Embed Size (px)

Citation preview

"9th Looking Ahead Conclave - Preparing for Turnaround“

Forecast of Automobiles Industry in FY16

ICRA Management Consulting Services Limited

Society of Indian Automobile Manufacturers

11th January 2015 New Delhi

Agenda

2

Macro -economic Environment

Sectoral Trends

Industry Outlook for FY16

Economic slowdown had a negative impact on Indian Auto

Sector

3

Parameter FY06-

FY11

FY12-

FY14

GDP Growth (%) 8.6 5.3

Manufacturing GDP growth (%) 9.1 2.6

Growth in Gross Fixed Capital Formation (GFCF)

(%) 11.4 4.3

Average Inflation rate (%) 6.2 7.4

INR vs. US$ (Rs./US$) 44.8 54.2

Annual average crude oil prices (US$/barrel) 72.3 90.1

CAGR growth in production (%)

Passenger Vehicles (PV) 17.9 (1.2)

Commercial Vehicles (CV) 14.2 (13.3)

Two Wheelers (2W) 11.9 4.6

Three Wheelers (3W) 13.0 (2.8)

Automotive Components 16.5 (3.6)

• Adverse impact on consumer sentiment

• Increase in cost of ownership – due to high fuel prices, interest rates

Domestic Sales Trends over past five years

4

0

50

100

150

200

250

Q1

FY

10

Q3F

Y10

Q1F

Y11

Q3F

Y11

Q1F

Y12

Q3F

Y12

Q1

FY

13

Q3F

Y13

Q1F

Y14

Q3F

Y14

Q1F

Y15

Un

its

(in

000s)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Q1F

Y10

Q3F

Y10

Q1F

Y11

Q3F

Y11

Q1F

Y12

Q3F

Y12

Q1F

Y13

Q3F

Y13

Q1F

Y14

Q3F

Y14

Q1F

Y15

0.0

0.3

0.5

0.8

1.0

Q1F

Y10

Q3F

Y10

Q1F

Y11

Q3F

Y11

Q1F

Y12

Q3F

Y12

Q1F

Y13

Q3F

Y13

Q1F

Y14

Q3F

Y14

Q1F

Y15

Un

its

(in

mn

)

Un

its

(in

mn

)

Source: SIAM, IMaCS analysis

FY12-FY14 (CAGR) = 5%

q-o-q (last 8 quarters) = 1.4%

Variation = 7.4%

FY12-FY14 (CAGR) = (2.6%)

q-o-q (last 8 quarters) = (0.4%)

Variation = 6.5%

FY12-FY14 (CAGR) = (11.1%)

q-o-q (last 8 quarters) = (1.7%)

Variation = 14.2%

2.0 2.5 2.6 2.7 2.5

1.9

0.5

0.7 0.8 0.8

0.6

0.6

0.4

0.5 0.5 0.5

0.5

0.4

9.4

11.8

13.4 13.8 14.8

12.1

0.0

3.0

6.0

9.0

12.0

15.0

0.0

1.0

2.0

3.0

4.0

5.0

FY10 FY11 FY12 FY13 FY14 FY15 (Apr-

Dec)

Un

its

(in

mn

)

Un

its

(in

mn

)

Passenger vehicles Commercial Vehicles

Three wheelers Two wheelers (RHS)

Three tier analytical framework of IMaCS’ demand

forecasting model

5

Mo

de

l C

om

po

ne

nts

Cau

sal P

art

s

1A) Causal Econometric model • Univariate Analysis -

economic , industrial and

other factors

• Zero order correlation

• Model / Segment specific

demand functional forms

• Forecast / In sample back

testing

• Substitution model

across categories

Price

Non-price

• ARIMA & VaR methods

Ad

ap

tive

Ad

jus

tme

nt

Mo

du

le

3) Adaptive adjustment to forecasts - based upon

Primary survey – OEMs, dealers on pent up

demand, stock position, discounts, model/ variants

discontinuities –M-M basis

Consistency check for feedback

recd. from OEMs, dealers using

statistical methods

Exogenous adjustment to

results from1+2

1B) Preference shifts - that cause

spikes in sales (e.g. new launches)

1C) Exogenous Impetus - e.g. excise

cut.

2) Time series components:

• Cyclic component - business cycles

• Seasonal component - seasonal

aberrations across every 12 month cycle

• Random Part - Correction

No

n-C

au

sal P

art

Specific models for different vehicle categories

6

IMaCS Forecasting Model – Coverage

Category Models - Category wise Coverage

Passenger Vehicles A1 A2 A3 A4,A5,

A6 UV

Two Wheelers Motorcycles Scooters Mopeds

Three Wheelers 3w Goods 3w

Passengers

LCV & MHCV SCV <3.5 LCV

MHCV 7.5

to12T MHCV Total Buses

Passenger Vehicles

7

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

mn

)

Mid size

0

0.1

0.2

0.3

0.4

0.5

0.6

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

mn

)

Micro, Mini & Compact

0

5

10

15

20

25

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3F

Y0

7

Q1F

Y0

8

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1F

Y1

3

Q3F

Y1

3

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

000s)

