Embed Size (px)

Citation preview

November 22, 2007

Industry SurveysAirlines

THIS ISSUE REPLACES THE ONE DATED MAY 24 , 2007 .THE NEXT UPDATE OF THIS SURVEY IS SCHEDULED FOR MAY 2008 .

CCoonnttaaccttss::

Inquiries &Client [email protected]

MediaMichael [email protected]

Replacement copies800.852.1641

Jim CorridoreAirlines Analyst

CURRENT ENVIRONMENT..................................................................1Chronic delays prompt increased government scrutiny

Delays unlikely to ground profitability Profitability seen for 2007 and 2008 Fares, yields have risen Open skies ahead? Where are the mergers? Labor costs down sharply, but still too high Pressure to “go green”

INDUSTRY PROFILE...............................................................................9Airlines still face extreme challenges

INDUSTRY TRENDS ...............................................................................10The impact of five years of multibillion-dollar losses Airlines struggle to survive Security costs rise Start-ups: many fail, a few thrive Small jets create opportunities in regional markets Embracing the Internet... International markets provide growth

HOW THE INDUSTRY OPERATES .............................................................17Providing transportation Industry structure Competitors on all sides Airline costs Operations overview Distribution changing with technology Regulation under deregulation Feds take jurisdiction over airport security

KEY INDUSTRY RATIOS AND STATISTICS ...................................................25HOW TO ANALYZE AN AIRLINE .............................................................27

Revenue-related factors Costs Profitability and load factor Balance sheet stability and cash burn Service and safety record Equity valuation

GLOSSARY .............................................................................................32

INDUSTRY REFERENCES.....................................................................33

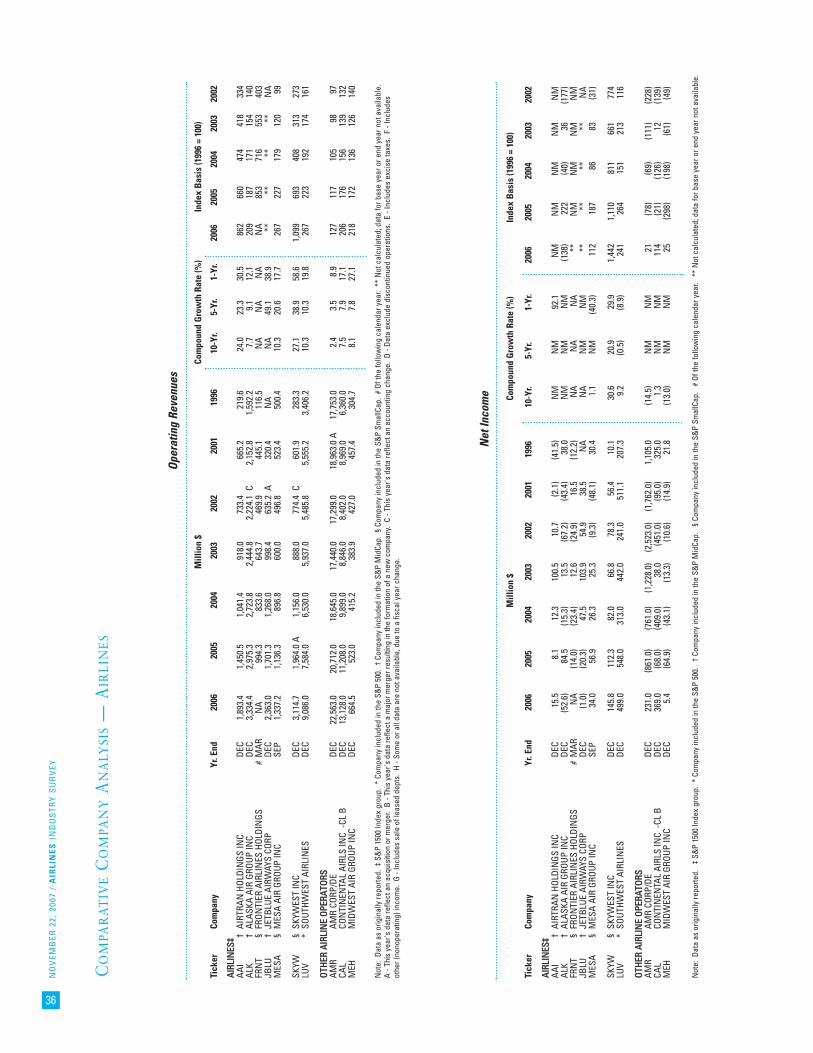

COMPARATIVE COMPANY ANALYSIS .............................................36

Executive Editor: Eileen M. Bossong-MartinesAssociate Editor: Joseph M. CodaCopy Editor: Brandon WilkersonStatistician: Sally Kathryn NuttallProduction: GraphMedia

Client Support: 1-800-523-4534Copyright © 2007 by Standard & Poor’sAll rights reserved.ISSN 0196-4666USPS No. 517-780Visit the Standard & Poor’s Web site:http://www.standardandpoors.com

STANDARD & POOR’S INDUSTRY SURVEYS is published weekly. Annualsubscription: $10,500. Please call for special pricing: 1-800-523-4534,option 2. Reproduction in whole or in part (including inputting into acomputer) prohibited except by permission of Standard & Poor’s.Executive and Editorial Office: Standard & Poor’s, 55 Water Street, NewYork, NY 10041. Standard & Poor’s is a division of The McGraw-HillCompanies. Officers of The McGraw-Hill Companies, Inc.: Harold McGrawIII, Chairman, President, and Chief Executive Officer; Kenneth M. Vittor,Executive Vice President and General Counsel; Robert J. Bahash,Executive Vice President and Chief Financial Officer; John Weisenseel,Senior Vice President, Treasury Operations. Periodicals postage paid atNew York, NY 10004 and additional mailing offices. POSTMASTER: Sendaddress changes to Standard & Poor’s, INDUSTRY SURVEYS, Attn: MailPrep, 55 Water Street, New York, NY 10041. Information has beenobtained by Standard & Poor’s INDUSTRY SURVEYS from sourcesbelieved to be reliable. However, because of the possibility of human ormechanical error by our sources, INDUSTRY SURVEYS, or others,INDUSTRY SURVEYS does not guarantee the accuracy, adequacy, orcompleteness of any information and is not responsible for any errors oromissions or for the results obtained from the use of such information.

VOLUME 175, NO. 47, SECTION 1 THIS ISSUE OF INDUSTRY SURVEYS INCLUDES 2 SECTIONS.

Standard & Poor’s Industry Surveys

If 2006 was known as the year the industry re-covered from five years of billion-dollar losses,2007 will surely be known as a year of frus-trating delays, cancellations, and poor cus-tomer service. The year started out with poorwinter weather, which led to numerous flightdelays and cancellations, as well as severalhighly publicized incidents of passengersstranded on planes for hours. Summer travelbrought severe airport congestion, the returnof long security lines, flight delays and cancel-lations even during good weather, and terribleon-time performance industrywide.

Standard & Poor’s does not believe there isan easy short-term solution to the complexgridlock and congestion problems plaguing theindustry. Nevertheless, there are several fixesthat we think could alleviate the pressure onthe system in the short term until a new airtraffic control system can be deployed, whichwould go a long way toward easing airportdelays and congestion. If the carriers them-selves are unable or unwilling to take somesteps, we think the US government, particular-ly heading into an election year, could step inand force some corrective action.

In fact, on September 20, 2007, the USHouse of Representatives passed an FAAfunding bill (H.R. 2881), which, along with

funding for the Federal Aviation Administra-tion (FAA), included demands that airlinesand airports come up with plans to providepassengers stranded by long delays withfood, water, and other basic amenities, andto allow passengers to deplane following ex-cessive delays. The White House was threat-ening a veto under the belief that thismeasure does not go far enough and wants abill that includes solutions to improve delaysas well. This bill could be the start of somere-regulation of the airline industry in orderto ease customer service problems.

The issue of overcrowded skies eased withthe airline industry downturn that started in2001. By 2006, however, industry trafficreached pre-2001 levels and delays againreared their ugly head, primarily during peaktravel periods. In the summer of 2007, thelevel of delays ratcheted up further. Year todate through August, the US airline indus-try’s on-time arrival rate was 72%, versus76% for the first eight months of 2006, ac-cording to the Bureau of Transportation Sta-tistics. For the month of August alone, theon-time arrival rate was 71.7%, versus75.8% a year earlier. Though sharply worsethan a year earlier, this was an improvementover July 2007’s on-time rate of 69.8%. Alsoin August 2007, complaints about airline ser-vice nearly doubled to 1,634, versus 864 inAugust 2006.

Standard & Poor’s believes that possibleshort-term solutions could include the FAAimposing restrictions on US carriers to flyfewer flights during peak periods, whichwould force airlines to spread more flightsout to off-peak periods. In addition, wethink that smaller regional and corporate jetscould be given less priority for take-off thanbigger legacy planes carrying more passen-gers. The FAA is already implementingchanges to flight paths in some major mar-kets including the New York metropolitanarea, which is partly intended to allow air

CURRENT ENVIRONMENT

Chronic delays prompt increased government scrutiny

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

1

DOMESTIC AIRLINE YIELDS(Year-to-year % change)

Source: Air Transport Association of America.

15

10

5

0

-5

-10

-15

-201998 1999 2000 2001 2002 2003 2004 2005 2006 2007

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

2

traffic controllers to spread flights out over agreater geographic area to increase air trafficdensity. Restrictions on the number of re-gional jets flown in congested markets couldalso be a partial solution, since regional jetscarry far fewer passengers than large jets, yettake up just as much time taxiing, taking off,and landing as other planes. If airlines wereforced to “upgauge” their fleets (flying big-ger jets rather than smaller planes that neces-sitate more take-offs), we think this couldalso help cut delays.

In the long term, the replacement of theoutdated air traffic control (ATC) system willbe necessary to ease congestion. This anti-quated system uses radar rather than themore sophisticated satellite-based GPS (glob-al positioning system) technology largelyavailable in passenger vehicles. In otherwords, the plane in which you are flyingdoesn’t have the same level of tracking so-phistication that you have available in yourcar. Though better technology is available,it will take many years and billions of dol-lars in spending to implement a new sys-tem, so Standard & Poor’s feels that flightdelays will be here for some time to come.

Delays unlikely to ground profitability

Standard & Poor’s believes that 2007 willbe looked back on as a year of sharp financialimprovement and profitability for the US air-line industry, following an improved year in2006. We also think that 2008 is likely to re-main profitable, though we are worried aboutthe impact of a slowing US economy and highoil prices. This follows 2006, when the US air-line industry saw sharp improvement in rev-enues, earnings, and passenger traffic, taking alarge step in the right direction after five yearsof multibillion-dollar losses.

Part of the reason for the industry’s recov-ery is reflected in the large number of airlinebankruptcies that took place in 2005. Atsome point between September 14, 2005,and September 27, 2006, five of the 11 ma-jor US airlines were operating under Chapter11 bankruptcy protection. All five of theseairlines — US Airways Group Inc., UALCorp. (parent of United Airlines), GlobalAero Logistics Inc. (formerly ATA Holdings,parent of ATA Airlines), Delta Air Lines Inc.,and Northwest Airlines — have emergedfrom bankruptcy.

Standard & Poor’s believes that the indus-try is now in the midst of a recovery, but onethat is somewhat fragile. The risks are numer-ous: a potential spike in oil prices, the effectsof a resurgence of concern over terrorism andincreased security impositions, and a slowingof the US economy. In addition, any sharp risein capacity plans at one or more of the carri-ers could put the industry recovery at risk bysparking a fare war. We believe that it is stilltoo soon to say that the industry is out of thewoods, especially given the still-shaky state ofmany airline balance sheets.

