Embed Size (px)

Citation preview

THE STATE OF GEORGETOWN 2016

C2 THE STATE OF GEORGETOWN 2016 REPORT

This report is a product of the staff of the Georgetown

Business Improvement District (BID). The judgments

herein do not necessarily reflect the views of the BID’s

Board of Directors or the members they represent.

Data for the State of Georgetown 2016 cover the

period January 1, 2015 to December 31, 2015, and

Q1 2016 where noted. The BID welcomes comments

and suggestions to improve this report and make

it more useful to readers. Please direct comments

to Jamie Scott, economic development manager,

about this reportcontents

3 Letter from the BID

4 Highlights and Trends

8 Resident Demographics

12 Visitor Profile and Spending

18 Retail and Restaurants

26 Office Market and Employees

34 Hotels

40 Transportation

Copyright © 2016 by the Georgetown Business Improvement District

RO

CK

CR

EE

K P

AR

KW

AY

RO

CK

CR

EE

K P

AR

KW

AY

N ST

N ST

DUMBARTON ST

O ST

O ST

P ST

P ST

VOLTA ST

Q ST

CAMBRIDGE PL

DENT PL

R ST

Q ST

R ST

DENT PL

RESERVOIR RD

PROSPECT ST

M ST

M ST

CADY’S ALLEY

WHITEHURST FWY

FR

AN

CIS

SC

OT

T K

EY

BR

IDG

E

BLUES ALLEY

WIS

CO

NSIN

AV

E

TH

OM

AS

JE

FF

ER

SO

N S

T

34

TH

ST

37

TH

ST

33

RD

ST

PO

TO

MA

C S

T

BA

NK

ST

31S

T S

T

30

TH

ST

29

TH

ST

28

TH

ST

27

TH

ST

32N

D S

T

35

TH

ST

36

TH

ST

WIS

CO

NSIN

AV

E

GEORGETOWN WATERFRONT PARK

C&O CANAL

K ST

POTOMAC RIVER

PO

TO

MA

C S

T

GRACE ST

PENNSYLVANIA AVE

PENNSYLVANIA AVE

WASHINGTON HARBOUR

The Georgetown BID Area

Source: Georgetown BID and data.octo.dc.gov THE STATE OF GEORGETOWN 2016 REPORT 1

THE STATE OF GEORGETOWN

2 THE STATE OF GEORGETOWN 2016 REPORT

THE STATE OF GEORGETOWN 2016 REPORT 3

LETTER FROM THE GEORGETOWN BID

Each year the Georgetown BID produces this State of Georgetown report to provide data and

analysis on key features of the Georgetown economy. We intend this report to be a resource for

BID members, brokers, community and government partners, and other audiences interested

in doing business in Georgetown. The State of Georgetown is an opportunity to analyze Georgetown’s

past performance and to consider its future in the city and regional economies.

Reflecting on the past year, we have many reasons to be optimistic about Georgetown’s future. After

years of high office vacancy, Georgetown was the strongest performing office submarket in the region

in 2015. The retail economy also showed strength as many new retailers opened in Georgetown or signed

leases to open in 2016. Visitors continued to shop, dine, and stay in Georgetown at strong levels, and the

commercial district remained a significant contributor to the District’s job and tax base.

But Georgetown is not immune to the dynamics of a changing city and economy, and as it has over the

course of its 265-year history, Georgetown must adapt. Georgetown merchants are competing in an

increasingly crowded marketplace, both online and across the region. Georgetown office buildings are

competing for tenants with submarkets that are awash in excess space—primarily in the suburbs. While

every established commercial district in the region has lost retail market share as new neighborhood

commercial districts emerge, population growth and spending patterns trending towards experiential

dining and shopping have kept sales strong. The BID, in collaboration with our members, residents,

and institutional and government partners, is working to ensure that we create and maintain a special

place that attracts both tenants and customers in the face of growing competition.

Earlier this year, we published a two-year update on Georgetown 2028, the 15-year action plan for

Georgetown. That plan continues to drive the BID’s agenda to preserve what’s great, fix what’s broken,

and create what’s missing to support a stronger and more sustainable commercial district. Through

interventions large and small we are working to make it easier to get to Georgetown and to create

a better experience for people once they’re here. This annual economic development report serves

as a complementary tool to understand Georgetown market performance year over year. We invite you

to read this report and additional resources, including the Georgetown 2028 two-year update report,

on our website, georgetowndc.com.

Joe Sternlieb

Georgetown BID CEO

Jamie Scott

Economic Development Manager

HIGHLIGHTS AND TRENDS

4 THE STATE OF GEORGETOWN 2016 REPORT

THE STATE OF GEORGETOWN 2016 REPORT 5

During calendar year 2015, Georgetown thrived as a vibrant

commercial district and continued to be a desirable place to work,

shop, and visit.

• Georgetown was the highest performing office submarket in the region in 2015,

with vacancy rates at 5.9%, due in part to average rental rates 16% lower than the

central business district.

• Retailer interest remained high. Georgetown saw online retailers opening brick-

and-mortar locations, including Birchbox and Warby Parker, and national brands

opening region-exclusive locations, including Sid Mashburn/Ann Mashburn.

• Retail vacancy increased in 2015, but many building owners began renovating

their spaces to bring in new retail tenants in 2016.

• Rising rents on M Street hastened the conversion of restaurants to retail, but new,

local restaurants opened on the side streets south of M Street, where rents are

lower, with more coming in 2016.

• The Georgetown BID, together with Advisory Neighborhood Commission (ANC)

2E and the Citizens Association of Georgetown (CAG), reached consensus on

ending the Georgetown liquor license cap and moratorium. (The ABC announced

the 27-year old moratorium would end on April 9th, 2016, just as this report was

going to press).

• Hotel performance was on par with 2014 performance, which saw rebounds over

the previous year in occupancy, and gains in revenue per available room and

total revenue.

6 THE STATE OF GEORGETOWN 2016 REPORT

ACCESS TO GEORGETOWN

Access is a critical element of the experience of working

in or visiting Georgetown. Improving access has the potential

to further strengthen Georgetown’s office, retail, and hotel

markets. To achieve this, the BID works with local and

regional partners to improve transportation services into and

within Georgetown.

In early 2016, the BID secured the final portion of the funding

for the Georgetown-Rosslyn Gondola feasibility study, to be

released later this year. The BID also installed six bike corrals

in Georgetown, creating capacity for an additional 60 bikes,

and Capital Bikeshare trips to and from Georgetown

increased for the third consecutive year. The H Street Streetcar

opened in February 2016, and the BID continues to advocate

for the extension of that line to Georgetown on dedicated

tracks that ensure a fast, reliable trip. Georgetown remains

an eminently walkable neighborhood, and the BID secured

approval to conduct sidewalk widenings on the 3200 block

of M Street for 30 weekends in 2016, providing more comfort

for pedestrians and shoppers.

The transportation landscape has also vastly changed with

the rise of Uber and other ridesharing services. These services

have, at least anecdotally, provided a seamless transportation

option to many Georgetown visitors, reducing the need

to drive and park. The evolution of ridesharing will continue

to influence the landscape of the Georgetown economy and

the use of public space.

ENHANCING THE GEORGETOWN EXPERIENCE

Consumers, visitors, and businesses continue to seek

authentic places and rich experiences. A healthy mix

of tenants and high quality space remains essential for

a successful commercial district, but experience is

increasingly important.

Employees increasingly want to work in buildings with

unique layouts and in a neighborhood with active outdoor

space, high quality restaurants beyond the typical business

lunch, and nighttime activities after work. For consumers,

particularly millennial consumers, dining is a major form

of entertainment, and they want to eat interesting food in

unique spaces. As more shoppers make internet purchases,

brick-and-mortar retailers can offer personal experiences

that do not exist online. Millennial consumers are also

less brand-loyal, and place value on brand narrative and

authenticity. Visitors staying in Georgetown hotels want

personalized—and local—services and experiences. And as

the District’s population and tourism continue to grow,

residents and visitors alike are seeking outdoor spaces that

provide recreational activities and a respite from the density

of urban life.

The BID continues to work on these items, and to integrate

the employee, consumer, and visitor experience with

Georgetown’s beautiful and historic public spaces.

THE STATE OF GEORGETOWN 2016 REPORT 7

DC RETAIL MARKET TRENDS

The District continued to experience a boom in retail and

restaurants in 2015, evidenced by new openings on 14th

Street, at The Shay and Atlantic Plumbing buildings in Shaw,

and in CityCenter, Union Market, Capitol Riverfront, and

beyond. Georgetown, long the primary neighborhood for

shopping and dining, faces increasing competition from other

neighborhoods. More than 700,000 square feet of retail

delivered across the city in 2015 and another 1.5 million

square feet are under construction for delivery by 2017.1

New neighborhoods have emerged as dining and shopping

destinations, with more to come at the Southwest Waterfront,

Capitol Riverfront, Union Market, Ivy City, and beyond.

Economic shifts are providing new opportunities for local

entrepreneurs offering food, drinks, and products made

in the District. In December 2015 Councilmember Charles

Allen (D-Ward 6) introduced the Made in DC Program

Establishment Act of 2015 to support locally designed and

manufactured products. The success of Union Kitchen, Union

Market, and other local markets, events, and food incubators

demonstrates the potential of this growing sector of the

District’s economy. Georgetown, as a proven commercial

district rich in local history and populated with unique spaces,

is an attractive location for new local businesses looking for

brick-and-mortar locations.

8 THE STATE OF GEORGETOWN 2016 REPORT

RESIDENTDEMOGRAPHICS

THE STATE OF GEORGETOWN 2016 REPORT 9

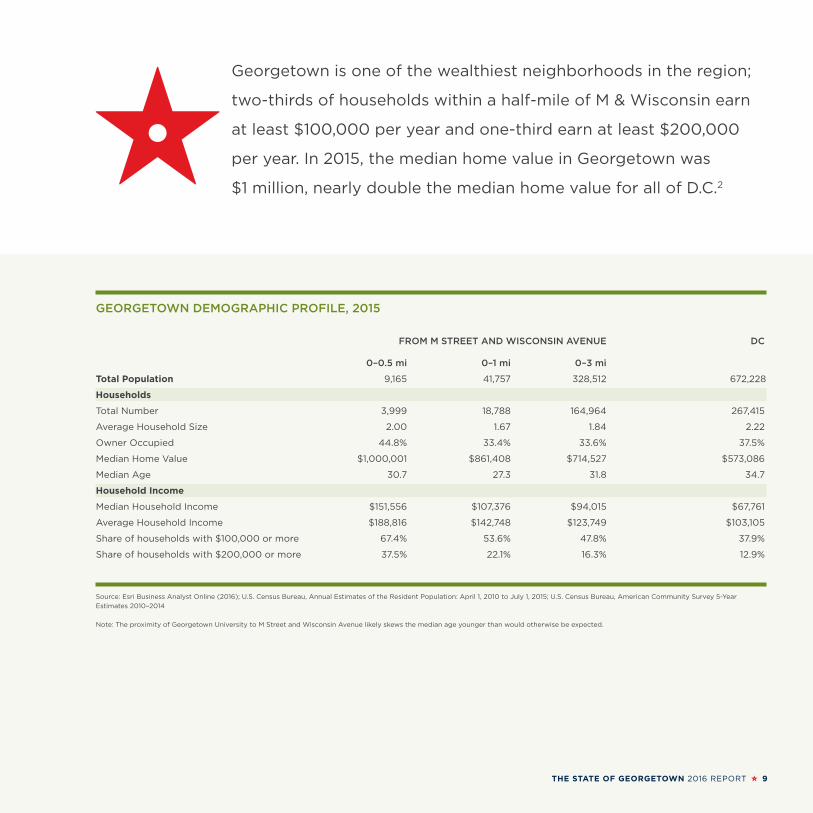

GEORGETOWN DEMOGRAPHIC PROFILE, 2015

FROM M STREET AND WISCONSIN AVENUE DC

0–0.5 mi 0–1 mi 0–3 mi

Total Population 9,165 41,757 328,512 672,228

Households

Total Number 3,999 18,788 164,964 267,415

Average Household Size 2.00 1.67 1.84 2.22

Owner Occupied 44.8% 33.4% 33.6% 37.5%

Median Home Value $1,000,001 $861,408 $714,527 $573,086

Median Age 30.7 27.3 31.8 34.7

Household Income

Median Household Income $151,556 $107,376 $94,015 $67,761

Average Household Income $188,816 $142,748 $123,749 $103,105

Share of households with $100,000 or more 67.4% 53.6% 47.8% 37.9%

Share of households with $200,000 or more 37.5% 22.1% 16.3% 12.9%

Source: Esri Business Analyst Online (2016); U.S. Census Bureau, Annual Estimates of the Resident Population: April 1, 2010 to July 1, 2015; U.S. Census Bureau, American Community Survey 5-Year

Estimates 2010–2014

Note: The proximity of Georgetown University to M Street and Wisconsin Avenue likely skews the median age younger than would otherwise be expected.

