Embed Size (px)

Citation preview

strategic report

Key trends 10

Our profile 12

Strategic priorities 17

Strategic governance 22

In a challenging economic and regulatory environment, our strategy should address the opportunities and threats presented by our environment. This report highlights selected trends, our profile, strategic priorities and our achievements so far.

IntroductionBusiness Report

Risk & Capital Report

Governance ReportAnnual Financial Statem

entsOther

Strategic Report9

ABN AMRO Group Annual Report 2014

Strategic Report

key trendsThis selection of trends could affect ABN AMRO’s strategy, execution and business model going forward.

Macroeconomic trendsAfter having contracted for the previous two years, gross

domestic product (GDP) in the eurozone inched up in

2014. Unlike in 2012 and 2013, growth of the Dutch

economy kept pace with the eurozone, growing slightly

in 2014. Private consumption and investment in the

Netherlands picked up. The export sector was once

again the pacesetter, having benefitted from an upturn

in global trade.

The prospects for the Dutch economy in 2015 look

positive. The United States is expected to remain on its

steady growth path, and emerging economies and the

eurozone could benefit from this. Lower energy prices and

a depreciated euro are expected to help the Netherlands

achieve higher growth in all market sectors in 2015 than in

2014, as the domestic drags on the economy (housing

market, government cutbacks and pension problems)

have clearly weakened.

ABN AMRO is particularly sensitive to the state of the

Dutch economy, an open and mature market well

positioned for recovery, though with limited upside in

GDP growth. This underlines the strategic importance

of maintaining our strong capital and liquidity position,

while selectively growing the business outside of

the Netherlands.

On a broader level, we will continue to monitor

the following risks (in random order):

Å re-ignition of the euro crisis;

Å risk of deflation in the eurozone;

Å interest rate increases in the US;

Å hard landing of China’s economy;

Å contagion effects from geopolitical developments

around Europe, Asia, the Middle East and Russia;

Å potential effects of the ECB’s Quantitative Easing (QE).

Regulatory and supervisory trendsUnder the Single Supervisory Mechanism (SSM)

implemented in November 2014, prudential supervision

over the largest banks established in EU member

states has been transferred to the ECB. The ECB is

expected to dominate the regulatory agenda and to

focus on topics besides capital, liquidity and risk exposure

amounts. Supervision is moving from principles-based to

rules-based standards and is expected to be much more

data driven.

The complexity and number of regulations is expected to

further increase. The evolving regulatory and supervisory

landscape in the European Union (EU) is challenging for

banks and there are concerns that this may lead to an

uneven playing field with banks in other regions, such as

the US and Asia.

ABN AMRO strongly focuses on timely implementation

of and compliance with new rules and regulations in

a cost-effective manner.

10 Strategic Report Key trends

Key trends

Technological trendsClients increasingly prefer to use digital solutions and

demand a multi-channel approach. Technological

developments in areas such as mobile banking, social

media, data analytics (‘big data’) and cloud computing

create opportunities for banks to respond to changing

client behaviour and needs.

The accelerating pace of innovation could pose challenges

to the business model of established banks. Leveraging

on new technologies, non-traditional banking players could

cause disruptions within short time spans. Technology

firms, which are not subject to the same regulatory

controls imposed on banks, have already entered parts

of the banking value chain. In the Dutch mortgage and

savings markets, these non-traditional players have

created increased competition.

In a world that is becoming ever more technologically

connected, the increasing risk of cybercrime is driving the

need for advanced security and detection measures.

ABN AMRO has decided to increase its investments in

technology in order to grasp opportunities to better serve

clients, create more value and respond to challenges

posed by non-traditional banking players.

Social trendsThe financial crisis damaged trust in the financial sector.

As a result of this and other factors, society expects

greater transparency in pricing, less complex products and

better value. Clients are increasingly seeking products and

services that fit their unique situation and expect a wider

range of digital solutions and direct channels. There is also

a growing demand for more environmentally friendly and

socially responsible solutions.

Social networks and cooperative platforms, combined

with a desire to be less reliant on banks, support the

existence of collaborative finance platforms such as

crowdfunding, peer-to-peer lending, social savings and

social lending.

Rapid technological advances in social media, mobile

banking, data analytics and cloud computing are helping

banks to better serve clients by using personal data to

perform individual profiling. As boundaries of privacy and

data protection are being explored, banks need to be

diligent in protecting clients’ privacy and be sensitive to

the evolving public concern and attitude towards sharing

of personal data.

