Embed Size (px)

Citation preview

© Target Publications Pvt. Ltd. No part of this book may be reproduced or transmitted in any form or by any means, C.D. ROM/Audio Video Cassettes or electronic, mechanical

including photocopying; recording or by any information storage and retrieval system without permission in writing from the Publisher.

BOOK-KEEPING & ACCOUNTANCY

SOLUTIONS STD. XII

Printed at: Repro Knowledgecast Ltd., Mumbai

10310_10540_JUP

Written as per the revised syllabus prescribed by the Maharashtra State Board

of Secondary and Higher Secondary Education, Pune.

P.O. No. 22956

Salient Features

• Solutions to all the Textual and Practice Problems

• Accurate solutions with precise formats

• Working Notes to simplify the problems

• Systematic presentation to alleviate the learning process

• Self evaluative in nature

Preface

"Std. XII Commerce: Book‐Keeping and Accountancy Solutions" has been designed to complement the “Std. XII

Commerce: Book‐Keeping and Accountancy” book. This book will enable the student to verify the solutions and

solve the questions independently. The book includes accurate solutions to all the Textual and Practice Problems with precise formats. Working

Notes have been provided to simplify the various complicated adjustments in the problems. The systematic and

consistent presentation of solutions alleviates the learning process for the student. We are sure, this study material will turn out to be a powerful resource for the students and facilitate them in

understanding the concepts of this subject in the most lucid way. The journey to create a book is strewn with triumphs, failures and near misses. If you think we've nearly missed

something or want to applaud us for our triumphs, we'd love to hear from you.

Please write to us at: [email protected]

Best of luck to all the aspirants! Yours faithfully,

Publisher

Sr. No. Chapter Page No.

2. Partnership Final Accounts 1

3. Reconstitution of Partnership (Admission of Partner) 82

4. Reconstitution of Partnership (Retirement of Partner) 137

5. Reconstitution of Partnership (Death of Partner) 169

6. Dissolution of Partnership Firm 191

7. Accounts of ‘Not for Profit’ Concerns 248

8. Single Entry System 286

9. Bill of Exchange (Trade Bill) 317

10. Company Accounts Part I (Accounting for Shares) 386

11. Company Accounts Part II (Accounting for Debentures) 419

12. Analysis of Financial Statements 440

Note: All Textual questions are represented by * mark.

1

Chapter 02: Partnership Final Accounts

*Sol. Q.1.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2009 Dr. Cr.

Particulars Amount

` Amount

`Particulars

Amount

` Amount

`To Opening Stock 18,000 By Sales 85,000

To Purchases 46,700 By Closing Stock 31,000

To Wages 9,900

Add: Outstanding Wages 1,400 11,300

To Carriage 3,200 To Gross Profit c/d 36,800

1,16,000 1,16,000

Profit and Loss Account for the year ended 31st Mar, 2009 Dr. Cr.

Particulars Amount

` Amount

`Particulars

Amount

` Amount

`To Reserve for Bad & By Gross Profit b/d 36,800

Doubtful Debts By Commission 1,800

Old Bad Debts 400 Add: Outstanding 1,200 3,000

Add: New Bad Debts 1,500

Add: New R.D.D.

Less: Old R.D.D. – 1,900

To Commission 4,600

To Postage and Telegram 3,600

To Insurance 1,200

Less: Prepaid Insurance 500 700

To Depreciation on Plant and

Machinery 4,070

To Salaries 10,500

Add: Outstanding Salaries 800 11,300 To Net Profit c/d

Ajay 6,815

Vijay 6,815 13,630 39,800 39,800

Partner’s Capital Account Dr. Cr.

Particulars Ajay

` Vijay

`Particulars

Ajay

` Vijay

` By Balance b/d 60,000 35,000

To Balance c/d 66,815 41,815 By Profit & Loss A/c 6,815 6,815 66,815 41,815 66,815 41,815

Textual Problems

Partnership Final Accounts 02

2

2

Std. XII : Commerce

Balance Sheet as on 31st Mar, 2009

Liabilities Amount

` Amount

`Assets

Amount `

Amount`

Capital Sundry Debtors 28,000 Ajay 66,815 Less: Bad debts 1,500 26,500

Vijay 41,815 1,08,630 Bills Receivable 5,000

Outstanding Expenses Investments 13,500Wages 1,400 Prepaid Insurance 500Salaries 800 2,200 Plant & Machinery 40,700

Sundry Creditors 25,000 Less: Depreciation (10%) 4,070 36,630

Bills Payable 6,000 Furniture 18,000 Cash in Hand 2,500 Prepaid Rent 7,000 Commission Receivable 1,200 Closing Stock 31,000 1,41,830 1,41,830

*Sol. Q.2.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2010 Dr. Cr.

Particulars Amount

` Amount

`Particulars

Amount `

Amount`

To Opening Stock 20,000 By Sales 70,000To Purchases 30,000 By Closing Stock 35,000Add: Unrecorded Purchases 4,000 34,000

To Wages 5,000 Add: Outstanding Wages 2,000 7,000

To Power and Fuel 3,000 To Gross Profit c/d 41,000 1,05,000 1,05,000

Profit and Loss Account for the year ended 31st Mar, 2010

Dr. Cr.

Particulars Amount

` Amount

`Particulars

Amount `

Amount`

To Reserve for Bad & By Gross Profit b/d 41,000Doubtful Debts By Discount 5,000Old Bad Debts Add: New Bad Debts 2,000 Add: New R.D.D. 500 Less: Old R.D.D. – 2,500

To Depreciation Land and Building 1,500 Machinery 2,500 4,000

To Salaries 10,000 Add: Outstanding Salaries 1,000 11,000

To Advertisement 6,000 Less: Prepaid (1 year) 3,000 3,000

To Insurance 2,000 To Rent 10,000 To Interest on Capital

Sanjay 2,000

Sudhir 1,500 3,500

3

Chapter 02: Partnership Final Accounts

To Net Profit c/d

Sanjay 6,000

Sudhir 4,000 10,000

46,000 46,000

Partner’s Capital Account

Dr. Cr.

Particulars Sanjay

`

Sudhir

`Particulars

Sanjay

`

Sudhir

`

To Drawings A/c 2,000 3,000 By Balance b/d 40,000 30,000

By Interest on Capital A/c 2,000 1,500

To Balance c/d 46,000 32,500 By Profit & Loss A/c 6,000 4,000

48,000 35,500 48,000 35,500

Balance Sheet as on 31st Mar, 2010

Liabilities Amount

`

Amount

`Assets

Amount

`

Amount

`

Capital Debtors 12,000

Sanjay 46,000 Less: Bad Debts 2,000

Sudhir 32,500 78,500 10,000

Outstanding Expenses: Less: R.D.D. (5%) 500 9,500

Wages 2,000 Land and Building 30,000

Salaries 1,000 3,000 Less: Depreciation (5%) 1,500 28,500

Sundry Creditors 21,000 Plant & Machinery 25,000

Add: Unrecorded Purchases 4,000 25,000 Less: Depreciation (10%) 2,500 22,500

Bills Payable 20,000 Furniture 16,000

Outstanding Rent 1,500 Prepaid Advertisement 3,000

Bills Receivable 8,000

Cash in Hand 5,500

Closing Stock 35,000

1,28,000 1,28,000 *Sol. Q.3.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2011

Dr. Cr.

