Embed Size (px)

Citation preview

State and Local Public FinanceSpring 2015, Professor Yinger

Lecture 7

Property Tax Capitalization

State and Local Public FinanceLecture 7: Property Tax Capitalization

Class Outline

What Is Property Tax Capitalization?

How Does Property Tax Capitalization Arise?

What Are the Implications of Property Tax Capitalization for Public Policy?

State and Local Public FinanceLecture 7: Property Tax Capitalization In 1969 an economist named Oates

(my professor) tested Tiebout’s positive hypothesis that people care about services in their community.

Tiebout’s hypothesis implies, said Oates, that better public services and lower property taxes will lead to higher property values.

This phenomenon known as capitalization.

Using data for suburbs in NJ, Oates found evidence of capitalization—and inspired a huge literature.

State and Local Public FinanceLecture 7: Property Tax Capitalization

What Is Property Tax Capitalization?

This class explains property tax capitalization and discusses its policy implications.

A more detailed discussion of property tax capitalization is available on my web site at http://faculty.maxwell.syr.edu/jyinger/E-Books/Housing_And_Commuting/Chapter_5.4.pdf.

State and Local Public FinanceLecture 7: Property Tax Capitalization The value of an asset equals the

present value of the net benefits from owning it.

Without property taxes, the amount someone is willing to pay for a house is the present value of the rental benefits, or

where P is the pre-tax price of housing services, H is housing services, r is the real discount rate, and L is the expected lifetime of a house.

21

...(1 )(1 ) (1 )(1 )

L

y Ly

PH PH PH PHVrr rr

State and Local Public FinanceLecture 7: Property Tax Capitalization

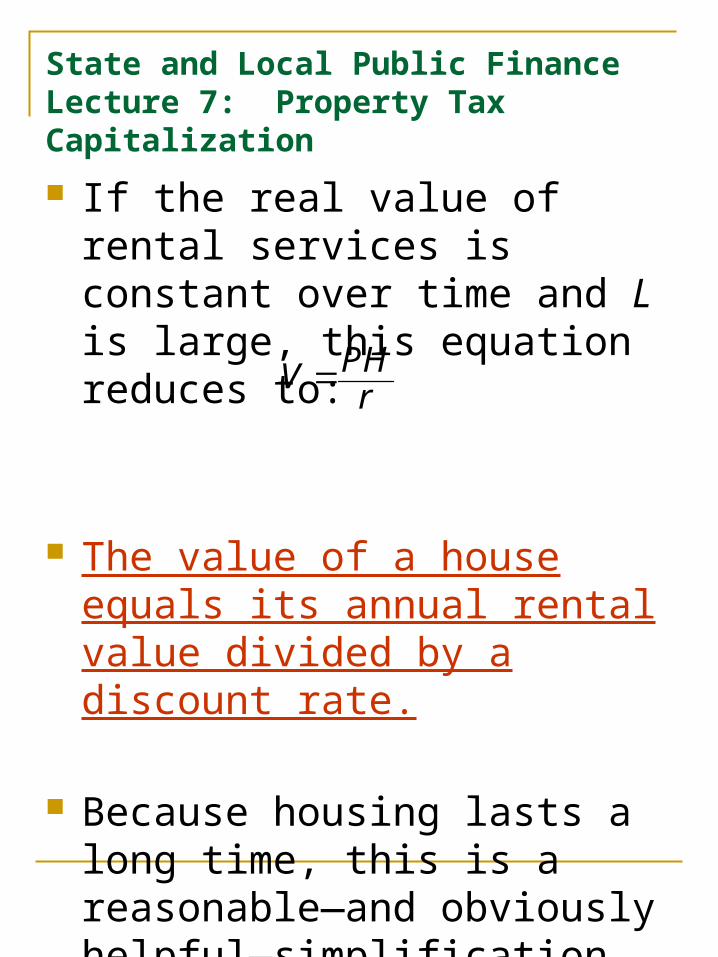

If the real value of rental services is constant over time and L is large, this equation reduces to:

The value of a house equals its annual rental value divided by a discount rate.

