Embed Size (px)

Citation preview

Super-Senior AAA CDOs and Other Derivatives Debacles

Christopher L. CulpCompassLexecon

and

The University of Chicago, Graduate School of Businessand

Universität Bern, Institut für Finanzmanagement

Email: [email protected]

GARP Academic Lecture SeriesGlobal Association of Risk Professionals (Zürich Chapter)

CfBS Center for Business Studies, Wengistrasse 1, CH-8004 Zürich6 March 2008

2

Agenda:

Subprime and the Credit CrisisContagionIssues for ConsiderationComparisons to Earlier DisastersQ&A

3

Subprime Loans

Mortgage Banker

High-Risk Borrower

House

Mortgage Broker

Principal & Interest

Cash to Purchase House

Subprime Loan

Purchase Price of House

Home Ownership

Collateral for Loan

4

U.S. Subprime Loan Growth

5

Housing Price Appreciation Slows

6

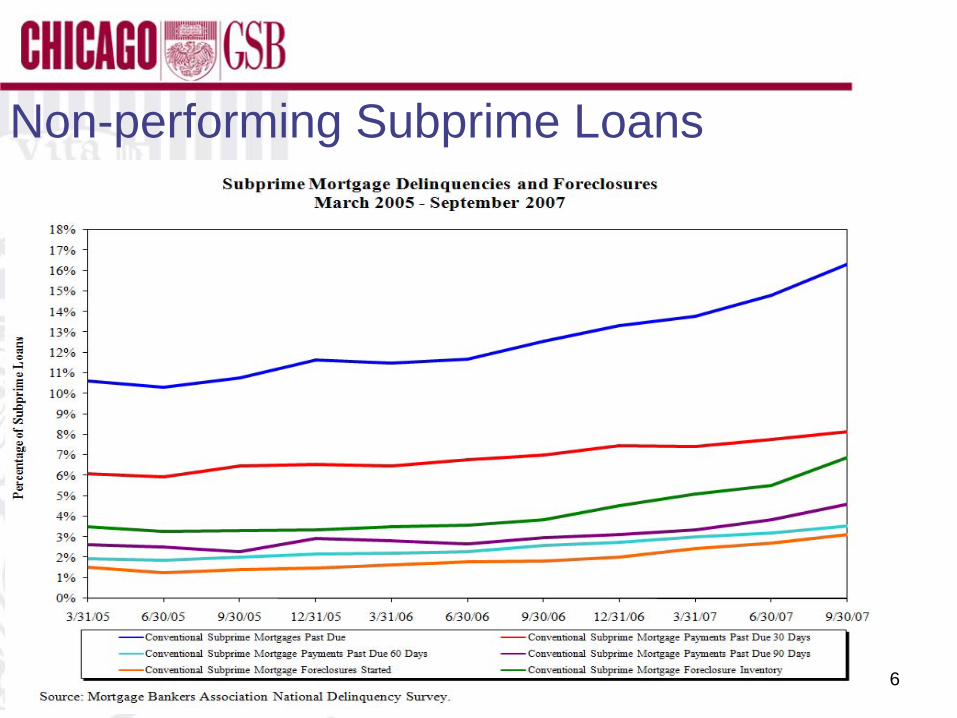

Non-performing Subprime Loans

7

Securitization of Subprime Loans

.

.

.

.

.

.

.

.

.

8

Subprime Loans Securitized into Residential Mortgage-Backed Securities (RMBS)

RMBSSubprime Loan

Subprime Loan

Subprime Loan

RMBSSubprime Loan

Subprime Loan

Subprime Loan

RMBS

.

.

.

.

.

.

.

.

.

9

RMBS Sold to…Funds

RMBSSubprime Loan

Subprime Loan

Subprime Loan

RMBSSubprime Loan

Subprime Loan

Subprime Loan

.

.

.

.

.

.

RMBS

Funds Investors

.

.

.

.

.

.

.

.

.

10

RMBSSubprime Loan

Subprime Loan

Subprime Loan

RMBSSubprime Loan

Subprime Loan

Subprime Loan

.

.

.

.

.

.

