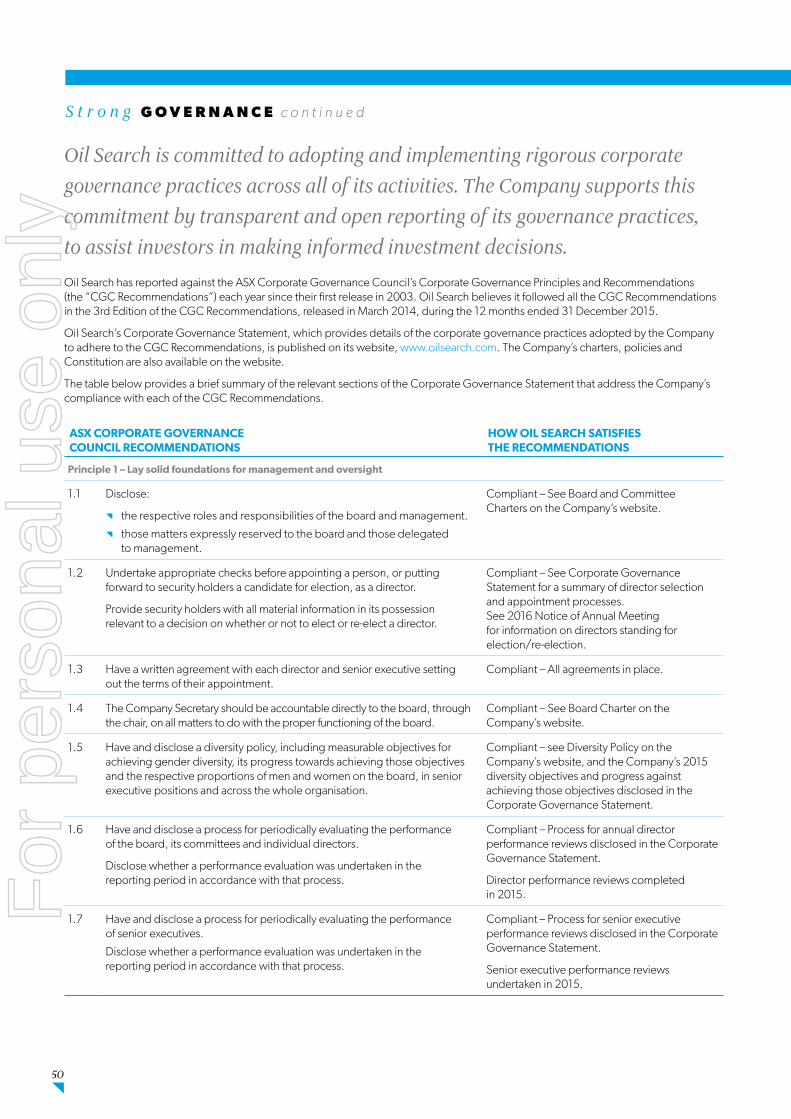

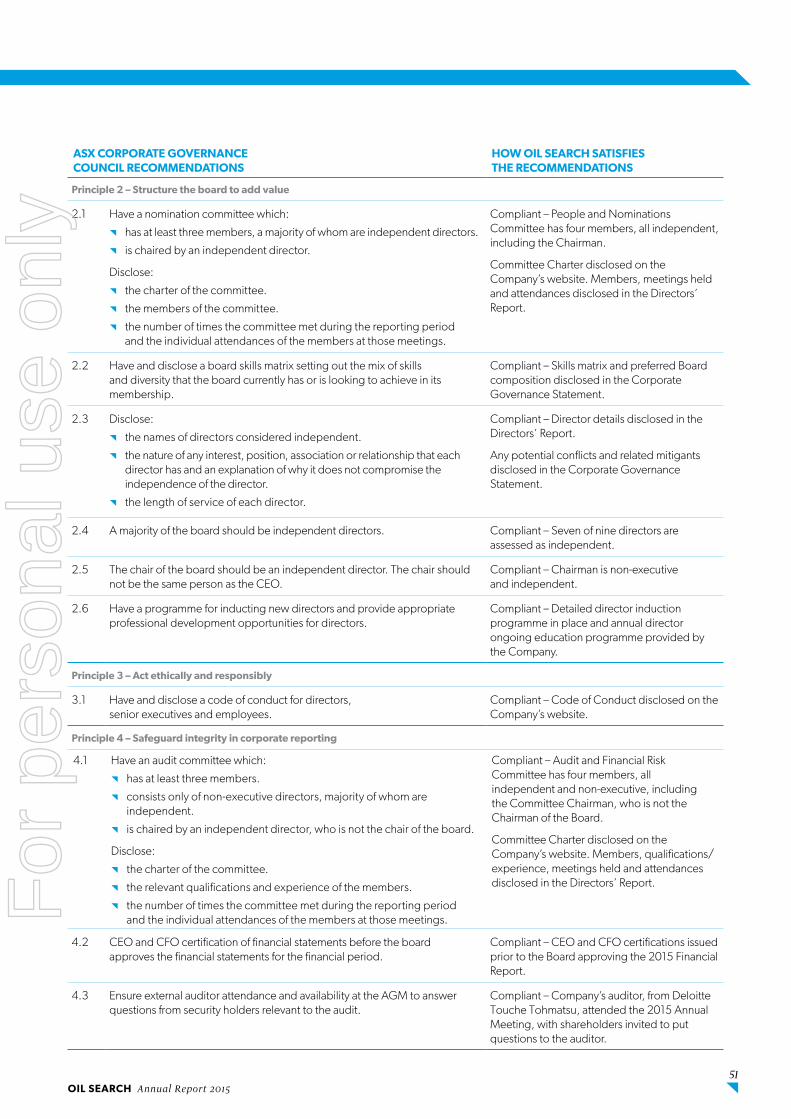

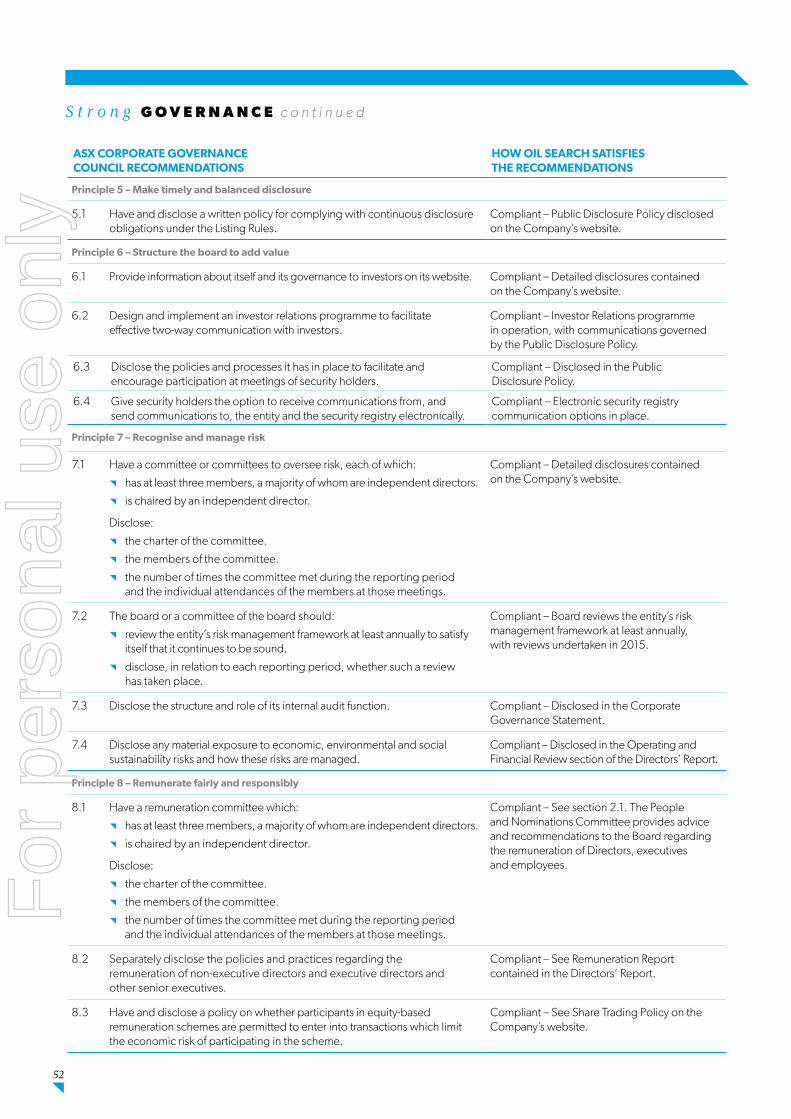

Embed Size (px)

Citation preview

A N N UA L R E P O R T 2015A N N UA L R E P O R T 2015

StrongFOUNDATIONS

i

For

per

sona

l use

onl

y

2 Our Vision, Our Values

4 Strong Performance

6 2015 Highlights

8 Strong Leadership

10 Strong Strategic Outlook

14 Strong Financial Management

16 Strong Executive Team

18 Strong Production

22 Strong Gas Growth

28 Strong Exploration Programme

32 Strong Commitment to Social Responsibility

36 Strong Organisational Capability

40 2015 Reserves and Resources

46 Licence Interests

48 Strong Governance

54 Financial Report Contents

55 Directors’ Report

88 Financial Statements

124 Shareholder Information

128 Ten-year Summary

130 Glossary

132 Corporate Directory

IBC About Oil Search

For

per

sona

l use

onl

y

… the key toFUTURE GROWTH

Oil Search’s history is deeply rooted in Papua New Guinea (PNG), where the

Company has operated since 1929. Over this time, Oil Search has developed strong

and genuine relationships with the PNG Government, regulators, landowners

and communities and an unrivalled understanding of how to operate successfully

and safely in PNG. The Company’s long-standing commitment to social responsibility

and sustainable development, which is fundamental to maintaining a stable

operating environment in PNG, has been instrumental in its success.

Oil Search remains committed to PNG and intends to leverage its strong foundations

to unlock the country’s full oil and gas potential, ensuring continued delivery of

long-term value to all stakeholders.

55 Directors’ Report

88 Financial Statements

124 Shareholder Information

128 Ten-year Summary

130 Glossary

132 Corporate Directory

IBC About Oil Search

1OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

To gen erate top q u ar t i le r e t ur n s

for sh ar ehol der s thr ough exc el len c e

in s o c ia l ly r e sp on sible oi l an d

ga s explorat ion an d pr o duc t ion

O U R V i s i o n

2

For

per

sona

l use

onl

y

O U R V a l u e s

Responsible

Respectintegrity

Diversity

Excellence

Caring

Passion

3OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

Strong PERFORMANCE

During 2015, Oil Search delivered a strong performance, both operationally and financially.

Production increased 52% to 29.3 million barrels of oil equivalent (mmboe), while core

profit declined 25%, despite nearly a 50% fall in the oil price compared to 2014.