Particulars Amount

`

Amount

` Particulars

Amount

`

Amount

`

To Opening Stock 32,000 By Sales 1,93,500

To Purchases 64,000 Less: Return Inward 3,500 1,90,000

Less: Return Outward 2,500 61,500 By Goods withdrawn by

To Carriage 1,500 Roshan 750

To Wages and Salaries 35,000

Less: Advance (Prepaid) 3,000 32,000 By Closing Stock 25,000 To Gross Profit c/d 88,750 2,15,750 2,15,750

4

4

Std. XII : Commerce

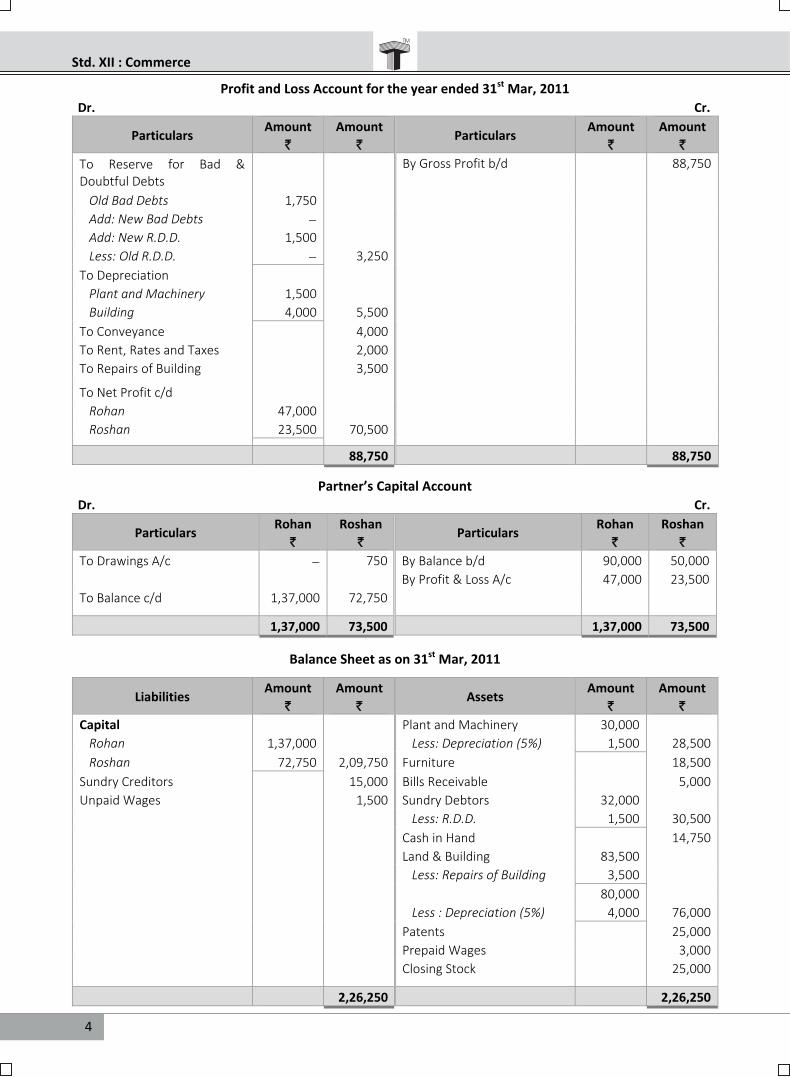

Profit and Loss Account for the year ended 31st Mar, 2011

Dr. Cr.

Particulars Amount

`

Amount

` Particulars

Amount

`

Amount

`

To Reserve for Bad & Doubtful Debts

By Gross Profit b/d 88,750

Old Bad Debts 1,750

Add: New Bad Debts

Add: New R.D.D. 1,500

Less: Old R.D.D. 3,250

To Depreciation

Plant and Machinery 1,500

Building 4,000 5,500

To Conveyance 4,000

To Rent, Rates and Taxes 2,000

To Repairs of Building 3,500 To Net Profit c/d

Rohan 47,000

Roshan 23,500 70,500 88,750 88,750

Partner’s Capital Account

Dr. Cr.

Particulars Rohan

`

Roshan

` Particulars

Rohan

`

Roshan

`

To Drawings A/c 750 By Balance b/d 90,000 50,000

By Profit & Loss A/c 47,000 23,500

To Balance c/d 1,37,000 72,750 1,37,000 73,500 1,37,000 73,500

Balance Sheet as on 31st Mar, 2011

Liabilities Amount

`

Amount

` Assets

Amount

`

Amount

`

Capital Plant and Machinery 30,000

Rohan 1,37,000 Less: Depreciation (5%) 1,500 28,500

Roshan 72,750 2,09,750 Furniture 18,500

Sundry Creditors 15,000 Bills Receivable 5,000

Unpaid Wages 1,500 Sundry Debtors 32,000

Less: R.D.D. 1,500 30,500

Cash in Hand 14,750

Land & Building 83,500

Less: Repairs of Building 3,500

80,000

Less : Depreciation (5%) 4,000 76,000

Patents 25,000

Prepaid Wages 3,000

Closing Stock 25,000 2,26,250 2,26,250

5

Chapter 02: Partnership Final Accounts

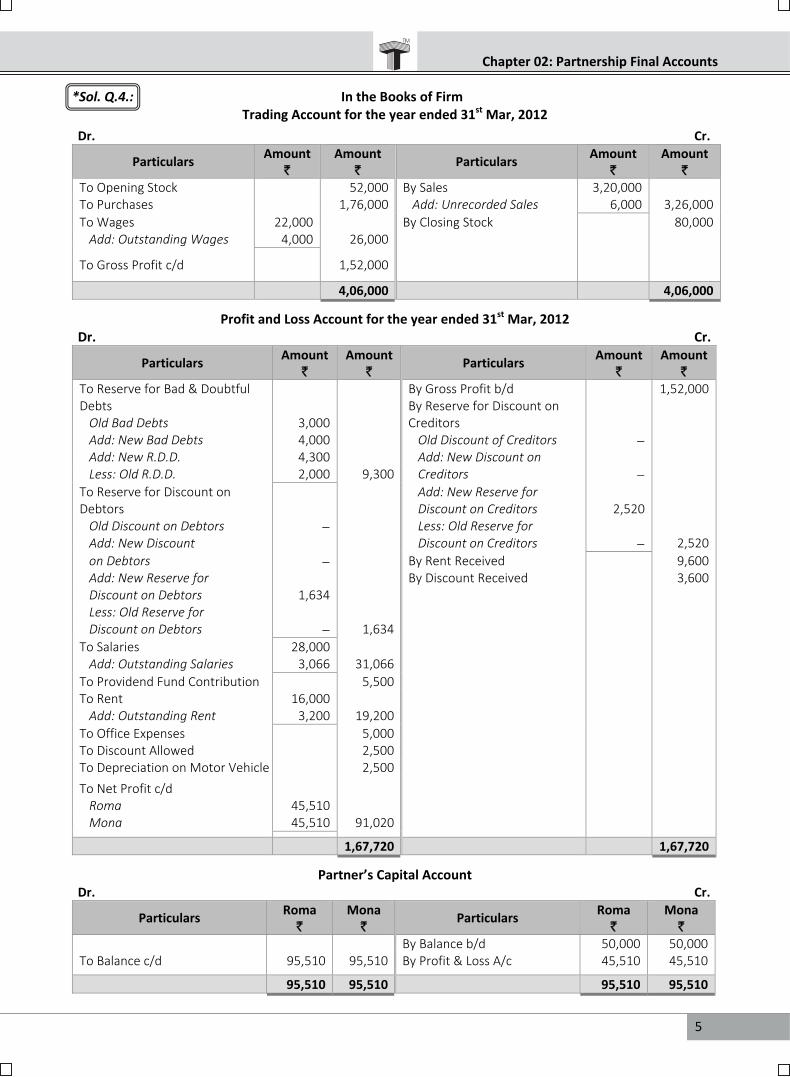

*Sol. Q.4.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2012

Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount `

Amount`

To Opening Stock 52,000 By Sales 3,20,000 To Purchases 1,76,000 Add: Unrecorded Sales 6,000 3,26,000

