Embed Size (px)

Citation preview

Beacon Securities Ltd.| 66 Wellington Street West, Suite 4050, Toronto, Ontario, M5K 1H1 |416.643.3830|www.beaconsecurities.ca

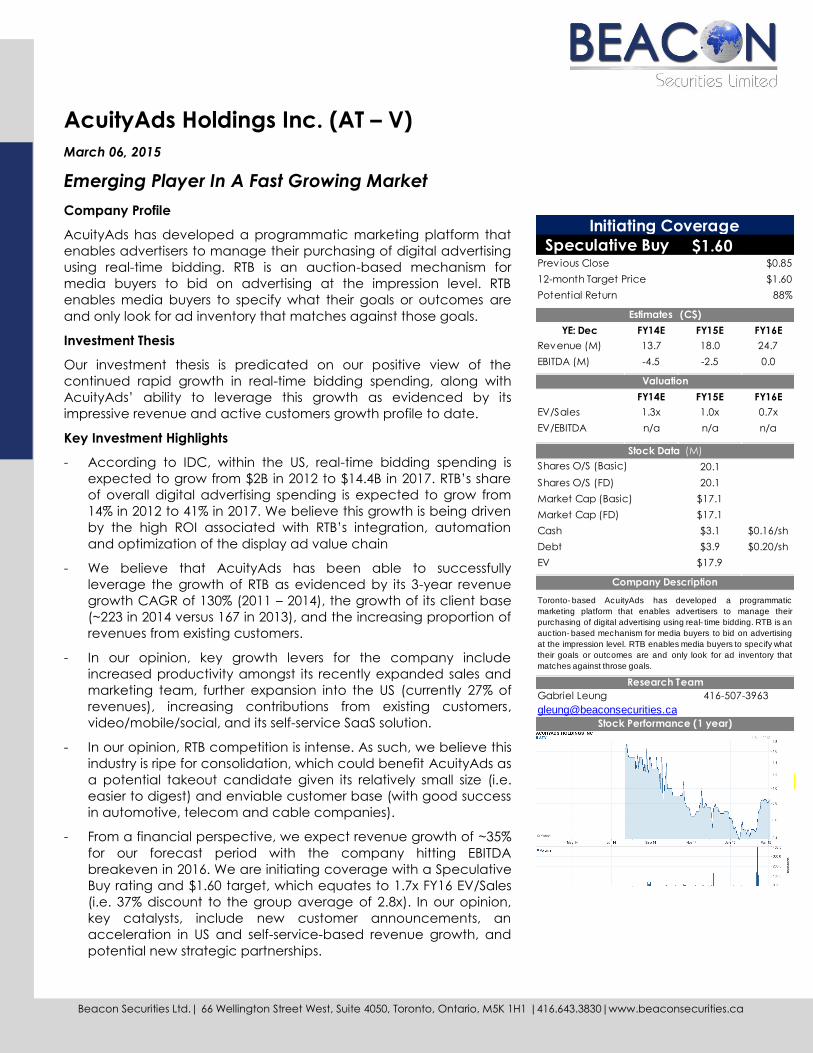

AcuityAds Holdings Inc. (AT – V)

March 06, 2015

Emerging Player In A Fast Growing Market

Company Profile

AcuityAds has developed a programmatic marketing platform that

enables advertisers to manage their purchasing of digital advertising

using real-time bidding. RTB is an auction-based mechanism for

media buyers to bid on advertising at the impression level. RTB

enables media buyers to specify what their goals or outcomes are

and only look for ad inventory that matches against those goals.

Investment Thesis

Our investment thesis is predicated on our positive view of the

continued rapid growth in real-time bidding spending, along with

AcuityAds’ ability to leverage this growth as evidenced by its

impressive revenue and active customers growth profile to date.

Key Investment Highlights

- According to IDC, within the US, real-time bidding spending is

expected to grow from $2B in 2012 to $14.4B in 2017. RTB’s share

of overall digital advertising spending is expected to grow from

14% in 2012 to 41% in 2017. We believe this growth is being driven

by the high ROI associated with RTB’s integration, automation

and optimization of the display ad value chain

- We believe that AcuityAds has been able to successfully

leverage the growth of RTB as evidenced by its 3-year revenue

growth CAGR of 130% (2011 – 2014), the growth of its client base

(~223 in 2014 versus 167 in 2013), and the increasing proportion of

revenues from existing customers.

- In our opinion, key growth levers for the company include

increased productivity amongst its recently expanded sales and

marketing team, further expansion into the US (currently 27% of

revenues), increasing contributions from existing customers,

video/mobile/social, and its self-service SaaS solution.

- In our opinion, RTB competition is intense. As such, we believe this

industry is ripe for consolidation, which could benefit AcuityAds as

a potential takeout candidate given its relatively small size (i.e.

easier to digest) and enviable customer base (with good success

in automotive, telecom and cable companies).

- From a financial perspective, we expect revenue growth of ~35%

for our forecast period with the company hitting EBITDA

breakeven in 2016. We are initiating coverage with a Speculative

Buy rating and $1.60 target, which equates to 1.7x FY16 EV/Sales

(i.e. 37% discount to the group average of 2.8x). In our opinion,

key catalysts, include new customer announcements, an

acceleration in US and self-service-based revenue growth, and

potential new strategic partnerships.

