Embed Size (px)

Citation preview

Smart Mobility in Israel

Powered by:

32 Smart Mobility in Israel

Tel AvivMarch 2019

Research: Yarden Halachmi, Eliya Cohen

Writing: Yarden Halachmi, Eliya Cohen

Analysis: Yarden Halachmi, Eliya Cohen

Editing: Gedalyah Reback, Eliya Cohen

Design: Hadas Shezaf

Special thanks to: Hemdat Sagi- Konnect

Credits

Copyright & DisclaimerGeek Media Online Communication Ltd ("Geekmedia"), the leading tech media company in Israel, is excited to offer you report focused on the Israeli ecosystem.

Geekmedia retains all rights to its database and to any of the information provided as part of this report and any rights related thereto. Nothing herein shall derogate from Geekmedia's right to continue using such information in any way. This report is protected by copyright law and no portion of this report may be photocopied, reproduced or scanned into an electronic system or transmitted, forwarded or distributed in any way without prior consent of Geekmedia.

The information contained in this report is derived from carefully selected sources we believe are reasonable, including without limitation, a database aggregated by Geekmedia. We do not guarantee its accuracy, reliability or completeness and nothing in this report shall be construed to be a representation of such a guarantee. Geekmedia accepts no responsibility for any liability arising from use of this report or its contents and nothing herein shall constitute or be construed as an offering of financial instruments, or as investment advice or recommendations by Geekmedia of an investment or business strategy.

This report contains forward-looking statements, including but not limited to comments regarding predictions. Forward-looking statements address future events and conditions and therefore involve inherent risks and uncertainties. We assume no liability for any such statements or for their interpretation, nor do we assume liability for future uses of information contained in this report or whatever actions you may take as a result of having been exposed to such information. Any advice received via this report should not be relied upon for personal, legal or financial decisions and you should consult an appropriate professional for specific advice tailored to your situation.

54 Smart Mobility in Israel

MethodologyAbout

Geektime is the largest tech platform in Israel, focusing on global innovation and reporting on the Israeli startup ecosystem. In addition to our in-house content, we are the primary voice for investors, entrepreneurs, fellow geeks and tech enthusiasts, helping them cut through regional boundaries and compete in the global marketplace.

Since its birth in 2009, Geektime has become the key startup and tech media outlet in Israel, providing our audience with their daily fix of news, updates and articles on various topics in technology, quickly becoming a withdrawal-inducing morning, afternoon and evening vice for its readers. Geektime boasts a reader base of more than 2,000,000 monthly visitors with a massive social media presence. These are die-hard tech lovers, entrepreneurs, C-level managers and developers who know their startups, devices and novel technologies — and Geektime is their trusted source for everything tech.

Beyond covering the technology sphere, Geektime, based in Tel Aviv, Israel, also produces and hosts many of Israel’s leading tech events, providing front and center media coverage of the latest and greatest coming out of the Israeli startup, IT and entrepreneurship scenes.

As part of our mission to become the hub for everything high tech, Geektime has launched the first Israeli employer branding platform, "Geektime Insider", and a walk-through guide for accelerators for the Israeli community, named "Geektime Accel".

In this report, we sought to combine our own in-house capabilities and complement them with as many external sources as possible (data, expertise and opinions). The report consists of data gathered by us with the help of many local industry experts and insiders – OSINT and HUMINT combined with information from our own database. The predictions chapter was based on insider information regarding technological and regulatory advancements uncovered and elaborated on in extensive research, and interviews, all bound to a coherent text by some of our best and brightest.

In this report, we try to give readers as clear an overview of the full scope of Israel’s mobility ecosystem as possible. In the deals chapter, we focus only on first deals, omitting transactions such as public-to-private, post-IPO M&As and secondary buyouts. The sample of companies featured in this report was chosen because either mobility is at the core of their product or mobility is at the center of their respective business plans. In addition, we showcase only companies with a substantive connection to Israel, such as those who continue to retain headquarters or the bulk of their staff in the country. Additionally, in this report, we chose only a few companies that showcase a desired point. We mention only a few of the amazing companies in each segment, but deeply respect all of the projects in our ecosystem.

About Geektime Research

Our research department is a unique team that focuses on data intelligence and analytics, with a deep understanding and familiarity of both high tech and startup industries worldwide. Our team of experts consists of techies, analysts and lawyers, with decades-long experience in tech, research, regulation and everything nice.

The sample will probably suffer from both Type I and Type II errors. especially for sectors as communications or cybersecurity, where the majority of the companies in the ecosystem claim to be connected to the mobility sector in some manner. Moreover, the stealth nature of some startups and projects should be considered although they do not impact the numbers presented here. Additionally, deal data –as always – is prone to underestimation due to several factors, such as confidentiality and secrecy.

Furthermore, as in any economic transaction, there were islands of missing data on account of the desire of one or more parties to a transaction or the terms of certain agreements.

We attempted to avoid bias. Our report is a sincere and deep effort to understand the general trends in the market and transmit real value to analysts, investors, entrepreneurs, and others who will read this report.

We are truly sorry if we unintentionally omitted one (or more) of the amazing, hard-working, brilliant projects that were worked in our ecosystem and want to assure you that it was not done on purpose. If we are lacking any data, be they large gaps or small details, if please inform us and we will amend our data. If you notice inaccuracies, companies that should have been included but were not, or numbers that do not make sense according to your personal knowledge, we would love to hear from you.

76 Smart Mobility in Israel

Cars provide mobility for billions of people around the world. For this to happen with maximum environmental compatibility, smart traffic management solutions and new utilization concepts will be required. The Volkswagen Group’s vision is to become a globally leading provider of sustainable mobility. In order to reach this goal, the group is investing heavily in the mobility of the future: over €44 billion have been budgeted up to the end of 2023 for e-mobility, autonomous driving, digital connectivity and new mobility services. The joint ventures in China will be spending a further €15 billion on the electric offensive over the coming years. E-Mobility

Volkswagen is driving e-mobility forward with a consistency and commitment unlike that of virtually any other automaker. The Group is planning to launch almost 70 new electric models in the next ten years – instead of the 50 previously planned. As a result, the projected number of vehicles to be built on the Group’s electric platforms in the next decade will increase from 15 million to 22 million.

The Volkswagen brand in particular will be putting attractive models at affordable prices on the road, paving the way for the breakthrough of electric vehicles worldwide. The electric strategy is based on the modular electric drive matrix (MEB), a technology platform developed specifically for electric vehicles. Expanding e-mobility is an important building block on the road to a CO2-neutral balance.

THE VOLKSWAGEN GROUP VISION ON SMART MOBILITY

Autonomous Driving

Volkswagen developing autonomous driving tech technologies in Munich, the US West Coast and soon in China as well. Partnerships play an important role in this transformation. For example, Volkswagen is cooperating with Mobileye and Champion Motors to develop the first ride-hailing service with driverless cars in Israel starting in 2019, as published in the Israeli media.

In addition, Volkswagen is also a new partner in the Chinese technology platform Apollo. The consortium founded by Internet company Baidu develops technologies for autonomous driving.

