Embed Size (px)

Citation preview

Dynamic MacroeconomicsSummer Term 2011

Christian Bayer

Universität Bonn

May 15, 2011

C. Bayer Dynamic Macro

Overview of the Course: My Part

1. Introduction, Basic Theory

2. Stochastic Fluctuations

3. Numerical Tools

4. Estimation

5. Equilibrium

6. Stationary heterogenous agent economies

7. Heterogeneous agent economies with aggregate fluctuations

C. Bayer Dynamic Macro

Literature

Primary reading:

I Heer, B. and A. Maussner (2009), "Dynamic General EquilibriumModelling", 2nd edition, Springer, Berlin.I cover roughly: Ch. 1, 4, 7, 8

Secondary reading:

I Adda, J. and R. Cooper (2004): "Dynamic Economics", MIT Press,Cambridge.

I Ljungqvist, L. und T. Sargent (2004): "Recursive MacroeconomicTheory", MIT press, Cambridge.

I Stockey, N.L. and Lucas, R.E. with E.C. Prescott (1989): "RecursiveMethods in Economic Dynamics", Chapters 4 and 9, HavardUniversity Press, Cambridge..

C. Bayer Dynamic Macro

Motivation:The standard incomplete markets model

Hugget (1993), Aiyagari (1994) and Krussel and Smith (1998)

C. Bayer Dynamic Macro

What we want to model...

I Consider an economy in which households supply labor, consumeand accumulate capital.

I They each face idiosyncratic risk as their endowment with effi ciencyunits of labor changes over time (they may be employed orunemployed for example).

I Other than in a standard (i.e. complete markets) macro model, wewant to assume that households cannot trade away theiridiosyncratic risk on complete asset markets (there is no perfectunemployment insurance).

I We want to assume that the only asset households can trade is aclaim on the aggregate stock of capital.

I We want to understand the quantitative implications.

C. Bayer Dynamic Macro

What do we need to model...

I How households make their consumption-savings decisions givenprices (forward looking behavior)?

I Heterogeneity of households in wealthI The effect of aggregate fluctuations on this heterogeneity and itsrepercussions on prices.

C. Bayer Dynamic Macro

Households

Putting this a little more formally:

I Continuum of households that obtain income from supplying labornt and assets at at prices wt and rt respectively.

I Households enjoy utility from consumption ct , are expected utilitymaximizers and are infinitely lived.

I They discount future utility by the discount factor β.

I [Labour supply nt ∈ [nmin, nmax] is an exogenous stochastic process.]

C. Bayer Dynamic Macro

Budget and borrowing constraints

I We want to assume (following Aiyagari, 1994) that there are nocontingent claims households can trade.

I Households can only self-insure using the asset a.I Asset holdings must satisfy that the household is able to serviceeventual debt in any case

a′ ≥ bI b is an exogenous debt limit (necessary to avoid Ponzi schemes ifr < 0). We will typically set b = 0.

C. Bayer Dynamic Macro

Household Planning ProblemSetup

I The planning problem of each households can be summarized in theBellman equation

max<at>t=1...∞at∈R+

E0∞

∑t=0

βtu (wtnt + at (1+ rt )− at+1)

I where the sequence < at > is contingent on the history ofrealizations for (wt , rt , nt ,Zt )

I Zt is an aggregate state of the economy that determines theprobability distributions for nt , i.e. it determines aggregateemployment.

C. Bayer Dynamic Macro

Household Planning ProblemIssues in Solving

I The planning problem

max<at>t=1...∞at∈R+

E0∞

∑t=0

βtu (wtnt + at (1+ rt )− at+1)

yields in general first order conditions, with occasionally bindingconstraints.

−βtu′ (ct ) + βt+1 (1+ rt ) u′ (ct+1) = λt

where λt is the Lagrangian multiplier on the non-negativityconstraint for at .

I This cannot be solved using local approximations!I Another diffi culty arises in form of the prices (wt , rt ), which mayfluctuate with aggregate employment and households need to formexpectations about these price movements.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Part 1Introduction,

Dynamic Programming: Basic Theoryand First Numerical Tools

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

TheoryNumerics

The Theory of Dynamic Programming

1. Back to Consumption Theory 101: Indirect Utility and ValueFunctions

2. Basic dynamic programming in a finite horizon environment

3. Stationary Problems and Infinite Horizon Dynamic Programming

4. Stochastic Dynamic Programming

5. Analytical Solutions and Numerical Analysis

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

TheoryNumerics

Numerical Analysis of Dynamic Programming Problems

1. Continuous vs. discrete decision problems

2. Discrete Approximations to a Continuous State Space

3. Value Function Iteration

4. Transition Probability Matrices and Markov Chain

5. Autoregressions and Tauchen’s Algorithm

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Indirect Utility

Recall from consumer theory the concept of indirect utility:

V (p, I ) = maxc≥0

u (c) , s.t. pc ≤ I .

Reflects the highest utility level, a household can achieve by consumptionchoice, given his income I and the price vector p.

I We can think of (p, I ) as indexing the state of the economy.I Therefore we will call (p, I ) the state vector.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Profit functions

I Analogously, we have the concept of a (short-run) profit function inproduction theory:

Π (p,w ,K ) = maxLpF (K , L)− wL− rK .

I Again, we can think of (p,w ,K ) as indexing the state of theeconomy for the firm.

I While the concept of indirect utility / reduced form profit functionsmainly helps in simplifying some analysis in static consumer theory(Slutsky-decomposition for example), it will turn out to be a verypowerful tool in a dynamic analysis.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

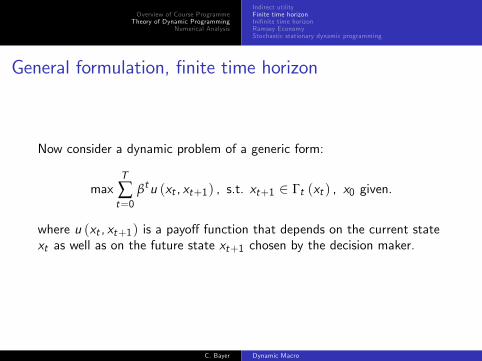

General formulation, finite time horizon

Now consider a dynamic problem of a generic form:

maxT

∑t=0

βtu (xt , xt+1) , s.t. xt+1 ∈ Γt (xt ) , x0 given.

where u (xt , xt+1) is a payoff function that depends on the current statext as well as on the future state xt+1 chosen by the decision maker.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

General formulation, finite time horizon

Denoting the indirect utility obtained as V (xt , t) , we can restate theProblem as a so called Bellman equation

V (xt , t) = u (xt , xt+1) + βV (xt+1, t + 1) , s.t. xt+1 ∈ Γt (xt ) .

where V exists if Γ is compact valued (Theorem of the Maximum).The time-index t reflects the fact that it matters how many remainingperiods there are.With finite horizon the optimization problem is necessarilynon-stationary, i.e. changes with time t.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

A cake eating example

To fix ideas consider the usage of a depletable resource (cake-eating)

maxT

∑t=0

βtu (ct ) , s.t. Wt+1 = Wt − ct , ct ≥ 0, W0 given.

