Embed Size (px)

Citation preview

PROSPECTUS SUMMARY

Société Maghrébine de crédit-bail - MAGHREBAIL

Capital increase in cash contribution reserved to former

shareholders and preferential subscription rights holders Share price: 680 Dhs

Nominal value: 100 Dhs Maximum number of shares to be issued: 358 862 new shares

Overall amount of the transaction: 244 026 160 Dhs

Subscription period: From 25/05/2015 to 24/06/2015 inclusive Subscription parity: 7 new shares for 20 PSR

FINANCIAL ADVISOR AND GLOBAL COORDINATOR

BODY IN CHARGE OF REGISTRATION IN THE CASABLANCA STOCK EXCHANGE

THE BODY IN CHARGE OF CENTRALIZING AND COLLECTING SUBSCRIPTIONS

Approval of CONSEIL DEONTOLOGIQUE DES VALEURS MOBILIERES (Financial authority)

Pursuant to the CDVM circular entered into force on April 1st, 2012, taken pursuant to Article 14 of Dahir No. 1-93-212 of 21 September 1993 concerning the Conseil Déontologique des Valeurs Mobilières (CDVM) and the information required from corporate entities making a public offering, as amended and supplemented, the original version of the present prospectus was approved by the CDVM on the 12th may 2015 under reference No.VI/EM/008/2015.

Capital increase in cash

Prospectus Summary 2

Disclaimer

The CDVM approved, on 12th may 2015, a prospectus related to the capital increase in cash of Maghrebail Company (hereinafter also referred to "Maghrebail" or the "Company").

The prospectus approved by the CDVM is available at any time at the head office of the Company and through its financial advisor. It is also made available within a maximum delay of 48 hours through order collecting bodies.

The prospectus is at the disposal of the general public in the head office of the Casablanca Stock Exchange and on its website www.casablanca-bourse.com. It is also available on the website of the CDVM www.cdvm.gov.ma.

Capital increase in cash

Prospectus Summary 3

PART I. OVERVIEW OF THE TRANSACTION

Capital increase in cash

Prospectus Summary 4

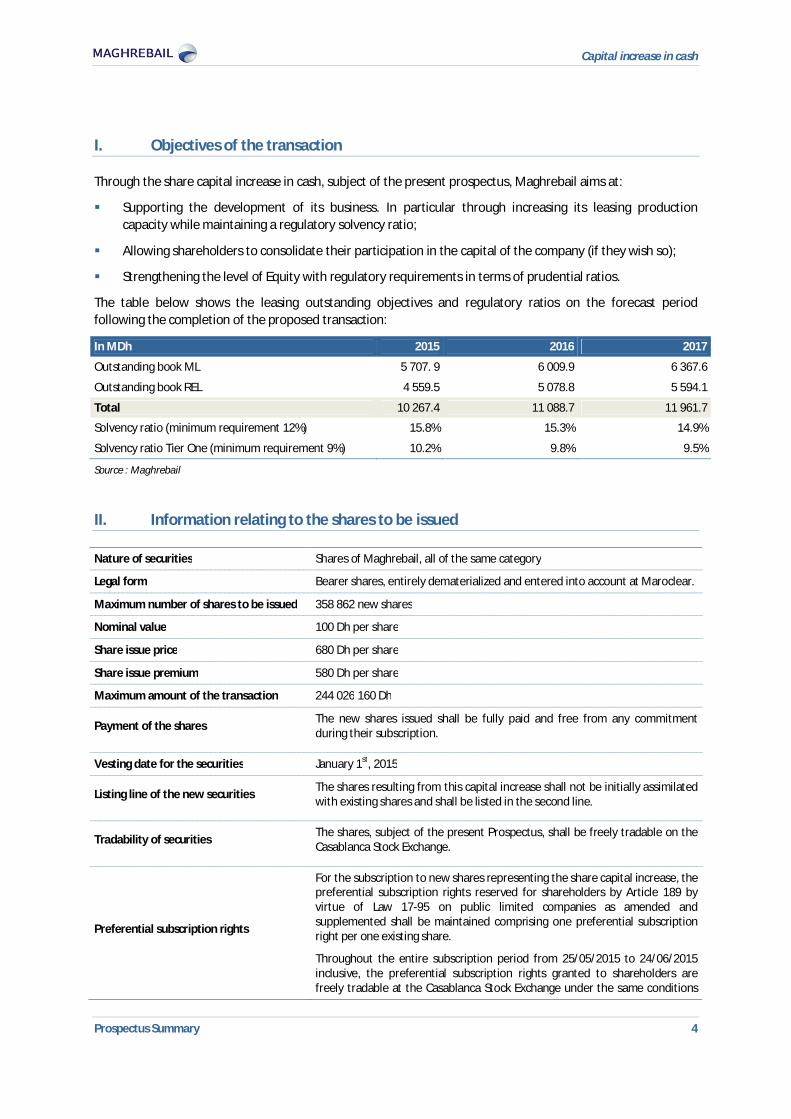

I. Objectives of the transaction

Through the share capital increase in cash, subject of the present prospectus, Maghrebail aims at:

Supporting the development of its business. In particular through increasing its leasing production capacity while maintaining a regulatory solvency ratio;

Allowing shareholders to consolidate their participation in the capital of the company (if they wish so);

Strengthening the level of Equity with regulatory requirements in terms of prudential ratios.

The table below shows the leasing outstanding objectives and regulatory ratios on the forecast period following the completion of the proposed transaction:

In MDh 2015 2016 2017

Outstanding book ML 5 707. 9 6 009.9 6 367.6

Outstanding book REL 4 559.5 5 078.8 5 594.1

Total 10 267.4 11 088.7 11 961.7

Solvency ratio (minimum requirement 12%) 15.8% 15.3% 14.9%

Solvency ratio Tier One (minimum requirement 9%) 10.2% 9.8% 9.5%

Source : Maghrebail

II. Information relating to the shares to be issued

Nature of securities Shares of Maghrebail, all of the same category

Legal form Bearer shares, entirely dematerialized and entered into account at Maroclear.

Maximum number of shares to be issued 358 862 new shares

Nominal value 100 Dh per share

Share issue price 680 Dh per share

Share issue premium 580 Dh per share

Maximum amount of the transaction 244 026 160 Dh

Payment of the shares The new shares issued shall be fully paid and free from any commitment during their subscription.

Vesting date for the securities January 1st, 2015

Listing line of the new securities The shares resulting from this capital increase shall not be initially assimilated with existing shares and shall be listed in the second line.

Tradability of securities The shares, subject of the present Prospectus, shall be freely tradable on the Casablanca Stock Exchange.

Preferential subscription rights

For the subscription to new shares representing the share capital increase, the preferential subscription rights reserved for shareholders by Article 189 by virtue of Law 17-95 on public limited companies as amended and supplemented shall be maintained comprising one preferential subscription right per one existing share.

Throughout the entire subscription period from 25/05/2015 to 24/06/2015 inclusive, the preferential subscription rights granted to shareholders are freely tradable at the Casablanca Stock Exchange under the same conditions

Capital increase in cash

Prospectus Summary 5

as Maghrebail shares. The preferential subscription must be exercised during this period under penalty of forfeiture.

Preferential subscription rights holders may subscribe irreducibly, at seven (7) new shares of one hundred (100) dirhams par value each for twenty (20) preferential subscription rights.

In addition, each shareholder may, if they desire, individually waive their preferential subscription rights.

Subscription to new shares is reserved to former shareholders of the company and preferential subscription rights holders. Therefore, they shall have irreducible subscription right on new shares to be issued.

Shareholders shall also have a subscription right for excess shares, regarding the distribution of shares not taken up by the exercise of subscription rights on an irreducible basis. This distribution shall be made in proportion to their shares in the capital and within the limit of their demands without attribution fraction.

