Embed Size (px)

Citation preview

SMSF Contributions – Getting Assets into your SMSF

Agenda

What is a contribution?

When is a contribution made?

In-Specie transfer of assets

Contribution caps

Contribution strategies

How can we help?

SMSF Contributions

What is a Contribution?

• Not defined in legislation or regulations.

• From Taxation Ruling TR 2010/1:

• “A contribution is anything of value that increases the capital of a

superannuation fund provided by a person whose purpose is to benefit one

or more particular members of the fund or all of the members in general”.

• Importantly a person’s purpose must be to increase the capital of a fund.

• As a general rule – a contribution is made when received by the fund.

SMSF Contributions

Types of Contributions

Concessional Contributions

• These are made from money that has yet to be taxed.

• The main examples are employer contributions (Superannuation Guarantee

and salary sacrifice).

• Personal deductible contributions (self-employed or someone without

employer support).

• Concessional contributions are capped at $30,000 pa for under 50.

• Age 50 or over the cap is $35,000 pa.

SMSF Contributions

Types of Contributions

Non-Concessional Contributions

• These are made from money that has already been taxed.

• The main examples are personal super contributions for which no tax

deduction is claimed.

• Annual cap is $180,000 or $540,000 using the bring-forward provisions.

• If aged under 65 at any time in the financial year can use the bring-forward

provisions even after turning 65.

• If more than the relevant cap contributed in a single amount the excess

must be refunded.

SMSF Contributions

Types of Contributions

CGT-exempt Contributions

• These are eligible contributions for small business owners.

• Available on the disposal of an ‘active business asset’.

• These contributions are capped at $1.355 million for the 15-year exemption.

• $500,000 for the retirement exemption.

• Separate from the non-concessional cap, but are considered tax-free

components.

SMSF Contributions

Who can Contribute?

• Mandated Employer – if you work for an employer that is required to

contribute on your behalf under law, an award or industrial agreement.

• Such contributions would include the Superannuation Guarantee (SG).

• There is no age limit for the Superannuation Guarantee (SG).

• Voluntary Employer and salary sacrifice – if you are under 65 and employed

or between 65 and 74 and satisfy the work test (40 hours in a 30-day

consecutive period).

• These contributions cease 28 days after the 75th Birthday.

SMSF Contributions

Who can Contribute?

• Personal deductible – if you:

– Are eligible to make personal super contributions (see above).

– Earn less than 10% of your income from eligible employment.

– Complete a valid “Notice of Intent” and receive an acknowledgement

from the fund Trustee.

• These contributions cease 28 days after the 75th Birthday.

SMSF Contributions

Who can Contribute?

• Personal – if you:

– Are Under 65.

– Between 65 and 74 and have been “gainfully employed” for at least 40

hours over a period of 30 consecutive days during the financial year in

which the contributions are to be made.

– If less than 65 on 1 July in a financial year can use the bring-forward

provisions after the age of 65.

• These contributions cease 28 days after the 75th Birthday.

SMSF Contributions

How is a Contribution made?

• This can be achieved in the following manner:

– Transferring money to an SMSF

– In-specie transfer of assets

– Increasing the value of assets owned by an SMSF

– Payment of an expense by a third party

– Forgiving a debt owed by the SMSF

– Rolling over benefits from another superannuation fund.

SMSF Contributions

Transferring money to an SMSF

• A contribution of funds as cash, or an electronic transfer, is made when the

amount is received by the superannuation provider or credited to the

relevant account.

• It is not until an amount is credited to a bank account of the superannuation

provider that a contribution will be taken to be made.

• A superannuation provider’s account statement would normally provide the

best evidence as to when a contribution is received.

SMSF Contributions

Transferring money to an SMSF

• However, in limited circumstances, other evidence may be used to

determine when a contribution is made:

– For example, a transfer of funds between the linked accounts of a

member of a self managed superannuation fund and the fund held at

the same financial institution.

– Evidence, such as a computer print-out recording the receipt of the

amount into an account of the superannuation provider, may be used to

establish the timing of the contribution.

