Embed Size (px)

Citation preview

Stochastic volatility models and hybrid

derivatives

Claudio Albanese

Department of Mathematics / Imperial College London

? ? ?

Presented at Bloomberg and at the Courant Institute, New

York University

New York, September 22nd, 2005

Co-authors.

• Oliver Chen

(National University of Singapore)

• Antonio Dalessandro

(Imperial College London)

• Manlio Trovato

(Merrill Lynch London)

available at:

www.imperial.ac.uk/mathfin

1

Contents.

• Part I. A stochastic volatility term structure model.

• Part II. Credit barrier models with functional lattices.

• Part III. Estimations under P and under Q.

• Part IV. Pricing credit-equity hybrids.

• PART V. Credit correlation modeling and synthetic CDOs.

• Part VI. Pricing credit-interest rate hybrids.

2

PART I. A stochastic volatility term structure model

It is widely recognized that fixed income exotics should be priced by

means of a stochastic volatility model. Callable constant maturity

swaps (CMS) are a particularly interesting case due to the sensitivity

of swap rates to implied swaption volatilities for very deep out of the

money strikes. In this paper we introduce a stochastic volatility term

structure model based on a continuous time lattice which allows for

a numerically stable and quite efficient methodology to price fixed

income exotics and evaluate hedge ratios.

3

Introduction

The history of interest rate models is characterized by a long series of

turns. The Black formula for caplets and swaptions was designed to

take as underlying a single forward rate under the appropriate forward

measure, see (Joshi & Rebonato 2003). This has the advantage to

lead to a simple pricing formula for European options but also the

limitation of not being extendable to callable contracts. To have a

more consistent model, short rate models where introduced in (Cox,

Ingersoll & Ross 1985), (Vasicek 1977), (Black & Karasinski 1991)

and (Hull & White 1993). These models are distinguished by the exact

specification of the spot rate dynamics through time, in particular the

form of the diffusion process, and hence the underlying distribution of

the spot rate.

4

LMM models

Next came LIBOR market models, also known as correlation models.

First introduced in (Brace, Gatarek & Musiela 1996) and (Jamshidian

1997), forward LIBOR models affirmed themselves as a mainstream

methodology and are now discussed in textbooks such as for instance

(Brigo & Mercurio 2001). Various extensions of forward LIBOR mod-

els that attempt to incorporate volatility smiles of interest rates have

been proposed. Local volatility type extensions were pioneered in

(Andersen & Andreasen 2000). A stochastic volatility extension is

proposed in (Andersen & Brotherton-Ratcliffe 2001), and is further

extended in (Andersen & Andreasen 2002). A different approach to

stochastic volatility forward LIBOR models is described in (Joshi &

Rebonato 2003). Jump-diffusion forward LIBOR models are treated

in (Glasserman & Merener 2001), (Glasserman & Kou 1999). A cali-

bration framework is proposed in (Piterbarg 2003).

5

Stochastic volatility models

Modeling stochastic volatility within LIBOR market models is a chal-

lenging task from an implementation viewpoint. In fact, Monte Carlo

methods tend to be slow and inefficient in the presence of a large num-

ber of factors. In a strive to achieve a more reliable pricing framework,

in recent years, we witnessed a move away from correlation models

and the emergence and recognition as market standard of the SABR

model by (S.Hagan, Kumar, S.Lesniewski & E.Woodward 2002) in the

fixed income domain.

6

SABR

SABR however is unlikely to be the definitive solution and is perhaps

rather just yet another stepping stone in a long chain. In fact, like-

wise to the Black formula approach, SABR takes up a single forward

rate under the corresponding forward measure as underlier. As a con-

sequence, within this framework it is not possible to price callable

swaps and Bermuda swaptions. There are also calibration inconsis-

tencies. Implied swaption volatilities with very large strikes are probed

by constant maturity swaps (CMS), structures which receive fixed, or

LIBOR plus a spread, and pay the equilibrium swap rate of a given

maturity. The asymptotic behavior of implied volatilities for very large

strikes turns out to flatten out to a constant, as opposed to diverging

rapidly as SABR would predict. Finally, some pricing inconsistencies

may emerge with SABR due to the fact that the model is solved by

means of asymptotic expansions with a finite, irreducible error.

7

Stochastic volatility term structure models

In this article we attempt to go beyond SABR by introducing a stochas-

tic volatility short rate model which has the correct asymptotic behav-

ior for implied swaption volatilities and can be used for callable swaps

and Bermuda swaptions. Our model is solved efficiently by means of

numerical linear algebra routines and is based on continuous time lat-

tices of a new type. No calculation requires the use of Montecarlo or

asymptotic methods and prices and hedge ratios are very stable, even

for extreme values of moneyness.

8

Nearly stationary calibration

Our model is made consistent with the term structure of interest rates

and the term structure of implied at-the-money volatilities by means

of a calibration procedure that greatly reduces the degree of time

dependency of coefficients. As a consequence, the model is nearly

stationary over time horizons in excess of 30 years.

9

Applications

In this presentation, I discuss the model by reviewing in detail an

implementation example. While leaving it up to the interested reader

to pursue the many conceivable variations and extensions, we describe

the salient features of our modeling by focusing in detail to the problem

of pricing and finding hedge ratios for Bermuda swaptions and callable

CMS swaps.

10

The model

Our model is built upon a specification of a short rate process rt

which combines local volatility, stochastic volatility and jumps. We

make our best effort to calibrate the model to a stationary process

and introduce the least possible degree of explicit time dependence in

such a way to refine fits of the term structure of interest rates and of

selected at-the-money swaption volatilites. The model is specified in

a largely non-parametric fashion within a functional analysis formalism

and expressed in terms of continuous time lattice models.

A sequence of several steps is required to specify the short rate process

rt.

11

The conditional local volatility processes

We introduce M states of volatility. The process conditioned to stay

in one of such states α ∈ 1, ...M is related to the solution rαt of the

following equation:

drαt = κα(θα − rαt)dt + σαrβααt dW. (1)

12

Short rate volatilities for each of the four volatility states

13

The functional analysis formalism

In the functional analysis formalism we use, these SDEs are associated

to the Markov generators

Lrα = κα(θα − rαt)

∂

∂r+

σ2αr

2βααt

2

∂2

∂r2. (2)

14

Functional lattices

To build a continuous time lattice (also called functional lattice), we

discretize the short rate variable and constrain it to belong to a finite

lattice Ω containing N +1 points r(x) ≥ 0, where x = 0, ...N , r(0) = 0

and the following ones are in increasing order. The discretized Markov

generator LrΩα is defined as the operator represented by a tridiagonal

matrix such that ∑yLr

Ωα(x, y) = 0∑yLr

Ωα(x, y)(y − x) = κα(θα − r(x))∑yLr

Ωα(x, y)(y − x)2 = σ2αr(x)2βα.

15

Model parameters

In our example, we select an inhomogeneous grid of N = 70 points

spanning short rates from 0% to 50%. We also choose to work with

M = 4 states for volatility and make the following parameter choices:

α σα βα θα κα

0 31% 30% 2.10% .171 46% 40% 5.50% .182 75% 50% 8.50% .233 100% 60% 12.00% .24

16

How to solve in the special case of a local volatility model (M=1)

and without jumps

Although our model is more complex than a simple local volatility

process, it is convenient to describe our resolution method in the

specific case of the operator LrΩα with constant α. This method can

then be generalized and is at the basis of other extensions such as the

introduction of jumps (see below).

