Embed Size (px)

Citation preview

34

Socio Economic Impact of Micro Finance Among

Rural Women- A Review Usha J.C1, Pradeep K V2

1, 2 Faculty of Commerce, Department of Management Studies, M. S. Ramaiah University of Applied Sciences,

Bengaluru 560 054 1Contact Author E- Mail: [email protected]

Abstract This review study endeavours to assess the socio economic impact of microfinance in empowering the rural women.

Microfinance transforms and uplifts the livelihood and self-esteem of the rural women. The noticeable changes has been

occurred due to microfinance initiated programme amongst the rural women members. Microfinance enhances the

confidence level and decision making ability of rural women. Microfinance reduced the dependency of rural women on

informal money lenders. The remarkable improvement in education and employment among the rural families are endorsed

as an achievement of microfinance. Despite the fact that microfinance helped in improving the standard of living of rural

women. Micro finance helped to face the challenges like dearth of entrepreneurial skill, experience and expertise amongst

the members. This study reveals how the microfinance lend a hand towards socio economic empowerment of rural women.

Key words: Women Empowerment, Microfinance, Socio economic impact, Micro credit _____________________________________________________________________________

1.0 INTRODUCTION

Recent developments claims that micro finance is new

developmental paradigm for plummeting poverty

through strengthening the low income group, especially

women in rural areas. The other anti-poverty programs

shows that, success lies in the participation of people at

the grass root level. Micro finance is the facility which

requires the people participation in the credit delivery,

recovery and linkage of microfinance institutions with

the intermediate called Self-help groups (SHG’s).

Micro finance connotes providing savings and credit

facilities for low income group of people especially

women. This facility is made available either to set up

business, expand the existing business, self-employment

activities or increase the house hold activities. The main

motto behind this programme is to empower in women in

urban as well as rural areas. Micro finance and self-help

groups not only worked as perfect remedy for poverty

but also empowered the women by building the

awareness. It gives them confidence, improves the

standard of living and helps in making decision making.

Micro finance does not restrict the empowerment only to

finance but also extends towards socio cultural and

political spheres within which borrower’s lives are

rooted.

1.1 Microfinance, Financial Inclusion and

Women Empowerment

Micro finance institutions play key role in smoothing the

financial inclusion as they stood for reach out rural poor.

Many of them function in small geographical area, to

have a greater understanding of issues and problems.

Financial inclusion means availing of financial facilities

at affordable rates for people who have less accessibility,

usually low and middle income segment of the society.

The lion’s share of the benefits of micro finance goes to

women. Empowerment is reflected in the capability set of human

being. The empowerment maybe individual or collective

empowerment. Self-help groups helped the rural women

not only in strengthening their financial empowerment

but also in other areas like social networking’s awareness

to the recent developments, inspirations to be financially

independent, self-employment etc.

SHG’s helped in boosting the self-confidence and active

decision making among the members. Micro loans

extended to the rural population without any collaterals.

All the members of SHG’s are jointly guarantee the

borrowings of the member.

Economically it empowers the women by, cumulating

savings, alleviation of poverty in the family, supports the

children’s education and helps in providing stability

during financial crisis of the family.

Social empowerment means it helps the rural women to

communicate with the society. Social interactions helps

in boosting the confidence and boldness to fight back

against the injustice.

Political empowerment means it gives the assertiveness

for the rural women for contesting in Panchayat election,

attending Grama Sabha meetings etc. It’s the financial

stability which gives the confidence to the rural women

to withstand any kind of crisis. There is no doubt in

saying micro finance empowers the rural women

1.2 Successful Models of Microfinance There are very successful microfinance models like

intermediate models which works with banking

principles which emphasizes on the borrowings as well

as savings to the clients either by directly or indirectly

self-help groups. Apart from this there is wholesale

banking model comprising of NGOs, expansion MFIs

expansion which provides the capacity building support

to members. Individual banking model works either in

Joint Liability Groups or individual liability group.

1.3 Recent Developments in Microfinance

Finance minister Arun Jaitely has proposed to create

Mudra bank (Micro Units Development Refinance

Agency) in the phase of financial inclusion and micro

finance. They are proposing Mudra Bank, with a mass of

Rs 20,000 crore, and credit guarantee of Rs 3,000 crore.