Profitability seen for 2007 and 2008

The 10 largest airlines in the US reported anet profit in 2006 of $1.6 billion excluding re-organization items at bankrupt carriers DeltaAir Lines (a loss of $7.2 billion) and North-west Airlines (a loss of $3.2 billion), and alsoexcluding reorganization items at UAL Corp.(gain of $22.9 billion upon emerging frombankruptcy). This net profit came on totalrevenues of $112.4 billion, an increase of11% over revenues of $101.4 billion in 2005.Excluding these reorganization items, the in-dustry returned to profitability for the firsttime since 2000. Also excluding reorganiza-tion items, seven of the 10 largest US airlineswere profitable in 2006, with only UALCorp., Alaska Air Group Inc., and JetBlueAirways Corp. unprofitable for the year.

Standard & Poor’s expects improving in-dustry fundamentals to lead to increasedprofitability in 2007. Standard & Poor’s cur-rently forecasts profits at all of the 10 largestUS carriers, with their aggregate profit hit-ting $3.1 billion in 2007. For 2008, we cur-rently forecast a profit of $4.1 billion for thetop ten US carriers.

Excluding reorganization items, the top10 US carriers lost about $4.0 billion in2005, on revenues of $101.4 billion. Accord-ing to our calculations, the net loss incurredby the top 10 carriers totaled $8.2 billion in2004 (on revenues of $85.8 billion), follow-ing losses of $4.5 billion ($81.6 billion) in2003, $11.1 billion ($80.9 billion) in 2002,and $7.6 billion ($87.2 billion) in 2001.

Airline equities have been a difficult placefor investors to make money. In 2006, theS&P Airlines subindex fell 7.7%, significant-ly underperforming the S&P 500 CompositeStock index, which rose 13.6% over the

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

3

same period. In 2005, the S&P Airlinessubindex rose a meager 1.4%, comparedwith a 3.0% rise in the S&P 500. Through2006, the five-year compound annual growthrate in the S&P Airlines subindex was–13.4%, compared with a 4.4% increase inthe S&P 500 over the same period. We be-lieve that the poor performance of the S&PAirlines subindex for the past few years re-flects high oil prices, airline bankruptcies,and serious questions as to when the indus-try will return to sustained profitability. Yearto date through October 19, 2007, the S&PAirlines subindex declined a further 15.0%,versus a 5.8% rise in the S&P 500.

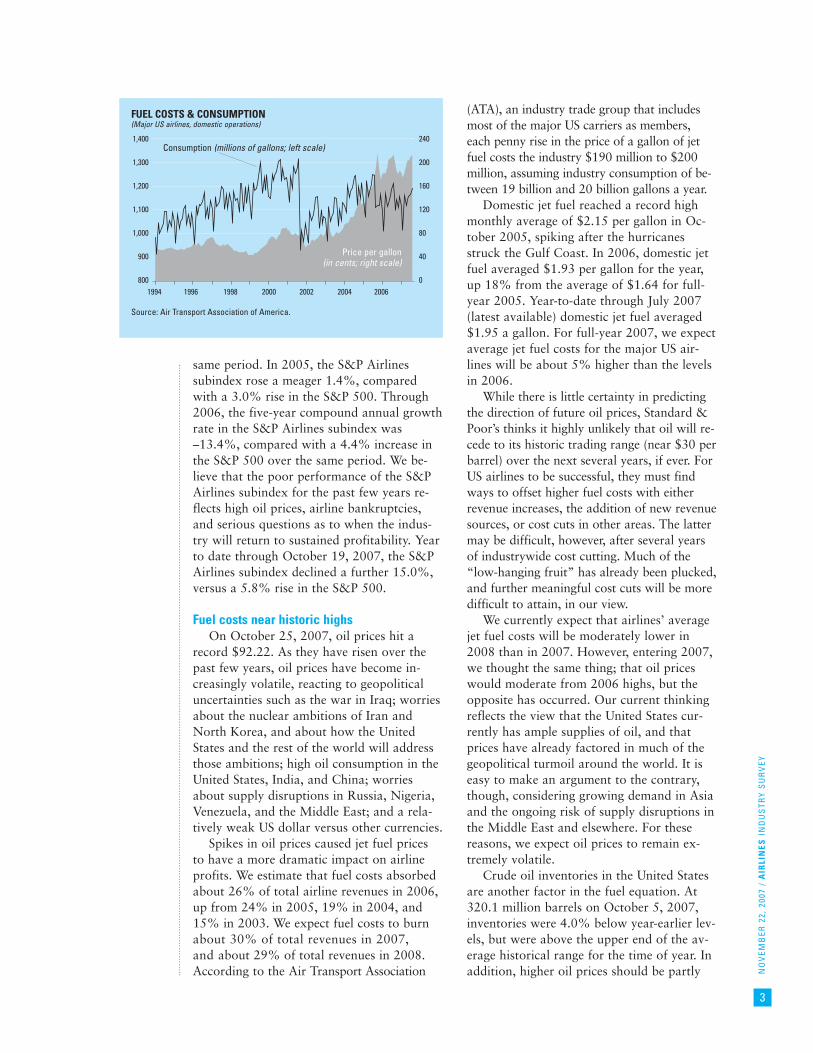

Fuel costs near historic highsOn October 25, 2007, oil prices hit a

record $92.22. As they have risen over thepast few years, oil prices have become in-creasingly volatile, reacting to geopoliticaluncertainties such as the war in Iraq; worriesabout the nuclear ambitions of Iran andNorth Korea, and about how the UnitedStates and the rest of the world will addressthose ambitions; high oil consumption in theUnited States, India, and China; worriesabout supply disruptions in Russia, Nigeria,Venezuela, and the Middle East; and a rela-tively weak US dollar versus other currencies.

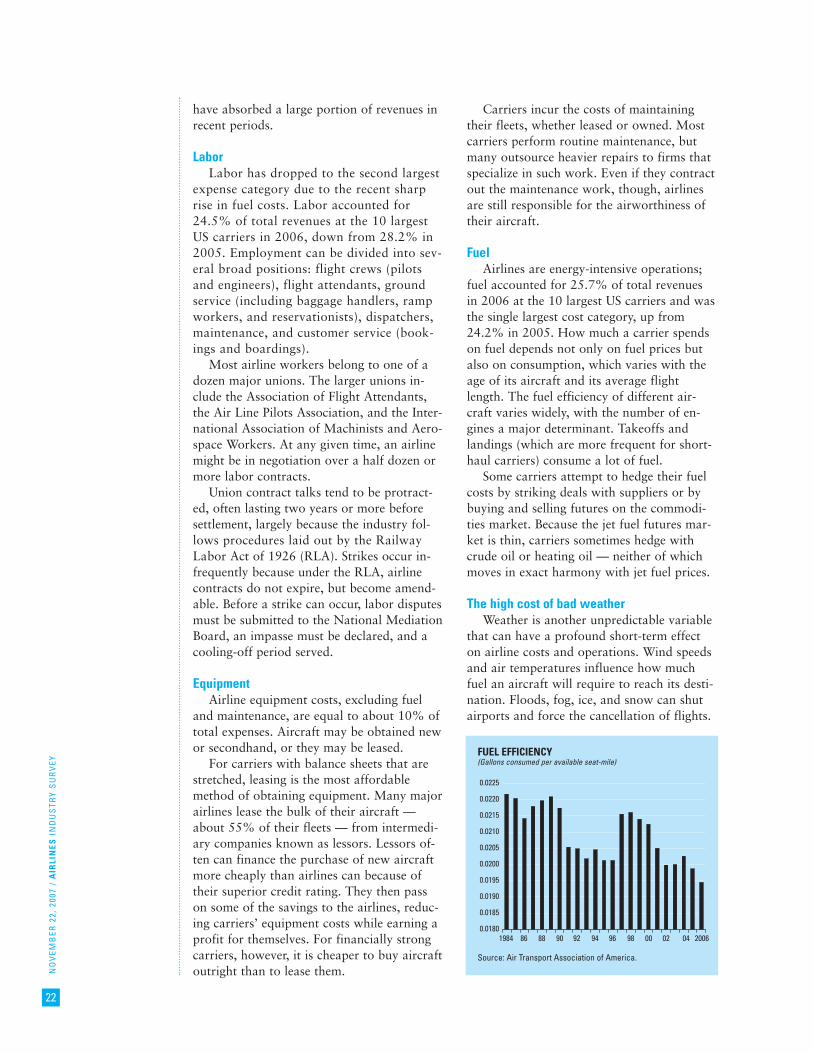

Spikes in oil prices caused jet fuel pricesto have a more dramatic impact on airlineprofits. We estimate that fuel costs absorbedabout 26% of total airline revenues in 2006,up from 24% in 2005, 19% in 2004, and15% in 2003. We expect fuel costs to burnabout 30% of total revenues in 2007,and about 29% of total revenues in 2008.According to the Air Transport Association

(ATA), an industry trade group that includesmost of the major US carriers as members,each penny rise in the price of a gallon of jetfuel costs the industry $190 million to $200million, assuming industry consumption of be-tween 19 billion and 20 billion gallons a year.

Domestic jet fuel reached a record highmonthly average of $2.15 per gallon in Oc-tober 2005, spiking after the hurricanesstruck the Gulf Coast. In 2006, domestic jetfuel averaged $1.93 per gallon for the year,up 18% from the average of $1.64 for full-year 2005. Year-to-date through July 2007(latest available) domestic jet fuel averaged$1.95 a gallon. For full-year 2007, we expectaverage jet fuel costs for the major US air-lines will be about 5% higher than the levelsin 2006.

While there is little certainty in predictingthe direction of future oil prices, Standard &Poor’s thinks it highly unlikely that oil will re-cede to its historic trading range (near $30 perbarrel) over the next several years, if ever. ForUS airlines to be successful, they must findways to offset higher fuel costs with eitherrevenue increases, the addition of new revenuesources, or cost cuts in other areas. The lattermay be difficult, however, after several yearsof industrywide cost cutting. Much of the“low-hanging fruit” has already been plucked,and further meaningful cost cuts will be moredifficult to attain, in our view.

We currently expect that airlines’ averagejet fuel costs will be moderately lower in2008 than in 2007. However, entering 2007,we thought the same thing; that oil priceswould moderate from 2006 highs, but theopposite has occurred. Our current thinkingreflects the view that the United States cur-rently has ample supplies of oil, and thatprices have already factored in much of thegeopolitical turmoil around the world. It iseasy to make an argument to the contrary,though, considering growing demand in Asiaand the ongoing risk of supply disruptions inthe Middle East and elsewhere. For thesereasons, we expect oil prices to remain ex-tremely volatile.

Crude oil inventories in the United Statesare another factor in the fuel equation. At320.1 million barrels on October 5, 2007,inventories were 4.0% below year-earlier lev-els, but were above the upper end of the av-erage historical range for the time of year. Inaddition, higher oil prices should be partly

FUEL COSTS & CONSUMPTION(Major US airlines, domestic operations)

Source: Air Transport Association of America.

1,400

1,300

1,200

1,100

1,000

900

800

240

200

160

120

80

40

01994 1996 1998 2000 2002 2004 2006

Consumption (millions of gallons; left scale)

Price per gallon(in cents; right scale)

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

4

offset by the use of more efficient fleets, ascarriers have retired their oldest, most fuel-guzzling planes. Some of the financiallystronger airlines are also at least partly pro-tected from price escalations by hedging con-tracts put in place when prices were lower.Even this, however, will not be nearlyenough to fully protect them from high jetfuel costs.