A4-A6

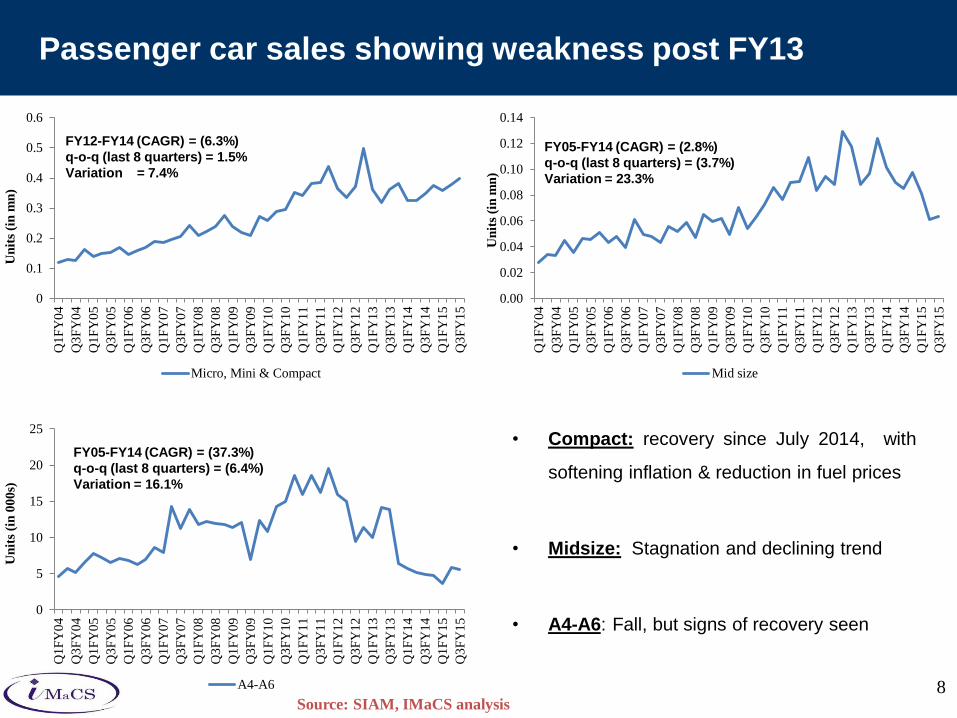

Passenger car sales showing weakness post FY13

8

FY12-FY14 (CAGR) = (6.3%)

q-o-q (last 8 quarters) = 1.5%

Variation = 7.4%

FY05-FY14 (CAGR) = (37.3%)

q-o-q (last 8 quarters) = (6.4%)

Variation = 16.1%

FY05-FY14 (CAGR) = (2.8%)

q-o-q (last 8 quarters) = (3.7%)

Variation = 23.3%

Source: SIAM, IMaCS analysis

• Compact: recovery since July 2014, with

softening inflation & reduction in fuel prices

• Midsize: Stagnation and declining trend

• A4-A6: Fall, but signs of recovery seen

0

10

20

30

40

50

60

70

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3F

Y0

7

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1F

Y1

3

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Th

ou

san

ds

MPVs

0

20

40

60

80

100

120

140

160

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

00

0s)

MUV/SUV

New model launches have driven growth in sales of SUVs

9

• After showcasing a growth of 21%, 10%,

23% and 51% respectively from FY09 to

FY13, the segment declined by 5.1% in

FY14 and still continues to remain weak

except for the festive season

• After witnessing strong growth of 41%, 42%

and 10% respectively from FY09 to FY12

the segment has showed signs of weakness

in FY13 and FY14 on account of no new

launches in the segment

• Current Fiscal outlook also continues to

remain bleak with the 3rd quarter showing a

decline in excess of 10%

FY12-FY14 = 19.5%

q-o-q (last 8 quarters) = (0.6%)

Variation = 8.1% (last 8 quarters)

FY12-FY14 = (9.9%)

q-o-q (last 8 quarters) = (4.4%)

Variation 14.7% (last 8 quarters)

Source: SIAM, IMaCS analysis

Demand drivers

10

Economic

• GDP q-q

• Excise Rates

• Interest rates

• Weighted Fuel prices

• Private Final Consumption Expenditure

(PFCE)

• WPI – Auto-parts index

Industrial

Variables

• New model launches

• Inventory levels

Other

factors

• Substitution from other category of

vehicles (A1 and Motorcycles/Scooters )

• Substitution within the category (A2 to

A3, A2 to Compact SUV, A3 to SUV etc.)

Zero order correlation matrix – Illustrative – A1&A2

segment

11

A1

GDP at

factor cost

(Q) PFCE

Excise

Duty

Interest

Rate Fuel Price

motorcycle

sales

scooter

sales

Motorcycle

+ Scooter A1A2

Pearson

Correlatio

n

1 .758**

.760**

-.357* .125 .761

**.822

**.823

**.835

**.679

**

Sig. (2-

tailed)

.000 .000 .020 .482 .000 .000 .000 .000 .000

N 42 42 42 42 34 42 42 42 42 42

Pearson

Correlatio

n

.758** 1 .983

**-.770

** -.201 .884**

.928**

.900**

.934**

.917**

Sig. (2-

tailed)

.000 .000 .000 .254 .000 .000 .000 .000 .000

N 42 42 42 42 34 42 42 42 42 42

Pearson

Correlatio

n

.760**

.983** 1 -.760

** -.187 .901**

.937**

.914**

.944**

.872**

Sig. (2-

tailed)

.000 .000 .000 .290 .000 .000 .000 .000 .000

N 42 42 42 42 34 42 42 42 42 42

Correlations

a1

gdpfcq

pfceo

Pearson

Correlatio

n

.679**

.917**

.872**

-.785** -.335 .711

**.875

**.774

**.855

** 1

Sig. (2-

tailed)

.000 .000 .000 .000 .053 .000 .000 .000 .000

N 42 42 42 42 34 42 42 42 42 42

a1a2

**. Correlation is significant at the 0.01 level (2-tailed).

*. Correlation is significant at the 0.05 level (2-tailed).