Furthermore, if the issue is not covered by the exercise of preferential subscription rights, the Assembly authorized the Board or its agent to collect from whom they prefer, and in the best interests of the company, new subscriptions for remaining shares, in order to complete the capital increase up to the maximum fixed amount of 250 million dirhams (issue premium included) ..

The preferential subscription rights may only be exercised up to a number of PSR allowing subscription to a whole number of new shares. Shareholders or transferees of PSR who do not own, as part of their subscription on an irreducible basis, a sufficient number of preferential subscription rights to obtain a whole number of new shares, shall proceed to the purchase or sale of shares before the subscription period and the purchase or sale of PSR to market conditions during the subscription period.

The preferential subscription rights forming odd lots may be sold or completed in the market during the subscription period.

The theoretical price of such preferential subscription rights (PSR) is calculated as follows:

PSR = (Closing Maghrebail share price on the eve of the date of posting of the PSR - Subscription Price - 2014 Dividend per share) x ([Number of new shares] / [Number of old shares + Number of new shares])

Scheduled listing date of new shares 02/07/2015

Characteristics of the listing of the preferential subscription rights

Code: 1601 Ticker: MABA Label: DS MAB(AN15 7P20)

Paying-off of the order book The Casablanca Stock Exchange shall carry out on the 20/05/2015 the paying of the order book value of Maghrebail

Rights associated with shares All shares have the same rights regarding both the distribution of profits and the distribution of liquidation proceeds. Each share entitles to one vote at the holding of meetings. There is no share that entitles its holder to a double vote.

Capital increase in cash

Prospectus Summary 6

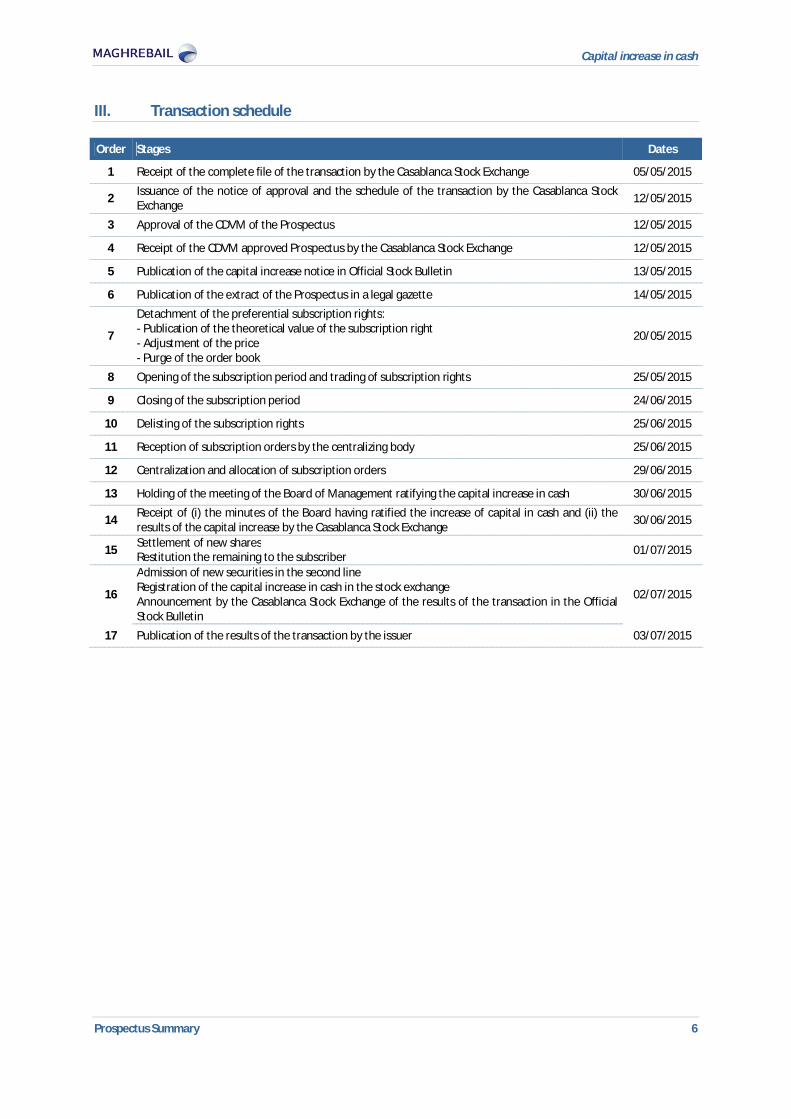

III. Transaction schedule

Order Stages Dates

1 Receipt of the complete file of the transaction by the Casablanca Stock Exchange 05/05/2015

2 Issuance of the notice of approval and the schedule of the transaction by the Casablanca Stock Exchange 12/05/2015

3 Approval of the CDVM of the Prospectus 12/05/2015 4 Receipt of the CDVM approved Prospectus by the Casablanca Stock Exchange 12/05/2015 5 Publication of the capital increase notice in Official Stock Bulletin 13/05/2015 6 Publication of the extract of the Prospectus in a legal gazette 14/05/2015

7

Detachment of the preferential subscription rights: - Publication of the theoretical value of the subscription right - Adjustment of the price - Purge of the order book

20/05/2015

8 Opening of the subscription period and trading of subscription rights 25/05/2015 9 Closing of the subscription period 24/06/2015

10 Delisting of the subscription rights 25/06/2015 11 Reception of subscription orders by the centralizing body 25/06/2015 12 Centralization and allocation of subscription orders 29/06/2015 13 Holding of the meeting of the Board of Management ratifying the capital increase in cash 30/06/2015

14 Receipt of (i) the minutes of the Board having ratified the increase of capital in cash and (ii) the results of the capital increase by the Casablanca Stock Exchange 30/06/2015

15 Settlement of new shares Restitution the remaining to the subscriber 01/07/2015

16

Admission of new securities in the second line Registration of the capital increase in cash in the stock exchange Announcement by the Casablanca Stock Exchange of the results of the transaction in the Official Stock Bulletin

02/07/2015

17 Publication of the results of the transaction by the issuer 03/07/2015

Capital increase in cash

Prospectus Summary 7

IV. Listing in the Stock Exchange

Trading characteristics of preferential subscription rights IV.1.

Scheduled listing date 25/05/2015

Code 1601

Ticker MABA

Label DS MAB(AN15 7P20)

Trading characteristics of the new shares IV.2.

Label MAB 2L J01/01/2015

Share code 21600 Ticker MAB2 Compartment 2nd compartment Business sector Financing companies and other financial activities Listing mode Continuous Maximum number of shares to be issued 358 862 new shares Listing line 2nd line Date of the first listing 02/07/2015 Institution in charge of the registration of the operation at the Casablanca Stock Exchange BMCE Capital Bourse

V. Financial Intermediaries

The financial intermediaries involved in the context of this capital increase are as follows:

Table 1 Financial intermediaries

Financial intermediaries Designation Address Contact details

Counseling Institution & Global Coordinator BMCE Capital Conseil 63, Boulevard My Youssef,

Casablanca +212 5 22 42 91 00

Centralizing Body BMCE Bank 157, Boulevard Hassan II, Casablanca +212 5 22 49 86 34

Institution in charge of the registration of the operation at the Casablanca Stock Exchange

