Embed Size (px)

Citation preview

Strategic Cost Strategic Cost ManagementManagement

Chapter 11Chapter 11

The Honda Business Modelfor Suppliers

Six-year planSix-year plan 100% understanding of all components 100% understanding of all components

of product costof product cost Lean supplier development concurrent Lean supplier development concurrent

engineeringengineering Flawless new product launchFlawless new product launch CommunicationsCommunications

22

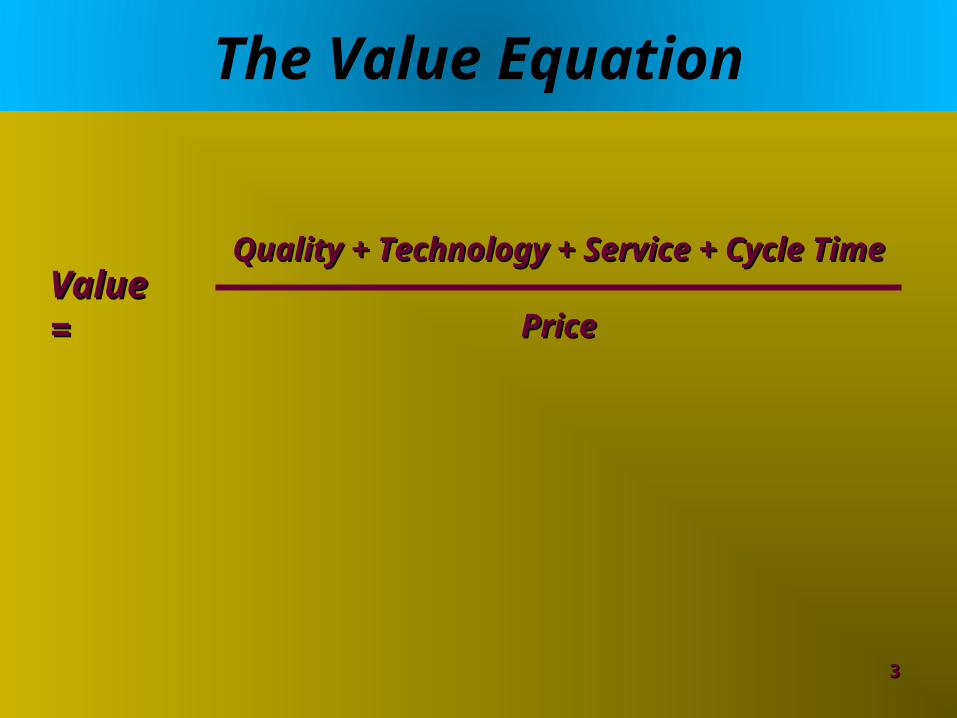

The Value Equation

33

Quality + Technology + Service + Cycle TimeQuality + Technology + Service + Cycle Time

PricePriceValueValue = =

Definitions

Price analysisPrice analysis Process of comparing supplier prices Process of comparing supplier prices

against external price benchmarksagainst external price benchmarks

Cost analysisCost analysis Process of analyzing each individual cost Process of analyzing each individual cost

element that makes up final priceelement that makes up final price

Total cost analysisTotal cost analysis Applies value equation across multiple Applies value equation across multiple

processesprocesses

44

Cost Management Approaches

Tier 2 Tier 2 SupplierSupplier

Tier 1 Tier 1 SupplierSupplier EnterpriseEnterprise CustomerCustomer ConsumerConsumer

55

Single Company Focused Cost-Reduction Initiatives

Strategic Cost Management –Finished Product/Service

Focus throughout theSupply Chain

Customer NeedsCustomer Needs

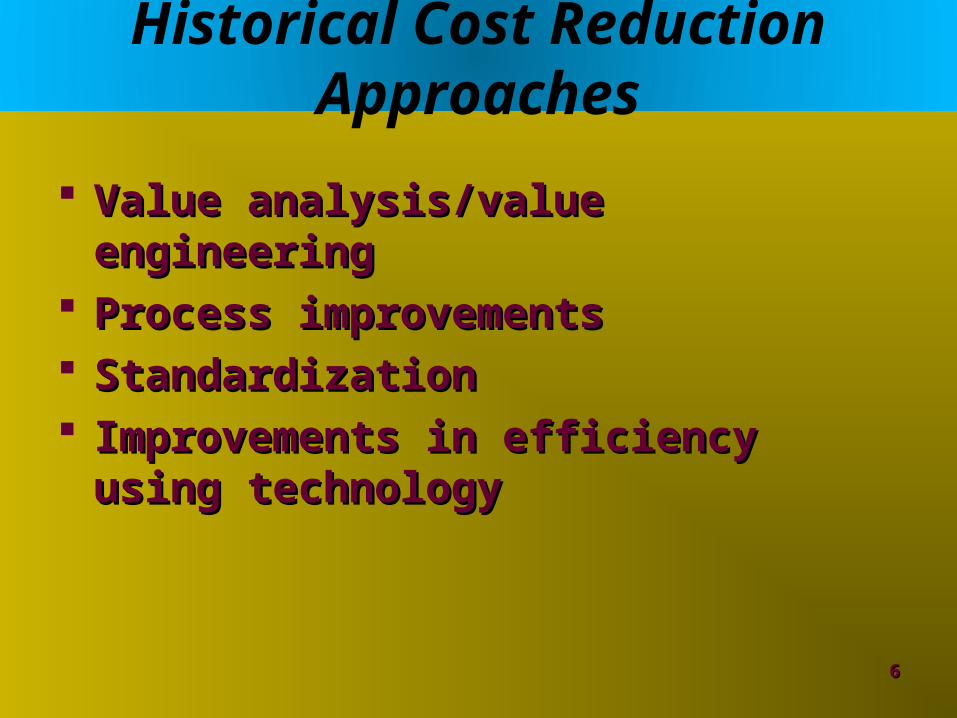

Historical Cost Reduction Approaches

Value analysis/value engineeringValue analysis/value engineering Process improvementsProcess improvements StandardizationStandardization Improvements in efficiency using Improvements in efficiency using

technologytechnology

66

Strategic Cost Management Processes

77

Most focus is

Most focus is

on a single

on a single

company

company

Need to

Need to migrate to a

migrate to a

supply chain

supply chain focusfocus

Strategic Cost Management Processes

Value analysis/Value engineeringValue analysis/Value engineering Team-basedTeam-based Cross-enterpriseCross-enterprise

On-site supplier developmentOn-site supplier development Process to accomplish supplier Process to accomplish supplier

continuous improvementcontinuous improvement

88

Strategic Cost Management Processes

Cross-enterprise cost improvementCross-enterprise cost improvement Joint effortJoint effort Costs identifiedCosts identified Cost drivers determinedCost drivers determined Strategies to improve executionStrategies to improve execution Results reviewResults review

Joint brainstormingJoint brainstorming Establish list of value-add projects and Establish list of value-add projects and

executeexecute99

Strategic Cost Management Processes

Supplier suggestion programsSupplier suggestion programs MotivateMotivate Act onAct on RewardReward Overall processOverall process

Supply chain compressionSupply chain compression Reducing number of levelsReducing number of levels Supplier consortiumsSupplier consortiums

1010

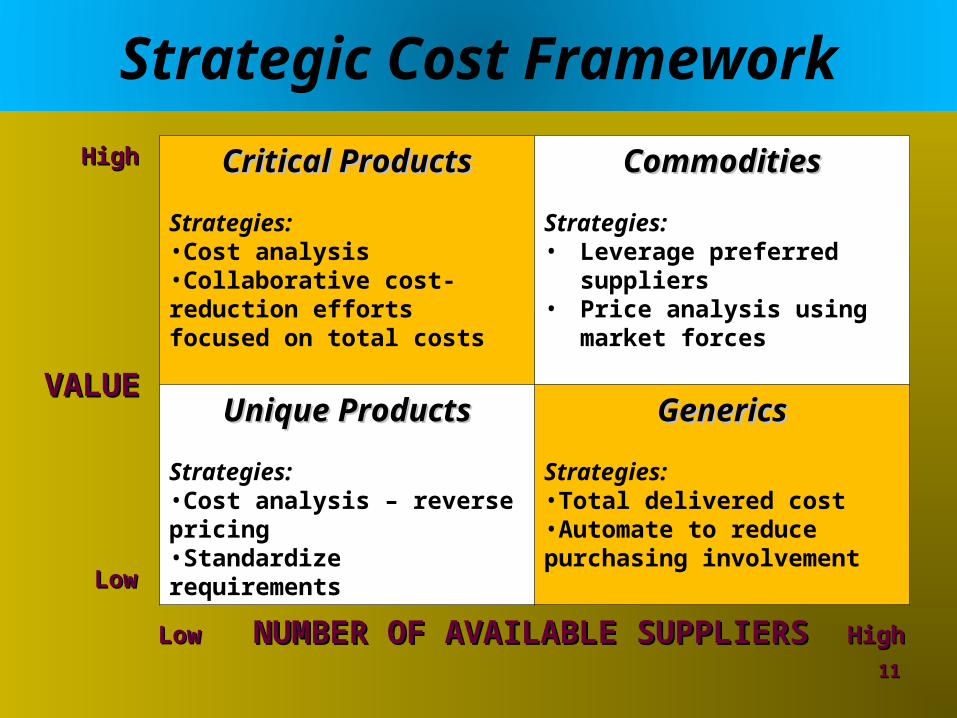

Strategic Cost Framework

Critical ProductsCritical Products

Strategies:•Cost analysis•Collaborative cost-reduction efforts focused on total costs