Functional Form & Related Statistics –A1& A2 Elasticity

Model

12

Causal model explains upto 87%

variability….. NOT good enough !

Ln (A1+A2 sales) = -0.982+.1.058 Ln (PFCE)

- 0.285 * Ln (Excise)

Model Summaryb

Model R R Square Adjusted

R Square

Std. Error of

the Estimate

.932a .868 .861 .12848

a. Predictors: (Constant), lnexcise, lnpfce

b. Dependent Variable: lna1a2

Coefficientsa

Model

Unstandardized

Coefficients

Standardize

d

Coefficients t Sig.

B Std.

Error Beta

1

(Constant

) -.982 2.094 -.469 .642

lnpfce 1.058 .141 .693 7.497 .000

lnexcise -.285 .092 -.285 -3.084 .004

a. Dependent Variable: lna1a2

Causal model alone does not explain short term demand

behaviour completely – E.g. New Model Launches

13

0

100

200

300

400

500

600

700

800

900

1000

Q1F

Y05

Q3F

Y05

Q1

FY

06

Q3F

Y06

Q1F

Y07

Q3F

Y07

Q1F

Y08

Q3F

Y08

Q1F

Y09

Q3F

Y09

Q1

FY

10

Q3F

Y10

Q1F

Y11

Q3F

Y11

Q1F

Y12

Q3F

Y12

Q1F

Y13

Q3F

Y13

Q1

FY

14

Q3F

Y14

Q1F

Y15

Un

its

(in

000s)

Actual Sales (A1 + A2) Model sales (A1 + A2)

0

50

100

150

200

250

300

350

400

450

500

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Un

its

(in

00

0s)

Actual Sales (UVs) Model sales (UVs)

Launch of Maruti Suzuki Alto

K10, Hyundai next gen i10

and i20 era and Nissan Micra

Launch of Mahindra

XUV 5oo, Bolero new

generation, Maruti

Suzuki Ertiga and

Renault Duster

Source: SIAM, IMaCS analysis

Revised estimates post time series correction –Q1 FY14 to

Q2 FY15

14

Actual Sales

(A1 + A2)

Model sales

(A1 + A2)

Q2FY14 325848 313872

Q3FY14 348893 356174

Q4FY14 375558 354283

Q1FY15 359297 374935

Q2FY15 379434 370010

Source: SIAM, IMaCS analysis

- Causal and time series adjustment increases model accuracy significantly

- The above estimates does NOT take into account module 3 adjustments –

This will further improve model accuracy

Launch of Maruti Suzuki Alto

K10, Hyundai next gen i10

and i20 era and Nissan Micra

Increase in petrol prices by 25%

and diesel prices by 47% over 11

month period, firm interest rate,

Passenger Cars to grow at 4.7% in FY16 with compact segment leading

the growth ( Results of Causal Model and Time Series Correction)

15

326

326

349

376

359

379

379

389

387

397

394

404

-9%

3%

-3% -2%

10% 16%

9%

4%

8%

5% 4% 4%

Q1F

Y14

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1

FY

15

Q2F

Y15

Q3

FY

15 E

Q4

FY

15 P

Q1

FY

16 P

Q2

FY

16 P

Q3

FY

16 P

Q4

FY

16 P

6

5

5

5

4

6

8

9

9

9

9

9

-9%

3%

-3% -2%

10%

16%

9%

4%

8% 5% 4% 4%

Q1

FY

14

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15 E

Q4

FY

15 P

Q1

FY

16 P

Q2

FY

16 P

Q3

FY

16 P

Q4

FY

16 P

• Recovery in GDP growth, cooling inflation lead

to reduction in interest rates and falling crude

prices to drive demand

• Compact and premium segment to benefit the

most as a slew of model launches are also

expected in those segments

• Premium segment expected to get push on

account of lower base and planned launches

102

90

85

97

81

61

68

70

71

70

70

70

-13%

1%

-12%

-21% -20%

-32%

-20%

-29%

-12%

14% 3% 1%

Q1F

Y14

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15 E

Q4F

Y15 P

Q1F

Y16 P

Q2F

Y16 P

Q3F

Y16 P

Q4F

Y16 P

All quarterly sales figures are in ‘000s, Source: SIAM, IMaCS analysis

FY16 growth: 5% Micro, Mini & Compact FY16 growth: 0.5% Midsize

A4 to A6 FY16 growth: 32%

Utility Vehicles to grow at 12% in FY16 with SUV segment

leading the growth

16

124

119

142

141

129

144

148

159

149

151

176

194

5%

-14%

-4% -7%

4%

22%

4%

13% 16%

5%

19% 22%

Q1

FY

14

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15 E

Q4

FY

15 P

Q1F

Y16 P

Q2F

Y16 P

Q3F

Y16 P

Q4F

Y16 P

49

53

47

42

42

46

49

48

49

48

49

40

-6%

4%

-25%

-32%

-14% -13%

4%

13% 16%

5% 2%

-15%

Q1

FY

14

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1F

Y15

Q2

FY

15

Q3

FY

15 E

Q4

FY

15 P

Q1

FY

16 P

Q2F

Y16 P

Q3

FY

16 P

Q4

FY

16 P

• SUV/MUV segment to continue its momentum in FY16 and is expected to witness strong

growth in H2FY16

• Also, there are a slew of model launches expected in the segment in the next fiscal

