Embed Size (px)

Citation preview

Sri Lanka Transmission Plans Including ExistingTransmission System and Generation & Demand

Forecast Inclusive of Existing Demand/Generation Scenario

Dr. H.M. WijekoonChief Engineer

(Transmission Planning)Ceylon Electricity Board

Sri Lanka

2nd Task Force 2 Meeting On “Advancement ofTransmission Systems Interconnections”

Government of Sri LankaMinistry of Power and Energy

Public Utilities Commissionof

Sri LankaCEB GenerationLicence GL

Consumers

CEB Disribution

Small Power Producers

Independent Power Producers

Lanka Electricity Company PVT Ltd.DL5

CEB Disribution

CEB DisributionLicence DL 2

CEB Disribution

CEB TransmissionLicence TL

Licence DL 1

Licence DL 4

Licence DL 3

Licensing

Licensing

GOSL PolicyDirections

Government of Sri LankaMinistry of Power and Energy

Public Utilities Commissionof

Sri LankaCEB GenerationLicence GL

Consumers

CEB Disribution

Small Power Producers

Independent Power Producers

Lanka Electricity Company PVT Ltd.DL5

CEB Disribution

CEB DisributionLicence DL 2

CEB Disribution

CEB TransmissionLicence TL

Licence DL 1

Licence DL 4

Licence DL 3

Licensing

Licensing

GOSL PolicyDirections

Organization ofthe Power Sector

Sri Lankan EconomyDemographic and Economic Indicators of Sri Lanka

Electricity and Economy

Units 2006 2007 2008 2009 2010 2011 2012

Mid-Year Population Millions 19.89 20.01 20.22 20.45 20.65 20.87 20.32

Population Growth Rate % 1.1 1.1 1.0 1.1 1.0 1.0 n.a

GDP Real Growth Rate % 7.7 6.8 6.0 3.5 8.0 8.2 6.4

GDP /Capita (Market prices) US$ 1,421 1,634 2,014 2,057 2,400 2,836 2,923

Exchange Rate (Avg.) LKR/US$ 103.96 110.62 108.33 114.94 113.06 110.57 127.60

GDP Const 2002 Prices Mill LKR 2,090,564 2,232,656 2,365,501 2,449,214 2,645,542 2,863,854 3,047,277

Sri Lanka Economy and Electricity

Source: Annual Report 2012, Central Bank of Sri LankaElectricity and Economy

Forecast of GDP Growth Rate in Real Terms

Year 2012 2013 2014 2015GDP GrowthRate (%)

7.2 8.0 8.3 8.5

Source: Annual Report 2011, Central Bank of Sri Lanka

3

Electricity Data for 2012 Installed capacity - 3334 MW

Peak Demand - 2146 MW

Electricity Generated - 11800 GWh

Generation Mix - Hydro 28% Thermal 72%

Capacity Mix - Hydro 46% Thermal 54%

System losses - 11%

Load Factor - 62.8%

Access to Electricity - 94%

Elec. Consumption per Capita - 515 kWh

Avg. Cost per unit (at selling point) - 22.13 Rs/kWh

Avg. selling price - 15.56 Rs/kWh

Installed capacity - 3334 MW

Peak Demand - 2146 MW

Electricity Generated - 11800 GWh

Generation Mix - Hydro 28% Thermal 72%

Capacity Mix - Hydro 46% Thermal 54%

System losses - 11%

Load Factor - 62.8%

Access to Electricity - 94%

Elec. Consumption per Capita - 515 kWh

Avg. Cost per unit (at selling point) - 22.13 Rs/kWh

Avg. selling price - 15.56 Rs/kWh

EXISTING GENERATING SYSTEM

Plant NameCapacity

(MW)Expected Annual Avg.