CommoditiesCommodities

Strategies:• Leverage preferred

suppliers• Price analysis using market

forces

Unique ProductsUnique Products

Strategies:•Cost analysis – reverse pricing•Standardize requirements

GenericsGenerics

Strategies:•Total delivered cost•Automate to reduce purchasing involvement

1111

VALUEVALUE

NUMBER OF AVAILABLE SUPPLIERSNUMBER OF AVAILABLE SUPPLIERS

HighHigh

HighHigh

LowLow

LowLow

Strategic Cost Framework

Generics (high supplier & low value)Generics (high supplier & low value) Competitive market with many potential Competitive market with many potential

supplierssuppliers Emphasize total delivered priceEmphasize total delivered price No need for detailed cost analysisNo need for detailed cost analysis Users order direct through supplier Users order direct through supplier

catalogs, p-cards, or e-procurementcatalogs, p-cards, or e-procurement

1212

Strategic Cost Framework

Commodities (high suppler & high Commodities (high suppler & high value)value) High-value products or servicesHigh-value products or services Competitive market situationCompetitive market situation Traditional bidding approachesTraditional bidding approaches Identify competitive pricing through price Identify competitive pricing through price

analysisanalysis

1313

Strategic Cost Framework

Unique products (low supplier & low Unique products (low supplier & low value)value) Few available suppliersFew available suppliers Relatively low valueRelatively low value Standardized productsStandardized products Try to move to generics quadrant over timeTry to move to generics quadrant over time

1414

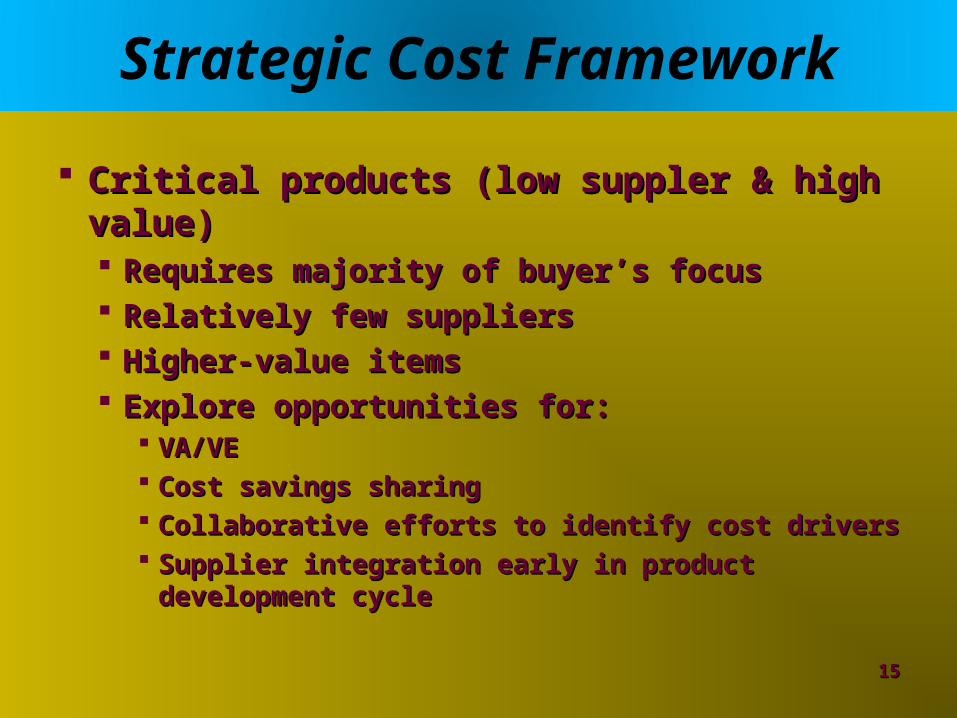

Strategic Cost Framework

Critical products (low suppler & high value)Critical products (low suppler & high value) Requires majority of buyer’s focusRequires majority of buyer’s focus Relatively few suppliersRelatively few suppliers Higher-value itemsHigher-value items Explore opportunities for:Explore opportunities for:

VA/VEVA/VE Cost savings sharingCost savings sharing Collaborative efforts to identify cost driversCollaborative efforts to identify cost drivers Supplier integration early in product development Supplier integration early in product development

cyclecycle

1515

Price vs. Cost vs. Total Cost Analyses

Price analysisPrice analysis Commodities and generics quadrantsCommodities and generics quadrants

Cost analysisCost analysis Unique and critical products quadrantsUnique and critical products quadrants

Total cost analysisTotal cost analysis All quadrantsAll quadrants

1616

Market-Based Pricing

1717

Supplier’sSupplier’sMarketMarket

Buyer’sBuyer’sMarketMarket

PRICEPRICE

VOLUMEVOLUME

SupplySupply

DemandDemand

Market Structure Analysis

Number of competitors in industryNumber of competitors in industry Relative similarity (or lack thereof) of Relative similarity (or lack thereof) of

competitive productscompetitive products Any existing barriers to entry for new Any existing barriers to entry for new

competitorscompetitors

1818

Market Structure Types

MonopolyMonopoly Single supplier marketSingle supplier market Unique product with no substitutesUnique product with no substitutes Large barriers to entryLarge barriers to entry

OligopolyOligopoly A few large suppliersA few large suppliers Pricing strategies of one supplier influence Pricing strategies of one supplier influence

others in industryothers in industry

1919

Market Structure Types

Perfect competitionPerfect competition Many small suppliersMany small suppliers Price is solely function of supply and Price is solely function of supply and

demanddemand Minimal barriers to entryMinimal barriers to entry

2020

Economic Conditions

Conditions favorable to supplierConditions favorable to supplier High level of capacity utilizationHigh level of capacity utilization Tight supplyTight supply Strong demandStrong demand

Conditions favorable to buyerConditions favorable to buyer Low level of capacity utilizationLow level of capacity utilization High level of supplyHigh level of supply Weak demandWeak demand

2121

Analyzing Supplier Pricing

Does supplier have long-term or short-Does supplier have long-term or short-term pricing strategy?term pricing strategy?

Is supplier price leader or price Is supplier price leader or price follower?follower?

Is supplier attempting to establish entry Is supplier attempting to establish entry barriers?barriers?

Is supplier using cost-based or market-Is supplier using cost-based or market-based approach?based approach?

2222

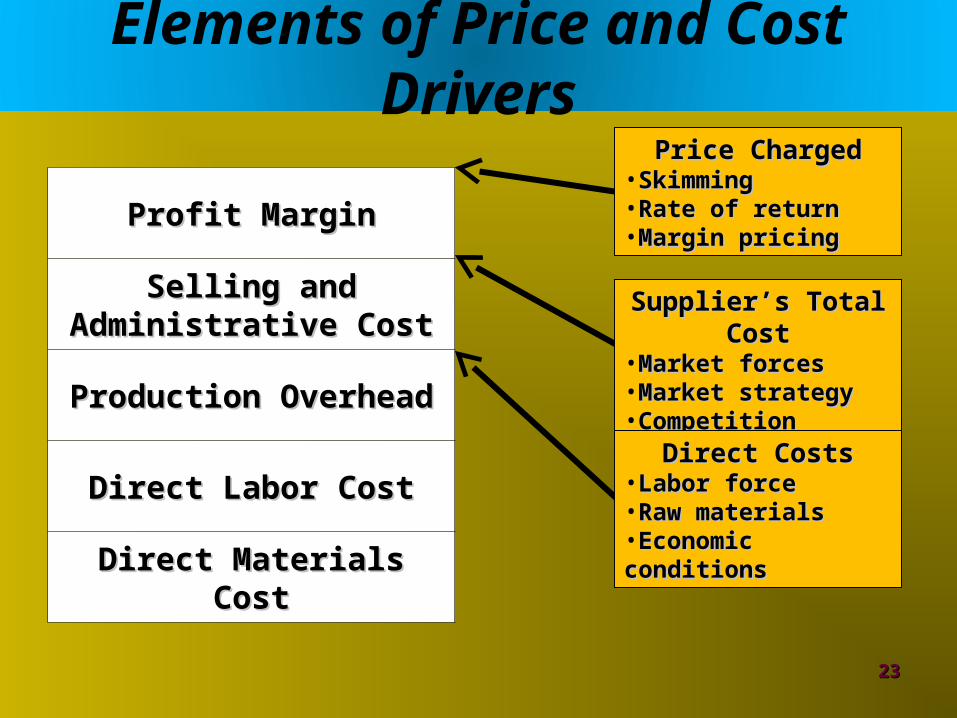

Elements of Price and Cost Drivers

Profit MarginProfit Margin

Selling and Selling and Administrative CostAdministrative Cost

Production OverheadProduction Overhead

Direct Labor CostDirect Labor Cost

Direct Materials CostDirect Materials Cost

2323

Price ChargedPrice Charged•SkimmingSkimming•Rate of returnRate of return•Margin pricingMargin pricing

Supplier’s Total CostSupplier’s Total Cost•Market forcesMarket forces•Market strategyMarket strategy•CompetitionCompetition

Direct CostsDirect Costs•Labor forceLabor force•Raw materialsRaw materials•Economic conditionsEconomic conditions

Market-Driven Pricing Models

Price volume modelPrice volume model Market-share modelMarket-share model Market skimming modelMarket skimming model Revenue pricing modelRevenue pricing model Promotional pricing modelPromotional pricing model Competition pricing modelCompetition pricing model Cash discountsCash discounts