35

Mudra Bank, will refinance microfinance institutions

through a Pradhan Mantri Mudra Yojana. This is yet

another attempt by the government to support micro

finance. Reserve Bank of India’s priority in financial

inclusion – providing formal channels of finance to the

under privileged - boosted the micro finance industry

especially rural women. Giving banking license to

“Bandhan” a successful micro finance institution that too

in the first stage of granting banking license reflected the

policy direction. This initiation expects the growth of

Microfinance sector by 24 percentage between FY15-19.

Micro finance industry in India faced serious challenges

during the Andhra Pradesh Crisis during 2010-2011.

Suicides of farmers who took the loan from microfinance

institutions and the unfair practices by MF institutions

forced the experts to predict the death of Indian micro

finance system. This forced the government and

regulators to take some initiatives in this direction.

Alteration of rules in microfinance industry by RBI

helped in revitalizing the microfinance industry and

making it profitable. It helped most of the rural women

to withstand the financial crisis. The industry exhibited a

loan growth of 42 percentage in 2014.

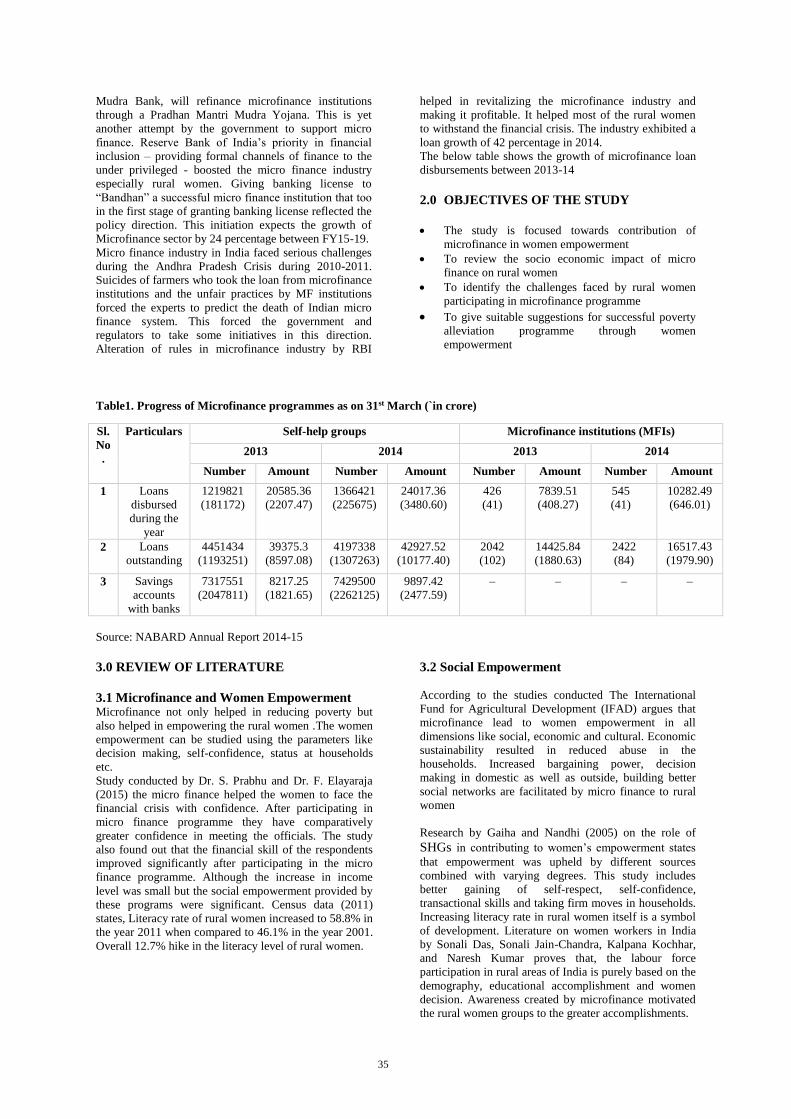

The below table shows the growth of microfinance loan

disbursements between 2013-14

2.0 OBJECTIVES OF THE STUDY

The study is focused towards contribution of

microfinance in women empowerment

To review the socio economic impact of micro

finance on rural women

To identify the challenges faced by rural women

participating in microfinance programme

To give suitable suggestions for successful poverty

alleviation programme through women

empowerment

Table1. Progress of Microfinance programmes as on 31st March (`in crore)

Source: NABARD Annual Report 2014-15

3.0 REVIEW OF LITERATURE

3.1 Microfinance and Women Empowerment Microfinance not only helped in reducing poverty but

also helped in empowering the rural women .The women

empowerment can be studied using the parameters like

decision making, self-confidence, status at households

etc.