Georgetown is one of the wealthiest neighborhoods in the region;

two-thirds of households within a half-mile of M & Wisconsin earn

at least $100,000 per year and one-third earn at least $200,000

per year. In 2015, the median home value in Georgetown was

$1 million, nearly double the median home value for all of D.C.2

10 THE STATE OF GEORGETOWN 2016 REPORT

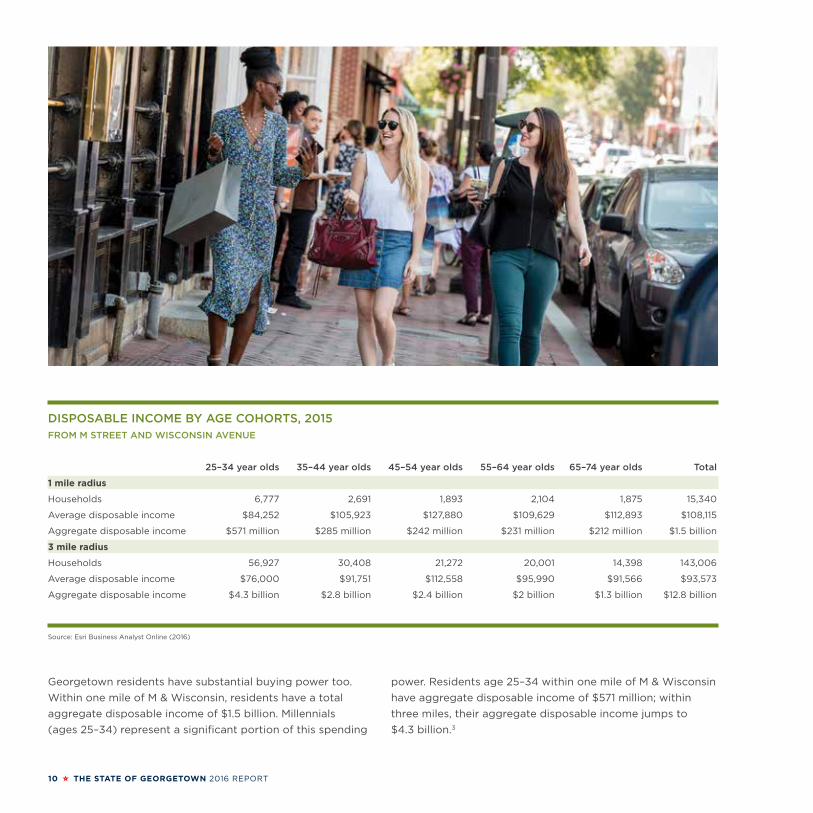

DISPOSABLE INCOME BY AGE COHORTS, 2015 FROM M STREET AND WISCONSIN AVENUE

25–34 year olds 35–44 year olds 45–54 year olds 55–64 year olds 65–74 year olds Total

1 mile radius

Households 6,777 2,691 1,893 2,104 1,875 15,340

Average disposable income $84,252 $105,923 $127,880 $109,629 $112,893 $108,115

Aggregate disposable income $571 million $285 million $242 million $231 million $212 million $1.5 billion

3 mile radius

Households 56,927 30,408 21,272 20,001 14,398 143,006

Average disposable income $76,000 $91,751 $112,558 $95,990 $91,566 $93,573

Aggregate disposable income $4.3 billion $2.8 billion $2.4 billion $2 billion $1.3 billion $12.8 billion

Source: Esri Business Analyst Online (2016)

Georgetown residents have substantial buying power too.

Within one mile of M & Wisconsin, residents have a total

aggregate disposable income of $1.5 billion. Millennials

(ages 25–34) represent a significant portion of this spending

power. Residents age 25–34 within one mile of M & Wisconsin

have aggregate disposable income of $571 million; within

three miles, their aggregate disposable income jumps to

$4.3 billion.3

THE STATE OF GEORGETOWN 2016 REPORT 11

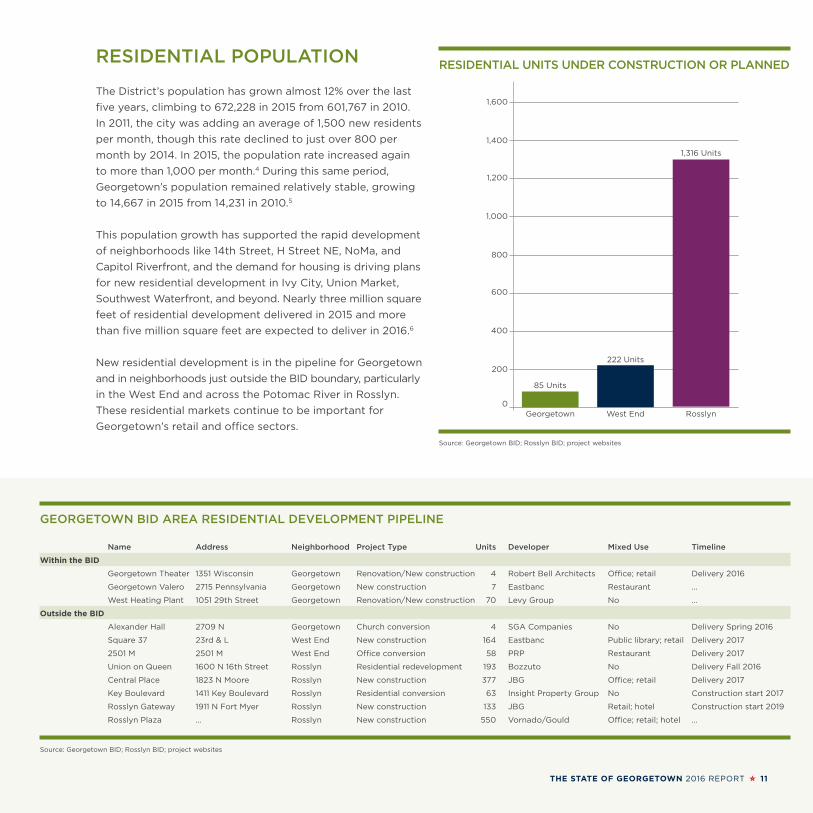

RESIDENTIAL POPULATION

The District’s population has grown almost 12% over the last

five years, climbing to 672,228 in 2015 from 601,767 in 2010.

In 2011, the city was adding an average of 1,500 new residents

per month, though this rate declined to just over 800 per

month by 2014. In 2015, the population rate increased again

to more than 1,000 per month.4 During this same period,

Georgetown’s population remained relatively stable, growing

to 14,667 in 2015 from 14,231 in 2010.5

This population growth has supported the rapid development

of neighborhoods like 14th Street, H Street NE, NoMa, and

Capitol Riverfront, and the demand for housing is driving plans

for new residential development in Ivy City, Union Market,

Southwest Waterfront, and beyond. Nearly three million square

feet of residential development delivered in 2015 and more

than five million square feet are expected to deliver in 2016.6

New residential development is in the pipeline for Georgetown

and in neighborhoods just outside the BID boundary, particularly

in the West End and across the Potomac River in Rosslyn.

These residential markets continue to be important for

Georgetown’s retail and office sectors.

GEORGETOWN BID AREA RESIDENTIAL DEVELOPMENT PIPELINE

Name Address Neighborhood Project Type Units Developer Mixed Use Timeline

Within the BID

Georgetown Theater 1351 Wisconsin Georgetown Renovation/New construction 4 Robert Bell Architects Office; retail Delivery 2016

Georgetown Valero 2715 Pennsylvania Georgetown New construction 7 Eastbanc Restaurant …

West Heating Plant 1051 29th Street Georgetown Renovation/New construction 70 Levy Group No …

Outside the BID

Alexander Hall 2709 N Georgetown Church conversion 4 SGA Companies No Delivery Spring 2016

Square 37 23rd & L West End New construction 164 Eastbanc Public library; retail Delivery 2017

2501 M 2501 M West End Office conversion 58 PRP Restaurant Delivery 2017

Union on Queen 1600 N 16th Street Rosslyn Residential redevelopment 193 Bozzuto No Delivery Fall 2016

Central Place 1823 N Moore Rosslyn New construction 377 JBG Office; retail Delivery 2017

Key Boulevard 1411 Key Boulevard Rosslyn Residential conversion 63 Insight Property Group No Construction start 2017

Rosslyn Gateway 1911 N Fort Myer Rosslyn New construction 133 JBG Retail; hotel Construction start 2019

Rosslyn Plaza … Rosslyn New construction 550 Vornado/Gould Office; retail; hotel …

Source: Georgetown BID; Rosslyn BID; project websites

RESIDENTIAL UNITS UNDER CONSTRUCTION OR PLANNED

Source: Georgetown BID; Rosslyn BID; project websites

1,600

1,400

1,200

1,000

800

600

400

200

0Georgetown West End Rosslyn

85 Units

222 Units

1,316 Units

12 THE STATE OF GEORGETOWN 2016 REPORT

VISITOR PROFILE AND SPENDING

SPENDING IN GEORGETOWN% OF GLOBAL CREDIT CARD SPENDING

District of Columbia Visitors DC Region Visitors Domestic Visitors, outside DC Region International Visitors

Location % of Total Spend Location % of Total Spend Location % of Total Spend Location % of Total Spend % of International Spend

20007 8% District of Columbia 29% New York/Northern NJ 4% United Kingdom 1% 11%

20016 4% Maryland Suburbs 10% Baltimore-Towson 2% Canada 1% 8%

20009 3% Virginia Suburbs 19% LA Long Beach 2% China 0.4% 6%

20008 3% Boston-Cambridge 2% France 0.4% 6%

20037 2% Philadelphia 1% Brazil 0.3% 5%

Rest of DC 9% San Francisco-Oakland 1% United Arab Emirates 0.2% 3.5%

Miami-Ft. Lauderdale 1% Other 4% 61.5%

Chicago 1%

Seattle 1%

Other 20%

DC 29% Region 58% Domestic 35% International 7%

Source: Buxton (2015)

Note: Percentages are derived from credit card purchase data for purchases made between October 1, 2013 and September 30, 2014

THE STATE OF GEORGETOWN 2016 REPORT 13

An estimated 26 percent of Georgetown visitors come from the

top three percent of America’s most affluent households, which

have annual discretionary incomes of at least $32,000.7 Among

DC-region residents, an estimated 22 percent of Georgetown

spending comes from residents in the top 50 wealthiest zip codes.8

These data are from credit card transactions within the Georgetown BID during

the period October 1, 2013–September 30, 2014, which we estimate represents

approximately 60% of credit card spending in Georgetown. We do not expect the

data to change significantly year over year, and we will report updated data from

2015–2016 in the State of Georgetown 2017.

14 THE STATE OF GEORGETOWN 2016 REPORT

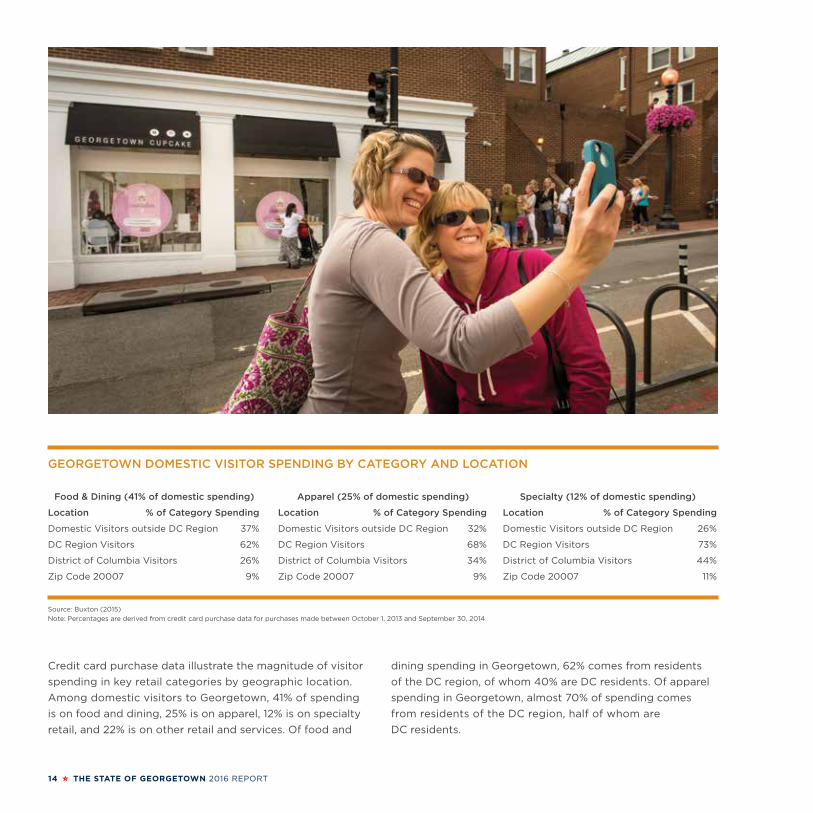

Credit card purchase data illustrate the magnitude of visitor

spending in key retail categories by geographic location.

