Embed Size (px)

Citation preview

State of the Nation’s Housing Markets

2nd Quarter 2010 Update

Kevin P. KaneChief Housing Market Analyst

Office of Policy Development and ResearchSpecial Thanks – Randall Goodnight (Ft. Worth)

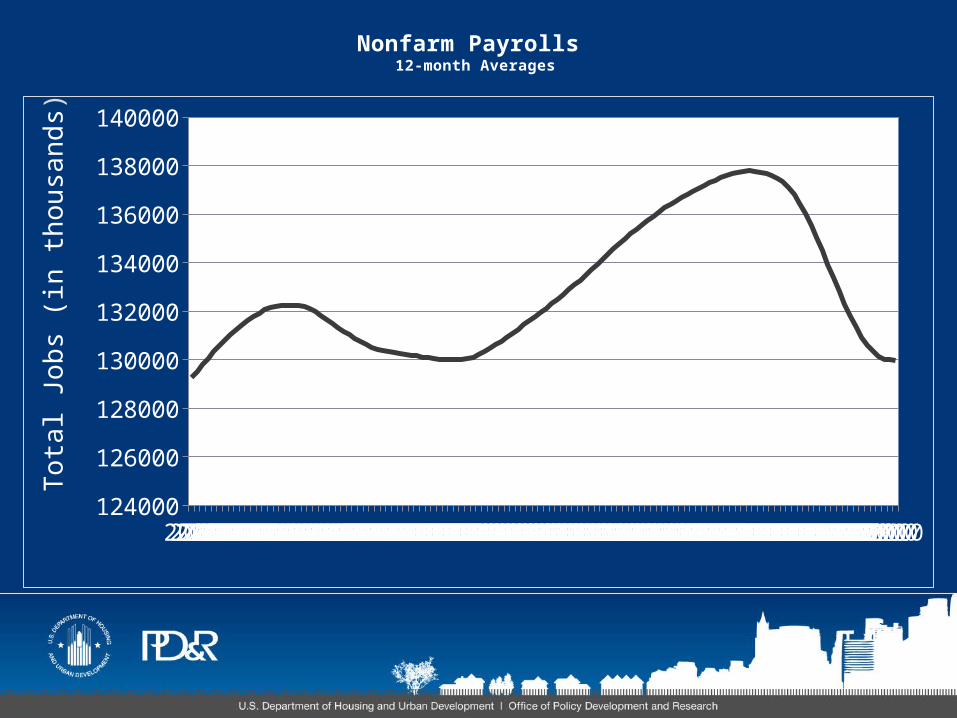

Nonfarm Payrolls 12-month Averages

200020002000200020002000200020002000200020002000200120012001200120012001200120012001200120012001200220022002200220022002200220022002200220022002200320032003200320032003200320032003200320032003200420042004200420042004200420042004200420042004200520052005200520052005200520052005200520052005200620062006200620062006200620062006200620062006200720072007200720072007200720072007200720072007200820082008200820082008200820082008200820082008200920092009200920092009200920092009200920092009201020102010201020102010124000

126000

128000

130000

132000

134000

136000

138000

140000

Tot

al J

obs

(in

thou

sand

s)