Study conducted by Dr. S. Prabhu and Dr. F. Elayaraja

(2015) the micro finance helped the women to face the

financial crisis with confidence. After participating in

micro finance programme they have comparatively

greater confidence in meeting the officials. The study

also found out that the financial skill of the respondents

improved significantly after participating in the micro

finance programme. Although the increase in income

level was small but the social empowerment provided by

these programs were significant. Census data (2011)

states, Literacy rate of rural women increased to 58.8% in

the year 2011 when compared to 46.1% in the year 2001.

Overall 12.7% hike in the literacy level of rural women.

3.2 Social Empowerment

According to the studies conducted The International

Fund for Agricultural Development (IFAD) argues that

microfinance lead to women empowerment in all

dimensions like social, economic and cultural. Economic

sustainability resulted in reduced abuse in the

households. Increased bargaining power, decision

making in domestic as well as outside, building better

social networks are facilitated by micro finance to rural

women

Research by Gaiha and Nandhi (2005) on the role of SHGs in contributing to women’s empowerment states

that empowerment was upheld by different sources

combined with varying degrees. This study includes

better gaining of self-respect, self-confidence,

transactional skills and taking firm moves in households.

Increasing literacy rate in rural women itself is a symbol

of development. Literature on women workers in India

by Sonali Das, Sonali Jain-Chandra, Kalpana Kochhar,

and Naresh Kumar proves that, the labour force

participation in rural areas of India is purely based on the

demography, educational accomplishment and women

decision. Awareness created by microfinance motivated

the rural women groups to the greater accomplishments.

Sl.

No

.

Particulars Self-help groups Microfinance institutions (MFIs)

2013 2014 2013 2014

Number Amount Number Amount Number Amount Number Amount

1 Loans

disbursed

during the

year

1219821

(181172)

20585.36

(2207.47)

1366421

(225675)

24017.36

(3480.60)

426

(41)

7839.51

(408.27)

545

(41)

10282.49

(646.01)

2 Loans

outstanding

4451434

(1193251)

39375.3

(8597.08)

4197338

(1307263)

42927.52

(10177.40)

2042

(102)

14425.84

(1880.63)

2422

(84)

16517.43

(1979.90)

3 Savings

accounts

with banks

7317551

(2047811)

8217.25

(1821.65)

7429500

(2262125)

9897.42

(2477.59)

– – – –

36

3.3 Economic Empowerment

Leach, F. & Sitaram, S. (2002) argues in their research

even though micro credit helped in social empowerment

of the women in rural areas, for economic empowerment

it requires knowledge and awareness about the business.

Ratul Lahkar(2012) states that, increase in the number of

MFI’s leads to over borrowing, especially the joint

liability of women members refrains them from availing

the micro credit as the risk of nonpayment is high. This

provided the incentive to take successive loans.

Microfinance to rural women has given a great

opportunity to the rural poor in India to attain reasonable

economic, social and cultural empowerment, leading to

better living standard and quality of life for participating

households.

Dixon-Mueller (1993) substantiates employment plays

vibrant role in women empowerment. Rural women

mainly depend on self-employment and unorganized

sector. Employment may empower the women by

providing financial freedom, social identity and

revelation for power structures free of kin networks.

Microfinance created new employment opportunities for

rural women in informal sector. (Dixon-Mueller, 1993).

SECC survey portrays employment in rural areas

progressed to 31.59 per cent to 6.62 crore in the year

2014 when compared to 2005.

3.4 Poverty Reduction

India is one of the fastest growing economies in the

world. Still a large population doesn’t have the access to

formal channels of banking in the country, especially the

rural poor. Microfinance is started as a movement for

poverty alleviation and financial inclusion in late

seventies. It helped in providing finance to a large

number of unbanked poor.

Study by Devaraja T.S.(2011)reveals that , saving habits

of the members improved significantly after participating

in the microfinance schemes. The dependency on local

money lenders reduced considerably and the social

awareness of members improved. Although the micro

finance paved the way for poverty alleviation it faces

some challenges like high interest rate, lack of skill

among members.

The accessibility of financial resources to assist rural

poor women turn out to be change agents. Micro finance

has worked for manifestation of rural women into self-

reliant. Rural women who are in the pole position, micro

credit effort help out start a extended chain of economic

movement.

Vijay Mahajan and G. Nagasri (2000) displays Micro

finance is retrieving financial services in an informally

formal direction, in flexible, reactive and thoughtful

manner, overcoming the barriers of formal sector like

high transaction cost, low scale of operation etc.