SMSF Contributions

In-specie transfer of listed shares or property

• A contribution by way of a transfer of an asset will be made when the

superannuation provider obtains ownership of the asset from the

contributor.

• Legal ownership – when the change of ownership or title is registered with

the Titles Office or Share Registry.

• Beneficial Ownership – when the seller gives the buyer a signed copy of the

transfer forms.

SMSF Contributions

In-specie transfer of listed shares or property

• The formal registration of the change of legal ownership occurs some time

after beneficial ownership of the property passes.

• In recognising this, the Commissioner accepts that a superannuation

provider may treat a contribution of property as made when beneficial

ownership of the property is obtained by the superannuation provider.

SMSF Contributions

Example – when In Specie contribution of real property is made

• Bob owns land on which retail premises have been constructed.

• Those premises include the site from which Bob runs his pharmacy

business.

• Bob decides to contribute the Business Real Property to his Self-Managed

Superannuation Fund.

• The fund has a Corporate Trustee, CarPharm Pty Ltd.

• Bob and his wife Janet are Directors.

SMSF Contributions

Example – when In Specie contribution of real property is made

• The Directors of CarPharm Pty Ltd resolve to accept the contribution of the

land on 1 June 2015.

• After obtaining advice from their Solicitor, Bob, as the owner of the land,

and Bob and Janet, as Directors of the Corporate Trustee, complete the

necessary land transfer forms.

• As Trustees they take possession of those forms and the relevant title

deeds on Monday, 29 June 2015.

• Therefore as at that date, Bob and Janet hold all the documents in

registrable form necessary to obtain registration of title to the land in their

capacity as Directors of the Corporate Trustee.

SMSF Contributions

Example – when In Specie contribution of real property is made

• Janet lodges the forms with the Registrar of Land Titles on 2 July 2015.

• CarPharm Pty Ltd is registered as owner of the land on 9 July 2015.

• What date is the contribution deemed to have been made?

• In these circumstances, Bob’s contribution will be made on 29 June

2015.

• Important consideration if looking to utilise the contribution caps.

SMSF Contributions

Example – when In Specie contribution of shares is made

• On 26 June 2015 Tony signs off an Off-Market Transfer form to effect a

contribution of shares from himself to Ronaldo Pty Ltd, the Trustee of his

Self-Managed Superannuation Fund.

• However, Tony leaves certain parts of the form blank for completion by his

Stockbroker, as the shares are Broker Sponsored.

• Tony posts the transfer form to his Broker on the same day.

• Tony’s Broker adds the omitted information on 2 July 2015 and completes

the transfer through CHESS.

• Ronaldo Pty Ltd is registered as a shareholder on 5 July 2015.

SMSF Contributions

Example – when In Specie contribution of shares is made

• What is the date the contribution to superannuation has been made?

• Tony’s contribution will be made on 2 July 2010.

• It is the day the relevant transfer form has been completed to registrable

form that a contribution has been made.

• In these circumstances, Tony’s contribution will be made on 2 July

2010.

• Again the timing is important with regard to contribution caps.

SMSF Contributions

Payment of fund expense

• The Commissioner recognises it has become common within some parts of

the superannuation industry for a person or employer to pay an expense on

behalf of a superannuation fund.

• The practice involves making journal entries after the expense is paid that:

– Re-classifies the expense payment as a superannuation contribution;

and

– Recognises the making of the contribution and payment of the

expenses in the accounts of the superannuation provider.

SMSF Contributions

Payment of fund expense

• Where a person pays an amount to a third party to satisfy a liability of a

superannuation fund, the fund is taken to have constructively received the

payment made to the third party on the superannuation fund’s behalf.

• The payment to the third party increases the capital of the fund because the

person’s payment of the superannuation fund’s expense extinguishes the

liability of the provider.

SMSF Contributions

Example – Contribution made by paying fund expense

• Snow has a Self-Managed Superannuation Fund of which she is the sole

member.

• During the 2014-15 income year Snow arranged accounting and audit

services to ensure the fund met its income tax and regulatory obligations for

the year ended 30 June 2014.