2424

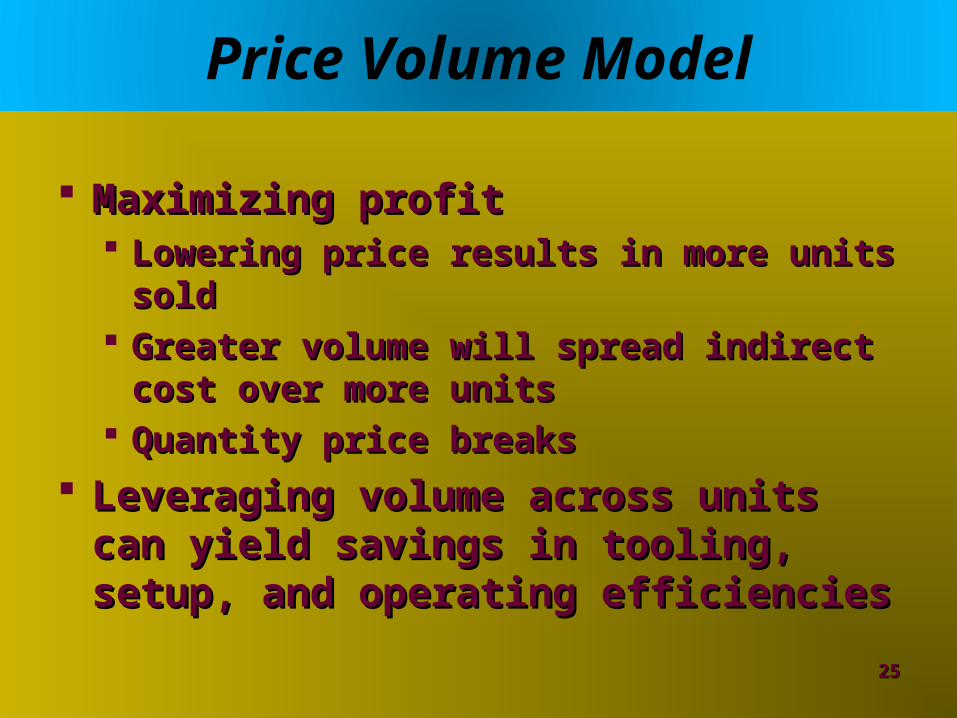

Price Volume Model

Maximizing profitMaximizing profit Lowering price results in more units soldLowering price results in more units sold Greater volume will spread indirect cost Greater volume will spread indirect cost

over more unitsover more units Quantity price breaksQuantity price breaks

Leveraging volume across units can Leveraging volume across units can yield savings in tooling, setup, and yield savings in tooling, setup, and operating efficienciesoperating efficiencies

2525

Market-Share Model

Long run profitability depends on level Long run profitability depends on level of market share obtainedof market share obtained

Also known as penetration pricingAlso known as penetration pricing Lower margins initially to increase Lower margins initially to increase

market sharemarket share Eventually spreads out indirect costs Eventually spreads out indirect costs

over greater volumeover greater volume

2626

Market-Skimming Model

Start with high price with high-end Start with high price with high-end productproduct

Then lower the price as the market Then lower the price as the market penetrates to exclude competitionpenetrates to exclude competition

Seed of revenue management (dynamic Seed of revenue management (dynamic pricing)pricing)

2727

Revenue pricing Model

Dynamic pricingDynamic pricing

Price differentiationPrice differentiation

Airline industryAirline industry

2828

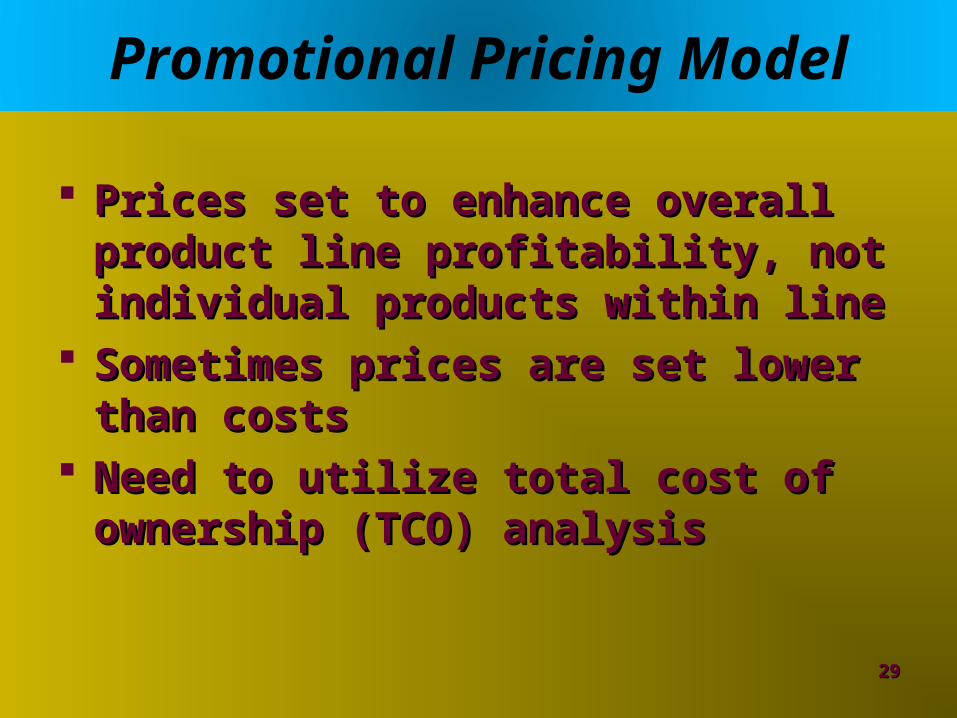

Promotional Pricing Model

Prices set to enhance overall product Prices set to enhance overall product line profitability, not individual line profitability, not individual products within lineproducts within line

Sometimes prices are set lower than Sometimes prices are set lower than costscosts

Need to utilize total cost of ownership Need to utilize total cost of ownership (TCO) analysis(TCO) analysis

2929

Competition Pricing Model

Focuses on reacting to actual or Focuses on reacting to actual or anticipated competitor pricinganticipated competitor pricing

What is highest price the supplier can What is highest price the supplier can charge and be just below its charge and be just below its competition?competition?

ExampleExample Reverse auctionsReverse auctions

3030

Cash Discounts

Incentives to buyer who pay invoices Incentives to buyer who pay invoices promptlypromptly

Example: 2/10, net 30Example: 2/10, net 30 Usually worthwhile to take advantage Usually worthwhile to take advantage