• MPV segment expected to shrink due to capacity constraints and now new model launch in

the category

All quarterly sales figures are in ‘000s

Source: SIAM, IMaCS analysis

FY16 growth: 15.5%

MUV/SUV

FY16 growth: 1.1% MPV

Two Wheelers

17

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

mn

)

Scooters

0

50

100

150

200

250

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

000s)

Mopeds

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

mn

)

Motorcycles

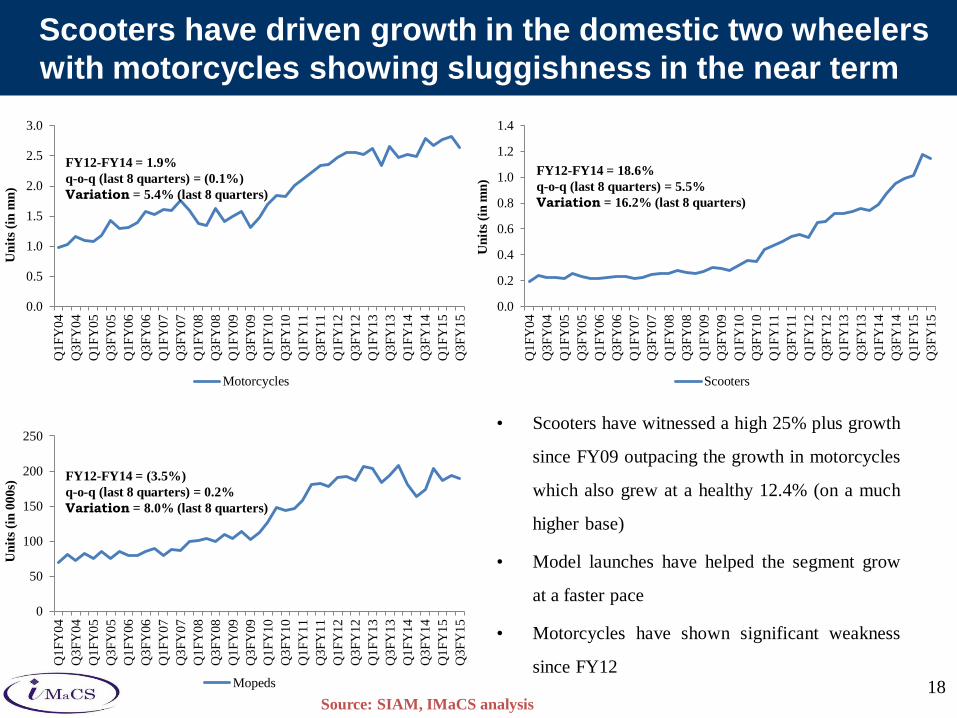

Scooters have driven growth in the domestic two wheelers

with motorcycles showing sluggishness in the near term

18

• Scooters have witnessed a high 25% plus growth

since FY09 outpacing the growth in motorcycles

which also grew at a healthy 12.4% (on a much

higher base)

• Model launches have helped the segment grow

at a faster pace

• Motorcycles have shown significant weakness

since FY12

FY12-FY14 = 1.9%

q-o-q (last 8 quarters) = (0.1%)

Variation = 5.4% (last 8 quarters)

FY12-FY14 = (3.5%)

q-o-q (last 8 quarters) = 0.2%

Variation = 8.0% (last 8 quarters)

FY12-FY14 = 18.6%

q-o-q (last 8 quarters) = 5.5%

Variation = 16.2% (last 8 quarters)

Source: SIAM, IMaCS analysis

Demand drivers

19

Economic

•Q-Q GDP

• Excise Rate

• Interest

•Weighted Fuel Price

• Private Final Consumption Expenditure (PFCE)

• Population in the age bracket of 15-29 years

•WPI – Auto-parts index

Industrial

Variables

•New model launches for scooters as well as

motorcycles

• Inventories

Other factors

• Substitution from other category of vehicles (A1 and

Motorcycles/Scooters etc.)

• Substitution within the category (scooters to

motorcycles, Motorcycles to Scooters etc.)