17

Spectral analysis

We start by considering the following pair of eigenvalue problems:

LrΩαun = λnun LrT

Ωαvn = λnvn

where the superscript T denotes matrix transposition, un and vn are

the right and left eigenvectors of LrΩα, respectively, whereas λn are the

corresponding eigenvalues. Except for the simplest cases, the Markov

generator LrΩα is not a symmetric matrix, hence un and vn are different.

18

Spectral analysis

Also, in general the eigenvalues are not real. We are only guaranteed

that their real part is non-positive Reλn ≤ 0 and that complex eigen-

values occur in complex conjugate pairs, in the sense that if λn is an

eigenvalue then also λn is an eigenvalue. We set boundary conditions

in such a way that there is absorption at the endpoints, and in par-

ticular at the point corresponding to zero rates r(0) = 0. With this

choice, we are also guaranteed that there exists a zero eigenvalue.

19

Spectral analysis

There is no guarantee, in the most general case, that there exists

a complete set of eigenfunctions. However, the chance that such a

complete set does not exist for a Markov generator specified non-

parametrically is zero, so we can safely assume that this is the case.

In the unlikely case that this assumption is not correct, the numerical

linear algebra routines needed to solve our lattice model will identify

the problem and a small perturbation of the given operator will suffice

to rectify the situation. Assuming completeness, the diagonalization

problem can be rewritten in the following matrix form:

LrΩα = UΛU−1 (3)

where U is the matrix having as columns the right eigenvectors and Λ

is the diagonal matrix having the eigenvalues λi as elements.

20

Functional calculus

Key to our constructions is the remark that, if the Markov generator

is diagonalisable, we can apply an arbitrary function F to it by means

of the following formula:

F (LrΩα) = UF (∗r

Ωα)U−1 (4)

This formula is at the basis of the so-called ”functional calculus”.

As Ito’s formula regarding functions of stochastic processes is central

in the mathematical Finance for diffusion processes, functional cal-

culus for Markov generators plays a pivotal role in our framework for

stochastic volatility models.

21

Functional calculus

This formula has several applications. An immediate one allows us to

express the pricing kernel u(r(x), t; r(y), T ) of the process as follows:

u(r(x), t; r(y), T ) = (e(T−t)LrΩα)(x, y) =

∑n

eλn(T−t)un(x)vn(y). (5)

22

Introducing jumps

At this stage of the construction one has the option to also add jumps.

Although in the example discussed in this paper we are mostly focused

on long dated callable swaps and swaptions for which we find that the

impact of jumps can be safely ignored, adding jumps involves negligible

additional complexities and is thus worth considering and implement-

ing in other situations. To add jumps, one can follow the following

procedure which accounts for the need to assign different intensities

to up-jumps and down-jumps. Jump processes are associated to a

special class of stochastic time changes given by monotonously non-

decreasing processes Tt with independent increments.

23

Stochastic time changes

The time changes characterizing Levy processes with symmetric jumps

are known as Bochner subordinators and are characterized by a Bochner

function φ(λ) such that

E0

[e−λTt

]= e−φ(λ)t (6)

24

The variance-gamma model

For example, the case of the variance gamma process which received

much attention in Finance corresponds to the function

φ(λ) =µ2

νlog

(1 + λ

µ

ν

)(7)

where µ is the mean rate and ν is the variance rate of the variance

gamma process.

25

The generator of the jump process

The generator of the jump process can be expressed using functional

calculus as the operator −φ(−LrΩα). To produce asymmetric jumps,

we specify the two parameters differently for the up and down jumps

and compute separately two Markov generators

L± = −φ±(−LrΩα) = −U±φ±(Λ)V± (8)

where:

φ±(λ) =µ2±

ν±log(1 + λ

µ±ν±

) (9)

26

The generator of the process with asymmetric jumps

The new generator for our process with asymmetric jumps is obtained

by combining the two generators above

LrjΩα =

0 · · · · · · · · · 0

L−(2,1) d(2,2) L+(2,3) · · · L+(2, n)... ... . . . · · · ...

L−(n− 1,1) L−(n− 1,2) · · · d(n− 1, n− 1) L+(n− 1, n)0 0 · · · · · · 0

27

Probability conservation and boundary conditions

Here the element of the diagonal are chosen in such a way to satisfy

probability conservation:

d(x, x) = −∑y 6=x

LrjΩα(x, y) (10)

Also notice that we have zeroed out the elements in the matrix at the

upper and lower boundary: this ensures that there is no probability

leakage in the process.

28

Drift condition

In our setting, we choose a short rate as a modeling primitive and

we thus do not need to impose a martingale condition. Otherwise,

were we working with a forward rate instead, the appropriate method

of restoring the martingale condition would be to modify the matrix

elements of the resulting generator on the first sub-diagonal and the

first super-diagonal.

29

The Local Levy generator

At this stage of the construction, we have therefore obtained a gener-

ator LrjΩα for the short rate process, whose dynamics is characterized

by a combination of state dependent local volatility and asymmetric

jumps. We note that the addition of jumps has not increased the di-

mensionality of the problem and is therefore computationally efficient.

30

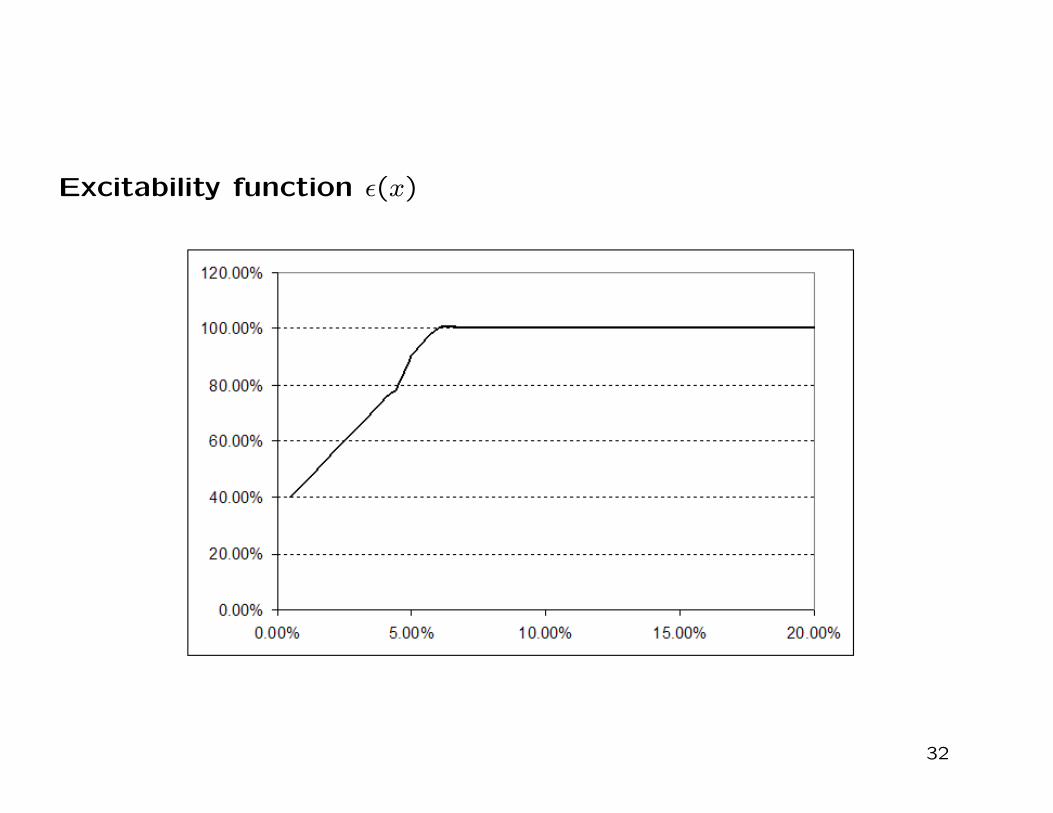

Modeling the dynamics of stochastic volatility

As a third step, we define a dynamics for stochastic volatility by as-

signing a Markov generator to the volatility state variable α which

depends on the rate coordinate x. Namely, conditioned to the rate

variable being x, the generator has the following form

Lsvx = ε(x)Lsv

+ + Lsv− (11)

where

Lsv+ =

−0.7 0.7 0 0

0 −1.1 0.8 0.30 0 −1.5 1.50 0 0 0

, Lsv− =

0 0 0 0

1.4 −1.4 0 00 3 −3 00 0 5 −5

.