4.0 FINDINGS

The success of micro finance lies in availing and proper

usage of funds for the required purpose. Proper training

facilities, skill developments and awareness should be

provided for empowerment of women economically

along with microcredit. Even though microfinance

claims that financial inclusion is their main moto, the rate

of interest charged by the MFI’s are quite high (12.25%

to 18%).

Being rural women as major borrowers of microcredit,

women entrepreneurs are not motivated to the required

level. The issues like polygamy and patriarchal society

works as blockades for empowerment of women in rural

areas.

5.0 SUGGESTIONS

Microfinance Institutions required to cut down the

interest rates to affordable levels of rural people and

increase the funds available for borrowings.

Microfinance institutions should also focus on skill

development and training for upcoming rural women

entrepreneurs

Microfinance institutions should build trust, unity and

bond among the members of SHGs

6.0 CONCLUSION

Micro finance is a panacea for issues faced by rural

women. Micro finance boosts self-confidence, financial

sustainability and social network building skills. It

supports underprivileged rural women in availing micro

credits denied by the other financial institutions.

Micro finance will inspire the rural women to reap the

benefits of micro credit and enable them to be self-

employed. Even though the income levels of the women

participants has not improved considerably microfinance

has left positive impression on the socio economic

aspects of women empowerment.

7.0 REFERENCES

(1) Chaudhury, Suman Kalyan, (2012). Rural

Microfinance and Micro-enterprise. 2nd ed. New

Delhi: Discovery Pub. House.

(2) Modi, D., Patel, M., & Patel, M. (2014). IOSR

Journal of Business and Management (IOSR-

JBM). Impact of Microfinance Services on Rural

Women Empowerment: An Empirical

Study, 16(11), 68-75.

(3) Lahkar, R., Pingali, V., & Sadhu, S. (2012). Does

Competition in the Microfinance Industry

Necessarily Mean Over-borrowing? Indian Institute

of Management Ahmedabad, 2-18.

(4) Prabhu, S., and F. Elayaraja. "A Study On Micro

Finance And Women Empowerment In Thanjavur

District." International Journal of Informative &

Futuristic Research 2.8 (2015): 2636-

643. International Journal of Informative &

Futuristic Research.

(5) Gaiha, R., and M. Nandhi (2005) Microfinance,

self-help groups and empowerment in Maharashtra.

Rome: International Fund for Agricultural

Development.

(6) Leach, F. & Sitaram, S. (2002, November).

Microfinance and women’s empowerment: a lesson

from India. Development in Practice, Vol. 12, No.

5, pp. 575-588.

37

(7) Devaraja, T.S., 2011. “Microfinance in India - A

Tool 20. Biswas, T. and P.P. Sengupta, College

Science in for Poverty Reduction”.

(8) Kulkarni, Vani S. (2011) Women’s empowerment

and microfinance: An Asian perspective study,

Occasional Paper 13, International Fund for

Agricultural Development, Rome.

(9) Nasir, Sibghatullah. "Microfinance in India:

Contemporary Issues and Challenges." Middle-East

Journal of Scientific Research 15.2 (2013): 191-99.

Print.

(10) Dixon-Mueller, R. (1993). Population policy and

women's rights: transforming reproductive

choice. Westport: Praeger.

(11) Vijay, Mahajan and G, Nagasri (2000).Building

Sustainable Microfinance Institutions in India. .

International Review of Business, Research Papers,

Vol. 3 No. 5 July 2000 pp. 102- 137.

(12) Kumar Sharma, E. "Union Budget 2015-16: Mudra

for Microfinance and Financial Inclusion

Growth." Business Today: Business News, Latest

Stock Market and Economy News India from

Businesstoday.in. Business Today, 28 Feb. 2015.

Web. <http://www.businesstoday.in>.

(13) "Annual Report 2014-

15."Https://www.nabard.org/english/annualreport.as

px. NABARD, 1 June 2015. Web.

(14) Gera, Ishaan. "Microfinance Sector Poised to Grow

Robustly in Five Years." VCCIRCLE. VCCIRCLE,

17 Apr. 2015. Web.

(15) Provisional Data of Socio Economic and Caste

Census (SECC) 2011 for Rural India Released

(Provisional Data of Socio Economic and Caste

Census (SECC) 2011 for Rural India Released)

(16) Socio Economic & Caste Census 2011: A mobile in

2 of every 3 rural homes, a salaried job in 1 of 10

(The Indian Express)