Embed Size (px)

Citation preview

Management

Accounting

2008 Solutions

By

Colin Davy and Danny Bruce

Table of Contents Chapter 1: Cost Concepts .................................................................. 1

Chapter 2: Manufacturing & Trading Statements ..........................11

Chapter 3: Cost-Volume-Profit Analysis......................................... 28

Chapter 4: The Cost Accounting Cycle........................................... 42

Chapter 5: Material & Labour ........................................................ 59

Chapter 6: Overhead Allocation ..................................................... 79

Chapter 7: Job Costing.................................................................... 87

Chapter 8: Responsibility Accounting ...........................................114

Chapter 9: Review Examinations ................................................. 122

Chapter 10: Class Examinations ................................................... 145 Regards Colin Davy & Danny Bruce

www.learnnowbiz.com ISBN: 1 876 602 856 Fourth Edition 2008 Published by P.O. Box 210 Bondi N.S.W. 2026 Phone: ( 02 ) 9314 5374 © This book is copyright and all rights are reserved. No part of this work is to be

reproduced other than in accordance with the Copyright Act, or with the written permission of the publishers.

Chapter 1: Cost Concepts

1

Chapter 1: Cost Concepts Chapter Review Solutions

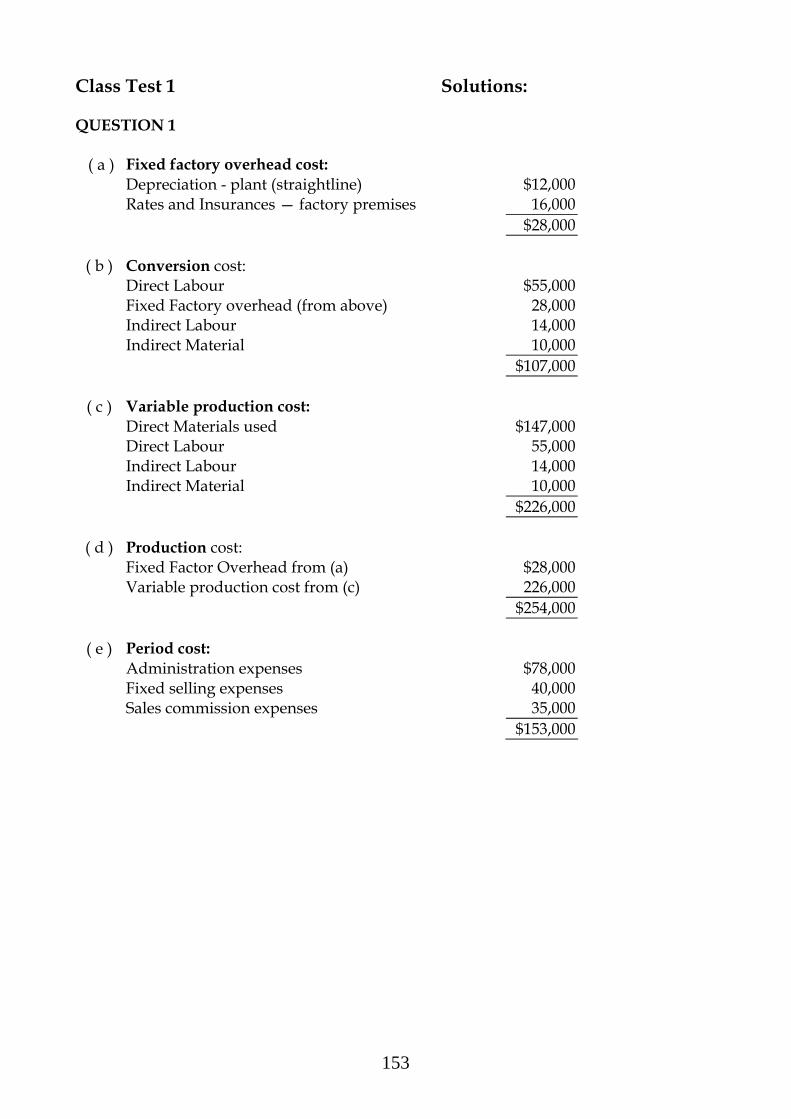

Questions 1. ( a ) By the nature of the item ( a natural classification ).

( b ) In their relation to the product. ( c ) With respect to the accounting period to which they apply. ( d ) In their tendency to vary with volume or activity. ( e ) In their relation to departments. ( f ) For planning and control. ( g ) For analytical processes.

2. Those costs which follow the product through inventories are product costs, and those which are directly applicable against income of the period without assignment to inventories are period costs. The classification is primarily useful in organising the accumulation of data to prepare financial statements. From the income statement point of view the problem of distinguishing between product and period costs is essentially one of timing the charges against revenue. For this purpose inventories are an essential means of carrying costs forward until the corresponding revenue accrues. For other purposes such as cost control, preparation of budgets, or pricing, the cost classification may be quite different.

3. ( a ) ( i ) Indirect ( b ) ( i ) Direct Material ( ii ) Direct ( ii ) Factory Overhead ( iii) Indirect ( iii ) Direct Material ( iv ) Factory Overhead

( c ) ( i ) Fixed ( d ) ( i ) Product

( ii ) Variable ( ii ) Period ( iii ) Fixed ( iii ) Product ( iv ) Period

( e ) ( i ) Fixed

( ii ) Variable ( iii ) Fixed ( iv ) Variable

( f ) ( i ) All direct costs of production.

( g ) ( iii ) Costs associated with conversion of raw materials into finished goods.

Management Accounting in Australia - Solutions

2

4. ( a ) ( i ) Fixed cost remain constant in total. - rent ( ii ) Variable rate per unit is constant- dir. wages ( iii ) Has elements of both - telephone

( b ) See text. 5. ( a ) Indirect, fixed

( b ) Indirect, variable ( c ) Indirect, fixed ( d ) Indirect, variable ( e ) Direct, variable ( f ) Indirect, fixed ( g ) Indirect, fixed ( h ) Indirect, fixed ( i ) Indirect, variable

6. Management accounting deals with the future, financial accounting the past. Management accounting is designed to facilitate internal decision-making, financial accounting - provision of information to external users. Management accounting does not conform to rules or accounting standards. Management accounting provides detailed information by cost and profit centres, financial - in aggregate.

7. ( i ) Direct ( ii ) Direct ( iii ) Indirect ( iv ) Direct

8. See text.

Chapter 1: Cost Concepts

3

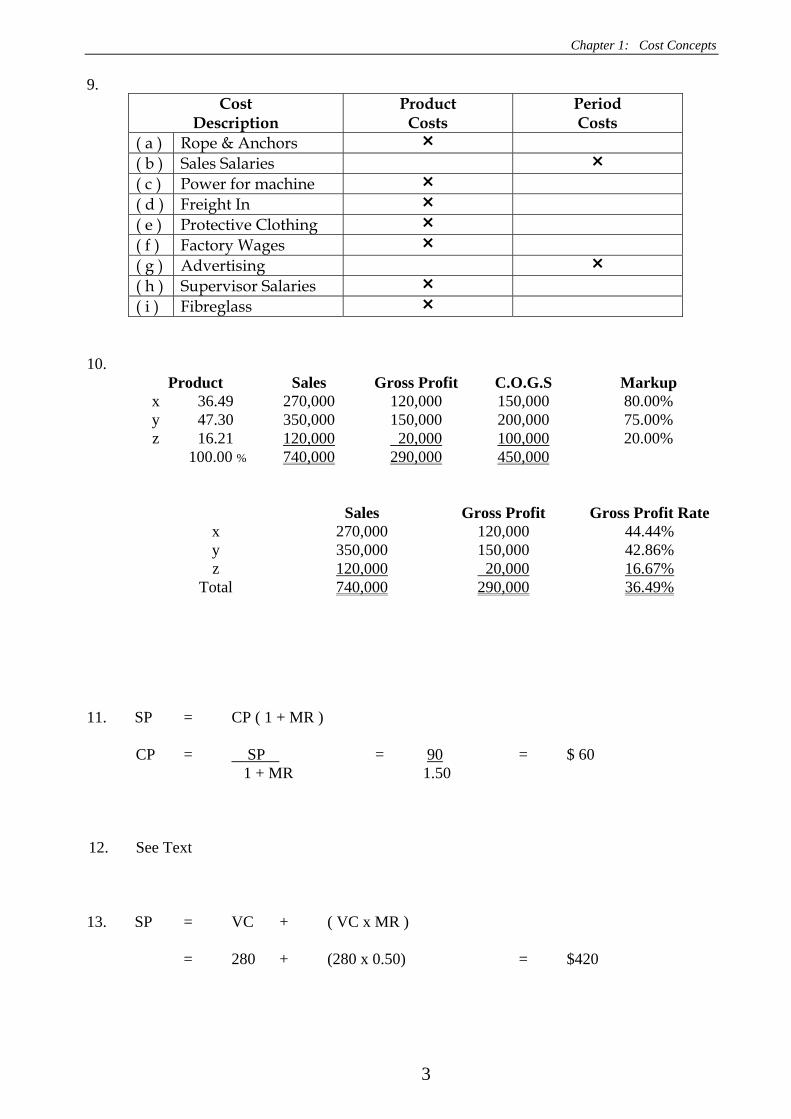

9. Cost

Description Product

Costs Period Costs

( a ) Rope & Anchors ( b ) Sales Salaries ( c ) Power for machine ( d ) Freight In ( e ) Protective Clothing ( f ) Factory Wages ( g ) Advertising ( h ) Supervisor Salaries ( i ) Fibreglass

10.

Product Sales Gross Profit C.O.G.S Markup x 36.49 270,000 120,000 150,000 80.00% y 47.30 350,000 150,000 200,000 75.00% z 16.21 120,000 20,000 100,000 20.00% 100.00 % 740,000 290,000 450,000

Sales Gross Profit Gross Profit Rate

x 270,000 120,000 44.44% y 350,000 150,000 42.86% z 120,000 20,000 16.67%

Total 740,000 290,000 36.49%

11. SP = CP ( 1 + MR )

CP = SP = 90 = $ 60 1 + MR 1.50

12. See Text 13. SP = VC + ( VC x MR )

= 280 + (280 x 0.50) = $420

Management Accounting in Australia - Solutions

4

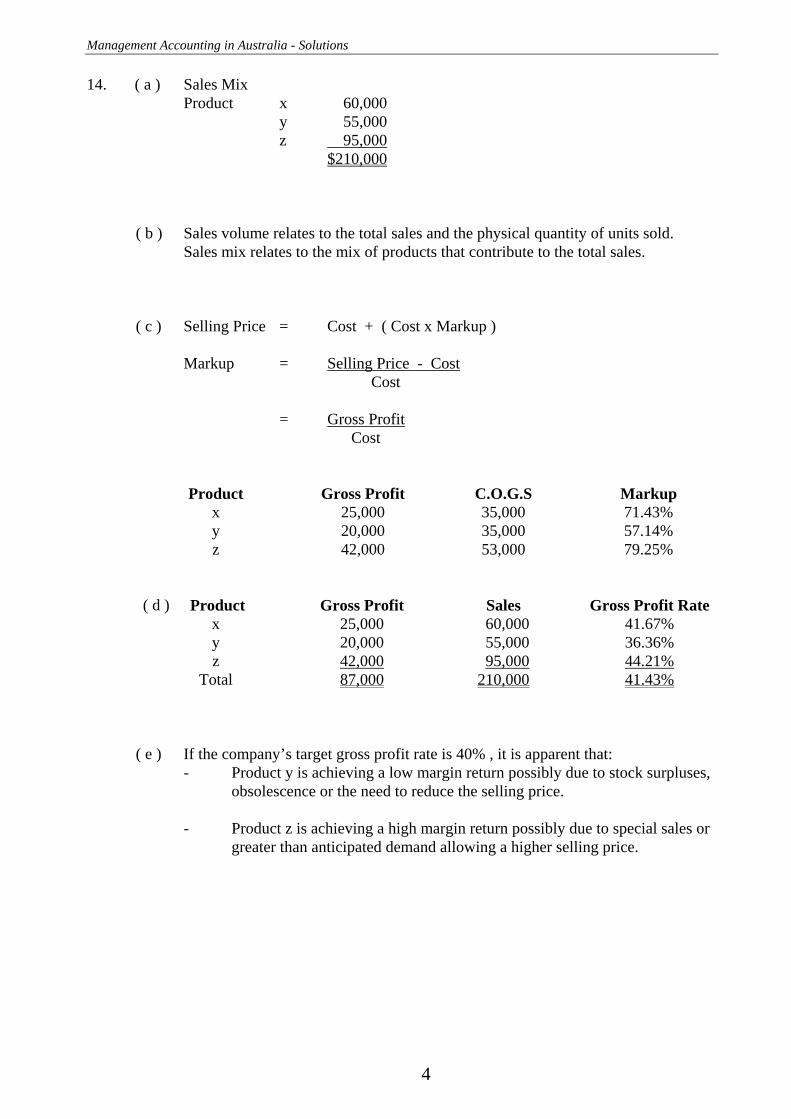

14. ( a ) Sales Mix Product x 60,000 y 55,000 z 95,000 $210,000 ( b ) Sales volume relates to the total sales and the physical quantity of units sold. Sales mix relates to the mix of products that contribute to the total sales. ( c ) Selling Price = Cost + ( Cost x Markup ) Markup = Selling Price - Cost Cost = Gross Profit Cost

Product Gross Profit C.O.G.S Markup x 25,000 35,000 71.43% y 20,000 35,000 57.14% z 42,000 53,000 79.25%

( d ) Product Gross Profit Sales Gross Profit Rate

x 25,000 60,000 41.67% y 20,000 55,000 36.36% z 42,000 95,000 44.21%

Total 87,000 210,000 41.43% ( e ) If the company’s target gross profit rate is 40% , it is apparent that: - Product y is achieving a low margin return possibly due to stock surpluses, obsolescence or the need to reduce the selling price. - Product z is achieving a high margin return possibly due to special sales or greater than anticipated demand allowing a higher selling price.

Chapter 1: Cost Concepts

5

15. ( a ) CBD Inner Metro Outer Metro Total Sales 15,000 12,000 16,000 43,000 Less Variable Costs 7,500 5,400 6,400 19,300 Contribution Margin 7,500 6,600 9,600 23,700 Less Fixed Costs 3,500 3,500 3,500 10,500 Net Profit 4,000 3,100 6,100 13,200

( b ) Outer Metro ( c ) Assume variable costs are a constant percentage of sales. CBD x = 3,500 + 0.50 x x = $7,000 where x = sales breakeven $ Inner Metro x = 3,500 + 0.45 x x = $6,364 Outer Metro x = 3,500 + 0.40 x x = $5,833

16. Sales price 200 100.00 Less Variable costs - 90 45.00 Contribution Margin 110 55.00

Break even quantity = Fixed Cost = $110,000 1,000 units Contribution Margin $110

Contribution Margin: $110 Contribution Margin Ratio 55%

Management Accounting in Australia - Solutions

6

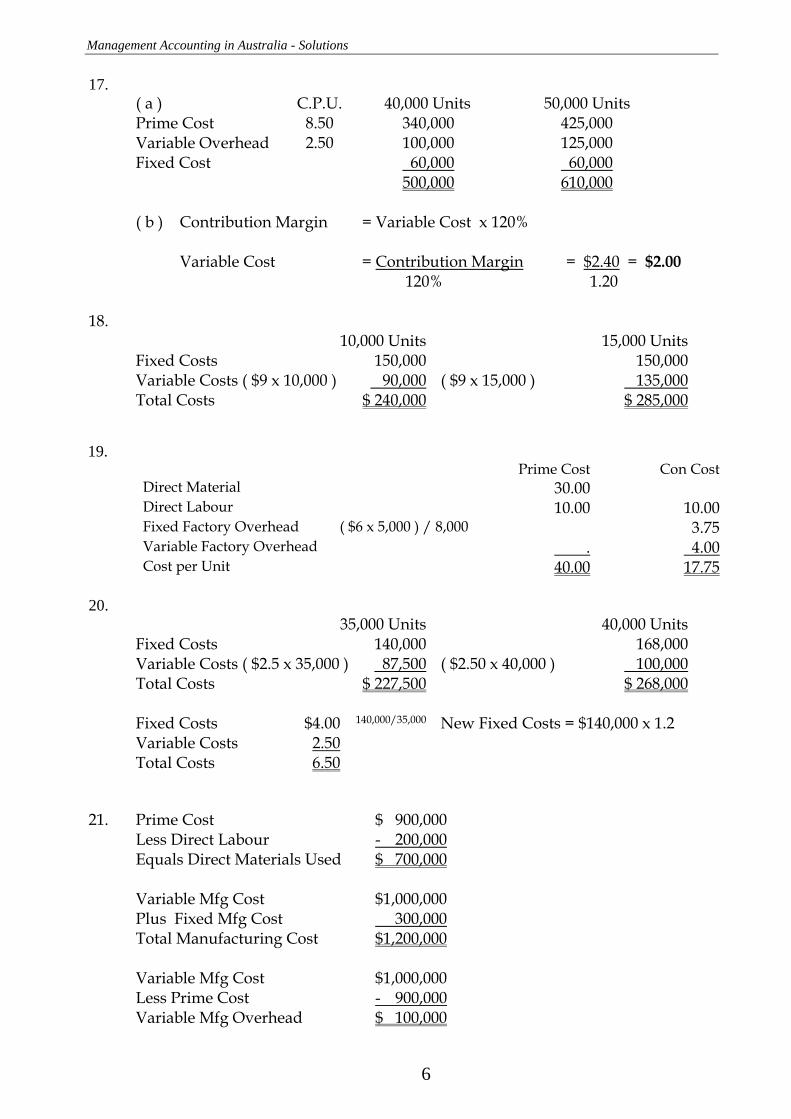

17. ( a ) C.P.U. 40,000 Units 50,000 Units Prime Cost 8.50 340,000 425,000 Variable Overhead 2.50 100,000 125,000 Fixed Cost 60,000 60,000 500,000 610,000 ( b ) Contribution Margin = Variable Cost x 120% Variable Cost = Contribution Margin = $2.40 = $2.00 120% 1.20

18. 10,000 Units 15,000 Units Fixed Costs 150,000 150,000 Variable Costs ( $9 x 10,000 ) 90,000 ( $9 x 15,000 ) 135,000 Total Costs $ 240,000 $ 285,000

19.

Prime Cost Con Cost Direct Material 30.00 Direct Labour 10.00 10.00 Fixed Factory Overhead ( $6 x 5,000 ) / 8,000 3.75 Variable Factory Overhead . 4.00 Cost per Unit 40.00 17.75

20.

35,000 Units 40,000 Units Fixed Costs 140,000 168,000 Variable Costs ( $2.5 x 35,000 ) 87,500 ( $2.50 x 40,000 ) 100,000 Total Costs $ 227,500 $ 268,000 Fixed Costs $4.00 140,000/35,000 New Fixed Costs = $140,000 x 1.2 Variable Costs 2.50 Total Costs 6.50

21. Prime Cost $ 900,000 Less Direct Labour - 200,000 Equals Direct Materials Used $ 700,000

Variable Mfg Cost $1,000,000 Plus Fixed Mfg Cost 300,000 Total Manufacturing Cost $1,200,000 Variable Mfg Cost $1,000,000 Less Prime Cost - 900,000 Variable Mfg Overhead $ 100,000

Chapter 1: Cost Concepts

7

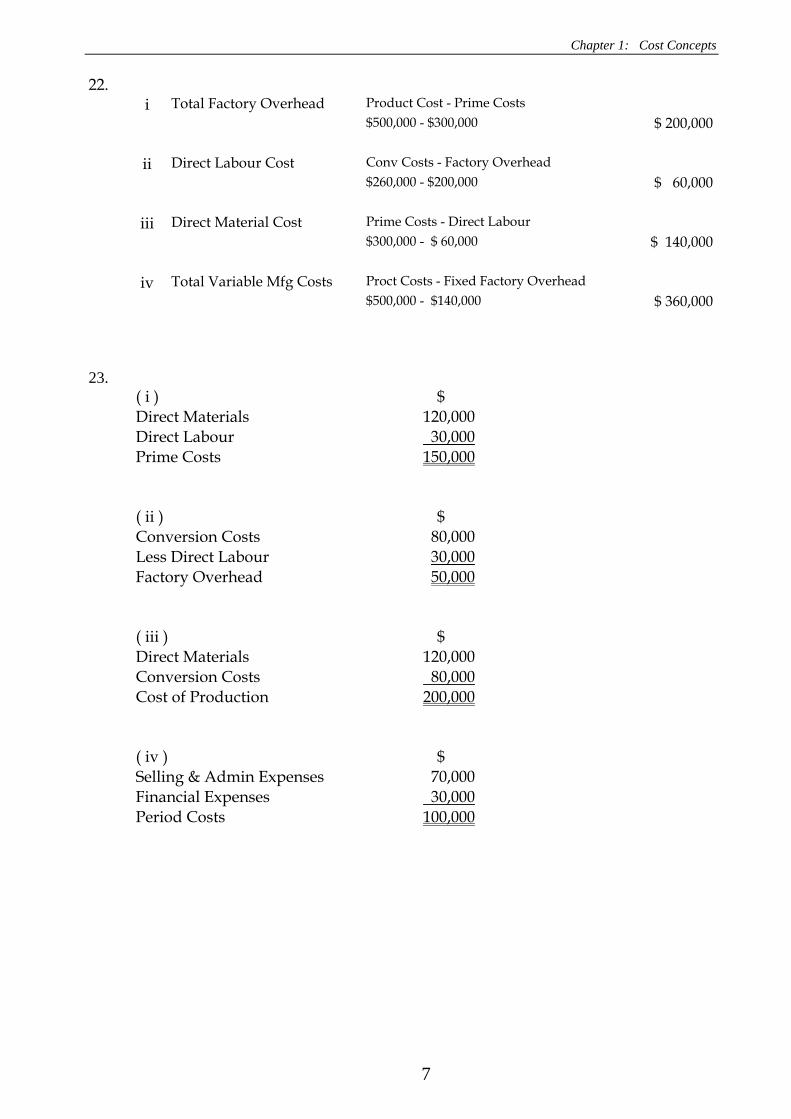

22. i Total Factory Overhead Product Cost - Prime Costs $500,000 - $300,000 $ 200,000

ii Direct Labour Cost Conv Costs - Factory Overhead $260,000 - $200,000 $ 60,000

iii Direct Material Cost Prime Costs - Direct Labour $300,000 - $ 60,000 $ 140,000

iv Total Variable Mfg Costs Proct Costs - Fixed Factory Overhead $500,000 - $140,000 $ 360,000

23. ( i ) $ Direct Materials 120,000 Direct Labour 30,000 Prime Costs 150,000 ( ii ) $ Conversion Costs 80,000 Less Direct Labour 30,000 Factory Overhead 50,000 ( iii ) $ Direct Materials 120,000 Conversion Costs 80,000 Cost of Production 200,000 ( iv ) $ Selling & Admin Expenses 70,000 Financial Expenses 30,000 Period Costs 100,000

Management Accounting in Australia - Solutions

8

Problems 24. ( a )

Prime Costs $500,000Less Direct Labour 150,000Direct Materials used 350,000 ( b ) Variable Manufacturing cost $525,000Add Fixed mfg. Overhead 75,000Total manufacturing cost 600,000 ( c ) Variable Manufacturing cost $525,000Less Prime Cost 500,000Variable mfg. overhead cost 25,000 Note: Total mfg cost comprises Direct Materials $350,000Direct labour 150,000Variable mfg. overhead cost 25,000Variable Manufacturing cost 525,000Add Fixed mfg. overhead 75,000Total manufacturing cost 600,000

25.

