Embed Size (px)

Citation preview

Issue 33 / November 2015

STEEL RAW MATERIALS MONTHLY

www.platts.com www.twitter.com/PlattsSteel METALS

CONTENTS

Iron Ore Market Focus 3

Iron Ore Data 5

Metallurgical Coal Market Focus 6

Metallurgical Coal Data 8

Scrap Market Focus 9

News 10

Special Report 15

Turkey ARC Monthly Data 23

Global Trade Highlights 24

Steel Raw Materials Monthly Averages 25

EDITORIAL

BRICs looking less sturdyHaving decided to take a look at the so-called BRIC (Brazil, Russia, India and China) economies from a steel demand perspective in this issue, it was a coincidence that Goldman Sachs, original coiner of the term, announced it had shut its BRIC fund, after it lost close to 90% of its value over the past five years. Brazil and Russia have been hit by falling oil prices (not to mention coal and iron ore and other commodities), while China’s massive economic growth seems to be finally running out of steam. India is expected to be the rising star of the four but its steel and economic growth trajectory are hard to plot with any certainty while it still has many age-old problems to solve. China and Brazil built up steel capacity on the basis that it would easily be absorbed by ongoing urbanization and development. Is India – already the world’s third-largest steel producer – in danger of making the same mistake?

World Steel Association said last month that global steel was in a period of low growth until “other developing regions…produce another major growth cycle.” Mexico, Indonesia, Nigeria and Turkey (the ‘MINTs’) are tipped by many to pick up from the BRICs, but the hyperbole is likely to be turned down on this occasion.

— Paul Bartholomew

KEY PRICE ASSESSMENT MONTHLY AVERAGES, OCTOBER 2015 Unit Average change % change

Platts IODEX Iron ore fines 62% Fe CFR North China $/dmt 53.25 -3.88 -6.79Platts Coking Coal, Premium low-vol FOB Australia $/mt 78.69 -1.59 -1.98Platts Ferrous Scrap HMS CFR Turkey $/mt 178.93 -24.73 -12.14

TSI Iron Ore Fines 62% Fe $/dmt 52.74 -3.61 -6.41Chinese imports (CFR North China port)TSI Coking Coal, Premium hard, $/mt 79.51 -2.51 -3.06Australian exports (FOB port)TSI Ferrous Scrap HMS 1&2 80:20, $/mt 178.55 -27.63 -13.40Turkish imports (CFR port)

Falling iron ore prices over October and into early November have eaten into the already thin margins of smaller Australian iron ore producers and it is mainly the weak Australian dollar that is providing any breathing space. Much of the cost saving gains made over the past 18 months have been eroded by the descent below $50/dry mt CFR for 62% Fe fines.

The Australian dollar averaged US$0.72 cents in the September quarter and is tipped by analysts and economists to trade at US$0.70-0.72 cents in the December quarter. With 62% Fe iron ore prices averaging $55/dmt in the September quarter, a near 30% foreign exchange margin was a lifesaver for smaller producers. For a long period until 2013, the Australian dollar had been at or even above parity with the US dollar, as a result of the strong prices of iron ore and other commodities, and the weaker US dollar due to the Federal Reserve’s QE program.

Cost saving gains eroded by falling ore priceNational Australia Bank has forecast the

Australian dollar will finish up around US$0.68 cents by the end of next year, which is roughly the consensus view, but UBS Wealth Management believes it could be lower at around US$0.65 cents. These views are premised on the Fed gradually lifting interest rates, along with no further rate cuts by the Reserve Bank of Australia. The RBA kept record low interest rates unchanged on November 3.

Fortescue Metals Group is working off expectations of an Australian dollar of US$0.72 cents in fiscal 2016 (ending June 30), according to its most recent operations report, which along with improved operating costs will give it an average C1 cost of $15-16/wet mt by mid-next year. If this can be achieved the Perth-based miner expects its cash breakeven price on a Platts 62% Fe basis to be around $36/dmt CFR by the end of FY2016, down from around $40/dmt CFR currently.

(continued on page 2)

FORTESCUE C1 COSTS VERSUS REALIZED PRICES

Source: FMG, Platts

0

20

40

60

80

100

120

Jul-Sep 2015Apr-Jun 2015Jan-Mar 2015Oct-Dec 2014July-Sep 2014Apr-Jun 2014Jan-Mar 2014

Realized price ($/dmt CFR)C1 cost ($/wmt)

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 2

Managing EditorPaul Bartholomew; Australia(+613-9631-2096)

Senior Managing EditorRuss McCulloch; Singapore(+65-6227-7811)

Editorial DirectorJoe Innace(+1-212-904-3484)

Global Content Director, Metals & TSISteven Randall

General Manager, MetalsAndrew Goodwin

Issue 33 / November 2015

Chief Content OfficerMartin Fraenkel

Platts PresidentImogen Dillon Hatcher

AdvertisingTel : +1-720-264-6631

Manager, Advertisement SalesKacey Comstock

STEEL RAW MATERIALS MONTHLY

2052-3572ISSN:

To reach Platts: E-mail:[email protected]; North America: Tel: 800-PLATTS-8; Latin America: Tel:+54-11-4121-4810; Europe & Middle East: Tel:+44-20-7176-6111; Asia Pacific: Tel:+65-6530-6430

ANY OTHER INVESTMENT DECISIONS. NEITHER PLATTS, NOR ITS AFFILIATES OR THEIR THIRD-PARTY LICENSORS GUARANTEE THE ADEQUACY, ACCURACY, TIMELINESS OR COMPLETENESS OF THE DATA OR ANY COMPONENT THEREOF OR ANY COMMUNICATIONS, INCLUDING BUT NOT LIMITED TO ORAL OR WRITTEN COMMUNICATIONS (WHETHER IN ELECTRONIC OR OTHER FORMAT), WITH RESPECT THERETO.

ACCORDINGLY, ANY USER OF THE DATA SHOULD NOT RELY ON ANY RATING OR OTHER OPINION CONTAINED THEREIN IN MAKING ANY INVESTMENT OR OTHER DECISION. PLATTS, ITS AFFILIATES AND THEIR THIRD-PARTY LICENSORS SHALL NOT BE SUBJECT TO ANY DAMAGES OR LIABILITY FOR ANY ERRORS, OMISSIONS OR DELAYS IN THE DATA. THE DATA AND ALL COMPONENTS THEREOF ARE PROVIDED ON AN “AS IS” BASIS AND YOUR USE OF THE DATA IS AT YOUR OWN RISK.

Limitation of Liability: IN NO EVENT WHATSOEVER SHALL PLATTS, ITS AFFILIATES OR THEIR THIRD-PARTY LICENSORS BE LIABLE FOR ANY INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE OR CONSEQUENTIAL DAMAGES, INCLUDING BUT NOT LIMITED TO LOSS OF PROFITS, TRADING LOSSES, OR LOST TIME OR GOODWILL, EVEN IF THEY HAVE BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES, WHETHER IN CONTRACT, TORT, STRICT LIABILITY OR OTHERWISE.

Permission is granted for those registered with the Copyright Clearance Center (CCC) to photocopy material herein for internal reference or personal use only, provided that appropriate payment is made to the CCC, 222 Rosewood Drive, Danvers, MA 01923, phone (978) 750-8400. Reproduction in any other form, or for any other purpose, is forbidden without express permission of McGraw Hill Financial. For article reprints contact: The YGS Group, phone +1-717-505-9701 x105. Text-only archives available on Dialog File 624, Data Star, Factiva, LexisNexis, and Westlaw.

Platts is a trademark of McGraw Hill Financial

Officers of the Corporation: Harold McGraw III, Chairman; Doug Peterson, President and Chief Executive Officer; David Goldenberg, Acting General Counsel; Jack F. Callahan Jr., Executive Vice President and Chief Financial Officer; Elizabeth O’Melia, Senior Vice President, Treasury Operations.

Restrictions on Use: You may use the prices, indexes, assessments and other related information (collectively, “Data”) in this publication only for your personal use or, if your company has a license from Platts and you are an “Authorized User,” for your company’s internal business. You may not publish, reproduce, distribute, retransmit, resell, create any derivative work from and/or otherwise provide access to Data or any portion thereof to any person (either within or outside your company including, but not limited to, via or as part of any internal electronic system or Internet site), firm or entity, other than as authorized by a separate license from Platts, including without limitation any subsidiary, parent or other entity that is affiliated with your company, it being understood that any approved use or distribution of the Data beyond the express uses authorized in this paragraph above is subject to the payment of additional fees to Platts.

Disclaimer: DATA IN THIS PUBLICATION IS BASED ON MATERIALS COLLECTED FROM ACTUAL MARKET PARTICIPANTS. PLATTS, ITS AFFILIATES AND ALL OF THEIR THIRD-PARTY LICENSORS DISCLAIM ANY AND ALL WARRANTIES, EXPRESS OR IMPLIED, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE AS TO THE DATA, OR THE RESULTS OBTAINED BY ITS USE OR AS TO THE PERFORMANCE THEREOF. A REFERENCE TO A PARTICULAR INVESTMENT, SECURITY, RATING OR ANY OBSERVATION CONCERNING A SECURITY OR INVESTMENT PROVIDED IN THE DATA IS NOT A RECOMMENDATION TO BUY, SELL OR HOLD SUCH INVESTMENT OR SECURITY OR MAKE

Steel Raw Materials Monthly is published monthly by Platts, a division of McGraw Hill Financial, registered office: 20 Canada Square, Canary Wharf, London, UK, E14 5LH.

Copyright © 2015 by Platts, McGraw Hill Financial

Fortescue reached its long-held 155 million mt/year capacity target on an annualized basis in the March 2014 quarter. In that quarter, the Platts 62% Fe index averaged $120/dmt, while Fortescue’s C1 costs were $34.88/wmt, and its realized sales price $107/dmt on a Platts 62% Fe basis. C1 costs accounted for 33% of the

Cost saving gains eroded by falling ore price...from page 1

realized sales price. In the September 2015 quarter (production capacity is now roughly 10 million mt/year higher), its C1 costs were $16.90/wmt, some 34% of the average sales price of $50/dmt in the quarter. So while the company’s C1 costs have roughly halved over the past 18 months, the proportion versus the realized sales price has not

shifted as much because iron ore prices have fallen so hard.

Freight costs have helped margins, averaging $5.6/mt in the September 2015 quarter compared with $8.8/mt in the March 2014 quarter, while oil and diesel prices have fallen significantly, along with the Australian dollar. Fortescue has also benefited from good demand for its 58% Fe material at a time when Chinese mills are keeping output low due to poor market conditions. This has served to narrow the spread with 62% Fe prices.

Following a recent analyst tour of Fortescue’s Pilbara operations, UBS said the company could reduce its all-in cash costs to $15/mt, its cash breakeven price “on a Platts 62% Fe equivalent basis would be $36/dmt CFR.”

Tougher for juniorsWhile Fortescue has the scale and ability to lower costs even further, some of its smaller rivals are more constrained. Fellow Pilbara iron ore miner Atlas Iron has tirelessly taken cost out of the business but almost foundered back in April when the 62% Fe iron ore price went below $50/mt CFR.

