Embed Size (px)

Citation preview

Strategist’s Handbook:Chart Updates

Yardeni Research, Inc.

July 12, 2018

Dr. Edward Yardeni516-972-7683

Please visit our sites atwww.yardeni.comblog.yardeni.com

thinking outside the box

Table Of Contents Table Of ContentsTable Of Contents

July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

Stock Prices 1S&P 500 Earnings, Revenues, Margins 2S&P 500 Revenues & Margins 3Forward Revenues, Earnings, & Margins 4S&P 500/400/600 Forward Earnings & Margins 5Blue Angels 6Valuation 7-8S&P 500 Sectors Forward P/Es 9S&P 500 Sectors Price Indexes 10S&P 500 Sectors Forward Earnings 11Equity Flows 12Dollar & Commodities 13Stocks & Commodities 14Big Picture 15US Economic Indicators 16-17China 18Eurozone 19Global 20

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20193.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

7/11

7/11

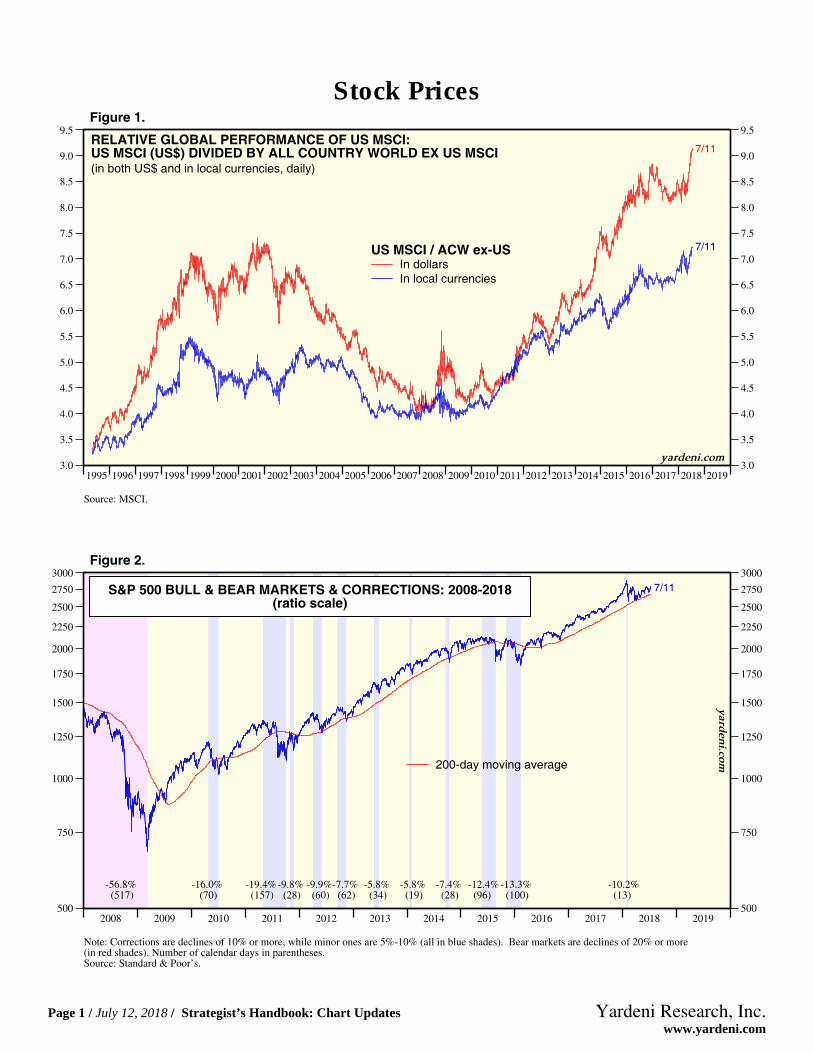

RELATIVE GLOBAL PERFORMANCE OF US MSCI:US MSCI (US$) DIVIDED BY ALL COUNTRY WORLD EX US MSCI(in both US$ and in local currencies, daily)

US MSCI / ACW ex-USIn dollarsIn local currencies

Source: MSCI.

yardeni.com

Figure 1.

