Embed Size (px)

Citation preview

© 2011 Wilkinson & Company LLP.All rights reserved.

1

Succession Planning for private business owners

By:Douglas M. Parker, CA CFPWilkinson & Company LLP

May, 2011

© 2011 Wilkinson & Company LLP.All rights reserved.

2

Failing to Plan is Planning to Fail

Sir Winston Churchill during WWII

© 2011 Wilkinson & Company LLP.All rights reserved.

3

Index

� What is succession planning?

� Basic questions to answer

� What are we transferring?

� Role of income tax

� Estate freeze

� Sample client

� Types of succession plans

� Valuation

� The preferred shares

� Farmers

� Other planning issues

� Our role as advisors

© 2011 Wilkinson & Company LLP.All rights reserved.

4

What is succession planning?

� The orderly transfer of a family owned business to the next generation or employees of the company

© 2011 Wilkinson & Company LLP.All rights reserved.

5

Basic questions to answer

� Why are we doing this?� To attract family members to the ownership of the

business

� To reduce future income taxes to the extent possible

� To provide for a regular income for the parents/founders once the business is transferred

� To provide for easy administration of an estate and the business upon death

� To retain key employees

© 2011 Wilkinson & Company LLP.All rights reserved.

6

Basic questions to answer

� To whom shall the business be transferred?

� Which child or children should acquire the business?

� Should the transfer be to employees?

� Can the transfer be to both children and employees?

© 2011 Wilkinson & Company LLP.All rights reserved.

7

Basic questions to answer

� What is the best time to perform the transfer?

� At what age is the parent best able to transfer the business?

� At what age is the child best able to acquire the business?

� Has the child decided upon a career?

� Is the child old (mature) enough to run the business?

� Does the child still need consulting advice?

� Can the child run certain aspects of the business?

© 2011 Wilkinson & Company LLP.All rights reserved.

8

What are we transferring?

� The business need not be incorporated, but incorporation will:

� facilitate the estate freeze

� split the attributes of shares

� earn dividends in the future

� transfer the ownership of the business but retain control

� enjoy the capital gains exemption:

� then the transfer almost always involves a corporation

© 2011 Wilkinson & Company LLP.All rights reserved.

9

What are we transferring?

� Not just dealing with “shares”� In law shares of a company are a “basket of

rights” and we can deal with those rights separately

� Can transfer separately� The current value of the business

� The increase in the future value of the business

� Votes and the voting control of the business

� Management of the business

� Entitlement to future income

© 2011 Wilkinson & Company LLP.All rights reserved.

10

What are we transferring?

� Are there assets in the company that we do not wish to transfer to the next generation or to employees?

� Are there assets we wish to transfer to another child, for example:� Land that is in the business

� Excess cash in the company

� Investments in the company

� Two separate businesses, both in the same corporation and only one is to be transferred

© 2011 Wilkinson & Company LLP.All rights reserved.

11

Role of income tax

� Why do we care about the implications of the Income Tax Act in succession planning?

� Transfers between spouses are at cost [that is, the value of the shares is irrelevant, the gain on any shares or any loss on the shares is ignored, unless they elect to transfer at fair market value]

� Transfers to other related persons (including children) are at fair market value (FMV)

� If the FMV of the shares exceeds the cost of the shares, then there is a resulting capital gain

© 2011 Wilkinson & Company LLP.All rights reserved.

12

Role of income tax

� Up to $750,000 of the capital gain on the transfer to a family member other than a spouse [unless they elect out] can be offset by the Capital Gains Exemption.

� The capital gains exemption is only available on shares of a “Qualified Small Business Corporation”

© 2011 Wilkinson & Company LLP.All rights reserved.

13

Role of income tax

� Qualified Small Business Corporation� At the time of transfer, 90% or more of the assets

are used in an active business

� Shares of the company have been held for at least 24 months and more than 50% of the assets during that time have been used in an active business in Canada� Generally, this excludes rental properties and

investment assets from being in a Qualified Small Business Corporation

� Certain holding companies can qualify

© 2011 Wilkinson & Company LLP.All rights reserved.

14

Role of income tax

� Estate Planning

� If the shares of a company are held until death, they will be transferred to the next generation at their then fair market value

� If the value of the company has risen between now and that time in the future, then the capital gain and the resulting income tax will be higher

� The only tax-free transfer is between spouses

© 2011 Wilkinson & Company LLP.All rights reserved.