Energy (GWh)Laxapana Complex

Canyon 60 160Wimalasurendra 50 112Old Laxapana 50 286New Laxapana 100 552Polpitiya 75 453Laxapana Total 335 1563

Mahaweli ComplexUpper Kotmale 150 409

Victoria 210 865

Committed plants for the study

• 35MW Broadlands HydropowerProject annual energy -126GWh

• 120 MW Uma Oya HydropowerProject annual energy - 231GWh

Hydro and Renewable

Victoria 210 865

Kotmale 201 498Randenigala 122 454Ukuwela 38 154Bowatenna 40 48Rantambe 49 239Mahaweli Total 810 2667

Other HydroSamanalawewa 120 344Kukule 70 300Small hydro 20Other Hydro Total 210 644

Wind plant 3

Existing Total 1355 4874

Committed plants for the study

• 35MW Broadlands HydropowerProject annual energy -126GWh

• 120 MW Uma Oya HydropowerProject annual energy - 231GWh

5

Thermal Plants

Plant Name

No of Units xName Plate

Capacity(MW)

No of Units xCapacity used

for Studies(MW)

AnnualMax.

Energy(GWh)

Puttalam Coal Power PlantPuttalam CPP-Phase I 1x300 1x275

Kelanitissa Power StationGas turbine (Old) 5 x 20 5 x 17 417

Committed plants for the study• Puttalam Coal Power Project Stage II

(Net 2x275MW)• 24MW Chunnakam Extension

power plant• 20MW Northern Power plant

Plant Retirements• 2019- 5x17 MW Kelanitissa Gas Turbines• 2019- 4x18 MW units at Sapugaskanda• 2023- 115 MW Kelanitissa Gas Turbine• 2023 -4x9 MW units at Sapugaskanda• 2025- 4x9 MW units at Sapugaskanda

EXISTING GENERATING SYSTEM

Gas turbine (Old) 5 x 20 5 x 17 417Gas turbine (New) 1 x 115 1 x 115 707Combined Cycle (JBIC) 1 x 165 1 x 165 1290Kelanitissa Total 380 365 2414

Sapugaskanda Power StationDiesel 4 x 20 4 x 18 472Diesel (Ext.) 8 x 10 8 x 9 504Sapugaskanda Total 160 144 976

Small Thermal PlantsChunnakam 1 x 8 - -Small Thermal Total 8 - -

Existing Total Thermal 848 784 3390

Plant Retirements• 2019- 5x17 MW Kelanitissa Gas Turbines• 2019- 4x18 MW units at Sapugaskanda• 2023- 115 MW Kelanitissa Gas Turbine• 2023 -4x9 MW units at Sapugaskanda• 2025- 4x9 MW units at Sapugaskanda

Recommended Plant Extensions by5 years up to year 2018• 22.5MW Lakdhanavi power plant• 20MW ACE Power Matara• 20MW ACE Power Horana

6

IPP Thermal PlantsEXISTING GENERATING SYSTEM

Plant NameCapacity

(MW)Capacity used

for Studies

Min . GuaranteedAnn. Energy

(GWh)Independent Power ProducersAsia Power LtdColombo Power (Pvt) LtdAES Kelanitissa (Pvt.) Ltd

Heladanavi (Pvt.) Ltd.ACE Power Embilipitiya Ltd

West Coast ( Pvt)Ltd.LakdhanaviACE Power MataraACE Power Horana

5164

163

100100

27022.524.824.8

4960

163

100100

27022.5

2020

300420

698697

156167167

Independent Power ProducersAsia Power LtdColombo Power (Pvt) LtdAES Kelanitissa (Pvt.) Ltd

Heladanavi (Pvt.) Ltd.ACE Power Embilipitiya Ltd

West Coast ( Pvt)Ltd.LakdhanaviACE Power MataraACE Power Horana

5164

163

100100

27022.524.824.8

4960

163

100100

27022.5

2020

300420

698697

156167167

Existing Total IPP 820.1 804.5 2605CommittedNorthern power 30 20 -Committed Total IPP 30 20

7Total Installed Capacity 3334 MW (Including Small Hydros and Wind)

Enhanced accessibility(2013)