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019500

750

1000

1250

1500

1750

2000

2250

2500

2750

3000

500

750

1000

1250

1500

1750

2000

2250

2500

2750

3000

S&P 500 BULL & BEAR MARKETS & CORRECTIONS: 2008-2018(ratio scale)

7/11

200-day moving average

-56.8% (517)

-16.0% (70)

-19.4% (157)

-9.8% (28)

-9.9% (60)

-7.7% (62)

-5.8% (34)

-5.8% (19)

-7.4% (28)

-12.4% (96)

-13.3% (100)

-10.2% (13)

Note: Corrections are declines of 10% or more, while minor ones are 5%-10% (all in blue shades). Bear markets are declines of 20% or more(in red shades). Number of calendar days in parentheses.Source: Standard & Poor’s.

yarden

i.com

Figure 2.

Stock Prices

Page 1 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

Figure 3.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019650

750

850

950

1050

1150

1250

1350

1450

650

750

850

950

1050

1150

1250

1350

1450

7/5

Q2

S&P 500 REVENUES PER SHARE: ACTUAL (S&P quarterly data) & FORWARD (TR weekly data)(dollars)

Revenues Per Share52-week Forward*

Actual (x4)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20190

20

40

60

80

100

120

140

160

180

0

20

40

60

80

100

120

140

160

180

Q1

7/5

Q1

S&P 500 EARNINGS PER SHARE: FORWARD & ACTUAL OPERATING EARNINGS(dollars)

Earnings Per Share52-week Forward*Thomson Reuters Operating (x4)S&P Operating (x4)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20190

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

7/5Q1

S&P 500 PROFIT MARGIN MEASURES(percent)

S&P 500 Operating Profit Margins

52-week Forward* (12.2)

Thomson Reuters (11.9)

S&P (11.4)

* Time-weighted average of consensus operating earnings estimates for current and next years. Source: Standard & Poor’s (for actual revenues) and Thomson Reuters I/B/E/S (for forward revenues), and Bureau of the Census.

yardeni.com

S&P 500 Earnings, Revenues, Margins

Page 2 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20-25

-20

-15

-10

-5

0

5

10

15

20

25

-25

-20

-15

-10

-5

0

5

10

15

20

25

May

S&P 500 AGGREGATE REVENUES & US BUSINESS SALES OF GOODS(yearly percent change)

S&P 500 Aggregate Revenues* (7.2)Business Sales of Goods** (8.4)

** Manufacturing and trade sales.* Revenues are derived by multiplying S&P 500 revenues per share by the S&P 500 divisor for each quarter.

Source: Census Bureau and Standard & Poor’s.

yardeni.com

Figure 4.

47 49 51 53 55 57 59 61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 212

3

4

5

6

7

8

9

10

11

12

13

2

3

4

5

6

7

8

9

10

11

12

13

S&P 500 OPERATING PROFIT MARGIN (Thomson Reuters data)& AFTER-TAX CORPORATE PROFIT MARGIN

(without IVA & CCAdj)

Corporate Profits After Tax*(as a percent of nominal GDP)

(blue line)Q1

S&P 500 Operating Profit MarginUsing TR Earnings**

(percent, quarterly, nsa)(red line)

Q1

Note: Shaded areas denote recessions according to the National Bureau of Economic Research.

* After-tax profits as reported to IRS excluding Inventory Valuation Adjustment (IVA) and Capital Consumption Adjustment (CCAdj), which restate thehistorical cost basis used in profits tax accounting for inventory withdrawals and depreciation to the current cost measures used in GDP.

** Operating Proft Margin derived using revenues from S&P and earnings from Thomson Reuters I/B/E/S.

Source: Standard & Poor’s, Thomson Reuters I/B/E/S and Bureau of Economic Analysis.

yardeni.com

Figure 5.

S&P 500 Revenues & Margins

Page 3 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

Figure 6.

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019900

1000

1100

1200

1300

1400

1500

900

1000

1100

1200

1300

1400

1500

18

197/5

17

S&P 500 REVENUES PER SHARE(consensus analysts estimates in dollars, weekly, ratio scale)

Consensus ForecastsAnnual RevenuesForward Revenues*

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 201950

75

100

125

150

175

200

50

75

100

125

150

175

200

7/5

17 1819

S&P 500 OPERATING EARNINGS PER SHARE(consensus analysts estimates in dollars, weekly, ratio scale)

Consensus ForecastsAnnual EarningsForward Earnings*

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20196

7

8

9

10

11

12

13

6

7

8

9

10

11

12

13

1819

7/517

yardeni.com

S&P 500 PROFIT MARGIN(using analysts average earnings and sales forecasts, percent)

Consensus Forecasts

Forward Margins* (12.2)Annual Margins

* Time-weighted average of the consensus estimates for current and next year. Source: Thomson Reuters I/B/E/S and Standard & Poor’s.