• Snow paid the accounting and audit fees for the fund from her own money.

• Snow did not reimburse her outlay from fund monies.

SMSF Contributions

Example – Contribution made by paying fund expense

• By satisfying a liability of the fund Snow has indirectly increased the capital

of the fund.

• Snow’s purpose of paying the liability of the fund without re-imbursement

increased the ultimate benefit she would receive from the fund.

• Therefore Snow made a contribution to the fund when she paid the

accounting and audit fees.

SMSF Contributions

Example – Contribution made by paying fund expense

• Be very careful if 65 or over and do not satisfy the work test.

• Members are unable to make a contribution to superannuation – even a

deemed superannuation contribution such as paying a fund expense.

• May be considered financial assistance to the SMSF or a loan.

• Could lead to significant financial penalties from the ATO!

SMSF Contributions

Non-concessional contributions cap

• If the member is 64 or less on 1 July of the financial year, the Non-

Concessional Contributions Cap is $180,000 per year or $540,000 over

three years.

• If the member is 65 but less than 75 on 1 July of the financial year, the Non-

Concessional Contributions Cap is $180,000 per year.

• Once a member attains age 65, superannuation funds can only accept

contributions if the member works at least 40 hours in a continuous 30 day

period in that same financial year, and

• PRIOR TO THE CONTRIBUTION BEING MADE!

SMSF Contributions

The “bring-forward” rule

• Taxpayers who are aged 64 or less on 1 July of the financial year may be

able to “bring forward” two years’ worth of their Non-Concessional

Contributions.

• $540,000 can be contributed over a three-year period.

• This “bring-forward” is not applied for or opted into.

• Once an eligible taxpayer’s Non-Concessional Contributions in the financial

year are greater than their Non-Concessional Contributions Cap (i.e.

$180,000) the “bring-forward” is automatically triggered.

SMSF Contributions

The “bring-forward” rule

SMSF Contributions

Example - The “bring-forward” rule

• During the 2014-15 financial year Brian, 40, makes personal contributions

of $210,000 to his fund, intending to claim a personal superannuation

deduction of $30,000.

• However, due to the downturn in his business, his taxable income for the

income year was only $15,000, so only $15,000 is allowable to him as a

personal superannuation deduction.

• Therefore, his Concessional Contributions for the financial year are $15,000

and his Non-Concessional Contributions are $195,000.

SMSF Contributions

Example - The “bring-forward” rule

• As Brian’s Non-Concessional Contributions ($195,000) were greater than

his Non-Concessional Contributions Cap ($180,000) and he was aged 64 or

less on 1 July of the financial year (and he was not already in a bring-

forward arrangement), the bring-forward rule is automatically triggered.

SMSF Contributions

Example - The “bring-forward” rule

• His first-year cap is three times the Non-Concessional Contributions Cap of

the first year – that is, $540,000.

• Brian’s second-year Non-Concessional Cap is his first-year cap ($540,000)

minus his first year contributions ($195,000) - that is, $345,000.

• Brian makes Non-Concessional Contributions of $180,000 in the second

year.

• Brian’s third-year Non-Concessional Contributions Cap is his second-year

cap ($345,000) minus his second-year contributions ($180,000) - that is,

$165,000.

SMSF Contributions

Example - The “bring-forward” rule

• Trent and Theo are twins. Both were aged 64 on 1 July of the financial year

but turn 65 in that year. Both are retired.

• Trent makes a contribution of $540,000 before he turns 65. He triggers the

bring-forward provisions and has a second year cap of $0.

• As he has no non-concessional contributions cap left, he makes no

contributions in either the second or third year.

SMSF Contributions

Example - The “bring-forward” rule

• However, Theo makes a contribution of $200,000 before he turns 65.

• He also triggers the bring-forward provisions, but his second-year cap is

$340,000.

• Theo sends a contribution of $180,000 to his fund on 30 June of the second

year.

• However, as he was 65 on 1 July of the second year and does not meet the

work test, his fund returns the amount.

