Embed Size (px)

DESCRIPTION

State of the Freeport Address Subic Bay Freport

Citation preview

2009 STATE OF THE FREEPORT ADDRESS(Part Two)

“A VISION OF TOMORROW”

by Armand C. ArrezaSBMA Administrator and CEO

Subic Bay Exhibition & Convention Center

23 February 2010

The President’s Vision

2

“The Subic-Clark corridor will be

the most competitive international

service and logistics center in the

Southeast Asian Region”

From the inaugural speech of

Her Excellency President Gloria Macapagal-Arroyo

When Chairman Salonga and I were appointed in Sept. 2005, the President

presented us with a challenge…

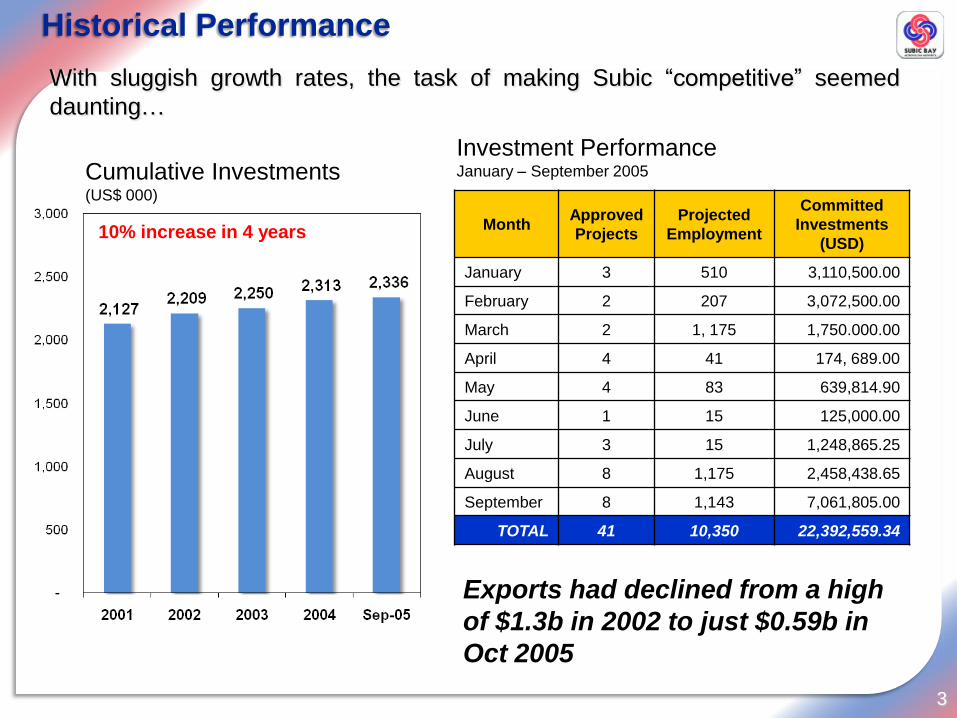

Historical Performance

3

10% increase in 4 years

Cumulative Investments (US$ 000)

MonthApproved

Projects

Projected

Employment

Committed

Investments

(USD)

January 3 510 3,110,500.00

February 2 207 3,072,500.00

March 2 1, 175 1,750.000.00

April 4 41 174, 689.00

May 4 83 639,814.90

June 1 15 125,000.00

July 3 15 1,248,865.25

August 8 1,175 2,458,438.65

September 8 1,143 7,061,805.00

TOTAL 41 10,350 22,392,559.34

Investment Performance January – September 2005

With sluggish growth rates, the task of making Subic ―competitive‖ seemed

daunting…

Exports had declined from a high

of $1.3b in 2002 to just $0.59b in

Oct 2005

4

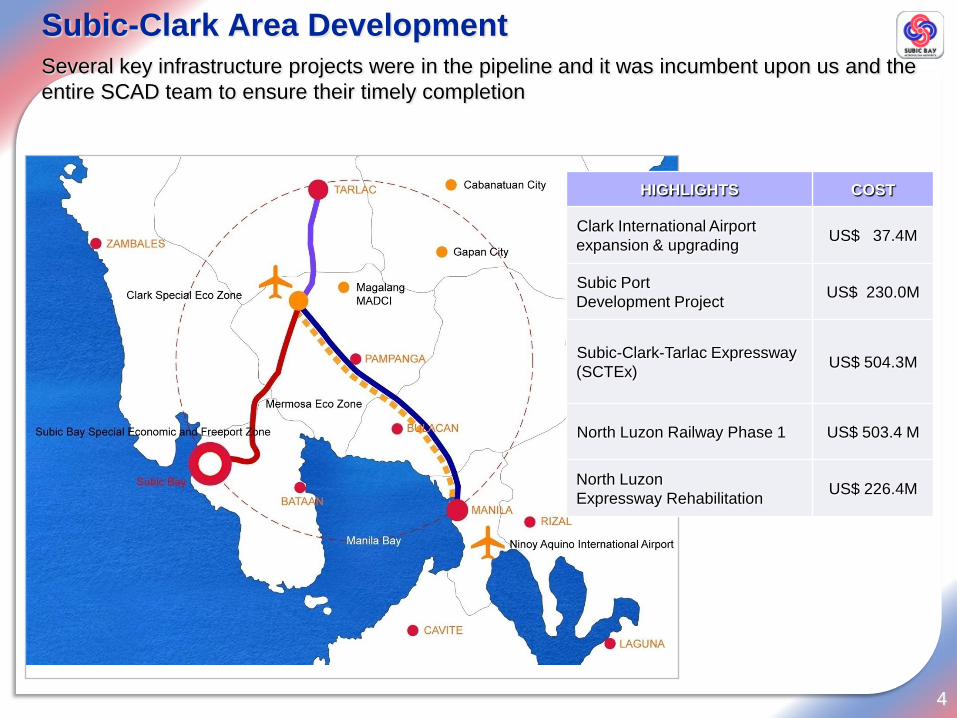

HIGHLIGHTS COST

Clark International Airport

expansion & upgradingUS$ 37.4M

Subic Port

Development ProjectUS$ 230.0M

Subic-Clark-Tarlac Expressway

(SCTEx)US$ 504.3M

North Luzon Railway Phase 1 US$ 503.4 M

North Luzon

Expressway RehabilitationUS$ 226.4M

Subic-Clark Area Development

Several key infrastructure projects were in the pipeline and it was incumbent upon us and the

entire SCAD team to ensure their timely completion

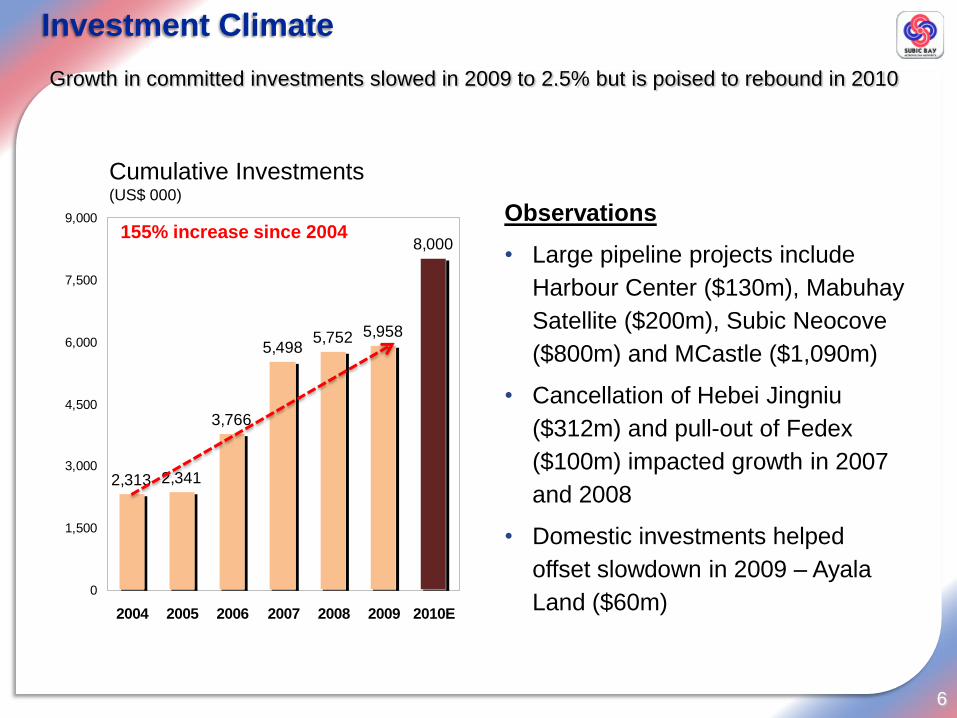

Investment Climate

5

Number of Investors

Nonetheless, by focusing on creating a more investor-friendly environment, the number of

investors continued to climb from 2005, growing at more than 20% per annum from 2006

to 2008

116% increase since 2004Observations

• Number of investors have almost

doubled since 2005

• Growth rate, however slowed to 7%

in 2009 from a high of 23% in 2008

due to the impact of Global Financial

Crisis

• Projects from domestic firms offset

slow-down in investments from

foreign firms

Investment Climate

6

2,313 2,341

3,766

5,4985,752

8,000

5,958

0

1,500

3,000

4,500

6,000

7,500

9,000

2004 2005 2006 2007 2008 2009 2010E

Cumulative Investments (US$ 000)

