Embed Size (px)

Citation preview

Analyst Presentation February 2015Richard Rushton –Managing Director

Strategy and Performance Overview

Strong performance in the core businessDespite economic headwinds and a challenging competitor environment, Distell continues to grow its position as South Africa’s leading producer of

ciders, wines and spirits with a strong increase in volumes and revenue in our domestic market and in several international markets

We are investing at an accelerated pace in our core brands, organisation capability, building Route To Market in Africa, and in owning the ‘last mile’ in

Southern Africa

To this end we have appointed a number of senior leaders who contribute greatly to the depth of global experience in our leadership team

2

Agenda

• Market Review

• Salient features of our performance

• Strategy Review & Close

123

3

• Macro Environment

• Key Industry Trends

12

Market Review

• Competitor Performance3

The Macro-EnvironmentSouth Africa: Slight GDP recovery as oil price feeds through• Consumer spending recovering

• Lower inflation outlook

• US$ strength

• Rand volatility set to continue

• SA’s electricity supply challenge

• Investment ratings due in June0.0

1.0

2.0

3.0

4.0

Q12014

Q22014

Q32014

Q42014 f

Q12015 f

Q22015 f

% G

row

th

RSA % Real Growth

Consumer spend Real income

Source: BER 5

The Macro-EnvironmentAfrica: GDP growth outlook favourable , but slowing

• Nigeria - oil price drop, Boko Haram, election driving uncertainty

• Angola - lower oil prices, Kwanza weakening, import restrictions

• East Africa growing - led by Kenya

• West Africa affected by Ebola – recovery later in 2015

• Kenya, Tanzania set to benefit as net oil importers

International: Global projections revised downward• Increased global geo-political risk – Russia, Middle East

• Slower China growth – at or below 7%

• Russia and Brazil face challenges

• Continued Euro Zone weakness – QE announced6

0% 10% 20% 30% 40% 50% 60% 70%

United States (241 mn litres)

Australia (105 mn litres)

South Africa (299 mn litres)

United Kingdom (981 mn litres)

Global (2177 mn litres)

% Volume Growth - 2014

Leading Cider Markets - 80% of Global Consumption

Industry Trends Cider remains the highest growing category

• Growth in global cider consumption x4 times faster than global alcoholic beverages; and x8 times more than global RTD growth

• SA cider growth moderating, still favourable market fundamentals for future growth

• Growth in global cider consumption x4 times faster than global alcoholic beverages; and x8 times more than global RTD growth

• SA cider growth moderating, still favourable market fundamentals for future growth

Sources: Euromonitor (2014)

Cider % of Total RTD Volumes

1%

18%

8%

6%

1%

7

Industry Trends Wine becomes an emerging market play

8

• Global wine consumption trends in line with total alcoholic beverages growth• Variable performance geographically: Emerging markets growing faster• Eurozone widely impacted• SA wine growth ahead of total alcohol market• Africa’s wine market remains largely untapped

• Global wine consumption trends in line with total alcoholic beverages growth• Variable performance geographically: Emerging markets growing faster• Eurozone widely impacted• SA wine growth ahead of total alcohol market• Africa’s wine market remains largely untapped

Sources: Wine intelligence; SAWIS (2014) -5% 5% 15%

Super Premium(Ave R/litre: R62)

Premium(Ave R/litre: R24)

Standard Price(Ave R/litre: R15)

Total(Ave R/litre:R28)

SA Wine Consumption 2014

% Value Growth % Vol Growth

-2% 0% 2% 4% 6% 8%

Australasia

Middle East & Africa

Latin America

Eastern Europe

North America

Asia Pacific

Western Europe

Global

Global Wine Consumption Volume Growth % 2014

% Share of Global Wine Consumption

40%23%13%11%7%3%2%

Industry Trends Headwinds for Cognac & Scotch Whisky Exports

Source: BNIC, HM Revenue & Customs

• Volumes of Scotch Whisky shipments declined by 1.2%• Cognac exports (shipment volumes) declined by 1.2%• Significant slump in sales to Eastern Europe led by Russia• Austerity measures affect cognac in China

• Volumes of Scotch Whisky shipments declined by 1.2%• Cognac exports (shipment volumes) declined by 1.2%• Significant slump in sales to Eastern Europe led by Russia• Austerity measures affect cognac in China

Cognac Export Volume Growth: Key BisquitMarkets July-December 2014 vs. History

Scotch Whisky: Volume Growth of Exports June-November 2014 vs. History

-1%-12%

65%-9%

32%-41%

-3%5%

16%

-80% -30% 20% 70%

Belgium

South Africa

Taïwan

France

USA

-76%-11%

-4%-2%

3%3%4%

15%

-100% -70% -40% -10% 20%

Eastern EuropeCentral & South…

AustralasiaOther Europe

North AmericaAfrica

AsiaMiddle East

9

Competitor Performance Distell ahead of competitors

10Source: Companies’ latest published trading results Data note: Net sales revenue excludes excise duties

• Distell performed well, outpacing leading competitors’ revenue growth− Emerging market footprint− Diverse brand portfolio (product and category mix)− Capability investment showing early benefits

• Competitors impacted by slowdown in Europe, China, Brazil and Russia.