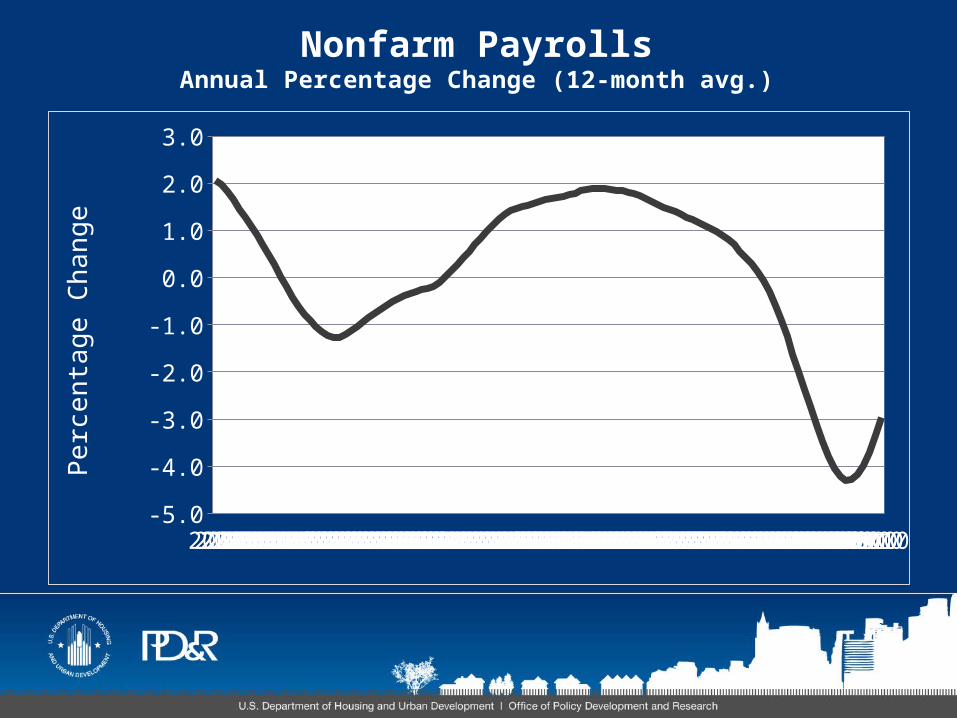

Nonfarm PayrollsAnnual Percentage Change (12-month avg.)

200120012001200120012001200120012001200120012001200220022002200220022002200220022002200220022002200320032003200320032003200320032003200320032003200420042004200420042004200420042004200420042004200520052005200520052005200520052005200520052005200620062006200620062006200620062006200620062006200720072007200720072007200720072007200720072007200820082008200820082008200820082008200820082008200920092009200920092009200920092009200920092009201020102010201020102010-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Per

cent

age

Cha

nge

Regional Nonfarm PayrollsPercentage Change 12 months ending June 2010

New E

nglan

d

Mid-

Atlant

ic

Midw

est

Great

Plai

ns

Pacific

-6-5-4-3-2-10

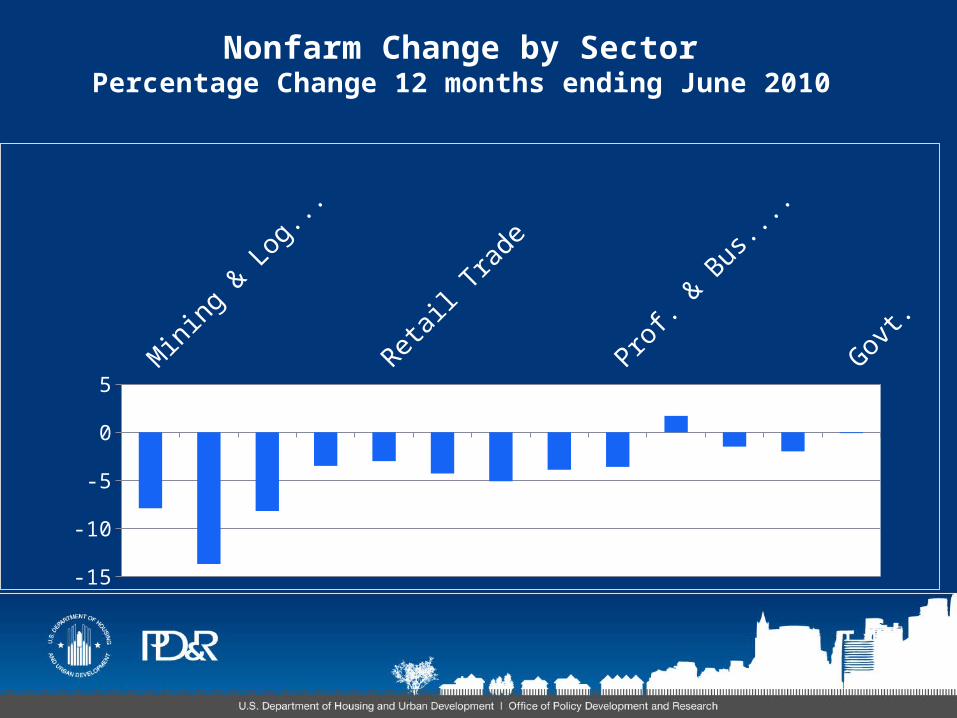

Nonfarm Change by SectorPercentage Change 12 months ending June 2010

Mini

ng &

Log

ging

Who

lesale

Tra

de

Info

rmat

ion

Ed. &

Hea

lth S

erv.