IntroductionBusiness Report

Risk & Capital Report

Governance ReportAnnual Financial Statem

entsOther

Strategic Report11

ABN AMRO Group Annual Report 2014

our profileThis section presents an overview of who we are, our values and the business principles which will guide us in achieving our mission and vision. We serve retail, private and corporate banking clients based on our in-depth financial expertise and extensive knowledge of numerous industry sectors.

Description of ABN AMROABN AMRO is a full-service bank with a primary focus on

the Netherlands and selective operations internationally,

employing 22,215 full-time staff. Based on our extensive

knowledge of numerous industry sectors, we serve retail,

private and corporate banking clients and offer in-depth

financial expertise.

Operating incomeby type of income(in %)

Net interest incomeNet fee and commission incomeOther operating income

2014EUR 8,055m

4

75

21

Operating income by business segment(in %)

Retail BankingPrivate BankingCorporate BankingGroup Functions

2014EUR 8,055m

1

49

35

15

Operating income by geography(in %)

The NetherlandsRest of EuropeRest of the world

2014EUR 8,055m

7

81

12

With a long-standing history in banking and roots that

go back for centuries, ABN AMRO emerged from the

financial crisis as a leading Dutch bank. Our business

profile and international footprint have changed while

our historic roots remain. Today, we have a high degree

of focus, operating domestically and in selected

international markets under several strong brand names.

Our deep focus on the Netherlands is complemented by

international operations where we have specific expertise

and hold leading market positions in selected activities.

In the Netherlands, we are a leading player in retail,

private and corporate banking. Our client base is stable and

generates recurring and resilient operating income, of which

over 95% consists of interest, fee and commission income.

ABN AMRO targets a moderate risk profile, which is

reflected in, among other things, three key elements:

(i) a clean balance sheet, (ii) a clear risk governance

structure and strong risk culture, and (iii) a solid capital

and liquidity position. This is maintained and strengthened

by strict risk appetite targets, a controlled and focused

growth strategy for selected international activities, and

disciplined capital allocation.

12 Strategic Report Our profile

Our profile

The Managing Board and senior managing directors

collectively have over twenty years of experience in the

Group across business segments or support functions or

both. Their excellent track records are reflected in their

leading the complex integration of ABN AMRO Bank and

FBN on time and within budget while structurally reducing

our cost base. Despite the complex integration process

and the challenging economic environment at the time,

ABN AMRO has delivered resilient operating income and

created a solid capital and liquidity position with the

support of its professional and highly engaged workforce.