$1.60$0.85

$1.60

88%

YE: Dec FY14E FY15E FY16E

Revenue (M) 13.7 18.0 24.7

EBITDA (M) -4.5 -2.5 0.0

FY14E FY15E FY16E

EV/Sales 1.3x 1.0x 0.7x

EV/EBITDA n/a n/a n/a

20.1

Shares O/S (FD) 20.1

Market Cap (Basic) $17.1

Market Cap (FD) $17.1

Cash $3.1 $0.16/sh

Debt $3.9 $0.20/sh

EV $17.9

Initiating Coverage

Previous Close

12-month Target Price

Potential Return

Estimates (C$)

Valuation

Company Description

Toronto- based AcuityAds has developed a programmatic

marketing platform that enables advertisers to manage their

purchasing of digital advertising using real- time bidding. RTB is an

auction- based mechanism for media buyers to bid on advertising

at the impression level. RTB enables media buyers to specify what

their goals or outcomes are and only look for ad inventory that

matches against throse goals.

Research Team

Speculative Buy

Stock Performance (1 year)

Stock Data (M)

Shares O/S (Basic)

Gabriel Leung 416-507-3963

Who They Are and What Do They Do?

• Toronto-based AcuityAds has developed a programmatic marketing platform that enables

advertisers to manage their purchasing of digital advertising using real-time bidding (“RTB”).

• RTB is an auction-based mechanism for media buyers to bid on advertising at the impression

level, as the ad impression takes place. RTB enables a media buyer to specify exactly what their

goals or outcomes are and look only for ad inventory that matches against those goals.

• By contrast, with direct buys, advertisers essentially buy impressions in bulk.

• The company was founded in 2011 and went public via an RTO with Wildlaw Capital CPC 2 in

July 2014. The company raised gross proceeds of $5.75M at $1.59/sh issuing 3.6M shares from

treasury.

• The company has offices in Canada, the US and its customers include both large Fortune 500

enterprise and small-to-medium sized businesses. The company currently has ~60 employees,

including 20 in sales.

1Gabriel Leung, 416-507-3963

Understanding The Programmatic RTB Industry

• What does “programmatic” mean?

– The term “programmatic” is the umbrella term for automated buying and selling of media.

• What is real-time bidding?

– RTB is a subset of programmatic and is an auction-based mechanism for media buyers to bid on

advertising at the impression level as the ad impression takes place.

• Who are the key players in RTB?

– Demand Side Platforms (e.g. AcuityAds): DSPs enable buyers (i.e. advertisers) to connect directly to

multiple sources of inventory supply and provide such benefits as workflow simplification, integrated

reporting, algorithmic buying optimization and the ability to make impression-level bids.

– Ad Exchanges: Powered marketplaces where ad networks, publishers, advertisers and other sources of

supply and demand meet to buy and sell media in continuous real-time auctions. Examples include

Google Ad Exchange, Microsoft Ad Exchange, AppNexus, etc.

– The Publisher: Provides the source of ad inventory (i.e. the digital spaces in which ads are served). Some

publishers may use Supply Side Platforms, or SSPs, to help better manage and sell their inventory.

2Gabriel Leung, 416-507-3963

How Does RTB Work?

At its most basic form, the RTB process unfolds like this:

• The publisher provides its inventory to an Ad Exchange, who is responsible for holding an auction,during which the DSPs, on behalf of the advertisers, will place a bid on each impression.

• The value of the bid is based on the value of that impression, as determined by the advertiser’sparameters with the DSP. (e.g. consumer profile #, demographics, consumer location, consumerinterests, page content, etc). The bidding process ensures that each impression is sold at the maximumprice, as dictated by real time market demand.

• RTB (for desktop display) leverages cookies, which are information that a website saves to yourcomputer using your web browser. A cookie allows sites to record your browsing activities – like whatpages and content you’ve looked at, when you visited, what you searched for, and whether you clickedon an ad. Data collected by cookies can be combined to create a profile of your online activities.Within mobile advertising, device identities such as indentifierForAdvertising (“IDFA”) for iOS devicesand Advertising ID for Android devices are used.

• Once the bidding is completed, the winner is chosen and the ad is served on the publisher’s website.

To summarize, the advertiser works with a DSP, which allows the advertiser to bid (in real-time) amongstbillions of daily impressions on ad exchanges. Based on a multitude of variables, bids are made forimpressions that have the highest probability of generating a desired action (e.g. signing up for moredetails, making a purchase, accessing a micro-site).

3Gabriel Leung, 416-507-3963

Where Does AcuityAds Fit In?

4Gabriel Leung, 416-507-3963

AcuityAds’ demand side platform enables advertisers to manage their purchasing of digitaladvertising in real-time using real-time bidding (“RTB”). The company purchases impressions foradvertisers through publishers, ad networks and exchanges. The company’s technology platformbenefits advertisers by enabling them to manage their bid amounts, meet specific performancemetrics and achieve consumer targeting goals. Advertisers benefit from AcuityAds algorithms,which help to improve efficiency and they can also optimize their campaigns based on hundreds ofreal-time data metrics (i.e. analytics).