• The fund will not report any contributions for Theo in the second year.

SMSF Contributions

Example - The “bring-forward” rule

• In the third year Theo’s bring-forward cap is again $340,000 (that is,

$340,000 - $0).

• He now takes on a job as a circus clown, working 10 hours a week, in order

to meet the work test.

• As he now meets the work test, his fund can accept member contributions

from him.

• He sends his fund a contribution of $340,000 on June 30 of the third year.

Question

• Can the Trustee of the fund accept the $340,000 contribution for the third

year from Theo?

SMSF Contributions

Example - The “bring-forward” rule

Answer

• No – as Theo was over 65 years old on 1 July of the financial year, his fund-

capped contribution limit for the third year is only $180,000 (despite the

bring-forward provisions being triggered) and the fund returns the excess

$160,000 to him.

• Theo has therefore only contributed $380,000 over the three years.

• If Theo had contributed the $340,000 in two amounts; say $180,000 and

$160,000 on different days the Trustee would have been able to accept

them as neither contribution is in excess of the $180,000 contribution cap.

• Source: ATO SuperUpdate August 2009

SMSF Contributions

Example - The non-concessional contribution cap

• A person, Richard, aged 55 years is a member of his SMSF (Old’n’Slow

Fund).

• During the 2014-15 financial year Richard made a contribution to

Old’n’Slow Fund by transferring an amount from his overseas bank

account.

• After conversion to Australian dollars the amount of the contribution was

$542,000. The full amount of the contribution was a non-concessional

contribution.

SMSF Contributions

Example - The non-concessional contribution cap

• The member, in his capacity as Trustee of Old’n’Slow Fund, has asked

whether the fund has to return the full amount of the contribution or only

$2,000, being the amount by which the contribution exceeds three times the

non-concessional contributions cap.

Question

• Is a Trustee of a SMSF required to return the whole of a fund-capped

contribution to a contributor if it is greater than three times the amount of

the non-concessional contributions cap for that financial year?

SMSF Contributions

Example - The non-concessional contribution cap

Answer

• As the member was aged 64 or less on 1 July of the financial year the

Trustee is only required to return that part of the fund-capped contribution

that exceeds three times the amount of the non-concessional contributions

Cap for the financial year.

• Had the member been aged 65 or more but less than 75 on 1 July of the

financial year, the Trustee would have been required to return that part of

the fund-capped contribution that exceeds the non-concessional

contributions cap for the financial year (i.e. $542,000 - $180,000 = $362,000

returned).

SMSF Contributions

Example - The non-concessional contribution cap

Answer

• For the 2014-15 financial year three times the amount of the non-

concessional contribution cap is $540,000.

• For the purposes of this regulation, the $540,000 is not reduced by other

non-concessional contributions made by the member to the Old’n’Slow

Fund (or any other fund) in that financial year or earlier financial years.

• In this case, the amount of $2,000 is required to be returned to the member

as $2,000 is the amount that the contribution of $542,000 exceeds three

times the Non-Concessional Contribution Cap for the 2014-15 financial year

of $540,000.

• Source: ATO ID 2008/90

SMSF Contributions

Refund of excess concessional contributions

• From 1 July 2013 excess concessional contributions refunded to the

member.

• Amount withdrawn is taxed at marginal tax rates, plus penalty interest to

reflect the fact the tax will be collected late.

• No limit to the number of times the refund can take place.

• Majority of ECT breaches are concessional contributions, which then

become non-concessional contributions.

• If excess not withdrawn then counts as a non-concessional contribution.

SMSF Contributions

Refund of excess non-concessional contributions

• Now LAW (received Royal Assent 19 March 2015).

• Refund of excess non-concessional contributions, plus associated earnings

can be released from super.

• Earnings taxed at individual’s marginal tax rate.

• The individual provided with ability to release excess plus earnings and

therefore have no excess non-concessional contributions.

• Applies from 1 July 2013 onwards.

• If contributions not released, the old laws apply.

SMSF Contributions

Refund of excess non-concessional contributions

• Commissioner must make a written determination.