Connectivity

With technology partners such as Microsoft, Volkswagen is developing the digital ecosystem for the connected mobility of the future. Connectivity will cover the entire value creation chain and all modes of transport, bringing about a momentous change.

New Mobility Services

In 2019 Volkswagen has launched MOIA - a highly efficient ride-pooling service with environmentally friendly electric vehicles in Hamburg and Hannover in Germany. Customers can book the service via a smartphone app and simply enter their location and destination and the MOIA vehicle arrives at a virtual stop no more than 250 meters away. Pooling individual journeys makes more efficient use of the streets – not least because the downtown parking situation is eased, with fewer drivers searching for a parking slot.

“I believe that Innovation is crucial for success and for the long-term existence of any technology company and Volkswagen Group is no exception. Driving innovation and transferring it into our products and services is therefore a core task for us. We will continue to offer our customers around the world products and services with outstanding technologies. With Konnect and our presence in Israel, we make sure that we are continuously at the forefront of innovation.” Axel Heinrich, Head of Volkswagen Group Innovation

Table of Contents

Executive Summary 10

Smart Mobility Overview 13

Israel Smart Mobility Market 16

Israel by the Numbers 19

Segments 29

Regulation and Public Spending 49

Predictions 55

98 Smart Mobility Report

Dear Innovators,

Less than a year ago we have launched Konnect- the Innovation and Business Development arm of Volkswagen Group and its twelve brands in the Israeli market.

Since its launch, Konnect has introduced and exposed numerous Israeli startups to the Volkswagen Group, facilitated several B2B delegations from abroad and supported on technological Projects and PoC’s on a wide variety of topics such as connectivity, sensors, Industry 4.0 and smart mobility.

It’s been an exciting journey for us and I am proud to see how many of our Volkswagen Group Brands are active in the market, identifying the need to work closely in this vibrant innovation eco-system and expanding the Volkswagen Group cooperation’s in Israel.

As a strong believer in the great talent coming from Israel and the value it offers to the Volkswagen Group, the Konnect team will continue to bring the “Chutzpa” element back to our Headquarters and push for more collaborations and business partnerships.

This Smart mobility report is a result of a unique collaboration with Geektime and we are excited to share it with our partners internally and externally, and emphasize Israel’s significance and relevance in the global mobility market.

If you wish to get in touch with our Group, please contact us: [email protected]

We wish you an enjoyable read. Lehitraot & Stay Konnected!

Stephanie VoxManaging Director, Konnect- Volkswagen Group Innovation Tel Aviv

Photo: Elad Malka

1110 Smart Mobility in Israel

Executive Summary

Executive Summary

World- According to the European Commission, the yearly European transport costs are over €1 trillion. almost 7% of the current EU’s GDP - The American economy lost more than $300B in 2017 because of traffic congestion, equivalent to 5.5B hours a year of waiting in traffic.

- A clean, safe, holistic, viable, inclusive and user-friendly solutions are required

Companies Sectors-The hardware sector, with 27% of the total companies, is currently the biggest sector.

-The software sector is the second largest and the leading sector over the last three years with 24 new companies.

-Data & diagnostics is the second largest sector over the last 3 years with 20% of the new companies.

Companies Segments-The autonomous segment, which showed consecutive growth between 2012-2017, is the leading segment with 78 companies.

-59 new companies were founded in the electrification segment making it the second largest segment.

-2016 was the best year for smart mobility companies. The data shows that 54 new companies were founded during that year.

Investments-$515M were raised through 2018, a 32% decline in funds invested in smart mobility startups from 2017.-There were 41 funding rounds in 2018, a 6% decline from 2017.-The average round size was $12.56M

The Cost of European

Transport in 2017

€1T

United States Congestion Costs in 2017

€250B(~$283B)

25% of that isEuropean

Congestion Costs

$300BTop Investors (2016 -2018)

Count Sum

1 Maniv Mobility Pitango Venture Capital

2 Canaan Partners Volkswagen Group

3 OurCrowd Daimler

Israeli Mobility Companies by Sectors

Data & Diagnostics53

Delivery15

Energy29

Fleet Management21

Hardware98

Navigation28

Safety23

Software64

Other30

Israeli Mobility Companies by Segments

Autonomous78

Connectivity46

Electrification59

Cyber17

MaaS29

Urban Smart Mobility50

Other82

Israel-Israel’s road congestion is the highest among all of the OECD members.

-It costs the local economy 1.5% of the annual GDP.

-The estimated yearly loss caused by congestion is NIS 35B.

-Reliance on private transportation is higher than the OECD average.

-The state comptroller of Israel published a special report regarding the dire state of public transportation in Israel, aligning with similar OECD reports which put Israel far behind its average.

-Investment in public transportation fell to less than 1% of the GDP between 2013 and 2018.

-The government invested as low as 0.7% of the country’s GNI in to public transport.

-The state of public transportation in the country remains problematic despite a NIS 4.8B subsidy which was transferred from the Israeli government to public bus services in 2017.

-According to the IMF, the infrastructure gap between the comparable countries and Israel amounts to 35-40% of the GDP

The Problems

The Solution

Smart MobilityOverview

1312 Smart Mobility in Israel

1514 Smart Mobility in Israel

Each of the aforementioned patterns requires a different solution to the aforementioned equation. Each one encapsulates a varying combination of mobility components. Moreover, each criteria (such as age, socioeconomic status, local geography, and gender) dictate variations in solving the equation. Economically speaking, the meeting point of preference hierarchies and of supply and demand, dictate the direction of the mobility ecosystem’s near-term evolution.

It is clear that there is a wide efficiency gap in the mobility universe which profusely bleeds resources and is needed to be closed. Technological innovation will help close that gap.

Smart MobilitySmart mobility seeks to solve the abundant problems presented by the traditional mobility industry via the implementation of cutting-edge technologies. The concept stretches through every mode of transportation. The list goes from buses to drones, kick scooters to autonomous vehicles, even walking. The term can be used in varying situations and currently

A recent study by the European Commission found that European Union transport costs over €1 trillion annually, which amounts to almost 7% of the current total EU GDP. This massive resource waste happens through air pollution, carbon emissions, congestion, accidents and other external costs. Congestion alone accounts for more than 25% of the cost. The hefty price of inefficiency is paid by society as a whole, rather than by the specific transportation users. Data regarding congestion costs in the US is no less discouraging. A study found that the American economy lost more than $300B in productivity in 2017 because of traffic congestion, accumulating to massive 5.5B hours a year wasted waiting in traffic.

*MobilityIn complicated terms, mobility is a resource optimisation equation solution, answer to which depends on network- based answers to various questions such as: Where from (origin)? Where to (destination)? How (what route)? What (a person, a group, freight, etc.)? In more simple terms, mobility is just moving from one geographical location to another.

Mobility Categories

Typology

1 32Individual Mobility Includes several modes of mobility which, serve the individual in his/her quest to get from point A to point B. This category includes examples such as private cars and micromobility solutions (bicycles, electric scooters, etc.).