Growth in committed investments slowed in 2009 to 2.5% but is poised to rebound in 2010

Observations

• Large pipeline projects include

Harbour Center ($130m), Mabuhay

Satellite ($200m), Subic Neocove

($800m) and MCastle ($1,090m)

• Cancellation of Hebei Jingniu

($312m) and pull-out of Fedex

($100m) impacted growth in 2007

and 2008

• Domestic investments helped

offset slowdown in 2009 – Ayala

Land ($60m)

155% increase since 2004

Investment Profile

7

Rank Industry Sector 2005 2006 2007 2008 2009 Total

1 Maritime & Port-related 6.21 1,003.74 4.35 4.35 26.95 1,044

2 Manufacturing 8.23 388.84 106.03 12.63 9.93 526

3 Tourism/Leisure 2.32 70.37 158.68 191.29 56.70 428

4 Utilities 0 0 431.64 1.52 0 433

2005-2009 Top 4 Industry Sectors

in terms of Committed Investments (US$M)

New projects reflect a shift from manufacturing investments to tourism related activities

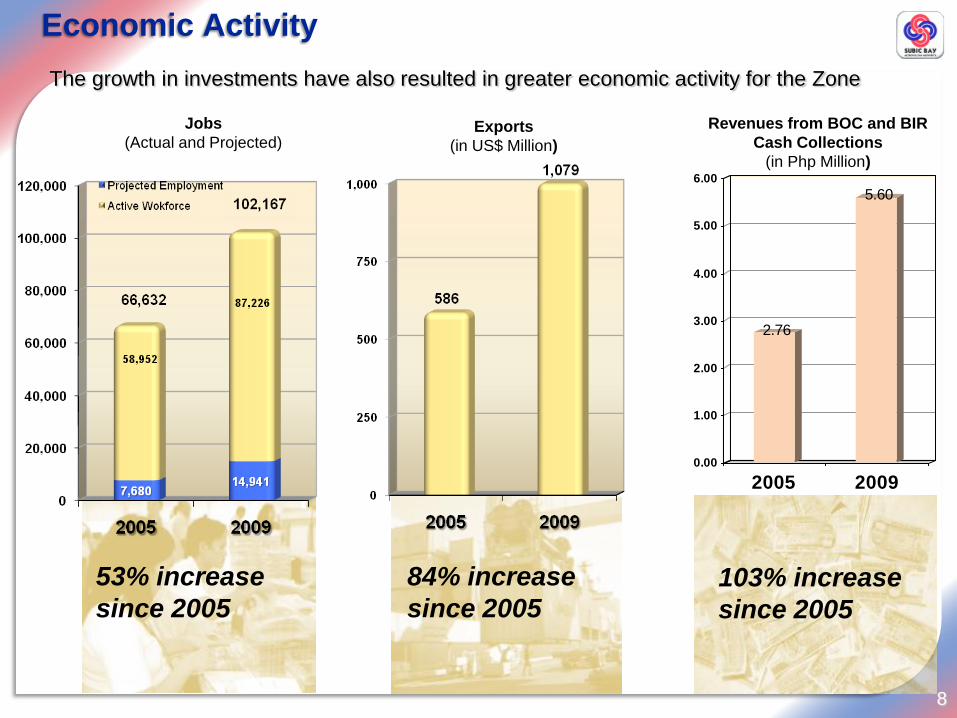

Economic Activity

8

2.76

5.60

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2005 2009

Revenues from BOC and BIR

Cash Collections

(in Php Million)

Exports

(in US$ Million)

Jobs

(Actual and Projected)

53% increase

since 2005

84% increase

since 2005103% increase

since 2005

The growth in investments have also resulted in greater economic activity for the Zone

Core Purpose – Broken Down to Stakeholders

9

Country

Local

CommunitiesInvestors

Employees

To unite around a sense of achievement

To create jobs and

economic opportunities

responsibly and

sustainably

To create a safe,

stable, efficient and

transparent business

environment where

companies can grow

To harness their talents to create a better

future for them and the country

SBMA’s Core Ideology

10

Core Ideology

C

O

R

E

V

A

L

U

E

S

Malasakit

• Bayanihan spirit, going the extra mile

• Common good over self-interest, care,

• Respect for the environment

• Social responsibility & accountability

• Enhancing, perpetuating gains of development

Excellence • Integrity

• Professionalism

• Discipline, world-class

Passion

• Fire that drives us to have ―Malasakit‖, Excellence &

Professionalism

• Innovative

• Commitment

C

O

R

E

P

U

R

P

O

S

E

To generate economic opportunities & livelihood as a

competitive maritime, logistics and eco-tourism hub in

East Asia.

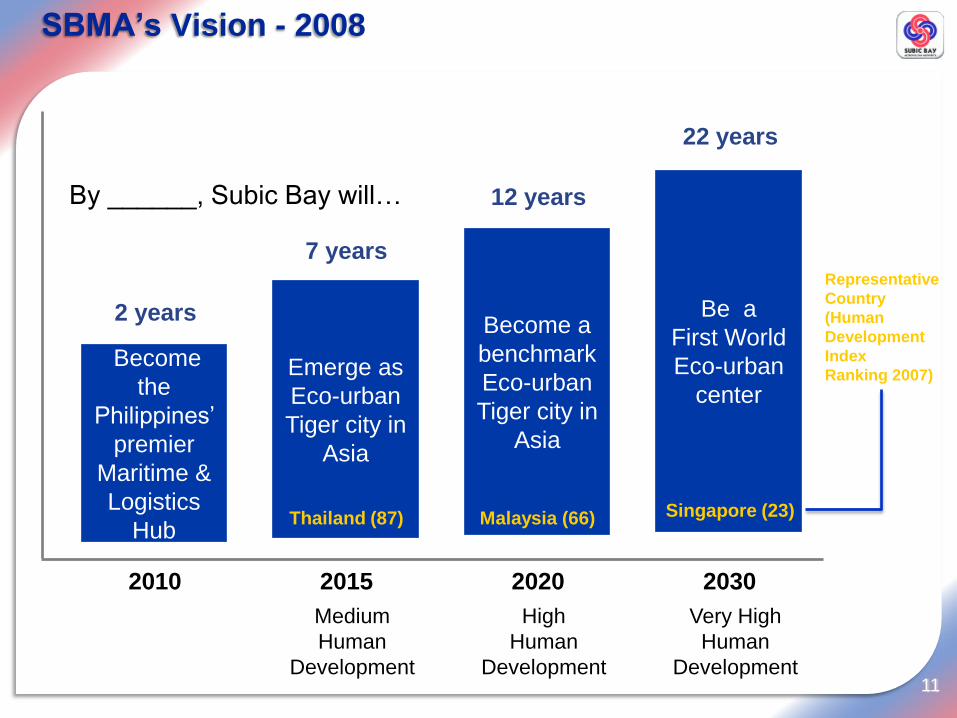

SBMA’s Vision - 2008

11

Become

the

Philippines’

premier

Maritime &

Logistics

Hub

2010

2 years

By ______, Subic Bay will…

Emerge as

Eco-urban

Tiger city in

Asia

2015

7 years

Thailand (87)

Become a

benchmark

Eco-urban

Tiger city in

Asia

2020

12 years

Malaysia (66)

Be a

First World

Eco-urban

center

2030

22 years

Singapore (23)

Medium

Human

Development

High

Human

Development

Very High

Human

Development

Representative

Country

(Human

Development

Index

Ranking 2007)