Forward Revenues, Earnings, & Margins

Page 4 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 201910

35

60

85

110

135

160

185

10

35

60

85

110

135

160

1857/5S&P 500/400/600 FORWARD EARNINGS

(dollars per share, ratio scale)

Forward Earnings*S&P 500 LargeCap (169.43)S&P 400 MidCap (119.67)S&P 600 SmallCap (59.10)

* Time-weighted average of consensus estimates for current year and next year.Source: Thomson Reuters I/B/E/S.

yardeni.com

Figure 7.

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20193

4

5

6

7

8

9

10

11

12

13

3

4

5

6

7

8

9

10

11

12

13

7/5

yardeni.com

S&P FORWARD PROFIT MARGINS*(using analysts average earnings and sales forecasts, percent)

Forward Profit Margins*S&P 500 (12.2)S&P 400 (7.7)S&P 600 (5.5)

* Time-weighted average of the consensus estimates for current and next year using forward earnings divided by forward revenues.Source: Thomson Reuters I/B/E/S and Standard & Poor’s.

Figure 8.

S&P 500/400/600 Forward Earnings & Margins

Page 5 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019600

800

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

3200

3400

600

800

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

3200

3400

x10

x11

x12

x13

x14

x15

x16

x17

x18

x19S&P 500, FORWARD EARNINGS, and VALUATION(weekly)

Actual 07/11/18Implied* 07/05/18

* Implied price index calculated using forward earnings times forward P/Es. Weekly data start January 2007.

Blue Angels: S&P 500

Source: Standard & Poor’s and Thomson Reuters I/B/E/S.

yardeni.com

Figure 9.

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019100

150

200

250

300

350

400

450

500

100

150

200

250

300

350

400

450

500

x8

x10

x12

x14

x16

ALL COUNTRY WORLD EX-US MSCI, FORWARD EARNINGS, & VALUATIONAll Country World Ex-US MSCI Index (In local currencies)07/11/18Blue Angels Implied Price Index*07/06/18

* Implied price index calculated using forward earnings times forward P/Es. Monthly through December 2005, weekly thereafter.Source: MSCI and Thomson Reuters I/B/E/S.

yardeni.com

Figure 10.

Blue Angels

Page 6 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20196

8

10

12

14

16

18

20

22

24

26

28

6

8

10

12

14

16

18

20

22

24

26

28

7/11

FORWARD P/E RATIOS FOR S&P STOCK PRICE INDEXES*(daily)

S&P 500 LargeCap (16.4)S&P 400 MidCap (16.6)S&P 600 SmallCap (17.7)

* Daily stock price index divided by 52-week forward consensus expected operating earnings per share.Source: Thomson Reuters I/B/E/S and Standard & Poor’s.

yardeni.com

Figure 11.

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20195

10

15

20

25

5

10

15

20

25

7/5

MSCI FORWARD P/E(weekly)

Forward P/E*

EMU (13.2)Emerging Markets (11.1)

US (16.3)

Japan (12.5)UK (13.1)

Capped at 20

yardeni.com

* Price divided by 12-month forward consensus expected operating earnings per share.Source: Thomson Reuters I/B/E/S.

Figure 12.

Valuation

Page 7 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 208

12

16

20

24

28

32

8

12

16

20

24

28

32

Q1

May

S&P 500 P/E RATIOSS&P 500 P/Es

Trailing (using operating earnings)* (20.7)Forward** (16.5)

* Using quarterly average of daily data for S&P 500 price index, and 4-quarter trailing operating earnings.** S&P 500 stock price index divided by S&P 500 12-month forward consensus expected operating earnings.

Source: Thomson Reuters I/B/E/S and Standard & Poor’s.

yardeni.com

Figure 13.

52 54 56 58 60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22-3

0

3

6

9

12

-3

0

3

6

9

12

S&P 500 REPORTED EARNINGS YIELD* MINUS CPI INFLATION RATE**

Q1

Latest (2.6)Average 3.3

* S&P 500 reported earnings as a percent of quarterly average S&P 500 index. Q4-2008 dropped because of negative value.** Year-over-year percent change in three-month average of each quarter.