“Crack spread” exacerbates the pain of highoil prices

Even as crude oil prices hover aroundrecord levels, something else is hurting theUS airline industry: the “crack spread.” Thismeasure — the cost difference between a bar-rel of oil and a barrel of refined jet fuel — hastraditionally hovered somewhere between $5and $10 a barrel; that is, jet fuel could costanywhere between $5 and $10 a barrel morethan crude oil. In the initial aftermath ofHurricanes Katrina and Rita, however, thatspread widened to about $60 a barrel, exac-erbating the difficulties the industry was al-ready facing. For full-year 2006, the crackspread averaged $16.64 a barrel, up 5%from the average of $15.84 for 2005 andwell above historical levels.

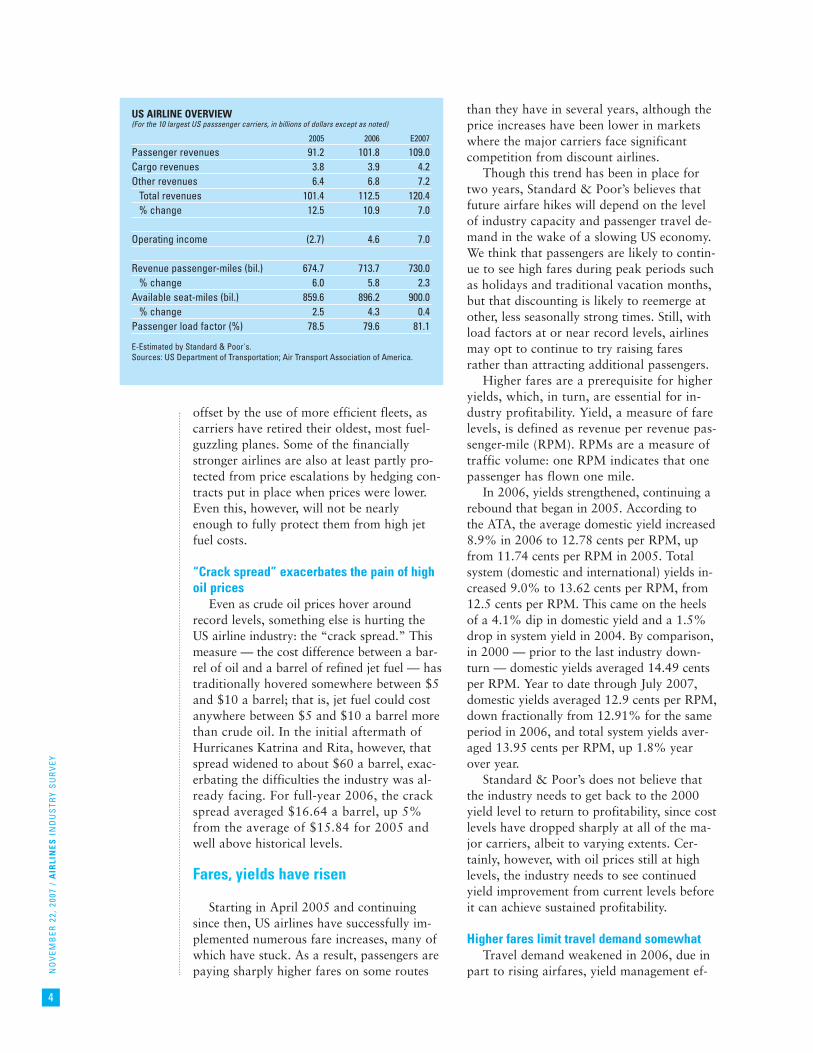

Fares, yields have risen

Starting in April 2005 and continuingsince then, US airlines have successfully im-plemented numerous fare increases, many ofwhich have stuck. As a result, passengers arepaying sharply higher fares on some routes

than they have in several years, although theprice increases have been lower in marketswhere the major carriers face significantcompetition from discount airlines.

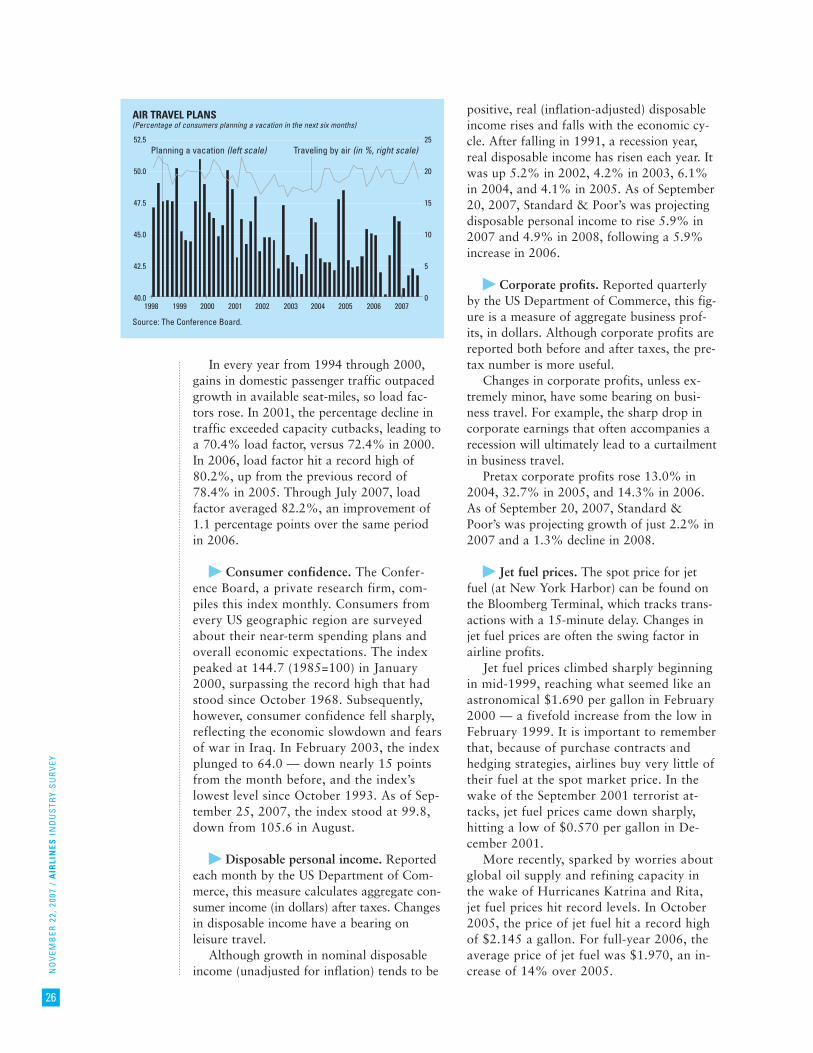

Though this trend has been in place fortwo years, Standard & Poor’s believes thatfuture airfare hikes will depend on the levelof industry capacity and passenger travel de-mand in the wake of a slowing US economy.We think that passengers are likely to contin-ue to see high fares during peak periods suchas holidays and traditional vacation months,but that discounting is likely to reemerge atother, less seasonally strong times. Still, withload factors at or near record levels, airlinesmay opt to continue to try raising faresrather than attracting additional passengers.

Higher fares are a prerequisite for higheryields, which, in turn, are essential for in-dustry profitability. Yield, a measure of farelevels, is defined as revenue per revenue pas-senger-mile (RPM). RPMs are a measure oftraffic volume: one RPM indicates that onepassenger has flown one mile.

In 2006, yields strengthened, continuing arebound that began in 2005. According tothe ATA, the average domestic yield increased8.9% in 2006 to 12.78 cents per RPM, upfrom 11.74 cents per RPM in 2005. Totalsystem (domestic and international) yields in-creased 9.0% to 13.62 cents per RPM, from12.5 cents per RPM. This came on the heelsof a 4.1% dip in domestic yield and a 1.5%drop in system yield in 2004. By comparison,in 2000 — prior to the last industry down-turn — domestic yields averaged 14.49 centsper RPM. Year to date through July 2007,domestic yields averaged 12.9 cents per RPM,down fractionally from 12.91% for the sameperiod in 2006, and total system yields aver-aged 13.95 cents per RPM, up 1.8% yearover year.

Standard & Poor’s does not believe thatthe industry needs to get back to the 2000yield level to return to profitability, since costlevels have dropped sharply at all of the ma-jor carriers, albeit to varying extents. Cer-tainly, however, with oil prices still at highlevels, the industry needs to see continuedyield improvement from current levels beforeit can achieve sustained profitability.

Higher fares limit travel demand somewhatTravel demand weakened in 2006, due in

part to rising airfares, yield management ef-

US AIRLINE OVERVIEW(For the 10 largest US passsenger carriers, in billions of dollars except as noted)

2005 2006 E2007

Passenger revenues 91.2 101.8 109.0 Cargo revenues 3.8 3.9 4.2 Other revenues 6.4 6.8 7.2

Total revenues 101.4 112.5 120.4 % change 12.5 10.9 7.0

Operating income (2.7) 4.6 7.0

Revenue passenger-miles (bil.) 674.7 713.7 730.0 % change 6.0 5.8 2.3

Available seat-miles (bil.) 859.6 896.2 900.0 % change 2.5 4.3 0.4

Passenger load factor (%) 78.5 79.6 81.1

E-Estimated by Standard & Poor's.Sources: US Department of Transportation; Air Transport Association of America.

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

5

forts at the carriers (they successfully restrict-ed the number of seats offered at sale prices),and lower industry capacity that made fewerseats available. According to the Air Trans-port Association, total domestic airline traf-fic fell 2.2% in 2006 to 379.4 billion RPMs.Still, with airfares rising and flights relativelyfull, domestic passenger revenues increased6.5% in 2006 after rising 3.2% in 2005.Standard & Poor’s currently expects flat do-mestic airline traffic for 2007.

Domestic capacity, as measured by avail-able seat-miles (ASMs, the total number ofseats multiplied by the total number of milesflown), declined 4.6% in 2006 to 468.3 bil-lion, after falling 2.8% in 2005. Standard &Poor’s is forecasting a 1.0% drop in capacityfor 2007. Domestic passenger load factor im-proved by 2.0 percentage points in 2006, hit-ting a record average of 81.0% for the year,after improving by 3.2 percentage points in2005, when it averaged 79.06%.

Terror fears to remain with usOn August 10, 2006, numerous individu-

als were arrested in relation to an alleged ter-rorist plot to mix liquids on board airlinersbound for the United States from Europe, inorder to create and then detonate explosivedevices while these planes were in flight. Inthe immediate aftermath of these arrests, air-ports instituted new security rules.

While the reemergence of worries aboutairline-related terrorist acts and the increasedhassle factor at airports have the potential toderail the nascent industry recovery, Stan-dard & Poor’s currently expects the overalleffect to be relatively minimal. We believethat these problems likely shaved about twopercentage points from unit revenue growthin the third quarter of 2006, but that theshort-term financial penalty was probablymore than offset by the positive impact ofthe recent drop in fuel prices.

Open skies ahead?

The European Union voted on and ap-proved an “open skies” aviation deal inMarch 2007. This two-year deal, which be-comes effective on March 28, 2008, will es-sentially open up restricted trans-Atlanticroutes and allow US airlines to fly anywherein the 27-nation European Union to anypoint in the United States. US carriers will

now be able to fly within Europe withoutgiving up similar domestic rights to interna-tional carriers. The deal is likely to open upthe London market to more competition, asmore carriers are likely to be awarded land-ing slots at Heathrow airport.

