Embed Size (px)

Citation preview

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

Top ten listed companies by market capitalization

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 NOW

TLKM TLKM TLKM TLKM ASII ASII ASII ASII BBCA HMSP HMSP TLKM ASII BUMI BBCA ASII TLKM BBCA HMSP HMSP HMSP BBCA TLKM BBCA

BBCA ASII UNVR BBCA BBCA HMSP BBCA BBCA ASII UNVR BBCA HMSP BBRI VALE BBRI BMRI BMRI BBRI BMRI TLKM TLKM TLKM ASII UNVR BMRI BBRI PGAS PGAS BBRI BMRI TLKM UNVR BBRI ASII UNVR BBRI PGAS BBCA ASII BBRI UNVR UNVR BBRI BMRI BMRI BBRI BBRI ASII UNVR BMRI BMRI UNVR HMSP TLKM UNVR BBRI UNVR BMRI BMRI BMRI HMSP PGAS HMSP ADRO PGAS GGRM PGAS PGAS PGAS GGRM GGRM GGRM ISAT HMSP ISAT UNTR ADRO UNTR GGRM SMGR GGRM BBNI BBNI BBNI

BDMN UNVR SMGR ICBP UNTR PGAS SMGR GGRM BBNI ICBP ICBP UNTR Source: Mirae Asset Sekuritas Indonesia Research

Note: Color represented by red (utilities), yellow (consumer discretionary), blue (financials), and green (consumer staples)

Strategy Focus Good things come to those who endure

Enduring the pain…

Market is trending sideways after a robust rally since the beginning of the year. We believe investors have begun to reassess the 1) long-term fundamental story of Indonesia’s consumption growth, 2) government's infrastructure development pledges, 3) commodity market outlook, and 4) escalating political risks.

…however, earnings growth still remains exciting Corporate earnings are still in their expansion mode as LQ45 companies’ net profits have come in at IDR51.2tr (+17.4% YoY). We believe a benign macro backdrop combined with favorable policy settings, have placed positive implications on corporate earnings. Heading into 2H17, we expect low probabilities of external shocks rocking our base case macro scenario. Further, we anticipate policy settings to remain supportive of continued earnings expansion.

We prefer banks, telco, healthcare, petrochem and developers We believe risk bias remains moderate. However, we believe investor appetite is undergoing a transitional shift. Our preferred sectors are: 1) financials (banks)—supportive macro backdrop is expected to ease provisioning burden on banks, 2) utilities (telco)—strong bargaining power over users and ample organic growth opportunities, 3) consumers (healthcare)—we still like the basic consumption growth story of Indonesia, but our view is now limited to consumers with online expansion capabilities, 4) basic industry (petrochem)—for the favorable supply and demand profile of petrochemical products, and 5) property (developers)—on the back of supportive policy measures, which should act as strong price catalysts.

Where do we go from here? We do not believe headwinds will turn into tailwinds. In addition, as we march closer to the 2019 presidential race, we expect to see more growth-oriented policies introduced by the administration—which should present a good upward boost to economic growth and corporate earnings. Bottom line, we retain our JCI target of 6,241pt for 2017F. Our five key calls are Bank Central Asia (BBCA), Telekomunikasi Indonesia (TLKM), Kalbe Farma (KLBF), Barito Pacific (BRPT), and Bumi Serpong Damai (BSDE).

Strategy Focus August 25, 2017

PT. Mirae Asset Sekuritas Indonesia Strategy Taye Shim +62-21-515-3281 [email protected]

Strategy Focus

2

August 25, 2017

Mirae Asset Daewoo Research

Time to cool down

Manufacturing vs. commodities

From a global market perspective, emerging markets (EM) have outperformed the developed markets (DM) year-to-date. At the center of this diverged performance is China—a country which aims to steer its economy away from manufacturing. At the same time, China is currently grappling with internal issues, such as soft landing its dinosaur economy and external issues related to escalating geopolitical risks. In the process, we notice that manufacturing EM economies (such as Korea, Vietnam, and Taiwan) have exhibited solid growth in both earnings and prices. On the other hand, commodities-driven EM economies (such as Indonesia and Malaysia) have been far from investors’ attention.

Figure 1. Price performance by countries (YTD) Figure 2. Quarterly earnings (RoE) trend

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research Note: Price as of Aug 23 close

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Rebalancing of risks: Foreigners selling equities but not bonds

Foreign investors have been selling off equities since May while maintaining their position in the fixed income space. We judge foreign investors have begun to unwind their risk positions as they look at Indonesia’s economic growth outlook with skepticism. As a quick reminder, 1Q17 GDP growth (5.0% YoY; released in May) fell below market expectations, and so did 2Q17 growth figures.

Figure 3. Foreign investors have been selling equities since May (post disappointing 1Q17 GDP release)…

Figure 4. …however, positions in fixed income remains largely unchanged

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: Ministry of Finance, Mirae Asset Sekuritas Indonesia Research

5

7

9

11

13

15

17

2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

KOSPI

JCI

FBMKLCI

VNIDEX

SHCOMP

(%)

30

32

34

36

38

40

300

400

500

600

700

800

900

1/14 7/14 1/15 7/15 1/16 7/16 1/17 7/17

Outstanding balance of gov. bond owned by foreigners (L)

Foreign ownership (R)

(IDRtr) (%)

10.9

24.7

9.2

12.4

17.0

3.4

6.0 5.2

12.4

1.7

24.5

12.513.2

8.0

2.0

15.2

1.3

16.8

11.7

5.9

16.9

0

5

10

15

20

25

30

MS

CI W

orld

MS

CI E

M

S&

P5

00

Me

xic

o

Bra

zil

FT

SE

10

0

Ge

rma

ny

Fra

nce

Italy

Jap

an

HK

Ta

iwa

n

Sin

ga

pore

Ma

laysia

Th

aila

nd

Vie

tna

m

Au

str

alia

Ko

rea

Indo

nesia

Sh

an

gh

ai

Ph

ilipp

ines

(%)

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1/16 3/16 5/16 7/16 9/16 11/16 1/17 3/17 5/17 7/17

(USDmn) 1Q17 GDP release

Strategy Focus

3

August 25, 2017

Mirae Asset Daewoo Research

Table 1. Recent economic growth review by Mirae Asset Sekuritas Indonesia Research

Quarter Comment

1Q17

During the first trading session on May 5th, Indonesia reported 1Q17 gross domestic product (GDP) growth of 5.01% YoY, missing the consensus forecast (5.1% YoY) and in line with our projection (5.03% YoY). Economic growth was largely supported by exports (+8.0% YoY), which were strong for the second consecutive quarter. Investment growth was generally stable, picking up 4.8% YoY. Government spending returned to positive territory (+2.7% YoY) after two consecutive quarters of decline, but was still slow compared to previous years; we suspect the Jakarta governor election played a part in the slower-than-normal spending growth. Private consumption growth was somewhat disappointing (+4.9% YoY), but we believe tax amnesty payments contributed to the squeeze.

