Embed Size (px)

Citation preview

Strategies to Navigate the “Play or Pay” Tax

Presented By:

Arthur Tacchino, JD

© 2011, National Association of Health Underwriters • www.nahu.org

© 2011, National Association of Health Underwriters • www.nahu.org

“Play or Pay” Penalty Tax

Employer Shared Responsibility Tax

© 2011, National Association of Health Underwriters • www.nahu.org

Play or Pay Tax

• Effective beginning in 2014

• Tax will be applicable to those employers that:

– Fail to offer healthcare coverage (Not Offering

Employer)

– Offer minimum essential coverage that is

“unaffordable” (Offering Employer)

© 2011, National Association of Health Underwriters • www.nahu.org

Who is Subject to this Tax?

• Applicable Large Employers

– 50 or more full-time equivalent employees in preceding

year

• Full-time = works more than 30 hours a week

• Equivalent employees = Non-full-timers hours/120 each month

• Add # of full-timers to equivalent employees = # of FTEs

– If employer was not in existence in previous year then

# of EE’s is based on expected EE’s this year

© 2011, National Association of Health Underwriters • www.nahu.org

Calculating FTEs

• Monthly calculation: average monthly FTEs at the end

of the year

• Example: 45 full-time employees

• 15 part-time employees: working 15 hours a week

• Total of 900 hours for the month/ 120 (statutorily

given)

• 7.5 equivalent employees + 45 full-timers

• =52.5 full-time equivalent employees for the month

© 2011, National Association of Health Underwriters • www.nahu.org

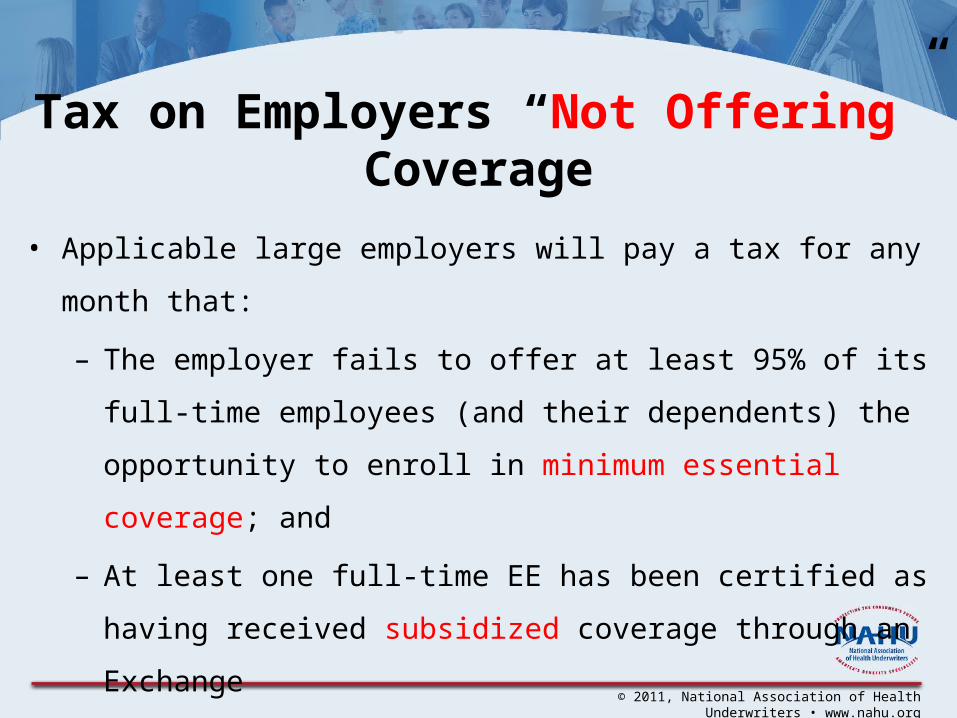

Tax on Employers “Not Offering” Coverage

• Applicable large employers will pay a tax for any month that:

– The employer fails to offer at least 95% of its full-time

employees (and their dependents) the opportunity to enroll in

minimum essential coverage; and

– At least one full-time EE has been certified as having received

subsidized coverage through an Exchange

• Tax is equal to $166.67 per month or $2,000 per year

© 2011, National Association of Health Underwriters • www.nahu.org

Calculating the Tax :Not Offering Coverage• ABC Inc. drops coverage in 2014

• They have 100 full-time employees (*not full-time equivalent

employees)

