Embed Size (px)

Citation preview

StretchPayStretchPay

The Credit Union Salary Advance The Credit Union Salary Advance Loan AlternativeLoan Alternative

Presented By: Doug Fecher, Presented By: Doug Fecher, President/CEO Wright-Patt CUPresident/CEO Wright-Patt CU

StretchPayStretchPay

What is it?What is it?

A special line-of-credit loan A special line-of-credit loan designed to make it easy and designed to make it easy and less expensive for members to less expensive for members to get short term credit. get short term credit.

How StretchPay BeganHow StretchPay Began

Outgrowth of City of Dayton Public Outgrowth of City of Dayton Public Meeting on Payday Lenders in 2000.Meeting on Payday Lenders in 2000.

Public Statement: “If you take away Public Statement: “If you take away the payday lenders, we’ll have the payday lenders, we’ll have nowhere to go when we need cash.”nowhere to go when we need cash.”

Public Statement: “We can’t go to Public Statement: “We can’t go to our credit union … they’ll turn us our credit union … they’ll turn us down just like the banks.”down just like the banks.”

The Public Was Right!The Public Was Right!

Credit Unions don’t make Credit Unions don’t make short term, low dollar short term, low dollar

loans to the credit-loans to the credit-impaired.impaired.

StretchPay Initial PrinciplesStretchPay Initial PrinciplesMake it as much like a payday loan Make it as much like a payday loan as possible. This means:as possible. This means:

Limited credit check.Limited credit check.No payroll deduction requirement.No payroll deduction requirement.Fast and easy to make advances.Fast and easy to make advances.

But: Make it more affordable for But: Make it more affordable for members, with better repayment members, with better repayment terms, and breakeven for the Credit terms, and breakeven for the Credit Union.Union.

StretchPay Initial PrinciplesStretchPay Initial Principles A line-of-credit (to reduce the A line-of-credit (to reduce the

costs of making advances) with costs of making advances) with one distinguishing feature: one distinguishing feature: Advances must be repaid in full Advances must be repaid in full before a new advance can be before a new advance can be taken.taken.

Interest rate of 18% ($3/month).Interest rate of 18% ($3/month). Maximum draw amount of $250.Maximum draw amount of $250. Must be repaid in full in 30-days.Must be repaid in full in 30-days.

StretchPay EvolutionStretchPay Evolution

Tested a no fee model, a $25 Tested a no fee model, a $25 annual fee model, and settled on annual fee model, and settled on $35 annual fee…$35 annual fee…

Developed pilot program with 11 Developed pilot program with 11 southwestern Ohio CUs to test southwestern Ohio CUs to test risk-sharing concept and risk-sharing concept and compete with Payday Lending compete with Payday Lending footprint…footprint…

““Fund” grew to over $50,000Fund” grew to over $50,000

StretchPay TodayStretchPay Today

Borrowers pay a $35 annual Borrowers pay a $35 annual fee for a $250 line-of-credit, fee for a $250 line-of-credit, and a $70 fee for a $500 line-and a $70 fee for a $500 line-of-credit…and 18% interest of-credit…and 18% interest on their advances. on their advances.

One Important Difference One Important Difference from Traditional Payday from Traditional Payday

Loans …Loans …

A borrower must repay their A borrower must repay their entire outstanding balance entire outstanding balance (plus interest) before any (plus interest) before any more advances are more advances are permitted.permitted.

A traditional payday A traditional payday lender might charge lender might charge $15/$100 borrowed $15/$100 borrowed for as little as a two for as little as a two week term.week term.

In other words . . .In other words . . .