15

Estate freeze

� Several definitions available, but essentially:� Transfer the future growth of the company to the

next generation but retain the existing value of the company with the parent, or

� Splitting the company ownership into two, one being the existing value of the company and the other the future growth in the value of the company

� For example, assume that a company is worth $1,000,000 today and that it will continue to grow [see next overhead]

© 2011 Wilkinson & Company LLP.All rights reserved.

16

Estate freeze

Current Value$1,000,000

Time ►

FutureValue

PreferredShares

CommonShares

© 2011 Wilkinson & Company LLP.All rights reserved.

17

Estate freeze

� The current value of the company is converted into preferred shares that are held by the parent and “locked” in value or fixed in value

� Common shares which are worthless today are gifted to the child and if the company grows, the increase in value is reflected in the value of the common shares

© 2011 Wilkinson & Company LLP.All rights reserved.

18

The Aged family – sample client

� Mr. Aged � 64 years of age, wife is second wife, she is 64

� Owns 100% of Old Co.� Fair market value of $1,000,000

� ACB and Paid-up Capital of $100

� Mr. Aged has not used any of his capital gains exemption

� Two sons (both of first marriage), one active in business, married, age 34

� Wants control for now, 50/50 at some later time when he wishes to semi-retire and then relinquish full control at a later date (or upon his death)

� Wants income to himself or his wife on these shares in the future

© 2011 Wilkinson & Company LLP.All rights reserved.

19

Types of succession plans

� Outright Sale

� Internal reorganization

� Holding company

� These are not all of the possible solutions, but the most common

© 2011 Wilkinson & Company LLP.All rights reserved.

20

Outright sale

� Mr. Aged sells the shares of Old Co to his son for $1,000,000

� He takes back a promissory note for $1,000,000 with interest at 3% on the unpaid balance

� Result, Mr. Aged will recognize a capital gain on the sale of $999,900 but:

� The gain may qualify for the capital gains exemption

� The unpaid amount (the promissory note) will qualify for a reserve (deferral) of the gain

© 2011 Wilkinson & Company LLP.All rights reserved.

21

Outright sale

� Advantages

� Simple --- easy to arrange

� Claim Capital Gains Exemption if available

� Take back promissory note payable “on demand” for unpaid amount to help transition plus offer some form of “control”

� Can spread capital gain over 5 years on promissory note (10 years when sold to a child or grandchild and company is a small business corporation) if proceeds are deferred

© 2011 Wilkinson & Company LLP.All rights reserved.

22

Outright sale

� Disadvantages� Income taxes to pay!!!!

� Now and in the future when (as) the Promissory Note is repaid

� Irreversible� No Family Law Act protection� Difficult to impose Price Adjustment Clause� Control to the parent may only be an illusion� Difficult to bring in income splitting, capital gains splitting� Difficult to provide for non-business son � Son has to find after-tax funds to finance purchase� Son cannot use a holding company to make purchase� Cannot forgive the promissory note without adverse tax consequences� Promissory note can become “statute barred”� Promissory note can become problematic if ownership of company

changes

© 2011 Wilkinson & Company LLP.All rights reserved.