BMCE Capital Bourse 140, Boulevard Hassan II, Casablanca +212 5 22 48 10 01

Order-Collecting Bodies All stakeholders

Capital increase in cash

Prospectus Summary 8

PART II. OVERVIEW OF MAGHREBAIL

Capital increase in cash

Prospectus Summary 9

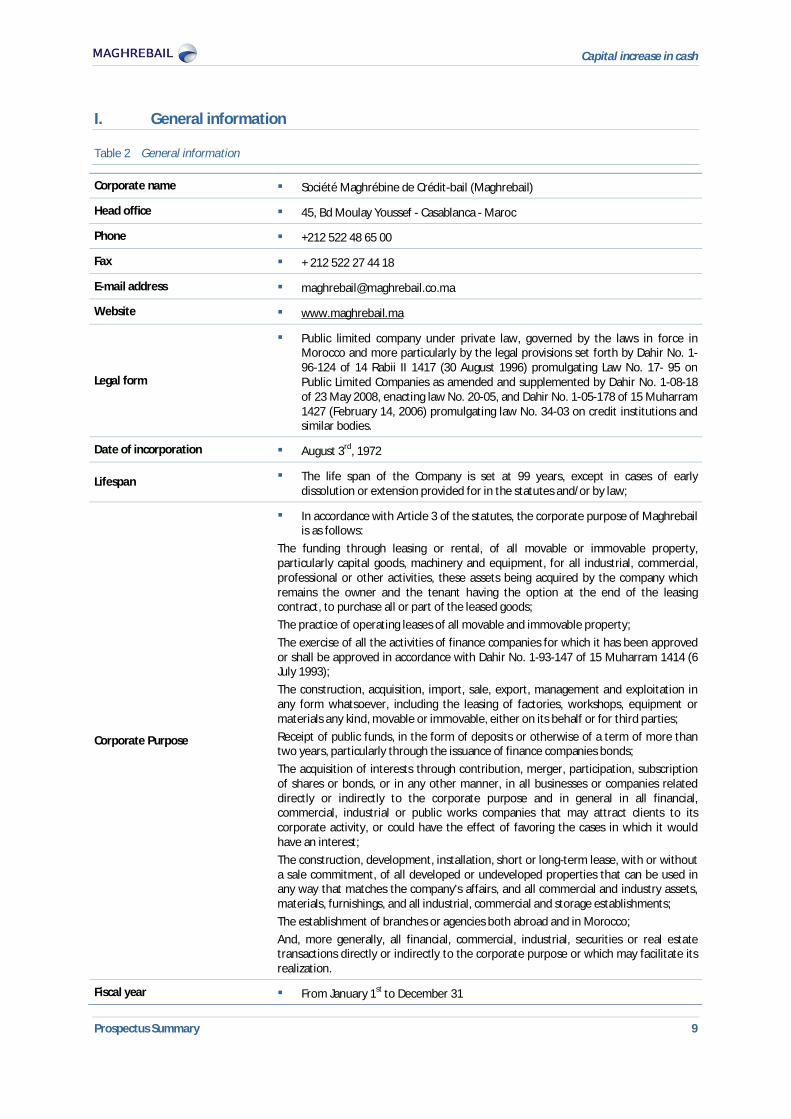

I. General information

Table 2 General information

Corporate name Société Maghrébine de Crédit-bail (Maghrebail)

Head office 45, Bd Moulay Youssef - Casablanca - Maroc

Phone +212 522 48 65 00

Fax + 212 522 27 44 18

E-mail address [email protected]

Website www.maghrebail.ma

Legal form

Public limited company under private law, governed by the laws in force in Morocco and more particularly by the legal provisions set forth by Dahir No. 1-96-124 of 14 Rabii II 1417 (30 August 1996) promulgating Law No. 17- 95 on Public Limited Companies as amended and supplemented by Dahir No. 1-08-18 of 23 May 2008, enacting law No. 20-05, and Dahir No. 1-05-178 of 15 Muharram 1427 (February 14, 2006) promulgating law No. 34-03 on credit institutions and similar bodies.

Date of incorporation August 3rd, 1972

Lifespan The life span of the Company is set at 99 years, except in cases of early dissolution or extension provided for in the statutes and/or by law;

Corporate Purpose

In accordance with Article 3 of the statutes, the corporate purpose of Maghrebail is as follows:

The funding through leasing or rental, of all movable or immovable property, particularly capital goods, machinery and equipment, for all industrial, commercial, professional or other activities, these assets being acquired by the company which remains the owner and the tenant having the option at the end of the leasing contract, to purchase all or part of the leased goods; The practice of operating leases of all movable and immovable property; The exercise of all the activities of finance companies for which it has been approved or shall be approved in accordance with Dahir No. 1-93-147 of 15 Muharram 1414 (6 July 1993); The construction, acquisition, import, sale, export, management and exploitation in any form whatsoever, including the leasing of factories, workshops, equipment or materials any kind, movable or immovable, either on its behalf or for third parties; Receipt of public funds, in the form of deposits or otherwise of a term of more than two years, particularly through the issuance of finance companies bonds; The acquisition of interests through contribution, merger, participation, subscription of shares or bonds, or in any other manner, in all businesses or companies related directly or indirectly to the corporate purpose and in general in all financial, commercial, industrial or public works companies that may attract clients to its corporate activity, or could have the effect of favoring the cases in which it would have an interest; The construction, development, installation, short or long-term lease, with or without a sale commitment, of all developed or undeveloped properties that can be used in any way that matches the company's affairs, and all commercial and industry assets, materials, furnishings, and all industrial, commercial and storage establishments; The establishment of branches or agencies both abroad and in Morocco; And, more generally, all financial, commercial, industrial, securities or real estate transactions directly or indirectly to the corporate purpose or which may facilitate its realization.

Fiscal year From January 1st to December 31

Capital increase in cash

Prospectus Summary 10

Social capital (31/12/2014) The capital amounts to 102,532,000 Dh divided into 1,025,320 shares of 100 Dh each

Premises for consulting legal documents

The statutes, minutes of General Meetings and auditors’ reports are available at the headquarters of Maghrebail: 45, Bd Moulay Youssef, Casablanca

Register of Commerce number RC 31611 in the Casablanca register of commerce

Laws and regulations applicable to the Company

By its legal form, Maghrebail is governed by the laws in force in Morocco, particularly Law No. 17-95 on Public Limited Companies as amended and supplemented by Dahir No. 1-08-18 of 23 May 2008 promulgating law No. 20-05.

By its activity, the Company is subject to: The Dahir No. 1-14-193 of 24 December 2014 promulgating the Law 103-12

on credit institutions and similar bodies; The order of the Minister of Finance and Privatization of 29/09/2006

determining the maximum conventional interest rate of credit institutions.

By the BSF issuing operation, Maghrebail is subject to all statutory and regulatory provisions relating to the financial market:

Law No. 35-94 on certain negotiable debt securities as amended and supplemented;

The Order of the Minister of Economy and Finance No. 692-00 of 25 Rabii II 1421 (28 July 2000) amending the order of Minister of Finance and foreign investments No. 2560-95 of 13 Jumada I 1416 (9 October 1995) on certain negotiable debt securities;

The circular of Bank Al Maghrib number: 3/G/96 on financing companies bonds;

CDVM Circular as amended in October 2014;

By its listing on the Casablanca Stock Exchange, the Company is subject to all statutory and regulatory provisions relating to financial markets, including:

The Dahir constituting law No. 1-93-211 of 4 rabii II 1414 (21 September 1993) on the Stock Exchange;

The General Regulations of the Stock Exchange approved by the Decree of the Minister of Economy and Finance No. 499-98 of 27 July 1998 and amended by the Decree of the Minister of Economy, Finance, Privatization and Tourism No. 1960-1901 of 30 October 2001. The later has been modified in the draft amendment of June 2004 which came into force in November 2004 and by the decree n ° 1268-1208 of 07/07 / 2008 as amended by Decree No. 30-14 of 6 January 2014;

The Dahir No. 1-07-09 of 28 rabii I 1428 (17 April 2007) promulgating Law No. 44-06 amending and supplementing Dahir promulgating Law No. 1-93-212 of 4 rabii II 1414 (21 September 1993) relating to the Conseil déontologique des valeurs mobilières and the information required from the companies making public offerings, as amended and supplemented;

The Dahir No. 1-96-246 promulgating Law No. 35-96 on the creation of a central depository and registration into account of certain securities as amended and supplemented by Law 43-02 ;

The General Regulations of the CDVM approved by Order of the Minister of Economy and Finance No. 822-08 of 7 rabii II 1429 (14 April 2008);

The general regulations of the central depository approved by Order of the Minister of Economy and Finance No. 932-98 of 16 April 1998 and amended by the Decree of the Minister of Economy, Finance, Privatization and Tourism No. 1961-1901 of 30 October 2001 and decree No. 77-05 of 17 March 2005;

Dahir No. 1-04-21 of 21 April 2004 promulgating Law No. 26-03 relating to public offerings on the stock market as amended and supplemented.

