Embed Size (px)

Citation preview

Salzburg Global Seminar

27 September – Salzburg, Austria

Sovereign Development

Funds and the Shifting

Wealth of Nations

Javier Santiso

Director and Chief Economist

OECD Development Centre

OECD Development Centre

A fundamental shift

• Emerging economies are returning to their historical position in the global economy - a rebalancing of the wealth of nations.

• “Decoupling” is no longer an appropriate concept, since the Centre is no longer the Centre, and the Periphery no longer Periphery.

• Sovereign Wealth Funds are at the heart of this process.

Joaquín Torres García

América Invertida, 1943

OECD Development Centre

Sovereign Wealth Funds in the global shifting of wealth1

New investment drivers in the emerging world2

Sovereign Development Funds?3

OECD Development Centre

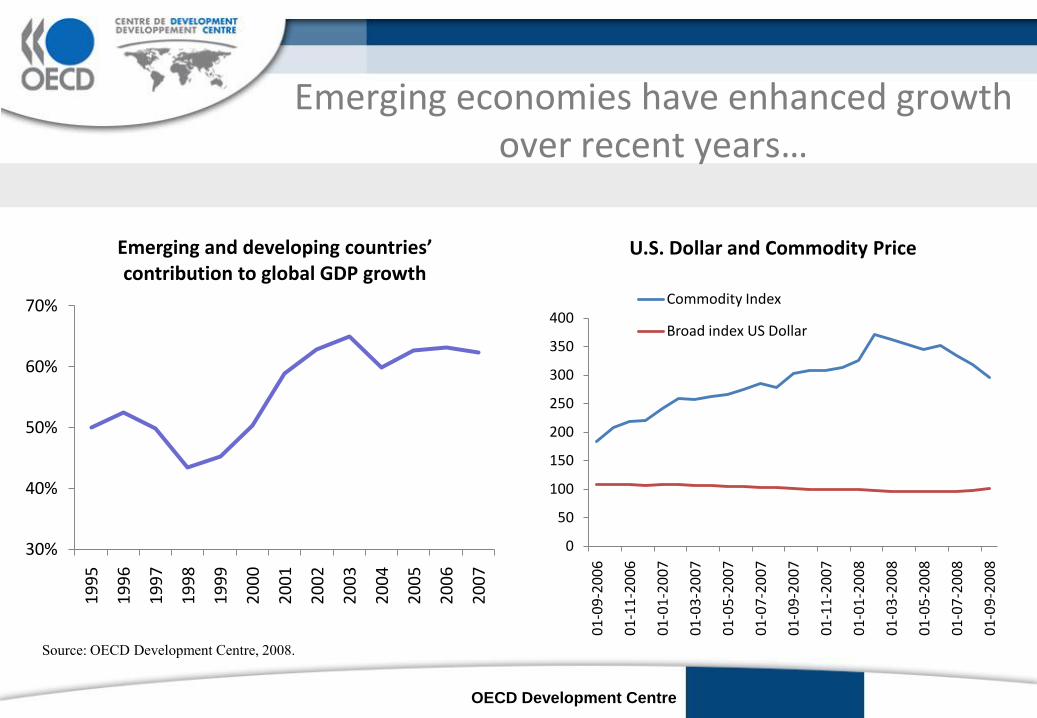

Emerging economies have enhanced growth over recent years…

30%

40%

50%

60%

70%

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

Emerging and developing countries’ contribution to global GDP growth

Source: OECD Development Centre, 2008.