Govt.

-15

-10

-5

0

5

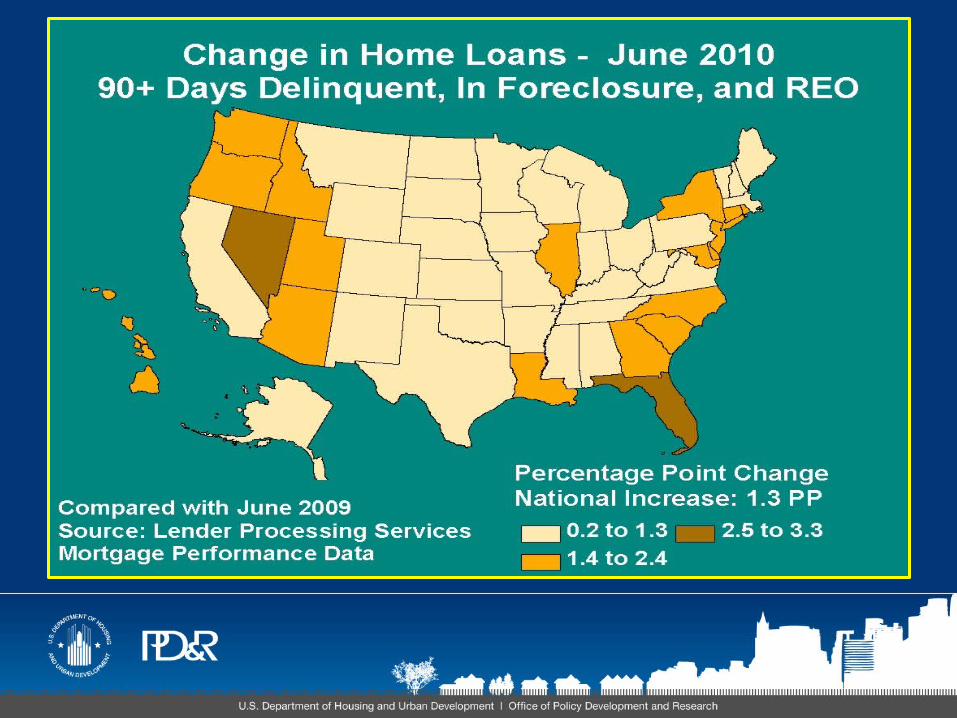

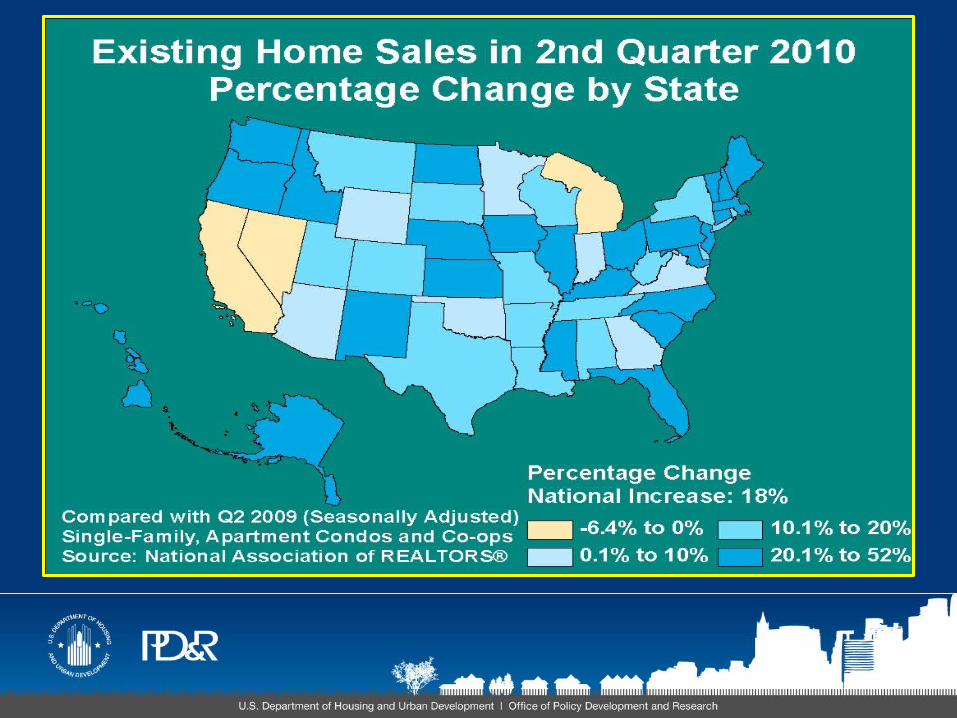

U.S. Housing Market Conditions: 2Q 2010 • Sales market conditions remain soft in much of the

