Embed Size (px)

Citation preview

SAMPLE C

ONTENT

SAMPLE C

ONTENT

ii

Preface

Lazy Bone Publications is a publication house founded and managed by Chartered Accountants. We started writing books with an aim that a student reading our books should enjoy, understand, grasp and remember the content. We aim to take education to the next level and this book is a step forward.

Book – Keeping & Accountancy is one of the most important subjects of Commerce stream. The knowledge gained this year will help in building a strong foundation for years to come. Through this book we have tried to explain theory in much simpler manner. This book is also filled with various practical problems. We sincerely hope that this book helps you in understanding the subject easily. When you understand the subject, it will be easy for you to remember it as well. This year is extremely important to you and we understand that. Smart Notes covers the entire syllabus and all possible questions that can be asked in your board exams.

We take this opportunity to thank all the students and teachers who have provided their feedback, suggestions and reviews. We thank our authors for their sincere efforts in enhancing the book.

We are open to your suggestions to make the book more student-friendly.

Mail us at [email protected]

SAMPLE C

ONTENT

iv

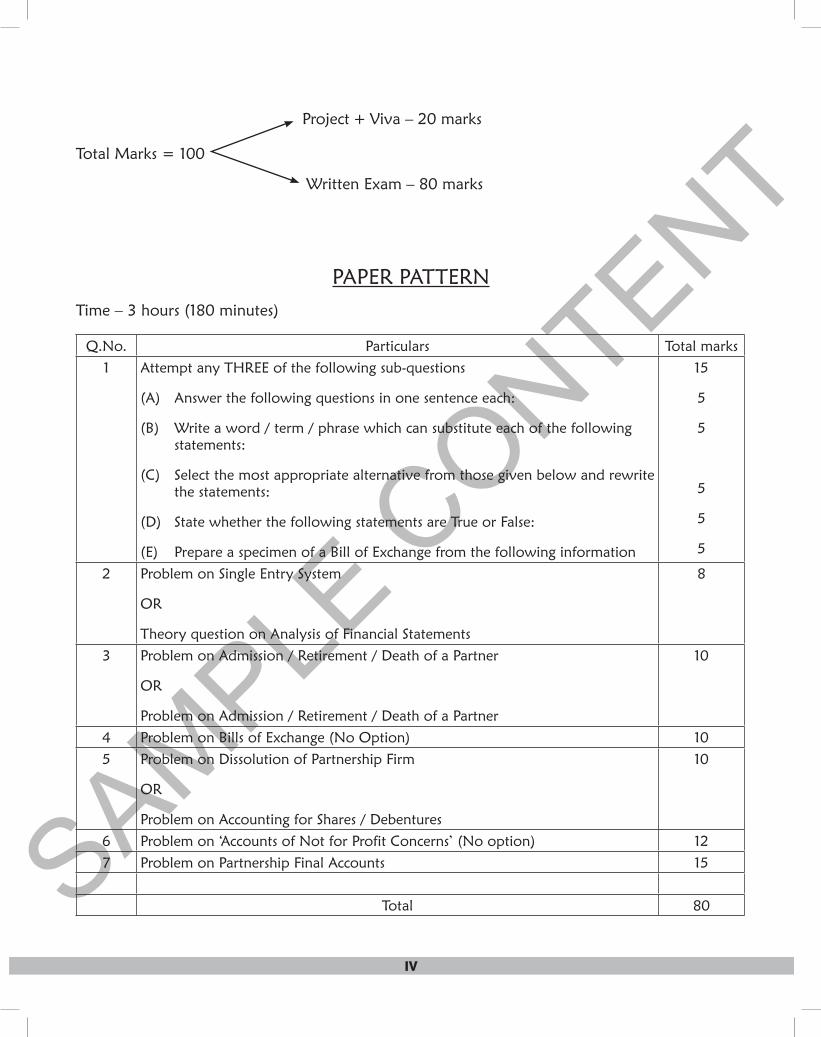

Project + Viva – 20 marks

Total Marks = 100

Written Exam – 80 marks

PAPER PATTERNTime – 3 hours (180 minutes)

Q.No. Particulars Total marks1 Attempt any THREE of the following sub-questions

(A) Answer the following questions in one sentence each:

(B) Write a word / term / phrase which can substitute each of the following statements:

(C) Select the most appropriate alternative from those given below and rewrite the statements:

(D) State whether the following statements are True or False:

(E) Prepare a specimen of a Bill of Exchange from the following information

15

5

5

5

5

5

2 Problem on Single Entry System

OR

Theory question on Analysis of Financial Statements

8

3 Problem on Admission / Retirement / Death of a Partner

OR

Problem on Admission / Retirement / Death of a Partner

10

4 Problem on Bills of Exchange (No Option) 105 Problem on Dissolution of Partnership Firm

OR

Problem on Accounting for Shares / Debentures

10

6 Problem on ‘Accounts of Not for Profit Concerns’ (No option) 127 Problem on Partnership Final Accounts 15

Total 80

SAMPLE C

ONTENT

v

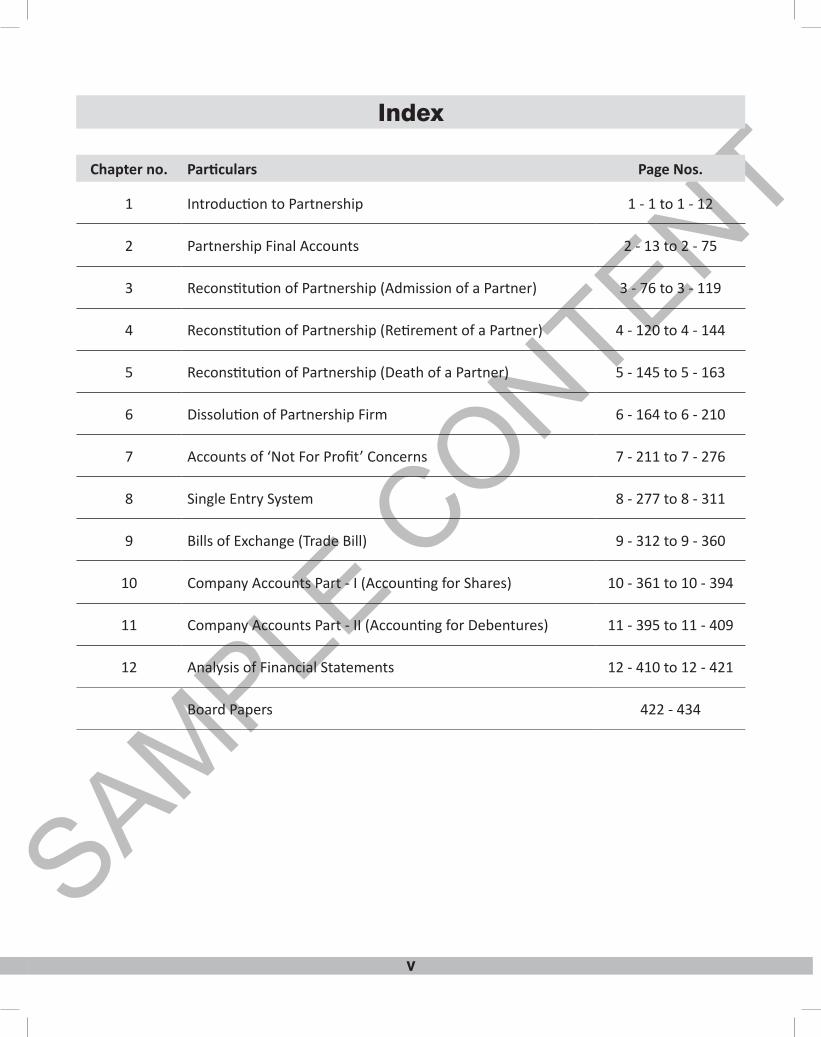

index

Chapter no. Particulars Page Nos.