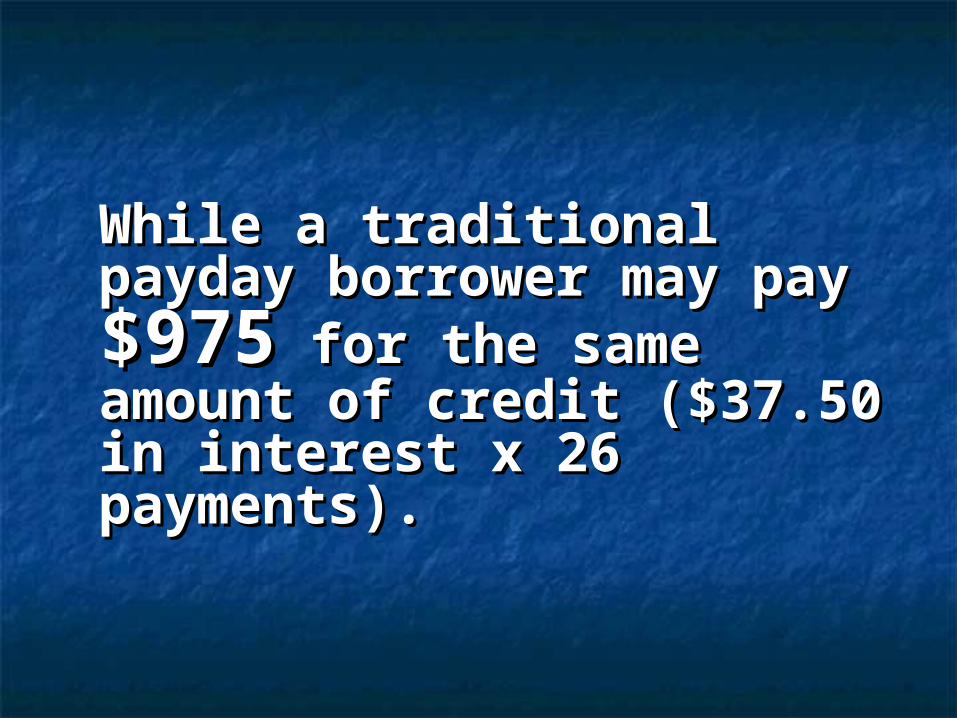

A StretchPay borrower A StretchPay borrower who takes 12 advances who takes 12 advances on a $250 line-of-credit on a $250 line-of-credit will pay approximately will pay approximately $77 in fees.$77 in fees.

While a traditional While a traditional payday borrower may payday borrower may pay pay $975$975 for the same for the same amount of credit ($37.50 amount of credit ($37.50 in interest x 26 in interest x 26 payments).payments).

StretchPay EvolutionStretchPay Evolution

Successful program that is being Successful program that is being expanded nationwide…expanded nationwide…

Supported by Filene REAL Supported by Filene REAL Solutions and Ohio Credit Union Solutions and Ohio Credit Union League…League…

Formed a CUSO to facilitate the Formed a CUSO to facilitate the risk-sharing and nationwide risk-sharing and nationwide implementation…implementation…

The CUSOThe CUSOCCredit unions offer redit unions offer StretchPay lines-of-credit StretchPay lines-of-credit in association with a non-in association with a non-profit CUSO called Credit profit CUSO called Credit Union Outreach Solutions, Union Outreach Solutions, Inc. (CUOSI).Inc. (CUOSI).

The CUSOThe CUSO

Each time you collect an Each time you collect an annual fee from a annual fee from a StretchPay borrower, you StretchPay borrower, you forward the fee to the forward the fee to the CUSO, which will, in turn, CUSO, which will, in turn, help your CU offset any help your CU offset any credit losses sustained credit losses sustained under the program.under the program.

Reimbursement for Reimbursement for Charged-Off LoansCharged-Off Loans

The CUSO will reimburse the The CUSO will reimburse the credit union for 90% of the credit credit union for 90% of the credit union’s losses.union’s losses.

10% coverage by the CU creates 10% coverage by the CU creates risk-sharing and encourages CUs risk-sharing and encourages CUs to make reasonable efforts to to make reasonable efforts to

collect on their lossescollect on their losses..

In other words …In other words …

You can offer members an You can offer members an alternative to payday alternative to payday lenders without incurring lenders without incurring the credit risk associated the credit risk associated with small dollar, with small dollar, minimally underwritten minimally underwritten loans.loans.

Minimal Underwriting Minimal Underwriting CriteriaCriteria

An applicant must …An applicant must …

Be a CU Member for at Be a CU Member for at least 60 days and not be least 60 days and not be delinquent on existing delinquent on existing loans or negative in any loans or negative in any share account.share account.

Minimal Underwriting Minimal Underwriting CriteriaCriteria

An applicant must …An applicant must …

Be at least 18 years old.Be at least 18 years old.

Minimal Underwriting Minimal Underwriting CriteriaCriteria

An applicant must …An applicant must …

Have verified income, not Have verified income, not be in the process of filing be in the process of filing for bankruptcy and not for bankruptcy and not caused any participating caused any participating CU a loss.CU a loss.

Specifics on StretchPay Specifics on StretchPay LoansLoans

Credit limits/minimum Credit limits/minimum advances -$250 ($35 annual advances -$250 ($35 annual fee) fee)

-$500 ($70 annual fee)-$500 ($70 annual fee)

30-Day Repayment Term30-Day Repayment Term

Specifics on StretchPay Specifics on StretchPay LoansLoans

Advances must be paid in full prior Advances must be paid in full prior to new/additional advances.to new/additional advances.

18% Interest Rate (or the maximum 18% Interest Rate (or the maximum permitted by applicable law, permitted by applicable law, whichever is lower).whichever is lower).

Payroll deduction is encouraged, Payroll deduction is encouraged, but not required.but not required.

Results to DateResults to Date

16 Ohio credit unions (and the 16 Ohio credit unions (and the Ohio League) belong to the Ohio League) belong to the StretchPay CUSO.StretchPay CUSO.