• If individuals elect to release the excess contribution it is irrevocable.

• Must be made within 60 days of the Commissioner’s determination.

• Associated earnings are approximated.

• Approximated earnings included in the individual’s assessable income.

• Earnings are calculated using an average of the General Interest Charge

(GIC) for the 4 quarters in the financial year.

• Compounded on a daily basis.

SMSF Contributions

Example

• Belinda had excess non-concessional contributions of $100,000 in the

2013/14 financial year.

• The Commissioner issues Belinda an excess non-concessional

determination on 1 November 2014.

• Earnings are calculated as follows:

• 0.02646575% x ($100,000 plus the sum of the earlier daily proxy amounts)

for the 489 day period from 1 July 2013 until 1 November 2014.

• The result of the formula is associated earnings of $13,814.

SMSF Contributions

Refund of excess non-concessional contributions

• If there is no longer any money in super (because the member has received

a lump sum payment) the full amount of the earnings will still be included in

the individual’s assessable income.

• A payment in response to a release authority must be paid from the tax-free

components.

• The amount released itself does not have any tax consequences for the

individual – other than the earnings included in assessable income.

• If there is not enough in the fund, the Commissioner may allow the member

to nominate another fund.

SMSF Contributions

Contribution Strategies – turning 65 in the FY

• If the member is 64 or less on 1 July of the financial year, the non-

concessional contributions cap is $180,000.

• Unless the bring-forward rule has been automatically triggered.

• To use the bring-forward rule if 65 or over, must trigger before turning 65.

• Must also satisfy the work test once turned 65.

SMSF Contributions

Example – turning 65 in the FY

• Bill is 64 on 1 July 2015.

• He contributes $190,000 non-concessional contribution to his SMSF.

• He has therefore triggered the bring-forward rule automatically.

• During the 2015-16 financial year, after turning 65, Bill wishes to contribute

a further $350,000 as a single contribution.

• He can do this, as he was 64 on 1 July 2015 (he has up until 30 June 2016

to make this contribution).

• The only requirement is that, after the age of 65, he must satisfy the

work test prior to making the contribution.

SMSF Contributions

Example – turning 65 in the FY

• If Bill does not use remainder of the bring-forward provisions in the 2015-16

financial year, he can still use them in 2016-17.

• Bill could still contribute $350,000 to his SMSF in 2016-17.

• Even though he is 65 years of age!

• However two elements must now be satisfied:

– He must satisfy the work test prior to the contribution

– Each contribution must be up to his fund-capped contribution limit.

• So $350,000 would need to be contributed in two lots – one for $180,000

and one for $170,000.

SMSF Contributions

Example – turning 65 in the FY

• Bill still has the bring-forward provisions in 2017-18.

• So even if he contributes nothing in 2016-17, he can still contribute

$350,000 in the following year.

• Again, two elements must now be satisfied:

– He must satisfy the work test prior to the contribution

– Each contribution must be up to his fund-capped contribution limit.

• $350,000 would need to be contributed in two lots as his fund-capped

contribution limit as a 65+ year-old is $180,000 (not indexed).

• The opportunity is lost thereafter.

SMSF Contributions

Using a Contributions Account

• It is like an suspense account as it holds contributions for a short time

before they are allocated to a member.

• Must be allocated within 28 days of the month following that in which the

contribution is made.

• Therefore a contribution made in June must be allocated to a member by

28 July.

• It is recorded against the member’s cap in the year of allocation – not the

year of contribution.

SMSF Contributions

Example - Using a Contributions Account

• Jason, aged 45, is a member of an SMSF and makes a personal

concessional contribution of $30,000 on 4 April 2015.

• He makes a further $30,000 personal concessional contribution on 28 June

2015.

• The contribution in June is applied to an unallocated contributions account

established in accordance with the fund’s governing rules.

• On 4 July 2015 the Trustee resolves to allocate the contribution to Jason.