1 Introduction to Partnership 1 - 1 to 1 - 12

2 Partnership Final Accounts 2 - 13 to 2 - 75

3 Reconstitution of Partnership (Admission of a Partner) 3 - 76 to 3 - 119

4 Reconstitution of Partnership (Retirement of a Partner) 4 - 120 to 4 - 144

5 Reconstitution of Partnership (Death of a Partner) 5 - 145 to 5 - 163

6 Dissolution of Partnership Firm 6 - 164 to 6 - 210

7 Accounts of ‘Not For Profit’ Concerns 7 - 211 to 7 - 276

8 Single Entry System 8 - 277 to 8 - 311

9 Bills of Exchange (Trade Bill) 9 - 312 to 9 - 360

10 Company Accounts Part - I (Accounting for Shares) 10 - 361 to 10 - 394

11 Company Accounts Part - II (Accounting for Debentures) 11 - 395 to 11 - 409

12 Analysis of Financial Statements 12 - 410 to 12 - 421

Board Papers 422 - 434

SAMPLE C

ONTENT

5 - 145

CHAPTER 5: RECONSTITUTION OF PARTNERSHIP (DEATH OF PARTNER)

Sr. No. Particulars Page No.

1. Theory 5 - 146

2. Section I :

Textbook Problems 5 - 147

3. Section II :

Board Problems 5 - 156

4. Section III :

Homework Problems 5 - 157

5. Section IV :

Objective Type Questions 5 - 162

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

5 - 146

A partner retires from the firm voluntarily. His retirement can be planned and he can decide to cease to be a partner from a specified date. But when it comes to death of a partner, it comes unplanned. It may happen on any date and even in the middle of the accounting period. On a partner’s death, he no longer remains a partner and it therefore leads to his compulsory retirement from the firm. Such a partner is called the deceased partner. The legal effects of a partner’s death are similar to his retirement in some cases. As far as accounting treatment is concerned, it remains same to a great extent to that in the case of retirement.

The following are aspects which are similar:-

1. New Profit sharing ratio

Profit sharing ratio may remain the same after the death of one of the partners or they may mutually agree to change the profit sharing ratio to a new one. Sometimes, the partnership deed may provide for the new ratio in case of death.

2. Gain / Benefit Ratio

Just as we calculated the gain ratio in retirement, we need to compute the gain ratio in case of death of a partner. If the new ratio remains the same as old ratio or is not mentioned, then the gain ratio is same as old ratio. If the new ratio is different than the old ratio, then the gain ratio changes and needs to be computed.

Gain Ratio = New Ratio – Old Ratio

3. Revaluation of Assets and Liabilities

Again, repeating the procedures followed during retirement of a partner, we may have to revalue assets and liabilities on death of a partner. The surplus or deficit is then transferred to all partners’ capital accounts including the deceased partner’s account.

4. Amounts that are due to a deceased partner’s executor /nominee /administrator a. Capital amount The amount of capital that the partner has brought in now needs to be returned. The capital is calculated from the

amount obtained from the last balance sheet provided and after adding/subtracting the following amounts. b. Amount in Current Account Just as the capital contribution needs to be returned, so also the amount that the capital has in his current account

needs to be returned. In case of a debit balance, the same needs to be recovered. c. Interest on Capital If the partnership deed provides for interest on capital, we need to calculate and credit the partner’s account. We

have to calculate the same for the period from the date of the last balance sheet till the date of death. d. Drawings If the deceased partner had made any drawings from the date of the last balance sheet till his death, we need to

debit his capital account for the same. e. Interest in Drawings In case there are drawings and the deed provides for interest on drawings, we need to calculate the same till the

date of his death and debit his account. f. Undistributed Profits/Accumulated Losses These are distributed to all the partners including the deceased partner in their old ratio. g. Share in Revaluation of Assets/Liabilities Similar to the procedure during a partner’s retirement, assets and liabilities may be revalued. The surplus or deficit

needs to be credited or debited respectively to the deceased partner’s capital account. h. Share in Goodwill The deceased partner’s share in goodwill, if any, has to be credited to his account. i. Salary to the Partner Salary is provided if the partnership deed mentions it. It has to be credited to the deceased partner’s account till

the date of his death. j. Profits earned till date of death Profits are finally calculated for the entire year. But, a partner may die at any time during the year. His share of

profit is calculated till the date of his death by estimating a certain rate of profit. It may be computed based on previous years’ average profits. This is then credited to his account.

SAMPLE C

ONTENTReconstitution of Partnership

(Death of Partner)

5 - 147

Section I : Textbook Problems

Q1. Following is the financial position of Vishal, Sagar & Amar who were equal partners. (S)

Balance Sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital Goodwill 6,000Vishal 12,000 Machinery 16,000Sagar 9,000 Stock 11,000Amar 8,000 Debtors 9,000Creditors 6,000 Bank 8,000Reserve Fund 9,000Profit & Loss 6,000

50,000 50,000

On 1st October, 2012 Amar died and following adjustments were made 1) Goodwill of the firm was appreciated by Rs. 3,600, however only Amar’s share in the appreciated value was raised

in the books. 2) RDD was maintained at 5% on debtors. 3) Stock is valued at Rs. 10,000 & machinery at Rs. 14,900. 4) Amar was to be given his share in the profit upto the date of death on the estimated profit based on previous year’s

profit Rs. 12,000. 5) Amount due to Amar was transferred to his executor’s loan account. Prepare: 1) Profit and Loss Adjustment Account 2) Balance Sheet of Vishal and Sagar. Answer: P & L Adjustment A/c: Rs. 2,550 (loss) Executor’s Loan A/c: Rs. 15,350

Balance Sheet Total: Rs. 50,650

Q2. Rajendra, Sangita and Sandhya were partners sharing profits and losses in the ratio of 2:2:1. Their Balance sheet as on 31st March, 2012 was as follows: (S)

Balance Sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital:Rajendra 40,000 Machinery 45,000Sangita 30,000 Stock 22,000Sandhya 20,000 Investment 24,000Creditors 18,000 Debtors 18,800 Bills Payable 22,000 Less: R.D.D 800 18,000

Cash 21,0001,30,000 1,30,000

Sangita died on 30th June, 2012. The following adjustments were made in the books of the firm. 1) Stock was revalued at Rs. 26,000. 2) Machinery was depreciated by 10%. 3) R.D.D is no longer necessary 4) Goodwill of the firm raised at Rs. 25,000. 5) 50% of the investment was taken over by Sandhya at book value and other 50% was sold at a Profit of Rs. 3,000. 6) The deceased partner’s share in profit upto the date of death was to be calculated on the basis of average profits

of last two years. Profit figures of last two years were Rs. 19,000 and Rs. 17,000.

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

5 - 148

Prepare:

1) Revaluation A/c.

2) Partner’s Capital A/c.

3) Balance Sheet as on 1st July, 2012.

Answer: Revaluation A/c: Rs. 3,300 (Profit) Legal heir’s loan A/c: Rs. 43,120

Balance Sheet Total: Rs. 1,48,100

Q3. Shrikant, Anita, Pardeshi were equal partners. Their Balance Sheet as on 31st March, 2012 was as under. (S)

Balance Sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital Machinery 20,000Shrikant 15,000 Stock 9,000Anita 12,000 Goodwill 10,000Pardeshi 8,000 Debtors 12,000Creditors 14,000 Less: R.D.D 1,000 11,000Reserve Fund 9,000 Bank 14,000Profit and Loss A/c 6,000

64,000 64,000

On 1st Oct, 2012, Pardeshi died and the following adjustments were made in the books.

1) Machinery revalued at Rs. 19,000 and stock Rs. 8,500.

2) R.D.D was maintained at Rs. 4,000.

3) Goodwill of the firm was appreciated by Rs. 3,000 however only Pardeshi’s share in the appreciated value was raised in the books.

4) Pardeshi was given his share of profit upto the date of death on the basis of estimated profit which was Rs. 3,600/- for the year 2012-2013.

5) Reserve fund of Shrikant and Anita kept in the business.

6) Amount due to Mr. Pardeshi was to be transferred to his executor’s loan account.

Prepare:

1) Profit and Loss Adjustment A/c.

2) Partner’s Capital Accounts.

3) Balance Sheet of Shrikant & Anita.

