Embed Size (px)

Citation preview

Some Economics Concepts

Definition of economics the study of how individuals and

societies use limited resources to satisfy unlimited wants.

Fundamental economic problem scarcity. Economics is the study of how

individuals and economies deal with the fundamental problem of scarcity.

As a result of scarcity, individuals and societies must make choices among competing alternatives.

Opportunity Cost

•Economics is all about trade offs

•Because of scarcity our choices require that in order to get something we must give something up

•What you give up to get something else is your opportunity cost.

Rational self-interest When an individual makes a choice

they go through a cost-benefit evaluation

This is the idea that an individual compares the opportunity costs to the benefits and chooses the option which benefits them most (rationality)

Positive and normative analysis

positive economics attempt to describe how the economy

functions relies on testable hypotheses

normative economics relies on value judgements to

evaluate or recommend alternative policies.

Economic methodology scientific method

observe a phenomenon, make simplifying assumptions and

formulate a hypothesis, generate predictions, and test the hypothesis.

Efficiency Economists strive to achieve 100%

efficiency known as Parato Efficiency

In Parato Efficiency society is 100 $ efficient and there is no way to improve on persons well being without reducing another ones.

Microeconomics

Microeconomics vs. macroeconomics

microeconomics - the study of individual economic decisions and choices and how they effect individual markets

Macroeconomics - brings all the individual markets together and observes the behavior of the entire market

Algebra and graphical analysis direct relationship

Direct relationship

Inverse relationship

Linear relationships A linear relationship possesses a

constant slope, defined as:

Demand and Supply

Markets In a market economy, the price of

a good is determined by the interaction of demand and supply

A market for a good is comprised of all the buyers and sellers of that particular good

Demand A relationship between price and

quantity demanded in a given time period

The quantity demanded is the amount of good buyers are willing to purchase at a set price

Demand schedule

Demand curve

Law of demand An inverse relationship exists

between the price of a good and the quantity demanded in a given time period,

Reasons: Related goods Income Tastes Expectations Number of buyers

Income If someone's income is lowered

they will be less willing to spend money on goods and vice versa

Normal goods Inferior goods

Income and demand: normal goods A good is a normal good if an increase in income

results in an increase in the demand for the good.

Income and demand: inferior goods A good is an inferior good if an increase in income

results in a reduction in the demand for the good.

Price of Related Goods Substitutes – a good which

causes a decline in the demand of another good if its price declines

Complement – a good which causes an increase in the demand of another good if its price declines

Change in the price of a substitute good Price of coffee rises:

Change in the price of a complementary good Price of DVDs rises:

Tastes The idea that if an buyers

perception of benefits from buying a good changes so will the buyers willingness to purchase the good

Expectations A higher expected future price will

increase current demand. A lower expected future price will decrease

current demand. A higher expected future income will

increase the demand for all normal goods. A lower expected future income will

reduce the demand for all normal goods.

Number of Buyers The market demand curve consists

of all the individual demand curves put together

So if there are more consumers in the market the market demand will increase

Change in quantity demanded vs. change in demand

Change in quantity demanded Change in demand

Market demand curve Market demand is the horizontal summation of

individual consumer demand curves

Supply the relationship that exists between the price of a good and the quantity

supplied in a given time period Quantity supplied is the amount that a seller is able to produce for a set price

Supply schedule

Demand curve

Law of supply A direct relationship exists

between the price of a good and the quantity supplied in a given time period

Reason for law of supply The law of supply is the

result of the law of increasing cost. As the quantity of a good

produced rises, the marginal opportunity cost rises.

Sellers will only produce and sell an additional unit of a good if the price rises above the marginal opportunity cost of producing the additional unit.

Change in supply vs. change in quantity supplied

Change in supply Change in quantity supplied

Individual firm and market supply curves The market supply curve is the

horizontal summation of the supply curves of individual firms. (This is equivalent to the relationship between individual and market demand curves.)

Determinants of supply Price received by supplier Input price technology the expectations of producers the number of producers Relative Goods

Price Received by Supplier This is the law of supply The more money the supplier

receives for the good he’s selling the more willing he/she will be to sell it

Price of resources (Input Price) Inputs are the goods the supplier has to

purchase in order to produce the supply As the price of a resource rises, profitability

declines, leading to a reduction in the quantity supplied at any price.