( a ) Prime Cost Direct Materials Fibreglass, resin etc. 12,000 Sailcloth 3,500 Rigging and fittings 3,000 Direct labour Production wages 10,000 28,500

( b ) Period cost General office rent 3,750 General office salaries 2,050 5,800

( c ) Fixed manufacturing cost Factory rent 2,500 Depreciation – factory equipment 700 3,200

( d ) Prime Cost + Variable factory Exp ( 28,500 + 500 ) 29,000

Chapter 1: Cost Concepts

9

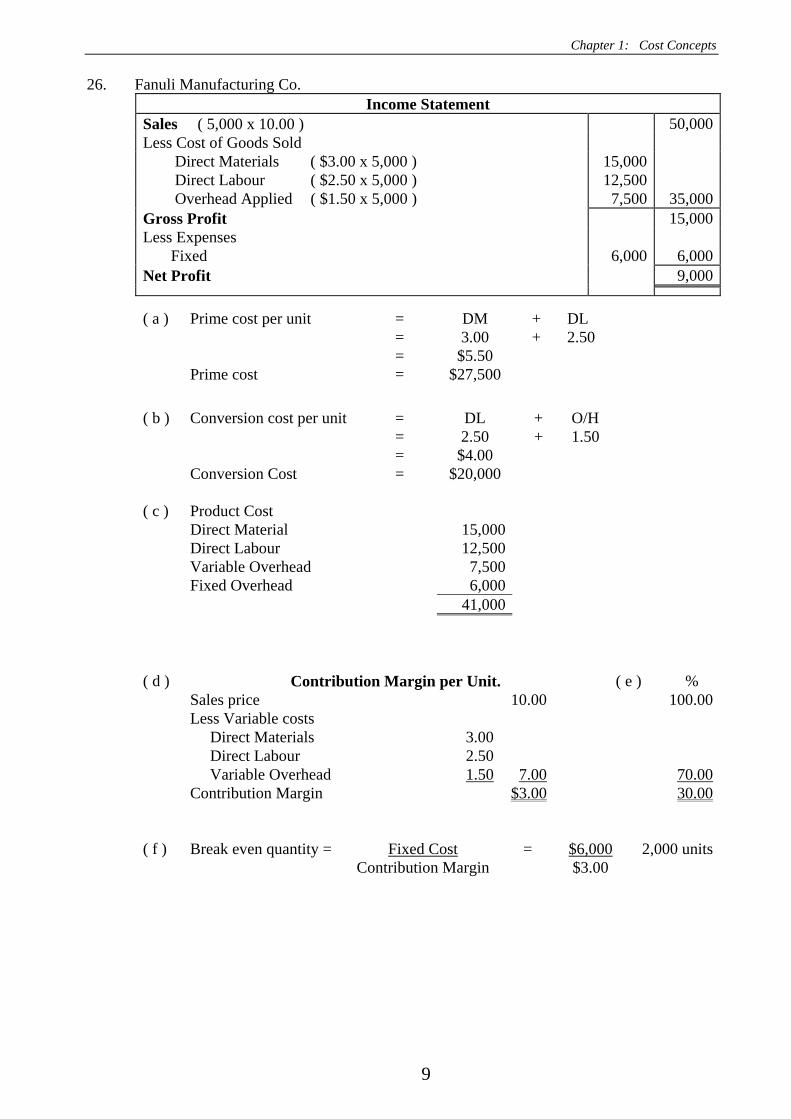

26. Fanuli Manufacturing Co. Income Statement

Sales ( 5,000 x 10.00 ) 50,000Less Cost of Goods Sold Direct Materials ( $3.00 x 5,000 ) 15,000 Direct Labour ( $2.50 x 5,000 ) 12,500 Overhead Applied ( $1.50 x 5,000 ) 7,500 35,000Gross Profit 15,000Less Expenses Fixed 6,000 6,000Net Profit 9,000

( a ) Prime cost per unit = DM + DL = 3.00 + 2.50 = $5.50 Prime cost = $27,500

( b ) Conversion cost per unit = DL + O/H = 2.50 + 1.50 = $4.00 Conversion Cost = $20,000 ( c ) Product Cost Direct Material 15,000 Direct Labour 12,500 Variable Overhead 7,500 Fixed Overhead 6,000 41,000

( d ) Contribution Margin per Unit. ( e ) % Sales price 10.00 100.00 Less Variable costs Direct Materials 3.00 Direct Labour 2.50 Variable Overhead 1.50 7.00 70.00 Contribution Margin $3.00 30.00

( f ) Break even quantity = Fixed Cost = $6,000 2,000 units Contribution Margin $3.00

Management Accounting in Australia - Solutions

10

27. ( a ) Conversion cost: Direct labour $80,000 Fixed manufacturing overhead 60,000 Variable manufacturing overhead 30,000 $170,000 ( b ) Product cost: Variable manufacturing $250,000 Fixed manufacturing overhead 60,000 $310,000 ( c ) Prime cost: Variable manufacturing $250,000 Less Variable manufacturing overhead 30,000 $220,000 ( d ) Period cost: Fixed selling and administration $110,000 Variable selling 70,000 $180,000 ( e ) Manufacturing overhead cost @ 60,000 units: Fixed manufacturing overhead $60,000 Variable manufacturing overhead $30,000 x 60,000 36,000 50,000 $96,000

28. ( a ) Direct Labour cost:

Conversion costs $150,000 Fixed manufacturing overhead - 56,000 Variable manufacturing overhead - 20,000 $ 74,000 ( b ) Variable conversion cost: Direct Labour $ 74,000 Variable manufacturing 20,000 $ 94,000 ( c ) Product cost: Prime cost $237,000 Fixed manufacturing overhead 56,000 Variable manufacturing overhead 20,000 $313,000 ( d ) Period cost: Fixed selling and administration $130,000 Variable selling 45,000 $175,000 ( e ) Manufacturing overhead cost @ 30,000 units: Fixed manufacturing overhead $56,000 Variable manufacturing overhead $20,000 x 30,000 30,000 20,000 $86,000

Chapter 2: Manufacturing & Trading Statements

11

Chapter 2: Manufacturing & Trading Statements Chapter Review Solutions

1. ( a ) Direct Material Cost Inventory 1/7/09 5,000 Purchases 25,000 30,000 Less Inventory 30/6/10 4,000 26,000

( b ) Direct Material Cost Inventory 1/7/08 4,000 Purchases 26,000 Freight on Purchases 1,000 31,000 Less Inventory 30/6/10 3,000 28,000

( c ) Direct Material Cost Inventory 1/7/09 5,000 Purchases 32,000 Freight & Other Charges 1,000 38,000 Less Inventory 30/6/10 8,000 30,000

( d ) Direct Material Cost Inventory 1/7/09 5,000 Purchases 30,000 Freight 1,000 Duty & Landing Charges 2,000 38,000 Less Inventory 30/6/10 6,000 32,000

( e ) Direct Material Cost Work in Progress 1/7/10 1,200 Inventory 1/7/10 6,500 Purchase 27,300 Freight Inwards 800 35,800 Less Work in Progress 30/6/11 700 Inventory 30/6/11 1,100 1,800 34,000

Management Accounting in Australia - Solutions

12

2. Direct Labour Costs Direct Labour Paid 48,000 Less Direct Labour. Accrued 1/7/09 1,400 46,600 Add DIRECT LABOUR. Accrued 30/6/10 2,200 48,800

3. Direct Labour Cost Direct Labour Paid 56,000 Less Direct Labour. Accrued 1/7/09 3,200 52,800 Add Direct Labour. Accrued 30/6/10 2,200 55,000

4. Work in Progress 1/7/09 11,800 Direct Labour Paid 52,000 + Accrued 30/6/10 1,100 Less Accrued 1/7/09 1,600 51,500 63,300 Less Work in Progress 30/6/10 3,300 60,000

5.

Manufacturing Overhead Factory Insurance 400 Factory Light & Power 1,800 Indirect Labour ( 400 + 15,000 - 400 ) 15,200 Machinery Repairs 1,300 Depreciation Machinery 5,900 Indirect Material ( 1,700 + 5,100 - 1,400 ) 5,400 30,000

6. Costs for the Period Manufacturing Overhead Work in Progress 1/7/09 2,200 Factory Insurance ( 500 - 100 ) 400 Factory Light & Power 2,300 Indirect Labour ( 17,000 + 600 - 400 ) 17,200 Machinery Repairs 400 Depreciation Machinery 4,500 Indirect Materials ( 1,400 + 7,000 - 1,600 ) 6,800 33,800 Less Work in Progress 30/6/10 1,800 32,000

7. By using method as in solution 5, number manufactured equals 7,000

W.I.P. O/bal 12,800 F.G.s 112,000 Cost of Prod 112,800 C/bal 13,600 125,600 125,600 Therefore cost per unit = $16.00 ( 112,000 / 7,000 )

Chapter 2: Manufacturing & Trading Statements

13

8. Factory Rates paid during year 2,500 Add Back prepayments 1/7/2009 1,200 3,700 Add Accrued 30/6/2010 600 To Manufacturing Account 4,300

9. Manufacturing Account

O / bal Work in Progress 4,000 Trading Account 30,000Direct Material 12,000 Cost of Production Direct Labour 8,000 Overhead 8,000 32,000 C/bal Work in Progress 2,000 30,000 30,000

10.

( a ) Raw Material Cost Work in Progress 1/7/08 2,000 Inventory 1/7/08 10,000 Purchases 60,000 Freight Inwards 2,000 Duty 5,000 79,000 Less Work in Progress 30/6/09 6,000 Inventory 30/6/09 16,000 22,000 57,000

( b ) Direct Labour Cost Work in Progress 1/7/09 2,000 Labour ( 25,000 + 2,000 - 1,000 ) 26,000 28,000 Less Work in Progress 30/6/10 6,000 22,000

( c ) Prime Cost Raw Materials 57,000 Direct Labour 22,000 79,000

Management Accounting in Australia - Solutions

14

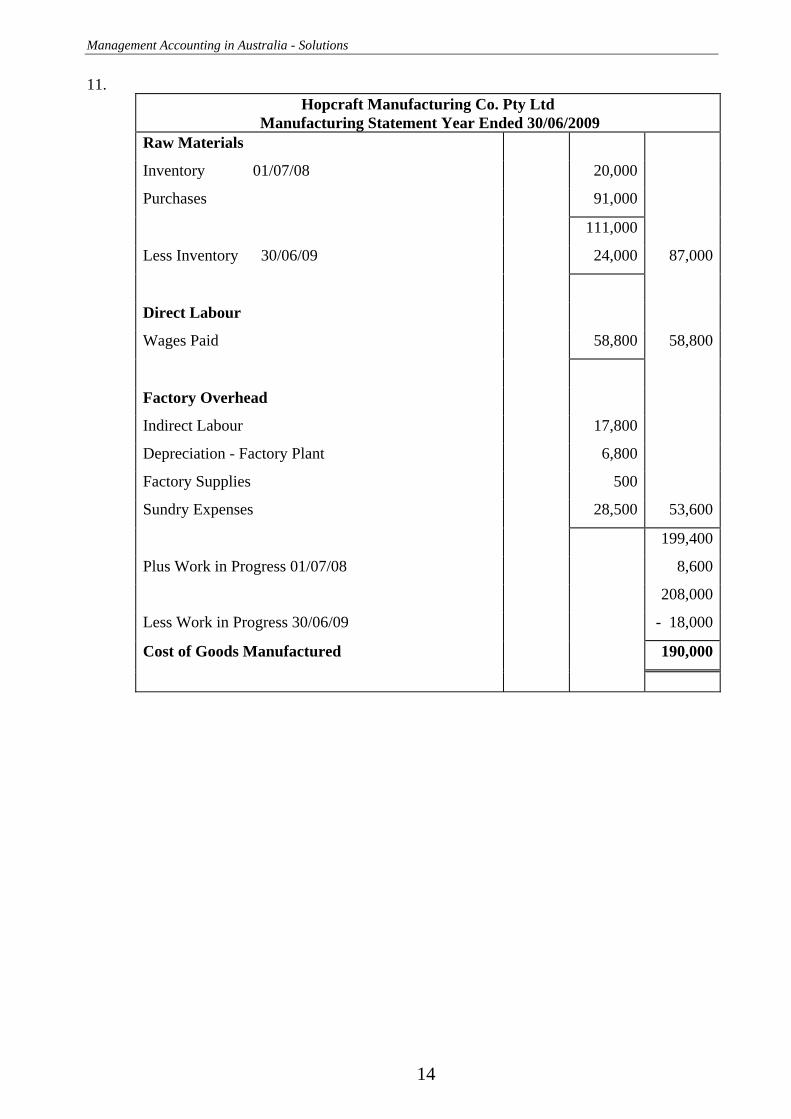

11. Hopcraft Manufacturing Co. Pty Ltd

Manufacturing Statement Year Ended 30/06/2009 Raw Materials

Inventory 01/07/08 20,000

Purchases 91,000

111,000

Less Inventory 30/06/09 24,000 87,000

Direct Labour

Wages Paid 58,800 58,800

Factory Overhead

Indirect Labour 17,800

Depreciation - Factory Plant 6,800

Factory Supplies 500

Sundry Expenses 28,500 53,600

199,400

Plus Work in Progress 01/07/08 8,600

208,000

Less Work in Progress 30/06/09 - 18,000

Cost of Goods Manufactured 190,000

Chapter 2: Manufacturing & Trading Statements

15

12.

Manufacturing Statement for the year ended 30 June 2009

Direct Materials

Inventory 1/07/08 7,500

Purchases 46,500

54,000

Less Inventory 30/06/09 4,000 50,000

Direct Labour

Labour paid 20,000 20,000

Factory Overhead

Supervisor 7,800

Depreciation - Manufacturing Plant 2,300

Factory Rates 5,200

Factory Supplies ( 1,400 – 400 ) 1,000

Insurance 1,100

Power 3,100

Repairs to Plant 4,200 24,700

Cost of Production this period 94,700

Work in Progress 01/07/08 13,300

108,000

Work in Progress 30/06/09 - 8,000

Cost of Goods Manufactured 100,000

Management Accounting in Australia - Solutions

16

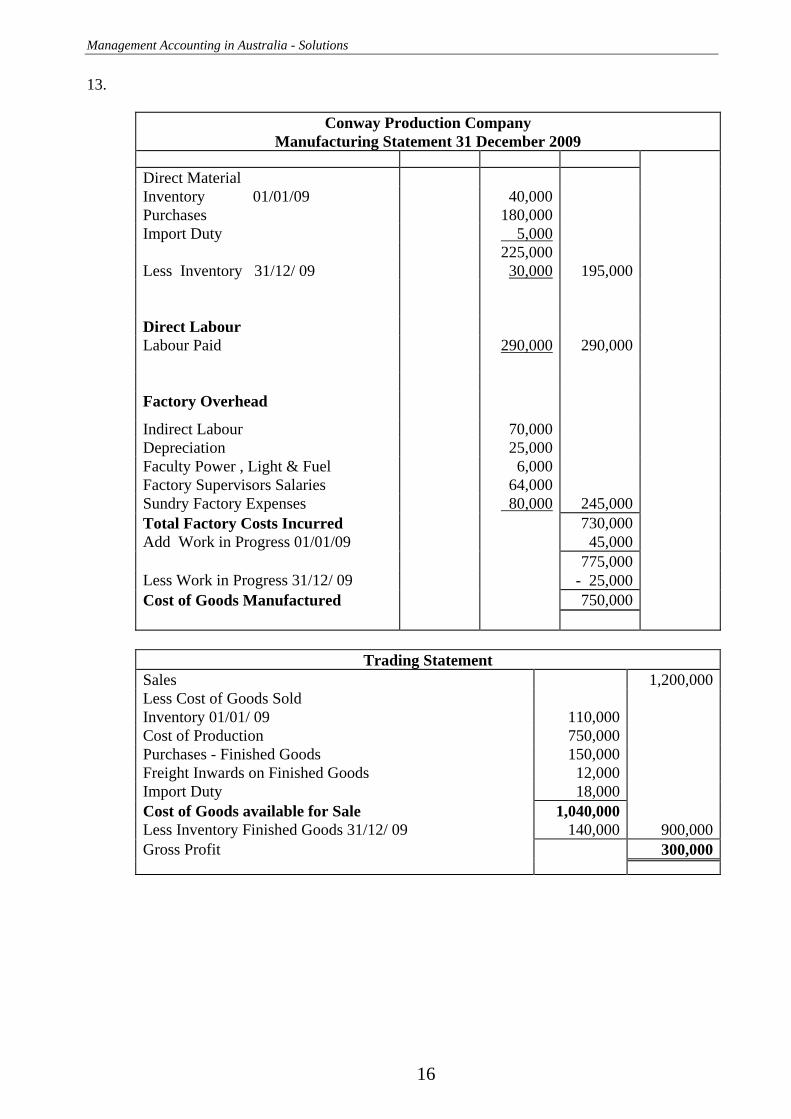

13.

Conway Production Company Manufacturing Statement 31 December 2009

Direct Material Inventory 01/01/09 40,000 Purchases 180,000 Import Duty 5,000 225,000 Less Inventory 31/12/ 09 30,000 195,000 Direct Labour Labour Paid 290,000 290,000 Factory Overhead

Indirect Labour 70,000 Depreciation 25,000 Faculty Power , Light & Fuel 6,000 Factory Supervisors Salaries 64,000 Sundry Factory Expenses 80,000 245,000 Total Factory Costs Incurred 730,000 Add Work in Progress 01/01/09 45,000 775,000 Less Work in Progress 31/12/ 09 - 25,000 Cost of Goods Manufactured 750,000

Trading Statement

Sales 1,200,000Less Cost of Goods Sold Inventory 01/01/ 09 110,000 Cost of Production 750,000 Purchases - Finished Goods 150,000 Freight Inwards on Finished Goods 12,000 Import Duty 18,000 Cost of Goods available for Sale 1,040,000 Less Inventory Finished Goods 31/12/ 09 140,000 900,000Gross Profit 300,000

Chapter 2: Manufacturing & Trading Statements

17

14. Rex Manufacturing Company Pty Ltd -Manufacturing Statement 31 December 2009

Direct Materials Inventory 01/01/09 8,400 Purchases 45,100 Duty on Raw Materials 1,400 54,900 Less Inventory 31/12/ 09 6,900 48,000 Direct Labour Labour Paid 62,000 62,000 Factory Overhead Indirect Labour 13,200 Holiday and Sick Pay 12,300 Factory Power, Light & Fuel 1,800 Factory Managers Salary 18,600 Sundry Factory Expenses 7,800 Depreciation Factory Plant 2,300 56,000 Cost of Production 166,000Work in Progress 01/01/ 09 4,000Less Work in Progress 31/12/ 09 - 10,000Cost of Goods Manufactured 160,000

15.

P. Hogan Manufacturing Statement - 30 June, 2009

Direct Materials Inventory 01/01/09 1,000 Purchases 145,000 Freight Inwards 400 146,400 Less Inventory 30/06/09 - 1,500 144,900 Direct Labour Labour ( 72,000 + 500 – 600 ) 71,900 71,900 Factory Overhead Factory Rent 50,000 Factory Supplies 2,000 Depreciation Factory Plant 11,000 Electricity 4,000 Indirect Labour 6,500 73,500 Cost of Production 290,300Work in Progress 01/01/09 1,200 291,500Less Work in Progress 31/12/09 - 1,500Cost of Goods Manufactured 290,000

Management Accounting in Australia - Solutions

18

16. Manufacturing Statement

30 June 2009 Direct Materials Inventory 1/7/ 08 3,200 Purchases 72,000 Duty on Raw Materials 3,200 Freight Inwards on Raw Material 3,600 82,000 Less Inventory 30/6/09 - 4,000 78,000 Direct Labour Labour ( 66,700 + 3,200 – 2,300 ) 67,600 67,600 Factory Overhead Factory Supplies 01/07/ 08 2,400 Purchases 10,400 12,800 Factory Supplies 30/06/09 – 1,600 11,200 Insurance 400 Factory Light & Power 1,600 Factory Managers Salary 12,000 Foreman’s Wages 8,000 Other Indirect Labour 6,400 Repairs to Machinery 2,000 Other Manufacturing Expenses 14,000 55,600 Cost of Production 201,200 Work in Progress 01/07/ 08 7,200 208,400 Less Work in Progress 30/06/ 09 - 11,200 Cost of Goods Manufactured 197,200

Chapter 2: Manufacturing & Trading Statements

19

17. Amalfi Manufacturing Co Pty Ltd

Manufacturing Statement 30 June 2009 Direct Materials Inventory 1/7/ 08 18,000 Purchases 100,000 Freight Inwards 5,000 123,000 Less Inventory 30/6/ 09 - 19,000 104,000 Direct Labour Labour Paid 80,000 80,000 Factory Overhead Factory Supplies 01/07/ 08 4,500 Purchases 10,000 14,500 Factory Supplies 30/06/09 – 5,500 9,000 Factory Expenses 45,400 Indirect Labour 20,000 74,400Cost of Production 258,400Work in Progress 1/7/ 08 5,500 263,900Less Work in Progress 30/6/ 09 8,500Cost of Goods Manufactured 255,400

Income Statement

Sales 480,000Less Cost of Goods Sold 290,400Inventory 1/7/08 10,000 Cost of Production 255,400 Purchases of Finished Goods 35,000 Freight Inwards 1,000 301,400 Less Inventory 30/6/ 09 11,000 Gross Profit 189,600Add other Operating Income 2,500Discount Received 2,500 192,100Less Expenditure Incurred 56,100Marketing Expenses 11,000 Advertising 4,800 Freight Outwards 6,200 General & Administrative Expenses 42,000 Office Salaries 30,000 Office Rent & Other Expenses 12,000 Financial Expenses 3,100 Discount Allowed 1,100 Interest on Bank Loan 2,000 Net ( Operating ) Profit 136,000

Management Accounting in Australia - Solutions

20

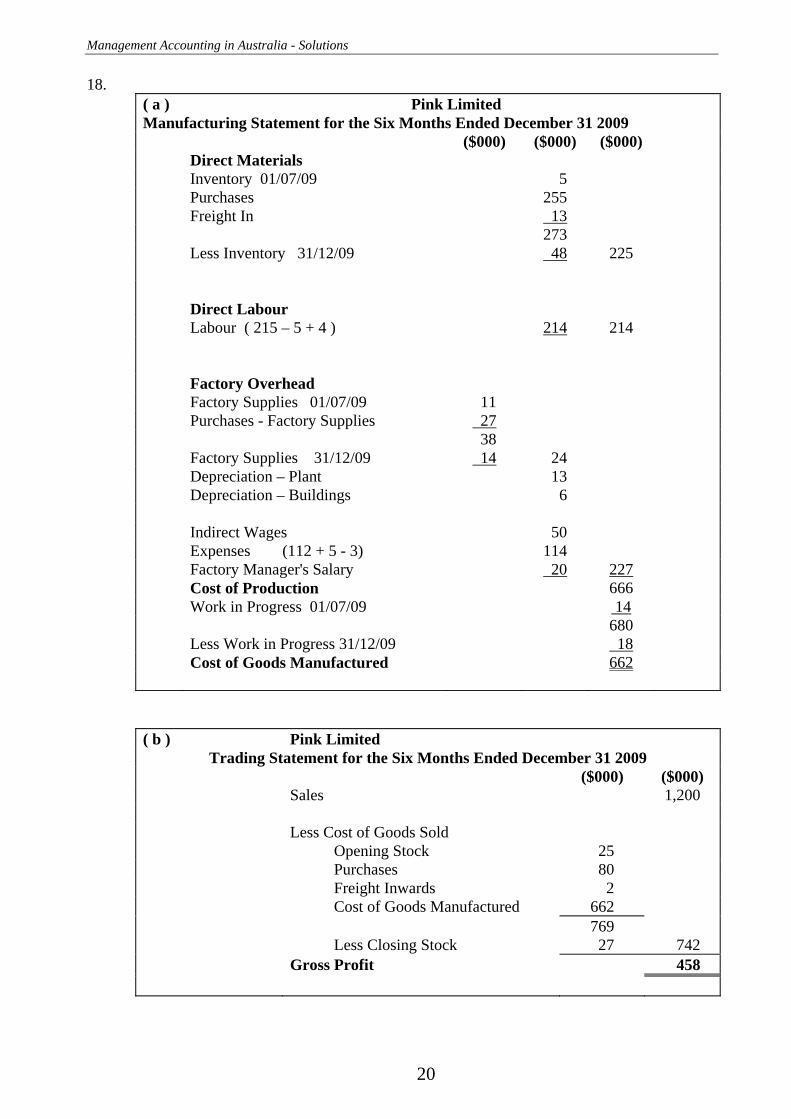

18. ( a ) Pink Limited Manufacturing Statement for the Six Months Ended December 31 2009 ($000) ($000) ($000) Direct Materials Inventory 01/07/09 5 Purchases 255 Freight In 13 273 Less Inventory 31/12/09 48 225 Direct Labour Labour ( 215 – 5 + 4 ) 214 214 Factory Overhead Factory Supplies 01/07/09 11 Purchases - Factory Supplies 27 38 Factory Supplies 31/12/09 14 24 Depreciation – Plant 13 Depreciation – Buildings 6 Indirect Wages 50 Expenses (112 + 5 - 3) 114 Factory Manager's Salary 20 227 Cost of Production 666 Work in Progress 01/07/09 14 680 Less Work in Progress 31/12/09 18 Cost of Goods Manufactured 662

( b ) Pink Limited

Trading Statement for the Six Months Ended December 31 2009 ($000) ($000) Sales 1,200 Less Cost of Goods Sold Opening Stock 25 Purchases 80 Freight Inwards 2 Cost of Goods Manufactured 662 769 Less Closing Stock 27 742 Gross Profit 458

Chapter 2: Manufacturing & Trading Statements

21

19. Direct Materials Bal 01/06/09 60,000 Purchases 240,000 300,000 Direct Materials - 65,000 235,000 Direct Labour Paid & Accrued ( 74,000 + 1,000 ) 75,000 75,000 Factory Overhead Factory Supplies 01/06/09 6,000 Purchases 18,000 24,000 Factory Supplies 30/06/09 - 4,000 20,000 Indirect Lab 10,000 Insurance ( 4,000 + 13,000 – 6,000 ) 11,000 Power – Factory 12,000 Depreciation * 16,000 Rent – Factory 15,000 General – Factory 18,000 102,000 Current Cost of Goods Manufactured 412,000 Plus Opening Balance of W.I.P. 35,000 447,000 Less Closing Balance of W.I.P. - 47,000 Cost of Goods Manufactured 400,000

Trading Statement for the Month June 2009 Sales 900,000

Cost of Goods Sold Finished Goods 01/06/09 100,000 Purchases 50,000 Cost of Goods Manufactured 400,000 550,000 Finished Goods 30/06/09 -50,000 500,000 Gross Profit 400,000 Note: Factory plant and machinery is depreciated at 20% p.a. straight-line. Balance 01 June 2009 960,000 0ne Month 80,000 20% 12 = 16,000

Management Accounting in Australia - Solutions

22

20. Manufacturing Statement for the six months ended 30th June, 2009 Direct Materials Material Inventory 01/01/09 30,000 Purchases 120,000 Cartage and Duty 10,000 160,000 Material Inventory 30/06/09 -10,000 150,000 Direct Labour Paid & Accrued ( 108,500 + 1,500 ) 110,000 110,000 Factory Overhead Factory Supplies 01/01/09 3,000 Purchases 12,000 15,000 Factory Supplies 30/06/09 -2,000 13,000 Indirect Labour ( 40,500 + 500 ) 41,000 Electricity 16,000 Rates ( 6,200 - 200 ) 6,000 General 4,000 Depreciation 15,000 95,000 355,000Work In Progress 01/01/09 44,000 399,000Work In Progress 30/06/09 - 39,000Cost of Goods Manufactured 360,000