Zero order correlation matrix – Illustrative – Motorcycles

segment

20

Motorcycle

s Scooters Fuel Price

Excise

duty

Interest

rates

GDP at

factor cost

(Q) PFCE

Population

of age 15-

29 years

Correlations

Pearson

Correlatio

n

-.241 -.101 .059 .222 1 -.176 -.151 -.211

Sig. (2-

tailed)

.176 .576 .744 .214 .326 .401 .237

N 33 33 33 33 33 33 33 33

Interest

rates

Pearson

Correlatio

n

.912**

.946**

.889**

-.368* -.151 .971

** 1 .803**

Sig. (2-

tailed)

.000 .000 .000 .035 .401 .000 .000

N 33 33 33 33 33 33 33 33

PFCE

Pearson

Correlatio

n

1 .932**

.906** -.240 -.241 .901

**.912

**.700

**

Sig. (2-

tailed)

.000 .000 .179 .176 .000 .000 .000

N 33 33 33 33 33 33 33 33

Motorcycle

s

*. Correlation is significant at the 0.05 level (2-tailed).

**. Correlation is significant at the 0.01 level (2-tailed).

Functional Form & Related Statistics – Motorcycles

Elasticity Model

21

Causal model explains upto 91%

variability…..

Ln (motorcycle sales) = -

14.590+0.742*Ln PFCE-

0.527*Ln interest rate

+6.914*LnAge

Standardiz

ed

Coefficient

s

B Std. Error Beta

(Constant) 14.590 6.805 2.144 .041

lnpfce .742 .234 .514 3.173 .004

lnint -.527 .202 -.207 -2.614 .014

lnage 6.914 2.866 .384 2.412 .022

1

a. Dependent Variable: lnmc

Coefficientsa

Model

Unstandardized

Coefficients

t Sig.

R R Square

Adjusted

R Square

Std. Error

of the

Estimate

1 .917a .841 .824 .10485

Model Summary

Model

a. Predictors: (Constant), lnage, lnint, lnpfce

Estimates subject to time series correction !

Backtest chart post time series correction –Q1 FY13 to Q3

FY15

22

Actual sales

(scooters)

Model sales

(scooters)

Q1FY13 720884 748462

Q2FY13 734714 689707

Q3FY13 756162 806876

Q4FY13 745192 777716

Q1FY14 785591 823482

Q2FY14 872330 840310

Q3FY14 953471 975315

Q4FY14 991352 965126

Q1FY15 1010422 1035611

Q2FY15 1179929 1091614

Q3FY15 1144591 1131898

Actual sales

(Motorcycles)

Model sales

(Motor cycles)

Q1FY13 2628949 2310365

Q2FY13 2341641 2395055

Q3FY13 2647753 2665567

Q4FY13 2466590 2584419

Q1FY14 2524316 2591805

Q2FY14 2489807 2669502

Q3FY14 2793399 2943172

Q4FY14 2672295 2949180

Q1FY15 2772573 2886606

Q2FY15 2826111 2785175

Q3FY15 2641923 2834352

Source: SIAM, IMaCS analysis

- Model is accurate upto 95%

- The present estimates does NOT take into account module 3 adjustments – Expected

to further improve forecast accuracy

Revised error rate chart post time series correction –Q1

FY13 to Q3 FY15

23 Source: SIAM, IMaCS analysis

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

Actual sales (scooters) Model sales (scooters)

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

Actual sales (Motorcycles) Model sales (Motor cycles)

18

1

164

17

4

20

4

18

6

19

4

19

0

197

20

7

21

8

21

1

21

6 -11% -10% -10%

-2%

3%

18%

9%

-3%

12% 12% 11% 10%

Q1

FY

14

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

E

Q1

FY

16

P

Q2

FY

16

P

Q3

FY

16

P

Q4

FY

16

P

Two wheelers to grow at 10.5% in FY16 with scooter

segment leading the growth

24

• Scooters to continue their growth momentum

• Capacity additions to benefit scooter

manufacturers

• Motorcycles and Mopeds showing some signs of

recovery; while motorcycles are expected to

show marginal growth, mopeds are expected to

fare better

All quarterly sales figures are in ‘000s, Source: SIAM, IMaCS analysis

FY16 growth: 6.4% Motorcycles FY16 growth: 20.5% Scooters

Mopeds FY16 growth: 11.1%

78

6

87

2

95

3

99

1

1,0

10

1,1

80

1,1

45

1,1

91

1,3

27

1,3

96

1,3

48

1,3

83

9%

19%

26%

33%

29%

35%

20% 20%

31%

18% 18% 16%

Q1F

Y1

4

Q2F

Y1

4

Q3F

Y1

4

Q4F

Y1

4

Q1F

Y1

5

Q2F

Y1

5

Q3F

Y1

5

Q4F

Y1

5 E

Q1F

Y1

6 P

Q2F

Y1

6 P

Q3F

Y1

6 P

Q4F

Y1

6 P

2,5

24

2,4

90

2,7

93

2,6

72

2,7

73

2,8

26

2,6

42

2,8

84

2,9

35

2,9

87

2,9

33

2,9

85

-4%

6% 6%

8% 10%

14%

-5%

8%

6% 6%

11%

3%

Q1F

Y1

4

Q2F

Y1

4

Q3F

Y1

4

Q4F

Y1

4

Q1F

Y1

5

Q2F

Y1

5

Q3F

Y1

5

Q4F

Y1

5 E

Q1F

Y1

6 P

Q2F

Y1

6 P

Q3F

Y1

6 P

Q4F

Y1

6 P

Commercial Vehicles

25

0

20

40

60

80

100

120

140

160

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

00

0s)

LCVs

0

20

40

60

80

100

120

140

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

00

0s)