Because housing lasts a long time, this is a reasonable—and obviously helpful—simplification.

PHVr

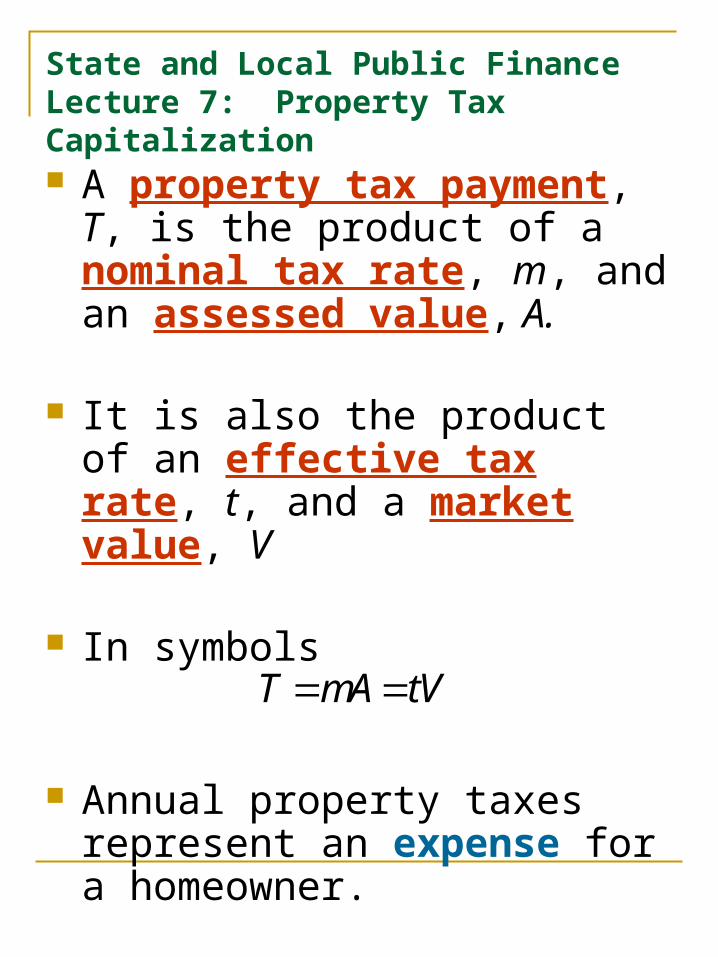

State and Local Public FinanceLecture 7: Property Tax Capitalization A property tax payment, T, is

the product of a nominal tax rate, m, and an assessed value, A.

It is also the product of an effective tax rate, t, and a market value, V

In symbols

Annual property taxes represent an expense for a homeowner.

T mA tV

State and Local Public FinanceLecture 7: Property Tax Capitalization

Adding property taxes as an expense, the house value equation becomes:

Note that property taxes are added as a flow because they must be paid every year.

1 1(1 ) (1 )

