Embed Size (px)

Citation preview

Standard on Auditing 700 (Revised)Standard on Auditing 705

Presented by: Khushroo B. PanthakyAssurance Head and Western Region Practice Leader

Walker, Chandiok & Co.Chartered Accountants

At: 26th Regional Conference of WIRC of ICAINCPA, Mumbai, 16 December 2011

Agenda

• Standard on Auditing 700 (Revised) on Forming an

Opinion and Reporting on Financial Statements

• Standard on Auditing 705 on Modifications to the Opinion

in the Independent Auditor’s Report

Standard on Auditing (SA) 700 (Revised)

Forming an Opinion and Reporting on Financial Statements

Introduction

• Earlier known as SA 700 (AAS 28), “ The Auditor’s Report on Financial

Statements”

• Deals with auditor’s responsibility to form an opinion on the financial

statements (FS)

• Deals with form and content of the auditor’s report issued on General

Purpose FS

• Promotes consistency in the auditor’s report which enables global

acceptance of the auditor’s report

• Consistency also helps promote user’s understanding and identify

unusual circumstances when they occur

• Effective for audits of FS for periods beginning on or after April 1, 2011

Objectives of the Auditor

• Form an opinion on the FS based on an evaluation of the conclusions drawn from the audit evidence obtained

• Express clearly the above opinion through a written report that also

describes the basis for the opinion

Key Definitions

• General Purpose FS – includes Balance Sheet, Statement of Profit and

Loss, Cash Flow Statement (where applicable) and statements and

explanatory notes which form part thereof, issued for the use of various stakeholders, Government and their agencies and the public

• General purpose framework – A financial reporting framework

designed to meet the common financial information needs of a wide range of users. The financial reporting framework may be a fair

presentation framework or a compliance framework

• Unmodified opinion – The opinion expressed by the auditor when the

auditor concludes that the FS are prepared, in all material respects, in accordance with the applicable financial reporting framework

Key Definitions

• Fair presentation framework - A financial reporting framework that

requires compliance with the requirements of the framework and

acknowledges that:

(i) To achieve explicitly or implicitly the fair presentation of thefinancial statements, it may be necessary for management to

provide disclosures beyond those specifically required by the

framework; or

(ii) It may be explicitly necessary for management to depart from arequirement of the framework to achieve fair presentation of the

financial statements. Such departures are expected to be

necessary only in extremely rare circumstances

Key Definitions

• Compliance framework - A financial reporting framework that requires

compliance with the requirements of the framework, but does not containthe acknowledgements in (i) or (ii) above

• Reference to “Financial Reporting Standards” in this SA means the

Accounting Standards promulgated by the Accounting StandardsBoard (ASB) of the ICAI or Accounting Standards, notified by the Central

Government by publishing the same as the Companies (Accounting

Standards) Rules, 2006, or the Accounting Standards for Local Bodiespromulgated by the Committee on Accounting Standards for Local Bodies

(CASLB) of the ICAI, as may be applicable

Forming an opinion on the Financial Statements

• Opinion on whether the FS are prepared, in all material respects, in

accordance with the applicable financial reporting framework

• The auditor shall conclude as to whether he has obtained reasonableassurance about whether the FS as a whole are free from materialmisstatement, whether due to fraud or error. That conclusion shall take

into account:

(a) The auditor’s conclusion whether sufficient appropriate auditevidence has been obtained

(b) The auditor’s conclusion, whether uncorrected misstatementsare material, individually or in aggregate; and

(c) The required evaluations (summarised in subsequent slides)

Forming an opinion on the Financial Statements

The auditor shall EVALUATE

• whether the FS are prepared, in all material

respects, in accordance with the requirements

of the applicable financial reporting framework

• qualitative aspects of the entity’s accountingpractices, including indicators of possible biasin management’s judgments

Forming an opinion on the Financial Statements

The auditor shall also evaluate whether, in view of the requirements of the

applicable financial reporting framework:

(a) The FS adequately disclose the significant accounting policiesselected and applied

(b) The accounting policies selected and applied are consistent with the applicable financial reporting framework and are

appropriate

(c) The accounting estimates made by management are reasonable

Forming an opinion on the Financial Statements

(d) The information presented in the FS is relevant, reliable, comparable and understandable