“We reduced our costs to $61/mt at Easter (April 3-6) from $85/mt,” David

ATLAS C1 COSTS VERSUS REALIZED PRICES

Source: AtlasNB: Average used of C1 range and Standard and Value Fines prices in Jan-June 2014

0

20

40

60

80

100

Jul-Sep 2015Apr-Jun 2015Jan-Mar 2015Oct-Dec 2014July-Sep 2014Apr-Jun 2014Jan-Mar 2014

Realized price (A$/dmt CFR)C1 cost (A$/wmt)

FORTESCUE’S OUTPUT, COSTS AND REALIZED PRICE Output C1 cost Realized price Platts 62% Fe average (million mt) ($/wmt) ($/dmt CFR) ($/dmt CFR)Jan-Mar 2014 29.60 34.88 107 120Apr-Jun 2014 43.80 34.03 82 103July-Sep 2014 42.90 32.08 71 90Oct-Dec 2014 43.60 28.48 63 74Jan-Mar 2015 35.50 25.90 48 55Apr-Jun 2015 42.10 22.16 52 60Jul-Sep 2015 45.10 16.90 50 55

Source: FMG, Platts (continued on page 14)

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 3

PLATTS MONTHLY AVERAGE IRON ORE PRICES, OCTOBER 2015 ($/dmt) Monthly average $ change % changeIODEX: Iron ore fines 62% Fe CFR North China 53.25 -3.88 -6.7963.5/63% Fe CFR North China 54.50 -4.23 -7.2165% Fe CFR North China 57.51 -5.02 -8.0358% Fe low Al CFR North China 48.53 -3.69 -7.0758% Fe CFR North China 45.78 -3.69 -7.4652% Fe CFR North China 36.06 -3.67 -9.23Per 1% Fe differential (Range 60-63.5% Fe) 0.98 0.00 0.41

TSI MONTHLY AVERAGE IRON ORE PRICES, OCTOBER 2015 ($/dmt) Monthly average $ change % change62% Fe fines, 3.5% Al, CFR Tianjin port 52.74 -3.61 -6.4058% Fe fines, 1.5% Al, CFR Qingdao port 48.89 -3.62 -6.9058% Fe fines, 3.5% Al, CFR Tianjin port 49.09 -3.62 -6.8762% Fe fines, 2% Al, CFR Qingdao port 53.94 -3.61 -6.2763.5/63% Fe fines, 3.5% Al, CFR Qingdao port 53.74 -3.61 -6.2965% Fe fines, 1% Al, CFR Qingdao port 58.34 -3.94 -6.32

China’s iron ore imports of 699.45 million mt over January-September were almost identical to the year-ago period, China Customs data shows. July-September quarter imports of 246.3 million mt were a record, however, beating the previous record of 242.1 million mt in the same quarter of 2014.

The September quarter is typically a strong one for Australian iron ore production and exports, joined this year by record output from Vale. Unfortunately, all of this supply has hit at a time of weak demand in China, due to low crude steel production and ever decreasing steel prices. Pig iron production over January-September of 528.3 million mt was down 3.3% on the same period a year earlier, while crude steel output of 609 million mt was 2.1% lower.

Port stocks have subsequently climbed again, putting more downwards pressure on iron ore prices, which appear to have settled below the $50/mt CFR level for the time being. Mysteel data shows port stocks at major Chinese ports had reached 82.68 million mt by the end of the first week in November, up almost 3 million mt from just a week earlier.

Iron ore spot trades were well down in the month of October (48 compared with 73 in September as observed by Platts), with fewer cargoes from BHP Billiton, and Vale selling mainly on a floating price basis.

Platts 62% Fe iron ore fines averaged $53.25/mt CFR in October, down $6.79/dry mt from the month before. The Steel Index’s price for the same material averaged $52.74/mt CFR in October, $6.41/mt lower than the September monthly average.

Chinese output drops offCapacity utilization at larger Chinese iron ore producers (those with capacity of more than 1 million mt/year) fell to just 51.6% by the

Prices under pressure as pre-winter restock proves elusive

IRON ORE MARKET FOCUS

first week of November from around 64% a fortnight earlier. Again it indicates that a seaborne spot price of $50/mt CFR is the pain point for many domestic producers. It was a similar situation in April this year – the previous time spot prices went below $50/mt – when a large chunk of domestic supply was switched off in favor of imports. But as soon as prices climb up above $50/mt, much of this local production is turned back

on again, showing the elasticity and market responsiveness of Chinese producers.

With little pre-winter restocking taking place, plentiful supply, and no sign of a turnaround in steel prices, iron ore prices could remain at a similar level for the rest of 2015. This is likely to result in domestic Chinese capacity utilization of less than 50% for the rest of the year and into 2016, a period when local production is typically lower in any case due to the colder winter months.

As for so-called ‘non-traditional’ iron

SGX - IRON ORE FORWARDS - 62% Fe ($/dmt CFR)

Source: SGX, TSI

38

43

48

53

Nov-18May-18Nov-17May-17Nov-16May-16Nov-15

01-Oct 30-Oct

PLATTS 62% & 58% Fe IRON ORE MONTHLY AVERAGES CFR CHINA ($/dmt)

Source: Platts

40

50

60

70

80

Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15Feb-15Jan-15Dec-14Nov-14

62% Fe 58% Fe

PLATTS OBSERVED IRON ORE SPOT TRADES BY VOLUME - JAN-OCT (number of trades)Rio 192BHP 104Vale 74Other 245Total 615

Source: Platts

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 4

IRON ORE MARKET FOCUS

IRON ORE PORT STOCKS IN CHINA (million mt)

Source: Mysteel

0

20

40

60

80

100

120

Oct-15Aug-15Jun-15Apr-15Feb-15Dec-14Oct-14

Australia BrazilTotal

PORT HEDLAND IRON ORE EXPORTS (million mt)

Source: Pilbara Ports Authority

0

10

20

30

40

15-OctAug-15Jun-15Apr-15Feb-15Dec-14Oct-14

China Rest of the world

ore supply, it is disappearing quickly, unable to compete with lower-cost, higher-quality material from Australia and Brazil. Producing nations outside of Australia, Brazil, South Africa and Ukraine now supply less than 10% of China’s iron ore needs. Australia and Brazil now account for 85% of Chinese iron ore imports, compared with around 75% in January-September last year. If the big four iron ore producing companies, Vale, Rio Tinto, BHP and Fortescue Metals Group, produce at a similar level in the final quarter of this year to the September quarter, they will have added an extra 75 million-80 million mt this year compared with CY2014. Softer October exports from Western Australia’s Port Hedland of 36.5 million mt, down from 39.4 million mt in September, suggest the final quarter could be a bit softer out of Australia.

More tons in 2016Next year could see a similar amount of new tons, though exports from the new Roy Hill project in Western Australia could be delayed until early 2016 and the company may not export the 20 million mt or so of iron ore that many analysts have built into their supply-demand models. Vale has also said it may trim output expectations slightly in response to the Samarco disaster. The new S11D project is around 75% complete and will likely start making a supply contribution towards the end of 2016. So next year could potentially be a bit slower in terms of additional supply than was thought a few months ago. Given market conditions and prices, the major producers may not be in a hurry to bring on new tons too quickly.

With Chinese demand for iron ore slowing, any additional supply will put the market under even more pressure and the major producers will need to take market share from each other as the size of the pie will likely get

slightly smaller rather than bigger.BHP’s July-September quarter iron ore

output of 67 million mt (on a 100% basis) was up 7% on last year and by 3% on the previous quarter. The ramp-up of its Jimblebar mine

and improved ore handling plant utilization at Newman helped support the stronger output. The Melbourne-headquartered company plans to produce 247 million mt in the twelve months to June 2016.

CHINESE MONTHLY IRON ORE IMPORTS (million mt)

Source: Platts

0

20

40

60

80

100

Sep-15Jul-15May-15Mar-15Jan-15Nov-14Sep-14

IRON ORE TRADING BY MAJORS (number of trades)

Source: Platts

0

20

40

60

80

100

Oct-15Aug-15Jun-15Apr-15Feb-15Dec-14Oct-14

BHP Billiton OtherRio TintoVale

CHINA’S IRON ORE IMPORT SOURCES JANUARY-SEPTEMBER 2013-2015 2013 2014 2015Australia 304.2 405.8 449.8Brazil 111 125.2 134.2South Africa 32.3 33.3 34.7Ukraine 12.4 13 16.3Other 141.3 122.2 64.4Total 601.2 699.5 699.4

Source: China Customs, GTIS

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 5

ATLANTIC BASIN IRON ORE PELLETS ($/mt)

Source: Platts

100

110

120

130

140

150

160

Nov-15Sep-15Jul-15May-15Mar-15Jan-15Nov-14

BIG 4 - QUARTERLY IRON ORE PRODUCTION (million wmt)

Source: Company reports

0

15

30

45

60

75

90

Q3 15Q1 15Q3 14Q1 14Q3 13Q1 13

*BHP and Rio 100% basis

Vale Rio Tinto* BHP* Fortescue

IRON ORE FREIGHT RATES - KEY ROUTES ($/wmt)

Source: Platts

0

5

10

15

20

25

Oct-15Aug-15Jun-15Apr-15Feb-15Dec-14Oct-14

Brazil West Australia

CHINA IRON ORE SPOT LUMP PREMIUM ($/dmtu)

Source: Platts

0.05

0.10

0.15

0.20

0.25

0.30

0.35

Jan-15Jan-15Jan-15Jan-15Jan-15Dec-14Oct-14

CHINESE CONCENTRATE 66% Fe ($/mt)

Source: Platts

80

90

100

110

120

130

Nov-15Sep-15Jul-15May-15Mar-15Jan-15Nov-14

CHINA IRON ORE CAPACITY UTILIZATION

Source: MySteel, Platts

(%) ($/mt)

0

20

40

60

80

100

Nov-15Sep-15Jul-15May-15Mar-15Jan-15Nov-1440

50

60

70

80

90

*Large: 1 mil mt/year +; Medium: 300k-1 mil mt/year; Small: sub 300k mt/year

Large Medium Small 62% iron ore prices (right)

FALLING IRON ORE AND SCRAP PRICES ($/mt)

Source: Platts

150

200

250

300

350

400

Oct-15Aug-15Jun-15Apr-15Feb-15Dec-14Oct-1440

50

60

70

80

90Iron ore IODEX (right)Scrap (left)

IRON ORE DATA

CONTRIBUTION TO CHINA’S IMPORTS (%)

Source: China Customs, GTIS

0

20

40

60

80

100

201520142013

Australia and Brazil Other

Rio had built up significant stockpiles at its Pilbara operations as its mines moved closer to 350 million mt/year production capacity and was able to push through a record 91.3 million mt in the September quarter, which was higher than Vale’s though

its output was still down on its Brazilian rival. Rio produced 86.1 million mt in the September quarter on a 100% basis, while Vale produced 88.2 million mt for the period.