0

50

100

150

200

250

300

350

400

01

-09

-20

06

01

-11

-20

06

01

-01

-20

07

01

-03

-20

07

01

-05

-20

07

01

-07

-20

07

01

-09

-20

07

01

-11

-20

07

01

-01

-20

08

01

-03

-20

08

01

-05

-20

08

01

-07

-20

08

01

-09

-20

08

U.S. Dollar and Commodity Price

Commodity Index

Broad index US Dollar

OECD Development Centre

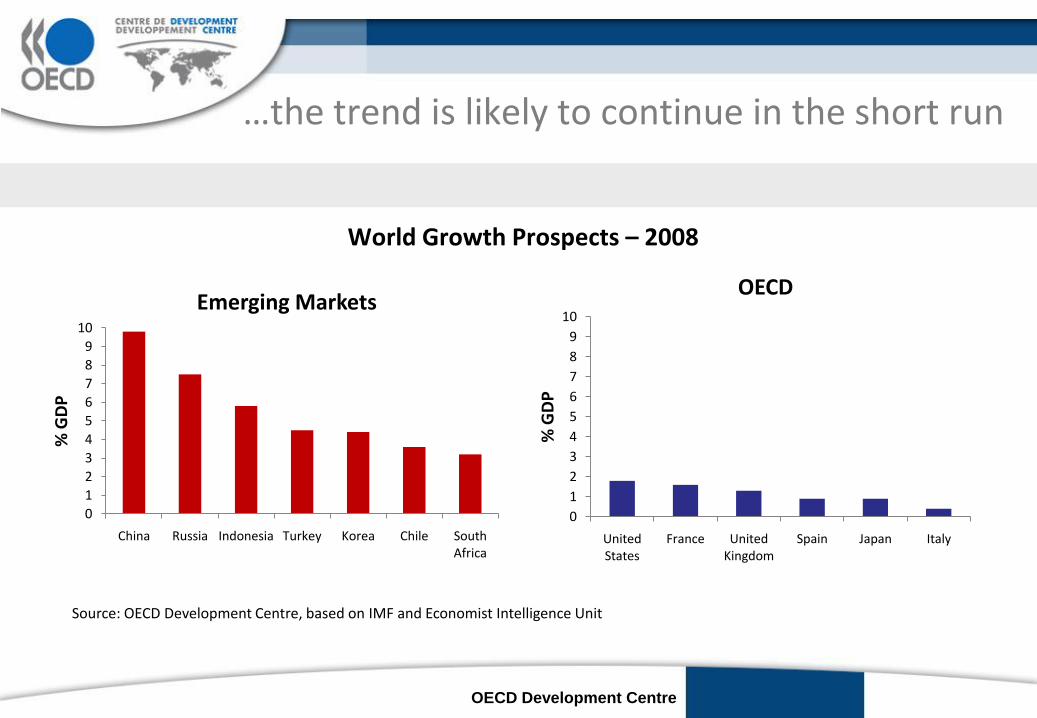

World Growth Prospects – 2008

0

1

2

3

4

5

6

7

8

9

10

China Russia Indonesia Turkey Korea Chile South Africa

% G

DP

Emerging Markets

0

1

2

3

4

5

6

7

8

9

10

United States

France United Kingdom

Spain Japan Italy%

GD

P

OECD

Source: OECD Development Centre, based on IMF and Economist Intelligence Unit

…the trend is likely to continue in the short run

OECD Development Centre

Emerging markets continue to accumulate foreign reserves…