2Q17

For 2Q17, Indonesia reported gross domestic product (GDP) growth of 5.01% YoY (vs. consensus forecast of 5.1% YoY and our projection of 5.2% YoY). Headline consumption growth came in at 4.95% YoY. We are disappointed by the consumption growth figure, considering that the Ramadan festive season fell entirely in 2Q17. Government spending was a drag on growth, coming in at -1.9% YoY; this was a particularly disappointing result given the government’s stated commitment to building growth momentum. Investment growth picked up 5.4% YoY, as was largely expected, and growth in exports (+3.4% YoY) and imports (+0.5% YoY) helped to cushion sluggish private consumption and government spending.

Source: Mirae Asset Sekuritas Indonesia Research

Too many extraordinary items clouding the numbers

General disappointment stems from two key expenditure components; namely, private consumption and government spending. However, we underscore the fact that there were too many one-off items over the past two quarters.

Private consumption: In 1Q17, we suspect that the tax amnesty program hampered the spending sentiment (cash outflow for declaration of assets). In 2Q17, there was a shift in the Eid al-Fitr holiday (from 3Q last year to 2Q this year)—which should have placed positive impact on spending. However, the positive excitement was offset by layoffs from multiple corporations and operation shutdown of 7-Eleven.

Government spending: The two rounds of Jakarta governor election (Feb 15 and April 19) kept government spending on a tight leash as uncertainties weighed on fund disbursement. Furthermore, we suspect the Eid al-Fitr holidays have kept government spending initiatives on slow mode.

In our recent macro report, we revised down our FY17 growth outlooks on private consumption (from 5.1% to 5.0%) and government spending (from 3.5% to 0.2%). We also made minor adjustments to the exports (from 2.6% to 3.1%) and imports (from 2.4% to 2.1%). The downward revisions to private consumption and government spending have brought down our FY17 GDP growth from 5.3% to 5.1%. We made no changes to our FY17 investment growth projection (5.1%), but we revised down our growth projection for FY18, factoring in the political uncertainties ahead of the 2019 presidential election.

Figure 5. Mirae’s revised macro projection

Source: Mirae Asset Sekuritas Indonesia Research

Strategy Focus

4

August 25, 2017

Mirae Asset Daewoo Research

Enduring the pain

Time to cool down the excitement: Since the start of the year, market has remained bullish, supported by active buying from foreign investors that drove the Jakarta Composite Index (JCI) to a record high. However, we are now witnessing the excitement cooling down as investors begin to reassess the 1) long-term fundamental story of Indonesia’s consumption growth, 2) government's infrastructure development promise, 3) commodity market outlook, and 4) escalating political risks.

Revisiting the consumption story: At the core of the sluggish consumption growth is ‘inflation’. We argue that inflation is a compelling argument for consumer companies to increase their product average selling prices (ASPs). Soft inflationary pressures are likely to keep investors concerned over the revenue growth of consumer companies.

Can the government spend on infrastructure? We believe there are structural bottlenecks to the government’s budget. We expect challenges to persist in keeping its infrastructure development pledges.

The supply and demand dynamics of commodities have yet to reach equilibrium. We expect supply concerns on crude oil and demand concerns building on crude palm oil (EU) and coal (China).

The key concern we have on the upcoming presidential election (April 17, 2019) is the potential spillover to the real economy.

We believe it is time to manage risks rather than become excited. We recommend investors to take conservative approach in their investment decisions. Please refer to our recent publication, “Enduring the pain”.

Figure 6. Please refer to our recent publication: “Enduring the pain”

Source: Mirae Asset Sekuritas Indonesia Research

Strategy Focus

5

August 25, 2017

Mirae Asset Daewoo Research

Corporate earnings still in their expansion mode

During the 2Q17, corporate earnings seem to still be expanding (broadly in line with our expectations). Companies within the LQ45 components have delivered net profits of IDR51.2tr (-0.1% QoQ; +17.4% YoY), which we judge to be fairly robust. We believe a benign macro backdrop combined with favorable policy settings have placed positive implications on corporate earnings.

However, dissecting the corporate earnings trend, we noticed growing polarization by industries. While financials, property, mining and trade (driven by United Tractors (UNTR)—which is highly correlated to mining) sectors drove the LQ45 earnings, other industries, such as consumers, infrastructure, miscellaneous, basic industry and agriculture, have heavily underperformed during 2Q17.

Heading into 3Q17, we expect the macro backdrop to remain supportive. Furthermore, a recent policy rate cut by the central bank should place positive earnings implications on the consumers, financials, infrastructure, miscellaneous industries as they have greater sensitivity to yield changes.

Table 2. Aggregated LQ45 net profit (IDRtr))

2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 QoQ YoY

Consumers 6.9 6.6 9.1 9.0 8.7 8.5 9.7 10.0 8.4 -16.7% -4.0% Financials 15.3 20.2 21.6 18.5 16.6 21.5 19.1 20.0 22.0 10.1% 32.4% Infrastructure 3.9 4.8 4.9 5.2 5.9 5.1 5.4 7.3 6.0 -17.9% 1.2% Trade 3.5 3.1 0.0 2.3 3.8 2.8 2.2 2.8 4.5 62.5% 18.9% Property 1.6 1.6 2.0 1.2 2.0 1.3 2.7 1.7 3.4 95.5% 65.6% Miscellaneous 4.1 3.9 2.5 3.1 4.0 4.2 3.9 5.1 4.3 -16.1% 6.6% Basic industry 2.2 1.9 2.5 2.0 2.4 1.7 2.3 1.2 0.8 -38.9% -68.5% Mining -2.1 -0.2 -17.4 0.4 -0.3 1.7 1.0 2.0 1.6 -16.6% NM Agriculture 0.4 (0.1) 0.6 0.5 0.4 0.5 1.2 1.2 0.3 -72.1% -25.0% Total 35.8 41.9 25.8 42.1 43.7 47.4 47.5 51.3 51.2 -0.1% 17.4% Source: Company data, Mirae Assetk Sekuritas Indonesia Research

Note: Earnings of 45 companies within LQ45 excluding Financial (BJBR), Infrastructure (PGAS), Property (LPKR, WIKA), Miscellaneous

