Embed Size (px)

Citation preview

State Oil Companies in Latin America: Performance and Outlook

GUSTAVO CORONEL 8205 Kentfield Court, Bethesda, MD 20817, USA

1. INTRODUCTION

1.1 THE PETROLEUM INDUSTRY IN LATIN AMERICA: AN OVERVIEW

The world supply and demand of hydrocarbons during the past 8 years has been characterized by a glut as well as by the significant loss of relative position of OPEC as a major source of supply. More than 60% of today’s supply of oil is coming from non-OPEC countries. New production from countries such as China, India, Brazil and Col- ombia has entered the market and has further weakened world oil prices. Unless OPEC and non-OPEC producers can reach lasting agree- ments on production, prices could be driven still lower, perhaps as low as US$10 barrel-’.

Meanwhile Latin America’s annual energy con- sumption has nearly doubled and is now about 2500 million barrels of oil equivalent. Of this consumption, 45% is oil and 15% is natural gas. Although the region, taken as a whole, is in balance because it produces 12% of the world’s total while consumption is about 10% of the total, there are profound differences in the pattern of production and consumption from country to country. As a result, the majority of countries are highly dependent on oil imports. Only five coun- tries are net exporters and three others are self- sufficient. The rest import 40-100% of their re- quirements, and some have to use more than 50%

of their export earnings to pay for their oil import bill.

The reasons for this high dependence on oil imports are several:

-the high density of urban population in the region, up to 80% in Venezuela, Argentina and Chile; -the lack of efficient mass-transport systems: millions of Latin Americans move in family cars and the region has a larger transport-to-GDP ratio than that of the USA or Japan; -intense inter-regional migrations; -the great distances between production and consumption centres, which stimulates the use of the type of energy most easily transported - oil; and -the rapid rate of industrialization which has taken place in the region during the past 20 years.

In response to this high level of oil dependence, countries in the region have adopted three basic policies:

(1) searching for indigenous sources of hydro- carbons;

(2) increased efforts in conservation of energy and an increase in the domestic prices of most hydrocarbon products; and

(3) substituting other energy sources, wher- ever possible, for hydrocarbons.

~

Gustavo Coronel is a former: member of the Petroleum of Venezuela Board of Directors

The views expressed in this article are the sole responsibility of the author.

Natural Resources Forum 0 United Nations, New York, 1988

375

3 76 GUSTAVO CORONEL NRF VOL. 12, NO. 4, 1988

The search for hydrocarbons has been very suc- cessful in some countries. In Brazil domestic pro- duction has increased by some 400 000 barrels day-' in the past 7 years. Argentina has found large volumes of natural gas and is actively ex- panding the use of this resource. Four years ago Colombia found a giant oilfield in the Northern plains, near the Venezuelan border. Venezuela has recently found a giant oilfield in the Eastern part of the country. Peru has also found signi- ficant natural gas deposits in the Amazonian jun- gle. In general, however, the majority of coun- tries are still far from the goal of self-sufficiency. This is due to the fact that petroleum exploration is costly. complex and time-consuming and that it is often hampered by political and legal matters.