country but continue to improve in many areas

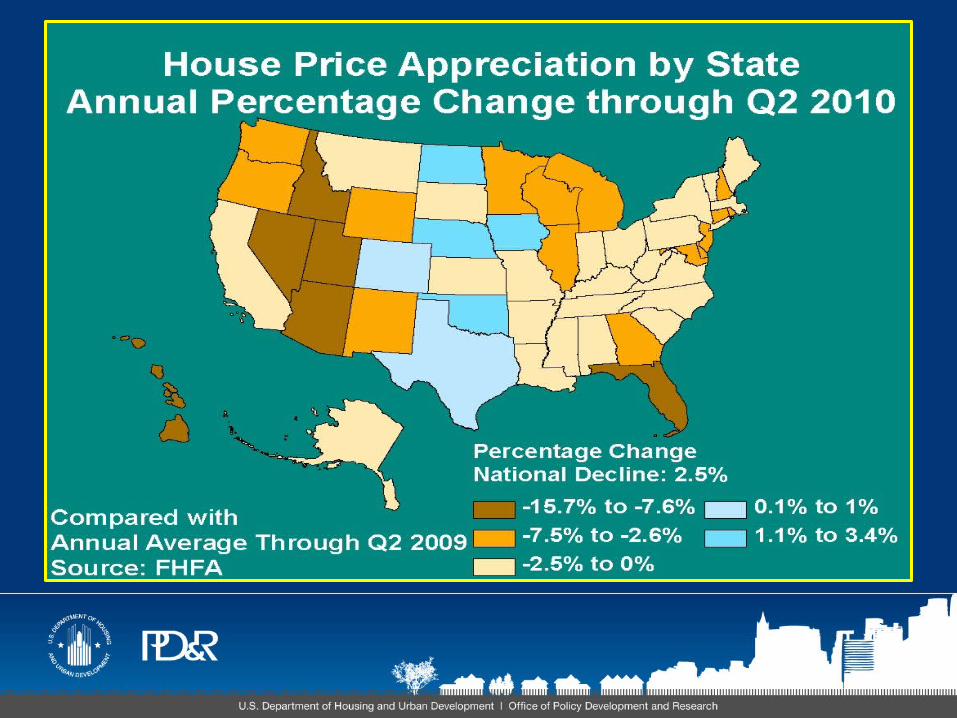

• Data on home sales prices indicate improvement

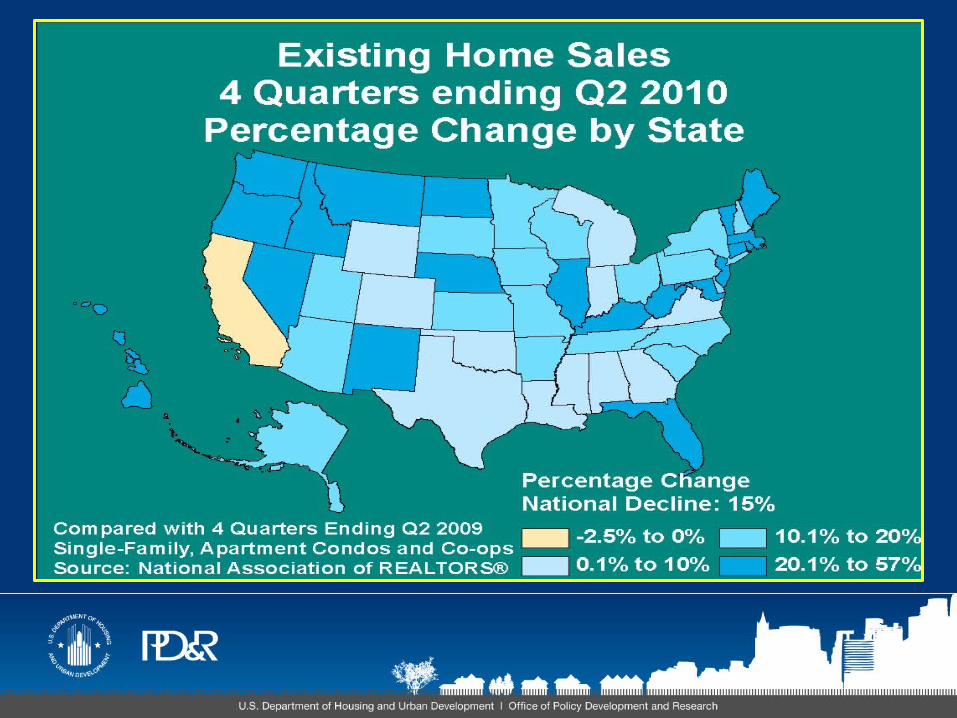

• Home sales are up (homebuyer tax credit)

• Inventories of new and existing homes for sale are down from a year ago and coming closer to balance

