Embed Size (px)

Citation preview

Advanced Electric Vehicle Architectures

Collaborative Project

Grant Agreement Number 265898

Deliverable D1.1

Societal scenarios and available technologies for electric vehicle architectures in 2020

Confidentiality level: Public

Status: Final

Executive Summary The objective of WP1 of ELVA is to provide the framework to develop the different vehicle

concepts in WP2 and WP3. For this purpose a review of existing future societal and

technological developments has been carried out in WP 1.1. The results of this review are

reported in this deliverable.

The review is divided into two parts:

A review of European and global roadmaps, strategy papers etc. for future road

transport in order to identify the main drivers and trends in our society with relation to

future traffic and vehicle concepts

An analysis of the state-of-the art and future trends of the vehicle technology and

standards concerning lightweight and functional materials, lightweight vehicle

architectures, electromagnetic compatibility, structural electric storage systems,

electric drive train technology, brake system technology as well as active and passive

safety

Preliminary findings of the review have been presented and discussed during a workshop

attended by ELVA partners, members of the Advisory Board as well as other stakeholders.

The feedback received during this workshop is incorporated in this report.

Deliverable D1.1

ELVA 2 SCP0-GA-2010-265898

Document Name

ELVA-110331-D11-V10-FINAL

Version Chart

Version Date Comment

0.1 7 April 2011 First draft version

0.2 11 April 2011 Updated version for review by all partners

1.0 28 April 2011 Final version

Authors

The following participants contributed to this deliverable:

Name Company Chapters

J. Wismans SAFER/Chalmers all

E.-M. Malmek SAFER/Chalmers 2

C. Karlsson SAFER/SP 4

N. Depner, M. Funcke, L. Ickert IKA 3, 7

M. Lesemann IKA all

B. Bayer, W. Schindler Continental 5, 6

G. Monfrino CRF all

M. Petiot Renault 5, 6

C. Ntchouzou VW 3

Coordinator

Dipl.-Ing. Micha Lesemann

RWTH Aachen University – Institut für Kraftfahrzeuge

Steinbachstraße 7 – 52074 Aachen – Germany

Phone +49 241 80 27535

Fax +49 241 80 22147

E-mail [email protected]

Copyright

© ELVA Consortium 2011

Deliverable D1.1

ELVA 3 SCP0-GA-2010-265898

Table of Contents

1 Introduction .................................................................................................................... 7

2 Driving forces and societal scenarios ............................................................................. 8

2.1 Introduction .............................................................................................................. 8

2.2 Scenarios ................................................................................................................ 9

2.3 Main driving forces ................................................................................................. 11

2.3.1 Environment and economy ................................................................................. 11

2.3.1.1 Economic growth......................................................................................... 12

2.3.1.2 Energy and resources ................................................................................. 16

2.3.1.3 Climate Change .......................................................................................... 20

2.3.1.4 Sustainability matters .................................................................................. 21

2.3.1.5 Efficiency – downsizing ............................................................................... 21

2.3.1.6 Business models ......................................................................................... 23

2.3.2 Society & Culture ............................................................................................... 23

2.3.2.1 Population Growth ....................................................................................... 23

2.3.2.2 Urbanisation ................................................................................................ 24

2.3.2.3 Values, attitudes and lifestyle ...................................................................... 24

2.3.2.4 Demand on cities ........................................................................................ 25

2.3.2.5 Demand on mobility solutions ..................................................................... 25

2.3.3 Public Policies and market trends ...................................................................... 26

2.4 Trends in the market for xEVs ............................................................................... 27

2.5 Discussions and conclusions ................................................................................. 32

3 Light weight material concepts and vehicle architectures ............................................. 34

3.1 Introduction ............................................................................................................ 34

3.2 Body in white material concepts and architectures................................................. 34

3.2.1 State of the Art ................................................................................................... 35

3.2.1.1 Large volume: Shell construction ................................................................ 35

3.2.1.2 Midsize and small volume: Aluminium space frame .................................... 36

3.2.1.3 High performance cars: Small volume with monocoque .............................. 37

3.2.2 Future trends beyond 2020 ................................................................................ 38

3.2.2.1 Large series ................................................................................................ 38

3.2.2.2 Midsize volume and small volume ............................................................... 39

Deliverable D1.1

ELVA 4 SCP0-GA-2010-265898

3.2.3 Summary ............................................................................................................ 41

3.2.4 Integration of the battery system ........................................................................ 42

3.2.5 Further future body concepts for weight reduction and functional integration ..... 43

3.3 Chassis material concepts ..................................................................................... 44

3.4 Interior material concepts ....................................................................................... 45

3.5 Conclusion ............................................................................................................. 46

4 State-of-the-art and outlook EMC ................................................................................ 48

4.1 Introduction to EMC and EMF ................................................................................ 48

4.2 State of the Art ....................................................................................................... 48

4.2.1 Overview of existing EMC standards .................................................................. 48

4.2.1.1 ISO ............................................................................................................. 49

4.2.1.2 IEC/CISPR .................................................................................................. 49

4.2.1.3 OEM standards ........................................................................................... 50

4.2.2 Electromagnetic Fields (EMF) ............................................................................ 50

4.2.2.1 Directives and ICNIRP ................................................................................ 50

4.3 General technology outlook up to 2030+................................................................ 51

4.3.1 EMC ................................................................................................................... 51

4.3.1.1 EMC test in charging phase ........................................................................ 51

4.3.1.2 Conducted EMC for power electronics ........................................................ 51

4.3.1.3 Magnetic fields ............................................................................................ 51

4.3.1.4 Composites and plastics ............................................................................. 51

4.3.1.5 Wireless inductive charging ......................................................................... 51

4.3.2 EMF ................................................................................................................... 52

4.3.2.1 Scientific development and trends ............................................................... 52

4.3.2.2 Product standards ....................................................................................... 52

4.3.2.3 Measurement technology LF magnetic fields .............................................. 52

4.4 Assessment ........................................................................................................... 53

4.5 Discussion and conclusions ................................................................................... 53

5 Electric Storage Systems and Electric Drive Train Technology .................................... 54

5.1 Introduction ............................................................................................................ 54

5.2 State-of-the-Art ...................................................................................................... 54

5.2.1 Battery ............................................................................................................... 54

Deliverable D1.1

ELVA 5 SCP0-GA-2010-265898

5.2.2 Drive train and brakes ........................................................................................ 56

5.2.3 Charging ............................................................................................................ 60

5.2.4 Thermal management ........................................................................................ 64

5.3 General technology outlook up to 2030+................................................................ 66

5.3.1 Market Analysis .................................................................................................. 66

5.3.2 Battery ............................................................................................................... 68

5.3.3 Drive train and brakes ........................................................................................ 69

5.3.4 Charging ............................................................................................................ 70

5.3.5 Thermal management ........................................................................................ 71

5.4 Discussion and Conclusions .................................................................................. 72

6 Brake System Technology and Related Active Safety ................................................. 74

6.1 Introduction ............................................................................................................ 74

6.2 State-of-the-Art ...................................................................................................... 74

6.3 General Technology Outlook up to 2030+ .............................................................. 75

6.4 Stability Control Functions and Driver Assistance Systems ................................... 79

6.5 Discussion and Conclusions .................................................................................. 81

7 State-of-the-art and trends in active and passive safety ............................................... 83

7.1 Introduction ............................................................................................................ 83

7.2 Active Safety .......................................................................................................... 85

7.2.1 DAS and ADAS systems .................................................................................... 85

7.2.2 Assessment methods ......................................................................................... 86

7.3 Passive safety ....................................................................................................... 87

7.3.1 Structural Components of Vehicles .................................................................... 87

7.3.2 Compatibility and Restraint Systems .................................................................. 89

7.3.3 Crash Standards ................................................................................................ 92

7.3.4 Requirements on electric vehicles and systems ................................................. 95

7.4 Discussion: outlook for 2020+ ................................................................................ 98

8 Discussion and Conclusions ...................................................................................... 100

8.1 Main drivers and trends ....................................................................................... 100

8.2 Light weight design .............................................................................................. 101

8.3 EMC .................................................................................................................... 102

8.4 Electric storage and drive train technology .......................................................... 102

Deliverable D1.1

ELVA 6 SCP0-GA-2010-265898

8.5 Brake technology ................................................................................................. 103

8.6 Vehicle safety ...................................................................................................... 103

9 Glossary .................................................................................................................... 105

10 Literature ................................................................................................................... 107

Deliverable D1.1

ELVA 7 SCP0-GA-2010-265898

1 Introduction

The objectives of WP1 of ELVA are to:

Identify societal and technological scenarios for 2020 and beyond

Identify future market needs and customer requirements for the EV in 2020 and

beyond

Translate input collected into vehicle specification supporting the development of

electric vehicle concepts in WP2 and 3

In this way WP 1 provides the framework to develop the different vehicle concepts which is

the core objective of the project. This report deals with the first objective of WP1 ―Identify

societal and technological scenarios for 2020 and beyond‖ and for this purpose a review of

existing future societal and technological developments has been carried out. The results of

this review are reported in the following chapters.