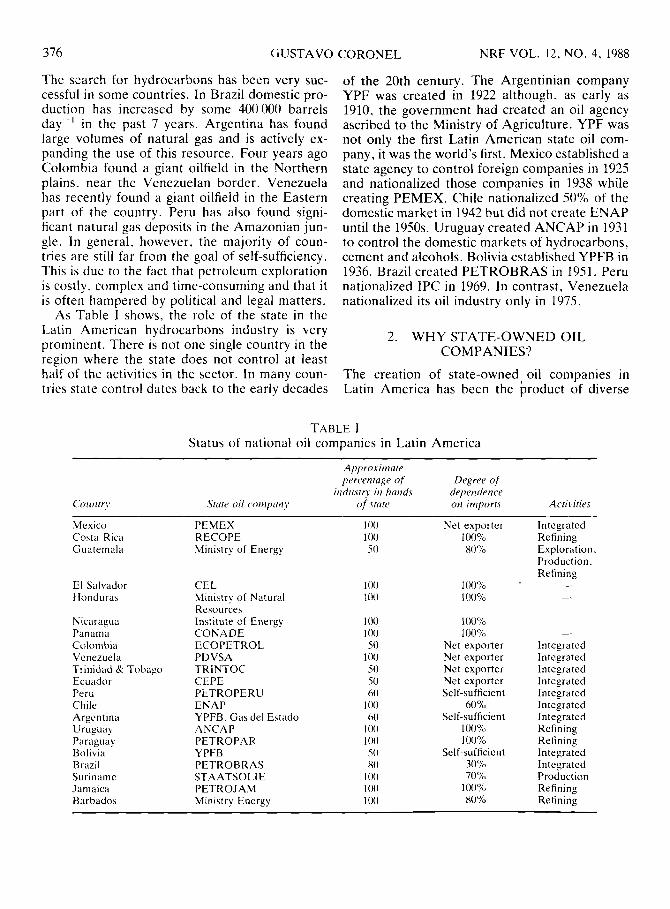

As Table I shows, the role of the state in the Latin American hydrocarbons industry is very prominent. There is not one single country in the region where the state does not control at least half of the activities in the sector. In many coun- tries state control dates back to the early decades

of the 20th century. The Argentinian company YPF was created in 1922 although. as early as 1910, the government had created an oil agency ascribed to the Ministry of Agriculture. YPF was not only the first Latin American state oil com- pany, it was the world's first. Mexico established a state agency to control foreign companies in 1925 and nationalized those companies in 1938 while creating PEMEX. Chile nationalized 50% of the domestic market in 1942 but did not create ENAP until the 1950s. Uruguay created ANCAP in 1931 to control the domestic markets of hydrocarbons, cement and alcohols. Bolivia established YPFB in 1936. Brazil created PETROBRAS in 1951. Peru nationalized IPC in 1969. In contrast, Venezuela nationalized its oil industry only in 1975.

2. WHY STATE-OWNED OIL COMPANIES'?

The creation of state-owned, oil companies in Latin America has been the product of diverse

TABLE I Status of national oil companies in Latin America

Approxinlore prrcentuge of' Drgrrr of

itldiisrry in hands di~penrlence Cortrlrr! Srrrre oil comprrtiy of . v rcr rc on in1port.t Acrivilies

Mexico Costa Kica G uat e ma1 ii

El Salvador Honduras

Nicaragua Panama Colombia Venezuela Trinidad 8r Tobago Ecuador Peru Chile Argentina Uruguay Paraguay Bolivia Brazil Suriname Jamaica Barbados

PEMEX RECOPE Ministry o f Energy

CEL Mmi\tr.i ot Natural Re\ource\ In\titute o f Energy CONADE ECOPETROL PDVSA TRINTOC CEPE PETROPERU E N A P YPFB. Gd\ del E\tddo ANCAP PETROPAR YPFB PETROBRAS STAATSOLI E PETROJAM Mini\try Encrgy

100 100

SO

Net exporter lOOo/u HO'X

100% 100%

100% 100""

Net exporter Net exporter Net exporter Net exporter Self-sufficient

60% Self-sufficient

100'%> 1 OO'X

Self-sufficient 30Y" 70'X

100% 80%

Integrated Refining Exploration. Production, Refining

-

Integrated Integrated Integrated Integrated Integrated Integrated Integrated Rcfining Refining Integrated Integrated Production Refining Refining

NRF VOL. 12, NO. 4, 1988 STATE OIL COMPANIES IN LATIN AMERICA 377

circumstances. In some cases they were the crea- tures of bitter confrontation between the govern- ment and private multinational firms. In others they were the product of a gradual increment of state control. The underlying reasons, however, were similar throughout the region. They in- cluded reasons such as the following.