Electrification Level inDecember 2013

60-80% 80-97%

<60%

>97%

Kurunegala

96 %

Moneragala

86%

Kilinochchi28%

Vavuniya

77 %

Trincomalee

88%

Polonnaruwa

88 %

Kegalle

96%

Batticoloa80%

Matale

95%Kandy

100 %

Nuwaraeliya

93%Ratnapura

89%Galle

100 %Hambantota

100%

Mullaithivu 25%

Anuradhapura

93 %

Badulla95%

Puttalam

95 %

Mannar87%

Ampara

95%

Matara

98 %

Kalutara

100%

Colombo100%

Gampaha100%

Jaffna 89 %

Electrification Level inDecember 2013

Enrich Life through Power

96%

60-80% 80-97%

<60%

>97%

Kurunegala

96 %

Moneragala

86%

Kilinochchi28%

Vavuniya

77 %

Trincomalee

88%

Polonnaruwa

88 %

Kegalle

96%

Batticoloa80%

Matale

95%Kandy

100 %

Nuwaraeliya

93%Ratnapura

89%Galle

100 %Hambantota

100%

Mullaithivu 25%

Anuradhapura

93 %

Badulla95%

Puttalam

95 %

Mannar87%

Ampara

95%

Matara

98 %

Kalutara

100%

Colombo100%

Gampaha100%

Jaffna 89 %

Hydro Capacity Variation During Last 3 Years

ELECTRICITY DEMAND FORECAST…

13

Sectorial Consumption of Electricity (2012)

Domestic Sectoro GDP Per Capitao Number of Domestic Consumer Accounts

ELECTRICITY DEMAND FORECAST

Methodology

• Econometric modelling has been adopted by CEB for theelectricity demand forecast.

• Sales figures of the past were analysed against followingindependent variables.

Domestic Sector

Industrial Sector

Commercial Sector

Other

o Number of Domestic Consumer Accounts

o Previous year sector electricity demand

o GDPo Previous year sector electricity demand

o GDPo Previous year sector electricity demand

o Time-trend analysis 14

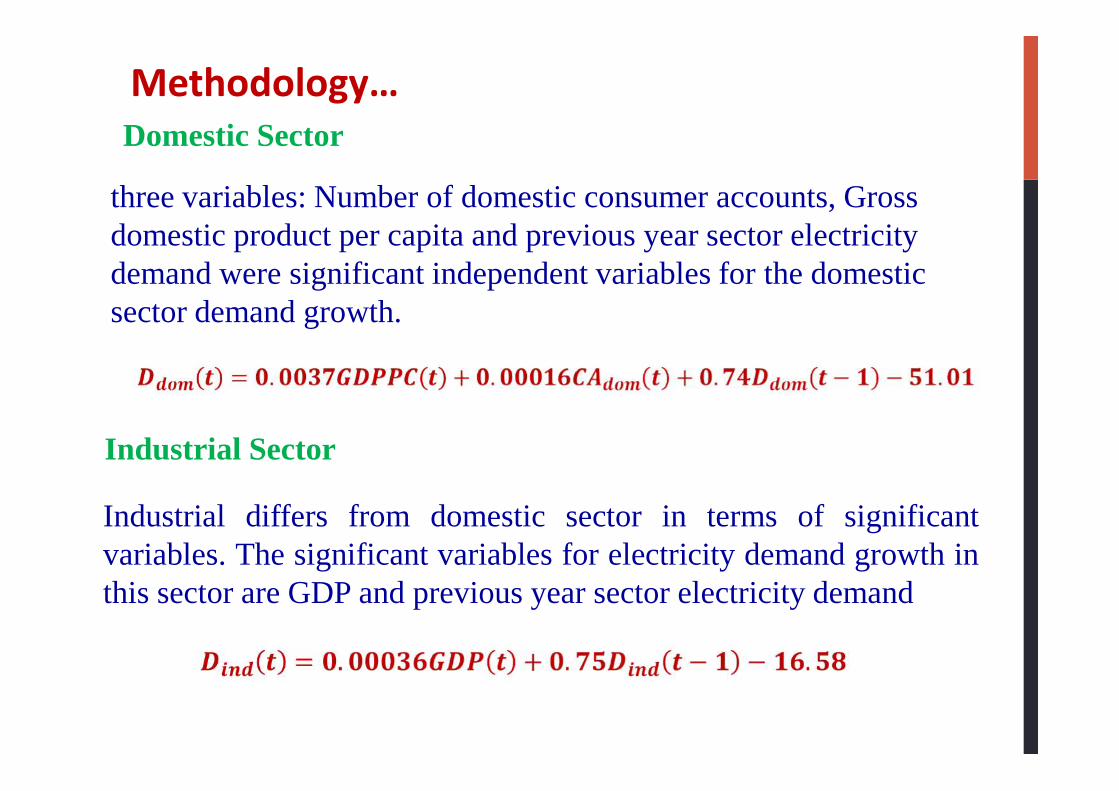

Methodology…Domestic Sector

three variables: Number of domestic consumer accounts, Grossdomestic product per capita and previous year sector electricitydemand were significant independent variables for the domesticsector demand growth.