Answer: P & L Adjustment A/c: Rs. 4,500 (loss) Executor’s loan A/c: Rs. 13,100

Balance Sheet Total: Rs. 61,100

Q4. Sudhakar, Madhukar and Raghunath were partners in a business sharing profit and losses in the ratio of 3:1:1 respectively. Their Balance Sheet as on 31st March, 2012 was as under. (S)

Balance Sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Sudhakar 40,000 Machinery 40,000Madhukar 30,000 Furniture 30,000Raghunath 20,000 Debtors 30,000Creditors 16,000 Cash 11,000General Reserves 5,000

1,11,000 1,11,000

SAMPLE C

ONTENTReconstitution of Partnership

(Death of Partner)

5 - 149

Raghunath died on 31st December, 2012 1) Machinery was to be revalued to Rs. 46,000 and furniture at Rs. 29,000/-. 2) The drawings of Raghunath upto the date of death amounted to Rs. 12,000/-. 3) Interest on capital was to be allowed at 10% p.a. 4) Interest on drawings was to be charged at 6% p.a. 5) His share of goodwill to be calculated on the basis of two years purchase of last four years average profit. His share of profit up the date of his death to be based on the profit of the previous year. Previous Profit figures = Rs. 70,000, Rs. 60,000, Rs. 30,000, Rs. 40,000 Prepare: 1) Raghunath’s Capital account showing the amount payable to his legal heir 2) Give the working of goodwill and profit.

Answer: P & L Adjustment A/c: Rs. 5,000 (Profit) Legal heir’s loan A/c: Rs. 36,960

Raghunaths share in Goodwill: Rs. 20,000 Raghunaths share in Profit: Rs. 6,000

Q5. Parag, Siddhesh, Nishu were partners sharing profit and losses in the ratio of 4:3:3. Their balance sheet was as follows:

(S)

Balance Sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital Sundry Assets 80,000Parag 40,000 Stock 30,000Siddhesh 40,000 Debtors 40,000Nishu 30,000 Less: R.D.D 2,000 38,000Creditors 22,000 Cash 12,000General Reserve 12,000Profit and Loss Account 16,000

1,60,000 1,60,000

Nishu died on 1st July, 2012 and the following adjustments were agreed 1) Sundry assets revalued to Rs. 90,000/-. 2) R.D.D was maintained at 10% on Debtors. 3) A provision for outstanding expenses was to be made for Rs 1,000/-. 4) His share of goodwill to be calculated on 3 years purchases of average profit of last 4 years. Profits of last four years were – Rs. 20,000, Rs. 22,000, Rs. 18,000, Rs. 12,000. 5) The deceased partner to be given his share of profit to the date of his death on the basis of average profits of last

two years. 6) His drawings till the death amounted to Rs. 27,825. Prepare: 1) Nishu’s Capital account showing the amount payable to his legal heir 2) Give the working of goodwill and profit.

Answer: P & L Adjustment A/c: Rs. 7,000 Legal heir’s loan A/c: Rs. 30,000

Nishu’s Share in profit: Rs. 1,125 Nishu’s share in goodwill: Rs. 16,200

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

5 - 150

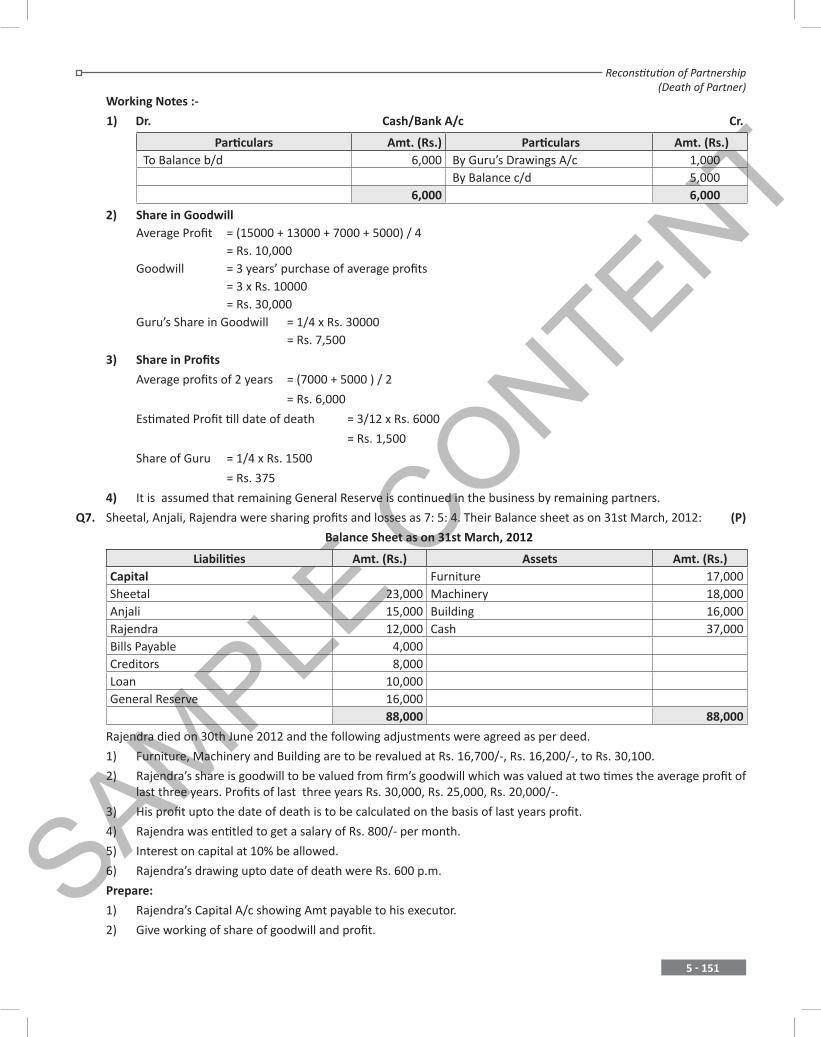

Q6. Vilas, Mangal, Guru were partners in a business sharing profits and losses in the ratio of 2: 1: 1 respectively. Their Balance sheet as on 31st March, 2012 was as follows: (P)

Balance Sheet as on 31st March 2012

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital Land and Building 6,000 Vilas 6,000 Debtors 5,000 Mangal 7,000 Stock 3,000 Guru 3,400 Cash 6,000Creditors 2,000General Reserve 1,600

20,000 20,000Guru died on 1st July, 2012

1) Land and Building was to be revalued to Rs. 7,000 and RDD was to be created of Rs. 200. 2) The drawing of Guru upto the date of his death amounted to Rs. 1,000/-. 3) Charge interest on drawing Rs. 100/-. 4) His share of goodwill should be calculated at ‘Three’ years purchase of the profits for the last four years which were

Rs. 15,000, Rs. 13,000, Rs. 7,000, Rs. 5,000. 5) The deceased partners share of profit upto the date of his death to be calculated on the basis of average profit of

last two years. Prepare: 1) Profit and Loss Adjustment A/c 2) Partners Capital A/c’s 3) Balance Sheet of the continuing firm. 4) Give working of share of profit and goodwill. Solution:

Dr. Profit & Loss Adjustment A/c Cr.

Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)To RDD A/c 200 By Land & Building A/c 1,000 To Profit on Revaluation transferred By Interest on Drawings A/c 100 Vilas’ Capital A/c 450 Mangal’s Capital A/c 225 Guru’s Capital A/c 225 900 1,100 1,100

Dr. Partner’s Capital Account Cr.

Particulars Vilas Mangal Guru Particulars Vilas Mangal Guru To Drawings A/c 1,000 By Balance b/d 6,000 7,000 3,400 To Interest on Drawings A/c 100 By Profit & Loss Adjustment A/c 450 225 225 To Guru’s Legal Heir’s Loan A/c 10,800 By General Reserve A/c 400 To Goodwill A/c 5,000 2,500 By Goodwill A/c 7,500 To Balance c/d 1,450 4,725 By Profit & Loss Suspense A/c 375 6,450 7,225 11,900 6,450 7,225 11,900

Balance sheet as on 1st July, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.) Capital A/c Land & Building 7,000 Vilas 1,450 Debtors 5,000 Mangal 4,725 6,175 Less: RDD 200 4,800 General Reserve 1,200 Stock 3,000 Guru’s Legal Heir’s Loan 10,800 Cash 5,000 Creditors 2,000 Profit & Loss Suspense A/c 375 20,175 20,175

SAMPLE C

ONTENTReconstitution of Partnership

(Death of Partner)

5 - 151

Working Notes :-

1) Dr. Cash/Bank A/c Cr.

