Embed Size (px)

Citation preview

SOLAR FARM FEASIBILITY STUDY

District Council of Mount Remarkable

November 2013

2 ITP/A0121 – November 2013

Solar Farm Feasibility Study

DISTRICT COUNCIL OF MOUNT REMARKABLE Client contract No.: 2013 – 062 MS (L)

IT Power reference: A0121

Solar Farm Feasibility Study

November 2013

Prepared by:

IT Power (Australia) Pty Limited

Southern Cross House,

6/9 McKay St, Turner, ACT, 2612,

PO Box 6127, O’Connor, ACT, 2602, Australia.

Tel. +61 2 6257 3511

Fax. +61 2 6257 3611

E-mail: [email protected]

http://www.itpau.com.au

Document control

File path & name C:\Users\Nic\Dropbox\A0121 MTR Solar Farm Feasibility\Final\131120 Final deliverables\A0121 131119 Solar Farm Feasibility Report.docx

Author Nic Jacobson, Joe Wyder, Simon Franklin

Project Manager Nic Jacobson

Approved Joe Wyder

Date 19 November 2013

Distribution level Final

Template: ITP REPORT Form 001

Issue: 01; Date: 20/04/12

ITP/A0121 – November 2013 3

Solar Farm Feasibility Study

About IT Power

The IT Power Group, formed in 1981, is a specialist renewable energy, energy efficiency and

carbon markets consulting company. The group has offices and projects throughout the world.

IT Power (Australia) was established in 2003 and has undertaken a wide range of projects,

including designing grid-connected renewable power systems, providing advice for government

policy, feasibility studies for large, off-grid power systems, developing micro-finance models for

community-owned power systems in developing countries and modelling large-scale power

systems for industrial use.

The staff at IT Power (Australia) have backgrounds in renewable energy and energy efficiency,

research, development and implementation, managing and reviewing government incentive

programs, high level policy analysis and research, including carbon markets, engineering design

and project management.

About this report

This report was commissioned by the District Council of Mount Remarkable with the assistance of

the Local Government Association of South Australia.

4 ITP/A0121 – November 2013

Solar Farm Feasibility Study

CONTENTS

EXECUTIVE SUMMARY ................................................................................................... 6

1. LARGE-SCALE SOLAR FARMS ............................................................................... 8

Economic benefits ....................................................................................................... 8

2. ESTABLISH THE VIABILITY OF LARGE-SCALE SOLAR FARMS IN THE SOUTHERN FLINDERS ............................................................................................. 9

Results ...................................................................................................................... 11

100 kW roof mounted system ................................................................................ 11

1 MW ground mounted system .............................................................................. 11

10 MW ground mounted system ............................................................................ 12

Analysis of the Cost-Value Gap ............................................................................. 12

3. REVIEW OF FUNDING OPPORTUNITIES ............................................................... 14

Renewable Energy Target ......................................................................................... 14

Carbon Price ............................................................................................................. 15

Clean Energy Finance Corporation (CEFC) .............................................................. 15

Australian Renewable Energy Agency ...................................................................... 16

Emerging Renewables Program ............................................................................ 16

Regional Australia’s Renewables Initiative ............................................................ 17

Accelerated Step Change Initiative (ASCI) ............................................................ 18

Renewable Energy Venture Capital Fund .............................................................. 18

Regional Development Australia Fund ...................................................................... 18

South Australian Government Support ...................................................................... 19

Summary of funding opportunities ............................................................................. 20

4. IDENTIFY PREFERRED AREAS FOR LARGE-SCALE SOLAR FARMS ............... 21

Multi-criteria analysis ................................................................................................. 21

Data sources .......................................................................................................... 21

Processing ............................................................................................................. 24

Combining the criteria ............................................................................................ 25

Results ................................................................................................................... 26

Investigation – improving the grid .............................................................................. 26

ITP/A0121 – November 2013 5

Solar Farm Feasibility Study

5. OPTIONS PAPER FOR COUNCIL ACTIONS .......................................................... 28

6. DISCUSSION ........................................................................................................ 30

Recommendations for further investigations ............................................................. 30

7. REFERENCES ........................................................................................................ 32

APPENDIX A.PREFERRED AREAS FOR A 1 MW SOLAR FARM ............................... 33

APPENDIX B.PREFERRED AREAS FOR A 10 MW SOLAR FARM ............................. 34

APPENDIX C.10 MW PREFERRED AREA FOR AN IMPROVED GRID ........................ 35

ITP/A0121 – November 2013 6

Solar Farm Feasibility Study

EXECUTIVE SUMMARY

The District Council of Mount Remarkable is investigating the potential of renewable energy, in

the form of large-scale solar farms to add to the economic development of the district. The key to

understanding this potential is to understand the current financial viability of these projects at a

suitable scale. Following from the viability, to make an informed decision on the next actions

requires understanding the financial support and incentives available to support the development,

the areas likely to be targeted by developers and what actions the Council can take to improve

the project economics and draw investment to the District.

The viability of large-scale photovoltaic solar farms in the District Council of Mount Remarkable

was investigated by estimating the levelised cost of energy produced and comparing the cost to

the current price of energy from projects of similar scale. The difference between the two prices

indicates the price barrier to the development of solar farms. To attract investment in solar farms

in the DCMR, the price barrier needs to be reduced, if not overcome. The LCOEs from the three

representative solar farms and the price barriers for each is given in the table below.

Representative solar farm 100 kW roof

mounted

1 MW ground

mounted

10 MW ground

mounted

LCOE1 ($/MWh) $175 $247 $187

Retail price ($/MWh) $120 to $140

Retail price barrier ($/MWh) $35 to $55

Wholesale price2 ($/MWh) $90 to $110 $90 to $110

Wholesale price barrier3 ($/MWh) $137 to $147 $77 to $97

Table 1 Price barriers for solar farms in the District Council of Mount Remarkable

To assist the understanding of the Council, a multi-criteria analysis was completed to identify the

areas of the Council most suited and favourable to the development of solar farms. The analysis

used scale factors to give weight to different constraints to development. The analysis was

conducted for the 1 MW and 10 MW ground mounted solar farms. The resulting maps are shown

in Appendix A and Appendix B.