Competent court in case of litigation Commercial Court of Casablanca

Applicable taxation regime as of 31/12/2014

Maghrebail is governed by commercial and tax laws applicable for finance companies. It should be noted that according to the budget law of 2008, the

Capital increase in cash

Prospectus Summary 11

corporate tax rate applicable to leasing companies is 37% and the VAT is 20%.

Since 2012, Maghrebail must pay tax on social cohesion introduced by the budget law of 2012.

II. Information on the capital of Maghrebail

General information II.1.

The share capital of Maghrebail amounts to 102,532,000 Dh fully paid and divided into 1,025,320 shares with a nominal value of 100 Dh each.

Evolution of the social capital of Maghrebail during the last 5 years II.2.

Over the past five years, no share capital transaction has taken place in Maghrebail.

Distribution of capital on the last 3 years II.3.

The table below shows the historical Maghrebail's shareholding in the period between 2012-2014:

Table 3 Shareholding of Maghrebail 2012-2014

Shareholders

31/12/2012 31/12/2013 Just before the transaction

Number of shares

% of the capital and voting rights

Number of shares

% of the capital and voting rights

Number of shares % of the capital and voting rights

BMCE Bank 522 913 51,0% 522 913 51,0% 522 913 51,0% RMA Watanya 239 712 23,4% 236 338 23,1% 236 338 23,1% Assurances Mamda 40 950 4,0% 40 950 4,0% 40 950 4,0% Assurances MCMA 40 950 4,0% 40 950 4,0% 40 950 4,0% Other holders 180 795 17,6% 184 169 18,0% 184 169 18,0% Total 1 025 320 100,0% 1 025 320 100,0% 1 025 320 100,0%

Source : Maghrebail

It should be noted that the shares of Maghrebail held by BMCE Bank and RMA Wataniya, are not the subject of any collateral.

By the end of 2013, the number of shares held by RMA Wataniya is down to 236,338, for the benefit of other holders holding 184,169 shares.

By the end of 2014, the shareholding of Maghrebail remains the same compared to the financial year of 2013, with a registered capital of 1,025,320 shares with a par value of 100 dirhams, distributed between BMCE Bank (51.0%), RMA Wataniya (23 1%) and other shareholders.

Capital increase in cash

Prospectus Summary 12

Management II.4.

Figure 1. Organization chart of Maghrebail as of 11/03/2015

Source : Maghrebail

Customers’ NetworkDivision A

Rachid TAHER

Customers’ NetworkDivision B

Islam YAACOUBI

Finance and AccountingDivision

Sophia EL ABBADI

Production Division Ilham OUGHLA

Credit RecoveryHicham BOUZIDY

Legal Division H.CHAIBAINOU

Casa Pro Division TPE R. TAHER

CORPORATE Division I. YAACOUBI

CASA EISES Division A. KHODAIRI

B South R. QUASM

BR South-central T. EL IDRISSI

BR Eastern

BR K.BENBOUAZZA M. AASSILA

B North A. LAMRABET

BR Center Y. ELBOUDA

FinancingDivision

CBI R. TAHER

MarketingControl

Accounting Management R. ANEDDAM

Treasury

Financial andRegulatory

CommunicationDepartment H. FAKHIR

Operating DepartmentM. AACHIBAT

Invoicing and ContractManagement

S. FILALI

Mutual AgreementCredit Recovery Dept.

Hamid FARKH

Contentious CreditRecovery Dept.

H. BOUZIDI

Consulting and LegalProceedings Dept.

J. BOUAZIZ

REL performance Dept. H. CHAIBAINOU

Chief executive officerAzeddine GUESSOUS

Credit Risk ManagerYasmina FACHTAG

Internal Control andCompliance

Hicham BENSLIMANE Managing Director

Reda DAIFI Permanent Control

DepartmentImane HAMDI

TPD OrganizationControl

Driss SOUIBA Administration and

LogisticsHabiba EL ALAOUI

IT Administration Khalid AYOUJIL

DPT Infrastructures etServices

K. AYOUJIL

Database and IB Dept.M. DANY

Human ResourcesManagement

Habiba EL ALAOUI

LogisticsYoussef HERMANI

Business DevelopmentDivision

Hicham KHANEBOUBI

Finance and Productiondivision

Ilham OUGHLA

Legal and CreditRecovery Division

Hassan CHAIBAINOU

Capital increase in cash

Prospectus Summary 13

PART III. BUSINESS, MARKET AND COMPETITION

Capital increase in cash

Prospectus Summary 14

I. Business of Maghrebail

Presentation of products I.1.

Maghrebail offers a wide range of products for both businesses and professionals:

Movables or Equipment Leasing (ML): provides funding for various movable properties such as office furniture, computer equipment, etc.

Real estate leasing "Immobail" (REL): is a property lease contract for professional use, with an average duration of 10 years. At the end of the contract, the lessor has the possibility of becoming owner of the property upon payment of the residual value.

Evolution of Maghrebail’s market share on the basis of net book value I.2.

Table 4 Maghrebail’s market share on the basis of net book value

In MDh 2012 2013 Var.% 2014 Var.%

Maghrebail1 book value 8 410 8 880 5,6% 9 552 7,5%

Sector book value 40 857 41 318 1,1% 41 845 1,3%

Maghrebail Market Share 20,6% 21,5% 0,9pts 22,8% 1,3pts

Source : Maghrebail

The net book value of Maghrebail reached 8 880 MDh in 2013 compared to 8 410 MDh in 2012 i.e. an evolution of 5.6% over the period of 2012-2013. In 2014, Maghrebail went on strengthening its market share, which stood at 22.8%, i.e. 1.3 basis points compared to 2013.

Maghrebail remains in third place with net assets that increased by 7.5% while the sector book value increases by 1.3% to reach 41 845 MDh in 2014.

The breakdown of the net outstanding of Maghrebail is as follows:

Table 5 Breakdown of the net outstanding between Movables Leasing (ML) and Real-estate Leasing (REL)

In MDh 2012 Percentage 2013 Percentage 2014 Percentage

Net outstanding ML of Magherbail 5 101 60,7% 5 312 59,8% 5 521 57,8%

Net outstanding REL of Maghrebail 3 309 39,3% 3 568 40,2% 4 031 42,2%

Net book total outstanding of Maghrebail 8 410 100,0% 8 880 100,0% 9 552 100,0%

Source : Maghrebail

The ML net book outstanding represents 57.8% of the net total outstanding at the end of 2014 (compared to 59.8% in 2013 and 60.7% in 2012), while the net outstanding REL represents 42.2% of the total outstanding (compared to 40.2% in 2013 and 39.3% in 2012). It should be noted that the share of the REL activity in the overall outstanding is growing steadily over the studied period.