Oil Search’s production assets have low operating costs and sustaining capital requirements

and generate positive cash flows even at current oil prices. In addition, the Company has

a strong balance sheet and sufficient liquidity to fund its globally-competitive gas growth

projects, which have the potential to deliver sector-leading returns to shareholders.

In 2015, Oil Search implemented a number of initiatives to recalibrate the business, aimed

at ensuring the Company can continue to deliver superior returns to its shareholders,

in a socially responsible way, in a ‘lower for longer’ oil price environment. This programme

to drive further efficiencies and innovation will continue in 2016.

4

in a challenging environment

For

per

sona

l use

onl

y

XX

5OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

2 0 1 5 H i g h l i g h t s

29.3 M M BOE

US$360 M I LLION

T o t a l p r o d u c t i o n

C o r e p r o f i t

6

For

per

sona

l use

onl

y

T o t a l p r o d u c t i o n ( M M B O E )

O p e r a t i n g c a s h f l o w ( U S $ M I L L I O N )

A v e r a g e r e a l i s e d o i l

a n d c o n d e n s a t e p r i c e ( U S $ P E R B A R R E L )

D i v i d e n d s p e r s h a r e ( U S C E N T S )

2015 BUSI N E SS OP T I M ISAT ION

PROGR A M M E

i n i t i a t i v e s w e r e i m p l e m e n t e d

t o a c h i e v e t h e a p p r o p r i a t e

o r g a n i s a t i o n a l a n d

r e s o u r c i n g s t r u c t u r e

t o d e l i v e r t h e C o m p a n y ’ s

c o r e p r i o r i t i e s i n a l o w

o i l p r i c e e n v i r o n m e n t

52% UP

4%

47%

42%

S a f e t y r e m a i n s a k e y

p r i o r i t y . T h e T R i R p e r

m i l l i o n h o u r s w o r k e d

i n 2 0 1 5 w a s 1 . 9 1 ,

d o w n f r o m 1 . 9 7 i n t h e

p r e v i o u s y e a r , d e s p i t e

m a n y w o r k p l a c e c h a n g e s

TOTA L R ECOR DA BL E I NCI DE NT R AT E (T R I R)

11 12 13 14 15 11 12 13 14 15

11 12 13 14 15 11 12 13 14 15 11 12 13 14 15

6.7

4 4 4

992

367

196

386

13.9

17.4 18

.8

12.2

116

114

111

98

6.4

6.7

19.3

51

29.

310

953

10.1

11 12 13 14 15

236

153 20

6

483

36

0

410

11 12 13 14 15 11 12 13 14 15

11 12 13 14 15 11 12 13 14 15 11 12 13 14 15

6.7

4 4 4

992

367

196

386

13.9

17.4 18

.8

12.2

116

114

111

98

6.4

6.7

19.3

51

29.

310

953

10.1

11 12 13 14 15

236

153 20

6

483

36

0

410

11 12 13 14 15 11 12 13 14 15

11 12 13 14 15 11 12 13 14 15 11 12 13 14 15

6.7

4 4 4

992

367

196

386

13.9

17.4 18

.8

12.2

116

114

111

98

6.4

6.7

19.3

51

29.

310

953

10.1

11 12 13 14 15

236

153 20

6

483

36

0

410

11 12 13 14 15 11 12 13 14 15

11 12 13 14 15 11 12 13 14 15 11 12 13 14 15

6.7

4 4 4

992

367

196

386

13.9

17.4 18

.8

12.2

116

114

111

98

6.4

6.7

19.3

51

29.

310

953

10.1

11 12 13 14 15

236

153 20

6

483

36

0

410

11 12 13 14 15 11 12 13 14 15

11 12 13 14 15 11 12 13 14 15 11 12 13 14 15

6.7

4 4 4

992

367

196

386

13.9

17.4 18

.8

12.2

116

114

111

98

6.4

6.7

19.3

51

29.

310

953

10.1

11 12 13 14 15

236

153 20

6

483

36

0

410

11 12 13 14 15 11 12 13 14 15

11 12 13 14 15 11 12 13 14 15 11 12 13 14 15

6.7

4 4 4

992

367

196

386

13.9

17.4 18

.8

12.2

116

114

111

98

6.4

6.7

19.3

51

29.

310

953

10.1

11 12 13 14 15

236

153 20

6

483

36

0

410

DOWN

DOWN

PAYOUT RATiO

C o r e p r o f i t

b e f o r e i m p a i r m e n t s ( U S $ M I L L I O N )

U n i t p r o d u c t i o n c o s t( U S $ P E R B A R R E L O F

O I L E Q U I V A L E N T )

25% 17% DOWNDOWN

4¢ SPECIAL

O i l S e a r c h ’ s o n e y e a r

T S R f e l l 1 2 % , r e f l e c t i n g

r e c e n t g l o b a l o i l p r i c e

w e a k n e s s . H o w e v e r

o v e r t h e p a s t 1 0 y e a r s ,

t h e C o m p a n y h a s

d e l i v e r e d a T S R o f 1 1 2 % ,

o u t p e r f o r m i n g t h e

A S X 2 0 0 a n d A S X 2 0 0

E n e r g y i n d i c e s

TOTA L SH A R E HOL DE R R ET U R N (TSR)

7OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

2015 was one of the most challenging years in

Oil Search’s history, with the average global oil

price nearly 50% lower than in 2014. However,

it was also one of the most successful for the

Company. Production reached an all-time high

of 29.3 mmboe, an increase of 52% compared

to 2014, driven by an excellent performance from

the PNG LNG Project and a solid contribution

from the Oil Search-operated PNG oil and gas

fields. While impacted by lower oil and gas prices,

the Company delivered a core profit of US$360

million before non-cash impairments, a strong

result given the oil price environment.

L E A D E R S H I P Strong

L E T T E R F R O M T H E C H A I R M A N

Consistent with our dividend policy to pay out between 35% and 50% of core profit to shareholders, an ordinary dividend of 10 US cents per share was paid for 2015, compared to a total of 14 US cents per share for 2014 (comprising an ordinary dividend of 10 US cents per share and a special dividend of four US cents per share). The Board continues to believe that a proportional dividend policy is appropriate in this time of volatile oil prices, enabling sufficient cash to be retained to invest in high-returning growth projects while still providing a return to shareholders. Given our financial strength, with US$910 million in cash and liquidity of close to US$1.7 billion at year end, our dividend reinvestment plan remains suspended.

The outlook for oil and LNG prices remains uncertain. With far fewer new oil and gas projects sanctioned in 2015 compared to previous years, we believe that global oil markets, which are currently oversupplied, will progressively rebalance as conventional oil production starts to decline. This should result in a gradual recovery in oil prices over the next few years. However, we expect, and are planning for, sustained low oil prices during 2016.

We implemented a number of organisational changes in 2015 to promote improved productivity and ensure the Company’s cost competitiveness.

8

For

per

sona

l use

onl

y

Production costs in 2015 were US$10.08 per barrel of oil equivalent (boe), down from US$12.21 per boe in 2014, despite several one-off costs associated with restructuring. We expect a further reduction in 2016, as the benefits of the changes made in 2015 are realised and additional initiatives to reduce costs and improve efficiency and productivity are undertaken. Oil Search’s breakeven oil price, after cash operating costs, sustaining capital and debt servicing, is approximately US$30 per barrel, highlighting the Company’s resilience to low oil prices. The strong liquidity position provides a further buffer in a low oil price environment.

With so many changes occurring within the Company, a key concern for the management team and Board in 2015 was, that our safety performance would suffer. Pleasingly, the Company achieved a slight improvement in Total Recordable Incidents and had no Lost Time Injuries, which is a credit to all Oil Search employees and reflects the strong safety culture embedded within the Company.

Looking to the future, we are very fortunate to have interests in two major LNG growth projects – the potential expansion of the PNG LNG Project and the proposed Papua LNG Project. Both are assessed by independent experts to be in the lowest quartile of development costs globally and

can generate significant shareholder value, even on more modest long-term oil and gas price expectations. Cash generated from our low cost producing assets and our strong balance sheet allow us to continue to invest in these high-returning growth opportunities, while many other proposed developments globally are being delayed or cancelled. The excellent performance of the PNG LNG Project, which is consistently and safely operating above nameplate capacity, has put PNG on the map as a reliable supplier of high heating value gas, located close to the key Asian markets. PNG LNG’s success provides us with confidence that, when these projects are ready for sanction, there will be demand for our gas from premium Asian buyers, despite the current oversupply of LNG.

During 2015, Woodside Petroleum submitted a highly conditional, scrip only proposal to the Oil Search Board to merge the two companies. Following extensive consultation with shareholders and a detailed assessment of the terms, the Oil Search Board rejected the proposal on the basis that it materially undervalued the Company and brought few, if any, benefits to Oil Search shareholders. Woodside subsequently withdrew the proposal. While the Company is in a strong position, operationally and financially, the Oil Search Board is open to any proposal

that reflects compelling value for Oil Search shareholders, which clearly this offer did not. The Board remains committed to acting in the best interests of shareholders at all times.

Strong leadership from the Oil Search Board, our Managing Director and the executive team was instrumental in driving the good performance achieved in 2015, despite it being a difficult year. I would like to thank all our employees for their contributions and my Board colleagues for their support and guidance. We look forward to 2016 with a degree of optimism, tempered by the recognition that the immediate and longer term market outlook will present both risk and opportunity. Our Company is well placed to meet the challenge.

Richard LeeCHAIRMAN

L E T T E R F R O M T H E C H A I R M A N

9OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

in light of sharply lower oil prices, in 2015 Oil Search reviewed the outcomes of the 2014 Strategic Review. The Company concluded that its core strategies remain appropriate and capable of generating significant value for stakeholders, even during a period of sustained low oil prices. The Company is committed, and has the financial capacity, to continue investing in its globally competitive LNG growth opportunities, through the present oil price cycle.

Peter BottenManaging Director

S T R A T E G I C O U T L O O K

Strong

In 2014, Oil Search undertook a major Strategic Review to prepare the Company for its next phase of growth. The Review concluded that shareholder returns would be maximised by the Company commercialising its existing gas resources in PNG. The Review also recognised the importance of maintaining Oil Search’s long-standing commitment to sustainable development, social responsibility and community relations.

In 2015, Oil Search carried out a careful re-examination of the results of the 2014 Strategic Review. It concluded that the core strategies remain the most appropriate way to deliver top quartile returns to shareholders.

A key component of Oil Search’s strategy to deliver long-term, high-value growth is the potential development of a third

train at the PNG LNG Project and the proposed new Papua LNG Project. Both developments are assessed by independent experts to be highly competitive relative to other proposed new LNG developments globally. Industry expert, Wood Mackenzie, ranks the projects in the lowest quartile for development costs, with PNG’s average LNG breakeven price almost 30% lower than proposed LNG projects in Australia.

In addition, Oil Search has developed a range of other strategic initiatives to further enhance shareholder value, including:

^ Increasing productivity and improving cost competitiveness through the implementation of a number of initiatives identified by the 2015 Business Optimisation Programme, outlined opposite.