The review is divided into two parts:

A review of European and global roadmaps, strategy papers etc. for future road

transport in order to identify the main drivers and trends in our society. This review

will be presented in chapter 2.

An analysis of the state-of-the art and future trends of the vehicle technology and

standards in some specific areas relevant for the development of future EVs. This

analysis is based on various technology studies and discussions with experts in the

relevant technology fields. This analyses is presented in the chapters 3-7 and

concerns the following topics:

o Light weight material concepts and vehicle architectures (chapter 3)

o Electro-magnetic compatibility (EMC) (chapter 4)

o Electric storage systems and electric drive train technology (chapter 5)

o Brake system technology with recuperation management and related active

safety (chapter 6)

o Active and passive safety including crash compatibility (chapter 7)

It should be noted here that technology is one of the important drivers in our society and

consequently also in chapter 2 some technology trends are included. However, they are

presented on a more general/generic level than in the technology focused chapters.

Preliminary findings of the review have been presented at a workshop in Brussels on 28

February 2011 attended by ELVA partners, members of the Advisory Board as well as other

stakeholders. The feedback received during this workshop is incorporated in this report.

A discussion and conclusion section concludes this report.

Deliverable D1.1

ELVA 8 SCP0-GA-2010-265898

2 Driving forces and societal scenarios

2.1 Introduction

The review in this chapter is based on more than 40 reports and studies describing the future

development of societies. The main purpose of this report is to summarise and structure the

material, analyse and define the main driving forces as well as describe basic interactions

and some of the relations. It also describes some fact and figures of the society by 2020 and

later, based upon the reports.

Most of the reports are based on the work of teams of experts, predicting the most likely

trends for various aspects included in the reports. Some other reports define targets for

instance for the year 2050 and may be defining extreme scenarios and back-casting from

that what will happen in the meantime. The findings from our study will serve as inspiration

and guidelines for the continued work in the ELVA project.

In section 2.2 the most important societal scenarios will be discussed. In section 2.3 the main

driving forces included in the various studies will be presented. They have been organised in

a structure similar to the ERTRAC report [1] (see also Annex A): Environment & Economy,

Society & Culture, Public Policies and Technology. Since Technology is also covered in the

remaining chapters of this report it will not be addressed as a separate sub-section under

driving forces. Trends in the market for electric vehicles will be presented in section 2.4.

Discussions and conclusions are included in chapter 2.5.

Fig. 2-1: A sustainable transport system is safe, energy efficient with no or low emissions,

and affordable [6]

Deliverable D1.1

ELVA 9 SCP0-GA-2010-265898

2.2 Scenarios

Several of the reports studied have the time frame 2030-2050, but the time frame for ELVA is

shorter: 2020+. To predict or describe a scenario 20-40 years ahead is associated with a

very high uncertainty. Several reports argue that on the other hand 10 years may be a short

period and not much may happen to our society by 2020. But it should be realized that the

actions taken (or rather not taken) today (year 2011) will effect and shape the future society.

In spite of that may be for 2020 not too much will change in our society it is good to look

ahead since cars developed for 2020+ may still be around up to 2040 and some of the long

term predictions may already influence the design which enters the market 2020+.

The reports studied are in general rather consistent as far as predictions are concerned. One

reason might be that the source material origins from traditional information channels and the

other reason might be that most of the predictions are based on extrapolations from today.

Most businesses today have long-term strategies in place which are based on the most

likely, foreseeable future developments. However, recent history has proven that contingency

planning based on different scenarios is gaining importance. Extreme scenarios can help

broaden decision makers‘ awareness of future developments which are not very likely, but

which could potentially have a fundamental impact on the industry or on specific companies.

Some of the most applicable scenario references for the ELVA-project are ERTRAC [1] and

SEVS [6] both with year 2030+ as time frame, as well as the ―Roadmap 2050, a practical

guide to a prosperous low-carbon Europe‖ [4] and the ―Shell energy scenario‘s to 2050‖ [7].

The methodologies used in these studies are rather different (forecasting vs. so-called back

casting), but they are quite unified regarding the driving forces. For example there is a

consensus regarding relation between population and economic growth and the urbanisation

trends (especially in the emerging countries and toward the development of mega cities).

Other important driving forces are the politician‘s pro-activity regarding incentives and

disincentives that will have a huge impact on customer‘s choice of transportation solutions

and in turn the penetrations of more energy efficient solutions like EVs. Individual values,

attitudes and lifestyle will also have a strong impact not only on the product and services

used by themselves but also on the business operations and the service providers. There is

also a common concern regarding climate change, congestions, safety and security and

limited energy resources.

In 2009 EU and G8 leaders agreed that CO2 emissions must be cut by 80 % by 2050, if

atmospheric CO2 is to stabilise at 450 PPM- and global warming stay below the safe level 2

degrees C. But 80 % decarbonisation overall by 2050 may require 95 % decarbonisation of

the road transport sector [4]. With the number of cars set to rise to 2.5 billion worldwide by

2050 (according EC 2010 [3]), this is not achievable through improvements of ICE. Ref. [4]

uses the back casting methodology and concludes that it is possible to fulfil the above targets

by 2050 but the transition needs to start immediately. They also conclude that there is not a

single solution, but rather a mix of both technologies and societal aspects.

The ERTRAC scenarios were prepared by ERTRAC stakeholders and other technical

experts, and are based on a comprehensive review of previously published information

related to energy, environment and mobility. The scenarios foresees (i) the most likely

outcome, called the ‗common sense‘ scenario; (ii) a more ‘enthusiastic’ alternative; and

Deliverable D1.1

ELVA 10 SCP0-GA-2010-265898

(iii) a more ‘pessimistic’ alternative. Fig. 2-2 illustrates the ERTRAC scenario process and the

3 resulting scenarios for 2030.

Fig. 2-2: ERTRAC scenario process [1]

The ―‖Shell energy scenario‘s to 2050‖ [7] report identifies 2 possible scenarios for 2050:

- The Scramble scenario that outlines the future consequences of pursuing the path

of least resistance now and postponing decisions to the future

- The Blueprints scenario that indicates a more pro-active approach based on supply

concerns, environmental interest and associated entrepreneurial opportunities

resulting in a significantly more positive outcome.

In the SEVS project [6], 4 societal scenarios have been specified that are illustrated in Fig. 2-

3. The scenario process in SEVS is the result of a detailed analysis of groups of driving

forces including demographic trends, life style changes, politics, environmental impact etc…

Two of the driving force groups namely ―politics‖ and ―personal values‖ were identified as

drivers with the largest uncertainty and with the largest impact on a future sustainable and

safe transport system. The 4 resulting scenarios have been based on these two groups of

drivers. The x-axis corresponds to personal values (in particular concerning travelling) and

the outcome of this driving force varies from no change (left) to radical change in

transportation patters (right). The y-axis corresponds to politics (in particular concerning

transportation legislation and incentives) and varies from political passive (bottom) and

proactive political control (top). The resulting scenarios in the 4 quadrants are denoted:

Incremental development, eco political, eco individual and radicalism in harmony,

respectively.

Deliverable D1.1

ELVA 11 SCP0-GA-2010-265898

Fig. 2-3: Four different societal scenarios resulting from the SEVS project [6]

The conclusion is that the scenarios included in the various reports are of interest as a

reference platform for ELVA but that the underlying driving forces, societal as well as

technology, and how they relate to each other, are even of greater interest. The four extreme

scenarios defined in the SEVS project might be good as a reference platform when

discussing the timeframe and the actions to take in ELVA.