AcuityAds generates revenues by using its programmatic marketing platform to deliver digitaladvertisements to consumers across online display, video, social and mobile channels.

The company offers both:

- Managed services where it provides complete execution of a digital advertising campaign foradvertising agencies and/or brands, and;

- Self-service technology where advertisers can use AcuityAds’ programmatic marketing platformto create and manage their own digital advertising campaigns and collect data and analysis (i.e.software-as-a-service platform).

The Ecosystem

5Gabriel Leung, 416-507-3963

Source: Company filings

How Programmatic Ad Buying Works

6Gabriel Leung, 416-507-3963

Source: Company filings

Automatic transaction between buyer and selling in <50 milliseconds

AcuityAds’ Competitive Advantages

7Gabriel Leung, 416-507-3963

Source: Company filings

Key Investment Highlights

8Gabriel Leung, 416-507-3963

• Growing Market Opportunity

• High ROI to Drive Adoption

• Impressive Traction To Date

• Potential Takeout Down the Road

Growing Market Opportunity

9Gabriel Leung, 416-507-3963

• According to research firm IDC, worldwide real-time bidding-based spending will grow from

$2.7B in 2012 to $20.8B in 2017.

• RTB’s share of total combined online and mobile display advertising spending will grow from 8%

to 28% during the same time.

• The US is expected to be the most advanced market. RTB spending is expected to grow from

$2B in 2012 to $14.4B in 2017.

• Within the US, the market share of RTB-based spending of all display ad spending, including

online and mobile display, will almost triple from 14% in 2012 to 41% in 2017.

• Mobile and video advertising are expected to be fast growing sub-sectors with revenue

contributions here growing from $243M in 2013 to $4.7B by 2017 within the US.

Growing Market Opportunity (cont’d)

10Gabriel Leung, 416-507-3963

US Real-Time Bidding ("RTB") Spending Forecast

Source: IDC

1,997

3,137

4,669

6,875

10,056

14,405

87%

57%

49%47%

46%

43%

30%

40%

50%

60%

70%

80%

90%

100%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2012 2013 2014 2015 2016 2017

RTB Spending Growth Y/Y (RHS)

($00

0)

Growing Market Opportunity (cont’d)

11Gabriel Leung, 416-507-3963

US Real-Time Bidding Spending Via Mobile And Online Video

Source: IDC

243

861

1,875

3,183

4,665

8%

18%

27%

32% 32%

0%

5%

10%

15%

20%

25%

30%

35%

0

1,000

2,000

3,000

4,000

5,000

6,000

2013 2014 2015 2016 2017

Mobile + Video RTB Spending % Of Total RTB Spending (RHS)

($00

0)

High ROI Helping To Drive Adoption

• By automating, integrating and optimizing the way display advertising is being traded and

served, we believe AcuityAd’s RTB programmatic platform allows publishers, advertisers and ad

agencies to improve their overall ROI, which is helping to accelerate adoption.

• To highlight the benefits associated with deploying AcuityAds, we have included case studies

involving Toyota and A&W.

• Toyota wanted to generate awareness of its upcoming sales event and increase traffic to its

showrooms through multimedia (online display, video, mobile and social media). By leveraging

AcuityAds’ programmatic platform, Toyota found:

– Video completion rates were extremely high at 90% (industry stands is 76.95%)

– Viewability reached a weekly high of 63.6% compared to the industry average of 31%.

– 0.00% of ads were delivered to non-human traffic, while the comScore average is 0.05%.

• Acuity helped Toyota achieve a 7.9% brand lift by the end of the campaign.

.

12Gabriel Leung, 416-507-3963

High ROI Helping To Drive Adoption

• Meanwhile, A&W was looking to educate consumers about its “A&W Pure Beef Guarantee”.

However, A&W was unsure as to whether programmatic buying could be effective in

communicating this branding message through digital media.

• AcuityAds elected to use comScore’s Validated Campaign Essentials (vCE) product on this

campaign. The purpose was to validate that the ads served through the Acuity Programmatic

Marketing Platform were delivered in-view, in the right geography, in a brand safe environment

and absent of non-human traffic. In addition, a Brand Survey Lift Pulse (BSL Pulse) study was

conducted to measure the lift in awareness attributed to the online campaign.

• Based on the vCE, Acuity performed strongly on several key measures:

– 99.8% of the impressions were delivered within the specified geographic area (comScore average:

97.8%);

– Only 0.01% of all impressions were served to fraudulent or non-human traffic. This is 5x less than

comScore’s average of 0.05%;

– 0.00% of ads were delivered in unsafe Brand environments (comScore average: 5.29%).

• According to comScore, this campaign saw 85% more lift than the average campaign

13Gabriel Leung, 416-507-3963

Impressive Traction To Date

• In our opinion, given the early stage of the company, the best way to measure its success to

date is via revenue and client growth. As highlighted in the accompanying page, 2014 revenues

(preliminary results have been released) increased 35% to $13.7M. We also understand that

active clients increased to 223 from 167 last year.