RMBS

Funds

SIVs

CP & SrNotes

MezzNotes

Capital Notes

InvestorsRMBS Sold to…SIVs/SIV-Lites

.

.

.

.

.

.

.

.

.

11

RMBSSubprime Loan

Subprime Loan

Subprime Loan

RMBSSubprime Loan

Subprime Loan

Subprime Loan

.

.

.

.

.

.

RMBS

Funds

SIVs

Cash ABS CDOs SuperSr

Senior

Mezz

Residual

CP & SrNotes

MezzNotes

Capital Notes

InvestorsRMBS Sold to…Cash ABS CDOs

.

.

.

.

.

.

.

.

.

12

RMBSSubprime Loan

Subprime Loan

Subprime Loan

RMBSSubprime Loan

Subprime Loan

Subprime Loan

.

.

.

.

.

.

RMBS

Funds

SIVs

Cash ABS CDOs SuperSr

Senior

Mezz

Residual

CP & SrNotes

MezzNotes

Capital Notes

Investors

Synthetic ABS

CDOs

Protection Sales

Protection Sales by…Synthetic ABS CDOs

.

.

.

.

.

.

.

.

.

13

RMBSSubprime Loan

Subprime Loan

Subprime Loan

RMBSSubprime Loan

Subprime Loan

Subprime Loan

.

.

.

.

.

.

RMBS

Funds

SIVs

ABx

Cash ABS CDOs SuperSr

Senior

Mezz

Residual35-100%

7-12%

3-7%

0-3%

.

.

.

Residual

CP & SrNotes

MezzNotes

Capital Notes

Investors

Synthetic ABS

CDOs

Protection Sales

Protection Sales

Protection Sales by…ABx Participants

.

.

.

.

.

.

.

.

.

14

RMBSSubprime Loan

Subprime Loan

Subprime Loan

RMBSSubprime Loan

Subprime Loan

Subprime Loan

.

.

.

.

.

.

RMBS

Funds

SIVs

ABx

Cash ABS CDOs SuperSr

Senior

Mezz

Residual35-100%

7-12%

3-7%

0-3%

.

.

.