(SRIL), Basic Industry (BRPT), Mining (ADRO, ANTM), Agriculture (SSMS). Component change: (Inclusion) BJBR, BMTR, and BRPT

(Exclusion) ASRI, CPIN, and ELSA

Figure 7. FX rate trend during 2Q17 Figure 8. Yield (10yr gov. bond) trend during 2Q17

Figure 9. Crude oil (WTI) price trend during 2Q17

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

12,000

12,200

12,400

12,600

12,800

13,000

13,200

13,400

13,600

March 31 June 30 Aug 18

(IDR)

6.5

6.6

6.7

6.8

6.9

7.0

7.1

March 31 June 30 Aug 18

(%)

40

42

44

46

48

50

52

54

March 31 June 30 Aug 18

(USD/b)

Strategy Focus

6

August 25, 2017

Mirae Asset Daewoo Research

Industry outlook

Financials: Switching our focus from top to bottom

Despite positive macro developments, we have yet to witness a solid loan growth recovery. Our base case is that top line earnings are unlikely to significantly improve as we have ruled out the possibility of a V-shaped loan growth recovery. Our assumptions are premised on the base that both supply and demand for corporate loan remain anemic. Furthermore, given that the financial market has turned boring after the recent bull market, we expect banks’ non-interest income to flatten out going forward.

Table 3. Total operating profit growth for BBCA (YoY, %)

Growth (YoY, %) 2013 2014 2015 2016 2017F 2018F

Net interest income 24.4 21.2 12.0 12.0 7.6 7.3 Non-interest income 24.6 17.5 28.5 13.2 7.7 9.7 Net commission income 15.7 15.5 14.7 12.5 7.3 8.8 Trading related income 93.0 -29.4 156.1 6.0 -16.4 14.9 Other non-interest income 48.0 162.0 25.8 26.6 37.0 9.8 Total operating profit 24.5 20.4 15.7 12.3 7.7 7.9 Source: Company data, Mirae Asset Sekuritas Indonesia Research

However, we believe banks’ bottom line earnings are set to improve as provisioning pressures are forecasted to subside. Economic growth rebound, prolonged low yield environment, and rising commodity prices are likely to place limited pressures on banks’ legacy exposures, in our view. As bottom line earnings improve, we expect to see valuations continue to grind up higher.

Table 4. Provisioning expenses and attributable net profit growth for BBCA (YoY, %)

Growth (YoY, %) 2013 2014 2015 2016 2017F 2018F

Net provisions 304.2 11.1 56.5 30.1 -15.2 -24.8 Attributable net profit 21.6 15.7 9.3 14.4 12.0 10.4 Source: Company data, Mirae Asset Sekuritas Indonesia Research

Furthermore, recent policy rate cut by the central bank should allow banks to enjoy wider spreads as most large-cap banks have strong deposit franchises. All in all, we believe banks to be the key beneficiaries in the current macro cycle and thus maintain our Overweight call on the sector. Among our banking universe, we keep Bank Central Asia (BBCA/Buy/TP IDR20,300) on our list of top picks.

Figure 10. Loan growth vs. deposit growth (BBCA) Figure 11. Asset quality trend (BMRI)

Source: BBCA, Mirae Asset Sekuritas Indonesia Research

Source: BMRI, Mirae Asset Sekuritas Indonesia Research

0

5

10

15

20

25

30

35

40

45

1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15 3Q15 1Q16 3Q16 1Q17

Loan growth

Deposit growth

(YoY, %)

1

2

3

4

5

6

7

0

50

100

150

200

250

1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17

NPL coverage ratio (L)

NPL ratio (R)

Precautionary loan ratio (R)

(%) (%)

Strategy Focus

7

August 25, 2017

Mirae Asset Daewoo Research

Consumers: Stuck in limbo

We believe investors have started to reassess the favorite long-term investment thesis of Indonesia: the world’s fourth most populous country, growing with a young demographic profile. We agree with the notion that Indonesia embeds huge consumption potential; however, we believe there is a shift in the investment angle in leveraging off Indonesia’s consumption story.

Turning our focus to the basics of revenue—derived by a simple equation of quantity multiplied by price (revenue = quantity x price)—we believe consumer companies are finding it increasingly difficult to grow their revenue as organic growth falters. All in all, we believe revenue growth driven by quantity is now behind us and argue that revenue growth will be driven by the price side of the equation.

Table 5. Global demand for instant noodles (mn servings)

2012 2013 2014 2015 2016

Indonesia 14,750 14,900 13,430 13,200 13,010 Growth (YoY, %) 1.0 -9.9 -1.7 -1.4 World 101,800 105,900 103,960 97,650 97,460 Growth (YoY, %) 4.0 -1.8 -6.1 -0.2 Source: World Instant Noodles Association, Mirae Asset Sekuritas Indonesia Research

In order for a consumer company to blend up their ASP, it will have to either 1) innovate a new product with improved features and sell it at a higher price or 2) increase the existing product price. The first option should involve prudent decision making by the management, given the heavy research and development (R&D) and market research. Further, revenue improvement is not imminent given the time lag between a new product launch and successful monetization. The second option should be widely reviewed by the management as it places immediate impact on the ASP blend. However, this should also be an elusive option to implement, given inflationary pressures (which is a good rational to raise existing product prices) are unlikely to build up in the near horizon.

Table 6. Headline and core inflation trends (Average, %)

2014 2015 2016 July 2017

Headline inflation 6.42 6.38 3.53 3.88 Core inflation 4.53 4.89 3.36 3.05 Source: BI, Mirae Asset Sekuritas Indonesia Research

Structural shift from consumers to utilities

We underscore that Telekomunikasi Indonesia (TLKM) is now the component with the largest weight within the JCI. We suspect that investors are structurally switching from consumer staples to utilities (higher bargaining power) to play the Indonesian consumption growth theme (see the following section of the report).