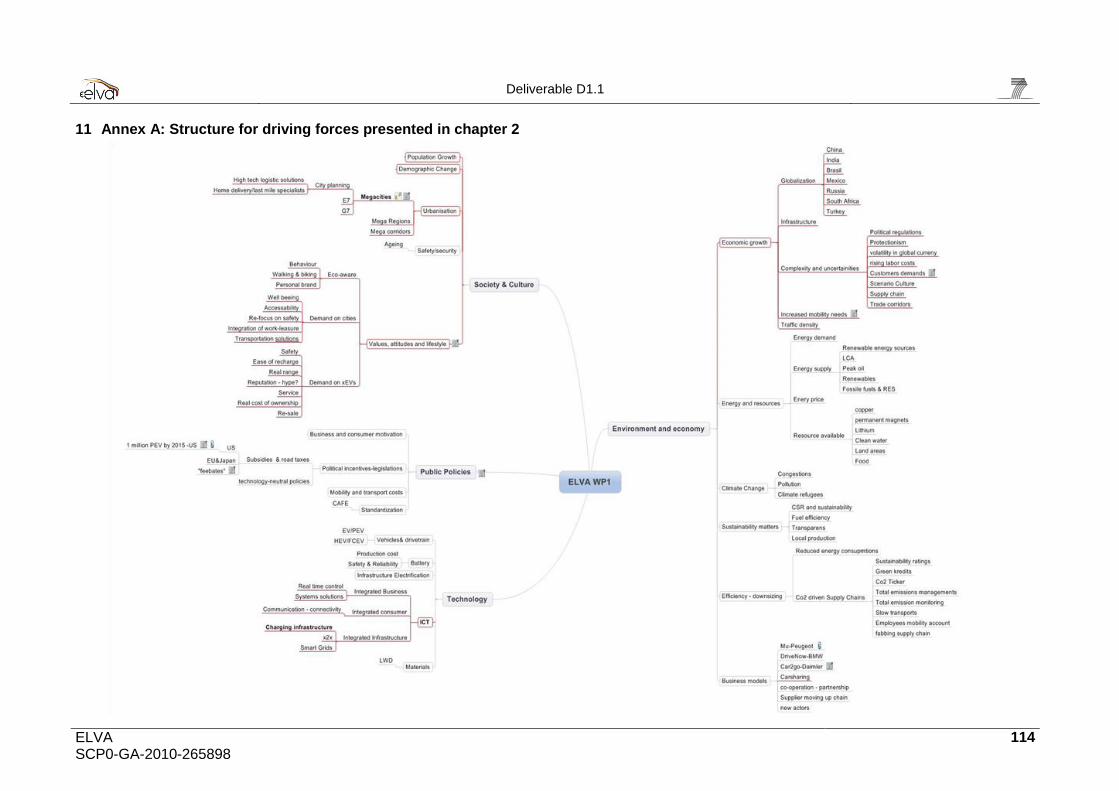

2.3 Main driving forces

Based on the reports reviewed a large number of driving forces were identified. They have

been structured taking the four ERTRAC categories (Environment & economy, Society &

Culture, Public Policies and Technology) as a basis [1]. Annex A illustrates the selected

structure were it should be realized that the positioning of some of the sub (and sub-sub etc.)

categories is rather arbitrary. For instance ―increased mobility needs‖ which is a sub-sub

category under the sub category ―economic growth‖ could have been put also under ―Society

and Culture‖. In fact many of the categories are strongly related and will influence each other.

Since ―Technology‖ is also covered in the remaining chapters of this report it will not be

addressed as a separate sub section under driving forces in this chapter 2.

2.3.1 Environment and economy

Regulatory actions taken by governments worldwide are now clearly pushing the auto

industry toward much more aggressive adoption of vehicle electrification. Many of these

initiatives can be traced back to rising concerns about greenhouse gas concentrations, and

the Kyoto Protocol of 1997.

In 2006 Sir David Stern published the first major research [14] which looked into the

economic consequences of climate change and rising GHG emissions. Stern concluded that

a rise of global temperature by more than 2°C would inevitably change global economic

conditions and could result in irrevocable changes to the way people live, work and

consume. The review argued that to prevent this from happening immediate policy change is

Deliverable D1.1

ELVA 12 SCP0-GA-2010-265898

required. An IEA (International Energy Agency) report published in 2008 indicated that in

order to limit the global increase in temperature to 2°C, atmospheric CO2 levels would need

to be limited to 450 parts per million by 2030 [25].

The transportation sector would need to pursue dramatic change, as it accounts for 44 % of

total CO2 emissions. To achieve the ―Scenario 450‖, light vehicles would need to reduce CO2

emissions by at least 49 % by 2030. In order to achieve this average output for the total light

vehicle stock, new vehicles would need to reduce emissions to an even larger extent. On

July 8, 2009 all members of the G8, pledged to adopt regulations which would limit the rise in

global temperature to 2°C [14].

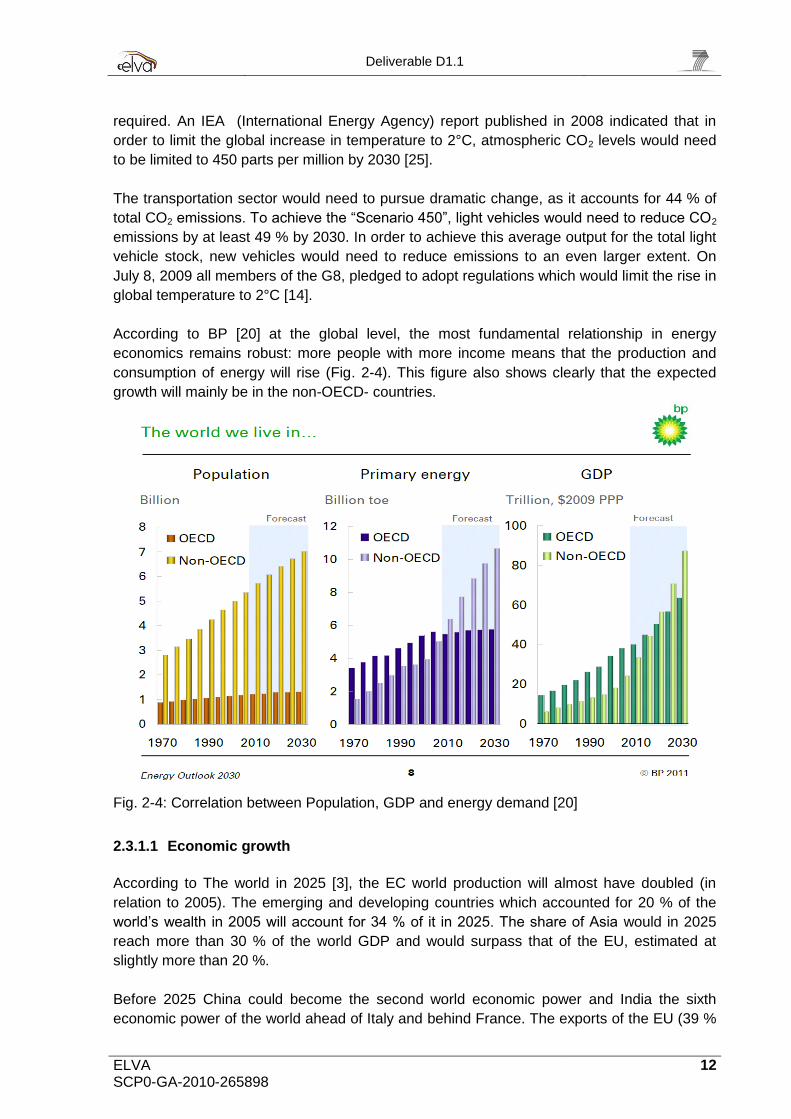

According to BP [20] at the global level, the most fundamental relationship in energy

economics remains robust: more people with more income means that the production and

consumption of energy will rise (Fig. 2-4). This figure also shows clearly that the expected

growth will mainly be in the non-OECD- countries.

Fig. 2-4: Correlation between Population, GDP and energy demand [20]

2.3.1.1 Economic growth

According to The world in 2025 [3], the EC world production will almost have doubled (in

relation to 2005). The emerging and developing countries which accounted for 20 % of the

world‘s wealth in 2005 will account for 34 % of it in 2025. The share of Asia would in 2025

reach more than 30 % of the world GDP and would surpass that of the EU, estimated at

slightly more than 20 %.

Before 2025 China could become the second world economic power and India the sixth

economic power of the world ahead of Italy and behind France. The exports of the EU (39 %

Deliverable D1.1

ELVA 13 SCP0-GA-2010-265898

of the world volume in 2005) could account for 32 % while the share of Asia increases from

29 % to 35 % [3]. Asia catches up with the US and EU in the area of research.

Globalization

In coming years the gap between emerging and developed countries in terms of trade power

will narrow. Logistics service providers in emerging markets will need to prepare for new

market structures. As logistics costs, as a proportion of total costs, continue to rise,

investments in improving efficiency will continue to gain momentum.

The establishment of free trade zones and resulting increases in foreign direct investment

will lead to above-average growth of the transportation and logistics industry in emerging

markets. In 2010 China and ASEAN1 established the world‘s third largest free-trade area

after the EU and the NAFTA. Foreign direct investment represents the most important source

of capital for emerging markets. In the emerging markets, the number of free trade zones is

expanding rapidly. Free trade zones have also been established in Brazil, China, Mexico,

Russia, South Africa, Turkey and additional emerging markets. China and some other

emerging countries outside of BRIC are increasingly making investments within other

emerging markets.