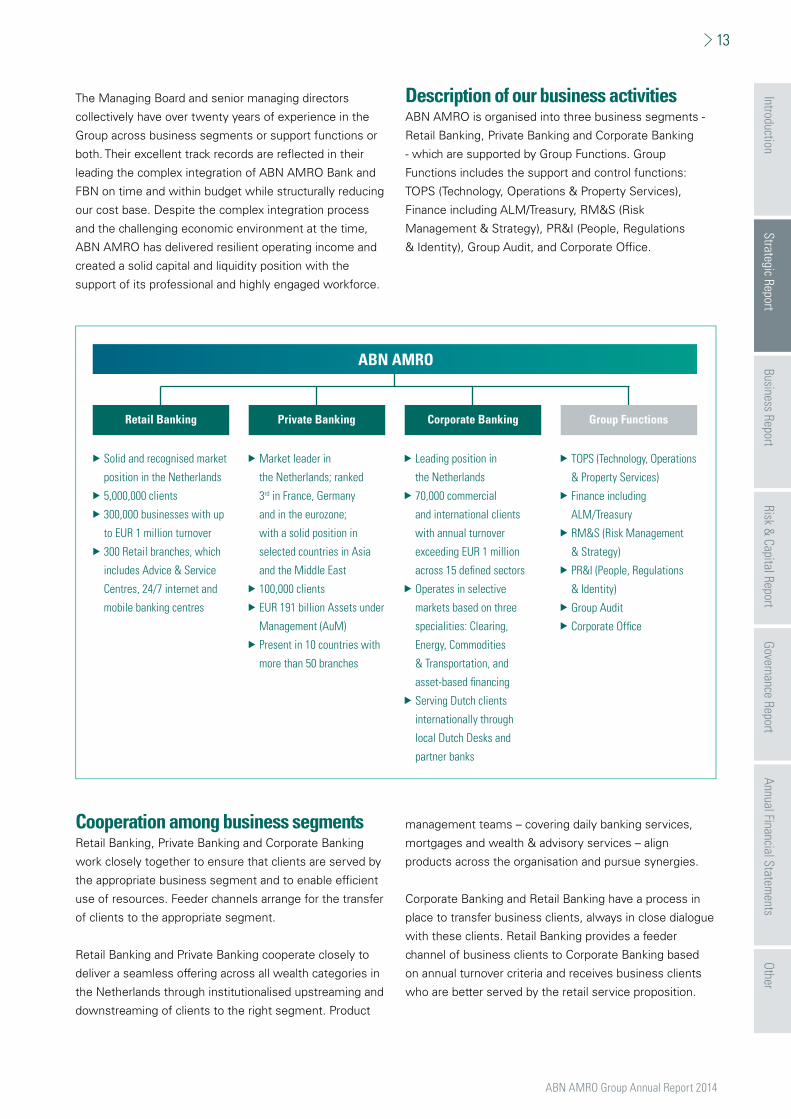

Description of our business activitiesABN AMRO is organised into three business segments -

Retail Banking, Private Banking and Corporate Banking

- which are supported by Group Functions. Group

Functions includes the support and control functions:

TOPS (Technology, Operations & Property Services),

Finance including ALM/Treasury, RM&S (Risk

Management & Strategy), PR&I (People, Regulations

& Identity), Group Audit, and Corporate Office.

Corporate Banking Group FunctionsRetail Banking Private Banking

ABN AMRO

Solid and recognised market

position in the Netherlands

5,000,000 clients

300,000 businesses with up

to EUR 1 million turnover

300 Retail branches, which

includes Advice & Service

Centres, 24/7 internet and

mobile banking centres

Market leader in

the Netherlands; ranked

3rd in France, Germany

and in the eurozone;

with a solid position in

selected countries in Asia

and the Middle East

100,000 clients

EUR 191 billion Assets under

Management (AuM)

Present in 10 countries with

more than 50 branches

Leading position in

the Netherlands

70,000 commercial

and international clients

with annual turnover

exceeding EUR 1 million

across 15 defined sectors

Operates in selective

markets based on three

specialities: Clearing,

Energy, Commodities

& Transportation, and

asset-based financing

Serving Dutch clients

internationally through

local Dutch Desks and

partner banks

TOPS (Technology, Operations

& Property Services)

Finance including

ALM/Treasury

RM&S (Risk Management

& Strategy)

PR&I (People, Regulations

& Identity)

Group Audit

Corporate Office

Cooperation among business segmentsRetail Banking, Private Banking and Corporate Banking

work closely together to ensure that clients are served by

the appropriate business segment and to enable efficient

use of resources. Feeder channels arrange for the transfer

of clients to the appropriate segment.

Retail Banking and Private Banking cooperate closely to

deliver a seamless offering across all wealth categories in

the Netherlands through institutionalised upstreaming and

downstreaming of clients to the right segment. Product

management teams – covering daily banking services,

mortgages and wealth & advisory services – align

products across the organisation and pursue synergies.

Corporate Banking and Retail Banking have a process in

place to transfer business clients, always in close dialogue

with these clients. Retail Banking provides a feeder

channel of business clients to Corporate Banking based

on annual turnover criteria and receives business clients

who are better served by the retail service proposition.

IntroductionBusiness Report

Risk & Capital Report

Governance ReportAnnual Financial Statem

entsOther

Strategic Report13

ABN AMRO Group Annual Report 2014

Private Banking and Corporate Banking cooperate mainly

by means of referrals. Corporate Banking introduces

eligible business owners, shareholders and executives

to Private Banking. Conversely, Private Banking refers

business owners and executives to Corporate Banking

for their business needs.

This cooperative environment allows for leveraging of

technology and client and product solutions.

SWOTThe following SWOT summary provides a brief overview

of ABN AMRO’s capabilities and the environment in which

it operates.

