Embed Size (px)

Citation preview

Sub-tropical Fruits: Tariffs, AGOA and Trade Negotiations

Subtropical Marketing Symposium

John Purchase & Tinashe Kapuya

4 November 2015

• Introduction

•Tariffs

•African Growth and Opportunities Act (AGOA)

•Trade agreements

•Sub-Trop trade• SA Agricultural trade balance & Export destinations• Export trends – a look at four fruit products• Composition of exports • Structure of exports of four sub-trop fruits

•Way forward

Outline for today…..

Tariffs

The wars of the future are trade wars, and these will not be regulated through World Trade Organisation (WTO) agreements, but by regional and bilateral trade agreements.

Tariff measures are increasingly being replaced by non-tariff barriers (NTB’s) as the preferred and dominant measure to restrict market access.

Region Avocadoes Macadamia nuts Litchis MangoesEurope and Eastern Europe

EU 0% 0% 0% 0%

Switzerland 0% 0% 0% 0%

Norway 0% 0% 0% 0%

Russia 3.8% 3% 3% 3%

African markets

EAC 25% 25% 25% 25%

SACU 0% 0% 0% 0%

SADC 0% 0% 0% 0%

- Zimbabwe 0% 0% 16% 15%

- Angola 50% 50% 50% 50%

- Malawi 15% 7.5% 15% 15%

Egypt 20% 10% 10% 20%

Ghana 20% 20% 20% 20%

Nigeria 20% 20% 20% 20%

Asia and the Far East

Hong Kong 0% 0% 0% 0%

Indonesia 5% 5% 5% 10%

Malaysia 5% 0% 7.5% 0%

China 25% 14.25% 21% 15%

Middle East

UAE 0% 0% 0% 0%

Saudi Arabia 0% 0% 0% 0%

Qatar 0% 0% 0% 0%

Kuwait 0% 0% 0% 0%

North America

USA 0% 0% 0% 0%

0% 0%

Applied Tariffs faced by South Africa per product per region

• African Growth and Opportunities Act (AGOA)

• Not a trade agreement

• Provides tariff free access for certain African products through eligibility criteria – recently revised

• New legislation allows a longer timeline, but with a provision of out-of-cycle reviews

• SA currently subject to such a review – very complex

• SA biggest beneficiary: motor vehicles, fruit, wine & nuts

• Market access concerns from USA: Chicken, beef & pork

• Transitioning into what looks like a reciprocal agreement

AGOA

• Paris agreement on chicken: 65 000 tons at 37% tariff

• Avian flu concerns – agreement on sanitary and food safety regulations a precondition

• SA missed deadline of 15 October

• Final deadline of 2 November

• SA could lose certain benefits, including fruit access – major risk

• Agbiz engagement with Min Rob Davies - confident of positive outcome

• Bilateral SACU-USA free trade agreement now an absolute necessity due to increased risks – previous failed attempt

• Agbiz liaising with USDA-FAS in this regard

• Could be more problematic to negotiate than SACU-EPA agreement.

AGOA

Key SA Trade Agreements in process :• The Tripartite Free Trade Agreement (T-FTA)• The Economic Partnership Agreement (EPA)• The Southern African Customs Union (SACU)• The Southern African Development Community Free Trade

Agreement (SADC- FTA)

WTO: Bali Trade Facilitation Agreement - Aims to standardize, streamline and speed-up customs processes around the world, helping to expedite the movement, release and clearance of goods -will significantly cut the costs of trade. Potential to increase global merchandise exports by up to $1 ,0 trillion dollars per annum.