of cash discountsof cash discounts Relatively high returnRelatively high return

3131

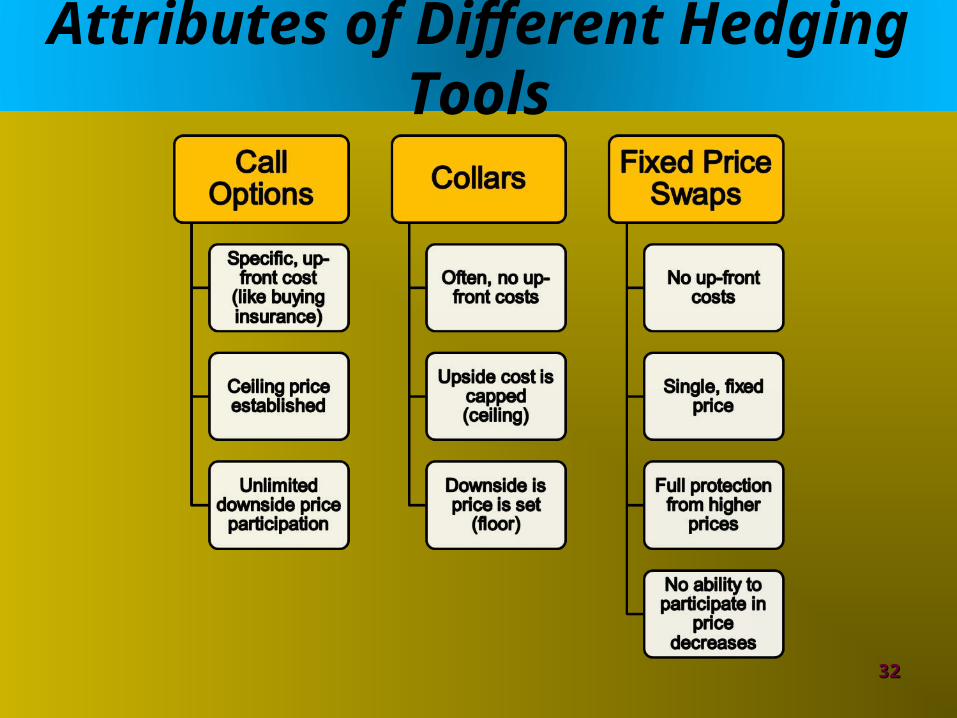

Attributes of Different Hedging Tools

3232

Customer Receives Differenc

e

Customer Buys a Fixed-Price Swap

3333

Swap Price

Net

Pri

ce

Underlying Market Price

HedgedUnhedged

Customer Receives Differenc

e

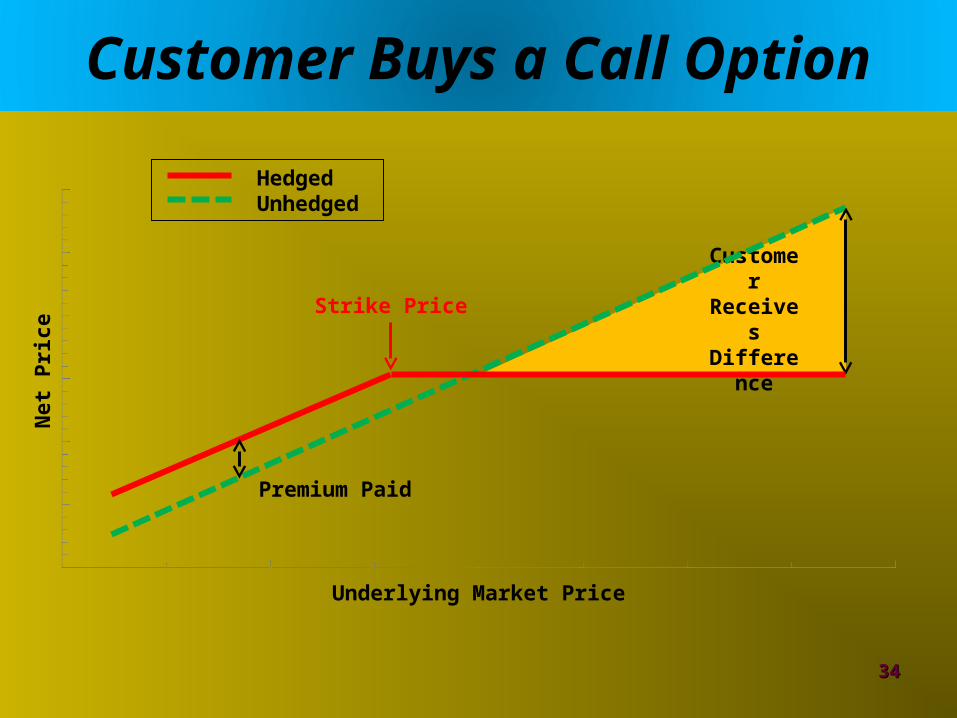

Customer Buys a Call Option

3434

Strike Price

Net

Pri

ce

Underlying Market Price

HedgedUnhedged

Premium Paid

Customer

Receives

Difference

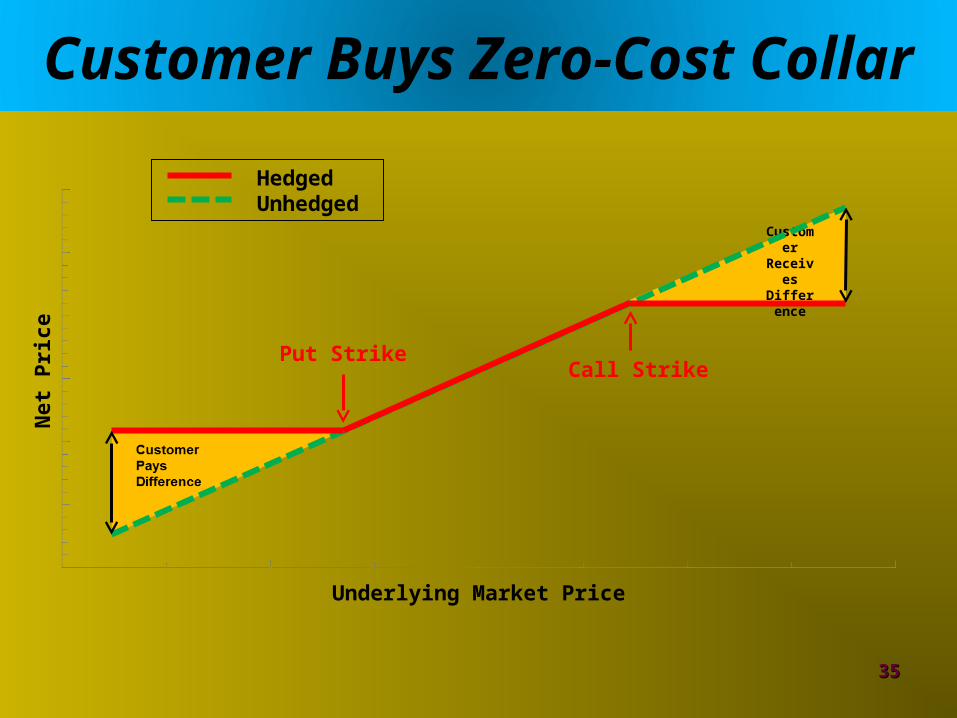

Customer Buys Zero-Cost Collar

3535

Call Strike

Net

Pri

ce

Underlying Market Price

HedgedUnhedged

Put Strike

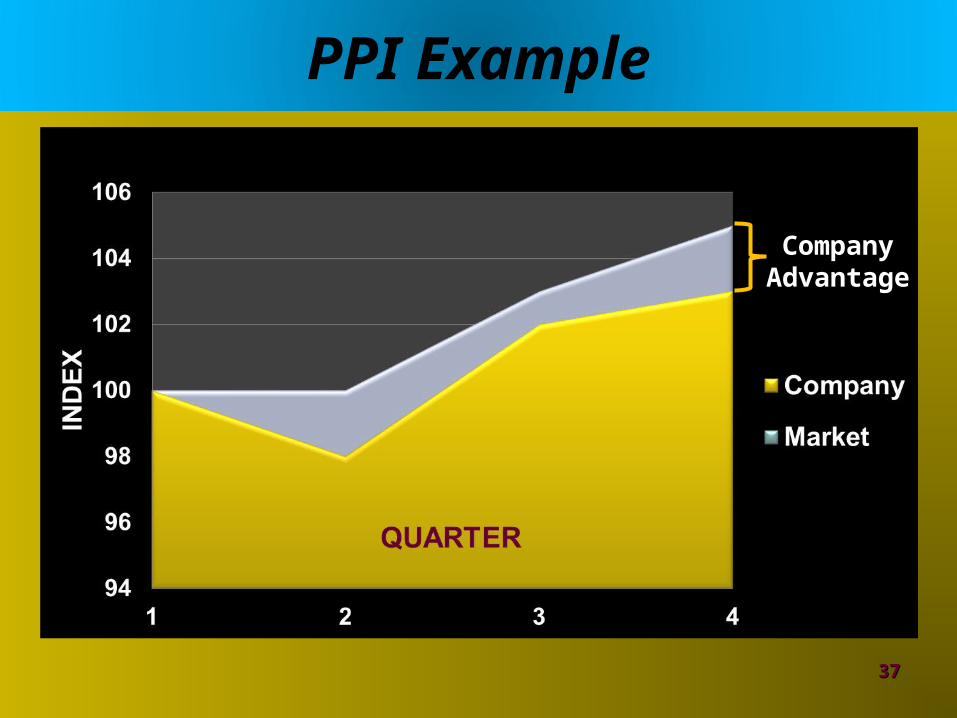

Producer Price Index (PPI)

Appropriate for market-based products Appropriate for market-based products where price is largely function of where price is largely function of supply and demandsupply and demand

Published by U.S. Bureau of Labor Published by U.S. Bureau of Labor Statistics (BLS)Statistics (BLS)

PPI tracks material price movements on PPI tracks material price movements on quarter-to-quarter basisquarter-to-quarter basis

3636

PPI Example

3737

Company Company AdvantageAdvantage

Cost Analysis Techniques

Cost-based pricing modelsCost-based pricing models Product specificationsProduct specifications Estimating supplier costs using reverse Estimating supplier costs using reverse

