Embed Size (px)

Citation preview

1

SRP Spain_ Metacase Insights into Youtube & GDN potential to reach harder-to-reach TV targets

Analysis based on the research on 25 multiscreen (TV+YT & GDN) campaigns

March 2.014

Google Confidential and Proprietary

CONTEXT

2

1 Research summary

2 Methodology and scope

3 Research results

3.0 Context_ Media audiences and online video consumption in Spain

3.1 Incremental reach generation

3.2 YouTube&GDN efficacy to reach lighter TV viewers

3.4 Impact on media planning cost efficiency

4 Testimonials

3

1. Research summary

Google Confidential and Proprietary

Research summary_ Key insights

4

1 YouTube & GDN generated relevant extra reach to TV; only YouTube added on average 6 incremental reach points to effective TV reach (5+ TV OTS)

2 TV allows advertisers to generate massive reach but in a really unbalanced way: TV concentrates almost 70% of GRP´s on only one third of audience

3 Youtube is effective to reach lighter TV viewers: more than 70% of its GRP´s served out of high TV viewers with an equilibrated contact distribution among different TV groups

4 Light TV viewers prove to be a valuable hard-to-reach target: they are younger, wealthier and more educated

5 Inclusion of Youtube & GDN optimizes media planning in terms of cost efficiency: cost saving on average was 12.9%

5

2. Methodology and Scope

Google Confidential and Proprietary

KANTAR WORLPANEL households (n: 8.400)

KANTAR WORLDPANEL individuals (n: 4.863)

Exposure to Digital based on impression tags

KANTAR MEDIA TV PANEL (n: 11.912)

Official Spain TV currency

Exposure to TV based on fusion to TV currency panel

(Kantar Media)

FIXED FUSION

Methodology How to accurately measure TV+Web exposure

• Fusion process is based on similarities among Kantar Media (TV) and Kantar Worldpanel (online) panelists.

• “Twins” are created based on socio-demographics, attitudes, TV channel profile, day band profile (multidimensional reduction) and 200 additional exclusive clusters.

6

Google Confidential and Proprietary

Methodology Media exposure is not based on declarative data

KANTAR WORLPANEL (DIGITAL) KANTAR MEDIA TV PANEL

CROSS MEDIA EXPOSURE

ONLINE YOUTUBE TV

7

Google Confidential and Proprietary

• 25 multiscreen (TV+YT & GDN) campaigns measured with top advertisers between July 2012 and September 2013. Wide range of different media plans, targets and verticals

Methodology Research scope

8

Google Confidential and Proprietary

Methodology Research scope (I)

Industry Announcer Target

(onliners) TV GRP

Total online impressions

Online planning

AUTO FORD Individuals 30-45 362 40.105.359 YouTube&GDN

AUTO SEAT Men 25-44 354 15.047.325 Youtube

AUTO CITROEN Individuals 30-45 533 14.954.751 YouTube&GDN

AUTO VOLKSWAGEN Men 25-50 569 11.948.684 YouTube

BEAUTY ARBORA Women 15-35 1760 12.551.780 Youtube

CPG NESCAFÉ Households 25-44. 1.344 24.506.704 YouTube&GDN

CPG LISTERINE Women 20-54 757 35.662.053 YouTube&GDN

CPG CPG BRAND Housewives +55 1315 65.076.968 GDN

CPG MCDONALDS Individuals 18-44 663 10.013.771 YouTube&GDN

CPG BRAUN Women 15-40 474 32.274.811 YouTube&GDN

CPG WIPP Women 25-45 660 7.880.863 YouTube

ENTERTAINMENT XBOX Men 18-49 411 9.211.278 Youtube

9

Google Confidential and Proprietary

Methodology Research scope (II)