Table 7. Top ten listed companies by market capitalization

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 NOW

TLKM TLKM TLKM TLKM ASII ASII ASII ASII BBCA HMSP HMSP TLKM ASII BUMI BBCA ASII TLKM BBCA HMSP HMSP HMSP BBCA TLKM BBCA

BBCA ASII UNVR BBCA BBCA HMSP BBCA BBCA ASII UNVR BBCA HMSP BBRI VALE BBRI BMRI BMRI BBRI BMRI TLKM TLKM TLKM ASII UNVR BMRI BBRI PGAS PGAS BBRI BMRI TLKM UNVR BBRI ASII UNVR BBRI PGAS BBCA ASII BBRI UNVR UNVR BBRI BMRI BMRI BBRI BBRI ASII UNVR BMRI BMRI UNVR HMSP TLKM UNVR BBRI UNVR BMRI BMRI BMRI HMSP PGAS HMSP ADRO PGAS GGRM PGAS PGAS PGAS GGRM GGRM GGRM ISAT HMSP ISAT UNTR ADRO UNTR GGRM SMGR GGRM BBNI BBNI BBNI

BDMN UNVR SMGR ICBP UNTR PGAS SMGR GGRM BBNI ICBP ICBP UNTR Source: Mirae Asset Sekuritas Indonesia Research

Note: Color represented by red (utilities), yellow (consumer discretionary), blue (financials), and green (consumer staples)

Strategy Focus

8

August 25, 2017

Mirae Asset Daewoo Research

Infrastructure: The competitive edge

Infrastructure (or utilities) operators are double-edged sword. On one side of the edge, it is highly regulated by the authorities given its nature of managing the base foundation of the economy. On the other side of the edge, utilities operators have greater bargaining power over the users—which we consider to be the competitive edge. We suggest three investment angles for consideration.

Strong pricing power

Unlike private consumer companies, infrastructure operators have fewer things to worry about when making pricing decisions. Given the government’s heavy reliance on upstream dividend, we do not believe inflation to be the key pricing consideration factor. Furthermore, we believe the low competition environment would act as a compelling argument that margins are likely to remain steady and elevated.

Table 8. Gross profit margin trend (%)

2010 2011 2012 2013 2014 2015 2016 2017F

TLKM 60.9 70.7 62.1 51.2 42.9 38.8 45.0 59.9 ICBP 26.9 26.9 26.6 27.1 26.6 28.4 30.8 30.9 Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Ample room for organic growth opportunities…

Growing competition from private operators (e.g., telco industry, toll road industry, etc.) may add concerns to investors. However, given the low infrastructure penetration, we believe there is ample room for all infrastructure operators to benefit (i.e., the pie is still big enough to share). According to World Bank, Indonesia ranked 62nd in the world in terms of infrastructure situation (vs. Korea 13th, China 39th).

…which means expansion will directly translate to revenue

Given the low infrastructure penetration and monopolistic nature, higher capex will directly drive infrastructure operators’ revenue higher (which is apparently not the case for private sector manufacturers).

Figure 12. (TLKM) Expansion drives revenue higher… Figure 13. …and also drives share price higher (TLKM)

Source: Company data, Mirae Asset Sekuritas Indonesia Research

Source: Company data, Mirae Asset Sekuritas Indonesia Research

Collectively, we believe infrastructure operators seem like a better fit to leverage off the long-term investment (consumption growth) thesis of Indonesia. We recommend investors Overweight infrastructure operators. Our favorite picks are Telekomunikasi Indonesia (TLKM/Under Review) and Jasa Marga (JSMR/Not Rated).

0

5,000

10,000

15,000

20,000

25,000

30,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2007 2009 2011 2013 2015 2017F

Revenue (L)

Trailing 12 m capex (R)

(IDR bn) (IDR bn)

0

5,000

10,000

15,000

20,000

25,000

30,000

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2009 2011 2013 2015 2017F

share price (L)

Trailing 12 m capex (R)

(IDR) (IDR bn)

Strategy Focus

9

August 25, 2017

Mirae Asset Daewoo Research

Property: Once bitten twice shy

Despite solid earnings growth (+96% QoQ; +66% YoY) in 2Q17, there has been growing concerns over the sustainability of earnings, especially on the builders. We suspect that this was largely driven by rising concerns over the state budget and soft inflationary pressures which led investors to stick to cash over real assets (i.e., property). We agree that valuations have corrected meaningfully from its peak (especially for builders), but we argue that there are little upside catalysts to reverse the sentiment for now.

We expect conflict of interest to remain on builders

Our analyst Franky Rivan recently downgraded his view on builders from Overweight to Neutral. Franky’s key arguments are centered on two key areas: 1) budget constraints and 2) upcoming presidential election.

Budget constraints are likely to impair the bullish market sentiment on the construction space. Furthermore, we see increasing chances of government demanding increased national service function—which should lead to a conflict of interest between the government and shareholders. Indeed, we are witnessing rising account receivable days across all builders.

The upcoming presidential election should also raise concerns over the current government’s priority. Franky highlights that subsidies tended to pick up during pre-election years.

Positive long-term outlook for developers, but short-term looks murky

Given the natural inflation hedging mechanism of property, coupled with long-term growth of middle-income households, we believe property developers have ample earnings growth potential over the longer horizon. However, in the near-term, we believe market appetite for cash will prevail over real assets as uncertainties persist.

Indeed, developers’ marketing sales growth tumbled 22.8% YoY due to the stagnant demand for properties. According to the latest home price data, we notice the decelerating pace of home prices, which support our view of sluggish property demand. Our analyst Franky holds a Neutral call on developers.

Despite short-term bumps, we see value over the longer investment horizon. Our preferred pick within the sector is Bumi Serpong Damai (BSDE/Buy/TP IDR2,210)

Figure 14. Builders’ days of receivables and GPM trend Figure 15. Decelerating pace of home prices

Source: Company data, Mirae Asset Sekuritas Indonesia Research Note: Based on internal calculations

Source: Bank Indonesia, Mirae Asset Sekuritas Indonesia Research

3.8

4.4

3.5 3.5

2.73.0

3.2

2.0

1.3

1.8

1.3

0.8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Average <36sqm 36~ 70sqm >70sqm

2Q14 vs. 2Q15

2Q15 vs. 2Q16

2Q16 vs. 2Q17

(YoY, %)

177

194184

214222

288

307

8

9

10

11

12

13

14

15

16

17

18

100

150

200

250

300

350

2011 2012 2013 2014 2015 2016 2017F

Days of receivables (L)

Gross profit margin (R)

(days) (%)

Strategy Focus

10

August 25, 2017

Mirae Asset Daewoo Research

Basic industry and chemicals: A mixed bag

The basic industry and chemical index is comprised 52% of cement companies. Others include pulp, chemical and, other basic-materials producing names. Given that most of the components within the basic industry are intermediate goods, they are generally sensitive to the manufacturing activity and the broad economic growth trends. Given the diverse nature of the components within the basic industry, we would like to focus our discussion on selective key industries.

Cement: Our analyst Mimi Halimin retains her Underweight recommendation on the cement sector, premised on overheated competition and sluggish demand growth (majority of cement producers’ sales are comprised of bag sales). However, despite negative earnings growth for the industry during 2Q17, shares of cement companies have outperformed in recent months. We suspect that this was largely due to the encouraging export figures—which investors seem to be excited about. Global Cement wrote in a recent article, “Cement producers in neighbouring countries beware!”