Industrial Sector

Industrial differs from domestic sector in terms of significantvariables. The significant variables for electricity demand growth inthis sector are GDP and previous year sector electricity demand

Commercial (General Purpose) Sector

Commercial sector significant variables for electricity demandgrowth are GDP and previous year sector electricity demand, sameindustrial sector.

Other Sector

The two consumer categories: religious purpose and street lighting areconsidered in the ‘other sector’. Because of the diverse nature of theconsumers included in this category, this category was analysedwithout any links to other social or demographic variables. Hence, atime-trend analysis was performed to predict the demand in this sector

Other Sector

NATIONAL ELECTRICITY DEMAND FORECAST (2012-2032)Year Demand (GWh) Gross Losses (%) Generation (GWh) Peak Demand (MW)2013 11,104 11.6 12,566 2,4512014 12,072 11.6 13,502 2,6922015 12,834 11.6 14,509 2,8942016 13,618 11.5 15,388 3,0172017 14,420 11.4 16,270 3,1932018 15,240 11.3 17,171 3,3832019 16,075 11.1 18,087 3,5562020 16,937 11.0 19,030 3,7312021 17,830 10.9 20,010 3,9202021 17,830 10.9 20,010 3,9202022 18,754 10.8 21,023 4,1252023 19,713 10.7 22,072 4,2872024 20,707 10.6 23,159 4,4992025 21,737 10.5 24,284 4,7172026 22,813 10.4 25,458 4,9482027 23,932 10.3 26,677 5,1872028 25,101 10.2 27,949 5,3692029 26,318 10.1 29,273 5,6252030 27,581 10.0 30,645 5,8932031 28,899 8.0 32,079 6,1712032 30,258 9.8 33,555 6,461

LONG TERM TRANSMISSIONDEVELOPMENT PLAN

2013 - 2022

CEYLON ELECTRICITY BOARDSRI LANKA

PRESENT TRANSMISSION NETWORK -2013

Transmission voltage levels 220 kV 132 kV

Transmission Lines/Cables – 2348 km 220 kV 502 km

132 kV 1846 km

o OH 1796 kmo UG 50 km

Grid Substations No | MVA 132/33 kV 48 3045 220/132/33 kV 5 2100 220/132 kV 2 405 220/33 kV 1 70 132/11kV 5 369

Transmission voltage levels 220 kV 132 kV

Transmission Lines/Cables – 2348 km 220 kV 502 km

132 kV 1846 km

o OH 1796 kmo UG 50 km

Grid Substations No | MVA 132/33 kV 48 3045 220/132/33 kV 5 2100 220/132 kV 2 405 220/33 kV 1 70 132/11kV 5 369

2013 SriLankan

TransmissionSystem

Transmission Planning Procedure

Preparation of Grid Demand Forecast

National Power Demand is allocated among theexisting grid substations considering the trends ofload variation, spot loads and distribution networkarrangements

Overloaded grid substations are identified afterconsidering possible load transferred to adjacent gridsubstations

Augmentations and construction of new gridsubstations are established

National Power Demand is allocated among theexisting grid substations considering the trends ofload variation, spot loads and distribution networkarrangements

Overloaded grid substations are identified afterconsidering possible load transferred to adjacent gridsubstations

Augmentations and construction of new gridsubstations are established

This process is repeated until the grid substation demandforecast meet the planning criteria

TransmissionPlanning

Procedure

Generation Expansion Plan

YEARRENEWABLEADDITIONS

THERMALADDITIONS

THERMALRETIREMENTS

2013 - -4x5 MW ACE Power Matara4x5 MW ACE Power Horana4x5.63 MW Lakdanavi

2014 -4x5 MW Northern Power3x8 MW Chunnakum Extension**1x300 MW Puttalam Coal (Stage II)

2015 -

1x300 MW Puttalam Coal (StageIII)3x75 MW Gas Turbine

6x16.6 MW Heladanavi Puttalam14x7.11 MW ACE PowerEmbilipitiya4x15 MW Colombo Power