Fortescue has kept output steady for around a year at an annualized 165 million mt/

year, indicating it has no wish to bring on extra supply at a time of weak iron ore prices. The Perth-based miner produced 45.1 million mt of iron ore in the September quarter, compared with 42.1 million mt in the previous quarter.

— Paul Bartholomew

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 6

PLATTS MONTHLY METALLURGICAL COAL ASSESSMENTS, OCTOBER 2015

Asia-Pacific coking coal ($/mt)

FOB CFR CFR Change Australia China India Australia China IndiaPremium Low Vol 78.69 85.91 87.92 -1.59 -1.87 -2.12HCC Peak Downs Region 79.69 86.91 88.92 -1.59 -1.87 -2.12HCC 64 Mid Vol 74.77 81.99 84.00 +0.99 +0.71 +0.46Low Vol PCI 65.03 72.25 74.26 +0.66 +0.39 +0.14Low Vol 12 Ash PCI 63.25 70.47 72.48 +0.04 -0.23 -0.48Semi Soft 61.35 68.57 70.58 -0.46 -0.73 -0.98Met Coke - - 136.91 - - -5.22

North China prompt port stock prices

Ex-stock Jingtang CFR Jingtang (Yuan/mt, incl VAT) equivalent ($/mt)*Premium Low Vol 685.00 84.75HCC 64 Mid Vol 673.00 83.19

*ex-stock price, net of VAT and port charges.

Atlantic coking coal ($/mt)

FOB US East Coast Change VM Ash SLow Vol HCC 81.920 -4.739 19% 8% 0.80%High Vol A 83.068 -4.421 32% 7% 0.85%High Vol B 77.955 -5.715 34% 8% 0.95%

Detailed methodology and specifications are found here:

http://platts.com/IM.Platts.Content/MethodologyReferences/MethodologySpecs/metcoalmethod.pdf

TSI MONTHLY AVERAGE METALLURGICAL COAL PRICES, OCTOBER 2015 ($/mt) Monthly $ % average change changePremium hard coking coal, FOB Australia 79.51 -2.51 -3.06Hard coking coal, FOB Australia 73.96 0.31 0.42Premium JM25 coking coal, CFR China 85.93 -1.61 -1.84Hard JM25 coking coal, CFR China 81.61 1.38 1.72

METALLURGICAL COAL MARKET FOCUS

India’s consumption of metallurgical coal and coke will continue to be subdued this year, with steel demand muzzled by poor performance of the country’s infrastructure and construction sectors, according to market sources. With a looming economic slowdown in China and languishing steel prices, observers say that a demand spurt in Asia’s third largest buyer of metallurgical coal is unlikely to materialize before 2016.

Crude steel production in India witnessed a robust first quarter, jumping 8.3% year-on-year, but a modest 0.8% increase to 45.07 million mt in the April-September period put a cap on the total gain this year. As a result, coal and coke import growth have stalled in recent months.

Despite surging 34.8% y-o-y in the first five months of 2015, Indian met coal imports have slipped for three consecutive months, falling 17.1% to 10.5 million mt in the June-August period, according to data compiled by Indian ship broker Interocean.

Semi-soft coking coal (SSCC) and pulverised coal injection (PCI) coal, both used in steelmaking, will continue to see imports rise sharply thanks to steelmakers’ ongoing focus on hot metal cost reduction, sources said. India’s met coke imports have also declined by more than a third, falling from 1.7 million mt in the January-July period from 2.7 million mt a year ago.

“India has largely undershot expectations of a strong 2015 because steel output has been hamstrung by an overall lack of domestic demand,” a marketing manager from an Australian mining firm said. “Our volumes to India have been static this year.”

Finished steel consumption during the April-September half rose only 4% y-o-y to 39.15 million mt, according to Joint Plant Committee estimates. This is much lower than earlier estimates of 6-7% forecast by analysts. Industry participants surveyed by Platts estimate that steel demand may not rise beyond 4-5% this fiscal to 80 million mt.

Prior expectations that significant growth in Indian met coal would offset China’s retreat from the seaborne market

Indian demand for met coal disappoints

have been overblown, according to one international trader. While overall Indian imports advanced 11%, Chinese coking coal import volumes (excluding PCI) plunged 19% within the same period to 32.4 million mt. This meant that international trading firms have shifted the focus to sell more spot cargoes to Europe and South America, rather than to India, the trading source said.

Several Indian buyers told Platts that they have hardly increased their overall procurement of met coal and coke due to chronic uncertainty of steel price directions. “We are already in the red, but we are not cutting production because we don’t want to incur the fixed costs of idling a furnace or underutilizing facilities,” a west Indian end-user said. “If raw materials prices don’t fall, then we might have to shut down eventually.”

AUSTRALIA AND US LOW VOL HCC MONTHLY AVERAGES ($/mt)

Source: Platts

70

80

90

100

110

120

Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15Feb-15Jan-15Dec-14Nov-14

HCC FOB AustraliaHCC FOB East Coast US

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 7

METALLURGICAL COAL MARKET FOCUS

October prices dip on soft Chinese demandTSI’s October monthly averages for Chinese imports of JM25 PHCC dropped 1.84% m-o-m to $85.93/mt while second tier JM25 HCC gained 1.72% m-o-m to $81.61/mt. TSI’s JM 25 Mid-vol Hard Coking Coal (PMV) index fell 0.1% in October to $83.17/mt CFR Jingtang port.

Platts premium low-vol HCC prices fell 1.6% from the previous month to average $78.69/mt FOB Australia in October.

Domestic Chinese coal prices were cut by some Yuan 50/mt in October, leaving seaborne cargos in a more precarious situation as local buyers focused on cheaper domestic material.

Coal buyers were lukewarm in October, and therefore sellers have tended to cross the bid/offer spreads in the hope of moving tonnages and cutting further losses. TSI FOB swaps traded 151,000 mt in October, increasing volumes for a third straight month.

— Kenneth Woo, Charlotte Rao

PLATTS MONTHLY METALLURGICAL COAL RELATIVITIES TABLE - OCT 30, 2015 Sep 30 Spread Spread CSR VM TM Ash S P Fluidity Vit % CFR China vs PLV vs HCC 64 ad ar ad ad ad ddpm $/mtPeak Downs 74 20.50 9.50 10.50 0.60 0.03 400 71 84.00 101.20%Saraji 72 18.50 10.00 10.50 0.60 0.03 160 66 83.00 100.00%

Premium Low Vol 71 21.50 9.70 9.30 0.50 0.045 500 65 83.00 100.00%

German Creek 70 19.00 10.50 9.50 0.54 0.06 180 70 82.00 98.80%Illawara 73 23.20 10.00 9.50 0.45 0.06 1200 53 81.50 98.19%Oaky North 69 23.00 10.00 9.50 0.60 0.07 1500 79 81.00 97.59%Oaky Creek 67 24.50 10.00 9.50 0.60 0.07 4000 80 81.00 97.59%Goonyella 68 23.40 10.00 8.90 0.52 0.03 1100 62 81.50 98.19%Goonyella C 70 23.50 10.00 9.90 0.55 0.04 1200 62 80.00 96.39%Peak Downs North 68 22.80 10.50 9.80 0.51 0.05 900 63 79.75 96.08% 100.00%Standard 70 23.50 10.00 9.50 0.45 0.09 100 54 79.75 96.08% 100.00%Premium 70 25.50 10.00 8.80 0.60 0.08 200 59 79.50 95.78% 99.69%Hail Creek 69 20.50 10.00 10.00 0.30 0.07 300 54 79.50 95.78%

HCC 64 Mid Vol 64 25.50 9.50 9.00 0.60 0.05 1700 55 79.75 96.08% 100.00%

Mavis Downs 63 22.00 10.00 8.00 0.35 0.05 75 79.75 100.00%Lake Vermont HCC 62 21.50 11.00 7.50 0.44 0.07 120 50 79.75 100.00%Carborough Downs 58 22.50 11.00 8.00 0.35 0.04 60 44 78.75 98.75%Middlemount Coking 57 19.00 10.00 10.00 0.50 0.04 50 75.75 94.98%Gregory 57 33.00 8.50 7.30 0.65 0.03 7500 76 75.00 94.04%

October 30 freight rates. Australia to China: Panamax = $6.45/mt Capesize = $5.65/mtNotes: ad = air-dried; ar = as received; CSR = coke strength after reaction; ddpm = dial divisions per minutePlatts monthly metallurgical coal assessments and relativities table provides April price assessments for various qualities of coking coal including Platts benchmark grades, premium low-vol and the mid-vol marker HCC 64 Mid Vol. The price information provided is determined mostly from transactional data and spot market assessments, but also where applicable from theoretical calculations using value-in-use (VIU).Platts has developed a normalization tool based on VIU data to track the relative values of several coal qualities. In calculating a theoretical value-in-use, Platts may apply linear penalties and premia within a certain range for coke strength after reaction (CSR), volatile matter, total moisture, ash and sulphur and non-linear adjustments for phosphorus, maximum fluidity and vitrinite percentage. For each of the latter, no adjustments are applied within a "normal range," but penalties or premia for these important price determinants are applied when specifications fall outside of the normal range.However, market observations have a stronger bearing on the relativities than VIU calculations, and theoretical VIU-based relativities are recalibrated by observing spot market data including bids, offers and trades for specific brands, and by observing the tradable or traded spreads between these brands.The final assessed value is a combination of the observed market activity, the editorial evaluation of the coal attributes and the results offered by the calculations. Particular market events and specific circumstances may also have an influence on the market for coking coal or individual grades. Platts observes and monitors all relevant market information for consideration in its assessments.Since the July 2014 analysis, the table represents relativities at the end of the last working day of each month, rather than an average of relativities through the month.Since the January 2014 analysis, the table represents relativities on a CFR China basis, rather than theoretical FOB Queensland basis. This is because discoverable relativities are more consistent CFR China, likely due to the fact that seaborne suppliers compete on a delivered basis. In addition, FOB Australia relativities have been observed to be less consistent, perhaps due to discriminatory pricing depending on the geographic destination.Source: Platts

ACT ON REAL-TIME COAL MARKET INTELLIGENCEGet all your Platts coal coverage delivered in real-time with Platts Global Coal Alert.