price analysisprice analysis Break-even analysisBreak-even analysis

3838

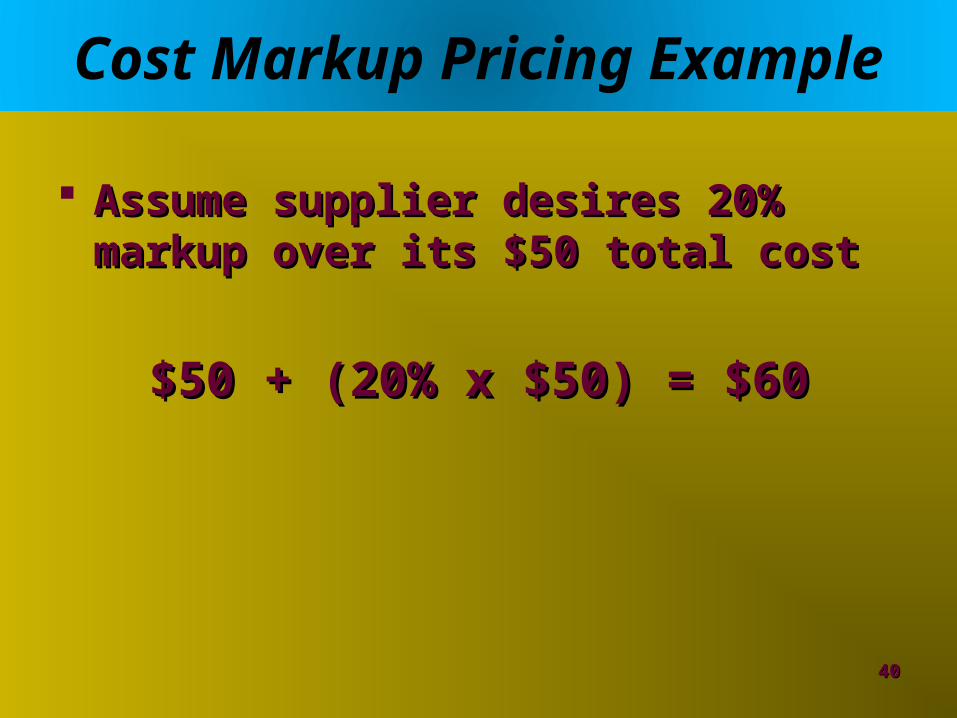

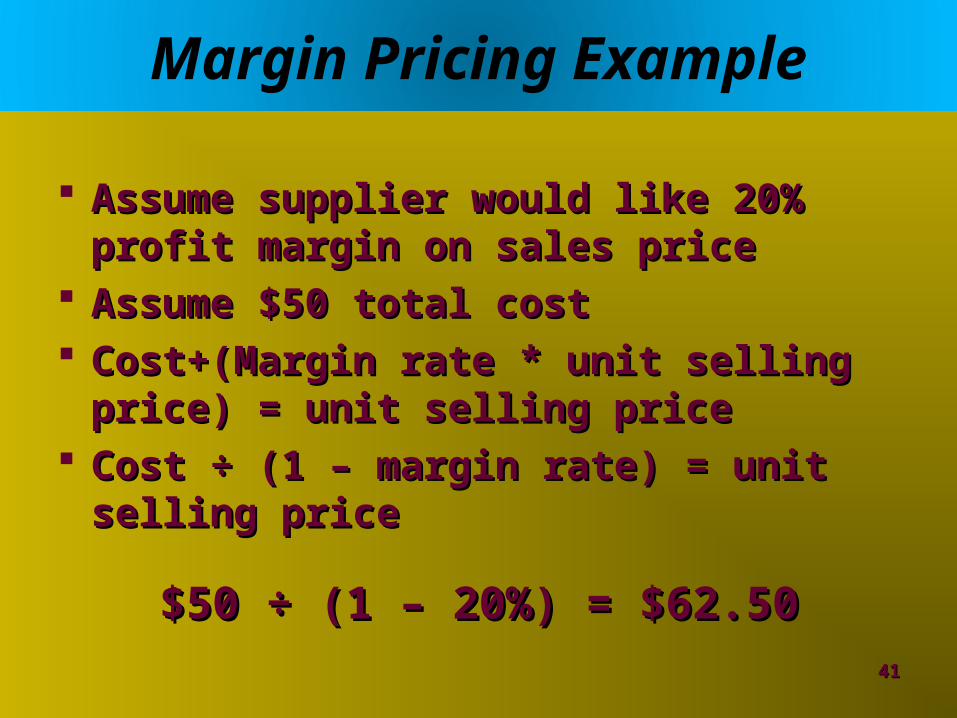

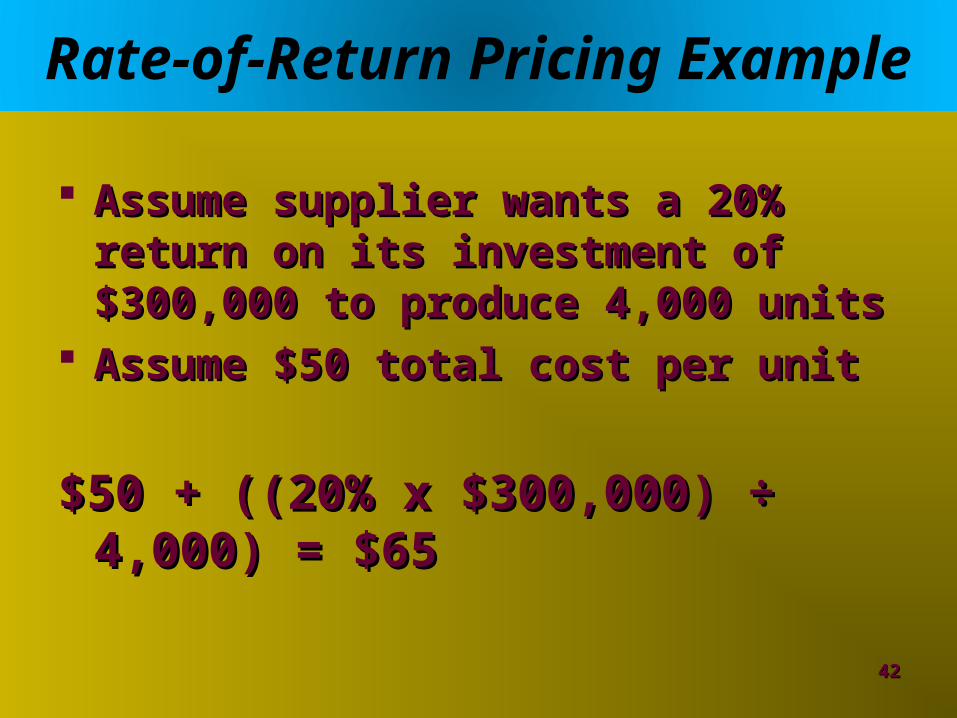

Cost-Based Pricing Models

Cost markup pricing modelCost markup pricing model Estimate costs and add markup %Estimate costs and add markup %

Margin pricing modelMargin pricing model Establish profit margin that is Establish profit margin that is

predetermined % of quoted pricepredetermined % of quoted price

Rate-of-return pricing modelRate-of-return pricing model Desired profit on financial investment is Desired profit on financial investment is

added to estimated costsadded to estimated costs

3939

Cost Markup Pricing Example

Assume supplier desires 20% markup Assume supplier desires 20% markup over its $50 total costover its $50 total cost

$50 + (20% x $50) = $60$50 + (20% x $50) = $60

4040

Margin Pricing Example

Assume supplier would like 20% profit Assume supplier would like 20% profit margin on sales pricemargin on sales price

Assume $50 total costAssume $50 total cost Cost+(Margin rate * unit selling price) = Cost+(Margin rate * unit selling price) =

unit selling priceunit selling price Cost ÷ (1 – margin rate) = unit selling Cost ÷ (1 – margin rate) = unit selling

priceprice

$50 ÷ (1 – 20%) = $62.50$50 ÷ (1 – 20%) = $62.504141

Rate-of-Return Pricing Example

Assume supplier wants a 20% return on Assume supplier wants a 20% return on its investment of $300,000 to produce its investment of $300,000 to produce 4,000 units4,000 units

Assume $50 total cost per unitAssume $50 total cost per unit

$50 + ((20% x $300,000) ÷ 4,000) = $65$50 + ((20% x $300,000) ÷ 4,000) = $65

4242

Product Specifications

Custom design and tooling increases Custom design and tooling increases product costsproduct costs Determine if added differentiation gives Determine if added differentiation gives

competitive advantage in marketplacecompetitive advantage in marketplace

Standardized components helps reduce Standardized components helps reduce product costsproduct costs

4343

Cost Analysis

Direct function of quality and Direct function of quality and availability of informationavailability of information

TechniquesTechniques Require detailed production cost Require detailed production cost

breakdownbreakdown Joint sharing of cost informationJoint sharing of cost information Early supplier design involvementEarly supplier design involvement

4444

Reverse Price Analysis

Also known as Also known as “should cost”“should cost” analysis analysis Can be used when supplier is reluctant to Can be used when supplier is reluctant to

share its proprietary cost datashare its proprietary cost data

Break down cost into basic componentsBreak down cost into basic components TechniquesTechniques

Internal engineering estimatesInternal engineering estimates Historical experience and judgmentHistorical experience and judgment Review of public financial documentsReview of public financial documents

4545

Reverse Price Analysis Example

Hypothetical price $20

Profit/SG&A allowance (15%) - 3

Subtotal $17

Direct material - 4

Subtotal $13

Direct labor - 3

Manufacturing burden (overhead) $10

4646

Opportunities for Cost Reduction

Plant utilizationPlant utilization Process capabilityProcess capability Learning curve effectLearning curve effect Supplier’s workforceSupplier’s workforce Management capabilityManagement capability Supply management efficiencySupply management efficiency

4747

Learning curve

A learning curve displays the relationship A learning curve displays the relationship between the per unit cost (or time) and the between the per unit cost (or time) and the cumulative quantity produced of a productcumulative quantity produced of a product

Basic Learning Curve Premise:Basic Learning Curve Premise:

The production cost (or time) per unit is The production cost (or time) per unit is

reduced by a fixed percentage (1-reduced by a fixed percentage (1-rr) each ) each

time that production is doubled.time that production is doubled.

4848

Learning curve

4949

DefinitionsDefinitions

CC11 = the cost (or time) of the 1= the cost (or time) of the 1stst unit unit

CCnn = the cost (or time) of the = the cost (or time) of the nnthth unit unit

CCmm = the cost (or time) of the = the cost (or time) of the mmthth unit unit

rr = the learning rate= the learning rate

= % of previous cost (or time) whenever= % of previous cost (or time) whenever

production is doubledproduction is doubled

aa = the learning curve constant (> 0)= the learning curve constant (> 0)

nn or m = total number of units produced or m = total number of units produced

Learning curve

5050

Basic Learning Curve FormulaBasic Learning Curve Formula

::CCnn = = CC11 ( (nn-a-a )= )=CC11 / ( / (nnaa))

Growth rate learning curve FormulaGrowth rate learning curve Formula

: : CCnn = = CCmm[(n/m)[(n/m)-a-a]]

Learning curve

5151

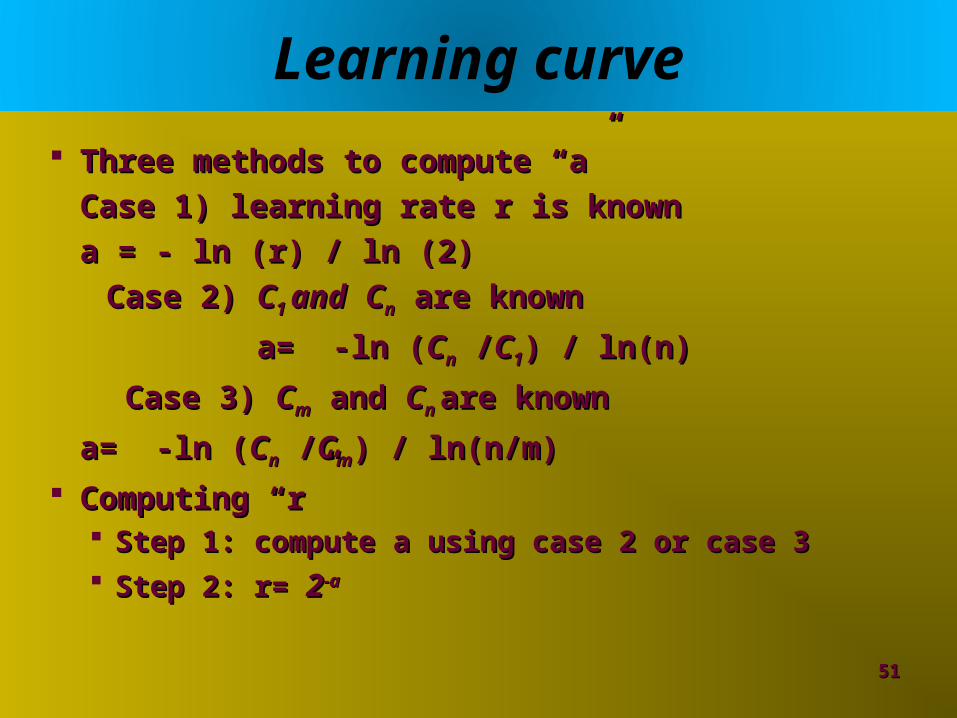

Three methods to compute “a”Three methods to compute “a”

Case 1) learning rate r is knownCase 1) learning rate r is known

a = - ln (r) / ln (2)a = - ln (r) / ln (2)

Case 2) Case 2) CC1 1 andand CCnn are known are known

a= -ln (a= -ln (CCnn / /CC11) / ln(n)) / ln(n)

Case 3) Case 3) CCmm and and CCn n are knownare known

a= -ln (a= -ln (CCnn / /CCmm) / ln(n/m)) / ln(n/m)

Computing “r”Computing “r” Step 1: compute a using case 2 or case 3Step 1: compute a using case 2 or case 3 Step 2: r= Step 2: r= 22-a-a