Table 9. Cement sales growth as of July 2017 (SMGR) (mn tons)

June 16 July 17 Change (%) 7M16 7M17 Change (%)

Domestic sales 1.52 2.25 47.5% 13.71 14.21 3.7% Export sales 0.08 0.21 153.9% 0.27 1.05 285.4% Total sales 1.61 2.46 53.1% 13.98 15.27 9.2% Source: Company data, Mirae Asset Sekuritas Indonesia Research

Poultry: Sluggish purchasing power recovery coupled with regulatory restrictions on corn and wheat imports have collectively placed negative repercussions on the poultry sector. In addition, the culling program initiated by the government in late-2015 is unlikely to be replicated in the near horizon, which leaves only the high base effect. Our analyst Mimi Halimin is Neutral on the poultry industry.

Petrochemical: There was one event which took investors by surprise—the inclusion of Barito Pacific (BRPT/Not rated) into the LQ45 index. BRPT is the mother company of the petrochemical manufacturer Chandra Asri (TPIA/Not rated). The inclusion is a compelling argument that petrochemical industry is positioning itself as the next economic driver of Indonesia. Given the sizable domestic supply shortage of petrochemical products, the nation is highly dependent on imports. Furthermore, given limited competition within the domestic market, we see ample opportunities ahead for BRPT and TPIA. We keep BRPT on our list of key calls given the 1) liquidity, 2) positive impact from the inclusion into the LQ45 index, and 3) valuation gap between the holding company and the operating company. We expect to see greater demand on the name in the event of MSCI and FTSE’s including BRPT into their indexes.

Table 10. Petrochemical market share

Item Total supply

Market share (%)

(mn tons) Chandra Asri Import Others

Olefin 2.6 52 24 24 Polyethylene 1.4 24 45 31 Polypropylene 1.6 29 53 18 Styrene Monomer 0.3 100 0 0 Source: Chandra Asri, Mirae Asset Sekuritas Indonesia Research

Table 11. Valuation (P/B) gap to narrow between BRPT and TPIA (12M trailing, x)

2011 2012 2013 2014 2015 2016 Now

BRPT 0.73 0.43 0.33 0.24 0.09 0.89 2.21 TPIA 1.09 1.96 0.95 0.93 0.95 4.42 4.59 Valuation gap 0.36 1.53 0.62 0.68 0.85 3.52 2.38 Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Strategy Focus

11

August 25, 2017

Mirae Asset Daewoo Research

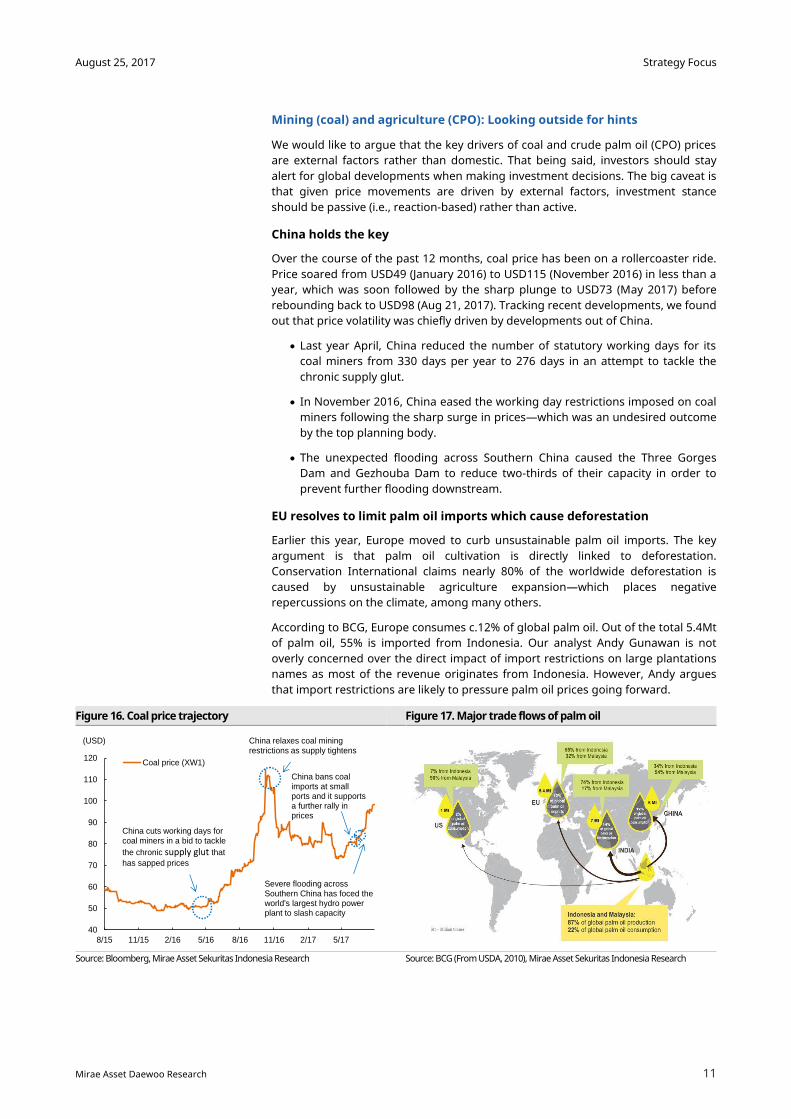

Mining (coal) and agriculture (CPO): Looking outside for hints

We would like to argue that the key drivers of coal and crude palm oil (CPO) prices are external factors rather than domestic. That being said, investors should stay alert for global developments when making investment decisions. The big caveat is that given price movements are driven by external factors, investment stance should be passive (i.e., reaction-based) rather than active.

China holds the key

Over the course of the past 12 months, coal price has been on a rollercoaster ride. Price soared from USD49 (January 2016) to USD115 (November 2016) in less than a year, which was soon followed by the sharp plunge to USD73 (May 2017) before rebounding back to USD98 (Aug 21, 2017). Tracking recent developments, we found out that price volatility was chiefly driven by developments out of China.

Last year April, China reduced the number of statutory working days for its coal miners from 330 days per year to 276 days in an attempt to tackle the chronic supply glut.

In November 2016, China eased the working day restrictions imposed on coal miners following the sharp surge in prices—which was an undesired outcome by the top planning body.

The unexpected flooding across Southern China caused the Three Gorges Dam and Gezhouba Dam to reduce two-thirds of their capacity in order to prevent further flooding downstream.