This valuable tool will allow you to:

■■ Save Time – Customize and access Platts coal content in one place■■ Act Faster – Access real-time market intelligence much faster than with a publication■■ Stay Current – See heards, news, prices and market commentary as they become available■■ Customize Content – choose the content based on your individual needs, regionally and globally

Contact us to take a free trial

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 8

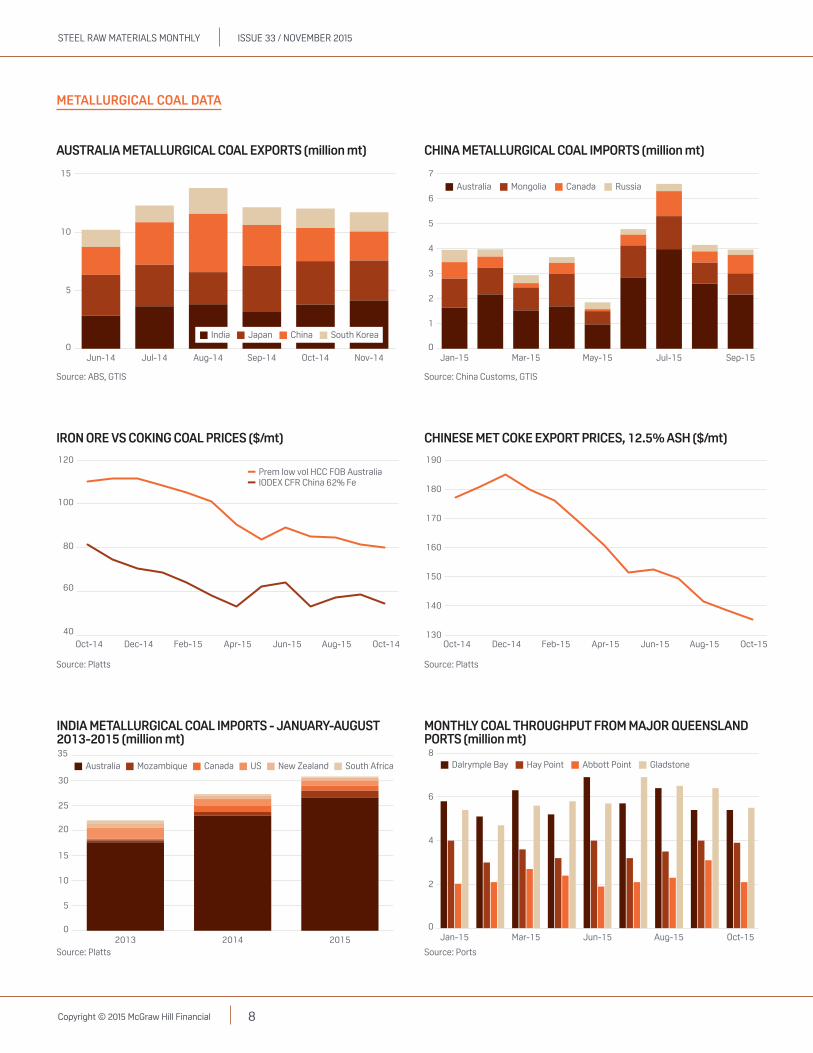

AUSTRALIA METALLURGICAL COAL EXPORTS (million mt)

Source: ABS, GTIS

0

5

10

15

Nov-14Oct-14Sep-14Aug-14Jul-14Jun-14

India Japan China South Korea

CHINA METALLURGICAL COAL IMPORTS (million mt)

Source: China Customs, GTIS

0

1

2

3

4

5

6

7

Sep-15Jul-15May-15Mar-15Jan-15

Australia Mongolia RussiaCanada

IRON ORE VS COKING COAL PRICES ($/mt)

Source: Platts

40

60

80

100

120

Oct-14Aug-15Jun-15Apr-15Feb-15Dec-14Oct-14

Prem low vol HCC FOB AustraliaIODEX CFR China 62% Fe

CHINESE MET COKE EXPORT PRICES, 12.5% ASH ($/mt)

Source: Platts

130

140

150

160

170

180

190

Oct-15Aug-15Jun-15Apr-15Feb-15Dec-14Oct-14

INDIA METALLURGICAL COAL IMPORTS - JANUARY-AUGUST2013-2015 (million mt)

Source: Platts

0

5

10

15

20

25

30

35

201520142013

MozambiqueAustralia USCanada South AfricaNew Zealand

MONTHLY COAL THROUGHPUT FROM MAJOR QUEENSLANDPORTS (million mt)

Source: Ports

0

2

4

6

8

Oct-15Aug-15Jun-15Mar-15Jan-15

Hay PointDalrymple Bay GladstoneAbbott Point

METALLURGICAL COAL DATA

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 9

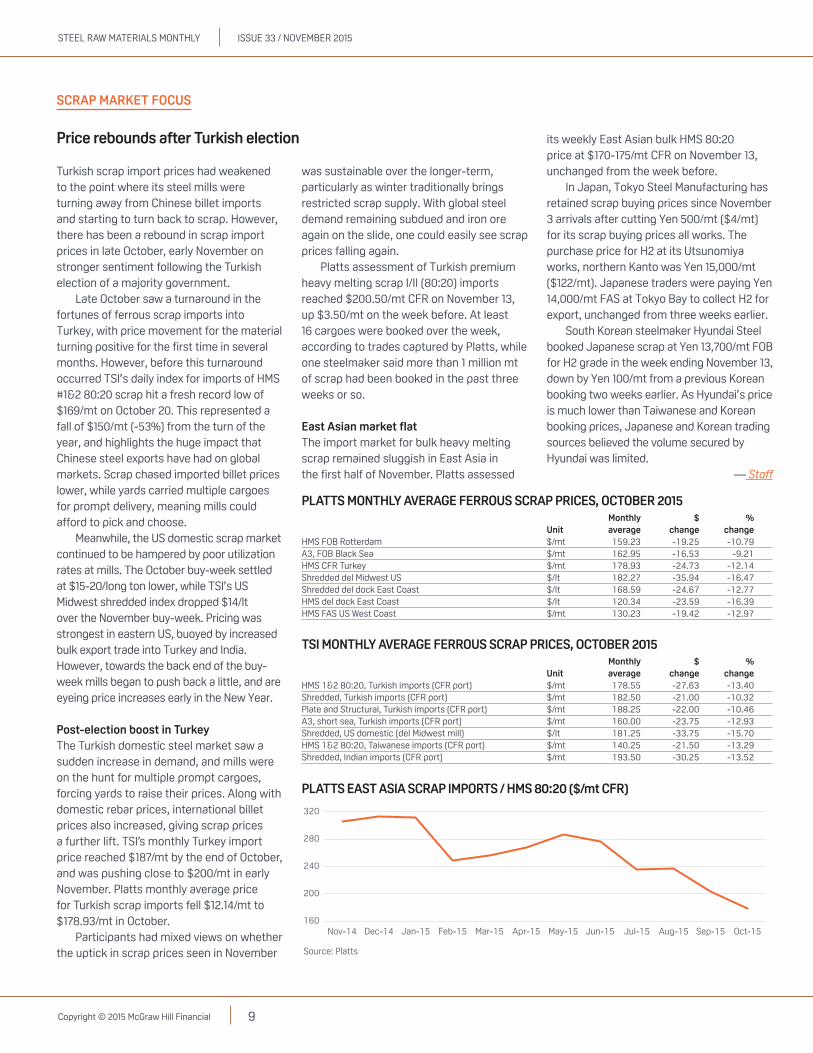

PLATTS MONTHLY AVERAGE FERROUS SCRAP PRICES, OCTOBER 2015 Monthly $ % Unit average change changeHMS FOB Rotterdam $/mt 159.23 -19.25 -10.79A3, FOB Black Sea $/mt 162.95 -16.53 -9.21HMS CFR Turkey $/mt 178.93 -24.73 -12.14Shredded del Midwest US $/lt 182.27 -35.94 -16.47Shredded del dock East Coast $/lt 168.59 -24.67 -12.77HMS del dock East Coast $/lt 120.34 -23.59 -16.39HMS FAS US West Coast $/mt 130.23 -19.42 -12.97

TSI MONTHLY AVERAGE FERROUS SCRAP PRICES, OCTOBER 2015 Monthly $ % Unit average change changeHMS 1&2 80:20, Turkish imports (CFR port) $/mt 178.55 -27.63 -13.40Shredded, Turkish imports (CFR port) $/mt 182.50 -21.00 -10.32Plate and Structural, Turkish imports (CFR port) $/mt 188.25 -22.00 -10.46A3, short sea, Turkish imports (CFR port) $/mt 160.00 -23.75 -12.93Shredded, US domestic (del Midwest mill) $/lt 181.25 -33.75 -15.70HMS 1&2 80:20, Taiwanese imports (CFR port) $/mt 140.25 -21.50 -13.29Shredded, Indian imports (CFR port) $/mt 193.50 -30.25 -13.52

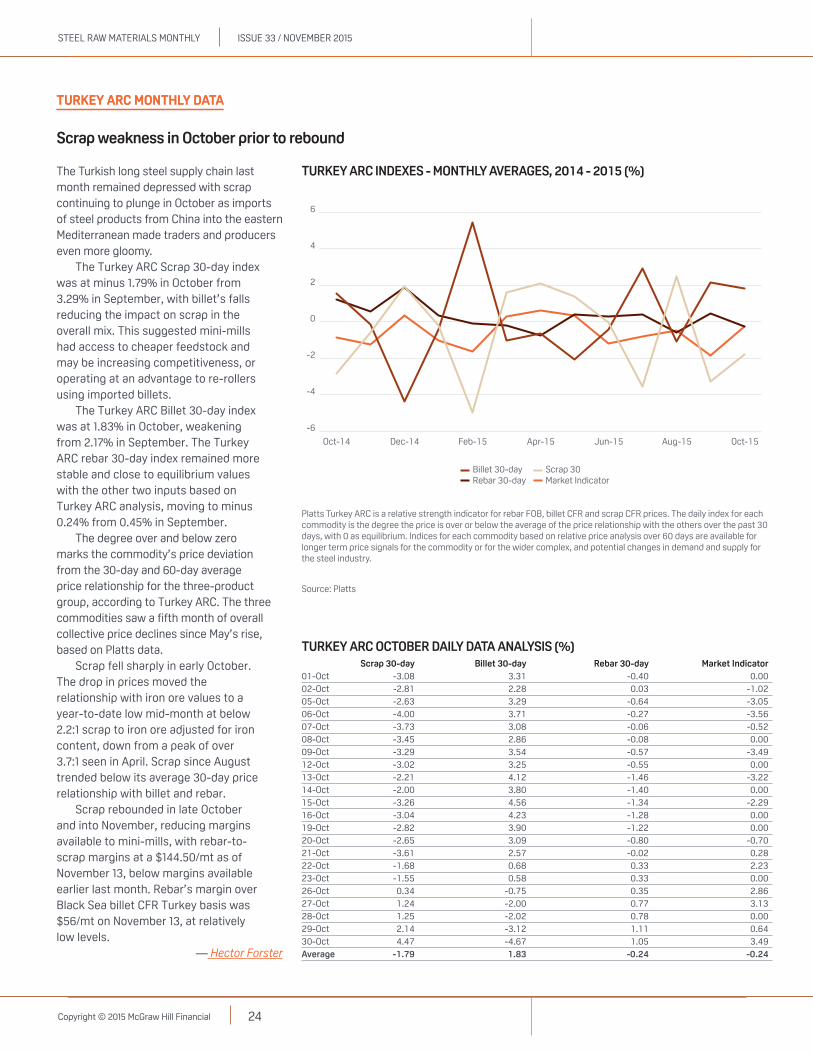

Turkish scrap import prices had weakened to the point where its steel mills were turning away from Chinese billet imports and starting to turn back to scrap. However, there has been a rebound in scrap import prices in late October, early November on stronger sentiment following the Turkish election of a majority government.