23

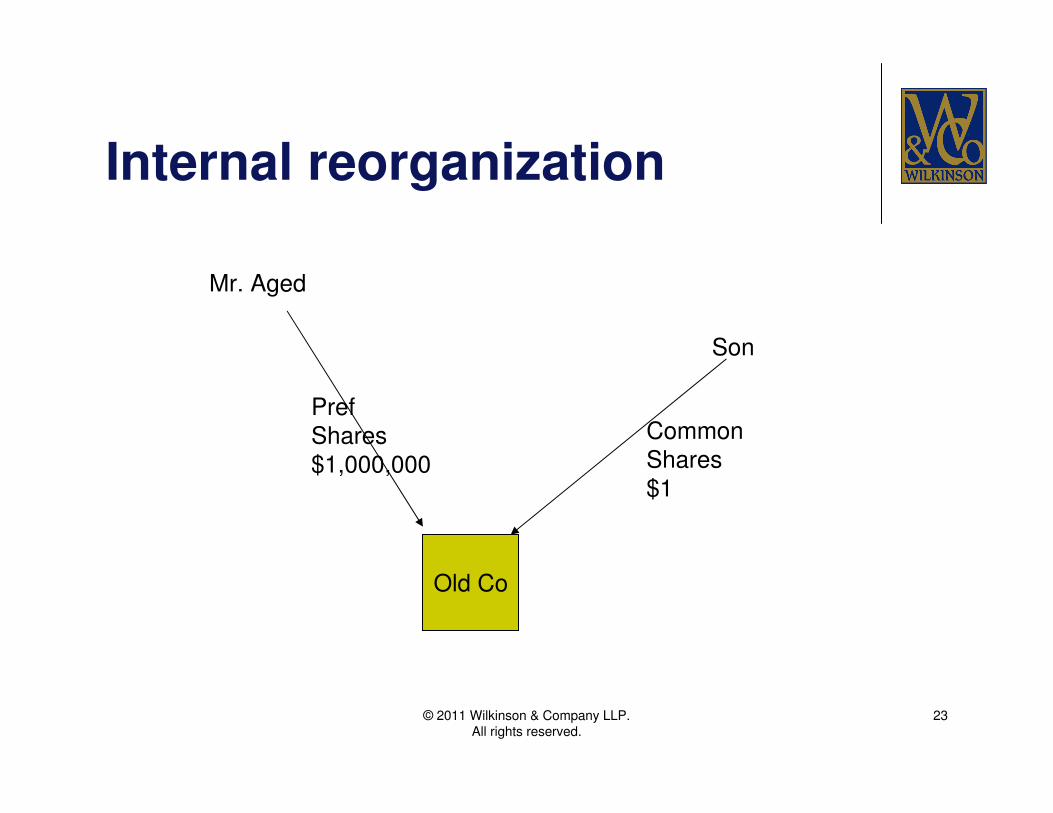

Internal reorganization

Old Co

Mr. Aged

Son

PrefShares$1,000,000

Common Shares$1

© 2011 Wilkinson & Company LLP.All rights reserved.

24

Internal reorganization

� Mr. Aged Exchanges his shares for: � Preferred shares, non-voting, redeemable and retractable

for $1,000,000 in the aggregate, Paid-up Capital for tax purposes of $100, non-cumulative fixed dividend of say 4%;

� 1,000 “thin” voting shares, no value, Paid-up Capital of $1

� Price adjustment clause on the Redemption/retraction amount [for CRA purposes]

� Issue common shares to Mr. Aged and he then gifts them to his business son

© 2011 Wilkinson & Company LLP.All rights reserved.

25

Internal reorganization

� Advantages� Exchange of common shares (old shares) owned by Mr. Aged for

new preferred shares is a “rollover”, i.e.. No gain recognized for income tax purposes

� No new company required, no election forms required� Can “elect out” of section 86 by subsection 85(1) and elect that

the exchange price is higher for tax purposes; use up the Capital Gains Exemption

� Thin voting shares can be retracted by Mr. Aged over time, giving control to son in stages

� Preferred shares can be left to spouse (or trust for her), other son or the business son

� Disadvantages� Parent gets less money after-tax than in an outright sale if the

preferred shares are redeemed

© 2011 Wilkinson & Company LLP.All rights reserved.

26

Internal reorganization

� Income Tax Concerns

� Must be in contemplation of a “reorganization of capital”

� Must surrender all of the shares held by Mr. Aged

� Income attribution could apply in the future if company ceases to be a small business corporation

© 2011 Wilkinson & Company LLP.All rights reserved.