To put this in the general form, expressing the problem only in terms ofstate variables Wt we replace ct = Wt −Wt+1

maxT

∑t=0

βtu (Wt −Wt+1) , s.t. Wt+1 ≤ Wt .

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

A cake eating example

As formulation in terms of the Bellman equation, we obtain

V (Wt , t) = max u (Wt −Wt+1) + βV (Wt+1, t + 1) , s.t. Wt+1 ≤ Wt .

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Bellman equations and infinite time horizon

While the dynamic programming (Bellman equation) approach generatessomewhat more information about the optimization problem in a finitehorizon setup than a direct attack on the problem, it is at the same timemore burdensome, since we need to determine V for each t.It becomes a powerful approach really only when we look at infinite timehorizon problems.These can be stationary, i.e. does not change in t, as the remainingtime until the end of the decision problem remains always ∞.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Stationary dynamic programming

If the problem is stationary (and a solution does exist), we can state theplanning problem as

V (x) = max u (x , y) + βV (y) s.t. y ∈ Γ (x) .

I Note however that not all infinite horizon problems are stationary.Sometimes a problem can be reformulated in stationary terms (Youknow that from econometrics).

I Also note that a solution may not exist.I The unknown of the Bellman equation is the function V (x)

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

An ExampleThe neo-classical growth model

A social planner wants to maximize the stream of utility fromconsumption in an economy, where

U = U (Ct )

Yt = Ct + It ; Yt = K αt

Kt+1 = (1− δ)Kt + It

V (K0) = max<Kt>t=1...∞

∞

∑t=0

βtU [C (Kt ,Kt+1)]

s.t. C = K αt + (1− δ)Kt −Kt+1

Kt+1 ≥ 0

Kt+1 ≤ K αt + (1− δ)Kt

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

An ExampleThe neo-classical growth model

We can rewrite this as

V (K ) = max<Kt>t=1...∞

∞

∑t=0

βtU [C (Kt ,Kt+1)] with Kt = K

= maxKt+1

{u (K ,Kt+1) + max

<Kt+1>t=1...∞β

∞

∑t=0

βtu [C (Kt+1,Kt+2)]

}= max

K ′∈Γ(K )

{u(K ,K ′

)+ βV

(K ′)}

Γ (K ) : = {k ∈ R+| k ≤ K α + (1− δ)K}u (K ,Kt+1) : = U [C (Kt ,Kt+1)]

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

When does a solution exist?

We can formulate the Bellman equation as a mapping

U (x) = T (V (x))

T [V (x)] = maxyu (x , y) + βV (y) s.t. y ∈ Γ (x) (1)

that maps function V to a new function U.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Some prerequisits

DefinitionA sequence (xn) is said to be a Cauchy sequence on the metric space(C , d) if for all ε > 0 there exists a n (ε) , such that for allm, n ≥ n (ε) : d (xm , xn) < ε.

LemmaIn a complete metric space, all Cauchy sequences converge, i.e. for anyCauchy sequence (xn) , there is an x ∈ C , such that d (xn , x)→ 0 asn→ ∞. (without proof)

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Some prerequisits

DefinitionThe mapping T is a contraction on the complete metric space {C , d} iffor any x , y ∈ C ⇒ Tx ,Ty ∈ C and for some ρ < 1 :d (Tx ,Ty) ≤ ρd (x , y) .

LemmaIf T is a contraction then T nx is a Cauchy sequence (to be proof asExcercise 1).

RemarkNote that the set of continuous bounded functions is a complete metricspace, with the sup-norm as metric.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Exercise 1

Show that if T is a contraction then T nx is a Cauchy sequence !

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Existence of a Solution to the Bellman equationThe contraction mapping theorem

TheoremIf the Bellman equation (1) defines T to be a contraction mapping onthe set of continuous bounded functions, then a solution to (1) exists.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Existence

Proof.1.) note that if (1) has a solution, then it is a fixed point of T and viceversa.2.) if the contraction mapping T has a fixed point, then it is unique: Let

Tx = x ,Ty = y ⇒d (x , y) = d (Tx ,Ty) ≤ ρd (x , y)

⇒ d (x , y) = 0

⇒ x = y

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Existence

Proof.3.) T is continuous, i.e. yn → y ⇒ Tyn → Ty as

d (Tyn ,Ty) ≤ ρd (yn , y)n→∞→ 0

⇒ Tyn → Ty

4.) the limit limn→∞ T nx =: x∗ exists because T nx is Cauchy (seeExercise 1).

5.) this implies

Tx∗ = T(limn→∞

T nx)

= limn→∞

TT nx = limn→∞

T n+1x = x∗,

so that x∗ is the fixed point of T , which concludes the proof.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

An algorithm to solve the Bellman equation

The proof to show existence of a solution to the Bellman equation isconstructive. It tells us how to find a solution to the Bellman equation:

1. Show that T is a contraction.

2. Start with some initial guess V0 and then construct a sequenceVn = TVn−1.

3. After a suffi ciently large number of iterations Vn will becomearbitrarily close to the solution V .

4. This algorithm is called "Value-Function-Iteration" (VFI).

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Blackwell’s condition

TheoremIf T fulfills the following conditions, then T is a contraction mapping onthe set of bounded and continuous functions:

1. T preserves boundedness.

2. T preserves continuity.

3. T is monotonic: w ≥ v ⇒ Tw ≥ Tv4. T satisfies discounting, i.e. there is some 0 ≤ β < 1, such that forany real valued constant c and any function v we haveT (v + c) ≤ Tv + βc .

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

A solution exists in the generic case

Theorem (Existence of the value function)Assume u (x , x ′) is real-valued, continuous, and bounded, 0 < β < 1,and that the constraint set Γ (s) is a non-empty, compact-valued, andcontinuous correspondence. Then there exists a unique continuous valuefunction V (s) that solves the Bellman equation (1) .

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Policy function

Theorem (Existence of the policy function)Assume u (x , x ′) is real-valued, continuous, strictly concave andbounded, 0 < β < 1, and that the set of potential states is a convexsubset of Rk and the constraint set Γ (s) is a non-empty,compact-valued, continuous, and convex correspondence. Then theunique value function V (s) is continuous and strictly concave. Moreoverthe optimal policy

φ (x) := arg maxy∈Γ(x )

u (x , y) + βV (x)

is a continuous (single-valued) function.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

A simple optimal capital accumulation model

I To put things into practice, we consider the Ramsey-Cass-Koopmansgrowth model in a simplified version:

I Consider a household having a utility function

u (ct , nt ) = ln (ct )

I The consumption good is produced from a depreciating capital good:

yt = zkαt , 0 < α < 1,

kt+1 = kt (1− δ) + it , 0 ≤ δ ≤ 1,yt = ct + it .

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

A simple optimal capital accumulation model

1. How can we put this into the terms of dynamic programming?

2. Consumption is the policy variable.3. Capital is the state variable.4.

V (kt ) = maxct≤yt−ityt=Ak α

tkt+1=kt (1−δ)+it

ln (ct ) + βV (kt+1) .