Repetitive Includes: 1. Daily work-to-home movement. 2. Routine actions such as weekly shopping. 3. Professional route patterns such as mail and package routes.

Freight Mobility The movement of goods. This category covers trucks, freight trains, and ships as the main means of this category of transportation. (also known by the Yiddish term: schlepping).

Transit/ Mass Mobility Includes the movement of several individuals together, usually in a pre scheduled route. In other words: planes, trains and buses.

Non- repetitive Consists of such components as: 1. Work-related a meeting, or a professional house call. 2. Recreational going to the theater, a restaurant or a movie. 3. Touristic long distance trips.

represents anything from marketplaces to the creation of flying autonomous vehicles. The technology used in the framework of the term can be as small as a computer chip designed for mobility AI, or as large as a whole fleet of cargo ships.

The solutions should be holistic, clean, safe, viable, user friendly and inclusive (not necessarily in that order). Smart mobility solutions should allow the traveler to choose the optimal, integrated door-to-door answer for her need. Moreover, the solution should address carbon-emission and pollution problems. Additionally, smart mobility should contribute to a sharp reduction in mobility-related injuries. To allow the smoothest and fastest integration into the everyday life and encourage high adoption rates, innovators should notice the economic and the inclusion aspects. Smart mobility solutions should be affordable and accessible, encouraging users to seamlessly adapt to the novel technologies.

The Cost of European

Transport in 2017

€1T25% of that is

European Congestion

Costs

United States Congestion Costs in 2017

€250B(~$283B)

$300B

Israel Overview

1716 Smart Mobility in Israel

IMF recently noted that the infrastructure gap between Israel and the comparable countries amounts to 35-40% of the GDP. A study conducted by McKinsey for an Israeli ministry reports a gap of 20% of the GDP.

Reliance on private transportation in Israel is disproportionately high compared to other OECD countries. In a 2014 OECD study on road traffic density per network length, Israel’s ratio was more than three times higher than the OECD average, with 325 vehicles per 1,000 citizens.

At least partially, this abnormal reliance on private transportation is due to acute public distrust in local public transportation solutions. The low satisfaction rates, partially stemming from chronically low efficiency, combined with the lack of public transportation during the Sabbath, seem to almost force the public to seek private mobility solutions.

The dire state of public transportation prompted the state comptroller of Israel to publish a special report (13/03/19) regarding the shortcomings of the mass transportation in the country. In the report, the comptroller’s office mentioned the high price of road

Israel Smart Mobility Market

Israel presents itself as an extremely interesting case study for mobility. There is a unique blend of challenges which present opportunities both for the growth and the evolution of the local ecosystem. and as it was proven before, the world.

Challenges

A 2018 OECD paper on Israel states that “Israel has a large infrastructure deficit, especially in public transport”. This deficit is causing the economy to lag behind in several areas, from massive road congestion, to pollution, to widening the wealth gap between social groups, partially based on geography.

For example, looking at congestion-related resource waste, the OECD recently estimated that road congestion in Israel is the highest among all organization members and costs the local economy as much as 1.5% of its GDP annually, about 30%-50% higher than the EU average (depending on the source of EU information). In 2016, the Israeli Ministry of

Finance, Israeli Ministry of Transport, and governmental planning agencies estimated the annual loss caused by congestion at NIS 35B (close to $10B at current exchange rate). They further forecast that, absent major changes, the losses liable to double by 2040 to NIS 70B, adding an hour per day per citizen on average to the time currently spent in traffic.

Moreover, the investment in public transportation fell to 0.9% of GDP in 2013-2018 (as stated by the Governor of the Bank of Israel), an almost 20% cut from the previous five year period in GDP percentage. Another OECD study found that the percent of governmental investment in public transportation in Israel was as low as 0.7% of the Israeli GNI, almost 15% lower than the OECD average. Additionally, a NIS 250B, 25-year strategic plan for development of public transportation by the Israeli Ministries of Finance and Transport published in 2012, fell farshort of expectations. In the first three years of execution, governmental investment was almost 45% less than planned, due to the slow implementation rates of the plan. A 2017 subsidy of NIS 4.8B transferred by the Israeli government to public bus services did little to improve transit services.

An assessment made by OECD states that, ”(t)he management and implementation of large infrastructure projects is often deficient, and the planning process is lengthy and weak.”Public investment in Israeli infrastructure has dropped below 2% of the local GDP in recent years, compared with an average of 3% dating back 25 years ago. The

Annual Cost of Congestion in Israel

₪35B

“Israel has a large infrastructure deficit, especially in public transport"

OECD 2018

congestion in Israel, the high density of transportation in the country, the low satisfaction rates from the public transportation service, the crowding of the transportation (buses and trains) during peak hours, the long travel times, bad connectivity between the means of transportation, unsatisfactory positioning of stations, and other factors.

The mother of invention

Plato’s statement in his monumental Republic, “necessity is the mother of invention” (Book II, 369c), is extremely appropriate in our case. When public solutions are lacking, private initiatives might close the evident gaps of preference and possibilities in the mobility ecosystem.

Moreover, underinvestment in infrastructure provides an opportunity for leapfrogging, or out-innovating countries that do not massively invest in the newest technologies due to relatively recent upgrades. In fact, one of the main recommendations of the 2018 OECD study was to“(u)se public-private partnership agreements, especially in public transport, following a careful and clear allocation of their risks”, which means that public sector funding in Israel should shift the environment in the right direction toward innovative mobility solutions.

As a result, the Israeli tech scene might be one of the better breeding grounds for mobility innovation in the world, with technology serving as a stopgap- closer which solves for real and critical needs of the market.

The most appropriate example of Israeli innovation is the biggest M&A deal in the history of the country. Mobileye, which had several rounds by some of the strongest global players, summing up to more than $500M, went public at a $4.2B valuation, raising $890M, delisting itself, later to be acquired for $15.3B, stands out as a great beacon for the local ecosystem.

Israel Overview

1918 Smart Mobility in Israel18 19Smart Mobility Report

Israel by the Numbers

In this section, we will provide a dissection of the Israeli mobility ecosystem across several dimensions. Sectors relates to the core of the companies’ product. We arranged the companies according to several different sectors in order to better understand the ecosystem division. Segments relates to the main use of the product by the various areas of mobility. Stages represents the current phase of the company and is divided across four categories (Seed, Early, Growth, Bootstrap). The years are related to the founding year of the companies by sector and by segment, while the years indicated in the investment section are related to the year of round completion, going back three years.