1 Based on 25 years for 1 and 10 MW and 10 years for 100 kW

2 Wholesale price is based on average NEM Pool Price and REC value

3 Wholesale price is based on average NEM Pool Price and REC value

ITP/A0121 – November 2013 7

Solar Farm Feasibility Study

The actions that can be taken by the Council are discussed in a separate Council Action Options

paper. The recommended actions for the District Council of Mount Remarkable selected from a

range of financial and facilitation based actions are:

Action Evaluation of impact Suitability for the District

A2 Soft loans Medium to High Suitable

B1 Fast track planning and

environmental approvals

Medium Suitable

B2 Re-zoning rural to renewable energy –

solar farm

Medium Suitable

Table 2 Recommend actions for DCMR

ITP/A0121 – November 2013 8

Solar Farm Feasibility Study

1. LARGE-SCALE SOLAR FARMS

There are two groups of solar technologies used for the conversion of solar energy to grid quality

electricity in large-scale solar farms. These are: photovoltaic systems and solar thermal systems.

A description of these two different technologies is available in Box 10.1 in Chapter 10 of the

Australian Energy Resource Assessment [1].

Solar thermal and concentrating photovoltaic systems will not be considered in this assessment.

They are currently less cost effective than flat photovoltaic module systems [2]. Solar thermal

systems for electricity generation are typically in the tens of megawatts scale and unsuitable for

connection to the existing distribution network in the Southern Flinders region. Concentrating

photovoltaic systems (CPV), as in use at the Alice Springs airport (Fresnel lenses) and near

Mildura (mirror parabolic dish), are not deployed widely as the capital cost of fixed PV has

decreased significantly relative to the cost of tracking CPV systems.

Figure 1 Concentrating solar PV at Alice Springs Airport4

This report will investigate the viability of solar farms using fixed array, flat photovoltaic module

systems. While tracking increases output, the additional capital and maintenance costs lead to

most large PV farms being fixed tilt.

Economic benefits

The economic benefits of developing large-scale solar farms extend beyond the boundary of the

project into the wider community. While estimates of these impacts are beyond the scope of this

document, the direct on going employment created by large-scale solar farms has been estimated

at 11 job years per MW during construction and 0.3 full-time equivalents per MW during operation

[3]. The development of a 10 MW system in the District would be expected to provide 110 job

years of employment over the construction period and a further 3 full time positions during the

operation of the plant.

4 http://www.alicesolarcity.com.au/solfocus-flat-plate-concentrator-systems

ITP/A0121 – November 2013 9

Solar Farm Feasibility Study

2. ESTABLISH THE VIABILITY OF LARGE-SCALE SOLAR FARMS IN THE SOUTHERN FLINDERS

In order to examine the financial viability of large-scale solar farms in the Southern Flinders a

number of different sized systems were considered. This is due to significant variation in the

financial characteristics of the difference sized solar farms. ITP conducted in-depth performance

and financial modelling for the following systems:

100 kW roof mounted system,

1 MW ground-mounted system, and

10 MW ground-mounted system.

Each of the different systems has its own unique characteristics that affect its overall financial

viability. Key items of note for the systems included:

The 100 kW system is eligible for Small Technology Certificates (STC) which significantly

reduce the upfront capital costs of the system

The 100 kW system (because it is (roof-mounted) requires a much simpler mounting

structure which reduces construction costs

The 100 kW system is able to be directly connected to the LV grid of the building on which

it is installed. This both reduces the grid connection costs for the project and increases the

potential revenue of the system through the off-setting of onsite electricity use.

The 1 MW system benefits from some economies of scale over the 100 kW system,

however, has increased grid-connection and civil costs.

The 10 MW system further benefits from economies of scale, however, requires a higher

grid voltage for network connection.

It is likely that only the larger plants would be able to attract commercial project finance

and therefore benefit from a reduced cost of capital.

The expected outputs for each of the systems considered were modelled using the industry

standard software package PVSyst. The modelled generation for each of the systems was

between 1,600 and 1,700 kWh/kWp/year. The smaller roof mounted system was at the lower end

of the production range, having lower output than the larger ground mounted systems. The

reduced output from the roof mounted system is primarily due to reduced airflow behind the

panels compared to the ground mount system leading to increased operating temperature of the

modules.

ITP/A0121 – November 2013 10

Solar Farm Feasibility Study

The key assumptions used in the financial models are shown in Table 3 below.

Capital costs

Representative Solar Farm

100 kW roof mounted 1 MW ground mounted 10 MW ground mounted

Item Cost per W (AUD)

Total cost (AUD)

Cost per W (AUD)

Total cost (AUD)

Cost per W (AUD)

Total cost (AUD)

PV modules $0.77 $77,000 $0.75 $750,000 $0.70 $7,000,000

Inverters (inc transformers for large systems)

$0.17 $17,000 $0.22 $220,000 $0.20 $2,000,000

BoS Components

$0.30 $30,000 $0.38 $380,000 $0.35 $3,500,000

Civil Works $0.00 $0 $0.25 $250,000 $0.20 $2,000,000

Labour $0.20 $20,000 $0.20 $200,000 $0.20 $2,000,000

Shipping & transport

$0.05 $5,000 $0.05 $50,000 $0.05 $500,000

Contingencies $0.05 $5,000 $0.05 $50,000 $0.05 $500,000

Engineering $0.00 $0 $0.10 $100,000 $0.10 $1,000,000

Grid Connection

$0.10 $10,000 $0.50 $500,000 $0.25 $2,500,000

Land $0.00 $0 $0.005 $5,000 $0.0025 $25,000

STC value $35/STC

-$0.73 -$72,500 $0.00 $0 $0.00 $0

TOTAL $0.91 $91,500 $2.51 $2,505,000 $2.10 $21,025,000

Table 3 Capital costs of large-scale solar farms in the District Council of Mount Remarkable

ITP/A0121 – November 2013 11

Solar Farm Feasibility Study

Results

100 kW roof mounted system

The key modelling assumptions for the 100 kW system were:

Capital Cost: $91,500

O&M Costs: 1% of capital

Roof lease costs: $2,000

Permits and approvals: $10,000

100% equity financed at 15% cost of equity

The results of the modelling for the 100 kW system are shown in Table 4 below.

Project lifetime 30 years 25 years 20 years 15 years 10 years 5 years

LCOE $0.132 $0.135 $0.141 $0.152 $0.175 $0.268

Table 4 LCOE - 100 kW roof mounted system

As many commercial buildings change occupiers relatively frequently a system life of 10 years

assumed when conducting further analysis.