Note: Shaded red areas denote S&P 500 bear market declines of 20% or more. Yellow areas show bull markets.Source: Standard & Poor’s and Bureau of Labor Statistics.

yardeni.com

Figure 14.

Valuation

Page 8 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

Figure 15.

06 07 08 09 10 11 12 13 14 15 16 17 18 198

10

12

14

16

18

20

7/5

S&P 500(forward P/E) P/E (16.1)

06 07 08 09 10 11 12 13 14 15 16 17 18 198

11

14

17

20

23

7/5

INDUSTRIALS(15.5)

06 07 08 09 10 11 12 13 14 15 16 17 18 1910

15

20

25

30

7/5

CONSUMER DISCRETIONARY

(20.3)

06 07 08 09 10 11 12 13 14 15 16 17 18 198

12

16

20

24

7/5

INFORMATION TECHNOLOGY(17.9)

06 07 08 09 10 11 12 13 14 15 16 17 18 1910

12

14

16

18

20

22

7/5

CONSUMER STAPLES(16.9)

06 07 08 09 10 11 12 13 14 15 16 17 18 195

10

15

20

25

7/5

MATERIALS(15.1)

06 07 08 09 10 11 12 13 14 15 16 17 18 195

15

25

35

45

55

65

7/5

ENERGY(17.2)

06 07 08 09 10 11 12 13 14 15 16 17 18 1915

25

35

45

55

65

75

7/5

REAL ESTATE(38.6)

06 07 08 09 10 11 12 13 14 15 16 17 18 196

8

10

12

14

16

18

20

7/5

FINANCIALS

Includes Real Estatethrough September 2016

(12.0)

06 07 08 09 10 11 12 13 14 15 16 17 18 198

10

12

14

16

18

20

22

7/5

TELECOMMUNICATION SERVICES(10.3)

06 07 08 09 10 11 12 13 14 15 16 17 18 198

10

12

14

16

18

20

7/5

HEALTH CARE

Source: Thomson Reuters I/B/E/S and Standard & Poor’s.

(15.0)

06 07 08 09 10 11 12 13 14 15 16 17 18 198

10

12

14

16

18

20

7/5

yardeni.com

UTILITIES(16.5)

S&P 500 Sectors Forward P/Es

Page 9 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

Figure 16.

2015 2016 2017 2018500550600650700750800850900950

CONSUMER DISCRETIONARY 7/11

S&P 500 sectorprice indexes

2015 2016 2017 2018400

500

600

700

800

INDUSTRIALS

7/11

2015 2016 2017 2018450

500

550

600

650

CONSUMER STAPLES

7/11

2015 2016 2017 2018600

800

1000

1200

1400

INFORMATION TECHNOLOGY 7/11

2015 2016 2017 2018350

425

500

575

650

725

ENERGY

7/11

2015 2016 2017 2018200

250

300

350

400

450

MATERIALS

7/11

2015 2016 2017 2018250

300

350

400

450

500

550

600

FINANCIALS

7/11

2015 2016 2017 2018125

150

175

200

225

TELECOMMUNICATION SERVICES

7/11

2015 2016 2017 2018700750800850900950

1000105011001150

HEALTH CARE

7/11

Source: Standard & Poor’s and Haver Analytics.

2015 2016 2017 2018200

225

250

275

300

UTILITIES

7/11

yardeni.com

S&P 500 Sectors Price Indexes

Page 10 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

Figure 17.

06 07 08 09 10 11 12 13 14 15 16 17 18 1960

90

120

150

180210

18 19 7/5S&P 500(forward earnings*)

