examination of achievement and strategy in the most important applicational sectors. Number of

manufacturers of supercapacitors and their variants that have that have supplied given sectors vs

number that target them for future expansion without having achieved significant sales so far

Industrial &

Commercial

Vehicles Consumer Utility Aerospace &

Military

Achievement 43 33 32

28 18

Intention 11

16

10

11

10

Total number of

manufacturers

targeting these

sectors

54

49 42 39 28

Source IDTechEx

This conclusion is supported by the facts that market leader Maxwell Technologies derived its

largest business from buses in 2012 and the largest order in that year was the Meidensha/Sojitz

$318 million (¥25bn) contract to supply two 2 MW Capapost regenerated energy storage units for

Hong Kong’s South Island Line metro project. Another large commitment was for Batscap to

supply large supercapacitors to go across the batteries in 22,000 Bluecars its parent company is

making for open rental in Paris and more are being made for open sale. That may be of the order of

$20 million. The similar application in Mazda pure electric cars also in 2012 may also involve a

substantial commitment. So the largest recent orders and the main delivery by the market leader

are in vehicles and vehicle/utility-related project. Everything points to the largest market for

supercapacitors now being in electrical engineering rather than electronics, the easy entry point

for beginners.

Our more detailed results below support this, though mobile phones are also a strong interest

where supercapacitor prices of one thousandth may eventually be compensated by selling one

thousand times the number. Most of the most popular potential markets will involve large orders

from a few companies, so there will be few winners, these being large suppliers in all likelihood. In

the case of the automotive industry, these large suppliers will sometimes not be the traditional Tier

One suppliers, the supercapacitor suppliers bypassing the traditional Tier One suppliers as has

already happened with supply of automotive lithium-ion batteries. Now for the detail.

Largest

recent

orders

Largest

recent

orders

Supercapacitor/ Ultracapacitor Strategies 2013-2025

5

© ID

Te

ch

Ex L

td

Table 1.1 Main achievements and objectives with supercapacitors and their derivatives by number of

manufacturers and putative manufacturers involved

Total interest Achievement Interest for the future

1. Office equipment, medical

and small electronics

47

Attracting

most

suppliers

42 5

2. Hybrid & pure electric on-

road vehicles

42 23 19 STRONG. Very large orders

will be available from a

relatively limited number of

customers

3. Conventional on-road

vehicles

34 20 14 STRONG. Very large orders

will be available from a

relatively limited number of

customers

4. Mobile phone & camera 32 7 25 STRONG Very large orders

will be available from a

relatively limited number of

customers

5. Remotely-read utility

meters

21 19 2

6. Vehicles off-road 27 9 18 STRONG Very large orders

will be available from a

relatively limited number of

customers

7. Photovoltaics 24 9 15 STRONG Very large orders

will be available from a

relatively limited number of

customers

8. Wind turbines 22 18 4

9. Train, trolleybus & tram 21 11 10 STRONG Very large orders

will be available from a

relatively limited number of

customers

10. Military 21 12 9

11. Toys & other consumer 20 19 1

12. Grid power factor

correction and frequency

control

18 6 12 STRONG Very large orders

will be available from a

relatively limited number of

customers but there are

many competing options

13. Audio 18 17 2

14. Grid storage 16 6 10 STRONG Very large orders

may be available from a

relatively limited number of

customers but there are

many competing options

15. Other energy harvesting

including thermoelectric

and piezoelectric

14 4 10 STRONG Large orders may

be available from a relatively

limited number of customers

16. Standby power & UPS not

on a grid scale

13 6 7

17. Aerospace 11 8 3

18. Telecoms inc GSM/GPRS

PC cards

7 6 1

19. Oil & Gas 5 4 1

20. Gaming machines 4 3 1

21. Heavy pulse power :

welding, metal forming,

robotics

4 2 2

Source IDTechEx

Supercapacitor/ Ultracapacitor Strategies 2013-2025

6

© ID

Te

ch

Ex L

td

Location of suppliers

Supercapacitors and their variants will be a multi-billion dollar business in 10 years mainly served

by the USA, Russia, Japan and Korea, if current trends continue. Europeans are users notably in

trains and buses, but, as suppliers, they are almost fast asleep with little leadership beyond

Skeleton Technologies in Estonia and a skimpy research base.

Indeed, the main reason that market leader Maxwell Technologies saw its supercapacitor sales

growth drop to single digits in 2012 was weakness in Europe. Maxwell Technologies has

supercapacitor sales of the order of $100 million with China being its strongest territory throughout

2012. With rapid increase in the number of manufacturers of supercapacitors and their variants,

Maxwell Technologies may be losing market share particularly to the rapidly growing number of

local suppliers in East Asia, one of which took the largest order in the world in 2012. Market growth

continuing at 30% or more is largely driven by East Asian demand supplied locally by a host of new

manufacturers but also underpinned by rapid adoption in such things as cars, buses, wind turbines

and backup power from the micro to the grid level in the other parts of the world.

A probable timeline for market adoption and technical achievements driving the growth of the

market for supercapacitors and their derivatives is as follows. Our projection of 30% compound

growth is supported by Nesscap commencing to triple output and Maxwell to increase it by 30%.

Additional supporting facts are the large increase in value of the largest orders being taken, the

growth of the end user markets such as bus production and the large number of new

manufacturers and applications continuing. Our interviews confirmed that suppliers see double

digit growth in future and our projection is one of the lowest among analysts.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

7

© ID

Te

ch

Ex L

td

Fig. 1.3 Probable timeline for market adoption by sector and technical achievements driving the growth of

the market for supercapacitors and their derivatives 2013-2025 with market value projections for

supercapacitors, cost and performance parameter improvements by year and, for comparison,

lithium-based batteries and pure/hybrid electric vehicles value market by year 2013-2025

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2025

Super-

capacitor/

super-

cabattery

global

market

$ billion

0.84 1.1 1.42 1.85 2.41 3.13 4.07 5.29 6.87 8.93 11.6 19.6

Market leader Maxwell Technologies either buys companies,

gets bought or loses its market leadership. Will the NASDAQ

listing lead to short-termism or to funding?