Strengths Weaknesses

Opportunities Threats

Leading player in the Dutch market as a full-service bank

with strong core and local brands

Low complexity, client-driven business model that

generates resilient operating income

Strong positions in selected international activities

Experienced senior management with a proven track

record in executing the integration of ABN AMRO Bank

and FBN, supported by a professional and highly

engaged workforce

Diversified mix of activities combined with a solid liquidity

position, well-capitalised and strong balance sheet

contributing to a moderate risk profile

Large exposure to and dependence on the Dutch economy

Growth opportunities in the Dutch home market limited

by current leading position

Solid but complex IT landscape following the integration

of ABN AMRO Bank and FBN

Suboptimal scale of businesses in a few countries

Dutch economy well-positioned to benefit from continued

momentum in the recovery in the global economy and

the eurozone

New technological developments can be leveraged

to respond to changing client behaviour and needs

Increasing client desire to be environmentally and

socially responsible provides opportunities for new

product development

Lowered barriers to enter other EU markets as a result

of the European Banking Union

Potential macroeconomic and geopolitical headwind

effects on the Netherlands and the eurozone

Mature market combined with ageing population

resulting in relatively limited GDP growth upside

Regulatory pressure, complexity and volume of regulation

New entrants in (parts of) the banking value chain

with potentially disruptive effects from the accelerating

pace of (technological) innovation

Increased competition from incumbents and

non-traditional players, especially in the mortgage

and savings markets

14 Strategic Report Our profile

Stakeholder managementABN AMRO strives to put clients’ interests first and to

create long-term, sustainable value for all of our

stakeholders, including clients, investors/shareholders,

employees, the environment and society at large. We take

the interests of these stakeholders seriously and believe it

is our responsibility to manage the impact of our activities.

In doing so, we focus on systematically balancing the

bank’s interests with those of our stakeholders. Our efforts

are discussed in the Strategic priorities section of this

Strategic Report.

ABN AMRO

Clients

Investors/Shareholders

EmployeesSociety

Environment

Regularly engaging in a dialogue helps us to identify

important areas for our stakeholders. We apply the

materiality principle when discussing sustainability topics.

This means that we focus on the issues that are most

important to our key stakeholders and to our business,

where we are actually in a position to influence

the outcomes.

IntroductionBusiness Report

Risk & Capital Report

Governance ReportAnnual Financial Statem

entsOther

Strategic Report15

ABN AMRO Group Annual Report 2014

Our core values, mission, vision and business principles

Our core values are embedded in the company culture

and reflect our identity. We want to be trusted by our

stakeholders and be professional in everything we do,

and we have the ambition to continuously improve.

Trusted Professional Ambitious

At ABN AMRO we believe trust is all

about establishing and maintaining

lasting relationships. We take the time

to get to know our clients by listening

to their specific needs and aspirations.

Our goal is to find the products and

services that are right for our clients.

When we make a promise, we always live

up to it; when we communicate with our

clients, we are always straightforward

and never have hidden agendas.

Our commitment to responsible banking

means we carefully weigh risks and returns

so that our clients know their money is in

good hands at all times.

At ABN AMRO we understand

banking. As true professionals,

we have a thorough grasp of the

banking industry and the discipline

to achieve results.

We genuinely believe in our profession and

take responsibility by saying ‘no’ if saying

‘yes’ would not do right by our clients.

We create solutions that are simple,

understandable and workable, and we

strive to improve ourselves every day by

working together and learning from one

another – and from our clients.

At ABN AMRO we are always

stretching ourselves and striving

to achieve more for our clients.

We always strive to improve

ourselves.

We make it our business to know what

is going on in the market and to respond

proactively, and we do everything possible

to understand what clients really need

and to design innovative solutions.

Our optimism about the future drives

our ambition to offer our clients more.

At ABN AMRO, we are not afraid to

venture outside our comfort zone to put

our ambition to work for our clients.

Our mission is:

Å to be successful through the success of our clients;

Å to strongly commit ourselves to and be positively

recognised for our position on sustainability and

transparency;

Å to be an organisation that has the best talent and

where people grow both professionally and personally.

Our vision is to be a professional, full-service bank with

a leadership role in the Dutch market. Internationally, we

aim to be a capability-led bank in selected businesses and

geographies. Our ambition is to be a top class employer.

Our business principles translate our core values, mission

and vision into our day-to-day actions.