(e) The FS provide adequate disclosures to enable the intended users

to understand the effect of material transactions and events on

the information conveyed in the FS; and

(f) The terminology used in the FS, including the title of each FS, is appropriate

Forming an opinion on the Financial Statements

In accordance with the fair presentation framework,the auditor shall evaluate whether the FS achieve

fair presentation, including consideration of:

a) The overall presentation, structure and content of the FS; and

b) Whether the FS, including the related notes,

represent the underlying transactions and

events in a manner that achieves fair presentation

The auditor shall also evaluate whether the FS adequately refer to or describe

the applicable financial reporting framework

Form of Opinion

Unmodified OpinionWhen the auditor concludes that the FS are prepared, in all material

respects, in accordance with the applicable financial reporting framework

Form of Opinion

Modified Opinion (SA 705) – Under what circumstances

When the auditor concludes that, based on audit evidence obtained, the FS as a whole are ‘not free’ from material misstatement; or

Is unable to obtain sufficient appropriate audit evidence to conclude

that the FS as a whole are free from material misstatement

Form of Opinion

Modified Opinion (SA 705)• If FS do not achieve fair presentation, the auditor shall discuss the matter

with management and, accordingly determine the need for modified opinion

• When the FS are prepared using the compliance framework, evaluation of fair presentation is not required. However, if under extremely rare

circumstances, the auditor concludes that such FS are misleading, the

auditor shall discuss the matter with management and accordingly

communicate it in the auditor’s report

Auditor’s report

• Shall be in writing

• Shall have a title clearly indicating report of an independent auditor

• Shall be addressed as required by the circumstances of the

engagement

• The introductory paragraph in the report shall:

(a) Identify the entity whose FS have been audited;

(b) State that the FS have been audited;

(c) Identify the title of each statement that comprises the FS;

(d) Refer to the summary of significant accounting policies and other

explanatory information; and

(e) Specify the date or period covered by each statement comprising

the FS.

Auditor’s report – Management’s Responsibility section

• The auditor’s report need not refer specifically to “management”, but

shall use the term that is appropriate in the context of the legal and/or

regulatory framework applicable to the entity. In case of some entities, the

appropriate reference may be to Those Charged With Governance (TCWG)

• The auditor’s report shall include a section with the heading Management’s[or other appropriate term] Responsibility for the Financial Statements”

• Management’s responsibility for the preparation of the FS is described in the

terms of the audit engagement. The description shall include an explanation

that management is responsible for the preparation of the FS

• This responsibility includes the design, implementation and maintenanceof internal control relevant to the preparation of FS that are free from

material misstatement, whether due to fraud or error

Auditor’s report – Management’s Responsibility section

• Where the FS are prepared in accordance with a fair presentation

framework, the explanation of management’s responsibility for the FS

shall refer to “the preparation and fair presentation of these FS”

Auditor’s report – Auditor’s Responsibility section

• The auditor’s report shall include a section with the heading “Auditor’sResponsibility”

• It shall state that the responsibility of the auditor is to express anopinion on the FS based on the audit

• It shall state that the audit was conducted in accordance with Standardson Auditing issued by the ICAI. It shall also explain that those

Standards require that the auditor comply with ethical requirements and

that the auditor planned and perform the audit to obtain reasonable

assurance about whether the FS are free from material misstatement

Auditor’s report – Auditor’s Responsibility section

• It shall describe an audit by stating that:

a) An audit involves performing procedures to obtain audit evidence

about the amounts and disclosures in the FS;

b) The procedures selected depend on the auditor’s judgment,including the assessment of the risks of material misstatement of the

FS, whether due to fraud or error

c) In making those risk assessments, the auditor considers internal

control relevant to the entity’s preparation of the FS in order todesign audit procedures that are appropriate in the circumstances,

but not for the purpose of expressing an opinion on theeffectiveness of the entity’s internal control

Auditor’s report – Auditor’s Responsibility section

d. In circumstances when the auditor also has a responsibility to

express an opinion on the effectiveness of internal control in

conjunction with the audit of the FS, the auditor shall omit thephrase that the auditor’s consideration of internal control is not for

the purpose of expressing an opinion on the effectiveness of internal

control; and

e. An audit also includes evaluating the appropriateness of theaccounting policies used and the reasonableness of accountingestimates made by management, as well as the overallpresentation of the FS