TransmissionPlanning

Procedure

2015 -

1x300 MW Puttalam Coal (StageIII)3x75 MW Gas Turbine

6x16.6 MW Heladanavi Puttalam14x7.11 MW ACE PowerEmbilipitiya4x15 MW Colombo Power

201635 MW Broadlands120 MW Uma Oya

- -

2017 - 1x105 MW Gas Turbine -

201827 MW Moragolla

Plant2x250 MW Trincomalee Coal Powerplant

4x5 MW Northern Power8x6.13 MW Asia Power

2019 - 2x300 MW Coal plant5x17 MW Kelanitissa GasTurbines4x18 MW Sapugaskanda diesel

2020 - - -2021 - 1x300 MW Coal plant -2022 49 MW Gin Ganga 1x300 MW Coal plant -

Evaluation of Planning CriteriaEnsures quality and reliability of supplyunder normal operating conditions as wellas under single contingency conditions1) Voltage Criteria2) Thermal Criteria3) Security Criteria4) Stability Criteria5) Short Circuit Criteria1) Voltage Criteria2) Thermal Criteria3) Security Criteria4) Stability Criteria5) Short Circuit Criteria

Scenarios investigated underNormal and Single Contingency

Conditions

GenerationScenario

Load Scenario

DayPeak

NightPeak

Minimum

GenerationScenario Day

PeakNightPeak

Minimum

Hydro Max. HMDP HMNP

OP

Thermal Max. TMDP TMNP

2013

Project Proposals by Study Year 2013-2022

2014

2015 2016

2017 20192022

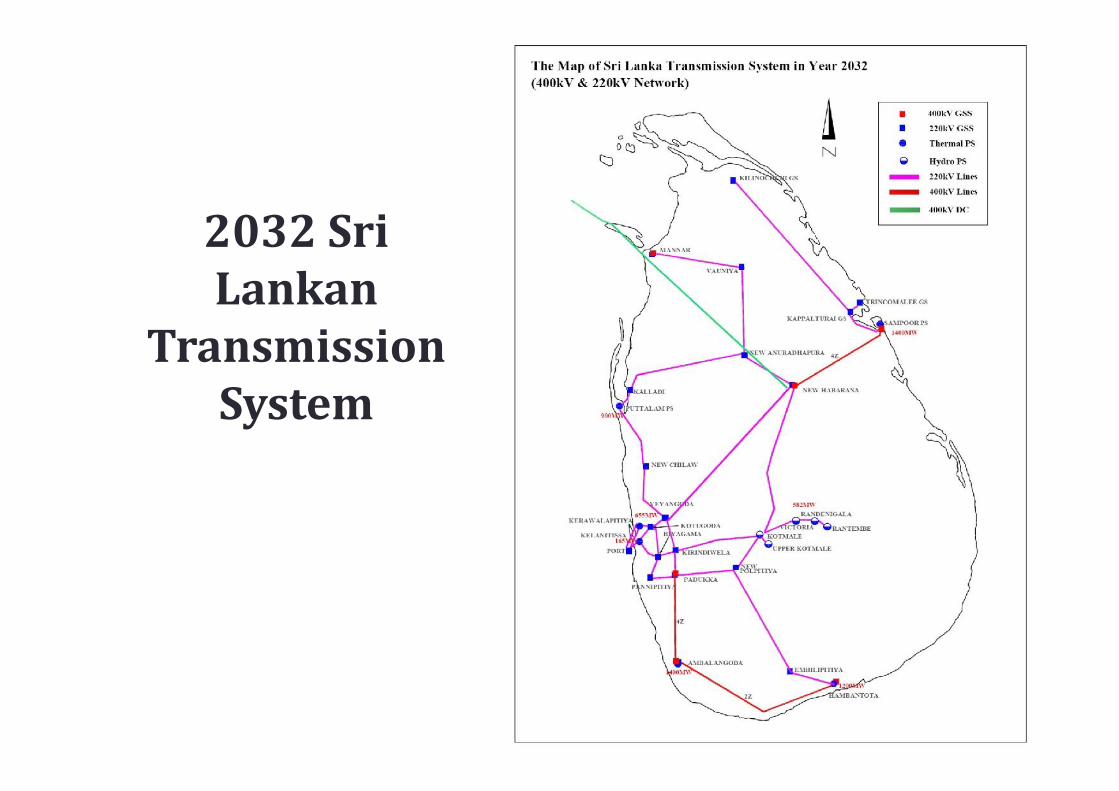

2032 SriLankan

TransmissionSystem

2032 SriLankan

TransmissionSystem

Total investment requirement from year 2013 to 2022

No. Name of Project Lender Cost(mUS$)