Over 35 credit unions (from Over 35 credit unions (from across the nation) and seven across the nation) and seven additional Leagues are additional Leagues are considering participation.considering participation.

Results to DateResults to Date

$93,000 in Membership Fees$93,000 in Membership Fees $40,000 left in fund from Pilot$40,000 left in fund from Pilot $51,000 fees collected YTD$51,000 fees collected YTD 14,000 Losses YTD 14,000 Losses YTD $171,000 in Fund Balance$171,000 in Fund Balance

To Join the ProgramTo Join the Program

Step One …Step One …

Obtain Approval from Obtain Approval from your Board of Directors.your Board of Directors.

To Join the ProgramTo Join the Program

Step Two …Step Two …

Join the CUOSI by signing Join the CUOSI by signing the membership the membership agreements and paying a agreements and paying a membership fee.membership fee.

The Membership FeeThe Membership Fee

CU pays a fee of $25 per $1 CU pays a fee of $25 per $1 million in assets, with a million in assets, with a maximum fee of $15,000. maximum fee of $15,000.

The fee is not an investment in The fee is not an investment in the CUSO, and should be the CUSO, and should be expensed on the CU’s books.expensed on the CU’s books.

To Join the ProgramTo Join the Program

Step Three …Step Three …

Adopt a StretchPay Loan Adopt a StretchPay Loan Policy and Procedure (a model Policy and Procedure (a model P&P will be provided for P&P will be provided for adoption by your credit adoption by your credit union).union).

To Join the ProgramTo Join the Program

Step Four …Step Four …

Set StretchPay up on your Set StretchPay up on your Data Processing System.Data Processing System.

To Join the ProgramTo Join the Program

Step Five …Step Five …

Set up StretchPay Documents Set up StretchPay Documents (line-of-credit app, note, (line-of-credit app, note, agreement, T-I-L disclosure, agreement, T-I-L disclosure, closing letter and monthly closing letter and monthly remittance form).remittance form).

To Join the ProgramTo Join the Program

Step Six …Step Six …

Train employees on the Train employees on the StretchPay Program.StretchPay Program.

To Join the ProgramTo Join the Program

Step Seven …Step Seven …

Set up the Monthly Set up the Monthly Accounting System for Accounting System for fees and loss recovery.fees and loss recovery.

To Join the ProgramTo Join the Program

Step Eight …Step Eight …

Set up a Collection Effort Set up a Collection Effort Program.Program.

To Join the ProgramTo Join the Program

Step Nine …Step Nine …

Market the Program.Market the Program.

To Join the ProgramTo Join the Program

Step Ten …Step Ten …

Offer the StretchPay Offer the StretchPay Program to your Members.Program to your Members.

Frequently Asked Frequently Asked QuestionsQuestions

““Is a CU required to offer both a Is a CU required to offer both a $250 and $500 line of credit?”$250 and $500 line of credit?”

No. A CU may offer the $250 No. A CU may offer the $250 credit line, the $500 credit line, credit line, the $500 credit line, or both.or both.

Frequently Asked Frequently Asked QuestionsQuestions

““Is there a minimum Is there a minimum income requirement for a income requirement for a member to open a member to open a StretchPay line-of-credit?”StretchPay line-of-credit?”

Not at this time.Not at this time.

Frequently Asked Frequently Asked QuestionsQuestions

““Is a checking account Is a checking account required to open a required to open a StretchPay line-of-credit?”StretchPay line-of-credit?”

Not system-wide, but each Not system-wide, but each CU has the option of having CU has the option of having such a requirement.such a requirement.

Frequently Asked Frequently Asked QuestionsQuestions

““How are comments regarding the How are comments regarding the operation of the CUSO, or the operation of the CUSO, or the StretchPay product, made to the StretchPay product, made to the CUSO?”CUSO?”

An Advisory Council (made up of all An Advisory Council (made up of all StretchPay CUs and some League StretchPay CUs and some League Reps) will meet regularly by Reps) will meet regularly by conference call to discuss these issues.conference call to discuss these issues.

Frequently Asked Frequently Asked QuestionsQuestions

““Would I receive help in marketing Would I receive help in marketing the program to my membership?”the program to my membership?”

Marketing materials have already Marketing materials have already been developed and will be made been developed and will be made available for participating credit available for participating credit unions --- CU would only pay unions --- CU would only pay printing costs and for printing costs and for customization.customization.

If you are interested . . If you are interested . . ..

Contact John Florian at Contact John Florian at [email protected]@ohiocul.org to receive to receive sample operating and product sample operating and product agreements, as well as an agreements, as well as an implementation guide that implementation guide that includes a program overview. includes a program overview.

Contact Information for Contact Information for Doug Fecher . . .Doug Fecher . . .

Doug Fecher, President/CEO Doug Fecher, President/CEO

Wright-Patt Credit UnionWright-Patt Credit Union

[email protected]@wpcu.coop

937-912-7394 937-912-7394