Trading Statement for the six month June 2009 Sales 600,000 Cost of Goods Sold Opening Bal Finished Goods 70,000 Purchases 30,000 Cost of Goods Manufactured 360,000 460,000 Closing Bal Finished Goods -20,000 440,000 Gross Profit 160,000

Chapter 2: Manufacturing & Trading Statements

23

21. ( a ) Kangan Manufacturing Statement $ $ $

Direct Materials Opening stock 21,000 Cartage Inwards 4,800 Purchases 96,800

122,600 Less: Closing stock - 21,480 101,120

Direct Labour Direct labour ( 76,950 + 2,000 ) 78,950 78,950

Factory Overhead Factory Supplies Inventory 1 July 1,900 Purchases 11,980 13,880 Less Inventory 30 June 2,360 11,520 Indirect Labour ( 32,340 + 1,060 ) 33,400 Rent ( 22,000 x 50% ) 11,000 Rates & Insurance ( 50% x ( 4,100 + 680 – 940 ) 1,920 Sundry 6,070 Depreciation ( 59,000 x 15% ) 8,850 72,760 252,830 Opening Bal Work In Progress 21,710 274,540 Less Closing Bal Work In Progress - 24,540 Cost of Goods Manufactured $ 250,000 ( b )

Trading Statement $ $

Sales 423,600 Less: Cost of goods sold Opening stock of finished goods 28,320 Cost of Goods Manufactured 250,000

278,320 Less: Closing stock of finished goods 4,720 273,600 Gross Profit $ 150,000

Management Accounting in Australia - Solutions

24

22. ( a ) Brook Vale Manufacturing Statement $ $ $

Direct Materials Opening stock 60,000 Freight Inwards 4,000 Purchases 266,000

330,000 Less: Closing stock - 30,000 300,000

Direct Labour Direct labour ( 123,500 – 1,000 + 2,500) 125,000

Factory Overhead Factory Supplies: Inventory 1 July 12,000 Purchases 38,000 50,000 Less Inventory 30 June 10,000 40,000 Indirect Labour ( Factory Forman ) 49,000 Insurance ( 25% x 4,000 ) + 6,000 7,000 Power 6,000 Depreciation 10,000 112,000 537,000 Opening Bal Work In Progress 35,000 572,000 Less Closing Bal Work In Progress - 20,000 Cost of Goods Manufactured 552,000 ( b )

Trading Statement $ $

Sales 1,140,000 Less: Cost of goods sold Opening stock of finished goods 25,000 Purchases 45,000 Freight Inwards 2,000 Cost of Goods Manufactured 552,000

624,000 Less: Closing stock of finished goods 32,000 592,000 Gross Profit 548,000

Chapter 2: Manufacturing & Trading Statements

25

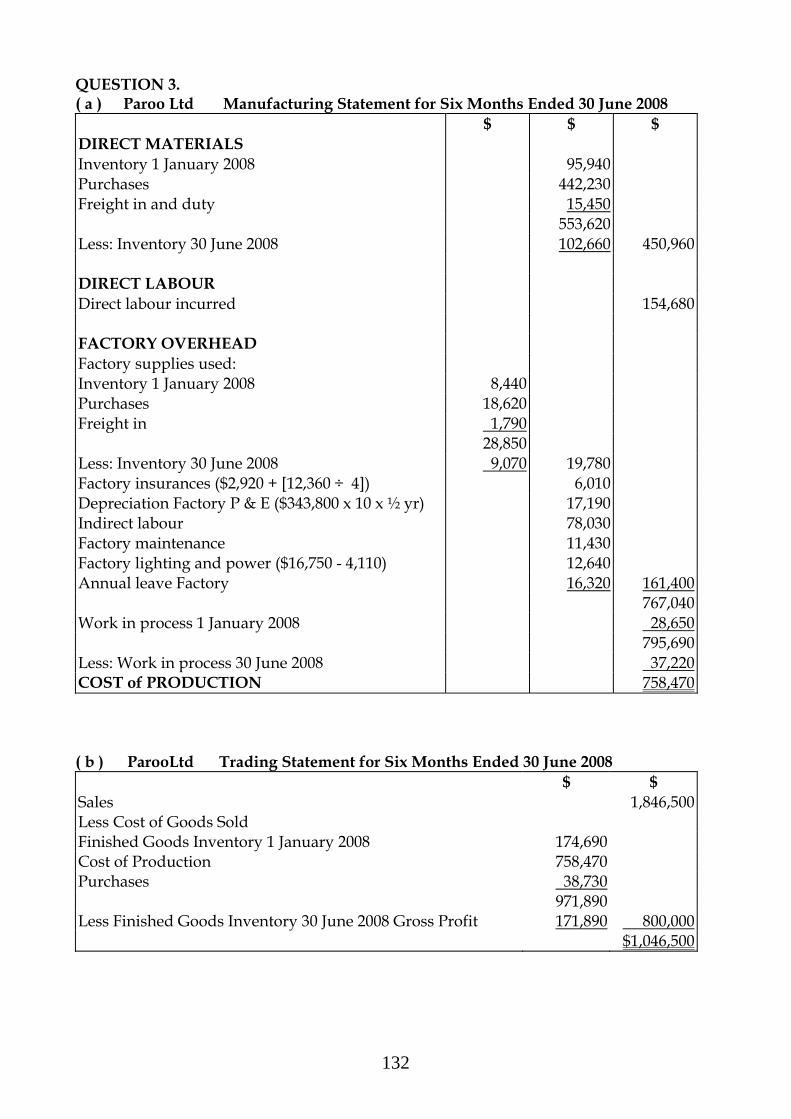

23. ( a ) Radoslow Ltd Manufacturing Statement $ $ $

Direct Materials Opening Inventory 66,000 Purchases 276,000 Freight inwards 12,000

354,000 Less: Closing Inventory 14,000 340,000

Direct Labour Direct labour ( 159,800 + 1,100 – 900 ) 160,000 160,000

Factory Overhead Factory Supplies Inventory 1 July 12,600 Purchases 32,400 45,000 Less Inventory 30 June 12,700 32,300 Indirect Labour 43,340 Insurance ( 3,960 + 3,000 – [ 3,960 x 10/12 ] ) 3,660 Power 5,200 Depreciation 10,500 95,000

595,000 Work In Progress 01/07/2008 15,000 610,000 Work In Progress 30/06/2009 - 10,000 Cost of Production 600,000 ( b )

Trading Statement $ $

Sales 900,000 Less: Cost of Goods Sold Opening Stock of Finished Goods 24,000 Cost of Goods Manufactured 600,000 Purchases 46,700 Freight 2,300

673,000 Less: Closing stock of finished goods 23,000 650,000 Gross Profit 250,000

Management Accounting in Australia - Solutions

26

24. ( a ) Lone Pine Ltd Manufacturing Statement for Year Ended 30 June 2009 DIRECT MATERIALS Inventory 1 July 2008 $ 25,000 Purchases 170,000 Freight inwards 5,000 200,000 Less: Inventory 30 June 2009 20,000 180,000 DIRECT LABOUR Direct Labour incurred ( $119,200 + 800 ) 120,000 120,000 FACTORY OVERHEAD Factory Supplies Inventory 1 July 2008 2,500 Purchases 17,500 20,000 Less: Inventory 30 June 2009 3,000 17,000 Indirect Labour 23,500 Factory Repairs and Maintenance 6,500 Factory Power ( $9,500 + 500 ) 10,000 Factory Waste disposal 3,300 Factory Insurance 4,500 Depreciation – Factory building & machinery 15,300 80,100 380,100 Work In Progress 01/07/08 19,900 400,000 Work In Progress 30/06/09 10,000 Cost of Goods Manufactured 390,000

( b ) Lone Pine Ltd Trading Statement for Year Ended 30 June 2009 Sales 800,000 Less Cost of Goods Sold Finished Goods Inventory 1 July 2008 33,400 Purchases 40,600 Freight Inwards 4,000 Cost of Goods Manufactured 390,000 468,000 Less Finished Goods Inventory 30 June 2009 18,000 450,000 Gross Profit $350,000

Chapter 2: Manufacturing & Trading Statements

27

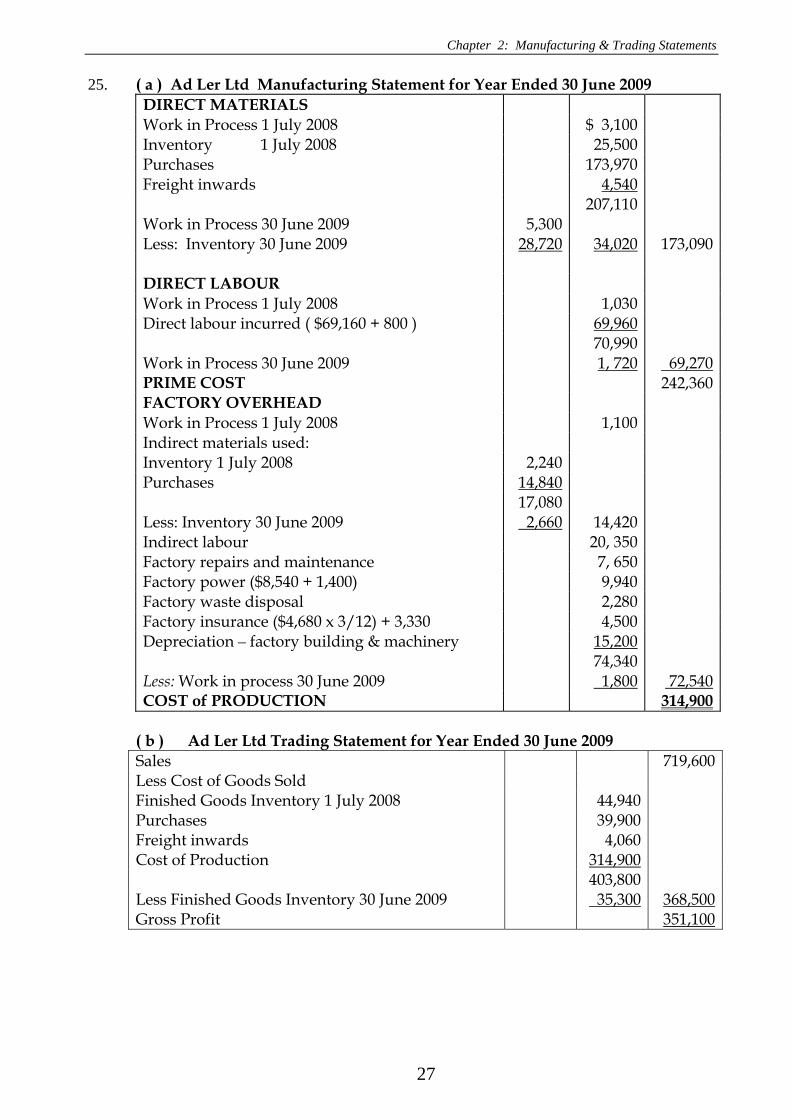

25. ( a ) Ad Ler Ltd Manufacturing Statement for Year Ended 30 June 2009 DIRECT MATERIALS Work in Process 1 July 2008 $ 3,100 Inventory 1 July 2008 25,500 Purchases 173,970 Freight inwards 4,540 207,110 Work in Process 30 June 2009 5,300 Less: Inventory 30 June 2009 28,720 34,020 173,090 DIRECT LABOUR Work in Process 1 July 2008 1,030 Direct labour incurred ( $69,160 + 800 ) 69,960 70,990 Work in Process 30 June 2009 1, 720 69,270 PRIME COST 242,360 FACTORY OVERHEAD Work in Process 1 July 2008 1,100 Indirect materials used: Inventory 1 July 2008 2,240 Purchases 14,840 17,080 Less: Inventory 30 June 2009 2,660 14,420 Indirect labour 20, 350 Factory repairs and maintenance 7, 650 Factory power ($8,540 + 1,400) 9,940 Factory waste disposal 2,280 Factory insurance ($4,680 x 3/12) + 3,330 4,500 Depreciation – factory building & machinery 15,200 74,340 Less: Work in process 30 June 2009 1,800 72,540 COST of PRODUCTION 314,900

( b ) Ad Ler Ltd Trading Statement for Year Ended 30 June 2009 Sales 719,600 Less Cost of Goods Sold Finished Goods Inventory 1 July 2008 44,940 Purchases 39,900 Freight inwards 4,060 Cost of Production 314,900 403,800 Less Finished Goods Inventory 30 June 2009 35,300 368,500 Gross Profit 351,100

Management Accounting in Australia - Solutions

28

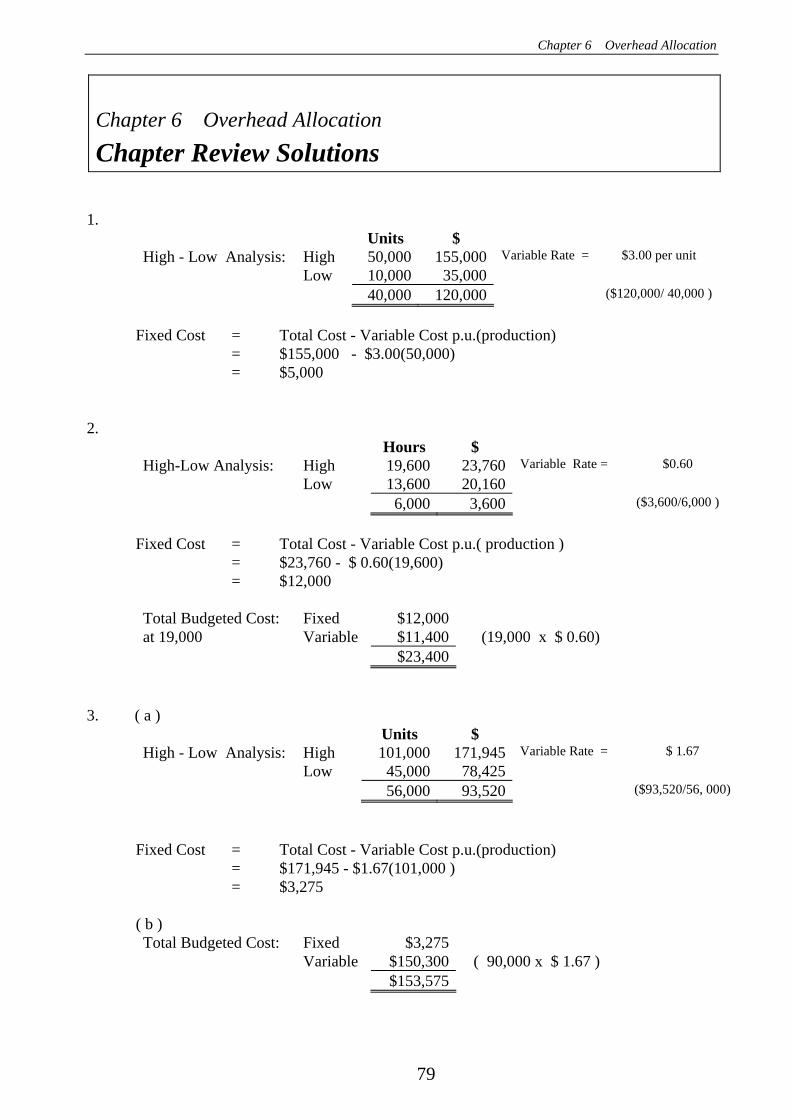

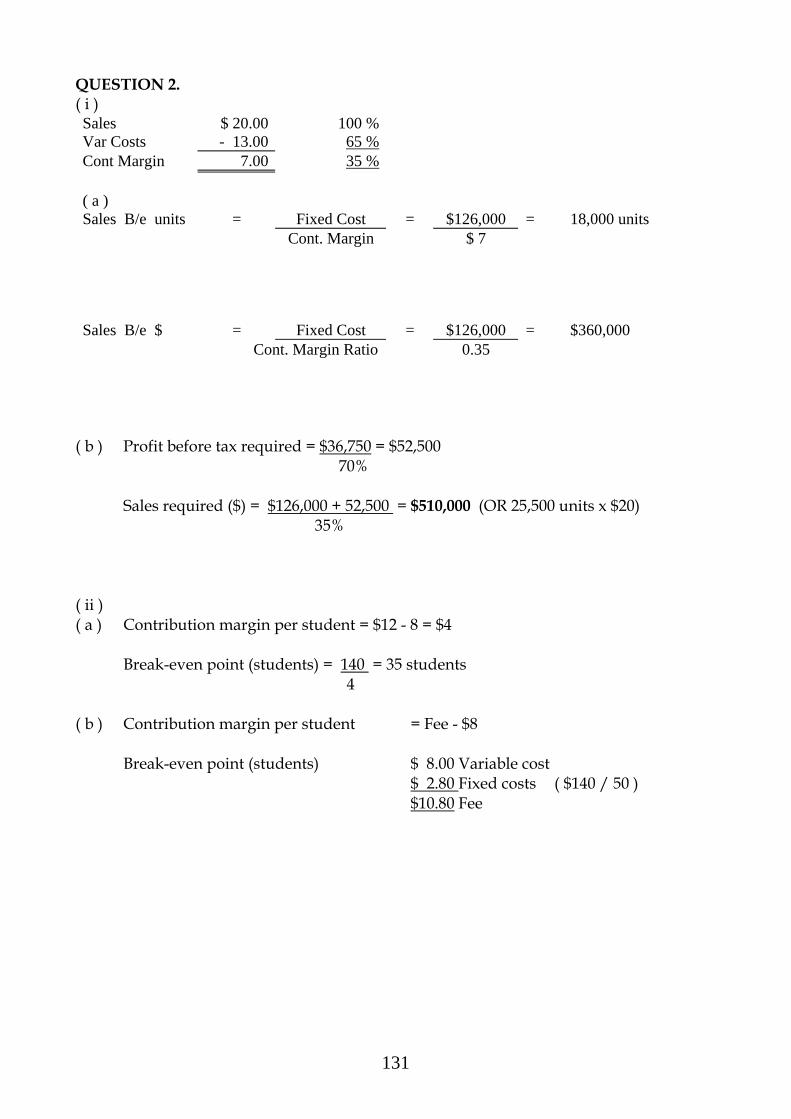

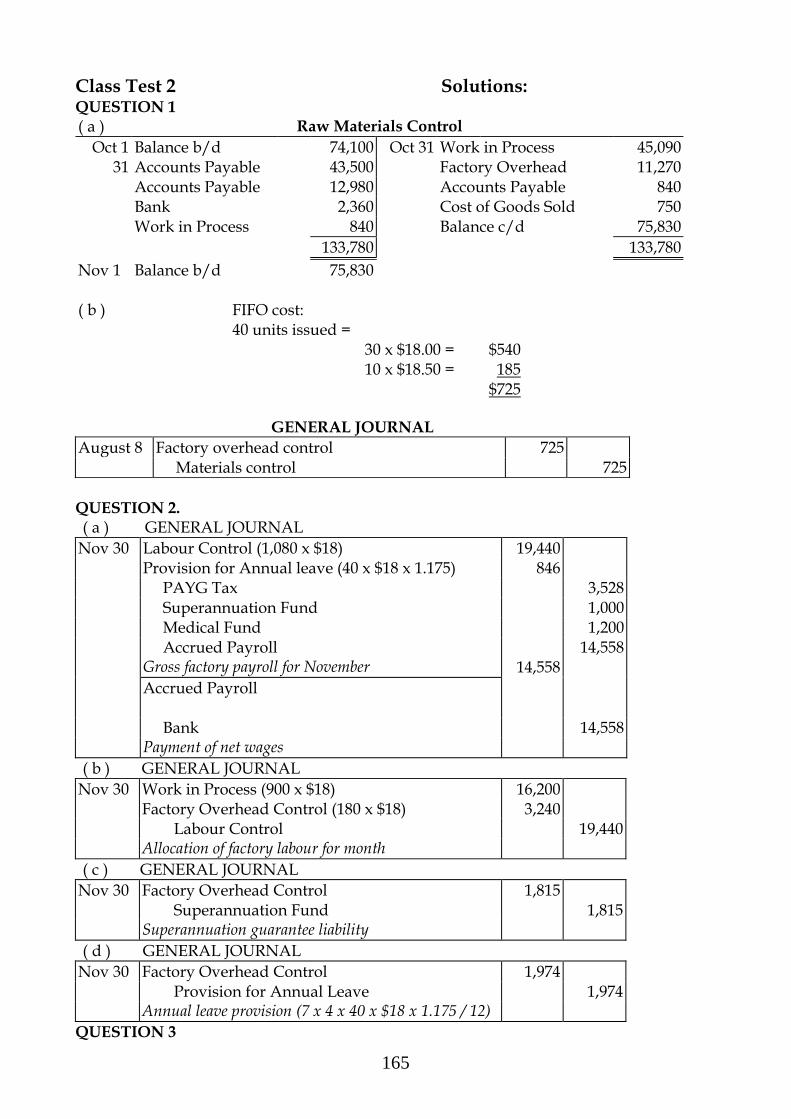

Chapter 3: Cost-Volume-Profit Analysis Chapter Review Solutions

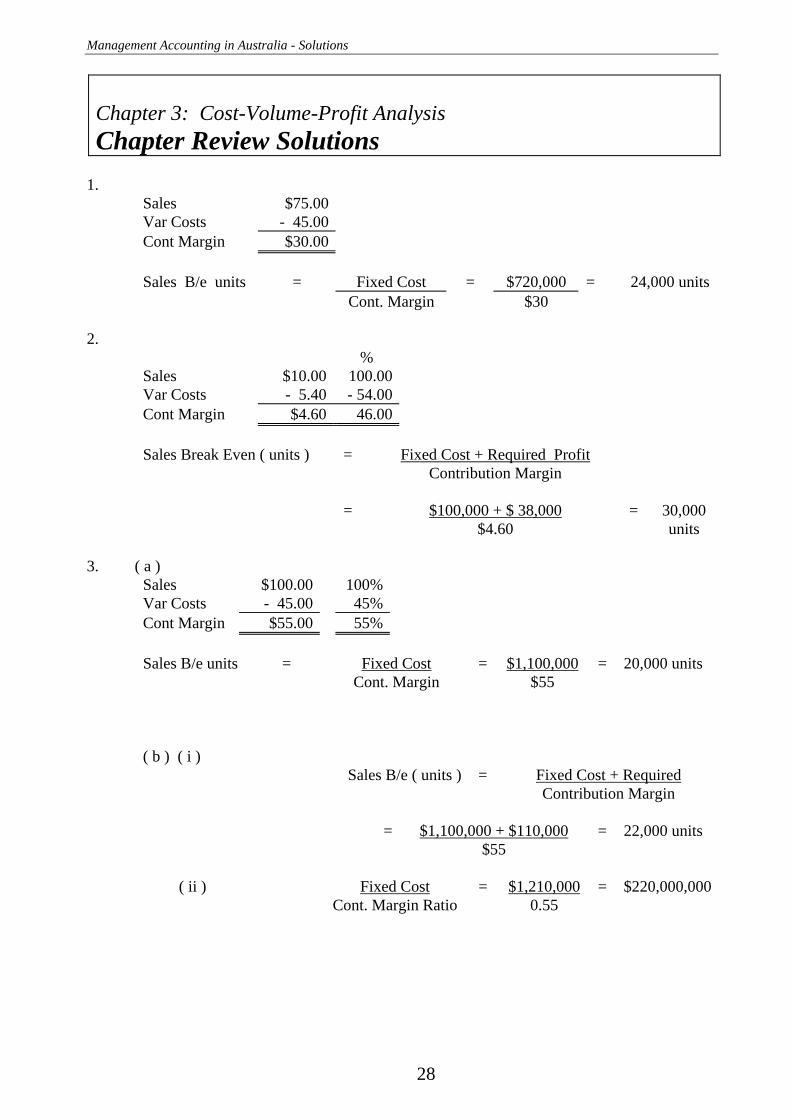

1.

Sales $75.00 Var Costs - 45.00 Cont Margin $30.00 Sales B/e units = Fixed Cost = $720,000 = 24,000 units Cont. Margin $30

2.