SMSF Contributions

Example - Using a Contributions Account

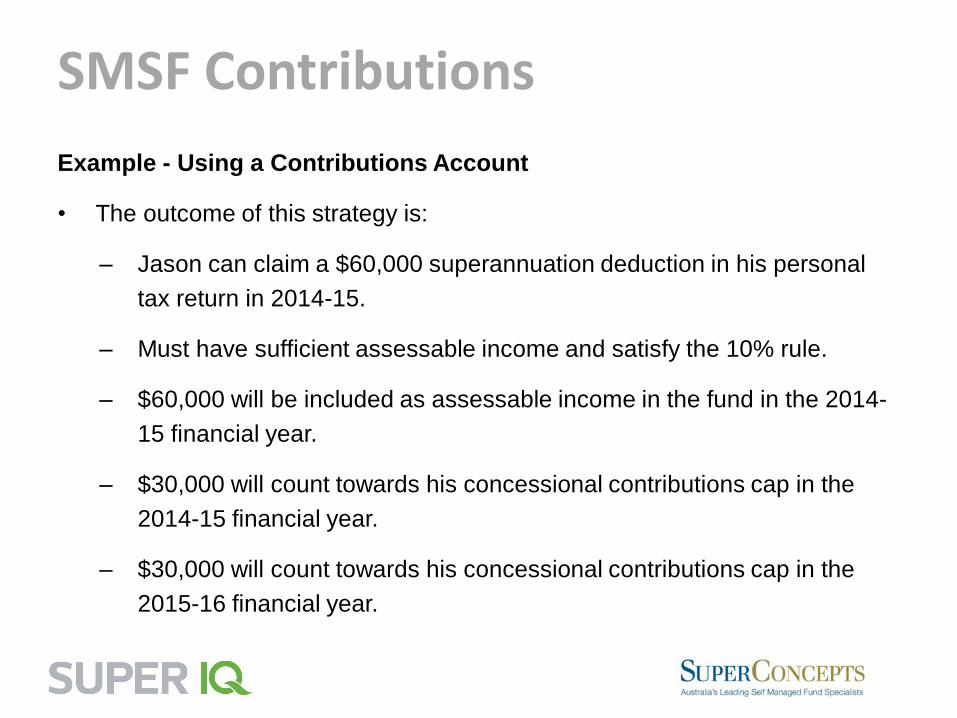

• The outcome of this strategy is:

– Jason can claim a $60,000 superannuation deduction in his personal

tax return in 2014-15.

– Must have sufficient assessable income and satisfy the 10% rule.

– $60,000 will be included as assessable income in the fund in the 2014-

15 financial year.

– $30,000 will count towards his concessional contributions cap in the

2014-15 financial year.

– $30,000 will count towards his concessional contributions cap in the

2015-16 financial year.

SMSF Contributions

Example - Using a Contributions Account

• The ATO systems cannot cope with this strategy.

• The ATO will incorrectly assume $30,000 has been allocated to Jason on 28

June 2015.

• This means an incorrect ATO Excess Contributions Tax (ECT) Notice will be

issued.

• Jason will then need to lodge an objection and explain how a Contributions

Account was being utilised.

• Must have supporting documentation!