Particulars Amt. (Rs.) Particulars Amt. (Rs.) To Balance b/d 6,000 By Guru’s Drawings A/c 1,000 By Balance c/d 5,000 6,000 6,000

2) Share in Goodwill Average Profit = (15000 + 13000 + 7000 + 5000) / 4 = Rs. 10,000 Goodwill = 3 years’ purchase of average profits = 3 x Rs. 10000 = Rs. 30,000 Guru’s Share in Goodwill = 1/4 x Rs. 30000 = Rs. 7,500

3) Share in Profits

Average profits of 2 years = (7000 + 5000 ) / 2

= Rs. 6,000

Estimated Profit till date of death = 3/12 x Rs. 6000

= Rs. 1,500

Share of Guru = 1/4 x Rs. 1500

= Rs. 375

4) It is assumed that remaining General Reserve is continued in the business by remaining partners.

Q7. Sheetal, Anjali, Rajendra were sharing profits and losses as 7: 5: 4. Their Balance sheet as on 31st March, 2012: (P)

Balance Sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital Furniture 17,000Sheetal 23,000 Machinery 18,000Anjali 15,000 Building 16,000Rajendra 12,000 Cash 37,000Bills Payable 4,000Creditors 8,000Loan 10,000General Reserve 16,000

88,000 88,000

Rajendra died on 30th June 2012 and the following adjustments were agreed as per deed.

1) Furniture, Machinery and Building are to be revalued at Rs. 16,700/-, Rs. 16,200/-, to Rs. 30,100.

2) Rajendra’s share is goodwill to be valued from firm’s goodwill which was valued at two times the average profit of last three years. Profits of last three years Rs. 30,000, Rs. 25,000, Rs. 20,000/-.

3) His profit upto the date of death is to be calculated on the basis of last years profit.

4) Rajendra was entitled to get a salary of Rs. 800/- per month.

5) Interest on capital at 10% be allowed.

6) Rajendra’s drawing upto date of death were Rs. 600 p.m.

Prepare:

1) Rajendra’s Capital A/c showing Amt payable to his executor.

2) Give working of share of goodwill and profit.

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

5 - 152

Solution:

Dr. Rajendra Capital A/c Cr.

Particulars Amt. (Rs.) Particulars Amt. (Rs.) To Drawings A/c 1,800 By Balance B/d 12,000 By Profit & Loss Adjustment A/c 3,000 By Salary A/c 2,400 To Executor’s Loan A/c 33,650 By Interest on Capital A/c 300 By Goodwill A/c 12,500 By General Reserve A/c 4,000 By Profit & Loss Suspense A/c 1,250 35,450 35,450

Dr. Profit & Loss Adjustment A/c Cr.

Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)To Furniture A/c 300 By Building A/c 14,100 To Machinery A/c 1,800 To Profit on Revaluation transferred Sheetal’s Capital A/c 5,250 Anjali’s Capital A/c 3,750 Rajendra’s Capital A/c 3,000 12,000 14,100 14,100

Working Notes 1) Share in Goodwill Average profits = (30000 + 25000 + 20000) / 3 = Rs. 25,000 Goodwill = 2 x Average profits = 2 x Rs. 25000 = Rs. 50,000 Rajendra’s Share = 4/16 x Rs. 50,000 = Rs. 12,500 2) Share in current profits Last year’s profit = Rs. 20,000 Estimated profit till date of death = Rs. 20000 x 3/12 = Rs. 5000 Share in profit = 4/16 x Rs. 5,000 = 1250

Q8. The Balance sheet of Mohan, Subash & Babi as on 31st December, 2011 was as under. They were sharing profits and losses in the ratio of 2: 1: 1. (P)

Balance sheet as on 31st December, 2011

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital Investments 20,000Mohan 25,000 Buildings 33,000Subash 15,000 Debtors 12,000Babi 15,000 Stock 28,000Creditors 30,000 Cash 8,000Reserve 16,000

1,01,000 1,01,000 Babi died on 1st July, 2012 and partnership deed provided that in the event of death of the partner his executor will be

entitled to be paid out.

1) Capital to the credit at the date of last balance sheet.

SAMPLE C

ONTENTReconstitution of Partnership

(Death of Partner)

5 - 153

2) Proportion of reserves.

3) Proportion of goodwill to calculated twice the average profits of last three years.

4) His proportion of profits to the date of death based on the average profits of the last three year plus 20%.

5) The net profits for last 3 years Rs. 18,000, Rs. 18,000, and Rs. 16,500.

6) Babi had withdrawn Rs. 6,000/- to the date of her death.

7) The investments were sold at par and the amount was paid off to Babi’s executor and the balance was transferred to loan A/c.

Prepare:

1. Babi’s Capital A/c only.

Solution:

Dr. Babi’s Capital A/c Cr.

Particulars Amt. (Rs.) Particulars Amt. (Rs.) To Drawings A/c 6,000 By Balance B/d 15,000 To Cash / Bank A/c 20,000 By Reserve A/c 4,000 By Goodwill A/c 8,750 To Loan A/c 4,375 By Profit & Loss Suspense A/c 2,625 30,375 30,375

Working Notes:

1) Average Profits = (18000 + 18000 + 16500)/3

= Rs. 17,500

Goodwill = 2 x Average profits

= 2 x Rs. 17500

= Rs. 35,000

Share in Goodwill = 1/4 x Rs. 35000

= Rs. 8,750

2) Average Profits = (18000 + 18000 + 16500)/3 = Rs. 17,500

Estimated profit for current year = Rs. 17,500 + Rs. 17,500 x 20% = Rs. 21,000

Estimated profits till date of death = Rs. 21000 x 6/12 = Rs. 10,500

Share in profit = 1/4 x 10,500 = Rs. 2,625

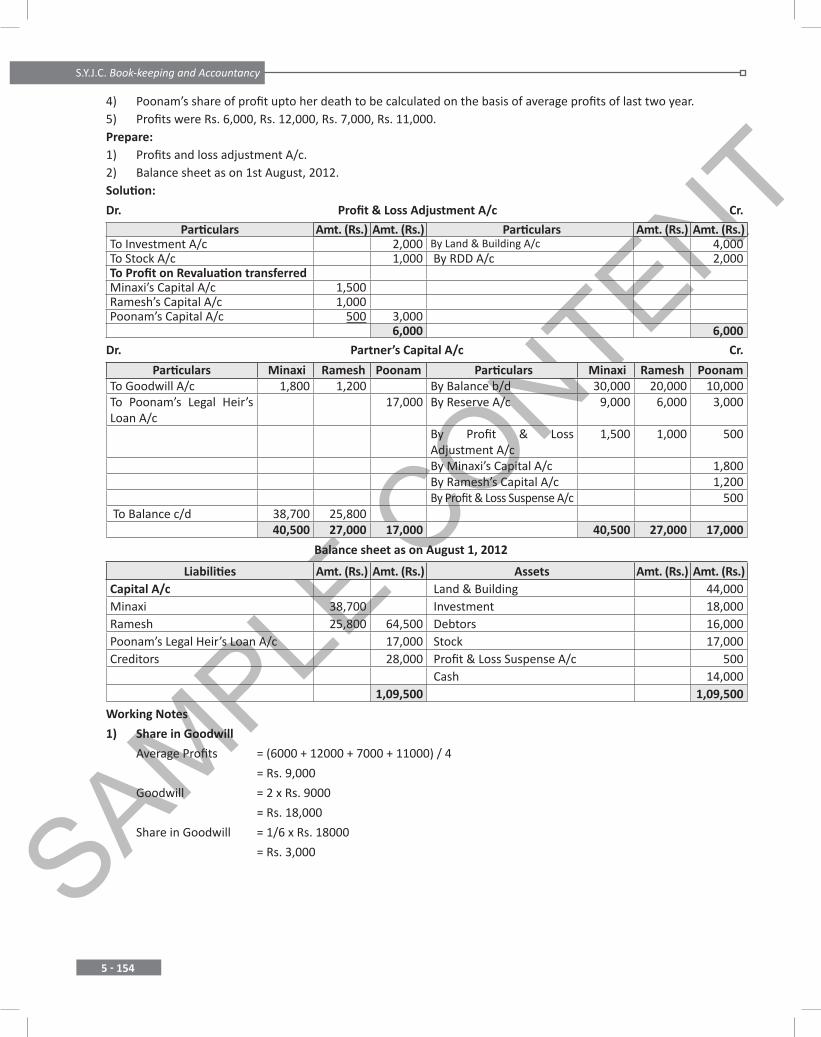

Q9. Minaxi, Ramesh and Poonam were partners sharing profits and losses in the proportion to their capitals. Their Balance sheet of the firm on 31st March, 2012 was as under: (P)