I aim to provide my clients with the best solutions

I take responsibility

I only take risksI understand

I build relationships through collaboration

I am a passionateprofessional

I am committed to sustainablebusiness practices

16 Strategic Report Our profile

strategic priorities

Strategic priorities

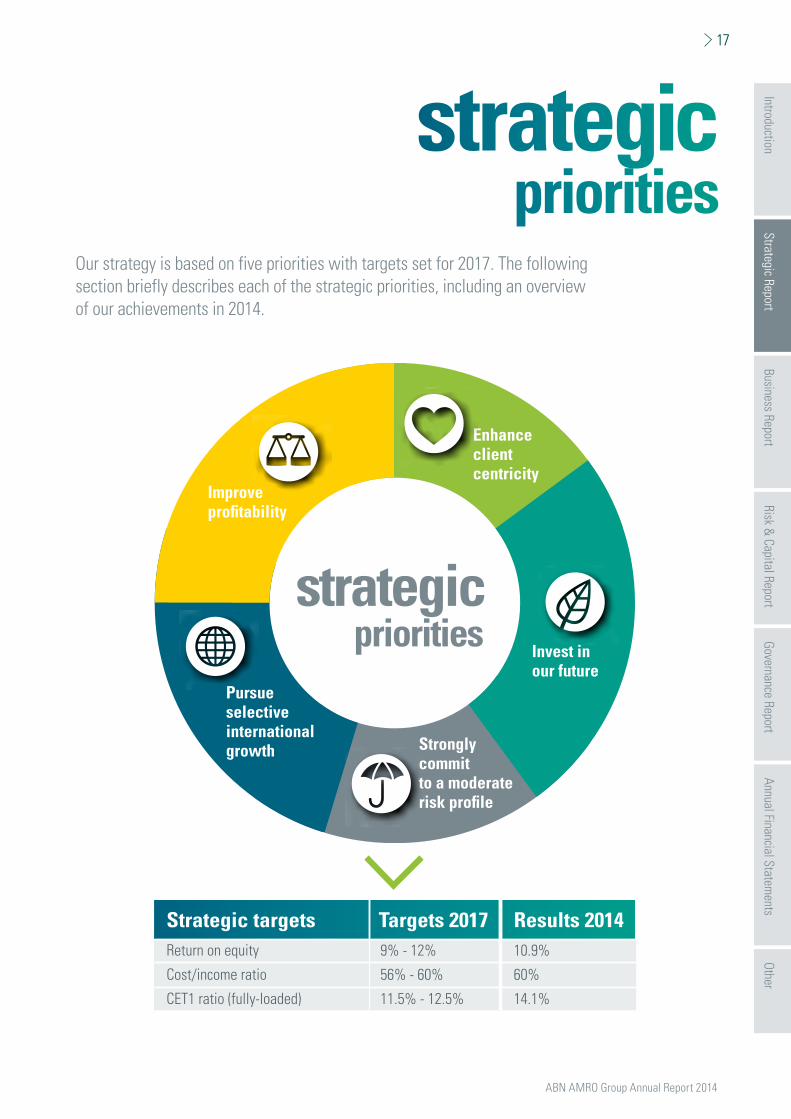

Our strategy is based on five priorities with targets set for 2017. The following section briefly describes each of the strategic priorities, including an overview of our achievements in 2014.

Enhanceclientcentricity

Invest inour future

Strongly committo a moderate risk profile

Pursueselectiveinternationalgrowth

Improveprofitability

strategicpriorities

Strategic targets Results 2014Targets 2017Return on equity

Cost/income ratio

CET1 ratio (fully-loaded)

9% - 12%

56% - 60%

11.5% - 12.5%

10.9%

60%

14.1%

IntroductionBusiness Report

Risk & Capital Report

Governance ReportAnnual Financial Statem

entsOther

Strategic Report17

ABN AMRO Group Annual Report 2014

Five strategic priorities

Quality and relevance of adviceUsing technology to better serve our clientsContinue Customer Excellence

Optimise balance sheetFurther diversificationGood capital and liquidity position

Capability-ledFitting moderate risk profileFitting efficiency focus

Improve top-line revenuesContinuous focus on costsManage on the basis of risk-adjusted return

Enhance client centricity

Strongly commit to a moderate risk profile

Pursue selective international growth

Improve profitability

Invest in our futureRe-engineer IT landscape & optimising processesPositively recognised on sustainability and transparencyRecognised as top class employer

Enhance client centricity ABN AMRO aims to stand out from other banks based

on the quality and relevance of our advice and services.

We intend to further distinguish ourselves by enhancing

our need-based client segmentation and providing

solutions that suit our clients’ unique situations.

In response to changing client needs in the Netherlands,

we have implemented changes in our retail branch opening

hours across the country, introducing evening and weekend

hours. We have also extended our webcam advisory

services to offer our clients greater flexibility and

convenience. The digital Retail Banking platform is also

used for the Private Banking website and app design in the

Netherlands. Outside the Netherlands, we are developing

an ambitious digital offering consisting of a blend of

omni-channel services combined with personal interaction.

We have introduced environmental, social and governance

(ESG) criteria in our investment processes, developed

a sustainability indicator to help private banking clients

make informed investment decisions and launched socially

responsible products.

We continued to raise financial awareness through

our Carefree Living (Zorgeloos Wonen) programme,

by reaching out to an additional 25,000 clients facing

potential arrears in 2014.

A strategic review was conducted for Capital Markets

Solutions, resulting in the winding down of our Equity

derivatives activities and a shift within Sales & Trading from

a product-oriented focus to a more client-oriented focus.