1 The net book outstanding of Maghrebail does not include unpaid and accrued rent receivables.

Capital increase in cash

Prospectus Summary 15

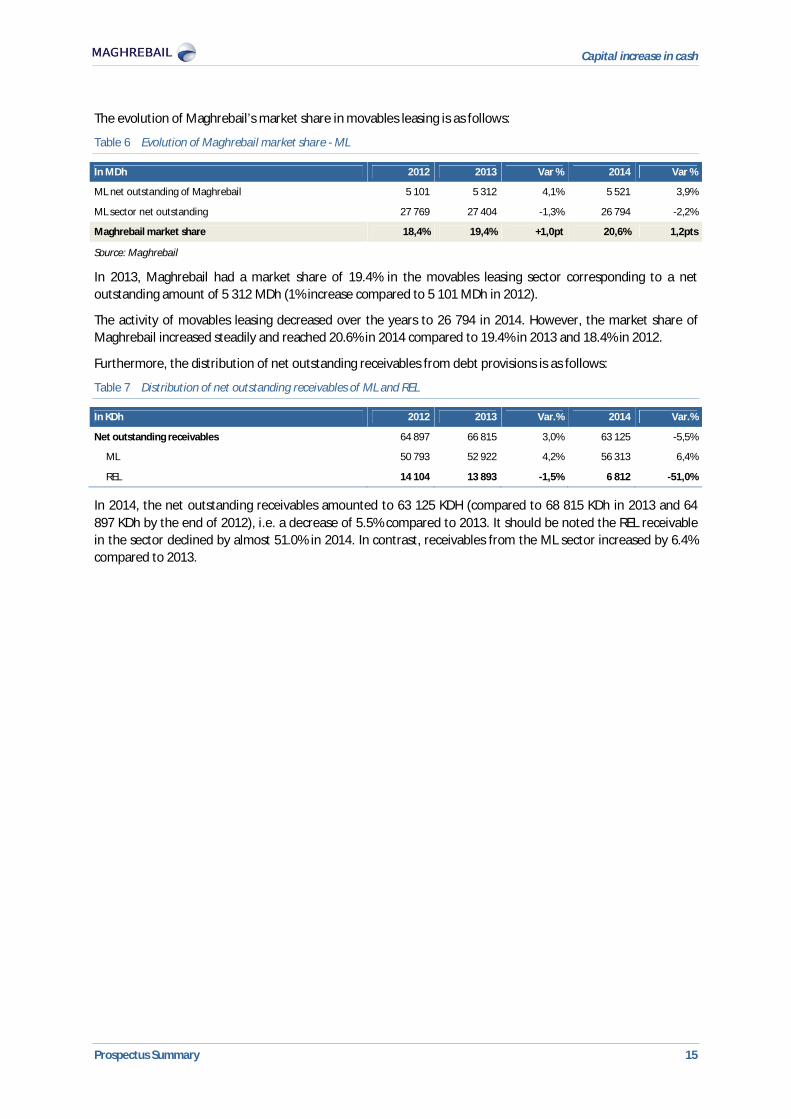

The evolution of Maghrebail’s market share in movables leasing is as follows:

Table 6 Evolution of Maghrebail market share - ML

In MDh 2012 2013 Var % 2014 Var %

ML net outstanding of Maghrebail 5 101 5 312 4,1% 5 521 3,9%

ML sector net outstanding 27 769 27 404 -1,3% 26 794 -2,2%

Maghrebail market share 18,4% 19,4% +1,0pt 20,6% 1,2pts

Source: Maghrebail

In 2013, Maghrebail had a market share of 19.4% in the movables leasing sector corresponding to a net outstanding amount of 5 312 MDh (1% increase compared to 5 101 MDh in 2012).

The activity of movables leasing decreased over the years to 26 794 in 2014. However, the market share of Maghrebail increased steadily and reached 20.6% in 2014 compared to 19.4% in 2013 and 18.4% in 2012.

Furthermore, the distribution of net outstanding receivables from debt provisions is as follows:

Table 7 Distribution of net outstanding receivables of ML and REL

In KDh 2012 2013 Var.% 2014 Var.%

Net outstanding receivables 64 897 66 815 3,0% 63 125 -5,5%

ML 50 793 52 922 4,2% 56 313 6,4%

REL 14 104 13 893 -1,5% 6 812 -51,0%

In 2014, the net outstanding receivables amounted to 63 125 KDH (compared to 68 815 KDh in 2013 and 64 897 KDh by the end of 2012), i.e. a decrease of 5.5% compared to 2013. It should be noted the REL receivable in the sector declined by almost 51.0% in 2014. In contrast, receivables from the ML sector increased by 6.4% compared to 2013.

Capital increase in cash

Prospectus Summary 16

Table 8 Evolution of the market share of Magherbail - REL

In MDh 2012 2013 Var % 2014 Var %

Maghrebail REL net outstanding 3 309 3 568 7,8% 4 031 13,0%

REL sector net outstanding 13 089 13 914 6,3% 15 051 8,2%

Maghrebail market share 25,3% 25,6% +0,3pt 26,8% 1,1pts

Source: Maghrebail

Maghrebail market share is gradually increasing over the period 2012-2014 to reach 4 031 MDh in 2014, i.e. an increase of 13.0% compared to 2013. It should be noted that the activity of the Real Estate Leasing is growing in its entirety. In fact, the REL sector net assets amounted to 15 051 representing an increase of 8.2% compared to 2013.

Furthermore, the breakdown of net book outstanding of Maghrebail is as follows:

Table 9 Sectorial breakdown of the net book outstanding of Maghrebail between 2012-2014

Business sector 2012 % 2013 % 2014 %

Services 3 684 43,8% 3 855 43,4% 4 308 45,1%

Business & retail 1 248 14,8% 1 434 16,2% 1 497 15,7%

Transport 661 7,9% 793 8,9% 958 10,0%

Miscellaneous 53 0,6% 49 0,6% 44 0,5%

Tertiary sector 5 646 67,1% 6 131 69,0% 6 807 71,3%

IMME 308 3,7% 193 2,2% 542 5,7%

Chemical and Para chemical industry 422 5,0% 576 6,5% 205 2,1%

Agri-food 536 6,4% 180 2,0% 526 5,5%

Textiles - leather - tannery 199 2,4% 546 6,1% 206 2,2%

Plastics & Rubber 81 1,0% 112 1,3% 109 1,1%

Paper and cardboard 110 1,3% 109 1,2% 139 1,5%

Industrial sector 1 656 19,7% 1 719 19,4% 1 727 18,1%

Construction - civil engineering 726 8,6% 746 8,4% 754 7,9%

Mining and drilling, construction materials 381 4,5% 282 3,2% 264 2,8%

Construction and energy sectors 1 107 13,2% 1 029 11,6% 1 018 10,7%

Total 8 410 100,0% 8 880 100,0% 9 552 100,0%

Source: Maghrebail

With regard to 2013, Tertiary sector represents 69.0% of the net book outstanding of Maghrebail, which means a 1.9pts increase compared to 2012. Industry is in second place with a share of 19.4% compared to 19.7% in 2012. Concerning the sectors of construction - civil engineering and Mining - drilling, their share is 11.6% of the total outstanding, i.e. a 1.6 pts decrease compared to 2012.

The tertiary sector continued to grow in 2014 to reach 6,807 MDh i.e. 71.3% of total net outstanding. However, the shares of other sectors in the total net outstanding are on a downtrend, particularly the industrial sector, whose share decreased from 19.4% to 18.1%.

Capital increase in cash

Prospectus Summary 17

Evolution of Maghrebail production I.3.

I.3.1. Evolution of Maghrebail production

Table 10 Evolution of Maghrebail market share between 2012 and 2014 - Production

in MDh 2012 2013 Var % 2014 Var %

Production of Maghrebail 2 719 2 769 1,8% 3 058 10,4%

Total Production 13 604 12 860 -5,5% 12 910 0,4%

Maghrebail market share 20,0% 21,5% 1,5 pts 23,7% 2,2 pts

Source: Maghrebail

In 2014, production evolved by 10.4% from 2013, averaging at 23.7% of the market (compared to 21.5% in 2013 and 20.0% in 2012).