Nippon Chemi-Con/United Chemi-Con gains share. Most of the

top players in supercapacitors/ supercabatteries lose market

share if only because so many new companies enter the

business

Increased percentage of sales are

supercabatteries and green

supercapacitors. Number of

manufacturers rises to 200 then

consolidation begins

First $1bn

manufacturers

created, mainly by

acquisitions

Li-ion

battery

market

$ billion

25.3 27.8 30.6 33.7 37.0 40.7 44.8 49.3 54.2 59.7 65.6 79.6

An increasing percentage of lithium-ion battery sales will generate the sale of a supercapacitor to go across it

Supercap/

Super

cabatttery

best

Wh/kg in

lab.with at

least

10kW/kg

45 47 49 52 56 61 67 74 93 96 200 300

Nano

Tune

Nano

Tune

plans

this with

up to

30kW/kg

in 2014

Half of

Li-ion

battery

energy

density,

closing

the gap

Super

cap/

Superca

bat.

best

Wh/kg in

volume

prodn

15 30 35 40 45 50 55 60 67 85 93 100

Serious impact on

lead acid battery

market which starts

to shrink rapidly for

many reasons

Serious impact on

lithium-ion battery

market which

continues to be

several times

larger but grows

more slowly

Cost $/kW

of power

version

10kW/kg,

5Wh/kg,

0.1mOhm

ESR

13 12 10 9.8 9.5 9.1 8.7 6.5

Yunasko

targets this

for 2014

Yunasko targets

This in 2020

Li-ion or

LiMetal

battery

Wh/kg in

prod-

uction

130 140 300 320 340 360 380 400 420 460 500 600

Envia

Systems

demo’d this

in lab in

2012.

Pure EV

car sales

surge

In 2012,

Nikkei

wrote

that

Toyota is

working

on this

Hybrid &

Pure

Electric

Vehicles

land, water

and

airborne

global EV

market

$ billion

64 75 87 104 123 145 172 206 242 264 290 322

An increasing percentage of hybrid and pure electric vehicles will use a large fast charge/discharge or main power

supercapacitor /supercabattery plus many small supercapacitors for regenerative brake backup, emergency door opening,

power circuit balancing etc

Integrated units will gradually become popular where the supercapacitor/ supercabattery is part of a more comprehensive

module, some of these modules being made by the supercapacitor manufacturer.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

8

© ID

Te

ch

Ex L

td

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2025

Gap closing

between energy

density of

supercapacitors/

supercabatteries

and batteries and

costs reduced,

boosting

applications.

Super

cap locos

in prod-

uction in

China. This

gives

limited

operation

without

catenary

Fuel cell cars, buses

and trucks in

production from

several major makers

many with power

supercapacitors

across the fuel cell

Most new phones &

cameras have

supercapacitor

flash. Apple USA

becomes a large

purchaser of

supercapacitors.

Samsung and Toyota

major on

supercapacitors as a

key enabling

technology for their

products

100K wind turbines installed

with supercapacitor pitch

control

Most hybrid buses made have

a supercapacitor instead

of a battery.

China over 70% of global bus

market and supplied locally

with buses and their

supercapacitors

Graphene supercapacitors in

volume production.

Green supercapacitors outsell

Others

Extensive sale of

supercapacitors/

supercabatteries as structural

components in vehicles,

phones etc.

Surge in consumer and hand-

tool applications

Wind

3-5% of

China’s

power –

big

supercap

market

including

Power

balancing

Chinese

get the

business

Supercapacitors

in most new

on-road ICE stop-

start vehicles.

Largest market is

in East Asia and

supplied locally

Supercapacitors

In power for most

material

handling vehicles

Super

caps widely

used for grid

power smooth

& other grid and

green power uses

Many

hand tools

use super

cap not battery

and they are used

as smart skin on

vehicles etc.

Source IDTechEx

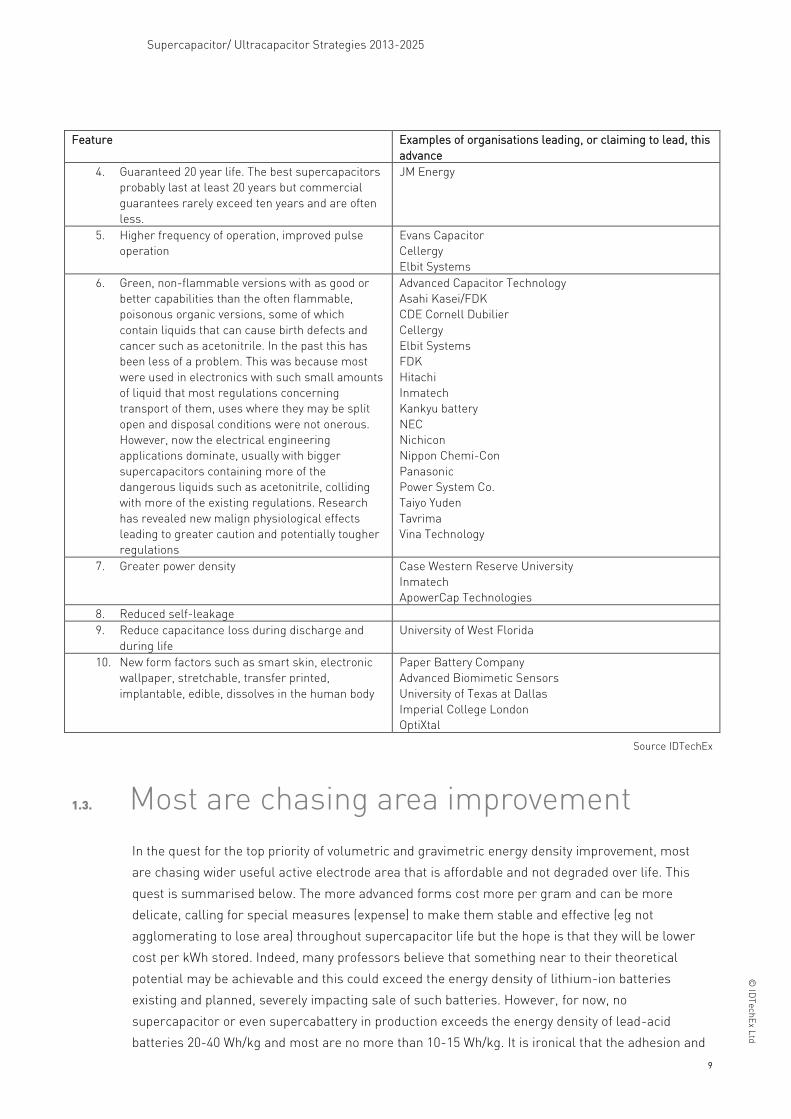

The primary advances that will create the largest add-on markets by value will be the following in

order of importance.

Table 1.2 The ten advances that will create the largest add-on markets for supercapacitors and their

derivatives in order of importance in creating market value with examples of organisations

leading the advance

Feature Examples of organisations leading, or claiming to lead, this

advance

1. Affordable, greater gravimetric and, less

important, volumetric energy density particularly

because it will allow more batteries to be

completely replaced and, where the

supercapacitor is used across a battery to protect

it and enhance its performance, less battery will

be needed. Less battery means improved system

reliability and potentially lower cost, not just

improved performance. Where this is achieved by

higher cell voltage there are other benefits such

as greater reliability and lower cost of high

voltage stacks because they have fewer

interconnects.