Privatisation will continue to be critical in emerging markets. The courier, express and parcel

(CEP) market is one of the strongest growing sectors of the T&L industry in a number of

emerging markets.

According to PWC [26], China has the world‘s largest population and India has the world‘s

fastest growing population. China currently holds a strong advantage, with significantly

superior infrastructure in place compared to India, and a respectable ranking of #27 on the

World Bank‘s Logistics Performance Index2. Seven of the world‘s twenty largest ports are

located in China. China is Brazil‘s largest trading partner.

The Transport & Logistic industry plays a crucial role in the China‘s future economic

development and promises strong and stable growth opportunities through 2030 [26].

China‘s emergence as a global economic player has been accompanied by a major internal

transformation. The economy has shifted from complete reliance on state-owned and

collective enterprises to a mixed economy where private enterprise plays an important role

and the number of state-owned enterprises has declined significantly.

China is the most important contributor to the enormous growth potential of the Asian CEP

market and the logistics sector is expected to growth [26].

The private sector is likely to play an increasingly important role in India’s transportation and

logistics industry in the future [26]. Goods transportation by road is almost entirely in private

1 The Association of Southeast Asian Nations (ASEAN), originally including Brunei, Indonesia, Malaysia,

Philippines, Singapore and Thailand, established the ASEAN Free Trade Area (AFTA) in 1992. 2The Logistics Performance Index is based on a worldwide survey of operators on the ground (global freight

forwarders and express carriers), providing feedback on the logistics ―friendliness‖ of the countries in which they operate and those with which they trade. They combine in-depth knowledge of the countries in which they operate with informed qualitative assessments of other countries with which they trade, and experience of global logistics environment.

Deliverable D1.1

ELVA 14 SCP0-GA-2010-265898

hands while bus operations are mostly in government hands. Levels of dissatisfaction about

the reliability, punctuality and quality of services from these organisations seem to be on the

rise among users. Attractive business opportunities will arise not only due to the increasing

demand for logistics services, but also from the market‘s high inefficiency and fragmentation

[26].

The establishment of free trade zones in Brazil has fostered strong economic growth, as

these have realised above national average growth and accelerated transport flows in the

designated regions [26]. Logistics service providers will profit from the upcoming mega-

events and the increased investment flows in the short and medium term.

Multinationals dominate the logistics demand in Mexico and have driven its growth

significantly. Mexico‘s logistics market will continue to expand in upcoming years. According

to PWC [26] more than 90 % of Mexican trade is under free trade agreements with more than

40 countries and regions, including the EU, Japan, Israel and much of Central and South

America. At the national level, greater attention to policies for regional development, anti-

corruption and bribery and functioning law enforcement would drive important and

sustainable growth for the logistics industry in Mexico.

In the future the logistics industry in Russia may benefit more from its geographic location

connecting East Asia and Europe. Introduction of port special economic zones will stimulate

internal and external trade flows between Asia, Europe and North America [26]. Russia today

is not considered as an important transportation corridor, as the main trade between Europe

and Asia takes on seaways. Russia will aim to take advantage of its beneficial position in the

future. In order to realise this vision, Russia needs to develop its railways and roads in order

to ensure rapid and cost-effective transportation options.

The Russian government is drafting policies directed at changing the state‘s export structure

from exporting primary products and resources to exporting integrated and advanced

technology products and services. This will stimulate the development of new transportation

corridors.

South Africa will become the starting point of a new transport corridor to Asia. Significant

investments in transport infrastructure and the logistics industry in Africa are needed since

the emergence of China as one of South Africa‘s main trading partners. African logistics

service providers who actively operate on the new transport corridor Africa - Asia will be able

to profit from growth. South African road-based logistics service providers are affected by

consolidation processes driven by the fast-moving consumer goods sector. Other modes of

transport are still dominated by a state-owned enterprise [26].

Turkey has a great deal of potential with its young population and its dynamic market

conditions. Turkey basically aims at minimising state involvement in industrial and

commercial activities and maximising private sector participation. The privatisation process

will mainly be completed by 2020, meanwhile being a market opportunity for investors in

transport infrastructure or for transport operators. The country‘s strategic geographic location

ensures a prominent role within future transit networks [26].

Deliverable D1.1

ELVA 15 SCP0-GA-2010-265898

Infrastructure

The quantity of goods needed to serve the world's rapidly growing global population will

increase over the next twenty years [26]. At present, industrialised countries look likely to

continue to keep a leading position in terms of transport infrastructure provision. While many

emerging countries are recording record levels of investment in transport infrastructure, they

are unlikely to bridge the existing gap completely by 2030. Currently transport infrastructure

investments tend to follow global capital flows; in practice this means transport infrastructure

investments focus on urban areas, and fast growing cities and mega cities.

Governments will need to take actions which help manage demand, including regulatory

measures such as road tolls or congestion charges, as an attempt of reducing traffic volumes

and by generating funds to reinvest in transport infrastructure.

With regards to the growth prospects of emerging countries, large investments are needed in

transport infrastructure development since today logistics service providers face significant

difficulties in transport operation. They will need to develop innovative supply methods (local

adaptability, simplicity). Logistics service providers looking to make strategic decisions about

entering new markets need to understand those markets fully; this means assessing both the

probable availability of capital and the willingness of governments to invest in transport

infrastructure. Public authorities and private investors will need to investigate various options

for sharing responsibility and risk [26].

The presence or absence of transport networks, which facilitate efficient supply chains, is

already a factor in investment decisions around the world; the ability to offer a solid

infrastructure is likely to become an even more important criterion in determining a country's

or region's competitiveness in the future. Trans-European transport networks (TEN-T) policy

has much increased the coordination in planning of infrastructure projects by the member

states in Europe. Transport infrastructure remains a deciding factor for the economic

prospects of a country [26].

Complexity and uncertainties

The complexity in the automotive industry will continue to increase because the future

transport solutions will be a part of a sustainable transport solution on a higher system level

e.g. city level. The vehicles and transport services will have to interact with several new

actors globally and locally [6]. Companies will need to develop or fine-tune their own specific

strategies for operating in diverse emerging markets. They will need to understand how

government regulation in each market affects them e.g. changing customs procedures, the

establishment of free trade zones, incentives for foreign direct investment or new

sustainability requirements. The larger and financially-better equipped companies will target

growth by looking for suitable mergers and acquisitions. Leading local players will become

increasingly important as partners and collaborators for multinationals from around the world.

Growth in developing countries contributes to volatility in global currency markets and to

protectionist sentiment in the developed world, for example different growth rates across

various emerging markets mean that rising labour costs can quickly change the relative

attractiveness of manufacturing locations.

Deliverable D1.1

ELVA 16 SCP0-GA-2010-265898

The rapid growth of cities and the growth of urban concentration, accompanied by a stronger

connectivity at the local and even international level (ICT), will cause at the same time very

complex (in particular ecological and social) challenges and opportunities (for example,

economic and cultural ones). The development of the future xEV market is highly dependent

on the customer‘s demands and the political regulations [6]. Politicians in so called smart

cities might legislate that only zero emission vehicles are permitted to drive in central cities.

Visionary governments may even go so far as to construct Eco-Cities. Other example is the

government‘s directions in China (5 years program) that might also have a strong effect on

the market penetration of xEVs by 2020.

Manufacturing and supply chain planners must deal with rising complexity. Companies must

continuously optimize their supply chains. Some companies are preparing splintering their

traditional monolithic supply chains into smaller and more flexible ones. They also treat their

supply chains as dynamic hedges against uncertainty by actively and regularly examining

their broader supply networks with an eye toward economic conditions five or ten years

ahead. In doing so, these companies are building diverse and more resilient portfolios of

supply chain assets that will be better suited to thrive in a more uncertain world.

The world‘s supply networks are changing. New trade corridors between Asia and Africa,

Asia and South America and within Asia will re-chart global supply chains. Trade volumes

will shift towards emerging markets and least developed countries will take their first steps

into the global marketplace. Turkey‘s growth is related in part to its geographic location which

serves as an important trade corridor between Europe and the Middle East.

Mobility needs

Transportation needs are growing strongly around the world. Continuing globalisation,

coupled with high growth rates of population density and GDP in some regions, means that

the flow of goods and people will continue to increase over time. Global trade in goods and

services is likely to rise more than threefold to US$27 trillion in 2030 [26].

According to Frost & Sullivan [13], there will be a strong need for increased mobility,

European Prediction for 2000-2020: freight transport: +50 %, passenger transport: +35 %

and Western Europe traffic growth at 2 % per year.