(12)

31

Excitability function ε(x)

32

The total generator

Out of the two generators we just defined, we form a Markov generator

L acting on functions of both the rate variable x and the volatility

variable α. This generator has matrix elements given as follows:

L(x, α; y, β) = LrjΩα(x, y)δα,β + Lsv

x (α, β)δxy. (13)

33

Numerical analysis

In our working example, the matrix L has total dimension MN = 280.

For matrices of this size, diagonalization routines such as dgeev in

LAPACK are very efficient. Since our underlier is a short rate though,

we are not interested in the pricing kernel but rather in the discounted

transition probabilities given by

p(x, t; y, T ) = E

[e−∫ Tt rsds, |rt = r(x), rT = r(y)

]. (14)

34

Numerical analysis

This kernel satisfies the following backward equation

∂

∂tp(x, t; y, T ) + (Lp)(x, t; y, T ) = r(x)p(x, t; y, T ). (15)

In functional calculus notations, the solution is given by

p(x, t; y, T ) = eG(T−t)(x, y) where G(x, y) ≡ L(x, y)− r(x)δxy.

(16)

35

Numerical analysis with stochastic volatility

The same diagonalization method illustrated above for the local volatil-

ity case applies also in this situation. By representing the matrix G in

the form

G = UΛU−1 (17)

where Λ is diagonal, and writing the matrix of discounted transition

probabilities as follows

eG(T−t) = UeΛ(T−t)U−1. (18)

36

Calibration and Pricing

In our example, to calibrate our model we aim at matching forward

swap rates and at-the-money swaption volatilities, both referring to

swaps of 5 year tenor. We start from the following data

1y 2y 3y 4y 5y 7y 10y 15y 20y 30yforward 2.999% 3.311% 3.587% 3.800% 3.984% 4.226% 4.393% 4.477% 4.301% 4.114%ATM vol 21.506% 19.443% 17.962% 16.967% 16.189% 14.897% 13.801% 12.460% 12.665% 11.728%

37

Nearly stationary calibration

The calibration procedure has two steps. In a first step we search for

a best fit using the model above without introducing any explicit time

dependency. In a second step, we then introduce time dependency to

achieve a perfect fit. As a consequence of this procedure, the degree

of time variability of model parameters is kept to a bare minimum.

To introduce time dependence we combine two operations: a shift of

the short rate by a time varying, deterministic function of time and a

deterministic time change, i.e.

rt → rt = b(t)rb(t) + a(t). (19)

38

Nearly stationary calibration

Here b(t) is monotonously increasing and b(t) denotes its time deriva-

tive. Using the new process, discounted transition probabilities can be

computed as follows:

E

[e−∫ Tt rsds, |rt = r(x), rT = r(y)

]= e−

∫ Tt a(s)dsG(x, b(t); y, b(T )) (20)

where G is the kernel for the stationary process defined above.

Our choice in the working example is b(t) = 1.095t + 0.008t2. The

function a(t) is then defined in such a way to match the term structure

of forward swap rates. This adjustment is given in the next slide.

39

Deterministic yield adjustment (EUR)

40

Degree of time dependence

As one can see from this picture, the yield adjustment is less than 20

basis points in absolute value. This ensures that the probability of the

modified short rate process rt to attain negative values is small. In a

typical implementation of the Hull-White model along similar lines, the

short rate adjustment is typically of a few percent. The discrepancy

is linked to the fact that the richer stochastic volatility model we

construct is capable of explaining most of the salient features of the

zero curve even with the constraint that the process be stationary.

41

Advantages of nearly stationary model calibration

The advantage of having a nearly stationary model is that the shapes

of yield curves that one obtains depend on the short rate and the

volatility state but are largely independent of time. The figure in

the next slide shows the yield curves corresponding to different initial

volatility states and different starting values for the short rate. As

the graphs indicate, yield curves are sensitive to the initial volatility

state as they raise if initial volatilities raise. Moreover graphs show

that curves invert for high values of the short rate. In our model, this

behavior is consistent over all time frames except for corrections of

the order of 10 basis points.

42

Yield curves for different values of the initial volatility state and

of the short rate

43

Pricing swaptions and callable constant maturity swaps

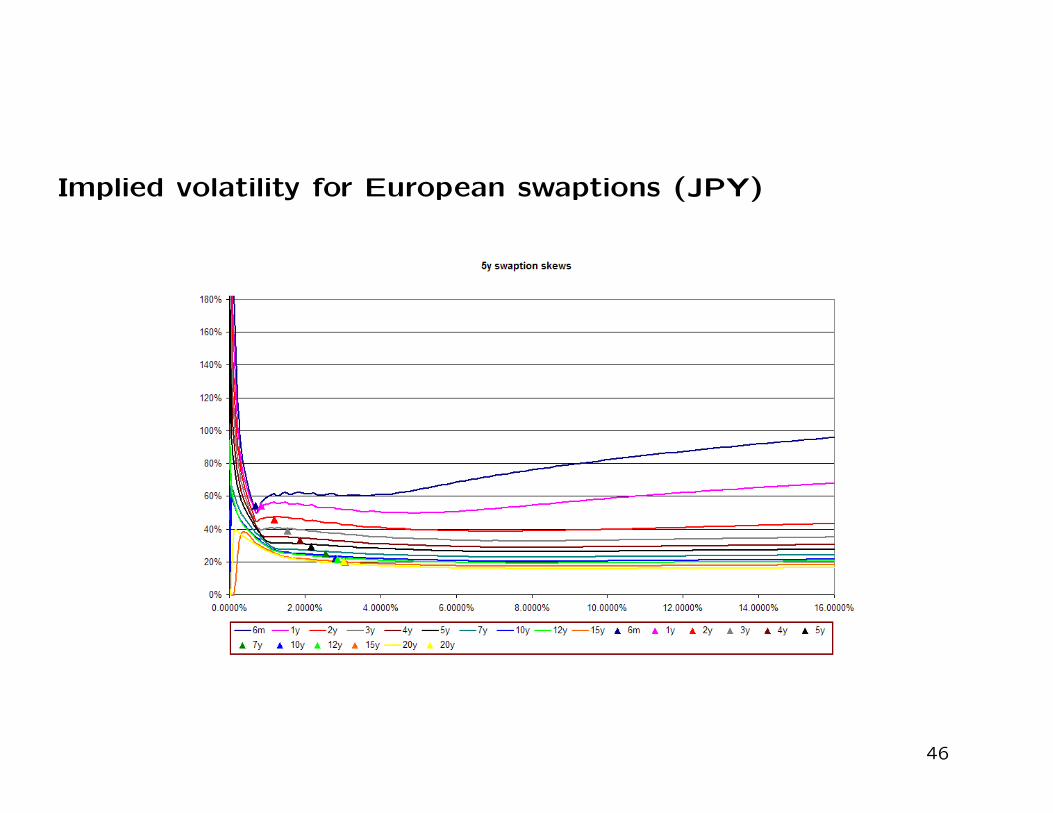

Implied volatilities for European swaptions are given in the next slide.