5. This problem fulfills all assumptions of our 2 central theorems.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Well this looks like a simple model, ....

I but ...I You’ll need a computer to solve it.I Unless you fix δ to 1,I which is what we will do for didactical reasons:

1. We learn to understand the problem2. We can compare approximate numerical solutions to the "true"analytical solution

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

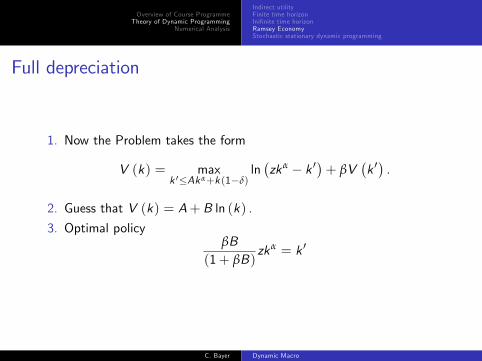

Full depreciation

I Now the Problem takes the form

V (k) = maxk ′≤Ak α+k (1−δ)

ln(zkα − k ′

)+ βV

(k ′).

I Guess that V (k) = A+ B ln (k) .I This yields the FOC for the optimal policy

− 1zkα − k ′ + βV ′

(k ′)= 0

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Full depreciation

I Now the Problem takes the form

V (k) = maxk ′≤Ak α+k (1−δ)

ln(zkα − k ′

)+ βV

(k ′).

I Guess that V (k) = A+ B ln (k) .I Plugging in the guess for V :(

zkα − k ′)−1

= βBk ′−1

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Full depreciation

I Now the Problem takes the form

V (k) = maxk ′≤Ak α+k (1−δ)

ln(zkα − k ′

)+ βV

(k ′).

I Guess that V (k) = A+ B ln (k) .I Plugging in the guess for V :

βB(zkα − k ′

)= k ′

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Full depreciation

1. Now the Problem takes the form

V (k) = maxk ′≤Ak α+k (1−δ)

ln(zkα − k ′

)+ βV

(k ′).

2. Guess that V (k) = A+ B ln (k) .

3. Optimal policyβB

(1+ βB)zkα = k ′

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Full depreciation

1. Now the Problem takes the form

V (k) = maxk ′≤Ak α+k (1−δ)

ln(zkα − k ′

)+ βV

(k ′).

2. Guess that V (k) = A+ B ln (k) .

3. Optimal policyβB

(1+ βB)y = k ′

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Full depreciation

Plug in optimal policy and V (k) = A+ B ln (k)

A+ B ln (k) = ln(zka

(1− βB

1+ βB

))+β

(A+ B ln

(βB

(1+ βB)zkα

))which can be restated as

A (1− β) + ln (k) [B − α (1+ βB)] =

ln (z) (1+ βB)− ln (1+ βB) (1+ βB) + βB ln (βB)

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Full depreciationTherefore

B = α (1+ βB)

B =α

1− αβ

This means1+ βB =

11− αβ

So that

A (1− β) =

(1

1− αβ

)[ln (z) + ln (1− αβ)] +

αβ

1− αβln(

αβ

1− αβ

)= ln (1− αβ) +

ln (z) + αβ ln (αβ)

1− αβ

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Interpretation

1. Indeed our guess solves the Bellman equation! (It is a fixed point ofT )

2. The household saves the fraction βB(1+βB ) = αβ of current income

y = zkα.

3. The analytical solution breaks down as soon as δ < 1.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Extending our model to stochastic environments

I So far we considered only situations in which all state variables wereperfectly controlled by the decision maker.

I However, this is unrealistic in most economic situations.

1. The situation may depend on some variable governed by a stochasticlaw of motion.

2. The situation may involve interdependent choices (i.e. a game)

I We’ll only look into the first case. The second case is morespecialized, but it is basically covered by applying the concept ofMarkov-perfect equilibria.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Extending our model to stochastic environments

I Thinking of stationary influences in terms of an additionally statevariable allows to integrate stochastic elements into the DP setup.

I We define the stochastic version of the Bellman equation as

V (x , ξ) = maxy∈Γ(x ,ξ)

u (x , y , ξ) + βEs ′V(y , ξ ′

).

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

Extending our model to stochastic environments

I What is needed is that the process governing s is an ergodic Markovprocess, i.e.

1. for a suffi ciently rich description of the history of the processcaptured by vector s , the transition probability is time and historyindependent

2. the process is stationary.

I Again, sometimes we may achieve stationarity by reformulating theproblem (e.g. consider a "cointegrated." system in which thedecision maker wishes to track ξ by adjusting the state x).

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Indirect utilityFinite time horizonInifinite time horizonRamsey EconomyStochastic stationary dynamic programming

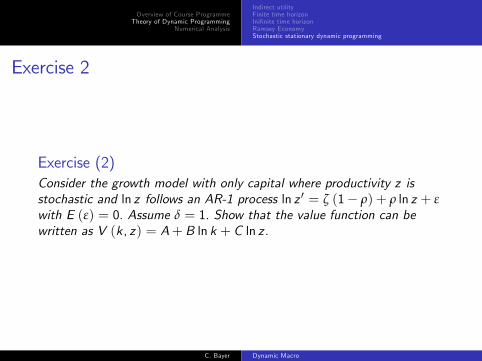

Exercise 2

Exercise (2)Consider the growth model with only capital where productivity z isstochastic and ln z follows an AR-1 process ln z ′ = ζ (1− ρ) + ρ ln z + εwith E (ε) = 0. Assume δ = 1. Show that the value function can bewritten as V (k, z) = A+ B ln k + C ln z .

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Getting started

The first algorithm we want to study is the Value Function Iterationoutlined before. It focuses on the Bellman equation, computing the valuefunctions by foward iterations from an initial guess. Independent of thesolution of choice, numerical analysis can be thought of as having 4 steps:

1. Choice of functional forms

2. Approximation

2.1 For methods involving discretization: Discretization of state andcontrol variables

2.2 For methods involving approximation of the policy function: Choiceof parametric family

3. Building the computer code

4. Evaluating numerical results: policy and value functions, simulation,estimation.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Functional Forms

To be able to solve a dynamic programming problem numerically, we needto specify all functions involved in the problem and assign values totheir parameters. Some functional forms are more common than others:

I Consumption: CRRA functions (log utility if γ = 1):u (c) = c1−γ−1

1−γ .

I Production: CES production functions (Cobb-Douglas functions if

ρ = 0) : f (~x) =(

∑i αi xρi

)1/ρ

I Aggregators: CES-functions: C (~c) =(

∑i αi cρi

)1/ρ

I Cost functions: linear, quadratic, fixed:C (x) = F + αx + β

2 (x − x)2

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Parameter choiceAfter choosing the functional forms involved in the dynamic programmingproblem we need to fix all parameters. There are various ways to do so:

I Take parameters published in other empirical studiesI Pros: quickest, most orthodox, most likely to be acceptedI cons: the estimations did not consider the effects you highlight inyour study and may be biased

I Perform calibrationI Pros: Relatively quick, actual data involved in the parameter choice(data guided)

I Cons: No standard errors for parameters (how reliable are theestimates)

I EstimationI Pros: Reliability of parameters is assessed, parameter consistentunder the model

I Cons: Can be very time consuming up to infeasible

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Discretization of the state space

I We need to define the space spanned by the state and controlvariables as well as the space of shocks in case of a stochasticproblem.