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

US

D b

illi

on

International reserves emerging countries

Brazil

China

India

Mexico

Russia

South Africa

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

US

D b

illi

on

International reservesDeveloped countries

Germany

France

Netherlands

Switzerland

UK

US

Source: OECD Development Centre, based on Economist Intelligence Unit

OECD Development Centre

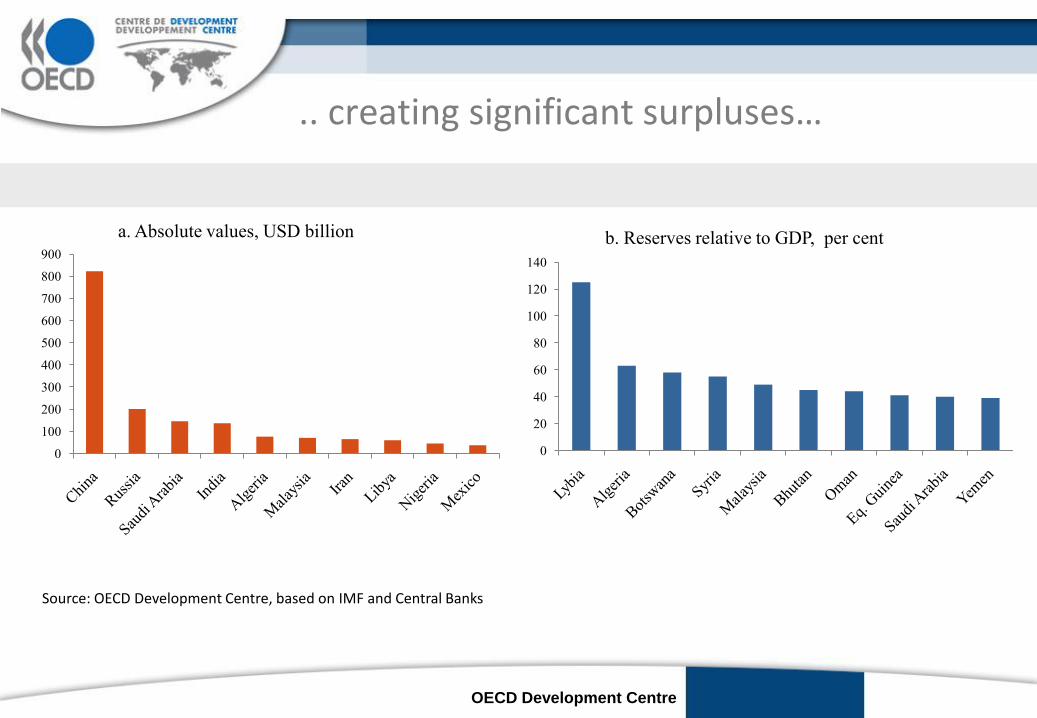

.. creating significant surpluses…

0

100

200

300

400

500

600

700

800

900

a. Absolute values, USD billion

0

20

40

60

80

100

120

140

b. Reserves relative to GDP, per cent

Source: OECD Development Centre, based on IMF and Central Banks

OECD Development Centre

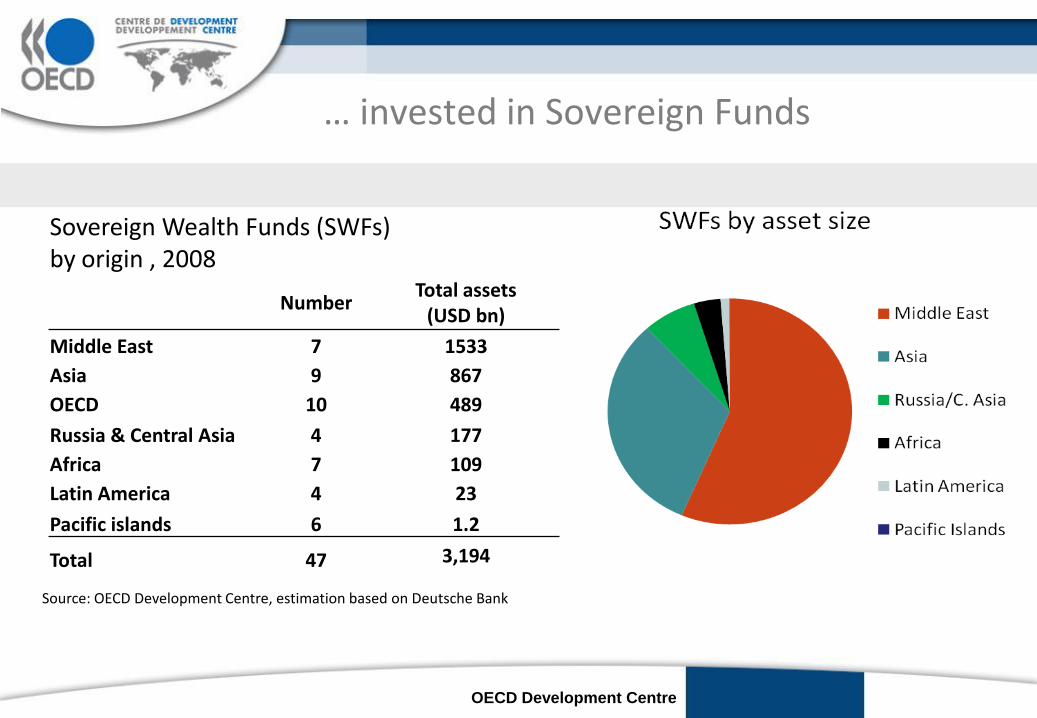

… invested in Sovereign Funds

Sovereign Wealth Funds (SWFs) by origin , 2008

NumberTotal assets

(USD bn)