Industry Announcer Target (onliners) TV GRP Total online impressions

Online planning

FINANCE BANCO POPULAR Individuals +30 1204 130.298.997 GDN

FINANCE BBVA Individuals 25-54 1707 8.924.800 Youtube

INSURANCE RASTREATOR Individuals 30-50 876 36.328.897 YouTube&GDN

INSURANCE GÉNESIS Individuals 30-55 312 68.991.922 YouTube&GDN

RETAIL IKEA Women 25-45 464 12.530.118 Youtube

RETAIL WORTEN Individuals +16 239 8.014.272 Youtube

RETAIL IKEA Women 25-45 483 35.095.957 YouTube&GDN

RETAIL DECATHLON Individuals 16 - 44 298 22.189.342 YouTube&GDN

RETAL EL CORTE INGLES Women 30-45 1139 28.308.498 YouTube&GDN

TECH ARSYS Individuals 25-45 748 51.296.086 YouTube&GDN

TECH MOVISTAR Individuals +16 2880 55.341.290 YouTube&GDN

TECH VODAFONE Individuals 25-45 787 41.449.865 YouTube&GDN

TECH ONO Individuals 25-54 1282 3.380.299 Youtube

10

11

3. Research results

12

3.0 Context_ Media exposure and online video consumption in Spain

Google Confidential and Proprietary

Media exposure in Spain Internet penetration evolution

26.9 32.4 34.3

37.5 41.1

45.4 49.3

53.0 57.1

61.4 66.5

13.6 16.8

19.7 22.2

26.2 29.9

34.3 38.4

42.5 48.2

56.4

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Monthly Dialy

More than 65% of total Spanish population (15+ y.o) are onliners and almost 55% connect daily

Source: EGM (III wave 2013); Base: Total spanish population 15+ 13

Google Confidential and Proprietary

Media exposure in Spain Internet penetration evolution

% of internet daily connection is growing particularly fast (+17% YoY)

Source: EGM (III wave 2013); Base: Total spanish population 15+ 14

8.3% 17%

Monthly Connection Daily Connection

Evolution of internet connection (% YoY _2.013 vs 2.012)

Google Confidential and Proprietary

Media exposure in Spain Total audience by media

34,246

26,151 23,926 23,563

16,772

12,181

5,824

1,242

Television Internet Radio Outdooradvertising

Magazines Newspapers Suplements Cinema

Although TV remains dominant, Digital is growing fast. In fact, Internet is just currently the second media that collects a highest audience volume in Spain

Source: EGM (III wave 2013); Base: Total spanish population 15+ 15

Google Confidential and Proprietary

Media exposure in Spain TV vs YouTube & GDN audience´s profile

Attending to demographic characteristics, YouTube & GDN audience is wealthier and younger than TV.

19.4

31.5

49.1 48.6 51.4

11.6

16.6 16.8

21.9

33.1 29.3

48.9

21.8

53.8

46.2

19.5 23.7 24.7

18.5

13.6

29.8

48.7

21.5

51.6 48.4

17.2

22.6 25.8

19.4 15.0

Uppermiddleclass

Middleclass

Lowermiddleclass

Male Female Persons:15-24

Persons:25-34

Persons:35-44

Persons:45-54

Persons:55+

TV audience GDN audience YouTube audience

Sources: Kantar (TV data_December 2013), Comscore (YouTube&GDN_December 2013); Base: Total spanish population 15+ 16

Social class (%) Age(%) Gender (%)

Google Confidential and Proprietary

Media exposure in Spain Monthly reach among total population (15+)

Only YouTube reaches more than 40% of total Spanish population (15+ y.o)

Sources: Kantar (TV data_December 2013), Comscore (YouTube&GDN_December 2013); Base: Total spanish population 15+ 17

9.2%

41.0%

45.1%

56.3%

58.4%

70.8%

73.5%

86.0%

93.6%

94.0%

95.1%

95.6%

96.3%

CANAL+ 1

YouTube

INTERECON…

TELEDEPORTE

GDN

DIVINITY

NEOX

La2

LA SEXTA

CUATRO

T5

La1

A3

Total monthly reach (Total population 15+ y.o.)