Central Processing Facility, Kutubu, PNG Highlands.

10

For

per

sona

l use

onl

y

^ Supporting the PNG LNG Project operator in its efforts to optimise production and debottleneck the existing two PNG LNG trains.

^ Reviewing the potential to accelerate the supply of gas from the Oil Search-operated Associated Gas fields to the PNG LNG Project, optimising future capital investment and operating costs and bringing forward the end of field life.

^ Promoting a cooperative development agenda between ExxonMobil and Total, to capture potential synergies from existing infrastructure and to forge potential new partnerships.

^ Appraising and developing existing discovered gas resources as potential sources of third party gas for the PNG LNG and Papua LNG projects and to underwrite potential local power projects.

^ Replenishing the Company’s exploration porfolio in PNG.

^ Adding value through judicious and strategic acquisitions, with a focus on new acreage and licences in PNG.

2015 BUSINESS OPTIMISATION PROGRAMME OUTCOMESDuring 2015, in addition to reassessing its core strategies, Oil Search undertook a comprehensive review of all aspects of its business. The review was focused on ensuring that the Company’s organisational and resourcing structure, skill sets and cost base were not only appropriate for a potentially prolonged period of subdued oil and gas prices, but also capable of delivering Oil Search’s growth objectives. A range of initiatives identified by the review were progressively rolled out over the second half of 2015 and will continue to be implemented during 2016. The key changes include:

^ Simplifying the Company’s organisational structure, which has resulted in a leaner and more efficient business model.

^ Strengthening the LNG growth and PNG exploration teams, to support the key activities that will drive long-term growth.

^ Enhancing integrated planning, to drive efficiency and productivity through better alignment of resources and activities with Company priorities.

^ Optimising operated production output by maximising plant uptime.

^ Optimising supply chain and procurement activities through re-negotiating all major contracts and evaluating and implementing partnering strategies and process optimisation.

^ Improving drilling performance through the use of new technologies and innovation in rig and partnering strategies.

^ Increasing capital discipline and re-prioritising work programmes, to focus on value-adding activities that will maximise returns based on revised oil prices.

^ Further building the capabilities of the Port Moresby head office and the Company’s PNG workforce, to progress Oil Search’s localisation and diversity objectives. This includes targeted programmes to elevate PNG citizens into senior positions and further localisation of the PNG workforce.

^ Progressing partnerships with the PNG Government and communities, on projects such as power solutions, national infrastructure, health and education, that benefit all PNG citizens and help ensure a stable operating environment.

Towards the end of 2015, a Performance and Innovation Office was launched, aimed at embedding a culture of continuous improvement into the Company, to provide ongoing business improvements.

The delivery of these initiatives is expected to result in a more productive, efficient and cost-effective organisation, reducing production costs for Oil Search’s operated assets by approximately 25% in 2016. The programme of driving further efficiencies and innovation will continue into 2016 and beyond.

R E DUCT ION

i n p r o d u c t i o n c o s t s

f o r o p e r a t e d a s s e t s

e x p e c t e d i n 2 0 1 6

~25%

THE COMPANY HAS SIX KEY STR ATEGIES

Sustain and optimise the Company’s oil and gas assets

Commercialise gas in PNG

Pursue high-value exploration opportunities

Contribute to a stable operating environment

Enhance organisational capability

Optimise capital management

1.

2.

3.

4.

5.

6.

11OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

ENSURING A STABLE OPERATING ENVIRONMENTOil Search has developed a comprehensive strategy of community and government engagement that helps promote operating stability and provides positive social impacts in the communities in which the Company works.

Oil Search’s employment and business development initiatives for project landowners, together with a range of health, infrastructure and social development programmes, give Oil Search unprecedented access to, and support from, local communities. The Company’s Private-Public Partnerships with Government have delivered major infrastructure for PNG, leveraging Oil Search’s development skills to provide cost-effective, corruption-free services, which include roads, hospitals, schools and major buildings, including the new National Football Stadium.

In 2015, significant progress was made by Oil Search, in partnership with the Government, on projects designed to provide domestic power solutions in PNG, which is one of the country’s key infrastructure and social challenges.

BUSINESS ENVIRONMENT OUTLOOKOver 2015, the Brent oil price fell 47%, from an average of US$99 per barrel in 2014 to US$52 per barrel in 2015, and in January 2016 dipped below US$30 per barrel for the first time in 12 years. The fall is the result of an oversupplied market, with a substantial increase in production from new tight oil in the US and a change in OPEC strategy, away from its traditional role as a swing producer, coinciding with slowing economic growth in China and Europe.

The global supply:demand imbalance has led to a significant increase in world oil inventories. While there is already evidence that non-OPEC supply is starting to taper off, it is anticipated that oil prices will continue to be volatile over the next few years, until inventory levels have been drawn down to more normal levels. The global industry reaction to lower oil and gas prices has been to put marginal projects on hold, reduce discretionary expenditure and seek contractor rate reductions. With equity funding becoming harder to obtain, there has been a clear focus on capital efficiency and prioritisation. Significant downsizing has occurred and major capital projects have stalled, with only five major oil and gas projects sanctioned in 2015 compared to 30-50 annually in recent years.

There is also currently an oversupply of LNG globally, which is expected to persist through to the end of this decade, driven by the start-up of production from several major projects in Australia and the US. In the short-term, the LNG price outlook is expected to reflect this supply overhang and the continued weakness in global oil prices. However, from early in the next decade, demand from key markets in Asia is expected to exceed supply, as existing long-term contracts expire and demand for gas grows, particularly given its status as a far lower carbon emitter than alternative fuels.

Given this backdrop, the Company’s two potential LNG growth projects, which are both targeting first gas sales early in the 2020s, are well positioned. With far fewer proposed LNG developments making progress, these projects have the opportunity to benefit from anticipated capital cost reductions, attract premium customers and commence production in a period of stronger pricing.

Shorter-term, the Company’s business planning for 2016 is based on the assumption that lower oil prices will continue through most of the year. However, in line with a range of independent oil watchers, the Company does not believe that the oil and gas industry, in its current configuration, is sustainable at present oil prices. Consequently, a gradual recovery in oil and gas prices is expected through 2017 and 2018, as the supply:demand imbalance moderates.

REJECTION OF WOODSIDE PROPOSALIn September 2015, Oil Search received a non-binding, conditional indicative proposal from Woodside, under which Woodside would acquire all the shares in Oil Search for a consideration of one Woodside share for every four Oil Search shares held.

The proposal was subject to the following conditions:

^ Completion by Woodside of satisfactory due diligence on Oil Search.

^ Execution of a mutually acceptable confidentiality agreement.

^ Oil Search granting an agreed period of exclusivity.

S t r o n g S T R A T E G I C O U T L O O K c o n t i n u e d

The National Football Stadium, one of nine infrastructure projects managed and delivered by Oil Search on behalf of the PNG Government in 2015, hosted its first game in February 2016.

12

For

per

sona

l use

onl

y

^ Oil Search obtaining support from key stakeholders and shareholders.

^ Woodside being satisfied that the transaction was likely to be supported by the PNG Government on acceptable terms.

Following a detailed evaluation of the proposal, the Board concluded that it was highly opportunistic, grossly undervalued the Company and diluted the growth profile available to Oil Search shareholders. In addition, Oil Search undertook substantial shareholder engagement, with the overwhelming feedback that the proposal had little merit. Consequently, the Board unanimously decided to reject the approach and in December, Woodside withdrew the proposal.

OUTLOOK FOR 2016Oil Search is in a strong position, with a low cost production base with modest sustaining capital requirements and a substantial liquidity buffer. As such, unlike some of our global energy peers, the Company is committed, and has the balance sheet capacity, to continue to judiciously invest in its growth opportunities. By investing through the cycle, Oil Search hopes to take advantage of lower construction costs and then benefit from an expected recovery in oil and LNG pricing when the projects come on-stream early in the next decade.

The Company regards the coming year as an ideal time to optimise its portfolio and has the ability to take advantage of acquisition opportunities, should strategic and well-priced assets become available. Oil Search looks forward to an exciting, if challenging, year ahead.

Peter BottenMANAGING DIRECTOR

S t r o n g S T R A T E G I C O U T L O O K c o n t i n u e d

OBJECTIVES for 2016

1. Deliver top quartile operating performance Maximise cash flows from operated production, minimise operating costs and prudently manage capital expenditure.

2. Expand the capacity of the PNG LNG Project and work towards delivering a potential third train Continue to support the operator, ExxonMobil, on further brownfield development of the PNG LNG Project.

3. Work towards delivering the Papua LNG Project Support Total in developing the Papua LNG Project, the next potential world-class LNG development in PNG, including pursuing cooperation and potential integration with the PNG LNG Project.

4. Accumulate high-value resources through exploration Replenish the PNG exploration portfolio through licence acquisition and prepare to drill high-potential wells that, if successful, can support longer-term growth.

5. Manage PNG country risk Continue to invest in activities in PNG that promote a stable operating environment.

6. Proactively manage balance sheet and cost performance Ensure that the Company is able to fund all commitments and prioritise work programmes that can deliver value in a low oil price environment.

7. Ongoing performance improvement deliveryDeliver identified initiatives and seek further productivity improvement opportunities, for delivery in 2016 onwards.

8. Enhance core Oil Search behaviours Demonstrate and strengthen leadership behaviours and ensure an increased commercial focus within all aspects of the business.

OIL SEARCH Annual Report 2015 13

For

per

sona

l use

onl

y

F I N A N C I A L M A N A G E M E N T

in 2015, Oil Search recalibrated its cost structures and implemented enhanced capital discipline throughout the business. This was aimed at ensuring the Company has the capacity to fund its current commitments and its attractive LNG growth projects, while accommodating dividend distributions during a potentially sustained period of low oil prices.

Stephen GardinerChief Financial Officer and Group Secretary

Strong

FINANCIAL PERFORMANCEOil Search reported a net loss of US$39.4 million in 2015 compared to a net profit of US$353.2 million in the previous year. The result included a US$399.3 million after-tax impairment charge due to the write-down of the carrying value of the Taza PSC in Kurdistan to nil. Excluding impairments, core profit was US$359.9 million, compared to US$482.8 million in 2014.

Total revenue was US$1.59 billion, 2% lower than the 2014 result. While sales of oil from operated fields fell 8%, sales of PNG LNG Project LNG more than doubled and condensate and naphtha sales volumes increased 80%, due to a full year of production and higher than anticipated production rates. This was offset by a 32% fall in the average realised LNG and gas price to US$9.44 per mmBtu and a 47% drop in the average realised oil and condensate price to US$51.36 per barrel, reflecting a collapse in global oil and gas prices.

Production costs on a per barrel of oil equivalent (boe) basis declined from US$12.21 per boe in 2014 to US$10.08 per boe in 2015, reflecting lower average PNG LNG Project unit production costs relative to average oil field unit production costs and cost reduction initiatives. Other operating costs increased from US$125.8 million to US$148.9 million, mainly due to higher selling and distribution costs from a full year of LNG sales and one-off restructuring costs. Depreciation and amortisation unit costs increased slightly from US$13.11 per boe in 2014 to US$13.28 per boe in 2015, due to a higher proportion of PNG LNG production.