Late October saw a turnaround in the fortunes of ferrous scrap imports into Turkey, with price movement for the material turning positive for the first time in several months. However, before this turnaround occurred TSI’s daily index for imports of HMS #1&2 80:20 scrap hit a fresh record low of $169/mt on October 20. This represented a fall of $150/mt (-53%) from the turn of the year, and highlights the huge impact that Chinese steel exports have had on global markets. Scrap chased imported billet prices lower, while yards carried multiple cargoes for prompt delivery, meaning mills could afford to pick and choose.

Meanwhile, the US domestic scrap market continued to be hampered by poor utilization rates at mills. The October buy-week settled at $15-20/long ton lower, while TSI’s US Midwest shredded index dropped $14/lt over the November buy-week. Pricing was strongest in eastern US, buoyed by increased bulk export trade into Turkey and India. However, towards the back end of the buy-week mills began to push back a little, and are eyeing price increases early in the New Year.

Post-election boost in TurkeyThe Turkish domestic steel market saw a sudden increase in demand, and mills were on the hunt for multiple prompt cargoes, forcing yards to raise their prices. Along with domestic rebar prices, international billet prices also increased, giving scrap prices a further lift. TSI’s monthly Turkey import price reached $187/mt by the end of October, and was pushing close to $200/mt in early November. Platts monthly average price for Turkish scrap imports fell $12.14/mt to $178.93/mt in October.

Participants had mixed views on whether the uptick in scrap prices seen in November

Price rebounds after Turkish election

SCRAP MARKET FOCUS

was sustainable over the longer-term, particularly as winter traditionally brings restricted scrap supply. With global steel demand remaining subdued and iron ore again on the slide, one could easily see scrap prices falling again.

Platts assessment of Turkish premium heavy melting scrap I/II (80:20) imports reached $200.50/mt CFR on November 13, up $3.50/mt on the week before. At least 16 cargoes were booked over the week, according to trades captured by Platts, while one steelmaker said more than 1 million mt of scrap had been booked in the past three weeks or so.

East Asian market flatThe import market for bulk heavy melting scrap remained sluggish in East Asia in the first half of November. Platts assessed

its weekly East Asian bulk HMS 80:20 price at $170-175/mt CFR on November 13, unchanged from the week before.

In Japan, Tokyo Steel Manufacturing has retained scrap buying prices since November 3 arrivals after cutting Yen 500/mt ($4/mt) for its scrap buying prices all works. The purchase price for H2 at its Utsunomiya works, northern Kanto was Yen 15,000/mt ($122/mt). Japanese traders were paying Yen 14,000/mt FAS at Tokyo Bay to collect H2 for export, unchanged from three weeks earlier.

South Korean steelmaker Hyundai Steel booked Japanese scrap at Yen 13,700/mt FOB for H2 grade in the week ending November 13, down by Yen 100/mt from a previous Korean booking two weeks earlier. As Hyundai’s price is much lower than Taiwanese and Korean booking prices, Japanese and Korean trading sources believed the volume secured by Hyundai was limited.

— Staff

PLATTS EAST ASIA SCRAP IMPORTS / HMS 80:20 ($/mt CFR)

Source: Platts

160

200

240

280

320

Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15Feb-15Jan-15Dec-14Nov-14

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 10

NEWS

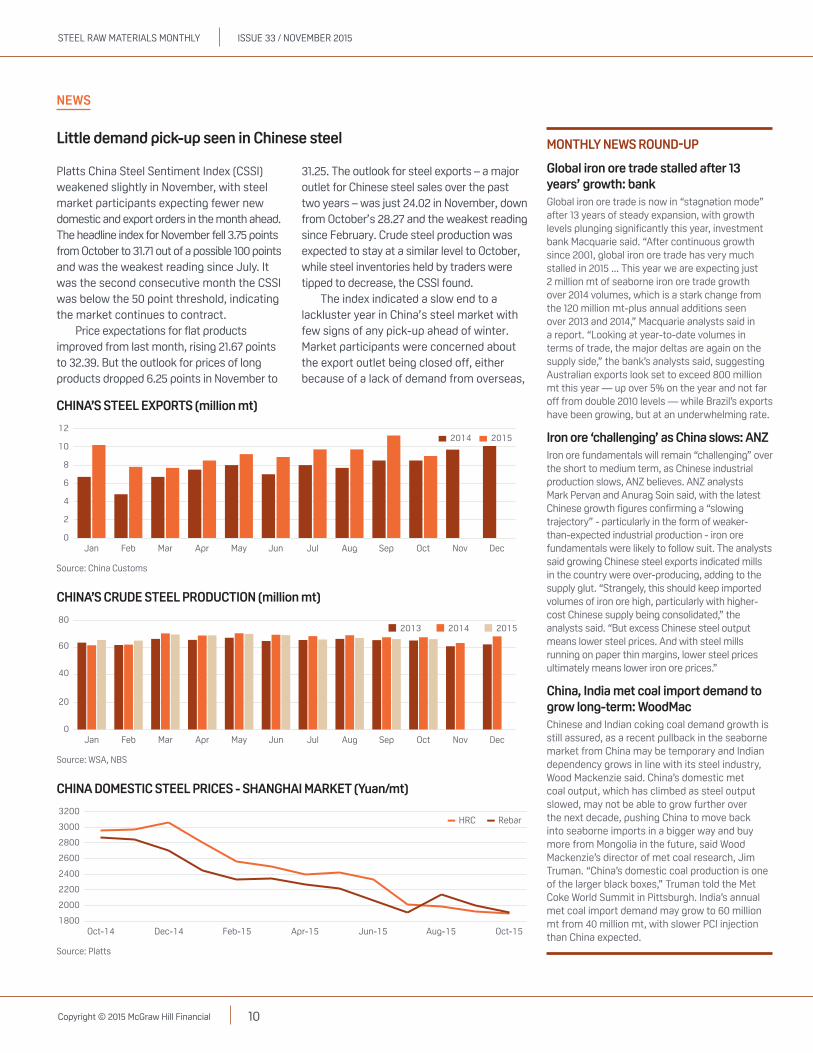

Platts China Steel Sentiment Index (CSSI) weakened slightly in November, with steel market participants expecting fewer new domestic and export orders in the month ahead. The headline index for November fell 3.75 points from October to 31.71 out of a possible 100 points and was the weakest reading since July. It was the second consecutive month the CSSI was below the 50 point threshold, indicating the market continues to contract.

Price expectations for flat products improved from last month, rising 21.67 points to 32.39. But the outlook for prices of long products dropped 6.25 points in November to

Little demand pick-up seen in Chinese steel MONTHLY NEWS ROUND-UP

Global iron ore trade stalled after 13 years’ growth: bankGlobal iron ore trade is now in “stagnation mode” after 13 years of steady expansion, with growth levels plunging significantly this year, investment bank Macquarie said. “After continuous growth since 2001, global iron ore trade has very much stalled in 2015 ... This year we are expecting just 2 million mt of seaborne iron ore trade growth over 2014 volumes, which is a stark change from the 120 million mt-plus annual additions seen over 2013 and 2014,” Macquarie analysts said in a report. “Looking at year-to-date volumes in terms of trade, the major deltas are again on the supply side,” the bank’s analysts said, suggesting Australian exports look set to exceed 800 million mt this year — up over 5% on the year and not far off from double 2010 levels — while Brazil’s exports have been growing, but at an underwhelming rate.

Iron ore ‘challenging’ as China slows: ANZIron ore fundamentals will remain “challenging” over the short to medium term, as Chinese industrial production slows, ANZ believes. ANZ analysts Mark Pervan and Anurag Soin said, with the latest Chinese growth figures confirming a “slowing trajectory” - particularly in the form of weaker-than-expected industrial production - iron ore fundamentals were likely to follow suit. The analysts said growing Chinese steel exports indicated mills in the country were over-producing, adding to the supply glut. “Strangely, this should keep imported volumes of iron ore high, particularly with higher-cost Chinese supply being consolidated,” the analysts said. “But excess Chinese steel output means lower steel prices. And with steel mills running on paper thin margins, lower steel prices ultimately means lower iron ore prices.”

China, India met coal import demand to grow long-term: WoodMacChinese and Indian coking coal demand growth is still assured, as a recent pullback in the seaborne market from China may be temporary and Indian dependency grows in line with its steel industry, Wood Mackenzie said. China’s domestic met coal output, which has climbed as steel output slowed, may not be able to grow further over the next decade, pushing China to move back into seaborne imports in a bigger way and buy more from Mongolia in the future, said Wood Mackenzie’s director of met coal research, Jim Truman. “China’s domestic coal production is one of the larger black boxes,” Truman told the Met Coke World Summit in Pittsburgh. India’s annual met coal import demand may grow to 60 million mt from 40 million mt, with slower PCI injection than China expected.

CHINA’S STEEL EXPORTS (million mt)

Source: China Customs

0

2

4

6

8

10

12

DecNovOctSepAugJulJunMayAprMarFebJan

2014 2015

CHINA’S CRUDE STEEL PRODUCTION (million mt)

Source: WSA, NBS

0

20

40

60

80

DecNovOctSepAugJulJunMayAprMarFebJan

2014 20152013

CHINA DOMESTIC STEEL PRICES - SHANGHAI MARKET (Yuan/mt)

Source: Platts

1800

2000

2200

2400

2600

2800

3000

3200

Oct-15Aug-15Jun-15Apr-15Feb-15Dec-14Oct-14

HRC Rebar

31.25. The outlook for steel exports – a major outlet for Chinese steel sales over the past two years – was just 24.02 in November, down from October’s 28.27 and the weakest reading since February. Crude steel production was expected to stay at a similar level to October, while steel inventories held by traders were tipped to decrease, the CSSI found.

The index indicated a slow end to a lackluster year in China’s steel market with few signs of any pick-up ahead of winter. Market participants were concerned about the export outlet being closed off, either because of a lack of demand from overseas,

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 11

Lump buyers floored by Rio Tinto’s term contract pricingSome contractual buyers of Rio Tinto lump are grappling with price exposure from the floor premiums set in their contracts, given the sharp decline in spot premiums this year. According to several contract buyers of Rio’s 62% Fe Pilbara Blend lump, the contractual premium is settled against the monthly average of weekly Platts spot lump assessments, adding a value premium of $0.005/dry metric ton unit. But in the event the monthly average of Platts lump premium assessment is lower than the floor premium set by Rio - which ranges from $0.01/dmtu to $0.06/dmtu among different buyers - the floor is used as the settlement instead.

Vale cuts Brazil Carajas ore project cost by $2 billionBrazilian mining giant Vale again lowered the estimated cost of its massive S11D Carajas iron ore project, this time by $2 billion. The new investment total of $14.4 billion represents a $5.3 billion drop from Vale’s original cost forecast of $19.7 billion, and a $2 billion cut from its latest estimate, in late 2014. The reduction was determined largely by the depreciation of the real against the US dollar, since most of the spending for the project was in the local currency. The total investment includes mine, processing plant and logistics (railway and port). By the end of the third quarter, Vale had already disbursed $8.4 billion into the project and this is expected to total $9.4 billion by year end. According to Vale, works at the S11D mine and respective processing plant was 75% complete, while the rail extension being built to connect the project to the Carajas Railroad (EFC) was 72% completed. The project should come online in the second half of 2016, but the exact date was to be announced in December at the New York Stock Exchange.