Google Confidential and Proprietary

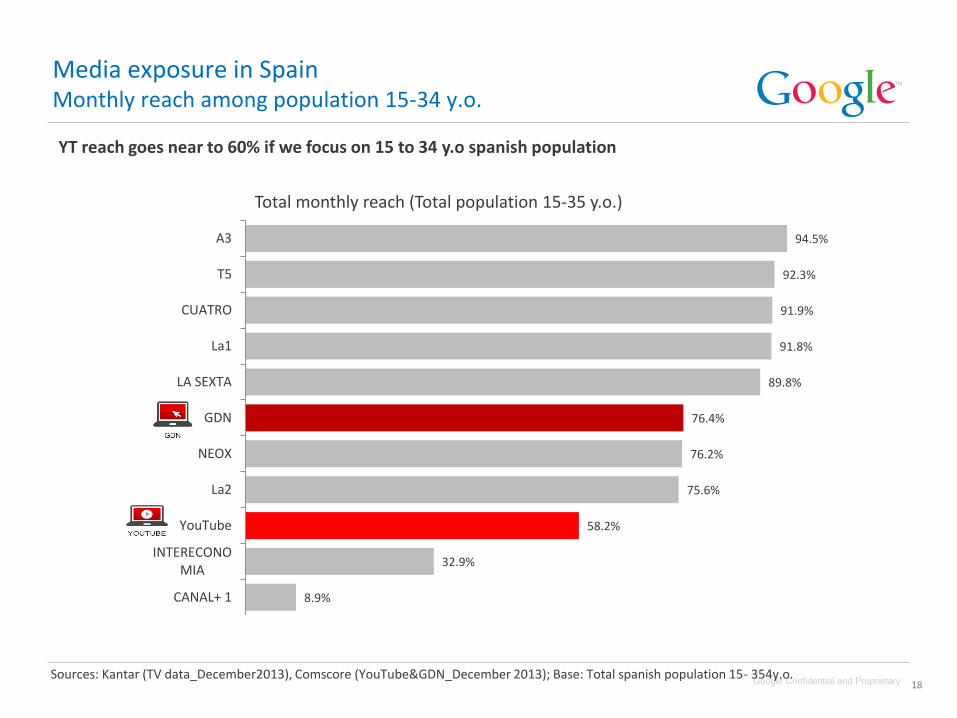

Media exposure in Spain Monthly reach among population 15-34 y.o.

YT reach goes near to 60% if we focus on 15 to 34 y.o spanish population

Sources: Kantar (TV data_December2013), Comscore (YouTube&GDN_December 2013); Base: Total spanish population 15- 354y.o. 18

8.9%

32.9%

58.2%

75.6%

76.2%

76.4%

89.8%

91.8%

91.9%

92.3%

94.5%

CANAL+ 1

INTERECONOMIA

YouTube

La2

NEOX

GDN

LA SEXTA

La1

CUATRO

T5

A3

Total monthly reach (Total population 15-35 y.o.)

Google Confidential and Proprietary

Media exposure in Spain Online video consumption

More than 19MM of Spaniards watch online videos regularly in YouTube (monthly average of 80.6 videos watched per viewer)

Sources: Comescore Videometrics (December 2013)

Online video metrics (December 2013)

Total Internet Audience

Total YouTube

Unique viewers (000) 23.373 19.926

Videos per viewer 242.2 80.6

Watched Videos (000) 5.661.151 1.607.333

Minutes per video 4.6 5.7

19

Google Confidential and Proprietary

December 2.013

Vs

April 2.013

Watched Videos

+53%

Minutes per video

-11%

Media exposure in Spain Online video consumption in YouTube

Total watched videos in Youtube increased 53% in the last 6 months while average length per video decreased slightly. It is remarkable that Youtube gained +12% penetration in population 55+ y.o

Sources: Comescore Videometrics (December 2013) 20

15-34 y.o. 35-54 y.o. +55 y.o.