To Wages 22,000 By Closing Stock 80,000Add: Outstanding Wages 4,000 26,000

To Gross Profit c/d 1,52,000 4,06,000 4,06,000

Profit and Loss Account for the year ended 31st Mar, 2012 Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount `

Amount`

To Reserve for Bad & Doubtful By Gross Profit b/d 1,52,000Debts By Reserve for Discount on Old Bad Debts 3,000 Creditors Add: New Bad Debts 4,000 Old Discount of Creditors Add: New R.D.D. 4,300 Add: New Discount on Less: Old R.D.D. 2,000 9,300 Creditors

To Reserve for Discount on Add: New Reserve for Debtors Discount on Creditors 2,520 Old Discount on Debtors Less: Old Reserve for Add: New Discount Discount on Creditors 2,520

on Debtors By Rent Received 9,600Add: New Reserve for By Discount Received 3,600Discount on Debtors 1,634 Less: Old Reserve for Discount on Debtors 1,634

To Salaries 28,000 Add: Outstanding Salaries 3,066 31,066

To Providend Fund Contribution 5,500 To Rent 16,000 Add: Outstanding Rent 3,200 19,200

To Office Expenses 5,000 To Discount Allowed 2,500 To Depreciation on Motor Vehicle 2,500 To Net Profit c/d Roma 45,510 Mona 45,510 91,020

1,67,720 1,67,720

Partner’s Capital Account Dr. Cr.

Particulars Roma

` Mona

` Particulars

Roma `

Mona`

By Balance b/d 50,000 50,000To Balance c/d 95,510 95,510 By Profit & Loss A/c 45,510 45,510 95,510 95,510 95,510 95,510

6

6

Std. XII : Commerce

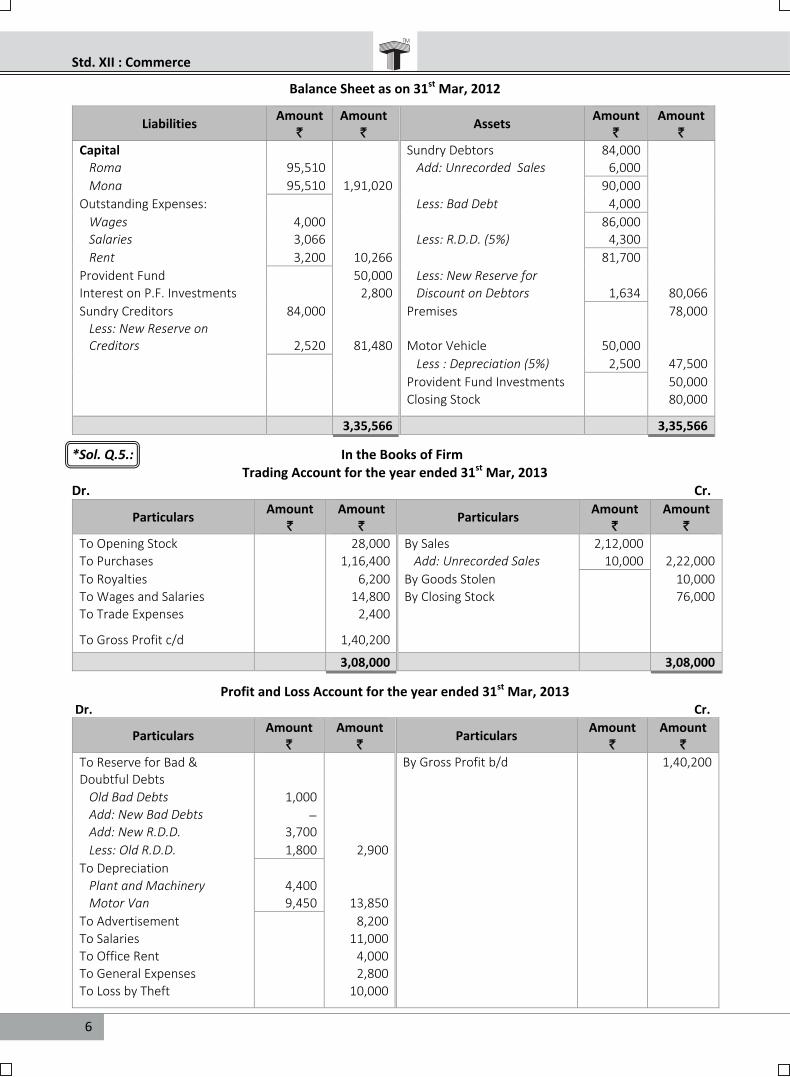

Balance Sheet as on 31st Mar, 2012

Liabilities Amount

` Amount

` Assets

Amount `

Amount `

Capital Sundry Debtors 84,000

Roma 95,510 Add: Unrecorded Sales 6,000

Mona 95,510 1,91,020 90,000

Outstanding Expenses: Less: Bad Debt 4,000

Wages 4,000 86,000 Salaries 3,066 Less: R.D.D. (5%) 4,300

Rent 3,200 10,266 81,700

Provident Fund 50,000 Less: New Reserve for

Interest on P.F. Investments 2,800 Discount on Debtors 1,634 80,066

Sundry Creditors 84,000 Premises 78,000Less: New Reserve on Creditors 2,520 81,480 Motor Vehicle 50,000