Small Commercial Vehicles

Small Commercial Vehicles have driven growth in the LCV

segment

26

• Since the creation of the Small Commercial Vehicles segment (launch of Tata Ace) in May 2005, the

segment has shown robust growth. For the first time since May 2005 the segment has showed signs of

deceleration in FY14

• Pick-up segment is showing slow and gradual recovery

• Other segments of LCV continue to remain stagnant owing to no newer options available

FY12-FY14 = 0.03%

q-o-q (last 8 quarters) = (3.5%)

Variation = 17.6% (last 8 quarters)

FY12-FY14 = (2.55%)

q-o-q (last 8 quarters) = (3.3%)

Variation = 17.2% (last 8 quarters)

Source: SIAM, IMaCS analysis

0

10

20

30

40

50

60

70

80

90

100

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

00

0s)

MHCVs

0

5

10

15

20

25

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

00

0s)

ICVs

0

5

10

15

20

25

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

000s)

Buses

Recovery signs visible in M&HCV post formation of new

government

27

• After a y-o-y decline for 27 straight months

since March 2012, the domestic MHCV industry

recorded a positive growth of 3% y-o-y in June

2014 and has stayed in green since then

• Sales of Heavy Commercial Vehicle (HCV)

goods (GVW >12tonnes) have outpaced that of

Intermediate Commercial Vehicle (ICV) (GVW

7.5-12tonnes)

FY12-FY14 = (21.4%)

q-o-q (last 8 quarters) = (3.0%)

Variation = 24.9% (last 8 quarters)

FY12-FY14 = (26.46%)

q-o-q (last 8 quarters) = (6.2%)

Variation = 16.1% (last 8 quarters)

x

Source: SIAM, IMaCS analysis

FY12-FY14 = (3.95%)

q-o-q (last 8 quarters) = 9.3%

Variation = 20.4% (last 8 quarters)

x

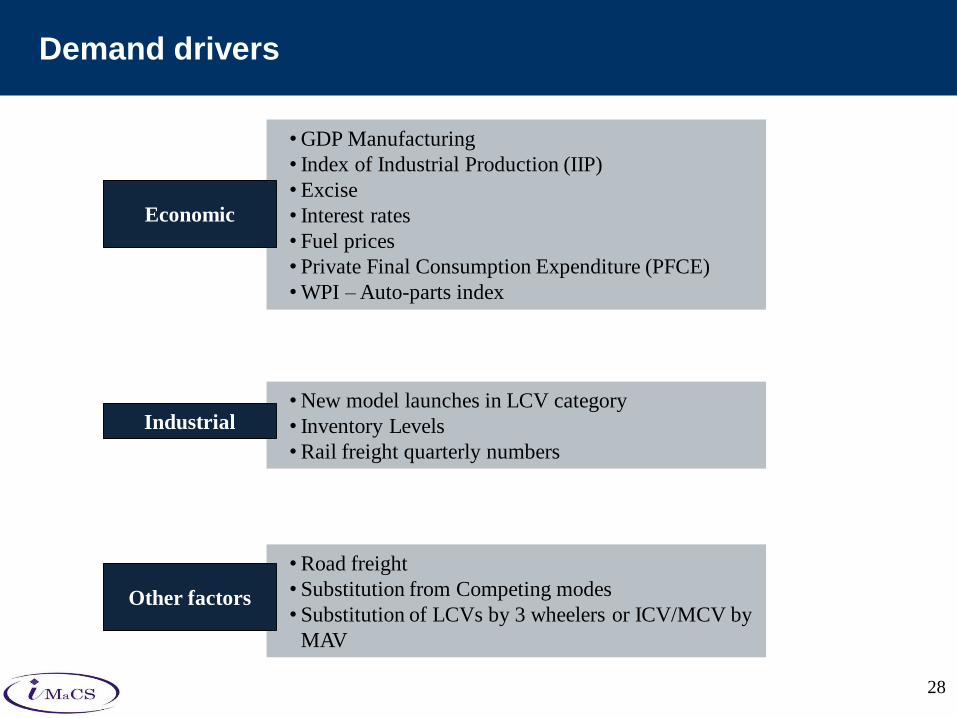

Demand drivers

28

Economic

•GDP Manufacturing

• Index of Industrial Production (IIP)

• Excise

• Interest rates

• Fuel prices

• Private Final Consumption Expenditure (PFCE)

•WPI – Auto-parts index

Industrial •New model launches in LCV category

• Inventory Levels

•Rail freight quarterly numbers

Other factors

•Road freight

• Substitution from Competing modes

• Substitution of LCVs by 3 wheelers or ICV/MCV by

MAV

Zero order correlation matrix – Illustrative – Small

Commercial Vehicles segment

29

SCV (<

3.5 T

GVW)

LCV (5 to

7T)

Diesel

prices

GDP Mfg

(Q) IIP

Freight

Movement

by rail

Interest

rates PFCE

Correlations

Pearson

Correlatio

n

.940**

-.845**

.832** 1 .988

**.974

** .082 .953**

Sig. (2-

tailed)

.000 .000 .000 .000 .000 .612 .000

N 41 41 41 41 41 41 41 41

GDP Mfg

(Q)

Pearson

Correlatio

n

1 -.791**

.801**

.940**

.900**

.905** .058 .663

**

Sig. (2-

tailed)

.000 .000 .000 .000 .000 .715 .000

N 42 42 42 41 42 42 42 42

SCV (<

3.5T GVW)

Functional Form & Related Statistics – Small Commercial

Vehicles Elasticity Model

30

R R Square

Adjusted

R Square

Std. Error

of the

Estimate

1 .977a .954 .953 .13431

Model

a. Predictors: (Constant), lngdpM

Model Summary

Standardiz

ed

Coefficient

s

B Std. Error Beta

(Constant) -8.787 .687 -12.797 .000

lngdpM 2.630 .092 .977 28.491 .000

1

a. Dependent Variable: ln3.5

Coefficientsa

Model

Unstandardized

Coefficients

t Sig.