• Just as impressive, we would note that growth from existing client is running at ~68% of

revenues, which we believe highlights the high ROI and strong service delivered by the

AcuityAds team (happy customers mean repeat customers).

• Another key point is that AcuityAd’s platform generates data, which can ultimately be used to

improve the efficiency of future campaigns and could act as a competitive differentiator. For

example, based on the outcome of a new car campaign, the company can determine what the

best parameters they should use for future campaigns (i.e. the platform gets smarter over time).

• As it relates to the company’s US business, although it was only 27% of last quarter (i.e. Q3)

revenues, it was up ~240% y/y and, we believe, could be an important near-term growth driver.

Likewise, we would note that the company’s self-service SaaS recurring revenue stream has

grown to $484k in Q3 2014 from $18k in the same period last year.

14Gabriel Leung, 416-507-3963

Impressive Traction To Date (cont’d)

15Gabriel Leung, 416-507-3963

AcuityAds: Active Customer Analysis

Source: Company filings

26

102

167

223

0

50

100

150

200

250

2011 2012 2013 TTM

AcuityAds: Revenue Growth Analysis

Source: Company filings

1.1

5.1

10.2

13.7

18.0

24.7

0

5

10

15

20

25

30

2011 2012 2103 2014e 2015e 2106e

($M

)

Potential Takeout Down The Road

16Gabriel Leung, 416-507-3963

• As is the case with many high growth sectors, particularly within adtech, we believe the market

for programmatic RTB solutions is very competitive, including several vendors such as

RocketFuel (FUEL – Q, NR), MediaMath (private), Chango (private), and advertising agency

desks, amongst others.

• Over time, we believe the high level of competition could lead to gross margin pressures, but

also a potential acceleration in M&A activity.

• Given AcuityAds’ relatively small size, yet enviable customer base and success to date, we

believe the company could find itself a potential takeout target for a larger competitor, agency

trading desk, or direct advertiser looking to acquire AcuityAds’ technology platform, strong

Canadian customer portfolio and domain/industry expertise (notably in automotive and

cable/telecom based on our conversations with customers).

Financial Analysis

17

• AcuityAds generates revenues from two sources: managed services and self-service

technology. With managed services, AcuityAds provides complete execution of a digital

advertising campaign. Revenues are recognized on a gross advertising spending basis. The

associated cost of good is the cost of media buying. We believe gross margins are in the ~50%

range here. Managed services contracts are short-term in nature, with a terms of 30 – 90 days.

• Self-service enable advertisers to use AcuityAds’ programmatic marketing platform to create

and manage their own digital advertising campaigns and collect data and analytics (i.e. think

software-as-a-service type revenues). Revenues are likewise recognized on a grossed up basis,

although gross margins are lower than managed services (we estimate ~35%). Contract terms

are also one year or longer, which provides better revenue visibility.

• The company sells primarily through its direct sales force, which consists of 20 reps.

• The company’s balance sheet currently stands at $3.1M, against $3.9M in debt (due January

2016 at a cost of debt of 17%). The company has tax loss carry-forwards of ~$7M.

• For the 9-months ended Sept. 2014, ~53% of revenues were derived from top 10 customers.

Gabriel Leung, 416-507-3963

Growth Assumptions

• We assume that the company grows revenues annually in the ~35% range for our forecast

period. We’ve assumed managed services growth of ~25% and self-service of ~80%.

• We’ve also modeled gross margins of ~47%, which is down from the 50% range in 2014 due to

the growing proportion of contributions from self-service, which carries a lower margin profile,

but longer contract terms.

• We are forecasting the company to cut its EBITDA loss by half in 2015 (versus 2014) thanks

partially to cost optimization activities from earlier this year. We also expected the company to

breakeven by 2016 due to revenue scaling higher.

• Based on the existing cash balance and our forecasted EBITDA burn, we anticipate the company

will likely require an equity financing in 2015.

• For the purposes of modeling, we have assumed a ~$3M raise in mid-2015 (at a 15% discount

to current prices). We have not factored contributions from acquisitions, although we believe the

company could be targeting companies that add scale or additional products to its technology

stack.

18Gabriel Leung, 416-507-3963

Initiating Coverage with A Speculative Buy Rating

• As highlighted by the list of comparable adtech-related companies in the next page, we derive

an average EV/Sales (FY+1) multiple of 2.8x against a 2-year revenue CAGR of 22%.

• By contrast, AcuityAds is currently trading at 0.7x EV/Sales against a 2-year revenue CAGR of

34%.

• In our opinion, AcuityAds’ valuation could start to expand as it moves closer to EBITDA

profitability.

• Applying a 1.7x EV/Sales multiple to our 2016E forecast for AcuityAds (i.e. 37% discount to the

group to reflect its smaller scale and EBITDA loss position), we derive a $1.60 target price. For

the purposes of our enterprise value calculation, we’ve applied our 2016 ending net cash

balance of $60k and $3.9M in debt, and shares outstanding of 24.4M (which includes a $3M

equity financing in mid-2015 at $0.70/sh).

• Given the ~86% potential rate of return, we are initiating coverage with a Speculative Buy rating.