Less : Depreciation (5%) 2,500 47,500

Provident Fund Investments 50,000

Closing Stock 80,000 3,35,566 3,35,566

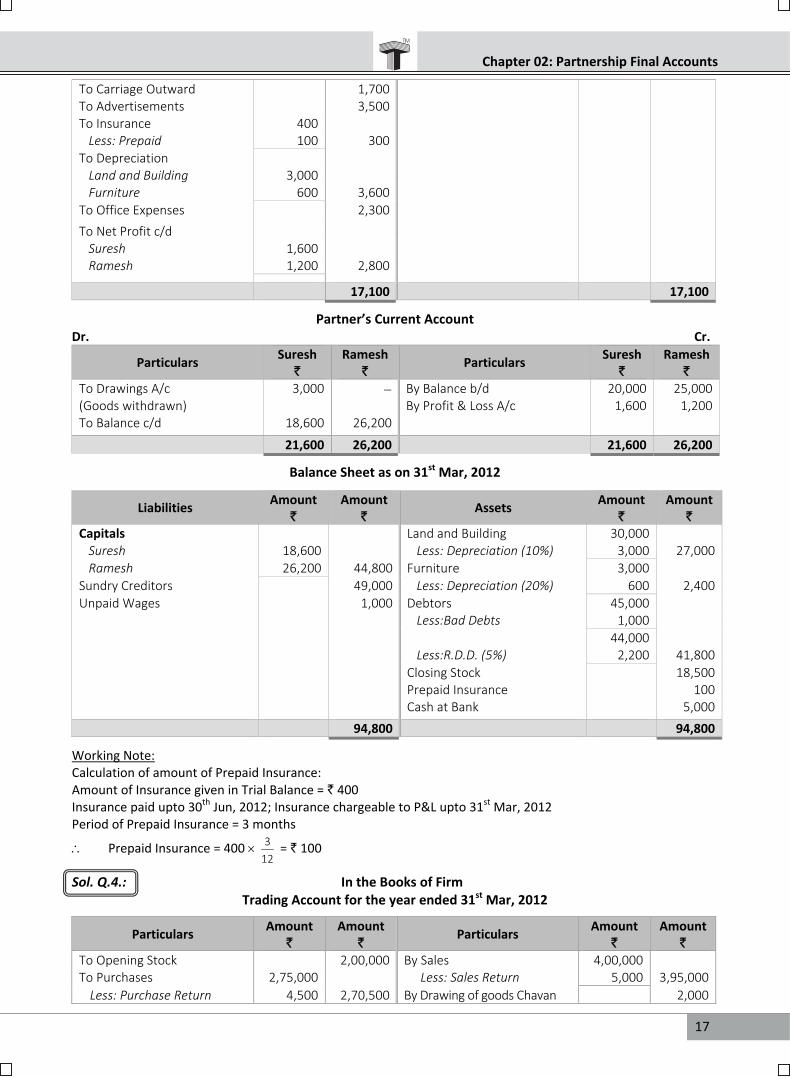

*Sol. Q.5.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2013 Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount `

Amount `

To Opening Stock 28,000 By Sales 2,12,000

To Purchases 1,16,400 Add: Unrecorded Sales 10,000 2,22,000

To Royalties 6,200 By Goods Stolen 10,000

To Wages and Salaries 14,800 By Closing Stock 76,000To Trade Expenses 2,400 To Gross Profit c/d 1,40,200 3,08,000 3,08,000

Profit and Loss Account for the year ended 31st Mar, 2013 Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount `

Amount `

To Reserve for Bad & Doubtful Debts

By Gross Profit b/d 1,40,200

Old Bad Debts 1,000

Add: New Bad Debts

Add: New R.D.D. 3,700

Less: Old R.D.D. 1,800 2,900

To Depreciation

Plant and Machinery 4,400 Motor Van 9,450 13,850

To Advertisement 8,200

To Salaries 11,000

To Office Rent 4,000 To General Expenses 2,800

To Loss by Theft 10,000

7

Chapter 02: Partnership Final Accounts

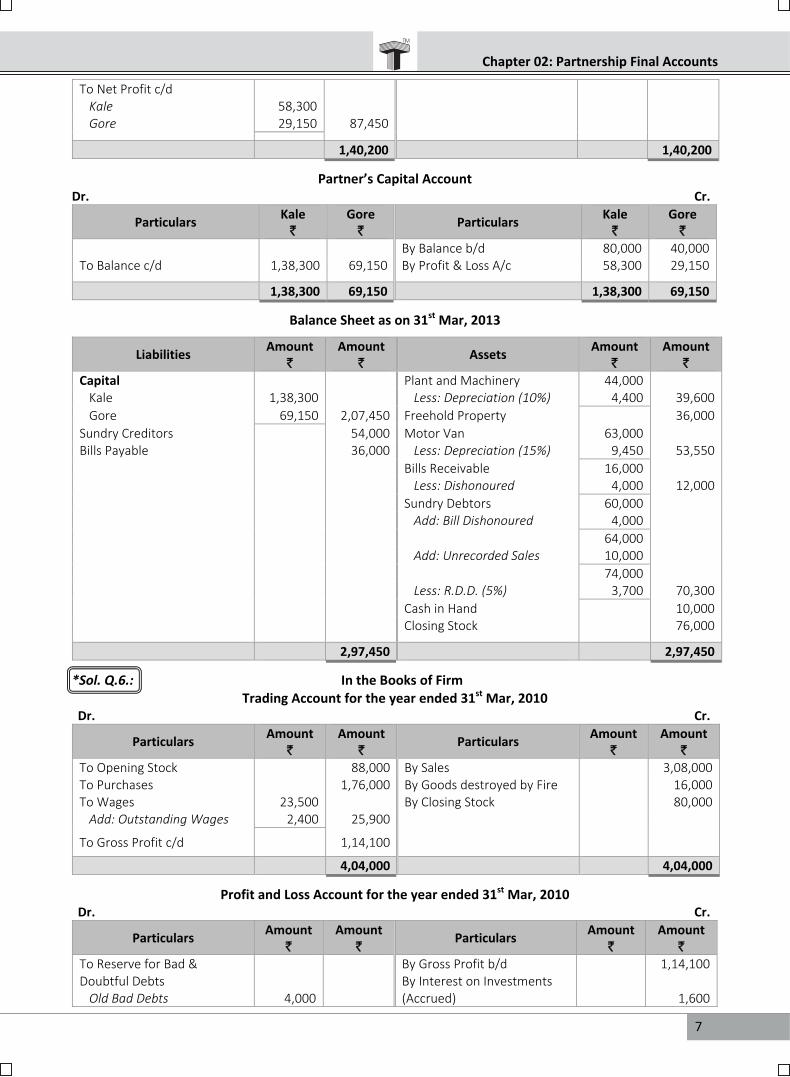

To Net Profit c/d Kale 58,300 Gore 29,150 87,450

1,40,200 1,40,200

Partner’s Capital Account

Dr. Cr.

Particulars Kale

` Gore

` Particulars

Kale `

Gore `

By Balance b/d 80,000 40,000To Balance c/d 1,38,300 69,150 By Profit & Loss A/c 58,300 29,150 1,38,300 69,150 1,38,300 69,150

Balance Sheet as on 31st Mar, 2013

Liabilities Amount

` Amount

` Assets

Amount `

Amount `

Capital Plant and Machinery 44,000 Kale 1,38,300 Less: Depreciation (10%) 4,400 39,600

Gore 69,150 2,07,450 Freehold Property 36,000

Sundry Creditors 54,000 Motor Van 63,000 Bills Payable 36,000 Less: Depreciation (15%) 9,450 53,550

Bills Receivable 16,000 Less: Dishonoured 4,000 12,000

Sundry Debtors 60,000 Add: Bill Dishonoured 4,000

64,000 Add: Unrecorded Sales 10,000

74,000 Less: R.D.D. (5%) 3,700 70,300

Cash in Hand 10,000 Closing Stock 76,000 2,97,450 2,97,450

*Sol. Q.6.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2010 Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount `

Amount `

To Opening Stock 88,000 By Sales 3,08,000To Purchases 1,76,000 By Goods destroyed by Fire 16,000To Wages 23,500 By Closing Stock 80,000Add: Outstanding Wages 2,400 25,900

To Gross Profit c/d 1,14,100 4,04,000 4,04,000

Profit and Loss Account for the year ended 31st Mar, 2010 Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount `

Amount `

To Reserve for Bad & By Gross Profit b/d 1,14,100Doubtful Debts By Interest on Investments Old Bad Debts 4,000 (Accrued) 1,600

8

8

Std. XII : Commerce

Add: New Bad Debts

Add: New R.D.D. 4,100

Less: Old R.D.D. 8,100

To Depreciation

Land and Building 6,500

Machinery 9,000 15,500

To Salaries 15,000

Add: Outstanding Salaries 3,000 18,000

To Office Expenses 8,000

To Bank Charges 2,600

To Legal Charges 3,000

Less: Prepaid Legal Charges 1,200 1,800

To Interest 3,600

To Export Duty 3,800

To Travelling Expenses 3,200

To Electricity Charges 2,300

To Loss by Fire 3,000

To Interest on Capital

Seeta 9,600

Geeta 9,600 19,200 To Net Profit c/d

Seeta 13,300

Geeta 13,300 26,600 1,15,700 1,15,700

Partner’s Current Account Dr. Cr.