1 MW ground mounted system

The key modelling assumptions for the 1 MW system were:

Capital Cost: $2.5M

O&M Costs: 1% of capital per year

Insurance and other costs: 1.3% of capital

Setup costs (permits and approvals, legal costs, etc): $204,000

Debt to equity: 60%

Cost of debt: 8%, Loan term: 15 years

Cost of equity: 15%

ITP/A0121 – November 2013 12

Solar Farm Feasibility Study

The results of the modelling for the 1 MW system are shown in Table 5 below.

Project lifetime 30 years 25 years 20 years 15 years 10 years 5 years

LCOE $0.242 $0.247 $0.257 $0.279 NA NA

Table 5 LCOE – 1 MW ground mounted system

As the loan term for the system is 15 years only LCOEs for a system life of 15 years of greater

are considered. The assumed system life for further analysis is 25 years.

10 MW ground mounted system

The key modelling assumptions for the 10 MW system were:

Capital Cost: $21M

O&M Costs: 1% of capital per year

Insurance and other costs: 0.6% of capital

Setup costs (permits and approvals, legal costs, etc): $1.09M

Debt to equity: 70%

Cost of debt: 8%, Loan term: 15 years

Cost of equity: 15%

The results of the modelling for the 10 MW system are shown in Table 6 below.

Project lifetime 30 years 25 years 20 years 15 years 10 years 5 years

LCOE LCOE $0.183 $0.187 $0.195 $0.212 NA

Table 6 LCOE – 10 MW ground mounted system

As the loan term for the system is 15 years only LCOEs for a system life of 15 years of greater

are considered. The assumed system life for further analysis is 25 years.

Analysis of the Cost-Value Gap

It is assumed that the 100 kW system would be able to offset the electrical usage of the building it

is installed on while the 1 MW and 10 MW systems would sell directly into the grid. As such, the

tariffs available for the systems fall into two categories; off-set retail electricity prices for the

smaller system and long term PPA pricing (based on NEM and LGC prices) for the larger

systems.

ITP/A0121 – November 2013 13

Solar Farm Feasibility Study

While retail electricity prices in many areas are quite high (relative to pool prices) the 100 kW roof

mounted system would only be able to offset the electricity consumption component of the tariff

as the system is unlikely to have an effect on demand charges for the site. Therefore, the value of

the off-set electricity is likely to be in the order of 12 to 14c/kWh ($120 to $140/MWh). At present,

any electricity feed into the grid from the roof mounted system is likely to only attract a value of

9.8c/kWh.

The PPA pricing for the large scale systems is likely to be similar to that of recent wind farm PPAs

in the area with an allowance for the time of day benefit due to the output profile of a solar farm

compared to a wind farm. The PPA price is likely to be in the order of $90 to $110/MWh.

Table 7 below shows provides a summary of the financial viability of large scale solar farms in the

region.

Representative solar farm 100 kW roof

mounted

1 MW ground

mounted

10 MW ground

mounted

LCOE ($/MWh) $175 $247 $187

Retail price ($/MWh) $120 to $140

Retail price barrier ($/MWh) $35 to $55

Wholesale price5 ($/MWh) $90 to $110 $90 to $110

Wholesale price barrier6 ($/MWh) $137 to $147 $77 to $97

Table 7 Price barriers for solar farms in the District Council of Mount Remarkable

The LCOE estimates for the ground mounted systems in Table 5 and Table 6 show a decreasing

cost of energy, and increasing viability of larger ground mounted solar farms through economies

scale effects. As a comparison, the feed in tariffs offered in recent ACT reverse auction for the

successful proposals: $186/MWh for a 7 MW solar farm and $178/MWh for a 13 MW solar farm

[4] are similar to the results above.

5 Wholesale price is based on average NEM Pool Price and REC value

6 Wholesale price is based on average NEM Pool Price and REC value

ITP/A0121 – November 2013 14

Solar Farm Feasibility Study

3. REVIEW OF FUNDING OPPORTUNITIES

This section provides a scan of the Commonwealth and external funding opportunities for solar

farms in the region.

The Australian Government has a range of measures which aim to increase the uptake of

renewable energy in Australia. These include the Renewable Energy Target (RET) of ‘20%

renewable energy by 2020’, carbon pricing, the Clean Energy Finance Corporation (CEFC) and

the Australian Renewable Energy Agency (ARENA).

How these measures may change after the Federal election will depend on the result for the

House of Representatives and the make up of the new Senate. This summary outlines the

measures existing at the start of the 2013-14 financial year. It does not explore in detail, the

various scenarios that may eventuate following the Federal election on 7 September 2013.

However, it is worth noting the Coalition has announced it intends to abolish the carbon price and

the CEFC. It has also announced that it intends to reduce ARENA’s budget and review the RET

in 2014. This introduces uncertainty for renewable generation investments due to the review’s

potential impact on renewable energy certificate prices.

Renewable Energy Target

The RET commenced in 2001 and is a legislative scheme that creates a guaranteed market for

renewable generation by using a mechanism of tradable certificates. Demand for the renewable

energy certificates is created by placing a legal obligation on liable entities, (mainly electricity

retailers) to surrender a calculated number of certificates each year.

On 1 January 2011, the RET was split into two parts:

Small-scale Renewable Energy Scheme, (SRES); and

Large-scale Renewable Energy Target, (LRET).

The SRES allows small-scale installations such as solar hot water systems, heat pump hot water

systems, residential PV systems, small-scale wind turbines and small-scale hydro systems to

create Small-scale Technology Certificates (STCs). Liable entities are required to surrender a

calculated amount of STCs each quarter.

Typically, for solar PV, the STCs are allocated based on a forecast output for 15 years,

(deeming). Deeming is only available for Small-scale Generation Units and for solar PV this is

defined as systems no more than 100 kW.

An STC is equivalent to 1 MWh of renewable generation and the STC clearing house effectively

caps their price at $40. However, as a tradeable commodity, the price fluctuates based on supply

ITP/A0121 – November 2013 15

Solar Farm Feasibility Study

and demand. The price fell to less than $20 in 2011 and the STC spot price was about $37 in

mid-2013. A 10 kW PV array installed in the region would be eligible to create 207 STCs.

The LRET allows larger renewable generation facilities to create Large-scale Generation

Certificates (LGCs). LGCs are also equivalent to 1 MWh of renewable generation but are created

on the metered output of the power station. This enables the renewable power station to have two

separate income streams, one from selling the electricity and the other from selling the LGCs.

However, these are often combined under a Power Purchase Agreement (PPA).