19Gabriel Leung, 416-507-3963

Comparable Company Valuation Analysis

20Gabriel Leung, 416-507-3963

Market 2-Year

Ticker S/O (M) Cap ($M) Currency FY - 1 FY1 FY + 1 Sales CAGR FY - 1 FY1 FY + 1 FY -1 FY1 FY + 1

Comps

Google GOOG-US 341 195,995 USD 2.6 x 2.3 x 1.9 x 16% 5.3 x 4.6 x 4.0 x 49% 48% 48%

Facebook FB-US 2,236 181,613 USD 13.7 x 10.0 x 7.6 x 35% 20.8 x 16.4 x 12.5 x 66% 61% 61%

Yahoo! YHOO-US 936 41,339 USD 7.9 x 8.0 x 7.9 x 0% 25.5 x 30.3 x 29.1 x 31% 26% 27%

Rocket Fuel FUEL-US 41 426 USD 1.0 x 0.7 x 0.6 x 27% -402.5 x -130.7 x 22.2 x 0% -1% 3%

Rubicon Project RUBI-US 37 711 USD 4.9 x 3.5 x 2.7 x 35% 32.2 x 29.3 x 16.5 x 15% 12% 16%

Marketo MKTO-US 41 1,112 USD 6.7 x 4.9 x 3.7 x 34% -53.1 x -40.7 x -80.1 x -13% -12% -5%

Constant Contact CTCT-US 32 1,379 USD 3.7 x 3.1 x 2.7 x 17% 20.1 x 16.1 x 12.7 x 18% 19% 21%

Millennial Media MM-US 139 223 USD 0.6 x 0.5 x 0.4 x 13% 16.3 x -6.2 x n/a 3% -8% n/a

Marin Software MRIN-US 37 246 USD 1.8 x 1.6 x 1.3 x 17% -10.8 x -16.2 x -40.0 x -17% -10% -3%

Tremor Video TRMR-US 51 132 USD 0.3 x 0.3 x 0.2 x 21% -4.9 x -8.1 x 32.7 x -7% -3% 1%

YuMe YUME-US 33 192 USD 0.7 x 0.6 x 0.6 x 14% 71.3 x 60.7 x 12.0 x 1% 1% 5%

Criteo CRTO-US 59 2,585 USD 6.1 x 4.6 x 3.6 x 31% 23.4 x 17.9 x 12.1 x 26% 26% 29%

Global Average 4.2 x 3.3 x 2.8 x 22% -21.4 x -2.2 x 3.1 x 14% 13% 18%

Global Median 3.1 x 2.7 x 2.3 x 19% 18.2 x 10.4 x 12.5 x 9% 6% 16%

AcuityAds AT-CA 20 18 CAD 1.3 x 1.0 x 0.7 x 34% -3.8 x -7.5 x 575.1 x -36% -14% 0%

AcuityAds Comparable Group Valuation Analysis

Source: Company filings, FactSet, Beacon Securities

EV/Sales EV/EBITDA EBITDA margins

Management Team

21Gabriel Leung, 416-507-3963

Experienced Board of Directors

22Gabriel Leung, 416-507-3963

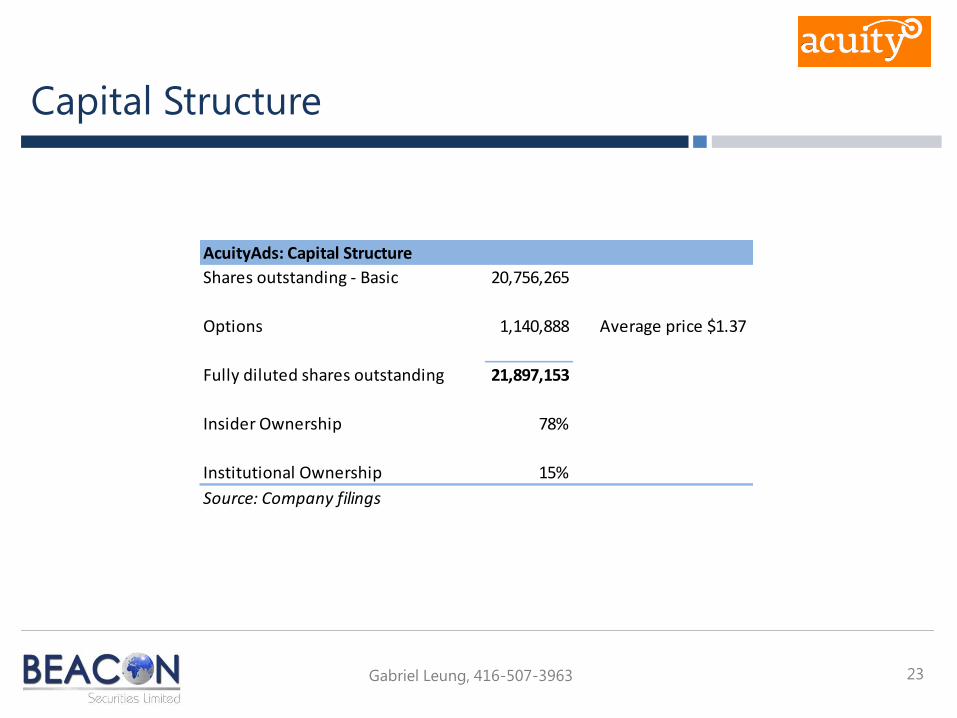

Capital Structure

23Gabriel Leung, 416-507-3963

Shares outstanding - Basic 20,756,265

Options 1,140,888 Average price $1.37

Fully diluted shares outstanding 21,897,153

Insider Ownership 78%

Institutional Ownership 15%

AcuityAds: Capital Structure

Source: Company filings

Risks To Our Analysis

• This is a relatively small company in ramp up mode with limited financial resources. As such, a