We think the deal could be beneficial forconsumers, as increased competition in someEuropean markets is likely to lead to lowerairfares. US carriers that do not currently en-joy landing slots at Heathrow, includingContinental Airlines Inc. and Delta, are likelyto benefit as well. Carriers such as United,American, and British Airways PLC, though,are likely to see increased competition andcould lose some coveted Heathrow landingslots. In addition, the deal could ultimatelyforce international airline industry consolida-tion, as the increased competition forces in-dustry consolidation. All of this is likely toplay out over several years: landing slotshave to be awarded, and the deal goes intoeffect a year from now.

Where are the mergers?

On November 15, 2006, US Airways pro-posed a merger with Delta Air Lines in a dealthat set the industry ablaze with merger spec-ulation. The proposed Delta–US Airwayscombination would have created the world’slargest airline. Delta successfully fought offthe merger, arguing to regulators, creditorsand employees that the airline was worthmore than the $8.0 billion original offer priceand the subsequently increased offer price of$10.2 billion. On January 31, 2007, US Air-ways rescinded its merger proposal.

Standard & Poor’s believes that themerger would have created a strong globalcompetitor, stronger than either of the car-riers on a standalone basis. In addition, wethink that the merger could have set up aseries of competing mergers as remainingcarriers could have potentially combined toincrease their ability to combat a combinedDelta–US Airways. We think Delta ulti-mately was worried that one of these po-tential mergers could have created astronger competitor. Despite rampant in-dustry speculation, no major deals have oc-curred as of October 2007. In fact, theonly other deal of recent note — the pro-posed merger of small regional player Mid-west Air Group Inc. by AirTran — was

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

6

fought off by MidWest by agreeing to beacquired in a private leveraged buyout.

Standard & Poor’s feels that it will take an-other industry downturn, with the return ofbillion-dollar losses, before any major industryconsolidation is to take place. We do thinkthat other leveraged private equity deals couldoccur, but the tightening of the US credit mar-ket in the aftermath of the subprime mortgagecrisis and housing slowdown should make itmore difficult to raise the necessary debt to fi-nance any prospective deal.

Airline industry restructuresIn general, Standard & Poor’s feels that sev-

eral factors — restrained industry capacity lev-els, a record percentage of seats filled onaverage, strong passenger demand, and risingprices — should drive improved revenuegrowth in 2007 and 2008. Oil prices remain asignificant worry, but any stabilization ormoderation could drive strong profit levels forthe first time in many years for much of the in-dustry. Nevertheless, the industry remains influx. In the midst of bankruptcies, restructur-ings, recoveries, mergers, and growth amongdiscounters, the changing shape of the airlineindustry is another dynamic variable thatcould sway results.

◆ Delta and Northwest. After strugglingfor some time, Delta and Northwest filed forChapter 11 bankruptcy protection on thesame day, September 14, 2005. Both carriersemerged from bankruptcy in the first half of2007 with sharply lower operating costs,lower debt levels, and streamlined opera-tions. So far the emergence of these carriershas not instigated another painful round ofcapacity hikes, airfare price cuts, and de-structive competition; they have so far beenmore restrained in how they have chosen tocompete, which could bode well for futureindustry prospects.

In bankruptcy, Delta has forced pay cutson its employees, eliminated its pilots’ pen-sion plan, and shrunk domestic capacitywhile increasing international capacity. Theairline also restructured aircraft operatingleases and debt obligations.

We believe that Northwest’s decision tofile for bankruptcy was influenced by thechanges in US bankruptcy laws that wentinto effect on October 17, 2005. Among oth-er changes, the revised law gave companies in

bankruptcy only 18 months to file a plan ofreorganization with the court; the previouslaw, in contrast, gave companies an almostunlimited amount of time (as highlighted byUnited spending more than three years underChapter 11 protection). Before its bankruptcyfiling, Northwest was battling a strike by itsmechanics union, as well as experiencing dif-ficult negotiations with flight attendants andpilots. In our view, once Northwest decidedthat it needed to file before October 17,2005, the company probably decided to fileeven sooner to protect as much of its cash aspossible.

In our view, Northwest was even more ag-gressive than Delta in pursuing cost cutsfrom labor groups, and the company under-went brutal negotiations with its mechanicsand flight attendants. In October 2006, aftera 14-month strike, mechanics agreed toterms with the company. Flight attendantshad a pay cut of 21% forced on them by thebankruptcy court.

◆ UAL out of bankruptcy. UAL — parentof United Airlines, the second largest airline inthe United States in terms of both revenuesand RPMs — filed for Chapter 11 bankruptcyprotection on December 9, 2002. This was amonumental event in the industry, given thatUnited accounted for about 25% of all RPMsflown by US scheduled airlines in 2002 andabout 24% of the US airline industry’s capaci-ty, as measured in ASMs.

On February 1, 2006, the bankruptcycourt confirmed UAL’s plan of reorganiza-tion, and the company emerged from Chap-ter 11 after operating for more than threeyears under bankruptcy protection. UALemerged with sharply lower operating costsand lower debt levels, and without the bur-den of a hugely underfunded pension plan,which was passed on to the US Pension Ben-efit Guarantee Corp. (PBGC), a governmentagency that insures the pensions of US cor-porations. In bankruptcy, United cut annualcosts by $7.0 billion, cut capacity by about20%, and sharply reduced debt and otherobligations. The company emerged frombankruptcy with about $3.0 billion in cash.

The company’s restructuring plan was cre-ated without long-term oil prices of over $60a barrel in mind, and may not have fully tak-en into account the extent to which discountcarriers have been driving pricing in the US

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

7

airline industry. Still, the company has afresh chance with lower debt, new capitaliza-tion, and no large underfunded pensionmake-up payments due.

Standard & Poor’s believes that United sub-stantially improved its competitive positionwhile in bankruptcy, but we also believe thatthe company still has higher operating coststhan most of its competitors. United’s strongbusiness travel market share and strong inter-national network could allow it to get a yieldpremium to peers in an industry upcycle,which is what we believe we currently are see-ing. If the company’s unit costs remain abovethose of its peers, though, we think that Unit-ed will remain susceptible to large losses dur-ing a future industry downturn.

◆ AMR: looking to cut debt. AMR Corp.,parent of American Airlines, posted net in-come of $231 million in 2006, following loss-es of $861 million in 2005, $761 million in2004, $1.3 billion in 2003, and $3.5 billionin 2002. In 2003, the airline was successful incoaxing $1.8 billion in annual cost reductionsfrom its unions. Labor concessions and othercost-cutting initiatives, including about $200million in givebacks by vendors and suppliers,were targeted to reduce AMR’s annual costsby about $4 billion.

Cost cuts, revenue increases, and sharpreductions in capital expenditures over thepast few years have led to a large increasein the company’s cash balances, which to-taled $5.2 billion at the end of 2006. Thesehigh cash levels, along with improving in-dustry prospects, lead us to believe thatAMR is not likely to file for bankruptcy atleast through the end of 2008.

If AMR is to survive in the longer term, itwill need to expand its cost-cutting and see asustained improvement in the industry envi-ronment. As of December 31, 2006, thecompany was saddled with $18.4 billion inlong-term debt and capital lease obligations,including current maturities and the presentvalue of operating leases. This was downfrom $20.1 billion a year earlier. Stockhold-ers’ equity was a negative $606 million, butthat had risen from a negative $1.4 billion ayear earlier. The company’s ability to staveoff bankruptcy has had a strong effect onAMR’s stock price since 2003. Since closingon December 31, 2002, at $6.60 a share, theshares increased more than six fold and

reached a high of $41.00 on January 17,2007, before the price settled to $23.76 onOctober 11.

◆ Continental: focus on Newark and in-ternational growth. Continental Airlines, thefourth largest US carrier, has been focused onusing its hub in Newark, New Jersey, as aninternational gateway. To this end, the com-pany has sharply increased international ca-pacity over the past year and a half, addingfrequencies and entering new European andAsian markets. Continental hopes to leverageits leading position in Newark to attractmore business travelers, an area in which italready leads most of its peers.

While many carriers have been cutting ca-pacity, Continental has been adding domesticcapacity, which has helped the carrier duringthe recent period of increasing fares. Stan-dard & Poor’s expects strong earnings forContinental in 2007 and 2008, following a$389 million net profit in 2006, which werethe carrier’s first profits from operationssince before September 11, 2001.

Low-cost carriers feel the heatAlthough the airline industry operating

environment was brutal from 2001 to 2005,carriers that operated with low costs and lowfares were generally able to cope better thantheir higher-cost counterparts. Notably,Southwest posted its 34th consecutive year ofnet income in 2006 — an amazing feat, giventhe cyclical nature of the business.

Two other low-cost carriers, JetBlue andAirTran, both performed better in 2006 thanin 2005, but both these carriers’ results aredisappointing when compared with prioryears. JetBlue posted a net loss of $1.0 mil-lion, which equates to $0.00 per share, onrevenues of $2.3 billion — better than the$20.2 million ($0.13 per share) loss that thecarrier experienced in 2005 on revenues of$1.7 billion, but sharply worse than net in-come of $0.29 per share and $0.65 per sharein 2004 and 2003, respectively. AirTran post-ed a $15.5 million net profit in 2006 ($0.17a share), on revenues of $1.9 billion — betterthan the $1.7 million net profit in 2005($0.02) on revenues of $1.5 billion. AirTran’snet profit in 2006 equates to a net margin ofjust 0.8%, sharply lower than the net profitof 10.9% that the carrier reported in 2003.The sharp rise in fuel costs over the past two

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

8

years has hurt both JetBlue and AirTran,while a successful fuel-hedging program hasprotected Southwest.

Southwest earned $499 million in 2006($0.61 a share), down from $548 million($0.67) in 2005. Although profits have re-mained below the levels of 2000, Southwesthas maintained its balance sheet health with-out cutting staff or capacity. In our opinion,Southwest is extremely well positioned relativeto its peers. We believe that Southwest will re-main profitable in 2007 and 2008 and willoutperform the industry financially over thenext few years.

Standard & Poor’s believes that the low-cost carriers are likely to continue to growrevenues at a much faster rate than the lega-cy carriers. Eventually, such carriers couldtake the lion’s share of the US air travel mar-ket, though such a shift would likely play outover many years.

Labor costs down sharply, but still too high

Standard & Poor’s estimated that laborcosts absorbed 24.5% of revenues at the 10largest US airlines in 2006, down from28.2% in 2005. While many of the majorairlines have succeeded in getting their workforces to give back a substantial portion oftheir wages, this percentage must come downfurther for the industry to return to sustain-able financial health. Pension and healthcarecosts, which have increased sharply in recentyears, are major contributors to the high per-centage of revenues absorbed by labor costs,and have partly offset increases in productiv-ity and pay cuts at many of the carriers.

We estimate that labor costs will experi-ence healthy declines in 2007, both on an ab-solute basis and as a percentage of revenues.We base this prediction largely on our expec-tation of wage and benefit cuts at Northwestand Delta, as well as likely lower pensioncosts on average, as a rise in the stock mar-ket could help underfunded pension plans.Higher interest rates, which we also expect,could allow airlines to raise their pension re-turn assumptions, thus decreasing theamount of pension underfunding (thoughthis will of course be partly offset by higherinterest expense at many airlines). In addi-tion, an increase in industry revenues shouldhelp lower labor costs as a percentage of rev-

enues. Finally, we expect continued pressureby most carriers on labor costs, both interms of absolute pay levels and through at-tempts to increase employee productivity.