• At least 1 full-time employee (only takes 1) goes to

exchange, is eligible for subsidy and enrolls in qualified health

plan with subsidy

• Tax is triggered – employer is notified

• Tax calculated on a monthly basis

© 2011, National Association of Health Underwriters • www.nahu.org

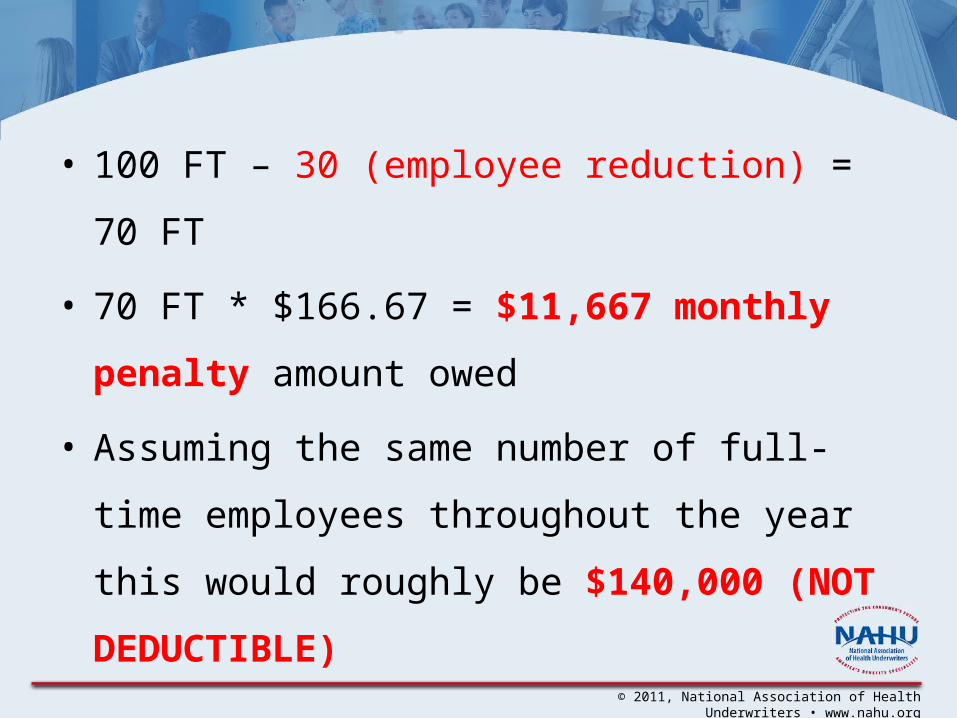

• 100 FT – 30 (employee reduction) = 70 FT

• 70 FT * $166.67 = $11,667 monthly penalty

amount owed

• Assuming the same number of full-time

employees throughout the year this would

roughly be $140,000 (NOT DEDUCTIBLE)

© 2011, National Association of Health Underwriters • www.nahu.org

Tax on “Offering Employers”• An “applicable large employer” will pay a penalty tax for

any month that:

– The employer offers to at least 95% of its full-time (and their

dependents) employees the opportunity in minimum essential

coverage under an eligible employer-sponsored plan for that month;