I In the simplest case, the problem will already be of discrete form(e.g. work - no work).

I In most economic situations, however, the spaces involved in thetheoretical problem will be defined on a continuous space. Forexample:

I Consumption choiceI InvestmentI AR(p) processes for shocks

I In all these cases we need a discrete approximation to the statespace.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Discretization of the state spaceI The discretization typically involves three choices

1. Bounds to the state space, e.g. take S = ×i[S i , S i

]for subsets

from Rk .2. Number of points in each dimension of the state space.3. Position of the points on the intervals.

I Each decision is non trivial and if possible should be made theoryguided:

I What is the relevant domain?I Reflecting boundaries: Are there states sL, sH such that

φ (s) < s∀s ≥ sHφ (s) > s∀s ≤ sL?

I In a deterministic model: reasonable sizeI In a stochastic model: suffi ciently large probability mass, goodapproximation of all relevant moments. (Models with emphasis onhigher order terms will need to be more accurate than modelsemphasizing only first moment.)

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Discretization of the state space: Problems

I Not necessarily do reflecting boundaries exist:I Cake eating example from the introduction:I It can be shown that the household optimally consumes a fraction(1− β) of the remaining cake each period

I φ (W ) = βWI Wn = βWn−1 = βnW0I This converges to zero, which is a point outside the feasible set ofcake-sizes if u (c) = ln (c) .

I Increasing the number of grid-points does not solve the problem: Nthe numerical solution V (N ) 9 V as N → ∞.

I Only approximations, redefining u, as e.g. in Exercise 3.

I Smaller problem: we often do not know the reflecting boundarieseven if they exist

I Then do a trial-and-error search

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Discretization of the state space: Exercise

Exercise (3)Solve the cake-eating problem analytically for u (c) = ln (c)! Then writea programme that solves a numerical approximation to this problem. Forthis approximation redefine

u (c) ={ln (c) c > Cln (C ) c ≤ C .

Compare the analytical and the numerical solution both graphically aswell as in terms of the max-norm for C = exp (−6.5)! What is theoptimal grid you should use? How does the approximation quality on[0.1, 2] change by altering C and by altering N.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Putting things to work: non-stochastic case

I Value function Iteration loops over

V n = T(V n−1

)= maxs ′∈Γ(s)

u(s, s ′

)+ βV n−1

(s ′)

until |V n − V n−1 | < critI To implement this, we specify N discrete points in the state spaces1, s2, ..., sN and denote V ni = V

n (si ) .I Note: In the stochastic case, V ni includes the expectations operator.I Let U (i) = (u(i , 1), u (i , 2) , ..., u (i ,N)) be the vector of allpossible instantaneous utility levels obtained by going from state i toj (if impossible, set to −∞).

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Putting things to work

I Optimizing starting from state i

V ni = max{U (i) + βVn−1

}I Denote ι′N = (1, ..., 1) , and stacking the above expression, we obtain

Vn = max{U+ βιNV

n−1}

where bold typeset indicates linewise stacked variables. Maximum isline-by-line.

I Note: MATLAB max does column-wise max, so you’ll need to usemax(x, 2)

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Putting things to work

I Switch to MATLAB! (Simple growth problem)

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Some remarks on effi cient programme codesI At least if you want to do estimation, you’ll be quickly running intoproblems with computation time.

I Therefore effi cient programming is essential.I In the programme codes presented there is some ineffi ciency.

I Utility levels that correspond to state-to-state transitions, forexample, are calculated each time the value functions is iterativelyredetermined.

I It would be better to calculate them at higher hierarchy and passthem on to Val_Fu_I.m.

I Use the MATLAB Profiler to find time expensive steps of thecalculation. Use M-Lint for hints on effi cient programming, e.g.pre-allocating growing variables in loops.

I Avoid loops by making use of Matrix-Algebra.I MATLAB can handle up to 3-dimensional arrays quickly, above thatdimensionality performance is worse than loops.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Exercise 4

Throughout this class we will build two computer-based models: (a) aneconomy with capital accumulation, including frictions to this; (b) amodel of optimal savings in an economy with incomplete markets and(endogenous) borrowing constraints.

Exercise (4)Write a MATLAB code that solves the simplifiedRamsey-Cass-Koopmans model for δ < 1 for fixed productivity z .

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Exercise 5Exercise (5)Consider the following model: A household is endowed with a fixedincome stream of yt = ρty0, ρ < (1+ r)−1 discounts future utility byfactor β and its felicity function (instantaneous utility) is a CRRAfunction

u (c) =c1−γ − 11− γ

.

The household can save and borrow at the risk-free rate r .

1. Derive optimal consumption for β (1+ r) = 1 for given currentlevels of non-human wealth D.

2. Write a MATLAB code that solves for optimal consumption givenV (D) for ρ = 1.

3. Solve for V by value function iteration, compare graphically to theanalytic solution for the policy function.

C. Bayer Dynamic Macro

Overview of Course ProgrammeTheory of Dynamic Programming

Numerical Analysis

Getting StartedFunctional Forms and ParameterizationDiscretization of the state spaceValue Function Iteration

Literature

Primary Reading:

I Heer, B. and A. Maussner (2009), "Dynamic General EquilibriumModelling", 2nd edition, Springer, Berlin. (Ch. 1)

Secondary reading:

I Adda, J. and R. Cooper (2004): "Dynamic Economics", MIT Press,Cambridge.

I Ljungqvist, L. und T. Sargent (2004): "Recursive MacroeconomicTheory", MIT press, Cambridge.

I Stockey, N.L. and Lucas, R.E. with E.C. Prescott (1989): "RecursiveMethods in Economic Dynamics", Chapters 4 and 9, Havard UniversityPress, Cambridge..

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Part 2Stochastic Fluctuations, Simulations and Further Numerical Tools

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

LiteratureProgramme of the week

Programme of the week

1. Discussing the Exercises

2. Modelling Stochastic Fluctuations

2.1 Markov Chains2.2 Tauchen’s Algorithm2.3 Simulating a Markov Chain

3. Further numerical tools to solve SDP

3.1 Policy Function Iteration3.2 Interpolation3.3 Multigrid Algorithms3.4 Projection methods

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Stochastic Fluctuations and Markov Chains

I We model stochastic fluctuations on a grid of discrete stochasticstates.

I If the stochastic fluctuations follow a stationary process, then theycan be modelled in terms of a Markov chain.

I A Markov chain is characterized by states si , i = 1...N and atransition probability matrix P =

(pij)that gives the probability to

move from state i to state j .