27

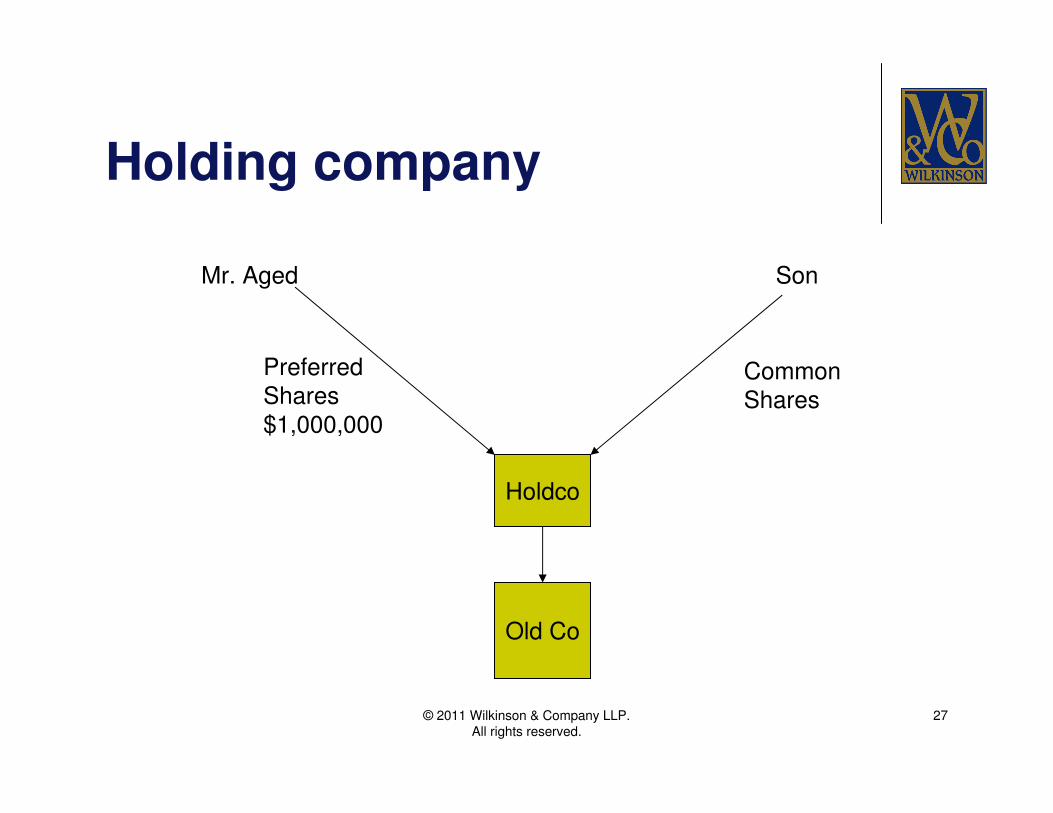

Holding company

Holdco

Old Co

Mr. Aged Son

PreferredShares$1,000,000

CommonShares

© 2011 Wilkinson & Company LLP.All rights reserved.

28

Holding company

� Mr. Aged transfers his shares of Old Co for shares of Holdco and takes back:

� Preferred shares, non-voting, redeemable and retractable for $1,000,000 in the aggregate, Paid-up Capital for tax purposes of $100, non-cumulative fixed dividend of say 4%;

� 1000 “thin” voting shares, no value, Paid-up Capital of $1

� Price adjustment clause on the Redemption/retraction amount for CRA purposes

� Issue common shares to Mr. Aged and he then gifts them to his business son

© 2011 Wilkinson & Company LLP.All rights reserved.

29

Holding company

� Advantages� The transfer of the shares of Old Co to Holdco is a “tax-free” rollover� Can use Holdco to receive cash dividends and lend back to Old Co

(creditor protection)� Can trigger Capital Gains Exemption on the election� Can introduce new shareholders in Old Co without being

shareholders of Holdco

� Disadvantages� Potential “double tax”� Creates a new company, and the related costs � Rollover election forms to be filed, not automatic� Holding company cannot issue debt or shares with a high paid-up

capital to Mr. Aged in excess of $100 without Mr. Aged realizing a dividend, i.e.. He is taxed on a dividend and not a capital gain [and it is not eligible for a Capital Gains Exemption]

© 2011 Wilkinson & Company LLP.All rights reserved.

30

Valuation

� The value of the shares before the transfer (estate freeze) must be determined

� The value of the shares taken back on the estate freeze (the preferred shares) must be equal in value to the shares surrendered. If the value is too low and there is a gift to the transferee, then there is an immediate capital gain to the transferee without an increase in the adjusted cost base to the transferor.

© 2011 Wilkinson & Company LLP.All rights reserved.

31

The preferred shares

� The terms of the preferred shares is what makes the Estate Freeze work. CRA also wants to see that the preferred shares meet their definition of appropriate value

� If the preferred shares do not meet CRA’s determination of the value of the old common shares, then a price adjustment clause is inserted into the documents that will adjust the value of the preferred shares taken back

© 2011 Wilkinson & Company LLP.All rights reserved.

32

The preferred shares

� CRA wish list in the terms of the preferred shares:

� Redeemable at the option of the company

� Retractable at the option of the holder

� No dividend can be paid on other classes of shares that would reduce the FMV of the freeze shares below their redemption price

� Voting rights on any matter involving a modification of the attributes of the shares

© 2011 Wilkinson & Company LLP.All rights reserved.

33

The preferred shares

� CRA wish list (continued)

� Absolute priority on all other classes in the event of wind-up, dissolution etc.

� Absolute priority on redemption of shares before any other class, and company cannot acquire shares of other classes before redemption of all preferred shares

� No restriction as to the transfer of the preferred shares [otherthan in a regular shareholders agreement – see below]

� Price adjustment clause to the redemption/retraction price if the FMV is not equal to the common shares

© 2011 Wilkinson & Company LLP.All rights reserved.