The penalty for not surrendering enough LGCs to meet a liability is $65 per LGC, which is not tax

deductable. This effectively caps the LGC price at about $93. However, since the market for

renewable energy certificates and LGCs commenced, there has been an oversupply of

certificates. In mid-2013, their spot price was around $32. It should be noted that the majority of

LGCs are purchased through long term PPAs and their price is not published.

A 1 MW solar farm generating 1,400 MWh per year would have an annual LGC income of around

$45,000, assuming a price of $32 / LGC.

Carbon Price

Operating in tandem with the RET, the carbon price commenced on 1 July 2012. This makes

large emitters of greenhouse gas emissions financially liable. Originally, the price was to be fixed

for three years before transitioning to an emissions trading scheme.

On 16 July 2013, the Prime Minister announced the government’s intention to bring the start date

of emissions trading forward to 1 July 2014. This is expected to reduce the carbon price from a

fixed $24/tonne to a floating price of less than $10/tonne due to linkages with European markets.

The Coalition has announced an intention to abolish the carbon price and if it gains a lower house

majority, the ability to do this will be determined by the make up of the Senate.

The carbon price increased the costs of fossil fuel generation and thus increased wholesale

electricity prices. This decreases the cost gap for new renewable generation. However, as the

LGC price is influenced by the difference between the wholesale electricity price and the cost of

wind energy, the overall effect on project economics is not significant at present.

Clean Energy Finance Corporation (CEFC)

The CEFC commenced operations on 1 July 2013 and has $10 billion to invest in firms and

projects utilising clean energy technologies as well as manufacturing businesses that focus on

producing the inputs required. It is commercially oriented and expected to make a positive return

on its investments. Capital that is returned from investments will be retained for reinvestment by

the CEFC, with the Board to determine the quantum of any dividends payable to the Australian

Renewable Energy Agency.

ITP/A0121 – November 2013 16

Solar Farm Feasibility Study

The CEFC, after assessing the risks and commercial returns, may make obtaining solar farm

finance slightly less difficult by providing some of the debt required to reach financial close on a

project.

Similar to the carbon price, the Coalition’s plan to abolish the CEFC will need a majority in both

houses of parliament.

Australian Renewable Energy Agency

ARENA commenced on 1 July, 2012 and provides financial assistance for:

research, development, demonstration, deployment and commercialisation of

renewable energy and related technologies; and

storage and sharing of knowledge and information about renewable energy

technologies.

It has a range of programs including

Emerging Renewables Program,

Regional Australia Renewables Initiative,

Accelerated Step Change Initiative, and

Renewable Energy Venture Capital Fund.

Emerging Renewables Program

The objectives of the Emerging Renewables Program are to provide funding to:

drive innovation of renewable energy technologies in Australia,

reduce or remove roadblocks,

achieve renewable energy industry development and capacity building in Australia,

and

support the delivery of ARENA’s Supporting High-value Australian Renewable Energy

knowledge initiative.

The Emerging Renewables Program provides funding for Projects or Measures.

Projects are defined as activities that:

Progress the development of a renewable energy technology along the technology

innovation chain, or

Develop or demonstrate a renewable energy technology to remove or reduce a

roadblock.

ITP/A0121 – November 2013 17

Solar Farm Feasibility Study

Measures are defined as:

Knowledge activities, in support of the program’s objectives,

Renewable energy industry development and capacity building activities, or

Preparatory activities for projects, including potential projects for funding by ARENA.

The Emerging Renewables Program is unlikely to support the straightforward deployment of a

solar farm in the region. A solar farm project is likely to need an innovative approach to

overcoming a roadblock for consideration for Emerging Renewables Program funding.

Regional Australia’s Renewables Initiative

The Regional Australia’s Renewables Initiative supports trials of renewable energy solutions in

regional and remote locations. It consists of two components:

Regional Australia’s Renewables Industry Program (I-RAR), and

Community and Regional Renewable Energy (CARRE) program.

The objectives of the I-RAR are to:

demonstrate a portfolio of renewable energy solutions, including hybrid and integrated

systems, in Australia off-grid and fringe-of-grid areas,

ensure knowledge is produced and disseminated regarding the deployment of renewable

energy solutions in remote areas catalysing further renewable energy uptake, and

remove roadblocks, leading to greater deployment of renewable energy solutions in off-

grid and fringe-of-grid areas.

To be eligible, projects must be larger than 1 MW and off-grid or fringe-of-grid. The definition of

fringe-of-grid is areas in the National Electricity Grid that are remote, where remote is as defined

in the Australian Statistical Geography Standard. The DCMR region is classified as Outer

Regional Australia and thus is not eligible under the I-RAR.

The objectives of the CARRE program are to:

demonstrate technical viability and system reliability of feeding more renewable energy

into isolated electricity systems and mini-grids,

facilitate the further development of supporting technologies and systems that will improve

renewable energy reliability and commercial success, such as system integration and

storage, through demonstration and deployment,

demonstrate the commercial viability of innovative business models, including community

ownership models, for renewable energy systems in these locations, and

ITP/A0121 – November 2013 18

Solar Farm Feasibility Study

develop and share knowledge and experience in implementing, operating and maintaining

renewable energy systems among regional energy suppliers and distributors and

commercial and community customers.

To be eligible for funding under the CARRE program, the applicant must be an Australian

electricity distributor and the project not connected to the main-grid. Thus the CARRE is unlikely

to support solar farms in the region.

Accelerated Step Change Initiative (ASCI)

The objectives of the ASCI are to fund projects above $20m each that allow ARENA to capitalise

on exceptional opportunities that are consistent with its General Funding Strategy but are not

captured through ARENA’s existing suite of initiatives and programs. It is unlikely that a solar farm

project in the region would be eligible for ASCI funding.

Renewable Energy Venture Capital Fund

This venture capital fund is managed by Southern Cross Venture Partners. The primary

objectives of the fund are to:

increase the number of Australian renewable energy and enabling technology companies

that are successful in Australian and overseas markets,

foster the skills and management capability of Australian renewable energy and enabling

technology companies by providing active investment management, and

leverage additional investment in Australian renewable energy technology and enabling

technology companies from the private sector, including from international sources.

This fund would not invest in solar farms in the region as it is more focused on commercialisation

of new technologies.

Regional Development Australia Fund

The Regional Development Australia Fund (RDAF) is administered by the Department of

Regional Australia, Local Government, Arts and Sports. The objective of the RDAF is to support

the economies and communities of Australia’s regions.