For 2008, Standard & Poor’s thinks theindustry will need to see higher average faresand strong passenger travel to help laborcosts fall as a percentage of total revenues.We believe much of the benefit of airlinebankruptcies to be in place and see somepressure on rates as unions attempt to regainsome of what they lost in wages and benefitsover the past five years.

Pressure to “go green”

Recently, some environmental activistshave voiced displeasure over the carbondioxide emissions (“carbon footprint”) ofairlines. This issue, in the face of the ongoingdebate on how to fight global warming,could become a public relations problem foran industry that scarcely needs another issue.

Airlines are currently fighting the percep-tion that they are a major cause of green-house gasses by listing all the ways they havereduced jet fuel usage over the past 10 years:modernizing their fleets to more fuel efficientplanes, efforts to control fuel use, and modi-fications to existing planes to increase fuelefficiency, to name a few. Though the airlinesmay have undertaken these initiatives to cutcosts in the wake of high oil prices, they areusing their accomplishments as a way to easeconcerns. However, Standard & Poor’s feelsthat this issue is only starting to gain atten-tion in the industry, and we expect airlines toface increasing pressure on this front overthe next few years. ■

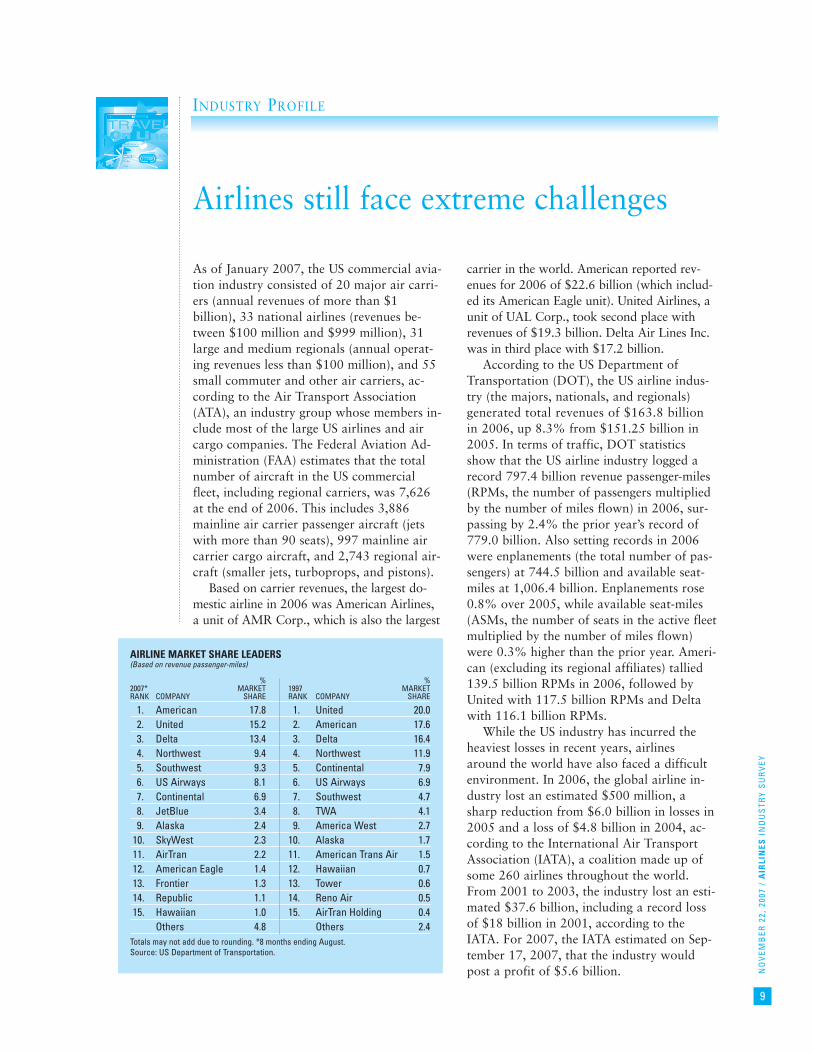

As of January 2007, the US commercial avia-tion industry consisted of 20 major air carri-ers (annual revenues of more than $1billion), 33 national airlines (revenues be-tween $100 million and $999 million), 31large and medium regionals (annual operat-ing revenues less than $100 million), and 55small commuter and other air carriers, ac-cording to the Air Transport Association(ATA), an industry group whose members in-clude most of the large US airlines and aircargo companies. The Federal Aviation Ad-ministration (FAA) estimates that the totalnumber of aircraft in the US commercialfleet, including regional carriers, was 7,626at the end of 2006. This includes 3,886mainline air carrier passenger aircraft (jetswith more than 90 seats), 997 mainline aircarrier cargo aircraft, and 2,743 regional air-craft (smaller jets, turboprops, and pistons).

Based on carrier revenues, the largest do-mestic airline in 2006 was American Airlines,a unit of AMR Corp., which is also the largest

carrier in the world. American reported rev-enues for 2006 of $22.6 billion (which includ-ed its American Eagle unit). United Airlines, aunit of UAL Corp., took second place withrevenues of $19.3 billion. Delta Air Lines Inc.was in third place with $17.2 billion.

According to the US Department ofTransportation (DOT), the US airline indus-try (the majors, nationals, and regionals)generated total revenues of $163.8 billionin 2006, up 8.3% from $151.25 billion in2005. In terms of traffic, DOT statisticsshow that the US airline industry logged arecord 797.4 billion revenue passenger-miles(RPMs, the number of passengers multipliedby the number of miles flown) in 2006, sur-passing by 2.4% the prior year’s record of779.0 billion. Also setting records in 2006were enplanements (the total number of pas-sengers) at 744.5 billion and available seat-miles at 1,006.4 billion. Enplanements rose0.8% over 2005, while available seat-miles(ASMs, the number of seats in the active fleetmultiplied by the number of miles flown)were 0.3% higher than the prior year. Ameri-can (excluding its regional affiliates) tallied139.5 billion RPMs in 2006, followed byUnited with 117.5 billion RPMs and Deltawith 116.1 billion RPMs.

While the US industry has incurred theheaviest losses in recent years, airlinesaround the world have also faced a difficultenvironment. In 2006, the global airline in-dustry lost an estimated $500 million, asharp reduction from $6.0 billion in losses in2005 and a loss of $4.8 billion in 2004, ac-cording to the International Air TransportAssociation (IATA), a coalition made up ofsome 260 airlines throughout the world.From 2001 to 2003, the industry lost an esti-mated $37.6 billion, including a record lossof $18 billion in 2001, according to theIATA. For 2007, the IATA estimated on Sep-tember 17, 2007, that the industry wouldpost a profit of $5.6 billion.

INDUSTRY PROFILE

Airlines still face extreme challenges

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

9

AIRLINE MARKET SHARE LEADERS(Based on revenue passenger-miles)

% % 2007* MARKET 1997 MARKETRANK COMPANY SHARE RANK COMPANY SHARE

1. American 17.8 1. United 20.0 2. United 15.2 2. American 17.6 3. Delta 13.4 3. Delta 16.4 4. Northwest 9.4 4. Northwest 11.9 5. Southwest 9.3 5. Continental 7.9 6. US Airways 8.1 6. US Airways 6.9 7. Continental 6.9 7. Southwest 4.7 8. JetBlue 3.4 8. TWA 4.1 9. Alaska 2.4 9. America West 2.7

10. SkyWest 2.3 10. Alaska 1.7 11. AirTran 2.2 11. American Trans Air 1.5 12. American Eagle 1.4 12. Hawaiian 0.7 13. Frontier 1.3 13. Tower 0.6 14. Republic 1.1 14. Reno Air 0.5 15. Hawaiian 1.0 15. AirTran Holding 0.4

Others 4.8 Others 2.4 Totals may not add due to rounding. *8 months ending August.Source: US Department of Transportation.

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

10

INDUSTRY TRENDS

The US airline industry’s operating envi-ronment has finally recovered from five yearsof multibillion-dollar losses that began afterthe events of September 11, 2001, when fourUS commercial jetliners were hijacked for usein terrorist attacks on America. Passengerrevenues and passenger traffic have recov-ered from the sustained industry downturn,and the US industry returned to profitabilityin 2006. The impact of the high level of sus-tained losses on the US airline industry, alongwith the changes necessitated in how an air-line operates in the wake of 9/11, have hadlingering effects on the US airline industry. Inthe past, economic downturns have led tolarge industry losses, but none of those peri-ods posed as severe a threat to the industry’ssurvival as did the aftermath of the 9/11 at-tacks. In addition to the near-term disruptionto revenues and the large industry losses, theindustry has faced longer-term problems, in-cluding a liquidity crunch and a severelyweakened financial condition.

The impact of five years of multibillion-dollar losses

In the first few months after September2001, air travel dropped off dramatically. Asthe airlines’ losses mounted and availablecash was rapidly depleted, most carriers wereforced to shoulder new debt by tapping theircredit lines and/or issuing bonds. These ac-tions were vital to help the carriers survivethe dramatic decline in passenger levels andfares, as well as the sharp increase in losses,but they left most of the major airlines bur-dened with huge debt loads. Five years ofmultibillion-dollar losses led to the bankrupt-cy of five of the 10 largest major airlines andan increased debt burden for many of theothers.

The higher interest expense and the lowerinterest and investment income that resultedweakened the airlines’ earnings power. In ad-dition, weakened balance sheets limited car-riers’ ability to increase capital expenditures,add to their networks, and survive anotherdownturn. Thus, the effects of the recent fi-nancial deterioration are still playing out.One side effect of this has been the carriers’insistence on carrying sharply higher cashlevels than at anytime in the past in order to

allow it to survive any future shocks to thesystem. For example, AMR Corp. had a cashbalance of $5.9 billion, including restrictedcash, at the end of the second quarter of2007, versus cash levels of $1.3 billion at theend of the second quarter of 2001. Similarly,Continental Airlines had second quarter2007 cash levels of $3.2 billion, including re-stricted cash, versus $1.0 billion at the end ofthe second quarter of 2001.

Today, when investors are increasinglyworried about balance sheet stability afterthe collapse of such companies as EnronCorp., WorldCom Inc., and others, many air-lines have extremely high debt levels. For ex-ample, AMR Corp., parent company ofAmerican Airlines, ended 2006 with totaldebt (including current maturities) of $18.4billion and negative stockholders’ equity of$606 million. Delta Air Lines Inc. ended2004 with debt of $13.9 billion and a nega-tive stockholders’ equity of $5.8 billion; thecompany subsequently filed for bankruptcyon September 14, 2005. Before it filed forbankruptcy, Northwest Airlines Corp. alsohad negative stockholders’ equity. In con-trast, Southwest Airlines Co. — which Stan-dard & Poor’s believes has the healthiestbalance sheet among all US airlines — had$1.7 billion in debt (including current matu-rities) and $6.4 billion in stockholders’ equi-ty at year-end 2006, for a debt-to-totalcapital ratio of 21% (excluding operatingleases).

Airlines struggle to survive

In today’s environment, the legacy majorcarriers face intense pressure to changecost structures and operational strategies.Delta and Northwest both filed for bank-ruptcy in September 2005. Delta emerged onApril 30, 2007, and Northwest emerged on May 31, 2007. UAL Corp., the parentcompany of United Airlines, filed for bank-ruptcy in December 2002, marking thelargest bankruptcy filing in the history of theUS aviation industry. UAL emerged frombankruptcy in February 2006. UAL was thesecond major US airline company to file forChapter 11 protection in 2002, following USAirways Group Inc. US Airways subsequent-ly emerged from bankruptcy, reentered it,and finally emerged again in September2005, after merging with America West

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

11

Holdings Corp. ATA Holdings Corp., parentof ATA Airlines (the tenth largest US airlineat the time), filed for bankruptcy protectionin October 2004; the company emerged frombankruptcy in February 2006. (See the “Cur-rent Environment” section of this Survey forfurther discussion of this topic.)