Beer Spirits Wine Cider, Wine & Spirits

Company SABMiller Heineken Pernod Ricard Diageo

Treasury Wine

Estates

Vina Concha Y

Toro Distell Ltd

(Normalised)Distell Ltd (Inflationadjusted)

Reported NSV Growth

1.5% 0.1% 1.0% -0.1% 3.6% 10.0% 10.5% 5.2%

• Corporate

• RSA

12

Salient features of our performance

• Africa3• International4

Key December 2014 YTD metrics

R10.997 bn369m litresR1.473 bn

R1 bn

reported revenue – up 10.5% on history

sold - up 3.7 % on prior year

normalised operating profit – an increase of 7.0% on history

normalised headline earnings - up 9.5% on prior year

Investments in capability accelerated for: Expanding African structures, Revenue Management, SA Sales Force Effectiveness , Supply Chain Excellence, Brand innovation, Strengthening People Capability

12

Strong results from our core South African operations!

• Volume growth of 6%

• Ciders continue to grow – innovation underway

• Wine -strong double digit volume/value growth

• 4th Street volume up 166%

• Brandy bottoming out-premiums growing

• SA whisky story emerging – Bains revenue +61%

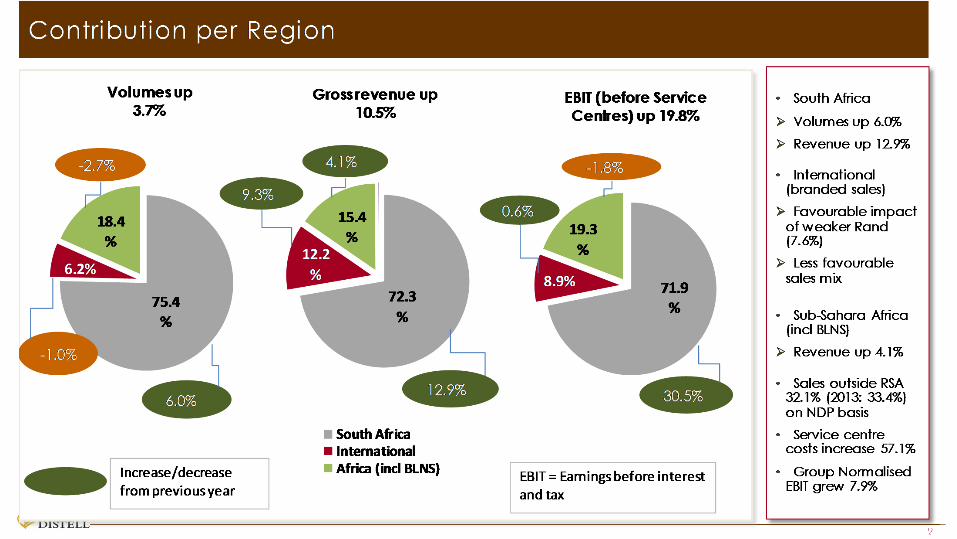

Revenue % Distell

RSA 12.9% 72.3%

Rev growth against history 13

SA Brandy showed early signs of stabilising

Brandy grew 1.7% - first growth period in many years

14

The ciders growth story

0200400600800

100012001400160018002000

2,000 2,002 2,004 2,006 2,008 2,010 2,012 2,014

Reve

nue

Inde

x

Cider Revenue Total Cider

15

Africa growing but Angola impacted by shipments….