Particulars Seeta

` Geeta

` Particulars

Seeta

` Geeta

` To Balance b/d – 4,000 By Balance b/d 5,000 –

By Interest on Capital A/c 9,600 9,600

To Balance c/d 27,900 18,900 By Profit & Loss A/c 13,300 13,300 27,900 22,900 27,900 22,900

Balance Sheet as on 31st Mar, 2010

Liabilities Amount

` Amount

` Assets

Amount

` Amount

` Capital A/c’s: Machinery 90,000

Seeta 1,20,000 Less: Depreciation (10%) 9,000 81,000

Geeta 1,20,000 2,40,000 Land and Building 1,30,000

Current A/c’s: Less: Depreciation (5%) 6,500 1,23,500

Seeta 27,900 Sundry Debtors 82,000

Geeta 18,900 46,800 Less: R.D.D. (5%) 4,100 77,900

Outstanding Expenses: Furniture 37,000

Wages 2,400 8% Debentures 40,000

Salaries 3,000 5,400 Add: Interest Receivable 1,600 41,600

Sundry Creditors 1,03,000 Insurance Claim 13,000

Bank Overdraft 60,000 Closing Stock 80,000

Prepaid Legal Charges 1,200 4,55,200 4,55,200

9

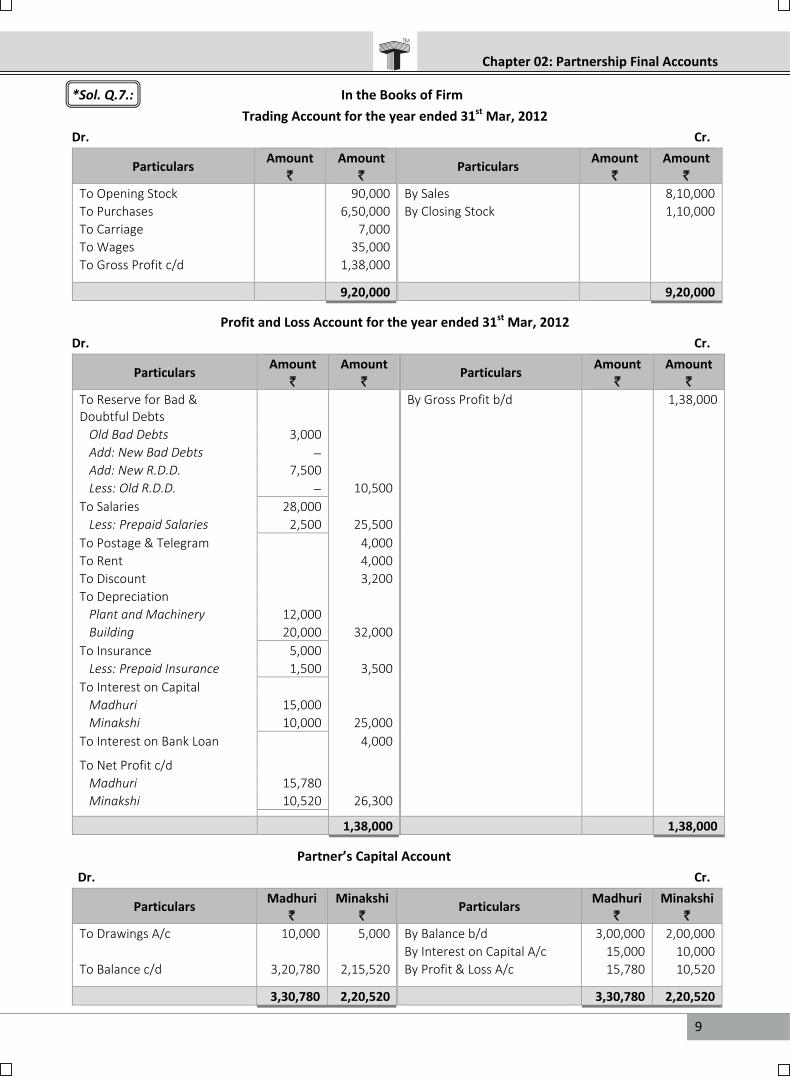

Chapter 02: Partnership Final Accounts *Sol. Q.7.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2012

Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount

` Amount

` To Opening Stock 90,000 By Sales 8,10,000

To Purchases 6,50,000 By Closing Stock 1,10,000

To Carriage 7,000

To Wages 35,000

To Gross Profit c/d 1,38,000 9,20,000 9,20,000

Profit and Loss Account for the year ended 31st Mar, 2012

Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount

` Amount

` To Reserve for Bad & Doubtful Debts

By Gross Profit b/d 1,38,000

Old Bad Debts 3,000

Add: New Bad Debts

Add: New R.D.D. 7,500

Less: Old R.D.D. 10,500

To Salaries 28,000

Less: Prepaid Salaries 2,500 25,500

To Postage & Telegram 4,000

To Rent 4,000

To Discount 3,200

To Depreciation

Plant and Machinery 12,000

Building 20,000 32,000

To Insurance 5,000

Less: Prepaid Insurance 1,500 3,500

To Interest on Capital

Madhuri 15,000

Minakshi 10,000 25,000

To Interest on Bank Loan 4,000 To Net Profit c/d

Madhuri 15,780

Minakshi 10,520 26,300 1,38,000 1,38,000 Partner’s Capital Account

Dr. Cr.

Particulars Madhuri

` Minakshi

` Particulars

Madhuri

` Minakshi

` To Drawings A/c 10,000 5,000 By Balance b/d 3,00,000 2,00,000

By Interest on Capital A/c 15,000 10,000

To Balance c/d 3,20,780 2,15,520 By Profit & Loss A/c 15,780 10,520 3,30,780 2,20,520 3,30,780 2,20,520

10

10

Std. XII : Commerce

Balance Sheet as on 31st Mar, 2012

Liabilities Amount

` Amount

` Assets

Amount `

Amount`

Capital Building 4,00,000 Madhuri 3,20,780 Less: Depreciation (5%) 20,000 3,80,000

Minakshi 2,15,520 5,36,300 Plant and Machinery 1,20,000

Sundry Creditors 1,00,000 Less: Depreciation (10%) 12,000 1,08,000

Outstanding Salaries 4,200 Sundry Debtors 1,50,000 8% Bank Loan 1,00,000 Less: R.D.D. (5%) 7,500 1,42,500

Add: Interest Payable 4,000 1,04,000 Prepaid Expenses:

Salaries 2,500 Insurance 1,500 4,000

Closing Stock 1,10,000 7,44,500 7,44,500

*Sol. Q.8.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2013 Dr. Cr.