and

– At least one full-time employee of the employer has been certified to

have received subsidized coverage through an Exchange

• The tax is equal to $250 per employee receiving subsidized

coverage through the exchange per month

© 2011, National Association of Health Underwriters • www.nahu.org

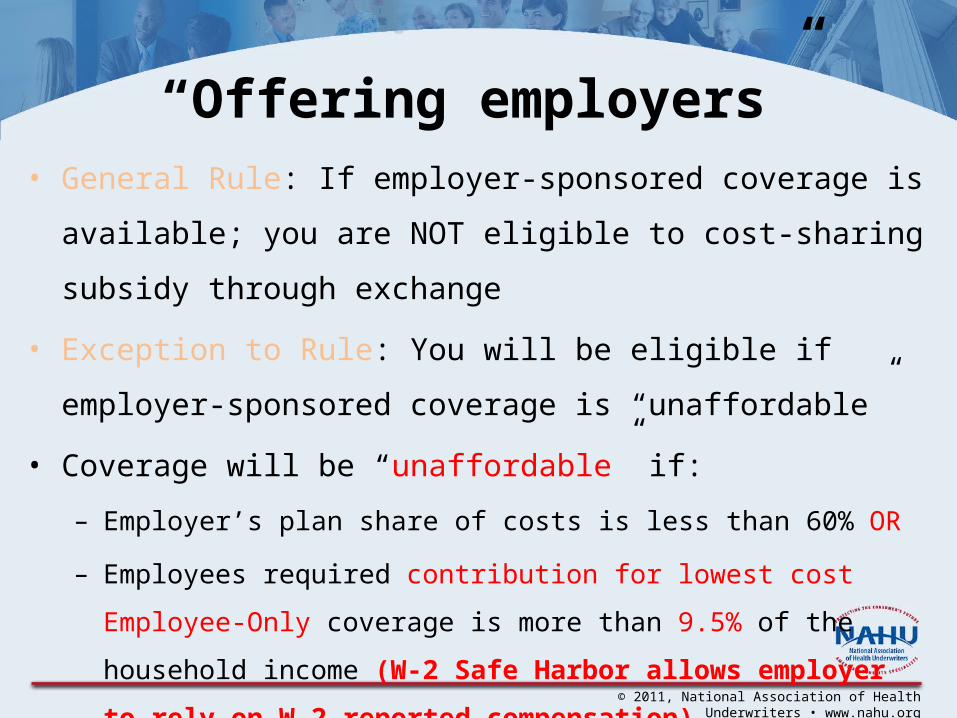

“Offering employers”• General Rule: If employer-sponsored coverage is available;

you are NOT eligible to cost-sharing subsidy through exchange

• Exception to Rule: You will be eligible if employer-sponsored

coverage is “unaffordable”

• Coverage will be “unaffordable” if:

– Employer’s plan share of costs is less than 60% OR

– Employees required contribution for lowest cost Employee-Only

coverage is more than 9.5% of the household income (W-2 Safe

Harbor allows employer to rely on W-2 reported compensation)

© 2011, National Association of Health Underwriters • www.nahu.org

Calculating the Tax: Offering Employer• ABC co. offers coverage in 2014: Required employee contribution for

lowest-cost employee only coverage is $4,000

• Rick is full-time and makes $35,000 (i.e. employer plan is more than

9.5% of his wages)

• Rick goes to exchange and receives affordability waiver after proving

employer plan is unaffordable

• Rick is eligible for subsidy based on household income, and enrolls in

qualified health plan

• $250 x 1 full-time employee = $250 monthly penalty for

employer

© 2011, National Association of Health Underwriters • www.nahu.org

Measurement Periods

• Ongoing employee, New Employee,

Variable Hourly employee

• 3 to 12 month length

• Tracking the hours worked by these

employees

• Determines whether they are “full-time” and

thus qualify during tax calculation

© 2011, National Association of Health Underwriters • www.nahu.org

Administrative Period

• Employer chooses 0 to 3 month period

• Total length of measurement and admin

period cannot exceed 13 months

• Time during which employer averages

hours worked by employees

© 2011, National Association of Health Underwriters • www.nahu.org

Stability Period

• The longer of 6 months or the length of the

measurement period

• During this timeframe, any employee that

averaged 30 or more hours worked a week during

measurement period is considered full-time,

regardless of how many hours they are working in

the actual timeframe

© 2011, National Association of Health Underwriters • www.nahu.org

Notes on Play or Pay Tax• Penalty tax is not deductible

• Transitional relief granted to plans that start on fiscal year

basis rather than calendar year

• If a “dependent” of a full-time employee receives subsidized

coverage through an exchange the tax is NOT triggered

• FTE Calculations drop the fraction – 49.8 is really 49 FTEs

• Aggregation rules apply when determining if employer is an

“applicable large employer”, but not for penalty assessment

© 2011, National Association of Health Underwriters • www.nahu.org

• Full-time employees that are not “offered” coverage

b/c they are in their 90 day waiting period do not count

for penalty assessment

• Full-time employees (and their dependents) – means

covering children up to age 26 – does not means

covers spouse

© 2011, National Association of Health Underwriters • www.nahu.org

• “Applicable large employers” will be required to

submit information reports – effective 2015 for 2014

plan year information

• Affordability Safe Harbors (9.5% of W-2 wages)

– W-2 Safe Harbor

– Rate of Pay Safe Harbor

– Federal Poverty Line Safe Harbor

© 2011, National Association of Health Underwriters • www.nahu.org

Strategies

• Continue offering coverage

• Decreasing Employer Contributions

• Stay under 50 FTE’s

• Drop Coverage

– Employee turnover, increased salaries, payroll

taxes, morale, productivity

• Sift full-timers to part-time status

© 2011, National Association of Health Underwriters • www.nahu.org

What will employers do?

© 2011, National Association of Health Underwriters • www.nahu.org

Q&A