18 Strategic Report Strategic priorities

We enhanced our sector-based approach in Corporate

Banking to ensure that each client is assigned to one of

the 15 sectors, benefiting from the pooling of knowledge

and specialised services.

Throughout the year, we continued to focus on Customer

Excellence (CE). Combining customer focus with

operational excellence, this was applied across products

and businesses in several countries.

We continuously take bank-wide initiatives to put our

clients’ interests centre stage in everything we do. In the

annual client satisfaction survey, the score for client

centricity rose from 52% to 53%, while client satisfaction

remained stable compared with 2013, with 50% of clients

rating our services favourably at scores of 8 and above.

Our ambition is to build on our client-centric approach

and make our clients promoters by giving them the best

experience. In line with our ambition, we intend to

implement the Net Promoter Score (NPS) methodology

in most of our business segments in 2015.

Invest in our future

Re-engineering the IT landscape and optimising processesThe TOPS 2020 programme was launched in 2013 and

aims to upgrade and simplify our IT landscape based on

three aspirations: easiest to do business with, creating

value through innovation and providing best-in-class

productivity.

In 2014, we finalised the blueprint for the new IT

landscape, which will be delivered in stages until 2020.

This will simplify our IT landscape, increase our agility and

reduce our cost base.

We extended our partnership with IBM in 2014. Under

the new agreement, IBM intends to, among other things,

implement and manage an on-premise cloud environment

for ABN AMRO. The dedicated on-premise cloud will help

us to improve our standard of service, achieve greater

operational efficiencies and provide innovative products

to our clients.

We expect to migrate the first applications to this cloud

environment in 2015. We also expect to implement a new

security concept designed to protect our employees’ and

clients’ digital information.

Positively recognised position on sustainability and transparencyABN AMRO aspires to achieve a positively recognised

position on sustainability and transparency.

Our sustainability strategy supports this commitment

and is based on four aspirations:

Å We pursue sustainable business operations;

Å We put our clients’ interests centre stage and build

sustainable relationships;

Å We use our financial expertise for the benefit of society;

Å We finance and invest for clients in a sustainable manner.

An inspired and engaged workforce is vital to the success

of our strategy. To this end, we promote sustainability

internally and encourage our staff to get involved.

Our efforts are clearly paying off: the score for sustainability

in the Employee Engagement Survey for 2014 rose to

61% from 45% in 2013.

In 2014, we translated our sustainability aspirations into

specific focus areas by implementing performance metrics

and targets to support our sustainability strategy in

practice. This will enable us to report on our progress

in an increasingly concrete and transparent manner.

For example, we started developing the Sustainability

Risk Management policy for investments, with a focus

on environmental, social and governance (ESG) criteria.

To further broaden the scope to include all of our

investments, we aim to set a threshold for investments

in line with the principles of the UN Global Compact.

We believe that value creation and sustainability go hand

in hand, and we support entrepreneurs that share our

vision. For example, our Social Impact Fund, which invests

in social enterprises, was positively received. ABN AMRO

Informal Investor Services brings together Private Banking

clients and SMEs. Private Banking clients invest in these

social enterprises and often offer advice as well.

In recent years, we have been focusing increasingly on tax

matters, which is supported by the materiality analysis we

performed in 2014. The prime issue here is whether or not

internationally operating businesses pay their fair share of

tax. To address this issue, we have increased transparency

by publishing our tax principles on our website and

providing country-by-country reporting on various income

items. More information can be found in the Annual

Financial Statements section in this report.

More details are provided in our Sustainability Report 2014.

IntroductionBusiness Report

Risk & Capital Report

Governance ReportAnnual Financial Statem

entsOther

Strategic Report19

ABN AMRO Group Annual Report 2014

Top Class EmployerMaking a difference to our customers now and in the

future requires a talented, committed workforce more

than ever. Our Top Class Employer strategy aims to inspire

employees to develop continuously and to make their

own, unique contribution to the bank’s sustainable growth.

Employees who take ownership of these goals are our

most valuable asset. They are at the heart of our ability to

build long-lasting relationships with our clients. We have

drawn up a roadmap with three aims:

Å Defining our meaningful corporate identity;

Å Developing a culture of excellence;

Å Creating the best place to work.

Managers at every level of the company play a pivotal role

in motivating employees to realise ABN AMRO’s goals

based on our corporate identity. They are the catalysts for

change. Our leadership programmes help managers

execute the strategy and develop an inspiring leadership

style. ABN AMRO introduced the Leadership Qualities to

clarify what is expected of our managers.