RDAF Round 5 closed on 22 July 2013. While electricity infrastructure is not listed as ineligible,

the announced projects for Round 4 are mainly transport, sport and tourism related. Further

information is available from the website: www.regional.gov.au/regional/programs/rdaf.aspx

The Flinders Ranges Council led a consortium of four local government councils, including the

District Council of Mount Remarkable, which was successful in obtaining RDAF Round 1 funding

for 10 solar power systems and 84 solar lights.

ITP/A0121 – November 2013 19

Solar Farm Feasibility Study

South Australian Government Support

The only South Australian Government funding program identified that may be relevant is the

Regional Development Fund (RDF).

The RDF has funding of $3 million year and is delivered by Primary Industries and Regions South

Australia (PIRSA). The guides for applicants are available from the website:

www.pir.sa.gov.au/regions/programs/rdf

The RDF offers grant funding of $50,000 to $200,000 through two streams:

i) Growing Stronger Regions

For non-metropolitan Regional Development Australia Associations to facilitate

regional economic development that directly delivers on:

South Australia’s Strategic Plan targets,

PIRSA Strategic Priorities,

South Australian Government’s seven priorities.

ii) Creating Competitive Regions – up to 50% eligible project costs

For non-metropolitan private sector businesses, industry associations, community

organisations, regional local government, and the South Australian non-metropolitan

Regional Development Australia Associations to leverage funds to support the

delivery of new regional employment and investment directly linked with the following

strategic priorities of the State Government:

premium food and wine from our clean environment,

growing advanced manufacturing, or

realising the benefits of the mining boom for all South Australians.

The Creating Competitive Regions 2014 funding round Expressions of Interest close on 27

September 2013. The Growing Stronger Regions - Guide for Applicants does not specify when

applications for this stream’s 2014 funding round closes. However, the 2013 funding round

closed on 28 September 2012.

The guide for applicants for both streams indicates that the following is not eligible:

projects undertaken on behalf of third parties, and

feasibility studies, business cases, plans and reports.

ITP/A0121 – November 2013 20

Solar Farm Feasibility Study

However, the Growing Stronger Regions – Guide for Applicants caveats the second dot point by

stating:

‘Feasibility studies, business cases, plans and reports will not be funded where they do not

form part of an established and broader program that meets the Regional Development

Fund Stream 1 purpose and objectives’

It is recommended that DCMR contact PIRSA’s Senior Regional Industry Liaison Officer on

(08) 8226 0218 to discuss how this program may support council activities and whether there is

any scope for funding solar farm developments in the region or their facilitation.

South Australian Feed-in Scheme

The South Australian solar feed-in scheme is open to electricity consumers that consume less

than 160 MWh per year. For PV systems that receive permission to connect after 30 September

2013, the minimum retailer payment is 9.8c/kWh (GST exc) to 31 December 2013. The minimum

retailer payment for 2014 and onwards is being reviewed by the Essential Services Commission

of South Australia. Submissions closed on 26 July 2013 and an outcome is expected before the

end of the year.

Summary of funding opportunities

As the Solar Flagships program has closed, there is no grant funding available from to support

the straightforward deployment of proven, renewable energy technologies, such as solar PV

farms, in the region.

The Australian Government’s principal support mechanism is the renewable energy target. This

market based mechanism, predominantly, assists the lowest cost forms of renewable energy

such as wind farms.

The Emerging Renewables Program may support a solar farm in the region, if it involves an

innovative approach to overcoming a roadblock that is replicable for future projects. As the NSW

government is funding several community solar farm feasibility studies7, it may be difficult to

identify an innovative approach that would attract Emerging Renewables Program funding.

7 http://www.environment.nsw.gov.au/resources/MinMedia/MinMedia13053001.pdf

ITP/A0121 – November 2013 21

Solar Farm Feasibility Study

4. IDENTIFY PREFERRED AREAS FOR LARGE-SCALE SOLAR FARMS

Identifying the preferred areas of the DCMR region is a key element of understanding the

opportunity presented by solar farms and the attractiveness of the District to investors.

Multi-criteria analysis

To assist the Council’s thinking the areas likely to be targeted by developers were identified

through a multi-criteria analysis. Using spatial information, that is electronic maps, ITP combined

the criteria that exclude8 solar farm development with those that have a variable9 impact on the

attractiveness for development to produce a colour-graded map that indicates the relative

attractiveness to developers of solar farms of each part of the District.

A separate analysis was carried out for the 1 MW and 10 MW solar farms as the electricity grid

connection requirements at the two scales are very different.

Data sources

Spatial information was obtained from public sources where possible. The Government of South

Australia and the Government of Australia operate internet-based data portals that provide a

range of spatial data. Where required, data was obtained directly from the custodian organisation.

Data was obtained from the sources listed in Table 8.

Source

Number

Data portal Internet address

1. South Australian Government

Data Directory

http://data.sa.gov.au/

2. Housing Property and Lands,

Spatial Data Downloads

Government of South Australia

http://www.sa.gov.au/subject/

Housing%2C+property+and+land/

Building+and+development/South+Australia

%27s+land+supply+and+planning+system/

Planning+data+for+research+and+mapping/

Spatial+data+downloads

8 Exclusions are factors that prohibit development. The converse of exclusion is allowed. They have a yes or no value.

9 Variables are factors that do not prohibit development, rather have a location specific value that is considered in

decision making.

ITP/A0121 – November 2013 22

Solar Farm Feasibility Study

Source

Number

Data portal Internet address

3. NatureMaps

Government of South Australia

http://www.naturemaps.sa.gov.au/

download_spatial_layers.html

4. National Elevation Data

Framework Portal

Government of Australia,

http://nedf.ga.gov.au/geoportal/

catalog/main/home.page

5. SA Power Networks http://www.sapowernetworks.com.au

6. Bureau of Meteorology http://www.bom.gov.au

Table 8 Spatial data sources

Community consultation

A discussion paper and request for opinions on solar farms was circulated to residents of DCMR

through the Council’s website10 on 23 August 2013. Following distribution to the community the

discussion paper was publicised to the industry via the Australian PV Association e-newsletter on

9 September 2013.

Community perspectives were not included in the analysis. No responses from the community

were received by 16 September 2013 supporting the decision not to use a community view based

criterion.

Exclusions

The criteria that exclude solar farm development are given in the table below. The table describes

which elements of each data set exclude and which allow solar farm development. These criteria

provide a yes or no answer for solar farm development.