Traffic density

The traffic density, especially in mega cities, will continue to increase. City planning will be

even more important as well as individuals‘ choice of transport solution. In cities there will be

a diversity of vehicles, and by 2030 there might be 2-wheelers and double lanes which will

increase the transport capacity [6].

2.3.1.2 Energy and resources

According to IEA [25], BP [20] and Shell [7], the global energy consumption growth will

continue, driven by industrialisation in the emerging regions – but efficiency improvements

are likely to accelerate. The net effect is although that global oil demand will increase.

Deliverable D1.1

ELVA 17 SCP0-GA-2010-265898

A greater diversity of resources delivers greater security of supply, which is an outcome

policymakers are likely to seek. The rationale for using a mix of sources rather than a few

technologies is that most technologies do not have sufficient theoretical capacity to supply all

demand, the EU‘s dependency on non-EU countries decreases and a more reliable energy

sourcing is achieved. A system that is less dependent on fossil fuels is more resilient against

resource depletion as well as cost dynamics related to the volatile global supply-and-demand

[4]. This requires closer transnational cooperation in transmission infrastructure, resource

planning, energy market regulation, and systems operation.

Energy demand

According to the IEA [25] in 2025 the world energy demand will have increased by 50 % in

relation to 2005 and will reach 15 billion tons oil equivalent. IEA estimates that from now to

2030 coal consumption, in particular for power stations in China and India, will increase by

more than 50 % (Fig. 2-5).

The fuel mix changes relatively slowly, due to long asset lifetimes, but gas and non-fossil

fuels gain share at the expense of coal and oil.

Fig. 2-5: Consumption growth [20]

Energy supply

Oil production will have started to stagnate (peak) and coal is expected to become the first

energy source between now and 2050. Meeting the expected growth will rely more and more

on alternative sources of energy supply, like natural gas liquids, bio fuels and unconventional

oil. But in 2025 oil will still largely be in the lead. Transport is still 97 % dependent on fossil

fuels, which has negative implications also for the security of energy supply.

The share of carbon-based energy should remain very largely dominant in 2030: Fossil fuels

(oil, coal and gas) account for 80 % of the world‘s primary energy mix while nuclear and

Deliverable D1.1

ELVA 18 SCP0-GA-2010-265898

renewables (hydro, wind, solar, etc.) account for 10 % each. In 2030, the European Union

will import almost 70 % of its energy needs.

According to BP [20], the global fuel mix continues to diversify and for the first time, non-

fossil fuels will be major sources of supply growth (Fig. 2-6). Energy policy and technology

lead to a slow-down in the growth of CO2 emissions from energy use, but not fast enough to

put the world on a safe carbon trajectory. OECD oil demand has peaked in 2005 and by

2030 will roughly be back at the level of 1990. Bio fuels will account for 9 % of global

transport fuels. Finally, China will be the world‘s largest oil consumer.

Fig. 2-6: World power generation [20]

Electric infrastructure capacity: the electricity demands of EVs are not expected to

overwhelm electric utilities‘ capacity. Only 4 % of electric utility capacity would be consumed

if 25 % of all U.S. vehicles were powered by electric [14]. Electric distribution infrastructure

could be strained during peak charging times, or in specific areas (such as a parking lot) that

have a disproportionate number of vehicles charging at once. Electric vehicle service

companies have focused on network management systems and software in order to

communicate with vehicles and/or charge points in order to ensure that this does not occur.

Israel Electric Corp estimates that, in a scenario where all Israeli vehicles are EVs by 2020,

they would require zero additional generation and transmission assets given the interaction

of EV service provider Better Place. If charging were done on an ad-hoc basis, generation

assets would have to increase by 21 % and transmission / distribution assets would have to

increase significantly [14].

Deliverable D1.1

ELVA 19 SCP0-GA-2010-265898

Energy price

The high energy prices will affect the total cost of transportation. Deutsche Bank‘s [14]

Integrated Oil Research Team sees potential for oil prices to rise dramatically, including

potential for a brief spike to $ 175 per barrel, given limited excess supply, rising demand, and

chronic underinvestment in new oil production. According to the IEA projection [25] fuel

prices are assumed to increase. Prices of coal and gas will increase by about 60 % over the

next 40 years, which is equivalent to a 1 % annual increase (in real terms). It will also

stimulate the penetration of alternative drive trains. The ERTRAC Strategic Research

Agenda shows the road transport energy source and propulsion technology towards 2050

(Fig. 2-7).

Fig. 2-7: ERTRAC transports evolution toward 2050 [36]

Resources available

Around 2025 the energy question should remain a source of major tension (economic and

geopolitical) due to the likely ―oil peak‖ and the energy needs of a world of 8 billion

individuals. The tensions will be both between production and consumption patterns and

between production/consumption patterns and natural resources.

The recycling of raw materials will become an important industrial activity. China accounted

for more than 50 % of the growth of the world consumption of industrial metals between 2002

and 2005. In the future the growth levels of emerging countries will maintain a high pressure

on the demand for raw materials. Many countries that are rich in resources apply

protectionist measures which stop or slow down exports of raw materials to Europe in order

to support their downstream industries.

Deliverable D1.1

ELVA 20 SCP0-GA-2010-265898

The leading producers and exporters of lithium ore today are Chile and Argentina, with the

largest reserves known to exist (and which are largely untapped) in Bolivia, along with lesser

amounts in China, Russia and North America. China and Russia are importers of lithium from

Chile, which is less costly than mining their own. Lithium can be recycled and reused, like

most other battery chemistries. The auto batteries are some of the most recycled consumer

item in the world, so a model for recycling already exists. Other materials in batteries that

also must be handling are e.g. copper and permanent magnets.

According to EC [3], 1.1 billion inhabitants do not have access to clean water today. In 2025

it is estimated that 3 billion people will not have clean water. The need for water will increase

sharply with the increases of the world population and of the rise in the standard of living in

emerging countries, creating strong tensions with the quantities available which are likely to

decrease due to climate change.

Climate changes may destroy important agriculture areas and this in combination with the

population growth will influence the future food prices [6].

2.3.1.3 Climate Change

Transport infrastructure and transport networks have profound effects on the environment.

These impacts will need to be assessed from a holistic, long-term perspective to ensure that

greenhouse gas emissions and other negative impacts on the environment are minimised.

Energy policy is driven by security as well as by climate change concerns. Measurements

taken by scientists since 2000 have shown that the world emissions of carbon dioxide grow

now more quickly than the most pessimistic scenario of IPCC [23].

Congestion

According to most of the reports in this study, the overall transportation is expected to

increase and the congestion will follow. According to Frost & Sullivan [13] the number of

vehicles increases five times faster in developing countries and the costs of congestion are

estimated to be 120 billion annually. Regulatory measures can help to provide funds to

reinvest in transport infrastructure and to reduce traffic volumes. Efficient pricing based on

external cost matches supply and demand at its most efficient point, leading to direct

economic benefits by reducing externalities, (i.e. congestion, pollution). Large-scale

implementation of road pricing is foreseen, so users as well as companies will have to pay

for the transportations in future [26].

Pollution

According to F&S, transportation equates to 21 % of emissions in which road transport

account for 71 % [13]. Air pollution caused by traffic is associated with nearly 700,000 deaths

per year, and this number is increasing [13]. CO2 emissions from road transportation are

growing at a rate of 29 % in Europe [13]. Emerging public health data on the impact of nano

particulates from diesels and other sources are said to be even more damning [6].

Deliverable D1.1

ELVA 21 SCP0-GA-2010-265898

2.3.1.4 Sustainability matters

Environmental costs will become an integral part of assessing the full costs of a transport

solution taking into account the entire life cycle of construction, operation and deconstruction

[26]. Holistic and environmental compatibility methods need to be implemented so the

transport sector can collaborate and thereby reduce emissions and congestions

[26].Transport solutions will increasingly be assessed on environmental compatibility.

Sustainability will also continue to gain in importance, so applying analyses or total value of

ownership methods will be critical [26]. An emphasis on innovation will also be critical in

finding more eco-friendly transport solutions.

2.3.1.5 Efficiency – downsizing

In July 2009, the leaders of the European Union and the G8 announced an objective to

reduce greenhouse gas emissions by at least 80 % below 1990 levels by 2050. In October

2009 the European Council set the appropriate abatement objective for Europe and other

developed economies at 80-95 % below 1990 levels by 2050 [4]. Achieving the 80 %

reduction means a transition to a new energy system both in the way energy is used and in

the way it is produced. It is virtually impossible to achieve an 80 % GHG reduction across the

economy without a 95 to 100 % decarbonised power and transport sector. Fig. 2-8 shows

that the transport sector has reduced during the last 10 years their emissions and is

expected to continue the reduction to almost half by 2020 compared to 2000 (EU) [16].