Particulars Amount

` Particulars

Amount`

To Opening Stock 83,000 By Sales 4,20,000To Purchases 1,97,000 By Goods withdrawn for To Carriage 7,000 Personal Use To Wages 7,500 Mahesh 2,000 To Motive Power 15,000 Umesh 1,500 3,500

By Closing Stock 76,000To Gross Profit c/d 1,90,000 4,99,500 4,99,500

Profit and Loss Account for the year ended 31st Mar, 2013 Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount `

Amount`

To Reserve for Bad & Doubtful Debts

By Gross Profit b/d 1,90,000

Old Bad Debt 6,400 Add: New Bad Debt 2,500 Add: New R.D.D. Less: Old R.D.D. 8,900

To Depreciation Building 10,500 Motor Van 7,040 17,540

To Salary 13,000 To Audit Fees 8,500 To Printing and Stationery 4,000 To Interest on Capital Mahesh 8,100 Umesh 5,400 13,500

To Mahesh’s Salary 6,500 To Umesh’s Commission 8,400 To Net Profit c/d Mahesh 65,796 Umesh 43,864 1,09,660

1,90,000 1,90,000

11

Chapter 02: Partnership Final Accounts

Partner’s Current Account Dr. Cr.

Particulars Mahesh

` Umesh

` Particulars

Mahesh `

Umesh`

To Drawings A/c (Goods) 2,000 1,500 By Balance b/d 16,200 10,800 By Interest on Capital A/c 8,100 5,400 By Salary A/c 6,500 By Commission A/c 8,400To Balance c/d 94,596 66,964 By Profit and Loss A/c 65,796 43,864 96,596 68,464 96,596 68,464

Balance Sheet as on 31st Mar, 2013

Liabilities Amount

` Amount

` Assets

Amount `

Amount`

Capital A/c’s: Building 1,50,000 Mahesh 1,62,000 Less: Depreciation (7%) 10,500 1,39,500

Umesh 1,08,000 2,70,000 Debtors 96,000

Current A/c’s: Less: Bad Debts 2,500 93,500

Mahesh 94,596 Machinery 72,000Umesh 66,964 1,61,560 Motor Van 88,000

Sundry Creditors 99,000 Less: Depreciation (8%) 7,040 80,960

Bank Overdraft 56,400 Cash at Bank 52,000 Investments 56,000 Loose Tools 17,000 Closing Stock 76,000 5,86,960 5,86,960

*Sol. Q.9.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2010 Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount `

Amount`

To Opening Stock 25,000 By Sales 4,30,000To Purchases 2,20,000 By Goods withdrawn for Add: Unrecorded Purchases 3,000 2,23,000 Personal Use by Mohini 2,000

To Wages and Salaries 23,000 By Closing Stock 80,000Add: Outstanding 2,500 25,500

To Manufacturing Expenses 9,000 To Factory Insurance 5,000 To Import Duty 11,500 To Gross Profit c/d 2,13,000 5,12,000 5,12,000

Profit and Loss Account for the year ended 31st Mar, 2010 Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount `

Amount`

To Reserve for Bad & By Gross Profit b/d 2,13,000Doubtful Debts By Discount 3,500Old Bad Debts By Interest on Government Add: New Bad Debts bonds 4,500Add: New R.D.D. 2,250 Less: Old R.D.D. 2,250

12

12

Std. XII : Commerce

To Discount 4,000

To Depreciation on Plant and

Machinery 7,500

To Advertisement 10,000

Less: Prepaid Advertisement 8,750 1,250

To Salaries and Wages 45,000

To Warehouse Rent 6,000 To Net Profit c/d

Mohini 77,500

Rohini 77,500 1,55,000 2,21,000 2,21,000

Partner’s Capital Account Dr. Cr.

Particulars Mohini

` Rohini

` Particulars

Mohini

` Rohini

` To Drawings A/c 2,000 By Balance b/d 1,20,000 90,000

By Profit and Loss A/c 77,500 77,500

To Balance c/d 1,95,500 1,67,500 1,97,500 1,67,500 1,97,500 1,67,500

Balance Sheet as on 31st Mar, 2010

Liabilities Amount

` Amount

` Assets

Amount

` Amount

` Capital Sundry Debtors 45,000

Mohini 1,95,500 Less: R.D.D. 2,250 42,750

Rohini 1,67,500 3,63,000 Bills Receivable 50,000

Sundry Creditors 35,000 Factory Building 1,30,000

Add: Unrecorded Purchases 3,000 38,000 Plant and Machinery 75,000

Bills Payable 45,000 Less: Depreciation (10%) 7,500 67,500

Outstanding Wages 2,500 Prepaid Advertisement 8,750

Cash in Hand 5,000

10% Government Bond 60,000

Add: Interest Receivable 4,500 64,500

Closing Stock 80,000 4,48,500 4,48,500

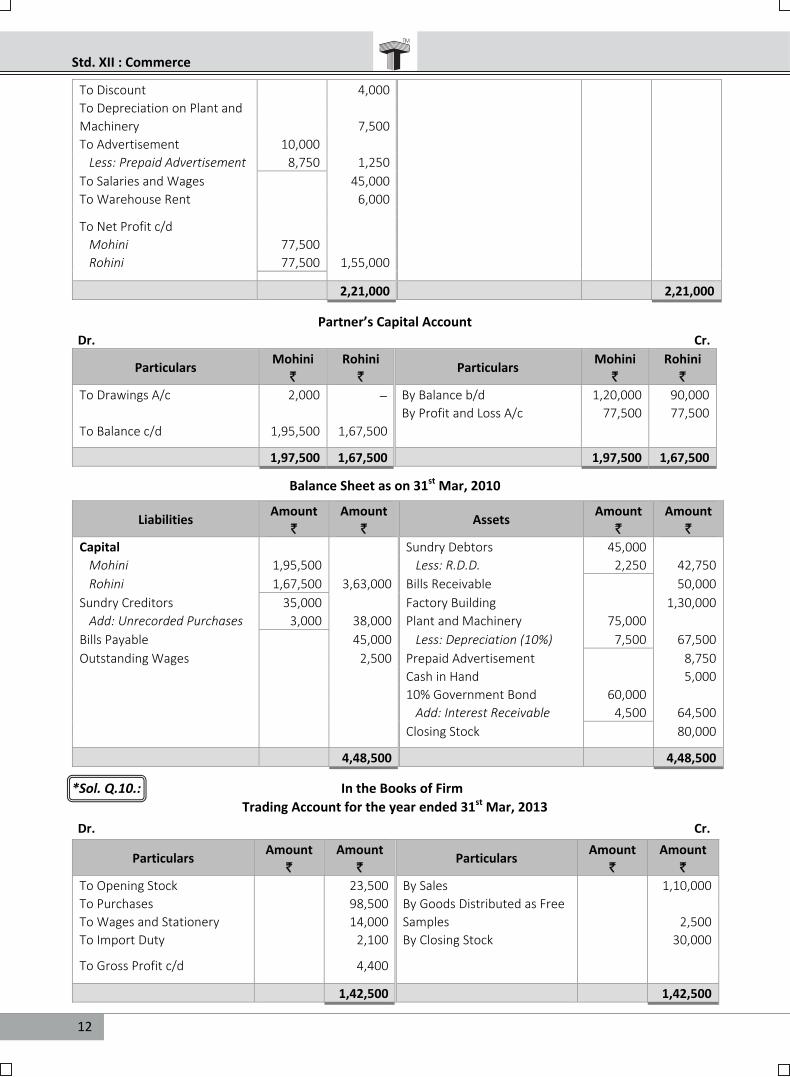

*Sol. Q.10.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2013

Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount

` Amount

` To Opening Stock 23,500 By Sales 1,10,000

To Purchases 98,500 By Goods Distributed as Free

To Wages and Stationery 14,000 Samples 2,500

To Import Duty 2,100 By Closing Stock 30,000 To Gross Profit c/d 4,400 1,42,500 1,42,500

13

Chapter 02: Partnership Final Accounts

Profit and Loss Account for the year ended 31st Mar, 2013

Dr. Cr.