Auditor’s report– Auditor’s Responsibility section

• Where the FS are prepared in accordance with a fair presentation

framework, the description of the audit in the auditor’s report shall refer to

“the entity’s preparation and fair presentation of the FS”

• It shall state whether the auditor believes that the audit evidence obtained

is sufficient and appropriate to provide a basis for the auditor’s opinion

Auditor’s opinion

• The auditor’s report shall include a section with the heading “Opinion”

• When expressing an unmodified opinion on FS prepared in accordance

with a fair presentation framework, the auditor’s opinion shall, unless

otherwise required by law or regulation, use one of the following phrases,

which are regarded as being equivalent:

a) The FS present fairly, in all material respects, in accordance with

[the applicable financial reporting framework]; or

b) The FS give a true and fair view of ------- in accordance with [the

applicable financial reporting framework]

• When expressing an unmodified opinion on FS prepared in accordance

with a compliance framework, the auditor’s opinion shall be that the FS

are prepared, in all material respects, in accordance with [the applicable

financial reporting framework]

Auditor’s opinion

When the applicable financial reporting framework

encompasses financial reporting standards and

legal or regulatory requirements, the framework is

identified in such terms as “………..the

information required by the Companies Act, 1956, in

the manner so required and (give a true and fair

view) in conformity with the accounting principles

generally accepted in India”.

Other Reporting Responsibilities

• If the auditor addresses other reporting responsibilitiesin the auditor’s report in addition to the responsibility

under the SAs, these shall be in a separate section inthe auditor’s report and sub-titled “Report on Other

Legal and Regulatory Requirements,” or otherwise as

appropriate to the content of the section

• The “Report on Other Legal and Regulatory

Requirements” shall follow the “Report on the Financial

Statements.”

• The separate section helps clearly distinguish them

from the auditor’s responsibility under the SAs

Other Requirements on Auditor’s report

• The auditor’s report shall be signed in the personal name with

membership number and the name of the audit firm with registration

number

• The auditor’s report shall be dated no earlier than the date on which the

auditor has obtained sufficient appropriate audit evidence on which to

base the auditor’s opinion on the FS, including evidence that:

a) All the statements that comprise the FS, including the related notes,

have been prepared; and

b) Those with the recognised authority have asserted that they have

taken responsibility for those FS.

• The auditor’s report shall name specific location, which is ordinarily the

city where the audit report is signed

Auditor’s report for audits conducted in accordance with SA and ISA

In addition to compliance with SAs, the auditor may have complied withthe International Standards on Auditing (ISAs). In such circumstances,

the auditor’s report may refer to ISAs in addition to the SAs, but the auditor

shall do so only if:

a) There is no conflict between the requirements in SAs and those in

ISAs that would lead the auditor (i) to form a different opinion, or (ii)

not to include an Emphasis of Matter paragraph that, in the

particular circumstances, is required by ISAs; and

b) The auditor’s report includes, at a minimum, each of the elementsset out in the previous slide when the auditor uses the layout or

wording specified by the SAs. Reference to law or regulation shall

be read as reference to the SAs. The auditor’s report shall thereby

identify such SAs.

Reference to more than one Financial Reporting Framework

• In some cases, the FS may represent that they are prepared in

accordance with two financial reporting frameworks (e.g., the national

framework and IFRS). This may be because management is required or

has chosen to prepare the FS in accordance with both frameworks

• Such description is appropriate only if the FS comply with each of the

frameworks individually and simultaneously without any need forreconciling statements

Material Modifications vis-à-vis ISA 700 – ‘Forming

an Opinion and Reporting on Financial Statements’

• Financial Reporting Standards for ISA 700 constitutes IFRS whereas for

SA 700, it represents Accounting Standards promulgated by the

Accounting Standards Board (ASB) of ICAI or notified by the Central

Government as part of Companies (Accounting Standards) Rules, 2006

• ISA 700 states that the auditor’s report shall name the location in thejurisdiction where the auditor practices. The requirement of mentioning

the auditor’s address has been replaced with the place of signature,

which is the name of the specific location, ordinarily the city where the audit

report is signed

• ISA 700 explains who is eligible for signing the auditor’s report in different

situations. In India, audit report is signed in the personal name of theauditor and in the name of the audit firm. The partner/proprietor signing