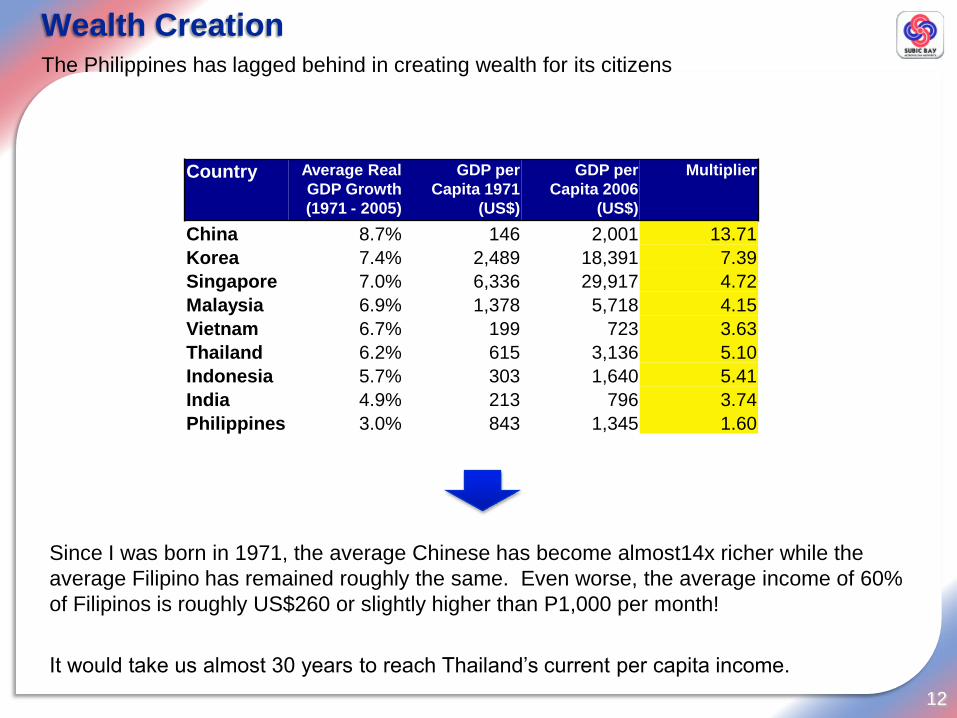

Wealth Creation

12

The Philippines has lagged behind in creating wealth for its citizens

Since I was born in 1971, the average Chinese has become almost14x richer while the

average Filipino has remained roughly the same. Even worse, the average income of 60%

of Filipinos is roughly US$260 or slightly higher than P1,000 per month!

It would take us almost 30 years to reach Thailand’s current per capita income.

Country Average Real

GDP Growth

(1971 - 2005)

GDP per

Capita 1971

(US$)

GDP per

Capita 2006

(US$)

Multiplier

China 8.7% 146 2,001 13.71

Korea 7.4% 2,489 18,391 7.39

Singapore 7.0% 6,336 29,917 4.72

Malaysia 6.9% 1,378 5,718 4.15

Vietnam 6.7% 199 723 3.63

Thailand 6.2% 615 3,136 5.10

Indonesia 5.7% 303 1,640 5.41

India 4.9% 213 796 3.74

Philippines 3.0% 843 1,345 1.60

Philippine Real GDP Growth Rate

13

Asian

Financial

Crisis

Power

Crisis

Anti-Marcos

Rallies

The Philippines has failed to sustain high levels of growth for prolonged periods

The Economic Pie simply is not getting bigger

2006 Philippine Family Income and Poverty Statistics

14

SOURCE: National Statistical Coordination Board (www.nscb.com.ph)

2000 2003 2006 2000 2003 2006

Nearly 27% of Filipino Families are officially ―poor‖ – equivalent to 33% of Filipinos or

30 million individuals

Subsistence = Food Threshold

= P4,177/month for family of 5

Poverty Line = Food Threshold + basic needs

= P6,274/month for family of 5

= P41/day/person!

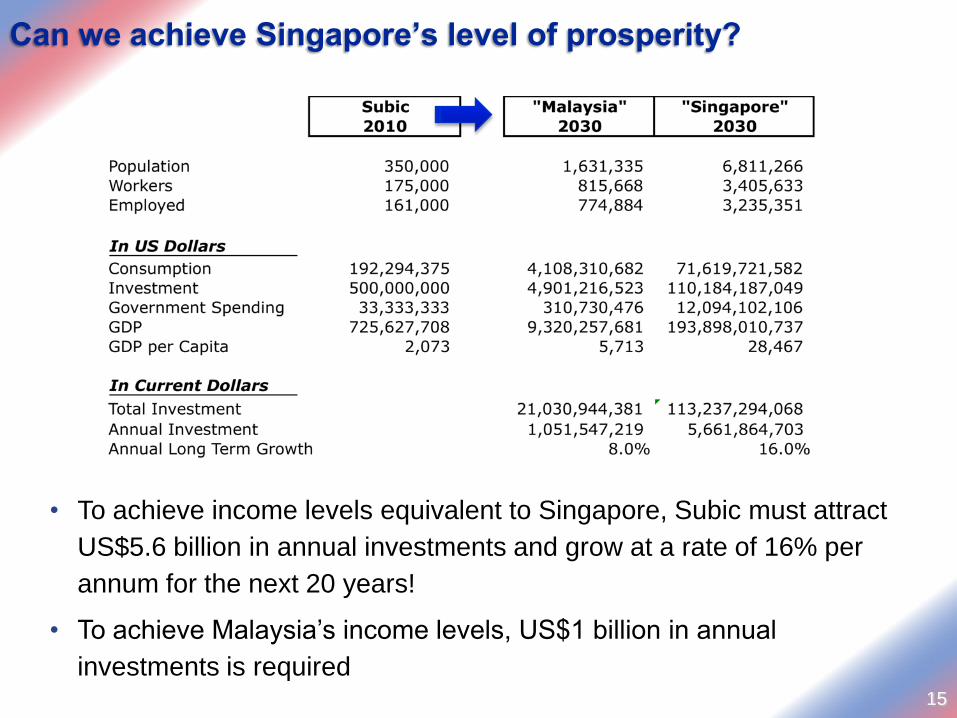

Can we achieve Singapore’s level of prosperity?

15

• To achieve income levels equivalent to Singapore, Subic must attract

US$5.6 billion in annual investments and grow at a rate of 16% per

annum for the next 20 years!

• To achieve Malaysia’s income levels, US$1 billion in annual

investments is required

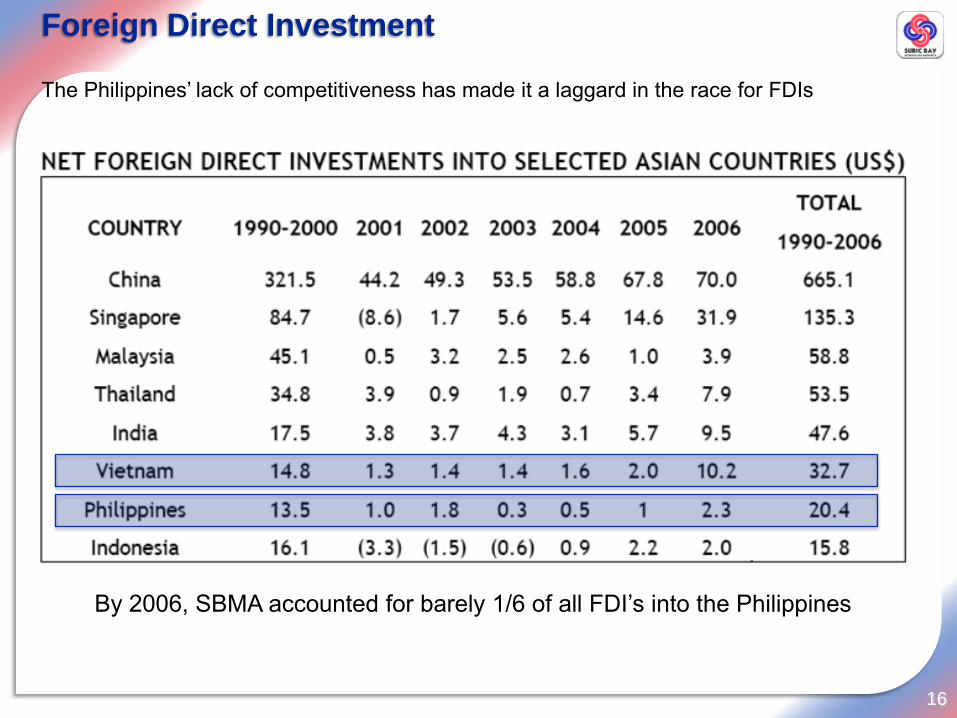

Foreign Direct Investment

16

The Philippines’ lack of competitiveness has made it a laggard in the race for FDIs