+3,9% +9,4% +12,4%

Evolution of YouTube Audience

2.013 vs year ago

3.1 Incremental reach generation

Google Confidential and Proprietary

Overlap TV + YT & GDN

19.1%

Only TV

62.9%

Exclusive YT & GDN reach :

+3.7 p%

Average TV reach (1+)

82.0%

Average YT & GDN reach (1+)

22.8%

Incremental reach generation YouTube&GDN additional reach to TV

YT & GDN added an average of 3.7 extra reach points to TV

Source: Kantar Worldpanel– internet users Base: 25 TV+YouTube&GDN campaigns measured in 2012/2013 22

Google Confidential and Proprietary

Tech Retail Finance Auto CPG

30.4% 16.5%

3.2% 4.4%

20.7%

5.2%

20.2%

3.5%

23.3%

2.8% Exclusive Youtube &GDN reach

Average Youtube &GDN reach

Incremental reach generation YouTube & GDN additional reach to TV_ Split by verticals

Source: Kantar Worldpanel cross media analysis– internet users Base TV+Youtube&GDN campaigns Telecom: 5; Retailers: 5; Finance: 4; Auto: 4; CPG: 7

20.695.088 27.377.657 61.136.154* 21.227.637 32.135.764 Av. YT & GDN Impressions

* Finance includes an only GDN (no YouTube) digital campaign of more than 130M of impressions

87.4% 71.8% 83% 81.1% 85.1% Average TV reach

23

Google Confidential and Proprietary

Overlap TV + YouTube

10.1%

Only TV

71.3%

Exclusive Youtube reach:

+2.0 p%

Average TV reach (1+)

81.4%

Average YT reach (1+)

12.1%

Incremental reach generation Only YouTube additional reach to TV

Only YouTube added an average of 2 extra reach points to TV

Source: Kantar Worldpanel– internet users Base: 23 TV+YouTube campaigns measured in 2012/2013 24

Google Confidential and Proprietary

Tech Retail Finance Auto CPG

Incremental reach generation Only YouTube additional reach to TV _Split by verticals

87.4% 71.8% 83% 81.1% 85.1% Average TV reach

14.8% 9.4%

2.3% 2.8%

9.1%

1.5%

11.8%

1.9%

13.9%

1.6% Exclusive Youtube reach

Average Youtube reach

11.161.276 8.459.042 7.119.529 9.081.040 8.640.898 Av. YT Impressions

Source: Kantar Worldpanel cross media analysis– internet users Base TV+Youtube campaigns measured Telecom: 5; Retailers: 5; Finance: 4; Auto: 4; CPG: 7 25

Google Confidential and Proprietary

Incremental reach generation YT & GDN additional reach on effective TV reach

TOTAL TV REACH

(+1 OTS)

TOTAL WEB REACH

(+1 OTS)

6.0 p% 4.3 p% 2.0 p% 12.1% 81.4%

TOTAL YouTube&GDN

82.0%

26

10.7 p% 7.6 p% 3.7 p% 22.8%

1+ OTS TV 3+ OTS TV 5+ OTS TV

Exclusive Digital reach by effective TV reach (%)

YouTube added an average of 6 additional points to effective TV reach (5+TV OTS)

Source: Kantar Worldpanel– internet users Base: 25 TV+YouTube&GDN campaigns measured in 2012/2013

Google Confidential and Proprietary

Incremental Youtube reach

14.8% 10.7% 12.5% Average Youtube reach

+ 3 p% +1.3 p% +2.3 p%

Incremental reach generation YouTube&GDN additional reach to TV_ Split by targets

Rate of incremental reach was slightly higher for campaigns targeted to males

Campaign target: 100% Males

Source: Kantar Worldpanel cross media analysis– internet users Base TV+ Youtube campaigns measured Men: 3; Women: 8; Individuals: 12

Av. TV reach 82.4% 83.4% 81%

Av. Impressions 12.069.096 9.725.087 8.226.017

Campaign target: 100% Females

Campaign target: Individuals (no gender segmentation)

27

Google Confidential and Proprietary

Incremental reach generation YouTube&GDN share of incremental reach

Attending to TV reach it is possible to calculate estimated share of incremental reach for YouTube&GDN (a regression analysis was run to confirm linear relation between both variables, and not significance outliners were detected among all 25 TV+Digital campaigns measured)

Av. Share of IR (16.7%)

On

line

(Yo

uTu

be&

GD

N) s

har

e o

f in

crem

enta

l rea

ch

TV reach

28

TV Reach

Source: Kantar Worldpanel– internet users Base: 25 TV+YouTube&GDN campaigns measured in 2012/2013