Here we graph extreme out of the money strikes of up to 15% for

swaptions of varying maturities where the deliverable is a 5Y swap.

One can notice that implied volatilities naturally flatten out at long

maturities, a behavior consistent with what observed in the CMS mar-

ket where such extreme strike levels are probed.

44

Implied volatility for European swaptions (EUR)

45

Implied volatility for European swaptions (JPY)

46

Term structure of implied 5Y swaption volatilities (JPY)

47

Bermuda swaptions

Exercise boundaries for 10Y Bermuda swaptions are given in the next

slides. The first graph refers to payer swaptions and the second to

receiver swaptions.

48

Exercise boundaries for payer Bermuda options

49

Exercise boundaries for receiver Bermuda options

The corresponding graphs for callable CMSs are given below. Notice

that the exercise boundaries depend on the volatility state.

50

Exercise boundaries for callable payer CMSs

51

Exercise boundaries for callable receiver CMSs

52

Sensitivities for Bermuda swaptions

Sensitivities for Bermuda swaptions are given in the next slides. These

sensitivities are computed by holding the volatility state variable fixed

and are defined as the derivative of the price for a 10Y payer Bermuda

swaption with respect to the rate of the 10Y swap.

53

Delta of a 10Y Bermuda swaption, with semi-annual exercise

schedule, with respect to the 10Y swap rate. This is computed

while holding fixed the volatility state variable.

54

Gamma of a 10Y Bermuda swaption, with semi-annual exercise

schedule, with respect to the 10Y swap rate. This is computed

while holding fixed the volatility state variable.

55

Sensitivities for Constant Maturity Swaps

Sensitivities of callable constant maturity swaps are given in the next

slides. The delta and gamma are computed similarly to what done for

Bermuda swaptions, while the vega is calculated instead with respect

to the 10Y into 5Y European swaption.

56

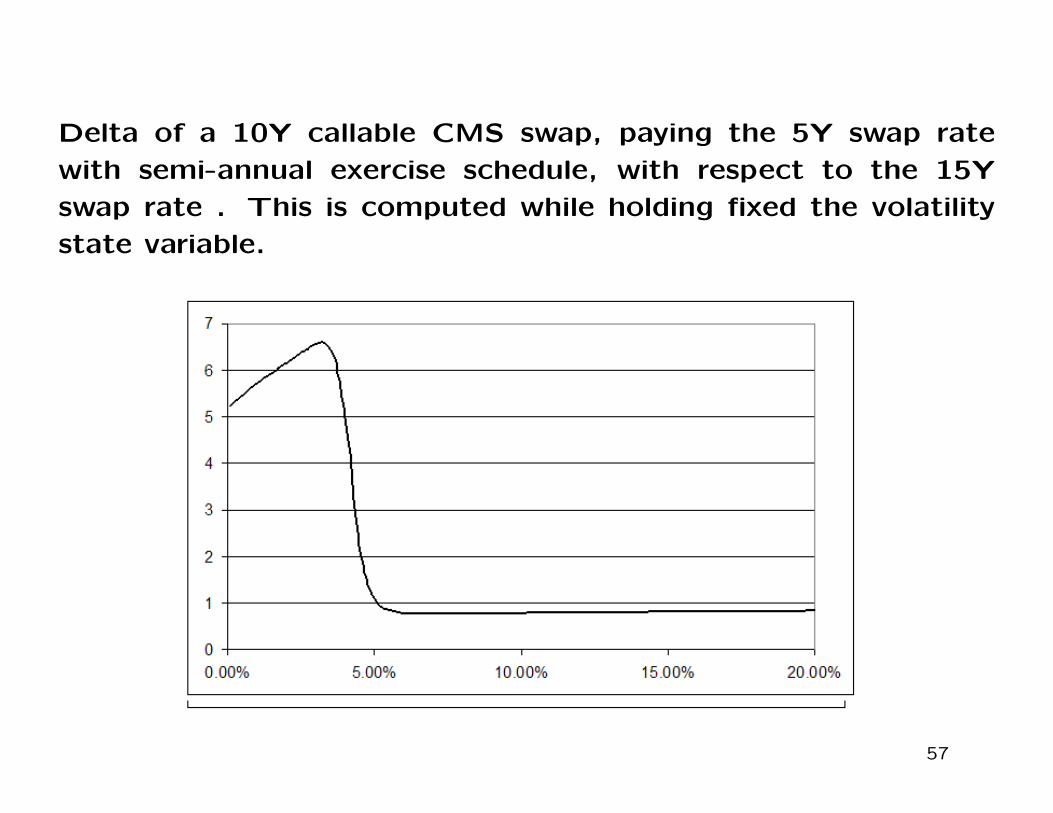

Delta of a 10Y callable CMS swap, paying the 5Y swap rate

with semi-annual exercise schedule, with respect to the 15Y

swap rate . This is computed while holding fixed the volatility

state variable.

57

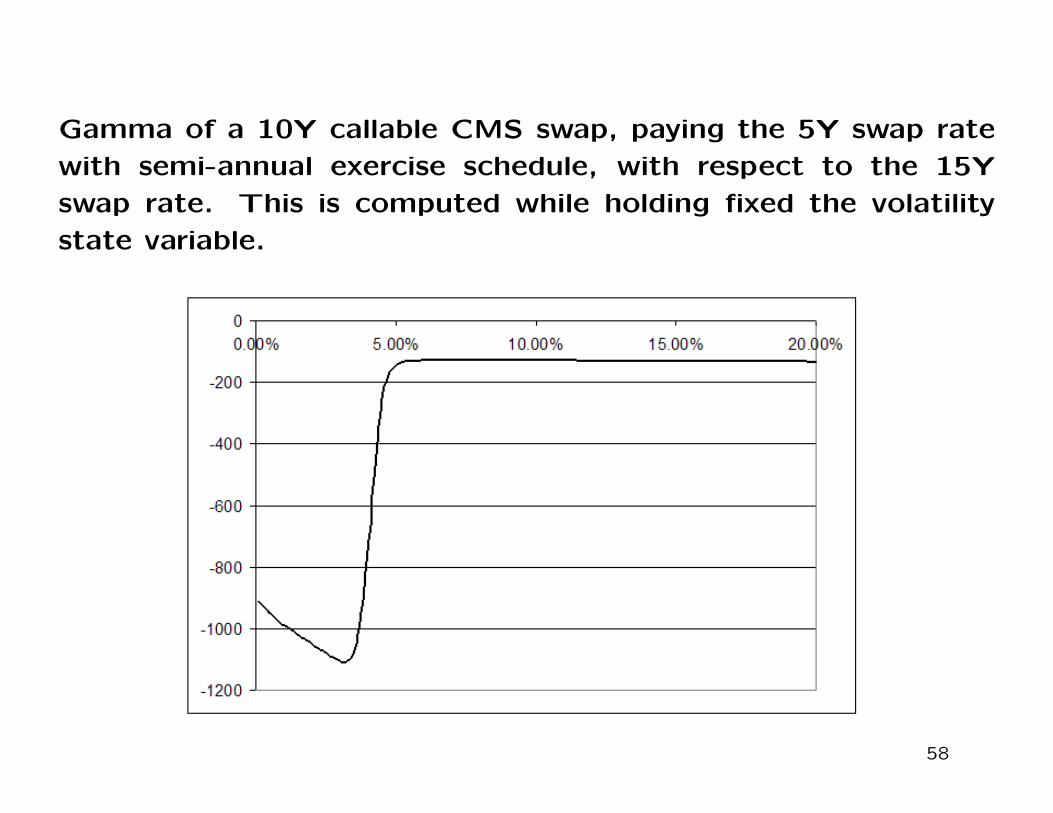

Gamma of a 10Y callable CMS swap, paying the 5Y swap rate

with semi-annual exercise schedule, with respect to the 15Y

swap rate. This is computed while holding fixed the volatility

state variable.