% Sales $10.00 100.00 Var Costs - 5.40 - 54.00 Cont Margin $4.60 46.00 Sales Break Even ( units ) = Fixed Cost + Required Profit Contribution Margin = $100,000 + $ 38,000 = 30,000 $4.60 units

3. ( a )

Sales $100.00 100% Var Costs - 45.00 45% Cont Margin $55.00 55% Sales B/e units = Fixed Cost = $1,100,000 = 20,000 units Cont. Margin $55 ( b ) ( i )

Sales B/e ( units ) = Fixed Cost + Required Contribution Margin

= $1,100,000 + $110,000 = 22,000 units

$55

( ii ) Fixed Cost = $1,210,000 = $220,000,000 Cont. Margin Ratio 0.55

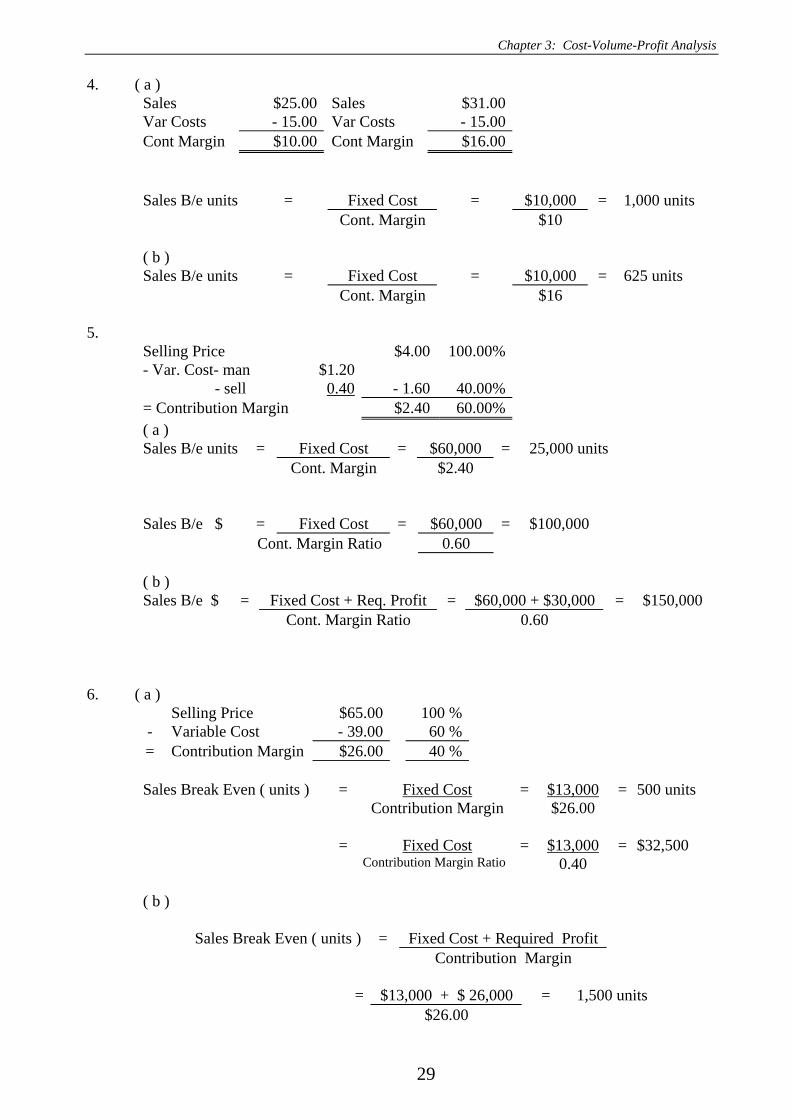

Chapter 3: Cost-Volume-Profit Analysis

29

4. ( a ) Sales $25.00 Sales $31.00 Var Costs - 15.00 Var Costs - 15.00 Cont Margin $10.00 Cont Margin $16.00 Sales B/e units = Fixed Cost = $10,000 = 1,000 units Cont. Margin $10 ( b ) Sales B/e units = Fixed Cost = $10,000 = 625 units Cont. Margin $16

5.

Selling Price $4.00 100.00% - Var. Cost- man $1.20 - sell 0.40 - 1.60 40.00% = Contribution Margin $2.40 60.00% ( a ) Sales B/e units = Fixed Cost = $60,000 = 25,000 units Cont. Margin $2.40 Sales B/e $ = Fixed Cost = $60,000 = $100,000 Cont. Margin Ratio 0.60 ( b ) Sales B/e $ = Fixed Cost + Req. Profit = $60,000 + $30,000 = $150,000 Cont. Margin Ratio 0.60

6. ( a ) Selling Price $65.00 100 % - Variable Cost - 39.00 60 % = Contribution Margin $26.00 40 %

Sales Break Even ( units ) = Fixed Cost = $13,000 = 500 units Contribution Margin $26.00 = Fixed Cost = $13,000 = $32,500 Contribution Margin Ratio 0.40 ( b ) Sales Break Even ( units ) = Fixed Cost + Required Profit Contribution Margin

= $13,000 + $ 26,000 = 1,500 units $26.00

Management Accounting in Australia - Solutions

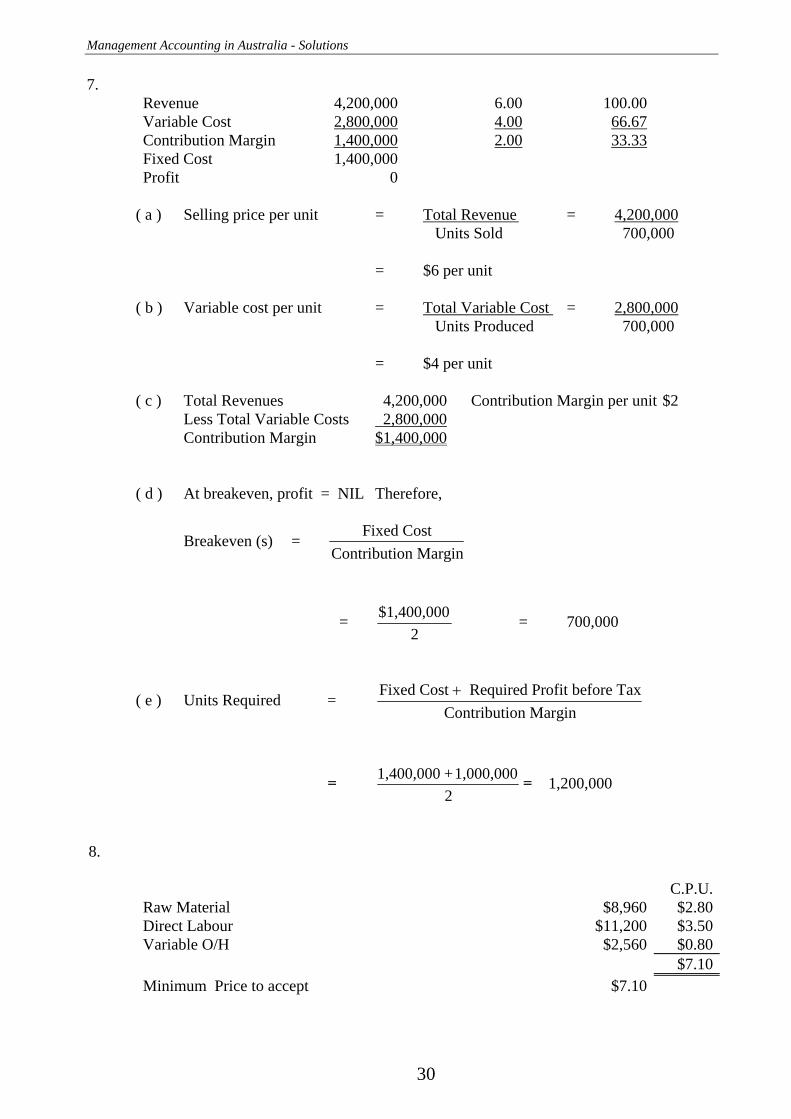

7. Revenue 4,200,000 6.00 100.00 Variable Cost 2,800,000 4.00 66.67 Contribution Margin 1,400,000 2.00 33.33 Fixed Cost 1,400,000 Profit 0

( a ) Selling price per unit = Total Revenue = 4,200,000 Units Sold 700,000 = $6 per unit ( b ) Variable cost per unit = Total Variable Cost = 2,800,000 Units Produced 700,000 = $4 per unit ( c ) Total Revenues 4,200,000 Contribution Margin per unit $2 Less Total Variable Costs 2,800,000 Contribution Margin $1,400,000 ( d ) At breakeven, profit = NIL Therefore,

Breakeven (s) = Fixed CostContribution Margin

= 2

$1,400,000 = 700,000

( e ) Units Required = Fixed Cost Required Profit before TaxContribution Margin+

= 2

1,000,000 + 1,400,000 = 1,200,000

8.

C.P.U.Raw Material $8,960 $2.80Direct Labour $11,200 $3.50Variable O/H $2,560 $0.80 $7.10Minimum Price to accept $7.10

30

Chapter 3: Cost-Volume-Profit Analysis

31

9. Sales 75 100.00 Variable Cost 25 33.33 Contribution Margin 50 66.67 Fixed Cost 300,000 Profit ?

( a ) Breakeven (s) = Fixed CostContribution Margin

= 50

$300,000 = 6,000 units

( b ) To make an operating profit of $15,000 Fixed Costs + Required Profit = 300,000 + 15,000 = 6,300 Units

Contribution Margin 50 ( c ) At 7,000 units,

Sales 7,000 x 75 525,000 Less Costs: Variable Costs 7,000 x 25 175,000 Equals Contribution Margin 350,000

Less Fixed Costs 300,000 Operating Profit $50,000

( d ) Sales 60 100.00

Less Variable Cost - 25 42.00 Equals Contribution Margin 35 58.00

Breakeven (s) = Fixed CostContribution Margin

= 35

$297,500 = 8,500 units

( e ) Sales 75 100.00

Less Variable Cost - 15 20.00 Equals Contribution Margin 60 80.00

Breakeven (s) = Fixed CostContribution Margin

= 60

$300,000 = 5,000 units

( f ) New fixed costs = 300,000 + 50,000 = $350,000 per annum

Breakeven (s) = Fixed CostContribution Margin

= 50

$350,000 = 7,000 units

Management Accounting in Australia - Solutions

10. Sales 12 100.00 Variable Cost 10 83.33 Contribution Margin 2 16.67 Fixed Cost 25,000 Profit ?

( a ) At breakeven profit = NIL

Breakeven (s) = Fixed CostContribution Margin

= 2

$25,000 = 12,500 units

( b ) Operating profit of $50,000 Fixed Costs + Required Profit = 25,000 + 50,000 = 37,500 Units

Contribution Margin 2 ( c ) Operating profit - 10% of sales revenue ( C.M. = 12 – 10 – 1.2 )

Breakeven (s) = Fixed CostContribution Margin

= 0.80

$25,000 = 31,250 units

( d ) Sales 12.00 100.00 Variable Cost Mfg 9.20 Variable Cost Mkt 2.00 11.20 93.33 Contribution Margin 0.80 6.67 Fixed Cost 25,000 Profit ?

Breakeven (s) = Fixed CostContribution Margin

= 0.80

$25,000 = 31,250 units

( e ) At 10,000 units Sales 10,000 x 12 120,000 Less Costs and expenses Variable Manufacturing costs 10,000 x 8 80,000 Variable marketing costs 10,000 x 2 20,000 100,000 Equals Contribution Margin 20,000 Fixed manufacturing costs 15,000 Fixed marketing and admin costs 10,000 25,000 Operating Loss - 5,000

32

Chapter 3: Cost-Volume-Profit Analysis

33

11. Revenue 130,000 20.00 100.00 Variable Cost 74,750 11.50 57.50 Contribution Margin 55,250 8.50 42.50 Fixed Cost 48,100 Profit 7,150

( a ) Required Sales = 10,200 = $24,000

0.4250

∴ sales must increase by $24,000 (154,000 - 130,000)

( b ) New Variable Exp. per Unit = $10.35 11.50 x 0.90 New Contribution Margin = $9.65 $20.00 - 10.35 New Sales Volume = 6,175 6,500 units x 0.95 ∴ new net profit = Contribution Margin - Fixed Expenses = (6,175 x 9.65) - (48,100 + 5,000) = 59,588.75 - 53,100 = $6,488.75 ∴ the company should not reduce sales commissions as the net profit would reduce

from $7,150 to $6,488.75. ( c ) New Variable Expenses = $12.65 11.50 x 1.1

New Fixed Expenses = $40,885 48,100 x 0.85 New Sales Volume = 7,800 units 6,500 x 1.2 Contribution Margin Ratio = 0.3675 1 - (12.65/20.00) Break-even = $111,252 40,885/0.3675 ( d ) New Sales = 8,320 units 6,500 x 1.28 New Contribution Margin = $70,720 8,320 x 8.50 Expected Net Profit = Contribution Margin - Fixed Expenses = 70,720 - 48,100 = 22,620 Actual Net Profit = $25,025 7,150 + (7,150 x 2.5) ∴ the company did better than expected.

Management Accounting in Australia - Solutions

12. Sales 600 100.00 Variable Cost 420 70.00 Contribution Margin 180 30.00 Fixed Cost 360,000 Profit ?

( a ) Breakeven Sales (units) = Fixed CostsContribution Margin

= 360,000180

= 2,000 units

Breakeven Sales ($) = Fixed CostsContribution Margin Ratio

= 0.30

360,000 = $1,200,000

( b ) Contribution Margin (1,800 machines x $180) $324,000 less: Fixed Costs 360,000 Net Less - 36,000 ( c ) Workings: Selling Price/unit = $600 Variable Cost/unit 425 Contribution Margin $175

Breakeven Sales (units) = 360,000175

= 2,057 units

2,057 units x $600 = $1,234,200

( d ) Sales (units) = Fixed Costs + Desired ProfitContribution Margin

= 180

180,000 + 360,000 = 180

540,000 = 3,000 units

( e ) 1. All costs can be classified into fixed and variable costs. 2. All costs are linear in the relevant range, i.e., variable basis change in total with a change in volume and fixed costs in total remain constant. 3. Selling price will not charge over the range of sales activity. 4. Cost efficiencies remain the same for each product.

34

Chapter 3: Cost-Volume-Profit Analysis

35

13. ( a ) $ per unit % Selling Price 576,000 8.00 100.00 Less Variable costs 216,000 3.00 37.50 Contribution margin per unit 360,000 5.00 62.50 Less Fixed Costs 200,000 Equals Profit 160,000

( b )

Break-even point ( units ) = $200,000 = 40,000 units $5.00

Break-even point ( $ ) = $200,000 = $320,000 0.625

( c )

Sales req for profit = $200,000 + $320,000 = 104,000 unitsof $320,000 $5.00

( d )

Margin of Safety = 576,000 – 320,000 = $256,000

( e )

$ per unit % Selling Price 8.00 100.00 Less Variable costs 2.00 25.00 Contribution margin per unit 6.00 75.00 ( i ) Sales B/even = $250,000 = 62,500 units $4.00

( f )

Selling Price 100.00Less Variable costs 37.50 Variable selling costs 12.50Contribution margin per unit 50.00

Break-even point ( $ ) = $200,000 = $400,000 0.5

Management Accounting in Australia - Solutions

36

14. Sales 40 100.00 Variable Cost 15 37.50 Contribution Margin 25 62.50 Fixed Cost 45,000 Profit ?

( a ) Fixed Costs . = $ 45,000 = 1,800 Units Contribution Margin $25.00 ( b ) Fixed Costs + Required Profit = $ 125,000 = 5,000 Units Contribution Margin $25.00 ( c ) Fixed Costs + Required Profit = $ 137,500 = 5,500 Units Contribution Margin $25.00 ( $64,750 / 0.7 ) = $92,500 ( d ) Sales ( 4,400 x $40.00 ) $176,000

Less Variable Costs ( 4,400 x $15.00 ) 66,000- Equals Contribution Margin 110,000

Less Fixed Costs - 45,000 Equals Profit $ 65,000

( e ) Sales ( 4,000 x $44.00 ) $176,000

Less Variable Costs ( 4,000 x $15.00 ) 60,000- Equals Contribution Margin 116,000

Less Fixed Costs - 45,000 Equals Profit $ 71,000

Chapter 3: Cost-Volume-Profit Analysis

37

15. ( a ) Revenue 1,920,000 80.00 100.00 Variable Cost 1,152,000 48.00 60.00 Contribution Margin 768,000 32.00 40.00 Fixed Cost 600,000 Profit 168,000

Fixed Costs . = $ 600,000 = 18,750 Units Contribution Margin $32 ( b ) Revenue 1,920,000 80.00 100.00 Variable Cost 1,152,000 60.00 75.00 Contribution Margin 768,000 20.00 25.00 Fixed Cost 600,000 Profit 168,000

Fixed Costs . = $ 600,000 = $2,400,000 Contribution Margin Ratio 0.25 ( c ) Hours = 1,920,000 = 24,000 hrs

80 Variable cost = 1,152,000 = $48 Hours 24,000

16. $ % Selling Price 500 100.00 Fixed Costs $ 900,000

- Variable Cost 300 60.00 = Contribution Margin 200 40.00

( a ) Fixed Costs = $ 900,000 = $ 2,250,000

Contribution Margin Ratio 0.40

( b ) Fixed Costs = $ 900,000 = 4,500 Units Contribution Margin 200.00

( c ) Sales 5,000 x $500 $ 2,500,000 - Variable Costs 5,000 x $300 $ 1,500,000 = Contribution Margin $ 1,000,000 - Fixed Costs $ 900,000 $ 100,000

( d ) Sales Actual $ 2,500,000 Sales Breakeven $ 2,250,000 Margin of Safety $ 250,000 10.00% $ 2,500,000

Management Accounting in Australia - Solutions

38

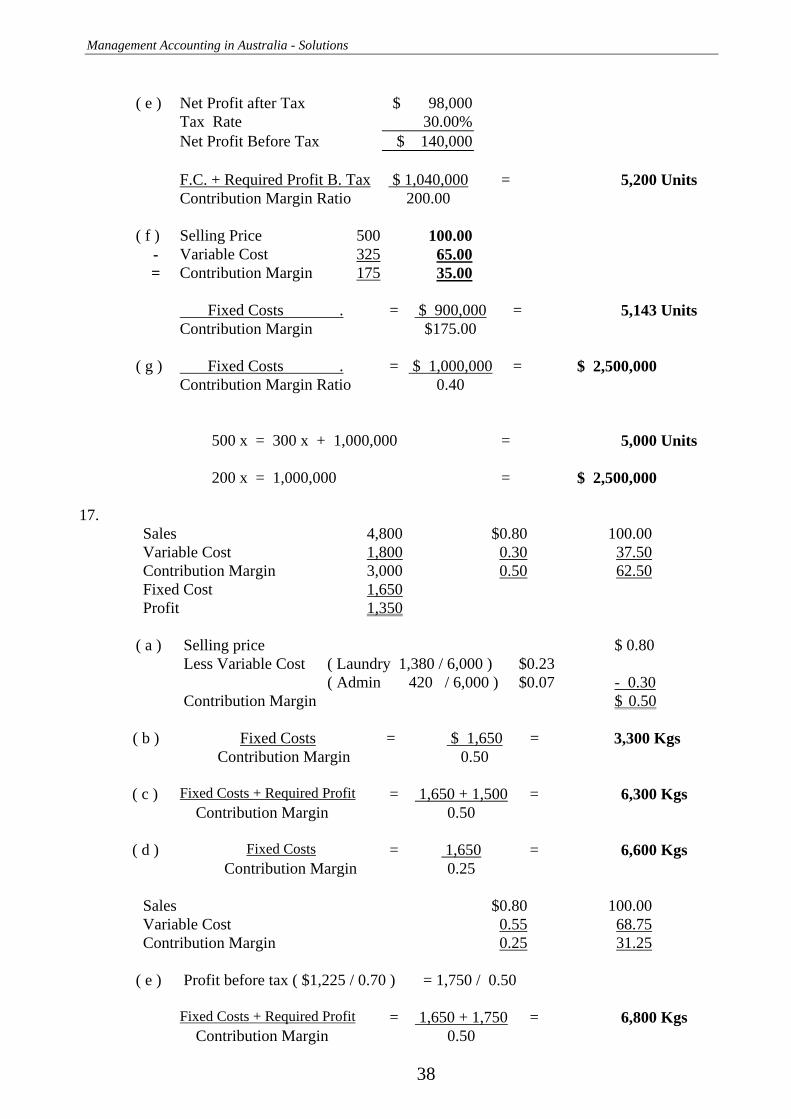

( e ) Net Profit after Tax $ 98,000

Tax Rate 30.00% Net Profit Before Tax $ 140,000 F.C. + Required Profit B. Tax $ 1,040,000 = 5,200 Units Contribution Margin Ratio 200.00

( f ) Selling Price 500 100.00

- Variable Cost 325 65.00 = Contribution Margin 175 35.00

Fixed Costs . = $ 900,000 = 5,143 Units Contribution Margin $175.00 ( g ) Fixed Costs . = $ 1,000,000 = $ 2,500,000 Contribution Margin Ratio 0.40

500 x = 300 x + 1,000,000 = 5,000 Units 200 x = 1,000,000 = $ 2,500,000

17.

Sales 4,800 $0.80 100.00 Variable Cost 1,800 0.30 37.50 Contribution Margin 3,000 0.50 62.50 Fixed Cost 1,650 Profit 1,350

( a ) Selling price $ 0.80

Less Variable Cost ( Laundry 1,380 / 6,000 ) $0.23 ( Admin 420 / 6,000 ) $0.07 - 0.30 Contribution Margin $ 0.50 ( b ) Fixed Costs = $ 1,650 = 3,300 Kgs

Contribution Margin 0.50

( c ) Fixed Costs + Required Profit = 1,650 + 1,500 = 6,300 Kgs Contribution Margin 0.50 ( d ) Fixed Costs = 1,650 = 6,600 Kgs Contribution Margin 0.25

Sales $0.80 100.00 Variable Cost 0.55 68.75 Contribution Margin 0.25 31.25

( e ) Profit before tax ( $1,225 / 0.70 ) = 1,750 / 0.50

Fixed Costs + Required Profit = 1,650 + 1,750 = 6,800 Kgs Contribution Margin 0.50

Chapter 3: Cost-Volume-Profit Analysis

39

18. Total C.P.U. % Sales 500,000 5.00 100 Less Variable costs 300,000 3.00 60 Contribution margin 200,000 2.00 40 Fixed Costs 60,000 Gross Profit 140,000

( a )

Break-even point ( Q ) = 60,000 / 2.00 = 30,000 units Break-even point ( $ ) = 60,000 / 0.40 = $150,000

( b )

Margin of Safety = 100,000 – 30,000 x 100 = 70.00% 100,000

( c )

Sales req for profit = 60,000 + 90,000 = $ 375,000 of $90,000 before tax ( 0.40 )

( d )

Sales req for profit = 60,000 + 60,000 = $ 300,000 of $42,000 after tax ( 0.40 )

( e )

Sales req for add = 100,000 + 60,000 = $ 400,000 fixed costs $40,000 ( 0.40 )

Management Accounting in Australia - Solutions

40

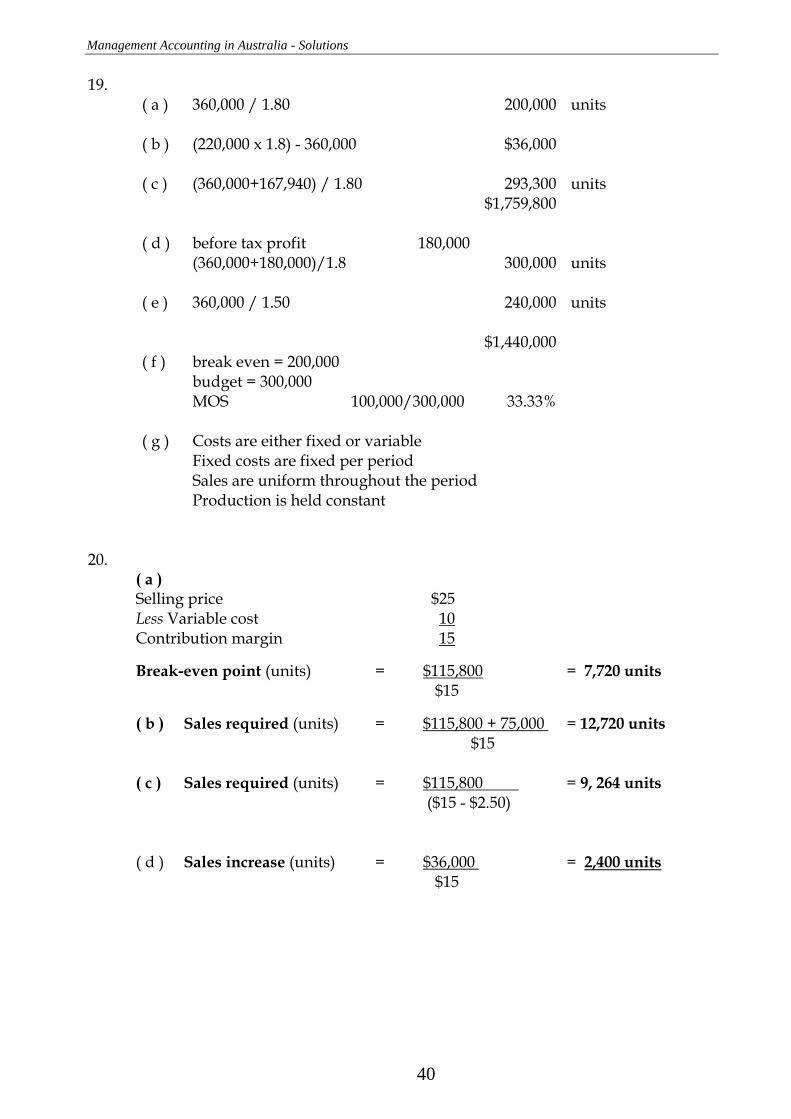

19. ( a ) 360,000 / 1.80 200,000 units ( b ) (220,000 x 1.8) - 360,000 $36,000 ( c ) (360,000+167,940) / 1.80 293,300 units $1,759,800 ( d ) before tax profit 180,000 (360,000+180,000)/1.8 300,000 units ( e ) 360,000 / 1.50 240,000 units $1,440,000 ( f ) break even = 200,000 budget = 300,000 MOS 100,000/300,000 33.33% ( g ) Costs are either fixed or variable Fixed costs are fixed per period Sales are uniform throughout the period Production is held constant

20.