Among domestic visitors to Georgetown, 41% of spending

is on food and dining, 25% is on apparel, 12% is on specialty

retail, and 22% is on other retail and services. Of food and

GEORGETOWN DOMESTIC VISITOR SPENDING BY CATEGORY AND LOCATION

Food & Dining (41% of domestic spending) Apparel (25% of domestic spending) Specialty (12% of domestic spending)

Location % of Category Spending Location % of Category Spending Location % of Category Spending

Domestic Visitors outside DC Region 37% Domestic Visitors outside DC Region 32% Domestic Visitors outside DC Region 26%

DC Region Visitors 62% DC Region Visitors 68% DC Region Visitors 73%

District of Columbia Visitors 26% District of Columbia Visitors 34% District of Columbia Visitors 44%

Zip Code 20007 9% Zip Code 20007 9% Zip Code 20007 11%

Source: Buxton (2015)

Note: Percentages are derived from credit card purchase data for purchases made between October 1, 2013 and September 30, 2014

dining spending in Georgetown, 62% comes from residents

of the DC region, of whom 40% are DC residents. Of apparel

spending in Georgetown, almost 70% of spending comes

from residents of the DC region, half of whom are

DC residents.

THE STATE OF GEORGETOWN 2016 REPORT 15

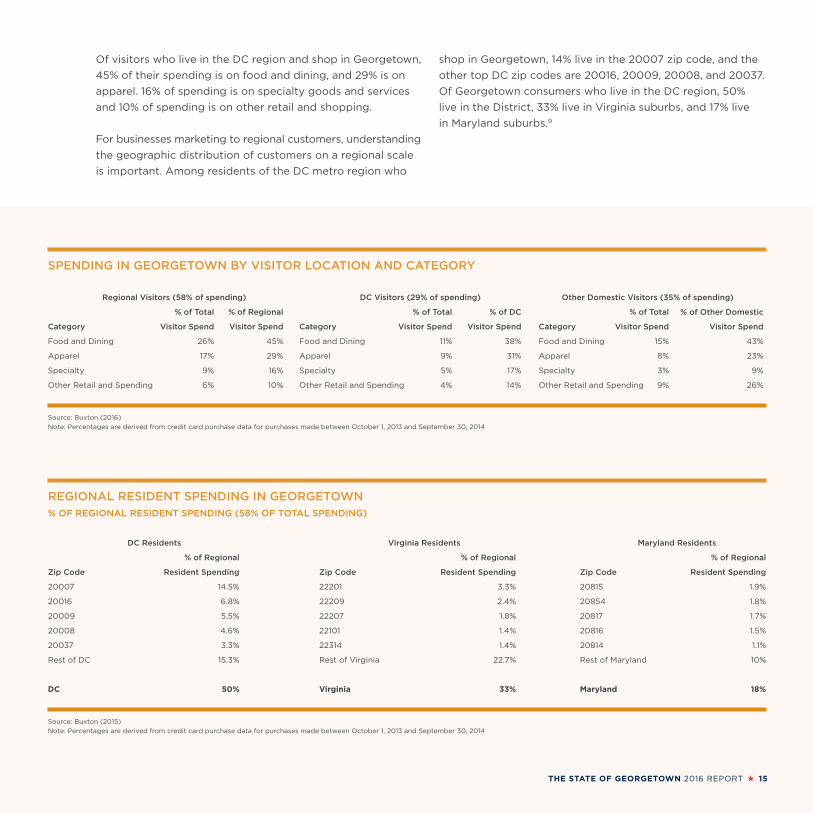

Of visitors who live in the DC region and shop in Georgetown,

45% of their spending is on food and dining, and 29% is on

apparel. 16% of spending is on specialty goods and services

and 10% of spending is on other retail and shopping.

For businesses marketing to regional customers, understanding

the geographic distribution of customers on a regional scale

is important. Among residents of the DC metro region who

SPENDING IN GEORGETOWN BY VISITOR LOCATION AND CATEGORY

Regional Visitors (58% of spending) DC Visitors (29% of spending) Other Domestic Visitors (35% of spending)

% of Total % of Regional % of Total % of DC % of Total % of Other Domestic

Category Visitor Spend Visitor Spend Category Visitor Spend Visitor Spend Category Visitor Spend Visitor Spend

Food and Dining 26% 45% Food and Dining 11% 38% Food and Dining 15% 43%

Apparel 17% 29% Apparel 9% 31% Apparel 8% 23%

Specialty 9% 16% Specialty 5% 17% Specialty 3% 9%

Other Retail and Spending 6% 10% Other Retail and Spending 4% 14% Other Retail and Spending 9% 26%

Source: Buxton (2016)

Note: Percentages are derived from credit card purchase data for purchases made between October 1, 2013 and September 30, 2014

REGIONAL RESIDENT SPENDING IN GEORGETOWN% OF REGIONAL RESIDENT SPENDING (58% OF TOTAL SPENDING)

DC Residents Virginia Residents Maryland Residents

% of Regional % of Regional % of Regional

Zip Code Resident Spending Zip Code Resident Spending Zip Code Resident Spending

20007 14.5% 22201 3.3% 20815 1.9%

20016 6.8% 22209 2.4% 20854 1.8%

20009 5.5% 22207 1.8% 20817 1.7%

20008 4.6% 22101 1.4% 20816 1.5%

20037 3.3% 22314 1.4% 20814 1.1%

Rest of DC 15.3% Rest of Virginia 22.7% Rest of Maryland 10%

DC 50% Virginia 33% Maryland 18%

Source: Buxton (2015)

Note: Percentages are derived from credit card purchase data for purchases made between October 1, 2013 and September 30, 2014

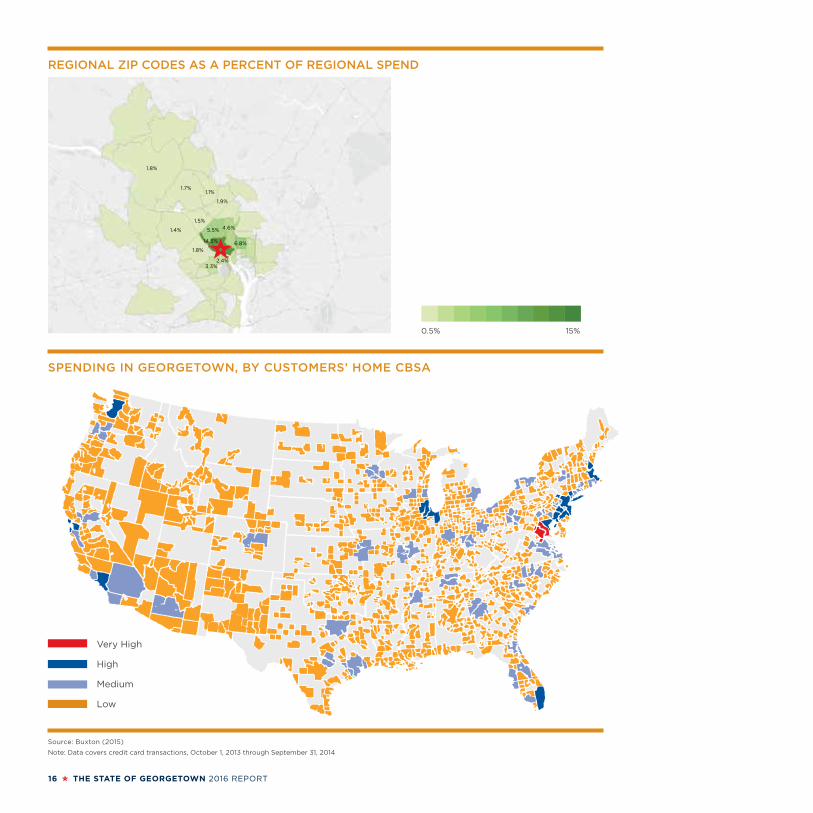

shop in Georgetown, 14% live in the 20007 zip code, and the

other top DC zip codes are 20016, 20009, 20008, and 20037.

Of Georgetown consumers who live in the DC region, 50%

live in the District, 33% live in Virginia suburbs, and 17% live

in Maryland suburbs.9

16 THE STATE OF GEORGETOWN 2016 REPORT

REGIONAL ZIP CODES AS A PERCENT OF REGIONAL SPEND

Very High

High

Medium

Low

SPENDING IN GEORGETOWN, BY CUSTOMERS’ HOME CBSA

Source: Buxton (2015)

Note: Data covers credit card transactions, October 1, 2013 through September 31, 2014

0.5% 15%

1.8%

1.7%1.1%

1.9%

1.5%

1.4%

1.8%

2.4%3.3%

5.5%

14.5% 6.8%

4.6%

THE STATE OF GEORGETOWN 2016 REPORT 17

TOP GEORGETOWN MARKET SEGMENTS SHARE OF DISCRETIONARY NO 3+

MARKET SEGMENT MARKET INCOME AGE CARS CARS PYSCHOGRAPHIC DESCRIPTION

Wealthy, influential, and 13% $32,000+ 51–65 18% 65% Put in long work days, but after hours like to soak

successful couples and up culture and nightlife. Typically the target market

families living in for expensive brands of cars, furnishings, and jewelry;

prestigious suburbs inconspicuous consumption is a foreign concept.

Idea of shopping is having a personal sales clerk at

a boutique or speciality store. Also patronize a wide

range of retailers, including upscale department

stores like Nordstrom and discount chains such as

Marshall’s and T.J. Maxx.

Younger, up-and-coming 14% $16-19,000 31–35 52% 16% Spend free time in local stores, restaurants and

singles living big city cultural venues. More than three times as likely to

lifestyles located within patronize bars and nightclubs. Avoid mainstream

top CBSA markets retailers, preferring local boutiques to any big-box

store. Try to keep within their budget and do not

devote much time to shopping. They take public

transportation and prefer not to travel distances

to shop or spend a long time browsing.

Wealthy and established 8% $32,000+ 66–75 14% 71% Make time for cultured and athletic pursuit. Like to

empty-nesting couples buy popular brands with reputations for being high

residing in suburban and quality and cutting edge. Frequent stores that offer

in-town homes designer apparel and high-end accessories. Lead

busy, time-pressed lives, so also turn to catalogs

and websites. Appreciate the thrill of the bargain

hunt at Marshall’s, T.J. Maxx, Costco, and Best Buy.

Young multi-ethnic singles 7% $6–7,000 25–30 54% 14% Active in the dating scene and often go out at night

living in midwest and to bars, restaurants, cinemas, dance performances

southern city centers and concerts featuring all kinds of music. Limited

budgets, but fond of shopping. Typically use the

Internet to plan a major shopping excursion. Can’t

afford high-end stores, but patronize mall boutiques

like Victoria’s Secret, Abercrombie & Fitch, Ann Taylor

and Banana Republic when they’re running sales.

Mature, upscale couples 7% $32,000+ 66–75 18% 56% With the luxury of both time and money, pursue

and singles in suburban leisure-intensive lifestyles. Like to dine out, go to

homes plays and concerts and shop for decorative antiques.

Don’t mind paying extra for high-quality goods and

brands they’ve known for decades. Fondness for

decorating their homes with purchases from

Williams-Sonoma and Crate and Barrel. Also buy

a wide variety of items through catalogs. Like to

drive hybrid, imported and premium cars.

Source: Buxton (2015) and Experian

18 THE STATE OF GEORGETOWN 2016 REPORT

RETAIL ANDRESTAURANTS

THE STATE OF GEORGETOWN 2016 REPORT 19

Georgetown remains the premier retail district in the region, with

450+ retailers to suit the needs of every shopper.

Region-exclusives: As one of the top shopping destinations in the

region, Georgetown is home to a large collection of region-exclusive retail locations,

including Alice & Olivia, AllSaints, Billy Reid, CB2, Frye, Gant, Goorin Bros. Hat Shop,

Ike Behar, John Fluevog, Jonathan Adler, Massimo Dutti, Rag and Bone, Rent the

Runway, Sid Mashburn/Ann Mashburn, Suitsupply, and Tory Burch.

Clicks to bricks: Online retailers find Georgetown an ideal place to open new

brick-and-mortar locations, with recent openings including Birchbox, Ledbury,

Tuckernuck (opening 2016), and Warby Parker.

Retail incubator: A number of iconic brands were born in Georgetown, including

Bluemercury, Georgetown Cupcake, SweetGreen, and Clyde’s, as well as rapidly

expanding regional favorites like DolceZZa and Baked & Wired.

Category leadership: Georgetown is the premier retail district for many products

and services, including athleisure wear, sneakers, specialty desserts, men’s fashion,

women’s fashion, vintage, bridal, salons, fitness studios, and home design.

Growing restaurant scene: The restaurant market saw new energy in 2015 and Q1

2016. New local restaurants and new concepts opened in Georgetown, including

Chaia Taco, Via Umbria, Sovereign, and Bar à Vin, with more to come in 2016.

Liquor License Moratorium: In 2015 the BID partnered with Advisory Neighborhood

Commission 2E (ANC) and the Citizens Association of Georgetown (CAG) to reach

a consensus approach to ending the Georgetown liquor license moratorium.