the audit report also needs to mention the firm registration number,

wherever applicable, and the membership number assigned by ICAI

Standard on Auditing (SA) 705

Modifications to the Opinion in the Independent Auditor’s Report

Introduction

• This SA deals with the auditor’s responsibility to issue an appropriate

report in circumstances when, in forming an opinion in accordance with SA

700 (Revised), a modification to the auditor’s opinion is necessary

• This SA establishes three types of modified opinions, namely, a

qualified opinion, an adverse opinion, and a disclaimer of opinion. The

decision on type of modified opinion depends upon:

a) The nature of the matter giving rise to the modification, i.e., whether the

FS are materially misstated or, in the case of an inability to obtain

sufficient appropriate audit evidence, may be materially misstated;

b) The auditor’s judgment about the pervasiveness of the effects or

possible effects of the matter on the FS

• This SA is effective for audits of FS beginning on or after April 1, 2011

Objective

A modified opinion on the FS is necessary when:

a) The auditor concludes, based on the audit evidence obtained, that

the FS as a whole are not free from material misstatement; or

b) The auditor is unable to obtain sufficient appropriate auditevidence to conclude that the FS as a whole are free from material

misstatement.

Definitions

• Pervasive – A term used to describe the effects on the FS of

misstatements or the possible effects on the FS of misstatements, if any,

that are undetected due to an inability to obtain sufficient appropriateaudit evidence. Pervasive effects on the FS are those that, in the

auditor’s judgment:

a) Are not confined to specific elements, accounts or items of the FS;

b) If so confined, represent or could represent a substantial proportion

of the FS; or

c) In relation to disclosures, are fundamental to users’ understanding

of the FS

• Modified opinion – A qualified opinion, an adverse opinion or a

disclaimer of opinion

Types of Modified Opinions

Qualified OpinionThe auditor shall express a qualified opinion when:

a) The auditor, having obtained sufficient appropriate audit evidence,

concludes that misstatements, individually or in the aggregate, arematerial, but not pervasive, to the FS; or

b) The auditor even though unable to obtain sufficient appropriate audit

evidence concludes that the possible effects on the FS of undetected

misstatements, if any, could be material but not pervasive

Adverse OpinionThe auditor shall express an adverse opinion when the auditor, having

obtained sufficient appropriate audit evidence, concludes that

misstatements, individually or in the aggregate, are both, material andpervasive to the Financial Statements

Types of Modified Opinions

Disclaimer of Opinion

• The auditor shall disclaim an opinion when the auditor is unable to obtainsufficient appropriate audit evidence on which to base the opinion, and

the auditor concludes that the possible effects on the FS of undetected

misstatements, if any, could be both material and pervasive

• The auditor shall disclaim an opinion when, in extremely rare

circumstances involving multiple uncertainties, the auditor concludes

that, notwithstanding having obtained sufficient appropriate audit evidence

regarding each of the individual uncertainties, it is not possible to form an

opinion on the FS due to the potential interaction of the uncertaintiesand their possible cumulative effect on the FS

Management imposed limitation after engagement acceptance

• If, after accepting the engagement, the auditor becomes aware of

management imposed limitation on the scope of the audit which is

likely to result in a qualified opinion or disclaimer of opinion, the auditor

shall request that management remove the limitation

• If management refuses to do so, the auditor shall communicate thematter to TCWG and determine whether it is possible to perform

alternative procedures to obtain sufficient appropriate audit evidence

Management imposed limitation after engagement acceptance

• If the auditor is unable to obtain sufficient appropriate audit evidence, the

auditor shall determine the implications as follows:

a) If the possible effects on the FS of undetected misstatements, could bematerial but not pervasive, the auditor shall qualify the opinion; or

b) If the possible effects on the FS of undetected misstatements, could beboth material and pervasive such that a qualification of the opinion

would be inadequate to communicate the gravity of the situation, the

auditor shall:

i) Resign from the audit, where practicable and not prohibited by law or

regulation; or

ii) If resignation from the audit before issuing the auditor’s report is not

practicable (for eg public sector entities) or possible, disclaim anopinion on the FS

Form and content of Modified Audit Report

• When the auditor modifies the opinion, he shall, include a paragraph in the

auditor’s report that provides a description of the matter giving rise to the

modification

• The auditor shall place this paragraph immediately before the opinionparagraph in the auditor’s report and use the heading “Basis for Qualified

Opinion”, “Basis for Adverse Opinion”, or “Basis for Disclaimer of Opinion”,

as appropriate

• If there is a material misstatement of the FS that relates to specific amounts

in the FS, the auditor shall include in the basis for modification paragraph, a

description and quantification of the financial effects of the

misstatement, unless impracticable.