Table 11 Evolution of Maghrebail production between 2012-2014

2012 2013 Var.% 2014 Var.%

ML

Completed projects 2 409 2 613 8,5% 2 622 0,3%

Amount (in MDh) 2 118 2 111 -0,3% 2 107 -0,2%

REL Completed projects 63 81 28,6% 94 16,0%

Amount (in MDh) 601 659 9,7% 951 44,3%

TOTAL Completed projects 2 472 2 694 9,0% 2 716 0,8%

Amount (in MDh) 2 719 2 769 1,8% 3 058 10,4%

Source: Maghrebail

In 2013, Maghrebail production amounted to 2 769 MDh, i.e. an increase of 1.8% compared to 2012. With the decline recorded in movables industry, production of Maghrebail was driven by amounts realized in real estate sector that increased from 601 MDh to 659 MDh, i.e. an increase of 9.7%, in line with the evolution of the number of completed projects amounting to 81 by the end of 2013.

In 2014, Maghrebail production totaled at 3 058 MDh. The production registered an evolution of 10.4% compared to 2013 mainly due to the amounts realized in real estate that increased from 659 MDh to 951 MDh, i.e. an increase of 44.3%.

By business segments, big businesses represent 58% of the production in 2014, compared to 29% for SMEs and 13% for the SOHO and professionals.

The near stagnation of ML financing at the end of 2014 is in line with the trend of Maghrebail ML sector, whose production was also down at the end of 2014.

Capital increase in cash

Prospectus Summary 18

Evolution of Maghrebail Movables Leasing (ML) market performance I.4.

Table 12 Compared market performance by 31/12/2014 – ML

2012 2013 Var. % 2014 Var. %

Approved transactions2 Number 2 836 3 006 6,0% 3 086 2,7%

Amount (in MDh) 2 690 2 629 -2,3% 2 474 -5,9%

Signed contracts3 Number 2 432 2 630 8,1% 2 638 0,3%

Amount (in MDh) 2 229 2 189 -1,8% 2 226 1,7%

Transactions carried out 4

Number 2 409 2 613 8,5% 2 622 0,3%

Amount (in MDh) 2 118 2 111 -0,3% 2 107 -0,2%

Source: Maghrebail

In 2013, operations approved in the movables leasing segment were up 6.0% and totaled at 3 006 cases. However, the amounts related to these transactions were down 2.3% with 2 629 MDh. The trend is the same for contracts signed. In fact, while the number of contracts signed rose by 8.1% at 2 630 units, the amounts contracted by 1.8% at 2 189 MDh. It is the same for the operations carried out. The latters, are up 8.5%, while the amounts relating thereto fell by 0.3% at 2 111 MDh.

In 2014, the number of approved movables leasing transactions rose by 2.7% reaching a total of 3 086 MDh. The number of contracts signed increased by 0.3% i.e. 2 638 contracts for the amount of 2 226 MDh (i.e., an increase of 1.7% compared to 2013). In terms of realized transactions, new acquisitions registered an increase of 0.3% compared to 2013, with 2 107 MDh.

Table 13 Distribution Maghrebail ML performance by type of equipment

In MDh 2012 % 2013 % 2014 %

Industrial machinery and equipment 751 35,5% 732 34,7% 783 37,2%

Computer and office equipment 218 10,3% 139 6,6% 95 4,5%

Utility vehicles 548 25,9% 547 25,9% 464 22,0%

Passenger vehicles 347 16,4% 382 18,1% 411 19,5%

Construction Equipment 229 10,8% 290 13,8% 302 14,3%

Miscellaneous 25 1,2% 19 0,9% 52 2,5%

Total 2 118 100,0% 2 109 100,0% 2 107 100,0%

Source: Maghrebail

In line with the decline in production in the ML sector in 2013, acquisitions of industrial machinery and equipment fell by 2.5% to reach 732 MDh and account for 34.7% of the total ML performance of Maghrebail. The ML segment is strongly impacted by the lower performance of computer and office equipment sector that fell by 36.2% to reach 139 MDh in 2013. Moreover, the decline in production of the ML sector is mitigated by the good performance of the construction segment that increased by 26.6% to reach 290 MDh, contributing with 13.8% in the total performance of the ML sector for the fiscal year of 2013.

2 Approved operations include all files submitted and approved by the committee. After the approval, the contract is sent to the customer

for their signature.

3 An operation is considered signed when contracts are returned signed by the client. In some cases, sent files yield no results and contracts

are not returned signed.

4 The transactions carried out are contracts that entitled their signees to get a loan over the course of each financial year.

Capital increase in cash

Prospectus Summary 19

In 2014, purchases of industrial machinery and equipment represented 37.2% of the total performance of movables leasing sector, i.e. a production up to 783 MDh. Utility vehicles, computer and office equipment, respectively fell to 2.1 and 3.9 basis points compared to 2013. Passenger vehicles as well as construction activities managed to get a bigger share of the total performance of Maghrebail’s LM sector.

In the breakdown of the overall production by type of property, land and constructions take the lead with 31.1% of the total performance, they are closely followed by machinery and industrial equipment 25.6%, utility vehicles take the third place with 15.2%, followed by passenger vehicles with 13.4% of the output by the end of 2014, and finally the construction machines represent 9.8% of the total performance.

I.4.1. Evolution of the Real Estate Leasing activity (REL) of Maghrebail market performance

Table 14 Compared market performance by 31/12/2014 – REL

2012 2013 Var. % 2014 Var. %

Approved transactions Number 92 105 14,1% 121 15,2%

Amount (in MDh) 1 263 896 -29,1% 1 302 45,3%

Signed contracts

Number 57 68 19,3% 91 33,8%

Amount (in MDh) 642 802 24,9% 1 150 43,4%

Transactions carried out *

Number 63 81 28,6% 94 16,0%

Amount (in MDh) 601 658 9,5% 951 44,5%

Source: Maghrebail – (*) takes into account contracts signed in n-1

In 2013, the number of approved transactions increased by 14,1% i.e. 105 cases, totaling a decline of 29.1% to reach 896 MDh. It should be noted that the number of signed contracts rose by 19.3% to reach 68 and the amounts relating thereto amounted to 802 MDh, with a 24.9%. The number of transactions rose by 28.6% with 81 cases for an amount of 658 MDh by late 2013.

In 2014, the number of approved operations regarding the Real Estate Leasing sector grew by 15.2% i.e. 121 cases for an amount of 1 302 MDh. It should be noted that signed contracts rose by 33.8% totaling at 1 150 MDh. In line with the signed contracts, the operations carried out are increasing both in volume and value. In fact, the number transactions carried out increased by 16.0% compared to 2013 for a total of 94 cases by the end of 2014 representing 951 MDh compared to 658 MDh in 2013.

Table 15 Distribution of Maghrebail REL performance by type of buildings

In MDh 2012 % 2013 % 2014 %

Industrial Buildings 44 7,3% 62 9,4% 133 14,0%

Stores 137 22,8% 311 47,3% 86 9,0%

Office spaces 140 23,3% 226 34,3% 502 52,8%

Hotels and Leisure 78 13,0% 0 0,0% 133 14,0%

Miscellaneous 202 33,6% 59 9,0% 97 10,2%

Total 601 100,0% 658 100,0% 951 100,0%

Source: Maghrebail

The fiscal year of 2013 ended with an important contribution from the funding of shops in the total REL performance of Maghrebail. In fact, it takes 47.3% of the total performance amounting to 311 MDh (compared to 137 MDh in 2012). Office spaces contributed with 34.3% (compared to 23.3% in 2012) of total REL performance (i.e. 226 MDh).