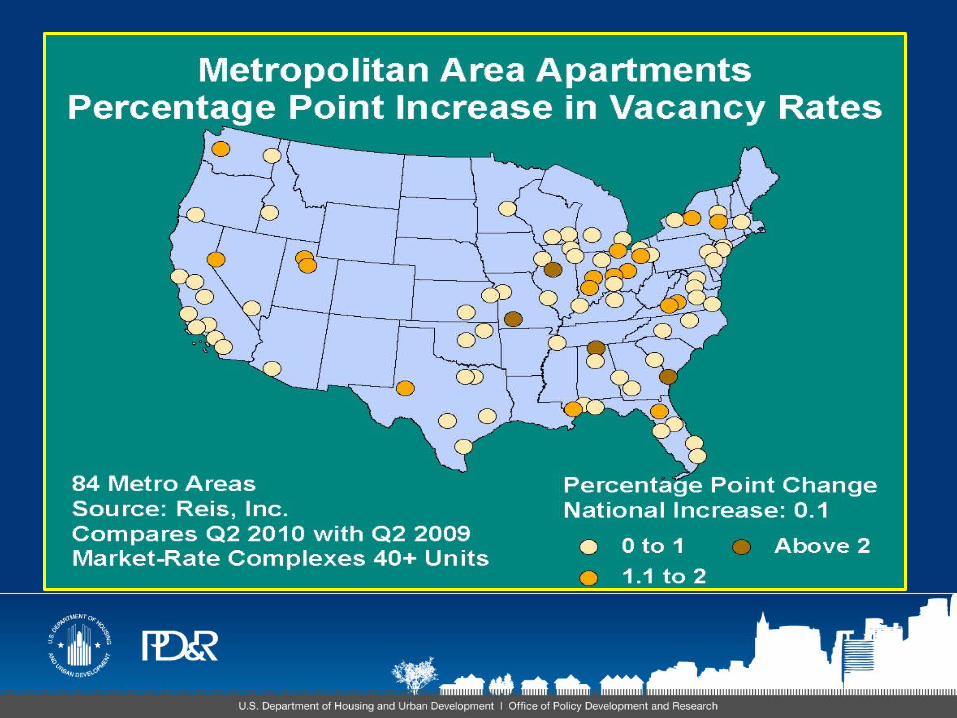

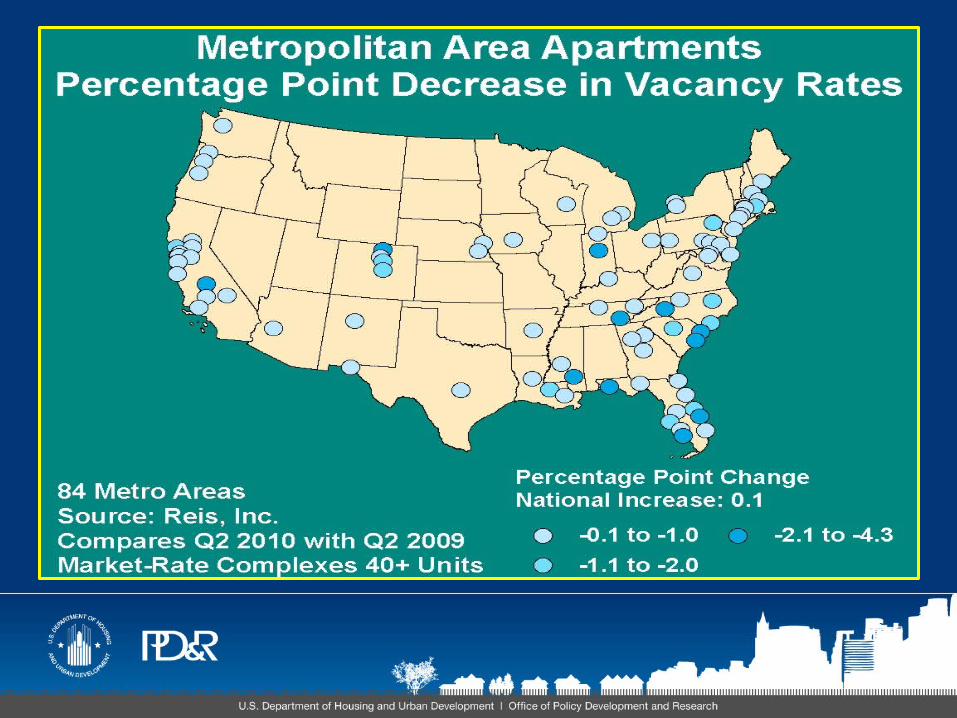

• Rental market conditions are mixed throughout the country

• Significant declines in multifamily permits have continued

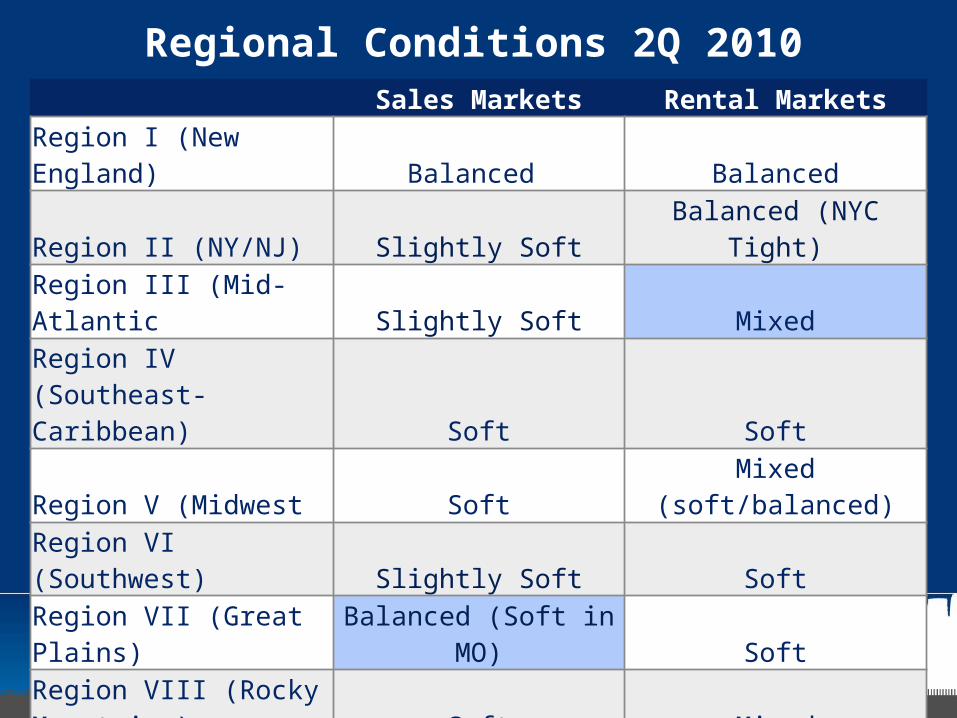

Regional Conditions 2Q 2010Sales Markets Rental Markets

Region I (New England) Balanced BalancedRegion II (NY/NJ) Slightly Soft Balanced (NYC Tight)Region III (Mid-Atlantic Slightly Soft MixedRegion IV (Southeast-Caribbean) Soft SoftRegion V (Midwest Soft Mixed (soft/balanced)Region VI (Southwest) Slightly Soft Soft