Exploration costs of US$50.9 million were expensed in 2015, 53% lower than in the previous year. US$37.2 million of this amount related to activities in PNG, including the exploration component of the Hides F1 well, while the remainder was associated with exploration activities in the Middle East and North Africa.

Net interest costs in 2015 were US$185.1 million, 43% higher than in 2014, primarily due to the expensing of a full year of PNG LNG Project borrowing costs.

As mentioned, an impairment charge of US$399.3 million was recognised, related to the Taza PSC in Kurdistan, following a reduction in estimated gross recoverable 2C contingent resources in the field, after the completion of appraisal drilling and testing in 2015. No other impairments were required, with all producing assets assessed against a range of short, medium and long-term oil prices, reflecting the robust economics of Oil Search’s producing assets.

The effective tax rate on 2015 core profit was 29.1%, compared to 36.9% in the previous year. The lower tax rate reflected a higher proportion of revenues which are taxed at the statutory rate for gas of 30% compared to 50% for oil income.

CASH FLOWSNet operating cash flow decreased slightly, from US$992.3 million in 2014 to US$952.7 million in 2015. Net investing cash outflow totalled US$535.6 million, including US$248.3 million spent on exploration and evaluation activities, US$141.6 million on PNG LNG Project development activities and US$119.6 million on PNG production activities.

14

For

per

sona

l use

onl

y

OUTLOOK for 2016

CAPITAL MANAGEMENT AND LIQUIDITYAt the end of 2015, Oil Search had net debt of US$3,318.2 million, comprising cash of US$910.5 million (including US$270.8 million escrowed in PNG LNG Project accounts) and debt of US$4,228.6 million, entirely drawn down from the PNG LNG Project finance facility. Since the PNG LNG Project achieved financial completion in February 2015, US$1.2 billion of cash distributions have been released to the Company. At year end, liquidity totalled US$1.7 billion, including US$748 million available from undrawn corporate revolving facilities. In December, the Company

successfully refinanced two US$125 million bilateral revolving credit facilities through a well-supported competitive bid process.

A 2015 final unfranked dividend of four US cents per share was declared, taking the total unfranked dividend for 2015, including the six cent interim dividend, to 10 US cents per share. This represented a dividend payout ratio of 42%, in line with the Company’s policy of distributing between 35% and 50% of core profit by way of dividends. The Board believes a proportional dividend policy, where dividend payments are aligned with the Company’s profitability, remains appropriate in the current volatile oil price environment.

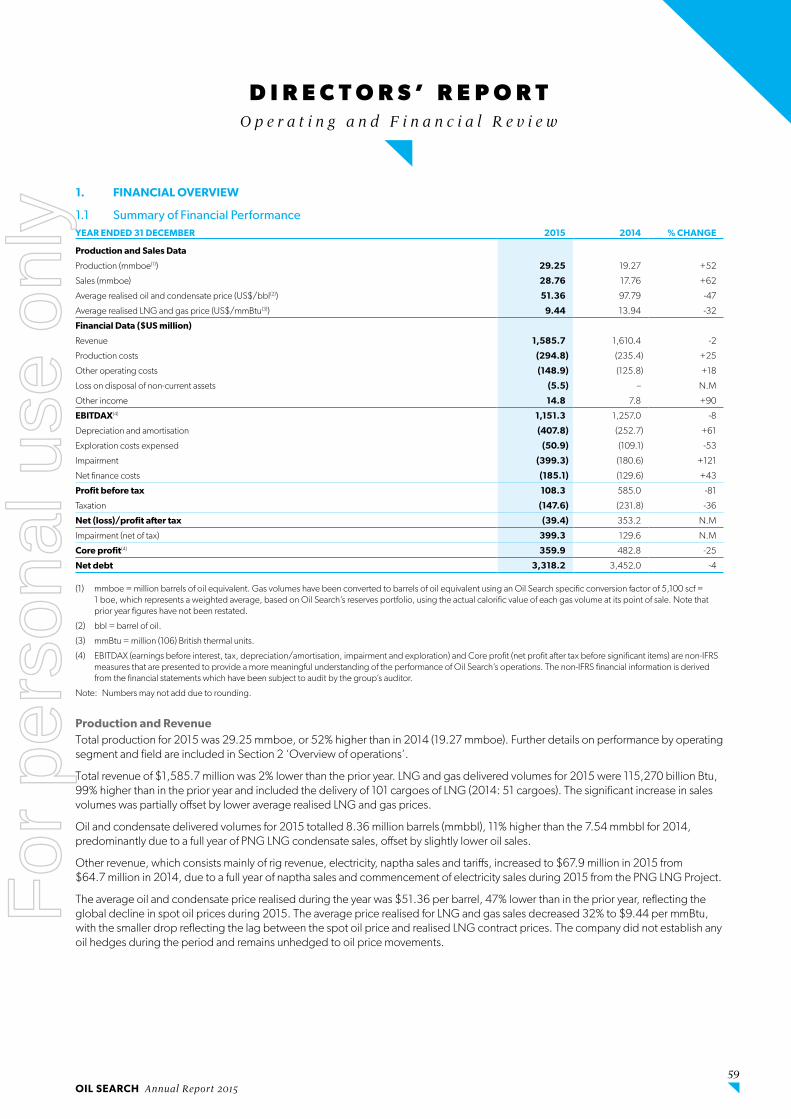

FINANCIAL PERFORMANCE SUMMARYYear to 31 December 2015 2014 % change

Total production mmboe 29.25 19.27 52%

Total sales mmboe 28.76 17.76 62%

Average realised oil and condensate price US$/bbl 51.36 97.79 (47%)

Average realised LNG and gas price US$/mmBtu 9.44 13.94 (32%)

Revenue from operations US$m 1,585.7 1,610.4 (2%)

EBITDAX(1) US$m 1,151.3 1,257.0 (8%)

Depreciation and amortisation US$m (407.8) (252.7) 61%

Exploration costs expensed US$m (50.9) (109.1) (53%)

EBIT(1) US$m 692.6 895.2 (23%)

Net interest income / (expense) US$m (185.1) (129.6) 43%

Impairment loss US$m (399.3) (180.6) 121%

Tax US$m (147.6) (231.8) (36%)

Net profit after tax(2) US$m (39.4) 353.2 (111%)

Impairment (net of tax) US$m 399.3 129.6 208%

Core profit(1) US$m 359.9 482.8 (25%)

Basic EPS(2) US¢/share (2.6) 23.8 (111%)

Basic EPS before significant items US¢/share 23.6 32.6 (27%)

Dividends per share US¢/share 10.0 14.0 (29%)

Operating cash flow US$m 952.7 992.3 (4%)

Net cash / (debt) US$m (3,318.2) (3,452.0) (4%)

(1) EBITDAX (earnings before interest, tax, depreciation/amortisation, impairment and exploration), EBIT (earnings before interest, impairment and tax) and Core Profit are non-IFRS measures that are presented to provide a more meaningful understanding of the performance of Oil Search’s operations. The non-IFRS financial information is unaudited but is derived from the financial statements which have been subject to audit by the Group’s auditor.

(2) Including significant items.

Oil Search enters 2016 in a strong financial position, benefiting from substantial liquidity, a low cost production base and modest sustaining capital requirements. Together with ongoing cash flow from producing assets, the Company has sufficient funds to support all current committed activities, including scheduled debt repayments and the continued judicious investment in its two highly competitive potential LNG growth projects.

In 2016, the Company will continue to drive further efficiencies and reduce costs. Production costs for Oil Search’s operated assets are expected to fall by approximately 25% in 2016, as the benefits of restructuring and cost reductions undertaken in 2015 are fully realised. In addition, total capital spend in 2016 is expected to be approximately 35% lower than in 2015, focused on the Company’s high-returning Highlands and Gulf gas commercialisation activities.

15OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

E X E C U T I V E T E A MStrong

Peter Botten, CBEManaging Director

Peter was appointed Managing Director of Oil Search in 1994. He has extensive worldwide experience in the oil and gas industry, previously holding various senior technical, managerial and board positions in a number of listed and government-owned organisations. He is currently a Council Member of the Australia PNG Business Council, Director of the Oil Search Foundation and Chairman of Business for Development Australia.

Gerea Aopi, CBEExecutive General Manager, Stakeholder Engagement

Gerea was appointed to the Executive Leadership Team in 1998 and joined the Board as an Executive Director in 2006. Prior to joining Oil Search, Gerea was Managing Director of Telikom PNG Ltd, held several very senior positions in the PNG public service and served as the Secretary of the Department of Finance and Planning.

Paul CholakosExecutive General Manager, Technical Services

Paul joined Oil Search in 2010, after more than 25 years’ experience in the international oil and gas and mining industries. He was appointed EGM, Technical Services in 2015, having previously held the roles of EGM, PNG Operations and EGM, Project Development. Paul played a significant part in the Company’s transition to a major LNG exporter through overseeing the Oil Search-operated elements of the PNG LNG Project.

Michael HerrettExecutive General Manager, Human Resources

Michael joined Oil Search in 2012, after more than 30 years with BHP Billiton in senior Human Resources roles, including Vice President positions based in the US, UK and Australia. He has extensive international HR experience, with previous responsibilities covering oil and gas, mining and manufacturing operations in Africa, Latin America, Asia, Australia and the US.

Stephen GardinerChief Financial Officer and Group Secretary

Stephen joined Oil Search in 2004, after a 20-year career in corporate finance at two of Australia’s largest multinational construction materials companies and a major Australian telecommunications company. Stephen was appointed Chief Financial Officer in 2012. Stephen is also the Group Secretary of Oil Search, a role he has held since May 2009.

16

For

per

sona

l use

onl

y

Dr Julian FowlesExecutive General Manager, PNG Business Unit

Julian joined Oil Search in 2012, after a 23-year career with a number of large international oil and gas companies, including 16 years with Shell. His worldwide experience encompasses technical and senior executive management across exploration, development and production operations and new business.

Dr Keiran WulffExecutive General Manager, Exploration and New Business

Keiran re-joined Oil Search in January 2015, having previously worked for the Company between 1995 and 2008. Keiran was formerly Managing Director of Buru Energy Limited and has more than 30 years’ worldwide experience in the oil and gas industry.

Ian MunroExecutive General Manager, Gas Business Development

Ian joined Oil Search in August 2013 to drive growth of the Company’s gas business and deliver opportunities for gas commercialisation. Ian’s career spans more than 27 years in the oil and gas industry, including senior technical and commercial roles at Mobil, ExxonMobil and Woodside Petroleum.

Glenn Darnley-StuartExecutive General Manager, Project Development

Glenn joined Oil Search in 2003, after seven years with Chevron and 20 years in the Australian Army. He spent his first five years with Oil Search as General Manager, PNG Operations, prior to being seconded to ExxonMobil as a Project Manager on the PNG LNG Project based in PNG. Glenn was appointed to the position of EGM, Project Development in early 2013.

17OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

PNG LNG PROJECTIn 2015, the PNG LNG Project contributed 22.2 mmboe net to Oil Search, 76% of the Company’s total production, of which 18.9 mmboe was LNG and 3.3 mmboe liquids (condensate and naphtha).

A number of milestones were celebrated by the Project, operated by ExxonMobil PNG Limited, during 2015. Financial completion was achieved in February 2015, allowing the distribution of Project cash flows to the co-venture partners to commence, the Project marked its first year of production in April 2015 and the 100th cargo was delivered in June 2015.

The Project operated consistently above the nameplate capacity of 6.9 million tonnes per annum (MTPA), averaging 7.4 MTPA in 2015, with facility processing performance improving progressively over

the year. As well as high levels of uptime at the LNG plant, the result was supported by strong upstream deliverability, with an excellent performance from the Hides wells, the Oil Search-operated Associated Gas (AG) fields and the Hides Gas Conditioning Plant (HGCP). Third party gas sales from the Oil Search-operated SE Gobe field commenced in May, adding gas volumes to help support the plant’s expanded capacity. Towards the end of the year, an extended high-rate production test took place to evaluate potential debottlenecking opportunities. It is anticipated that further work to optimise the installed capacity will take place in 2016.

Most importantly, the Project’s strong performance was achieved safely, continuing its record of zero Lost Time Incidents since production began.

P R O D U C T I O N

Total production in 2015 was 29.3 mmboe, 52% higher than in the previous year and an all-time record for the Company. This reflected an outstanding performance by the PNG LNG Project, which operated at an annualised production rate of approximately 7.4 MTPA during 2015, and a stable contribution from the operated PNG oil fields, which was an excellent outcome given their maturity.

Julian Fowles EGM, PNG Business UnitGlenn Darnley-Stuart EGM, Project Development Paul Cholakos EGM, Technical Services

Strong

By the end of 2015, the PNG LNG Project had delivered 156 LNG cargoes since the start of production in 2014.

18

For

per

sona

l use

onl

y

Solid demand for PNG LNG Project gas Since the commencement of exports, the PNG LNG Project has established a reputation as a very reliable gas supplier. The product has been well received by the market, due to its high heating value, which is well suited to the Asian reticulation network, while PNG’s proximity to key Asian LNG markets means shorter shipping times and represents geographical diversification for customers. In 2015, 101 LNG cargoes were sold, of which nearly 80% was sold under the Project’s four long-term sales agreements. The ramp-up of contract sales reached the plateau level of 6.6 MTPA in the fourth quarter of 2015. Good demand was also seen for the Project’s additional volumes, with more than 70% of uncontracted cargoes acquired by the Project’s long-term contract customers and the balance sold to a range of top tier LNG buyers. 31.5 equivalent cargoes of Kutubu Blend, comprising production from the Oil Search-operated PNG oil fields and condensate from the PNG LNG Project, as well as eight cargoes of naphtha from the PNG LNG Project, were also sold.

Ongoing development activities Development drilling activities on the Angore gas field continued during 2015. Two wells, Angore A1 and A2, were completed as future producers. The Hides F1 development well was successfully logged and cased in the Toro reservoir as a future producer for the Project and is expected to be tied into the HGCP in late 2017/2018. Structural mapping to delineate the distribution and volume of gas reserves in the Hides field was undertaken during the year.

Oil Search’s role in gas and liquids delivery to the PNG LNG ProjectDuring 2015, an average of 118 million standard cubic feet per day (mmscf/day) of gas was supplied to the PNG LNG Project by Oil Search from the AG and SE Gobe fields, representing approximately 12% of the total gas delivered to the LNG plant. The Kutubu and Gobe Main fields contributed an average of more than 65 mmscf/d and 30 mmscf/d, respectively, over the year. Third party gas sales from the SE Gobe field to the Project commenced in May at an average rate of more than 30 mmscf/d.

L N G c a r g o e s w e r e

s o l d i n 2 0 1 5

o f t h e P N G L N G

P r o j e c t p r o d u c t i o n

w o r k f o r c e c o m p r i s e d

P N G c i t i z e n s a t

t h e e n d o f 2 0 1 5

l o n g - t e r m

c o n t r a c t c u s t o m e r s :

S i n o p e c ( C h i n a )

T E P C O ( J a p a n )

O s a k a G a s ( J a p a n )

C P C ( T a i w a n )

~80%

4

2015 PRODUCTION SUMMARY(1)

YEAR TO 31 DECEMBER 2015 2014 % Change

GAS PRODUCTION mmscf mmscf Net to OSH

PNG LNG Project LNG(2) 96,646 52,199 +85%

Hides GTE Gas Production(3) 5,312 5,675 -6%

SE Gobe Gas to PNG LNG(4) 1,886 – N/M

Total Gas 103,844 57,874 +79%

OIL AND LIQUIDS PRODUCTION mmbbl mmbbl

Kutubu 3.80 3.69 +3%

Moran 1.56 1.99 -22%

Gobe Main 0.03 0.03 -5%

SE Gobe 0.12 0.13 -8%

SE Mananda – 0.01 N/M

Total Oil 5.51 5.85 -6%

PNG LNG Project Liquids 3.27 1.96 +67%

Hides GTE Liquids(3) 0.11 0.12 -8%

Total Liquids 8.89 7.93 +12%

TOTAL PRODUCTION(5) 29.25 19.27 +52%

(1) Numbers may not add due to rounding.

(2) Production net of fuel, flare, shrinkage and SE Gobe wet gas.

(3) Hides GTE production is reported on a 100% basis for gas and associated liquids purchased by the Hides GTE Project Participant (Oil Search 100%) for processing and sale to the Porgera power station. Sales gas volumes are inclusive of approximately 2% unrecovered process gas.

(4) SE Gobe wet gas reported at inlet to plant, inclusive of fuel, flare and naphtha.

(5) Gas and LNG volumes for 2015 have been converted to barrels of oil equivalent using an Oil Search specific conversion factor of 5,100 scf = 1 boe which represents a weighted average based on Oil Search’s reserves portfolio, using the actual calorific value of each gas volume at its point of sale. Minor variations to the conversion factors may occur over time.

101

19OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

The Oil Search-operated liquids export system, comprising the transportation of liquids through 270 kilometres of pipeline from the Highlands to the Kumul Marine Terminal located offshore in the Gulf of Papua, handled 10.6 mmbbl (approximately 30,000 bbl/d) of condensate from the PNG LNG Project in 2015. A high level of uptime was maintained in the export system during the year and this will remain a focus in 2016.

Oil Search has identified a potentially valuable opportunity to accelerate gas supply to the PNG LNG Project from the Kutubu, Agogo and Moran AG fields, which it operates. As well as providing increased gas delivery flexibility, this would optimise capital investment, bring forward the end of AG field life and reduce the future cost of supporting ageing facilities and wells, in the face of declining oil production. Initial discussions with the PNG LNG Project operator were completed in 2015 and Oil Search has since formed an internal project team which will conduct a feasibility study on this opportunity during 2016.

PNG LNG workforce and business development At the end of 2015, the Project production workforce, including employees and contractors, totalled more than 2,400, of which 79% were PNG citizens. This compared to 3,500 at the end of 2014, as the demobilisation of development personnel continued.

During 2015, the operator provided more than 65,000 hours of training through more than 2,300 training programmes. Also during the year, six Lancos and 200 non-Lanco PNG businesses were contracted by the operator to provide services, including labour hire, maintenance, transportation, security, freight and logistics to the Project. In 2015, the Project spent approximately Kina 515 million (US$182 million) on PNG-based services, including approximately Kina 187 million (US$66 million) spent with Lancos. Since 2010, the PNG LNG Project has generated expenditures of more than Kina 11.5 billion (US$4.5 billion) in-country, including Kina 2.9 billion (US$1.1 billion) with Lancos.

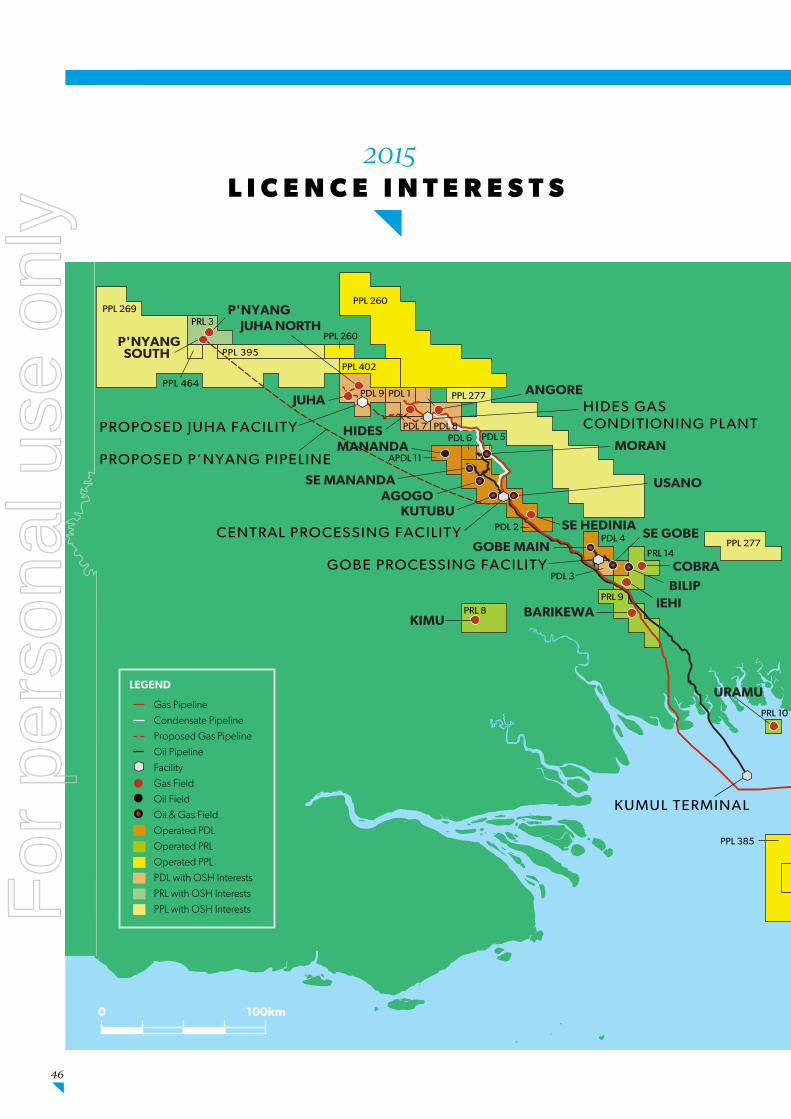

PORT MORESBY

KUMUL TERMINAL

PPL 269PRL 3

PRL 15

PPL 385

PPL 260

PPL 244

PPL 402

PPL 339

PPL 277

PPL 339

PRL 10

PRL 8PRL 9

PRL 14

PDL 4PDL 2

PDL 6

APDL 11

PDL 5

PDL 1

PDL 8

PDL 9

PDL 7

0 100km

PPL 464

PPL 395

PDL 3

Papua New Guinea

BISMARCK SEA

GULF OF PAPUA

PPL 339

PPL 339

PPL 339

PPL 339

PPL 339

PPL 339 PPL 339

PPL 277

PPL 260

ANGORE

HIDES GAS CONDITIONING PLANT

GOBE PROCESSING FACILITY

CENTRAL PROCESSING FACILITY GOBE MAIN

USANOAGOGO

KUTUBU

MORAN

JUHA

HIDESPROPOSED JUHA FACILITY

PNG LNG PLANT

SE GOBE

MANANDA

BILIP

BARIKEWA

SE HEDINIA

HAGANA

FLINDERS

ELK-ANTELOPE

COBRA

P'NYANG

URAMU

P'NYANGSOUTH

IEHIKIMU

JUHA NORTH

SE MANANDA

s u c c e s s r a t e a c h i e v e d

f o r o i l f i e l d d e v e l o p m e n t

w e l l s d r i l l e d s i n c e

O i l S e a r c h c o m m e n c e d

o p e r a t o r s h i p i n 2 0 0 3

~85%

S t r o n g P R O D U C T I O N c o n t i n u e d

LEGEND

Gas Pipeline Condensate Pipeline Proposed Gas Pipeline Oil Pipeline Facility Gas Field Oil Field Oil & Gas Field