Particulars Amount

`

Amount

` Particulars

Amount

`

Amount

`

To Reserve for Bad & By Gross Profit b/d 4,400

Doubtful Debts

Old Bad Debts 1,000

Add: New Bad Debts 1,500

Add: New R.D.D. –

Less: Old R.D.D. – 2,500

To Salaries and Wages 12,000

To Postage and Telegram 1,750

Less: Unused 250 1,500

To Advertisement 5,000

Add: Goods Distributed as Free Samples 2,500 7,500

To Carriage Outward 1,800

To Printing and Stationery 4,600

Less: Unused 400 4,200

To Depreciation

Leasehold Premises 4,000 By Net Loss c/d

Plant and Machinery (10%) 7,000 11,000 Sanjay 19,550

To Interest on Bank Loan 3,000 Vijay 19,550 39,100

43,500 43,500

Partner’s Capital Account

Dr. Cr.

Particulars Sanjay

`

Vijay

`Particulars

Sanjay

`

Vijay

`

To Profit and Loss A/c (Loss) 19,550 19,550 By Balance b/d 45,000 45,000

To Balance c/d 25,450 25,450 45,000 45,000 45,000 45,000

Balance Sheet as on 31st Mar, 2013

Liabilities Amount

`

Amount

`Assets

Amount

`

Amount

`

Capital Leasehold Premises 80,000

Sanjay 25,450 Less: Written Off 4,000 76,000

Vijay 25,450 50,900 Plant and Machinery 70,000

Sundry Creditors 72,700 Less: Depreciation (10%) 7,000 63,000

Bills Payable 40,000 Sundry Debtors 45,800

Outstanding Audit Fees 5,900 Less: Bad Debts 1,500 44,300

10% Bank Loan 60,000 Bills Receivable 16,700

Add: Interest Payable 3,000 63,000 Unused Postage Stamps 250

Unused Stationery 400

Cash in Hand 1,850

Closing Stock 30,000 2,32,500 2,32,500

14

14

Std. XII : Commerce Sol. Q.1.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2012

Dr. Cr.

Particulars Amount

`

Amount

` Particulars

Amount

`

Amount

`

To Opening Stock A/c 20,000 By Sales A/c 3,50,000

To Purchases A/c 2,02,000 By Closing Stock A/c 40,000

Less: Return Outwards 2,000 2,00,000

To Wages A/c 10,000

Add: Outstanding Wages 2,000 12,000 To Gross Profit c/d 1,58,000 3,90,000 3,90,000

Profit and Loss Account for the year ended 31st Mar, 2012

Dr. Cr.

Particulars Amount

`

Amount

` Particulars

Amount

`

Amount

`

To Reserve for Bad & By Gross Profit b/d 1,58,000

Doubtful Debts A/c By Interest on Investment A/c 3,500

Old Bad Debts – Add: Accrued Interest 500 4,000

Add: New Bad Debts 1,000

Add: New R.D.D. –

Less: Old R.D.D. 1,000 –

To Salaries A/c 5,000

Add: Outstanding Salaries 1,000 6,000

To Insurance A/c 4,000

Less: Prepaid Insurance 500 3,500

To Rent & Taxes A/c 12,000

To Depreciation A/c

Building 5,000

Furniture 3,000 8,000 To Net Profit c/d

Amit 66,250

Vipul 44,167

Sumit 22,083 1,32,500 1,62,000 1,62,000

Partner’s Capital Account

Dr. Cr.

Particulars Amit

`

Vipul

`

Sumit

` Particulars

Amit

`

Vipul

`

Sumit

`

By Balance b/d 1,00,000 80,000 50,000

By Profit & Loss

To Balance c/d 1,66,250 1,24,167 72,083 A/c 66,250 44,167 22,083 1,66,250 1,24,167 72,083 1,66,250 1,24,167 72,083

Practice Problems

15

Chapter 02: Partnership Final Accounts

Balance Sheet as on 31st Mar, 2012

Liabilities Amount

` Amount

` Assets

Amount `

Amount`

Capital Debtors 80,000 Amit 1,66,250 Less: New Bad Debts Vipul 1,24,167 Written Off 1,000 79,000

Sumit 72,083 3,62,500 Furniture 30,000

Creditors 8,000 Less: Depreciation 10% 3,000 27,000

Bills Payable 4,000 Building 1,00,000 Outstanding Rent 2,000 Less: Depreciation 5% 5,000 95,000

Outstanding Expenses Prepaid Insurance 500Wages 2,000 Investment 50,000 Salaries 1,000 3,000 Add: Accrued Interest 500 50,500

Cash in Hand 17,500 Bills Receivable 30,000 Patent 40,000 Closing Stock 40,000 3,79,500 3,79,500

Working Notes: Calculation of amount of depreciation:

i. Building = 1,00,000 1212

5

100= ` 5,000 ii. Furniture = 30,000 12

12 10

100= ` 3,000

Sol. Q.2.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2013 Dr. Cr.

Particulars Amount

` Amount

` Particulars

Amount `

Amount`

To Opening Stock A/c 1,80,000 By Sales A/c 5,25,000To Purchases A/c 2,40,000 By Closing Stock A/c 2,00,000To Carriage Inward A/c 12,000 To Gross Profit c/d 2,93,000 7,25,000 7,25,000

Profit and Loss Account for the year ended 31st Mar, 2013

Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount

` Amount

` To Reserve for Bad & By Gross Profit b/d 2,93,000Doubtful Debts A/c By Rent A/c 22,000 Old Bad Debts – Less: Advance Rent 5,000 17,000

Add: New Bad Debts 20,000 Add: New R.D.D. – Less: Old R.D.D. – 20,000

To Salary and Wages A/c 24,000 Add: Outstanding Salary and Wages 6,000 30,000

To Insurance A/c 12,000 Less: Prepaid Insurance 3,000 9,000

To Discount A/c 9,000 To Travelling Expenses A/c 13,000 To Postage and Telegrams A/c 7,000

16

16

Std. XII : Commerce

To Depreciation A/c

Furniture 28,000 To Net Profit c/d Sanjay 97,000

Keshav 97,000 1,94,000 3,10,000 3,10,000

Partner’s Capital Account

Dr. Cr.