Annual consensusestimatesForward earnings

06 07 08 09 10 11 12 13 14 15 16 17 18 1913

19

25

31

3743

1819 7/5INDUSTRIALS

06 07 08 09 10 11 12 13 14 15 16 17 18 195

17

29

4153

18 19 7/5CONSUMER DISCRETIONARY

06 07 08 09 10 11 12 13 14 15 16 17 18 1915

30

45

60

75

1819

7/5INFORMATION TECHNOLOGY

06 07 08 09 10 11 12 13 14 15 16 17 18 1913

19

25

31

37

18 19 7/5CONSUMER STAPLES

06 07 08 09 10 11 12 13 14 15 16 17 18 196

12

18

24

30

18 197/5MATERIALS

06 07 08 09 10 11 12 13 14 15 16 17 18 198

28

48

6888

108

18 197/5

ENERGY

06 07 08 09 10 11 12 13 14 15 16 17 18 191

3

5

79

19 7/517 18REAL ESTATE

06 07 08 09 10 11 12 13 14 15 16 17 18 198

20

32

4456

1819 7/5

FINANCIALS

Includes Real Estatethrough September 2016

06 07 08 09 10 11 12 13 14 15 16 17 18 197

9

11

13

15

17

1819

7/5TELECOMMUNICATIONS SERVICES

06 07 08 09 10 11 12 13 14 15 16 17 18 1920

35

50

65

80

18 19 7/5HEALTH CARE

* Time-weighted average (in blue) of consensus operating earnings estimates for current and next year (in red). Source: Thomson Reuters I/B/E/S.

06 07 08 09 10 11 12 13 14 15 16 17 18 1911

12

13

14

15

161718

1819 7/5

UTILITIES

yardeni.com

S&P 500 Sectors Forward Earnings

Page 11 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

0

600

1200

1800

2400

3000

3600

0

600

1200

1800

2400

3000

3600

Q2

Q1

Jun

Q2

Q1

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 20203

4

5

6

7

8

9

10

11

12

13

3

4

5

6

7

8

9

10

11

12

13

7/6

7/6

S&P 500 DIVIDENDS & BUYBACKS(billion dollars, annualized)

Buybacks

Dividends

S&P 500 Index

S&P 500 FORWARD EARNINGS YIELD & CORPORATE BOND YIELD(percent)

Investment GradeCorporate Bond Yield** (4.1)

S&P 500 Forward Earnings Yield* (6.1)

* Forward earnings (time-weighted average of consensus operating earnings estimates for current and next year) divided by S&P 500 index.** BoA Merrill Lynch data for AA-AAA yields.

Source: Thomson Reuters I/B/E/S, Federal Reserve Board, and Standard & Poor’s.

yardeni.com

Figure 18.

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20190

50

100

150

200

250

300

350

400

0

50

100

150

200

250

300

350

400

May

EQUITY ETFs*(yearly net inflows, billion dollars)

* Net share issuance by equity ETFs.Source: Investment Company Institute.

yard

eni.

com

Figure 19.

Equity Flows

Page 12 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 2080

90

100

110

120

130

100

200

300

400

500

600

700

800

900

1000

7/11

7/11

S&P GOLDMAN SACHS COMMODITY INDEX & TRADE-WEIGHTED DOLLAR(daily)

Goldman SachsCommodity Index(nearby futures price)

JP Morgan NominalBroad EffectiveExchange Rate*

Source: Standard & Poor’s, JP Morgan, and Haver Analytics.

yardeni.com

Figure 20.

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 202020

30

40

50

60

70

80

90

100

110

120

130

140

150

160

130

125

120

115

110

105

100

95

90

85

7/11

7/11

BRENT CRUDE OIL PRICE & TRADE-WEIGHTED DOLLAR

JP Morgan NominalBroad Effective Exchange Rate**(inverted scale)

Brent Crude Oil Futures Price*(dollars per barrel)

* Nearby futures price.** Argentina, Australia, Brazil, Bulgaria, Canada, Chile, China, Colombia, Croatia, Czech Republic, Denmark, Ecuador, Egypt, France, Germany, Hong Kong,

Hungary, Japan, India, Indonesia, Israel, Italy, Korea, Kuwait, Malaysia, Mexico, Morocco, New Zealand, Nigeria, Norway, Pakistan, Panama, Peru,Philippines, Poland, Romania, Russia Saudi Arabia, Singapore, South Africa, Spain, Sweden, Switzerland, Taiwan, Thailand, Turkey, United Kingdom,Ukraine, Uruguay, Venezuela, Vietnam, and United States. Source: JP Morgan and Haver Analytics.

yardeni.com

Figure 21.

Dollar & Commodities

Page 13 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019600

800

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

80

90

100

110

120

130

140

150

160

170

180

190

200

210

6/30

S&P 500 INDEX & YRI WEEKLY LEADING INDEX

S&P 500 Index

YRI Weekly Leading Index*

* Average of Consumer Comfort Index (which is a four-week average) and the four-week average of Boom-Bust Barometer, which is CRB raw industrialsspot price index (weekly average) divided by weekly initial unemployment claims.Source: Bloomberg, Commodity Research Bureau, Bureau of Labor Statistics, and Standard & Poor’s.

yardeni.com

Figure 22.