58

Vega of a 10Y callable CMS swap, paying the 5Y swap rate with

semi-annual exercise schedule, with respect to the 10Y into 5Y

European swaption price. This is computed while holding fixed

the short rate.

59

Conclusions

We present a stochastic volatility term structure model, providing a

consistent framework for pricing European and Bermuda options, as

well as callable CMS swaps. The model is built upon a specification

of a short rate process, which combines local volatility, stochastic

volatility and jumps. The richness of the model allows to keep the

degree of time variability of model parameters to a bare minimum,

and obtain a nearly stationary behaviour. The solution methodology

is based on a new type of continuous time lattices, which allow for a

numerically stable and quite efficient technique to price fixed income

exotics and evaluate hedge ratios.

60

PART II. Credit Barrier Models

Statistical data that we would like a credit model to fit includes:

• historical default probabilities given an initial credit rating

• historical transition probabilities between credit ratings

• interest rate spreads due to credit quality

61

Credit-rating based models

The early models of this class considered the credit-rating migration

and default process as a discrete, time-homogenous Markov chain

and took the historical transition probability matrix as the Markov

transition matrix.

Deficiencies:

• difficult to correlate

• risk-neutralization leads to unintuitive results

62

Analytic closed form solutions versus numerical linear algebra

methods

The former framework for credit barrier models leveraged on solvable

models.

In the newer version recently developed we have a flexible non-parametric

framework, whereby tractability comes from the use of numerical lin-

ear algebra as opposed to coming from the analytical tractability of

special functions.

63

The underling diffusion process

The first building block of our construction is a Markov chain process

xt on the lattice Ω = 0, h, ..., hN ⊂ [0,1] where N is a positive integer

and h = 1/N . In the case of a discretized diffusion with state depen-

dent drift and volatility, the infinitesimal generator L, of the process

xt is a tridiagonal matrix and can be expressed as follows in terms of

finite difference operators:

Lx = a(x)∆ + [b(x)− a(x)]∇+

where x ∈ Ω and

(∆f)(x) = f(x+1)+f(x−1)−2f(x), and (∇+f)(x) = f(x+1)−f(x).

(21)

64

Continuous space limit

To ensure the existence of a continuous space limit, we derive the

functions a(x), b(x) from a drift function µ(ξ) and a volatility function

σ(ξ), where ξ ∈ [0,1], which is identifiable as the credit quality process

and can be expressed in terms of its infinitesimal by imposing the

following conditions: ∑y L(x, y)(y − x) = µ(hx)∑y L(x, y)(y − x)2 = σ(hx)2∑

y L(x, y) = 0

65

The P and the Q measure

In our model, we actually use two drift functions: µP (ξ) and µQ(ξ),

one defining the P or statistical measure and the latter modeling the Q

or pricing measure. We postulate that the only difference between the

P and the Q measure lies in the specification of these two drift func-

tions. Correspondingly, we use the subscripts P and Q to identify the

Markov generator and transition probabilities under the corresponding

measure. Whenever the subscripts are omitted as here below, formulas

apply to both the P and the Q measure.

66

Eigenvalue problems and functional calculus

To manipulate the Markov generator by means of functional calculus,

the first step is to diagonalize it. Let λn be the eigenvalues of the

operator L and let un(x) and vn(x) be the right eigenvectors, so that

Lun = λnun.

67

Numerical methods for eigenvalue problems

In most cases, Markov generators admit a complete set of eigenvec-

tors. Although there are exceptions where diagonalization is not pos-

sible and one can reduce the operator at most to a non trivial Jordan

form with non-zero off-diagonal elements, these exceptional situations

occur very rarely both in a measure theoretic sense, as exceptions span

a set of zero measure, and in a topological sense as their complement

is dense in the space of all generators. In practical terms, this implies

that non-diagonalizable operators arise very rarely if at all in practice

and whenever they do, a professional numerical diagonalization algo-

rithm would detect the problem and a small perturbation of the model

parameters would rectify. To carry out numerical diagonalization, we

find that the function dgeev in the public domain package LAPACK is

quite suitable.

68

Diagonalizing the Markov generator

We just assume that the operator L admits a complete set of eigen-

vectors. In this case, we can form the matrix U whose columns are

given by the eigenvectors un(x) and write

L = UΛU−1. (22)

We denote with V the operator U−1 and with vn(x) its row vectors.

69

Functional calculus

Key to our constructions is the remark that if the matrix operator Lis diagonalizable we can apply an arbitrary function F to it by means

of the following formula:

F (L) = UF (Λ)U−1 (23)

This formula is at the basis of the so-called ”functional calculus”. As

Ito’s formula regarding functions of stochastic processes is central in

the stochastic analysis for diffusion processes, functional calculus for

Markov generators plays a pivotal role in our framework for stochastic

volatility models. This formula has several applications. An immediate

one allows us to express the pricing kernel u(x, t; y, t′) of the process

as follows:

u(x, t; y, t′) = (e(t′−t)L)(x, y) =

∑n

eλn(t′−t)un(x)vn(y). (24)

70

Introducing jumps

At this stage of the construction we add jumps. Jumps are ubiquitous

in credit model and we find that a jump component is necessary in

order to reconcile observed default probabilities with credit migration

probabilities. Within our framework, adding jumps involves marginal

additional complexities from the numerical viewpoint.

71

Asymmetric jumps

To reflect asymmetries in the jump intensities, we model separately

up and down jumps. A particularly interesting class of jump processes

is associated to stochastic time changes given by monotonously non-

decreasing processes Tt with independent increments. These time

changes are known as Bochner subordinators and are characterized by

a Bochner function φ(λ) such that

E0

[e−λTt

]= e−φ(λ)t (25)

For example, the case of the variance gamma process which received

much attention in Finance corresponds to the function

φ(λ) =µ2

νlog

(1 + λ

µ

ν

)(26)

where µ is the mean rate and ν is the variance rate of the variance

gamma process.

72

Functional calculus with subordinated generators

The generator of the jump process corresponding to the subordination

of a process of generator L can be expressed using functional calculus

as the operator −φ(−L). To produce asymmetric jumps, we specify

the two parameters differently for the up and down jumps and compute

separately two Markov generators

L± = −φ±(−L) = −U±φ(−Λ±)V± (27)

where:

φ±(λ) =µ2±

ν±log

(1 + λ

µ±ν±

)(28)

73

Generators with asymmetric jumps

The new generator for our process with asymmetric jumps is obtained

by combining the two generators above

L =

0 · · · · · · · · · 0

L−(2,1) d(2,2) L+(2,3) · · · L+(2, n)... ... . . . · · · ...