slower than expected pick up in adoption of the company’s RTB platform could constrain the

company’s financial resources. Based on our growth projections, we anticipate AcuityAds could

require additional financing over the near-term, which creates potential financing/dilution risks.

• AcuityAds uses “cookies” (small text files) in connection with its Programmatic Marketing

Platform. Without cookie data, Acuity may bid on advertising without as much insight into

activity that has taken place through an Internet user’s browser thereby undermining the

effectiveness of AcuityAd’s Programmatic Marketing Platform. Cookies may easily be deleted or

blocked by Internet users. In addition, some Internet browsers block third party cookies by

default, and other Internet browsers may implement similar features in the future. Certain

international jurisdictions have adopted and implemented legislation that negatively impacts the

use of cookies for online advertising, and additional jurisdictions may do so in the future.

24Gabriel Leung, 416-507-3963

Risks To Our Analysis

• If a “Do Not Track” browser setting is adopted by many internet users, and the standard either

imposed by legislation or agreed upon by standard setting groups, prohibits AcuityAds from

using non-personal information as it currently does, then that could hinder growth of

advertising and content production on the web generally, cause AcuityAds to change its

business practices, and adversely affect its business.

• This is a competitive market and includes both direct competitors such as Rocket Fuel,

MediaMath, and Chango, and also indirect competitors in the form of media agency trading

desks. We believe the high level of competition could put pressure on AcuityAds’ gross margin

profile over time, but also increase the probability of consolidation activity (with AcuityAds’ being

a potential target).

25Gabriel Leung, 416-507-3963

March 5, 2015 | Page 26 Gabriel Leung | 416-507-3963 | [email protected]

AcuityAds Holdings Inc.

AcuityAds Income Statement

2011 2012 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014e 2014e 2015e 2016e

(C$) Dec-11 Dec-12 31-Dec-13 31-Mar-14 30-Jun-14 30-Sep-14 31-Dec-14 31-Dec-14 31-Dec-15 31-Dec-16

Revenues:

Managed Services 9,971,207 2,619,108 2,889,041 2,806,179 3,700,000 12,014,328 15,199,569 19,151,457

Growth q/q 10.3% -2.9% 31.9%

Growth y/y 18.3% 7.2% 32.0% 26.0% 20.5% 26.5% 26.0%

Self-service technology 185,177 157,709 300,996 483,651 700,000 1,642,356 2,850,000 5,500,000

Growth q/q 90.9% 60.7% 44.7%

Growth y/y n/a 225.3% 2640.1% 833.3% 786.9% 73.5% 93.0%

Total revenues 1,116,716 5,074,364 10,156,384 2,776,817 3,190,037 3,289,830 4,400,000 13,656,684 18,049,569 24,651,457

Growth q/q 14.9% 3.1% 33.7%

Growth y/y 354.4% 100.2% 25.4% 14.4% 53.5% 46.1% 34.5% 32.2% 36.6%

Media costs 681,390 2,453,693 4,259,422 1,315,094 1,655,606 1,578,715 2,305,000 6,854,415 9,604,280 13,342,243

% of revenues 61.0% 48.4% 41.9% 47.4% 51.9% 48.0% 52.4% 50.2% 53.2% 54.1%

Gross profit 435,326 2,620,671 5,896,962 1,461,723 1,534,431 1,711,115 2,095,000 6,802,269 8,445,289 11,309,214

Gross margins 39.0% 51.6% 58.1% 52.6% 48.1% 52.0% 47.6% 49.8% 46.8% 45.9%

Operating expenses:

Employee compensation and benefits 274,930 1,330,022 3,308,319 1,278,136 2,460,455 2,364,557 2,420,000 8,523,148 8,388,218 8,628,010

% of revenues 24.6% 26.2% 32.6% 46.0% 77.1% 71.9% 55.0% 62.4% 46.5% 35.0%

G&A 638,306 1,671,557 2,038,728 590,051 1,266,056 869,079 893,200 3,618,386 3,363,807 3,500,507

% of revenues 57.2% 32.9% 20.1% 21.2% 39.7% 26.4% 20.3% 26.5% 18.6% 14.2%

Listing expense 0 0 0 0 0 352,253 0 352,253 0 0

Depreciation 2,004 14,262 88,539 36,293 52,569 65,969 65,969 220,800 263,876 263,876

Total expenses 915,240 3,015,841 5,435,586 1,904,480 3,779,080 3,651,858 3,379,169 12,714,587 12,015,902 12,392,393