Residual

MezzCDOs

SuperSr

Senior

Mezz

Residual

CP & SrNotes

MezzNotes

Capital Notes

Investors

Synthetic ABS

CDOs

Protection Sales

Protection Sales

Exposure Acquired by…Mezzanine CDOs

15

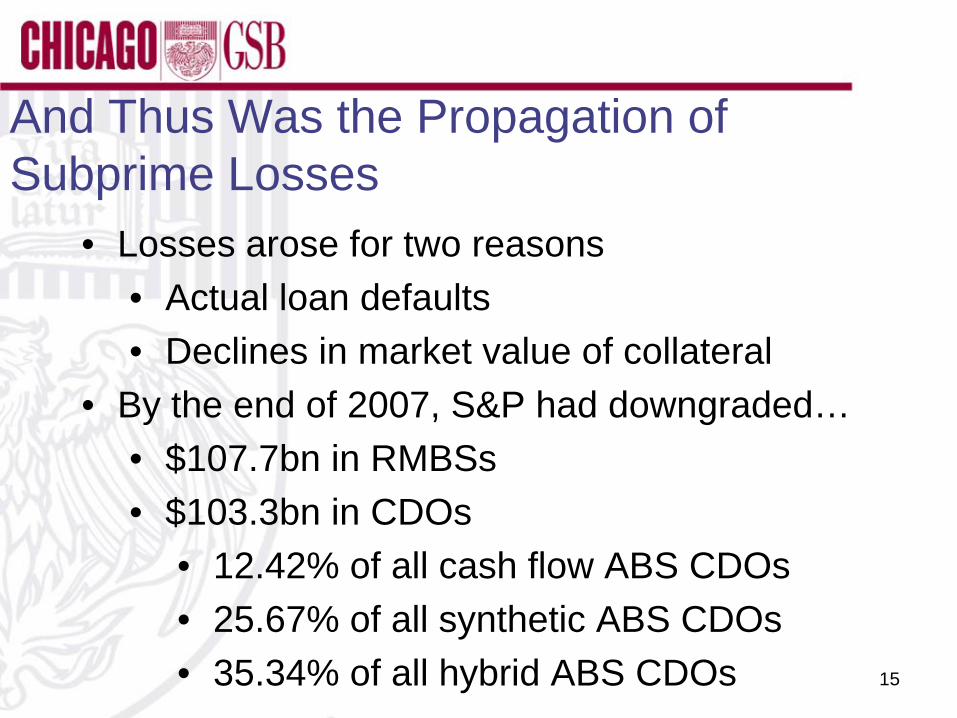

And Thus Was the Propagation of Subprime Losses

• Losses arose for two reasons• Actual loan defaults• Declines in market value of collateral

• By the end of 2007, S&P had downgraded…• $107.7bn in RMBSs• $103.3bn in CDOs

• 12.42% of all cash flow ABS CDOs• 25.67% of all synthetic ABS CDOs• 35.34% of all hybrid ABS CDOs

16

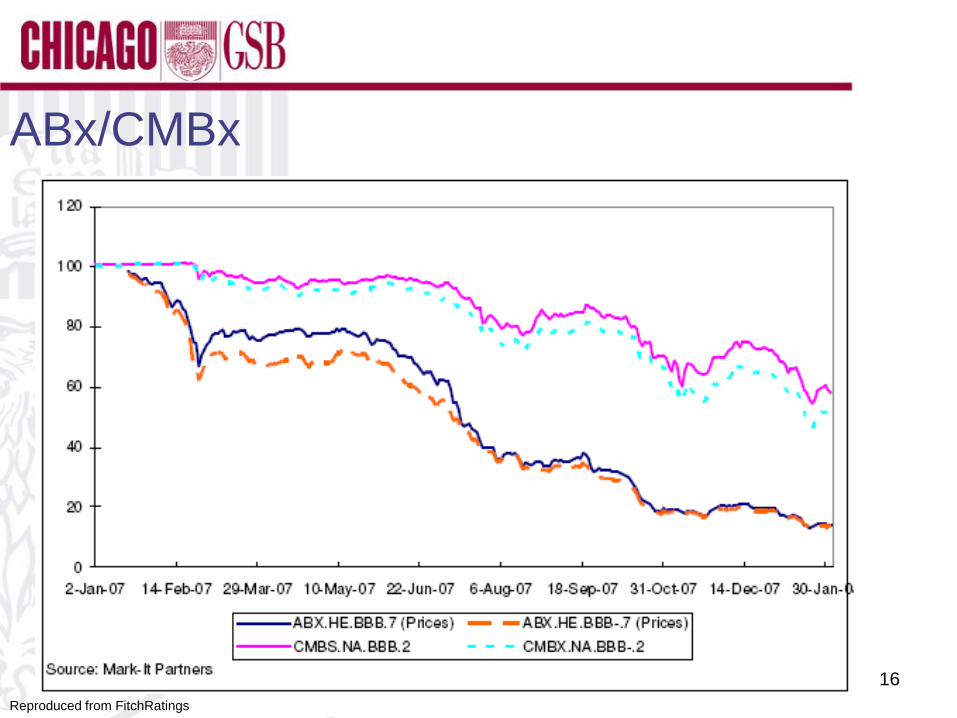

ABx/CMBx

Reproduced from FitchRatings

17

New CDO Issuance Plummets

18

Agenda:

Subprime & the Credit CrisisContagionIssues for ConsiderationComparisons to Earlier DisastersQ&A

19

Interbank Funding Markets

20

ABCP

21

CDx

22

Impacts of Heightened CDx Spread Volatilities• Higher spreads between credit qualities, heightened

spread volatility, and increased CDS basis volatility• Problematic for MV CDO structures (e.g., CPDOs)• High spread vols appeal to relative value traders:

• Hedge funds and other “basis traders” are bouncing between markets looking for the good deal of the day

• This makes it difficult to count on these players for “stable supply” at any given time

23

LCDx

24

CLOs and Syndicated Leveraged Loans• Although few CLOs have been downgraded,

contagion has taken its toll on CLOs• Disappearance of negative carry trades• Losses by major CLO purchasers (e.g., banks &