( a ) Selling price $25 Less Variable cost 10 Contribution margin 15

Break-even point (units) = $115,800 = 7,720 units $15

( b ) Sales required (units) = $115,800 + 75,000 = 12,720 units $15 ( c ) Sales required (units) = $115,800 = 9, 264 units ($15 - $2.50) ( d ) Sales increase (units) = $36,000 = 2,400 units $15

Chapter 3: Cost-Volume-Profit Analysis

41

21 % Selling Price 16.00 100.00 Variable Cost 8.00 50.00 Contribution Margin 8.00 50.00

( a ) Break-even point (units) = $55,000 = 6,875 units $8

Break-even point ( $ ) = $55,000 = $110,000 0.50 ( b ) Profit before tax $28,000 Sales required (units) = $55,000 + $28,000 = 10, 375 units $8

( c ) Profit after tax $31,500 Sales required (units) = $55,000 + $45,000 = 12, 500 units $8

( d ) Margin on Safety = 12,900 - 6,875 = 6,025 units

= 6,025 x $16 = $96,400

Management Accounting in Australia - Solutions

42

Chapter 4: The Cost Accounting Cycle

Chapter Review Solutions

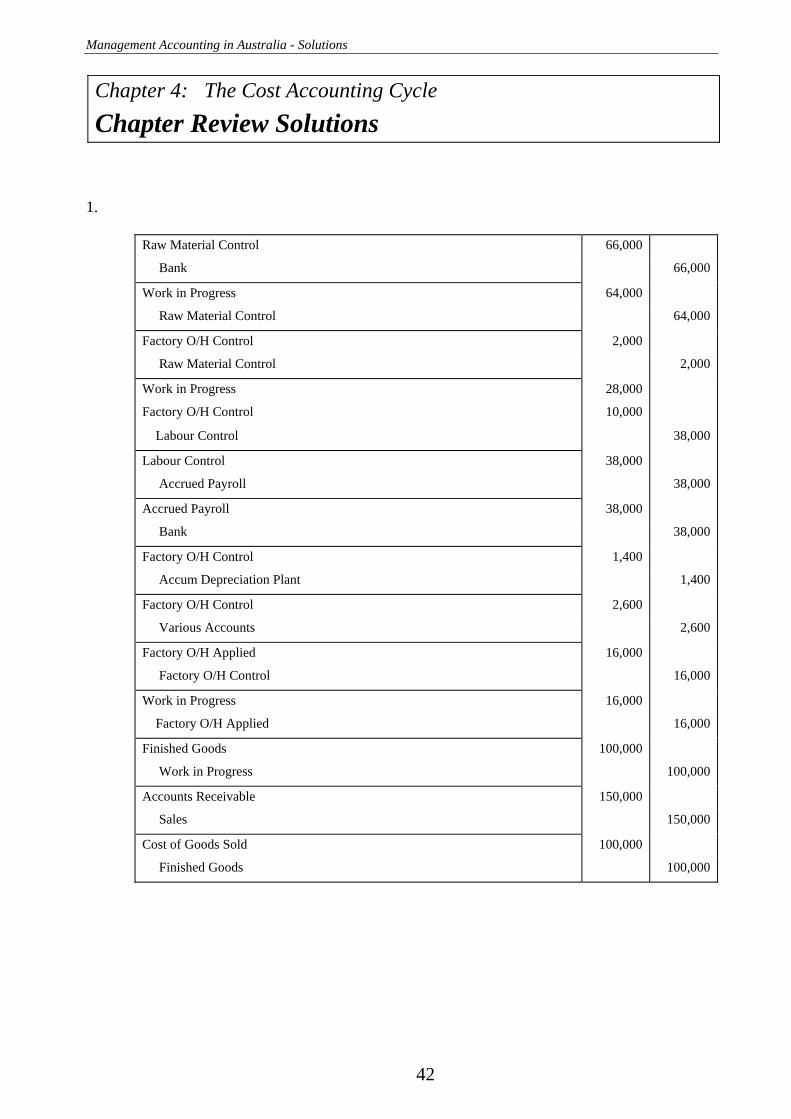

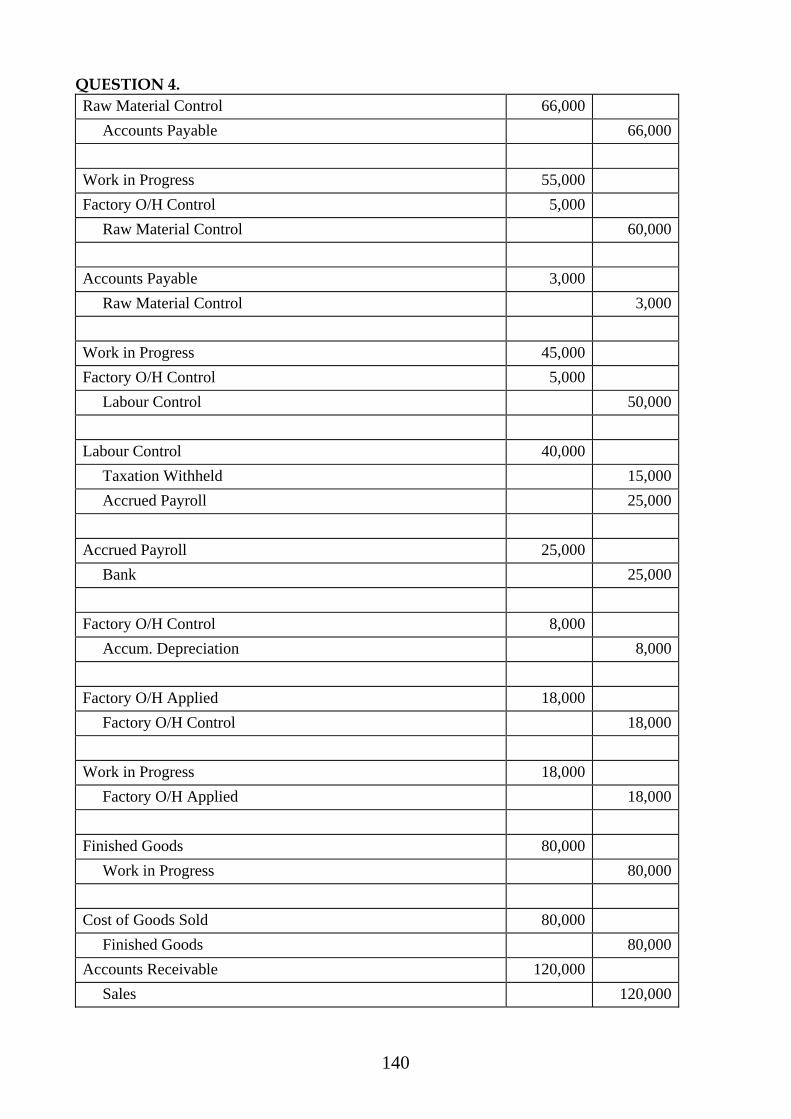

1.

Raw Material Control 66,000

Bank 66,000

Work in Progress 64,000

Raw Material Control 64,000

Factory O/H Control 2,000

Raw Material Control 2,000

Work in Progress 28,000

Factory O/H Control 10,000

Labour Control 38,000

Labour Control 38,000

Accrued Payroll 38,000

Accrued Payroll 38,000

Bank 38,000

Factory O/H Control 1,400

Accum Depreciation Plant 1,400

Factory O/H Control 2,600

Various Accounts 2,600

Factory O/H Applied 16,000

Factory O/H Control 16,000

Work in Progress 16,000

Factory O/H Applied 16,000

Finished Goods 100,000

Work in Progress 100,000

Accounts Receivable 150,000

Sales 150,000

Cost of Goods Sold 100,000

Finished Goods 100,000

Chapter 4: The Cost Accounting Cycle

43

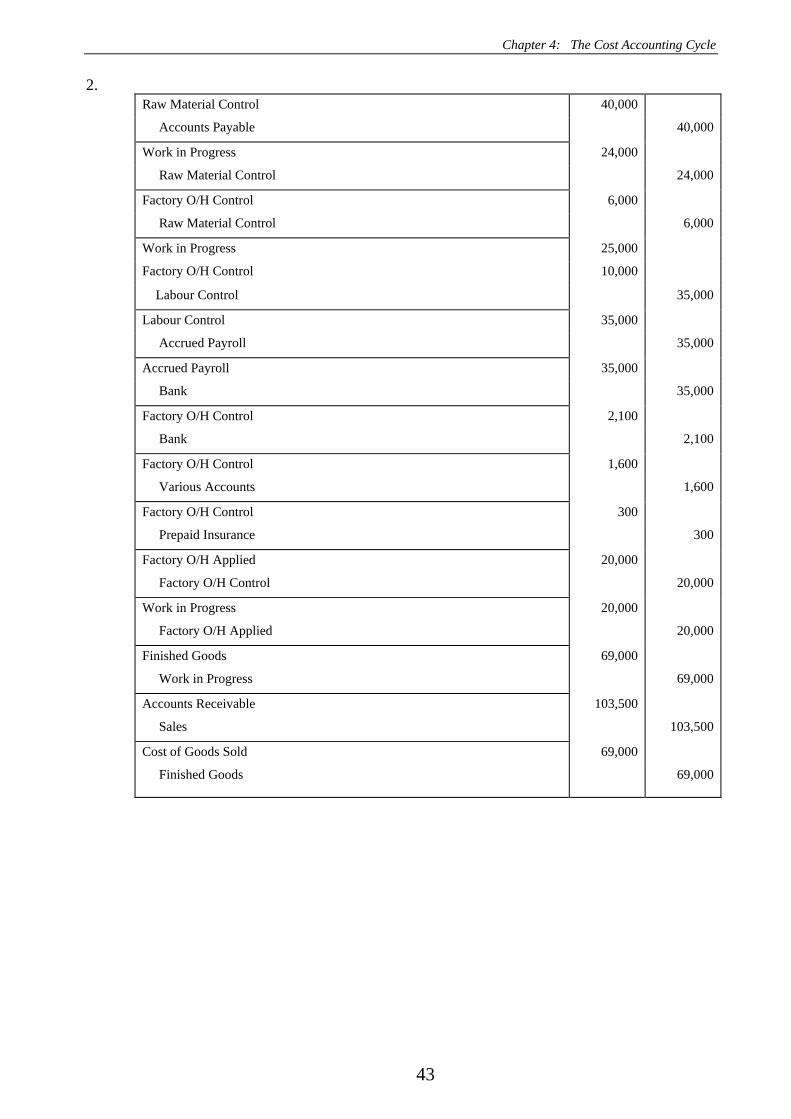

2. Raw Material Control 40,000

Accounts Payable 40,000

Work in Progress 24,000

Raw Material Control 24,000

Factory O/H Control 6,000

Raw Material Control 6,000

Work in Progress 25,000

Factory O/H Control 10,000

Labour Control 35,000

Labour Control 35,000

Accrued Payroll 35,000

Accrued Payroll 35,000

Bank 35,000

Factory O/H Control 2,100

Bank 2,100

Factory O/H Control 1,600

Various Accounts 1,600

Factory O/H Control 300

Prepaid Insurance 300

Factory O/H Applied 20,000

Factory O/H Control 20,000

Work in Progress 20,000

Factory O/H Applied 20,000

Finished Goods 69,000

Work in Progress 69,000

Accounts Receivable 103,500

Sales 103,500

Cost of Goods Sold 69,000

Finished Goods 69,000

Management Accounting in Australia - Solutions

44

3.

Raw Material Control 20,000

A/c Payable 20,000

Work in Progress 15,000

Factory O/H Control 2,000

Raw Material Control 17,000

Work in Progress 17,000

Factory O/H Control 2,000

Labour Control 19,000

Labour Control 19,000

PAYG Tax Withheld 3,000

Accrued Payroll 16,000

Accrued Payroll 16,000

Bank 16,000

Factory O/H Control 8,500

Bank ( Rent Paid ) 8,500

Factory O/H Control 7,500

Accumulated Depreciation Plant 7,500

Factory O/H Applied 20,000

Factory O/H Control 20,000

Work in Progress 20,000

Factory O/H Applied 20,000

Finished Goods 32,000

Work in Progress 32,000

Accounts Receivable 29,000

Sales 29,000

Cost of Goods Sold 22,000

Finished Goods 22,000

Chapter 4: The Cost Accounting Cycle

45

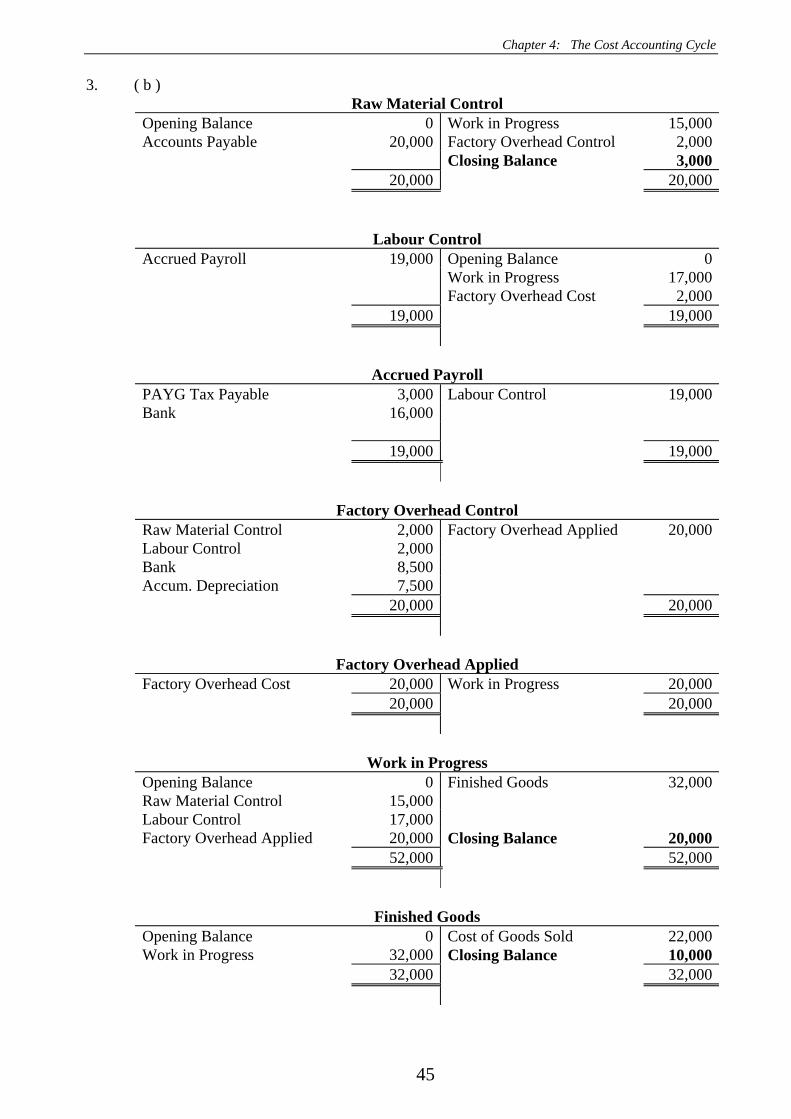

3. ( b ) Raw Material Control

Opening Balance 0 Work in Progress 15,000Accounts Payable 20,000 Factory Overhead Control 2,000 Closing Balance 3,000 20,000 20,000

Labour Control Accrued Payroll 19,000 Opening Balance 0 Work in Progress 17,000 Factory Overhead Cost 2,000 19,000 19,000

Accrued Payroll PAYG Tax Payable 3,000 Labour Control 19,000Bank 16,000 19,000 19,000

Factory Overhead Control Raw Material Control 2,000 Factory Overhead Applied 20,000Labour Control 2,000 Bank 8,500 Accum. Depreciation 7,500 20,000 20,000

Factory Overhead Applied Factory Overhead Cost 20,000 Work in Progress 20,000 20,000 20,000

Work in Progress Opening Balance 0 Finished Goods 32,000Raw Material Control 15,000 Labour Control 17,000 Factory Overhead Applied 20,000 Closing Balance 20,000 52,000 52,000

Finished Goods Opening Balance 0 Cost of Goods Sold 22,000Work in Progress 32,000 Closing Balance 10,000 32,000 32,000

Management Accounting in Australia - Solutions

46

4. Raw Material Control 60,000 Accounts Payable 60,000Work in Progress 44,000 Factory O/H Control 16,000 Raw Material Control 60,000Work in Progress 26,000 Factory O/H Control 4,000 Labour Control 30,000Labour Control 30,000 Taxation Withheld 10,000 Accrued Payroll 20,000Accrued Payroll 20,000 Bank 20,000Factory O/H Control 10,000 Accum. Depreciation 10,000Factory O/H Applied 30,000 Factory O/H Control 30,000Work in Progress 30,000 Factory O/H Applied 30,000Finished Goods 90,000 Work in Progress 90,000Cost of Goods Sold 50,000 Finished Goods 50,000Accounts Receivable 75,000 Sales 75,000

Chapter 4: The Cost Accounting Cycle

47

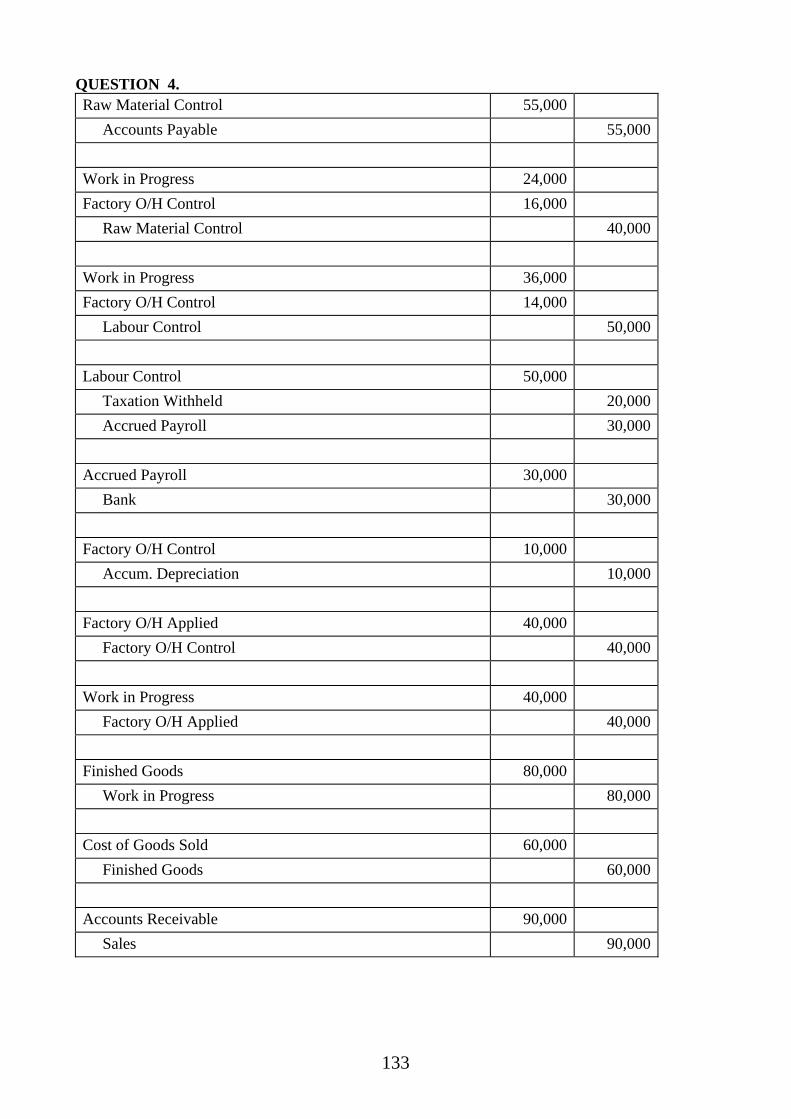

5. Raw Material Control 50,000 Accounts Payable 50,000Work in Progress 32,000 Factory O/H Control 10,000 Raw Material Control 42,000Accounts Payable 2,000 Raw Material Control 2,000Work in Progress 40,000 Factory O/H Control 10,000 Labour Control 50,000Labour Control 50,000 Taxation Withheld 15,000 Accrued Payroll 35,000Accrued Payroll 35,000 Bank 35,000Factory O/H Control 20,000 Accum. Depreciation 20,000Factory O/H Applied 40,000 Factory O/H Control 40,000Work in Progress 40,000 Factory O/H Applied 40,000Finished Goods 80,000 Work in Progress 80,000Cost of Goods Sold 80,000 Finished Goods 80,000Accounts Receivable 160,000 Sales 160,000

Management Accounting in Australia - Solutions

48

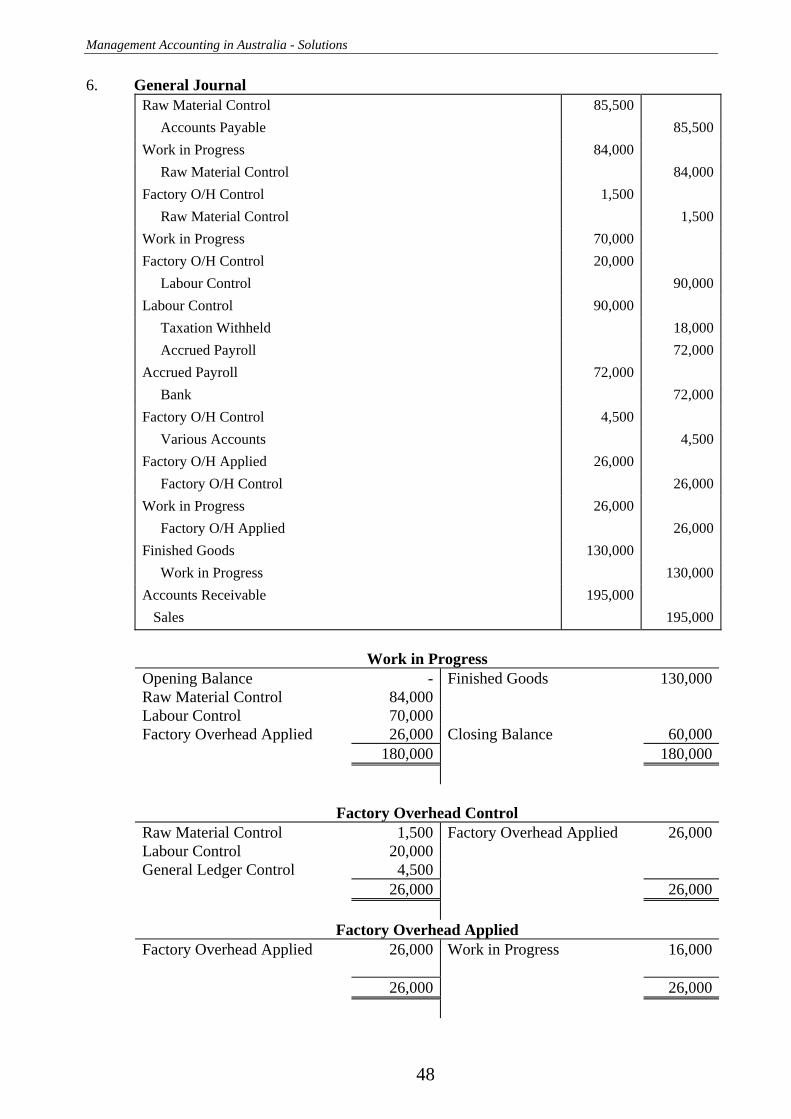

6. General Journal Raw Material Control 85,500 Accounts Payable 85,500Work in Progress 84,000 Raw Material Control 84,000Factory O/H Control 1,500 Raw Material Control 1,500Work in Progress 70,000 Factory O/H Control 20,000 Labour Control 90,000Labour Control 90,000 Taxation Withheld 18,000 Accrued Payroll 72,000Accrued Payroll 72,000 Bank 72,000Factory O/H Control 4,500 Various Accounts 4,500Factory O/H Applied 26,000 Factory O/H Control 26,000Work in Progress 26,000 Factory O/H Applied 26,000Finished Goods 130,000 Work in Progress 130,000Accounts Receivable 195,000 Sales 195,000

Work in Progress

Opening Balance - Finished Goods 130,000Raw Material Control 84,000 Labour Control 70,000 Factory Overhead Applied 26,000 Closing Balance 60,000 180,000 180,000

Factory Overhead Control Raw Material Control 1,500 Factory Overhead Applied 26,000Labour Control 20,000 General Ledger Control 4,500 26,000 26,000

Factory Overhead Applied Factory Overhead Applied 26,000 Work in Progress 16,000 26,000 26,000