OSH non-operated OSH operated PNG LNG Project Gas Fields PNG LNG Project Facilities Non PNG LNG Gas/Oil Fields

Oil Search’s licence interests in PNG.

20

For

per

sona

l use

onl

y

PNG LNG beneficiary identification During 2015, Oil Search continued to support the PNG Government and the operator to progress the PNG LNG Project Landowner Benefits Identification Programme. Royalty payments from the sale of Project LNG and liquids continue to be paid into a Government-nominated trust account with the Bank of Papua New Guinea for future distribution to landowners.

PNG OPERATED OIL AND GAS PRODUCTION In 2015, Oil Search achieved total net operated production of 7.03 mmboe, produced at a gross average rate of 35,165 boepd. This was similar to production in 2014 of 7.08 mmboe, an excellent outcome given the maturity of the fields. Net crude oil production for the year was 5.51 mmbbl, with the Kutubu and Moran fields contributing more than 95% of total oil produced, while gas and liquids production from the Hides Gas-to-Electricity (GTE) Project was 1.15 mmboe and SE Gobe gas sales to the PNG LNG Project contributed 0.37 mmboe. This compared to net oil production of 5.85 mmbbl and gas and liquids production of 1.23 mmboe in 2014.

Production from the Kutubu complex of fields increased 3%, largely due to an excellent performance from the Usano field, where reservoir management strategies developed and implemented in recent years continued to yield material gains in oil production. Production from Usano has increased from approximately 2,000 bopd in mid-2013 to sustained rates of more than 5,500 bopd in 2014 and 2015. At Agogo, production optimisation from three reservoirs accessed via existing backlimb wells and recent development wells in the Agogo forelimb resulted in an average production rate gain of 1,000 bopd compared to the previous year.

At Moran, the Moran 16 ST1 development well encountered oil in the targeted Toro and Digimu reservoirs close to prognosis and was brought online in May at a rate of 1,500 bopd. However, total production was impacted by a number of mechanical issues in the Moran 2X ST2 and NW Moran 1 ST5 wells. Successful sidetracks were undertaken in both wells, which were brought back online late in the year.

Oil production rates at the Gobe Main and SE Gobe fields were maintained at similar levels to 2014, reflecting stable facilities uptime. During the year, gas

exports to the PNG LNG Project ramped up materially, with third party gas sales commencing from SE Gobe in May 2015. Together with gas from Gobe Main, 19.2 billion cubic feet (bcf) gross of gas was exported from the Gobe fields to the PNG LNG Project during the year. The Gobe Processing Facility now exports in excess of 15,000 boepd of oil and gas, compared to approximately 2,000 boepd prior to Gobe Main and SE Gobe gas sales commencing.

Gas sales from the Hides GTE Project to the Porgera Gold Mine fell 6% in 2015. This reflected the impact of a major drought in PNG in the second half of the year, which resulted in a temporary closure of the Porgera mine.

Adding value in a low oil price environmentSince assuming oil field operatorship in 2003, Oil Search has drilled 43 development wells with a success rate of approximately 85%. Over the past four years alone, the Company has added nearly 50 mmbbls of oil (gross) to 1P reserves through high resolution reservoir modelling, development drilling and field management. However, traditional opportunities to extract oil from these mature reservoirs have become commercially challenging in the low oil price environment. In light of this, the Company’s strategy for 2016 is to optimise production from its operated oil fields by driving operating efficiencies through reduced planned downtime and improving reliability through integrated activity planning.

PROCESS SAFETYIn 2015, the Process Safety Improvement Plan (PSIP) focused on updating hazard and operability studies, identifying potential major accident events and using a systematic process to review the current status of controls to prevent them from occurring. Assessment of Oil Search’s producing wells confirmed that all wells are safe and also identified opportunities to further reduce risk. Work also commenced on embedding Oil Search’s approach to managing process safety into the Company’s management system. Once complete, this will help provide assurance that process safety is being properly managed and ensure the gains achieved through the implementation of the PSIP are sustained.

FOCUS ITEMS for 2016

PNG LNG PROJECT

^ Continue to provide a reliable supply of gas from the Kutubu, Gobe Main and SE Gobe fields and ensure a high level of facilities availability from the liquids export system via the Kumul Marine Terminal.

^ Support the Project operator in analysing opportunities for further production optimisation and debottlenecking.

^ Undertake a feasibility study on the potential accelerated gas blow down of the AG fields to the Project.

PNG OPERATED PRODUCTION

^ Enhance production performance through reducing unplanned downtime and improving the reliability of the production facilities.

^ Continue to focus on well integrity and process safety.

2016 PRODUCTION OUTLOOK(1)

Oil Search-operated (PNG oil and gas) 5.7 – 6.2 mmboe(2),(3)

PNG LNG Project

LNG 95 – 100 bcf

Liquids 3.3 – 3.5 mmbbl

Total PNG LNG Project 22 – 23 mmboe(2)

Total production 27.5 – 29.5 mmboe

(1) Numbers may not add due to rounding.

(2) Gas volumes have been converted to barrels of oil equivalent using an Oil Search specific conversion factor of 5,100 scf = 1 boe, which represents a weighted average, based on Oil Search’s reserves portfolio, using the actual calorific value of each gas volume at its point of sale.

(3) Includes 2.8 – 3.0 bcf (net) of SE Gobe gas (OSH – 22.34%) sold to the PNG LNG Project.

21OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

PNG LNG PROJECT EXPANSION

P’nyang gas field MoU signedIn January 2015, ExxonMobil PNG Limited, operator of the PNG LNG Project and PRL 3, and the PNG Government signed a Memorandum of Understanding (MoU) regarding the development of the P’nyang field in PRL 3 (Oil Search – 38.51%). Under the MoU, P’nyang gas will be brought into the PNG LNG Project to support production, including production optimisation and debottlenecking of the existing two trains, a potential third LNG train and the supply of electricity and gas for domestic power. This was a significant milestone for the PRL 3 Joint Venture (JV), as it provided a clear framework for the

award of a Petroleum Development Licence (PDL) for the P’nyang field. In addition, the MoU included a timeline, agreed by the JV and the Government, targeting a final investment decision on a potential third LNG train by the end of 2017.

In line with the MoU, in early 2015, the JV submitted a PDL application for the field to the PNG Government, with work towards the formal award of the PDL continuing during the year. Assisted by logistics support from the JV, the Department of Petroleum and Energy undertook fieldwork to identify project landowners and held information sessions in the project area regarding the development. Additional village-based information sessions, building on a Ministerial determination of eligible

G A S G R O W T H

Gas commercialisation activities in the Highlands and Gulf Province in PNG made significant progress in 2015. PNG LNG Project expansion and the Papua LNG Project have the potential to deliver at least two, and possibly three, additional LNG trains in PNG, which, once on-stream, would double Oil Search’s production. The Company’s extensive gas exploration portfolio in PNG has the potential to support further gas commercialisation.

Ian MunroExecutive General Manager,Gas Business Development

Strong

Co-location of LNG plant sites will allow the opportunity to drive capital efficient expansion, operational synergies and schedule optimisation between the potential PNG LNG Project expansion and the proposed Papua LNG Project.

SPACE AVAILABLE FOR EXPANSION TRAINS

EXISTING PNG LNG PLANT

PROPOSED PAPUA LNG PLANT SITE AT CAUTION BAY

22

For

per

sona

l use

onl

y

P’nyang Gas Field Clans and Villages, are expected to take place in 2016, prior to landowner development forums.

Once the PDL is awarded, the intention is to integrate P’nyang into the PNG LNG Project, to support the proven additional production capacity within the Project’s existing two trains, domestic market opportunities and a potential third train. The incorporation of P’nyang into PNG LNG is regarded as the optimal outcome for all stakeholders. A brownfield development will benefit from the stable and transparent fiscal terms already agreed with the Government, a relatively straightforward expansion of the existing project finance facility to provide debt funding and the use of existing downstream PNG LNG Project infrastructure, significantly reducing development costs. The upstream development of P’nyang will include new gas and liquids pipelines that tie into existing project infrastructure at Kutubu. The pipeline route, which was agreed by the JV in 2015, may help facilitate the development of stranded gas fields in the Western Forelands region.

In April 2015, a key commitment under the MoU was fulfilled, with the execution of a power sale agreement by ExxonMobil, on behalf of the PNG LNG/PRL 3 co-venturers, for the supply of up to 25 megawatts of electricity to PNG Power Limited for use in Port Moresby. Power deliveries from the PNG LNG plant to PNG Power commenced in early July, ensuring a reliable supply of electricity during the Pacific Games and demonstrating the JV’s commitment to the Government and the people of PNG.

Preparatory works for further drilling on the P’nyang field took place during 2015. The objective of this drilling is to allow the reclassification of some of the 2C contingent resources to the 1C category, to support marketing of additional PNG LNG volumes. Oil Search is working closely with the operator, including providing environmental and community expertise and staff and logistics for pad construction. In 2015 and early 2016, Oil Search supported the delivery of community awareness and

a site-specific environmental and social impact assessment of the planned drilling activity. P’nyang South 2, in the south-east of the field and the first of potentially two wells on P’nyang, is presently targeted to spud in the second half of 2016.