Middle East 7 1533

Asia 9 867

OECD 10 489

Russia & Central Asia 4 177

Africa 7 109

Latin America 4 23

Pacific islands 6 1.2

Total 47 3,194

Source: OECD Development Centre, estimation based on Deutsche Bank

OECD Development Centre

Sovereign wealth funds in the global shifting of wealth1

New investment drivers in the emerging world2

Sovereign Development Funds?3

OECD Development Centre

Source: OECD Development Centre 2007, based on Thomson Datastream (Economist Intelligence Unit).

Note: Emerging countries refer to Latin American and Asian only.

Emerging economies have become major actors in mobilising capital

OECD Development Centre

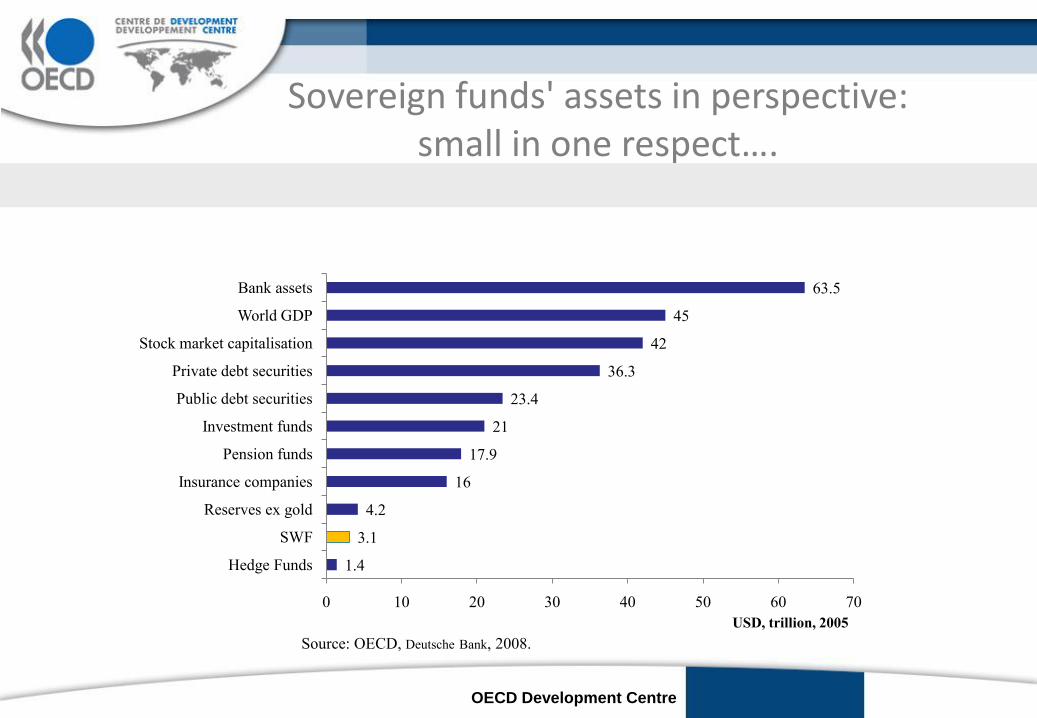

Sovereign funds' assets in perspective: small in one respect….

Source: OECD, Deutsche Bank, 2008.