Chapter 4: The Cost Accounting Cycle

49

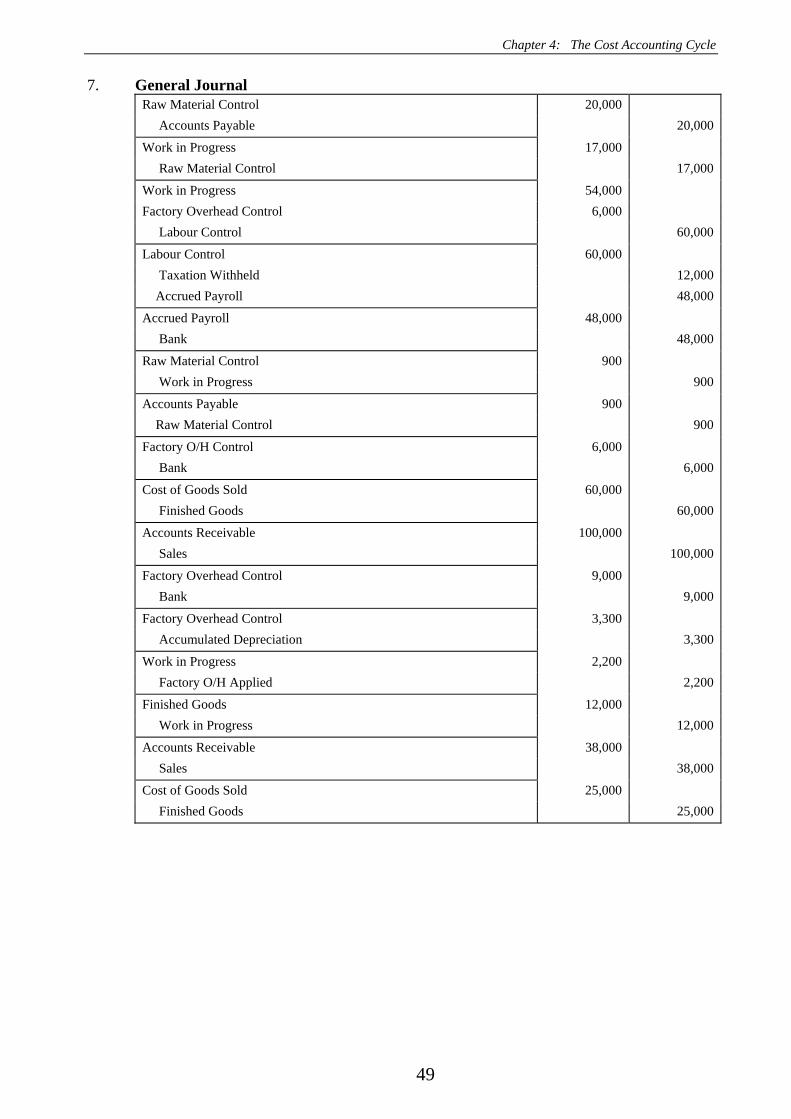

7. General Journal Raw Material Control 20,000 Accounts Payable 20,000

Work in Progress 17,000 Raw Material Control 17,000

Work in Progress 54,000 Factory Overhead Control 6,000 Labour Control 60,000

Labour Control 60,000 Taxation Withheld 12,000 Accrued Payroll 48,000

Accrued Payroll 48,000 Bank 48,000

Raw Material Control 900 Work in Progress 900

Accounts Payable 900 Raw Material Control 900

Factory O/H Control 6,000 Bank 6,000

Cost of Goods Sold 60,000 Finished Goods 60,000

Accounts Receivable 100,000 Sales 100,000

Factory Overhead Control 9,000 Bank 9,000

Factory Overhead Control 3,300 Accumulated Depreciation 3,300

Work in Progress 2,200 Factory O/H Applied 2,200

Finished Goods 12,000 Work in Progress 12,000

Accounts Receivable 38,000 Sales 38,000

Cost of Goods Sold 25,000 Finished Goods 25,000

Management Accounting in Australia - Solutions

50

8. General Journal Raw Material Control 44,000 Accounts Payable 44,000

Work in Progress 24,000 Raw Material Control 24,000

Factory O/H Control 16,000 Raw Material Control 16,000

Work in Progress 26,000 Factory O/H Control 4,000 Labour Control 30,000

Labour Control 30,000 Taxation Withheld 6,000 Accrued Payroll 24,000

Accrued Payroll 24,000 Bank 24,000

Factory O/H Control 5,000 Accum. Depreciation 5,000

Factory O/H Applied 25,000 Factory O/H Control 25,000

Work in Progress 25,000 Factory O/H Applied 25,000

Finished Goods 70,000 Work in Progress 70,000

Cost of Goods Sold 62,500 Finished Goods 62,500

Accounts Receivable 100,000 Sales 100,000

Raw Material Control

Opening Balance 8,000 Work in Progress 24,000 Accounts Payable 44,000 Factory Overhead Control 16,000 Closing Balance 12,000 52,000 52,000

Factory Overhead Control Raw Material Control 16,000 Factory Overhead Applied 25,000 Labour Control 4,000 Accumulated Depreciation 5,000 25,000 25,000

Factory Overhead Applied

Factory Overhead Control 25,000 Work In Progress 25,000 25,000 25,000

Work in Progress Opening Balance - Finished Goods 70,000 Raw Material Control 24,000 Labour Control 26,000 Factory Overhead Applied 25,000 Closing Balance 5,000 75,000 75,000

Finished Goods Opening Balance - Cost of Goods Sold 62,500 Finished Goods 70,000 Closing Balance 7,500 70,000 70,000

Chapter 4: The Cost Accounting Cycle

51

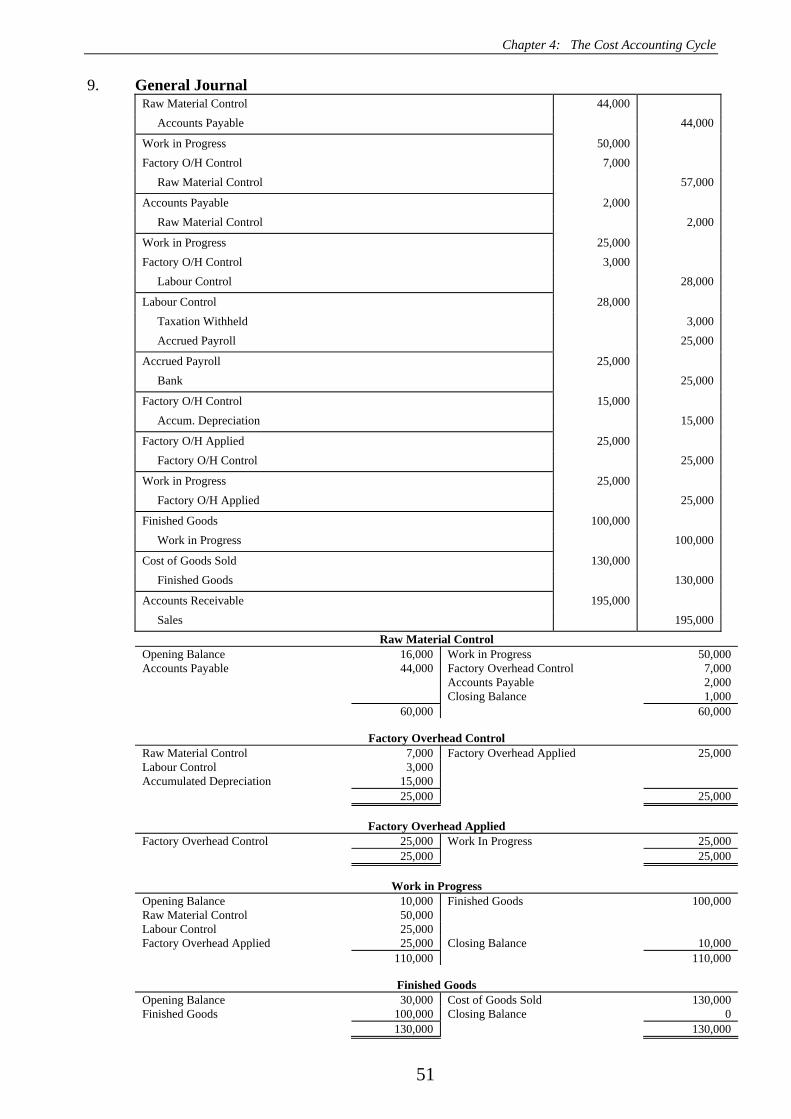

9. General Journal Raw Material Control 44,000 Accounts Payable 44,000

Work in Progress 50,000 Factory O/H Control 7,000 Raw Material Control 57,000

Accounts Payable 2,000 Raw Material Control 2,000

Work in Progress 25,000 Factory O/H Control 3,000 Labour Control 28,000

Labour Control 28,000 Taxation Withheld 3,000 Accrued Payroll 25,000

Accrued Payroll 25,000 Bank 25,000

Factory O/H Control 15,000 Accum. Depreciation 15,000

Factory O/H Applied 25,000 Factory O/H Control 25,000

Work in Progress 25,000 Factory O/H Applied 25,000

Finished Goods 100,000 Work in Progress 100,000

Cost of Goods Sold 130,000 Finished Goods 130,000

Accounts Receivable 195,000 Sales 195,000

Raw Material Control Opening Balance 16,000 Work in Progress 50,000 Accounts Payable 44,000 Factory Overhead Control 7,000 Accounts Payable 2,000 Closing Balance 1,000 60,000 60,000

Factory Overhead Control Raw Material Control 7,000 Factory Overhead Applied 25,000 Labour Control 3,000 Accumulated Depreciation 15,000 25,000 25,000

Factory Overhead Applied

Factory Overhead Control 25,000 Work In Progress 25,000 25,000 25,000

Work in Progress Opening Balance 10,000 Finished Goods 100,000 Raw Material Control 50,000 Labour Control 25,000 Factory Overhead Applied 25,000 Closing Balance 10,000 110,000 110,000

Finished Goods Opening Balance 30,000 Cost of Goods Sold 130,000 Finished Goods 100,000 Closing Balance 0 130,000 130,000

Management Accounting in Australia - Solutions

52

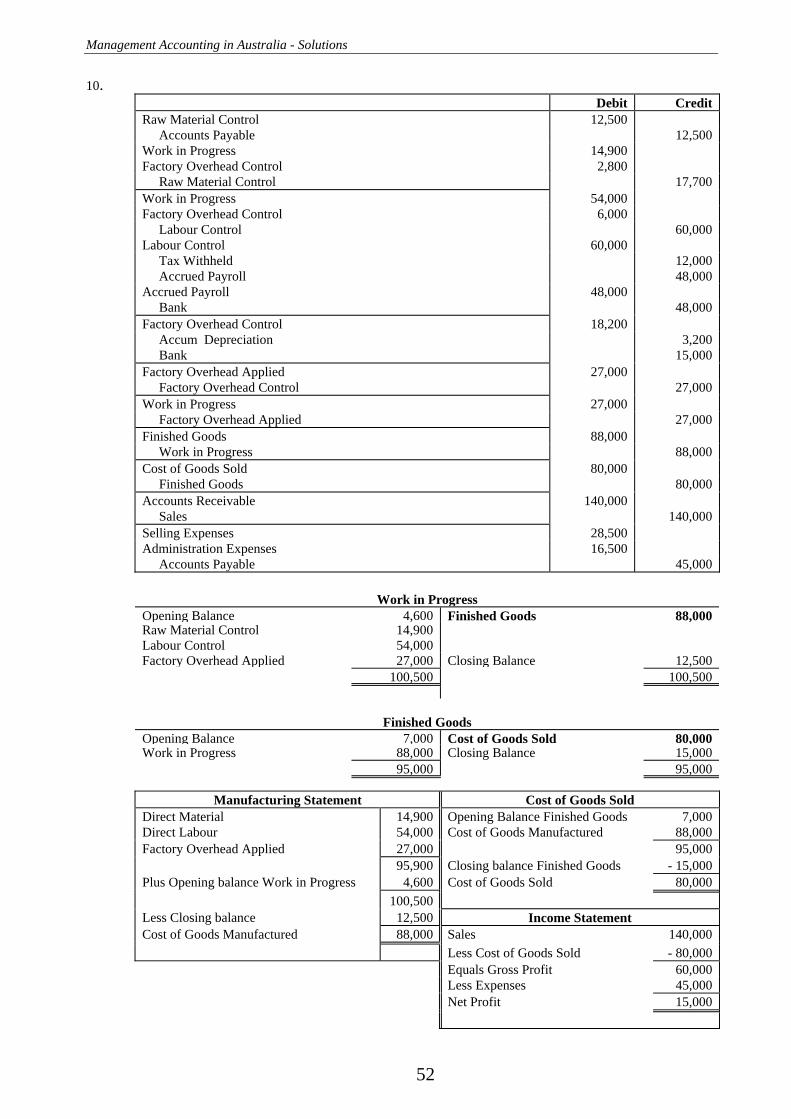

10. Debit Credit Raw Material Control 12,500 Accounts Payable 12,500 Work in Progress 14,900 Factory Overhead Control 2,800 Raw Material Control 17,700 Work in Progress 54,000 Factory Overhead Control 6,000 Labour Control 60,000 Labour Control 60,000 Tax Withheld 12,000 Accrued Payroll 48,000 Accrued Payroll 48,000 Bank 48,000 Factory Overhead Control 18,200 Accum Depreciation 3,200 Bank 15,000 Factory Overhead Applied 27,000 Factory Overhead Control 27,000 Work in Progress 27,000 Factory Overhead Applied 27,000 Finished Goods 88,000 Work in Progress 88,000 Cost of Goods Sold 80,000 Finished Goods 80,000 Accounts Receivable 140,000 Sales 140,000 Selling Expenses 28,500 Administration Expenses 16,500 Accounts Payable 45,000

Work in Progress

Opening Balance 4,600 Finished Goods 88,000Raw Material Control 14,900Labour Control 54,000Factory Overhead Applied 27,000 Closing Balance 12,500 100,500 100,500

Finished Goods

Opening Balance 7,000 Cost of Goods Sold 80,000Work in Progress 88,000 Closing Balance 15,000 95,000 95,000

Manufacturing Statement Cost of Goods Sold Direct Material 14,900 Opening Balance Finished Goods 7,000Direct Labour 54,000 Cost of Goods Manufactured 88,000Factory Overhead Applied 27,000 95,000 95,900 Closing balance Finished Goods - 15,000Plus Opening balance Work in Progress 4,600 Cost of Goods Sold 80,000 100,500 Less Closing balance 12,500 Income Statement Cost of Goods Manufactured 88,000 Sales 140,000 Less Cost of Goods Sold - 80,000 Equals Gross Profit 60,000 Less Expenses 45,000 Net Profit 15,000

Chapter 4: The Cost Accounting Cycle

53

11. Debit Credit Raw Material Control 25,000 Accounts Payable 25,000 Accounts Payable 5,000 Raw Material Control 5,000 Work in Progress 20,000 Factory Overhead Control 4,000 Raw Material Control 24,000 Work in Progress 35,000 Factory Overhead Control 11,000 Labour Control 46,000 Labour Control 46,000 Tax Withheld 16,100 Accrued Payroll 29,900 Accrued Payroll 29,900 Bank 29,900 Factory Overhead Control 7,500 Accumulated Depreciation 3,000 Prepaid Insurance 500 Bank 4,000 Factory Overhead Applied 22,500 Actual Factory Overhead Control 22,500 Work in Progress 21,000 Applied Factory Overhead Applied 21,000 Cost of Goods Sold 1,500 Factory Overhead Applied 1,500 Finished Goods 80,000 Work in Progress 80,000 Cost of Goods Sold 84,000 Finished Goods 84,000 Accounts Receivable 151,200 Sales 151,200 Selling Expenses 18,000 Administrative Expenses 19,200 Accounts Payable 37,200

Manufacturing Statement Cost of Goods Sold

Direct Material 20,000 Opening Balance Finished Goods 10,000Direct Labour 35,000 Cost of Goods Manufactured 80,000Factory Overhead Applied 21,000 90,000 76,000 Opening Balance Finished Goods - 6,000Plus Opening balance Work in Progress 14,000 Cost of Goods Sold 84,000 90,000 plus Underapplied Overhead 1,500Less Closing balance 10,000 Cost of Goods Sold 85,500Cost of Goods Manufactured 80,000

Factory Overhead Control Income Statement

Raw M Control 4,000 F O A 22,500 Sales 151,200Labour Costs 11,000 Cost of Goods Sold 85,500Other 7,500 Equals Gross Profit 65,700 22,500 22,500 Less Expenses 37,200 Net Profit 28,500

Factory Overhead Applied F O C 22,500 W I P 21,000 C O G S 1,500 22,500 22,500

Management Accounting in Australia - Solutions

54

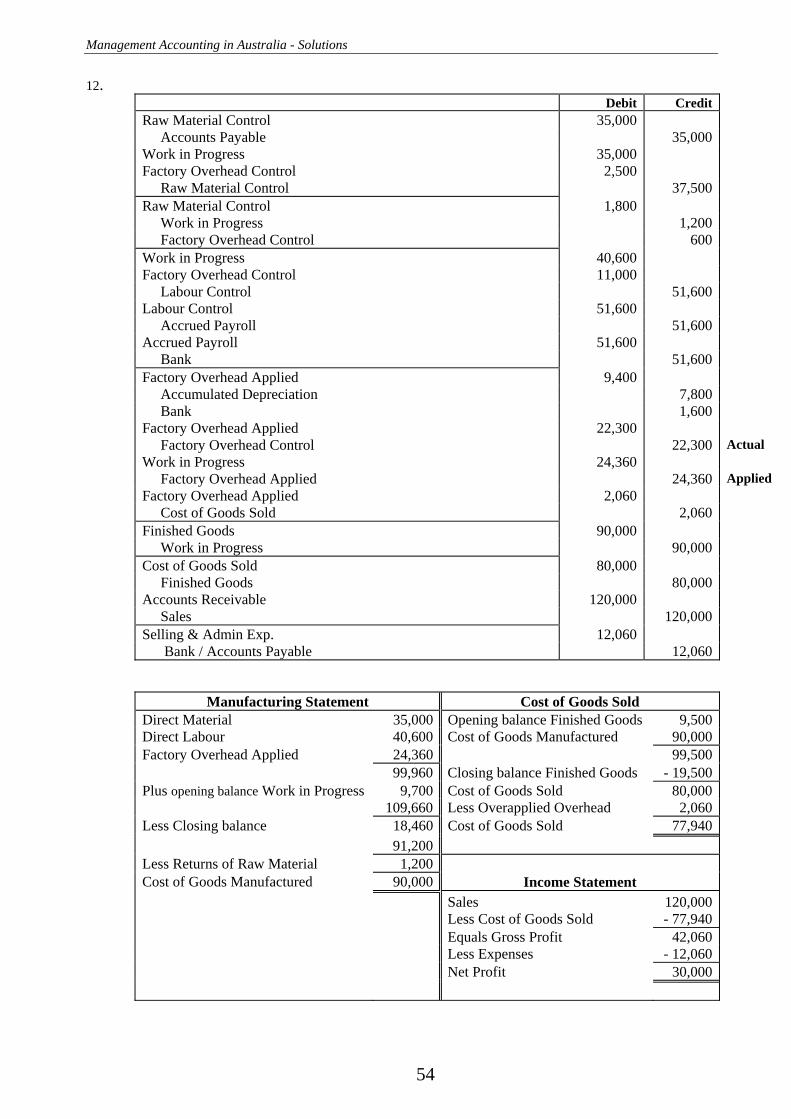

12. Debit Credit Raw Material Control 35,000 Accounts Payable 35,000Work in Progress 35,000 Factory Overhead Control 2,500 Raw Material Control 37,500Raw Material Control 1,800 Work in Progress 1,200 Factory Overhead Control 600Work in Progress 40,600 Factory Overhead Control 11,000 Labour Control 51,600Labour Control 51,600 Accrued Payroll 51,600Accrued Payroll 51,600 Bank 51,600Factory Overhead Applied 9,400 Accumulated Depreciation 7,800 Bank 1,600Factory Overhead Applied 22,300 Factory Overhead Control 22,300 Actual Work in Progress 24,360 Factory Overhead Applied 24,360 Applied Factory Overhead Applied 2,060 Cost of Goods Sold 2,060Finished Goods 90,000 Work in Progress 90,000Cost of Goods Sold 80,000 Finished Goods 80,000Accounts Receivable 120,000 Sales 120,000Selling & Admin Exp. 12,060 Bank / Accounts Payable 12,060

Manufacturing Statement Cost of Goods Sold Direct Material 35,000 Opening balance Finished Goods 9,500Direct Labour 40,600 Cost of Goods Manufactured 90,000Factory Overhead Applied 24,360 99,500 99,960 Closing balance Finished Goods - 19,500Plus opening balance Work in Progress 9,700 Cost of Goods Sold 80,000 109,660 Less Overapplied Overhead 2,060Less Closing balance 18,460 Cost of Goods Sold 77,940 91,200Less Returns of Raw Material 1,200Cost of Goods Manufactured 90,000 Income Statement Sales 120,000 Less Cost of Goods Sold - 77,940 Equals Gross Profit 42,060 Less Expenses - 12,060 Net Profit 30,000

Chapter 4: The Cost Accounting Cycle

55

13. Raw Material Control

Opening balance 14,000 Work in Progress 18,600 Accounts Payable 22,000 Factory Overhead Control 2,400 Closing balance 15,000 36,000 36,000

Labour Control Accrued Payroll 23,400 Work in Progress 24,000 Tax Payable 10,200 Factory Overhead Control 10,000 Union Dues 400 34,000 34,000

Work in Progress Opening balance 15,200 Finished Goods 60,000 Raw Material Control 18,600 Labour Control 24,000 Factory Overhead Applied 18,000 Closing balance 15,800 75,800 75,800

Finished Goods Opening balance 15,000 Cost of Goods Sold 50,000 Work in Progress 60,000 Closing balance 25,000 75,000 75,000 Total Manufacturing Costs $ 60,600 Less Raw Material Costs - 18,600 Equals Conversion Costs $ 42,000 Conversion Costs $ 42,000 = $ 24,000 ( L.C. ) 1.75

Factory Overhead Control Raw Material Control 2,400 Factory Overhead Applied 18,000 Labour Control 10,000 Account Depreciation 2,200 Prepaid Insurance 400 Bank 3,000 18,000 18,000

Factory Overhead Applied Factory Overhead Control 18,000 Work in Progress 18,000 18,000 18,000

Manufacturing Statement Cost of Goods Sold Direct Material $ 18,600 O/Bal Finished Goods $ 15,000Direct Labour 24,000 Cost of Goods Manufactured 60,000Factory Overhead Applied 18,000 $ 75,000 $ 60,600 C/Bal Finished Goods -25,000 Plus O/Bal Work in Progress. 15,200 Cost of Goods Sold $ 50,000 75,800 Less C/Bal 15,800 Statement of Financial Performance Cost of Goods Manufactured $ 60,000 Sales $ 100,000 Less Cost of Goods Sold -50,000 Equals Gross Profit $ 50,000 Less Expenses -25,000 Net Profit $ 25,000

Management Accounting in Australia - Solutions

56

14. Raw Material Control

Opening Balance 40,000 Work in Progress 162,000Accounts Payable 170,000 Factory Overhead Control 18,000 Closing Balance 30,000 210,000 210,000

Work in ProgressOpening Balance 50,000 Finished Goods 410,000Raw Material Control 162,000 Labour Control 192,000 Factory Overhead Applied 96,000 Closing Balance 90,000 500,000 500,000

Finished GoodsOpening Balance 40,000 Cost of Goods Sold 400,000Work in Progress 410,000 Closing Balance 50,000 450,000 450,000

15. ( a ) Debit CreditRaw Material Control 55,000 Accounts Payable 55,000Work in Progress 68,000 Factory Overhead Control 5,600 Raw Material Control 73,600Work in Progress 85,000 Factory Overhead Control 10,500 Labour Control 95,500Labour Control 95,500 Tax Withheld 20,000 Accrued Payroll 75,500Accrued Payroll 75,500 Bank 75,500Factory Overhead Control 14,000 Accounts Payable 14,000Bank 310,000 Accounts Receivable 310,000Accounts Payable 109,000 Bank 109,000Factory Overhead Control 1,600 Accum. Depn. – Plant 1,600Factory Overhead Applied 31,700 Factory Overhead Control 31,700

Chapter 4: The Cost Accounting Cycle

57

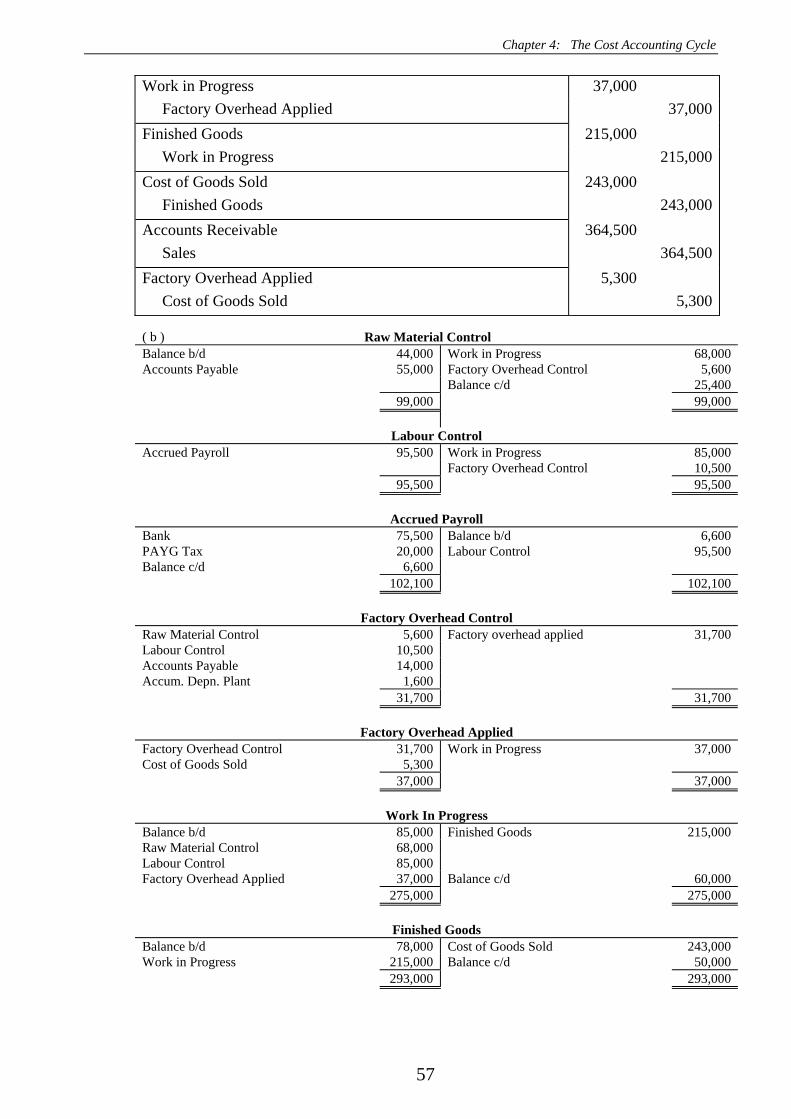

Work in Progress 37,000 Factory Overhead Applied 37,000Finished Goods 215,000 Work in Progress 215,000Cost of Goods Sold 243,000 Finished Goods 243,000Accounts Receivable 364,500 Sales 364,500Factory Overhead Applied 5,300 Cost of Goods Sold 5,300 ( b ) Raw Material Control Balance b/d 44,000 Work in Progress 68,000 Accounts Payable 55,000 Factory Overhead Control 5,600 Balance c/d 25,400 99,000 99,000