L−(n− 1, n) L−(n− 1,2) · · · d(n− 1, n− 1) L+(n− 1, n)0 0 · · · · · · 0

Here the element of the diagonal are chosen in such a way to satisfy

the condition of probability conservation

d(i, i) = −∑j 6=i

L(i, j) (29)

Also notice that we have zeroed out the elements in the matrix at the

upper and lower boundary: this ensures that there is no probability

leakage in the process.

74

Adding jumps

At this stage of the construction, we have therefore obtained a gen-

erator Lj for the process of distance to default, whose dynamics is

characterized by a combination of state dependent local volatility and

asymmetric jumps. We note that the addition of jumps has not in-

creased the dimensionality of the problem and is therefore computa-

tionally efficient.

75

PART III: Estimation and calibration: P measure

We first estimate the process for distance to default xt with respect to

the statistical measure P by matching transition probabilities over one

year and default probabilities over time horizons of 1, 3 and 5 years.

A credit rating system consists of a number K of different classes. In

the case of the extended system by Moody’s, K = 18 and the ratings

are:

0,1, . . . ,17 ↔ Default,Caa,B3,Ba3,Ba2, . . . ,Aa3,Aa2,Aa1,Aaa

76

Introducing barriers

We subdivide the nodes of the lattice Ω into K subintervals of adjacent

nodes:

Ii = [xi−1, ...xi] (30)

where 0 = x0 < x1 < ... < xK = N and #(xi − xi−1) = NK , for i =

1, ..., K. The interval Ii corresponds to the i-th rating class. If a

process is in Ii at time t, then is said to have a credit rating of i. ∀i,

xi ∈ Ii denotes the initial node. The conditional transition probability

pij(t) that an obligor with a given initial rating i at time 0 will have

a rating j at a later time t > 0 can be estimated by matching it with

historical averages provided by credit assessment institutions.

77

Introducing barriers

For our purposes, we model this quantity as follows:

pij(t) =

aj−1∑y=aj−1

uP (0, xi; t, y).

where xi is a point in the interval Ii which represents the barycenter

of the population density in that credit class and is part of the model

specification. For simplicity’s sake, we take xi to be the midpoint of

the interval Ii.

78

The state of default

Absorption into the state x = 0 is interpreted as the occurrence of

default. The probability that starting from the initial rating i and

reaching a state of default by time t is given by

pDi (t) = uP (0, xi; t,0).

The model under P is characterized by a drift function µP (ξ), a

volatility function σ(ξ) and jump intensities. The first two func-

tions are graphed below, while the variance rates we estimated are

ν+ = 7.5, ν− = 4.

79

Local volatility σ(ξ) vs. distance to default

80

Local drifts µP (ξ) and µQ(ξ) vs distance to default under the P

and the Q measure, respectively.

81

Comparison of discrete model (lines) and historical (dots) one

year transition probabilities.

82

Comparison of discrete model (lines) and historical (dots) de-

fault probabilities.

83

Estimation and calibration: Q measure

Risk neutralization is defined by changing the drift function µP (ξ) into

µQ(ξ), while leaving everything else unaltered.

The new drift is chosen in such a way to fit spread curves. Term

structures of probability of default for each rating class are given by

qDi (t) = uQ(0, xi; t,0). (31)

84

CDX index spreads

In our example, we use CDS spreads for 125 names in the Dow Jones

CDX index. We looked at 5 datasets by Mark-it Partners correspond-

ing to the last business days of the months of January, February,

March, April and May 2005. The datasets provide CDS spreads at

maturities: 6m, 1y, 2y, 3y, 5y, 7y, 10y and tentative recovery rates for

each name. We insist that the CDS spreads be matched by our model

and take the liberty of adjusting the term structure of recovery rate

for each name. Besides having to estimate the drift under Q we also

estimate the current distance to default for each name. The objective

is to ensure that the term structure of recovery rates be as flat as

possible and as close as possible to the tentative input value.

85

Comparison of discrete model (lines) and market (dots) for

spread curves of investment grade bonds (Data taken 02/10/2003)

86

Comparison of discrete model (lines) and market (dots) for

spread curves of speculative grade bonds (Data taken 02/10/2003)

87

Liquidity spreads

From these pictures one can notice a systematic bias in spreads. Our

model appears to systematically underestimate BB spreads and over-

estimate BBB spreads.

This can be interpreted in terms of the differential liquidity in the two

market sectors.

88

CDS Spreads: Investment Grades (Data from March 2005)

89

CDS Spreads: Non-Investment Grades (Data from March 2005)

90

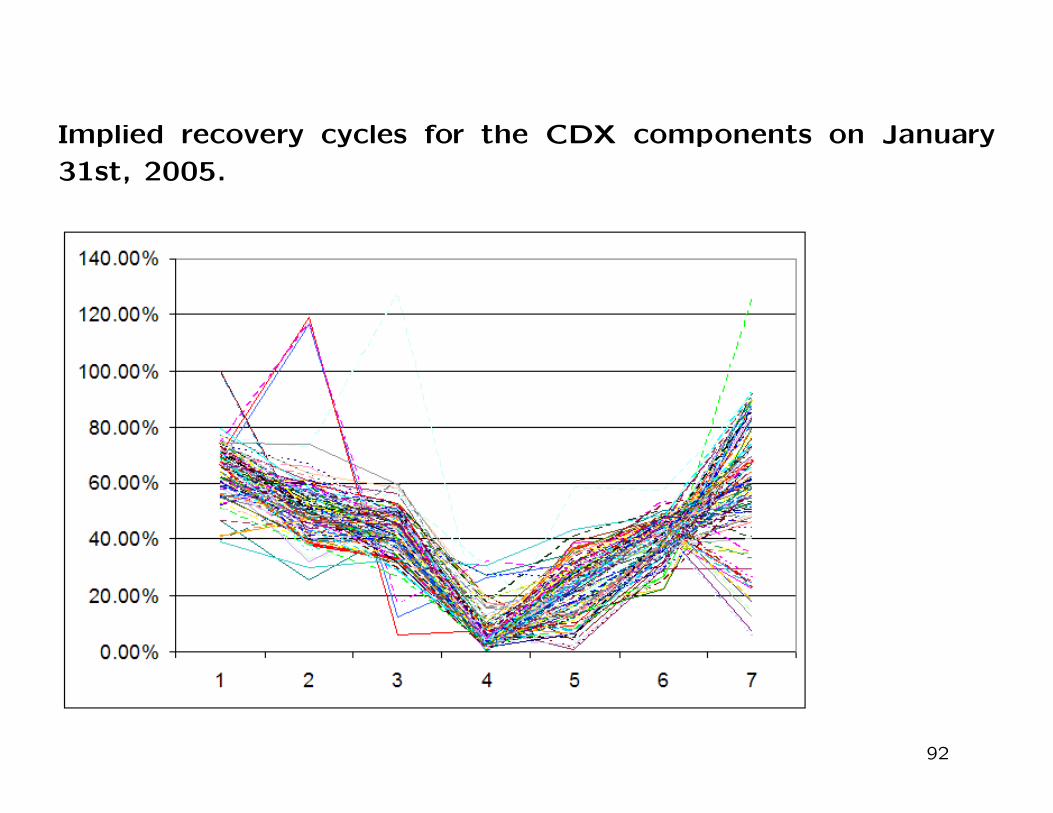

Implied term structure of recovery rates

We observe that the implied term structures of recovery rates are

highly correlated across names and to the general spread level. This is

not surprising as recovery levels are known to be linked to the economic

cycle. Hence implied recoveries reflect the market perception of the

future economic cycle. As we compare the implied recovery cycles

on the last business day of January, March and May 2005, we notice

that the implied recovery cycle appears equally pronounced in the three

months. However, the ones in January and March show a much greater

degree of coherence across names, perhaps a signature of the fact that

in January and March markets were rather tranquil and efficient, while

in May 2005 dislocations occurred.