Region VII (Great Plains) Balanced (Soft in MO) SoftRegion VIII (Rocky Mountains) Soft MixedRegion IX (Pacific) Soft Mixed Region X (Northwest) Soft Balanced

National Home Price IndicesBased on Qtr. To Same Qtr. Previous Year

1992

1993

1995

1996

1998

1999

2001

2002

2004

2005

2007

2008

2010

-25.00-20.00-15.00-10.00

-5.000.005.00

10.0015.0020.00

S&P/Case-Schiller Price Index (NSA)

FHFA Purchase Only Index (SA)

% C

hang

e, y

ear

ago

SF Permit ActivityDuring 12 Months Ending

June-09 June-100

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

Percentage Change in SF Activity12 Months Ending 6/09 to 6/10

New E

ngland

New Y

ork-N

ew J

ersey

Mid

-Atla

ntic

Southeast-C

aribbean

Mid

west

Southw

est

Gre

at Pla

ins

Rocky Mounta

ins

Pacific

Northw

est0.0

5.0

10.0

15.0

20.0

MF Permit ActivityDuring 12 Months Ending

June-09 June-100

50,000

100,000

150,000

200,000

250,000

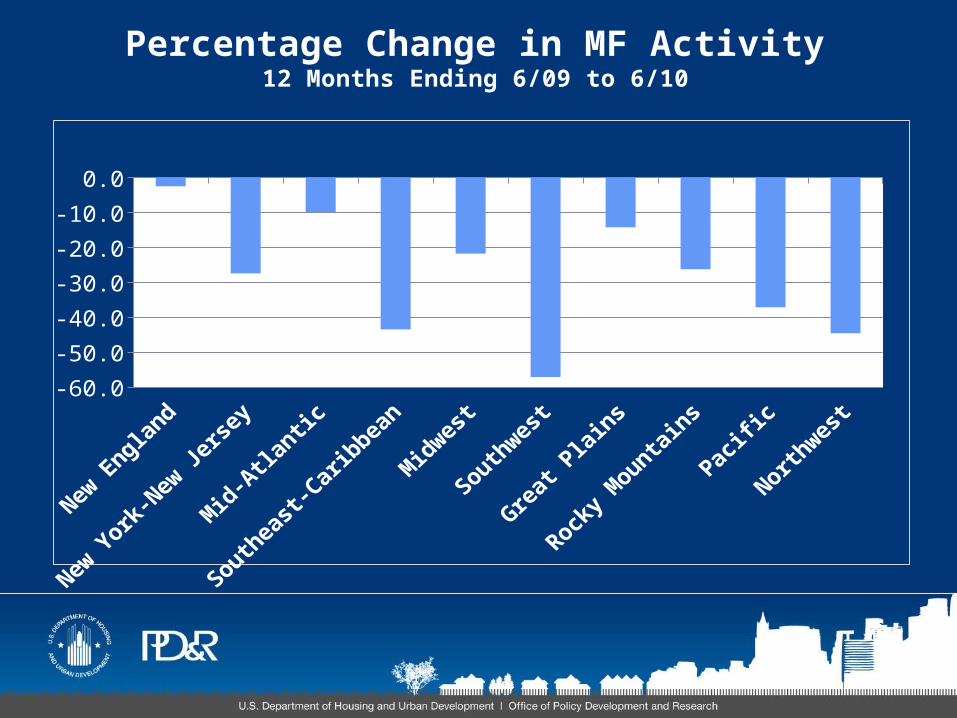

Percentage Change in MF Activity12 Months Ending 6/09 to 6/10

-60.0

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

For additional information:

• U.S. Housing Market Conditions Report 2Q 2010 available at www.huduser.org

• Contact your local Regional or Field Economist

• Contact me at [email protected]