Operating income -479,914 -395,170 461,376 -442,757 -2,244,649 -1,940,743 -1,284,169 -5,912,318 -3,570,613 -1,083,179

Operating margins -43.0% -7.8% 4.5% -15.9% -70.4% -59.0% -29.2% -43.3% -19.8% -4.4%

EBITDA -376,849 -284,687 741,199 -383,576 -2,160,928 -1,309,488 -1,005,167 -4,859,159 -2,454,605 32,829

EBITDA margins -33.7% -5.6% 7.3% -13.8% -67.7% -39.8% -22.8% -35.6% -13.6% 0.1%

Finance income 0 0 0 0 0 -12,579 0 -12,579 0 0

Finance costs 81,111 227,832 516,276 214,133 180,316 191,386 191,386 777,221 765,544 765,544

Foreign exchange (gain) loss 14,744 -23,606 42,884 68,760 -35,725 63,181 0 96,216 0 0

95,855 204,226 559,160 282,893 144,591 241,988 191,386 860,858 765,544 765,544

Income before taxes -575,769 -599,396 -97,784 -725,650 -2,389,240 -2,182,731 -1,475,555 -6,773,176 -4,336,157 -1,848,723

Income taxes 0 0 0 8,386 2,885 0 0 11,271 0 0

Income tax rate 0.0% 0.0% 0.0% -1.2% -0.1% 0.0% 0.0% -0.2% 0.0% 0.0%

Net income -575,769 -599,396 -97,784 -734,036 -2,392,125 -2,182,731 -1,475,555 -6,784,447 -4,336,157 -1,848,723

Net margins -51.6% -11.8% -1.0% -26.4% -75.0% -66.3% -33.5% -49.7% -24.0% -7.5%

EPS:

Basic -0.04 -0.04 -0.01 -0.04 -0.14 -0.11 -0.07 -0.37 -0.19 -0.08

FD -0.04 -0.04 -0.01 -0.04 -0.14 -0.11 -0.07 -0.37 -0.19 -0.08

Shares outstanding:

Basic 15,384,615 15,384,615 15,820,766 16,834,760 16,834,760 20,096,619 20,096,619 18,465,689 22,239,476 24,382,333

FD 15,384,615 15,384,615 15,820,766 16,834,760 16,834,760 20,096,619 20,096,619 18,465,689 22,239,476 24,382,333

Source: Company filings, Beacon Securities

March 5, 2015 | Page 27 Gabriel Leung | 416-507-3963 | [email protected]

AcuityAds Holdings Inc.

2011 2012 2013 Q1 2014 Q2 2014 Q3 2014

(C$) Dec-11 Dec-12 31-Dec-13 31-Mar-14 30-Jun-14 30-Sep-14

Assets:

Current assets:

Cash and cash equivalents 0 60,498 120,467 446,034 139,912 3,117,550

Accounts receivable 623,563 1,932,653 3,057,764 3,221,932 3,209,223 3,220,291

Other current assets 5,879 33,668 178,105 270,050 552,061 281,347

Investment tax credits receivable 276,067 491,764 1,091,764 1,191,764 450,000 450,000

Total current assets 905,509 2,518,583 4,448,100 5,129,780 4,351,196 7,069,188

Non-current assets:

Property and equipment 11,358 72,451 436,232 491,840 652,717 729,766

Total assets 916,867 2,591,034 4,884,332 5,621,620 5,003,913 7,798,954

Liabilities:

Current

Bank indebtedness 93,379

Accounts payable and accrued liabilities 683,968 3,191,664 2,359,827 2,444,518 3,720,350 3,666,202

Promissory notes payable 0 0 2,913,133 3,912,797 0 0

Due to related parties 1,085,829 848,854 616,657

Current portion of obligations under capital lease 27,507 91,542 132,700

Total current liabilities 1,863,176 4,040,518 5,272,960 6,384,822 4,428,549 3,798,902

Non-current liabilities:

Promissory notes payable 3,925,255 3,937,711

Due to related parties 608,249 626,500 0 0

Obligations under capital notes 51,681 155,407 218,601

Repayable government grant 150,000 150,000

Total liabilities 1,863,176 4,040,518 5,881,209 7,063,003 8,659,211 8,105,214

Shareholders' deficiency -946,309 -1,449,484 -996,877 -1,441,383 -3,655,298 -306,260

Total liabilites and shareholder equity 916,867 2,591,034 4,884,332 5,621,620 5,003,913 7,798,954

AcuityAds Balance Sheet

Source: Company filings, Beacon Securities

March 5, 2015 | Page 28 Gabriel Leung | 416-507-3963 | [email protected]

AcuityAds Holdings Inc.