1.4

3.1

4.2

16

17.9

21

23.4

36.3

42

45

63.5

0 10 20 30 40 50 60 70

Hedge Funds

SWF

Reserves ex gold

Insurance companies

Pension funds

Investment funds

Public debt securities

Private debt securities

Stock market capitalisation

World GDP

Bank assets

USD, trillion, 2005

OECD Development Centre

… yet fast becoming heavyweights as an asset class

0 500 1000 1500 2000 2500 3000 3500

SWFs total assets

Barclay's Global Investors

State Street Global Advisors

Hedge Fund assets

United Arab Emirates

China

Singapore

Private equity assets

Norway

Saudi Arabia

Kuwait

Hong Kong

Russia

USD billionFinancial institutions’ total assets, 2007

Source: OECD, Deutsche Bank, 2008.

OECD Development Centre

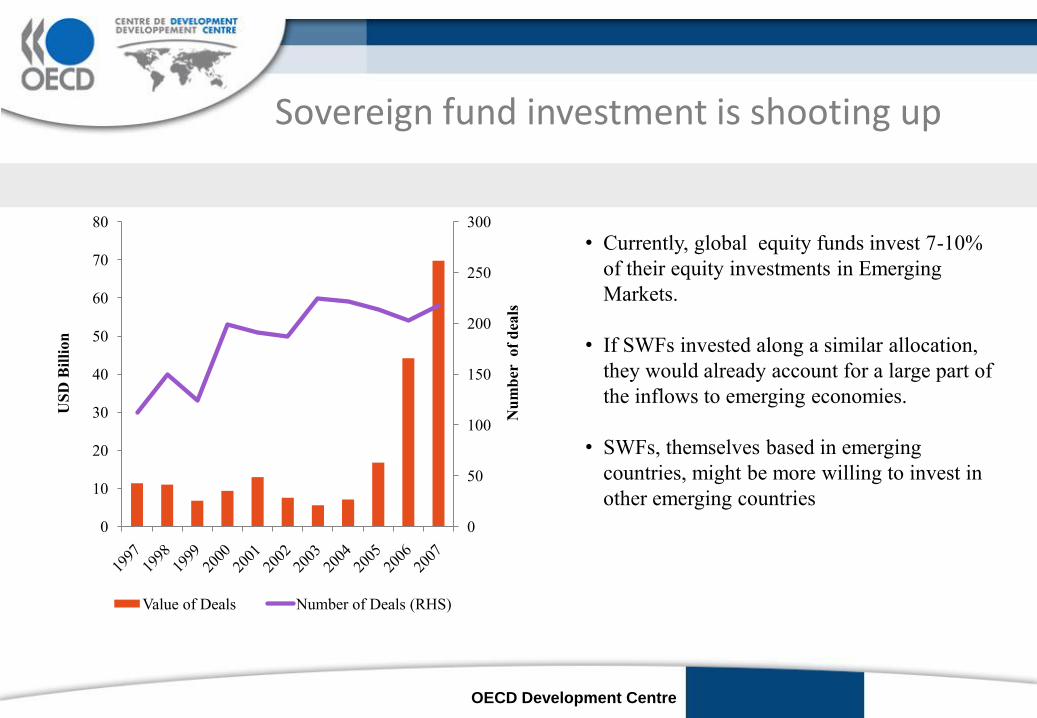

Sovereign fund investment is shooting up

0

50

100

150

200

250

300

0

10

20

30

40

50

60

70

80

Nu

mb

er

of

dea

ls

US

D B

illi

on

Value of Deals Number of Deals (RHS)

• Currently, global equity funds invest 7-10%

of their equity investments in Emerging

Markets.

• If SWFs invested along a similar allocation,

they would already account for a large part of

the inflows to emerging economies.

• SWFs, themselves based in emerging

countries, might be more willing to invest in

other emerging countries

OECD Development Centre

0 500 1000 1500 2000 2500 3000 3500

SWFs total assets

Potential 2018 SWF flows to EM

United Arab Emirates: ADIA

Norway: Pension Fund Global

Potential current SWF flows to EM

Singapore: GIC

Kuwait: KIA

China: CIC

Russia: Stabilisation Fund

Singapore: Temasek

Development Aid DAC donors

USD billionEmerging market investment potential by SWFs

•Allocations from Sovereign Development Funds to

emerging and developing countries could generate inflows

of over $100 billion/year over the next 10 years

•With such huge potential flows, it is critical to address

SWF impact on developing world early on.