EU resolves to limit palm oil imports which cause deforestation

Earlier this year, Europe moved to curb unsustainable palm oil imports. The key argument is that palm oil cultivation is directly linked to deforestation. Conservation International claims nearly 80% of the worldwide deforestation is caused by unsustainable agriculture expansion—which places negative repercussions on the climate, among many others.

According to BCG, Europe consumes c.12% of global palm oil. Out of the total 5.4Mt of palm oil, 55% is imported from Indonesia. Our analyst Andy Gunawan is not overly concerned over the direct impact of import restrictions on large plantations names as most of the revenue originates from Indonesia. However, Andy argues that import restrictions are likely to pressure palm oil prices going forward.

Figure 16. Coal price trajectory Figure 17. Major trade flows of palm oil

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: BCG (From USDA, 2010), Mirae Asset Sekuritas Indonesia Research

40

50

60

70

80

90

100

110

120

8/15 11/15 2/16 5/16 8/16 11/16 2/17 5/17

Coal price (XW1)

(USD)

China cuts working days for coal miners in a bid to tackle

the chronic supply glut that

has sapped prices

China relaxes coal mining restrictions as supply tightens

Severe flooding across Southern China has foced the world's largest hydro power plant to slash capacity

China bans coal imports at small ports and it supports a further rally in prices

Strategy Focus

12

August 25, 2017

Mirae Asset Daewoo Research

Trade (retail): Turnaround looks less imminent

The retail sector seems to be grappling with profitability during changing times. As of 1H17, we see stiff headwinds on retailers evidenced by the prolonged slump in their same store sales growth (SSSG) prints, driving stock prices lower.

Table 12. Same store sales growth by companies

MAPI ACES RALS LPPF MPPA

2012 14.0% 11.3% 8.8% 11.1% 7.8% 2013 10.0% 5.0% 2.2% 12.1% 4.5% 2014 9.0% 3.1% 0.6% 10.7% 5.4% 2015 4.0% 0.5% -2.7% 6.8% -1.9% 2016 3.0% 1.4% 6.3% 5.5% -4.5% Source: Company data, Mirae Asset Sekuritas Indonesia Research

We ascribe this to the 1) combination of high bas effect in 2016, 2) overly optimistic revenue targets for 2017, 3) stagnating GDP, as well as 4) shift of consumer shopping preferences.

For example, hypermarket operator, Matahari Putra Prima (MPPA/Sell/TP IDR825), is struggling to boost revenue amid mushrooming small-sized grocery retailers, such as minimarkets and convenience stores, which highlights consumers’ reluctance to go through heavy traffic congestion to shop. Furthermore, minimarkets are increasingly favored by consumers due to their 1) convenient locations, 2) longer operating hours, and 3) attractive pricing thanks to many in-store promotions.

Evidenced by the success of convenience-oriented stores, we suspect consumers’ preference to have evolved towards less time-consuming shopping experience and lower product-pricing. That being said, the recent online shopping boom is arguably due to the convenient nature (accessible from mobile phones) and lower pricing.

Although the e-commerce is still in its infant stage and a large portion of transactions stem from social media and messaging apps, we believe e-commerce is poised to disrupt offline retailers given its rapid development. While the well-established offline retailers have built their proprietary e-commerce platforms, online heavyweight champions, such as Lazada, Shopee, and Tokopedia, continue to threaten the incumbent, backed by heavy investments from venture capitalists and/or private equities (we have to admit the fact that there is too much money in the market). In addition, our on-the-ground observation tells us that individual online sellers are armed with strong advantage over offline sellers as they provide personal interaction to their users (vs. limited experience in offline stores).

Strategy Focus

13

August 25, 2017

Mirae Asset Daewoo Research

Miscellaneous industry (automotive): Rising competition

On top of consumers’ closing up their wallets, the market is concerned about rising competition in the automotive industry. The main crux of investor concern lies on the fact that competition is escalating during a time when consumers’ purchasing intention is losing steam. When market is growing, competition is less of a threat as the pie is large enough for all market participants to share. However, when market stops growing, competition becomes a blow, not a pinch.

Table 13. Indonesia annual car sales (thousand units)

2010 2011 2012 2013 2014 2015 2016 2017F

Car sales 764.7 894.2 1,116.2 1,229.9 1,208.0 1,013.3 1,061.9 1,060.8 Change (YoY, %) 57.3 16.9 24.8 10.2 -1.8 -16.1 4.8 -0.1 Source: Gaikindo, Mirae Asset Sekuritas Indonesia Research

Note: 2017 estimates are annualized figures as of 7M17

New kids on the block

According to Indonesia investment coordinating board (BPKM), total direct investment increased 12.7% YoY from IDR151.6tr to IDR170.9tr. BPKM Chairman Lembong said that “investment has grown quite well", boosted by completion of Mitsubishi, Wuling and Krakatau Osaka Steel factories.

Mitsubishi recently introduced the all-new Xpander (XM crossover MPV) which is produced at the company's new factory in Indonesia. Furthermore, Wuling has recently opened its new factory (inaugurated by Vice President Jusuf Kalla), which can roll out 120,000 units per year (representing 11% of last year’s total car sales).

Key takeouts from our visit to GIIAS

Our analyst, Franky Rivan, recently visited the GIIAS—Indonesia’s largest auto show—and here we would like to highlight a part of his report:

…Market competition is likely to tighten due to newcomers (Mitsubishi Xpander and Wuling Confero) in the low multipurpose vehicle (LMPV) segment. According to our on-the-ground check, the Xpander and Confero sold more than 4,000 and 500 units, respectively, at the GIIAS event alone…

Franky reiterated his Trading Buy call on ASII, but we believe headwinds are likely to remain stiff for the automaker for the time being. From a strategy angle, we are Underweight on the sector until we see some encouraging signs of consumption appetite recovery.

Figure 18. Mitsubishi Xpander Figure 19. Wuling Confero S Figure 20. Test driving the Confero S

Source: Mirae Asset Sekuritas Indonesia Research

Source: Mirae Asset Sekuritas Indonesia Research

Source: Mirae Asset Sekuritas Indonesia Research

Strategy Focus

14

August 25, 2017

Mirae Asset Daewoo Research

Where do we go from here?

Challenging, but we see no derailment to Indonesia’s growth story

Investors are going to reassess the risks in the near-term. In the transition process, we expect to see investor appetite migration to selective industries. However, we do not believe prevailing risks to fundamentally derail the earnings generating ability of corporate Indonesia.

Furthermore, as we head a step closer to the 2019 presidential election, we expect to see more growth-oriented policies introduced by the administration—which should present a good upward boost to economic growth and corporate earnings. Indeed, we are encouraged by the central bank’s recent rate cut initiative and potential upward revision to the current loan-to-value regulation.