10

http://www.mtr.sa.gov.au/page.aspx?u=148

ITP/A0121 – November 2013 23

Solar Farm Feasibility Study

Criteria Values excluding solar farms

Values allowing solar farms

Source Number, Data Set Name, Specific URL11

National Parks

All values indicating a park or reserve

Nil 1, Conservation Reserve Boundaries http://data.sa.gov.au/dataset/conservation-reserve-boundaries

Native vegetation

All values indicating native vegetation

Nil 3, Native Vegetation Cover – Statewide (Dataset #826)

Land use All categories except for those listed in Values Allowing column

Agriculture, Livestock, Industry, Rural residential > 2.5 Ha, Vacant > 2.5 Ha

2, Generalised Land Use

Planning zones

Rural Living. All categories except for those listed in Values Allowing column.

Rural, Deferred Urban, Industrial, Infrastructure

2, Land development zones

Bushfire risk High, Medium

General 1, Bushfire Protection Areas http://data.sa.gov.au/dataset/bushfire-protection-areas

Table 9 Criteria excluding solar farm development

Variable impacts

Criteria that have a variable impact on the attractiveness for solar farm development on the basis

of location, or criteria where the value varies across the area under consideration are discussed

in the following table. The table describes the basis for the variable to influence the attractiveness

for solar farm development. The table also indicates the source of the data, the data sets used

and the specific source of the information.

11

If different from the source URL or website address

ITP/A0121 – November 2013 24

Solar Farm Feasibility Study

Variable Measure Source, Data Set Name, Specific URL12

Electricity network

Cost based on distance to suitable connection to network

5, HV Line, HV Cable, LV Line, LV Cable, Substations

Terrain Slope North facing slopes above 30° are not suitable. South facing slopes above 10° are not suitable.

Derived from 4, 1 second SRTM Derived Digital Elevation Model (DEM) version 1.0

Terrain Shading Hours of shading Derived from 4, 1 second SRTM Derived Digital Elevation Model (DEM) version 1.0

Solar resource Annual average MJ/m2 6, Annual Average DNI (1997 – 2007)

Table 10 Criteria with variable impacts on solar farm development

Processing

The next step in the multi-criteria analysis is to process each of the criteria to create a gridded

data set or a raster map13 of values representing the exclusion or variable. The criteria that are

provided in this format require little more processing than identifying the range of values and

working out an appropriate scaling or weighting factor.

Criteria that are provided as vector or line data, where each part of the drawing is described be a

start and end point or a start point and a direction and distance, the information needs to be

converted to a raster. For exclusions the map is converted to a raster where each cell has a yes

or no value.

For the grid network, the criterion is the cost of the connection as determined by: the type of

connection, either line or substation; the rated capacity of the connection; the voltage at the

connection point; and the distance from the connection point. The shortest distance to a

connection point is calculated for each point. Then the cost equation from Table 11 is applied to

create a map of grid connection costs.

12

If different from the source URL or website address 13

A raster is an image composed of points or pixels. Each point has a reference and value.

ITP/A0121 – November 2013 25

Solar Farm Feasibility Study

Solar farm 33 kV line 33 kV substation 11 kV feeder 11 kV

substation

10MW $2.2 million +

$300,000/km

$2.0 million +

$300,000/km Cannot take load

$1.2 million +

$250,000/km

1MW Cost Prohibitive Cost Prohibitive $800,000 +

$200,000/km

$600,000 +

$200,000/km

Table 11 Grid connection cost criterion

An important constraint on the development of solar farms in the District is the capacity of the

network. The SA Power Networks annual planning document [5] provides detailed information on

the rated capacity of the lines and substations across South Australia. In the District, there are a

limited number of lines and substations that have a rated capacity that can accept a 10 MW load

or generator. This limits the areas where a 10 MW solar farm can be economically connected.

For the solar resource the existing raster is used without refinement. However, the solar resource

information used has a 5 km grid resolution which leads to artefacts in the final mapping. This can

be seen clearly in Appendix B in the area to the north-northwest of the Baroota substation. These

step changes could be avoided using higher resolution solar resource data.

The terrain in the District is included in the analysis and is based on a ~30 m resolution digital

elevation model (DEM). The DEM was processed to calculate shading from the terrain, areas of

high slope, and areas of moderate south-facing slope.

Combining the criteria

Once the exclusions and variables have been processed into rasters, they are combined. At each

point each exclusion is evaluated in turn by a simple logic statement14. If a point is excluded by a

layer, no further evaluation is carried out. If the exclusions layers exclude a point, a numeric value

such as -9999 is included in the results layer, and no further evaluation takes place. If after all the

exclusions have been evaluated, the point is still included, the cost of the development is

calculated at the point using the equations such as this for the 10 MW solar farm:

10MW_cost_total = ($19,610,000 + lowest value from (10MW_33kVcost,

10MW_11kVSubcost, 10MW_33kVcost, 10MW_11kVSubcost)) * (20 / Solar_Resource)

14

Such as if X then Y else Z

ITP/A0121 – November 2013 26

Solar Farm Feasibility Study

The result of combining the raster layers using the logic and equations is a total cost, expressed

as millions of dollars.

Results

The resulting raster maps were then presented for printing at A3 size. They are also provided in

Appendix A Preferred Areas for a 1 MW solar farm and Appendix B Preferred Areas for a 10 MW

solar farm. The A3 maps are supplied.

The connection cost is a key variable component of the overall cost of solar farm. For the 10 MW

solar farm, a 1 km connection to a 33 kV substation represents about 12% of the total capital

cost. As the length of the connection increases, proportional cost of the grid connection increases

and so does the LCOE, making the cost value gap for a solar farm project larger.

The preferred area maps show the exclusion zones as transparent and the possible areas

shaded with a graduated range of colour. The graduated colour is based on the total cost of

developing the solar farm and shows the cost increasing with distance from the grid connection

point. The quality of the solar resource indicates that the preference is for areas toward the north

of the district.

The maps indicate that the preferred locations for a 10 MW solar farm are in the immediate

vicinity of the Murraytown and Baroota substations and the line connecting Murraytown to

Baroota and then to Bungama.

For the 1 MW solar farm the grid does not present the same limitation as the 10 MW solar farm.

In this case, the preferred areas follow the 33 kV and 11 kV lines and centre on the substations.

As the cost of connecting to substation is lower than breaking in to a line, a solar farm can be

developed further from a substation at the same cost.