34

The preferred shares

� CRA wish list (continued)

� Along with the above, CRA is concerned that the preferred shareholder cannot reverse the freeze or easily thaw the freeze by having a discretionary dividend on the preferred shares --- they should bear a fixed “reasonable” dividend rate per annum

� Say 4% to 6%

� This dividend rate is very important since it will determine the retirement income (in part) of the freezor

© 2011 Wilkinson & Company LLP.All rights reserved.

35

The preferred shares

� Problems encountered with these attributes:

� Retraction at the option of the holder

� What about future holders, changing circumstances

� Does this place an undue influence of the holder over the company?

� Non-cumulative fixed dividend of x% can be onerous� Make the fixed dividend rate a monthly rate instead

� Decline in the value of the company below the redemption/retraction price� How does CRA perceive value when the value of the company has

declined?

� Should the preferred shares be voting or use Thin Voting shares

� Can they be voting only to the first holder?

© 2011 Wilkinson & Company LLP.All rights reserved.

36

Farmers

� Special rules exist for owners of:

� Qualified farm property

� For example, Land, equipment or quota used in farming

� Qualified farm corporations

� A corporation principally involved in farming

� Qualified farm partnerships

� A partnership principally involved in farming

� The above three definitions (referred to as “farm assets” in this presentation) are complex and deserve a seminar on their own

© 2011 Wilkinson & Company LLP.All rights reserved.

37

Farmers

� The fair market value rule for transfers between family members is ignored in the case of these three types of farm assets

� The transfer for income tax purposes can be anywhere between cost and fair market value of the property --- therefore:� Any capital gain or recapture on depreciable property and

quota can be totally avoided when the farm assets are transferred to the next generation(s)

� If transfer at “cost” – becomes a “rollover” and there are no income tax implications

� If transferred for an amount above cost, capital gain may qualify for the Capital Gains Exemption

© 2011 Wilkinson & Company LLP.All rights reserved.

38

Other planning issues

� Shareholders’ Agreement

� You are not the only shareholder now, and the new shareholders can have their own wishes, family problems etc.

� Consider the three “D’s”

� Death

� Dispute

� Disability

© 2011 Wilkinson & Company LLP.All rights reserved.

39

Other planning issues

� Family Law Act

� To avoid the spouse of a child making a claim against the shares held by the child, consider taking back common shares personally and then gifting them to the child with an express exemption from their net family property

� A recent Court case denied this exemption, so it may not work

© 2011 Wilkinson & Company LLP.All rights reserved.

40

Other planning issues

� Wills

� The wills of all of the parties are now more important

� Deal with the shares on death

� Do the preferred shares go the spouse, or a trust for the spouse?

� Should the preferred shares be retracted/redeemed now that Mr. Aged is deceased?

� Should dividends become mandatory on the death of the first holder and now held by the spouse?

� Should the shares go to the business son or to both, and the business son has to buy out the interest of his siblings?

© 2011 Wilkinson & Company LLP.All rights reserved.

41

Other planning issues

� Spousal Trust� Trust created by Mr. Aged now or on his death for

the spouse, she will receive:� All the income from the trust while she is alive

� She is the only person who can receive the income while she is alive

� If capital is distributed from the trust, she must be the only beneficiary

� The capital of the trust can go to Mr. Aged’s children after her death

© 2011 Wilkinson & Company LLP.All rights reserved.

42

Other planning issues

� Life Insurance

� There is often a need for life insurance at this time to cover:

� Taxes arising on death of one of the shareholders

� Provide for the redemption of the shares of the deceased to “buy” out the spouse or estate

� Provide life insurance on the “key man” in the business

� Life insurance at this time is often corporate owned and it can (up to a limit) be returned tax-free to the shareholder or estate

© 2011 Wilkinson & Company LLP.All rights reserved.

43

The overall plan

� The succession plan is made of five parts

� These parts are interrelated

� Lack of, or insufficient use of, one part of the plan will greatly diminish the plan

� The focus of my presentation has been on the tax structure, since that is often the driving force from the accountant’s point of view, but the other components are equally important

© 2011 Wilkinson & Company LLP.All rights reserved.

44

Tax Structure

Shareholders’Agreement

WillsLifeInsurance

RetirementIncome

© 2011 Wilkinson & Company LLP.All rights reserved.

45

Our role as advisors

� As Accountants, we often� Design the succession plan

� Determine the value of the company

� Communicate with the lawyers the required documents that need to be created (amended)

� Coordinate with the parties the steps that are taken

� Review all of the documents and explain them to the parties

� File necessary election forms with the CRA