MONTHLY NEWS ROUND-UP

CHINESE CRUDE STEEL PRODUCTION 2015 (million mt) Blast furnace output Total outputJan-15 62.3 65.5Feb-15 56.3 65.0Mar-15 60.2 69.5Apr-15 59.4 68.9May-15 60.9 69.9Jun-15 62.3 68.9

Source: WSA

CHINA MILL ANNOUNCED CLOSURES AND MAINTENANCE (mt/year)Mill Volume impact Stoppage statusBayi Iron & Steel 3,000,000 IndefiniteShougang 80,000 One week from late AugustGuofeng I&S 140,000 34 days from August 3Shagang 200,000 Diverted to export rather than domestic sales

Source: Platts

or because low prices will make exports increasingly uneconomic.

Steel inventory levels have been high but traders expected stocks to start falling over the next month, mainly due to some production cuts at mills rather than to a lift in demand.

The CSSI reflects expectations of market participants for the month ahead. A CSSI reading above 50 indicates an increase/expansion and a reading below 50 indicates a decrease/contraction. It is based on a survey of approximately 50-75 China-based market participants including traders, stockists and steel producers.

Manufacturing may have bottomedChina’s manufacturing industry showed signs of stability in October on stronger export

PLATTS CHINA STEEL SENTIMENT INDEX HISTORY (points out of 100)

Source: Platts

0

20

40

60

80

Nov-15Jun-15Jan-15Aug-14Mar-14Oct-13May-13

CHINA REBAR AND HRC EXPORTS ($/mt FOB China)

Source: Platts

250

300

350

400

450

500

Oct-15Aug-15Jun-15Apr-15Feb-15Dec-14Oct-14

HRC Rebar

CHINA PURCHASING MANAGERS’ INDEX

Source: Caixin, NBS

47

48

49

50

51

Oct-15Aug-15Jun-15Apr-15Feb-15Dec-14Oct-14

O�cial PMI Caixin PMI

orders although, similarly to steel, companies had to trim prices to attract buyers.

Caixin’s manufacturing purchasing managers’ index improved to 48.3 points in October from 47.2 in September. While still below the 50 threshold, it was the strongest result since June. With the exception of February, the Caixin (formerly HSBC) PMI has been under 50 all year.

China’s ‘official’ manufacturing PMI, published by the National Bureau of Statistics, was flat in October at 49.8. It was the third consecutive month this PMI has been under 50. The official PMI for the steel industry though slipped again, with October dipping by 1.5 basis points on month to 42.2 [see other article].

Caixin’s PMI for October found that export orders rebounded after three weak

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 12

months due to improved demand. Inventory levels rose for the third consecutive month, while price discounting eased from September but “remained sharp overall.” Manufacturing output fell for the sixth month in a row in October though the rate of reduction was the slowest for four months.

“Nearly 16% of panelists noted lower cost burdens (compared with less than 1% indicating an increase), with a number of firms linking the fall to lower raw material prices, particularly for metals,” Caixin noted.

Caixin chief economist He Fan said there were signs that “previous stimulating measures had begun to take effect” but warned that weak overall demand and lower bulk commodity prices “remain the biggest obstacle to economic growth.” Weakening domestic hot rolled coil prices indicate any positive impact from an improving manufacturing sector may take some time to flow through, and soft domestic demand for finished goods may continue to weigh on steel prices.

The NBS PMI, which breaks down the results by enterprise segment, found that larger manufacturers had recovered from an August low of 49.9 to 51 in October, while small companies reported an 8-month low of 46.6 in October. The total new order index rose to 50.3 in October from 50.2 in September, though production fell to 52.2 from 52.3.

— Paul Bartholomew

NEW BF CAPACITY ADDITIONS IN CHINA - 2013-2015Company Region (city) Capacity mt/year DateShanxi zhongyang Iron & Steel Shanxi (Lvliang) 1,500,000 2013Qinyou Special Metal Material Co., Ltd. Jiangsu (Yangzhou) 1,000,000 2013Xuzhou Huahong Special Steel Jiangsu (Xuzhou) 900,000 2013Minmetals Yingkou Medium Plate Co.,Ltd Liaoning (Yingkou) 2,000,000 2013Hunan Valin Lianyuan Iron & Steel Hunan 2,500,000 2013Baosteel Group Xinjiang Bayi Iron & Steel Xinjiang (Baicheng) 1,380,000 2013Wuhu Xinxing Ductile Iron Pipes Co.,Ltd. Anhui (Wuhu) 1,000,000 2013Wuhan Iron & Steel Group Echeng Iron & Steel Co.,Ltd. (Egang) Hubei (Ezhou) 1,500,000 2013Guangshui Huaxin Metallurgical Hubei (Wuhan) 500,000 2013Xinjiang Kunlun Iron & Steel Xinjiang 800,000 2013Tianjin Metallurgy Group Zhasan Youfa Steel Tianjin 1,200,000 2013Xinjiang Kunyu Iron & Steel Xinjiang (Kuian) 500,000 2013Hebei Xinda Iron & Steel Jilin 1,500,000 2013Yunnan Anning Yongchang Iron & Steel Yunnan (Anning) 1,000,000 2013Anyang Iron & Steel Co.,Ltd. Henan (Anyang) 4,000,000 2013Lianfeng Iron & Steel (Zhangjiagang) Co.,Ltd. Jiangsu (Zhangjiagang) 1,134,000 2013Xinjiang Kunyu Iron & Steel Xinjiang (Kuian) 500,000 2013Sanbao Metallurgical (Fujian) Group Fujian (Zhangzhou) 500,000 2013Shandong Qilu Xintong Steel Pipe Shandong (Liaocheng) 1,000,000 20132013 Total 24,414,000Nanjing Iron & Steel Co.,Ltd. Jiangsu (Nanjing) 3,600,000 2014Pangang Group Xichang New Steel Enterprise Co.,Ltd. Sichuan (Xichang) 1,500,000 2014Baotou Iron & Steel Inner Mongolia 5,000,000 2014Tonghua Iron & Steel Co., Ltd. Jilin 2,200,000 20142014 Total 12,300,000Qingdao Iron & Steel Shandong (Qingdao) 4,000,000 2015Baosteel Group Guangdong (Zhanjiang) 9,000,000 2015Maanshan Iron & Steel Anhui (Maanshan) 2,000,000 2016Bohai Iron & Steel Hebei (Tangshan) 2,000,000 2017Rizhao Iron & Steel Shandong 8,500,000 2017

Source: Platts

PLATTS CHINA STEEL SENTIMENT INDEX – NOVEMBER 2015* Nov-15 Change from October (points)CSSI (Total New Orders) 31.71 -3.75New Domestic Orders 32.38 -3.71New Export Orders 24.02 -4.25Steel Production 42.59 0.66Steel Prices (flat products) 32.39 21.67Stocks held by traders 44.3 -26.9

*A figure over 50 indicates expectations of an increase; under 50 indicates a decrease

Source: Platts

Iron ore - China’s week-long holiday at the start of October put a dent in

SGX iron ore curve below $40/mt for late 2016

IMPLIED CHINESE STEELMAKER MARGIN ($/mt CFR)

Source: TSI, SGX

140

160

180

200

220

240

Jan-17Oct-16Jul-16Apr-16Jan-16Oct-15

traded iron ore derivatives volumes when compared with September’s level.

However, year-on-year, total off-shore trade in US$ denominated iron ore swaps, options and futures of more than 90 million mt cleared against TSI’s 62% Fe iron ore benchmark on Singapore Exchange (SGX) and CME Group was up by nearly 60% on the previous year (which experienced a similar seasonal dip in volumes). The forward curve was little changed over October – most market participants having already priced in negative expectations for the coming year – but there was still some volatility in the front months, the November contract trading in a range between $47-52/dmt. Moving into the start of

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 13

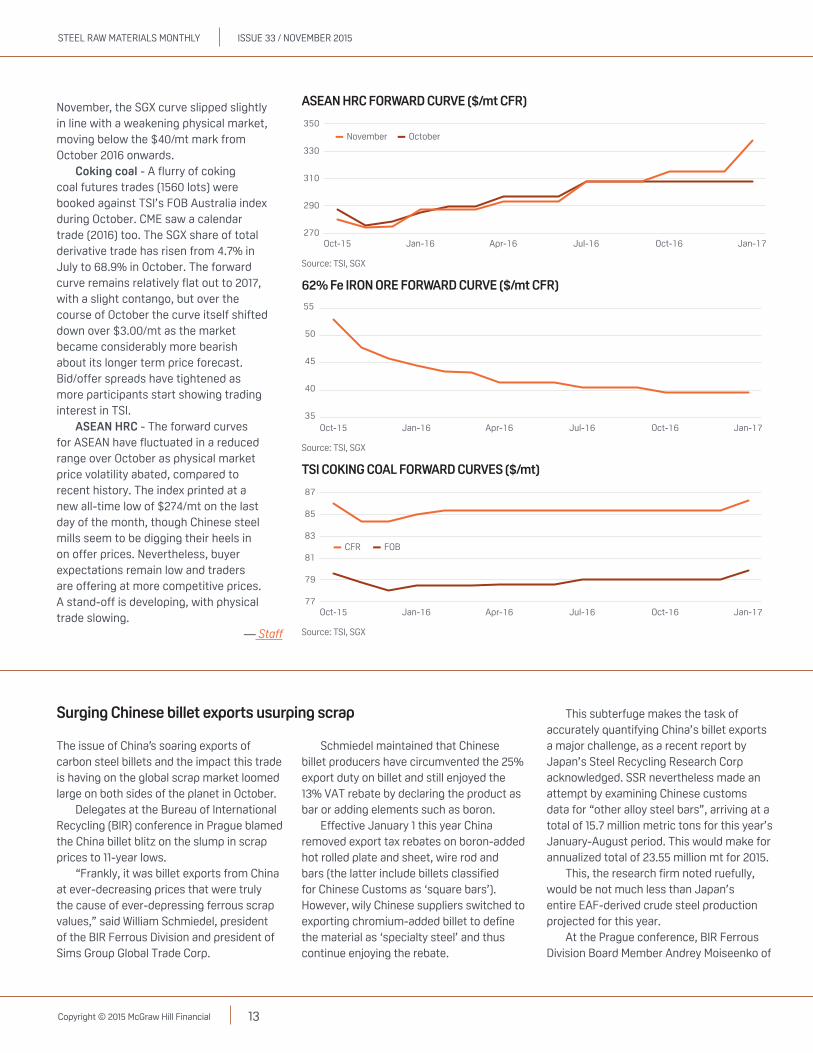

November, the SGX curve slipped slightly in line with a weakening physical market, moving below the $40/mt mark from October 2016 onwards.