•SWFs sheer size has the potential to dwarf ODA flows to

developing world

Source: OECD, JP Morgan, Deutsche Bank, 2008.

with the potential to reach USD 1.4 trillion to emerging markets over the coming decade

OECD Development Centre

Sovereign wealth funds in the global shifting of wealth1

New investment drivers in the emerging world2

Sovereign Development Funds?3

OECD Development Centre

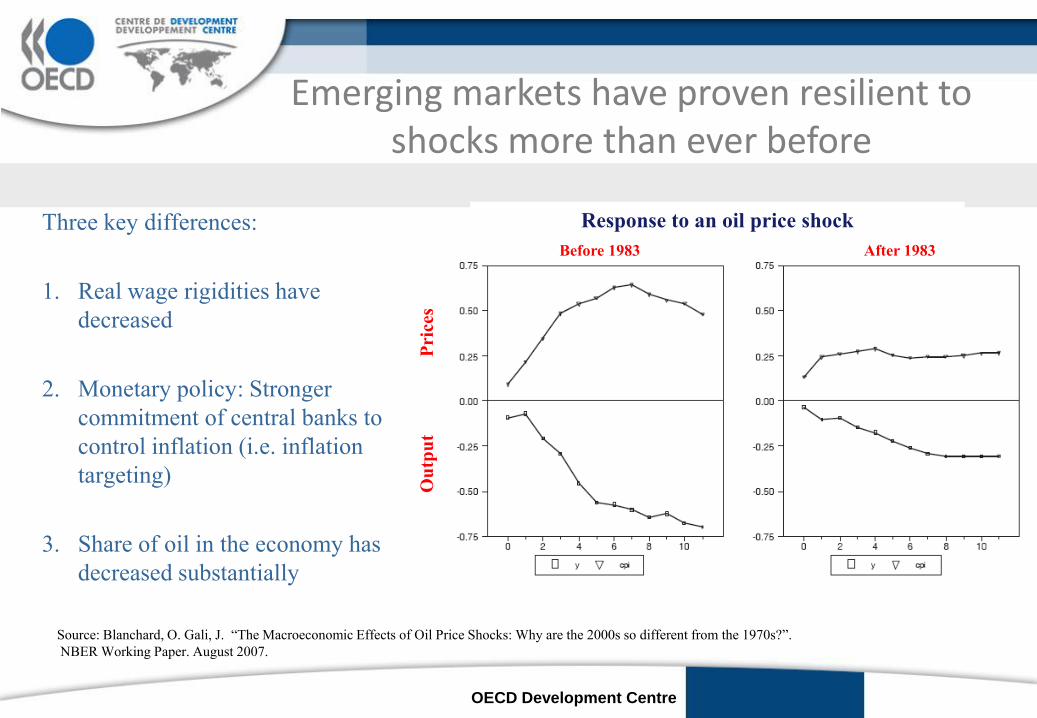

Emerging markets have proven resilient to shocks more than ever before

Three key differences:

1. Real wage rigidities have

decreased

2. Monetary policy: Stronger

commitment of central banks to

control inflation (i.e. inflation

targeting)

3. Share of oil in the economy has

decreased substantially

Source: Blanchard, O. Gali, J. “The Macroeconomic Effects of Oil Price Shocks: Why are the 2000s so different from the 1970s?”.

NBER Working Paper. August 2007.

Ou

tpu

tP

rice

s

Before 1983 After 1983

Response to an oil price shock

OECD Development Centre

• Sovereign funds seeking higher returns will find fast growing emerging

markets attractive

• Emerging market SWFS seem like ideal investors for developing countries:

long-term (not short-term speculators),

• Geographical, language and “familiarity effects” could mean lower information

asymmetries for emerging market investors.

• If Developed country protectionist urges solidify, this may drive EM SWFs

further into developing regions.