This is achieved by increasing cell voltage and/or

capacitance because E=0.5CV2

Cell voltage records are being set by Vina Technology, and

Nisshinbo both at 3V and JM Energy 3.8V (LiC) LithChem

Energy 3.9V at present. C is increased primarily by

increasing the usable active electrode area or making a

supercabattery but there is also scope to move from thick

current collectors, presently at up to 40 microns to thinner

ones, maybe down to 5 microns. Those tackling electrode

area successfully include

State University of New York at Binghampton

Elbit Systems

Graphene Energy

JR Micro

Nanotune Technologies

Skeleton Technologies

University of Kentucky

Yunasko

2. Lower price for existing capabilities Chinese suppliers

Maxwell Technologies

Inmatech

ApowerCap Technologies

NanoTune

3. More imaginative marketing opening up new

applications

Nippon Chemi-Con

Maxwell Technologies

Supercapacitor/ Ultracapacitor Strategies 2013-2025

9

© ID

Te

ch

Ex L

td

Feature Examples of organisations leading, or claiming to lead, this

advance

4. Guaranteed 20 year life. The best supercapacitors

probably last at least 20 years but commercial

guarantees rarely exceed ten years and are often

less.

JM Energy

5. Higher frequency of operation, improved pulse

operation

Evans Capacitor

Cellergy

Elbit Systems

6. Green, non-flammable versions with as good or

better capabilities than the often flammable,

poisonous organic versions, some of which

contain liquids that can cause birth defects and

cancer such as acetonitrile. In the past this has

been less of a problem. This was because most

were used in electronics with such small amounts

of liquid that most regulations concerning

transport of them, uses where they may be split

open and disposal conditions were not onerous.

However, now the electrical engineering

applications dominate, usually with bigger

supercapacitors containing more of the

dangerous liquids such as acetonitrile, colliding

with more of the existing regulations. Research

has revealed new malign physiological effects

leading to greater caution and potentially tougher

regulations

Advanced Capacitor Technology

Asahi Kasei/FDK

CDE Cornell Dubilier

Cellergy

Elbit Systems

FDK

Hitachi

Inmatech

Kankyu battery

NEC

Nichicon

Nippon Chemi-Con

Panasonic

Power System Co.

Taiyo Yuden

Tavrima

Vina Technology

7. Greater power density Case Western Reserve University

Inmatech

ApowerCap Technologies

8. Reduced self-leakage

9. Reduce capacitance loss during discharge and

during life

University of West Florida

10. New form factors such as smart skin, electronic

wallpaper, stretchable, transfer printed,

implantable, edible, dissolves in the human body

Paper Battery Company

Advanced Biomimetic Sensors

University of Texas at Dallas

Imperial College London

OptiXtal

Source IDTechEx

1.3. Most are chasing area improvement

In the quest for the top priority of volumetric and gravimetric energy density improvement, most

are chasing wider useful active electrode area that is affordable and not degraded over life. This

quest is summarised below. The more advanced forms cost more per gram and can be more

delicate, calling for special measures (expense) to make them stable and effective (eg not

agglomerating to lose area) throughout supercapacitor life but the hope is that they will be lower

cost per kWh stored. Indeed, many professors believe that something near to their theoretical

potential may be achievable and this could exceed the energy density of lithium-ion batteries

existing and planned, severely impacting sale of such batteries. However, for now, no

supercapacitor or even supercabattery in production exceeds the energy density of lead-acid

batteries 20-40 Wh/kg and most are no more than 10-15 Wh/kg. It is ironical that the adhesion and

Supercapacitor/ Ultracapacitor Strategies 2013-2025

10

© ID

Te

ch

Ex L

td

series resistance problems of lithium-ion batteries caused by swelling and movement during use,

due to the electrochemistry, recur in supercapacitors for a different reason. Here the active

electrode layer is more delicate and presents much less area to the current collector that can be

gripped, so adhesion and series resistance are still challenging even though the supercapacitor,

being electrostatic in action, does not swell and shrink during cycling.

Fig. 1.4 Some of the main ways in which greater supercapacitor energy density is being sought by the route

of increasing useful carbon area per unit volume or weight

Source IDTechEx

1.4. Even lower temperature

Supercapacitors are already popular in cold countries because they lose only a few percent of

charge availability at minus twenty to minus forty degrees centigrade. Maxwell Technologies

successfully offers a drop-in replacement for one of the three lead acid batteries in a typical truck

so it can start cold after hotel facilities have drained some of the lead-acid power overnight and

these low temperatures make up to 50% of what remains in the lead-acid batteries unavailable but

there is even more to go. Drexel University reported as follows in March 2012.

“Many people can relate to the hardship of starting a vehicle during a bitter cold morning before

work. It takes a huge amount of power relative to a warm sunny day for two reasons: the

mechanical parts of an engine require more power to start moving when cold (motor oil becomes

viscous, like honey), and the battery operates at a very low efficiency because the ions in electrolyte

solution move much slower at freezing temperatures.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

11

© ID

Te

ch

Ex L

td

A collaboration between researchers at Drexel University in Philadelphia, The University of Texas at

Austin, and Paul Sabatier University in Toulouse, France have recently engineered a supercapacitor

system that can operate efficiently at very low temperatures - as low as -50 °C (-58 °F). Just

published in the journal Nano Energy, their work involves a unique nanostructured carbon material

deemed activated microwave exfoliated graphite oxide ("a-MEGO"), which was inspired by the

recent interest in graphene. Graphene, which is an atomically thin layer of carbon, has many

applications in energy storage and generation.

Combined with a-MEGO is an electrolyte called an ionic liquid. These are salts like sodium chloride,

but are liquid at room temperature or below. The a-MEGO material has a high surface area, with

about 2 grams having the surface area of a football field; as a result, a-MEGO is able to store a

large amount of charge on its surface as a supercapacitor. The unique electrolyte, which is a

mixture of ionic liquids, allows for operation at low temperature. Commercial supercapacitors, by

comparison, use an electrolyte that will fail at temperatures below -25 °C (-13 °F). Finally,

supercapacitors will last for more than 10 years and up to 1 million charge/discharge cycles,

compared to batteries that will last a couple years for about 1 thousand cycles. Imagine never

having to change your car battery!

This study reinforces the potential of graphene in energy storage applications, but also

demonstrates that only the right combination of an electrode material and an electrolyte leads to

truly outstanding performance. This opens the door to development of even better supercapacitors

using safe and non-flammable ionic liquid electrolytes.”

1.5. Price and functional issues

Today, the upfront cost of a supercapacitor is almost never lower than the component or circuit

replaced such as a tantalum or aluminium electrolytic capacitor or a battery. Despite this, the high

up front cost of a supercapacitor does not prevent the occurrence of cost saving over life for

systems where supercapacitors are introduced. This is partly because supercapacitors last longer

and take more punishment than batteries.