Fig. 2-9 shows that according to ECF [4], even though the carbon emissions have been

reduced, more efforts are needed to reduce emissions. The staples in the picture shows that

the emissions from transportation and energy use , between 2010-2050, will increase, while

the staple to the right shows the decarbonisation target by 2050. Notice the emission gap

between the predicted emissions by 2050 compared to the EU targets by 2050.

Fig. 2-8: The average Carbon Emission [14]

Deliverable D1.1

ELVA 22 SCP0-GA-2010-265898

Fig. 2-9: Nearly full decarbonisation in transport [4]

Fig. 2-10 shows a mix of vehicles with different drivetrains that could be one possible

scenario to be achieved by 2050 [4].

Fig. 2-10: Mix of drive trains [4]

Deliverable D1.1

ELVA 23 SCP0-GA-2010-265898

2.3.1.6 Business models

According to Deutsche Bank [14] a very large market opportunity appears to be developing

through the emergence of new business models based on the cost advantage of electricity

versus gasoline driving. Combined with government incentives already in place, these

business models have the potential to dramatically lower the entry price for electric vehicle

and potentially making them cheaper to purchase and operate.

Several automakers, finance, and infrastructure companies have been discussing business

models that could help facilitate more rapid EV market penetration. An emerging group of EV

infrastructure companies believe EVs can be cheaper than ICEs, at the point of purchase

[14]. The most advanced amongst the emerging group of EV infrastructure companies,

―Better Place‖, has based its businesses on the premise that EV purchases should be

structured with a leasing of the batteries. This will move the customers initial cost from the

purchasing process to the operation/driving process, resulting in a lower purchasing price.

―They believe this will be a pre-requisite for EVs to capture a significant share of the mass.

Better Place intends to provide vehicle batteries to consumers at no upfront cost, and then

sell consumers ―Miles‖, i.e. a per mile fee, equivalent to the per mile cost of driving a gasoline

powered vehicle, which would cover the cost of the battery, electricity, widespread charging

infrastructure, and a return on Better Place‘s investment‖ [14].

Car Sharing is a financial alternative to private ownership. Environmental friendly car sharing

companies in Sweden are e.g. Move About (www.moveabout.se) and SunFleet

(www.sunfleet.com). Traditional automakers have also initiated new business models e.g.

Peugeot Mu (www.mu.peugeot.co.uk)), Daimler car sharing subsidiary car2go

(www.car2go.com) and soon coming BMW DriveNow (www.drive-now.com).

2.3.2 Society & Culture

Several of the reports refer to the strong correlation between population and economic

growth. The emerging markets will count for the major growth and it is there that changes in

demographics and consumer behaviours could have the most significant impact of the future

society as well as business [26].

2.3.2.1 Population Growth

Population growth and the density are key indicators for the assessment of future needs for

private and public transportation needs. The world‘s population is continuing to expand and

is expected to grow by 20 % to reach 8 billion inhabitants, by 2025 [3]. According to the

United Nations [3], 97 % of this growth will occur in the developing countries (Asia, Africa),

resulting in that 61 % of the world population will be in Asia by 2025 [3]. The population of

India will approach the population of China (which will have started to decrease) and will

need extensive infrastructure enhancements. The Saudi Arabia, Turkey and the United

Kingdom are also expecting significant increases in population density. The smaller

emerging economies of Vietnam and Indonesia, part of the so-called ―Next-11‖, might

become the world's largest economies in the 21st century along with the BRICs. Other

countries such as Russia will experience no change in population density, and in some

Deliverable D1.1

ELVA 24 SCP0-GA-2010-265898

countries such as Germany, Poland and Japan, population density is even likely to decrease

[26]. The European population is expected to decrease from 2012, because of the high

proportion of elderly people. In 2025, the population of EU will only account for 6.5 % of the

world population [3].

The cities in developing countries will account for 95 % of urban growth in the next twenty

years and will shelter almost 4 billion inhabitants in 2025. The number of the inhabitants of

slums at world level will double between now and 2025 to reach more than 1.5 billion.

2.3.2.2 Urbanisation

According to the European Commission in ―The world in 2025‖ [3], 11 out of the 20 first

megacities in the world (those with more than 10 million inhabitants) will be in Asia as well as

17 of the 30 towns of 5 to 10 million inhabitants and 184 of the 364 cities between 1 and 5

million.

This long-term mega trend in population movement towards the city is the result of two

underlying force fields: the exponential growth in world population (with an average growth

rate of approx. 1.2 % per annum) and the rural-urban drift (due to the relatively more

favourable socio-economic opportunities in urban agglomerations). This leads to new

challenges for policy makers, like congestion, environmental degradation and effects of

climate change. Modern network cities have turned into spearheads of (supra-) regional and

(supra-) national power, not only from a socio-economic perspective (business,

innovativeness, jobs, wealth, migration, entrepreneurial dynamics), but also from a geo-

political perspective and a technological perspective (mobility, transport and energy systems,

ICT).

Urban areas are the main drivers of growth in the European economy. A thriving urban area

must be able to ensure the sustainable accessibility and mobility of urban systems (including

logistics) and simultaneously develop effective measures to minimise its ecological footprint.

European urban areas must attract, retain and even nurture highly mobile, creative,

innovative firms. Transport infrastructure is perceived as one of the greatest economic and

environmental challenges for mega cities [26]. Whereas North American and European cities

are mostly concerned about the maintenance of their ageing transport infrastructure,

emerging cities face the challenge of rapidly building up new basic transport infrastructure

capacities, increased congestion and growing environmental awareness will prompt a

widespread division of mega cities into sub-cities. Governments must manage urban

transport infrastructure and undertake long-term transport planning in order to deliver

sustainable urban areas. Regardless of how city structures will develop, logistics service

providers will need to rethink city delivery services programmes and develop innovative city

logistics solutions (e.g. last-mile services, home deliveries) [26].

2.3.2.3 Values, attitudes and lifestyle

Environment-related requirements and the dependence on raw materials produced abroad

will push the EU towards a new way of producing, of consuming, of living, of moving, etc. It

will have to step up its efforts to become the uncontested leader at world level of this ―socio-

Deliverable D1.1

ELVA 25 SCP0-GA-2010-265898

ecological‖ transition, in particular as the world market for ―green‖ goods and services is

expected to double from 1 370 billion dollars a year currently to 2 740 billion dollars around

2020 [3]. It is the changes in social behaviour which will contribute, if they are stimulated by

appropriate policies, to a drastic reduction in energy consumption and the market penetration

of new technologies like xEVs.

By 2030 a highly integrated and service driven information society will have emerged in

which the consumer takes part actively and continuously regardless of his/her location

(home, work, commuting, leisure). Especially in the urban areas a wide variety of on-line

services provided by advanced, cheap digital outlets. To achieve sustainable transport

solutions the connectivity of people and vehicles to the infrastructure will be a pre-requisite

[8].

Eco-aware

According to Deutsche Bank [14.] an increased societal concern regarding environmental-

climate risks can and will affect purchase decisions. People will be more empowered and

well informed. They will also become increasingly watchful and wary about how companies

perform outside the manufacturing and distribution processes. Corporate social responsibility

will become markedly more important to the consumer. A number of surveys for instance

show that in many cities the modal share of cycling has grown significantly in recent years,

and this trend will continue [18].

2.3.2.4 Demand on cities

People will value cities based upon the possibility of well-being, accessibility, safety and

security, the possibility to combine and integrate work-leisure and the mobility solutions. The

vision of an ―Eco-City‖ describes a city which is designed to create the smallest

environmental footprint and lowest quantity of pollution possible [26]. An Eco-City would be

largely self-sufficient, with minimal reliance on the surrounding countryside, and use power

generated onsite from renewable energy. Further targets of such eco-cities comprise the

implementation of zero-emission transport systems, zero-energy constructions, and energy

conservation systems and devices. Eco-cities are currently planned in different countries

worldwide, e.g. Masdar City in Abu Dhabi, as well as other projects in Australia, China,

Sweden, United Kingdom and United States. Transportation would be electronically powered

and freight transport would often be located in the underground of the city, while passenger

transport can be handled via small vehicles on ground level.