• Timing is felicitous: many African / Emerging Market countries have

considerably improved governance & investment climate over recent years (16

functioning stock markets in Africa today – 5 in 1980’s)

SWFs are well adapted to investing in emerging regions

OECD Development Centre

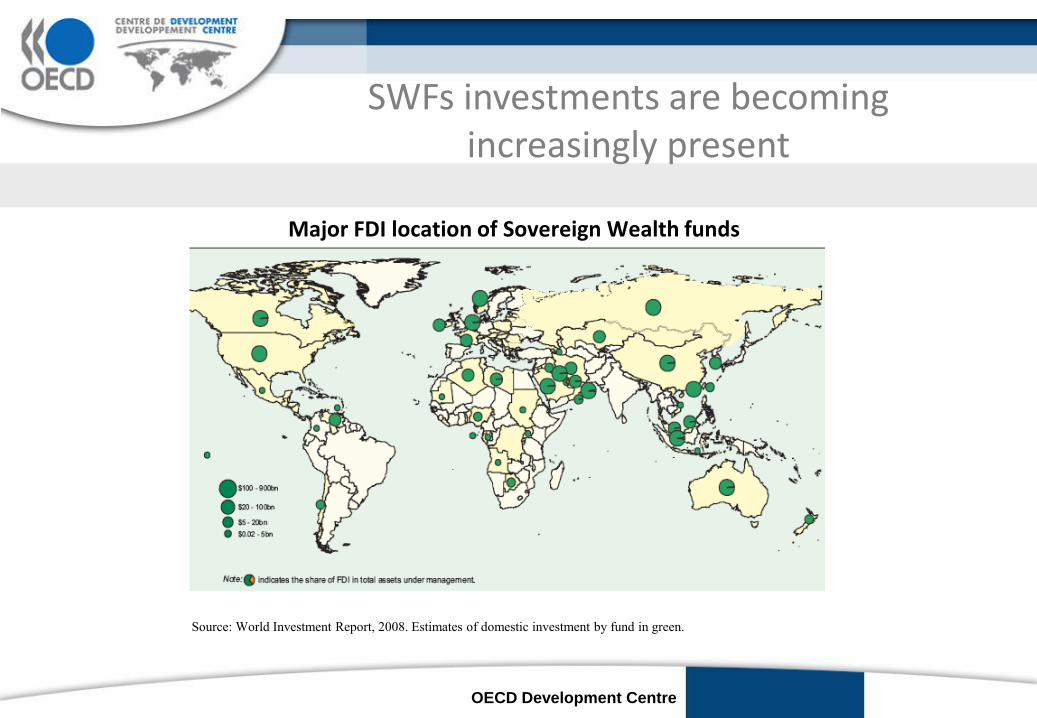

Major FDI location of Sovereign Wealth funds

SWFs investments are becoming increasingly present

Source: World Investment Report, 2008. Estimates of domestic investment by fund in green.