The main functions that supercapacitors will perform over the coming decade are shown below

with examples of appropriate applications. Relative to batteries, working at very low temperatures

and fast charging without fast discharging in a given application are less important than the other

functions and combinations of function shown relative to batteries. Note that most of them can be

described as electrical engineering rather than electronics, this being the trend in market value as

well. Pulse power and bridging power applications tend to combine high power density ie fast

charging and fast discharging relative to batteries.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

12

© ID

Te

ch

Ex L

td

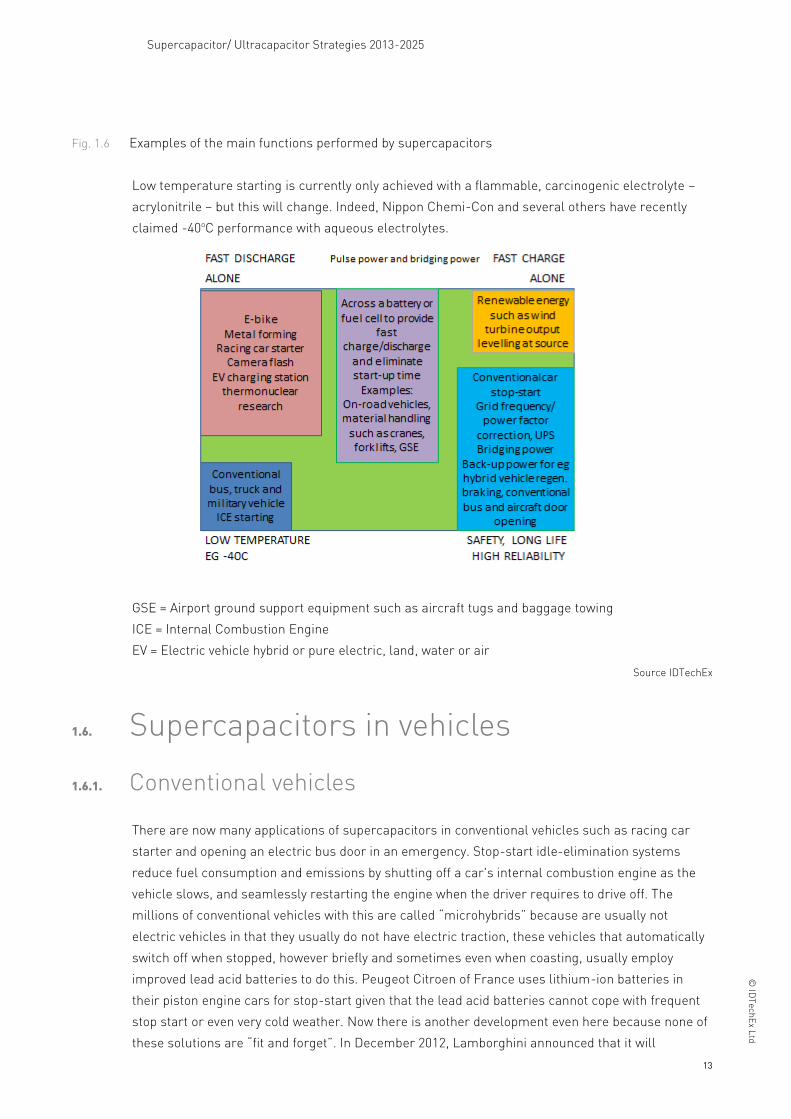

Fig. 1.5 The main functions that supercapacitors will perform over the coming decade

FAST DISCHARGE Pulse power & bridging power

Alone Alone

FAST CHARGE

LOW TEMPERATUREEG -40C

SAFETY, LONGLIFEHIGH RELIABILITY

MAINAPPLICATIONS

2013-2023

Source IDTechEx

These benefits are particularly useful in replacing, partially replacing, enhancing and extending the

life of rechargeable batteries.

Examples of the main functions performed by supercapacitors in 2013 are shown below.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

13

© ID

Te

ch

Ex L

td

Fig. 1.6 Examples of the main functions performed by supercapacitors

Low temperature starting is currently only achieved with a flammable, carcinogenic electrolyte –

acrylonitrile – but this will change. Indeed, Nippon Chemi-Con and several others have recently

claimed -40oC performance with aqueous electrolytes.

GSE = Airport ground support equipment such as aircraft tugs and baggage towing

ICE = Internal Combustion Engine

EV = Electric vehicle hybrid or pure electric, land, water or air

Source IDTechEx

1.6. Supercapacitors in vehicles

1.6.1. Conventional vehicles

There are now many applications of supercapacitors in conventional vehicles such as racing car

starter and opening an electric bus door in an emergency. Stop-start idle-elimination systems

reduce fuel consumption and emissions by shutting off a car's internal combustion engine as the

vehicle slows, and seamlessly restarting the engine when the driver requires to drive off. The

millions of conventional vehicles with this are called “microhybrids” because are usually not

electric vehicles in that they usually do not have electric traction, these vehicles that automatically

switch off when stopped, however briefly and sometimes even when coasting, usually employ

improved lead acid batteries to do this. Peugeot Citroen of France uses lithium-ion batteries in

their piston engine cars for stop-start given that the lead acid batteries cannot cope with frequent

stop start or even very cold weather. Now there is another development even here because none of

these solutions are “fit and forget”. In December 2012, Lamborghini announced that it will

Supercapacitor/ Ultracapacitor Strategies 2013-2025

14

© ID

Te

ch

Ex L

td

incorporate Maxwell “ultracapacitors” to support a stop-start idle-elimination system in their

Aventador conventional cars which are due to go into production shortly. The idle-elimination

system is an important element of Lamborghini's announced program to reduce its new models'

CO2 emissions by 35 percent by 2015. Incorporating the six-cell ultracapacitor module for added

cranking power to ensure efficient restarting for the 12-cylinder, 700-horse power Aventador also

enabled Lamborghini to reduce the size and weight of the battery to further enhance performance.

The system originally was designed by Dimac, Maxwell's ultracapacitor distribution partner in Italy.

The production system will be supplied by the Continental Engineering Services unit of Continental

AG, one of the world's leading automotive electronics and mechatronics suppliers. Ultracapacitors

provide burst power to re-start the engine, relieving the car's battery of high current, repetitive

cycling that can shorten battery life.

"This design win with one of the world's leading producers of high-performance autos provides

additional validation of ultracapacitors as an enabling technology for fuel-efficiency and reduced

emissions in passenger, commercial and public transit vehicles," said David Schramm, Maxwell's

president and chief executive officer. "We continue to focus on penetrating the large and

strategically important automotive and transportation markets by aligning ourselves with industry

leaders such as Lamborghini and Continental, and continuously strengthening our design,

engineering and production capabilities."