Capital increase in cash

Prospectus Summary 20

In 2014, the share allocated to the financing of industrial buildings increased by 5.4 points and stood at 14.0%. The respective shares of shops, office spaces and hotels moved respectively from 22.8%, 23.3% and 13.0% in 2012 to 9.0%, 52.8% and 14.0% in 2014. It should be noted that the office spaces have experienced the largest increase in 2014.

On an additional note, the Audit Committee proposed to the Board of Management on 28/03/2012 that the limits on office spaces and commercial premises have to be increased, recommending a very careful case by case monitoring of the financing of office spaces whose offer will consequently increase with the CFC project. Furthermore, the Committee recommended extreme caution in the new funding of any hotel establishment. These recommendations partly justify the evolution of the distribution of the REL production by property type over the studied period.

Capital increase in cash

Prospectus Summary 21

PART IV. FINANCIAL SITUATION OF MAGHREBAIL

Capital increase in cash

Prospectus Summary 22

Presentation of management balances I.1.

The following table shows the management balances of Maghrebail for the period 2012-2014:

Table 16 Statement of management balances

In KDh 2012 2013 Var. % 2014 Var. % Interests and similar revenues 722 590 -18,2% 810 37,3% Interests and similar expenses 336 846 364 536 8,2% 382 194 4,8%

Interest Margin -336 125 -363 946 -8,3% -381 384 -4,8%

Income from leased property 2 576 711 2 768 892 7,5% 2 820 252 1,9% Expenses on leased property 2 039 364 2 148 453 5,3% 2 197 831 2,3%

Income from leasing transactions 537 346 620 439 15,5% 622 421 0,3%

Commission margin -4 176 -3 093 25,9% -2 275 -26,4%

Other banking income 2 647 1 870 -29,4% 1 142 -39,0% Other banking expenses 58 83 44,3% 112 34,8% Net banking income 199 635 255 188 27,8% 239 791 -6,0% Results from equity investments - - - - - Other operating income 2 682 3 816 42,3% 2 019 -47,1% Other operating expenses 3 385 1 836 -45,8% 1 029 -44,0% General operating expenses 61 658 61 704 0,1% 64 857 5,1% Gross operating income 137 273 195 464 42,4% 175 925 -10,0% Allocations net of reversals on provisions to cover non performing loans and commitments by signature 66 099 68 761 4,0% 59 328 -13,7%

Other allocations net of reversals on provisions -13 000 12 000 n/s 2 000 -83,3% Current income 84 174 114 703 36,3% 114 597 -0,1%

Non-current income -4 724 371 n/s 4 133 n/s Corporate tax 25 758 48 389 87,9% 46 352 -4,2% Net income 53 693 66 685 24,2% 72 377 8,5% Source : Maghrebail

Capital increase in cash

Prospectus Summary 23

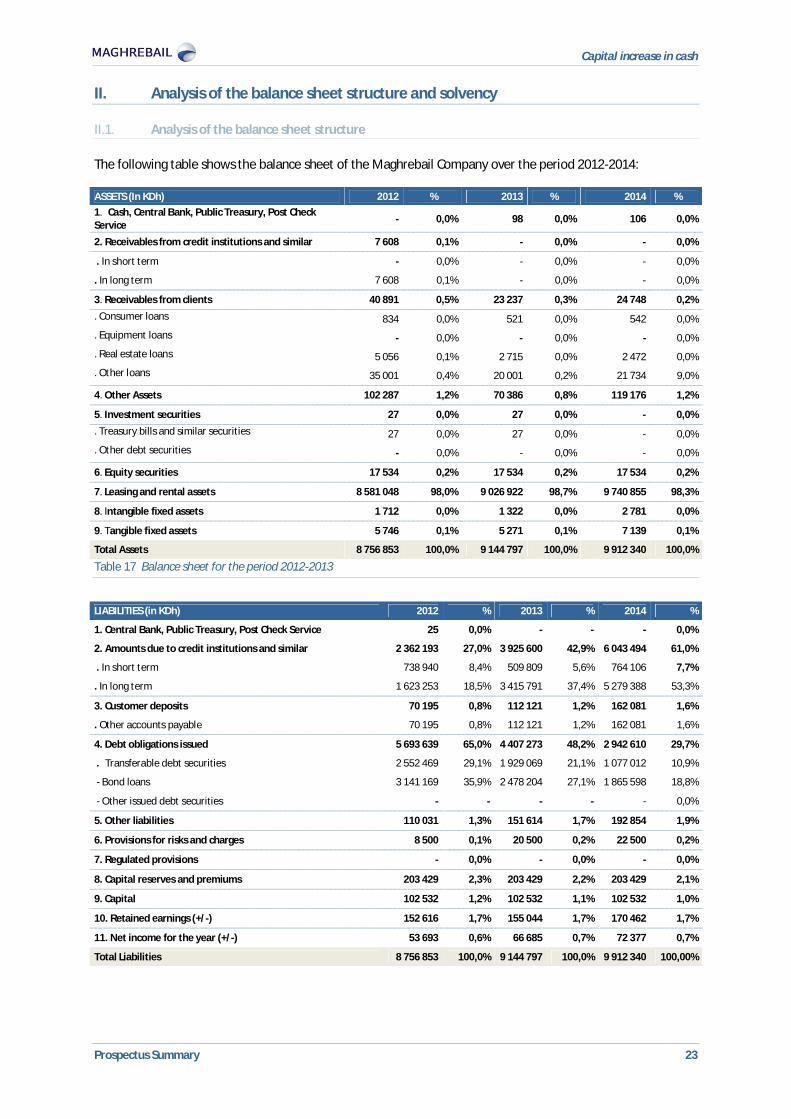

II. Analysis of the balance sheet structure and solvency

Analysis of the balance sheet structure II.1.

The following table shows the balance sheet of the Maghrebail Company over the period 2012-2014:

Table 17 Balance sheet for the period 2012-2013

LIABILITIES (in KDh) 2012 % 2013 % 2014 %

1. Central Bank, Public Treasury, Post Check Service 25 0,0% - - - 0,0%

2. Amounts due to credit institutions and similar 2 362 193 27,0% 3 925 600 42,9% 6 043 494 61,0%

. In short term 738 940 8,4% 509 809 5,6% 764 106 7,7%

. In long term 1 623 253 18,5% 3 415 791 37,4% 5 279 388 53,3%

3. Customer deposits 70 195 0,8% 112 121 1,2% 162 081 1,6%

. Other accounts payable 70 195 0,8% 112 121 1,2% 162 081 1,6%

4. Debt obligations issued 5 693 639 65,0% 4 407 273 48,2% 2 942 610 29,7%

. Transferable debt securities 2 552 469 29,1% 1 929 069 21,1% 1 077 012 10,9%

- Bond loans 3 141 169 35,9% 2 478 204 27,1% 1 865 598 18,8%

- Other issued debt securities - - - - - 0,0%

5. Other liabilities 110 031 1,3% 151 614 1,7% 192 854 1,9%

6. Provisions for risks and charges 8 500 0,1% 20 500 0,2% 22 500 0,2%

7. Regulated provisions - 0,0% - 0,0% - 0,0%

8. Capital reserves and premiums 203 429 2,3% 203 429 2,2% 203 429 2,1%

9. Capital 102 532 1,2% 102 532 1,1% 102 532 1,0%

10. Retained earnings (+/-) 152 616 1,7% 155 044 1,7% 170 462 1,7%

11. Net income for the year (+/-) 53 693 0,6% 66 685 0,7% 72 377 0,7%

Total Liabilities 8 756 853 100,0% 9 144 797 100,0% 9 912 340 100,00%

ASSETS (In KDh) 2012 % 2013 % 2014 % 1. Cash, Central Bank, Public Treasury, Post Check Service - 0,0% 98 0,0% 106 0,0%