Balance Sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital Land and Building 40,000Minaxi 30,000 Investment 20,000Ramesh 20,000 Debtors 16,000Poonam 10,000 Less: R. D. D. 2,000 14,000Creditors 28,000 Stock 18,000Reserve 18,000 Cash 14,000

1,06,000 1,06,000

Poonam died on 1st August, 2012 and the following adjustments were made 1) Assets revalued as under- Land & Building Rs. 44,000, Investment Rs. 18,000, Stock Rs. 17,000. 2) All debtors were good. 3) Goodwill of the firm valued at two times the average profits of the last 4 years. No goodwill account to be shown

in the books of the firm.

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

5 - 154

4) Poonam’s share of profit upto her death to be calculated on the basis of average profits of last two year. 5) Profits were Rs. 6,000, Rs. 12,000, Rs. 7,000, Rs. 11,000. Prepare: 1) Profits and loss adjustment A/c. 2) Balance sheet as on 1st August, 2012. Solution:

Dr. Profit & Loss Adjustment A/c Cr.

Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)To Investment A/c 2,000 By Land & Building A/c 4,000 To Stock A/c 1,000 By RDD A/c 2,000 To Profit on Revaluation transferred Minaxi’s Capital A/c 1,500 Ramesh’s Capital A/c 1,000 Poonam’s Capital A/c 500 3,000 6,000 6,000

Dr. Partner’s Capital A/c Cr.

Particulars Minaxi Ramesh Poonam Particulars Minaxi Ramesh Poonam To Goodwill A/c 1,800 1,200 By Balance b/d 30,000 20,000 10,000 To Poonam’s Legal Heir’s Loan A/c

17,000 By Reserve A/c 9,000 6,000 3,000

By Profit & Loss Adjustment A/c

1,500 1,000 500

By Minaxi’s Capital A/c 1,800By Ramesh’s Capital A/c 1,200

By Profit & Loss Suspense A/c 500 To Balance c/d 38,700 25,800

40,500 27,000 17,000 40,500 27,000 17,000

Balance sheet as on August 1, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital A/c Land & Building 44,000 Minaxi 38,700 Investment 18,000 Ramesh 25,800 64,500 Debtors 16,000 Poonam’s Legal Heir’s Loan A/c 17,000 Stock 17,000 Creditors 28,000 Profit & Loss Suspense A/c 500

Cash 14,000 1,09,500 1,09,500

Working Notes

1) Share in Goodwill

Average Profits = (6000 + 12000 + 7000 + 11000) / 4

= Rs. 9,000

Goodwill = 2 x Rs. 9000

= Rs. 18,000

Share in Goodwill = 1/6 x Rs. 18000

= Rs. 3,000

SAMPLE C

ONTENTReconstitution of Partnership

(Death of Partner)

5 - 155

2) Share in Profits

Average Profits of last 2 years = (7000 + 11000) / 2

= Rs. 9,000

Estimated Profit till date of death = Rs. 9000 x 4/12

= Rs. 3,000

Share in Profit = 1/6 x Rs. 3,0 00

= Rs. 500

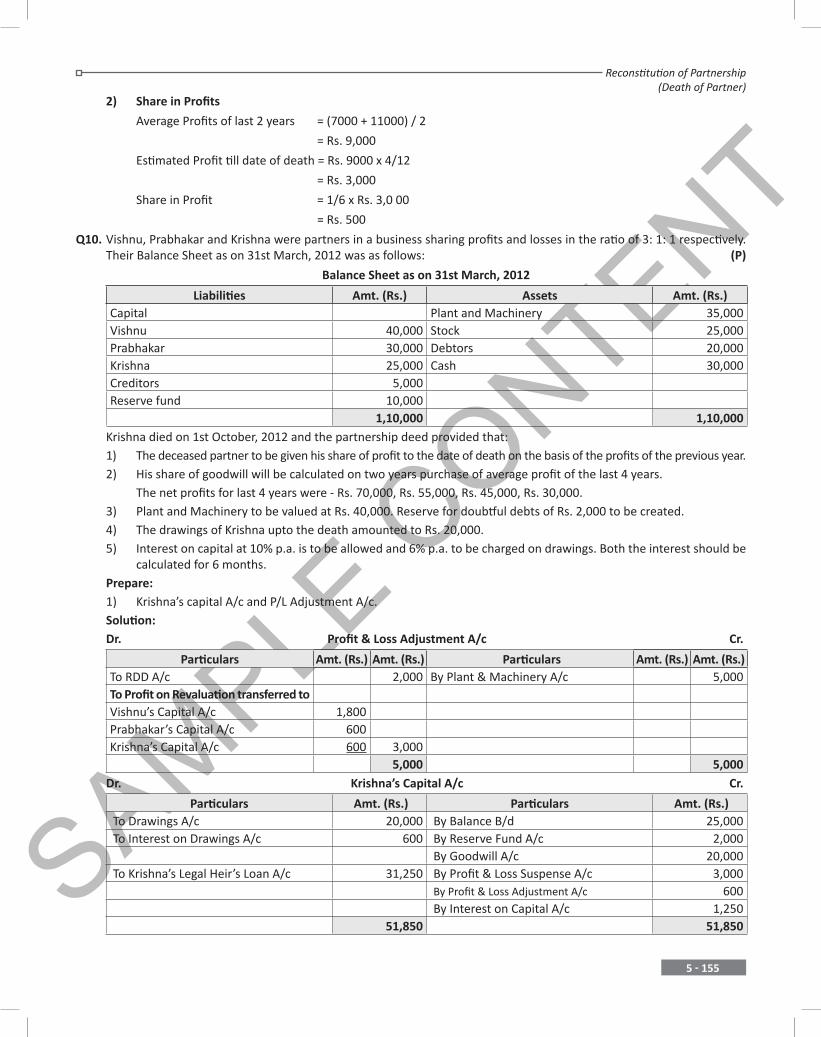

Q10. Vishnu, Prabhakar and Krishna were partners in a business sharing profits and losses in the ratio of 3: 1: 1 respectively. Their Balance Sheet as on 31st March, 2012 was as follows: (P)

Balance Sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital Plant and Machinery 35,000Vishnu 40,000 Stock 25,000Prabhakar 30,000 Debtors 20,000Krishna 25,000 Cash 30,000Creditors 5,000Reserve fund 10,000

1,10,000 1,10,000 Krishna died on 1st October, 2012 and the partnership deed provided that: 1) The deceased partner to be given his share of profit to the date of death on the basis of the profits of the previous year. 2) His share of goodwill will be calculated on two years purchase of average profit of the last 4 years. The net profits for last 4 years were - Rs. 70,000, Rs. 55,000, Rs. 45,000, Rs. 30,000. 3) Plant and Machinery to be valued at Rs. 40,000. Reserve for doubtful debts of Rs. 2,000 to be created. 4) The drawings of Krishna upto the death amounted to Rs. 20,000. 5) Interest on capital at 10% p.a. is to be allowed and 6% p.a. to be charged on drawings. Both the interest should be

calculated for 6 months. Prepare: 1) Krishna’s capital A/c and P/L Adjustment A/c. Solution: Dr. Profit & Loss Adjustment A/c Cr.