20 THE STATE OF GEORGETOWN 2016 REPORT

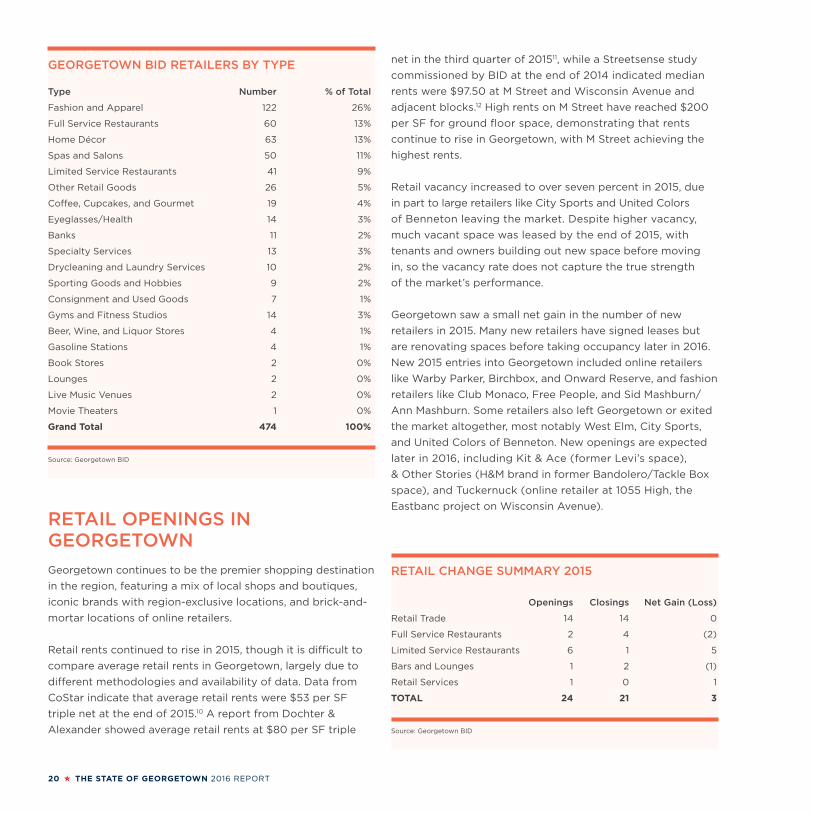

GEORGETOWN BID RETAILERS BY TYPE

Type Number % of Total

Fashion and Apparel 122 26%

Full Service Restaurants 60 13%

Home Décor 63 13%

Spas and Salons 50 11%

Limited Service Restaurants 41 9%

Other Retail Goods 26 5%

Coffee, Cupcakes, and Gourmet 19 4%

Eyeglasses/Health 14 3%

Banks 11 2%

Specialty Services 13 3%

Drycleaning and Laundry Services 10 2%

Sporting Goods and Hobbies 9 2%

Consignment and Used Goods 7 1%

Gyms and Fitness Studios 14 3%

Beer, Wine, and Liquor Stores 4 1%

Gasoline Stations 4 1%

Book Stores 2 0%

Lounges 2 0%

Live Music Venues 2 0%

Movie Theaters 1 0%

Grand Total 474 100%

Source: Georgetown BID

RETAIL CHANGE SUMMARY 2015

Openings Closings Net Gain (Loss)

Retail Trade 14 14 0

Full Service Restaurants 2 4 (2)

Limited Service Restaurants 6 1 5

Bars and Lounges 1 2 (1)

Retail Services 1 0 1

TOTAL 24 21 3

Source: Georgetown BID

RETAIL OPENINGS IN GEORGETOWN

Georgetown continues to be the premier shopping destination

in the region, featuring a mix of local shops and boutiques,

iconic brands with region-exclusive locations, and brick-and-

mortar locations of online retailers.

Retail rents continued to rise in 2015, though it is difficult to

compare average retail rents in Georgetown, largely due to

different methodologies and availability of data. Data from

CoStar indicate that average retail rents were $53 per SF

triple net at the end of 2015.10 A report from Dochter &

Alexander showed average retail rents at $80 per SF triple

net in the third quarter of 201511, while a Streetsense study

commissioned by BID at the end of 2014 indicated median

rents were $97.50 at M Street and Wisconsin Avenue and

adjacent blocks.12 High rents on M Street have reached $200

per SF for ground floor space, demonstrating that rents

continue to rise in Georgetown, with M Street achieving the

highest rents.

Retail vacancy increased to over seven percent in 2015, due

in part to large retailers like City Sports and United Colors

of Benneton leaving the market. Despite higher vacancy,

much vacant space was leased by the end of 2015, with

tenants and owners building out new space before moving

in, so the vacancy rate does not capture the true strength

of the market’s performance.

Georgetown saw a small net gain in the number of new

retailers in 2015. Many new retailers have signed leases but

are renovating spaces before taking occupancy later in 2016.

New 2015 entries into Georgetown included online retailers

like Warby Parker, Birchbox, and Onward Reserve, and fashion

retailers like Club Monaco, Free People, and Sid Mashburn/

Ann Mashburn. Some retailers also left Georgetown or exited

the market altogether, most notably West Elm, City Sports,

and United Colors of Benneton. New openings are expected

later in 2016, including Kit & Ace (former Levi’s space),

& Other Stories (H&M brand in former Bandolero/Tackle Box

space), and Tuckernuck (online retailer at 1055 High, the

Eastbanc project on Wisconsin Avenue).

THE STATE OF GEORGETOWN 2016 REPORT 21

GEORGETOWN BID RETAIL OPENINGS AND CLOSINGS, 2015

2015 OPENINGS 2015 CLOSINGS

RETAIL Calligaris Kate Spade Saturday

Circa Lighting True Religion

Vaporfi Duo

Lynn Louisa Sabun Home

Free People Urban Chic

Sid Mashburn/Ann Mashburn Britt Ryan

Warby Parker Metro Interiors

Francesca’s Jack Wills

Onward Reserve West Elm

Georgetown Olive Oil Company Pedini

Club Monaco All We Art

Birchbox United Colors of Benetton

Thos. Moser (new location) City Sports

Little Birdie’s (new location) Helia’s

FULL SERVICE RESTAURANTS Orange Anchor Tackle Box

Maxime Steak Frites Yummi Crawfish

Mama Rouge

Rialto

LIMITED SERVICE RESTAURANTS Via Umbria (expanded eating space) Little Penguin

Chaia Farm to Taco

Postmodern Foods

Red Toque Café

Curry & Pie

Crumbs & Whiskers

BARS AND LOUNGES The Alex Rhino Bar and Pumphouse

Prince Café

RETAIL SERVICES Soulcycle

POPUPS American Field

Madda Fella

Source: Georgetown BID

22 THE STATE OF GEORGETOWN 2016 REPORT

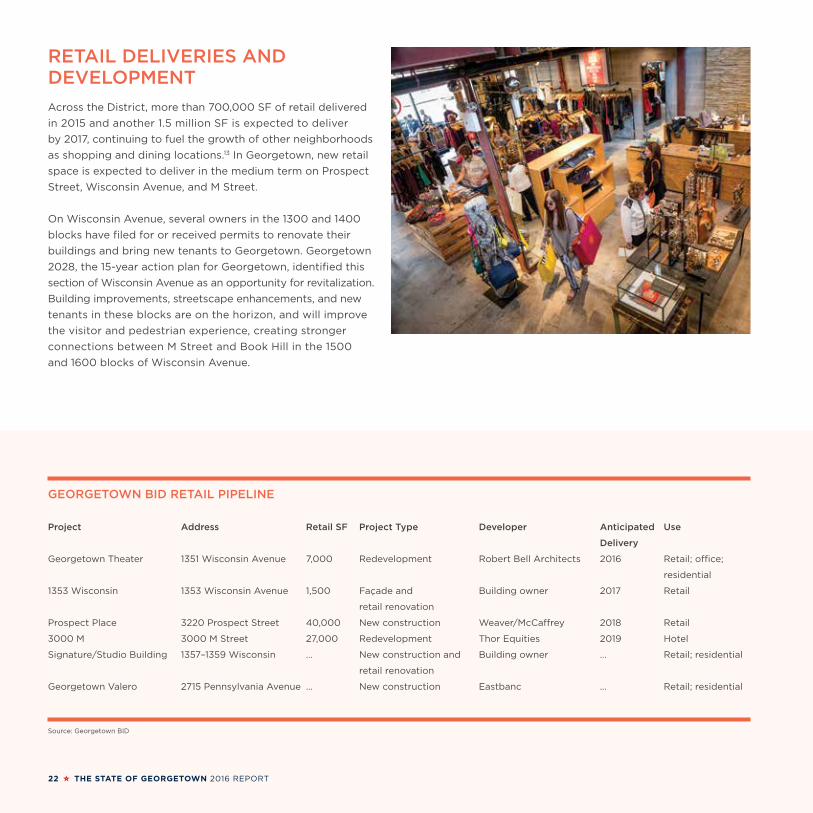

RETAIL DELIVERIES AND DEVELOPMENT

Across the District, more than 700,000 SF of retail delivered

in 2015 and another 1.5 million SF is expected to deliver

by 2017, continuing to fuel the growth of other neighborhoods

as shopping and dining locations.13 In Georgetown, new retail

space is expected to deliver in the medium term on Prospect

Street, Wisconsin Avenue, and M Street.

On Wisconsin Avenue, several owners in the 1300 and 1400

blocks have filed for or received permits to renovate their

buildings and bring new tenants to Georgetown. Georgetown

2028, the 15-year action plan for Georgetown, identified this

section of Wisconsin Avenue as an opportunity for revitalization.

Building improvements, streetscape enhancements, and new

tenants in these blocks are on the horizon, and will improve

the visitor and pedestrian experience, creating stronger

connections between M Street and Book Hill in the 1500

and 1600 blocks of Wisconsin Avenue.

GEORGETOWN BID RETAIL PIPELINE

Project Address Retail SF Project Type Developer Anticipated Use

Delivery

Georgetown Theater 1351 Wisconsin Avenue 7,000 Redevelopment Robert Bell Architects 2016 Retail; office;

residential

1353 Wisconsin 1353 Wisconsin Avenue 1,500 Façade and Building owner 2017 Retail

retail renovation

Prospect Place 3220 Prospect Street 40,000 New construction Weaver/McCaffrey 2018 Retail

3000 M 3000 M Street 27,000 Redevelopment Thor Equities 2019 Hotel

Signature/Studio Building 1357–1359 Wisconsin … New construction and Building owner … Retail; residential

retail renovation

Georgetown Valero 2715 Pennsylvania Avenue … New construction Eastbanc … Retail; residential

Source: Georgetown BID

THE STATE OF GEORGETOWN 2016 REPORT 23

RESTAURANTS

Georgetown has not been as dominant a restaurant scene in

recent years as it was in the 80s and 90s. Rising rents on M

Street, increasing competition from other neighborhoods, and

regulatory burdens on new liquor licenses all contributed to

changes in the Georgetown restaurant market. Georgetown’s

ratio of restaurants to retail is approximately 25%, lower than

the 50% on 14th Street and approximately 40% on Bethesda

Row. While Georgetown’s retail has continued to perform

well, a healthy mix of restaurants is essential for foot traffic

that helps drive retail sales.

However, several new restaurants opened in 2015 and the first

quarter of 2016, including Chaia Taco, Postmodern Foods, and

Jaco Taco and Juice Bar. Via Umbria reopened on Wisconsin

Avenue with a larger food market and a second floor dining

space for events, cooking demonstrations, and communal

dinners. Sovereign, the long-awaited Belgian beer restaurant

by Neighborhood Restaurant Group (Churchkey, Bluejacket,

Iron Gate) opened in Champion’s Alley in February 2016.

Washingtonian Magazine also named Fiola Mare the best

restaurant in D.C. in 2016.

With M Street rents continuing to increase, we expect the

trend of restaurants opening on the side streets between

M and K Streets to continue in 2016. Georgetown 2028

identified these streets as target areas for new retail

development to support a growing Waterfront District and

better connect M Street with the Georgetown Waterfront.

These streets also present opportunities to support

brick-and-mortar locations for local food entrepreneurs.