2011 2012 2013 Q1 2014 Q2 2014 Q3 2014

(C$) Dec-11 Dec-12 31-Dec-13 31-Mar-14 30-Jun-14 30-Sep-14

Cash flows from (used in) operating activities:

Loss for the year -575,769 -599,396 -97,784 -732,244 -2,393,917 -2,198,727

Adjustments

Depreciation of property and equipment 2,004 14,262 88,539 36,293 52,569 65,969

Finance costs 81,111 227,832 516,276 214,133 180,316 191,387

Finance income -12,579

Share-based compensation 101,061 96,221 191,284 22,888 31,152 213,033

Reverse takeover consideration included in listing expense 205,174

Change in non-cash operating working capital:

Accounts receivable -591,147 -1,309,090 -1,125,111 -164,166 12,707 -11,068

Other current assets -5,879 -27,789 -144,437 -91,945 -282,011 270,714

Investments tax credits receivable -259,741 -215,697 -600,000 -100,000 741,764 0

Accounts payable and accrued liabilities 509,072 2,507,697 -831,838 83,898 1,274,196 -51,719

-163,519 1,293,436 -1,905,287 1,101 2,010,693 870,911

Interest paid -19,456 -118,808 -410,827 -179,434 -175,663 -168,781

Operating cash flow -758,744 575,232 -2,413,898 -910,577 -558,887 -1,496,597

Cash used in investing activities:

Additions to property and equipment -13,362 -75,355 -452,320 -12,713 -28,810 -15,317

Investing cash flow -13,362 -75,355 -452,320 -12,713 -28,810 -15,317

Cash flows from (used in) financing activities:

Net proceeds from promissary notes, net of issuance costs 2,891,416 984,007 2 -2

Proceeds (repayments) of amounts due to related parties, net 685,100 -346,000 -324,336 -400 -616,657

Repayment of capital leases -16,877 -23,347

Proceeds from private placement, net of issue costs 5,124,558

Proceeds from the issuance of common shares and warrants 900 250,022 250,000 -250,000 0

Proceeds from the exercise of stock options 109,885 14,850 148,850 5,000

Proceeds from the exercise of warrants 250,000 0

Proceeds related to repayable government grant 150,000 0

Dividends paid -800 0

Financing cash flow 686,000 -346,000 2,926,187 1,248,857 281,575 4,489,552

Changes in cash -86,106 153,877 59,969 325,567 -306,122 2,977,638

Cash, beginning of year -7,273 -93,379 60,498 120,467 446,034 139,912

Cash, end of year -93,379 60,498 120,467 446,034 139,912 3,117,550

Source: Company filings, Beacon Securities

AcuityAds Cash Flow Statement

Beacon Securities Ltd.| 66 Wellington Street West, Suite 4050, Toronto, Ontario, M5K 1H1 |416.643.3830|www.beaconsecurities.ca

Disclosure Requirements

Does Beacon, or its affiliates or analysts collectively, beneficially own 1% or more of any class of the issuer's equity securities? Yes No

Does the analyst who prepared this research report have a position, either long or short, in any of the issuer’s securities? Yes No

Does Beacon Securities beneficially own more than 1% of equity securities of the issuer? Yes No

Has any director, partner, or officer of Beacon Securities, or the analyst involved in the preparation of the research report, received remuneration for

any services provided to the securities issuer during the preceding 12 months?

Yes No

Has Beacon Securities performed investment banking services in the past 12 months and received compensation for investment banking services for

this issuer in the past 12 months? Yes No

Was the analyst who prepared this research report compensated from revenues generated solely by the Beacon Securities Investment Banking

Department? Yes No

Does any director, officer, or employee of Beacon Securities serve as a director, officer, or in any advisory capacity to the issuer? Yes No

Are there any material conflicts of interest with Beacon Securities or the analyst who prepared the report and the issuer? Yes No

Is Beacon Securities a market maker in the equity of the issuer? Yes No

Has the analyst visited the head office of the issuer and viewed its operations in a limited context? Yes No

Did the issuer pay for or reimburse the analyst for the travel expenses? Yes No

All information contained herein has been collected and compiled by Beacon Securities Limited, an independently owned and operated member of

the IIROC. All facts and statistical data have been obtained or ascertained from sources, which we believe to be reliable, but are not warranted as

accurate or complete.

All projections and estimates are the expressed opinion of Beacon Securities Limited, and are subject to change without notice. Beacon Securities

Limited takes no responsibility for any errors or omissions contained herein, and accepts no legal responsibility from any losses resulting from investment

decisions based on the content of this report.

This report is provided for informational purposes only and does not constitute an offer or solicitation to buy or sell securities discussed herein. Based on

their volatility, income structure, or eligibility for sale, the securities mentioned herein may not be suitable or available for all investors in all countries.

Dissemination

Beacon Securities distributes its research products simultaneously, via email, to its authorized client base. All research is then available on

www.beaconsecurities.ca via login and password.

Analyst Certification

The Beacon Securities Analyst named on the report hereby certifies that the recommendations and/or opinions expressed herein accurately

reflect such research analyst’s personal views about the company and securities that are the subject of the report; or any other companies

mentioned in the report that are also covered by the named analyst. In addition, no part of the research analyst’s compensation is, or will

be, directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report.

![6-6 Modeling Real-World Data with Sinusoidal Functions · Model 2: Graphing Calculator y 1.60 sin (0.51t 1.60) 12.12 y 1.60 sin [0.51(9.5) 1.60] 12.12 y 11.95484295 On September 30,](https://img.dokumen.tips/doc/110x75/5f20dbf37a97cc6aa36f9307/6-6-modeling-real-world-data-with-sinusoidal-functions-model-2-graphing-calculator.jpg)