2120 Smart Mobility in Israel

Un-known Earlier 2010 2011 2012 2013 2014 2015 2016 2017 2018 Sum

0 8 2 4 4 4 6 2 10 10 3 53

0 0 0 0 0 3 4 2 2 4 0 15

1 7 0 1 2 3 4 2 6 3 0 29

3 7 0 0 0 1 0 2 4 2 2 21

4 20 1 7 10 8 13 14 12 7 2 98

0 6 1 1 0 4 5 6 2 2 1 28

3 1 0 2 1 0 4 1 6 3 2 23

2 9 4 4 3 4 2 12 10 12 2 64

5 3 1 2 1 5 4 4 2 3 0 30

18 61 9 21 21 32 42 45 54 46 12

Israel Numbers

Israeli Mobility Companies Founding by Year, by Sector

Data & Diagnostics

Delivery

Navigation

Fleet Management

Software

Energy

Safety

Hardware

Other

Sum

By Sectors

Companies

Israeli Mobility Companies by Stage, by SectorSeed Early BootstrappedGrowth

Data &

Diagnostics

Delivery

Navigation

Fleet

Management

Software

Energ

y

Safety

Hardware

Other

30

35

12

8

3

1111

2

5

3

16

3

6

2

14

2

7

13

20

9 10

20

14

9

5

10

5

4

6

17

5

6

2

17

6

13

53 15 29 21 98 28 23 64 30

The biggest sector among the mobility companies is hardware, with 98 companies, which sums up to 27% of the total companies count. However, over the last 3 years, the hardware sector consists of less than 20% of the new companies count, ranking it third. The second largest overall, the software sector is leading in the last three years, with 24 new companies founded between 2016-2018 which are 21% of the total. The third largest overall sector is data & diagnostics, with 23 new companies during this period which is 20% of the total count. Only five navigation focused companies were

founded during the last 3 years, making it the smallest sector in this count.

The hardware sector is the leading sector in every stage. 25% of the seed stage companies belong to the hardware sector. Out of the early stages companies, 25% belong to the hardware sector and 34% of the growth stage companies are hardware related. Interestingly, the three leading sectors (hardware, software and data) sum to more than two thirds of all eraly stage startups, and more than half of all bootstrapped projects.

Number of Companies

2322 Smart Mobility in Israel

Israeli Mobility Companies Founding by Year, by Segment

By Segment

Companies

Autonomous

Connectivity

Urban Smart Mobility

Cyber

Electrification

MaaS

Other

Sum

Un-known Earlier 2010 2011 2012 2013 2014 2015 2016 2017 2018 Sum

0 13 1 4 3 5 8 12 13 14 5 78

6 7 2 2 1 8 4 7 5 2 2 46

2 11 2 6 8 6 7 3 7 7 0 59

0 1 2 0 1 1 0 2 6 3 1 17

1 2 0 5 0 1 4 4 3 7 2 29

0 8 1 1 4 3 8 9 10 6 0 50

9 19 1 3 4 8 11 8 10 7 2 82

18 61 9 21 21 32 42 45 54 46 12

Israeli Mobility Companies by Stage, by SegmentSeed Early BootstrappedGrowth

Autonomous

Connectivity

Cyber

MaaS

Urban Smart

Mobility Oth

er

Electr

ifica

tion

78 46 59 17 29 50 82

Number of Companies

26

1717 18

10

7

1613

6

21

12

57

5

13

18

712

32

7

1429

18

5

1224

8

Israel Numbers

The leading segment of this report is Autonomous, which showed consecutive growth over six years between 2012-2017. Although there was a 64% decline in the amount of new companies in 2018, it is still on top of the list with 78 companies. Electrification, although no new companies were founded in 2018, is the second largest segment, with 59 companies overall. On a yearly view, 2013 saw a 53% increase, from 21 to 32, in the amount of new companies in those segments. This trend reached it peak in 2016, when 56 new companies were founded. 2017 saw a 17.4% decline and in 2018 only 12 new companies were founded, which means there has been a 73.9% decline.

Autonomous is the leading segment among the early stages, consisting 30% of the seed stage companies and 26% of the early stage companies. Electrification is the largest sector among the growth stage companies with 24 companies, 33% of the total count. Urban smart mobility (32% of the total) has only one more company than Autonomous (30% of the total) when looking at bootstrapped companies.

2524 Smart Mobility in Israel

Israel Numbers

Investment2016 2017 2018

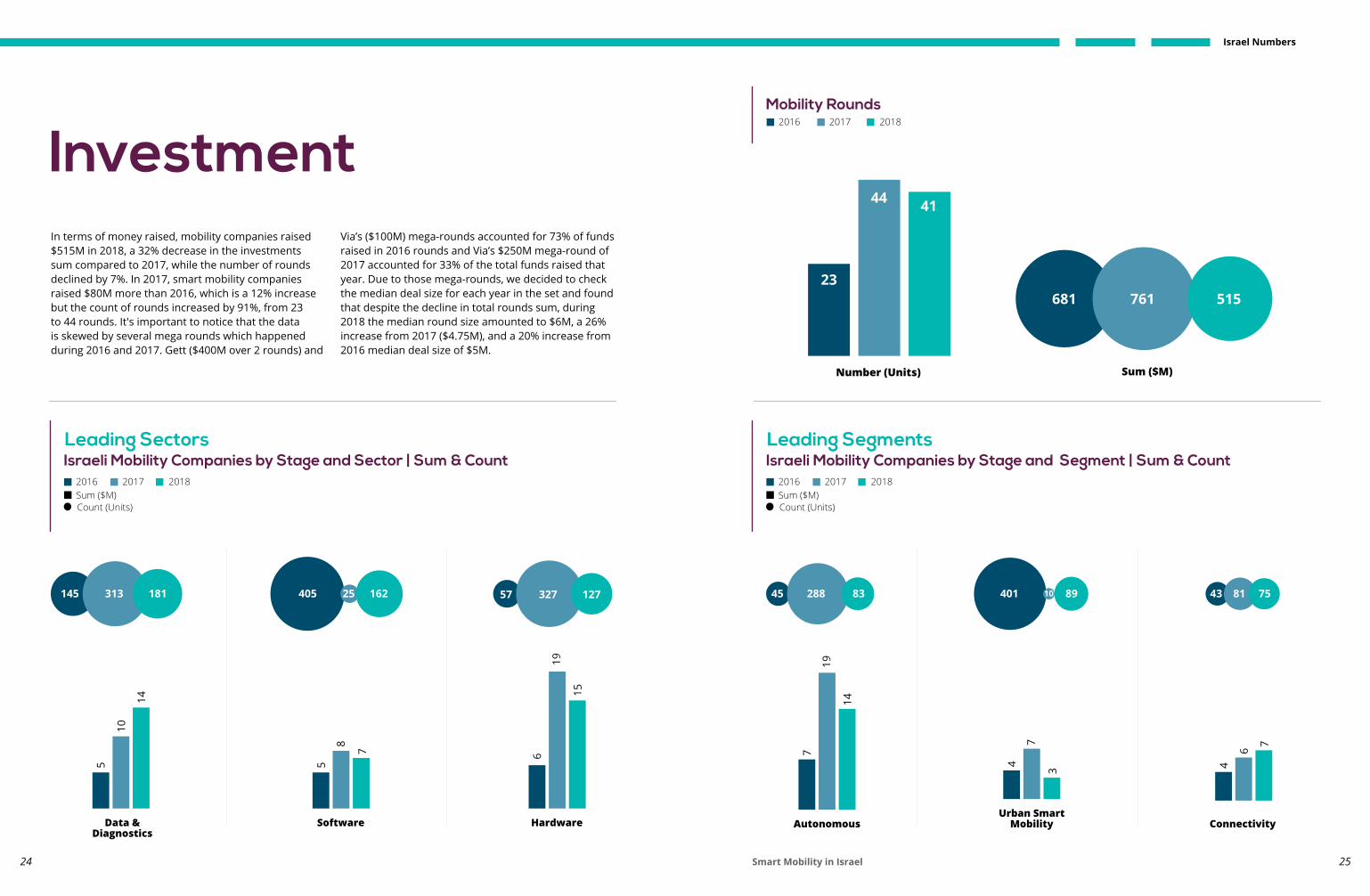

In terms of money raised, mobility companies raised $515M in 2018, a 32% decrease in the investments sum compared to 2017, while the number of rounds declined by 7%. In 2017, smart mobility companies raised $80M more than 2016, which is a 12% increase but the count of rounds increased by 91%, from 23 to 44 rounds. It's important to notice that the data is skewed by several mega rounds which happened during 2016 and 2017. Gett ($400M over 2 rounds) and