1.6.2. Electric vehicles

Clearly vehicles are a major focus because the properties of existing supercapacitors are

appropriate to many functions in vehicles. A more detailed view of the vehicle market is shown

below.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

15

© ID

Te

ch

Ex L

td

Fig. 1.7 The evolution from conventional to various types of electric vehicle related to supercapacitor

applications in them today, where hybrids and pure electric versions are a primary target

Source IDTechEx

In contrast to the massive success with pure electric e-bikes, which sometimes use

supercapacitors, forklift and boats, the pure electric on-road cars are a failure today. They sell

globally at a fraction of the number of even pure electric golf cars where demand is 150,000 yearly,

let alone pure electric power chairs and 3 and 4 wheel scooters for the disabled at around 1.3

million yearly or pure electric e-bikes at over 30 million yearly.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

16

© ID

Te

ch

Ex L

td

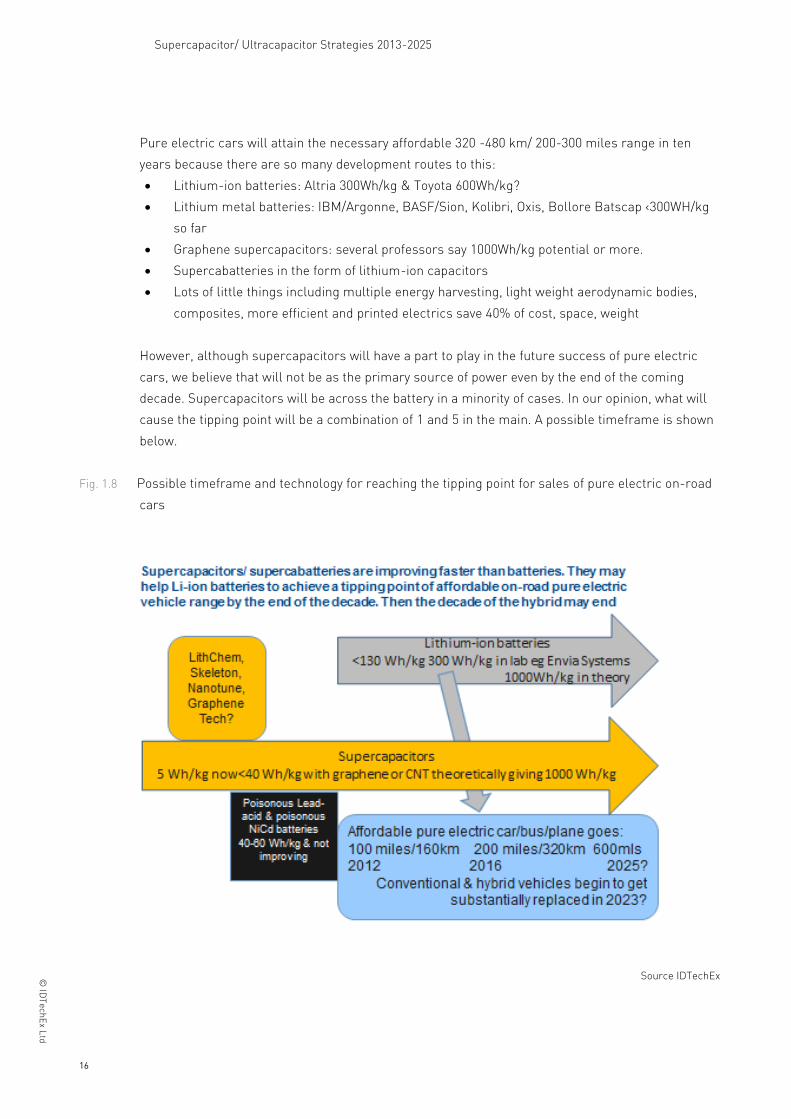

Pure electric cars will attain the necessary affordable 320 -480 km/ 200-300 miles range in ten

years because there are so many development routes to this:

Lithium-ion batteries: Altria 300Wh/kg & Toyota 600Wh/kg?

Lithium metal batteries: IBM/Argonne, BASF/Sion, Kolibri, Oxis, Bollore Batscap <300WH/kg

so far

Graphene supercapacitors: several professors say 1000Wh/kg potential or more.

Supercabatteries in the form of lithium-ion capacitors

Lots of little things including multiple energy harvesting, light weight aerodynamic bodies,

composites, more efficient and printed electrics save 40% of cost, space, weight

However, although supercapacitors will have a part to play in the future success of pure electric

cars, we believe that will not be as the primary source of power even by the end of the coming

decade. Supercapacitors will be across the battery in a minority of cases. In our opinion, what will

cause the tipping point will be a combination of 1 and 5 in the main. A possible timeframe is shown

below.

Fig. 1.8 Possible timeframe and technology for reaching the tipping point for sales of pure electric on-road

cars

Source IDTechEx

Supercapacitor/ Ultracapacitor Strategies 2013-2025

17

© ID

Te

ch

Ex L

td

1.7. Incidence of the different technologies

1.7.1. Incidence of manufacturers by operating principle

The number of manufacturers and putative manufacturers of supercapacitors/supercabatteries by

six sub-categories of technology is shown below.

Fig. 1.9 The number of manufacturers and putative manufacturers of supercapacitors/supercabatteries by

six sub-categories of technology

Symmetric supercapacitor EDLC

6574%

Supercabattery based on lithium LiC

1416%

Ionicliquid

6%

Supercabattery based on nickel battery

AEDLCNi 2

2%

Pseudocapacitor RuO2 part electrostatic, part

electrochemical2

2%

Tantalum electrolytic/ supercapacitor

TaHybrid 1

1%

Source IDTechEx

1.7.2. Incidence of current collector and active electrode

types

Current collectors are mainly aluminium for symmetrical EDLCs. The active electrode material is

mainly vegetable-derived carbon which is “activated” by solvents to give high area and an active

surface generating efficient electrochemical double layers. An increasing minority use larger-area

carbon such as carbon from carbide, aerogel carbon, carbon nanotubes CNT or nano-onions or

graphene, sometimes curved to deter re-agglomeration, though much of this work is currently pre-

production and not yet anywhere near to its theoretical capacitance and energy density or even

significantly better than coconut-based active-electrode carbon in supercapacitors. Some cells are

Supercapacitor/ Ultracapacitor Strategies 2013-2025

18

© ID

Te

ch

Ex L

td

reaching higher voltage giving the prospect of higher energy density and reliability, since fewer

interconnects are generated and energy density is proportional to the square of voltage. The

current collectors are usually aluminium foil for acetonitrile and other organic electrolytes and 3D

conductive polymer film for aqueous electrolytes though pre-coating aluminium foil with a carbon-

based elastomer is being trialled to protect the foil from aqueous electrolyte. Such slot coated

eleastonmers are often used to grip difficult active electrode materials such as graphene and CNT.