By 2006, SBMA accounted for barely 1/6 of all FDI’s into the Philippines

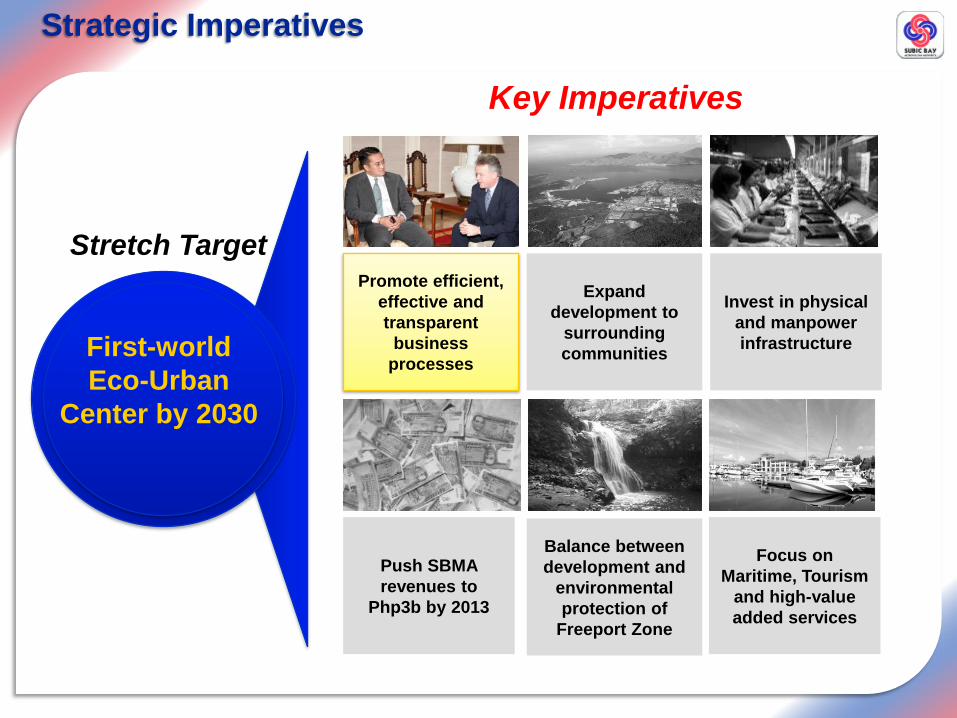

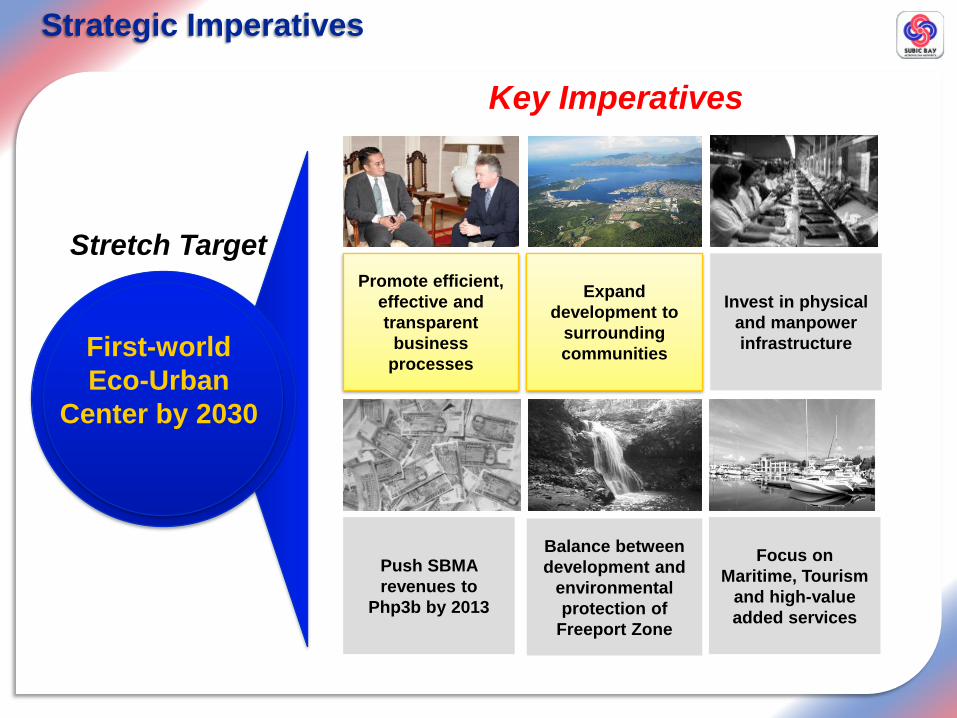

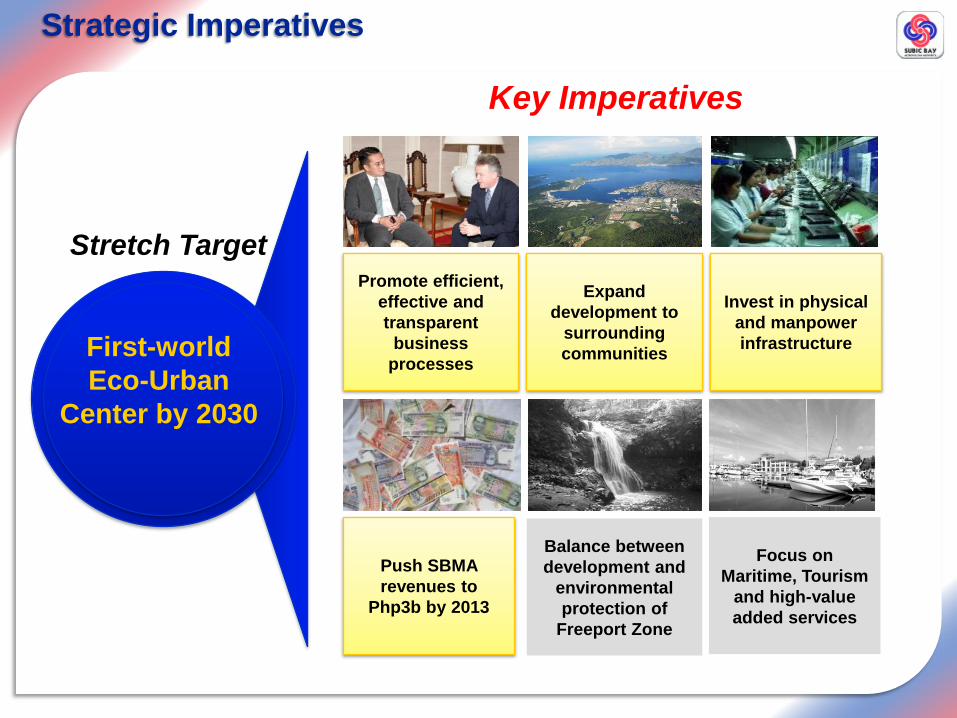

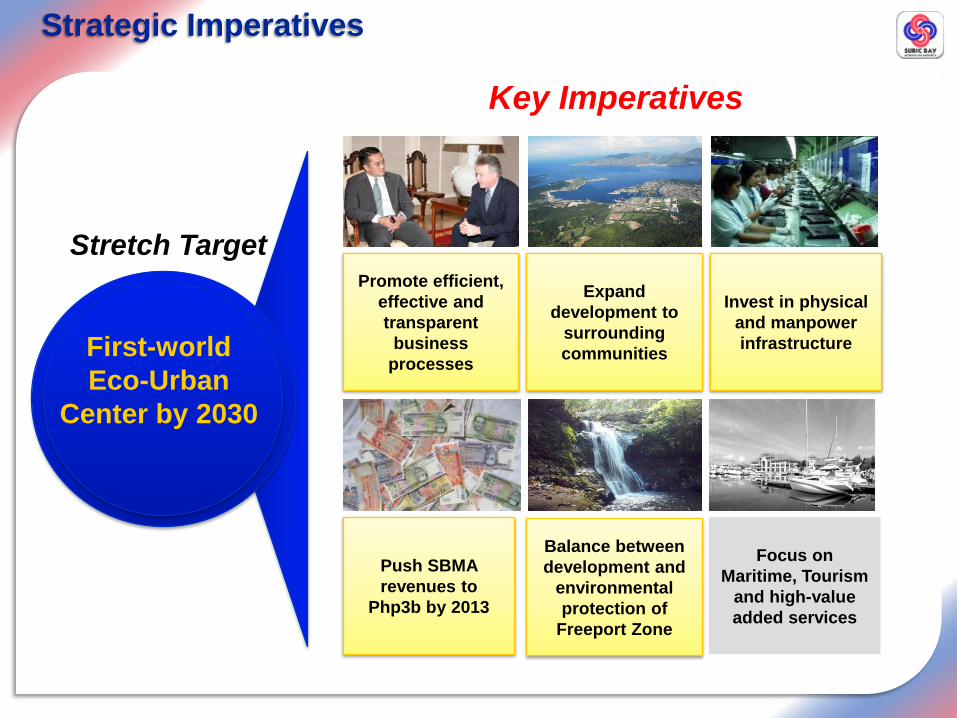

Strategic Imperatives

First-world

Eco-Urban

Center by 2030

Promote efficient,

effective and

transparent

business

processes

Expand

development to

surrounding

communities

Invest in physical

and manpower

infrastructure

Key Imperatives

Stretch Target

Push SBMA

revenues to

Php3b by 2013

Balance between

development and

environmental

protection of

Freeport Zone

Focus on

Maritime, Tourism

and high-value

added services

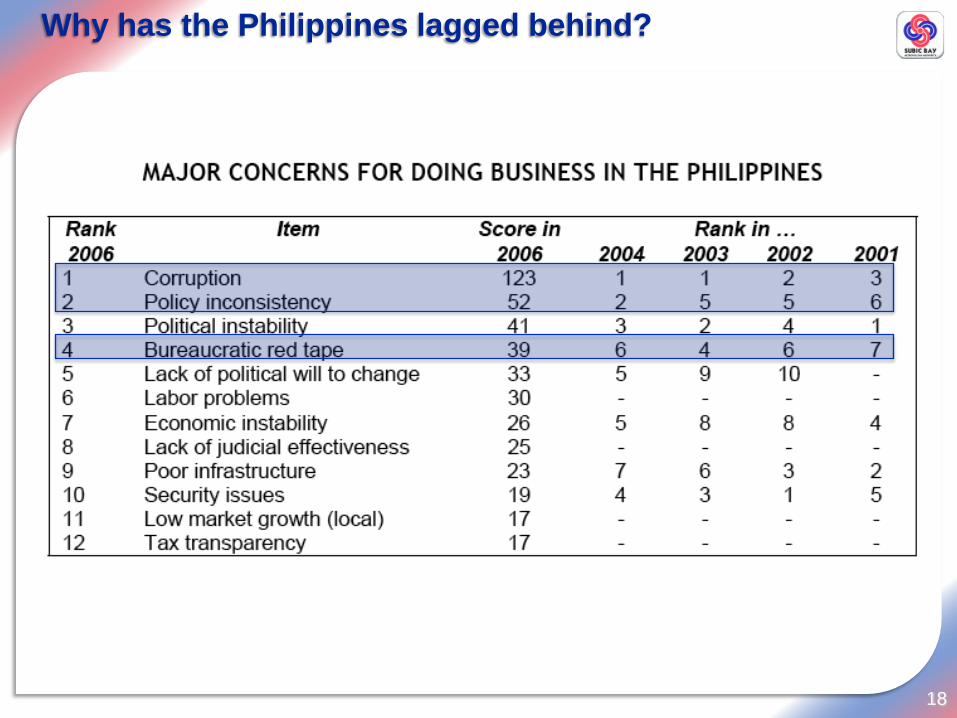

Why has the Philippines lagged behind?

18

Corruption

19

Stopping corruption is one thing, changing the perception is another…