Learning curve

5252

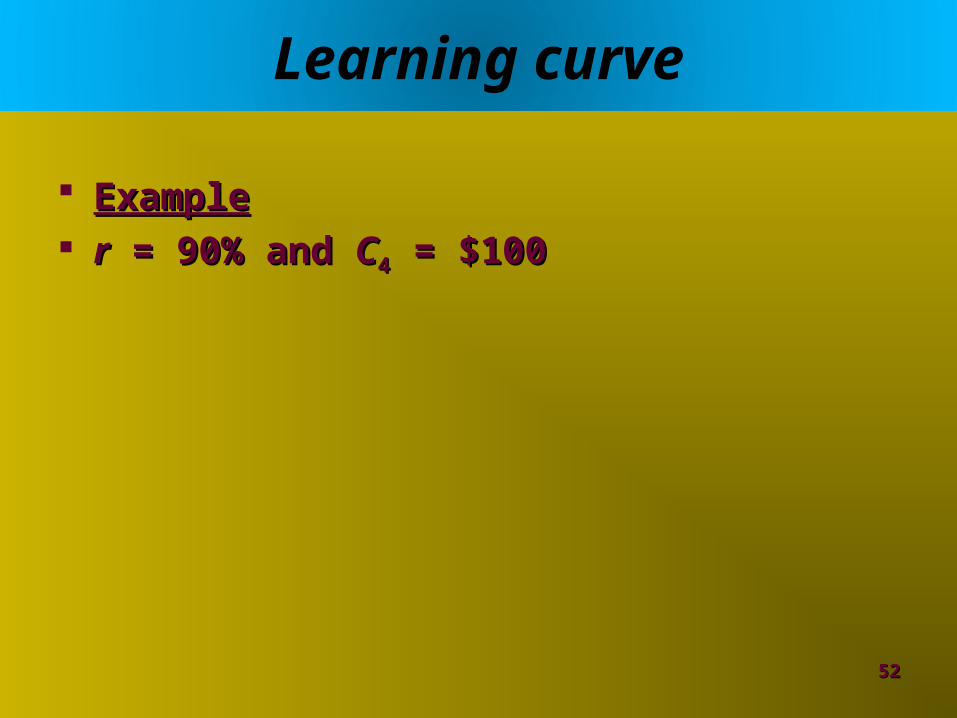

ExampleExample rr = 90% and = 90% and CC44 = $100 = $100

Learning curve

5353

Example 1Example 1

Production Airlines manufactures small jets. Production Airlines manufactures small jets. The initial jet required 400 labor days to The initial jet required 400 labor days to complete. complete.

Assuming an 80% learning rate, how many Assuming an 80% learning rate, how many labor days will be required for the 20labor days will be required for the 20thth jet. jet.

Learning curve

5454

Example 2Example 2

Suppose it costs a firm $60.00 to produce the Suppose it costs a firm $60.00 to produce the 11stst unit and $48.00 to produce 160 unit and $48.00 to produce 160thth unit. unit. What is the learning rate for this company?What is the learning rate for this company?

Learning curve

5555

Example 3Example 3

Suppose it costs a firm $1200 to produce the Suppose it costs a firm $1200 to produce the 2,0002,000thth unit and its learning rate is 75%. unit and its learning rate is 75%. How much should it cost to produce the How much should it cost to produce the 8,0008,000thth unit? unit?

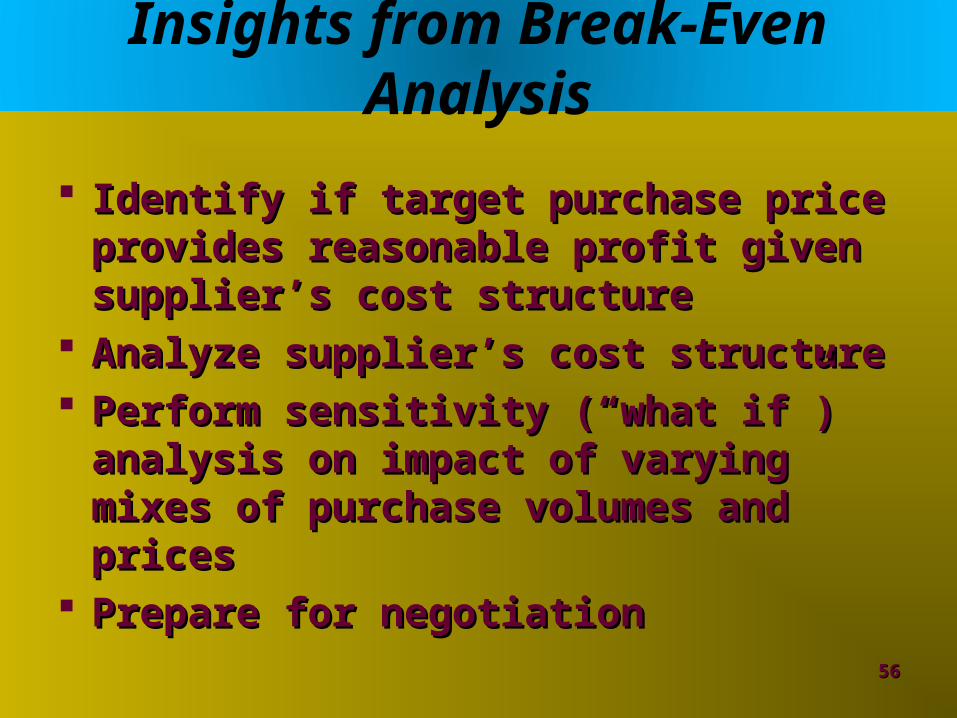

Insights from Break-Even Analysis

Identify if target purchase price Identify if target purchase price provides reasonable profit given provides reasonable profit given supplier’s cost structuresupplier’s cost structure

Analyze supplier’s cost structureAnalyze supplier’s cost structure Perform sensitivity (“what if”) analysis Perform sensitivity (“what if”) analysis

on impact of varying mixes of purchase on impact of varying mixes of purchase volumes and pricesvolumes and prices

Prepare for negotiationPrepare for negotiation

5656

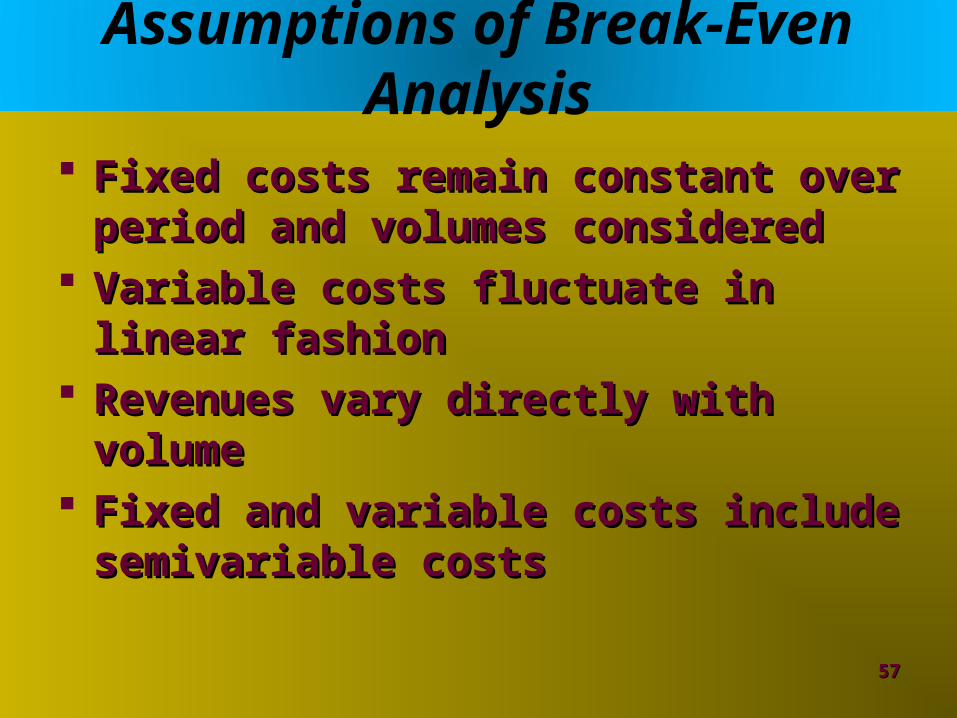

Assumptions of Break-Even Analysis

Fixed costs remain constant over Fixed costs remain constant over period and volumes consideredperiod and volumes considered

Variable costs fluctuate in linear Variable costs fluctuate in linear fashionfashion

Revenues vary directly with volumeRevenues vary directly with volume Fixed and variable costs include Fixed and variable costs include

semivariable costssemivariable costs

5757

Assumptions of Break-Even Analysis

Considers total cost rather than Considers total cost rather than average costsaverage costs

There are minimal joint costsThere are minimal joint costs Considers only quantitative factorsConsiders only quantitative factors

5858

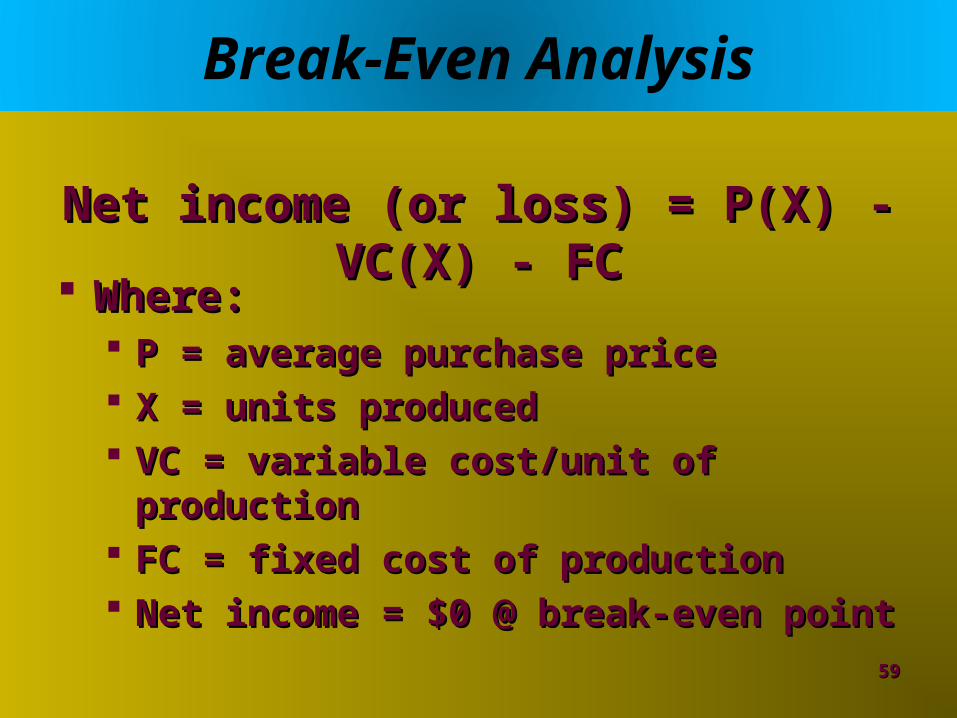

Break-Even Analysis

Where:Where: P = average purchase priceP = average purchase price X = units producedX = units produced VC = variable cost/unit of productionVC = variable cost/unit of production FC = fixed cost of productionFC = fixed cost of production Net income = $0 @ break-even pointNet income = $0 @ break-even point