2.3.2.5 Demand on mobility solutions

The consumer of 2020 is more likely to be interested in flexible access to different types of

transportation. Bundled in the price would be scalable access to additional vehicles. Lifestyle

changes will allow access to luxury or larger vehicles during weekends, as an example, while

a small, efficient vehicle will suffice for daily commuting needs. The emergence of ―mega

cities‖ and the growth in public and alternative transportation options will be a key influencer

to changing lifestyles. Multiple transportation models will be used and more than 50 % will

use the public transportation by 2020 [13]. This will necessitate the creation of a seamless

Deliverable D1.1

ELVA 26 SCP0-GA-2010-265898

mobility experience between automobiles and these alternatives. The industry will need to

respond with ownership models and technology to integrate these options. The increased

emphasis on environmental, safety, personalization, traffic congestion and alternative

transportation will have a major impact on how and what people choose for their mobility

needs. Traditional criteria such as price, reliability and brand will have much less an impact in

the decision process of the future consumer [8].

One key reason that mass commercialization of xEVs may proceed slowly over the next

decade is that mainstream retail purchasers are careful about investing in new technologies

that are not fully understood. There are a variety of uncertainties about exactly how much

money will be saved by xEVs (savings depend on uncertain forecasts of fuel and electricity

prices), how reliable and safe the batteries will be, how convenient and costly it will be to

recharge a PEV, how easy it will be to have the vehicle serviced, and how difficult it will be to

resell the vehicle. If customer expectations are inflated (by automakers, dealers, power

companies, environmental groups, and/or government officials) relative to what is actually

experienced, the reputation damage to the technology could be significant and possibly

irreparable [12.].

According to The Report of an Expert Panel [12] there are four market factors, each of which

can be influenced by public policy, that present the greatest potential for altering the

competitive position of PEVs in the vehicle market:

1. Energy prices;

2. Battery characteristics (safety, reliability, and production costs);

3. The availability of convenient and affordable recharging infrastructure;

4. The pace of progress with PEVs compared to competing technologies, such

as refinements to the internal combustion engine, conventional hybrids,

advanced bio fuels, natural gas vehicles, and fuel cell vehicles.

2.3.3 Public Policies and market trends

In July 2009, the leaders of the European Union and the G8 announced an objective to

reduce greenhouse gas emissions by at least 80 % below 1990 levels by 2050 [3]. In

October 2009 the European Council set the appropriate abatement objective for Europe and

other developed economies at 80-95 % below 1990 levels by 2050 [3].

In order to achieve its central policy objective of reducing GHG emissions by 20 % by 2020

against 1990 levels, the EU has put together an energy-policy package [3]. Transport,

accounting for about 20 % of European CO2 emissions is one of the targeted areas for

improvement, with passenger cars (12 % of total) presenting the biggest contributor. In its

effort to become the leading low carbon society the EU has put a tough regulatory framework

in place, requiring Europe to take the global lead in fuel economy improvements.

In late 2007 the European Commission introduced its regulatory framework for regulating

automotive CO2 emissions starting in 2012 [3]. The regulations target average new car fleet

emissions of 130g/km, and will be phased in through 2015 (65 % of new car sales will have

to comply in 2012, gradually rising to 100 % by 2015). For 2020 the EU target is set to 95

g/km.

Deliverable D1.1

ELVA 27 SCP0-GA-2010-265898

According to DB [14],‖it is estimated that when combining all efforts to improve the ICE that

are currently under development, CO2 emissions could theoretically be improved by an

additional 30 %-40 %, bringing the weighted new vehicle CO2 emissions down to 105-

110g/km‖. The implication is that increased electrification appears to be inevitable since it

seems to be impossible to achieve a 95g/km target using conventional ICE technology.

Given the substantially lower CO2 footprint of xEV, adding these vehicles into the mix would

bring down fleet average statistics substantially (Fig. 2-11).

2.4 Trends in the market for xEVs

DB [14] expects increasingly compelling financial incentives/penalties from governments like

rebates on high efficiency vehicle purchases and taxes on low efficiency vehicle purchases.

Congestion charges will become increasingly prevalent, providing an economic incentive for

consumers to shift away from less efficient modes of transportation. Currently 30 % of all

countries have already made the transition towards a CO2-based system. Several European

larger cities are penalizing larger gas guzzlers and favour electrified power trains through

congestion charges for inner city traffic ―feebates‖.

Governments around the world have dramatically ratcheted up subsidies for xEV purchases.

High profile programs include credits of up to $7,500 in the U.S., €5,000 in France, and RMB

60,000 ($8,800, for public use vehicles) in China. Denmark, Israel, Japan, Spain, and others

also offer substantial financial incentives for these products [14].

Fig. 2-11: Vehicle mix and CO2 emissions [14]

Deliverable D1.1

ELVA 28 SCP0-GA-2010-265898

There has also been significant financial support for manufacturers of ―advanced technology‖

vehicles, batteries, components, and infrastructure. According to DB [14] Boston Consulting

Group estimates that governments worldwide have already pledged to spend $15 billion in

this area over the next 5 years (EV projects accounted for a large proportion of the US

Department Of Energy‘s $25 billion Advanced Technology Vehicle loan and $2.4 billion grant

programs).

Part of the European fiscal stimulus has been oriented toward infrastructure for electric

driving, and build-out of battery technology [14]. For example, France has dedicated €1.5

billion on infrastructure to recharge vehicle batteries with a target of achieving 4.4 million

vehicle recharge points by 2020 and the French government is providing loans to transform

existing OEM plants into EV factories.

President Obama called for putting one million electric vehicles on the road by 2015,

affirming and highlighting a goal aimed at building U.S. leadership in technologies that

reduce U.S. dependence on oil [14]. xEVs represent in the US a key pathway for reducing

petroleum dependence, enhancing environmental stewardship and promoting transportation

sustainability, while creating high quality jobs and economic growth.

According to DB [14] the IHS Global Insight estimates that the number of xEV models will

rise to at least 150 by 2014 and that at least 200 models will be available by 2019.

Furthermore they expect HEVs and PHEVs/EVs to each represent 11 %-12 % of US market

sales (total of 23 %) (Fig. 2-12)

Fig. 2-12: US market by 2020 [14]

According to DB [14], there will be a limited demand for full hybrids, and much higher

demand for PHEVs (14 % of the market by 2020). PHEVs would enable most consumers to

perform their daily commutes almost exclusively in electric drive mode. DB [14] notes that

PHEVs are viewed as particularly attractive for larger premium vehicles, as the relative price

increase will be smaller. They also forecast that full EVs will rise to 1 % of total market by

2015 in Europe and to approximately 5 %-6 % by 2020 (Fig. 2-13).

Deliverable D1.1

ELVA 29 SCP0-GA-2010-265898

Fig. 2-13: EU market by 2020 [14]

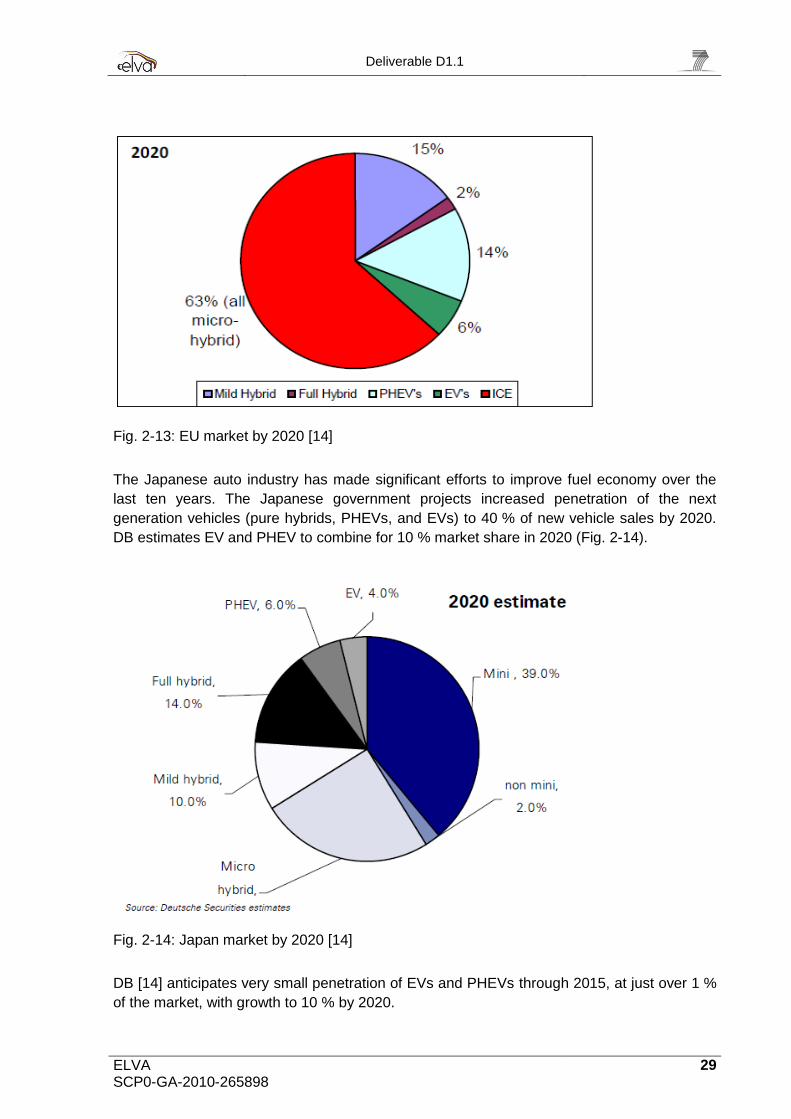

The Japanese auto industry has made significant efforts to improve fuel economy over the

last ten years. The Japanese government projects increased penetration of the next

generation vehicles (pure hybrids, PHEVs, and EVs) to 40 % of new vehicle sales by 2020.