Technological improvements Technological improvements (and any changes that raise the

productivity of labor) lower production costs and increase profitability.

Expectations and supply An increase in the expected future

price of a good or service results in a reduction in current supply.

The supplier will hold off on selling his goods if he can sell them for a greater profit later.

Increase in the Number of Sellers

Prices of other goods More than one firm produces and sells

the same good or a relative good Because of this firms compete with each

other to sell more goods and in order to do so they have to lower their prices below that of their competition

Without this effect all markets would be monopolistic and we would all be screwed

Equilibrium…the fun never stops

Market equilibrium

Price above equilibrium If the price exceeds the equilibrium price,

a surplus occurs:

Price below equilibrium If the price is below the equilibrium

a shortage occurs:

Consumer and Producer Surplus

Consumer surplus – the utility (or level of satisfaction) a buyer receives by being able to purchase a product for a price less then the maximum they were willing to pay

Producer surplus – the amount that producers benefit by selling at a market price which is greater than the minimum they would be willing to sell for

Consumer/Producer Surplus Visualized

Consumer surplus Individuals buy an item only if they

receive a net gain from the purchase (i.e., total benefit exceeds opportunity cost.)

This net gain is called “consumer surplus.”

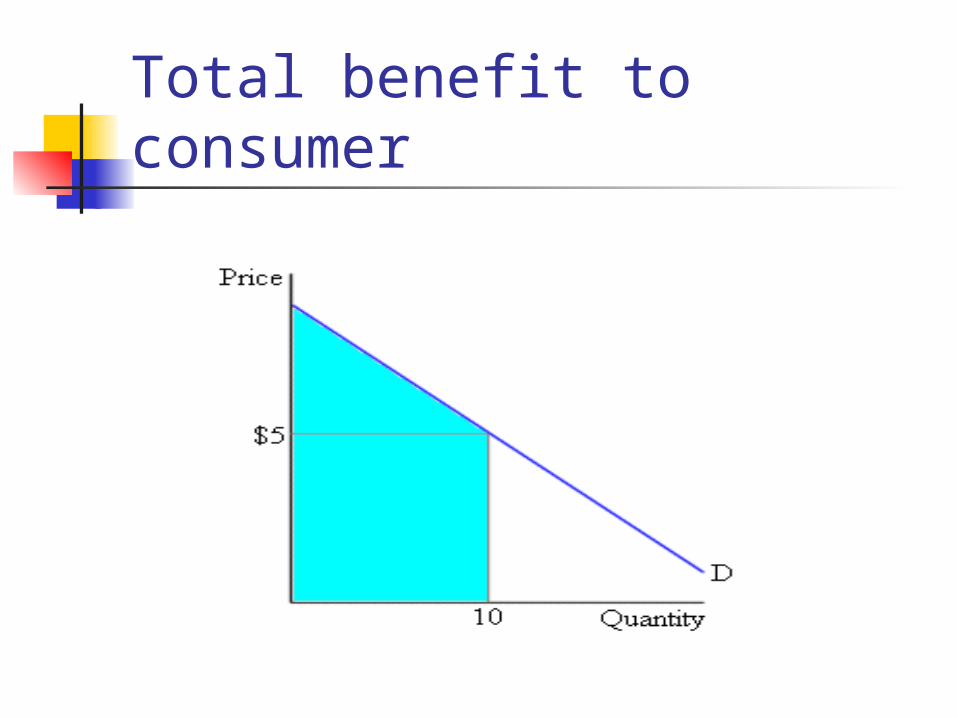

Example Suppose that an individual buys 10

units of a good when the price is $5

Benefits and cost of first unit

• Benefit = blue + green rectangles (=$9)

• Cost = green rectangle (=$5)

• Consumer surplus = blue rectangle (=$4)

Total benefit to consumer

Total cost to consumer

Consumer surplus

Demand rises

Demand falls

Supply rises

Supply falls

Price ceiling Price ceiling - legally mandated

maximum price Purpose: keep price below the

market equilibrium price

Price ceiling (continued)

Price floor price floor - legally mandated

minimum price designed to maintain a price above

the equilibrium level

Price floor (continued)

Elasticity

Elasticity A measure of the responsiveness

of one variable (quantity demanded or supplied) to a change in another variable (price)

Most commonly used elasticity: price elasticity of demand, defined as:

Price elasticity of demand =

Price elasticity of demand Demand is said to be:

elastic when Ed > 1, unit elastic when Ed = 1, and inelastic when Ed < 1.