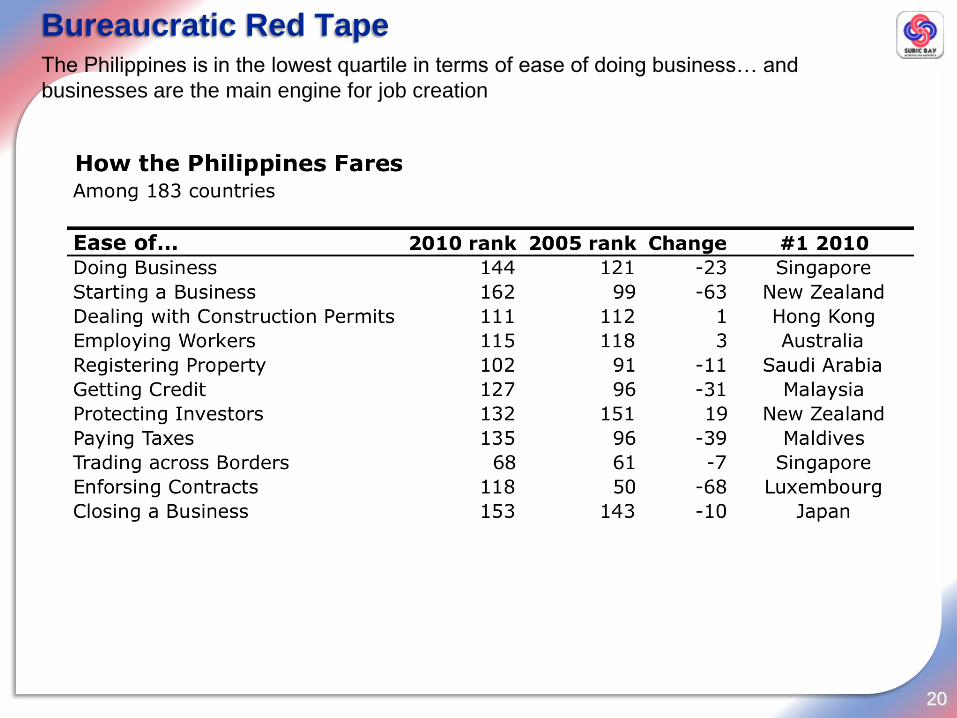

Bureaucratic Red Tape

20

The Philippines is in the lowest quartile in terms of ease of doing business… and

businesses are the main engine for job creation

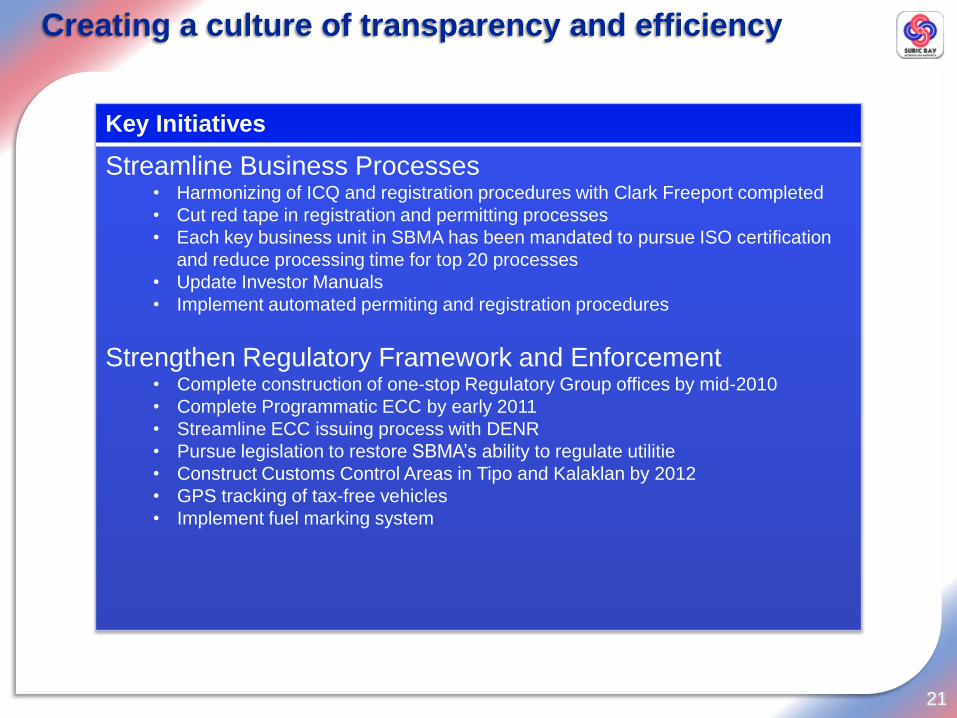

Creating a culture of transparency and efficiency

21

Key Initiatives

Streamline Business Processes• Harmonizing of ICQ and registration procedures with Clark Freeport completed

• Cut red tape in registration and permitting processes

• Each key business unit in SBMA has been mandated to pursue ISO certification

and reduce processing time for top 20 processes

• Update Investor Manuals

• Implement automated permiting and registration procedures

Strengthen Regulatory Framework and Enforcement• Complete construction of one-stop Regulatory Group offices by mid-2010