Causal model explains upto 96%

variability….

Ln (SCV sales) = -8.787+2.630*Ln

gdpM

Forecast improves after including time series correction –

Q1 FY14 to Q3 FY15

31

Actual

sales

(SCVs)

Model sales

(SCVs)

Q1FY14 90534 79554

Q2FY14 90977 83539

Q3FY14 90383 85760

Q4FY14 88063 84592

Q1FY15 70567 73655

Q2FY15 80672 78202

Q3FY15 79828 77292

- Causal and time series adjustment get the forecast to about 96% accuracy

- The present estimates does NOT take into account module 3 adjustments – Expected

to further increase forecast accuracy

Revised error rate chart post time series correction –Q1

FY14 to Q3 FY15

32

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15 Q3FY15

Actual sales (SCVs) Model sales (SCVs)

0

10000

20000

30000

40000

50000

60000

Q4FY14 Q1FY15 Q2FY15 Q3FY15

Actual sales (MHCVs) Model sales (MHCVs)

SCVs to showcase marginal growth in FY16

33

• Small Commercial Vehicles expected to perform better on account on improvement in demand of

consumables reflected by improving PFCE

• Other segments of LCVs to continue its sluggishness

All quarterly sales figures are in ‘000s

Source: SIAM, IMaCS analysis

FY16 growth: 4.7% Small Commercial Vehicles

FY16 growth: 4.4% Other LCVs

91 91 90 88 71 81 80 77 81 81 80 81

-3%

-14%

-21%

-29%

-22%

-11% -12% -12%

15%

0.02% -0.1%

5%

Q1F

Y14

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15 E

Q1F

Y16 P

Q2F

Y16 P

Q3F

Y16 P

Q4F

Y16 P

Small Commercial Vehicles y-o-y growth

98 98 97 96 77 88 87 84 88 88 87 88

-4%

-15%

-22%

-29%

-21%

-11% -10% -12%

14%

0% 0%

5%

Q1F

Y14

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15 E

Q1F

Y16 P

Q2F

Y16 P

Q3F

Y16 P

Q4F

Y16 P

LCVs y-o-y growth

43 39 33 46 41 46 49 50 46 46 45 46

-18%

-37% -32%

-20%

-7%

16%

47%

10% 13%

0%

-9% -9%

Q1

FY

14

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

E

Q1

FY

16

P

Q2

FY

16

P

Q3

FY

16

P

Q4

FY

16

P

13 10 9 10 8 9 10 9 8 8 8 8

-5%

-27%

-37% -40%

-36%

-12%

12%

-8%

-2%

-12%

-19%

-9%

Q1

FY

14

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

E

Q1

FY

16

P

Q2

FY

16

P

Q3

FY

16

P

Q4

FY

16

P

MAVs to lead recovery; however buses to face

sluggishness on account of withdrawal of JNNURM

34 All quarterly sales figures are in ‘000s

Source: SIAM, IMaCS analysis

• Withdrawal of JnNURM scheme to impact the

bus segment significantly

• MHCVs expected to show strong recovery lead

by growth in MAVs

• ICVs would continue their downtrend owing to

loss of business to MCVs on account of better

cost economics

FY16 growth: (10.1%) ICV FY16 growth: (1.6%) MHCVs

FY16 growth: (11%) Buses

21 14 11 15 20 15 14 15 13 13 15 15

1%

-14%

0%

-12%

-5%

3%

37%

-3%

-32%

-10%

2% 2%

Q1

FY

14

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

E

Q1

FY

16

P

Q2

FY

16

P

Q3

FY

16

P

Q4

FY

16

P

Three wheelers

35

0

20

40

60

80

100

120

140

160

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

00

0s)

3W Passengers

0

5

10

15

20

25

30

35

40

45

50

Q1

FY

04

Q3

FY

04

Q1

FY

05

Q3

FY

05

Q1

FY

06

Q3

FY

06

Q1

FY

07

Q3

FY

07

Q1

FY

08

Q3

FY

08

Q1

FY

09

Q3

FY

09

Q1

FY

10

Q3

FY

10

Q1

FY

11

Q3

FY

11

Q1

FY

12

Q3

FY

12

Q1

FY

13

Q3

FY

13

Q1

FY

14

Q3

FY

14

Q1

FY

15

Q3

FY

15

Un

its

(in

00

0s)

3W Goods

Growth driven by 3 wheeler passengers

36

• Since the launch of Tata Ace in May 2005, 3 wheeler goods have showed continuous deceleration in

growth and from Q3FY10 they have been range bound

• Growth in 3 wheelers is on account of growth in the passenger segment. Current fiscal has seen strong

growth on account of additional rickshaw permits being issued by several state governments