* Incl. BNLS, all reported against history

Angola: Timing of shipments, PY sell-in ahead of duty increases. In- market sales up 18%

Kenya: KHEAL 26% stake - growth

Ghana: In-market sales 11%, In country bottling facility

Zimbabwe & Tanzania: Strong in-market performances via SABMiller JV’sEquity income up > 30%

Nigeria: Currently seeding brands, normalising stocks and building RTM

16

Revenue % Distell

Africa* 4.1% 15.4%Africa* (excl Angola) 7.2%

% AfricaBNLS 10.4% 53.6%Angola -4.5% 21.1%Zambia 76.2% 5.5%Mozambique 70.7% 5.0%Kenya 12.5% 2.7%Ghana 21.3% 2.0%Zimbabwe 18.9% 1.9%Nigeria -69.7% 1.9%

Sluggish international growth – key markets under pressure

Revenue

International 9.3% 12.2%%Cont Distell

• European weakness :− Russia (spirits), UK (cider) and Sweden (wine)

• Latin America buoyant-Amarula growth

• North America revenue +12% without IBC RTM transaction

• Taiwan value +69% - favorable product mix

• BSD & Bisquit face headwinds despite lift in December− Scottish Leader re-launched November− Black Bottle launched in France, Germany and South Africa

17

• Our Aspirations

• Strategy and Initiatives

12

Strategy Review

18

A Reminder of our Aspirations• A dominant regional alcoholic beverage brand and RTM owner

− #1 Cider company globally− #2 Alcoholic beverages company in SA− Leading player in core markets of Africa− Presence in at least one major international market/geography − Scale positions established in core markets

• Integrate BSD acquisition• A differentiated player

− Core ciders, wines and spirits resonating across different consumer occasions

• Enhance operating margins, cost and working capital efficiency• Unlock value from our wine assets

19

LEADSELECTED

EMERGING MARKETS

OWN THE LAST MILE

SCALE UPEXCELLENCE

CARE AND CONTRIBUTESHAPE THE

FUTURE

CRAFT DISTINCTIVE & COMPELLING

BRANDS

Corporate Strategy-Initiatives and UpdateStrategic Aspiration:Double revenue and profit by 2020!

Key initiatives:• Grow and win in RSA

• Expand into Africa & one major international market

• Leverage core brand portfolio

• Build scale positions in core markets and segments

20

LEAD SELECTED MARKETS!Organic Growth –TOP 10 markets

• SA performs!

• Distell brands competitive in key African markets

• Focused investment in Ghana & Kenya

• Nigeria & Angola - RTM alternatives advanced

• Nordics – down with SA wine-RTM and portfolio focus

• Taiwan holds promise!

• Brazil rev +78%

21

CRAFT DISTINCTIVE & COMPELLING BRAND PORTFOLIOS

• Accessible power brands deliver solid performances - Richelieu, 3 Ships, Hunter's, AH Crackling & 4th Street

• Accessible wines: revenue up 13%

• SA wine growth in all segments

• Pursuing new cider growth

• Positive value growth in “luxury brands”

• New Black Bottle launch underway-select markets, Revenue+13%

• Bisquit shows strong SA growth, underperforms in China

22

Category YTD Dec 2014Rev

GrowthContribution

DistellAccessible Power Brands 9% 87.0%"Luxury" Brands 17% 8.0%Vineyards & Estates 6% 4.0%

OWN THE LAST MILE –COMPETE IN THE STREET!

• SA Sales Force Effectiveness -increased coverage and service− YTD: 5 688 mainstream outlets, 60 sales people − Embedding execution standards - hard work ahead− Exceeding targets and ROI

• African RTM capability build continues− Detailed portfolio/RTM plans completed - Nigeria & Angola− Detailed brand & channel activity grids rolled out in selected markets − Ghana SFA pilot success

− Angola to commence− 230 in-country sales people trained

• Taiwan RTM expansion – deploy people and bulk up portfolio

23

SCALE UP EXCELLENCE• Supply Chain reliability & Customer service a major priority!

− Expansion of Springs capacity on track

− Freeze plant grows efficiency levels

• Supply Chain capability strengthened with senior appointments

• Network Optimization project underway

• Centralised Procurement - implement in waves

• Revenue Management - exceeding targets

24

SHAPE THE FUTURE!

• Senior appointments strengthen leadership team

• HR leadership in place, succession plan completed

• HR / Talent systems scoped & preferred ICT solution identified

• Change enablement capability build commenced

• Corporate strategy alignment process on track

• ICT architecture reviewed, strategy developed & approved

25

CARE AND CONTRIBUTE

• Role of corporate brand clarified

• Localised apple concentrate sourcing project formally commenced

• Transformation strategy developed to guide BBBEE progress

• Wine value unlocking strategy commenced

• Role of Distell Development Trust agreed• Align and prioritise CSI opportunities