• Complete Programmatic ECC by early 2011

• Streamline ECC issuing process with DENR

• Pursue legislation to restore SBMA’s ability to regulate utilitie

• Construct Customs Control Areas in Tipo and Kalaklan by 2012

• GPS tracking of tax-free vehicles

• Implement fuel marking system

Strategic Imperatives

First-world

Eco-Urban

Center by 2030

Promote efficient,

effective and

transparent

business

processes

Expand

development to

surrounding

communities

Invest in physical

and manpower

infrastructure

Key Imperatives

Stretch Target

Push SBMA

revenues to

Php3b by 2013

Balance between

development and

environmental

protection of

Freeport Zone

Focus on

Maritime, Tourism

and high-value

added services

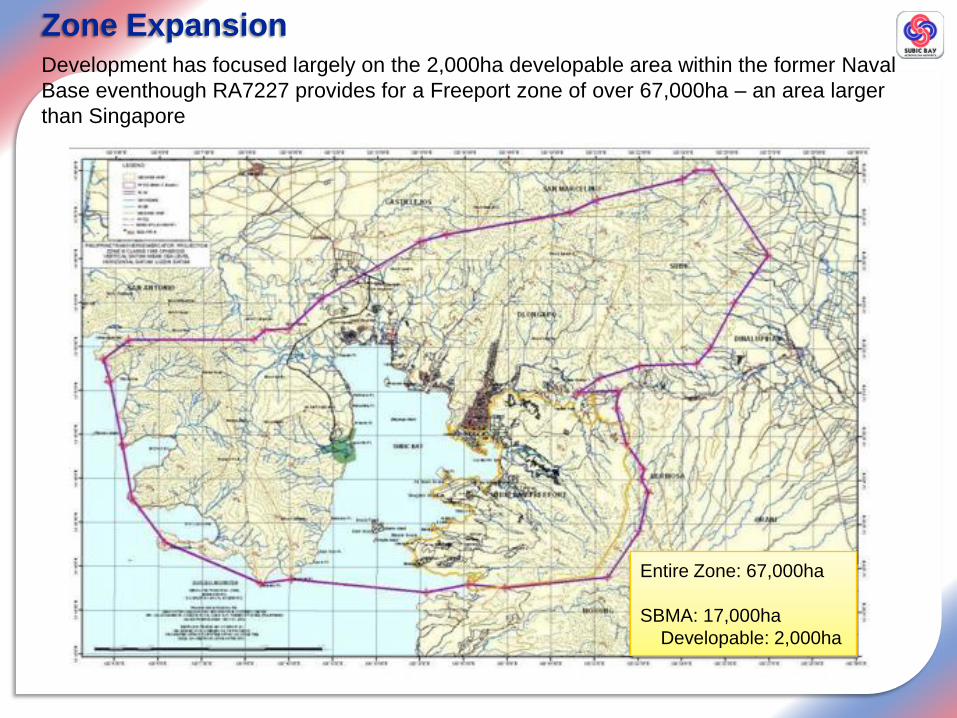

Zone ExpansionDevelopment has focused largely on the 2,000ha developable area within the former Naval

Base eventhough RA7227 provides for a Freeport zone of over 67,000ha – an area larger

than Singapore

Entire Zone: 67,000ha

SBMA: 17,000ha

Developable: 2,000ha

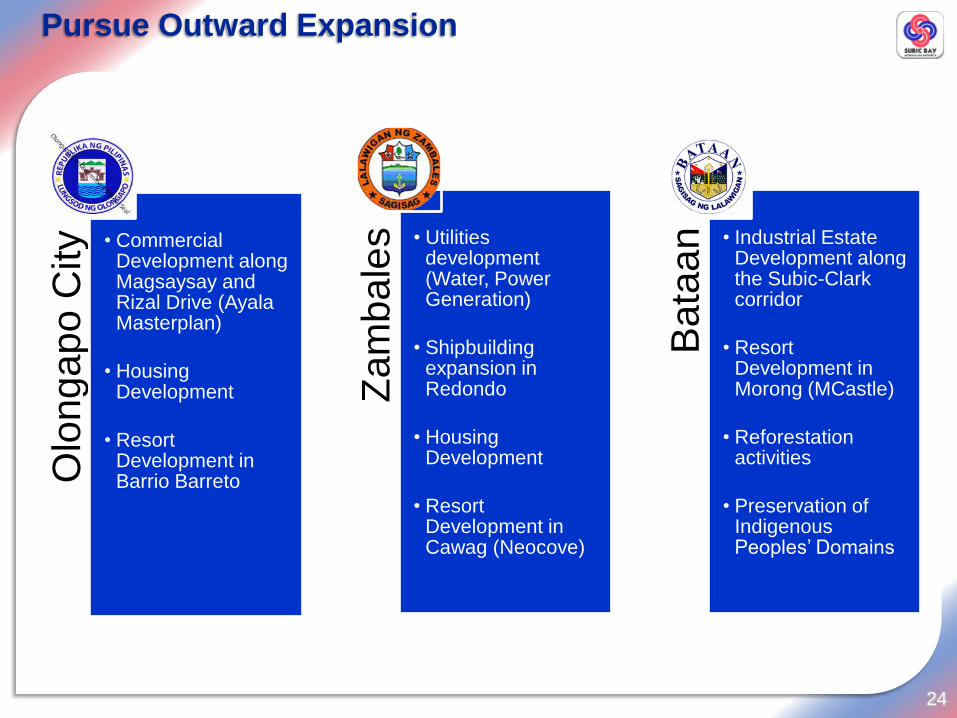

Pursue Outward Expansion

24

Olo

ng

apo

City • Commercial

Development along Magsaysay and Rizal Drive (Ayala Masterplan)

• Housing Development

• Resort Development in Barrio Barreto

Za

mb

ale

s • Utilities development (Water, Power Generation)

• Shipbuilding expansion in Redondo

• Housing Development

• Resort Development in Cawag (Neocove)

Bata

an • Industrial Estate

Development along the Subic-Clark corridor

• Resort Development in Morong (MCastle)

• Reforestation activities

• Preservation of Indigenous Peoples’ Domains

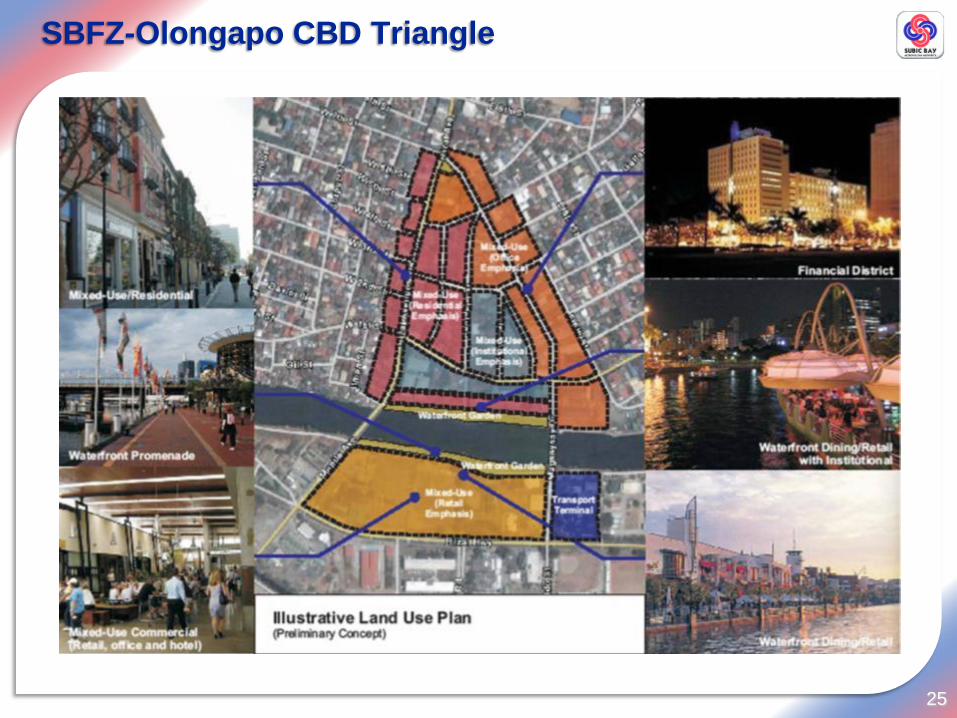

SBFZ-Olongapo CBD Triangle

25

Strategic Imperatives

First-world

Eco-Urban

Center by 2030

Promote efficient,

effective and

transparent

business

processes

Expand

development to

surrounding

communities

Invest in physical

and manpower

infrastructure

Key Imperatives

Stretch Target

Push SBMA

revenues to

Php3b by 2013

Balance between

development and

environmental

protection of

Freeport Zone

Focus on

Maritime, Tourism

and high-value

added services

Infrastructure

27

The Philippines must build more infrastructure to attract businesses

Manpower Development

28

Of the 2 million Filipino Children born in 2010

Percent Number

100% 2,000,000 Primary School Age

94% 1,888,000 Start Grade 1

67% 1,349,920 Reach Grade 6

64% 1,280,000 Start High School

19% 380,000 Drop-out

45% 900,000 Finish High School

24% 480,000 Enter College

17% 340,000 Drop-out

7% 140,000 Finish College

6% 112,000 No Education

27% 538,080 Up to Grade 6

22% 449,920 Up to High School

38% 760,000 Some College

7% 140,000 Finish College

Education is the way out of poverty… not in the Philippines!