(1) The World Wars. Both the First and the Second World War made countries acutely con- scious of the strategic importance of petroleum and of the necessity of establishing significant state control over indigenous hydrocarbon re- sources.

(2) The increasing power of the Seven Sisters oil companies. During the first half of the century, the major international oil companies increas- ingly dominated the world market in hydro- carbons, kept the participation of producing countries at a low level and totally controlled the refining and marketing components of the indus- try. This increasing power put fear and distrust in the heart and minds of Latin American political leaders.

( 3 ) A feeling of dependence and national in- feriority. This feeling was associated with the control of their domestic hydrocarbons resources by foreign companies and with the apparent in- ability of local staff to rise to the highest hierar- chical levels of those companies. (4) Political ideology. Latin American govern-

ments, even the most conservative ones, have traditionally prided themselves in being nationa- listic and revolutionary. For those governments the obvious targets of nationalization were the big, unpopular foreign oil companies which had few, if any, allies even in their countries of origin.

(5) Internal politics. In several countries nationalization of foreign oil companies was done as a way to increase the popularity of the govern- ment in power or to consolidate the power of a political group or party.

( 6 ) The need to know more about the industry. The creation of state-owned oil companies par- tially responded to a need to know more about the industry. In countries where this industry was the main source of income, this need was obvious. However, this did not appear to be the primary factor in the creation of state-owned oil com- panies even in those countries. If it had been, the

step would probably have been taken much ear- lier than it was.

3 . THE SWING O F THE PENDULUM

From the moment oil was first discovered in Santa Cruz, Bolivia, in 1875, until the end of the 1950s. the large transnational oil companies had decisive control over hydrocarbon production in Latin America and almost total control over marketing in those countries. This was certainly true in countries such as Venezuela and Trinidad. However, from about 1955 onwards there was a significant acceleration of state ownership in the Latin American oil industry in general and of the domestic refining and marketing sectors in par- ticular. This interest of governments in increasing their control over the oil industry had several important reasons, including the following.

(1) The influence of the price cycles of pet- roleum (Fig. 1). Since 1878 oil prices have ex- perienced about 10 cycles of peaks and valleys, including six prominent ones coming approx- imately every 20 years. The acceleration of state control over the industry seems to have been triggered by price increases, especially those of the rnid-l950s, and have been given a definitive push by the significant increases of the mid-1970s.

(2) The creation of OPEC. OPEC was created in 1961 as a mechanism of defence, essentially designed to keep oil prices from falling. The political events of the Middle East in the early 1970s, especially in Iran and Libya, turned this defensive mechanism into a formidable political weapon which largely ended the dominance of the

2 3 4 5 6

1900 1970 2000 Years

Fig. 1. Major price cycles in the petroleum industry.

378 GUSTAVO CORONEL NRF VOL. 12. NO. 4. 1988

transnational oil companies and created a totally new world petroleum system.

(3) The proliferation of independent, smaller multinationals. The emergence of numerous new actors in the world petroleum scene in the 1960s severely eroded the monolithic power of the ma- jor transnational oil companies. The best-known case of this phenomenon was that of Occidental Petroleum entering Libya, Bolivia and Venezuela and negotiating in a manner which departed sub- stantially from the orthodox and predictable be- haviour of the larger transnational oil companies.

(4) The changing role of the state. During the past 30 years Latin American countries have ex- perienced increasing shortages of financial re- sources combined with significant population growth. In countries with substantial petroleum reserves, the oil industry is one of the most impor- tant sources of foreign exchange. At the same time the increasing price of oil in the world mar- kets during the 1970s led to increasing interest on the part of governments in locating domestic sources of hydrocarbons. The intensely nationa- listic political atmosphere prevailing during those years discouraged the participation of private capital in these efforts and stimulated direct state participation.