Labour Control Accrued Payroll 95,500 Work in Progress 85,000 Factory Overhead Control 10,500 95,500 95,500

Accrued Payroll Bank 75,500 Balance b/d 6,600 PAYG Tax 20,000 Labour Control 95,500 Balance c/d 6,600 102,100 102,100

Factory Overhead Control Raw Material Control 5,600 Factory overhead applied 31,700 Labour Control 10,500 Accounts Payable 14,000 Accum. Depn. Plant 1,600 31,700 31,700

Factory Overhead Applied Factory Overhead Control 31,700 Work in Progress 37,000 Cost of Goods Sold 5,300 37,000 37,000

Work In Progress Balance b/d 85,000 Finished Goods 215,000 Raw Material Control 68,000 Labour Control 85,000 Factory Overhead Applied 37,000 Balance c/d 60,000 275,000 275,000

Finished Goods Balance b/d 78,000 Cost of Goods Sold 243,000 Work in Progress 215,000 Balance c/d 50,000 293,000 293,000

Management Accounting in Australia - Solutions

58

Accounts Payable

Bank 109,000 Balance b/d 65,400 Balance c/d 25,400 Raw Material Control 55,000 Factory Overhead Control 14,000 134,400 134,400

Sales Accounts Receivable 364,500

Cost Of Goods Sold Finished Goods 243,000 Factory Overhead Applied 5,300 Balance c/d 237,700 243,000 243,000

Accounts Receivable Balance b/d 32,000 Bank 310,000 Sales 364,500 Balance c/d 86,500 396,500 396,500

Accumulated Depreciation - Plant Balance b/d 92,000 Factory Overhead Control 1,600 93,600

Bank Balance b/d 15,000 Accrued Payroll + PAYE Tax 95,500 Accounts Receivable 310,000 Accounts Payable 109,000 Balance c/d 120,500 325,000 325,000

Plant & Machinery Balance b/d 192,000

Paid Up Capital Balance b/d 220,000

Retained Earnings Balance b/d 62,000

Trial Balance Debit CreditRaw Material Control 25,400 Work in Progress 60,000 Finished Goods 50,000 Accounts Receivable 86,500 Bank 120,500 Plant 192,000 Accounts Payable 25,400Accrued Payroll 6,600Accum. Depreciation 93,600Retained Earnings 62,000Paid Up Capital 220,000Sales 364,500Cost of Goods Sold 237,700 772,100 772,100

Chapter 5: Material & Labour

59

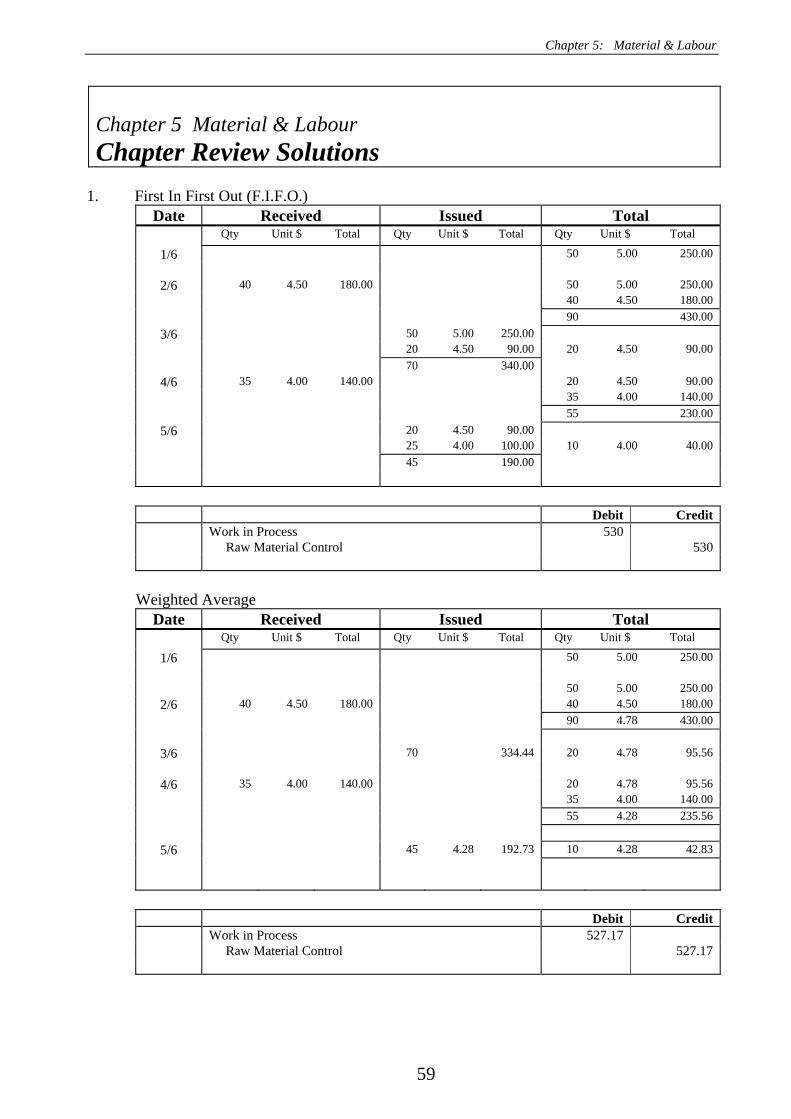

Chapter 5 Material & Labour Chapter Review Solutions

1. First In First Out (F.I.F.O.)

Date Received Issued Total Qty Unit $ Total Qty Unit $ Total Qty Unit $ Total

1/6 50 5.00 250.00

2/6 40 4.50 180.00 50 5.00 250.00 40 4.50 180.00 90 430.00

3/6 50 5.00 250.00 20 4.50 90.00 20 4.50 90.00 70 340.00

4/6 35 4.00 140.00 20 4.50 90.00 35 4.00 140.00 55 230.00

5/6 20 4.50 90.00 25 4.00 100.00 10 4.00 40.00 45 190.00

Debit Credit Work in Process 530 Raw Material Control 530

Weighted Average

Date Received Issued Total Qty Unit $ Total Qty Unit $ Total Qty Unit $ Total

1/6 50 5.00 250.00 50 5.00 250.00

2/6 40 4.50 180.00 40 4.50 180.00 90 4.78 430.00

3/6 70 334.44 20 4.78 95.56

4/6 35 4.00 140.00 20 4.78 95.56 35 4.00 140.00 55 4.28 235.56

5/6 45 4.28 192.73 10 4.28 42.83

Debit Credit Work in Process 527.17 Raw Material Control 527.17

Management Accounting in Australia - Solutions

60

2. First In First Out (F.I.F.O.)

Date Received Issued Total Qty Unit $ Total Qty Unit $ Total Qty Unit $ Total

1/12 150 15.00 2,250

6/12 150 15.50 2,325 150 15.00 2,250 150 15.50 2,325 300 4,575 150 15.00 2,250

10/12 30 15.50 465 120 15.50 1,860 180 2,715 120 15.50 1,860

21/12 150 15.60 2,340 150 15.60 2,340 270 4,200 120 15.50 1,860

23/12 40 15.60 624 110 15.60 1,716

160 2,484

Weighted Average Date Received Issued Total

Qty Unit $ Total Qty Unit $ Total Qty Unit $ Total

1/12 150 15.00 2,250 150 15.00 2,325

6/12 150 15.50 2,325 150 15.00 2,250 300 15.25 4,575

10/12 180 15.25 2,745 120 15.25 1,830 150 15.60 2,340

21/12 150 15.60 2,340 120 15.25 1,830 270 15.44 4,170

23/12 160 15.44 2,471 110 15.44 1,699

Chapter 5: Material & Labour

61

3. First In First Out (F.I.F.O.) ( a ) Stock Card Date Received Issued Total

Qty Unit $ Total Qty Unit $ Total Qty Unit $ Total

1/7 500 4.00 2,000

4/7 200 5.00 1,000 500 4.00 2,000 200 5.00 1,000 700 3,000

8/7 100 4.00 400 400 4.00 1,600 200 5.00 1,000 600 2,600

12/7 - 100 5.00 - 500 400 4.00 1,600 100 5.00 500 500 2,100

15/7 200 4.00 800 200 4.00 800 100 5.00 500 300 1,300

19/7 300 6.00 1,800 200 4.00 800 100 5.00 500 300 6.00 1,800 600 3,100

24/7 200 4.00 800 100 5.00 500 100 6.00 600 200 6.00 1,200 400 1,900

29/7 - 100 4.00 - 400 100 4.00 400 200 6.00 1,200 300 1,600

31/7 50 4.00 200 50 4.00 200 200 6.00 1,200 250 1,400

Debit Credit

( b ) Work in Process 2,700 Raw Material Control 2,700

( c ) Factory Overhead Control 200 Raw Material Control 200 50 units loss @ $4.00 per unit

( d ) Accounts Payable 300 Raw Material Control 300 300 units overcharged @ $1.00 per unit

Management Accounting in Australia - Solutions

62

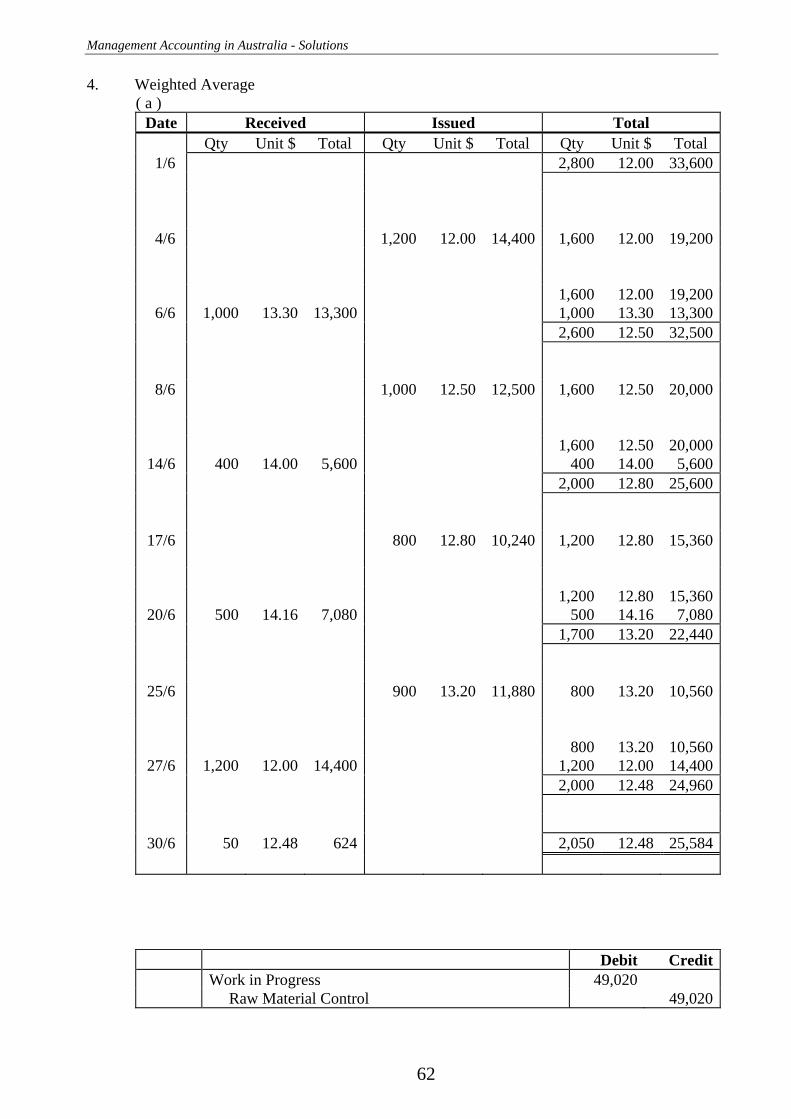

4. Weighted Average ( a )

Date Received Issued Total Qty Unit $ Total Qty Unit $ Total Qty Unit $ Total

1/6 2,800 12.00 33,600

4/6 1,200 12.00 14,400 1,600 12.00 19,200 1,600 12.00 19,200

6/6 1,000 13.30 13,300 1,000 13.30 13,300 2,600 12.50 32,500

8/6 1,000 12.50 12,500 1,600 12.50 20,000 1,600 12.50 20,000

14/6 400 14.00 5,600 400 14.00 5,600 2,000 12.80 25,600

17/6 800 12.80 10,240 1,200 12.80 15,360 1,200 12.80 15,360

20/6 500 14.16 7,080 500 14.16 7,080 1,700 13.20 22,440

25/6 900 13.20 11,880 800 13.20 10,560 800 13.20 10,560

27/6 1,200 12.00 14,400 1,200 12.00 14,400 2,000 12.48 24,960

30/6 50 12.48 624 2,050 12.48 25,584

Debit Credit Work in Progress 49,020 Raw Material Control 49,020

Chapter 5: Material & Labour

63

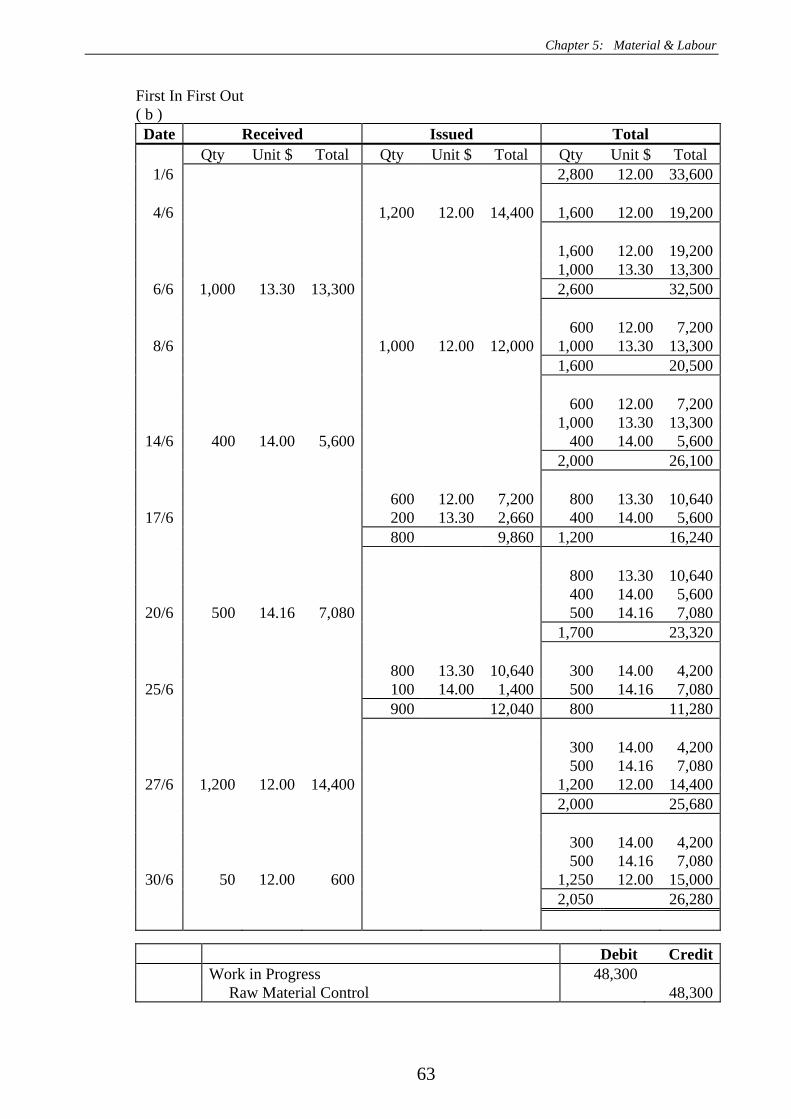

First In First Out ( b ) Date Received Issued Total

Qty Unit $ Total Qty Unit $ Total Qty Unit $ Total 1/6 2,800 12.00 33,600

4/6 1,200 12.00 14,400 1,600 12.00 19,200

1,600 12.00 19,200 1,000 13.30 13,300

6/6 1,000 13.30 13,300 2,600 32,500 600 12.00 7,200

8/6 1,000 12.00 12,000 1,000 13.30 13,300 1,600 20,500 600 12.00 7,200 1,000 13.30 13,300

14/6 400 14.00 5,600 400 14.00 5,600 2,000 26,100 600 12.00 7,200 800 13.30 10,640

17/6 200 13.30 2,660 400 14.00 5,600 800 9,860 1,200 16,240 800 13.30 10,640 400 14.00 5,600

20/6 500 14.16 7,080 500 14.16 7,080 1,700 23,320 800 13.30 10,640 300 14.00 4,200

25/6 100 14.00 1,400 500 14.16 7,080 900 12,040 800 11,280 300 14.00 4,200 500 14.16 7,080

27/6 1,200 12.00 14,400 1,200 12.00 14,400 2,000 25,680 300 14.00 4,200 500 14.16 7,080

30/6 50 12.00 600 1,250 12.00 15,000 2,050 26,280

Debit Credit Work in Progress 48,300 Raw Material Control 48,300

Management Accounting in Australia - Solutions

64

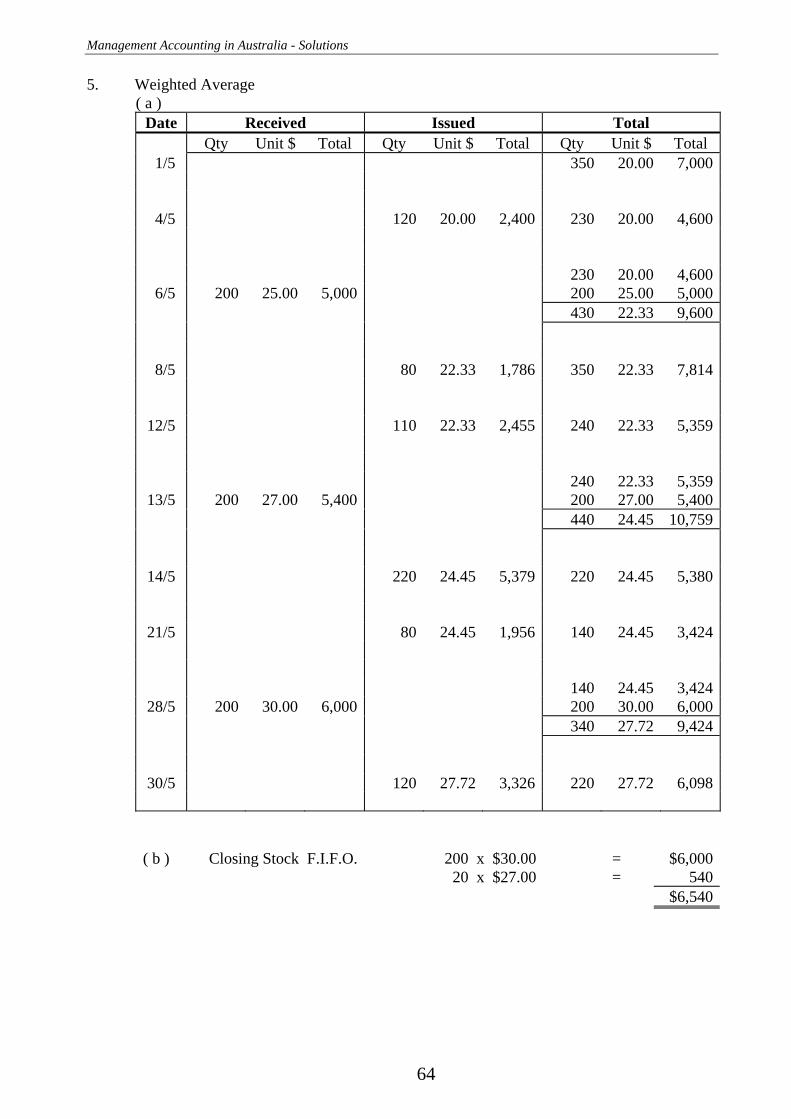

5. Weighted Average ( a )

Date Received Issued Total Qty Unit $ Total Qty Unit $ Total Qty Unit $ Total

1/5 350 20.00 7,000

4/5 120 20.00 2,400 230 20.00 4,600 230 20.00 4,600

6/5 200 25.00 5,000 200 25.00 5,000 430 22.33 9,600

8/5 80 22.33 1,786 350 22.33 7,814

12/5 110 22.33 2,455 240 22.33 5,359 240 22.33 5,359

13/5 200 27.00 5,400 200 27.00 5,400 440 24.45 10,759

14/5 220 24.45 5,379 220 24.45 5,380

21/5 80 24.45 1,956 140 24.45 3,424 140 24.45 3,424

28/5 200 30.00 6,000 200 30.00 6,000 340 27.72 9,424

30/5 120 27.72 3,326 220 27.72 6,098

( b ) Closing Stock F.I.F.O. 200 x $30.00 = $6,000 20 x $27.00 = 540 $6,540

Chapter 5: Material & Labour

65

6. ( a ) Weighted Average Date Received Issued Total

Qty Unit $ Total Qty Unit $ Total Qty Unit $ Total

1/6 400 25.00 10,000 400 25.00 10,000 200 26.00 5,200

6/6 200 26.00 5,200 600 25.33 15,200

7/6 170 25.33 4,307 430 25.33 10,893 - 20 26.00 - 520

9/6 - 20 26.00 - 520 430 25.33 10,893 410 25.30 10,373

17/6 130 25.30 3,289 280 25.30 7,084 280 25.30 7,084

23/6 120 27.00 3,240 120 27.00 3,240 400 25.81 10,324 400 25.81 10,324

25/6 140 28.00 3,920 140 28.00 3,920 540 26.38 14,244

28/6 160 26.38 4,221 380 26.38 10,023 380 26.38 10,024

30/6 - 10 25.30 - 253 10 25.30 253 390 26.35 10,277

30/6 5 26.35 132 385 26.35 10,145

Purchases Debit Credit Raw Material Control 12,360 Creditors 12,360 Returns Creditors 520 Raw Material Control 520 F.I.F.O Debit Credit Issues Work in Progress 11,560 Raw Material Control 11,560 Returns Raw Material Control 250 Work in Progress 250

Weighted Average Debit Credit Issues Work in Progress 11,817 Raw Material Control 11,817 Returns Raw Material Control 253 Work in Progress 253

Management Accounting in Australia - Solutions

66

6. ( b ) First In First Out (F.I.F.O.) Date Received Issued Total Qty Unit $ Total Qty Unit $ Total Qty Unit $ Total 1/6 400 25.00 10,000 400 25.00 10,000 200 26.00 5,2006/6 200 26.00 5,200 600 15,200 230 25.00 5,750 170 25.00 4,250 200 26.00 5,200 430 10,950 230 25.00 5,7509/6 - 20 26.00 - 520 180 26.00 4,680 410 10,430 100 25.00 2,50017/6 130 25.00 3,250 180 26.00 4,680 280 7,180 100 25.00 2,500 180 26.00 4,68023/6 120 27.00 3,240 120 27.00 3,240 400 10,420 100 25.00 2,500 180 26.00 4,680 120 27.00 3,24025/6 140 28.00 3,920 140 28.00 3,920 540 14,340 120 26.00 3,120 100 25.00 2,500 120 27.00 3,24028/6 60 26.00 1,560 140 28.00 3,920 160 4,060 380 10,280 10 25.00 250 120 26.00 3,120 120 27.00 3,24030/6 - 10 25.00 - 250 140 28.00 3,920 390 10,530 5 25.00 175 120 26.00 3,120 120 27.00 3,24030/6 5 25.00 125 140 28.00 3,920 385 10,405

Chapter 5: Material & Labour

67

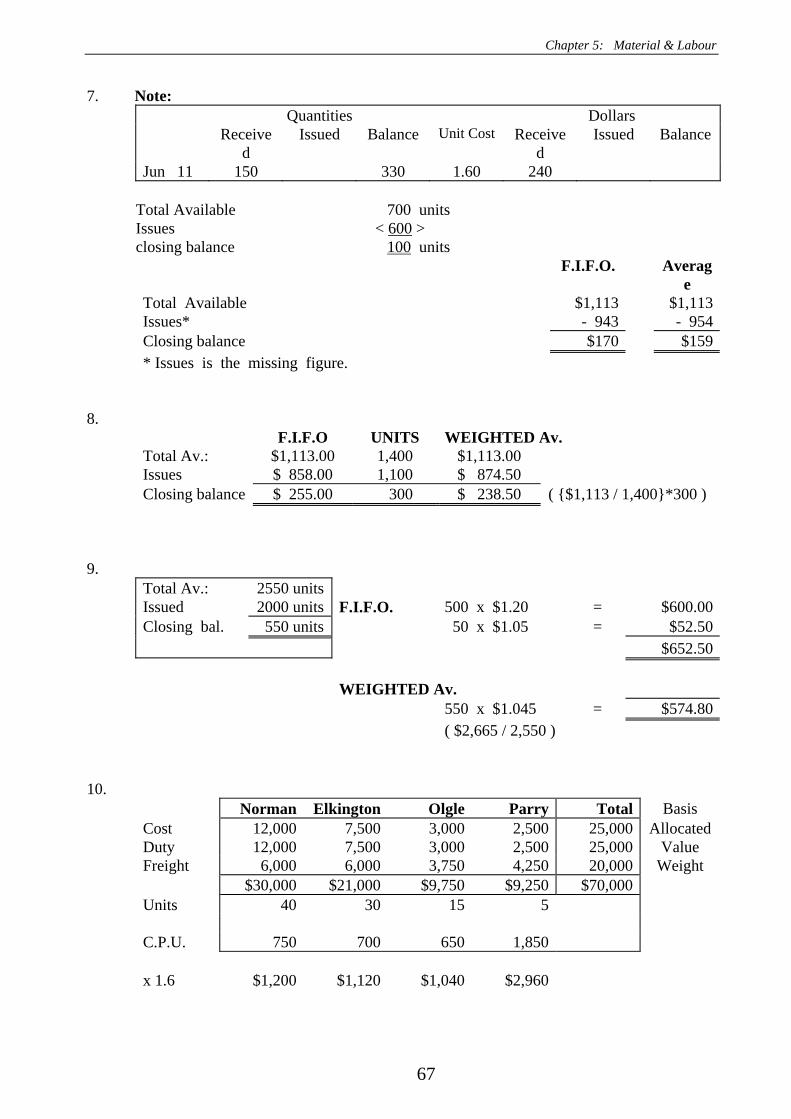

7. Note: Quantities Dollars Receive

d Issued Balance Unit Cost Receive

d Issued Balance

Jun 11 150 330 1.60 240

Total Available 700 units Issues < 600 > closing balance 100 units F.I.F.O. Averag

e Total Available $1,113 $1,113Issues* - 943 - 954Closing balance $170 $159* Issues is the missing figure.