But simply possessing talent is not enough: it is every

employee’s responsibility to use their talent. Equally, it is

the bank’s responsibility to support every employee’s

professional development. We intend to introduce the

Talent Identification Tool in 2015, a method to facilitate

open dialogue between managers and staff.

To ensure that employees are given the opportunity to

continuously improve their expertise and skills in a culture

of excellence, we now offer talent development

programmes to staff bank-wide rather than exclusively

to a small group.

A new collective labour agreement was concluded with

the trade unions to give employees the autonomy to

personalise their working conditions, allowing them to

create their best place to work.

We have evaluated our Top Class Employer strategy and

are proud to report that we have improved on key metrics.

Employee engagement scores rose further to 76% in

2014. In terms of gender diversity, we increased the

percentage of women in senior and upper middle-

management positions. Our efforts are reflected in the

annual Dutch Intermediair Image Survey, as our position

as a Top Class Employer in the Netherlands further

improved in 2014.

Strongly commit to a moderate risk profileABN AMRO is committed to maintaining a moderate risk

profile, which is reflected in, among other things, three

key elements: (i) a clean balance sheet, (ii) a clear risk

governance structure and strong risk culture, and (iii) a

solid capital and liquidity position. Internationally, we focus

on capabilities and geographies where we have a proven

track record and a right to win.

We are pleased that our prudent risk management

approach resulted in our comfortably passing the ECB’s

comprehensive assessment, which consisted of the Asset

Quality Review and a stress test. This was carried out in

preparation of the ECB taking over the supervisory role

from DNB in November 2014.

We continued to optimise the sector-based risk approach

throughout the Risk Management organisation based on

improved risk knowledge and awareness. This has helped

us to better monitor and manage portfolio intake and

sector concentrations. This approach, together with the

recovery of the Dutch economy, resulted in a decrease of

loan impairments, primarily in our mortgage and business

banking within Commercial Clients.

Bank-wide operational risk awareness was strengthened

through rigorous training and e-learning programmes.

This resulted from implementation of the Advanced

Measurement Approach (AMA) for calculating operational

risk exposure for internal purposes. The application for

AMA status will be submitted to the regulators in 2015.

In late 2014, we formally applied to use the Internal Model

Approach (IMA) for market risk in the trading book. While

regulatory approval is pending, the approach is being

applied for internal risk management purposes and for

economic capital computations.

We review our risk appetite annually and continue to focus

on actively managing it based on capital, liquidity and

interest rate risks. We increasingly manage our bank

based on risk-adjusted return on risk-adjusted capital

(RARORAC) to ensure that our capital is employed in

the most efficient way.

With the fourth profitable year in a row, we further

improved our capital buffer. ABN AMRO had a fully loaded

CET1 ratio of 14.1% at year-end 2014, which is above our

target range of 11.5-12.5%.

20 Strategic Report Strategic priorities

Pursue selective international growthABN AMRO intends to grow in businesses where we

have a strong and proven track record (capability-led

growth) and that fit into our moderate risk profile. We

intend to build upon the ABN AMRO brand awareness and

aim to match our local assets and liabilities over time.

In 2014, we completed the integration of the private

banking activities of Credit Suisse into Bethmann Bank,

our private bank in Germany. Bethmann Bank is now the

third largest private bank in Germany. We also entered into

a strategic global agreement with IndusInd Bank Limited,

a new generation Indian bank, to support our Asian private

banking business.

In Austria, we introduced MoneYou, our retail banking

online savings platform.

Clearing established a local clearing unit in Brazil to

conduct clearing activities for existing clients and

expanded further in the US by servicing existing and

acquiring new clients.

ECT Clients further expanded in the US and Asia.

We set up new Leasing branches in the United Kingdom

and Germany, employing local staff with a track record in

these markets.

Improve profitabilityThe underlying cost/income ratio improved by four

percentage points, from 64% in 2013 to 60% in 2014,

which is at the upper end of the targeted range of 56-60%

we set for 2017. This result was achieved thanks mainly to

our re-pricing efforts, leading to margin improvements on

products across most segments. Growth of net interest

income more than offset the modest cost increase,

leading to the improvement in the cost/income ratio.

Underlying ROE improved from 5.5% in 2013 to 10.9%

in 2014, which is within the 9-12% target range for 2017.