The combination of all of the above factors led to a bigger role of the state in the petroleum indus- tries of the region.

4. PERFORMANCE

In general, state-owned enterprises do not have a good business record, either in developed or in developing countries. However, in the Fortune foreign 500 list of firms for 1981, five of the best 10 were public enterprises and all of them were petroleum companies. This is not surprising be- cause, as John D . Rockefeller used to say, ‘The best business in the world was a well managed oil company and the second best, a badly managed oil company’. This is so because the margins between production and selling costs have tradi- tionally been very large. However, the only pet- roleum companies that managed to lose money during recent years were all state-owned, that is until the world price of oil collapsed in 1985,

forcing numerous private companies into bank- ruptcy.

In Latin America the state-owned petroleum companies share some characteristics which have influenced their performance. Some of these characteristics are listed below.

(1) Pronounced isolation from other com- panies and industries within the region. Although the Latin American hydrocarbon sector acquires about US$6000 million per year in goods and services, only 7% of those acquisitions come from within the region: in the same fashion, only 10% of the consulting services are contracted to re- gional firms. During a 1986 exhibition of pet- roleum goods and services, held in Buenos Aires, most of the stands belonged to extraregional firms and most of the equipment of local origin was made under foreign licence.

The few countries which have a large hydrocar- bons service sector face increasingly saturated markets at home and have an urgent need to export. This has not yet happened due to a shortage of capital for financing, bureaucratic red-tape, excessive protectionism and to the lack of an efficient regional information system.

(2) Insufficient contact with technological and managerial innovation. The relative scarcity of financial resources in most countries of the region has usually meant that state-owned petroleum companies are utilized by governments as foreign- exchange generators but are rarely given enough resources to keep technologically and organiza- tionally strong. As a result, equipment tends to become obsolete, training is neglected and, after a few years, the companies lose significant money-generating capacity, always to the surprise of the political sectors which have kept them short of funds.

(3) Weak planning. Most of the Latin Amer- ican countries have been under severe economic stress for the past decade. Mounting external debt, decreasing prices for their exports and high inflation rates have combined to produce social and political unrest in the region. In this atmos- phere of extreme uncertainty, national planning has become a neglected tool, both by govern- ments and by the state-owned petroleum com- panies. Although several companies in the region

NRF VOL. 12, NO. 4, 1988 STATE OIL COMPANIES IN LATIN AMERICA 379

plan in a very orderly and systematic manner, most Latin American oil companies have either abandoned planning as a cyclic exercise or have never done it. The argument frequently used is that no planning can be done when uncertainty is so high. However, it is precisely to deal with extreme uncertainty that planning is urgently re- quired.

(4) External influences in decision-making. The interface between the political, labour and technocratic sector in Latin America has tradi- tionally been blurred. This has been most evident in the petroleum sector because of the signi- ficance of petroleum to the economic and social environment of the region. The influence of poli- tics in the quality, promptness and nature of decisions taken by the management of state oil companies can be seen in the following:

(a) the appointment of political figures to the top management jobs of the petroleum com- panies;

(b) promotion systems based on political affiliation rather than on meritocratic ranking;

(c) the appointment of the Minister of the sector to head the petroleum company;

(d) political bargaining in the consideration and approval by the legislative branch of the government of the budgets of state-owned pet- roleum companies;

(e) pressure on the state oil companies to favour politically friendly contractors;

(f) attempts at legislative control of state- owned oil company programmes;

(g) influence of labour unions in management decisions;

(h) pressures on the state oil companies to finance social o r community projects which bear no relation to petroleum matters; and

(i) political bias, usually against foreign oil companies in their attempts to associate them- selves with the state-owned petroleum com- panies.