Federal grants, loan guarantees bailed out industry

After fierce lobbying by the airline indus-try, which contended that costs of the war inIraq and government-mandated security mea-sures were harming the industry, PresidentGeorge W. Bush signed the EmergencyWartime Supplemental Appropriations Act onApril 16, 2003. Under the law, the Trans-portation Security Administration (TSA) dis-bursed pretax payments totaling $2.29 billionin May 2003. This money was intended to re-imburse carriers for the security fees that theyhad paid to the TSA since February 2002.Congress set aside an additional $100 millionto compensate airlines for reinforcing airlinecockpit doors. Because of the cash grants,most of the top 10 carriers reported a profitin the second quarter of 2003 and were ableto sharply curtail net losses for the full year.

The cash grants in May 2003 representedthe second round of bailouts to the airline in-dustry. On September 22, 2001, PresidentBush signed into law the Air TransportationSafety and System Stabilization Act, whichwas intended to compensate the airlines fordirect and indirect losses associated with theterrorist attacks in September 2001. Includedin the plan was $5 billion in direct cashgrants to be distributed to carriers based ontraffic and the possible granting of $10 bil-lion in industry loan guarantees.

Will merger activity pick up?The merger in September 2005 of bank-

rupt US Airways with America West Hold-ings Corp., which created the new USAirways, could have been the start of a newfocus on mergers in the US airline industry.However, US Airways’ subsequent attempt tomerge with Delta Air Lines was blocked byDelta, which successfully argued to its credi-tors that Delta’s own standalone plan wouldcreate more value for creditors and otherstakeholders. (See the “Current Environ-ment” section of this Survey for further dis-cussion of this topic.)

Before the US Airways merger, there hadbeen no significant merger and acquisitionactivity in the US airline industry since theUS Department of Justice (DOJ) blocked theproposed combination of US Airways andUnited Airlines in July 2001. That deal wasblocked because the DOJ felt it would havegiven United too large a share in too manymarkets. Both carriers eventually ended up inbankruptcy court.

Standard & Poor’s thinks that the mergerof America West and US Airways, in con-junction with the increase of private equityleveraged buyout deals in the US over thepast two years, is likely to have led to in-creased interest in potential mergers in theairline industry. Whether this translates intoany actual consolidation, however, remainsto be seen. The industry’s overcapacity, com-bined with many carriers’ weakened balancesheets and high debt levels, remain as signifi-cant barriers to major airline mergers.

Indeed, many of the carriers that wouldtraditionally do the acquiring are not in aposition to finance mergers. We expect thelargest carriers to continue to shrink capaci-ty, conserve cash, and try to restore prof-itability before chasing market share gains.Still, we no longer think it is out of the ques-tion for one of the smaller carriers to besnapped up by Southwest or another lower-cost carrier with the financial resources tomake a deal. We also think a combination ofmajor airlines that includes one of the carri-ers in bankruptcy, or one that recentlyemerged from bankruptcy, like UAL Corp., isa possibility.

US Airways merger with America West creates the fifth largest US carrier

On September 27, 2005, US Airways,then the seventh largest US carrier, completedits merger with America West Holdings, theparent company of America West Airlines(eighth largest). America West was the sur-viving company in the merger, but it adoptedthe corporate name US Airways Group Inc.

The combined company, now the fifthlargest US airline, started out with about$2.5 billion in cash, 38,000 employees, and anetwork that offers about 2,700 flights, serv-ing 233 destinations from major hubs inPhoenix, Charlotte, and Philadelphia, withsecondary hubs in Las Vegas, Pittsburgh,Boston, New York (LaGuardia), and Wash-

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

12

ington, D.C. (Reagan National). Under Fed-eral Aviation Administration safety and otherregulations, the two companies have contin-ued to fly separately (for a period of abouttwo years), but they immediately combinedscheduling and other operations.

Standard & Poor’s thinks that the mergerhas been a success, as the new US Airways hassharply cut costs and has achieved many of itsrevenue and cost synergy targets. We think thecombined carrier is financially stronger theneither carrier was on a standalone basis, andit should be better equipped to handle thenext industry downturn, when it occurs.

In our view, it is favorable that the mergercombined a carrier with too much of its routenetwork locked on the East Coast (US Air-ways) with a highly West Coast–centric airline(America West) to form an airline with a

more diversified geographic footprint acrossthe United States. In addition, US Airways, inbankruptcy, had already done a lot of thehard work of cutting costs and eliminating itspension plan; as a result, its overall cost struc-ture was close to that of America West. Final-ly, the merger attracted more capital — bothnew equity and new debt financing — thanthe company had expected.

US Airways originally filed for bankrupt-cy protection on August 11, 2002, despitehaving gained concessions from its workforce and conditional approval of a loanguarantee of $900 million from the AirTransportation Stabilization Board (ATSB).After emerging from that bankruptcy filingon March 18, 2003, the carrier continued tohave a higher cost structure than its peers,and it experienced large losses. External fac-

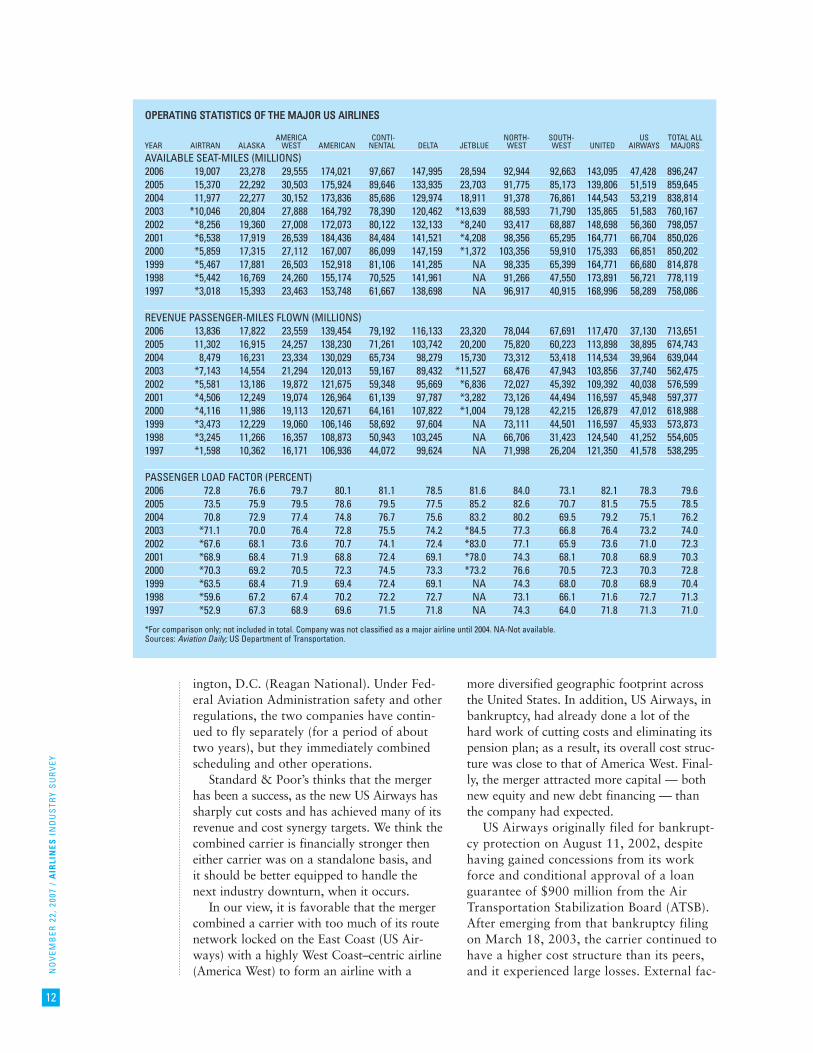

OOPPEERRAATTIINNGG SSTTAATTIISSTTIICCSS OOFF TTHHEE MMAAJJOORR UUSS AAIIRRLLIINNEESS

AMERICA CONTI- NORTH- SOUTH- US TOTAL ALL YEAR AIRTRAN ALASKA WEST AMERICAN NENTAL DELTA JETBLUE WEST WEST UNITED AIRWAYS MAJORS

AVAILABLE SEAT-MILES (MILLIONS)2006 19,007 23,278 29,555 174,021 97,667 147,995 28,594 92,944 92,663 143,095 47,428 896,247 2005 15,370 22,292 30,503 175,924 89,646 133,935 23,703 91,775 85,173 139,806 51,519 859,645 2004 11,977 22,277 30,152 173,836 85,686 129,974 18,911 91,378 76,861 144,543 53,219 838,814 2003 *10,046 20,804 27,888 164,792 78,390 120,462 *13,639 88,593 71,790 135,865 51,583 760,167 2002 *8,256 19,360 27,008 172,073 80,122 132,133 *8,240 93,417 68,887 148,698 56,360 798,057 2001 *6,538 17,919 26,539 184,436 84,484 141,521 *4,208 98,356 65,295 164,771 66,704 850,026 2000 *5,859 17,315 27,112 167,007 86,099 147,159 *1,372 103,356 59,910 175,393 66,851 850,202 1999 *5,467 17,881 26,503 152,918 81,106 141,285 NA 98,335 65,399 164,771 66,680 814,878 1998 *5,442 16,769 24,260 155,174 70,525 141,961 NA 91,266 47,550 173,891 56,721 778,119 1997 *3,018 15,393 23,463 153,748 61,667 138,698 NA 96,917 40,915 168,996 58,289 758,086

REVENUE PASSENGER-MILES FLOWN (MILLIONS)2006 13,836 17,822 23,559 139,454 79,192 116,133 23,320 78,044 67,691 117,470 37,130 713,651 2005 11,302 16,915 24,257 138,230 71,261 103,742 20,200 75,820 60,223 113,898 38,895 674,743 2004 8,479 16,231 23,334 130,029 65,734 98,279 15,730 73,312 53,418 114,534 39,964 639,044 2003 *7,143 14,554 21,294 120,013 59,167 89,432 *11,527 68,476 47,943 103,856 37,740 562,475 2002 *5,581 13,186 19,872 121,675 59,348 95,669 *6,836 72,027 45,392 109,392 40,038 576,599 2001 *4,506 12,249 19,074 126,964 61,139 97,787 *3,282 73,126 44,494 116,597 45,948 597,377 2000 *4,116 11,986 19,113 120,671 64,161 107,822 *1,004 79,128 42,215 126,879 47,012 618,988 1999 *3,473 12,229 19,060 106,146 58,692 97,604 NA 73,111 44,501 116,597 45,933 573,873 1998 *3,245 11,266 16,357 108,873 50,943 103,245 NA 66,706 31,423 124,540 41,252 554,605 1997 *1,598 10,362 16,171 106,936 44,072 99,624 NA 71,998 26,204 121,350 41,578 538,295

PASSENGER LOAD FACTOR (PERCENT)2006 72.8 76.6 79.7 80.1 81.1 78.5 81.6 84.0 73.1 82.1 78.3 79.6 2005 73.5 75.9 79.5 78.6 79.5 77.5 85.2 82.6 70.7 81.5 75.5 78.5 2004 70.8 72.9 77.4 74.8 76.7 75.6 83.2 80.2 69.5 79.2 75.1 76.2 2003 *71.1 70.0 76.4 72.8 75.5 74.2 *84.5 77.3 66.8 76.4 73.2 74.0 2002 *67.6 68.1 73.6 70.7 74.1 72.4 *83.0 77.1 65.9 73.6 71.0 72.3 2001 *68.9 68.4 71.9 68.8 72.4 69.1 *78.0 74.3 68.1 70.8 68.9 70.3 2000 *70.3 69.2 70.5 72.3 74.5 73.3 *73.2 76.6 70.5 72.3 70.3 72.8 1999 *63.5 68.4 71.9 69.4 72.4 69.1 NA 74.3 68.0 70.8 68.9 70.4 1998 *59.6 67.2 67.4 70.2 72.2 72.7 NA 73.1 66.1 71.6 72.7 71.3 1997 *52.9 67.3 68.9 69.6 71.5 71.8 NA 74.3 64.0 71.8 71.3 71.0

*For comparison only; not included in total. Company was not classified as a major airline until 2004. NA-Not available.Sources: Aviation Daily; US Department of Transportation.