OECD Development Centre

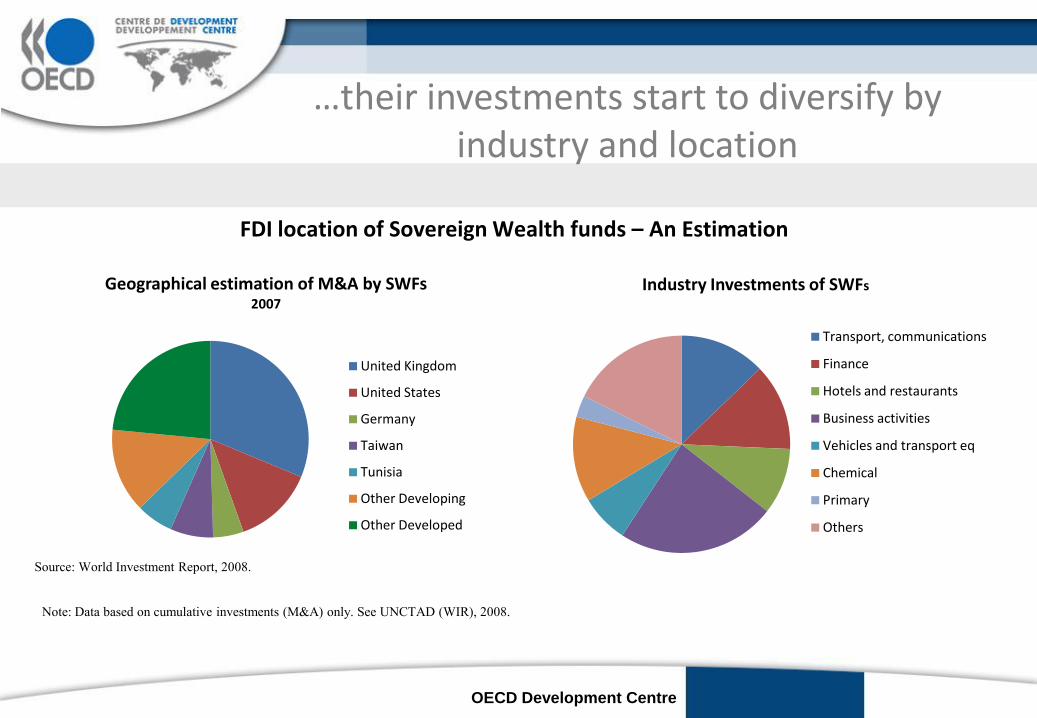

FDI location of Sovereign Wealth funds – An Estimation

…their investments start to diversify by industry and location

Source: World Investment Report, 2008.

Geographical estimation of M&A by SWFs2007

United Kingdom

United States

Germany

Taiwan

Tunisia

Other Developing

Other Developed

Note: Data based on cumulative investments (M&A) only. See UNCTAD (WIR), 2008.

Industry Investments of SWFs

Transport, communications

Finance

Hotels and restaurants

Business activities

Vehicles and transport eq

Chemical

Primary

Others

OECD Development Centre

Information Asymmetries

• What information? Accounting practices, corporate culture, political events, the structure of asset markets and their institutions.

• Market participants do not share the same information. Emerging SWFs have experience, firsthand knowledge of emerging countries institutional and infrastructure shortcomings.

• they are themselves from an emerging investor universe and have historical informational/network advantages (Gulf states in North Africa, Indians in East Africa, Chinese in South-East Asia, Russian in Central Asia)

An emerging market ‘home bias’?

OECD Development Centre

• Sovereign Wealth Funds signal a major reshaping of the world’s economy. They may grow to become key actors of development finance: Sovereign Development Funds.

• If SWFs were to allocate 10% of their portfolio to other emerging and developing economies over the next decade, this could generate inflows of USD 1 400 billion.

• The international investment of sovereign funds is already increasing. Domestically, they are development finance institutions. Abroad, they seek performance and returns.

• Collaboration and peer-learning between different actors can be promoted.

Sovereign Development Funds: What next?

Salzburg Global Seminar

27 September – Salzburg, Austria

Sovereign Development

Funds and the Shifting

Wealth of Nations

Javier Santiso

Director and Chief Economist

OECD Development Centre

OECD Development Centre

ANNEX

OECD Development Centre

Case Studies: what’s going on in Asia and the Middle East?

Temasek (Singapore) Asia represents 40% of its portfolio, including ICICI Bank,

Tata Sky, Tata Teleservices, Mahindra & Mahindra. Gulf SWFs are increasing their exposure to Asia: targeting 10-30% of total

portfolio towards Asia

Kuwait Investment Authority $750 billion stake in Industrial and Commercial Bank of China.

Qatar Investment Authority Stake in Industrial and Commercial Bank of China

Dubai International Capital 30% of portfolio to allocated to Emerging Asia. Early 2008 announced that will invest $ 5 billion in China, India and Japan. Also

MENA Infrastructure Fund (‘MENA IF’), a US$500 million sector-specific fund targeting investment opportunities in infrastructure projects in the MENA region

Increasing regional exposure for Asian and Middle Eastern funds