SIVs) have depressed demand for CLO tranches• Warehouse lines pulled• Forced unwinds by MV CLOs

• Severe impact on leveraged loan market • CLOs were 60%+ of the institutional demand• Huge forward loan calendar in Summer 2007• Significant slowdown in leveraged loan

syndication

25

Leveraged Loans, April 2007 – Dec 2007

26

Constant Proportion Debt Obligations (CPDOs)

• CPDO NAVs decline as index spreads widen• Rating agency actions

• Downgrade warnings last fall• Actual downgrades in late Feb 2008

• Fear that NAV cash-out triggers will exacerbate index market volatility

• “Vindication” for CPDO critics? • Did the design and structure of these products make

them fundamentally vulnerable from the beginning?

27

Leveraged Super-Senior Notes (LSSNs)

• LSSN triggers may be MtM, loss only, or spread & loss• Triggers allow protection buyers to increase the

notional on the protection swap and force protection sellers to meet calls for new collateral

• Failure to post new collateral after a trigger event entitles the protection buyer to liquidate collateral and unwind the protection swap – we’re starting to see this

• Conduit holdings• Several conduits have disclosed LSSN exposures• Significant conduit exposures could transmit LSSN

problems back into the ABCP markets

.

.

.

.

.

.

.

.

.

Bank & Monoline Exposures

RMBSSubprime Loan

Subprime Loan

Subprime Loan

RMBSSubprime Loan

Subprime Loan

Subprime Loan

.

.

.

.

.

.

RMBS

Funds

SIVs

ABS CDOs

BanksSponsors & Investors

Sponsors & Liquidity Support

Arrangers & Underwriters

Monolines

Hedging of Subprime

Exposure and Super-Senior

Tranches

Wraps & Guaranties

MezzCDOs

Arrangers & Underwriters

Wraps & Guaranties

Super-Senior Exposure

Super-Senior Exposure

29

Bank CDS Spreads

30

Declared Write-Downs Through 1/17/08

US$ billionsMerrill Lynch & Co. Inc. 22.0

Citigroup Inc. 21.0

UBS AG 14.8

Morgan Stanley 9.6

Group of 13 Other Large Complex Financial Institutions* 23.3

Total 90.7*: Bank of America Corp., Barclays Bank PLC, The Bear Stearns Cos. Inc., BNP Paribas, Credit Suisse Group (U.S. GAAP), Deutsche Bank AG, The Goldman Sachs Group Inc., HSBC Holdings PLC, ING Groep NV, JPMorgan Chase & Co., Lehman BrothersHoldings Inc., The Royal Bank of Scotland Group PLC, Société Générale. Source: Standard & Poor’s, After the Credit Boom, Banks and Brokers Face a Sobering Year in 2008 (January 17, 2008), p.2.

Declared Write-Downs of CDOs, Subprime RMBS, and Leveraged Loans for SelectedLarge Complex Financial Institutions (as of January 17, 2008)

31

Monoline CDS Spreads

32

Monoline Spillover Effects

• Auction-rate muni securities market is frozen• Threat of defaults on wrapped CDO & CDO2 tranches• Fear of non-performing super-senior CDS hedges –

some very disturbing estimates of potential losses have been disclosed by banks if a monoline fails

• Some of the more extreme doomsday scenarios posit that the failure of a big monoline could…• Wipe out a large bank• Devastate muni investors and municipalities

33

Agenda:

Subprime & the Credit CrisisContagionIssues for ConsiderationComparisons to Earlier DisastersQ&A

34

1. Correlation Modeling

• Propagation of losses through SF waterfalls creates correlation linkages

• Contagion affects spread vols and correlations in non-subprime markets (e.g., CDX.NA.IG)

• Which question should we be asking?• How do we model these correlation shocks?• Can we model these correlation shocks?

35

2. Transparency & Due Diligence

• Should an investor buy a SF product if she really does not know what’s behind it?• Does the manager/sponsor know?• Will they tell you?• Will it matter if they do (see Issue #1)?

• SF deal arrangers and underwriters• Is this an opportunity to significantly enhance

investor risk disclosures?• Can they?