SMSF Contributions

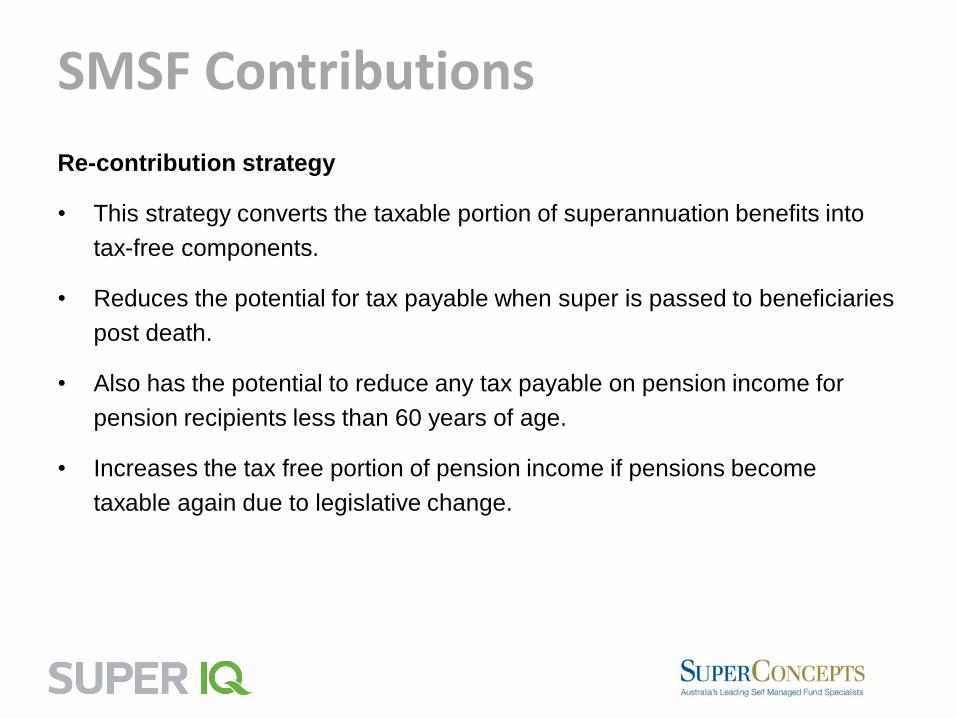

Re-contribution strategy

• This strategy converts the taxable portion of superannuation benefits into

tax-free components.

• Reduces the potential for tax payable when super is passed to beneficiaries

post death.

• Also has the potential to reduce any tax payable on pension income for

pension recipients less than 60 years of age.

• Increases the tax free portion of pension income if pensions become

taxable again due to legislative change.

SMSF Contributions

Example - Re-contribution strategy

• Peter, 57, and retired, has $400,000 in his SMSF.

• $200,000 is a taxable component.

• Peter could withdraw $360,000 from his SMSF and the tax situation would

be as follows:

– $180,000 tax free component – 0% tax.

– $180,000 taxable component – tax free up to low tax threshold of

$185,000

• Therefore the tax impost would be nil.

SMSF Contributions

Example - Re-contribution strategy

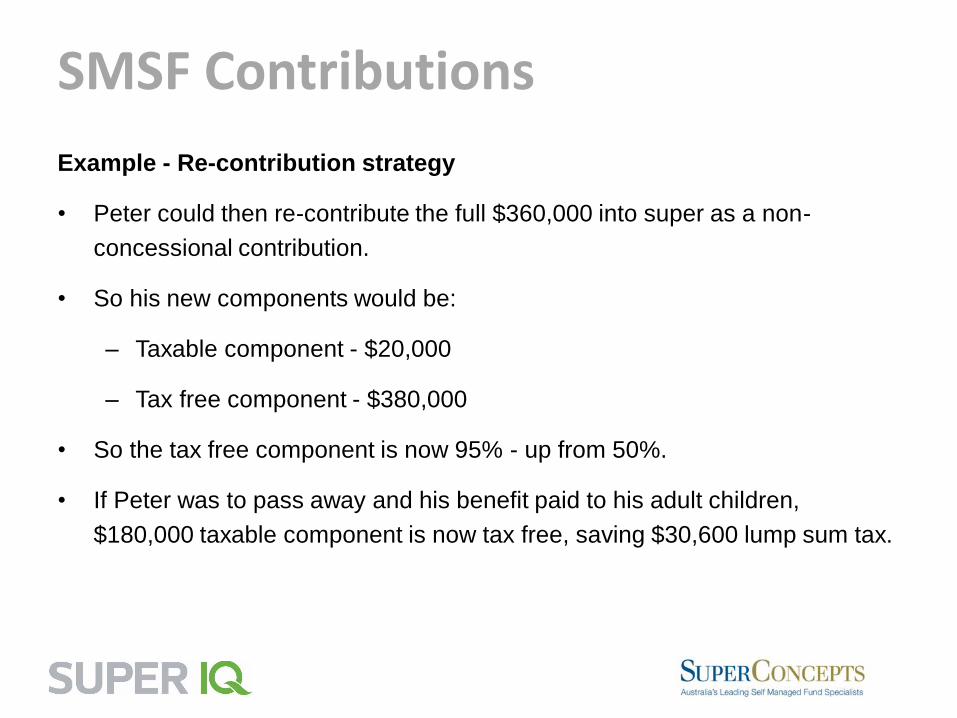

• Peter could then re-contribute the full $360,000 into super as a non-

concessional contribution.