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

13

tors exacerbated the company’s difficulties:the industry environment worsened further,with high oil prices, overcapacity, and de-pressed airfares. On September 14, 2004,US Airways filed for bankruptcy for thesecond time in three years, where it stayeduntil the merger with America West wascompleted.

Security costs rise

Since the terrorist strikes in 2001, a num-ber of federally mandated security measureshave been put into effect — both to reassurethe flying public and to prevent future occur-rences. Although the government has subsi-dized the added security costs and provided a$2.3 billion cash grant in 2003, the industrywill continue to bear significant ongoing se-curity costs.

Airlines are now required to either screenall bags for explosives or make sure each bagis matched to a passenger seated on thatflight. Both are time-consuming and expen-sive initiatives.

The new security measures have made flyingless convenient for travelers. The increased se-curity measures and new baggage checking re-quirements mean longer lines at airports, bothto check in and to pass through security. Mostairlines, though, have done a good job of re-ducing wait times by adding security lanes.

Start-ups: many fail, a few thrive

The US airline industry historically hasseemed to attract funding for new start-ups,even though the failure rate for these compa-nies is high. The airline business is notoriousfor profit volatility, and the problems facedby start-ups have been exacerbated in the af-termath of September 2001, as large lossesand lower traffic levels have tested their stay-ing power.

New carriers are more likely to pursueniche markets or regional service agreementsthan to go head-to-head against a major air-line, since they cannot offer the same fre-quency of flights. If start-ups offer deeplydiscounted fares, the major airlines willmatch the fares, while maintaining high fareson all noncompeting flights.

Overall, the current crop of low-fare,start-up carriers has not proven to be bettermanaged or capitalized than its predecessors.

One major exception is JetBlue AirwaysCorp., which we think is the biggest threat toindustry price stability since Southwest Air-lines entered the business in 1971. JetBlue

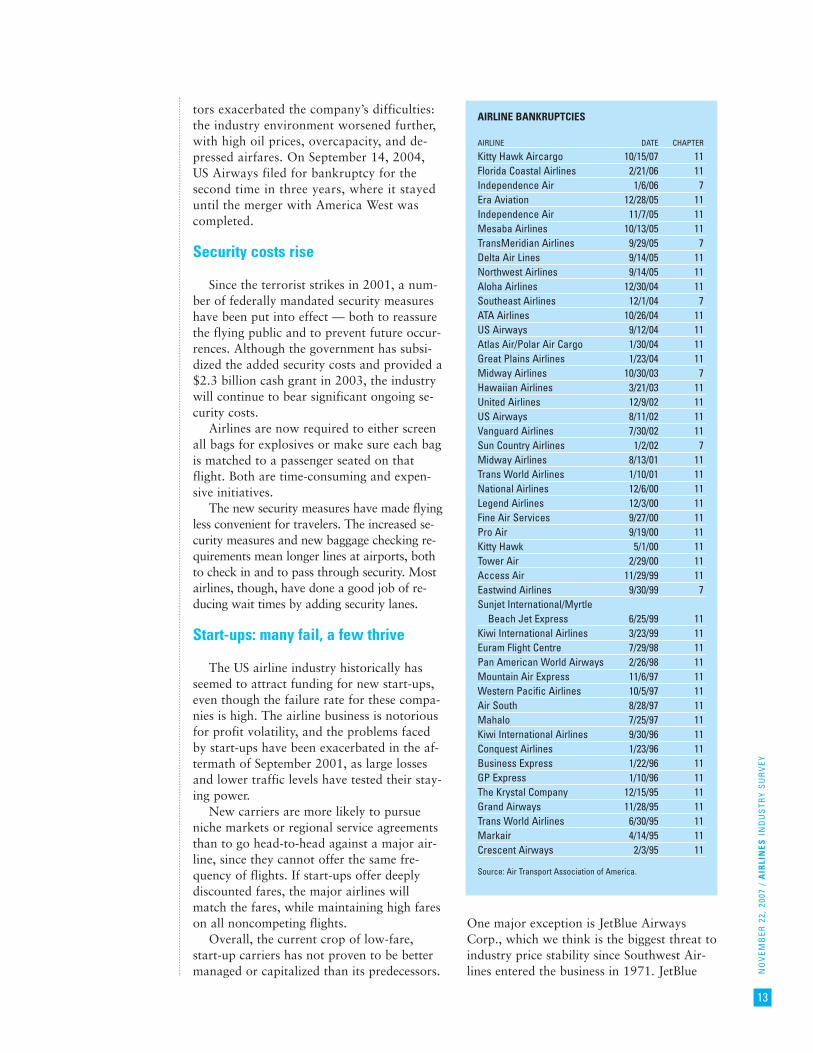

AIRLINE BANKRUPTCIES

AIRLINE DATE CHAPTER

Kitty Hawk Aircargo 10/15/07 11Florida Coastal Airlines 2/21/06 11Independence Air 1/6/06 7Era Aviation 12/28/05 11Independence Air 11/7/05 11Mesaba Airlines 10/13/05 11 TransMeridian Airlines 9/29/05 7 Delta Air Lines 9/14/05 11 Northwest Airlines 9/14/05 11 Aloha Airlines 12/30/04 11 Southeast Airlines 12/1/04 7 ATA Airlines 10/26/04 11 US Airways 9/12/04 11 Atlas Air/Polar Air Cargo 1/30/04 11 Great Plains Airlines 1/23/04 11 Midway Airlines 10/30/03 7 Hawaiian Airlines 3/21/03 11 United Airlines 12/9/02 11 US Airways 8/11/02 11 Vanguard Airlines 7/30/02 11 Sun Country Airlines 1/2/02 7 Midway Airlines 8/13/01 11 Trans World Airlines 1/10/01 11 National Airlines 12/6/00 11 Legend Airlines 12/3/00 11 Fine Air Services 9/27/00 11 Pro Air 9/19/00 11 Kitty Hawk 5/1/00 11 Tower Air 2/29/00 11 Access Air 11/29/99 11 Eastwind Airlines 9/30/99 7 Sunjet International/Myrtle

Beach Jet Express 6/25/99 11 Kiwi International Airlines 3/23/99 11 Euram Flight Centre 7/29/98 11 Pan American World Airways 2/26/98 11 Mountain Air Express 11/6/97 11 Western Pacific Airlines 10/5/97 11 Air South 8/28/97 11 Mahalo 7/25/97 11 Kiwi International Airlines 9/30/96 11 Conquest Airlines 1/23/96 11 Business Express 1/22/96 11 GP Express 1/10/96 11 The Krystal Company 12/15/95 11 Grand Airways 11/28/95 11 Trans World Airlines 6/30/95 11 Markair 4/14/95 11 Crescent Airways 2/3/95 11

Source: Air Transport Association of America.

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

14

initiated service out of New York City’s JohnF. Kennedy International Airport in February2000. The carrier is well capitalized, usesbrand-new jets, and, since its launch, hasgenerated high load factors on its point-to-point route structure. However, rising fuelprices and intense price competition led to aloss for the carrier in 2005 and 2006, thoughStandard & Poor’s predicts a modest returnto profitability for the carrier in 2007.

Recent failuresAmong recent airline failures, Indepen-

dence Airlines — a regional airline that wasoriginally a regional partner of United Air-lines before trying to compete against Unit-ed and the other majors — filed for Chapter 7liquidation on January 6, 2006, after aprevious Chapter 11 filing on November 7,2005. Mesaba Airlines, a regional airlinethat operates as a Northwest connectioncarrier, filed for bankruptcy on October 13,2005, shortly after Northwest failed tomake certain financial payments to Mesabaand announced severe cutbacks in its con-tract with the company. Transmeridian Air-lines, a small charter airline operating outof about a dozen cities, filed for Chapter 7liquidation on September 29, 2005.

Aloha Airlines filed for Chapter 11 pro-tection on December 30, 2004, but emergedon February 17, 2006. ATA Holdings, parentcompany of ATA Airlines, filed for Chapter11 protection on October 26, 2004; at thetime, ATA was the tenth largest US airline.The carrier emerged from Chapter 11 protec-tion on February 28, 2005. Hawaiian Air-lines Inc., a subsidiary of Hawaiian HoldingsInc., filed for Chapter 11 bankruptcy protec-tion on March 21, 2003; the carrier emergedfrom bankruptcy on June 2, 2005. (See the“Airline bankruptcies” table for a larger list.)

Small jets create opportunities in regional markets

Regional jets — small jet planes that flyshorter distances and have fewer seats than dolarge mainline jets — were first introduced inthe late 1980s. The first airline to embrace theregional jet was Comair Inc. (now whollyowned by Delta). Demand for these planes be-gan to take off about 1995, when Brazil’s Em-braer-Empresa Brasileira de Aeronáutica SAand Canada’s Bombardier Inc. introduced low-

cost jet planes, with 50 to 70 seats, for $15million to $20 million each.

Regional jets open new marketsThe regional jet has stimulated air travel

over shorter segments by getting people outof cars, buses, and trains and onto planes.With its low purchase price and operatingcosts, the regional jet has transformed short-haul markets, previously abandoned by ma-jor airlines, into viable destinations. Theregional jet also offers greater range and pas-senger comfort than does the turbopropplane. It can handle routes of 1,300 miles —up to 2,300 nautical miles in some cases —while most propeller planes are confined toflights of 350 miles or less.

Major airlines’ regional affiliates use thesesmall jets to provide off-peak service when de-mand is insufficient to warrant a standard100-plus seat aircraft. Regional jets can beprofitable for such service because theirbreak-even can approach a 50% level, versusa much higher load factor — historicallyabout 65%, but in the past few years, closerto 85% — needed for large jets in a normalindustry environment. By offering round-the-clock service in this manner, an airline gainsappeal among business travelers, who accountfor some 70% of regional jet passengers.

With regional jets gaining in range, theyare increasingly being used not only to feedpassengers into hub airports, but also to pro-vide point-to-point competition against carri-ers employing full-sized jets.

Regional airlines and majors have a symbiotic relationship

Given the severe financial trouble thatthe US airline industry has faced in the pastfew years, many of the major carriers havebeen forced to sell or reduce their invest-ments in regional airlines in order to raisecash. Notably, in September 2005, Deltasold its regional subsidiary, Atlantic South-east Airlines, to SkyWest Airlines in orderto raise cash. Continental Airlines Inc.gradually sold its stake in ExpressJet Hold-ings Inc., which was once wholly owned byContinental. In 2003, Northwest con-tributed the stock of one of its regional air-line subsidiaries, Pinnacle Airlines, to itspension plan to offset plan liabilities.