Particulars Amt. (Rs.) Amt. (Rs.) Particulars Amt. (Rs.) Amt. (Rs.)To RDD A/c 2,000 By Plant & Machinery A/c 5,000 To Profit on Revaluation transferred to Vishnu’s Capital A/c 1,800 Prabhakar’s Capital A/c 600 Krishna’s Capital A/c 600 3,000 5,000 5,000

Dr. Krishna’s Capital A/c Cr.

Particulars Amt. (Rs.) Particulars Amt. (Rs.) To Drawings A/c 20,000 By Balance B/d 25,000 To Interest on Drawings A/c 600 By Reserve Fund A/c 2,000 By Goodwill A/c 20,000 To Krishna’s Legal Heir’s Loan A/c 31,250 By Profit & Loss Suspense A/c 3,000 By Profit & Loss Adjustment A/c 600 By Interest on Capital A/c 1,250 51,850 51,850

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

5 - 156

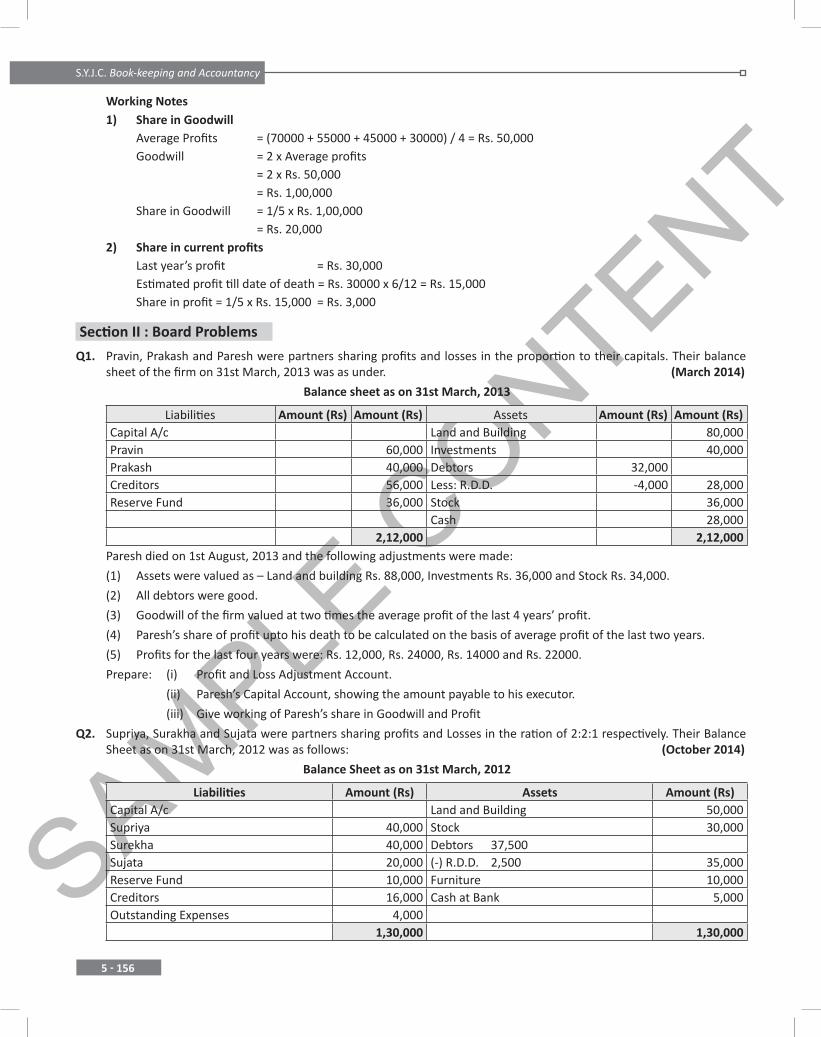

Working Notes 1) Share in Goodwill Average Profits = (70000 + 55000 + 45000 + 30000) / 4 = Rs. 50,000 Goodwill = 2 x Average profits = 2 x Rs. 50,000 = Rs. 1,00,000 Share in Goodwill = 1/5 x Rs. 1,00,000 = Rs. 20,000 2) Share in current profits Last year’s profit = Rs. 30,000 Estimated profit till date of death = Rs. 30000 x 6/12 = Rs. 15,000 Share in profit = 1/5 x Rs. 15,000 = Rs. 3,000

Section II : Board Problems

Q1. Pravin, Prakash and Paresh were partners sharing profits and losses in the proportion to their capitals. Their balance sheet of the firm on 31st March, 2013 was as under. (March 2014)

Balance sheet as on 31st March, 2013

Liabilities Amount (Rs) Amount (Rs) Assets Amount (Rs) Amount (Rs)Capital A/c Land and Building 80,000Pravin 60,000 Investments 40,000Prakash 40,000 Debtors 32,000Creditors 56,000 Less: R.D.D. -4,000 28,000Reserve Fund 36,000 Stock 36,000

Cash 28,0002,12,000 2,12,000

Paresh died on 1st August, 2013 and the following adjustments were made:

(1) Assets were valued as – Land and building Rs. 88,000, Investments Rs. 36,000 and Stock Rs. 34,000.

(2) All debtors were good.

(3) Goodwill of the firm valued at two times the average profit of the last 4 years’ profit.

(4) Paresh’s share of profit upto his death to be calculated on the basis of average profit of the last two years.

(5) Profits for the last four years were: Rs. 12,000, Rs. 24000, Rs. 14000 and Rs. 22000.

Prepare: (i) Profit and Loss Adjustment Account.

(ii) Paresh’s Capital Account, showing the amount payable to his executor.

(iii) Give working of Paresh’s share in Goodwill and Profit

Q2. Supriya, Surakha and Sujata were partners sharing profits and Losses in the ration of 2:2:1 respectively. Their Balance Sheet as on 31st March, 2012 was as follows: (October 2014)

Balance Sheet as on 31st March, 2012

Liabilities Amount (Rs) Assets Amount (Rs)Capital A/c Land and Building 50,000Supriya 40,000 Stock 30,000Surekha 40,000 Debtors 37,500Sujata 20,000 (-) R.D.D. 2,500 35,000Reserve Fund 10,000 Furniture 10,000Creditors 16,000 Cash at Bank 5,000Outstanding Expenses 4,000

1,30,000 1,30,000

SAMPLE C

ONTENTReconstitution of Partnership

(Death of Partner)

5 - 157

Sujata died on 1st July, 2012 and the adjustments were agreed to as per the deed as follows:

(1) Land and Building to be valued at Rs. 60,000 and all debtors were good.

(2) Stock to be depreciated by 10%.

(3) The drawing of Sujata up to the date of her death amounted to Rs. 2,000.

(4) Interest on capital was to be allowed at 10% p.a.

(5) The deceased partner’s share of goodwill is to be valued at 2 years’ purchase of average profit of last 3 years.

The profits were:

2009 – 10 = Rs. 15,000

2010 – 11 = Rs. 17,000

2011 – 12 = Rs. 13,000

(6) The deceased partner’s share of profit up to the date of her death should be based on average profit of the last two years.

You are required to prepare:

(a) Profit and Loss Adjustment Account.

(b) Sujata’s Capital Account showing the balance payable to her Executor’s Loan Account.