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 200

500

1000

1500

200

300

400

500

600

700

7/11

7/11

EMERGING MARKETS MSCI STOCK PRICE INDEX (in dollars)& INDUSTRIALS COMMODITY PRICE INDEX(daily)

Emerging MarketsMSCI Stock Price Index(in dollars)

CRB Raw IndustrialsSpot Price Index*

* Includes copper scrap, lead scrap, steel scrap, tin, zinc, burlap, cotton, print cloth, wool tops, hides, rosin, rubber, and tallow.Source: MSCI and Commodity Research Bureau.

yardeni.com

Figure 23.

Stocks & Commodities

Page 14 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

1800 1810 1820 1830 1840 1850 1860 1870 1880 1890 1900 1910 1920 1930 1940 195020

40

60

80

100

20

40

60

80

100CONSUMER PRICE INDEX*: 1800-1947

War of 1812(1812-1815)

Civil War(1861-1865)

World War I(1914-1918)

World War II(1939-1945)

* Annual data. Base index from 1800 to 1947 is 1967 = 100.** 1982-84=100.

Source: Census Bureau, Historical Statistics of the United States

yardeni.com

1948 1958 1968 1978 1988 1998 2008 2018 20280

50

100

150

200

250

300

0

50

100

150

200

250

300

MayCPI**Cold War(1947-1989)

Figure 24.

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 220

1

2

3

4

5

6

7

8

9

10

11

34

36

38

40

42

44

46

48

50

52

May

AGE WAVE & INFLATION

Inflation Trend**

Age Wave*

Source: Bureau of Labor Statistics.** Five-year moving average of yearly percent change in CPI.* Percent of labor force 16-34 years old.

yardeni.com

Figure 25.

Big Picture

Page 15 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20194.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