Coking coal - A flurry of coking coal futures trades (1560 lots) were booked against TSI’s FOB Australia index during October. CME saw a calendar trade (2016) too. The SGX share of total derivative trade has risen from 4.7% in July to 68.9% in October. The forward curve remains relatively flat out to 2017, with a slight contango, but over the course of October the curve itself shifted down over $3.00/mt as the market became considerably more bearish about its longer term price forecast. Bid/offer spreads have tightened as more participants start showing trading interest in TSI.

ASEAN HRC - The forward curves for ASEAN have fluctuated in a reduced range over October as physical market price volatility abated, compared to recent history. The index printed at a new all-time low of $274/mt on the last day of the month, though Chinese steel mills seem to be digging their heels in on offer prices. Nevertheless, buyer expectations remain low and traders are offering at more competitive prices. A stand-off is developing, with physical trade slowing.

— Staff

TSI COKING COAL FORWARD CURVES ($/mt)

Source: TSI, SGX

77

79

81

83

85

87

Jan-17Oct-16Jul-16Apr-16Jan-16Oct-15

CFR FOB

62% Fe IRON ORE FORWARD CURVE ($/mt CFR)

Source: TSI, SGX

35

40

45

50

55

Jan-17Oct-16Jul-16Apr-16Jan-16Oct-15

ASEAN HRC FORWARD CURVE ($/mt CFR)

Source: TSI, SGX

270

290

310

330

350

Jan-17Oct-16Jul-16Apr-16Jan-16Oct-15

November October

The issue of China’s soaring exports of carbon steel billets and the impact this trade is having on the global scrap market loomed large on both sides of the planet in October.

Delegates at the Bureau of International Recycling (BIR) conference in Prague blamed the China billet blitz on the slump in scrap prices to 11-year lows.

“Frankly, it was billet exports from China at ever-decreasing prices that were truly the cause of ever-depressing ferrous scrap values,” said William Schmiedel, president of the BIR Ferrous Division and president of Sims Group Global Trade Corp.

Surging Chinese billet exports usurping scrap

Schmiedel maintained that Chinese billet producers have circumvented the 25% export duty on billet and still enjoyed the 13% VAT rebate by declaring the product as bar or adding elements such as boron.

Effective January 1 this year China removed export tax rebates on boron-added hot rolled plate and sheet, wire rod and bars (the latter include billets classified for Chinese Customs as ‘square bars’). However, wily Chinese suppliers switched to exporting chromium-added billet to define the material as ‘specialty steel’ and thus continue enjoying the rebate.

This subterfuge makes the task of accurately quantifying China’s billet exports a major challenge, as a recent report by Japan’s Steel Recycling Research Corp acknowledged. SSR nevertheless made an attempt by examining Chinese customs data for “other alloy steel bars”, arriving at a total of 15.7 million metric tons for this year’s January-August period. This would make for annualized total of 23.55 million mt for 2015.

This, the research firm noted ruefully, would be not much less than Japan’s entire EAF-derived crude steel production projected for this year.

At the Prague conference, BIR Ferrous Division Board Member Andrey Moiseenko of

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 14

Ukraine’s Ukrmet said that if Chinese billet exports continue at current volumes there will be significant changes in the global ferrous scrap market.

“We should see structural changes in Turkey,” Moiseenko told Platts. “Some mills will disappear. If [current billet volumes] continue, things will change everywhere for scrap.”

For the Japanese scrap traders, their concerns are nearer to home. The SSR calculated that during this year’s first eight months, China’s exports of billets to South Korea – both disguised and genuine alloy billets – reached 1.4 million mt, which annualized would make for shipments of 2.1 million mt for the full year.

South Korea remains Japan’s single-largest export destination for ferrous scrap, taking 2.48 million mt between January and September this year, accounting for 41% of Japan’s total scrap exports over the period.

Japanese scrap concernsWhat worries the Japanese scrap dealers and traders is that this was nearly 20% down on the same period last year – a drop they associate directly with the increasing reliance of Korean mini-mills on imported Chinese billets.

And it’s not just Japanese scrap that the Koreans are eschewing. Korean customs data shows that during the same January-September period, the country’s scrap imports from all sources plunged by 44%

EAST ASIA BILLET IMPORT PRICES ($/mt)

Source: Platts

250

300

350

400

450

500

550

600

Oct-15Jun-15Feb-15Oct-14Jun-14Feb-14Oct-13Jun-13Feb-13

to 4.5 million mt. Indeed, the US – Korea’s second-largest supplier after Japan – saw its liftings halve over the nine months to just 780,000 mt, the Korean data shows.

The concern in Japan is that if the Chinese mills continue to push their billet into South Korea at the present rate, Japan’s scrap exports could fall by 1 million mt/year. At present scrap prices, that would be the equivalent of $124 million annually in lost business.

In an internal strategy paper obtained by Platts from an Asian scrap merchant, there was speculation over when the flood of Chinese billet would cease.

“By examining billet exports in terms of financial, social and political value, we can first see that no, massive exports will not go on indefinitely,” the merchant wrote. “The timing of the end of billet would either be the beginning of 2016, if China decides to limit exports for trade diplomacy reasons, or in the

worst case after industry consolidation during 2016-2020. The financial and social costs would suggest sooner rather than later.”

The merchant estimated Chinese steel costs equate to $32,000 per worker annually. Sims Group president Schmiedel estimated a per capita loss of around $25,000-$30,000 per employee. “It will be cheaper to pension out these workers than continue to operate at these loss levels,” he said, adding that Beijing is aware of this anomaly.

Tom Bird, head of UK-based Mettalis Recycling agreed that “clearly” there needs to be change in the approach by China.

“Producing steel at the current rate is not sustainable in the long term. [Financial losses are] attracting the attention of Beijing. There is international pressure, this can only be a benefit moving forward,” he told Platts.

— Nicholas Tolomeo, Russ McCulloch

Flanagan told an investor lunch in Melbourne in July. “Normally, if you pull $300 million of costs out of the business that would be enough to make money, but it wasn’t at Easter time. The price fell to $46/mt and the way we were selling iron ore then meant we were actually getting about A$46/mt ($34/mt) but it was costing us A$61/mt ($45/mt) to produce and sell it,” he said.

The C1 cost proportion of the miner’s average realized price in the September 2015 fell to around 57%, compared with 86% for the April-June quarter. Despite all the cost-saving efforts, the falling iron ore price means

Cost saving gains eroded by falling ore price...from page 2

the C1 cost proportion is not much different to the March 2014 quarter when the Platts 62% Fe price was $120/mt CFR. Atlas has said previously that the Australian dollar’s weakness against the US dollar has become like a natural hedge. The miner is also hedging “collars, caps and fixed price cargoes” to better insure itself against lower prices.

Atlas renegotiated terms with its contractors in April and extracted some additional margin from royalty payment deferrals, and from more favorable terms on some haulage and port arrangements from the relevant authorities. There may not be

much more scope for cost cutting if prices go even lower.

Fellow Pilbara junior BC Iron is also hedging some iron ore volumes and foreign exchange rates to protect its breakeven price. It managed to cut A$6/wmt from its costs in the September quarter to A$52/wmt ($36.6/wmt) out of a realized price of $47/dmt CFR.

Mount Gibson Iron’s pit wall collapse at its Koolan Island mine in the Kimberly region of Western Australia reduced its production capacity to around 4.5 million-5 million wmt/year. Its all-in costs of A$52/wmt FOB ($36.6/wmt) in the September quarter against a realized sales price of $40/dmt FOB shows the company’s margins are extremely slim.

— Paul Bartholomew

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 15

SPECIAL REPORT: BATTLING BRICS

When then Goldman Sachs economist Jim O’Neill coined the term BRICs in 2001, China was at the start of a decade of surging economic growth, with GDP averaging around 10.5% a year. If not for the global economic crisis years of 2008 and 2009, when China’s export markets were severely affected, it would have been stronger still. Since 2012, however, the Chinese economy has slowed markedly, down to levels closer to 7%, as the tail of Beijing’s 2008-2009 Yuan 4 trillion ($586 billion) stimulus program started to recede.

Many argue the stimulus package was responsible for fueling debt at provincial governments and state-owned enterprises, resulting in the overcapacity issues – particularly in steel and housing – that China is dealing with today.

With China’s economy expanding year after year, companies both inside and outside of China believed the good times

China – shift to lower gear as economy transitions

MANUFACTURING PURCHASING MANAGERS’ INDICES �PMI � POINTS

42

44

46

48

50

52

54

Oct-15Aug-15Jun-15Apr-15Feb-15

(index)

Source: Markit Economics

ChinaIndia BrazilRussia

BRICS STEEL CONSUMPTION

0

200

400

600

800

BrazilRussiaIndiaChina

(million mt)

Source: worldsteel*Forecast.

2014 2015 (f)* 2016 (f)* % = Year-on-year change-3.3% -3.5% -2.0%

+3.1% +7.3% +7.6%-0.7% -10.4% -1.0% -8.6% -12.8% +0.5%

would last forever. Chinese steel mills – both state- and privately-owned – rapidly built up production capacity to support the country’s rapid development and urbanization. Iron ore companies, such as BHP Billiton and Rio Tinto (along with newcomer Fortescue Metals Group and a flotilla of ‘junior’ miners) embarked on huge capacity expansions to feed steel production that was expected to surpass 1 billion metric tons/year by next decade. Indeed, there was never any notion that China might slow one day; or at least not by much.

But just as the pace of China’s growth astonished so many, its slowdown has also surprised. The country’s fixed-asset investment fell to a near 15-year low in August and the much-mooted build-out of central, not to mention western China, has been slower than expected and certainly less steel-intensive than urbanization along the eastern seaboard.

In a September report from CLSA, analysts noted that China’s steel consumption had decoupled from GDP growth for the fifth consecutive year in 2015. This was a “logical” trend for a developing economy, CLSA argued, as steel was usually “at the forefront of the economic development cycle due to the need to build out capacity.”

In September, Standard & Poor’s downgraded its GDP outlook for China next year to 6.3% from 6.6% with 2017 revised to 6.1% from 6.3%. (In fact, many believe China’s true GDP is already closer to 6% than 7%).

Last year, China’s steel consumption fell 3.4% year-on-year, its first reversal in three decades. World Steel Association has forecast China’s steel consumption will fall 3.5% this year and by a further 2% in 2016. The country’s steel production in 2015 appears on track to fall 1-2% on last year. Even BHP has scaled back its outlook for China’s steel output to 935 million-985 million mt by the middle of next decade from 1 billion mt previously. Rio insists Chinese output will still creep up by around 1% a year to reach 1 billion mt by 2030.

The boom years have seen China build up crude steel production capacity of some 1.1 billion mt/year, of which it is using just 73% currently, Platts estimates.