(c) Working notes for calculation of (a) Goodwill and (b) Profit till the date of Sujata’s death

Section III – Homework Problems

Q1. Balance sheet as on 31st March, 2012Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)

Capital A/c Land & Building 59,000 Sheetal 20,000 Machinery 26,000 Ashish 20,000 Vehicle 12,000 Neha 20,000 60,000 Stock 5,000 Sundry Creditors 65,000 Debtors 20,000 Bills Payable 13,000 Less: RDD 1,000 19,000

Cash/Bank 2,000 Profit & Loss A/c 15,000

1,38,000 1,38,000 Partners were sharing profits & losses equally. Neha passed away on 1st July, 2012. 1) Goodwill to be calculated as 3 years’ purchase of past 3 years’ average profits which were as follows Rs. 10,000,

Rs. 12,000 and Rs. 14,000. Goodwill to be raised only for Neha’s share 2) Share in profits to be calculated as average of last 3 years’ profits plus 20%. 3) Interest on Neha’s capital to be provided at 10%pa. 4) Neha had made drawings of Rs. 5,000 till date of death. 5) Interest on drawings is Rs. 100 for the period on Neha’s drawings. Prepare 1) Neha’s Capital A/c 2) Working of Goodwill and Share in Profits. Answer: Neha’s Legal heir’s loan A/c: Rs. 23,600/- Goodwill of the firm: Rs. 36,000/-

Share in Profit : Rs. 1,200/-

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

5 - 158

Q2. Balance sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital A/c Factory 75,000 Heena 50,000 Furniture 35,000 Sheena 64,000 Investment 25,000 Leena 45,000 1,59,000 Stock 55,000 Debtors 45,000 General Reserve 60,000 Less: RDD 4,000 41,000 Sundry Creditors 20,000 Cash / Bank 8,000 2,39,000 2,39,000

Partners were sharing profits & losses in the ratio 2:1:3. Leena expired on 1st October, 2012. 1) Goodwill of the firm to be raised to Rs. 60,000. 2) Share in profits to be computed as average of last 2 years’ profits which were Rs. 23,000 and Rs. 57,000. 3) Goodwill not to appear in the books. 4) Rent of Rs. 2,000 was unpaid. 5) Factory to be appreciated by 20%. 6) Investment to be written down to market value of Rs. 22,000. 7) Interest on Leena’s capital to be provided for at 5%. Prepare 1) Profit & Loss Adjustment A/c. 2) Partners’ Capital A/c. Answer: Profit on revaluation: Rs. 10,000 Leena’s Legal heir’s loan A/c: Rs. 1,21,125

Q3. Balance sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital A/c Land & Building 50,000 Iyer 60,000 Vehicle 25,000 Murthy 50,000 Investment 36,000 Shetty 40,000 1,50,000 Stock 33,500 Reserve Fund 24,000 Debtors 27,500 Sundry Creditors 26,000 Cash/Bank 28,000 2,00,000 2,00,000

Partners were sharing profits & losses in the ratio 3:2:1. Shetty died on 1st September, 2012. 1) Goodwill to be raised to Shetty’s share of Rs. 7,500. 2) Share in profits to be computed by increasing last year’s profit of Rs. 40,000 by 50%. 3) Sundry Creditors of Rs. 1,500 to be written off. 4) Investments to be revised upwards by Rs. 14,000. 5) Shetty made drawings of Rs. 10,000 till date of his death. Interest to be charged for the period at 10%pa. Prepare 1) Profit & Loss Adjustment A/c. 2) Shetty’s Capital A/c.

Answer: Shetty’s Legal heir’s loan A/c: Rs. 47,834 Profit & Loss Adjustment A/c: Rs. 15,500 (Profit)

SAMPLE C

ONTENTReconstitution of Partnership

(Death of Partner)

5 - 159

Q4. Balance sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital A/c Goodwill 35,000 Axar 25,000 Land & Building 57,000 Virat 35,000 Machinery 10,000 Gautam 25,000 85,000 Stock 20,000 General Reserve 40,000 Debtors 25,000 Sundry Creditors 25,000 Less: RDD 2,000 23,000 Unpaid Rent 1,000 Cash/Bank 6,000 1,51,000 1,51,000

Partners were sharing profits & losses in the ratio 1:2:1. Gautam died on July 1, 2012. 1) Goodwill to be raised by Rs. 20,000, but only Gautam’s share to be raised. 2) Share in Profits to be calculated by taking into account last 2 years’ profits which were Rs. 30,000 and Rs. 40,000. 3) RDD to be maintained at 10% of debtors. 4) Land & Building and Machinery were to be appreciated by 10% and 15% respectively. 5) Stock of Rs. 2,000 to be written off. 6) Gautam had made drawings of Rs. 5,000 till date of death. Prepare 1) Profit & Loss Adjustment A/c. 2) Partners’ Capital A/c. 3) Balance sheet. Answer: Profit on revaluation: Rs. 4,700 Gautam Legal heir’s loan A/c: Rs. 38,363

Balance Sheet total: Rs. 1,57,888

Q5. Balance sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.) Capital A/c Land & Building 26,000 Neelima 15,000 Furniture 17,000 Subhash 21,000 Vehicle 13,000 Saurabh 31,000 67,000 Stock 11,000 General Reserve 12,000 Debtors 22,500 Sundry Creditors 16,000 Less: RDD 1,500 21,000 Bills Payable 4,000 Cash/Bank 11,000 99,000 99,000

Partners were sharing profits & losses in the ratio 6:3:1. Saurabh expired on 1st June, 2012. 1) Goodwill of the firm to be raised to Rs. 40,000. 2) Share in Profit to be calculated by assuming last year’s profit of Rs. 12,000 plus a raise of 25%. 3) Goodwill to remain in the books of the firm. 4) All debtors were considered good. 5) Land & Building to be revalued upwards to Rs. 50,000. 6) Stock to be written off of Rs. 2,000. Prepare 1) Profit & Loss Adjustment A/c 2) Partners’ Capital A/c 3) Balance sheet

Answer: Profit & Loss Adjustment A/c: Rs. 23,500 (Profit) Saurabh’s Legal heir’s loan A/c: Rs. 38,800

Balance Sheet total: Rs. 1,62,750

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

5 - 160

Q6. Balance sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital A/c Building 1,44,000 Shah 1,00,000 Furniture 26,000 Vora 1,50,000 Investment 98,000 Thakker 80,000 3,30,000 Stock 54,000 Debtors 66,000 Sundry Creditors 60,000 Less: RDD 6,000 60,000 Bills Payable 23,000 Cash / Bank 4,000 Profit & Loss A/c 27,000 4,13,000 4,13,000

Partners were sharing profits & losses in the ratio 1:1:1. Thakker died on 1st July, 2012. 1) Goodwill to be calculated as 2 years’ purchase of past 3 years’ average profits which were as follows: Rs. 80,000, Rs. 90,000 and Rs. 1,20,000. 2) Share in profits to be computed as average of 3 years’ profits plus 40%. 3) R.D.D. to be written back to 5% of debtors. 4) Drawings by Thakker till date of his death were Rs. 20,000. Interest on drawings to be charged at 10%pa. 5) Furniture to be depreciated by 10%. 6) Stock to be revised upwards by Rs. 26,000. Prepare 1) Thakker’s Capital A/c 2) Working of Goodwill and Share in Profits.

Answer: Profit & Loss Adjustment A/c: Rs. 26,100 (Profit) Thakker’s Legal heir’s loan A/c: Rs. 1,34,923

Q7. Balance sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital A/c Land & Building 56,000 Amar 11,000 Furniture 24,000 Akbar 22,000 Vehicle 16,000 Anthony 44,000 77,000 Stock 10,000 Reserve Fund 28,000 Debtors 6,000 Sundry Creditors 12,000 Cash / Bank 5,000 1,17,000 1,17,000

Partners were sharing profits & losses in the ratio of their capitals. Anthony passed away on 1st September, 2012. 1) Goodwill to be calculated as 3 years’ purchase of past 4 years’ average profits which were as follows Rs. 3,000,

Rs. 5,000, Rs. 6,000, Rs. 7,500. 2) Share in profits to be based on last year’s profit plus 33 1/3%. 3) Goodwill to not appear in the books of the firm. 4) R.D.D. to be provided for at 15% of debtors. 5) Sundry Creditors were undervalued by Rs. 8,000. 6) Depreciate Furniture by Rs. 4,000 and Vehicle by Rs. 2,000. 7) Anthony had made drawings of Rs. 4,000 till date of death. Prepare 1) Profit & Loss Adjustment A/c. 2) Partners’ Capital A/c. 3) Balance sheet.