1.7.3. Electrolytes

It is the electrolyte that burns in a supercapacitor just as it is in lithium-ion batteries. In both cases

the traditional electrolytes are wet and toxic (eg giving off HCN that can kill in an enclosed space) in

the main. Accordingly, solid/ gel polymer electrolytes were developed for both that lack the toxicity.

They can still be flammable but to less an extent than volatile acetonitrile and they are usually not

subject to the stringent regulations restricting transport and use of large acetonitrile

supercapacitors. With supercapacitors things have gone farther than with batteries, so many

manufacturers now offer, usually exclusively, aqueous electrolytes such as sufuric acid. They have

very little restriction concerning disposal after use. The choice of electrolytes is therefore

acetonitrile, which is alleged to cause birth defects and cancer, and a rapidly increasing percentage

of companies that offer aqueous electrolytes or the relatively new ionic liquids that are inherently

ionically conductive, needing no solvent. The distribution is shown below

Incidence of acetonitrile, aqueous electrolytes/solid polymer electrolytes and ionic liquids by

number of supercapacitor and supercabattery manufacturer using them.

Fig. 1.10 Incidence of manufacturers of various types of supercapacitor and variant by operating principle

Acetonitrile51%

Aqueous43%

Ionicliquid6%

Source IDTechEx

Supercapacitor/ Ultracapacitor Strategies 2013-2025

19

© ID

Te

ch

Ex L

td

1.7.4. Solid electrolytes

In March 2013, it was announced that scientists at Oak Ridge National Laboratory have developed

the first high-performance, nanostructured solid electrolyte for more energy-dense lithium ion

batteries.

Today's lithium-ion batteries rely on a liquid electrolyte, the material that conducts ions between

the negatively charged anode and positive cathode. But liquid electrolytes often entail safety issues

because of their flammability, especially as researchers try to pack more energy in a smaller

battery volume. Building batteries with a solid electrolyte, as ORNL researchers have

demonstrated, could overcome these safety concerns and size constraints.

"To make a safer, lightweight battery, we need the design at the beginning to have safety in mind,"

said ORNL's Chengdu Liang, who led the newly published study in the Journal of the American

Chemical Society. "We started with a conventional material that is highly stable in a battery system

- in particular one that is compatible with a lithium metal anode."

The ability to use pure lithium metal as an anode could ultimately yield batteries five to 10 times

more powerful than current versions, which employ carbon based anodes.

"Cycling highly reactive lithium metal in flammable organic electrolytes causes serious safety

concerns," Liang said. "A solid electrolyte enables the lithium metal to cycle well, with highly

enhanced safety."

The ORNL team developed its solid electrolyte by manipulating a material called lithium

thiophosphate so that it could conduct ions 1,000 times faster than its natural bulk form. The

researchers used a chemical process called nanostructuring, which alters the structure of the

crystals that make up the material.

"Think about it in terms of a big crystal of quartz vs. very fine beach sand," said coauthor Adam

Rondinone. "You can have the same total volume of material, but it's broken up into very small

particles that are packed together. It's made of the same atoms in roughly the same proportions,

but at the nanoscale the structure is different. And now this solid material conducts lithium ions at

a much greater rate than the original large crystal."

The researchers are continuing to test lab scale battery cells, and a patent on the team's invention

is pending.

"We use a room-temperature, solution-based reaction that we believe can be easily scaled up,"

Rondinone said. "It's an energy-efficient way to make large amounts of this material."

For information about industry collaboration opportunities, please visit the ORNL Partnerships

website at http://www.ornl.gov/adm/partnerships/index.shtml

Supercapacitor/ Ultracapacitor Strategies 2013-2025

20

© ID

Te

ch

Ex L

td

The study is published as "Anomalous High Ionic Conductivity of Nanoporous ß-Li3PS4," and its

ORNL coauthors are Zengcai Liu, Wujun Fu, Andrew Payzant, Xiang Yu, Zili Wu, Nancy Dudney, Jim

Kiggans, Kunlun Hong, Adam Rondinone and Chengdu Liang. The work was sponsored by the

Division of Materials Sciences and Engineering in DOE's Office of Science.

The materials synthesis and characterization were supported by the Center for Nanophase

Materials Sciences at ORNL. CNMS is one of the five DOE Nanoscale Science Research Centers

supported by the DOE Office of Science, premier national user facilities for interdisciplinary

research at the nanoscale. Together the NSRCs comprise a suite of complementary facilities that

provide researchers with state-of-the-art capabilities to fabricate, process, characterize and model

nanoscale materials, and constitute the largest infrastructure investment of the National

Nanotechnology Initiative. The NSRCs are located at DOE's Argonne, Brookhaven, Lawrence

Berkeley, Oak Ridge and Sandia and Los Alamos national laboratories. For more information about

the DOE NSRCs, please visit http://science.energy.gov/bes/suf/user-facilities/nanoscale-science-

research-centers/ . ORNL is managed by UT-Battelle for the Department of Energy's Office of

Science.

1.8. Achieving the impossible

In many cases something previously impossible is achieved by introducing supercapacitors. In

others, the performance of an existing component is enhanced by having a supercapacitor across it

or by replacing it. Here are some examples.

Fig. 1.11 Component displacement mapped as a function of benefits relative to batteries conferred by

supercapacitors

Source IDTechEx

Supercapacitor/ Ultracapacitor Strategies 2013-2025

21

© ID

Te

ch

Ex L

td

Relative to electrolytic capacitors, previously the capacitors with highest energy density,

supercapacitors have few of the above advantages. Here their advantages mainly relate to higher

capacitance and power density than the best capacitors in this respect and, for very high

capacitance, sometimes lower cost partly due to the mounting, connection and enclosure costs of

the equivalent huge array of electrolytic capacitors, which bring with them many extra failure

modes and even greater size if they are to be non-polar like most supercapacitors. However, there

are far fewer market opportunities in this as opposed to replacing or partly replacing batteries.