Following Mintzberg’s power configuration in organizations (Table 11), many of the state-owned petroleum companies of the region can be class- ified as government instruments, whereas a few are essentially meritocratic and still others are an

TABLE I1 Power configuration in organizations

Type of influence Power

lnrernal configiiraiion Exiernal

Passive Professional Meritocratic Dominating Bureaucratic Instrument Passive Personalized Autocracy Divided Politicized Political arena

Source: Mintzberg. H. 1983. Power In and Around Organiza- tions. Prentice-Hall. Englewood Cliffs, New Jersey, p. 307.

integral part of the political landscape of their countries.

In general, state-owned petroleum companies in Latin America fall into three groups:

Group 1 . Those companies having experienced personnel, relatively solid management, state-of- the-art technology and relative financial inde- pendence. There are probably no more than three companies in this category.

Group 2. Companies having some experienced personnel, relatively good management, fair tech- nology and a weak financial situation. There are two to four companies in this category.

Group 3. Companies having some good techni- cal personnel, unstable management, rather obsolete technological equipment and a very weak financial situation. Most other companies in Latin America are in this group.

The major enemies of good performance by these companies are not technical or even financial, but institutional and political. Today most technical obstacles can be overcome. Exploration techni- ques, secondary recovery methods, deep conver- sion refining and pipeline engineering have reached very high levels of sophistication, to the point where few known reservoirs in Latin Amer- ica can be said to be unexploitable for technical reasons. Financial constraints are more severe, especially because of the critical economic situa- tion of most countries in the region. Still, much can be done by means of an intelligent policy of association with the international private sector and through the co-operation of multilateral de-

380 GUSTAVO CORONEL NRF VOL. 12, NO. 4, 1988

velopment banks. It is in the institutional environ- ment where most of the real problems lie. The energy sector of most countries in the region frequently lacks an integrated plan. In many in- stances there is considerable competition between subsectors such as electricity, nuclear and hydro- carbons for scarce state resources, a competition which is often resolved through political, rather than managerial, means. The companies often lack sound managerial information and financial control systems, and not infrequently there is instability at middle and high management levels. There is the case of a state-owned oil company having six general managers in 2 years, or the case of the company in which the entire top manage- ment team was replaced following a change in government. It is not unusual for state-owned oil companies in Latin America to become instru- ments of the national government for the borrow- ing abroad of large amounts of capital not for the use of the companies themselves, but for the use of the central government. The political and financial pressures applied by the central govern- ment can often result in the state-owned pet- roleum companies committing themselves to un- clear, vague social objectives which eventually result in large financial losses and demoralization of the staff in the affected companies. In some instances these pressures have led to the resigna- tion of high-quality professional managers.

5 . OUTLOOK

Although the performance of state-owned pet- roleum companies in Latin America has not been optimal, the outlook does not have to be bleak. Much could be done in a relatively short time by changing some of the approaches and attitudes which have prevailed for many years. Among the ingredients for success which have already work- ed extremely well in some of these companies are the following.

(1) A professional, stable management. This has been the key to success in several of the existing state-owned petroleum companies in the region. The permanence of qualified, professional managers in the top jobs of their companies lends credibility to the companies, motivates personnel who work for them, and permits objective and knowledgeable decision-making.

(2) A meritocratic system for personnel de- velopment. Organizations can rarely develop a healthy culture without a meritrocratic basis for promotion, career development and planning. Organizations where promotions depend on other considerations, be they political or nepotic, usual- ly have a low level of employee satisfaction and, as a result, a low efficiency. The case for a meri- tocratic system of personnel development should be an obvious one, but it has had to fight an uphill battle in many of the state-owned petroleum com- panies of the region.

(3) Financial self-sufficiency. The case for the financial self-sufficiency of state-owned pet- roleum companies cannot be overstated. When- ever a company has to compete for funds with other state companies and agencies or with socially oriented projects, it can never have the guarantee that the funds will be available.