Answer: Loss on revaluation: Rs. 14,900 Anthony’s Legal heir’s loan A/c: Rs. 59,081

Balance Sheet total: Rs. 1,08,481

SAMPLE C

ONTENTReconstitution of Partnership

(Death of Partner)

5 - 161

Q8. Balance sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital A/c Factory 80,000 Pam 40,000 Machinery 40,000 Sam 20,000 Investment 20,000 Cam 40,000 1,00,000 Stock 10,000 Reserve Fund 40,000 Debtors 20,000 Sundry Creditors 25,000 Cash / Bank 10,000 Bills Payable 15,000 1,80,000 1,80,000

Partners were sharing profits & losses in the ratio 1:2:1. Cam died on 1st December, 2012. 1) Goodwill raised to Cam’s share of Rs. 25,000. Goodwill to be written off. 2) Share in profits to be based on last year’s profit of Rs. 1,00,000. 3) Bills Payable of Rs. 5,000 to be written off. 4) Machinery was undervalued by 20%. 5) Stock of Rs. 2,000 to be written off. 6) Interest on Cam’s capital to be provided for at 10% where as on drawings at 5%. 7) Cam had made drawings till date of death of Rs. 3,000. Prepare 1) Profit & Loss Adjustment A/c 2) Cam’s Capital A/c Answer: Profit on revaluation: Rs. 13,000 Cam’s Legal heir’s loan A/c: Rs. 94,484/-

Q9. Balance sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital A/c Land & Building 60,000 Kishor 65,000 Factory 50,000 Prakash 75,000 Investment 45,000 Deepak 25,000 1,65,000 Stock 35,000 Profit & Loss A/c 36,000 Debtors 25,000 Sundry Creditors 24,000 Cash / Bank 10,000 2,25,000 2,25,000

Partners were sharing profits & losses in the ratio 3:4:5. Deepak died on 1st July, 2012. 1) Goodwill to be calculated as 2 years’ purchase of past 4 years’ average profits which were as follows Rs. 27,000,

Rs. 35,000, Rs. 15,000 and Rs. 55,000. 2) Share in profit to be average of last 3 years’ profits. 3) Goodwill to be written back. 4) Factory to be depreciated by 10%. 5) Deepak had made drawings of Rs. 5,000 till date of his death. 6) RDD to be maintained at 10%. Prepare 1) Profit & Loss Adjustment A/c 2) Partners’ Capital A/c 3) Balance sheet Answer: Profit & Loss Adjustment A/c: Rs. 7,500 Deepak’s Legal heir’s loan A/c: Rs. 63,021

Balance Sheet total: Rs. 2,16,146

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

5 - 162

Q10. Balance sheet as on 31st March, 2012

Liabilities Amt. (Rs.) Amt. (Rs.) Assets Amt. (Rs.) Amt. (Rs.)Capital A/c Factory 3,36,000 Kulkarni 1,50,000 Machinery 2,39,000 Nene 2,00,000 Vehicle 35,000 Gokhale 3,00,000 6,50,000 Stock 1,58,000 General Reserve 1,30,000 Debtors 2,25,400 Sundry Creditors 2,00,500 Less: RDD 5,400 2,20,000 Bills Payable 10,500 Cash/Bank 3,000 9,91,000 9,91,000

Partners were sharing profits & losses in the ratio of their capitals. Gokhale passed away on 1st August, 2012. 1) Goodwill to be calculated as 3 years’ purchase of past 3 years’ average profits which were as follows Rs. 1,00,000,

Rs. 1,50,000, Rs. 2,50,000. 2) Share in profits is assumed as average of last 2 years’ profits. 3) Goodwill to be raised to Gokhale’s share. 4) R.D.D. to be raised to 10% of debtors. 5) Machinery to be depreciated by 10%. Factory to be revised upwards to Rs. 4,00,000. 6) Interest on Gokhale’s capital to be provided at 10%pa. Prepare 1) Profit & Loss Adjustment A/c 2) Gokhale’s Capital A/c

Answer: Profit & Loss Adjustment A/c: Rs. 22,960 (Profit) Gokhale’s Legal heir’s loan A/c: Rs. 6,42,135

Section IV : Objective Type Questions

Q.1. Objective Type Questions:(A) Answer one sentence only.1. What is gain ratio or benefit ratio?Ans. Profit of the deceased partner is distributed among the remaining partners in their old profit sharing ratio or as per the

new profit sharing ratio; such extra profit added to the continuing partners is known as Gain ratio.2. How is gain ratio calculated?Ans. Gain ratio is calculated in the following manner: Gain ratio= New ratio- old ratio3. When is gain ratio required to be calculated?Ans. Gain ratio is calculated when any partner dies in the old or existing partnership firm.4. How would you treat general reserve on death of a partner?Ans. The amount is distributed among all partners in their profit sharing ratio.5. How much amount due to deceased partner is calculated?Ans. The amount due to deceased partner is calculated till the date the deceased partner renders services to the business

i.e. till the date of death.6. How is amount due to deceased partner settled?Ans. The amount due to the deceased partner is transferred to his legal heir or representative’s loan a/c or executor after

completing all legal formalities.7. How is the share of deceased partner in accrued profit calculated?Ans. The share of deceased partner is calculated on the assumed basis of average profit of previous years and credited to

deceased partners capital a/c.8. How is a debit balance of profit & loss account dealt with on death of a partner?Ans. On the death of a partner, debit balance of Profit & loss a/c is transferred to partners capital or current a/c in their profit

sharing ratio.

SAMPLE C

ONTENTReconstitution of Partnership

(Death of Partner)

5 - 163

(B) Write a word or a term or a phrase which can substitute each of the following statements.

1. The account which shows revaluation of assets and liabilities. Revaluation A/c or profit and loss adjustment A/c

2. Excess of credit side over debit side of revaluation account. Profit on Revaluation3. The method under which payment is made to retiring partner in installment. Installment method4. Excess of proportionate at capital over actual capital. Deficit5. The account to which deceased partners capital balance is transferred. Deceased Partner’s Executors

Loan Account6. The partner who died. Deceased Partner7. A person who represent the deceased partner. Legal heir or executor(C) Fill in the blanks with appropriate alternative given in the brackets.

1. Gain ratio is calculated on _______________. (a) admission of a partner (b) retirement of a partner (c) death of a partner (d) retirement or death of a partner

retirement or death of a partner

2. Gain ratio is the ratio in which _______________. (a) the old partner gains on admission of a new partner (b) the goodwill of a new partner on admission is credited to old partners (c) the continuing partner’s benefits on retirement or death of a partner (d) none of the above

the continuing partner’s benefits on retirement or death of a partner

3. Share of profit of a deceased partner till the date of death is ___________. (a) debited to P/L Adjustment A/c (b) credited to P/L Adjustment A/c (c) debited to P/L Suspense A/c (d) credited to P/L Suspense A/c

debited to P/L Suspense A/c

4. An amount received from the Insurance Company against the joint life policy is _________. (a) debited to deceased partner (b) credited to deceased partner (c) credited to continuing partners capital a/c (d) credited to all partners capital a/c in their profit sharing ratio

credited to all partners capital a/c in their profit sharing ratio

5. M.N.S. are partners in a firm having joint life policy of Rs. 10,00,000 on which premium has been paid by a firm. M dies and his legal representatives want the whole amount of the policy where as N & S want to distribute the amount among all the partners.

(a) M’s representatives and correct (b) N & S are correct (c) All are wrong (d) Insurance company will decide

N & S are correct

6. Interest on drawing due from deceased partner till the date of death is __________ to his capital a/c (a) debited (b) credited (c) none of the above

Debited

(D) State whether the following statements are TRUE/FALSE

1. Deceased partner is entitled to his share of goodwill. True2. Deceased partner is not entitled to his share of general reserve. False3. The capital account of a deceased partner always shows a debit balance.

4. An amount due to a deceased partner is transferred to his executor’s loan A/c.

False

True5. If goodwill is written off deceased partner’s capital account is debited. False6. Death of partner is like a compulsory retirement. True7. Total amount due to deceased partner is paid in cash to executor immediately after his death. False8. On the death of a partner, his share in the goodwill is divided equally among continuing partners. False9. Deceased Partner’s share in profit upto the date of his death will be debited to his capital A/c. False