2. Receivables from credit institutions and similar 7 608 0,1% - 0,0% - 0,0%

. In short term - 0,0% - 0,0% - 0,0%

. In long term 7 608 0,1% - 0,0% - 0,0%

3. Receivables from clients 40 891 0,5% 23 237 0,3% 24 748 0,2% . Consumer loans 834 0,0% 521 0,0% 542 0,0% . Equipment loans - 0,0% - 0,0% - 0,0% . Real estate loans 5 056 0,1% 2 715 0,0% 2 472 0,0% . Other loans 35 001 0,4% 20 001 0,2% 21 734 9,0%

4. Other Assets 102 287 1,2% 70 386 0,8% 119 176 1,2%

5. Investment securities 27 0,0% 27 0,0% - 0,0% . Treasury bills and similar securities 27 0,0% 27 0,0% - 0,0% . Other debt securities - 0,0% - 0,0% - 0,0%

6. Equity securities 17 534 0,2% 17 534 0,2% 17 534 0,2%

7. Leasing and rental assets 8 581 048 98,0% 9 026 922 98,7% 9 740 855 98,3%

8. Intangible fixed assets 1 712 0,0% 1 322 0,0% 2 781 0,0%

9. Tangible fixed assets 5 746 0,1% 5 271 0,1% 7 139 0,1%

Total Assets 8 756 853 100,0% 9 144 797 100,0% 9 912 340 100,0%

Capital increase in cash

Prospectus Summary 24

PART V. RISK FACTORS

Capital increase in cash

Prospectus Summary 25

I. Client related risks

Maghrebail implemented systems ensuring the knowledge and rating of customers that allows to control the risk:

Better assessment of credit risk by the risk department prior to the approval of the credit committee;

Customers and transactions rating device;

Collective decision-making of the credit committee;

Compliance with the set limits by sector and by type of material established by the Board of Management;

Credit risk exposures reporting by nature of asset, customer segment...

Review of the loss ratio;

Review of risk division ratios.

Furthermore, the implementation of the scoring tool for the SOHOs will be implemented jointly with the BMCE during the first semester of 2015.

Maghrebail does not possess stress test to test the company's level of resistance, following an economic downturn and deterioration in the quality of the counterparty.

II. Market related risks

The solvency ratio called "Mc Donough", introduced by the Basel II agreements, takes into account other types of risks other than credit risk, i.e. the market risk and operational risk.

Market risk is the risk of loss or devaluation of positions taken by the Company as a result of changes in prices or rates on the market. This risk applies to the following instruments: interest rate products (bonds, interest rate derivatives), equities, currencies and commodities.

The risk on fixed-income and equity is measured based on the "trading portfolio", that is to say, the positions held by the bank for its own account in an objective of short-term gain, as opposed to "normal" financing and investment activities. However, the capital required to cover positions in foreign exchange and commodities applies to all of these positions.

In 2014, Maghrebail’s solvency ratio stood at 10.3%, well below the regulatory solvency ratio of 12%. The transaction, subject of the present prospectus, aims to strengthen the capital of Maghrebail in order to meet the regulatory solvency ratio.

III. Operating risk

As a credit institution, Maghrebail is exposed to operating risk. In fact, Basel II defines operational risk as the direct or indirect losses due to inadequacy or failure of procedures (absent or incomplete test or control, insecure procedure, etc.), personnel (error, malicious acts or fraud) and internal systems (computer failure) or external (flood, fire, etc.). This definition also includes legal risk.

In order to manage this risk, Maghrebail has a strong internal control system. The Company has an Audit and Internal Control Committee whose role is to minimize financial, operational or non-compliance risks of the Company and increase the quality of published financial information. Thus, the entire Maghrebail internal control system complies with the directives of Bank Al Maghrib.

In 2010, the Board of Directors of Maghrebail decided to keep outsourcing the internal audit function under the supervision of General Management of the Company and appoint Fidaroc Grand Thornton as internal auditor starting from the fiscal year of 2011.

It should be noted that according to the internal audit report (2nd half of 2014), the risk map highlights the gross risks only and the rating of the level of control without ruling on the net risks.

Capital increase in cash

Prospectus Summary 26

IV. Risk of changes in interest rates

Like all credit institutions, Maghrebail is exposed to the risk of changes in the MCIR (maximum conventional interest rate). This rate caps Maghrebail’s output rates and therefore determines its margin. However, it is less exposed to changes to lower MCIR given the fact that its output rates are well below the maximum MCIR.

Moreover, a decrease in this rate promotes prepayment that allows customers to benefit from a new loan at a more attractive interest rates. Moreover, prepayment is originally a mechanical decrease in the average output rate and a shift in the backing of jobs and resources. It should be noted that the practice of prepayment remains minor due to additional cost it entails which makes it not profitable for the customer.

For the period from April 1st, 2014 to March 31, 2015, the said rate was set at 14.39%.

V. Risk of backing use to the supply

With regard to the nature of their activity, credit companies are required to back their use to the resources having substantially similar characteristics in terms of duration. Maghrebail meets this requirement by diversifying its sources of funding (use of BSF, bonds, bank loans, etc.).

Moreover, Maghrebail maintains an active watch on market conditions to improve its intermediation margin.

VI. Competition risks

The leasing sector in Morocco is now experiencing a trend towards concentration, giving rise to specialized groups, with bigger size and enjoying a leading position in the market. Thus, in 2009, Chaabi leasing and Maroc Leasing companies merged forming a reference group in the leasing sector in Morocco with a combined market share of 25.9% in 2012 in terms of production, thus taking the second place after Wafabail which holds a 27.2% market share and is positioning itself as a leader in the same year. This trend continues in 2013, Maroc Leasing occupying the second position with a market share of 23.3% in terms of production and Wafabail in the first place with a market share of 29.5%. In 2014, Maghrebail is second with 23.7% market share in terms of production followed by Maroc Leasing, which holds 20.8% over the same period. Wafabail retains its leading position with 29.9% market share in 2014.

In the movables leasing segment, Maghrebail held the second place in 2014 with a 21.6% market share behind Wafabail with 30.9%.

In the segment of real estate leasing, Maghrebail held the leading position in 2014 with a 30.1% market share followed by Wafabail and Maroc Leasing with 27.1% and 21.9% respectively.

Given this concentration of Real Estate Leasing business in Morocco and the risk of loss of "leadership", Maghrebail is strengthening its position in the market through a "customer" and "service” oriented strategy. This strategy aims to safeguard the position of the company on the market and even to gain more market shares in the movables and real estate leasing segments.

Capital increase in cash

Prospectus Summary 27

VII. Regulatory risks

As a finance company operating in the movables and real estate leasing, Maghrebail is subject to current regulations enforced by Bank Al Maghrib, particularly in relation to compliance with prudential standards.

Given the constant evolution of the movables and real estate leasing sectors in Morocco and the national and international economic conditions, Bank Al Maghrib authorities may consider a tightening of regulations in force that may influence the strategy and mode of operation of all operators. This tightening of regulations could intervene to protect and further structure the movables and real estate leasing sectors in Morocco. Faced with such regulatory risks which would affect all national operators, Maghrebail undertakes to implement the necessary and sufficient measures to meet the new criteria imposed while minimizing potential negative impacts on the profitability of the business and maintaining its position in the movables and real estate leasing sectors in Morocco.

Capital increase in cash

Prospectus Summary 28

Disclaimer

The abovementioned information constitute only a part of the Prospectus approved by the Conseil Déontologique des Valeurs Mobilières (CDVM) under reference No. n° VI/EM/008/2015 on 12th may 2015. The CDVM recommends the reading of the full Prospectus made available for the public in French.