Jun

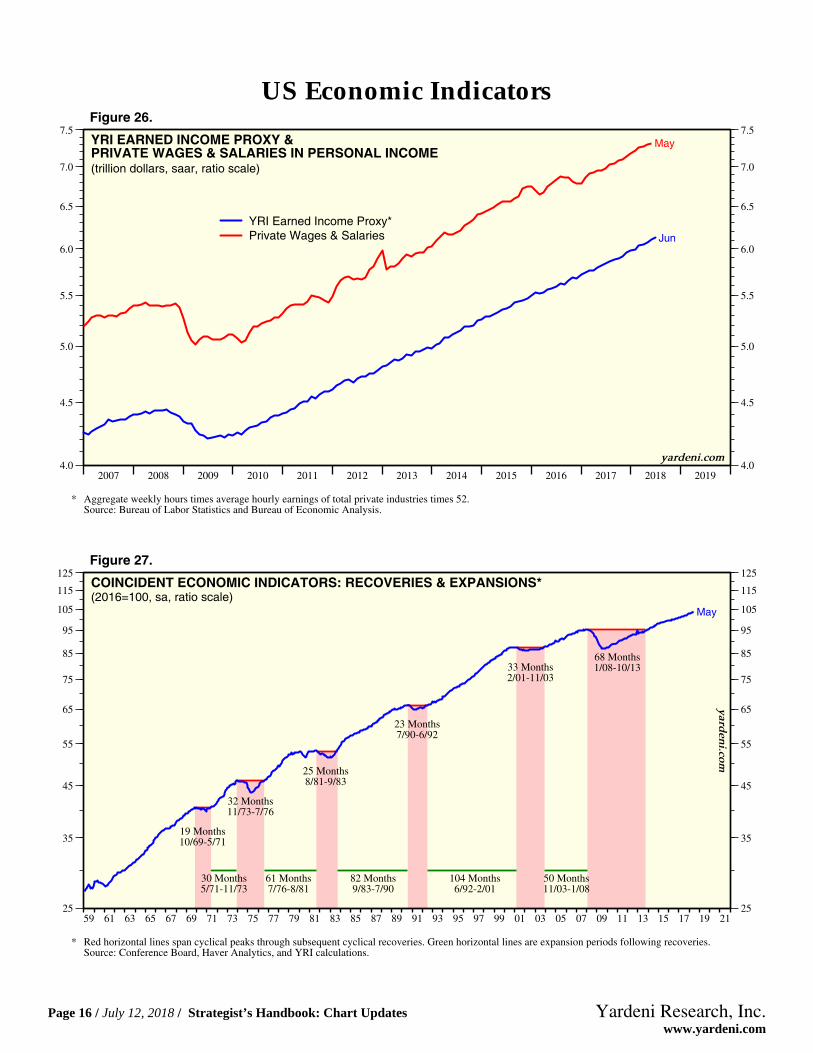

MayYRI EARNED INCOME PROXY &PRIVATE WAGES & SALARIES IN PERSONAL INCOME(trillion dollars, saar, ratio scale)

YRI Earned Income Proxy*Private Wages & Salaries

* Aggregate weekly hours times average hourly earnings of total private industries times 52.Source: Bureau of Labor Statistics and Bureau of Economic Analysis.

yardeni.com

Figure 26.

59 61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 2125

35

45

55

65

75

85

95

105

115

125

25

35

45

55

65

75

85

95

105

115

125

68 Months1/08-10/1333 Months

2/01-11/03

23 Months7/90-6/92

25 Months8/81-9/83

32 Months11/73-7/76

19 Months10/69-5/71

30 Months5/71-11/73

61 Months7/76-8/81

82 Months9/83-7/90

104 Months6/92-2/01

50 Months11/03-1/08

May

COINCIDENT ECONOMIC INDICATORS: RECOVERIES & EXPANSIONS*(2016=100, sa, ratio scale)

* Red horizontal lines span cyclical peaks through subsequent cyclical recoveries. Green horizontal lines are expansion periods following recoveries.Source: Conference Board, Haver Analytics, and YRI calculations.

yarden

i.com

Figure 27.

US Economic Indicators

Page 16 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 2040

60

80

100

120

140

40

60

80

100

120

140

2016

2017

REAL CONSUMER INCOME & SPENDING PER HOUSEHOLD*(thousand 2009 dollars, saar)

Real Income & Spending per Household*Personal Income (122.3)Personal Consumption Expenditures (99.7)Disposable Personal Income (107.0)Money Income** (75.0)

* All series deflated using Personal Consumption Expenditures Deflator.** Mean household income.

Source: Bureau of Economic Analysis, Bureau of the Census and Current Population Reports.

yardeni.com

Figure 28.

48 50 52 54 56 58 60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 2210

20

30

40

50

60

70

8090100110120130140150

10

20

30

40

50

60

70

8090

100110120130140150

CMANUFACTURING PRODUCTION & CAPACITY

(2012=100, ratio scale)May

May

ManufacturingProductionCapacity

yardeni.com

Note: C = China joined WTO on December 11, 2001. Shaded areas denote recessions according to the National Bureau of Economic Research.Source: Federal Reserve Board.

Figure 29.

US Economic Indicators

Page 17 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20-10

-5

0

5

10

15

20

25

-10

-5

0

5

10

15

20

25

May

Jun

CHINA: INDUSTRIAL PRODUCTION & PRODUCER PRICE INDEX(yearly percent change)

Industrial Production* (6.8)PPI: TotalIndustrial Products (4.7)

* Value added basis.Source: IMF International Financial Statistics and China National Bureau of Statistics.

yardeni.com

Figure 30.

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20190

5

10

15

20

25

30

0

5

10

15

20

25

30

May

May

May

BANK LOANS & MONEY SUPPLY(trillion US dollars)

China: Bank Loans (nsa) (20.0)US: Bank Loans (sa) (9.3)China: M2 (27.3)

Source: Federal Reserve Board and People’s Bank of China.

yardeni.com

Figure 31.

China

Page 18 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 202050

60

70

80

90

100

110

120

130

50

60

70

80

90

100

110

120

130EUROZONE: INDUSTRIAL PRODUCTIONEXCLUDING CONSTRUCTION(January 2006=100)

Germany (May=119.0)France (May=93.0)Italy (May=87.6)Spain (May=81.8)

Eurozone (Apr=103.9)

Source: Haver Analytics.

yardeni.com

Figure 32.