The lower TV reach , the higher the YT share

of exclusive reach

Google Confidential and Proprietary

Incremental reach generation YouTube & GDN share of incremental reach

17.6 of total Youtube reach was exclusive (not double up with TV) and 50% of Youtube exposed received less than 5 TV OTS

Source: Kantar Worldpanel– internet users Base: 25 TV+YouTube&GDN campaigns measured in 2012/2013 29

16.7

34.8

48.5

0%

100%

1+ TV OTS 3+ TV OTS 5+ TV OTS

YT & GDN share of incremental reach (100= Total YT & GDN reach)

17.6

36.1

50.1

0%

100%

1+ TV OTS 3+ TV OTS 5+ TV OTS

YT share of incremental reach (100= Total YT reach)

% of exclusive reach

% of double up reach with TV

3.2 YouTube & GDN efficacy to reach lighter TV viewers

Google Confidential and Proprietary

YouTube&GDN efficacy to reach lighter TV viewers Tercile analysis

Tercile analysis consists in splitting the audience in groups depending on level of exposure to TV campaign

TOTAL TV EXPOSED AUDIENCE NON TV EXPOSED AUDIENCE

× 1/3

High TV exposed

The 33% of TV exposed who

received the most TV contacts

1/3 1/3 Medium TV

exposed

Light TV exposed

The 33% of TV exposed who

received the least TV contacts

Non TV exposed

Those who were not exposed to

the TV campaign at all

31

Google Confidential and Proprietary

YouTube&GDN efficacy to reach lighter TV viewers TV OTS distribution

32

TV shows an unbalanced contacts distribution: the highest 3rd had x7.3 TV OTS more than the lowest 3rd

100

1/3 0.0

1/3

1/3

Non TV exposed Total High TV exposed Medium TV exposed Low TV exposed

The 1/3 of those exposed to Tv

campaigns that were most exposed to them

The 1/3 of those exposed to TV campaigns

that were medium exposed to them

The 1/3 of those exposed to TV

campaigns that were less exposed to them

Exposed to TV campaigns

Non exposed to TV campaigns

19.6 TV OTS

7.8 TV OTS

2.7 TV OTS

The highest 3rd had x7.3 TV OTS more than the lowest 3rd

OTS = Opportunity To See = one single contact with the ad in a given media

Source: Kantar Worldpanel– internet users Base: 25 TV+YouTube&GDN campaigns measured in 2012/2013

Google Confidential and Proprietary

YouTube&GDN efficacy to reach lighter TV viewers OTS distribution by media

33

TV contacts distribution tends to concentrate on “High exposed” audience while impact of technology (frequency capping, negative RMKT…) allows YouTube to show a much more equilibrated distribution

11.4

19.9

7.8

2.7

0.0

3.4 3.1 3.2 3.1 3.7

Total High TV exposed Medium TV exposed Low TV exposed Non TV

OTS by different levels of TV exposure (Average)

Total TV YouTube

Total Youtube&GDN (av.) 4.2 4.1 4.0 4.6

Source: Kantar Worldpanel– internet users Base: 25 TV+YouTube&GDN campaigns measured in 2012/2013

Google Confidential and Proprietary 34

Youtube proved to be particularly effective at delivering additional GRP´s among lighter TV viewers

100

64.8

25.8

9.2

0

100

26.3 27.9 27.2

18.2

100

27.2 26.1 27

19.3

Total High TV exposed Medium TV exposed Low TV exposed Non TV

Media GRPs distribution by different levels of TV exposure (%)

Total TV Youtube&GDN Only YouTube

Almost 70% of TV GRP´s delivered to 1/3

of audience

More than 70% of YouTube GRP´s delivered out of high TV viewers

Source: Kantar Worldpanel– internet users Base: 25 TV+YouTube&GDN campaigns measured in 2012/2013

YouTube&GDN efficacy to reach lighter TV viewers GRP´s distribution by media

Google Confidential and Proprietary

YouTube&GDN efficacy to reach lighter TV viewers Light TV viewer´s profile

Light TV viewers are more likely to be younger, wealthier and more educated.