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Stochastic Fluctuations and Markov Chains

I If we denote the stochastic states by si and the states directlydetermined by policy choice by xj , then it is useful to define thevalue function as a matrix

V =(vij)i=1...Nj=1...M

=(V(si , xj

))i=1...Nj=1...M

.

I Then we can calculate the expected value as

Es(V(s′, x ′

))= PV =

(∑kpik vkj

)i=1...Nj=1...M

.

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Markov ChainsI For details see Sargent/Ljungqvist, Ch. 2, I will be brief andintroduce mainly some notation / definitions.

I For a given probability distribution π0, the recursion

πt = Pπt−1

determines the sequence of probability distributions for the MarkovChain.

I The limit t → ∞ of πt is called the "time invariant", "stationary"or " ergodic" distribution of the Markov Chain.

I Since

π∗ = limt→∞

Ptπ0

Pπ∗ = P limt→∞

Ptπ0 = limt→∞

Ptπ0 = π∗.

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Markov Chains

I This limit distribution hence solves

(I − P)π∗ = 0

and corresponds to the unit-eigenvector of P (if the limit exists).I The limit does exist if for some k ≥ 1 all elements ofPk = P × P × · · · × P︸ ︷︷ ︸

k times

are strictly positive (i.e. it is possible to

reach each state from each state after k steps).I We can calculate it as limt→∞ Ptei , ei is the i-th unit-vector

ei :=(0 . . . 1

i−th position. . . 0

).

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Markov Chains, Two examples

ExampleThe Markov chain characterised by

P =

1/2 1/2 01/2 0 1/20 1/2 1/2

has an ergodic distribution, since

P2 =

12

14

14

14

12

14

14

14

12

is positive everywhere.

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Markov Chains, Two examples

ExampleThe Markov chain characterised by

P =

1/2 1/2 0 01/2 1/2 0 00 0 1/2 1/20 0 1/2 1/2

has no ergodic distribution, since the upper and the lower block of statesdo not "connect".

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Markov Chain Approximation of AR(1) Processes

I Economic theory often assumes that the stochastic variable follows astationary AR(p) process with normal innovations εt , particularlyp = 1 is most common.

I Tauchen (1987) suggests an algorithm to approximate such aprocess by a Markov chain.

I Consider the following process

yt = µ (1− ρ) + ρyt−1 + εt , εt ∼ N(0, σ2

(1− ρ2

))I The ergodic distribution of this process is N

(µ, σ2

).

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Markov Chain Approximation of AR(1) ProcessesAn example

Consider the 3-state Markov Chain

z1 = −√1.5σ, z2 = 0, z3 =

√1.5σ

with transition probabilities

P =

1− p p 0p/2 1− p p/20 p 1− p

The ergodic distribution π solves

(I − P)π = 0

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Markov Chain Approximation of AR(1) ProcessesAn example

Hence p −p 0−p/2 p −p/20 −p p

π1π2π3

= 0

so that πi = 1/3.This yields

I E (z) = 0

I and E(z2)= 1

3

(32σ2 + 0+ 3

2σ2)= σ2

I and finally

E (zt+1zt ) = 13

((1− p) 32σ2 + 0+ (1− p) 32σ2

)= (1− p) σ2.

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Exercise 6

Exercise (6)Calculate conditional variances E

(z2t+1 |zt = zi

)− E (zt+1 |zt = zi )2,

and unconditional skewness and kurtosis for the above three state MarkovChain. How do these compare to a normally distributed AR-1 process.

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Markov Chain Approximation of AR(1) Processes

I We want to discretize the process over N gridpoints, reflecting Nbins.

I Two sensible ways to choose gridpoints:

1. Take a α % mass interval of the ergodic distribution (e.g. µ± 2σ)and use equidistant points

2. Choose the N bins such that each has a probability measure of 1N inthe ergodic distribution

I The first option is much easier to calculate. The latter should yield abetter approximation - though it not always does.

I For very large N the numerical advantage of the first option makesthis the option of choice.

I However, if a high degree of accuracy is necessary Tauchen’s methodis preferable and a large number of points is necessary for higherorder behavior.

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

First option: equidistant

3 2 1 0 1 2 30

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

x

φ (x

)

Normpdfgrid centersbin bounds

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Second option: equi-likely / importance sampling

3 2 1 0 1 2 30

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

x

φ (x

)

Normpdfgrid centersbin bounds

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Tauchen’s Algorithm

The Algorithm goes in three steps

1. Generate N bins to discretize the state space

Y = [y1, y2)︸ ︷︷ ︸Y1

∪ [y2, y3)︸ ︷︷ ︸∪Y2

...∪ [yN , yN+1 ]︸ ︷︷ ︸YN

2. Calculate the conditional expectation for each bin. This is to beused as the representative element of the bin in the solution of thenumerical model (grid of Y ).

3. Calculate transition probabilities pi ,j = P(yt+1 ∈ Yj |yt ∈ Yi

)

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Generate BinsTo obtain a grid that is a good approximation at points that are reachedoften, we choose the boundaries of bins Yi such that

P (y ∈ Yi ) = Φ(yi+1 − µ

σ

)−Φ

(yi − µ

σ

)=1N,

where Φ is the CDF of a standard normal. That is we make all binsequally likely to occur in the long run, i.e. in the ergodic distributionof y .Therefore, we choose boundaries, such that

Φ(yi+1 − µ

σ

)=iN

or

yi = σΦ−1(i − 1N

)+ µ.

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Representative elementI The next step is to calculate the “centers”of the bins as

zi = E (y |y ∈ Yi ) .

I Plugging in the distribution function φ (x) = 1√2πexp

(− x 22

)of a

standard normally distributed variable, we obtain

zi =

∫ yi+1−µσ

yi−µσ

(σx + µ) φ (x) dx

P (y ∈ Yi )

I Observe that∫xφ (x) dx = −φ (x) + F and P (y ∈ Yi ) = N−1

I Then, we obtain

zi = Nσ

[φ

(yi − µ

σ

)− φ

(yi+1 − µ

σ

)]+ µ

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Calculating Transitions

I The last - and in any terms most complicated - step is to calculatetransitions.

I For each x ∈ Yi there are many “targets” in Yj that can be reached

Yi Yj

xI And then there are many x ∈ Yi to start from.

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Calculating Transitions

I Fix one x ∈ Yi . What is the probability to reach an y ∈ Yj ?I We need

yj ≤ ρx + µ (1− ρ) + ε

andyj+1 ≥ ρx + µ (1− ρ) + ε

I To put it differently

ε ∈[yj − ρx − µ (1− ρ) , yj+1 − ρx − µ (1− ρ)

]

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Calculating TransitionsI With ε being normally

(0, σ2

(1− ρ2

))distributed, we obtain with

σ2ε = σ2(1− ρ2

)P(yt+1 ∈ Yj ∩ yt = x

)=

Φ(yj+1 − ρx − µ (1− ρ)

σε

)−Φ

(yj − ρx − µ (1− ρ)

σε

)I Integrating over all x (weighted by their density), we obtain

P(yt+1 ∈ Yj ∩ yt ∈ Yi

)=

1√2πσ

∫ yi+1yi

exp

{− (x − µ)2

σ2

}×

Φ(yj+1 − ρx − µ (1− ρ)

σε

)−Φ

(yj − ρx − µ (1− ρ)

σε

)dx

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Calculating Transitions

I Finally, making use of P (yt ∈ Yi ) = 1N , we obtain

pi ,j = P(yt+1 ∈ Yj |yt ∈ Yi

)=

N√2πσ

∫ yi+1yi

exp

{− (x − µ)2

σ2

}×

Φ(yj+1 − ρx − µ (1− ρ)

σε

)−Φ

(yj − ρx − µ (1− ρ)

σε

)dx

I The latter integral has to be determined numerically.I This is computationally burdensome!