L L

y yy y

PH tVVr r

PH tVr r

State and Local Public FinanceLecture 7: Property Tax Capitalization

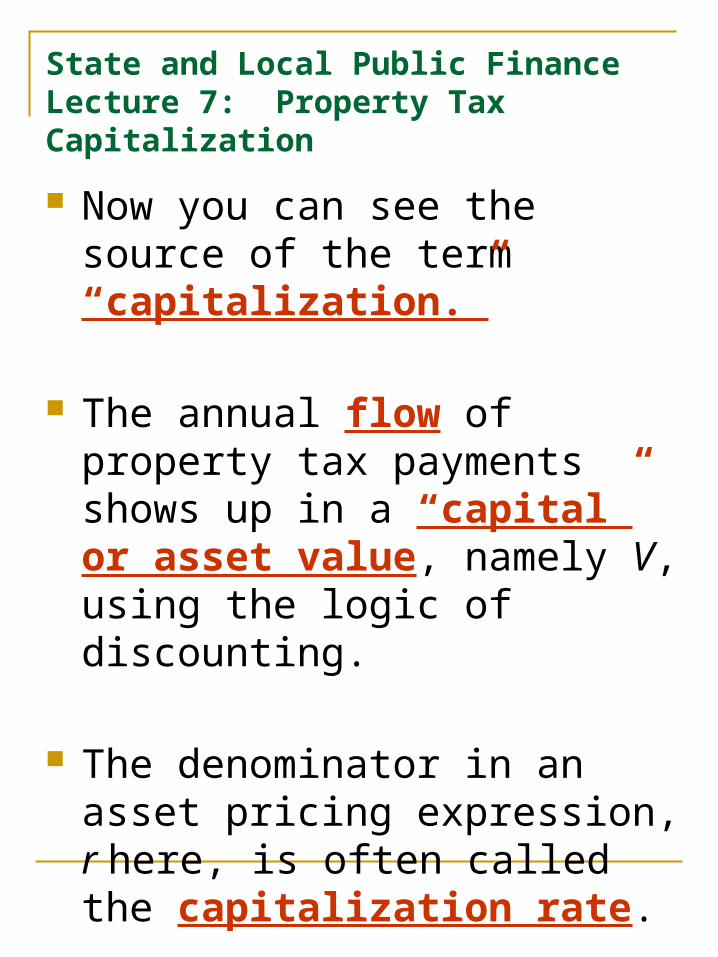

Now you can see the source of the term “capitalization.”

The annual flow of property tax payments shows up in a “capital” or asset value, namely V, using the logic of discounting.

The denominator in an asset pricing expression, r here, is often called the capitalization rate.

State and Local Public FinanceLecture 7: Property Tax Capitalization

This equation assumes that property taxes are fully capitalized.

As we will see, this might not be the case, so a more general form is:

where β is the “degree of property tax capitalization;” i.e., the impact of a $1 increase in the present value of property taxes on the value of a house.

1 1(1 ) (1 )

L L

y yy y

tVPHVr r

tVPHr r

State and Local Public FinanceLecture 7: Property Tax Capitalization A value of β equal to 1.0

corresponds to full capitalization.

A value of β equal to 0.0 corresponds to no capitalization.

If β equals 0.5 a $1 increase in the present value of property taxes leads to a $0.50 decrease in the value of a house.

The value of β need not be the same under all circumstances.

State and Local Public FinanceLecture 7: Property Tax Capitalization

Solving the above for V yields the final capitalization equation:

Thus, houses with higher effective property tax rates (t) will have lower values (V).

The strength of this relationship depends on β.

PHVr t

State and Local Public FinanceLecture 7: Property Tax Capitalization

One can also derive a change form of the capitalization equation:

where Δ stands for change and 1 and 2 indicate time periods.

Thus, an increase in t (relative to other houses) will result in a decrease in V.

1 2

tVV r t

State and Local Public FinanceLecture 7: Property Tax Capitalization

These equations apply within a community.

Recall that

Poor assessments result in higher assessment-sales ratios, and hence higher effective tax rates, for some houses than for others.

These equations also apply across communities, which may have very different effective tax rates.

At mV

State and Local Public FinanceLecture 7: Property Tax CapitalizationHow Does Tax Capitalization Arise?

Real estate brokers indicate anticipated property tax payments so buyers can make comparisons across houses.

Lenders require mortgage plus tax payments to equal a fixed percentage of an applicant’s income.

An increase in T must be offset by a drop in the mortgage, and hence a drop in how much the applicant can pay for the house, V.

State and Local Public FinanceLecture 7: Property Tax Capitalization

Evidence on Property Tax Capitalization

Every reasonable study of property tax capitalization finds a statistically significant negative impact of property taxes on house values.

Estimates of β vary from 15 to 100 percent.

The main reason for this variation appears to involve expectations.