24 THE STATE OF GEORGETOWN 2016 REPORT

N STN ST

DUMBARTON ST

O ST

O ST

P ST

P ST

VOLTA ST

Q ST

CAMBRIDGE PL

DENT PL

R ST

Q ST

DENT PL

RESERVOIR RD

PROSPECT ST

M STM ST

CADY’S ALLEY

WHITEHURST FWY

BLUES ALLEY

TH

OM

AS

JE

FF

ER

SO

N S

T

34

TH

ST

33

RD

ST

PO

TO

MA

C S

T

BA

NK

ST

31S

T S

T

30

TH

ST

29

TH

ST

28

TH

ST

27

TH

ST

32

ND

ST

35

TH

ST

WIS

CO

NS

IN A

VE

C&O CANAL

K ST

POTOMAC RIVER

Via Umbria

Jaco Juice and Taco Bar

Beard Papa’s

Crumbs & Whiskers

Postmodern Foods

Maxime Steak Frites

Bar à Vin

Red Toque Cafe

Chaia

SovereignCurry & Pie

GEORGETOWNRESTAURANTS

New for 2015/Q1 2016

Source: Georgetown BID

THE STATE OF GEORGETOWN 2016 REPORT 25

FOOT TRAFFIC BY MONTH

Source: Georgetown BID, data collected Q1 2015–Q4 2015

N STN ST

DUMBARTON ST

O ST

O ST

P ST

P ST

VOLTA ST

Q ST

CAMBRIDGE PL

DENT PL

R ST

Q ST

DENT PL

RESERVOIR RD

PROSPECT ST

M STM ST

CADY’S ALLEY

WHITEHURST FWY

BLUES ALLEY

TH

OM

AS

JE

FF

ER

SO

N S

T

34

TH

ST

33

RD

ST

PO

TO

MA

C S

T

BA

NK

ST

31S

T S

T

30

TH

ST

29

TH

ST

28

TH

ST

27

TH

ST

32

ND

ST

35

TH

ST

WIS

CO

NS

IN A

VE

C&O CANAL

K ST

POTOMAC RIVER

Via Umbria

Jaco Juice and Taco Bar

Beard Papa’s

Crumbs & Whiskers

Postmodern Foods

Maxime Steak Frites

Bar à Vin

Red Toque Cafe

Chaia

SovereignCurry & Pie

12%

11%

10%

9%

8%

7%

6%

5%

4%

% T

OTA

L A

NN

UA

L F

OO

T T

RA

FF

IC

JANUA

RY

FEBRUARY

MARCH

APRIL

MAY

JUNE

JULY

AUGUST

SEPTEMBER

OCTO

BER

NOVEM

BER

DECEM

BER

M St & Wisconsin

1325 Wisconsin

2929 M St

1629 Wisconsin

1050 Thomas Jefferson

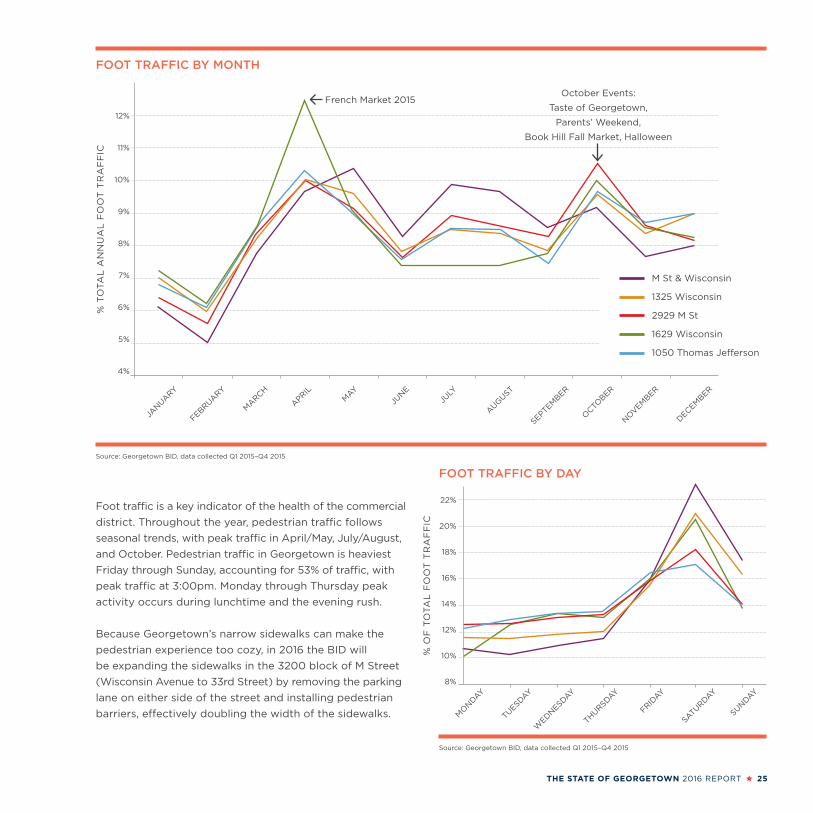

Foot traffic is a key indicator of the health of the commercial

district. Throughout the year, pedestrian traffic follows

seasonal trends, with peak traffic in April/May, July/August,

and October. Pedestrian traffic in Georgetown is heaviest

Friday through Sunday, accounting for 53% of traffic, with

peak traffic at 3:00pm. Monday through Thursday peak

activity occurs during lunchtime and the evening rush.

Because Georgetown’s narrow sidewalks can make the

pedestrian experience too cozy, in 2016 the BID will

be expanding the sidewalks in the 3200 block of M Street

(Wisconsin Avenue to 33rd Street) by removing the parking

lane on either side of the street and installing pedestrian

barriers, effectively doubling the width of the sidewalks.

French Market 2015 October Events:

Taste of Georgetown,

Parents’ Weekend,

Book Hill Fall Market, Halloween

FOOT TRAFFIC BY DAY

Source: Georgetown BID, data collected Q1 2015–Q4 2015

MO

NDAY

TUESDAY

WED

NESDAY

THURSDAY

FRIDAY

SATU

RDAY

SUNDAY

22%

20%

18%

16%

14%

12%

10%

8%

% O

F T

OTA

L F

OO

T T

RA

FF

IC

26 THE STATE OF GEORGETOWN 2016 REPORT

OFFICE MARKET AND EMPLOYEES

THE STATE OF GEORGETOWN 2016 REPORT 27

The District’s office market performed well in 2015. Overall office

vacancy held steady at just over 10 percent, lower than the

Suburban Maryland and Northern Virginia submarkets, while

average asking office rents climbed to over $50 per square foot (SF).

Georgetown’s office market improved for the fourth year in a row,

and in 2015 it was the strongest performing office submarket in the region. Office

occupancy climbed to 94.1%, the highest of any submarket and the third straight

year of occupancy above 90%. Rents have remained stable and affordable, closing

2015 at $42.54 per SF for average asking rents.14

Georgetown’s office market features a diversity of tenants, including law firms,

technology companies, nonprofits and associations, professional services firms,

and architecture and design firms. Across the region, office tenants are increasingly

seeking smaller, unique offices in neighborhoods rich in amenities. Georgetown’s

mix of trophy waterfront buildings and small spaces in historic buildings, set against

the backdrop of a vibrant retail district and active public spaces, is well suited to

meet these needs.

28 THE STATE OF GEORGETOWN 2016 REPORT

OFFICE OCCUPANCY RATES, BY SELECTED SUBMARKETS, 2011–2015

Source: CoStar (2016)

95%

90%

85%

80%

75%

70%2011 2012 2013 2014 2015

Georgetown

CBD

Bethesda-Chevy Chase

DC - Citywide

Tysons

Rosslyn-Ballston Corridor

94.1%

89.4%

AVERAGE GROSS RENTAL RATE, BY SELECTED SUBMARKETS, 2011–2015

Source: CoStar (2016)

$50

$45

$40

$35

$30

$25

$202011 2012 2013 2014 2015

$50.25PER SF

$42.54PER SF

AV

ER

AG

E G

RO

SS

RE

NTA

L R

AT

EO

CC

UP

AN

CY

RA

TE

THE STATE OF GEORGETOWN 2016 REPORT 29

AVERAGE OFFICE VACANCY RATES, 2011–2015, BY SELECTED SUBMARKETS Average Vacancy Rates

Submarket 2011 2012 2013 2014 2015

DC - Citywide 11.0% 9.9% 10.1% 10.5% 10.6%

DC Submarkets

Georgetown 12.9% 12.0% 9.0% 7.6% 5.9%

Southwest 18.1% 5.6% 10.0% 8.7% 9.3%

CBD 9.9% 10.3% 10.1% 9.4% 9.4%

Uptown 7.9% 7.0% 6.9% 10.5% 10.3%

Capitol Hill 11.4% 10.2% 8.3% 12.2% 10.5%

West End 7.2% 6.3% 4.7% 13.7% 11.1%

East End 9.2% 10.2% 9.9% 10.8% 12.1%

Capitol Riverfront 15.6% 16.2% 18.8% 17.3% 13.1%

NoMa 15.1% 10.9% 12.3% 12.8% 13.6%

Northern Virginia/Suburban Maryland Submarkets

Bethesda-Chevy Chase 9.4% 9.7% 8.6% 10.3% 10.5%

Silver Spring 11.1% 10.5% 10.6% 9.5% 10.8%

Tysons 15.5% 16.0% 15.6% 17.3% 17.4%

Crystal City 12.7% 22.6% 24.1% 25.6% 20.3%

Rosslyn-Ballston Corridor 12.9% 14.0% 17.5% 21.3% 21.4%

Source: CoStar (2016)

AVERAGE OFFICE RENTAL RATES, 2011–2015, BY SELECTED SUBMARKETS Average Gross Rental Rates per SF

Submarket 2011 2012 2013 2014 2015

DC - Citywide $48.51 $48.02 $48.77 $49.84 $50.25

DC Submarkets

Uptown $36.27 $39.40 $38.06 $39.25 $40.40

Capitol Riverfront $44.17 $43.40 $42.66 $40.67 $41.56

Georgetown $42.83 $41.31 $41.73 $42.38 $42.54

Southwest $50.97 $50.03 $49.70 $48.56 $47.05

NoMa $46.59 $46.87 $46.68 $47.42 $48.48

CBD $49.08 $50.72 $50.10 $50.89 $50.67

West End $41.21 $50.33 $50.54 $52.81 $52.21

Capitol Hill $51.47 $52.81 $53.16 $54.25 $52.74

East End $52.56 $52.44 $51.68 $53.11 $54.58

Northern Virginia/Suburban Maryland Submarkets

Silver Spring $28.03 $27.41 $27.21 $27.60 $27.64

Tysons $30.26 $33.78 $31.49 $32.40 $31.21

Bethesda-Chevy Chase $34.83 $35.84 $36.83 $35.35 $36.95

Crystal City $40.02 $40.54 $40.35 $38.37 $37.62

Rosslyn-Ballston Corridor $41.11 $41.58 $41.73 $41.00 $40.46

Source: CoStar (2016)

30 THE STATE OF GEORGETOWN 2016 REPORT

OFFICE ABSORPTION

Most of the new office absorption in Georgetown and across

the District was in Class A buildings, which comprise more

than half of Georgetown office space, indicating a continuation

of tenant flight to quality. In Georgetown net absorption

of Class A has been positive for four straight years, while

Class B and C absorption has been relatively flat over the

same period.15

As Class A demand has increased, construction of new Class

A space citywide is expected to continue, potentially leaving

more Class B and C space vacant. Since Georgetown office

inventory is not expected to increase in the future, building

owners will need to continue renewing Class B and C buildings

to provide higher quality space that also meets the needs

of tenants seeking smaller, unique spaces that encourage

creativity and reinforce brand identity, rather than the typical

large office floorplate.

GEORGETOWN OFFICE NET ABSORPTION (SF) BY CLASS OF SPACE, 2015

Source: CoStar (2016)

60K

50K

40K

30K

20K

10K

0K

-10KA B/C

59,000

-3,905

SQ

UA

RE

FO

OTA

GE

WASHINGTON METRO AREA OFFICE NET ABSORPTION (SF) BY CLASS OF SPACE, 2015

Source: CoStar (2016)

2200K

2000K

1800K

1600K

1400K

1200K

1000K

800K

600K

400K

200K

0K

-200K

A B/C

SQ

UA

RE

FO

OTA

GE

2,100,000

-151,000

THE STATE OF GEORGETOWN 2016 REPORT 31

GEORGETOWN OFFICE BUILDINGS AS A PERCENT OF INVENTORY, BY BUILDING CLASS

0K 1000K500K 2000K1500K 3000K2500K 3500K

A B C

OFFICE BUILDING SUMMARY STATISTICS BY CLASS

Building Class Buildings Total Inventory % of Inventory Vacant SF Vacancy Rate Occupancy Rate Rent per SF

All Classes 131 3,407,729 100% 201,341 5.9% 94.1% $42.57

A 9 1,702,663 50% 102,796 6.0% 94.0% $47.37

B 54 1,422,595 42% 84,587 5.9% 94.1% $37.63

C 68 282,471 8% 13,958 4.9% 95.1% $47.25

Source: CoStar (2016)

TOTAL INVENTORY

32 THE STATE OF GEORGETOWN 2016 REPORT

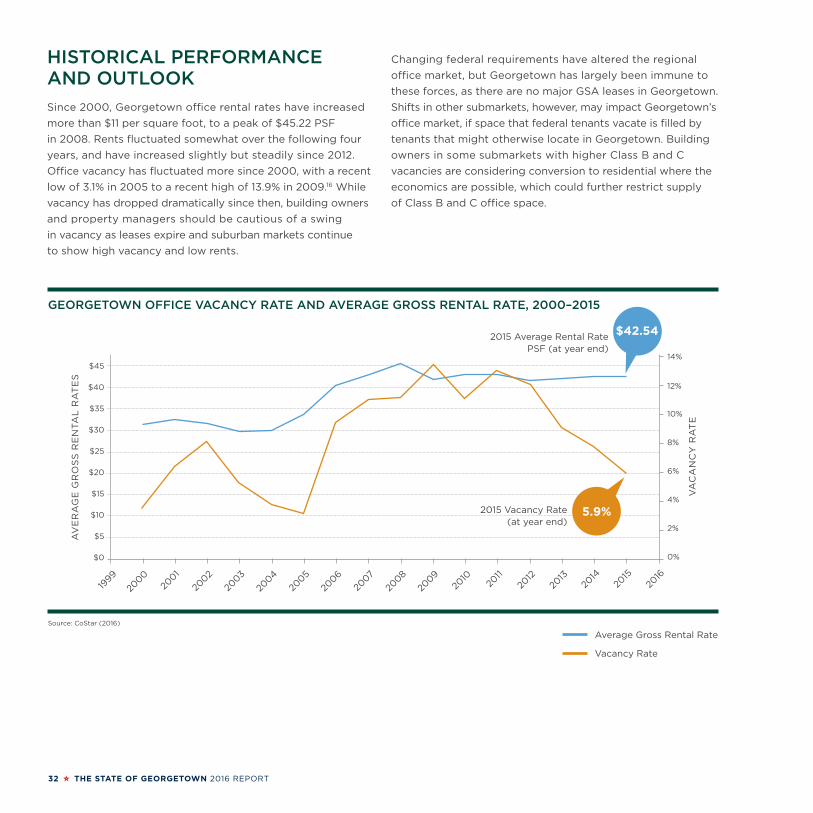

HISTORICAL PERFORMANCE AND OUTLOOK

Since 2000, Georgetown office rental rates have increased

more than $11 per square foot, to a peak of $45.22 PSF

in 2008. Rents fluctuated somewhat over the following four

years, and have increased slightly but steadily since 2012.