5959

Net income (or loss) = P(X) - VC(X) - FCNet income (or loss) = P(X) - VC(X) - FC

Break-Even Analysis Example

6060

Total Costs

Fixed Costs

Break-Even Break-Even PointPoint

$30,000

$75,000$75,000

Revenue / Cost ($)

Volume7,5007,500 9,000

Profit

• Target price - $10/unitTarget price - $10/unit• Fixed costs - $30,000Fixed costs - $30,000• Variable costs - $6/unitVariable costs - $6/unit• Forecast purchase volume - Forecast purchase volume - 9,000 units9,000 units

Total Total RevenuesRevenues

Break-Even Example

6161

Net income (or loss) = P(X) - VC(X) - FCNet income (or loss) = P(X) - VC(X) - FC

$$6,0006,000 = $10(9,000) - $6(9,000) - $30,000 = $10(9,000) - $6(9,000) - $30,000

$0 = $10($0 = $10(7,5007,500) - $6() - $6(7,5007,500) - $30,000) - $30,000

Forecasted Volume:Forecasted Volume:

Break-Even Volume:Break-Even Volume:

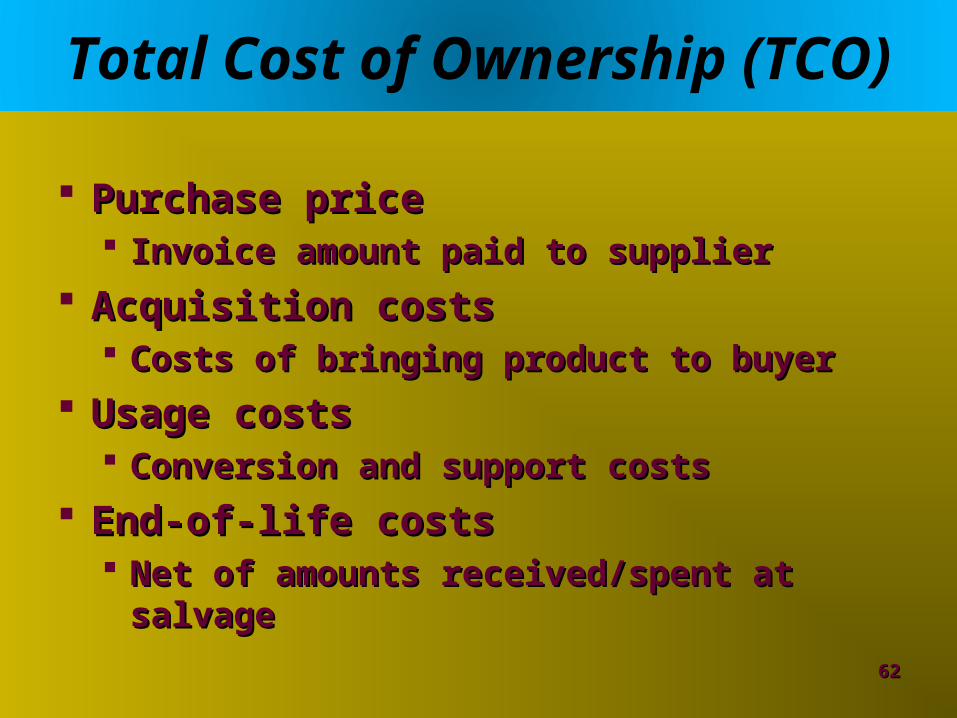

Total Cost of Ownership (TCO)

Purchase pricePurchase price Invoice amount paid to supplierInvoice amount paid to supplier

Acquisition costsAcquisition costs Costs of bringing product to buyerCosts of bringing product to buyer

Usage costsUsage costs Conversion and support costsConversion and support costs

End-of-life costsEnd-of-life costs Net of amounts received/spent at salvageNet of amounts received/spent at salvage

6262

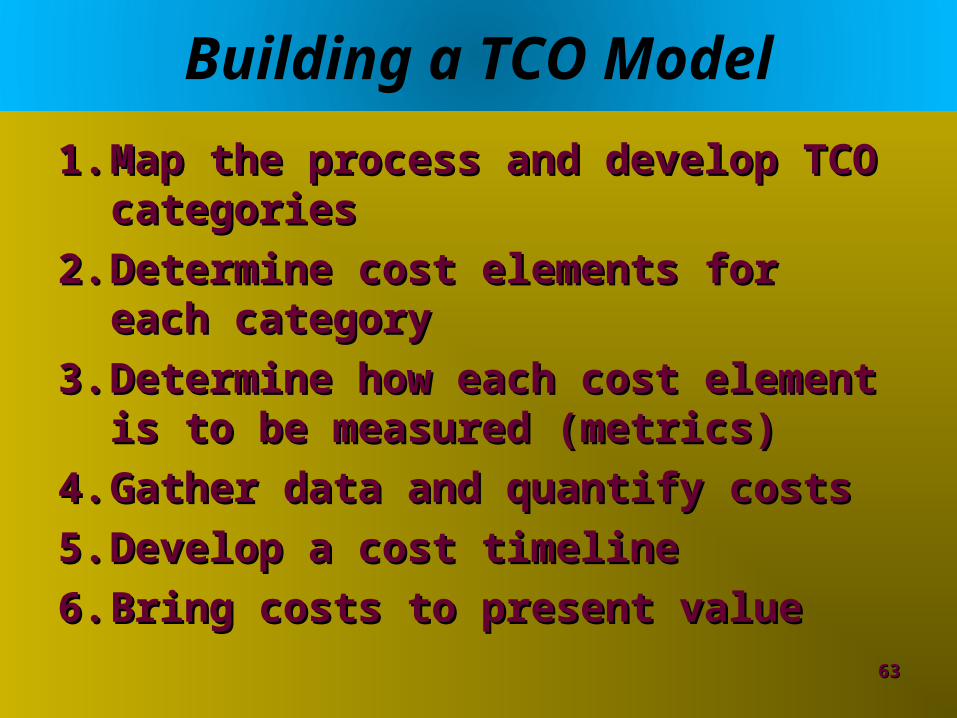

Building a TCO Model

1.1. Map the process and develop TCO Map the process and develop TCO categoriescategories

2.2. Determine cost elements for each Determine cost elements for each categorycategory

3.3. Determine how each cost element is to Determine how each cost element is to be measured (metrics)be measured (metrics)

4.4. Gather data and quantify costsGather data and quantify costs

5.5. Develop a cost timelineDevelop a cost timeline

6.6. Bring costs to present valueBring costs to present value6363

Opportunity Costs

DefinedDefined Cost of next best alternativeCost of next best alternative

Examples:Examples: Lost salesLost sales Lost productivityLost productivity DowntimeDowntime

6464

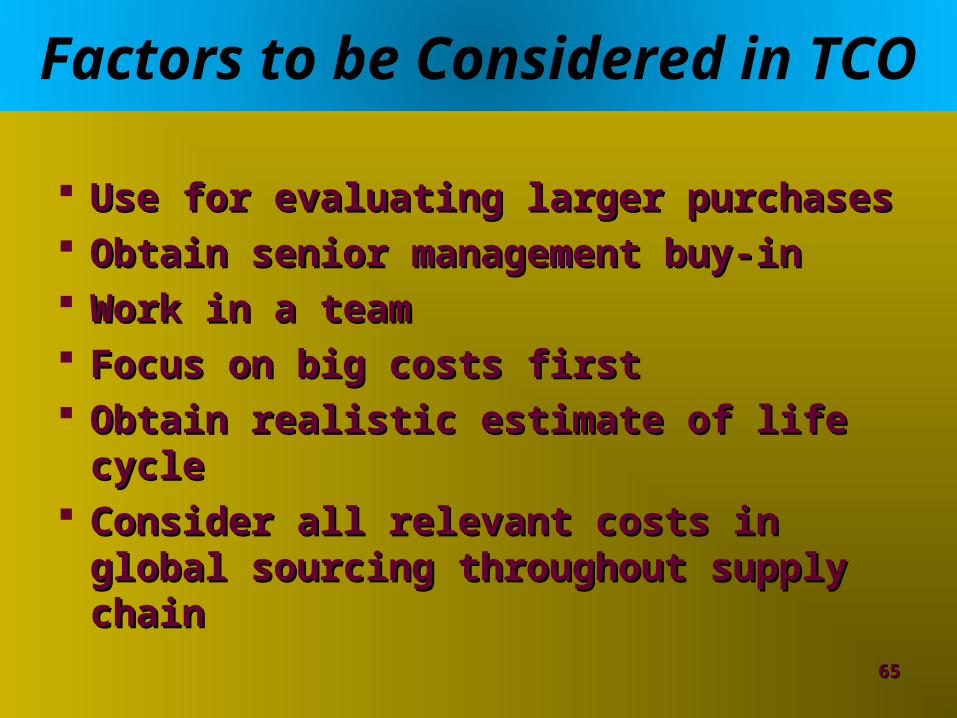

Factors to be Considered in TCO

Use for evaluating larger purchasesUse for evaluating larger purchases Obtain senior management buy-inObtain senior management buy-in Work in a teamWork in a team Focus on big costs firstFocus on big costs first Obtain realistic estimate of life cycleObtain realistic estimate of life cycle Consider all relevant costs in global Consider all relevant costs in global

sourcing throughout supply chainsourcing throughout supply chain

6565

TCO Model Example

Cost Elements Cost Measures for 1,000 PCs

Purchase price:• Hardware• Software licenses A, B, and C

• $1,200/PC – supplier quote• $450/PC – supplier quotes (3)