Figure 21. CPI vs. policy rate

Source: BI, Mirae Asset Sekuritas Indonesia Research

We retain our JCI target of 6,241pt for 2017F

We keep our JCI target of 6,241pt for 2017F unchanged. Our JCI target embeds a P/B multiple of 2.7x, which is at par with the ten-year historical average. Given the steady earnings, stable global macro developments, and market-friendly policy settings, we expect to see moderated valuation expansion to take place until the end of the year. Our target price of 6,241pt implies 6.1% upside potential from August 22 close.

Figure 22. Valuation trend for JCI

Source: Mirae Asset Sekuritas Indonesia Research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1/05 1/07 1/09 1/11 1/13 1/15 1/17

(Trailing P/B, x)

LT target 3.5x

Post GFC to tapertantrum avg. 2.9x

Trough cycle 2.0x

10yr avg. 2.7x (TP)

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

0

1

2

3

4

5

6

7

8

9

2/10 8/10 2/11 8/11 2/12 8/12 2/13 8/13 2/14 8/14 2/15 8/15 2/16 8/16 2/17

Policy rate (R) CPI (YoY, L)(YoY, %) (%)

Strategy Focus

15

August 25, 2017

Mirae Asset Daewoo Research

Our key calls are: BBCA, TLKM, KLBF, BRPT, and BSDE

We prefer large caps over small caps and value over growth stocks. Our five key investment calls are Bank Central Asia (BBCA/Trading Buy/TP IDR20,300), Telekomunikasi Indonesia (TLKM/Under Review), Kalbe Farma (KLBF/Under Review), Barito Pacific (BRPT/Not Rated) and Bumi Serpong Damai (BSDE/Buy/TP IDR2,210). We exclude Waskita Beton Precast (WSBP/Not Rated) from our key call list due to the uncertainties related to government spending and include BSDE following the favorable policy settings by the government.

Table 14. Key investment call by Mirae Asset Sekuritas

Company name Ticker P/E (17F, x) RoE (17F, %) Notes

Bank Central Asia BBCA 20.6 18.8 Proven track record of earnings stability Economic recovery to improve asset quality metrics and drive bottom line

earnings higher

Kalbe Farma KLBF 32.7 19.7 Growing health awareness, especially after the Universal Healthcare program Easier access to medical services should bring higher volume KLBF is targeting specific therapies such as cancer, diabetes, and biosimilar, etc.

Telekomunikasi Indonesia TLKM 20.4 25.6 Indonesia’s long-term consumption story is changing – We like the strong

bargaining power of utilities companies, especially TLKM Strong balance sheet and cash flow to enable strong market dominance

Barito Pacific BRPT 11.9 (Trailing)

20.7 (Trailing)

Inclusion to the LQ45 leads us to believe that BRPT will be included into MSCI /FTSE indexes and we expect to see crowded trade on BRPT

We expect narrowing of the valuation gap between BRPT/TPIA

Bumi Serpong Damai BSDE 13.3 18.2 Unfolding of favorable policy settings for developers—recent rate cut and

possible upward revisions to the loan-to-value (LTV) regulation to pace positive impact on developers

Source: Bloomberg estimates, Mirae Asset Sekuritas Indonesia Research

Strategy Focus

16

August 25, 2017

Daewoo Securities Research

APPENDIX 1

Important Disclosures & Disclaimers

Stock Ratings Industry Ratings

Buy Relative performance of 20% or greater Overweight Fundamentals are favorable or improving

Trading Buy Relative performance of 10% or greater, but with volatility Neutral Fundamentals are steady without any material changes

Hold Relative performance of -10% and 10% Underweight Fundamentals are unfavorable or worsening

Sell Relative performance of -10%

* Our investment rating is a guide to the relative return of the stock versus the market over the next 12 months. * Although it is not part of the official ratings at Mirae Asset Sekuritas Indonesia, we may call a trading opportunity in case there is a technical or short-term material development. * The target price was determined by the research analyst through valuation methods discussed in this report, in part based on the analyst’s estimate of future earnings. The achievement of the target price may be impeded by risks related to the subject securities and companies, as well as general market and economic conditions. Analyst Certification Opinions expressed in this publication about the subject securities and companies accurately reflect the personal views of the Analysts primarily responsible for this report. PT. Mirae Asset Seukritas Indonesia (“Mirae Asset Daewoo”) policy prohibits its Analysts and members of their households from owning securities of any company in the Analyst’s area of coverage, and the Analysts do not serve as an officer, director or advisory board member of the subject companies. Except as otherwise specified herein, the Analysts have not received any compensation or any other benefits from the subject companies in the past 12 months and have not been promised the same in connection with this report. No part of the compensation of the Analysts was, is, or will be directly or indirectly related to the specific recommendations or views contained in this report but, like all employees of Mirae Asset Daewoo, the Analysts receive compensation that is determined by overall firm profitability, which includes revenues from, among other business units, the institutional equities, investment banking, proprietary trading and private client division. At the time of publication of this report, the Analysts do not know or have reason to know of any actual, material conflict of interest of the Analyst or Mirae Asset Daewoo except as otherwise stated herein. Disclaimers This report is published by Mirae Asset Daewoo, a broker-dealer registered in the Republic of Indonesia and a member of the Indonesia Stock Exchange. Information and opinions contained herein have been compiled in good faith and from sources believed to be reliable, but such information has not been independently verified and Mirae Asset Daewoo makes no guarantee, representation or warranty, express or implied, as to the fairness, accuracy, completeness or correctness of the information and opinions contained herein or of any translation into English from the Indonesian language. In case of an English translation of a report prepared in the Indonesian language, the original Indonesian language report may have been made available to investors in advance of this report. The intended recipients of this report are sophisticated institutional investors who have substantial knowledge of the local business environment, its common practices, laws and accounting principles and no person whose receipt or use of this report would violate any laws and regulations or subject Mirae Asset Daewoo and its affiliates to registration or licensing requirements in any jurisdiction shall receive or make any use hereof. This report is for general information purposes only and it is not and shall not be construed as an offer or a solicitation of an offer to effect transactions in any securities or other financial instruments. The report does not constitute investment advice to any person and such person shall not be treated as a client of Mirae Asset Daewoo by virtue of receiving this report. This report does not take into account the particular investment objectives, financial situations, or needs of individual clients. The report is not to be relied upon in substitution for the exercise of independent judgment. Information and opinions contained herein are as of the date hereof and are subject to change without notice. The price and value of the investments referred to in this report and the income from them may depreciate or appreciate, and investors may incur losses on investments. Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. Mirae Asset Daewoo, its affiliates and their directors, officers, employees and agents do not accept any liability for any loss arising out of the use hereof. Mirae Asset Daewoo may have issued other reports that are inconsistent with, and reach different conclusions from, the opinions presented in this report. The reports may reflect different assumptions, views and analytical methods of the analysts who prepared them. Mirae Asset Daewoo may make investment decisions that are inconsistent with the opinions and views expressed in this research report. Mirae Asset Daewoo, its affiliates and their directors, officers, employees and agents may have long or short positions in any of the subject securities at any time and may make a purchase or sale, or offer to make a purchase or sale, of any such securities or other financial instruments from time to time in the open market or otherwise, in each case either as principals or agents. Mirae Asset Daewoo and its affiliates may have had, or may be expecting to enter into, business relationships with the subject companies to provide investment banking, market-making or other financial services as are permitted under applicable laws and regulations. No part of this document may be copied or reproduced in any manner or form or redistributed or published, in whole or in part, without the prior written consent of Mirae Asset Daewoo.