91

Implied recovery cycles for the CDX components on January

31st, 2005.

92

Implied recovery cycles for the CDX components on March 31st,

2005.

93

Implied recovery cycles for the CDX components on May 31st,

2005.

94

Risk-neutral transition probabilities

In the risk-neutral setting we can also calculate risk-neutral transition

probabilities. These are necessary to price credit-rating dependent

options.

How do we expect risk-neutral transition probabilities to behave? In-

dependent of the model, since risk-neutral default probabilities are

greater than historical default probabilities, one would expect down-

grades in credit-rating to be more probable in the risk-neutral setting

than historically.

95

96

97

98

PART IV. Equity default swaps (EDS)

Equity default swaps are a new class of instruments that several dealers

started marketing this year. They are defined as out of the money

American digital puts struck at 30% of the spot price. Typical maturity

is 5 years and the premium is paid in installments by means of a semi-

annual coupon stream.

In this example, I will compare CEV prices with the prices one obtains

from credit barrier models. The latter, are models estimated to ag-

gregate data, namely the credit transition matrix, default probabilities

and credit spread curves. The credit equity mapping is obtained by

fitting at-the-money implied volatilities as a function of the ratings.

99

Main Finding

It appears that the market is currently pricing EDSs by means of

diffusion local volatility models and that this is not entirely consistent

with credit derivative data. The marked differences in prices are due

to the fact that the credit barrier model accounts for the phenomenon

of ”fallen angels” by introducing and calibrating a jump component in

the process.

100

Credit-Equity mapping

101

Mapping to equity

The credit quality is mapped to equity prices via a deterministic, mono-

tonic function Φ at some horizon date T :

ST (ζ) = erTΦ(ζ)

For ti < T , we take the discounted expectation of Φ:

Sti(ζ) = ertiE[Φ(ζ)|ζti]

102

A snapshot of market EDS spreads

103

Credit quality versus stock price (the credit equity mapping)

104

Local volatility

105

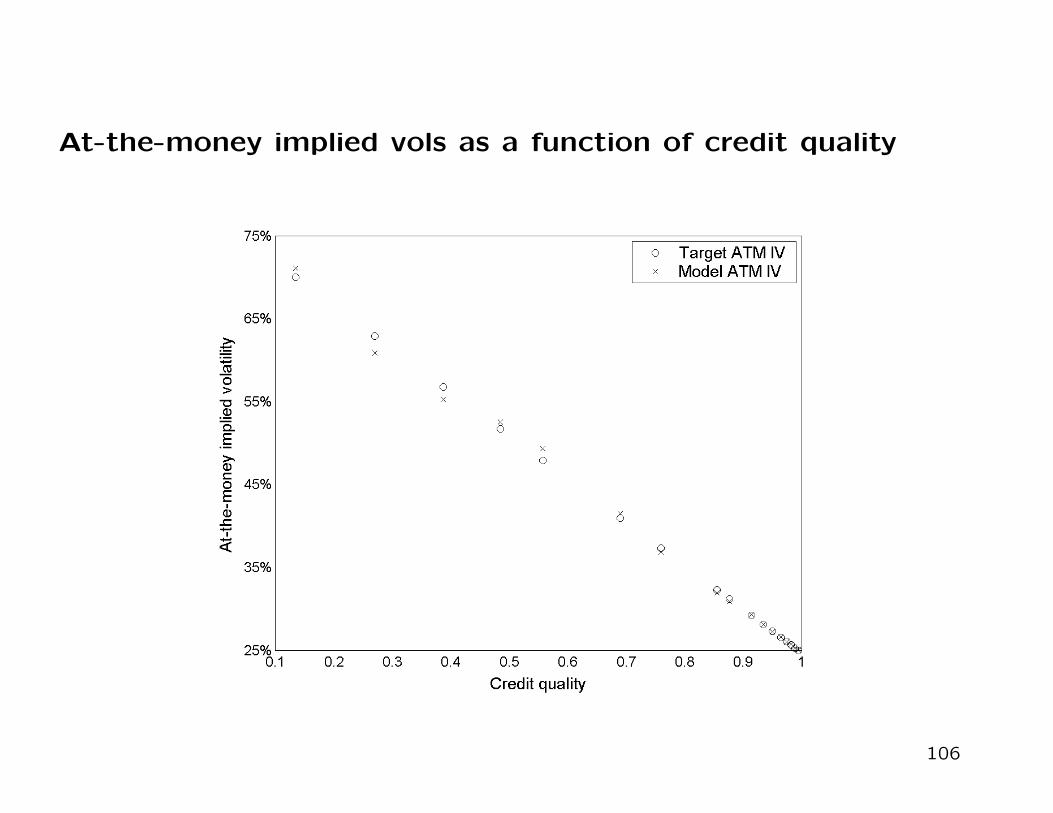

At-the-money implied vols as a function of credit quality

106

EDS spreads as a function of rating

107

CDS to EDS spread ratio as a function of rating

108

CDS to EDS spread ratio based on the CEV model

109

PART V. Credit correlation modeling and lattice models for

synthetic CDOs.

Having characterized the process for credit quality xt and identified

starting points for each individual procsess, the next step is to in-

troduce correlations by conditioning to economic cycle scenarios, thus

introducing a correlation structure among the credit quality processes.

The economic cycle is modeled by means of a non-recombining lat-

tice of the structure sketched below. The underlying index variable is

allowed to take up two values on each period ∆t. An upturn corre-

sponds to a ”good” period while a downturn to a ”bad” period for

the economy. In our example, we chose the time step to be ∆t = 1y

and find that this choice is sufficient to provide great flexibility in the

tuning of the correlation structure.

110

Conditioning the Lattice to a Market Index

To explain our methodology to introduce correlations, we consider

first a simple case whereby the model is characterized by a pair of

complementary transition probabilities w, (1−w) ∈ [0,1] at each node,

which we assume constant. In order to condition the continuous time

lattice corresponding to a given credit quality process to the economic

index variable we introduce the notion of local beta given by function

β(ξ) which provides the corresponding sensitivity. The limiting cases of

β(ξ) = 0 and β(ξ) = 1 correspond to zero and full correlation between

a name with a given credit quality hx ∈ [0,1] and the cycle variable.

Along the path of each given scenario on the tree, the unconditional

kernel of the credit quality process is replaced by conditional transition

probabilities defined as follows:

u±w,β(t, x; t + ∆t, y) = (1− β(hx))u0(t, x; t + ∆t, y) + β(hx)u±1 (t, x; t + ∆t, y)

111

Here u0 = u is the unconditional kernel and corresponds to a zero

β(hx). In the opposite case of β(hx) = 1, conditional kernel u±1 (x, y)

has the following form:

u+1 (x, y) =

1

1− w

u(x, y) if y > m(w, x)(w −

∑y>m(w,x) u(x, a(w, x))

)if y = m(w, x)

u(x, y) = 0 if y < m(w, x)

(32)

and

u−1 (x, y) =1

w

0 if y > m(w, x)

u(x, m(w, x))− u+1 (x, m(w, x)) if y = m(w, x)

u(x, y) if y < a(w, x).