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Calculating Transitions

I Therefore an approximation to the Tauchen approximation is

pi ,j = P(yt+1 ∈ Yj |yt = zi

)=

Φ(yj+1 − ρzi − µ (1− ρ)

σε

)−Φ

(yj − ρzi − µ (1− ρ)

σε

)I This can also be used for equi-spaced grids!

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Exercises 7

Exercise (7)Program both the simplified and the full Tauchen (1987) algorithm!

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Exercises 8Exercise (8)Simulate both alternative Tauchen approximations as well as equispacedgrid approximations (with ±2σ grid) to the process

yt = 0.9yt−1 + εt

for N = 5, N = 25, N = 100 points of the grid and 1000 time periods.Estimate with OLS

yt = µ+ ρ11yt−1 + ρ12yt−2 + β1y3t−1 + εt .

y2t = µ+ ρ21yt−1 + ρ22yt−2 + β2y3t−1 + εt .

y3t = µ+ ρ31yt−1 + ρ32yt−2 + β3y3t−1 + εt .

Repeat the simulation and estimation 100 times for randomized y0.Compare the estimation results also to a continuous simulation of theprocess.

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

How to simulate a Markov chain

1. If we want to simulate a Markov chain with transition matrix P, weneed to start with some initial state s0 = i .

2. We calculate Π =(πi ,j

)=(

∑jk=1 pi ,k).

3. We start with t = 0.

4. Then we draw a uniformly (0, 1) distributed variable ut .

5. and find j such that πst ,j−1 < ut ≤ πst ,j . This is state st+1 = j .

6. We repeat steps 4 and 5 until t = T .

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

Alternative Simulation Procedure

1. In case the Markov chain approximates a continuous data generatingprocess, e.g. an AR-1,

2. then we can alternatively simulate the DGP itself and later replacethe realisations by the mean of the bin in which they fall.

3. This means, that we generate first a series xt , t = 1...T from thetrue DGP.

4. Then we find j , such that yj < xt ≤ yj+1.5. And obtain the series of simulated values as xt = zj .

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

A stochastic growth model

I We extend the capital accumulation model to a situation, in whichln z follows a stationary AR-1 process, with autocorrelation ρ = 0.8and variance σ = 0.5. (See MATLAB code)

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

Markov ChainsTauchen’s AlgorithmExerciseHow to simulate a Markov ChainApplication

The consumption-savings modelExercise 9 and 10

Exercise (9)Extend the consumption model to a situation, in which income y iscomposed of a log-normal stochastic part x , which follows a stationaryAR-1 process, with autocorrelation ρ and a fixed part τ. Note that youneed to set (1+ r) < β because asset holdings drift to infinity otherwise,Moreover, assume households can only borrow up to τ/r (the amountthey can credibly promise to repay). Assume log-utility in this and thefollowing exercises.

Exercise (10)A Bewley Model of Money. Assume that τ = r = 0, i.e. householdscannot borrow and the asset they save in bears no interest (money).Simulate an agent over T=1000 periods of time and calculate theaverage asset holding of the agent. Do so for various levels of long-rununcertainty and persistence. Plot the results!

C. Bayer Dynamic Macro

Overview of Course ProgrammeModelling stochastic fluctuations

Literature

LiteraturePrimary Reading:

I Heer, B. and A. Maussner (2009), "Dynamic General EquilibriumModelling", 2nd edition, Springer, Berlin. (Ch. 12)

Secondary reading:

I Adda, J. and R. Cooper (2004): "Dynamic Economics", MIT Press,Cambridge.

I Ljungqvist, L. und T. Sargent (2004): "Recursive MacroeconomicTheory", MIT press, Cambridge.

I Stockey, N.L. and Lucas, R.E. with E.C. Prescott (1989): "RecursiveMethods in Economic Dynamics", Chapters 4 and 9, Havard UniversityPress, Cambridge..

I Tauchen, G. (1986): "Finite state Markov-chain approximation tounivariate and vector autoregressions", Economic Letters, 20, 177-81.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Part 3Further Numerical Tools

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

LiteratureProgramme of this Part

Programme of this Part

1. Discussing the Exercises

2. Further numerical tools to solve SDP

2.1 Policy Function Iteration2.2 Interpolation2.3 Multigrid Algorithms2.4 Projection methods

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function Iteration

I While the Value Function Iteration is an intuitive solution algorithmthat directly stems from the proof of existence of a solution to theBellman equation, it is at the same time relatively slow.

I In the worst case, each iteration step reduces the distance betweenthe true solution and the current guess of the value function only byfactor β.

I In other words the discount factor β equals rate of convergence ofthe algorithm.

I For this reason we will discuss algorithms to speed up the solution ofthe Bellman equation in the following.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function IterationI The first algorithm that we want to go through is Policy FunctionIteration, aka Howard’s Improvement Algorithm.

I While Value Function Iteration assumes that the policy functionis applied once, Policy Function Iteration assumes that the policyfunction is applied forever:

I For Value Function Iteration, we have

hn (s) = argmax u(s, s ′

)+ βEVn

(s ′)

Vn+1 (s) = u (s, hn (s)) + βEVn (hn (s))

I For Policy Function Iteration, we define

hn (s) = argmax u(s, s ′

)+ βEVn

(s ′)

Vn+1 (s) =∞

∑t=0

βtu (st , hn (st ))

st = hn (st−1)

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function Iteration

I It is handy to put this into matrix notation.I First stack the states into a vector, such that {s1, . . . , sN } are allpossible states the value function is defined on.

I Note that not necessarily all states can be reached with certainty bythe agent’s choice.

I For example, let the state space be productivity a ∈ {a1, . . . , aM }(chosen by nature) and capital k ∈ {k1, . . . , kH } (chosen by theagent), then N = HM and

s1 = (a1, k1) , s2 = (a2, k1) , . . . , sM+1 = (a1, k2) , . . . , sN = (aM , kH ) .

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function Iteration

I Let v = (vi )i=1...N = [v (si )]i=1...Nbe the value function writen asa vector that contains the value for any state si .

I Let u =(ui ,j)i=1...Nj=1...M

=[u(si , s ′j

)]i=1...Nj=1...M

denote the

contemporaneous utility obtained by the transition from state si tosj (let it be chosen or stochastic).