In this day and age, it’s not labor, capital or natural resources that dictate a country’s

competitive edge—it is knowledge. Educated people get jobs or, at least, have a far better

chance at doing so. An educated workforce attracts investment. That creates jobs, and

national wealth.

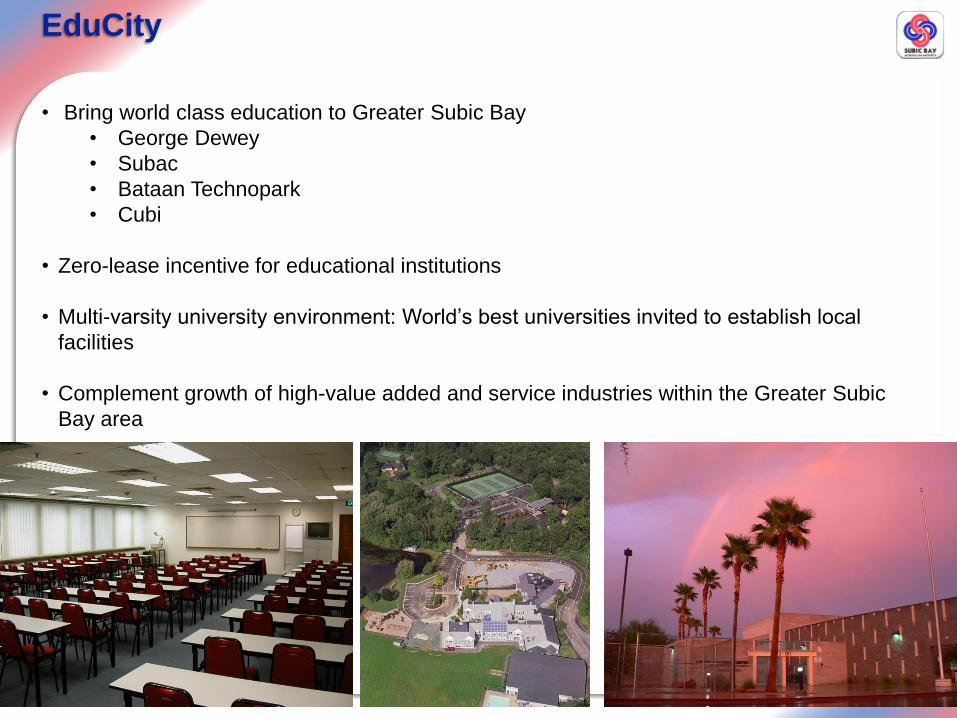

EduCity

29

• Bring world class education to Greater Subic Bay

• George Dewey

• Subac

• Bataan Technopark

• Cubi

• Zero-lease incentive for educational institutions

• Multi-varsity university environment: World’s best universities invited to establish local

facilities

• Complement growth of high-value added and service industries within the Greater Subic

Bay area

Strategic Imperatives

First-world

Eco-Urban

Center by 2030

Promote efficient,

effective and

transparent

business

processes

Expand

development to

surrounding

communities

Invest in physical

and manpower

infrastructure

Key Imperatives

Stretch Target

Push SBMA

revenues to

Php3b by 2013

Balance between

development and

environmental

protection of

Freeport Zone

Focus on

Maritime, Tourism

and high-value

added services

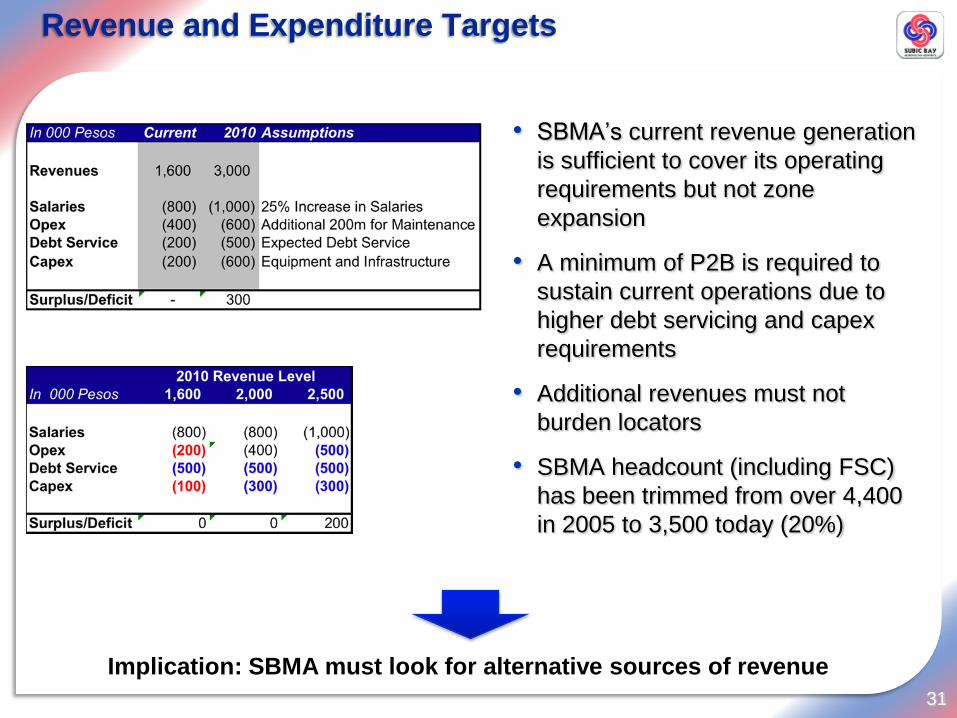

Revenue and Expenditure Targets

31

• SBMA’s current revenue generation

is sufficient to cover its operating

requirements but not zone

expansion

• A minimum of P2B is required to

sustain current operations due to

higher debt servicing and capex

requirements

• Additional revenues must not

burden locators

• SBMA headcount (including FSC)

has been trimmed from over 4,400

in 2005 to 3,500 today (20%)

Implication: SBMA must look for alternative sources of revenue

Strategic Imperatives

First-world

Eco-Urban

Center by 2030

Promote efficient,

effective and

transparent

business

processes

Expand

development to

surrounding

communities

Invest in physical

and manpower

infrastructure

Key Imperatives

Stretch Target

Push SBMA

revenues to

Php3b by 2013

Balance between

development and

environmental

protection of

Freeport Zone

Focus on

Maritime, Tourism

and high-value

added services

Key Initiatives

33

1st Subic Bay Water Summit

• Forging of common agenda for the

sustainable management of local water

resources among all stakeholders

Reforestation Program

• Total Area Planted: 156.49 ha

• Total No. of Trees Planted: 287,233

Clean Air Program

• Shift to LPG-powered public utilities and

SBMA service vehicles in the next 5

years

Environment

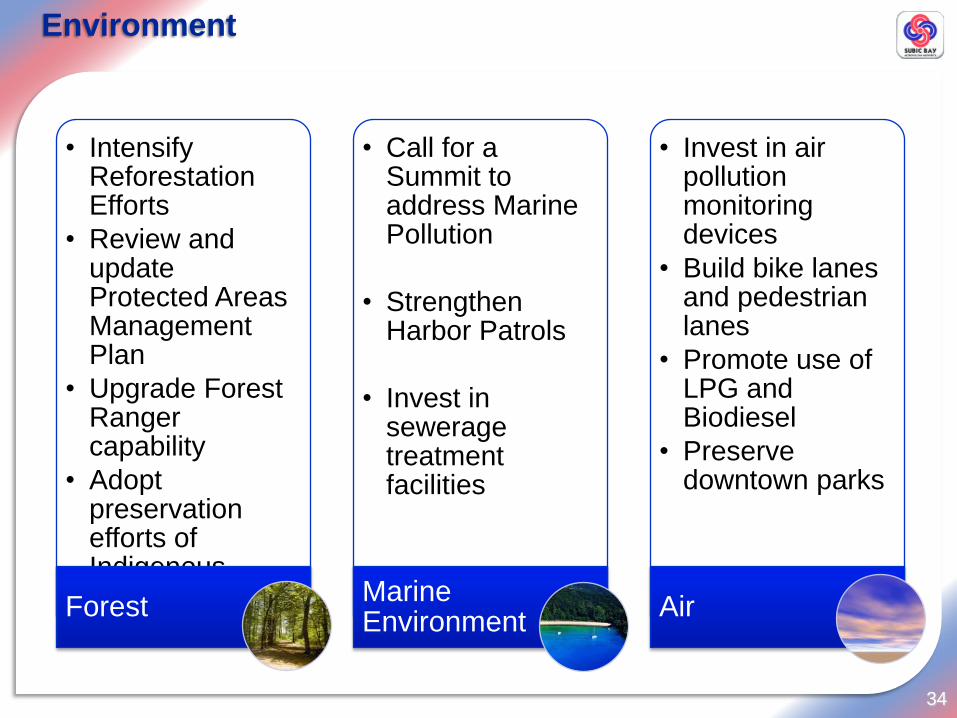

34

• Intensify Reforestation Efforts

• Review and update Protected Areas Management Plan

• Upgrade Forest Ranger capability

• Adopt preservation efforts of Indigenous TribesForest

• Call for a Summit to address Marine Pollution

• Strengthen Harbor Patrols

• Invest in sewerage treatment facilities

Marine Environment

• Invest in air pollution monitoring devices

• Build bike lanes and pedestrian lanes

• Promote use of LPG and Biodiesel

• Preserve downtown parks

Air

Renewable Energy Sources

35

• According to WWF, the Philippines has more than 1,000

wind sites with a potential capacity of at least 7,400

megawatts – enough to power 19 million homes.