1 Clean Energy & Access Improvement Project ADB 1352 Augmentation of GS for Absorption of

Renewable EnergyGOSL 8

3 Augmentation of GS for Absorption ofRenewable Energy

ADB 130

4 Installation of Rantambe Inter- bus transformer GOSL/CEB 31

Projects Under Implementation

4 Installation of Rantambe Inter- bus transformer GOSL/CEB 315 Clean Energy & Network Efficiency

Improvement ProjectADB 130

6 Habarana – Veyangoda 220kV TransmissionProject

JICA 105

7 Greater Colombo Transmission & DistributionLoss Reduaction Project

JICA 205

Total (mUS$) 744

No. Name of Project Lender Cost(mUS$)

1 Construction of GS for RE Absorption FDA 302 Green Power Development and Energy

Efficiency Improvement ProgrammeADB 180

3 45th Yen Loan Package JICA 150Total (mUS$) 360

Projects Securing Funds

India - Sri Lanka Electricity GridInterconnection

Background Pre-feasibility study conducted with the assistance of USAID in

2002 by Nexant Inc.

Review of the Pre-feasibility study with assistance of USAID in2006 by Nexant/ Power Grid Corporation of India

Bilateral discussions by Secretary , Ministry of Power and EnergySri Lanka and Secretary Ministry of Power, India in Dec 2006.

Cabinet of Ministers approved in principle in Dec 2006, to studythe feasibility of power interconnection and to appoint aSteering Committee Co- Chaired by Secretaries of PowerMinistries and to appoint a Task Force for technical, commercial,regulatory and legal aspects.

36

Pre-feasibility study conducted with the assistance of USAID in2002 by Nexant Inc.

Review of the Pre-feasibility study with assistance of USAID in2006 by Nexant/ Power Grid Corporation of India

Bilateral discussions by Secretary , Ministry of Power and EnergySri Lanka and Secretary Ministry of Power, India in Dec 2006.

Cabinet of Ministers approved in principle in Dec 2006, to studythe feasibility of power interconnection and to appoint aSteering Committee Co- Chaired by Secretaries of PowerMinistries and to appoint a Task Force for technical, commercial,regulatory and legal aspects.

Background Conts. A MOU on Feasibility Study for India- Sri Lanka

Electricity Grid Interconnection was signed amongGOSL, GOI, CEB and Power Grid Corporation of IndiaLimited (PGCIL) on 9th June 2010.

Executing Agencies; CEB and PGCIL are jointly carryingout the feasibility study

37

A MOU on Feasibility Study for India- Sri LankaElectricity Grid Interconnection was signed amongGOSL, GOI, CEB and Power Grid Corporation of IndiaLimited (PGCIL) on 9th June 2010.

Executing Agencies; CEB and PGCIL are jointly carryingout the feasibility study

Benefits and Opportunities forSri Lanka

• Opportunity to enter into India Power Exchange forenergy trading

• Access to electricity from cheaper sources of powergeneration in the South Asia Region

• Reduction in operational cost through better resourcemanagement

• Meeting growing power demand with importedpower

• Improved load profile - valley filling• Improved system reliability and security

17 June 2014 38

• Opportunity to enter into India Power Exchange forenergy trading

• Access to electricity from cheaper sources of powergeneration in the South Asia Region

• Reduction in operational cost through better resourcemanagement

• Meeting growing power demand with importedpower

• Improved load profile - valley filling• Improved system reliability and security

Line RouteMaduari Panaikulam

130km Thiruketis-waram

120kmA’Pura

110kmsubmarineoverhead overhead

High voltage direct current (HVDC), operating at ±400 kV Total interconnection capacity will be 1000 MW

Potential for Power Exchange Contracts• Short term contracts

– Monthly average prices reported in Indian short term market are inthe range of 6.68 to 9.52 UScts/kWh (capacity + energy)

– monthly average purchase prices forecast for Sri Lanka are in therange of 6.50 to 13.46 UScts/kWh (energy only)