• If it is not practicable to quantify the financial effects, the auditor shall stateso in the basis for modification paragraph

Opinion paragraph in Modified Audit Report

• When the auditor modifies the audit opinion, he shall use the heading“Qualified Opinion”, “Adverse Opinion”, or “Disclaimer of Opinion”, as

appropriate, for the opinion paragraph

• When the auditor expresses a qualified opinion due to a material

misstatement in the FS, the auditor shall state in the opinion paragraph that,

except for the effects of the matter(s) described in the Basis for Qualified

Opinion paragraph:

a) The FS present fairly, in all material respects in accordance with the

applicable financial reporting framework when reporting in accordance

with a fair presentation framework; or

b) The FS have been prepared, in all material respects, in accordance

with the applicable financial reporting framework when reporting in

accordance with a compliance framework

Opinion paragraph in Modified Audit Report

• When the modification arises from an inability to obtain sufficient

appropriate audit evidence, the auditor shall use the corresponding phrase

“except for the possible effects of the matter(s)...” for the modified

opinion

• When the auditor expresses an adverse opinion, he shall state in the

opinion paragraph that, because of the significance of the matter(s)described in the Basis for Adverse Opinion paragraph:

a) The FS do not present fairly in accordance with the applicable

financial reporting framework, when reporting is in accordance with a

fair presentation framework; or

b) The FS have not been prepared, in all material respects, in

accordance with the applicable financial reporting framework when

reporting is in accordance with a compliance framework

Description of Auditor’s responsibility – Modified Opinion

• In a qualified or adverse opinion, the auditor shall amend the descriptionof the auditor’s responsibility to state that the auditor believes that the

audit evidence obtained is sufficient and appropriate to provide a basis for

the auditor’s modified audit opinion

• In a disclaimer of opinion, the auditor shall amend the introductoryparagraph of the auditor’s report to state that the auditor was engaged to

audit the FS. The auditor shall also amend the description of the auditor’s

responsibility and the scope of the audit to state only the following: “Our

responsibility is to express an opinion on the FS based on conducting the

audit in accordance with SAs issued by the ICAI. Because of the matter(s)

described in the Basis for Disclaimer of Opinion paragraph, however, we

were not able to obtain sufficient appropriate audit evidence to provide a

basis for an audit opinion”

Communication with Those Charged With Governance (TCWG)

• When the auditor expects to modify the opinion in the auditor’s report, the

auditor shall communicate with TCWG the circumstances that led to the

expected modification and the proposed wording of the modification

• The auditor should seek the concurrence of TCWG regarding the facts of

the matter(s) giving rise to the expected modification(s), or to confirmmatters of disagreement with management as such; and

• TCWG to have an opportunity, where appropriate, to provide the auditorwith further information and explanations in respect of the matter(s)

giving rise to the expected modification(s)