Only a few years ago, the major automotive and railway rolling stock manufacturers rarely saw

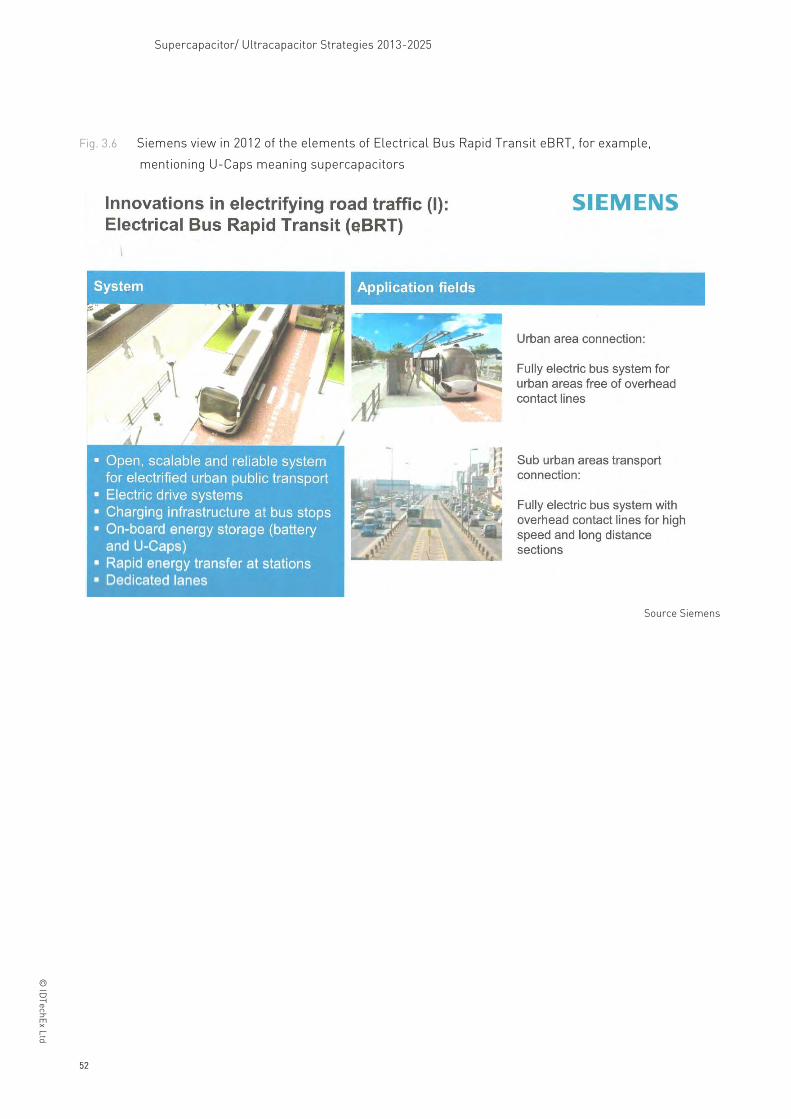

supercapacitors as part of their toolkit. However, nowadays almost all of them do. A Siemens view

presented in 2012 of the elements of Electrical Bus Rapid Transit eBRT, for example, mentioned

supercapacitors as part of the new design toolkit. Below we give just a few examples of the way in

which supercapacitors and their variants are replacing, or partly replacing other components,

particularly rechargeable batteries, this despite their energy density being inferior as yet. As energy

density improves – a priority we have observed in research – the pace of replacing batteries will

quicken.

Table 1.3 15 examples of component displacement by supercapacitors in 2012-3

Use Action Result Effect on

battery or

capacitor

market

Pure

electric

and fuel

cell

bikes,

cars,

buses,

material

handling

vehicles,

earth

moving

vehicles,

trucks,

trams,

trains,

cranes

and

military

vehicles

Put across

the battery –

typically

lithium-ion

batteries - or

fuel cell

Faster charging stations and regenerative braking, energy harvesting shock absorbers etc

can be used without damaging the battery. Sometimes more of the battery’s energy can be

used ie the battery can be used to a deeper state of discharge, extending the range of the

vehicle. In the case of fuel cells, it compensates for start-up time and provides surges of

power for eg starting off with a vehicle, accelerating or climbing a hill or earthmoving or

heavy lifting. Fuel cells and batteries have poor power density. In a system that eliminates an

internal combustion engine, you get little or no noise, land or air pollution. Military vehicles

have almost no heat or gas signature for missiles to home in on. Below and left: Mazda pure

electric car adds a supercapacitor across the Nippon Chemi-Con battery to protect it and

enhance performance.

Source IDTechEx

Bollore Pininfarina Bluecar below is a pure electric car which has a Batscap supercapacitor

to enhance performance and protect the battery. Bollore has introduced the Blue Car and it

is commercially available for daily rentals. The version currently on the road does not use

ultracapacitors, but is battery only. The next version is intended to use caps as well as being

available for sale to consumers.

Lithium-ion

battery

market

reduced in

value

compared

with the

partial

alternative

of over-

sizing the

battery.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

22

© ID

Te

ch

Ex L

td

Use Action Result Effect on

battery or

capacitor

market

Source Bollore

The Kleenspeed KAR pure electric prototype shown below also has a supercapacitor across

the battery.

Source Kleenspeed

Below: the Riversimple car in the UK replaces the lithium-ion battery across its fuel cell

with a Maxwell Technologies supercapacitor.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

23

© ID

Te

ch

Ex L

td

Use Action Result Effect on

battery or

capacitor

market

Source IDTechEx

Replacing

one of the

lead acid

batteries in a

truck for

cold starting

eg -20C to -

40C when

the lead acid

battery can

release no

more than

half its

power

Truck almost always starts even in the coldest weather and after the hotel facilities have

been used overnight with the engine off. New regulations often ban engine idling.

Source IDTechEx

Reduces the

lead acid

battery

market

Completely

replacing all

batteries in a

pure electric

vehicle

where

frequent

recharging is

practicable

to compen-

Longer life and faster charge and discharge at higher up front cost but possibly lower cost-

over-life due to tolerating tougher duty cycle with less maintenance and longer life.

Improved safety and reliability and almost no maintenance. Sinautec bus with

supercapacitors and no battery picking up overhead power at bus stop.

Lithium-ion

battery

market is

reduced in

value:

batteries not

needed

Supercapacitor/ Ultracapacitor Strategies 2013-2025

24

© ID

Te

ch

Ex L

td

Use Action Result Effect on

battery or

capacitor

market

sate for the

energy

density being

no better

than that of a

lead-acid

battery today

(a limitation

that will not

exist at some

time in the

future)

Source Sinautec

Hybrid

electric

vehicles

Replacing

the battery in

a hybrid

electric

vehicle like

this one in

Russia

shown right

that uses

ELIT super

capacitors

and the MAN

Lion’s City

Hybrid bus in

Germany

that also

uses a

super-

capacitor

instead of a

battery

shown.

Source ELIT

Reduces the

market for

lithium-ion

batteries

Supercapacitor/ Ultracapacitor Strategies 2013-2025

25

© ID

Te

ch

Ex L

td

Use Action Result Effect on

battery or

capacitor

market

Source MAN presentation at IAA Electric Vehicle Congress Hannover 2012

The Toyota hybrid TS030 racing car below was a winner in 2012 with Nisshinbo

supercapacitors replacing the battery

Source Toyota

Light

Train

Uses super-

capacitor

energy

storage to

operate

without an

external

power

Wireless operation seen as cheaper and less visually-intrusive than conventional

electrification. Demonstrated August 2012. Commercial production by 2014 - viable for use

in more than 100 smaller and medium-sized Chinese cities, as well as export.