– During peak hours, Sri Lanka can make use of the lower cost Indianshort term market

– During off peak, the excess coal based generation in Sri Lankacould be sold to the Indian short term market

• Long term contracts– Owing to economies of scale, Sri Lanka signing up with an Indian

UMPP could be cheaper than building own plants– Similarly, if Sri Lanka can build an UMPP, it can also serve the

Indian base load, owing to the persistent shortfall in India

• Short term contracts– Monthly average prices reported in Indian short term market are in

the range of 6.68 to 9.52 UScts/kWh (capacity + energy)– monthly average purchase prices forecast for Sri Lanka are in the

range of 6.50 to 13.46 UScts/kWh (energy only)– During peak hours, Sri Lanka can make use of the lower cost Indian

short term market– During off peak, the excess coal based generation in Sri Lanka

could be sold to the Indian short term market

• Long term contracts– Owing to economies of scale, Sri Lanka signing up with an Indian

UMPP could be cheaper than building own plants– Similarly, if Sri Lanka can build an UMPP, it can also serve the

Indian base load, owing to the persistent shortfall in India

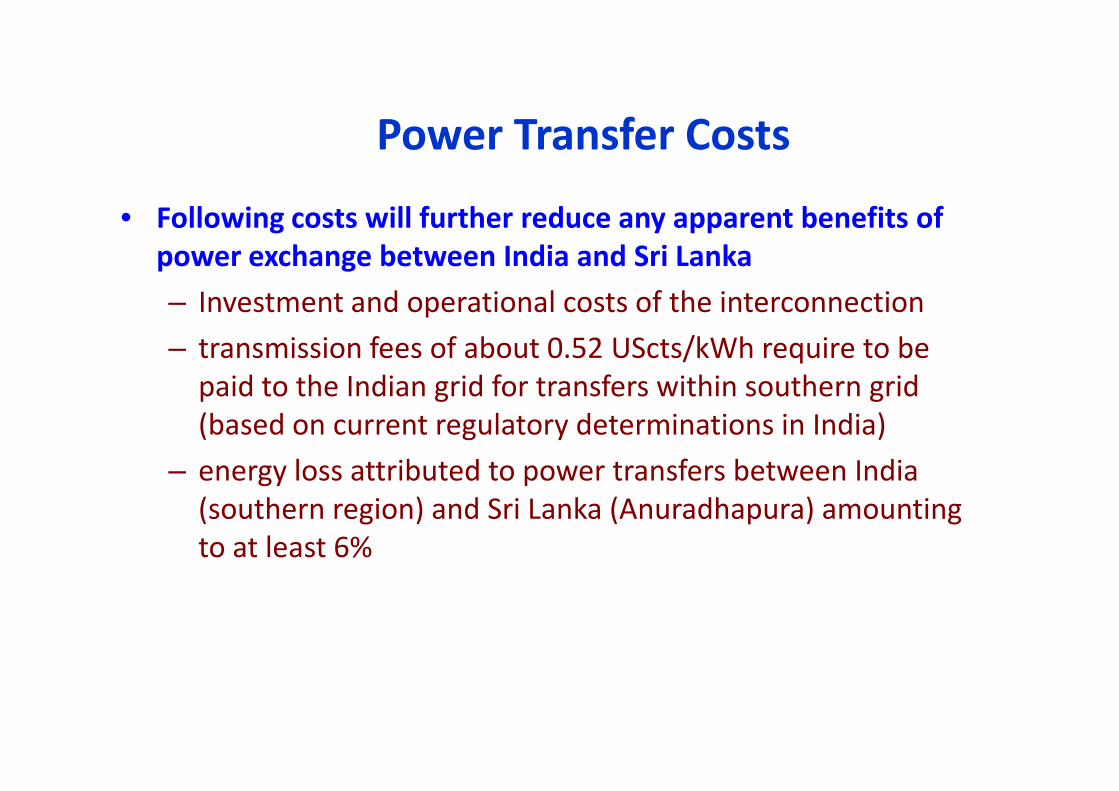

Power Transfer Costs

• Following costs will further reduce any apparent benefits ofpower exchange between India and Sri Lanka– Investment and operational costs of the interconnection– transmission fees of about 0.52 UScts/kWh require to be

paid to the Indian grid for transfers within southern grid(based on current regulatory determinations in India)