I Let H =(hi ,j)i=1...Nj=1...N

denote the stochastic policy function. That is

as a transition matrix, which displays the probability that h (si ) = sj .I Let T denote the operator defined by the Bellman equation.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function Iteration

I V satisfies V = TV .I Using the notation from before, we know that

v = H (u+ βv)

where Hu is the vector of instantaneous utility obtained under H inall possible states

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function IterationI Putting these consideration into an algorithm, we obtain

vn = Hn (u+ βvn)

I and we can solve for vn given Hn by inverting the relationship

vn = (I − βHn)−1 Hnu

I The next step is to find the policy function Hn+1 that defines theoptimal policy given vn .

I This means, we search for Hn+1, such that

Hn+1 (u+ βvn) = Tvn .Hn+1u+ (βHn+1 − I ) vn = (T − I ) vn

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function Iteration: Interpretation

I We can understand policy function iteration as a version ofNewton’s algorithm to find a zero of (T − I ) .

I Replacing Hn+1u by (IMN − βHn+1) vn+1, we obtain

(I − βHn+1) vn+1 − (I − βHn+1) vn = (T − I ) vn

I This can be expressed as

vn+1 = vn + (I − βHn+1)−1 (T − I ) vn

I and (βHn+1 − I )−1 can be regarded as the gradient of (T − I ) .I (Newton’s algorithm: solve G (z) = 0, zn+1 = zn − G ′ (zn)G (zn))

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function Iteration: caveats

I Policy Function Iteration becomes time consuming for larger gridsizes as L = (I − βHn+1) has to be inverted.

I There are some algorithms to speed this up.I Inversion of a matrix can be parallelized.I Alternatively: Apply βHn just a number of times, making use of

(I − βHn+1)−1 = lim

S→∞

S

∑s=0

βsHsn+1

and approximating this for a small S .

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function Iteration: Comparison of running times

50 100 150 200 250 300 350 400 450 5000

5

10

15

20

25

30

35

number of grid points

runn

ing

time

[sec

]VFIPFI

Both algorithms exhibit polynomial behavior in the number of points!C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function Iteration: Relative running times

50 100 150 200 250 300 350 400 450 5002

3

4

5

6

7

8

number of grid points

rela

tive

runn

ing

time

VFI

/PFI

The larger the number of gridpoints, the smaller the advantage of thePFI!

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Policy Function Iteration: Exercise

Exercise (11 in class)Write a MATLAB code that solves the stochastic growth problem usingPFI! Compare running times to VFI for a N ×N grid forN = 10, 50, 150, 250 points.

Exercise (12)Write a MATLAB code that solves the stochastic consumption-savingsproblem using PFI! Compare running times to VFI for a N ×N grid forN = 10, 50, 150, 250 points.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Interpolation

I Since the computation costs increase exponentially in the number ofpoints it may be a good alternative to interpolate points betweengrid points.

I Let xi , i = 1...N be points at which we know fi = f (xi ) . We wantto approximate the function f for off-grid points.

I We’ll go through 3 methods: least-squares approximation,linear-interpolation, spline interpolation.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Least squares interpolationI One method to approximate a function is to estimate thecoeffi cients ψ of a polynomial expression

f (x) =n

∑j=1

ψj cj (x)

where ci (x) are known baseline functions such as cj (x) = x j .I Better than ordinary polynomials are usually Chebyshev polynomialsof which the baseline functions are

cj (x) = cos (j arccos x)

I These are orthogonal in function space, and the regressor matricesI In practice these methods do not perform very well:Fluctuation, overshooting, ....

I The approximation does not necessarily equal the function atxi

I Advantage: little Information needs to be stored!C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Linear Interpolation

I A computationally easy alternative is to fit a piecewise linearfunction.

I For each point x at which we want to evaluate our approximation wefind the next smaller point about which we have informationxi < x ≤ xi+1.

I Then we calculate

f (x) = fi +fi+1 − fixi+1 − xi

(x − xi ) .

I The formula is easily extended to higher order cases.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Linear Interpolation

I It is implemented in MATLAB as default for interp1, interp2,interp3, interpn.

I Fhat=interp1(xi,fi,x)I Fhat=interp2(xij,yij,fij,x,y), x,y equal dimensional matricesdefining the values of x and y in f (x , y)

I MATLAB can also extrapolate using linear interpolation(Fhat=interp1(xi,fi,x,linear,extrapval))

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Spline Interpolation

I While the linear interpolation methos leads to an interpolatedfunction f that is continuous, this function typically is non smooth.

I This non-differentiability may translate into non-differentiable policyfunctions.

I Spline interpolation evades this issue. It approximates the functionlocally by a cubic polynomial

fi (x) = fi−1 + ai (x − xi−1) + bi (x − xi−1)2 + ci (x − xi−1)3 ,x ∈ [xi−1, xi ] , i = 2, ...,N

f1 (x1) = f1

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Spline InterpolationI This gives 3N − 3 parameters to be determined.I Imposing continuity on the function and its first two derivativesyields a system of 3N − 5 non-linear equations constraining thechoice of a, b, c

fi+1 (xi ) = fi (xi ) , i = 1, ...N − 1f ′i+1 (xi ) = f ′i (xi ) , i = 2, ...,N − 1f ′′i+1 (xi ) = f ′′i (xi ) , i = 2, ...,N − 1

I

fi = fi−1 + ai (xi − xi−1) + bi (xi − xi−1)2 + ci (xi − xi−1)3

ai+1 = ai + 2bi (xi − xi−1) + 3ci (xi − xi−1)2

bi+1 = bi + 3ci (xi − xi−1)

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Spline InterpolationI

ai =fi − fi−1(xi − xi−1)

− bi (xi − xi−1)− ci (xi − xi−1)2

ai+1 = ai + 2bi (xi − xi−1) + 3ci (xi − xi−1)2

ci =bi+1 − bi3 (xi − xi−1)

I

ai =fi − fi−1(xi − xi−1)

−(23bi + bi+1

)(xi − xi−1)

ai+1 = ai + (bi+1 + bi ) (xi − xi−1)

ci =bi+1 − bi3 (xi − xi−1)

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Spline Interpolation

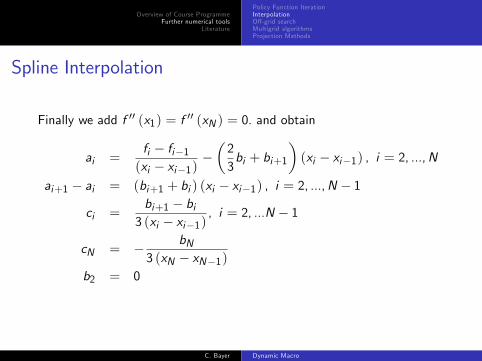

Finally we add f ′′ (x1) = f ′′ (xN ) = 0. and obtain

ai =fi − fi−1(xi − xi−1)

−(23bi + bi+1

)(xi − xi−1) , i = 2, ...,N

ai+1 − ai = (bi+1 + bi ) (xi − xi−1) , i = 2, ...,N − 1

ci =bi+1 − bi3 (xi − xi−1)

, i = 2, ...N − 1

cN = − bN3 (xN − xN−1)

b2 = 0

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Spline Interpolation

While spline interpolation is very accurate, it is very time consuming if Nis large.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Comparison of interpolation methods

0 1 2 3 4 5 6 7 80.5

1

1.5

2

2.5

3

3.5functionLS interpolationlinear interpolationspline interpolation

I Spline interpolation gives best results.I Linear interpolation is not bad either, yet, derivatives are constantbetween base points..