Via’s ($100M) mega-rounds accounted for 73% of funds raised in 2016 rounds and Via’s $250M mega-round of 2017 accounted for 33% of the total funds raised that year. Due to those mega-rounds, we decided to check the median deal size for each year in the set and found that despite the decline in total rounds sum, during 2018 the median round size amounted to $6M, a 26% increase from 2017 ($4.75M), and a 20% increase from 2016 median deal size of $5M.

Mobility Rounds

Number (Units) Sum ($M)

4144

23681

Autonomous

7

19

14

45 288 83

Hardware

6

19

15

57 327 127

Data & Diagnostics

5

10

14

145 313 181

Software

5

8

7

405 25 162

Urban Smart Mobility

4

7

3

401 10 89

Connectivity

4

6

7

43 7581

Israeli Mobility Companies by Stage and Sector | Sum & CountLeading Sectors

2016Sum ($M)Count (Units)

2017 2018

Israeli Mobility Companies by Stage and Segment | Sum & CountLeading Segments

2016Sum ($M)Count (Units)

2017 2018

515761

2726 Smart Mobility in Israel

Israel Numbers

Leading Investors

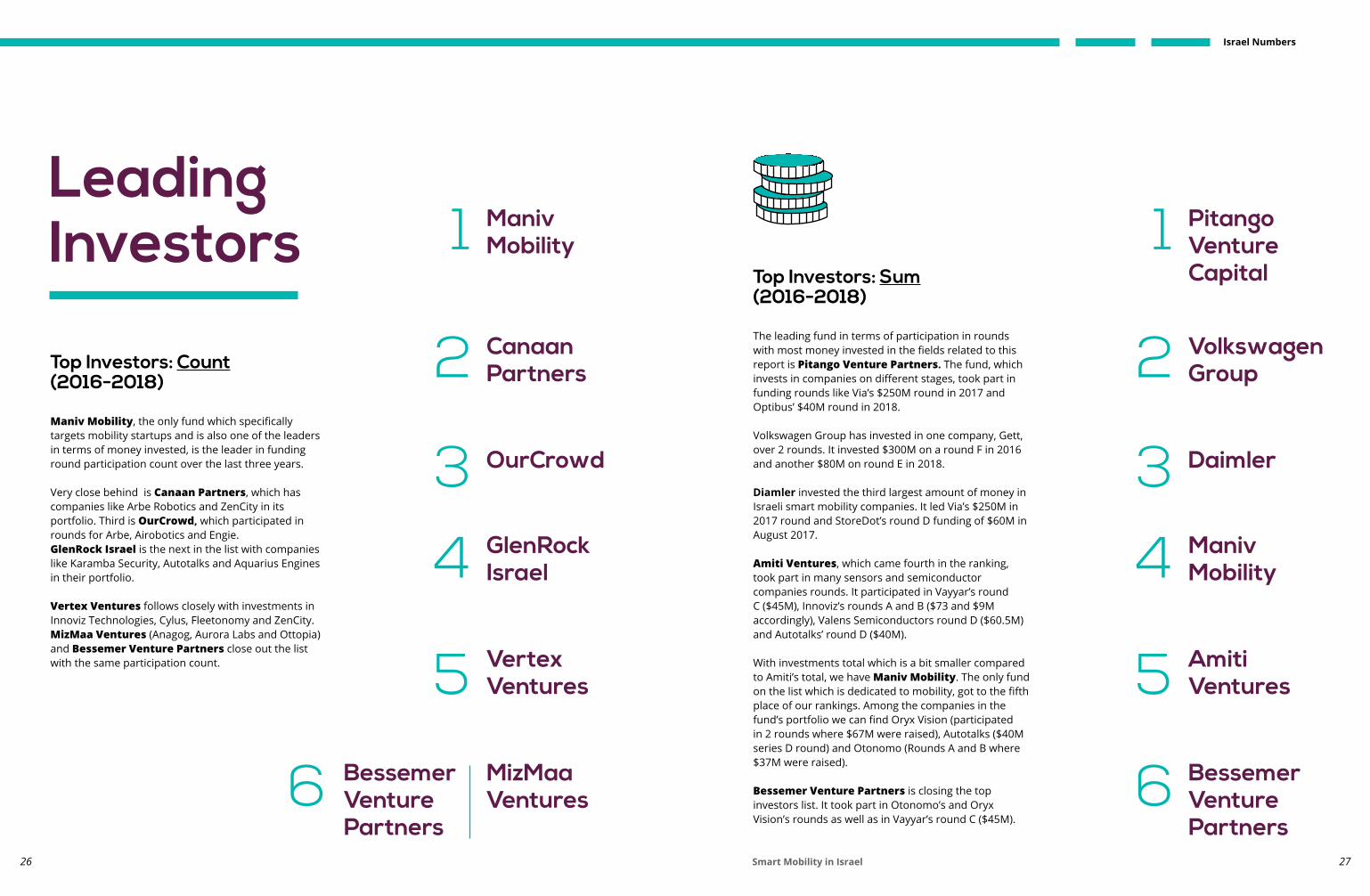

The leading fund in terms of participation in rounds with most money invested in the fields related to this report is Pitango Venture Partners. The fund, which invests in companies on different stages, took part in funding rounds like Via’s $250M round in 2017 and Optibus’ $40M round in 2018.

Volkswagen Group has invested in one company, Gett, over 2 rounds. It invested $300M on a round F in 2016 and another $80M on round E in 2018.

Diamler invested the third largest amount of money in Israeli smart mobility companies. It led Via’s $250M in 2017 round and StoreDot’s round D funding of $60M in August 2017.

Amiti Ventures, which came fourth in the ranking, took part in many sensors and semiconductor companies rounds. It participated in Vayyar’s round C ($45M), Innoviz’s rounds A and B ($73 and $9M accordingly), Valens Semiconductors round D ($60.5M) and Autotalks’ round D ($40M).

With investments total which is a bit smaller compared to Amiti’s total, we have Maniv Mobility. The only fund on the list which is dedicated to mobility, got to the fifth place of our rankings. Among the companies in the fund’s portfolio we can find Oryx Vision (participated in 2 rounds where $67M were raised), Autotalks ($40M series D round) and Otonomo (Rounds A and B where $37M were raised).