DB estimates EV and PHEV to combine for 10 % market share in 2020 (Fig. 2-14).

Fig. 2-14: Japan market by 2020 [14]

DB [14] anticipates very small penetration of EVs and PHEVs through 2015, at just over 1 %

of the market, with growth to 10 % by 2020.

Deliverable D1.1

ELVA 30 SCP0-GA-2010-265898

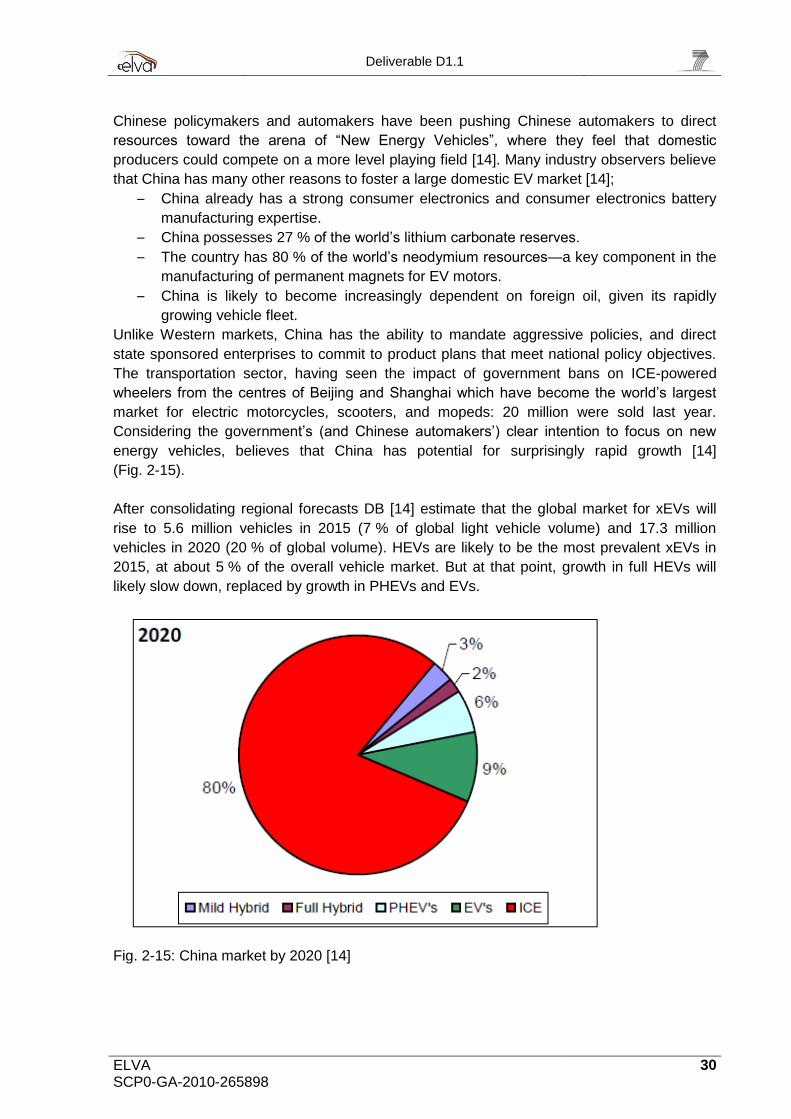

Chinese policymakers and automakers have been pushing Chinese automakers to direct

resources toward the arena of ―New Energy Vehicles‖, where they feel that domestic

producers could compete on a more level playing field [14]. Many industry observers believe

that China has many other reasons to foster a large domestic EV market [14];

– China already has a strong consumer electronics and consumer electronics battery

manufacturing expertise.

– China possesses 27 % of the world‘s lithium carbonate reserves.

– The country has 80 % of the world‘s neodymium resources—a key component in the

manufacturing of permanent magnets for EV motors.

– China is likely to become increasingly dependent on foreign oil, given its rapidly

growing vehicle fleet.

Unlike Western markets, China has the ability to mandate aggressive policies, and direct

state sponsored enterprises to commit to product plans that meet national policy objectives.

The transportation sector, having seen the impact of government bans on ICE-powered

wheelers from the centres of Beijing and Shanghai which have become the world‘s largest

market for electric motorcycles, scooters, and mopeds: 20 million were sold last year.

Considering the government‘s (and Chinese automakers‘) clear intention to focus on new

energy vehicles, believes that China has potential for surprisingly rapid growth [14]

(Fig. 2-15).

After consolidating regional forecasts DB [14] estimate that the global market for xEVs will

rise to 5.6 million vehicles in 2015 (7 % of global light vehicle volume) and 17.3 million

vehicles in 2020 (20 % of global volume). HEVs are likely to be the most prevalent xEVs in

2015, at about 5 % of the overall vehicle market. But at that point, growth in full HEVs will

likely slow down, replaced by growth in PHEVs and EVs.

Fig. 2-15: China market by 2020 [14]

Deliverable D1.1

ELVA 31 SCP0-GA-2010-265898

By 2020, DB believes PHEVs / EVs will approach 11 % of the global market, with HEVs at

just below 9 % (Fig. 2-16). By region China is expected to catch up to the US by 2020 (Fig.

2-17) but xEV adoption will likely lag in other emerging markets [14].

The government Korea believes that the country has an edge in the global electric vehicle

race as some Korean companies have leadership in battery technology [14].

Fig. 2-16: Global xEV volume by type [14]

Fig. 2-17: Global volume by region [14]

Deliverable D1.1

ELVA 32 SCP0-GA-2010-265898

2.5 Discussions and conclusions

About 40 reports have been studied. Most of them are predictions and extrapolations for

2020-2025, based on today‘s society and technology, while a few reports are descriptions of

scenarios for 2030-2050. The main purpose of this chapter is to summarise and structure the

material and identify, analyse and define the main driving forces as well as describe basic

interactions and some of the relations between these driving forces.

The reports studied are very consistent regarding the driving forces: population and

economic growth, demographical changes, urbanisation and the development of mega cities.

According to the UN [3], between now and 2025, the world population will increase by 20 %

to reach 8 billion inhabitants (6.5 today). 97 % of this growth will occur in the developing

countries (Asia, Africa), and it is expected that the quantity of goods needed to serve the

world's rapidly growing global population will increase over the next 20 years. The increased

demand of energy and other resources will follow, especially in China. Almost all reports

studied estimates that the energy demand and the CO2 emissions will continue to increase

by 2020. According to IEA [25] in 2025 the world energy demand will have increased by

50 % in relation to 2005 and estimates that from now to 2030 coal consumption, in particular

for power stations in China and India, will increase by more than 50 %.

Several reports also emphasise a common concern regarding climate change, congestions,

limited resources, and safety and security. In 2009 the EU and G8 leaders agreed that CO2

emissions must be cut by 80 % by 2050, if atmospheric CO2 is to stabilise at 450 PPM – and

global warming stay below the safe level 2 °C. But 80 % decarbonisation overall by 2050

may (according to McKinsey) require 95 % decarbonisation of the road transport sector [3].

Achieving the 80 % reduction means a transition to a new energy system both in the way

energy is used and in the way it is produced. The scenario report [4] concludes that it is

possible to fulfil the 80 % reduction by 2050 and provides a roadmap (scenario) for this. For

the transport sector, as well as for the power sector, this implies decarbonisation by 95 %,

without negative effects on safety.

Important aspects of a sustainable transportation solution are energy efficiency, reduction of

limited resources used, a fuel shift and a transition toward renewable energy resources

(RES) (on a lifecycle basis). To achieve this, three important driving forces are necessary:

1. Technology development (vehicles, batteries, infrastructure and ICT)

2. Political incentives, disincentives and legislations

3. Customer and individuals behaviour, values and attitudes

Most reports argue that the market penetration of electrical vehicles is an important part of

the solution, but it can be seen that the penetration of xEVs on the market will still be quite