Perfectly elastic demand

Perfectly inelastic demand

Elasticity & slope

a price increase from $1 to $2 represents a 100% increase in price,

a price increase from $2 to $3 represents a 50% increase in price,

a price increase from $3 to $4 represents a 33% increase in price, and

a price increase from $10 to $11 represents a 10% increase in price.

Notice that, even though the price increases by $1 in each case, the percentage change in price becomes smaller when the starting value is larger.

Elasticity along a linear demand curve

Elasticity along a linear demand curve

Determinants of price elasticity

Price elasticity is relatively high when:

close substitutes are available the good or service is a large share

of the consumer's budget (necessities)

a longer time period is considered (time horizon)

Price elasticity of supply

Perfectly inelastic supply

Perfectly elastic supply

Determinants of supply elasticity Ease of Entry and Exit Scarce Resources Time Horizon

Elasticity and total revenue Total revenue = price x quantity What happens to total revenue if

the price rises?

Price elasticity of demand =

Elasticity and TR (cont.)

A reduction in price will lead to: an increase in TR when demand is elastic. a decrease in TR when demand is inelastic. an unchanged level of total revenue when

demand is unit elastic.

Price elasticity of demand =

Elasticity and TR (cont.)

In a similar manner, an increase in price will lead to: a decrease in TR when demand is elastic. an increase in TR when demand is inelastic. an unchanged level of total revenue when

demand is unit elastic.

Price elasticity of demand =

…...Let’s Stick to the Non-confusing Example

Everyone's Favorite…Taxes!!!!

Tax incidence distribution of the burden of a tax

depends on the elasticities of demand and supply.

When supply is more elastic than demand, consumers bear a larger share of the tax burden.

Producers bear a larger share of the burden of a tax when demand is more elastic than supply.

Costs and production

Production possibilities curve Assumptions:

A fixed quantity and quality of available resources

A fixed level of technology

Specialization and trade Adam Smith – economic growth is

caused by increased specialization and division of labor.

Specialization and trade As noted by Adam Smith,

specialization and trade are inextricably linked.

Adam Smith used this argument to support free trade among nations.

Absolute and comparative advantage Absolute advantage – an individual

(or country) is more productive than other individuals (or countries).

Comparative advantage – an individual (or country) may produce a good at a lower opportunity cost than can other individuals (or countries).