• 3 Wheeler passenger continues to remain a highly regulatory driven segment

FY12-FY14 = (5.9%)

q-o-q (last 8 quarters) = 1.0%

Variation = 8.9% (last 8 quarters)

FY12-FY14 = (2.7%)

q-o-q (last 8 quarters) = 0.04%

Variation = 14.7% (last 8 quarters)

Source: SIAM, IMaCS analysis

Demand drivers

37

Economic

• GDP (Q)

• Index of Industrial Production (IIP)

• Excise Rate

• Interest rates

• Fuel prices

•Growth in Private Final Consumption Expenditure

(PFCE)

•WPI – Auto-parts index

Industrial • Inventory

•New launches

Other factors

• Substitution from Small Commercial Vehicles

Zero order correlation matrix – Illustrative – 3 wheeler

passenger segment

38

3 wheeler

Goods

3 wheeler

Passenge

rs Fuel Price IIP PFCE

Interest

rates

GDP at

factor cost

Correlations

Pearson

Correlatio

n

-.584**

.948**

.883**

.912** 1 -.008 .979

**

Sig. (2-

tailed)

.000 .000 .000 .000 .960 .000

N 37 37 37 37 37 37 37

PFCE

Pearson

Correlatio-.559

**.942

**.880

**.923

**.979

** -.093 1

Sig. (2-

tailed)

.000 .000 .000 .000 .000 .556

N 37 37 39 39 37 42 42

GDP at

factor cost

(Q)

Pearson

Correlatio

n

-.495** 1 .851

**.866

**.948

** .041 .942**

Sig. (2-

tailed)

.002 .000 .000 .000 .809 .000

N 37 37 37 37 37 37 37

3 wheeler

passenge

rs

**. Correlation is significant at the 0.01 level (2-tailed).

Functional Form & Related Statistics – 3 wheeler passenger

segment Elasticity Model

39

R R Square

Adjusted

R Square

Std. Error

of the

Estimate

1 .942a .888 .882 .11957

Model Summary

Model

a. Predictors: (Constant), LNGDP, LNPFCE

Standardiz

ed

Coefficient

s

B Std. Error Beta

(Constant) -10.970 1.288 -8.515 .000

LNPFCE 1.521 .288 .869 5.276 .000

LNGDP .118 .249 .078 .473 .639

1

a. Dependent Variable: LN3WP

Coefficientsa

Model

Unstandardized

Coefficients

t Sig.

Causal model explains upto 89%

variability….. NOT good enough !

Ln (3WP sales) = -10.970+1.521*Ln

PFCE+0.118*LnGDP

Revised forecast chart post time series correction –Q1

FY14 to Q3 FY15

40

Q1F

Y07

Q3F

Y07

Q1F

Y08

Q3F

Y08

Q1F

Y09

Q3

FY

09

Q1F

Y10

Q3F

Y10

Q1F

Y11

Q3F

Y11

Q1F

Y12

Q3F

Y12

Q1

FY

13

Q3F

Y13

Q1F

Y14

Q3F

Y14

Q1F

Y15

3W passenger actual sales 3W passenger model sales

Source: SIAM, IMaCS analysis

3W

passenger

actual sales

3W

passenger

model sales

Q1FY13 89467 98333

Q2FY13 115433 117920

Q3FY13 125817 118169

Q4FY13 110401 110809

Q1FY14 87304 95113

Q2FY14 109353 98910

Q3FY14 99735 106979

Q4FY14 88531 119369

Q1FY15 98844 110521

Q2FY15 136059 127968

Q3FY15 107444 96832

- Causal and time series adjustment has reduced the error rates significantly

- The present estimates does NOT take into account module 3 adjustments – Expected

to reduce error rates significantly

3 wheeler goods would continue to remain sluggish while passenger

3W sales would decline owing to higher base ( unless exogenous

impetus – e.g. new licenses issued)

41

• 3 wheeler passenger to record marginal deceleration in growth on account of higher base of FY15

• Majority of 3 wheeler goods demand would again come only from the replacement segment as it

would continue to face stiff competition from Small Commercial Vehicles

• Another round of release of permits could lead to a reversal in deceleration of 3 wheeler

passengers growth

All quarterly sales figures are in ‘000s

Source: SIAM, IMaCS analysis

FY16 growth: (0.4%) 3 Wheeler Goods FY16 growth: (4.0%) 3 wheeler passengers

21

22

25

26

22

25

26

23

24

25

24

24

-2%

-9%

-2%

3% 6%

15%

4%

-14%

5%

-2%

-9%

5%

Q1

FY

14

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4F

Y1

5 E

Q1F

Y1

6 P

Q2F

Y1

6 P

Q3F

Y1

6 P

Q4F

Y1

6 P

3W Goods y-o-y growth

87

109

100

89

99

136

107

101

104

108

107

105

-2% -5%

-21% -20%

13%

24%

8%

14%

6%

-20%

0% 5%

Q1

FY

14

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4F

Y1

5 E

Q1F

Y1

6 P

Q2F

Y1

6 P

Q3F

Y1

6 P

Q4F

Y1

6 P

3W Passengers y-o-y growth

Discussions

42