36

3. Delegated Monitoring• As the credit crisis unfolded, did investors fall prey to an

inability to differentiate AAA deals, leading to suspicions that all AAA-rated SF deals were “lemons”?

• Was this a result of investors relying too much on “delegated monitoring” or too little on their own due diligence?

• Was there a failure of delegated monitoring?• A thought B was doing the risk analysis• B thought C was doing the risk analysis• C thought D was doing the risk analysis• D wasn’t doing the risk analysis

37

4. Rating Agency Policy Issues

• Were the downgrades too slow in coming?• How can we avoid “hung markets” as traders wait to

see what is downgraded and how far?• Do investors rely too heavily on ratings?• Do rating agencies have the right incentives? • Are “conflict of interest” concerns legitimate or

overstated?• Is the NRSRO designation process adequately

competitive?

38

5. Rating Agency Models & Criteria

• Are correlation and systematic risk adequately incorporated into ratings criteria and models?

• Will the new rating agency capital models & criteria help avoid SF problems in the future? Or are they placebos?

• Can the rating agencies assess market risk arising from credit risk as well as they can assess credit risk?

• Do MV CDO ratings criteria lead to too much volatility for “through-the-cycle” ratings?

• Should products with principal at risk ever get a AAA?• Should spreads on AAA-rated products differ

depending on the type of product?

39

6. Monolines• How do we deal with what now seems like excessive

bank credit exposure concentration to the monolines?• If a wrap is only as good as its wrapper…

• Are we relying too heavily on monolines as delegated monitors?

• Are monolines comfortable playing this role?• Have monolines moved too far toward underwriting

market risk by guaranteeing MV and MtM structures?• Do the proposals to separate monoline muni and SF

guaranty businesses make sense?• Were the late Feb reaffirmations of Ambac and MBIA

ratings by S&P “real,” or just stopgap measures?

40

Agenda:

Subprime & the Credit CrisisContagionIssues for ConsiderationComparisons to Earlier DisastersQ&A

41

Long-Term Capital Management

• Similarities:• Severe shifts in correlations• Bank exposures

• Differences:• LTCM’s problems were a genuine surprise, whereas

at least some of the subprime losses were anticipated

• LTCM was hit with an exogenous shock, whereas many of the subprime losses have been endogenous (i.e., propagated through SF waterfalls)

42

MG Refining & Marketing

• Similarities:• Problems triggered by cash flows tied to MV

changes and MtM• Spread and basis trading losses

• Differences:• Many subprime losses were balance sheet losses,

whereas most of MGRM’s losses became real only when the program was prematurely ended

• MGRM’s loss was firm-specific, whereas subprime losses are not

• MGRM’s MV and MtM problems arose from futures variation margin, not MV triggers

43

Bankers Trust Corporate Swaps

• Similarities:• Lack of transparency• Possible lack of due diligence• Suitability issues

• Differences:• BT’s counterparties that had problems (e.g., P&G)

were corporates, whereas most subprime losers have been financials

• The BT swaps were ostensibly “hedges,” whereas most subprime-related losses have been on investments

44

Barings

• Similarities:• Poorly defined internal controls on certain types of

transactions and strategies• Inadequate P&L attribution

• Differences:• Barings had a single trader trying to beat the

market, whereas subprime involved deliberate investments in a whole class of products

• Leeson lied to Barings about what he was doing, whereas structured credit activity was institutionally blessed (albeit perhaps with under-appreciated risks)

45

Orange County

• Similarities:• Chasing high yields can expose you to high risks• Disclosing a trading strategy does not necessarily

mean that investors understand and appreciate the risks of that strategy

• Beware of leverage (e.g., CPDOs/LSSNs)• Differences:

• Orange County pursued a fairly simple strategy with fairly basic financial instruments, whereas subprime SF losses arose from more complex credit arbstrategies involving more complex products

46

Agenda:

Subprime & the Credit CrisisContagionIssues for ConsiderationComparisons to Earlier DisastersQ&A

![[NERA] Subprime and Synthetic CDOs 2010](https://img.dokumen.tips/doc/110x75/55cf8dfd550346703b8d59ca/nera-subprime-and-synthetic-cdos-2010.jpg)