– energy loss attributed to power transfers between India(southern region) and Sri Lanka (Anuradhapura) amountingto at least 6%

• Following costs will further reduce any apparent benefits ofpower exchange between India and Sri Lanka– Investment and operational costs of the interconnection– transmission fees of about 0.52 UScts/kWh require to be

paid to the Indian grid for transfers within southern grid(based on current regulatory determinations in India)

– energy loss attributed to power transfers between India(southern region) and Sri Lanka (Anuradhapura) amountingto at least 6%

Legal and Regulatory Issues

CEB needs to be empowered to enter into cross-border power transfers The Transmission and Bulk Supply license held by CEB

is required to be amended Dispute resolution in the Sri Lanka Electricity Act

requires to be further strengthened CEB Act has to be amended to enable the functions of

trader or broker, as relevant

CEB needs to be empowered to enter into cross-border power transfers The Transmission and Bulk Supply license held by CEB

is required to be amended Dispute resolution in the Sri Lanka Electricity Act

requires to be further strengthened CEB Act has to be amended to enable the functions of

trader or broker, as relevant

To achieve project viability The project must be structured as a 1x500 MW monopolar

interconnection with no specific assets or commitments now toraise the capacity to 1000 MW If the project costs are further reduced by reconsidering the

routing options, the 1x500 MW monopolar option has thepotential to be viable Target project cost for a POWERGRID-CEB joint venture to be

profitable is 372.4 MUSD (excluding customs duty and taxes),which at present is estimated to be 554 MUSD Both Sri Lanka and India be allowed participation in the wholesale

market in each others’ country, with full options and freedom toparticipate in the short-term, day-ahead and unscheduledinterchanges market Sri Lankan power system shall relax its maximum load share

condition and allow the interconnection to supply at the optimalcapacity level

The project must be structured as a 1x500 MW monopolarinterconnection with no specific assets or commitments now toraise the capacity to 1000 MW If the project costs are further reduced by reconsidering the

routing options, the 1x500 MW monopolar option has thepotential to be viable Target project cost for a POWERGRID-CEB joint venture to be

profitable is 372.4 MUSD (excluding customs duty and taxes),which at present is estimated to be 554 MUSD Both Sri Lanka and India be allowed participation in the wholesale

market in each others’ country, with full options and freedom toparticipate in the short-term, day-ahead and unscheduledinterchanges market Sri Lankan power system shall relax its maximum load share

condition and allow the interconnection to supply at the optimalcapacity level

Revised Electricity Grid Interconnection

190 km

50km

Madurai

Thalai Mannar50km

140 km

NewAnuradhapura

Thalai Mannar

Thank YouDr. H.M. Wijekoon

Ceylon Electricity [email protected]

Ceylon Electricity Board 45

Thank YouDr. H.M. Wijekoon

Ceylon Electricity [email protected]

Voltage Criteria

Bus bar

voltage

Allowable voltage variation (%)

Normal operatingcondition

Single contingencycondition

Bus bar

voltageNormal operating

conditionSingle contingency

condition

220 kV 10% 10%

132 kV 10% 10%

Thermal Criteria

Loading of any element should not exceed theirrated thermal loading values for steady statecondition

Loading of any element should not exceed theirrated thermal loading values for steady statecondition

Security Criteria

After outage of any element, the system shouldbe able to meet the distribution demandmaintaining the specified voltage levels andremaining circuits should not exceed theiremergency ratings.

After outage of any element, the system shouldbe able to meet the distribution demandmaintaining the specified voltage levels andremaining circuits should not exceed theiremergency ratings.

Stability Criteria

Ensures the system stability during andafter disturbances in case of

Three Phase fault at any overhead lineterminal cleared by successful andunsuccessful re-closing

Loss of any generation unit

Load rejection

Ensures the system stability during andafter disturbances in case of

Three Phase fault at any overhead lineterminal cleared by successful andunsuccessful re-closing

Loss of any generation unit

Load rejection

Short Circuit Criteria

BusbarVoltage System

Maximum 3Phase Fault

level (kA)

132kV andabove

Over head 40.0

UG Cable 40.0132kV and

above UG Cable 40.0

33kVOver head 25.0

UG Cable 25.0

11kV UG Cable 25.0