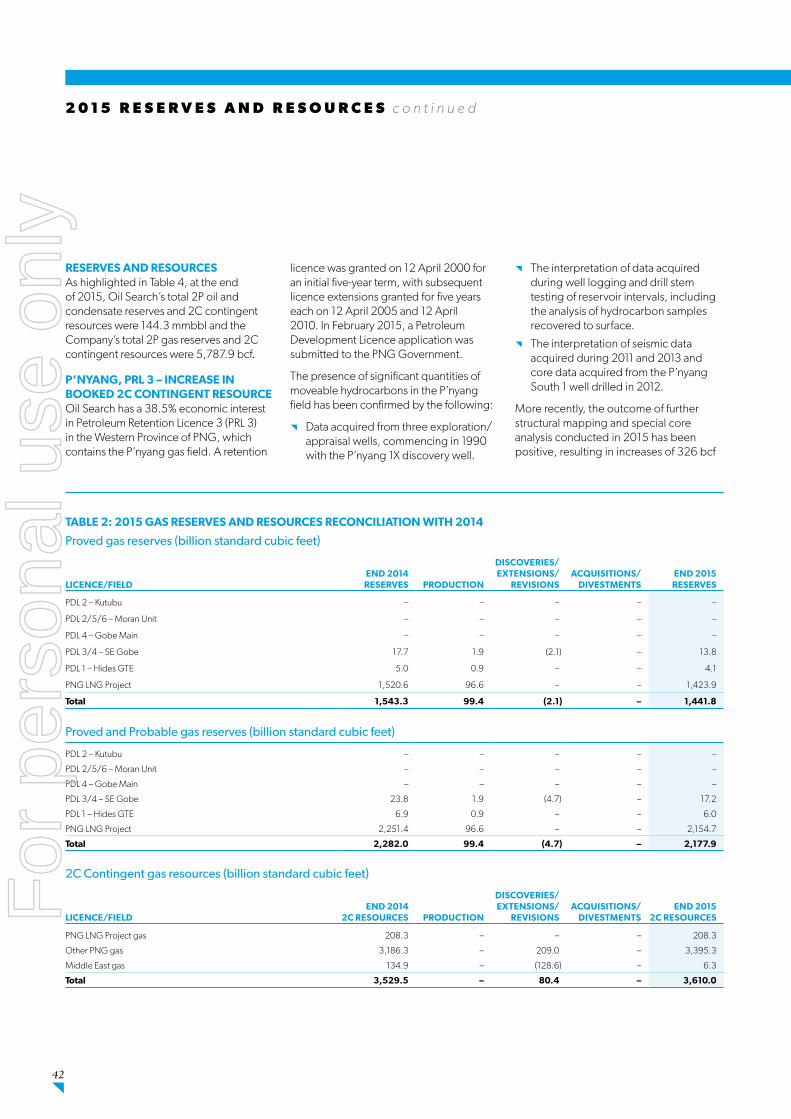

Following the evaluation of new seismic and well data, the Company’s estimate of gross 2C contingent gas resources for the field has increased from 2.6 trillion cubic feet (tcf) to 3.5 tcf. (See 2015 Reserves and Resources for further detail).

PNG LNG Project fields In early 2015, Hides F1 (Hides Deep), a dual development/exploration well, successfully intersected the producing Toro reservoir and was logged and cased as a future producer for the PNG LNG Project. The deeper exploration target, the Koi-Iange interval, was not hydrocarbon bearing and the exploration component abandoned.

Gas resource evaluation activities at Hides, using data obtained from the development wells drilled to date, remain ongoing. The PNG LNG Project participants plan to undertake an independent gas re-certification of Project reserves, including Hides and the AG fields, in 2016, to provide greater certainty regarding the volume of gas available to support high-value PNG LNG expansion.

2016 Highlands drilling campaignIn addition to P’nyang, the 2016 Highlands drilling campaign is planned to include the Muruk 1 exploration well in PPL 402 (Oil Search – 50%, operator), following the completion of the remote rig site. Muruk is a multi-tcf exploration prospect, on-trend with, and located approximately 40 kilometres north-west of, the Hides field. If successful, Muruk could be a potential new source of gas for PNG LNG expansion. (See Strong Exploration Programme section for further detail).

BENEFITS OF PNG LNG PROJECT EXPANSION

^ Stable and transparent fiscal regime agreed with the PNG Government

^ Straightforward expansion of existing US$15.5 billion project finance facility

^ Brownfield development can leverage existing infrastructure and engineering, materially reducing capital requirements and expediting the schedule

O i l S e a r c h ’ s e s t i m a t e

o f g r o s s 2 C c o n t i n g e n t

g a s r e s o u r c e s f o r

P ’ n y a n g h a s i n c r e a s e d

m a t e r i a l l y , f r o m 2 . 6 t c f

3.5tcf

23OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

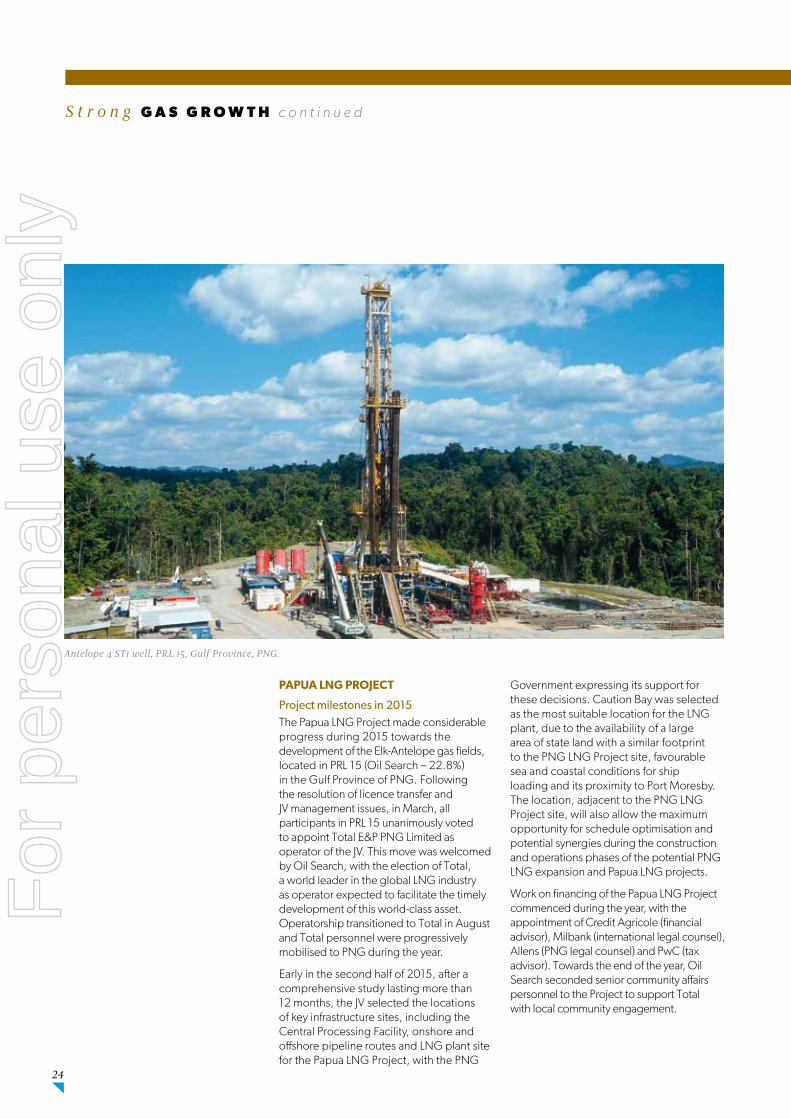

PAPUA LNG PROJECT

Project milestones in 2015The Papua LNG Project made considerable progress during 2015 towards the development of the Elk-Antelope gas fields, located in PRL 15 (Oil Search – 22.8%) in the Gulf Province of PNG. Following the resolution of licence transfer and JV management issues, in March, all participants in PRL 15 unanimously voted to appoint Total E&P PNG Limited as operator of the JV. This move was welcomed by Oil Search, with the election of Total, a world leader in the global LNG industry as operator expected to facilitate the timely development of this world-class asset. Operatorship transitioned to Total in August and Total personnel were progressively mobilised to PNG during the year.

Early in the second half of 2015, after a comprehensive study lasting more than 12 months, the JV selected the locations of key infrastructure sites, including the Central Processing Facility, onshore and offshore pipeline routes and LNG plant site for the Papua LNG Project, with the PNG

Government expressing its support for these decisions. Caution Bay was selected as the most suitable location for the LNG plant, due to the availability of a large area of state land with a similar footprint to the PNG LNG Project site, favourable sea and coastal conditions for ship loading and its proximity to Port Moresby. The location, adjacent to the PNG LNG Project site, will also allow the maximum opportunity for schedule optimisation and potential synergies during the construction and operations phases of the potential PNG LNG expansion and Papua LNG projects.

Work on financing of the Papua LNG Project commenced during the year, with the appointment of Credit Agricole (financial advisor), Milbank (international legal counsel), Allens (PNG legal counsel) and PwC (tax advisor). Towards the end of the year, Oil Search seconded senior community affairs personnel to the Project to support Total with local community engagement.

S t r o n g G A S G R O W T H c o n t i n u e d

Antelope 4 ST1 well, PRL 15, Gulf Province, PNG.

24

For

per

sona

l use

onl

y

Encouraging appraisal results to dateDuring the year, two appraisal wells, Antelope 4 ST1, located at the southern margin of the field, and Antelope 5, on the western flank, were drilled. The well results confirmed that the high quality carbonate reservoir extends to the south and west of the structure. In June, an extended well test of Antelope 5 confirmed a substantial resource base, excellent reservoir quality and deliverability and demonstrated strong pressure communication between the Antelope 5 and Antelope 1 wells. Shortly after the end of the year, a second production test of Antelope 5, with observation of pressure movements at Antelope 1, was conducted. Preliminary analysis has confirmed the excellent reservoir quality and strong connectivity seen in the initial production test, with further analysis underway to quantify reservoir properties.

Antelope 6, located two kilometres east-southeast of Antelope 3, spudded in late December. The well, which is expected to reach total depth during the first quarter of 2016, is designed to appraise the eastern extent of the structure close to the gas-water contact. A further appraisal well, Antelope 7, to assess potential resource upside to the west of the currently-mapped field, is under consideration by the JV for drilling in the second half of 2016. A decision on the well will be made once the results of Antelope 6 drilling and Antelope 5 testing are evaluated.

Preliminary interpretation of the Antelope 4, Antelope 4 ST1 and Antelope 5 appraisal well results and seismic reprocessing has been positive and, subject to completion of appraisal drilling, Oil Search’s estimate of the gross 2C contingent resource could increase from the currently booked 5.3 tcf of raw gas. Given this, Oil Search remains confident that the Elk-Antelope fields have sufficient gas resources to underpin at least one 5 MTPA LNG train and, depending on the outcome of the appraisal programme, potentially two smaller-sized trains.

Certification of PRL 15Preparations for independent gas certification of the Elk-Antelope fields commenced in 2015, in line with the agreement between Oil Search and the sellers of the Pac LNG Group Companies relating to the Company’s acquisition of its interest in PRL 15. Two world-class certifiers, Netherland Sewell and Associates and Gaffney Cline and Associates, have been engaged. The certification commenced in the first quarter of 2016, with results anticipated around mid-year.