Mega-Regional Trade Agreements:

• Trans Pacific Partnership case in point – Risk to SA

Trade agreements

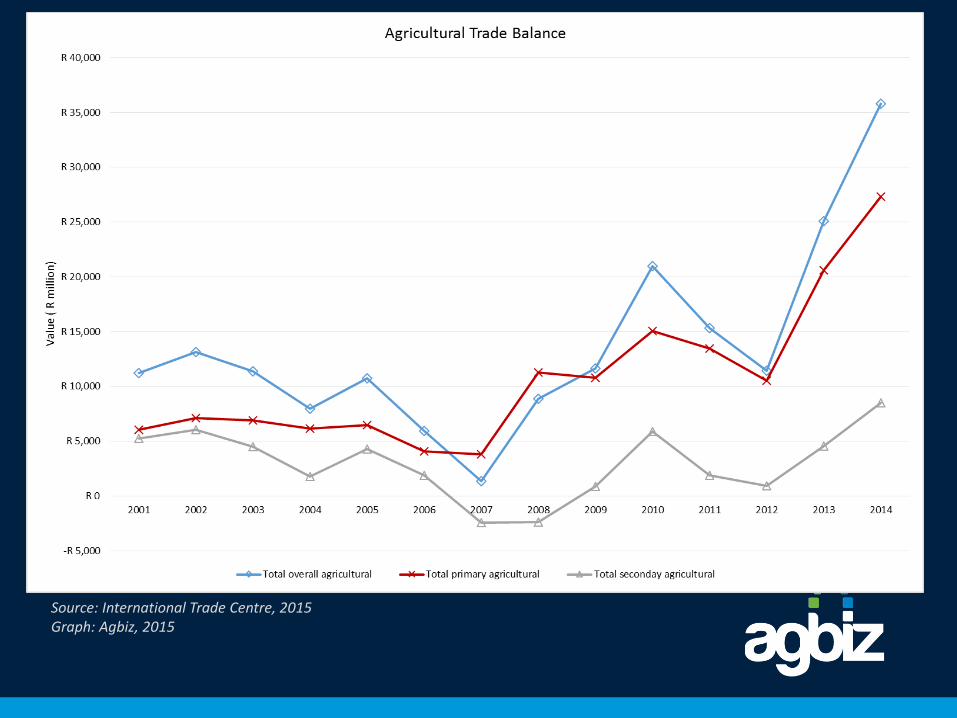

Source: International Trade Centre, 2015Graph: Agbiz, 2015

Trends in sub-tropical fruit exports (2005-2014)

-

50

100

150

200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Va

lue

of

Ex

po

rts

(U

S$

mil

lio

ns

)

Mangoes Avocadoes Macadamia nuts Litchis

Composition of sub-tropical fruit exports (2005-2014)

16% 17%13%

9% 7% 6%3% 6%

2% 3%

65%

46%

44%

33%

27% 31%

18%

33%

30% 28%

21%

34%47%

48%

64%

50%56% 61%

19%

37%

22% 23%19%

15% 15%12% 11%

8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Sh

are

of e

xp

ort

s (

%)

Mangoes Avocadoes Macadamia nuts Litchis

Structure of SA’s macadamia exports

SA is the largest exporter of macadamia in the world

Africa 0.1%

USA11%

EU 7%

ME0.5%

Asia & Far East

79%

Structure of SA’s avocado exports

South Africa is the 8th largest exporter of avocadoes in the world

Africa1%

EU 95%

Asia & Far East

1%ME 1%

Structure of SA’s mango exports

ME3%

Africa62%

Asia & Far East

6%

EU 14%

SA the 34th largest export of mangoes in the world

Structure of SA’s litchi exports

Asia & Far East

5%ME5%

EU45%

Africa 39%

SA is the 15th largest exporter of litchis in the world

• Export diversification and market development remain vital for the future growth of the broader industry

• A need to rebalance the export structure is important to ensure over-reliance on key markets is addressed

• New emerging opportunities in the USA, but this remains uncertain. The AGOA out-of-cycle reviews represent the biggest threat/risk to expansion in the USA

• South Africa is in the middle of an out-of-cycle review at the moment, and the outcome of this review is unknown

• EU remains a “low volume - high value market”, with Africa being a “high volume – low value market”

Way forward…..

www.agbiz.co.zawww.jadafa.co.za

Thank you