The full-year underlying net profit doubled to

EUR 1,551 million, on the back of higher net interest

income and lower loan impairments. The decrease in the

level of loan impairments is the result of the initial

recovery of the Dutch economy. In addition, we further

strengthened our credit management, increased the level

of early warning monitoring and improved our

understanding of sector-specific risk by conducting

extensive research and tightening credit requirements for

new clients. These initiatives, together with the recovery

of the Dutch economy, largely contributed to the

improvement of net profit and ROE.

IntroductionBusiness Report

Risk & Capital Report

Governance ReportAnnual Financial Statem

entsOther

Strategic Report21

ABN AMRO Group Annual Report 2014

strategic governance

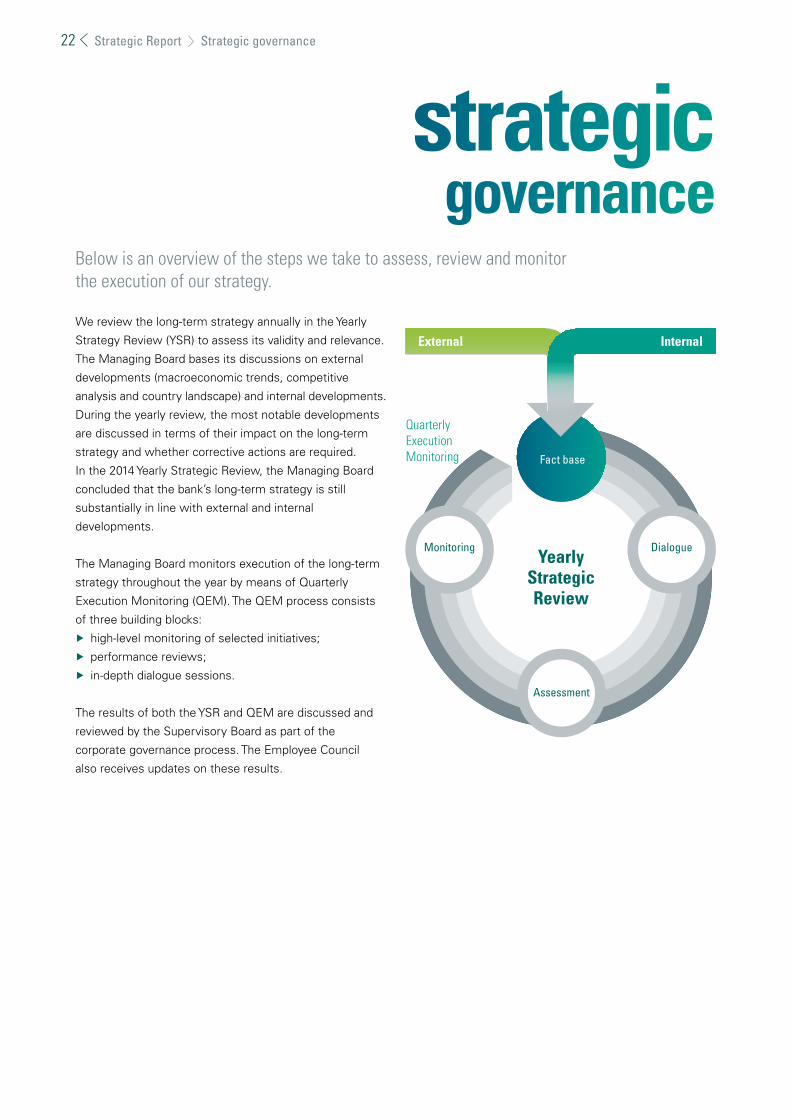

Below is an overview of the steps we take to assess, review and monitor the execution of our strategy.

We review the long-term strategy annually in the Yearly

Strategy Review (YSR) to assess its validity and relevance.

The Managing Board bases its discussions on external

developments (macroeconomic trends, competitive

analysis and country landscape) and internal developments.

During the yearly review, the most notable developments

are discussed in terms of their impact on the long-term

strategy and whether corrective actions are required.

In the 2014 Yearly Strategic Review, the Managing Board

concluded that the bank’s long-term strategy is still

substantially in line with external and internal

developments.

The Managing Board monitors execution of the long-term

strategy throughout the year by means of Quarterly

Execution Monitoring (QEM). The QEM process consists

of three building blocks:

Å high-level monitoring of selected initiatives;

Å performance reviews;

Å in-depth dialogue sessions.

The results of both the YSR and QEM are discussed and

reviewed by the Supervisory Board as part of the

corporate governance process. The Employee Council

also receives updates on these results.

Assessment

DialogueMonitoring

Fact base

YearlyStrategicReview

QuarterlyExecutionMonitoring

External Internal

22 Strategic Report Strategic governance

Strategic governance