Completion of the appraisal programme and confirmation of the resource size will enable the selection of the final development concept, including the sizing and capacity of upstream and downstream facilities. This development concept will determine the Basis of Design, including a decision on the number of LNG trains, followed by entry into Front End Engineering and Design, with Oil Search anticipating a Final Investment Decision on the Project in 2018.

S t r o n g G A S G R O W T H c o n t i n u e d

BENEFITS OF THE PAPUA LNG PROJECT

^ Proximity of the Elk-Antelope fields to:

The Purari River, enabling cost-effective transport of equipment and people to site

The LNG plant site, with approximately a 330 kilometre pipeline required

^ Relatively flat up-stream terrain

^ Location of the LNG plant adjacent to the PNG LNG Project site, providing the opportunity for potential integration and cooperation with PNG LNG

Location of key infrastructure sites for the proposed Papua LNG Project.

PORT MORESBY

PPL 269PRL 3

PRL 15

PPL 260

PPL 402

PPL 277

PRL 14

PDL 4PDL 2

PDL 6

APDL 11

PDL 5

PDL 1

PDL 8

PDL 9

PDL 7

0 100km

PPL 464

PPL 395

PDL 3

Papua New Guinea

BISMARCK SEA

GULF OF PAPUA

PPL 260

KEREMA

0 100km

PROPOSED CENTRAL PROCESSING FACILITY

PROPOSED PLANT LOCATION

PROPOSED PIPELINE ROUTEPNG LNG PIPELINE

ELK-ANTELOPE GAS FIELDS

PNG LNG PLANT

25OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

S t r o n g G A S G R O W T H c o n t i n u e d

MAXIMISING THE VALUE OF THE NEXT PHASE OF LNG DEVELOPMENT IN PNG Oil Search believes that there is an excellent opportunity to maximise the value of the potential PNG LNG Project expansion and the proposed Papua LNG Project through cooperation and integration. The use of existing infrastructure and the co-location of plant sites would help drive capital efficient investment, cost and operational synergies and schedule acceleration, maximising returns for all stakeholders, including the PNG Government, landowners and co-venturers. Generating maximum shared value through working together is particularly important if there is an extended period of low oil and gas prices.

With equity interests in the North-West Highlands and Gulf Province gas hubs and existing resource infrastructure in PNG, Oil Search is in a unique position to play a lead role in gas commercialisation activities, to ensure the most cost-effective development of future LNG trains. The Company intends to leverage its superior in-country operating experience, strong Government, community and landowner relationships, PNG basin expertise and experience gained from the PNG LNG Project to support operators, ExxonMobil and Total, and to promote a cooperative agenda for the next phase of LNG development in PNG.

DEMAND FOR LNG FROM PNG The global LNG market is becoming increasingly competitive, due to a range of new projects in Australia coming on-stream and the emergence of the US as a significant new gas exporter. Based on current forecasts, the LNG market appears well supplied until the end of this decade. However, early in the next decade, demand is expected to surpass contracted supply, particularly in the Asia Pacific region. This reflects the expiry of several existing long-term contracts and the expected deferral or delay of sanctioning of a number of proposed projects due to challenging economics at current low prices. Oil Search believes that this will provide a market window for the potential third PNG LNG train and the proposed Papua LNG Project, allowing these high heating value gas projects to secure premium Asian markets.

Given the sharp decline in oil and gas prices, only low cost projects are likely to proceed to development in the short-to-medium term. Both the potential third PNG LNG train and the Papua LNG Project continue to offer the prospect of attractive returns, despite the present oil price weakness. This view is supported by a range of independent experts, which rank these two projects as among the most commercially attractive globally and therefore the most likely to be sanctioned in the next two to three years.

MIDDLE EAST

N AMERICA

S AMERICA

SW EUROPE

NW EUROPE

ASEAN

JAPAN KOREA MARKER COUNTRIES

INDIA

CHINA

TOTAL LNG DEMAND

Source: Wood Mackenzie, LNG Tool, Dec ‘15

GLOBAL LNG DEMAND V CONTRACTED SUPPLY

2000 2005 2010 2015 2020 2025 2030 2035

600

500

400

300

200

100

0

MTP

A

26

For

per

sona

l use

onl

y

PNG POWER INITIATIVES Oil Search believes that the delivery of reliable, competitively priced power is a political and social priority in PNG and an important aspect of maintaining a stable operating environment. In 2015, the Company worked closely with the PNG Government and Government-owned PNG Power Ltd (PPL) on the Ramu Power Project, a multi-phase long-term power delivery project which aims to provide up to 100 megawatts (MW) of additional electricity generating capacity and to connect up to one million people to a larger and improved electricity grid by 2030.

The first phase of the Ramu Power Project was completed in April, with the upgrade and provision of diesel to PPL’s power plant in Tari, enabling the commencement of continuous 24-hour power supply in the town. In September, Oil Search signed a statement of intent with PPL on the next phases of the Ramu Power Project, which was followed by the signing of two Power Purchase Agreements (PPAs) – the PNG Biomass Independent Power Producer

(IPP) PPA and the Highlands IPP PPA – with PPL in December.

Under the Biomass PPA, PNG Biomass IPP (Oil Search – 70%) will use wood chips, primarily sourced from new plantation trees grown and harvested in the Markham Valley, to deliver up to 30 MW of biomass-fired baseload power for the Ramu Grid. The Highlands PPA involves the construction by Highlands IPP (Oil Search – 100%), of an initial 2 MW gas-fired pilot power project located near Hides in the Hela Province, with potential to ramp up to 5 MW in the short-term and up to 65 MW by 2030. Subject to the execution of a binding gas supply agreement, the Highlands IPP is designed to provide cost-effective baseload, peaking and back-up power to the Hela and Southern Highlands Provinces.

These activities are complementary to the power initiatives being undertaken by the PNG LNG Project on behalf of the co-venturers.

S t r o n g G A S G R O W T H c o n t i n u e d

FOCUS ITEMS for 2016

PNG LNG PROJECT EXPANSION

^ Obtain a PDL over the P’nyang field, followed by the integration of P’nyang into the PNG LNG Project.

^ Prepare to drill the Muruk 1 exploration well, the P’nyang South 2 well and evaluate a potential second P’nyang well.

PAPUA LNG PROJECT

^ Complete drilling and testing of the Antelope 6 appraisal well.

^ Determine whether to drill the Antelope 7 appraisal well.

^ Complete the Oil Search resource certification of the Elk-Antelope fields.

^ Select the final development concept for Papua LNG and confirm the Basis of Design.

k e y p o w e r

i n i t i a t i v e s e n t e r e d

i n t o d u r i n g 2 0 1 5

3

Oil Search’s partnership with PNG Power Ltd in the Ramu Power Project seeks to bring together the best of public and private enterprise skills.

27OIL SEARCH Annual Report 2015

For

per

sona

l use

onl

y

PNG GAS EXPLORATIONIn 2015, Oil Search undertook a detailed review of PNG’s hydrocarbon basins, which confirmed that there is significant exploration upside, particularly for gas, with an estimated 5 billion barrels of oil equivalent yet to be found (YTF) (1),(2). A systematic exploration and appraisal programme targeting 5 – 6 tcf of unrisked gas resources commenced in 2015, with the acquisition of 194 kilometres of 2D seismic and preparations to commence drilling in 2016. In addition, as part of a strategic expansion and high-grading of its PNG acreage portfolio, in 2015 Oil Search entered three new exploration licences, PPL 269 and PPL 402 in the Highlands and PPL 339 in the Gulf, and submitted eight new licence applications, the majority in conjunction with its major LNG project partners, ExxonMobil and Total.

North-West HighlandsOil Search has identified 3 – 4 tcf (3) of mean gross prospective resources in the North-West Highlands, including the high-potential Muruk exploration prospect in PPL 402 and Strickland prospect in PPL 269.

In 2015, Oil Search acquired a 100% interest in PPL 402(4), located north of the Juha and Hides fields. During the year, 102 kilometres of 2D seismic data was acquired in this and adjacent licences. Processing and interpretation of the seismic has matured the Muruk exploration prospect in PPL 402. Muruk 1, which is expected to spud in 2016, subject to well pad completion, is a multi-tcf exploration prospect, located close to the existing PNG LNG fields. Operated by Oil Search, the Muruk 1 well will target gas in the Toro reservoir and, should it be successful, could provide a new source of gas for PNG LNG

E X P L O R A T I O N P R O G R A M M E

Oil Search recognises that it is essential to invest in exploration through the oil price cycle, to ensure that the Company has an ongoing pipeline of future growth opportunities. The current period of low oil prices presents an opportunity for Oil Search to optimise its portfolio and tighten its focus on PNG, particularly on exploration activities that will support the ongoing commercialisation of gas.

Keiran WulffExecutive General Manager,Exploration and New Business

Strong

Seismic acquisition in the PNG Highlands.

28

For

per

sona

l use

onl

y

Project expansion. Oil Search estimates that Muruk 1 has approximately a 20% chance of success.

During the year, Oil Search finalised the acquisition of a 10% interest in PPL 269. The operator, Repsol, completed a 72 kilometre 2D seismic programme in the licence and matured the Strickland prospect, located west of the Juha field, for drilling. The Strickland exploration wells are expected to spud in the second quarter of 2016, targeting gas in the Darai limestone and in the Toro Formation sandstone reservoir. The Darai limestone represents a new play in this part of PNG. Oil Search believes the primary Toro target has approximately a 25% chance of success.

Gulf and Forelands Oil Search has identified an estimated 1 tcf (5) of mean gross prospective gas resources and appraisal upside of approximately 1 tcf of gross 2C resources in existing discovered gas fields in the Gulf and Forelands regions.

In May, Oil Search exercised its option with Kina Petroleum Limited to farm into a 70% interest(6) in PPL 339 in the Gulf

Province, following indications from high resolution gravity, magnetic and 2D seismic data of potentially prospective structures. This included the identification of the Kalangar prospect, located in the Eastern Papuan Basin, which is on-trend with the Antelope field and believed to be an Antelope-lookalike, carbonate build-up. The Kalangar 1 exploration well is expected to be drilled during the dry weather window in early 2017. Kalangar is assessed to have approximately a 15% chance of success. If the results are positive, Kalangar will open up an important and new prospective trend in the Gulf Province.

Preparatory work continued for appraisal of the existing gas discoveries in PRL 8 (Kimu), PRL 9 (Barikewa) and PRL 10 (Uramu) in the Gulf and Forelands regions. Reassessment and remapping of the discoveries has indicated potentially material 2C gas resource upside, which will be confirmed by appraisal drilling planned for 2016/2017. The drilling programme is expected to commence with the Barikewa 3 well in PRL 9 (Oil Search – 45.1%, operator) in late 2016/early 2017.

PORT MORESBY

PPL 269PRL 3

PRL 15