Light TV viewers TV viewing (less than 160 min

day)

High TV viewers TV viewing (+ 320 min/day)

% Upper middle class

% population aged 25-54 y.o

% employed (currently working)

% higher education (university degree)

% Daily internet connection

100

100

100

100

100

130

140

148

228

149

35 Sources: Kantar (TV data 2013); Base: Total spanish population 15+

Indexed data (100= High Tv viewers)

3.3 Impact on media planning cost efficiency

Google Confidential and Proprietary

Impact on media planning cost efficiency

How much would it have cost to achieve total TV+Internet campaign reach with an only TV planning strategy?

100 87.7

12.3

TV Multiscreen (TV+Internet)

YouTube&GDN

TV

Average budget distribution (23 campaigns measured): • Internet: 12% • TV: 88%

37 Source: Kantar Worldpanel– internet users Base: 23 TV+YouTube&GDN campaigns measured in 2012/2013

Google Confidential and Proprietary

Impact on media planning cost efficiency TV reach curve (av.)

TV investment

TV reach

38

The last points of TV reach prove to be really expensive

Cost per reach point

INDEX: 39

Cost per point

INDEX: 607 Cost per point INDEX: 179

The last 4 points of reach are 6 times more

expensive than average TV reach

TV cost per reach point INDEX=100

Source: Kantar Worldpanel– internet users Base: 23 TV+YouTube&GDN campaigns measured in 2012/2013

Google Confidential and Proprietary

Impact on media planning cost efficiency How much would it have cost to achieve total campaign reach with an only TV planning strategy?

39

On average, to attain the equivalent reach of the multiscreen campaign (TV+YT & GDN) with an only TV planning strategy a 12.9% spending increment would have been required (6% for only YouTube)

Source: Kantar Worldpanel– internet users Base: 23 TV+YouTube&GDN campaigns measured in 2012/2013

Efficiency analysis TV + Youtube&GDN Efficiency analysis TV + Youtube (only)

Google Confidential and Proprietary

Impact on media planning cost efficiency

TV ONLY TV + Youtube & GDN

Share Shift

TOTAL CAMPAIGN NET REACH

40 Source: Kantar Worldpanel– internet users Base: 23 TV+YouTube&GDN campaigns measured in 2012/2013

41

4. Testimonials

Google Confidential and Proprietary

Testimonial_ NESTLE

“The research help us to confirm that online media is effective at generating incremental reach to TV, and give us the opportunity to impact the lightest tv viewers, which are

really hard to impact with standard advertising campaigns”.

Beatriz Ortiz de Zárate_

Media & Consumer Management Director Nestle Spain

42

Google Confidential and Proprietary

Testimonial_ Ford

“The main insights we obtained from the research is the online media potential to optimize TV campaigns in terms of both GRP´s and frequencies distribution. As a consequence, It was also proved its positive impact on media planning cost efficiency”.

Santiago Sainz Marketing Director Ford Spain

43

Google Confidential and Proprietary

Testimonial_ IKEA

“The research showed us how by including Youtube into the media mix, we can take advantage of both massive and

targeted communication. That kind of tests really encourage us to be even more creative to develop effective

and efficient media planning strategies!”.

Miguel Angel Orbaneja_ IKEA Digital Media Manager

44

Google Confidential and Proprietary

Testimonial_ Johnson & Johnson

“The research truly put into value real potential of online video. Online media not only efficiently generated relevant extra reach, but also contributed to a better distribution of total campaign GRP´s allowing us to increase impact on those lightest TV viewers” Ignacio Entrena Media & Digital Manager Johnson & Johnson

45

Google Confidential and Proprietary

Testimonial_ BBVA

"The study proves the relevancy of including Youtube in ambitious media planning strategies, not only due to the fact that it impact exclusive segments of target that would be almost impossible to reach with TV, but also because it allows advertisers to be more cost efficient“

Carlos Pérez Beruete BBVA Director of Brand Strategy

46

47

thank you!