Office vacancy has fluctuated more since 2000, with a recent

low of 3.1% in 2005 to a recent high of 13.9% in 2009.16 While

vacancy has dropped dramatically since then, building owners

and property managers should be cautious of a swing

in vacancy as leases expire and suburban markets continue

to show high vacancy and low rents.

Changing federal requirements have altered the regional

office market, but Georgetown has largely been immune to

these forces, as there are no major GSA leases in Georgetown.

Shifts in other submarkets, however, may impact Georgetown’s

office market, if space that federal tenants vacate is filled by

tenants that might otherwise locate in Georgetown. Building

owners in some submarkets with higher Class B and C

vacancies are considering conversion to residential where the

economics are possible, which could further restrict supply

of Class B and C office space.

GEORGETOWN OFFICE VACANCY RATE AND AVERAGE GROSS RENTAL RATE, 2000–2015

Source: CoStar (2016)

Average Gross Rental Rate

Vacancy Rate

$45

$40

$35

$30

$25

$20

$15

$10

$5

$0

AV

ER

AG

E G

RO

SS

RE

NTA

L R

AT

ES

VA

CA

NC

Y R

AT

E

14%

12%

10%

8%

6%

4%

2%

0%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2000

2014

2015

2016

1999

2015 Average Rental Rate PSF (at year end)

2015 Vacancy Rate(at year end)

5.9%

$42.54

THE STATE OF GEORGETOWN 2016 REPORT 33

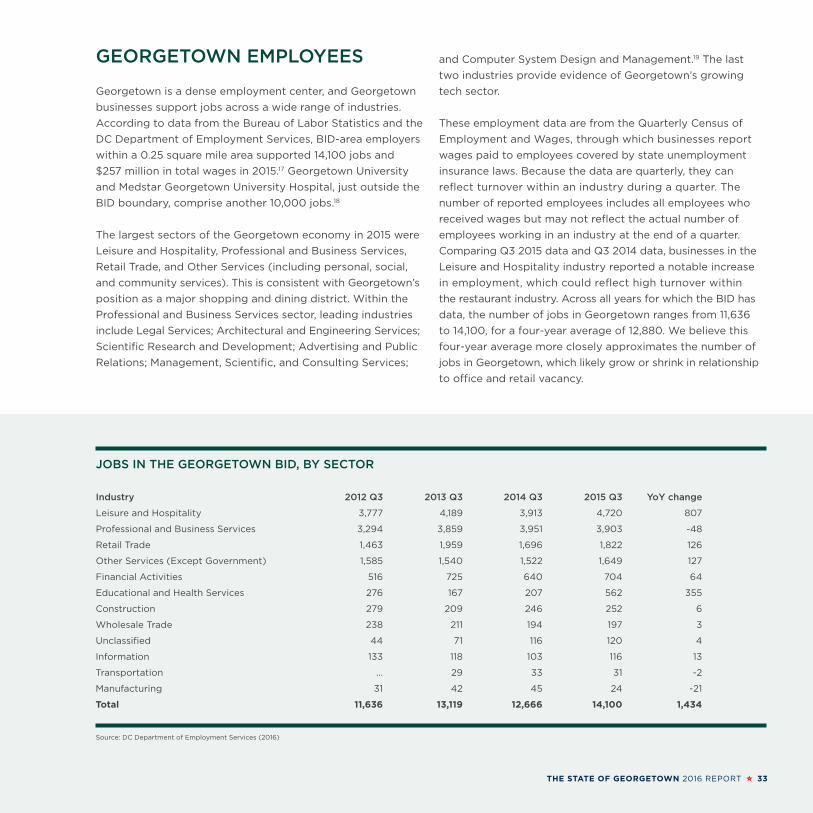

GEORGETOWN EMPLOYEES

Georgetown is a dense employment center, and Georgetown

businesses support jobs across a wide range of industries.

According to data from the Bureau of Labor Statistics and the

DC Department of Employment Services, BID-area employers

within a 0.25 square mile area supported 14,100 jobs and

$257 million in total wages in 2015.17 Georgetown University

and Medstar Georgetown University Hospital, just outside the

BID boundary, comprise another 10,000 jobs.18

The largest sectors of the Georgetown economy in 2015 were

Leisure and Hospitality, Professional and Business Services,

Retail Trade, and Other Services (including personal, social,

and community services). This is consistent with Georgetown’s

position as a major shopping and dining district. Within the

Professional and Business Services sector, leading industries

include Legal Services; Architectural and Engineering Services;

Scientific Research and Development; Advertising and Public

Relations; Management, Scientific, and Consulting Services;

and Computer System Design and Management.19 The last

two industries provide evidence of Georgetown’s growing

tech sector.

These employment data are from the Quarterly Census of

Employment and Wages, through which businesses report

wages paid to employees covered by state unemployment

insurance laws. Because the data are quarterly, they can

reflect turnover within an industry during a quarter. The

number of reported employees includes all employees who

received wages but may not reflect the actual number of

employees working in an industry at the end of a quarter.

Comparing Q3 2015 data and Q3 2014 data, businesses in the

Leisure and Hospitality industry reported a notable increase

in employment, which could reflect high turnover within

the restaurant industry. Across all years for which the BID has

data, the number of jobs in Georgetown ranges from 11,636

to 14,100, for a four-year average of 12,880. We believe this

four-year average more closely approximates the number of

jobs in Georgetown, which likely grow or shrink in relationship

to office and retail vacancy.

JOBS IN THE GEORGETOWN BID, BY SECTOR

Industry 2012 Q3 2013 Q3 2014 Q3 2015 Q3 YoY change

Leisure and Hospitality 3,777 4,189 3,913 4,720 807

Professional and Business Services 3,294 3,859 3,951 3,903 -48

Retail Trade 1,463 1,959 1,696 1,822 126

Other Services (Except Government) 1,585 1,540 1,522 1,649 127

Financial Activities 516 725 640 704 64

Educational and Health Services 276 167 207 562 355

Construction 279 209 246 252 6

Wholesale Trade 238 211 194 197 3

Unclassified 44 71 116 120 4

Information 133 118 103 116 13

Transportation … 29 33 31 -2

Manufacturing 31 42 45 24 -21

Total 11,636 13,119 12,666 14,100 1,434

Source: DC Department of Employment Services (2016)

34 THE STATE OF GEORGETOWN 2016 REPORT

HOTELS

THE STATE OF GEORGETOWN 2016 REPORT 35

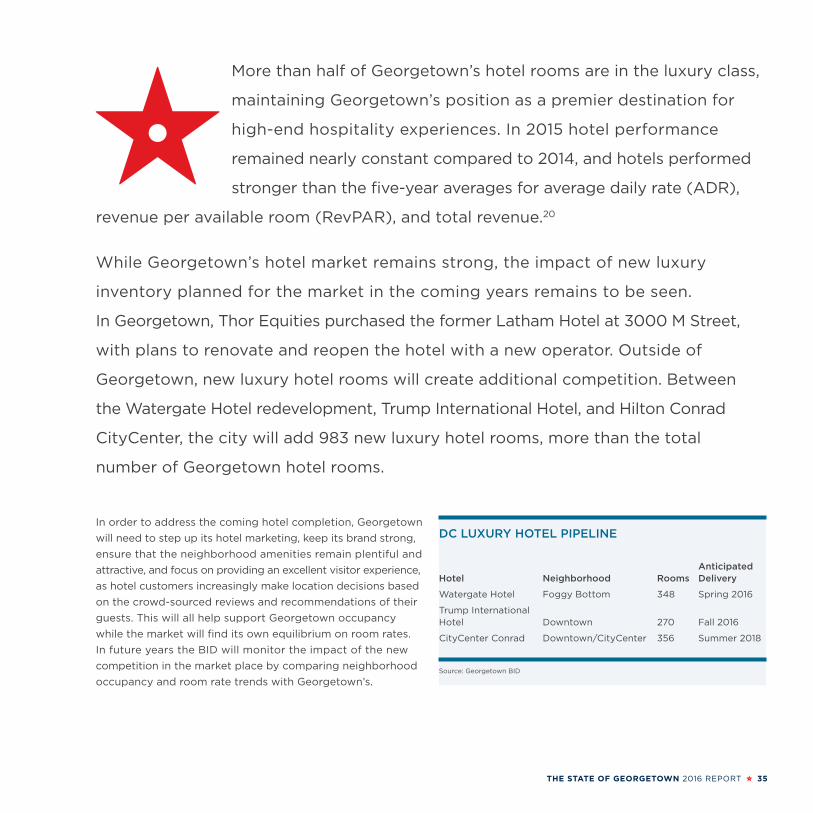

DC LUXURY HOTEL PIPELINE

AnticipatedHotel Neighborhood Rooms Delivery

Watergate Hotel Foggy Bottom 348 Spring 2016

Trump International Hotel Downtown 270 Fall 2016

CityCenter Conrad Downtown/CityCenter 356 Summer 2018

Source: Georgetown BID

More than half of Georgetown’s hotel rooms are in the luxury class,

maintaining Georgetown’s position as a premier destination for

high-end hospitality experiences. In 2015 hotel performance

remained nearly constant compared to 2014, and hotels performed

stronger than the five-year averages for average daily rate (ADR),

revenue per available room (RevPAR), and total revenue.20

While Georgetown’s hotel market remains strong, the impact of new luxury

inventory planned for the market in the coming years remains to be seen.

In Georgetown, Thor Equities purchased the former Latham Hotel at 3000 M Street,

with plans to renovate and reopen the hotel with a new operator. Outside of

Georgetown, new luxury hotel rooms will create additional competition. Between

the Watergate Hotel redevelopment, Trump International Hotel, and Hilton Conrad

CityCenter, the city will add 983 new luxury hotel rooms, more than the total

number of Georgetown hotel rooms.

In order to address the coming hotel completion, Georgetown

will need to step up its hotel marketing, keep its brand strong,

ensure that the neighborhood amenities remain plentiful and

attractive, and focus on providing an excellent visitor experience,

as hotel customers increasingly make location decisions based

on the crowd-sourced reviews and recommendations of their

guests. This will all help support Georgetown occupancy

while the market will find its own equilibrium on room rates.

In future years the BID will monitor the impact of the new

competition in the market place by comparing neighborhood

occupancy and room rate trends with Georgetown’s.