Bessemer Venture Partners is closing the top investors list. It took part in Otonomo’s and Oryx Vision’s rounds as well as in Vayyar’s round C ($45M).

Top Investors: Sum (2016-2018)

4

5

6

Amiti Ventures

Bessemer Venture Partners

1

2

3

Pitango Venture Capital

Volkswagen Group

Daimler

Maniv Mobility

Maniv Mobility, the only fund which specifically targets mobility startups and is also one of the leaders in terms of money invested, is the leader in funding round participation count over the last three years.

Very close behind is Canaan Partners, which has companies like Arbe Robotics and ZenCity in its portfolio. Third is OurCrowd, which participated in rounds for Arbe, Airobotics and Engie.GlenRock Israel is the next in the list with companies like Karamba Security, Autotalks and Aquarius Engines in their portfolio.

Vertex Ventures follows closely with investments in Innoviz Technologies, Cylus, Fleetonomy and ZenCity. MizMaa Ventures (Anagog, Aurora Labs and Ottopia) and Bessemer Venture Partners close out the list with the same participation count.

Top Investors: Count (2016-2018)

4

5

6

Vertex Ventures

Bessemer Venture Partners

1

2

3

Maniv Mobility

Canaan Partners

OurCrowd

GlenRock Israel

MizMaa Ventures

2928 Smart Mobility in Israel28 29Smart Mobility Report

Segments

There are many ways by which the smart mobility market can be segmented. Here we chose to highlight five of the largest: Mobility-as-a-Service (MaaS), Electrification, Autonomous Vehicles (AV), Connectivity and Urban Smart Mobility. Each one of these is connected to the others, and all are intertwined into one futuristic fabric which might solve many of the problems humanity faces currently and is about to confront in the future.

Segmentation

3130 Smart Mobility in Israel

Mobility as a Service (MaaS) is an alternative model to mean-of-transportation ownership. It allows for pinpoint solutions to transportation challenges without the need for the user to deal with the periphery of transportation (such as parking, garage, etc.). While autonomous vehicles, electric transportation and connectivity garner the most attention in the smart mobility realm, the rise in MaaS seems to be a term which encompasses the biggest change in the future of transportation infrastructure.

Mobility as a Service

1 2Seamless IntegrationCurrently, there are many available transportation methods: car-sharing, ridesharing, bikesharing, buses, trains, trams and others that solve a fragment of the transportation conundrum. Each of those has its own logistical, scheduling, and availability limitations. Additionally, MaaS platforms integrate several mobility options into a single ecosystem. The MaaS platform integrates required data such as prices or where and when to switch between mobility solutions, allowing booking all available services in one place.

Service Instead of Ownership MaaS platforms eliminate the need to personally own means of transportation (a car, a motorbike, a scooter, an electric bicycle, etc.) by offering temporary use of the mean of transportation. For example, instead of buying a car, purchasing insurance and complementary products related to it, or investing the time and effort dedicated to car maintainence, MaaS customers can simply streamline rental. This stands as an alternative to the above-mentioned expenses which affords personal car use for just 5% of the day, the average personal car use rate in the west.

MaaS platforms offer two main uses:

Companies *As indicated above, much of MaaS is represented by shared economy solutions. Technological advances came to mobility that previously allowed the introduction of the shared economy into every aspect of human interaction. The ability to locally solve market deficiencies by utilizing a non-hierarchical model proved to be seamlessly fit to the seemingly inherent problems of the traditional mobility universe. While the regulation of this model is globally lacking, the rate of popular adoption leaves the regulators mightily struggling with a rapidly evolving reality.

The harbinger of the sector in Israel was the 2008 born Car2Go, a platform for short period carsharing, which was acquired a year later by the Shagrir group. The inspiration behind Car2Go was the American company Zipcar, which was launched in 2000 and went public in 2011 raising $174M. At the beginning of its life, Car2Go had issues establishing itself due to lack of support from municipalities and the public at large, the former refusing to dedicate parking spaces for the initiative and the latter hesitant to adopt such a disruptive initiative.

Now, a decade later, Car2Go has dedicated parking spaces around Tel Aviv, Jerusalem, Haifa and three other cities in Israel. Car2Go operates the Tel Aviv municipality’s MaaS service- Auto-Tel, which is one of the world leading MaaS services in terms of amount of rides and average daily driving distance. According to Auto-Tel, last December it broke the average daily ride record of over 1,400 rides. Each of the company’s vehicles was responsible for an average of 168 rides and 3,450 minutes of use, an 82% rise year-on-year. Auto-Tel currently has 8,500 paying subscribers, while 96% of its users live in Tel Aviv and Jaffa.

Tel-O-Fun bicycle share, Tel Aviv. Photo by: Assafk88, Wikimedia Commons

Segmentation

3332 Smart Mobility in Israel

Perhaps the best known and standard bearer of the local sector (and in the world alongside Transit and Citymapper) is Moovit. Since its 2011 founding, the real-time transit tracker has raised $131.5M, $50M of which on a Series D funding round in February 2018. Moovit offers its users real-time ETA data for public transportation by combining crowdsourced input and data from ride operators, increasing satisfaction from the public transportation customers. Recently, the app added a new feature allowing private car drivers to offer carpooling as a service, mostly to commuters.

A similar initiative comes from Weelz, that sets itself out to be a kind of Airbnb for private cars. The bootstrapped company was established in 2017 as a vehicle-sharing platform that lets owners rent out their vehicles instead of leaving them idle at times they would otherwise not be in use. Rather than spending money on parking, owners can make money by lending their cars out. After choosing from available listings based on price and location, a user would send his or her request to the owner, who can personally approve or deny the request. Weelz has its own insurance in case of damage in order to protect the car owner’s insurance policy and history.

AI is in use by Teporto, a one-year-old bootstrap startup laying out efficient routes for shuttle providers while adjusting it to each commuter’s needs. Its “dynamic routing” system frequently updates schedules and routes, enabling the provider smarter resources management and flexibility when needed.

GoTo Mobility is a Tel Aviv-based seed-stage startup offering a white-label software for vehicle sharing that allows mobility providers and operators to implement sharing business models on a single platform simultaneously. The company has embarked on developing their product as an end-to-end solution where operators can mix and match different rental needs (one-way, round trip, peer-to-peer etc.).

Founded in 2016, RouteValet has raised $700,000 in seed round and grants, aims to combine data on all available transportation methods to provide users calculating the shortest and fastest routes from A to B.

Optibus, which raised $40M in a Series B round in December 2018, has developed its own route optimization tool. Its product, Optimize, is a patent-pending optimization system that provided real-time scheduling to help reduce operation costs for clients. The company also offers products like OnTime for real-time adjustment to unplanned events, OnDemand for operators to add more rides to the same route, and OnSchedule, to choose the most effective route.

Outside of the city streets, we find the travel service booking company Bookaway, for trains, ferries and bus operators. The company helps business owners worldwide reach out to clients before their take-off from their home country offering their services before the clients' landing in their destination while enabling travelers an easy and affordable trip booking platform.