New steel capacity is slowing, from around 25 million mt in 2013 to 12.3 million mt in 2014, with a similar volume coming on stream this year, largely from Baosteel, according to data collected by Platts. Existing production is being trimmed in response to weak market conditions, but as yet there have been no major output cuts or mothballing of facilities, such as those seen in other parts of the world. New environmental targets could further curb steel output in coming years. In short, like Chinese GDP, steel output and consumption have peaked and are now on their way down.

Different hands at the tillerVery little was said beforehand about the likely impact of the new administration led by Xi Jinping and Li Keqiang that replaced

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 16

Hu Jintao and Wen Jiabao in March 2012 – at least not from or about the steel and resources sectors. It was assumed the pair would continue the strategies of the former administration; one which in the words of a senior Asia-based economist, “threw money at everything!” But Xi-Li have subsequently focused on more measured and sustainable growth, transitioning the economy to one driven by the wealthier population’s need for new cars and fridges, rather than more government investment in infrastructure and a reliance on exports.

However, the journey is not proving to be easy. S&P’s Academic Council surmised in an October meeting that: “There are significant risks building in the Chinese economy that could tip the balance toward a much more implosive scenario, and the chances that the country’s leaders can carry out a planned transformation toward a more services-based economy without suffering a sharp slowdown are becoming smaller.”

Beijing has started to tackle the country’s corruption problem, which some say has contributed to the slowdown. Deals aren’t getting done as easily as before. Pollution is another issue high on Beijing’s agenda, which has a serious social

impact. But the sense is that pressure on companies, including steel mills, to comply with new environmental regulations is relaxed at times of slower economic growth.

Provincial governments need to meet their revenue and tax targets, while maintaining employment.

The central government’s intervention in the Shanghai stock exchange crash earlier this year indicated the shift to a more market-driven economy may be some time away. China still dances to its own economic tune, and is not subject to the same rules as other countries. It is this that attracts the ire of steelmakers in the US, EU and other regions as domestic producers lose market share to Chinese imports. In contrast, surprisingly few steel companies or larger traders in China have failed, despite a lack of cash and extremely low steel prices over the past two years, which suggests they continue to be propped up by provincial governments, or are just hanging on by their fingertips.

Haixin Iron & Steel declared bankruptcy last year. In October, state-owned trader Sinosteel Corp was rumored to have defaulted on bank loans worth billions of yuan, which it later denied. A month later, Chinese coking coal producer Hidili Industry International Development Ltd missed a principal payment on an outstanding US dollar bond. Many smaller steel and iron

CHINA’S STEEL EXPORTS (million mt)

Source: China Customs

0

2

4

6

8

10

12

DecNovOctSepAugJulJunMayAprMarFebJan

2014 2015

CRUDE STEEL PRODUCTION JANUARY�SEPTEMBER 2014�2015

0

100

200

300

400

500

600

700

BrazilRussiaIndiaChina

(million mt)

Source: worldsteel

2014 2015 % = Year-on-year change-2.1%

+3.1% -0.5% -1.2%

China’s economic growth prospects getting murkier. Photo: Platts

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 17

ore trading companies have closed their doors. But considering Baosteel’s research department estimates the 100 top steel companies in China lost a collective $3.1 billion over January-August this year, it is remarkable there have been almost no casualties among larger entities.

Running out of steamThe huge stimulus package in the financial crisis period was aimed at boosting domestic growth at a time when the rest of the globe’s economies were in the doldrums. But local demand is now back at GFC levels. Property construction accounts for around 50% of Chinese steel consumption but is being weighed down by a massive oversupply of new apartments – some 40 million or more on some estimates. Regardless of an improvement in sales – which is largely occurring in tier 1&2 cities rather than in smaller cities where the oversupply is at its worst – working through the supply backlog will take a long time.

Much of China’s success over the past decade has been built on productivity gains as workers moved from rural areas to factories. But there are fewer available cheap workers these days, wages have risen, meaning China is less competitive than before, and subsequently some manufacturing – the other key market for steel demand – is being relocated to other countries, including even the US.

Manufacturing activity data is the weakest in six years. Auto production and sales are patchy, while shipping manufacturing has also been lackluster in an oversupplied market.

In Markit’s Business Outlook Survey for China, released on November 9, it found the “weakest level of optimism amongst Chinese companies since data collection began late-2009.” This was highlighted by a net balance of just +17% of firms expecting business activity to rise over the next year, down from a previous low of +23% in June. Markit said this was “broadly in line with that seen across the BRIC nations as a whole (+18%).”

Relying on offshore marketsTo the chagrin of international steel companies, China has resorted to export

S&P GDP GROWTH SUMMARY (%)

Source: S&P

-5

0

5

10

BrazilRussiaIndiaChina

2016 201720152014

CHINA STEEL MANUFACTURING VS STEEL OUTPUT

Source: Platts

(million mt) (points)

0

20

40

60

80

Jul-15Jun-15May-15Apr-15Mar-15Feb-15Jan-1547

48

49

50

51

PMI (right)Steel output (left)

markets over the past year to offload its excess steel capacity at a time of extremely weak domestic demand. Over January-October China exported 92 million mt of steel, compared with a 73.4 million mt over the same period last year. Relatively weaker October exports of 9 million mt, down almost 20% month-on-month, suggest overseas appetite for Chinese steel could be starting to wane slightly. But it is too early to tell if the lower export figure is due to a plethora of potential dumping investigations hanging over Chinese steel imports. To date, China has managed to maintain its overall export levels by redirecting material away from countries threatening trade sanctions into other regions.

Chinese authorities removed an export tax rebate on certain alloy steel products at the start of the year in a bid to deter exports. But they appear to have become more sanguine about the export level as the year has proceeded, knowing there is not the domestic demand to absorb so much steel.

China’s big plan is to export its expertise, financial muscle and even workers under its ‘one belt, one road’ strategy – which can be interpreted as Beijing’s global ‘soft power’ push, as well as

another way of supporting its state-owned steel producers, contractors and engineers. It has been estimated that more than 60 countries could benefit from Beijing’s largesse, whereby China lends countries the funds to develop infrastructure largely fulfilled by Chinese companies. Steel mills in northern China’s Hebei province have discussed relocating capacity to emerging countries, perhaps in support of ‘one belt, one road.’ But as the UK’s recent “red carpet treatment” for Xi Jinping indicates, it is not just emerging nations that want to deepen relations with China.

While China may no longer be the shining beacon among the BRICs – many expect the strong growth to come from India now – it remains the most important country in global steel markets. More clarity around Beijing’s thinking will come to light when China announces its long-awaited ‘Steel Industry Restructuring Policy’ as part of its 13th 5-year plan that begins in 2016.

Certainly, the iron ore producers will hope that China can somehow maintain its strong steel production, otherwise prices will come under even more pressure.

— Paul Bartholomew

STEEL RAW MATERIALS MONTHLY ISSUE 33 / NOVEMBER 2015

Copyright © 2015 McGraw Hill Financial 18

INDIA’S OVERALL STEEL IMPORTS DURING APRIL-SEPTEMBER (mt) 2015 2014 Change y-o-yChina 1,591,460 1,343,850 18%South Korea 1,516,320 855,050 77%Japan 1,147,270 654,060 80%Russia 215,870 84,510 155%Ukraine 148,810 222,360 -33%Other countries 1,282,210 1,028,490 25%Total Steel 5,928,940 4,188,320 42%

Source: Joint Plant Committee

INDIAN IRON ORE IMPORTS-EXPORTS JANUARY-AUGUST 2013-2015 (million mt) 2013 2014 2015South Africa 456,824 1,275,799 4,022,655Brazil - - 2,292,870Oman - 41,632 2,129,429Australia 107,540 317,778 607,168Total imports 1,109,773 2,060,856 9,336,545Total exports 9,745,781 8,218,547 2,728,749Net exports 8,636,008 6,157,691 -6,607,796

Source: Ministry of Commerce, GTIS

India’s ambition to increase steel production to 300 million metric tons/year has been thwarted by slower than expected growth in consumption. Market pundits dropped India’s steel consumption estimates to 4-5% from an earlier forecast of 6-7%. The World Steel Association’s estimate for Indian demand this year is for a 7.1% year-on-year rise to 81.5 million mt and a further 7.6% climb next year to 87.6 million mt.

Industry participants surveyed by Platts estimate that steel demand may rise 4-5% this financial year (ending March 31 2016) to 80 million mt. This is reflected in recent data published by the Joint Plant Committee, which shows India’s overall finished steel consumption rose 4.5% y-o-y to 46.2 million mt during the April-October half.

Meanwhile, India’s overall steel capacity increased by 46% over the previous five years to an estimated 110 million mt/year during the fiscal ended March 2015, from levels of 75 million mt/year in fiscal year 2009-2010. However, steel consumption, which rose by a strong 11.9% during FY2010-2011, has declined since then by 2.4% each year, according to a report published on November 5 by Mumbai-based research agency India Ratings

Further propelling the overcapacity problem is the new capacity being completed by companies such as Tata Steel, Steel Authority of India Limited (Sail) and JSW Steel, which will result in an additional 12-14 million mt/year becoming operational in the current fiscal.

Domestic demand stuttersSteel demand declined due to a slump in the construction, capital goods and automobile sectors, which are the main consumers

of steel, the report said. This resulted in estimated capacity utilization for integrated steelmakers in India falling to 81% in fiscal 2014-2015 from 88% in the fiscal ending March 2010.

The national budget delivered in late February allocated investments of Rupees 140 billion ($2.1 billion) and Rupees 100 billion for road and railway projects respectively in the current fiscal. However, the execution of big ticket infrastructure items, such as metro rail networks in various cities and highway widening projects, has been delayed due to land acquisition, financing and regulatory approval hurdles.

Similarly, Prime Minister Narendra Modi’s ‘Make in India’ initiative aims to transform India into a manufacturing hub by encouraging investment in the industrial sector. The initiative aims at increasing the share of the manufacturing sector in the country’s GDP from the current 16% to 25% by 2022. However, the rate of growth of industrial production during fiscal 2014-2015 was only 2.3%, far below the rate of GDP growth.

India’s manufacturing sector experienced a further slowdown in October, mirroring the decline in the country’s steel output. Nikkei India’s purchasing managers index (PMI) recorded a 22-month low of 50.7 in October, from 51.2 in September.

Steel forms about 2% of GDP and about 16% of the industrial sector. But a recent study by the National Council of Applied Economic Research found that current conditions of India’s steel industry were “dismal”, with very low profits, low capacity utilization and dim prospects of new private investment, either foreign or domestic.

Analysts believe that a proper implementation of ‘Make in India’, coupled with aligned infrastructure development, will boost steel demand growth by 10-12% during 2018-2019 to 2024-2025, reaching 160-180 million mt by 2024-25.

India’s per capita steel consumption was 59.4 kgs in 2014, according to the World Steel Association. This is much lower than per capital steel consumption of the largest steel producer China at 510 kgs. India’s is unlikely to ever reach a similar level.

To stimulate consumer spending, the

Reserve Bank of India (RBI) dropped the bank repo rate by a total of 125 basis points over four rate cuts since January in an attempt to encourage banks to drop their lending rates. To date, this has not had the desired effect, in terms of raising consumer borrowings.