Disclosures As of the publication date, PT. Mirae Asset Sekuritas Indonesia, and/or its affiliates do not have any special interest with the subject company and do not own 1% or more of the subject company's shares outstanding.

Strategy Focus

17

August 25, 2017

Mirae Asset Daewoo Research

Distribution United Kingdom: This report is being distributed by Mirae Asset Securities (UK) Ltd. in the United Kingdom only to (i) investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”), and (ii) high net worth companies and other persons to whom it may lawfully be communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons together being referred to as “Relevant Persons”). This report is directed only at Relevant Persons. Any person who is not a Relevant Person should not act or rely on this report or any of its contents. United States: This report is distributed in the U.S. by Mirae Asset Securities (USA) Inc., a member of FINRA/SIPC, and is only intended for major institutional investors as defined in Rule 15a-6(b)(4) under the U.S. Securities Exchange Act of 1934. All U.S. persons that receive this document by their acceptance thereof represent and warrant that they are a major institutional investor and have not received this report under any express or implied understanding that they will direct commission income to Mirae Asset Daewoo or its affiliates. Any U.S. recipient of this document wishing to effect a transaction in any securities discussed herein should contact and place orders with Mirae Asset Securities (USA) Inc., which accepts responsibility for the contents of this report in the U.S. The securities described in this report may not have been registered under the U.S. Securities Act of 1933, as amended, and, in such case, may not be offered or sold in the U.S. or to U.S. persons absent registration or an applicable exemption from the registration requirements. Hong Kong: This document has been approved for distribution in Hong Kong by Mirae Asset Securities (HK) Ltd., which is regulated by the Hong Kong Securities and Futures Commission. The contents of this report have not been reviewed by any regulatory authority in Hong Kong. This report is for distribution only to professional investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong Kong (Cap. 571, Laws of Hong Kong) and any rules made thereunder and may not be redistributed in whole or in part in Hong Kong to any person. All Other Jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact Mirae Asset Daewoo or its affiliates only if distribution to or use by such customer of this report would not violate applicable laws and regulations and not subject Mirae Asset Daewoo and its affiliates to any registration or licensing requirement within such jurisdiction. Mirae Asset Daewoo International Network

Mirae Asset Daewoo Co., Ltd. (Seoul) Mirae Asset Securities (HK) Ltd. Mirae Asset Securities (UK) Ltd. Global Equity Sales Team Mirae Asset Center 1 Building 26 Eulji-ro 5-gil, Jung-gu, Seoul 04539 Korea

Suites 1109-1114, 11th Floor Two International Finance Centre 8 Finance Street, Central Hong Kong China

41st Floor, Tower 42 25 Old Broad Street, London EC2N 1HQ United Kingdom

Tel: 82-2-3774-2124 Tel: 852-2845-6332 Tel: 44-20-7982-8000

Mirae Asset Securities (USA) Inc. Mirae Asset Wealth Management (USA) Inc. Mirae Asset Wealth Management (Brazil) CCTVM 810 Seventh Avenue, 37th Floor New York, NY 10019 USA

555 S. Flower Street, Suite 4410, Los Angeles, California 90071 USA

Rua Funchal, 418, 18th Floor, E-Tower Building Vila Olimpia Sao Paulo - SP 04551-060 Brasil

Tel: 1-212-407-1000 Tel: 1-213-262-3807 Tel: 55-11-2789-2100

PT. Mirae Asset Sekuritas Indonesia Mirae Asset Securities (Singapore) Pte. Ltd. Mirae Asset Securities (Vietnam) LLC Equity Tower Building Lt. 50 Sudirman Central Business District Jl. Jend. Sudirman, Kav. 52-53 Jakarta Selatan 12190 Indonesia

6 Battery Road, #11-01 Singapore 049909 Republic of Singapore

7F, Saigon Royal Building 91 Pasteur St. District 1, Ben Nghe Ward, Ho Chi Minh City Vietnam

Tel: 62-21-515-3281 Tel: 65-6671-9845 Tel: 84-8-3911-0633 (ext.110)

Mirae Asset Securities Mongolia UTsK LLC Mirae Asset Investment Advisory (Beijing) Co., Ltd Beijing Representative Office

#406, Blue Sky Tower, Peace Avenue 17 1 Khoroo, Sukhbaatar District Ulaanbaatar 14240 Mongolia

2401B, 24th Floor, East Tower, Twin Towers B12 Jianguomenwai Avenue, Chaoyang District Beijing 100022 China

2401A, 24th Floor, East Tower, Twin Towers B12 Jianguomenwai Avenue, Chaoyang District Beijing 100022 China

Tel: 976-7011-0806 Tel: 86-10-6567-9699 Tel: 86-10-6567-9699 (ext. 3300)

Shanghai Representative Office Ho Chi Minh Representative Office

38T31, 38F, Shanghai World Financial Center 100 Century Avenue, Pudong New Area Shanghai 200120 China

7F, Saigon Royal Building 91 Pasteur St. District 1, Ben Nghe Ward, Ho Chi Minh City Vietnam

Tel: 86-21-5013-6392 Tel: 84-8-3910-7715

![PT CHANDRA ASRI PETROCHEMICAL TBK [TPIA.JK]barito-pacific.com/files/Investor relations/managementPresentation/c… · PT CHANDRA ASRI PETROCHEMICAL TBK [TPIA.JK] Citi Asia Pacific](https://img.dokumen.tips/doc/110x75/607fc4a288f0f94c624ff284/pt-chandra-asri-petrochemical-tbk-tpiajkbarito-relationsmanagementpresentationc.jpg)