*

**

VC investors worldwide have put a lot of attention in on-demand ride-hailing apps. For example, in 2018, Uber raised $1.25B in a Series G round, Lyft getting $1.7B, China’s Didi Chuxing more than $5B in two rounds and Singapore-based Grab raised $5.4B in two rounds (and $550M so far in 2019). With such a saturated market, these ridesharing giants and their VC investors are looking for new and additional mobility solutions.

They have realized the potential of integrating MaaS models like bike-sharing, electric scooter services and very-short-term rental cars into their existing platforms. This has led to the birth of micro-mobility renting services such as Uber Jump, Lyft Scooters and GrabWheels. Newer players on the Israeli micro-mobility scene have become the apple of investors’ eyes in the last year; projects like Bird, Lime and Wind have in 2018 raised $400M, $405M and $22M respectively. Lime added an additional $310M in February 2019.

Helsinki, Finland aims to initiate a city-wide MaaS system by 2025, designed around the mobility needs of individual users. The goal is to make city transport infrastructure more environmentally friendly and more efficient. The program encourages the utilization of empty car seats for ridesharing in order to reduce the amount of cars on the road, hoping fewer cars per square kilometer can

make room for more bike lanes and micro-mobility commuting. This includes encouraging the adoption of on-demand ride services, increasing competition in the local cab market.These services will be united into one centralized system all accessible with one transport card (Like Oyster in London or Rav-Kav in Israel), which will reduce complexity and make the mobility network more user-friendly.

Segmentation

Electrification

Using electricity in place of fossil fuels is a milestone for the mobility industry. Electrification helps create cleaner urban space by reducing the number of fossil fuel-related emissions (CO2, carbon monoxide, various nitrogen oxides, particulate matter, etc.), noise pollution, and the waste associated with gas-powered vehicles like discarded parts and other hazardous fluids (oil and coolants). The adoption of electric vehicles is gaining speed due to the rise in public awareness for environmental issues and the lower production costs which lead to more affordable final sale prices for consumers. For example, lithium-Ion batteries have come down heavily in terms of price and are projected to fall to as low as $100 per unit by 2025.

In addition to traditional vehicles, electrification has enabled the creation of micro-mobility solutions such as the electric bike and the electric scooter. Those modes of transportation allow users to leave their private car or taxi services behind when short-distance city journeys are required, saving time and effort for themselves and solving the acute congestion and parking urban problems while doing so.

Another major aspect of electrification is the development of smart infrastructure such as photovoltaic roads and pavements. Photovoltaic technology can turn any street, parking or highway into an electricity generator or solar energy accumulator, enabling better utilization of both urban and intercity spaces.

Companies EVR Motors develops electric motor for vehicles. The technology behind their engine allows the creation of efficient, light-weight and high-powered engines which don’t require cooling. They also develop generator technology for communal wind turbines. Its lightweight and direct-drive generator is reportedly adapted to different RPM inputs and sources. The design uses magnets on both sides of the generator. Such design removes the iron from the rotor and uses less electrical steel. It also does not require cooling.

Another notable hardware producer is SolwarWat, which has raised $3.1M in seed funding and provides photovoltaic modules. The company’s products reduce costs and can be used for solar panels, electric vehicles, roads and pavements and other photovoltaic integrated products.

The smart mobility industry also pushes the energy industry into creating better and cleaner products which will be integrated with transportation methods. Phinergy developed a metal-air based battery system which has high energy density and zero emissions. The company raised $50M for their product. The fully recyclable system has been successfully integrated into electric vehicles, transportation modes and other industries.

StoreDot, which has so far raised $146M, $20M of which from BP, has also developed a new kind of lithium-ion-based battery, purporting less risk of internal shorting, which in turn extends the battery’s life. The amino acids used to manufacture the battery replace standard lithium components and improve battery performance, allowing up to four times more discharge/charge cycles compared to usual battery, shorten charging time and offer more safety.

Another local company in the Li-ion battery market is ETV Energy. They have raised $12M so far for a “next generation” of Li-ion batteries and offer a micro-turbine-based range extender.

In order to manage the EV charging process, Driivz has developed a cloud-based charging management solution and thus far raised $12M. Their product is tailored to charging network operators, vehicle manufacturers and suppliers. The software manages the various aspects of the process: charging, account management and billing.

Electric vehicle charging station. Photo by: Wikimedia Commons, the free media repository

3534 Smart Mobility in Israel

Segmentation

3736 Smart Mobility in Israel

Autonomy

Autonomous vehicles (AV), also called driverless or self-driving cars, can navigate and overcome obstacles without the assistance of a human handler. They detect their surroundings by using a variety of technologies such as visual sensors, radar (using radio waves to determine the range, velocity and angle of objects), LiDAR (measuring distance by shining a laser onto a target), odometry, night vision, etc. The input is processed by AI and is transformed into orders which are executed by the car systems without human intervention. Numerous technology companies, car manufacturers and ride-sharing companies are currently collaborating in order to develop autonomous vehicles and supporting technologies.

It is accustomed to divide the levels of AV into five main levels. A fully autonomous car can execute all the tasks performed by a human driver without human intervention (level 4A) and to communicate with the surrounding infrastructures (level 4B). A semi-autonomous car uses driver-assisted (or driver assistance) technologies but requires a human driver to intervene in case of emergency (levels 1-3). Level 0 represents a regular, pre-autonomy car.

There are several aspects of our lives that should improve with the introduction of AVs: safety, security, traffic-related resource waste, business efficiency and financial savings. In terms of safety, the number

of accidents will drop, due to the elimination of the biggest contributor to road accidents, the human factor. AV will ideally minimize traffic congestion due to V2V communication and coordination, shorten travel times and integrate with other smart city functions. In terms of business, AV will lead to the creation and consolidation of new business models (such as MaaS) and owners will be able to rent out cars when they don’t use them. They may even be more likely to approve rental requests since they do not have to assess the driving capabilities of the renter, who would only be a passenger. The personal financial benefits from renting your unused items are clear, but AV will allow savings on delivery costs and will save the costs of holding a private car. It could also free up real estate dedicated to parking, as well as further reduce congestion since the search for parking spaces is a major contributing factor to traffic jams in the city.

Some of the biggest winners from full AV might be the reigning MaaS giants, such as Uber and Lyft. Both are currently bleeding cash, partially due to the disproportionate driver fees currently transferred to the drivers of the platforms. For example, over the last year Lyft had to pay almost three times its annual revenue (268%) to the drivers of the platform. Switching to AV might prove to be just the action which would shift these companies into the green pastures of profitability.

Companies Nexar, which has raised $44.5M, employs computer vision and sensor fusion algorithms, leveraging the iPhone’s sensors (e.g., its accelerometer, gyroscope, compass and proximity sensors among others) to analyze and understand the car’s surroundings to provide documentation in case of an accident. The depth of Nexar’s on-device analysis allows it to create a new kind of precision accident report that completely transforms the insurance claims process. Nexar can even add a video of the accident itself to the claim, alongside a detailed reconstruction based on the iPhone’s sensor readings.