(33)

where

m(w, x) = inf

m = 0, ...N |

∑y<m

u(x, y) ≤ w

. (34)

Notice that, for all specifications of β(ξ) and w ∈ [0,1], we have that

u(x, y) = wu−β (x, y) + (1− w)u+β (x, y). (35)

Conditioning is achieved by forming a weighted sum over all paths in

the event tree. On a given path, we use u−β for a bad period scenario

and u+β for a good one. The weight of a path is the product of

a number of factors w equal to the number of bad periods and a

number of factors (1−w) for each one of the good periods. With this

method, marginal probabilities are kept unchanged while correlations

are induced on the single name processes. More specifically, one can

price all credit sensitive instruments specified with the given names one

can first evaluate the conditional prices PΓ by means of the following

multiperiod kernel:

e(ti−ti−1)Lγi · . . . · e(tn−tn−1)Lγi.

where Γ = γ1, . . . , γn runs over the sets of conditional paths due to

the scenario of the index. The (unconditional) price is then given by:

P =∑Γ

wn−(Γ)(1− w)n+(Γ)PΓ.

This construction can be generalized. Consider a number M > 1 of

percentile levels 0 < w1 < ... < wM < 1 and let qi ∈ [0,1], i = 1...M be

a corresponding set of probabilities summing up to one, i.e.∑

i qi = 1.

Then we can set

u±−→w ,β(t, x; t + ∆t, y) =

M∑i=1

qiu±wi,β

(t, x; t + ∆t, y). (36)

The formulas above extend also to this case as long as one replaces

the weight w with the average weight∑

i qiwi.

The choices we make for the March and June datasets are graphed

below. Here one can observe that the levels we were led to choose in

June are lower and the probabilities more uneven than in March. This

can be interpreted as saying that the model is detecting a higher level

of implied correlation between jumps in the June data than in March.

Specifications for the weights qi and percentile levels wi.

112

The local beta function

Modeling correlation is key to pricing basket credit derivatives. Buyers

and sellers of basket credit derivatives have a wide range of arbitrage-

free prices to choose from, and it is the market that determines, both in

principle and in practice, a definite price. In our framework, tranches

of varying seniority are priced by calibrating the local beta function

β(ξ).

113

Specifications for the function β(x) in March and June 2005.

114

Decoupling of correlation

Notice that as an effect of GM and Ford being downgraded, the local

beta function responded by lowering on the side of low quality grades

while rising on the high qualities. This resulted in a simultaneous fall

of equity prices and widening of senior spreads.

115

Contagion skew

A useful graph to assess the impact of the specification of the local

β(ξ) function on our correlation model is the contagion skew in the

next slide. This graph is constructed as follows: we first compute the

unconditional default probabilities as a function of credit quality. Next,

for each value of credit quality, assuming that a name of that quality

defaults within a time horizon of 5 years, we compute the conditional

probability of defaults for all other name. Finally, we take an average

over all values of credit quality of the ratio between the conditional

and unconditional probabilities. As the graph shows, the higher is the

credit quality of a defaulted name, the larger is the impact on all other

names. The steepness of this curve controls precisely the discrepancy

between prices for senior tranches as compared to junior ones.

116

Contagion Skew: ratio between conditional and unconditional

probability of defaults, where conditioning is with respect to the

default of a name whose credit quality is on the X axis.

117

Pricing CDOs

Although CDX index tranches are written on 125 underlying names, we

observe that our lattice model performs quite efficiently. We separate

the numerical analysis in two different steps. In the first we go through

all names and generate conditional lattices. We choose ∆t = 1y and a

time horizon of 5y, so that we obtain a total of 32 scenarios. This is a

pre-processing step which is independent of the CDO structure. This

step typically takes a few minutes for a hundred names and could

be carried out periodically and offline for the universe of all traded

names. The pricing step instead takes only a few seconds and requires

generating the probability distribution function for CDO portfolios over

the given time horizon.

118

Expected Loss Distribution for CDX index tranches in March

2005

119

Expected Loss Distribution for CDX index tranches in June 2005

120

Pricing CDOs

The model can be calibrated by adjusting the function β(ξ), ξ ∈ [0,1],

the thresholds wi, i = 1, ...M and the corresponding probabilities qi.

121

Tranche prices for March 20th 2005

attachment detachment spread mktspread0% 3% 499.6 bp (+32% uff) 500 bp(+32% uff)3% 6% 187.4 bp 189bp6% 9% 108.6 bp 64bp9% 12% 56.5 bp 22bp12% 22% 6.7 bp 8bp

where ”uff” stands for ”upfront fee”.

122

Calibration

Notice that a good agreement can be reached with the equity, junior

mezzanine and senior tranche. On the other hand, the model appears

to over-estimate the price of the two senior mezzanine tranches 6-9

and 9-12 by a factor 2-3. This might be in relation to the high degree

of liquidity of these tranches and appetite for this risk profile.

123

Tranche prices for June 20th 2005

attachment detachment spread mktspread0% 3% 499.7 bp (+49% uff) 500 bp(+49% uff)3% 6% 170.1 bp 177bp6% 9% 30.4 bp 54bp9% 12% 27.5 bp 24bp12% 22% 10.0 bp 12bp

124

Hedge ratios of the various CDO tranches for March 2005 plot-ted against 5Y CDS spreads.

125

Hedge ratios.

One can notice that the hedge curves for the equity and the junior

mezzanine are fairly different and as a consequence it does not appear

as appropriate to use the mezzanine as a proxy to hedge credit expo-

sure at the equity tranche level. The differentiation among the two

profiles is a direct consequence of the steep aspect of the local beta

function.

126

Conclusions

We propose a novel approach to dynamic credit correlation modeling

that is based on continuous time lattice models correlated by con-

ditioning to a non-recombining tree. The model describes not only

default events but also rating transitions and spread dynamics, while

single name marginal processes are preserved.

127

PART VI. Credit-interest rate hybrids

Functional lattices for the dynamic CDO model and for the term struc-

ture model covered above can be combined and correlated while pre-

serving the specification of marginal processes. This opens the possi-

bility of pricing credit - interest rate hybrid instruments.

As an example of these applications, in the following, we consider

cancellable interest rate swaps which are linked to the default of either

one name in the CDX index, or to the first default event of a name

in a given basket, or to the default of the CDX equity tranche. We

also consider interest floors that cancel upon the default of the equity

tranche. In all cases, we evaluate also hedge ratios.

128

Single name, credit linked cancelable swaps

129

First to default cancelable interest rate swap

130

Basis of a CDO subordinated interest rate swap

131

Hedge ratios for a CDO subordinated interest rate swap

132

Price of a CDO subordinated interest rate floor

133

Hedge ratios for a CDO subordinated interest rate floor

134

Conclusions

We find that our model is well suited for interest rate hybrids. It is

numerical efficient and since it does not involve a Montecarlo step,

hedge ratios have no simulation noise.

We find that, within a local beta model for credit correlations, hedge

profiles tend to be relatively higher for the better quality ratings which

are more correlated to the business cycle.

135