Particulars Sanjay

` Keshav

` Particulars

Sanjay `

Keshav `

By Balance b/d 5,00,000 3,00,000

By Profit & Loss A/c 97,000 97,000

To Balance c/d 5,97,000 3,97,000 5,97,000 3,97,000 5,97,000 3,97,000

Balance Sheet as on 31st Mar, 2013

Liabilities Amount

` Amount

` Assets

Amount `

Amount `

Capital Debtors 2,10,000Sanjay 5,97,000 Furniture 2,80,000

Keshav 3,97,000 9,94,000 Less: Depreciation 10% 28,000 2,52,000

Sundry Creditors 1,00,000 Land and Building 4,00,000Bills Payable 78,000 Prepaid Insurance 3,000

Outstanding Expenses Cash in Hand 38,000

Salary and Wages 6,000 Bills Receivable 80,000Advance Rent 5,000 Closing Stock 2,00,000 11,83,000 11,83,000

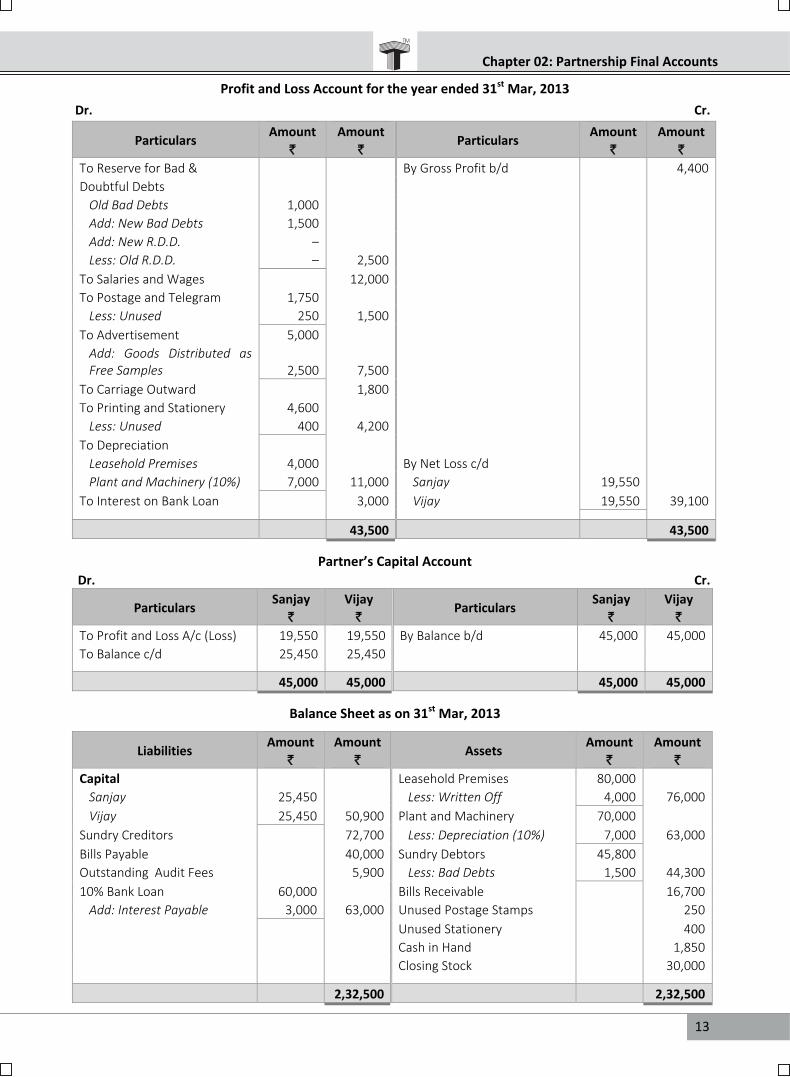

Sol. Q.3.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2012 Dr. Cr.

Particulars Amount

` Amount

`Particulars

Amount `

Amount `

To Opening Stock 25,000 By Sales 1,42,600

To Purchases 90,000 By Goods Taken Over 3,000

To Wages 24,000 By Closing Stock 18,500 To Factory Expenses 8,000 To Gross Profit c/d 17,100 1,64,100 1,64,100

Profit and Loss Account for the year ended 31st Mar, 2012 Dr. Cr.

Particulars Amount

` Amount

`Particulars

Amount `

Amount `

To Reserve for Bad & By Gross Profit b/d 17,100 Doubtful Debts

Old Bad Debts 700 Add: New Bad Debts 1,000

Add: New R.D.D. 2,200

Less: Old R.D.D. 1,000 2,900

17

Chapter 02: Partnership Final Accounts

To Carriage Outward 1,700 To Advertisements 3,500 To Insurance 400 Less: Prepaid 100 300

To Depreciation Land and Building 3,000 Furniture 600 3,600

To Office Expenses 2,300 To Net Profit c/d Suresh 1,600 Ramesh 1,200 2,800

17,100 17,100

Partner’s Current Account

Dr. Cr.

Particulars Suresh

` Ramesh

`Particulars

Suresh `

Ramesh `

To Drawings A/c 3,000 By Balance b/d 20,000 25,000 (Goods withdrawn) By Profit & Loss A/c 1,600 1,200 To Balance c/d 18,600 26,200 21,600 26,200 21,600 26,200

Balance Sheet as on 31st Mar, 2012

Liabilities Amount

` Amount

`Assets

Amount `

Amount `

Capitals Land and Building 30,000 Suresh 18,600 Less: Depreciation (10%) 3,000 27,000

Ramesh 26,200 44,800 Furniture 3,000

Sundry Creditors 49,000 Less: Depreciation (20%) 600 2,400

Unpaid Wages 1,000 Debtors 45,000 Less:Bad Debts 1,000

44,000 Less:R.D.D. (5%) 2,200 41,800

Closing Stock 18,500 Prepaid Insurance 100 Cash at Bank 5,000 94,800 94,800 Working Note: Calculation of amount of Prepaid Insurance: Amount of Insurance given in Trial Balance = ` 400 Insurance paid upto 30th Jun, 2012; Insurance chargeable to P&L upto 31st Mar, 2012 Period of Prepaid Insurance = 3 months

Prepaid Insurance = 400 312

= ` 100

Sol. Q.4.: In the Books of Firm

Trading Account for the year ended 31st Mar, 2012 Dr Cr

Particulars Amount

` Amount

`Particulars

Amount `

Amount `

To Opening Stock 2,00,000 By Sales 4,00,000 To Purchases 2,75,000 Less: Sales Return 5,000 3,95,000

Less: Purchase Return 4,500 2,70,500 By Drawing of goods Chavan 2,000

446

446

Std. XII : Commerce Sol. Q.24.: Net Profit = ` 2,80,000; Net Sales = ` 5,00,000

Net Profit Ratio = Net Profit

100Net Sales

= 2,80,000

1005,00,000

= 56%

Sol. Q.25.: Fixed Assets = ` 5,00,000; Balance Sheet Total = ` 10,00,000

Percentage of Fixed Assets to Total Assets = Fixed Assets

100Total Assets

= 5,00,000

10010,00,000

= 50%

Sol. Q.26.: Total Sales = ` 1,00,000; Sales Returns = ` 10,000; Cost of Goods Sold = ` 50,000 Net Sales = Total Sales Sales Returns = 1,00,000 10,000 = ` 90,000 Gross Profit = Net Sales Cost of Goods Sold = 90,000 50,000 = ` 40,000

Gross Profit Ratio = Gross Profit

100Net Sales

= 40,000

10090,000

= 44.44%

Sol. Q.27.: Current Assets = ` 6,00,000; Current Liabilities = ` 3,00,000

Current Ratio = Current Assets

Current Liabilities=

6,00,000 6 2

3,00,000 3 1

Current Ratio = 2 : 1 Sol. Q.28.: Net Profit = ` 1,00,000; Total Sales = ` 1,80,000; Sales Returns = ` 30,000 Net Sales = Total Sales Sales Returns = 1,80,000 30,000 = ` 1,50,000

Net Profit Ratio = Net Profit

100Net Sales

= 1,00,000

× 1001,50,000

= 66.67%

Sol. Q.29.: Net Profit before Interest, Tax and Dividend = ` 4,00,000; Total Capital Invested = ` 10,00,000

Return on Investments (ROI) = Profit before Interest, Tax andDividend

Capital Employed 100 = 4,00,000

10,00,000 100 = 40%