I With insuffi cient degrees of freedom, LS interpolation performsbadly.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Off-grid search

I We can use interpolation methods to approximate dynamicprogramming problems.

I So far we considered approximations to the continuous state-spaceproblem

V (s) = maxy∈Γ(s)

u(s, s ′, ξ

)+ βV

(s ′).

by using a fine grid {s1, . . . , sN } for s and then solving by iteratingover the approximated, discretized problem.

Vn = max{U+ ιNV

n−1}.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Off-grid search

Alternatively, we can define

V n (s) = Interpolation({V ni , si}i=1...N , s

)and update the base points, allowing for policies outside the grid{si}i=1...N .

V n+1i = maxy∈Γ(si )

u(si , s

′, ξ)+ βV n

(s ′)

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Off-grid searchExample

Exercise (13)Use the non-stochastic growth model with δ = 1.

1. Define a 10 point grid for k.

2. Use spline interpolation to solve for the value function, starting withV = 0 as initial guess, save running times.

3. Compare to the true value function at the grid points and noteaverage absolute difference.

4. Run a sequence of on-grid value function iterations withN = 10, 20, 40, 80, 160, 320 points. Compare average absolutedifference to the true model and running times with the off-gridsearch code.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Chow and Tsitsiklis’(1991) Multigrid VFI

I We have seen that computation time for Value FunctionIteration as well as Policy Function Iteration grows polynomiallyin the number of grid points. (This can also been shown formallyusing complexity theory, see Rust (1996))

I Conversely this means that for small problems we can calculate thesolution relatively quickly.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Chow and Tsitsiklis’(1991) Multigrid VFI

I Chow and Tsitsiklis (1991) suggest an algorithm that rests on thisinsight:

1. First solve the SDP on a sparse grid of points by VFI: This yields V ∗02. Increase the number of grid points in each dimension by factor 2.3. Obtain an initial guess V 01 for the value function on the new grid byinterpolation from the solution on the coarser grid.

4. Perform value function iteration to obtain V ∗1 for the enlarged grid.5. Repeat steps (2) to (4) until the grid is fine enough.

I Ideally the critical value for termination of the VFI decreases byfactor 2 in each grid iteration.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Chow and Tsitsiklis’(1991) Multigrid VFI

I Chow and Tsitsiklis (1991) show that this algorithm almost reachesthe effi ciency bound (in terms of worst case complexity) foralgorithms to solve SDP.

I In practical applications the algorithm is linear in the number ofgridpoints.

I This does not hold true if VFI is to be replaced by PFI, becausecomplexity in the latter case stems from inverting the Policy matrix.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Chow and Tsitsiklis’(1991) Multigrid VFI

I For practical purposes a mixed algorithm outperforms:I Use a multigrid PFI until the total number of gridpoints is about 500.I Then switch to VFI.

I One has to trade off grid generation time (e.g. Tauchen) againstmultigrid time saving.

I A further practical advantage of the multigrid algorithm comes indealing with outside loops: endogenous contracts, market clearingconditions, stationary equilibria etc.

I The following graphics compares computing times for the stochasticgrowth model:

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Comparison of running times

50 100 150 200 250 300 350 400 450 500 5500

5

10

15

20

25

30

35

number of grid points

runn

ing

time

[sec

]

VFIPFIMultigrid VFIMultigrid PFImixed Multigrid

VFI-Multigrid is linear, PFI-Multigrid is not!

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Multigrid VFI: Code

Switch to MATLAB, discuss code!

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Multigrid VFI: Exercises

Exercise (14a in class)Program a multigrid VFI algorithm to solve the stochastic income,consumption-savings problem using the simplified Tauchen procedure torepresent the AR-1 income process.

Exercise (14b)Extend the stochastic growth model such that utility is obtained from anaggregate of current and lagged consumption. Assume u (Ct ) = ln Ct

and Ct =(

αc−1t + (1− α) c−1t−1

)−1. Use a multigrid algorithm to solve

the model. Simulate the model! What effect does the change inpreferences have on the persistence of consumption? Compare the resultsfor α = 1, α = 0.8, α = 0.5. How can you interpret the model?

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Projection Methods

I All the before mentioned algorithms rely on the calculation of thevalue function to obtain the policy function, which is in mostapplications the object of interest.

I Projection methods directly solve for the policy function withoutsolving for the value function by invoking the Euler equation.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Euler equation

I Consider a SDP

V (s) = maxc∈Γ(s)s ′=f (s ,c )

u (c) + βEV(s ′)

I The first order condition is

u′ (c) + βEV ′(s ′)f ′c (s, c) = 0

I Optimality (envelope theorem) implies

V ′ (s) = βEV ′(s ′)f ′s (s, c)

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Euler equation

I Therefore first order condition is

u′ (c)f ′s (s, c)f ′c (s, c)

= −V ′ (s)

I Plugging this back in yields the Euler equation

u′ (c) = βE(u′(c ′)f ′s(s ′, c ′

))I The optimal policy trades off marginal utility today and discountedexpected marginal utility tomorrow, taking into account the relativemarginal effect of c and s on the future state s ′.

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Projection methods

I Projection methods exploit the Euler equation

u′ (c)− βE(u′(c ′)f ′s(s ′, c ′

))= 0

I Define the policy function c = h (s), then we can rewrite the Eulerequation as

Fh (s) := u′ (h (s))

− βE(u′ (h (f (s, h (s)))) f ′s (f (s, h (s)) , h (f (s, h (s))))

)= 0

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Projection methods

I Projection methods parametrize h, for example by a Chebyshevpolynomial.

h (s) =n

∑i=1

ψi ci (xi )

and we need to determine ψi , i = 1, ..., n.I Ideally the base functions should look alike the policy function.I We cannot expect Fh (s) = 0 for all s.I Therefore we minimize ||Fh || for some appropriate metric ||·||.I The metric is from the class ||F || =

∫A F (a) g (a) da, where g is

some weighting function

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Least square metric

I One possible metric is the least square metric.I This leads to the minimization problem

minψ

∫ [Fh (s)

]2 dsI The integral has to be solved numerically

C. Bayer Dynamic Macro

Overview of Course ProgrammeFurther numerical tools

Literature

Policy Function IterationInterpolationOff-grid searchMultigrid algorithmsProjection Methods

Collocation method

I An alternative metric uses the mass point function as weighting.I This function takes value 1 if x = xi for a pre-specified set of points.I If one uses n points, the ψi become exactly identified and thereforethe collocation method forces Fh to be exactly zero at xi .