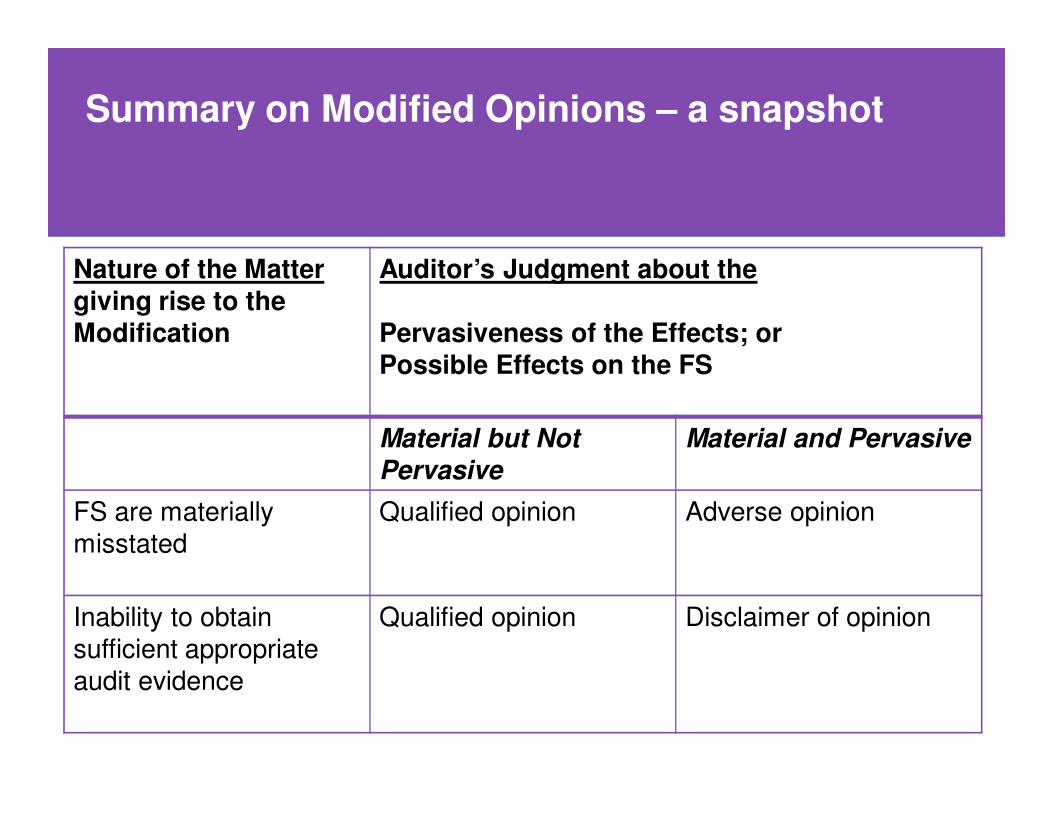

Summary on Modified Opinions – a snapshot

Nature of the Mattergiving rise to theModification

Auditor’s Judgment about the

Pervasiveness of the Effects; or Possible Effects on the FS

Material but Not

Pervasive

Material and Pervasive

FS are materially

misstated

Qualified opinion Adverse opinion

Inability to obtain

sufficient appropriate

audit evidence

Qualified opinion Disclaimer of opinion

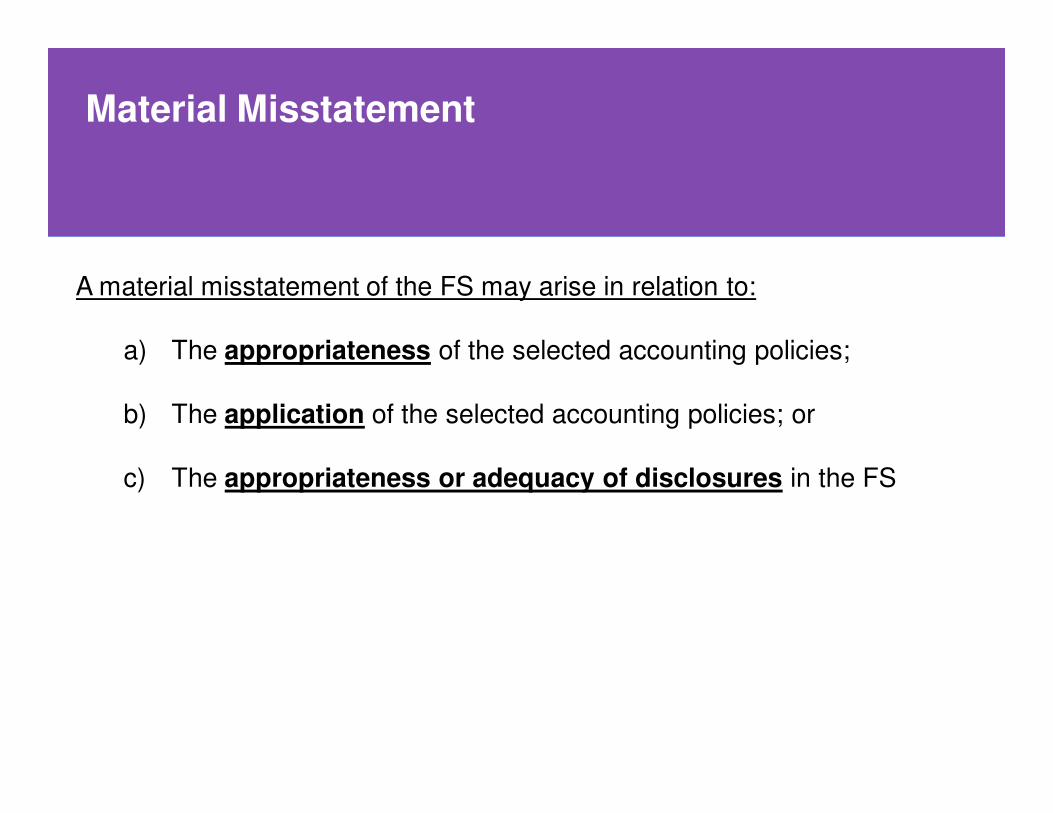

Material Misstatement

A material misstatement of the FS may arise in relation to:

a) The appropriateness of the selected accounting policies;

b) The application of the selected accounting policies; or

c) The appropriateness or adequacy of disclosures in the FS

Material modifications vis-à-vis ISA 705, “Modifications to the Opinion in the Independent Auditor’s Report

ISA 705 requires the auditor to include in the basis for modification paragraph,

a description and quantification of the financial effect of themisstatement. Since the said paragraph covers only the effect of the

individual quantification of the misstatement on the FS, that paragraph hasbeen changed also to include the effect of the aggregate quantificationsof the misstatements on the FS

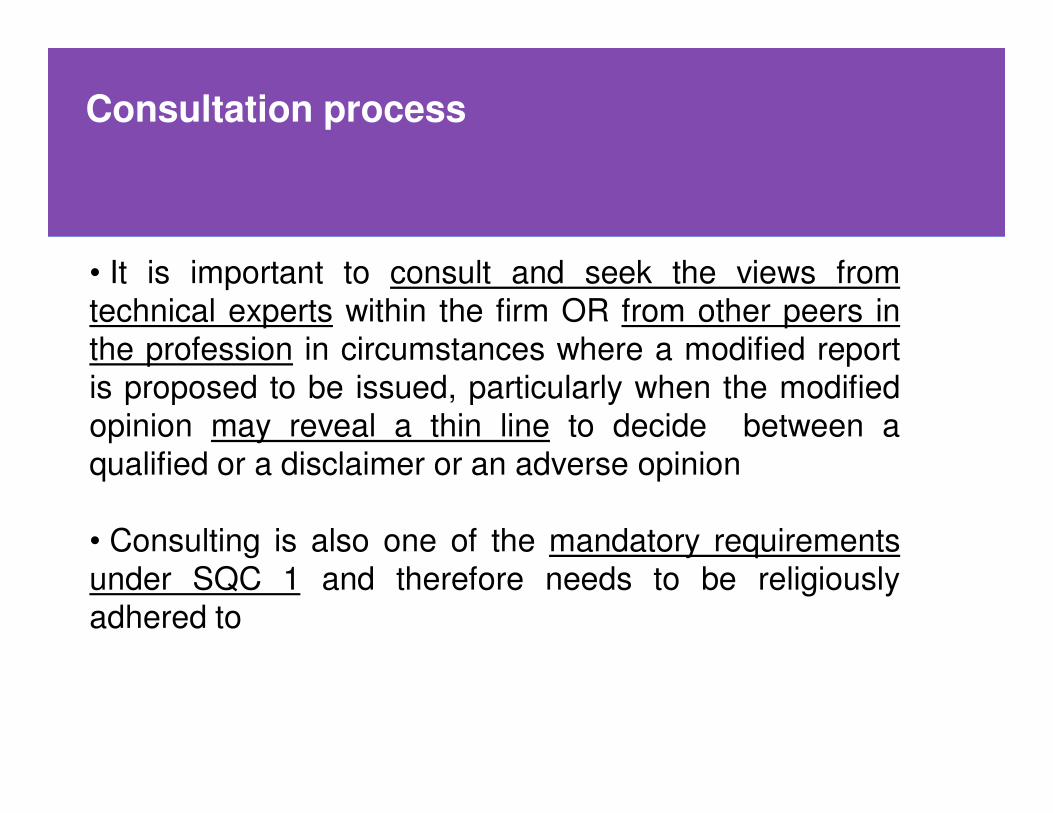

Consultation process

• It is important to consult and seek the views from

technical experts within the firm OR from other peers in

the profession in circumstances where a modified report

is proposed to be issued, particularly when the modified

opinion may reveal a thin line to decide between a

qualified or a disclaimer or an adverse opinion

• Consulting is also one of the mandatory requirements

under SQC 1 and therefore needs to be religiously

adhered to

Thank you very much for a patient listening