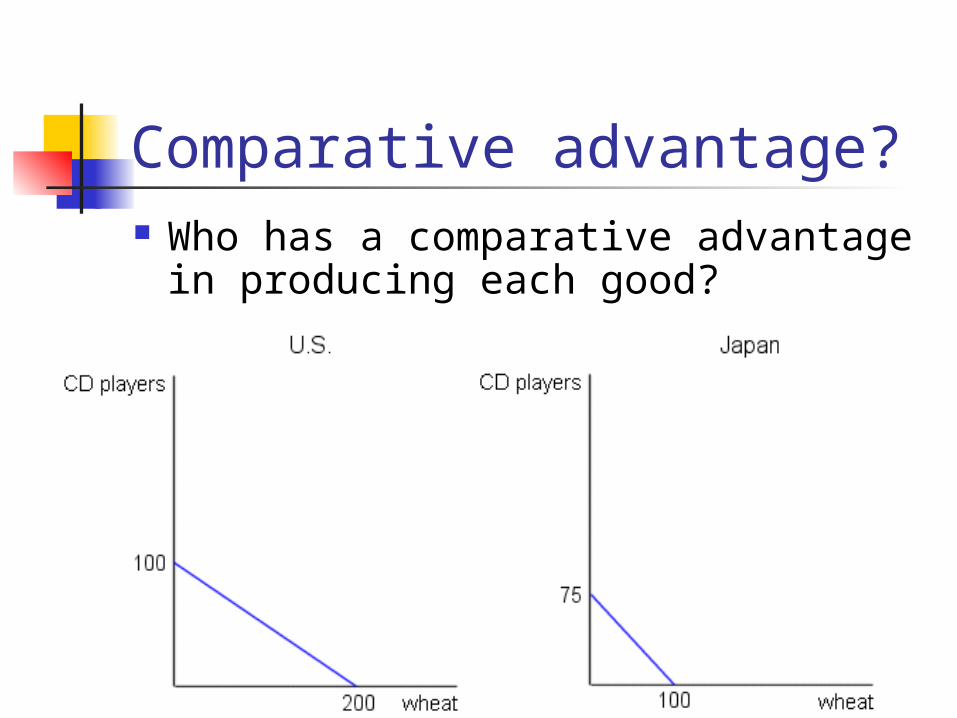

Example: U.S. and Japan Suppose the U.S. and Japan produce only

two goods: CD players and wheat.

Absolute advantage? Who has an absolute advantage in

producing each good?

Comparative advantage? Who has a comparative advantage

in producing each good?

Gains from trade Opportunity cost of CD player in U.S. = 2

units of wheat Opportunity cost of CD player in Japan =

4/3 unit of wheat If Japan produces and trades each CD

player to the U.S. for more than 4/3 of a unit of wheat but less than 2 units of wheat, both the U.S. and Japan gain from trade and can consume more goods than they could produce by themselves.

Gains from trade (continued) Note that the U.S. has a comparative

advantage in producing wheat. Countries always expand their

consumption possibilities by engaging in trade (since they acquire goods at a lower opportunity cost than if they produced them themselves).

Free trade? If each country specializes in the

production of those goods in which it possesses a comparative advantage and trades with other countries, global output and consumption is increased.

Robinson and Crusoe? Really USAD……Really?

Profit Motive and Behavior of Firms Profit = total revenue – total cost (costs will likely only include only

monetary expenses) Total cost is comprised of expenses

plus all monetary opportunity costs

Different Costs The costs that do not depend on

production and can’t change in the short run are called fixed costs

However costs that can be varied in the short run are called variable costs

Marginal Cost Notice in figure 23 that when you

go down 1 row there are 50 more loaves of bread produced; however, there is an additional cost for producing more goods

This increase in cost when producing an additional unit of output is called the marginal cost

How to find marginal cost (increase in total cost) MC = ------------------------------------- (increase in quantity

produced)

Law of Diminishing Returns Next notice that the maximum

profit is made when marginal cost is equal to marginal revenue

Think of the marginal cost as the opportunity cost for making an extra unit of good and the marginal revenue as the profit for making that extra unit

Law of Diminishing Returns as the level of a variable input

rises in a production process in which other inputs are fixed, output ultimately increases by progressively smaller increments

So this means that at some point it’s no longer productive to make that extra unit of good

Imperfect Markets

Monopolies A monopoly is an extreme case in

which there is a market with only one producer

Ownership Monopolies Government-Created Monopolies Natural Monopolies

Why Monopolies Are Bad? Because the supplier can charge

whatever amount he/she wants for the product and there is no competition to force the supplier to lower the prices on goods

Price discrimination different customers are charged

different prices for the same product, due to differences in price elasticity of demand

higher prices for those customers who have the most inelastic demand

lower prices for those customers who have a more elastic demand.

Price discrimination (cont.) customers who are willing to pay

the highest prices are charged a high price, and

customers who are more sensitive to price differentials are charged a low price.

Next up…Oligopolies An oligopoly is a market with very

few suppliers Not quite as bad as a monopoly

but still Example: OPEC (Organization of

Petroleum Exporting Countries)

Creative Destruction A term coined by the Australian

economist Joseph Schumpeter “creative destruction” states

that as new industries surged, older industries grow more slowly, stagnate, and shrink

Market failures Not all markets are perfect and

sometimes a market failure will occur when externalities or breakdowns in the system of private property cause markets to deviate from the socially efficient outcome

Oh the Government Pork Barrel Politics – elected

officials introduce projects that steer money into their of pockets

Logrolling – vote trading within legislation