It should be noted that this analysis did not consider all possible variables influencing

development decision. The cost of land access not considered as a variable across the District,

although it is generally known that the areas of higher and more reliable rainfall are more

valuable. Further investigations could incorporate rainfall information as a proxy for land value.

Investigation – improving the grid

A ‘what if’ investigation of the impact on the areas preferred for development of a 10 MW solar

farm of improving the grid in the District was carried out. The preferred areas for 10 MW solar

farms were reassessed using the assumption that all of the 33 kV distribution lines, 33 kV

substations and 11 kV substations have the capacity to accept a 10 MW solar farm. In this case,

as expected, the preferred areas follow the lines, with a focus on the area near the Wilmington

substation. The results, a third preferred areas map was produced and is presented in Appendix

C. Further explanation of this investigation follows.

ITP/A0121 – November 2013 27

Solar Farm Feasibility Study

The preferred area maps highlight the attraction of solar farms to proximity to the electricity

network and in particular the substations. At substations, it is possible to add extra equipment and

connect, minimising costs. Connection to a power line requires additional equipment compared to

a substation connection thereby increasing costs. Any connection to the electricity distribution

system in the District will require the approval of SA Power Networks.

The SA Power Networks’ Electricity System Development Plan 2012 [5] provides details of the

lines and substations in their network. In the District the network consists primarily of 33 kV

distribution lines. The transmission connection point at Baroota supplies lines to Murraytown and

Bungama. The line to the Murraytown non-zone substation transformer has a capacity of 10 MVA.

This transformer supplies lines to:

Melrose (5.6 MVA) then Wilmington (7.6 MVA)

Booleroo Centre then Orroroo (7 MVA)

Gladstone (5.6 MVA)

The substations at Melrose, Booleroo and Wilmington all have transformers rated at 1 MVA.

What this means is that in the District the 10 MW solar farm can only be connected to the

Baroota or Murraytown substations or the line from Bungama to Murrarytown without requiring

extensive and expensive upgrades to the existing lines and substations.

ITP/A0121 – November 2013 28

Solar Farm Feasibility Study

5. OPTIONS PAPER FOR COUNCIL ACTIONS

The options for a local government in Australia to take action to attract and support investment in

renewable energy in their area of governance are limited. This limitation is a result of the

jurisdictional responsibilities delegated from the Government of Australia to the State

Governments and then to Local Governments. The delegation of powers varies from State to

State. In South Australia, Local Government is responsible for the provision of local services and

regulation of activities at a regional level. The use of a feed-in-tariff or portfolio standard for

example are outside the powers of Local Governments in South Australia.

In the areas of economic development and renewable energy, the Council has limited areas

under its direct control where it can take action and influence the economics. While both

Commonwealth and State governments have the power to levy taxes and duties, Local

government does not. Council’s also have limited budgets with their income generated primarily

from rates. Increasing their rates to provide support for commercial projects may not be

welcomed by their constituents.

To identify options that are available to Local Governments literature on the experience and

practices used in other countries and jurisdictions were reviewed to prepare a separate Council

Options Paper. To increase the applicability of this research, a range of options were identified

and assessed. As expected, some are not well suited to utilisation by all councils.

The literature review was open to all types of support mechanism and then filtered to produce a

list of the options suitable to the policy and regulatory powers of Local Government. The literature

reviewed includes, but is not limited to:

Compendium of Best Practices, Sharing Local and State Successes in Energy Efficiency

and Renewable Energy from the United States [6]

Deploying Renewables 2011: Best and Future Policy Practice [7]

Deploying Renewables: Principles for Effective Policies [8]

The Database of State Incentives for Renewables and Efficiency [9]

The current economics of solar farms is the main barrier to their deployment. As the modelling in

Section 2 of this report shows there is a significant gap between the value of energy from solar

farms and the cost of energy from solar farms. To assess the benefits of implementing the action,

its impact on the economics of solar farm development was considered qualitatively.

Council Options Paper identifies two broad groups of potential actions, Financial Actions and

Facilitation Actions. The Financial based incentives or actions provide direct financial support or

savings to the solar farm. Facilitation based incentives may indirectly reduce the cost of

ITP/A0121 – November 2013 29

Solar Farm Feasibility Study

developing the solar farm or make the process of obtaining approval for the solar farm more

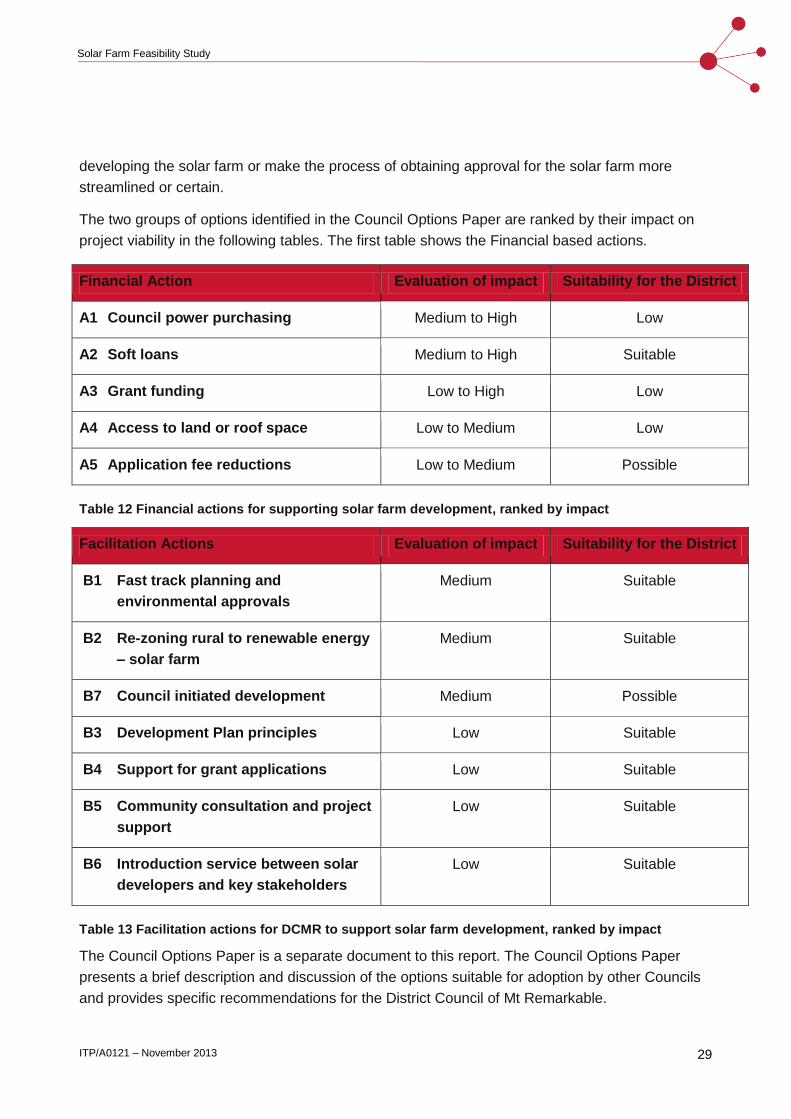

streamlined or certain.