• So his new components would be:

– Taxable component - $20,000

– Tax free component - $380,000

• So the tax free component is now 95% - up from 50%.

• If Peter was to pass away and his benefit paid to his adult children,

$180,000 taxable component is now tax free, saving $30,600 lump sum tax.

SMSF Contributions

Example - Re-contribution strategy

• Is this Part IVA – i.e. tax avoidance?

• No – the ATO have stated this is not tax avoidance.

Tax free component Taxable component

Initial super balance $200,000 $200,000

Withdrawal $180,000 $180,000

Remaining components in fund $20,000 $20,000

Re-contribution strategy $360,000

Components after re-contribution $380,000 $20,000

SMSF Contributions

Conclusion – Utilise contributions strategies!

• Superannuation is the best tax structure for retirement savings.

• Understand how the caps work and how to best utilise them.

• Timing of contributions is crucial – especially in-specie contributions.

• If approaching 65 consider maximising benefits using the bring-forward rule.

• If looking to maximise a tax deduction in a particular financial year, look at

utilising the use of an Unallocated Contributions Account.

• And a re-contribution strategy can provide enhanced estate planning

benefits as well as future-proof your benefit against legislative risk.

Services to support SMSF Trustees

How can we help?

• Contact your Fund Accountant or Client Service Representative for

– Contribution rules

– In-specie transfer of assets

– Concessional and non-concessional caps

• Use your Dashboard functionality to ensure you do not breach the caps and

to make the most of your caps!

• Speak with our Technical Team if:

– You or any of your clients have breached the caps

– You would like to make an appointment to discuss contribution and other strategies

Disclaimer

This presentation was prepared by SuperIQ Pty Ltd (ABN 27 147 105 164) (“SIQ”).

Material contained in this presentation is a summary only and is based on information believed to be reliable and received from sources within themarket. The information is believed to be accurate at the time of compilation and is provided by SIQ in good faith. However, the statements includingassumptions and conclusions are not intended to be a comprehensive statement of relevant practice or law that is often complex and can change. It isnot the intention of SIQ that this presentation be used as the primary source of readers’ information but as an adjunct to their own resources andtraining.

To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. SuperIQ does notguarantee the performance of any fund or the return of an investor's capital. No representation is given, warranty made or responsibility taken as tothe accuracy, timeliness or completeness of any information or recommendation contained in this publication and SIQ will not be liable to the readerin contract or tort (including for negligence) or otherwise for any loss or damage arising as a result of the reader relying on any such information orrecommendation (except in so far as any statutory liability cannot be excluded).

Individual circumstances, in particular relating to self managed superannuation funds, may vary greatly. This presentation has been prepared forgeneral information purposes only and not having regard to any particular person’s investment objectives, financial situation or needs. Accordingly,no recommendation (express or implied) or other information should be acted upon without obtaining specific advice from an authorisedrepresentative.

See your future clearly

1300 660 598

superiq.com.au

1800 625 644

superconcepts.com.au

![SMSF webinar Sep 14.pptx [Read-Only]€¦ · •Changes to Asset tests mean less people accessing the pension or receiving smaller benefits. Super Statistics •Contributions for](https://img.dokumen.tips/doc/110x75/5ff747ec33c5e0391d3d7980/smsf-webinar-sep-14pptx-read-only-achanges-to-asset-tests-mean-less-people.jpg)

![SMSF Borrowing Rules[1]](https://img.dokumen.tips/doc/110x75/577d20e71a28ab4e1e93feca/smsf-borrowing-rules1.jpg)