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019-8

-6

-4

-2

0

2

4

6

60

70

80

90

100

110

120

130

Jun

EUROZONE: ECONOMIC SENTIMENT INDICATOR* & REAL GDP

Real GDP(yearly percent change) (2.5)

Economic Sentiment Indicator*(long-term average=100, sa) (112.3)

* The overall economic sentiment indicator (ESI) is derived from the industrial (weight 40%), service (30%), consumer (20%), construction (5%), andretail trade (5%) confidence indicators.Source: Statistical Office of the European Communities, European Commission, and Haver Analytics.

yardeni.com

Figure 33.

Eurozone

Page 19 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 2022

20

18

16

14

12

10

8

6

4

2

0

-2

-4

-6

-8

-10

-12

-14

-16

-18

-20

-22

-2

-1

0

1

2

May

7/6

IMPLIED WORLD EX-US CAPITAL FLOWS & TRADE-WEIGHTED DOLLAR

JP Morgan NominalBroad EffectiveExchange Rate(inverted scale,yearly percent change)

Implied World Ex-USCapital Flows*(trillion dollars)

* 12-month change in non-gold international reserves minus 12-month sum of the merchandise trade surplus (deficit). US trade deficit multiplied by -1.0.Source: International Monetary Fund and JP Morgan.

yardeni.com

Figure 34.

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 20203

4

5

6

7

8

9

10

11

12

13

14

15

16

600

800

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

QE1 QE2 QE3

S&P 500 INDEX & QE7/11

S&P 500 Index

Total ofFed, ECB, BOJ

Note: QE1 (11/25/08) = Fed starts buying $1.24tn in mortgage securities. QE1 expanded (3/16/2009) = Fed starts buying $300bn in Treasuries.QE2 (11/3/10) = Fed starts buying $600bn in Treasuries. QE3 (9/13/12) = Fed starts buying $40bn/month in mortgage securities (open ended).QE3 expanded (12/12/12) = Fed starts buying $45bn/month in Treasuries.Source: Federal Reserve Board, Standard & Poor’s and Haver Analytics.

yardeni.com

Figure 35.

Global

Page 20 / July 12, 2018 / Strategist’s Handbook: Chart Updates www.yardeni.com

Yardeni Research, Inc.

http://blog.yardeni.com

http://blog.yardeni.com

Copyright (c) Yardeni Research, Inc. 2018. All rights reserved. The informationcontained herein has been obtained from sources believed to be reliable, but is notnecessarily complete and its accuracy cannot be guaranteed. No representation orwarranty, express or implied, is made as to the fairness, accuracy, completeness, orcorrectness of the information and opinions contained herein. The views and the otherinformation provided are subject to change without notice. All reports posted onwww.yardeni.com, blog.yardeni.com, and YRI’s Apps for iPads and iPhones are issuedwithout regard to the specific investment objectives, financial situation, or particular needsof any specific recipient and are not to be construed as a solicitation or an offer to buy or sellany securities or related financial instruments. Past performance is not necessarily a guideto future results. Company fundamentals and earnings may be mentioned occasionally, butshould not be construed as a recommendation to buy, sell, or hold the company’s stock.Predictions, forecasts, and estimates for any and all markets should not be construed asrecommendations to buy, sell, or hold any security--including mutual funds, futurescontracts, and exchange traded funds, or any similar instruments.

The text, images, and other materials contained or displayed on any Yardeni Research, Inc.product, service, report, email or website are proprietary to Yardeni Research, Inc. andconstitute valuable intellectual property. No material from any part of www.yardeni.com, blog.yardeni.com, and YRI’s Apps for iPads and iPhones may be downloaded, transmitted,broadcast, transferred, assigned, reproduced or in any other way used or otherwisedisseminated in any form to any person or entity, without the explicit written consent ofYardeni Research, Inc. All unauthorized reproduction or other use of material from YardeniResearch, Inc. shall be deemed willful infringement(s) of this copyright and other proprietaryand intellectual property rights, including but not limited to, rights of privacy. YardeniResearch, Inc. expressly reserves all rights in connection with its intellectual property,including without limitation the right to block the transfer of its products and services and/orto track usage thereof, through electronic tracking technology, and all other lawful means,now known or hereafter devised. Yardeni Research, Inc. reserves the right, without furthernotice, to pursue to the fullest extent allowed by the law any and all criminal and civilremedies for the violation of its rights.

The recipient should check any email and any attachments for the presence of viruses.Yardeni Research, Inc. accepts no liability for any damage caused by any virus transmittedby this company’s emails, website, blog and Apps. Additional information available onrequest.