State and Local Public FinanceLecture 7: Property Tax Capitalization

So far, current tax differences across houses are implicitly assumed to persist indefinitely.

But if tax differences are not expected to persist, the capitalization of current differences, β, declines.

A difference observed today that will disappear upon sale has no impact on V.

A difference observed today that is expected to last one year will have only a tiny impact on sales price.

State and Local Public FinanceLecture 7: Property Tax Capitalization In Massachusetts, revaluations were

required by the state supreme court, but enforcement was weak. Communities knew they could avoid

revaluation for many years. Existing tax differences were expected to

persist, but not forever.

A study of capitalization in Massachusetts (by myself and three other scholars) found that current tax differences were capitalized at a rate of 32 percent. This is consistent with the expectation

that current tax differences would disappear in 13 years.

State and Local Public FinanceLecture 7: Property Tax Capitalization In Syracuse in the early 1990s,

revaluation had not occurred for decades and did not appear likely to happen any time soon.

But the city council unexpectedly decided to revalue.

A study of capitalization in Syracuse by Eisenberg (a PA Ph.D. student) found capitalization rates near 100 percent—exactly what the theory predicts when tax differences are expected to persist.

State and Local Public FinanceLecture 7: Property Tax Capitalization If property taxes are fully

capitalized, then any tax changes show up in house values immediately and there is no way to escape them.

An owner with a tax increase must either stay and pay the higher tax or leave and suffer a capital loss.

An owner with a tax cut gets a capital gain.

Moreover, the loss is the full present value of the future increases in taxes.

State and Local Public FinanceLecture 7: Property Tax Capitalization

Property Tax Capitalization and Public Policy

Because of these gains and losses, tax capitalization has bizarre implications for public policy.

Consider revaluation, which is a systematic revision of all assessed values.

Revaluation leads to capital gains for homeowners who were over-assessed and to capital losses for homeowners who were under-assessed.

State and Local Public FinanceLecture 7: Property Tax Capitalization For long-term residents, these

changes are fair.

A resident who has been underassessed for a long time has been given, in effect, a loan from the city and revaluation just claims back this “loan.”

But for new residents, these changes are not fair.

If someone bought an under-assessed house one day and the change is announced the next, this person has a capital loss even though she did not benefit from the poor assessment system.

State and Local Public FinanceLecture 7: Property Tax Capitalization Two ways to minimize this

fairness problem:

First, introduce a long lag between announcement and implementation. This lag allows owners at the time of announcement to escape some of the burden of the tax changes.

Second, make sure houses are revalued upon re-sale, which they were not in Massachusetts or Syracuse.

State and Local Public FinanceLecture 7: Property Tax Capitalization So a revaluation imposes some unfair

gains and losses but restores fairness in the near term and boosts faith in local government. This trade only makes sense if

assessments are updated regularly. Otherwise, gains and losses are handed

out each year as assessment errors mount.

Poor assessments also lead to court cases, which the city usually loses. People who buy over-assessed property

pay low prices—and then can sue the city for a rebate because of unfairly high taxes.

This happened in Boston, to the tune of tens of millions of dollars.

The only way to avoid this crazy situation is to keep assessments up to date!

State and Local Public FinanceLecture 7: Property Tax Capitalization Proposition 13 in California

represents another unusual case.

The proposition fixes assessment growth at 2%, so the assessment/ sales ratio, and hence t, declines over time for long-term owners.

This cannot be turned into a capital gain because houses are revalued upon sale.

But it represents a gift to long-term owners and it discourages mobility.

The U.S. Supreme Court said this was legal. Voters in California and a few other states like this reward to long-term residents; I don’t.

State and Local Public FinanceLecture 7: Property Tax Capitalization

Looking ahead

Property tax capitalization is a critical issue in economic development policy.

If property tax breaks are capitalized into the price of business property, then owners of this property at the time a tax break is announced may receive all the benefits even if they do not change their behavior,

And future owners (exactly the people the policy is intended to attract) may receive no benefits at all.