(4) A participatory, open management style. The management style of state-owned enterprises as an extension of the management style of the central government is often authoritarian and/or paternalistic. State-owned petroleum companies face tough competition in world markets and should be able to react swiftly to external events. This is impossible unless communication works freely throughout the company and decision- making is sufficiently decentralized. ’

( 5 ) A low profile. The higher the public profile a state-owned petroleum company keeps, the more controversy it will tend to create. These companies should be neither spectacularly suc- cessful nor too much of a failure, because in either case they will probably become the object of undue attention. Companies should keep a deli- cate, difficult balance between a technocratic, closed organization and a political one. The pure- ly technocratic attitude will inevitably cause the resentment of the political sector while the poli- tical attitude will inevitably lead to loss of efficiency.

(6) A plan of association with the private, transnational petroleum companies. There is no doubt that most of the financial and technical resources in the petroleum industry are in the hands of transnational oil companies. The busi- ness of those companies is to produce and market hydrocarbons and, in order to do this, they will go to any country which offers them the possibility of making a profit and working under stable and

NRF VOL. 12, NO. 4, 1988 STATE OIL COMPANIES IN LATIN AMERICA 381

clear rules. To join forces with the transnational petroleum companies is not ideological surrender and does not need to imply lack of nationalism. It is a business decision, better taken with the head than with the heart.

(7) Regional integration. The most obvious imbalance in the Latin American hydrocarbons scene is in the geographic distribution of the resources. Whereas some countries are extremely rich in petroleum deposits, others lack them almost completely. Some have liquid hydrocar- bons and others have mostly gas with little liquid fractions. Although there might be much gas in southern Chile, for example, Chilean gas markets are in the north. The natural gas finds of Peru are hundreds of miles away from their potential mar- kets, which are located on the other side of the Andes. Argentina has significant gas reserves, whereas Uruguay has none. The possibilities for large-scale regional integration projects are, therefore, both numerous and excellent: Argenti- nian gas to northern Chile and to Uruguay; Boli- vian gas to Brazil and oil products to northern Chile: refining regional centres serving Central America or the Caribbean island-states; transport of Colombian crude oils through Venezuelan pipelines, etc. However, the most obvious candi- date for regional integration is the field of goods and services, where there is a US$6000 million year-' market waiting to be tapped by Latin American state-owned petroleum companies and related service organizations.

6. IS THE PENDULUM SWINGING BACK?

The critical economic conditions prevailing in Latin America combined with the generally lack- lustre performance of state-owned enterprises are producing an increasing trend towards privatiza- tion throughout the region. For example, in

Venezuela the state has equity participation in about 367 companies. These companies, exclud- ing the petroleum companies, lost about US$2000 million in 1981 and a similar amount in 1982. As a result there is a programme under way to priva- tize many of these companies and to eliminate others. Similar programmes are under way in Chile, Mexico, Argentina and Brazil. State capi- talism is apparently on the way out, and a policy of readjustment of the public sector is clearly in.

In the case of the state-owned petroleum com- panies the trend towards privatization is much less apparent, due to the pronounced economic and political significance petroleum has through- out the region. However, PETROBRAS shares are now being traded on the Brazilian stock mar- ket and there are increasing examples of associa- tion of Latin American state-owned petroleum companies with the private sector, in the form of both risk ventures and mixed companies in the refining and petrochemical fields. Again, the Venezuelan case is illustrative. PDVSA has brought significant equity in companies such as VEBA oil in Germany, CITGO in the USA and NYNAS in Sweden, and the Government is tak- ing a much more liberal attitude towards private participation in coal, refining and petrochemical ventures in the country. ENAP in Chile is build- ing petrochemical plants in association with US companies. Peru is considering the creation of a mixed company with Shell to develop the natural gas finds of the Amazonian jungle.

It therefore seems that the period of intense nationalism and distrust of foreign companies is ending and a more pragmatic, business-like approach is starting. It can only be hoped that the future brings success to the Latin American pet- roleum industry, and that the main objective of self-sufficiency is finally realized for as many as possible of the countries in the region.