The two groups of options identified in the Council Options Paper are ranked by their impact on

project viability in the following tables. The first table shows the Financial based actions.

Financial Action Evaluation of impact Suitability for the District

A1 Council power purchasing Medium to High Low

A2 Soft loans Medium to High Suitable

A3 Grant funding Low to High Low

A4 Access to land or roof space Low to Medium Low

A5 Application fee reductions Low to Medium Possible

Table 12 Financial actions for supporting solar farm development, ranked by impact

Facilitation Actions Evaluation of impact Suitability for the District

B1 Fast track planning and

environmental approvals

Medium Suitable

B2 Re-zoning rural to renewable energy

– solar farm

Medium Suitable

B7 Council initiated development Medium Possible

B3 Development Plan principles Low Suitable

B4 Support for grant applications Low Suitable

B5 Community consultation and project

support

Low Suitable

B6 Introduction service between solar

developers and key stakeholders

Low Suitable

Table 13 Facilitation actions for DCMR to support solar farm development, ranked by impact

The Council Options Paper is a separate document to this report. The Council Options Paper

presents a brief description and discussion of the options suitable for adoption by other Councils

and provides specific recommendations for the District Council of Mt Remarkable.

ITP/A0121 – November 2013 30

Solar Farm Feasibility Study

6. DISCUSSION

The cost value gap for large scale solar farms in the District of Mount Remarkable is sufficient to

make action by the Council unlikely to remove it entirely. Action by the Council would instead set

out to make the District more attractive for developers than other regions.

The DCMR has a competitive solar resource; land is suitable and accessible, making it as

prospective for solar farm development as many other areas of the State and Australia. By

implementing one or more actions, DCMR could increase its attractiveness for investment and

promoting them to the solar farm industry.

The recommended Council Actions for DCMR are:

Action Evaluation of impact Suitability for the District

A2 Soft loans Medium to High Suitable

B1 Fast track planning and

environmental approvals

Medium Suitable

B2 Re-zoning rural to renewable energy –

solar farm

Medium Suitable

Table 14 Recommend actions for DCMR

Action A1 Council power purchasing is not recommended for the DCMR due to the size of the

demand from Council operations and the extensive use of solar power.

When considered together, the cost value gap and the preferred areas for solar farm it is clear

that the attractiveness of the District for 10 MW solar farms in the District is limited. When

considering 1 MW solar farms, there are more siting options however the economics are less

favourable.

Recommendations for further investigations

The review of the electricity network in the District identified limited opportunities to connect a

10 MW solar farm at competitive cost. At the 1 MW scale, the opportunity for cost effective

connection is greater, however the economics are less favourable. Investigation of an

intermediate size solar farm of around 5 MW could be undertaken to understand the cost – value

gap at this scale and the impacts of the grid network.

ITP/A0121 – November 2013 31

Solar Farm Feasibility Study

The solar resource information used is based on a 5 km grid that introduces some artefacts into

the preferred area maps. It is recommended that higher resolution solar data is obtained and

used in the mapping to avoid artefacts.

It is noted that this analysis did not consider all possible variables influencing development

decision. The cost of land access not considered as a variable across the District, although it is

generally known that the areas of higher and more reliable rainfall are more valuable. Further

investigations could incorporate rainfall information as a proxy for land value.

ITP/A0121 – November 2013 32

Solar Farm Feasibility Study

7. REFERENCES

[1] Geoscience Australia and ABARE, “Australian Energy Resource Assessment,” Canberra,

2010.

[2] Bureau of Resources and Energy Economics, “Australian Energy Technology Assessment,”

Canberra, 2012.

[3] J. Rutovitz and S. Harris, “Calculating global energy sector jobs: 2012 methodology,”

Prepared for Greenpeace International by the Institute for Sustainable Futures, University of

New South Wales, Sydney, 2012.

[4] G. Parkinson, “ACT Solar Auction won by Elementus, Zhenfa Solar,” 19 August 2013.

[Online]. Available: http://reneweconomy.com.au/2013/act-solar-auction-won-by-elementus-

zhenfa-solar-67633. [Accessed 27 August 2013].

[5] ETSA Utilities, “Electricity System Development Plan,” Adelaide, 2012.

[6] Renewable Energy and Energy Efficiency Partnership (REEEP), Alliance to Save Energy,

American Council On Renewable Energy, “Compendium of Best Practices, SHaring Local

and State Successes in Energy Efficiency and Renewable Energy from the United States,”

2010.

[7] International Energy Agency, “Deploying Renewables 2011: Best and Future Policy Practice,”

Paris, 2011.

[8] International Energy Agency, “Deploying Renewables: Principles for Effective Policies,” Paris,

2008.

[9] North Carolina State University, under NREL Subcontract No. XEU-0-99515-01, “Database of

State Incentives for Renewables and Efficiency,” [Online]. Available: http://www.dsireusa.org.

[Accessed 19 August 2013].

[10] State Electoral Office, “An introduction to Local Government,” 2006.

[11] G. Parkinson, “FRV to build 20MW solar PV plant after winningACT auction,” 5 September

2012. [Online]. Available: http://reneweconomy.com.au/2012/frv-to-build-20mw-solar-pv-

plant-after-winning-act-auction-50595. [Accessed 27 August 2013].

ITP/A0121 – November 2013 33

Solar Farm Feasibility Study

APPENDIX A. PREFERRED AREAS FOR A 1 MW SOLAR FARM

ITP/A0121 – November 2013 34

Solar Farm Feasibility Study

APPENDIX B. PREFERRED AREAS FOR A 10 MW SOLAR FARM

ITP/A0121 – November 2013 35

Solar Farm Feasibility Study

APPENDIX C. 10 MW PREFERRED AREA FOR AN IMPROVED GRID

ITP/A0121 – November 2013 2

Title