Supercapacitor/ Ultracapacitor Strategies 2013-2025

26

© ID

Te

ch

Ex L

td

Use Action Result Effect on

battery or

capacitor

market

supply.

Underfloor

power pick-

ups 30 sec

(2km) charge

the roof-

mounted

super

capacitor

unit from a

fixed supply

while train is

standing at

station.

Energy re-

generated

during

braking is

recovered

for reuse.

Source CSR Zhuzhou Electric Locomotive

Siemens has something similar in Germany with a supercapacitor set across a NiMH battery

in a streetcar that can cover 2.5km untethered. Again regenerative braking is made possible.

Power consumption reduced by one third and carbon dioxide sharply down. Overhead power

cables removed from where they are a visual blight and where they are a problem at

intersections.

Genève tram operator TPG is testing a prototype supercapacitor energy storage unit which

allows braking energy to be recovered, and enables a tram to run for short distances without

an external power supply.

Source Tango Trams

The 1 tonne supercapacitor unit has been installed on the roof of one of a batch of 32 Tango

trams being delivered to TPG by Stadler Rail. It can store the equivalent of the entire kinetic

energy of an empty tram moving at 55 km/h, according to Stadler, and is more effective than

batteries at absorbing and releasing the high short-term currents produced during braking.

Energy regenerated during braking is reused as the vehicle starts to move, when its power

requirement is highest. The stored energy can also power the tram for at least 400 m if the

overhead supply should fail. A distance of 1500 m has been achieved with careful driving

under low-acceleration, low-speed test conditions.

The prototype is undergoing extensive testing by TPG, Stadler and traction equipment

supplier ABB. Its energy consumption is being compared with the rest of the Tango fleet

equipped for conventional regenerative braking which feeds current back into the overhead

supply. If the tests prove successful, the other 31 Tango vehicles for TPG could be equipped

with supercapacitors 'relatively easily'. Source of the Geneva story: Railway Gazette

Wind

turbine

Pitch control

when

electrics fail

Replacing

previous

emergency

backup such

as a lithium-

ion

rechargeable

battery or a

lithium

thionyl

chloride

battery with

Faster more reliable pitch control backup prevents explosive destruction of the turbine in a

high wind if electrics fail

Reduces the

market for

lithium-ion

or other

back-up

batteries

Supercapacitor/ Ultracapacitor Strategies 2013-2025

27

© ID

Te

ch

Ex L

td

Use Action Result Effect on

battery or

capacitor

market

conventional

capacitors

.

Metal

forming

and

welding

Replacing

banks of

electrolytic

capacitors in

a much

smaller

space

provided the

longer time

constant is

tolerable

Smaller, lighter weight equipment Reduces

capacitor

market

Camera

flash eg

in mobile

phones

Replacing

electrolytic

capacitor/

halogen bulb

with super

capacitor/

high power

LED

Flash pictures can be taken from farther away because more energy can be discharged

within the severe space constraints

Source Murata

Reduces

electro-

lytic

capacitor

market

Cordless

drill with

except-

ional fast

charging

Replacing

lithium-ion

battery

Cordless drill for use in space developed by NASA with supercapacitors and no battery.

Commercial versions are now available from such companies as Demain International sold

through Top Link Industrial Co. as are battery free flashlights etc. Benefits include long,

maintenance-free life with lower cost of ownership, faster charging and greener credentials

in some cases.

Replaces

lithium-ion

batteries

Supercapacitor/ Ultracapacitor Strategies 2013-2025

28

© ID

Te

ch

Ex L

td

Use Action Result Effect on

battery or

capacitor

market

Source NASA

Source IDTechEx

The basic functions can be summarised as reaching market acceptance in the following sequence,

with a few notable exceptions. Most of these functions can be seen commercially now but we are

forecasting when major supercapacitor business will result from them and suppliers currently

obtaining major sales in these.

Table 1.4 Supercapacitor functions reaching major market acceptance 2013-2023 with some of the

companies leading the success by sector

Energy regeneration/ energy harvesting and surge power, particularly by battery enhancement and protection in road vehicles, material handling.

Backup power, notably for emergencies, and peak assist

Start up and peak assist power eg for fuel cells, office machines, remote metering

Energy regeneration/ energy harvesting and surge power, by fuel cell enhancement and protection

Pulse power for radar, welding, metal forming, camera flash etc and high frequency uses in electronics

Main traction power, particularly vehicles and load moving

Maxwell Technologies Nippon ChemiCon Batscap

Maxwell Technologies Nesscap LSMtron

Nesscap Energy LSMtron

Maxwell Technologies Ioxus JM Energy Skeleton Technologies

Nesscap Energy Yunasko Cap-XX Murata

LithChem Energy JM Energy Skeleton Technologies Asahi Kasei/FDK Hitachi Kankyu

Source IDTechEx

It is therefore unlikely that the current largest manufacturers, with Maxwell Technologies in the

lead, will stay in that position over the next ten years. However, it is too early to bet on who, if

2013 2018 2023

Supercapacitor/ Ultracapacitor Strategies 2013-2025

29

© ID

Te

ch

Ex L

td

anyone, will take their place. It is likely to include acquisitive companies offering broad capability

including high energy density, non-flammable, cleaner devices and other attributes in an affordable

package for electrical engineering applications and marketing and possibly manufacturing them

globally. With the winner having one billion dollars in sales within 15 years, this race is starting to

attract some very large companies.

1.9. Manufacturers and putative

manufacturers

We have investigated the following manufacturers and putative manufacturers and also others in

the value chain, the work taking place almost entirely in the last quarter of 2012 with following

updates and extensions.

Table 1.5 80 manufacturers, putative manufacturers and commercial companies developing

supercapacitors, supercabatteries and carbon-enhanced lead batteries for commercialisation

with country, website and device technology.

EDLC = Symmetric supercapacitor

LiC = Supercabattery based on lithium

PbC = Supercabattery or carbon-enhanced battery based on lead battery

AEDLCNi = Supercabattery based on nickel battery

PseudoC = Pseudocapacitor RuO2 part electrostatic, part electrochemical

TaHybrid = Tantalum electrolytic/ supercapacitor construction

CNT = carbon nanotube. Gp = Graphene.

Yellow = not yet trading

Company Country Website Technology

1. ABSL EnerSys UK http://www.abslspaceproducts.com http://www.enersys.com EDLC carbon

2. Ada

Technologies

USA http://www.adatech.com EDLC carbon

3. Advanced

Capacitor

Technologies

Japan http://www.act.jp/eng/ LiC

4. ApowerCap

Technologies

Ukraine http://www.apowercap.com EDLC carbon

5. Asahi Kasei –

FDK

Japan http://www.fdk.co.jp LiC

6. AVX USA

(Mexico)

http://www.avx.com EDLC carbon

7. Axion Power