36 THE STATE OF GEORGETOWN 2016 REPORT

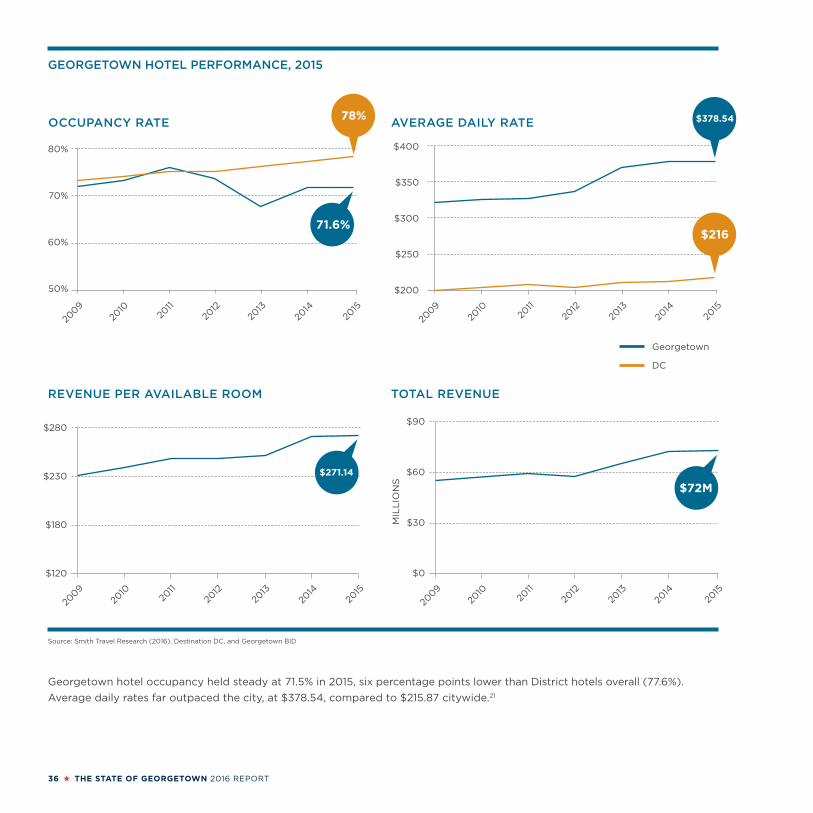

GEORGETOWN HOTEL PERFORMANCE, 2015

Source: Smith Travel Research (2016), Destination DC, and Georgetown BID

Georgetown hotel occupancy held steady at 71.5% in 2015, six percentage points lower than District hotels overall (77.6%).

Average daily rates far outpaced the city, at $378.54, compared to $215.87 citywide.21

N ST

N ST

DUMBARTON ST

O ST

O ST

P ST

P ST

VOLTA ST

Q ST

CAMBRIDGE PL

DENT PL

R ST

Q ST

R ST

DENT PL

RESERVOIR RD

PROSPECT STM ST

M ST

CADY’S ALLEY

WHITEHURST FWY

BLUES ALLEY

TH

OM

AS

JE

FF

ER

SO

N S

T

34

TH

ST

37

TH

ST

33

RD

ST

PO

TO

MA

C S

T

BA

NK

ST

31S

T S

T

30

TH

ST

29

TH

ST

28

TH

ST

27

TH

ST

32N

D S

T

35

TH

ST

36

TH

ST

WIS

CO

NSIN

AV

E

Georgetown Inn (96 rooms)

The Graham Hotel (57 rooms)

Four Seasons Hotel

Washington, DC (222 rooms)

The Capella Georgetown (49 rooms)

[became Rosewood Washington, DC in April 2016]

Ritz-Carlton (86 rooms)

Georgetown Suites (221 rooms)

POTOMAC RIVER

C&O CANAL

RO

CK

CR

EE

K P

AR

KW

AY

GEORGETOWN WATERFRONT PARK

Georgetown Suites Harbour

80%

70%

60%

50%

2009

2010

2011

2012

2013

2014

78%OCCUPANCY RATE

2015

71.6%

$400

$350

$300

$250

$200

$378.54AVERAGE DAILY RATE

$216

2009

2010

2011

2012

2013

2014

2015

$280

$230

$180

$120

REVENUE PER AVAILABLE ROOM

Georgetown

DC

2009

2010

2011

2012

2013

2014

2015

$271.14

$90

$60

$30

$0

MIL

LIO

NS

$72M

TOTAL REVENUE

2009

2010

2011

2012

2013

2014

2015

N ST

N ST

DUMBARTON ST

O ST

O ST

P ST

P ST

VOLTA ST

Q ST

CAMBRIDGE PL

DENT PL

R ST

Q ST

R ST

DENT PL

RESERVOIR RD

PROSPECT STM ST

M ST

CADY’S ALLEY

WHITEHURST FWY

BLUES ALLEY

TH

OM

AS

JE

FF

ER

SO

N S

T

34

TH

ST

37

TH

ST

33

RD

ST

PO

TO

MA

C S

T

BA

NK

ST

31S

T S

T

30

TH

ST

29

TH

ST

28

TH

ST

27

TH

ST

32N

D S

T

35

TH

ST

36

TH

ST

WIS

CO

NSIN

AV

E

Georgetown Inn (96 rooms)

The Graham Hotel (57 rooms)

Four Seasons Hotel

Washington, DC (222 rooms)

The Capella Georgetown (49 rooms)

[became Rosewood Washington, DC in April 2016]

Ritz-Carlton (86 rooms)

Georgetown Suites (221 rooms)

POTOMAC RIVER

C&O CANAL

RO

CK

CR

EE

K P

AR

KW

AY

GEORGETOWN WATERFRONT PARK

Georgetown Suites Harbour

GEORGETOWN HOTELS

Source: Source: Smith Travel Research (2016) and Georgetown BID

THE STATE OF GEORGETOWN 2016 REPORT 37

38 THE STATE OF GEORGETOWN 2016 REPORT

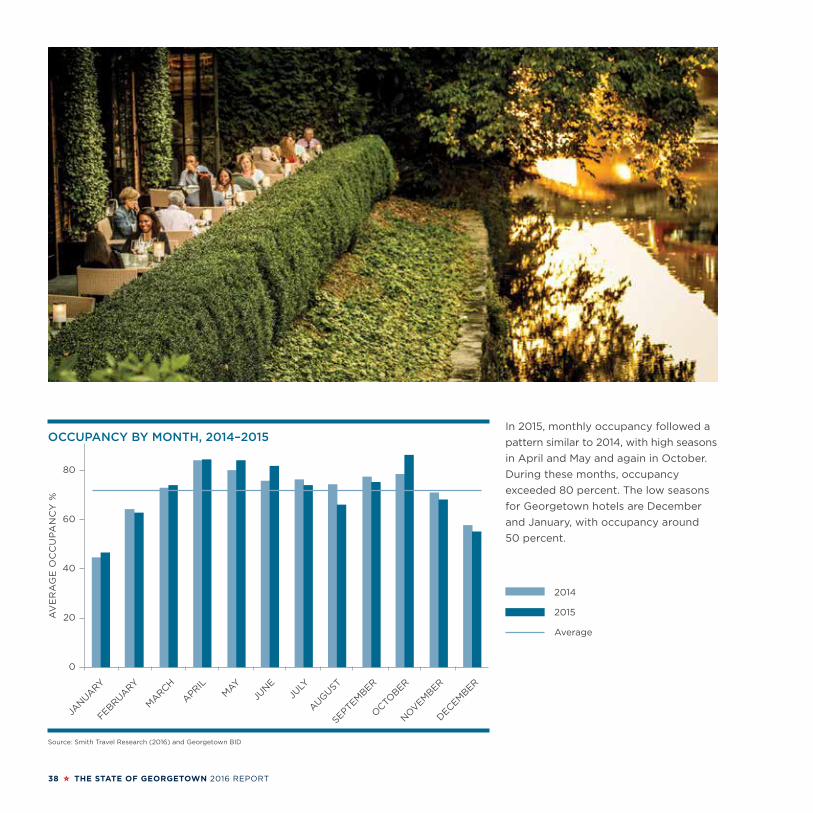

In 2015, monthly occupancy followed a

pattern similar to 2014, with high seasons

in April and May and again in October.

During these months, occupancy

exceeded 80 percent. The low seasons

for Georgetown hotels are December

and January, with occupancy around

50 percent.

OCCUPANCY BY MONTH, 2014–2015

Source: Smith Travel Research (2016) and Georgetown BID

AV

ER

AG

E O

CC

UP

AN

CY

%

JANUA

RY

FEBRUARY

MARCH

APRIL

MAY

JUNE

JULY

AUGUST

SEPTEMBER

OCTO

BER

NOVEM

BER

DECEM

BER

80

60

40

20

0

2014

2015

Average

THE STATE OF GEORGETOWN 2016 REPORT 39

40 THE STATE OF GEORGETOWN 2016 REPORT

TRANSPORTATION

THE STATE OF GEORGETOWN 2016 REPORT 41

Improving access to and within Georgetown is essential to strengthen the

retail and office markets, and enhance the visitor experience. Despite

a lack of direct Metrorail access, Georgetown is accessible by a wide

range of modes, including biking, walking, Metrobus, Circulator, and private automobile.

The BID is also working with partners in DC and Arlington County to study the

feasibility of an aerial gondola connecting the Rosslyn metro station with Georgetown,

and continues to advocate for a streetcar line to Georgetown on dedicated tracks.

MID-DAY TRAVEL TIMES FROM GEORGETOWN VS. FARRAGUT SQUARE

Source: Georgetown BID and Capital Bikeshare

Dupont Circle

Rosslyn

US Capitol

Union Station

Bethesda

Tysons Corner

Farragut Square

Georgetown

Farragut Square

Georgetown

Farragut Square

Georgetown

Farragut Square

Georgetown

Farragut Square

Georgetown

Farragut Square

Georgetown

DESTINATION ORIGIN 0 10 20 30 40

MINUTES TRAVEL TIME 0 10 20 30 40

The Georgetown

commercial district

provides quick access

to the GW Parkway,

I-66, Route 50, Rock

Creek Parkway,

and I-395. Travel

times to Capitol Hill,

Northern Virginia,

and Montgomery

County are all the

same, or faster than,

from the CBD.

N ST

N ST

DUMBARTON ST

O ST

O ST

P ST

P ST

VOLTA ST

Q ST

CAMBRIDGE PL

DENT PL

R ST

Q ST

R ST

DENT PL

RESERVOIR RD

PROSPECT STM ST

M ST

CADY’S ALLEY

WHITEHURST FWY

BLUES ALLEY

TH

OM

AS

JE

FF

ER

SO

N S

T

34

TH

ST

37

TH

ST

33

RD

ST

PO

TO

MA

C S

T

BA

NK

ST

31S

T S

T

30

TH

ST

29

TH

ST

28

TH

ST

27

TH

ST

32N

D S

T

35

TH

ST

36

TH

ST

POTOMAC RIVER

C&O CANAL

RO

CK

CR

EE

K P

AR

KW

AY

GEORGETOWN WATERFRONT PARK

38B, D5, Rosslyn-Georgetown-Dupont

G2

G2

D1, D2, D6

31, 33, 30N

, 30S, U

nion Station-Georg

etown

WIS

CO

NSIN

AV

E

42 THE STATE OF GEORGETOWN 2016 REPORT

Capital Bikeshare StationParking Garage/Lot

Source: DC Office of the Chief Technology Officer (2016) and Georgetown BID

GEORGETOWN BIKESHARE, PARKING, CIRCULATOR & METROBUS

THE STATE OF GEORGETOWN 2016 REPORT 43

BICYCLING

Bicycling continues to be an important mode for visitors and

employees to travel to Georgetown. Capital Bikeshare ridership

increased for the third straight year in 2015, with 210,965 trips

to and from Georgetown’s six stations.22 In addition to Capital

Bikeshare, three major bike trails—the Capital Crescent Trail,

Rock Creek Trail, and M Street cycletrack—end in or are

immediately adjacent to Georgetown.

Of Capital Bikeshare trips ending in Georgetown, trips by

registered users increased five percent compared to 2014 and

trips by casual users and tourists increased 18%. Compared

to all other BIDs, Georgetown was one of the most popular

commercial district destinations in 2015—Georgetown had

the third highest number of casual user trips ending at

stations within the BID and the highest number of casual

user trips per station.23

BIKESHARE TRIPS TO/FROM GEORGETOWN, BY STATION, 2012–2015

Source: Capital Bikeshare (2016) and Georgetown BID

200K

150K

100K

50K

02012 2013 2014

34th & Water Street NW (Installed July 9, 2014)

37th & O Street NW/Georgetown University

C&O Canal & Wisconsin Avenue NW

Georgetown Harbor/30th Street NW

M Street & Pennsylvania Avenue NW

Wisconsin Avenue & O Street NW (Installed April 25, 2013)

2015

44 THE STATE OF GEORGETOWN 2016 REPORT

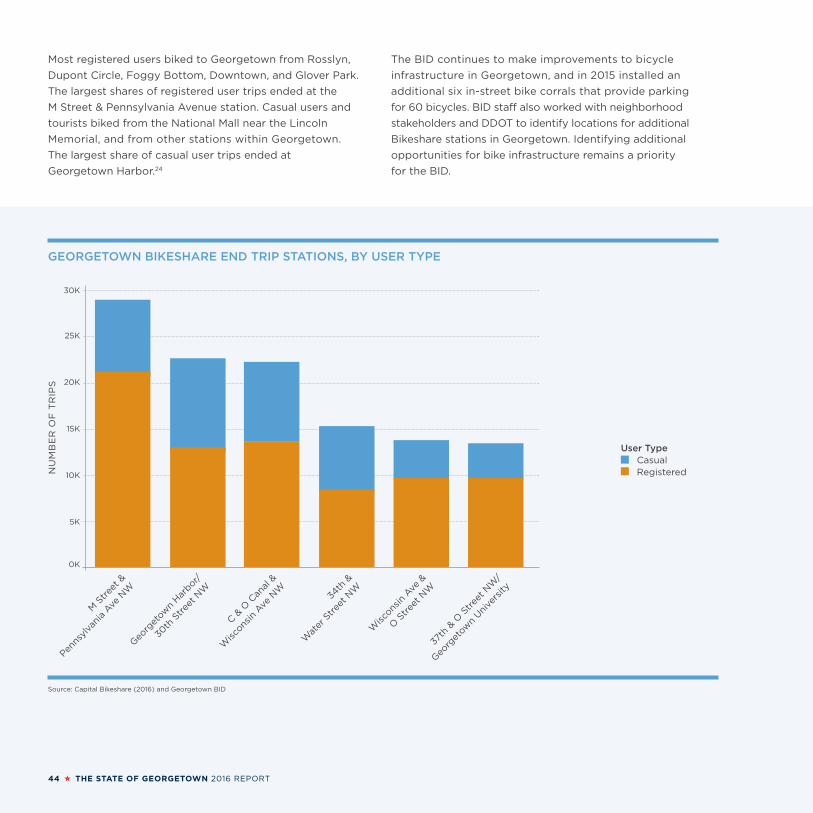

Most registered users biked to Georgetown from Rosslyn,

Dupont Circle, Foggy Bottom, Downtown, and Glover Park.