8. F.I.F.O UNITS WEIGHTED Av.

Total Av.: $1,113.00 1,400 $1,113.00 Issues $ 858.00 1,100 $ 874.50 Closing balance $ 255.00 300 $ 238.50 ( {$1,113 / 1,400}*300 )

9. Total Av.: 2550 units Issued 2000 units F.I.F.O. 500 x $1.20 = $600.00Closing bal. 550 units 50 x $1.05 = $52.50 $652.50 WEIGHTED Av. 550 x $1.045 = $574.80 ( $2,665 / 2,550 )

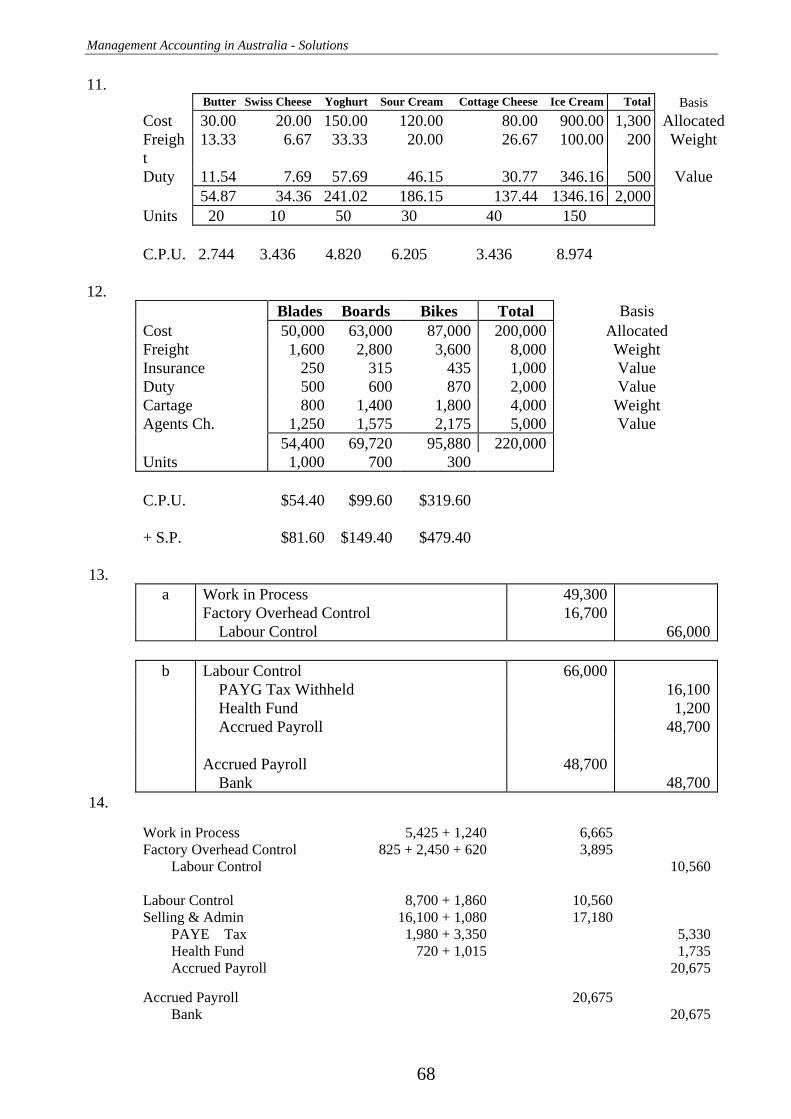

10. Norman Elkington Olgle Parry Total Basis Cost 12,000 7,500 3,000 2,500 25,000 Allocated Duty 12,000 7,500 3,000 2,500 25,000 Value Freight 6,000 6,000 3,750 4,250 20,000 Weight $30,000 $21,000 $9,750 $9,250 $70,000 Units 40 30 15 5 C.P.U. 750 700 650 1,850 x 1.6 $1,200 $1,120 $1,040 $2,960

Management Accounting in Australia - Solutions

68

11. Butter Swiss Cheese Yoghurt Sour Cream Cottage Cheese Ice Cream Total Basis

Cost 30.00 20.00 150.00 120.00 80.00 900.00 1,300 Allocated Freight

13.33 6.67 33.33 20.00 26.67 100.00 200 Weight

Duty 11.54 7.69 57.69 46.15 30.77 346.16 500 Value 54.87 34.36 241.02 186.15 137.44 1346.16 2,000 Units 20 10 50 30 40 150 C.P.U. 2.744 3.436 4.820 6.205 3.436 8.974

12.

Blades Boards Bikes Total Basis Cost 50,000 63,000 87,000 200,000 Allocated Freight 1,600 2,800 3,600 8,000 Weight Insurance 250 315 435 1,000 Value Duty 500 600 870 2,000 Value Cartage 800 1,400 1,800 4,000 Weight Agents Ch. 1,250 1,575 2,175 5,000 Value 54,400 69,720 95,880 220,000 Units 1,000 700 300 C.P.U. $54.40 $99.60 $319.60 + S.P. $81.60 $149.40 $479.40

13.

a Work in Process 49,300 Factory Overhead Control 16,700 Labour Control 66,000

b Labour Control 66,000 PAYG Tax Withheld 16,100 Health Fund 1,200 Accrued Payroll 48,700 Accrued Payroll 48,700 Bank 48,700

14. Work in Process 5,425 + 1,240 6,665 Factory Overhead Control 825 + 2,450 + 620 3,895 Labour Control 10,560 Labour Control 8,700 + 1,860 10,560 Selling & Admin 16,100 + 1,080 17,180

PAYE Tax 1,980 + 3,350 5,330 Health Fund 720 + 1,015 1,735 Accrued Payroll 20,675

Accrued Payroll 20,675 Bank 20,675

Chapter 5: Material & Labour

69

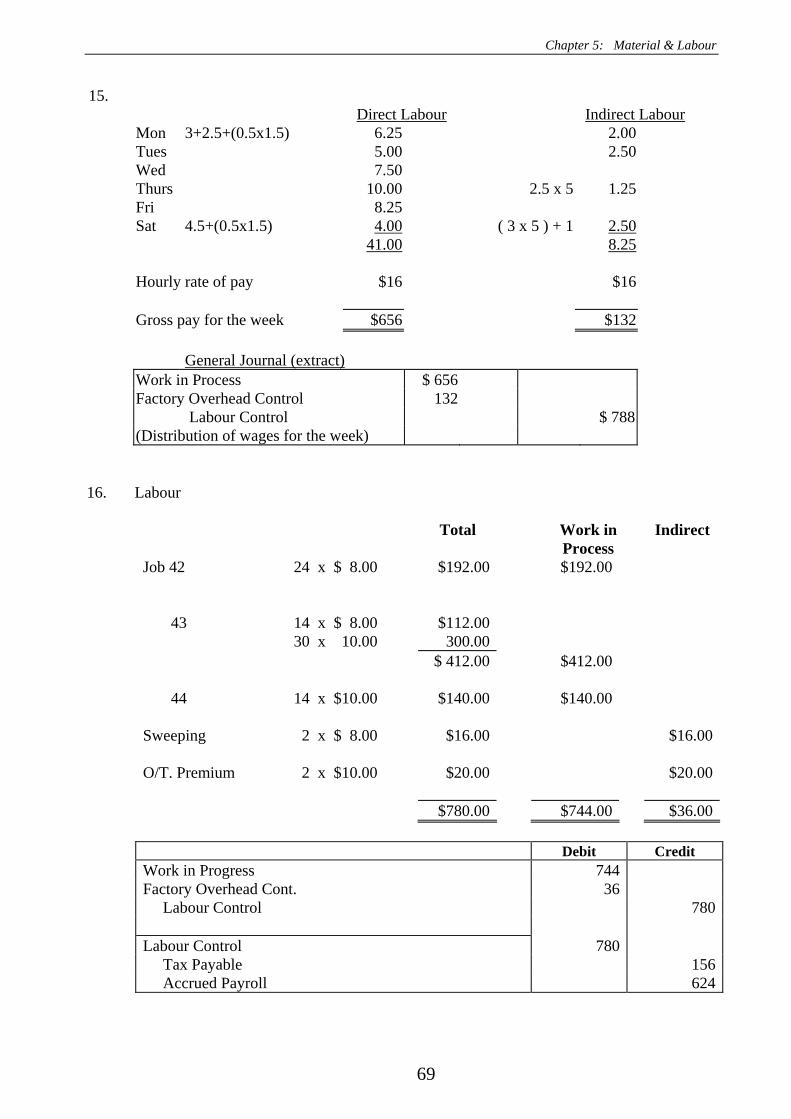

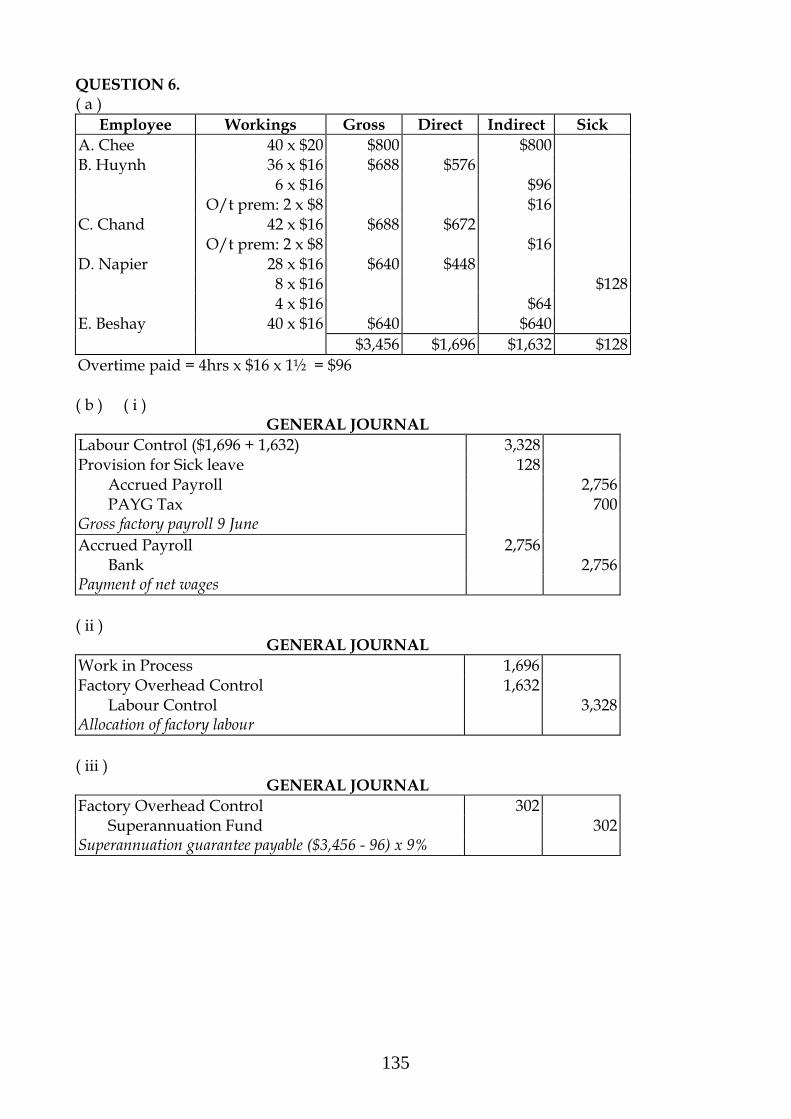

15. Direct Labour Indirect Labour Mon 3+2.5+(0.5x1.5) 6.25 2.00 Tues 5.00 2.50 Wed 7.50 Thurs 10.00 2.5 x 5 1.25 Fri 8.25 Sat 4.5+(0.5x1.5) 4.00 ( 3 x 5 ) + 1 2.50

41.00 8.25

Hourly rate of pay $16 $16 Gross pay for the week $656 $132

General Journal (extract)

Work in Process $ 656 Factory Overhead Control 132

Labour Control $ 788 (Distribution of wages for the week)

16. Labour Total Work in

Process Indirect

Job 42 24 x $ 8.00 $192.00 $192.00 43 14 x $ 8.00 $112.00 30 x 10.00 300.00 $ 412.00 $412.00 44 14 x $10.00 $140.00 $140.00 Sweeping 2 x $ 8.00 $16.00 $16.00 O/T. Premium 2 x $10.00 $20.00 $20.00 $780.00 $744.00 $36.00 Debit Credit Work in Progress 744 Factory Overhead Cont. 36 Labour Control 780 Labour Control 780 Tax Payable 156 Accrued Payroll 624

Management Accounting in Australia - Solutions

70

17. Employee Hrs. Rate Gross Tax ( 25 % ) Net Bourne ( 42 + 1 ) 43 $12 $516.00 $129.00 $387.00 Ward (40 ) 40 9 $360.00 ( 6 x 1.5 ) 9 9 81.00 $441.00 $110.25 $330.75 Craven 40 9 $360.00 ( 8 x 1.5 ) 12 9 108.00 $468.00 $117.00 $351.00 Thomas 38 9 $342.00 2 9 18.00 $360.00 $90.00 $270.00 $1,785.00 $446.25 $1,338.75

Hours Schedule Normal

Time Overtime Overtime Premium Idle Time Direct Indirect

Bourne 40 2 1 43 Ward 40 6 3 49 Craven 40 8 4 48 4 Thomas 38 2 38 2 135 49

W.I.P. $1,215.00 ( 135 Hrs @ $ 9.00 ) F.O.C. $570.00 ( Supervisor + O / T Premium + Idle Time ) $516.00 + $ 36.00 ( 4 hrs @ $9.00 ) + $ 18.00 ( 2 hrs @ $ 9.00 ) $1,785.00

Debit Credit Work In Progress 1,215.00 Factory O/ H Control 570.00 Labour Control 1,785.00 Labour Control 1,785.00 PAYG. Tax Payable 446.25 Accrued Payroll 1,338.75 Accrued Payroll 1,338.75 Bank 1,338.75

Chapter 5: Material & Labour

71

18. Days W.I.P. F.O.C. Absent Total Tue 7 1 8 Wed 8 8 Thur 7 2.5* 9.5 Fri 8 8 Mon 8 8 30 hrs 3.5 hrs 8 hrs 41.5 hrs

Normal Time 6 hrs Only O / T Premium to F.O.C. O / T Time 1 hrs *.5 Hrs + 2 hrs clean up = 2.5 hrs 7 hrs Debit Credit Work In Progress 300 ( 30 x $ 10 ) Factory O/H Control 35 ( 3.5 x $ 10 ) Provision for Sick Pay 80 ( 8 x $ 10 ) Labour Control 415 ( 41.5 x $ 10 )

19.

a Work in Process 170,000 Factory Overhead Control 16,000 Labour Control 186,000

b Labour Control 181,400 Prov for Sick Leave 600 Prov for Annual Leave 8,000 PAYG Tax Withheld 40,000 Super 9,000 Medical 6,000 Union Dues 400 Accrued Payroll 134,600 Accrued Payroll 134,600 Bank 134,600

c Factory Overhead Control 16,740 Prov for Sick Leave 5,580 Prov for Public Holidays 3,720 Prov for Annual Leave 7,440

Management Accounting in Australia - Solutions

72

20. ( Note: 13 pay periods p. a. ) * ( a ) Debit Credit Work In Progress 26,832 ( 2,216 + 20 ) ( $ 12 ) Factory O/H. Control 7,920 ( 315 + 10 ) ( $ 12 ) + $ 2,820 + $ 1,200 Prov. An. Leave 2,820 ( 15 x 4 x 40 x $12 x 1.175 )( 1/12 ) * Prov. Sick Pay 1,200 ( 15 x 10 x 8 x $12 )( 1/12 ) * Labour Control 30,732

Debit CreditFactory Overhead Control 1,500Prepaid Workers Comp. Ins. 1,500

21.

Annual Weeks Av. 52 Base Rate 9.00 - Annual Leave 4 ( 4/45 $ 9 ) ( 1.175 ) $0.94 ( including loading ) - Sick Leave. 2 ( 2/45 $ 9 ) $0.40 - Public Holidays 1 ( 1/45 $ 9 ) $0.20 Weeks Available 45 Charge Rate $ 10.54

22.

Hourly Rate $ 20.0000 Annual Leave 4/45 $ 1.7778 Loading 17.50% $ 0.3111 Sick Leave 1/45 $ 0.4444 Public Holidays 2/45 $ 0.8889 Total $ 23.4222

Payroll Tax 23.4222 x 6% $ 1.4053 W.C.I. 23.4222 x 10% $ 2.3422 Superannuation 23.1111 x 9% $ 2.0800

$ 29.2497

Chapter 5: Material & Labour

73

23. Hourly Rate 10.0000 Annual Leave 4/44 0.9091 Loading 17.50% 0.1591 Sick Leave 2/44 0.4545 Public Holidays 2/44 0.4545 Total 11.9773

Payroll Tax 11.9773 x 6% $0.7186 W.C.I. 11.9733 x 10% $1.1977 Superannuation 11.9773 - 0.1591 x 9% $1.0636

$14.9572

24. Productive Weeks = 52 – 9 = 43 weeks $ per Hour Wages Paid 12.0000 Annual Leave (4/43) 1.1163 Annual Leave Loading (17 ½ %) 0.1953 Other Leave (5/43) 1.3953 14.7069 Superannuation* 14.5116 x 9% 1.3060 Payroll Tax 14.7069 x 6% 0.8824 W.C.I. 14.7069 x 3% 0.4412 2.6296 * ( 14.7069 - 0.1953 ) $ 17.3365

25 Labour Charge Rates Total pay p.a. $380 per week x 52 weeks $19,760 + Leave Loading weeks 4 $380 0.175 $ 266 $20,026 Total weeks 52 Annual leave -4 Overtime Premium 1.5 Sick Leave -2 Public Holidays -2 Leave Loading 0.175 Weeks Available 44 Hours Sick 15 Annual Leave Pay 150 Tax Rate 30% Superannuation 9%

44 Number of working weeks x 37.5 hours per week = 1,650 Annual hours Gross Charge Rate = Total wages / annual hours $ 12.1370

Management Accounting in Australia - Solutions

74

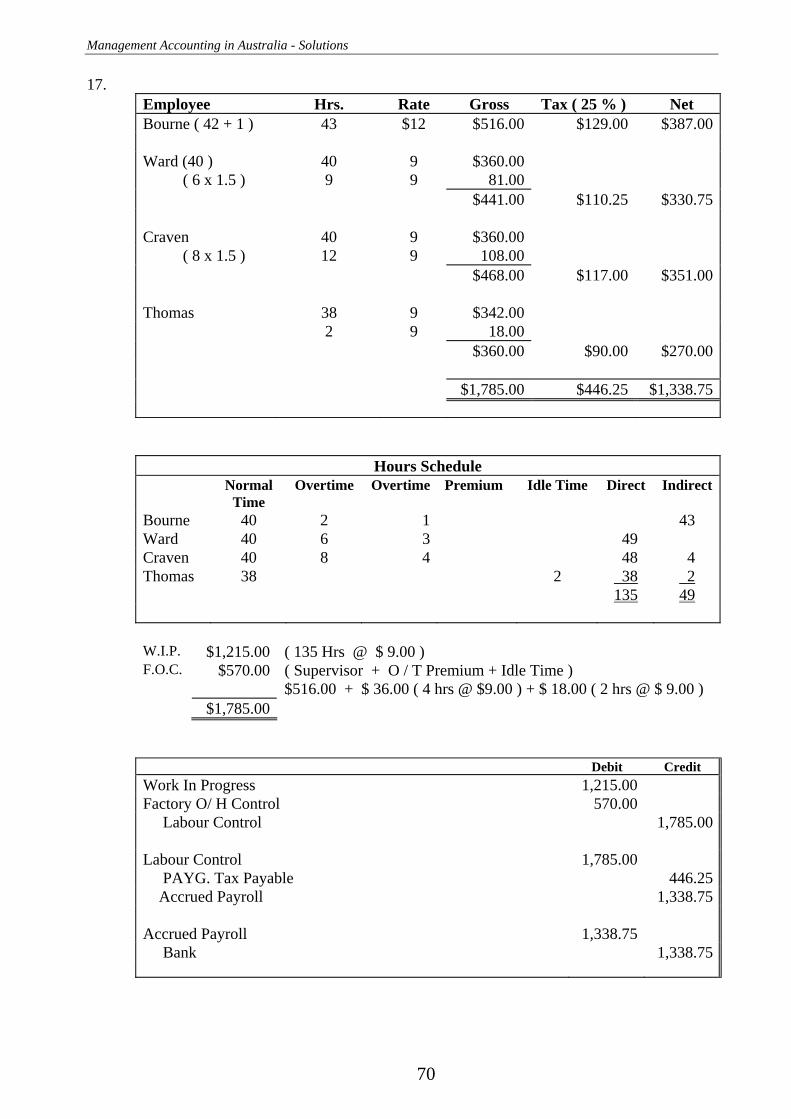

Reconciliation: Normal

Time Overtime

Base Rate: $380 Hrs p.w. 37.5 An Leave 0.09090 weeks 10.1333 10.1333 15.2000 + Loading 0.92121 x loading 0.1750 1.0824 Loading 0.1612 Public Holidays 0.04545 weeks 10.1333 0.4606 Sick Leave 0.04545 weeks 10.1333 0.4606 Gross Rate: 12.1370 15.2000 Super ( Gross Rate - An Leave Loading ) 9% 12.1370 - 0.1612 11.9758 x 9% 1.0778 Payroll Tax Normal Time 12.1370 x 8% 0.9710 Overtime 15.2000 x 8% 1.2160W.C.I. Normal Time 12.1370 x 6% 0.7282 Overtime 15.2000 x 6% 0.9120 Charge Rate 14.9140 17.3280Overtime Premium 2.4140

26.

Total pay p.a. $630 per week x 52 weeks $32,760 + Leave Loading weeks 6 $630 0.175 $ 662 $33,422

Total weeks 52 Annual leave -6 Overtime Premium 1.5 Sick Leave -2 Public Holidays -2 Leave Loading 0.175 Weeks Available 42 Hours Sick ( unpaid ) 14 Annual Leave Pay 35 Tax Rate 30% Superannuation 9%

42 Number of working weeks x 35 hours per week = 1,470 Annual hours Gross Charge Rate = Total wages / annual hours $ 22.7357

Chapter 5: Material & Labour

75

Reconcilation: Normal

Time Overtime

Base Rate: $630 Hrs p.w. 35 18.0000 27.0000 An Leave 0.1429 weeks 18.0000 + Loading 2.5714 x loading 0.1750 3.0214 Loading 0.4500 Public Holidays 0.0476 weeks 18.0000 0.8571 Sick Leave 0.0476 weeks 18.0000 0.8571 Gross Rate: 22.7356 27.0000 Super ( Gross Rate - An Leave Loading ) 9% 22.7356 - 0.4500 22.2856 x 9% 2.0057 Payroll Tax 6% Normal Time 22.7356 x 6% 1.3641 Overtime 27.0000 x 6% 1.6200 W.C.I. 9% Normal Time 22.7356 x 9% 2.0462 Overtime 27.0000 x 9% 2.4300Charge Rate 28.1516 31.0500Overtime Premium 2.8984 Time Sheet Analysis: 620 Direct Total Hours Worked 700 80 Indirect Normal Time 651 Overtime 49 Accrual: Debit Credit Work in Process Direct Hrs 620 x Ch Rate 27.2602 16,901

Factory Overhead Control Indirect Hrs 80 x Ch Rate 27.2602 2,181

Factory Overhead Control Overtime Hrs 49 x O.T. Pre 3.7898 186

Accrued Payroll Normal Time 651 x Base Rate 18.0000 13,041

Overtime 49 x O.T. Base 27.0000