Acquisition costs:• Sourcing• Administration

• 2 FTE employees @ $85K and $170K for 2 months• 1 P.O. @ $150, 12 invoices @ $40 each

Usage costs:• Installation• Equipment support• Network support• Warranty• Opportunity cost – lost productivity

• $700/PC• $120/month/PC – supplier quote• $100/month – supplier quote• $120/PC for 3-year warranty• Downtime: 15 hours/PC/year @ $30/hour

End-of-life costs• Salvage value • $36/PC

6666

TCO Model Example

6767

Cost Elements Present Year 1 Year 2 Year 3 Purchase Price:

Hardware $ 1,200,000

Software licenses A, B, and C $ 450,000

Acquisition Costs: Sourcing $ 42,500

Administration $ 150 $ 480 $ 480 $ 480

Usage Costs: Opportunity cost – productivity $ 450,000 $ 450,000 $ 450,000

Installation $ 700,000

Equipment support $ 1,440,000 $ 1,440,000 $ 1,440,000

Network support $ 1,200,000 $ 1,200,000 $ 1,200,000

Warranty $ 120,000

End-of-Life Costs: Salvage value $ (36,000)

Total $ 2,512,650 $ 3,090,480 $ 3,090,480 $ 3,054,480

Present Values @ 12% $ 2,512,650 $ 2,759,799 $ 2,463,113 $ 2,174,790

Collaborative Cost Management

Target pricingTarget pricing Used in new product developmentUsed in new product development Sales Price – Profit = Allowable CostSales Price – Profit = Allowable Cost Gap in cost becomes cost reduction goalGap in cost becomes cost reduction goal

Cost savings sharingCost savings sharing Sharing of continuous improvement Sharing of continuous improvement

benefitsbenefits Financial incentives to supplier to pursue Financial incentives to supplier to pursue

cost reductioncost reduction

6868

Target and Cost-Based Pricing

Agreement on supplier’s full costsAgreement on supplier’s full costs Built upon high degree of …Built upon high degree of …

TrustTrust Information sharingInformation sharing Joint problem solvingJoint problem solving

Need to manage risks associated with Need to manage risks associated with target pricingtarget pricing Especially volume variabilityEspecially volume variability

6969

Target and Cost-Based Pricing

Identify and agree on:Identify and agree on: Product volumesProduct volumes Target product costs at different points in Target product costs at different points in

timetime Quantifiable productivity and quality Quantifiable productivity and quality

improvement projectionsimprovement projections Asset base and rate of return requirementsAsset base and rate of return requirements When cost sharing savings starts and how When cost sharing savings starts and how

calculatedcalculated

7070

When to Use Collaborative Cost Management Approaches

Not appropriate for all sourced itemsNot appropriate for all sourced items Supplier contributes high levels of Supplier contributes high levels of

value-addedvalue-added Complex, customized itemsComplex, customized items For products requiring conversion from For products requiring conversion from

raw materials through supplier’s designraw materials through supplier’s design

7171

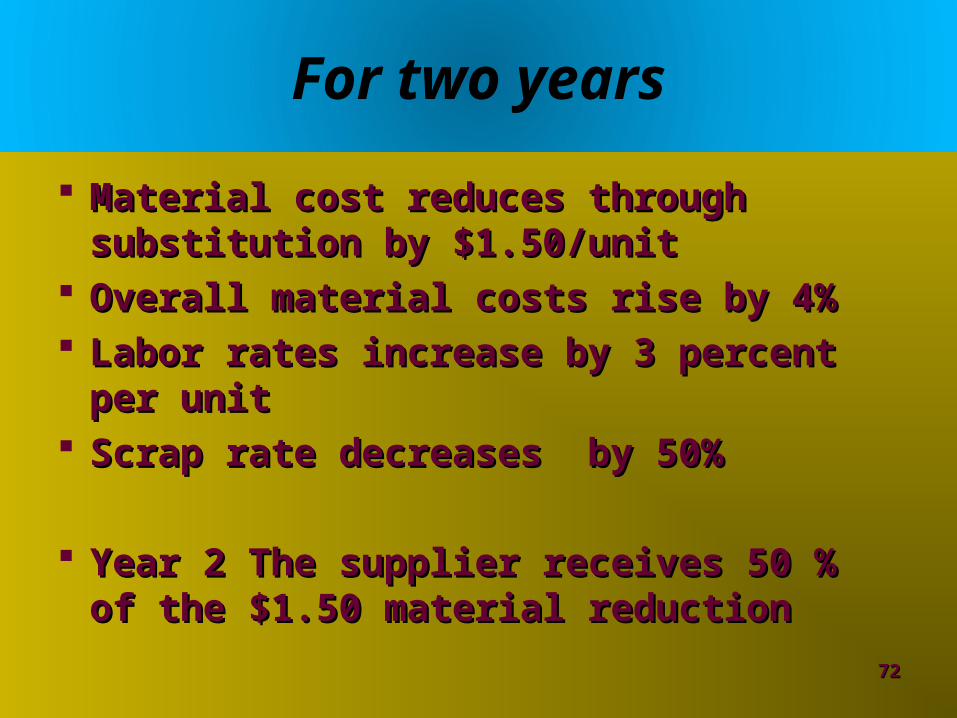

For two years

Material cost reduces through Material cost reduces through substitution by $1.50/unitsubstitution by $1.50/unit

Overall material costs rise by 4%Overall material costs rise by 4% Labor rates increase by 3 percent per unitLabor rates increase by 3 percent per unit Scrap rate decreases by 50%Scrap rate decreases by 50%

Year 2 The supplier receives 50 % of the Year 2 The supplier receives 50 % of the $1.50 material reduction$1.50 material reduction

7272

Cost-Based Pricing Example

First-year target price = $61.00

Negotiated/AnalyzedCost Structure

• Material• Labor rate• Burden rate• Scrap rate• SG&A expense rate• Effective volume range• Projected product life• ROI agreement

• $20/unit• $8.50/unit• 200% of direct labor• 10%• 10% of mfg cost• 125,000 units/year ± 10%• 2 years• 30%

Supplier InvestmentTotal Supplier Investment

Year 1$3,000,000$5,000,000

Year 2$2,000,000

Cost Savings Sharing(50/50)

• Direct labor• Scrap rate

• 10% annual reduction• 50% annual reduction

7373

Cost-Based Pricing Example

7474

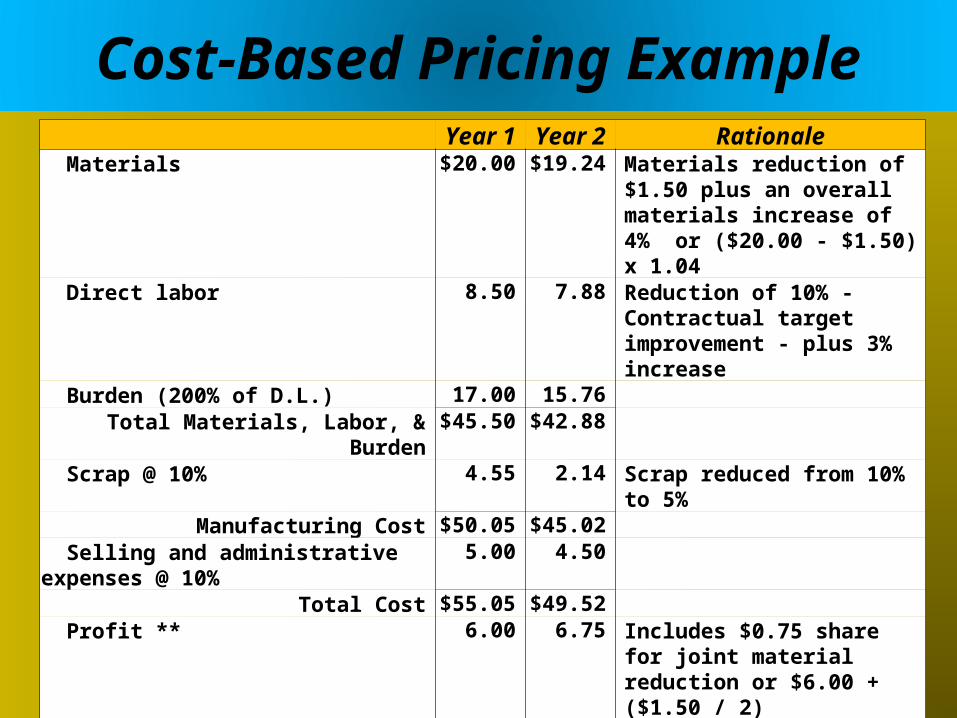

Year 1 Year 2 Rationale Materials $20.00 $19.24 Materials reduction of $1.50 plus

an overall materials increase of 4% or ($20.00 - $1.50) x 1.04

Direct labor 8.50 7.88 Reduction of 10% - Contractual target improvement - plus 3% increase

Burden (200% of D.L.) 17.00 15.76Total Materials, Labor, & Burden $45.50 $42.88

Scrap @ 10% 4.55 2.14 Scrap reduced from 10% to 5% Manufacturing Cost $50.05 $45.02

Selling and administrative expenses @ 10% 5.00 4.50Total Cost $55.05 $49.52

Profit ** 6.00 6.75 Includes $0.75 share for joint material reduction or $6.00 + ($1.50 / 2)

Selling price $61.05 $56.27 New selling price after Year 1 improvements

** Profit based on 30% return on investment negotiated in agreement ($5 million over 2-year investment x 0.3) / 250,000 total units = $6.00 profit/unit

![Untitled-2 [] ape.pdf · Customer Satisfaction Qualified Suppliers ... HONDA MOTORCYCLES HONDA ACTIVA TVS ACCESS TVS SCOOTY TVS XL SUPER . 3 Excellence in Quality 9-255 REAR WHELL](https://img.dokumen.tips/doc/110x75/5acc8eaa7f8b9a875a8cbf0b/untitled-2-apepdfcustomer-satisfaction-qualified-suppliers-honda-motorcycles.jpg)