• Possible site in SBFZ: Redondo Ridge

• It is estimated that the Philippines ―could save US$2.9

billion in fossil-fuel imports over the next 10 years, if the

country’s cast renewal energy resources are tapped‖.

Strategic Imperatives

First-world

Eco-Urban

Center by 2030

Promote efficient,

effective and

transparent

business

processes

Expand

development to

surrounding

communities

Invest in physical

and manpower

infrastructure

Key Imperatives

Stretch Target

Push SBMA

revenues to

Php3b by 2013

Balance between

development and

environmental

protection of

Freeport Zone

Focus on

Maritime, Tourism

and high-value

added services

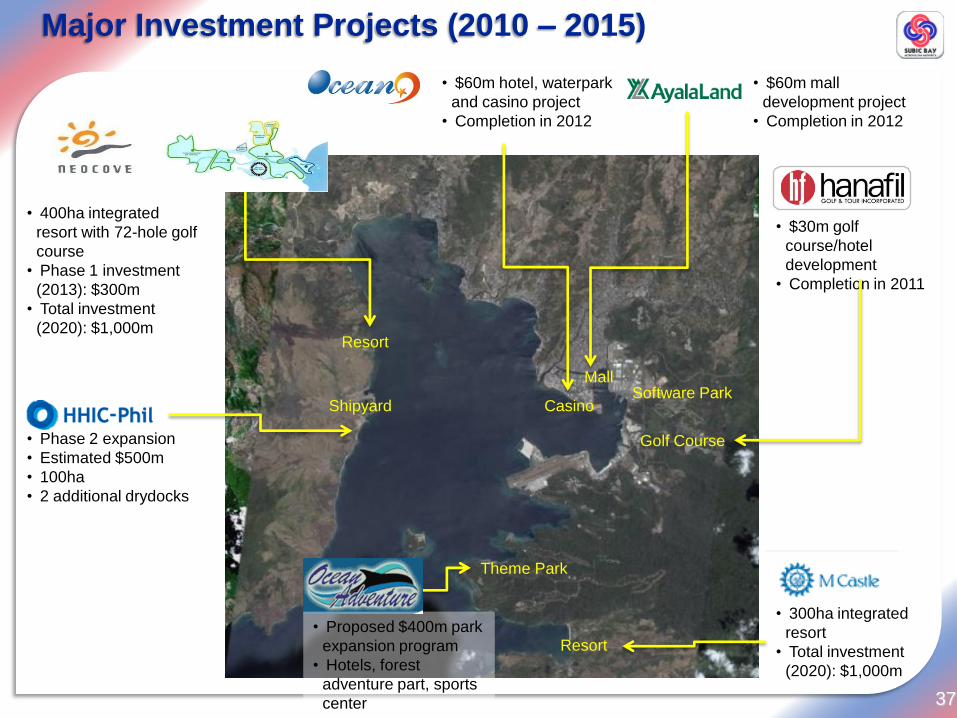

Major Investment Projects (2010 – 2015)

37

• Phase 2 expansion

• Estimated $500m

• 100ha

• 2 additional drydocks

• 400ha integrated

resort with 72-hole golf

course

• Phase 1 investment

(2013): $300m

• Total investment

(2020): $1,000m

• $60m hotel, waterpark

and casino project

• Completion in 2012

• $60m mall

development project

• Completion in 2012

Shipyard

Resort

Casino

MallSoftware Park

• $30m golf

course/hotel

development

• Completion in 2011

Golf Course

• Proposed $400m park

expansion program

• Hotels, forest

adventure part, sports

center

Theme Park

• 300ha integrated

resort

• Total investment

(2020): $1,000m

Resort

Before Construction (March 2006)

Subic Shipyard

November 2008

During Construction (January 2007)

Economic Impact

• Employment: 16,874 – Shipyard

• Annual Payroll: Php 3.25 billion

• Annual Exports: US$1 billion (2009 est)

• Investment (Phase 1): US$1.6 billion;

additional investments planned in

Cagayan de Oro and Subic Bay

• Focus should be in encouraging

integration with local companies

International Destination Resorts

39

The development of complete destination resorts, anchored by international brand hotel

chains can serve as strong tourist magnets

40

Downtown Development

Gateway

District

Downtown

Olongapo

Central Business

District

Proposed

Technology

Park

Proposed Mall

Hotel /Entertainment

Row

Cruise Ship

Terminal

Golf Course

Convention

Facilities

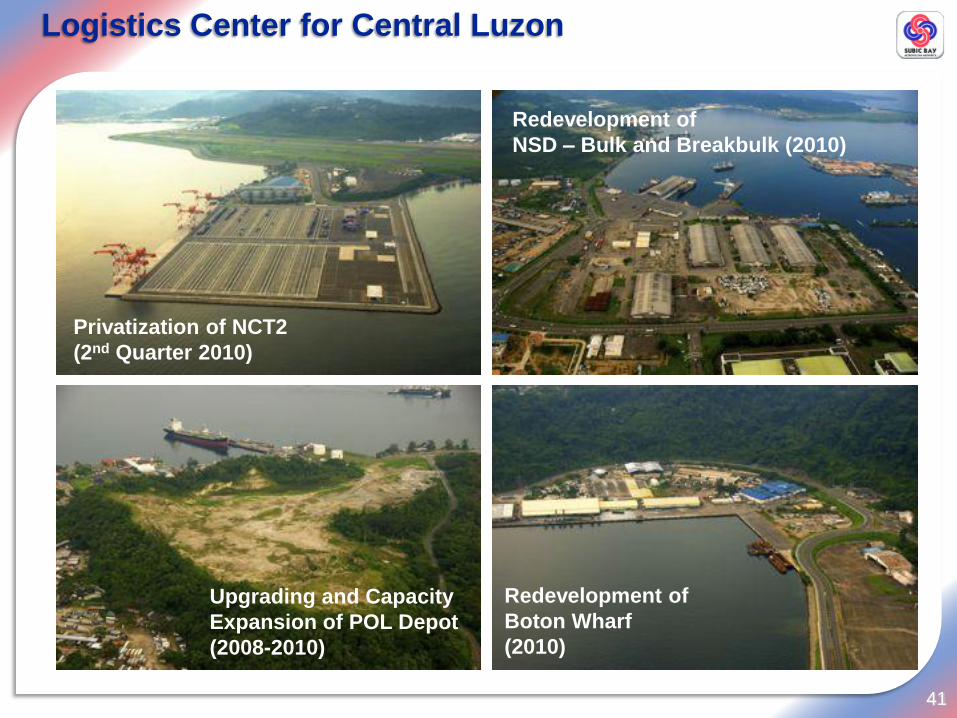

Logistics Center for Central Luzon

41

Privatization of NCT2

(2nd Quarter 2010)

Upgrading and Capacity

Expansion of POL Depot

(2008-2010)

Redevelopment of

NSD – Bulk and Breakbulk (2010)

Redevelopment of

Boton Wharf

(2010)

End of Presentation

![[loop] - inelis.sk popis.pdf · NF P PF Sofa Sofa mit Seitenteilverstel-Sofa groß Sofa groß mit Seitenteilver-lung stellung ... doporučujeme z naší řady 10006 plexisklo L010](https://img.dokumen.tips/doc/110x75/5b9dd92909d3f2de128d08e0/loop-popispdf-nf-p-pf-sofa-sofa-mit-seitenteilverstel-sofa-gross-sofa-gross.jpg)