Embed Size (px)

DESCRIPTION

hghggh

Citation preview

III. Substantive Testing of Balances and Analytical Procedures

1. Substantive Testing of Cash

Assertions Audit Objectives Audit ProceduresI. Existence or

OccurrenceA. To determine

whether cash exists at day-end and cash-related transactions occur within the day.

B. To determine that all cash balances of the client are reflected on the balance sheet at day-end.

1. Obtain analysis of cash balance and reconcile to the general ledger.

2. Confirm cash balances as of balance sheet date.

3. Perform cash count procedures for cash on hand.

II. Completeness C. To determine whether all cash transactions are recorded in the proper accounting period.

4. Prepare proof of cash and reconcile cash transaction occurring during a specified period as they are recorded by the client.

5. Verify the client’s cut-off of cash receipts and cash disbursements.

III. Valuation or Allocation

D. To determine if cash is recorded and presented at the proper amount.

6. Verify cash on hand under receivership. This is in addition to the foregoing procedures which will enable the auditor to verify proper valuation of cash.

IV. Presentation and Disclosure

E. To determine whether cash is presented in accordance with GAAP.

7. Investigate any voucher representing large or unusual payments to related parties.

8. Evaluate proper financial statements presentation and disclosure of cash.

2. Substantive Testing of Sales

Assertions Audit Objectives Audit ProceduresI. Existence or

OccurrenceII. Rights and

Obligations.

1. Perform analytical procedures to determine whether recorded sales appear reasonable.

III. Completeness A. To determine that all transactions relative to sales have been recorded in the proper accounting period.

2. Test cut-off of sales which are recorded in the proper accounting period.

3. Substantive Testing of Cost of Goods Sold

Assertions Audit Objectives Audit ProceduresI. Existence or

OccurrenceA. To determine

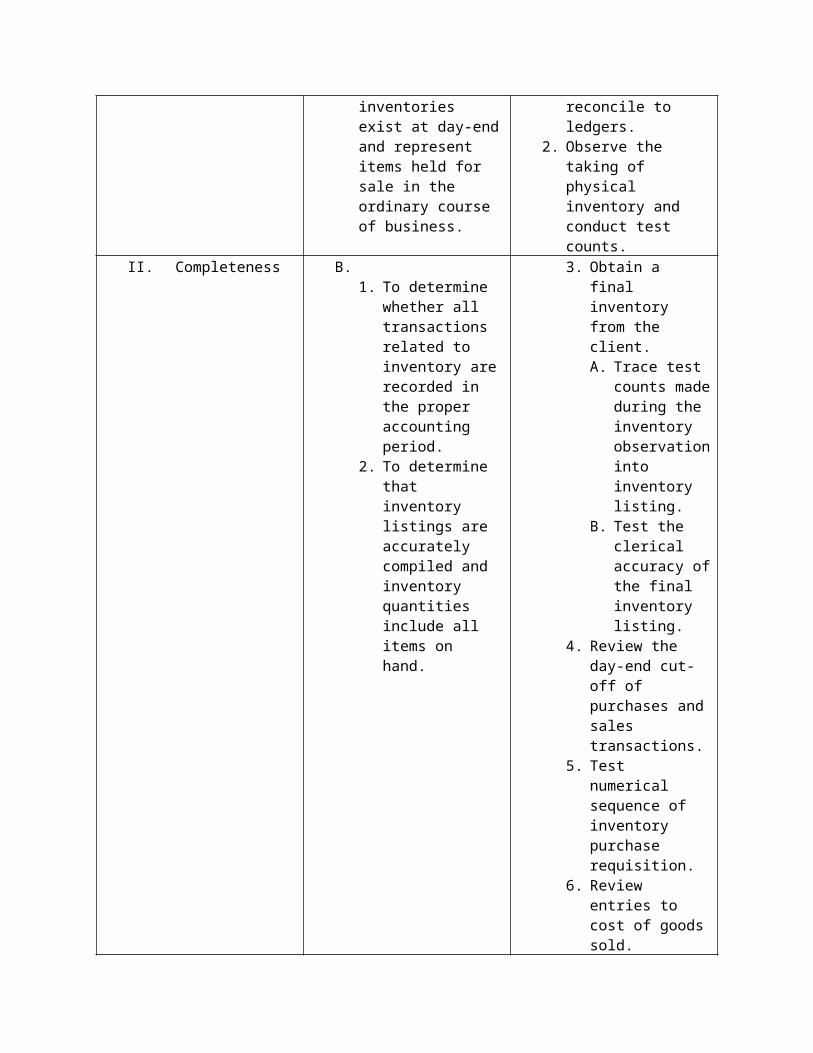

whether inventories exist at day-end and represent items held for sale in the ordinary course of business.

1. Obtain listings of inventory and reconcile to ledgers.

2. Observe the taking of physical inventory and conduct test counts.

II. Completeness B.1. To determine

whether all transactions related to inventory are recorded in the proper accounting period.

2. To determine that inventory listings are accurately compiled and inventory quantities include all items on hand.

3. Obtain a final inventory from the client.A. Trace test

counts made during the inventory observation into inventory listing.

B. Test the clerical accuracy of the final inventory listing.

4. Review the day-end cut-off of purchases and

sales transactions.

5. Test numerical sequence of inventory purchase requisition.

6. Review entries to cost of goods sold.

7. Perform analytical review related to inventories and cost of goods sold.

III. Valuation or Alocation

C. To determine whether the inventories are properly stated with respect to

Cost determine by an acceptable method consistently applied.

8. Evaluate the basis and methods of inventory pricing.

9. Vouch and test inventory pricing.

10.Check inventory for quality and/ or obsolescence.

IV. Presentation and Disclosure

D. To determine that the inventories and cost of goods sold are presented and classified in the financial statements in accordance with PAS or PFRS.

11.Determine the existence of inventory.

12.Evaluate financial statement presentation of inventories and cost of goods sold including adequacy of disclosure.

4. Substantive Testing of Prepaid Expenses (Supplies)

Assertions Audit Objectives Audit Procedures1. To ascertain the

correctness of prepaid or deferred amount at the end of the period as

A. Vouch purchases of supplies on a test basis.

B. Conduct physical count of supplies

well as the amounts consume or had expired, if any, during the period under review.

inventory on a test basis.