• Step change initiatives aimed at addressing BBBEE

26

Thank you

Merwe Botha –Financial Director

1

Financial Results

Index

2

Salient features

Delivering value

Operating costs

Earnings and profit performance

Investment in operating assets

Cash flow and financing

ABCDEF

Delivering value

3

Operating profit

Salient features1

2

3 Headline earnings

4

Reported NormalisedSales volumes up 3.7% 3.7%Revenue up 10.5% 10.5%EBITDA -1.0% 9.9%Operating profit -4.6% 7.0%Headline earnings -7.6% 9.5%Growth in total assets 10.6%

Sal ient features of our performance to December 2014

5

6

Delivering value

7

Managing the underlying drivers of shareholder value

Contribution per region

Contribution per category

1

2

3

8

Rm Rm Trend Trend2014/15 Report Normal2013/14 9.0% 10.8% 990.3 1,071.8 92.4 109.5

9.1% 9.2%

ReportedNormalised 5.55% 6.64% 10,997 9,948 110.5

5.60% 5.65%

0.62 0.62 17,851 16,147 110.6

10.8% 12.6%

17,851 16,147 110.6Gearing

1.94 1.90

9,200 8,487 108.4

Equity and liabilities

Total equity

Return on Equity (ROE)

Revenue

Net Profit after Tax (NPAT)

Total assets

NPAT%

Return on assets (ROA)

Asset turn

Managing the underlying drivers of shareholder value

2013/14 Full year: 15.9% (normalised)

9

10

Operating costs

11

Operating expenses1

12

13

Earnings and profit performance

14

Margin management

Growth in operating profit

Headline earnings

123

15

16

17

Investment in operating assets

Net operating assets1

18

19

Cash flow and financing

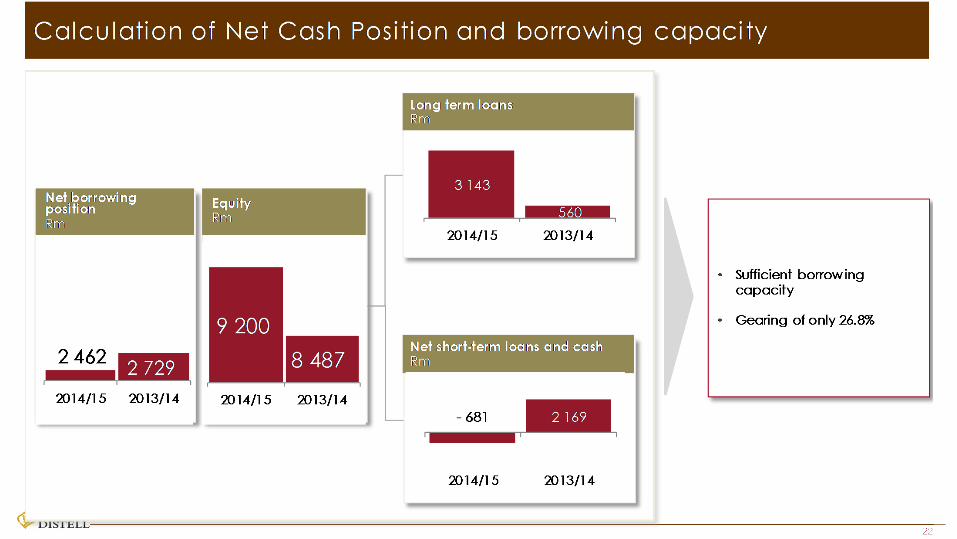

Cash outflow and funding

Net cash position and borrowing capacity

1

2

20

21

22

Summary

1

23

Summary of performance

Summary

24

Satisfactory but uneven topline growth under challenging trading conditions

Efficiency gains reinvested in building capacity and capability to support future growth

Steep increases in excise duties impact margins

Gross margins improves marginally

Operating margin contracted from 13.8% to 13.4%

Disciplined investment and maintaining asset turn

Strong cash generation

Thank you

25

Questions?• This presentation contains ‘forward-looking’ statements, including specifically all statements that

express market forecasts; Distell’s commentary on macro and industry related market trends;and projections related to Distell’s business strategy.

• All forward-looking statements contained in this presentation involve risk and uncertainty sincethey are dependent on assumptions of circumstances that will occur in the future. There aremultiple variables which could cause actual results to differ from the forward-looking statementswhich are not within Distell’s management control. Such variables include, but are not limitedto, political, macro and socio-economic changes; legal and regulatory changes; litigationdevelopments; technological changes; environmental risks and changes in consumer trends,among others.

• As such, you are cautioned not to place undue reliance on the forward-looking statementscontained herein, as they apply only as at the date of this presentation.

• There is no obligation on Distell in the future to provide updates on forward-looking statementscontained in this presentation to reflect any changes in Distell’s projections with regard theretoor any changes in events or underlying assumptions on which any such statement is based.