The largest shares of registered user trips ended at the

M Street & Pennsylvania Avenue station. Casual users and

tourists biked from the National Mall near the Lincoln

Memorial, and from other stations within Georgetown.

The largest share of casual user trips ended at

Georgetown Harbor.24

The BID continues to make improvements to bicycle

infrastructure in Georgetown, and in 2015 installed an

additional six in-street bike corrals that provide parking

for 60 bicycles. BID staff also worked with neighborhood

stakeholders and DDOT to identify locations for additional

Bikeshare stations in Georgetown. Identifying additional

opportunities for bike infrastructure remains a priority

for the BID.

GEORGETOWN BIKESHARE END TRIP STATIONS, BY USER TYPE

Source: Capital Bikeshare (2016) and Georgetown BID

30K

25K

20K

15K

10K

5K

0K

NU

MB

ER

OF

TR

IPS

M S

tree

t &

Penns

ylva

nia

Ave N

W

Geo

rget

own

Har

bor/

30th

Stree

t NW

C & O

Can

al &

Wisco

nsin

Ave

NW

34th

&

Wat

er S

tree

t NW

Wisco

nsin

Ave

&

O S

tree

t NW

37th

& O

Stree

t NW

/

Geo

rget

own

Uni

vers

ity

User Type Casual Registered

THE STATE OF GEORGETOWN 2016 REPORT 45

User Type Casual Registered

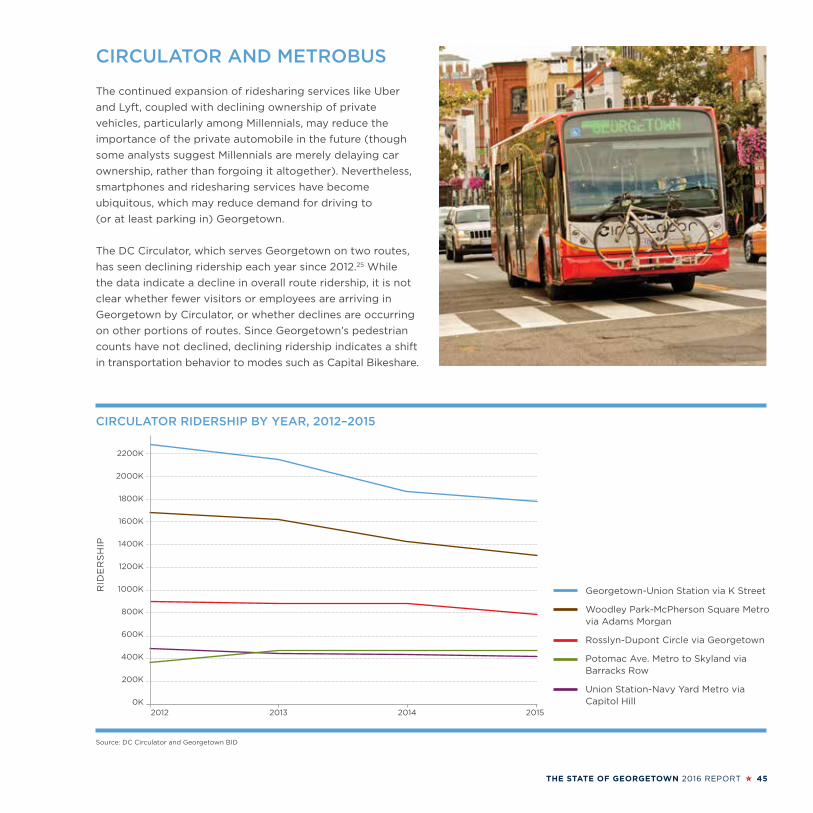

CIRCULATOR AND METROBUS

The continued expansion of ridesharing services like Uber

and Lyft, coupled with declining ownership of private

vehicles, particularly among Millennials, may reduce the

importance of the private automobile in the future (though

some analysts suggest Millennials are merely delaying car

ownership, rather than forgoing it altogether). Nevertheless,

smartphones and ridesharing services have become

ubiquitous, which may reduce demand for driving to

(or at least parking in) Georgetown.

The DC Circulator, which serves Georgetown on two routes,

has seen declining ridership each year since 2012.25 While

the data indicate a decline in overall route ridership, it is not

clear whether fewer visitors or employees are arriving in

Georgetown by Circulator, or whether declines are occurring

on other portions of routes. Since Georgetown’s pedestrian

counts have not declined, declining ridership indicates a shift

in transportation behavior to modes such as Capital Bikeshare.

CIRCULATOR RIDERSHIP BY YEAR, 2012–2015

Source: DC Circulator and Georgetown BID

Georgetown-Union Station via K Street

Woodley Park-McPherson Square Metro via Adams Morgan

Rosslyn-Dupont Circle via Georgetown

Potomac Ave. Metro to Skyland via Barracks Row

Union Station-Navy Yard Metro via Capitol Hill

2200K

2000K

1800K

1600K

1400K

1200K

1000K

800K

600K

400K

200K

0K

RID

ER

SH

IP

2012 2013 2014 2015

46 THE STATE OF GEORGETOWN 2016 REPORT

Metrobus ridership data indicate that approximately 3,000

people board buses in Georgetown on an average weekday

and a similar number disembark. The most popular routes

serving the commercial district are the 38B, 31, and 33.26 Since

Georgetown does not have a metro station, these routes are

critical because they connect Georgetown with the Rosslyn

and Foggy Bottom metro stations and downtown, and serve

significant population centers in Arlington and the Wisconsin

Avenue corridor. Heavy ridership on the 38B provides

further evidence in support of an aerial gondola connecting

Georgetown and Rosslyn.

Metrorail ridership has declined overall from 2011–2015,

likely due in part to continued maintenance and rebuilding,

and ridership at the Foggy Bottom and Rosslyn stations, the

two closest stations to Georgetown, have declined as well.

Along with declining Circulator ridership, these data indicate

a recent shift in transportation patterns among employees

and visitors.

GEORGETOWN METROBUS RIDERSHIP BY MOST HEAVILY-USED ROUTES

BOARDING ALIGHTING

Route Direction Destination Weekday Saturday Sunday Weekday Saturday Sunday

38B East Farragut Square 248 121 93 501 291 222

38B West Ballston 538 352 292 155 87 74

31 North Friendship Heights 423 382 235 138 97 68

31 South Potomac Park 176 129 67 336 299 203

33 North Friendship Heights 418 295 249 175 129 77

33 South Archives 213 161 104 345 295 224

2238 1900 1380 1907 1686 1213

Source: WMATA Ridecheck Plus, 2015 data; note: all data are averages

METRORAIL RIDERSHIP, 2011–2015

Route 2011 2012 2013 2014 2015

System Wide 743,961 744,918 725,770 721,804 712,843

Foggy Bottom 21,318 22,827 22,512 22,053 21,462

Rosslyn 17,158 16,718 15,632 15,460 14,815

METRORAIL AVERAGE DAILY BOARDINGS, 2011–2015

Source: WMATA 2015 Historical Metrorail Ridership

RID

ER

SH

IP

800K

700K

600K

2011 2012 2013 2014 2015

25K

20K

15K

2011 2012 2013 2014 2015

System Wide

Foggy Bottom

Rosslyn

THE STATE OF GEORGETOWN 2016 REPORT 47

WHERE GEORGETOWN BID AREA EMPLOYEES LIVE

Source: US Census Bureau (2016), OnTheMap application, 2014 data

WHERE GEORGETOWN RESIDENTS WORK

Source: US Census Bureau (2016), OnTheMap application, 2014 data

Understanding the travel patterns of residents and employees

is essential for understanding and improving Georgetown’s

transportation needs. 60% of Georgetown residents work in

the District, mostly within Georgetown, West End, Downtown,

and the East End. Employees who work within the BID are

split evenly among the District, Virginia, and Maryland, with

approximately one-third of area employees living in each.

Among District residents, the largest concentrations live in

Georgetown and Glover Park. Other dense pockets include

Dupont Circle, Logan Circle, Mount Pleasant/Columbia

Heights, Shaw, and NoMa.27

48 THE STATE OF GEORGETOWN 2016 REPORT

Endnotes:1 Washington, DC Economic Partnership Development Report

2015–2016

2 Esri Business Analyst Online (2016)

3 Ibid

4 US Census Bureau, Estimates of Population Change and Rankings, 2015 data

5 Esri Business Analyst Online (2016). Note: For the purposes of this estimate, “Georgetown” is defined as DC Census Tracts 1, 2.01, and 2.02 in the 2010 US Census. These tracts cover the area south of Whitehaven Street to the Potomac River. To the west, the area is bounded by 35th Street until Reservoir Road, and then by the western border of Georgetown University, which is included. To the east, the area is bounded by Rock Creek.

6 Washington, DC Economic Partnership Development Report 2015–2016

7 Buxton (2015)

8 Buxton (2015) and Georgetown BID

9 Ibid

10 CoStar (2016)

11 Dochter & Alexander Q3 2015 Retail Market Report

12 Streetsense (2014)

13 Washington, DC Economic Partnership Development Report 2015–2016

14 CoStar (2016)

15 Ibid

16 Ibid

17 DC Department of Employment Services, Q3 2015 data from the Quarterly Census of Employment and Wages

18 Georgetown University in the District of Columbia (2015) and personal correspondence

19 DC Department of Employment Services

20 Smith Travel Research (2016)

21 Destination DC (2016)

22 Capital Bikeshare, 2015 trip history data

23 Ibid

24 Ibid

25 DC Circulator Ridership Data, 2012–2015

26 WMATA Ridecheck Plus, 2015 data

27 US Census Bureau, OnTheMap Application, 2014 data

Notes:Unless otherwise noted, “Georgetown” is defined for statistical purposes as 2010 DC Census Tracts 1, 2.01, and 2.02. These tracts cover the area south of Whitehaven Street to the Potomac River. To the west, the area is bounded by 35th Street until Reservoir Road, and then by the western border of Georgetown University (which is included). To the east, the area is bounded by Rock Creek. For a detailed map, refer to: http://www.census.gov/geo/www/maps/pl10_map_suite/tract.html.

The “Georgetown BID area” is comprised of the commercial corridors along Wisconsin Avenue (between M Street and R Street) and M Street (between 27th Street and 37th Street, and inclusive of the commercial areas of Prospect Street) as well as the commercial areas south of M Street to the Potomac River. For the statistical analysis in this report, BID staff used a contiguous geo-spatial boundary derived from GIS shape files available from the DC Office of the Chief Technology Officer (data.octo.dc.gov). This is the fourth State of Georgetown report undertaken by the Georgetown BID. The BID intends to publish this report annually, using data from each volume as benchmarks and monitors of progress against which the future health of the neighborhood economy will be measured. The staff welcomes comments and suggestions on how to improve and expand this report to be most useful to its readers. Please direct comments to Jamie Scott, economic development manager, at [email protected].

While all data in this publication was produced by the BID or obtained from the sources cited, the BID does not guarantee the accuracy of the data included in this publication; the staff welcomes opportunities and partnerships to refine available data.

BID Staff:

Jamie Scott, lead author

Joe Sternlieb, CEO

Maggie Downing, Sherman Gardner, Will Handsfield, Nancy Miyahira, Terrie Rouse (Georgetown Heritage), Annelies van Vonno, John Wiebenson, Ted Williford, Debbie Young

Design: Fuszion

Photography: Sam Kittner for the Georgetown BID, except page 7 photo by James Jackson, courtesy Chaia; page 34 photo courtesy The Graham Hotel; page 39 photo courtesy The Four Seasons Hotel Washington, DC.

Special thanks to Eric Brown (Buxton), John Kangethe (DOES), Kim Lucas (DDOT), Greg McFarland (WMATA), Chad Shuskey (Washington DC Economic Partnership), Michelle Tierney (Rosslyn BID), Kate Thompson (Destination DC), and Ric Wise (BLS).

GEORGETOWN BUSINESS IMPROVEMENT DISTRICT1000 Potomac St., NW | Suite 122Washington, D.C. 20007T: 202.298.9222 x208 | F: [email protected]