The relationship between the major andregional airlines is reciprocal. The majors

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

15

cannot rely solely on their own expensiveaircraft and crews to gather passengers tofeed into their hubs. The regionals dependon major carriers to provide connectingflights at central hub airports for up to60% of their passengers. The major airlinesalso provide credibility, worldwide market-ing power, and the all-important designatorcode in the computer reservation system(CRS). To be successful, regional and majorairlines must work as a seamless operationusing a single system for booking andboarding.

According to the Regional Airline Associ-ation, a trade group representing smaller air-lines, about 70 regional airlines were inoperation in 2005 (latest available). BackAviation Solutions, a provider of consultingand data information services to the aviationindustry, predicts that no more than 50 re-gional carriers will exist by 2010.

At the same time, the overall number ofregional jets in operation should continue torise sharply. The Federal Aviation Adminis-tration (FAA) predicts that the US regionalaircraft fleet (both jets and turboprops) willreach 3,851 by 2017, up from 2,862 as ofDecember 31, 2005. Although many of thenew regional jets on order are intended to re-place older turboprops, the large number ofincoming jets should lead to an overall in-crease in the number of regional aircraft inservice.

Labor contracts restrict use of regional jetsAll pilot contracts have “scope” clauses,

which establish the definition (or scope) ofpilots’ jobs, and dictate who may or may notperform those jobs. Scope clauses in manyexisting labor contracts severely limit theability of some airlines to participate in theregional jet market boom. American Airlines,for instance, can fly an unlimited number ofregional jets with 45 seats or less, but can flya maximum of 67 jets with 45 to 70 seats.

Many observers see the biggest emergingsegment of the regional jet market in 70- to100-seat aircraft, which began rolling off theassembly lines in 2002. Bombardier and Em-braer are the two main manufacturers ofthese regional jets. Pilots at mainline carriers,who make substantially higher salaries thanthose at regional operators, have seen manyof their routes displaced by regional affiliatesoperating these larger jets.

Embracing the Internet...

The Internet has had a profound effect onthe way airlines price and distribute theirproduct. By selling tickets online, airlineshave dramatically cut distribution costs byeliminating paper shuffling, bypassing agents,and reducing airline staff. On the otherhand, the Internet has led to more competi-tive pricing.

Since 1995, carriers have had home pageson the World Wide Web. Initially, these sitesdisplayed schedule and fleet information, aswell as promotional material. Today, travel-ers can use these sites to check the status oftheir frequent-flyer accounts, and more im-portantly, to book flights and select seats.

Online travel operations, such as ExpediaInc., Travelocity.com LP, and Orbitz Inc.,have taken significant market share from tra-ditional travel agents. Despite the Internet’scommercial success in this market, accuratemeasurements of the amount of air travel be-ing booked online are hard to come by. Ac-cording to PhoCusWright, an independenttravel tourism and hospitality industry re-search firm, online travel sales will accountfor about 52% of all bookings in 2007, sur-passing offline bookings for the first time. In2007, according to eMarketer, an Internetmarket research and trend analysis firm, USonline travel sales will total $94 billion, ris-ing 19% over 2006.

...to help cut costsIn 1995, Alaska Airlines (a unit of Alaska

Air Group Inc.) became the first airline to al-low tickets to be booked via the Internet.Alaska booked about 39% of its tickets on itsown Web site in 2006. The company hassince been surpassed by many of its competi-tors, particularly discounters like JetBlue,whose strategy is to keep costs low throughextensive use of its own Web site and reserva-tion agents. JetBlue, which is now considereda major airline, leads all majors in bookingsover the Internet. In 2006, JetBlue booked79% of its sales on its own Web site.

Most US airlines now get a significantportion of revenues from online bookings.Southwest Airlines obtained 70% of its rev-enues from sales through its own Web site in2006. Continental Airlines, a former laggardin online bookings, got about 24% of its rev-enues in 2006 from its own Web site.

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

16

The Internet’s appeal for airlines is appar-ent. A commercial Web site can be kept openfor business 24 hours a day, seven days aweek. It allows an airline to reduce the num-ber of customer service agents, since fewersuch employees are needed to answer flightinformation questions. Southwest Airlines re-ported in 2002 that its Internet bookingscost about one dollar to make, while its costto book with a travel agent was between $6and $8. Tickets booked through Southwest’sown agents cost several dollars.

Indeed, a big incentive for airlines to dis-tribute tickets via the Internet is to reducetravel agent commissions. In 2002, US air-lines cut base commission rates entirely ondomestic flights (as discussed in the “Howthe Industry Operates” section of this Sur-vey). Recent cuts in commission rates and in-creased Internet sales are the major reasonsfor the trend toward lower commission costs.

On the down side, however, the Internetmay ultimately hurt airline profitability bymaking travelers too price-sensitive. Withairfares changing at lightning speed and theInternet keeping customers apprised of thesechanges, airlines must respond quickly tomatch rivals’ fare cuts. Consequently, therange of fares that competing airlines cancharge on a point-to-point route will tend tobe extremely compressed. In addition, thepremium charged for travel booked on shortnotice has eroded. Airlines cannot use busi-ness travel as effectively to subsidize dis-counted pleasure travel, now that businesstravelers can make low-price, near-term trav-el arrangements online.

E-tickets reduce costsEver on the lookout to cut costs, airlines

have enthusiastically embraced “ticketlesstravel” — the practice of issuing electronictickets (e-tickets) to customers. E-tickets arebooked in the usual manner — online,through a travel agent, or directly throughthe airline — but no paper ticket is issued.Instead, passengers are issued an e-ticketnumber. They can print boarding passes athome, obtain boarding passes at the airportcheck-in counter, or get them from an auto-mated dispensing machine, which is activatedwith a credit card, frequent-flyer card, or e-ticket number.

According to United Airlines, electronicticketing eliminates 14 accounting and pro-

cessing procedures and thus costs just 50cents per ticket, versus $8 for paper. Much ofthe savings comes from not having to mailactual tickets. Travelers can get a receipt anditinerary via fax or e-mail, or at the airport.E-tickets are now the norm: Standard &Poor’s estimates that they accounted forabout 96% of tickets sold in 2006.

Improving serviceMany travelers appreciate the speed of air

travel. However, the process leaves much tobe desired, with long lines to check in andobtain boarding passes, and frequent delaysor cancellations of flights. Conditions wors-ened when the airlines had to instituteheightened security measures.

Technology has helped with some of theseproblems. For example, many airlines’ pas-sengers can skip the boarding pass counterby printing their own documents throughtheir personal computers. In addition, agrowing number of airlines have installedhundreds of self-service kiosks that allowpassengers to check in luggage, obtain board-ing passes, and check their frequent-flyercredits. Such kiosks have been around in oneform or another since 1995.

International markets provide growth

Particularly in light of the brutal competi-tion in the US domestic market, many USairlines see international markets as an av-enue for profitable growth. For US-based air-lines, international revenue passenger-miles(RPMs) and enplanements climbed at com-pound annual growth rates of 4.3% and2.7%, respectively, between 1993 and 2000,versus 5.3% and 4.5% growth for domestictravel. However, along with the domestic USmarket, international travel slowed after Sep-tember 11, 2001.

International enplanements declined 6.3%in 2001, then another 0.2% in 2002 and1.8% in 2003. In 2004, however, internationalenplanements increased 13.9%, breaking thedownward trend and outpacing domesticgrowth (domestic enplanements rose 4.8% thatyear). International enplanements increased9.4% in 2005 and 6.8% in 2006; in both 2005and 2006, international enplanements out-paced growth in domestic enplanements.

To compete effectively for internationaltraffic, airlines need a level playing field.

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

17

This requires the enactment of “open skies”aviation treaties: bilateral agreements that re-duce economic regulation of airlines and al-low code sharing, alliances, and partialownership deals among international carri-ers. However, domestic routes in the UnitedStates and overseas remain closed to foreigncompetition. The practice of “cabotage” —the transport of passengers by a foreign car-rier for purely domestic flights — is illegal inall nations.

Since the late 1970s, the US governmenthas favored deregulation of international avi-ation markets. Because domestic carriers suf-fered heavy losses following US deregulation,the government did not pursue open skiespolicies until the early 1990s. In the past fewyears, the government has been pursuingopen skies treaties aggressively. Most no-tably, on March 23, 2007, the US signed anopen skies agreement with the EuropeanUnion; this agreement, scheduled to go intoeffect in March 2008, supersedes individualopen skies treaties with individual Europeannations. (For more details, see the “CurrentEnvironment” section of this Survey.)

The world’s first open skies pact wasreached in 1992 between the United Statesand the Netherlands. By November 2006,some 77 nations had signed agreements withthe United States. Not all of these aviationpacts provide for unfettered competition, butall move strongly in that direction, providingfor phased-in deregulation.

Global partneringInternational alliances are crucial to

achieving profits on many internationalroutes. Having a global partner that feedstraffic through a hub generates numerousbenefits. By facilitating smoother connectionsand stimulating traffic, an alliance can help acarrier to dramatically lower its costs, cutfares, and increase flight frequency, withoutrequiring substantial investment in additionalaircraft, airport facilities, or route authority.

Alliance partners realize cost savings inseveral ways: by sharing cargo and passengerterminal facilities; integrating frequent-flyerprograms; consolidating sales, maintenance,and administrative operations; combining in-formation technologies; coordinating adver-tising; and engaging in joint procurementwhere feasible. Alliances are currently struc-tured so that partners remain independent

entities, but with coordinated schedules andcombined frequent-flyer programs.

Alliances aid airlines abroadThere are currently three major global

airline alliances: Star Alliance, anchored byUnited Airlines and Deutsche LufthansaAG (which also includes US Airways);OneWorld, with American Airlines andBritish Airways PLC; and SkyTeam, withDelta, Continental, Northwest, Air France-KLM SA, and Royal Dutch Airlines. Eachalliance also involves several secondarycarriers. For now, Star remains the biggestalliance, with over 16,000 daily departuresto 855 airports as of May 2007.

HOW THE INDUSTRY OPERATES

Few inventions have had as profound aninfluence on the way people live, work, andexperience the world as the airplane. Byshortening travel time from weeks to hours,air travel has altered our concept of distance.The world has become smaller, as people canvisit and conduct business in places onceconsidered far-flung.

The transformation of the Wright broth-ers’ early twentieth-century invention from anovelty to a commercial industry requiredconsiderable technological refinements andgovernment assistance. Until the 1920s, theairplane was envisioned principally as a mili-tary tool. That view broadened in 1925,when airplanes began carrying mail. Withthe passage of the Air Commerce Act of1926, the US airport and air traffic controlinfrastructure began to take shape.

To promote the then-fledgling passengertravel industry, the Watres Act of 1930changed the airmail fee structure: fees paidto air carriers to move mail were increasedexpressly to subsidize passenger service. Fur-thering the cause of air travel was the intro-duction in the United States of the jet aircraftfor passenger service in 1958. With greaterseating capacity and faster speeds, the jetdramatically cut operating costs and thus fa-cilitated lower fares.

The industry was deregulated in 1978,freeing it from government control of fares,routes, merger and acquisition activity, andalliances. This step helped to complete thetransformation of air travel from a luxury to

NO

VEM

BER

22,

200

7 /

AIR

LIN

ES I

ND

US

TRY

SU

RV

EY

18

a mass-market service. Government involve-ment is still evident in controls over interna-tional routes, however, and the US Depart-ment of Justice (DOJ) has halted some merg-er attempts, as discussed in the “IndustryTrends” section of this Survey.

Providing transportation