Vayyar, having raised $81M since its founding in 2011, has positioned itself as a leading company in the field of imaging sensors. The company has developed a 3D-imaging chip based on radio frequency that is purportedly capable of “seeing through” solid materials. It turns any mobile device to a 3D-imaging system and can operate in different vision conditions including poor weather like fog, smog, smoke, rain, snow, etc.

Innoviz Technologies develops key technologies of AVs - smart 3D sensing, sensor fusion, accurate mapping and localization. They have raised $82M already and were in the process of raising another $100M when this report was published. Their first product is a high definition solid state LiDAR (HD-SSL) at a significantly lower cost and at a smaller size than existing solutions.

Another LiDAR centered company, Oryx Vision, has raised $67M. Oryx’s solution uses infrared (IR), which interpret the distance, velocity and direction of the object. This is instead of lasers. The system has no moving parts and is resistant to the effects of sunlight (glare).

Cortica, which has raised $68M to date, has created an autonomous AI incorporating image recognition and aiming to teach machines to use them in order to “think”. The company has developed its CorTex product, which specializes in identifying humans and objects in video and image files. Another technology the company offers is Image2Text, which can recognize concepts and elements from the input media and transfer them into keywords and even organize them according to relevancy.

Sedric: Volkswagen Self-Driving Car. Photo by: Volkswagen AG

Segmentation

3938 Smart Mobility in Israel

ConnectivityConnectivity can also be thought of as a sort of ‘IoT for mobility’ – it connects vehicles, roads, traffic lights etc. with equipped internet access, allowing them to communicate one with all the others.

There are 5 modes of communication between the vehicle and its surroundings:

1 4

5

3

2

Vehicle to Infrastructure (V2I) Allows the vehicle to communicate with road infrastructure itself, traffic lights and other non-moving objects which enhances mobility efficiency and safety.

Vehicle to Cloud (V2C) Allows vehicles to connect to a database and to utilize information gathered by other vehicles or by manual updates.

Vehicle to Everything (V2X) Allows vehicles to connect to all types of connected devices, infrastructures and modes of transportation.

Vehicle to Vehicle (V2V) The communication between vehicles regarding the vehicles’ surrounding. This communication mode allows vehicles to transfer information about speed, traffic updates and avoiding collisions by sharing planned routes and course corrections. Synchronized traffic thanks to V2V can also lead to lower congestion, as congestion can be caused by delayed driver reactions and unanticipated drive maneuvers such as lane changes.

Vehicle to Pedestrian (V2P) Allowing pedestrians and vehicles to communicate increases safety. It can be used by picking up sensor data of nearby devices to signal to a moving car about nearby hikers, cyclists and people on the road during bad weather or nighttime conditions. It will also help in daylight in urban conditions, as jaywalkers or pedestrians obscured by parked vehicles or other obstructions make them more vulnerable to oncoming traffic.

AV’s software could recognize unexpected details like broken signs, malfunctioning traffic lights and parked vehicles it encounters, as well as foresee possible contacts with bikes, scooters or pedestrians. The communication between vehicles will allow a vehicle which has encountered an unusual situation to send a notification to other vehicles in its surrounding area and prepare them to handle the situation or to pick an alternative route. Additionally, connected vehicles could send reports of such damaged infrastructure to a centralized maintenance or local enforcement authority, perhaps automatically entering repairs or at least inspection of that infrastructure into an automated task management system.

Connectivity also benefits the environment, as infrastructure can use less electricity due to its ability to use sensor networks in order to detect approaching vehicles and work only on per need basis. This might save a significant amount of needless electricity waste and reduce the severe light pollution in cities.

*There are currently 317 million streetlights in the world. This number will grow to 363 million by 2027. The Netherlands, which is famous for its biking culture, upgraded a dark 10-kilometer-long bike route from Woensdrecht to Bergen op Zoom with a new LED-based smart system. The lights automatically turn on when vehicles or cyclists pass by and turn off once they are a certain distance away. Though the installation of such a lighting system is pricier than a traditional one, it consumes far less electricity during operation, saving money in the long-term, is more durable and serves as a basis for future connectivity projects.

**

To implement the advantages of such technologies, large quantities of data analysis and diagnostics are required. NoTraffic, which raised $3.3M in a seed round, has built a traffic management tool based on data collected from V2I communication and computer vision algorithms. This particular combination of data purportedly enables the tracking of all road users and the optimization of traffic accordingly.

Similar yet divergent, Waycare Technologies has developed a platform for municipalities to take advantage of data collected from local traffic. WayCare then helps those cities utilize the collected data from AVs and connected transportation modes in order to manage the city’s roads in a more efficient and pragmatic way. The company has thus far which raised $2.85M in seed funding.

Ayalon Highways (the operator of route 20 among other projects) chose ACiiST Smart Networks to turn its streets into smart roads. The company utilities the lighting infrastructure to install its system for V2I communications. MetropoLAN, ACiiST’s product, is cyber-secured, requires minimal resources and entails little regular traffic disruption for installation.

Using the existing lighting system as a platform is also what bootstrapped startup Tondo is doing. The company manufactures a plug-and-play device which connects to existing lighting infrastructure and is controlled remotely, leading to cost and energy savings. Additionally, the device helps discover real-time failures or damage which speeds up response time from the operator’s side. The data collected from the system supports decision-making regarding light fixture repairs, dimming hours and other data samples required for greener use.

Leaving lighting infrastructures behind, but still in the plug-and-play realm, there is hereO, which has raised $4.85M so far and created a purportedly end-to-end IoT plug-and-play device that converts traditional devices into “smart” device by integrating new capabilities.

The most notable hardware provider in the sector in terms of money raised is Valens, which has raised $164M to date, $63M of which from a Series E round in November 2018. Valens is the developer of HDBaseT technology, which distributes HD content over long distances (up to 100 meters) without compressing it. The HDBaseT software and chipset is integrated into an AV’s entertainment, safety and autonomous systems. Aiming to improve mobility and reduce accidents with its V2X chipset is Autotalks. Autotalks raised more than $70M, and offers a secured, high-performing communication device for V2X communication. Its device – made for AVs, pedestrians and other mobility methods – gathers data from sensors with poor-sight and no-sight scenarios in mind.

Intellicon also aims to manage traffic at junctions and where traffic lights are installed but with V2X communication. The company built smartphone-connected adaptive traffic signal system which would locate and calculate the amount of oncoming traffic before prioritizing lighting signals accordingly. The system is equipped with the ability to prioritize emergency vehicles, police cars and public transport.

Otonomo’s product also connects to an external source to share and integrate data. The company, which has raised $40M so far, developed a V2C platform where data gathered from cars is analyzed (after anonymization) and then sent back into the ecosystem in the form of recommendations. Otonomo purports to create new high margin revenues for OEMs, as well as for connected and autonomous car ecosystem providers.

According to the US-based Energy Information Administration (EIA), 232 billion kilowatt hours (kWh) of electricity were consumed by the local commercial and residential sectors for lighting. This amount of consumption is around 6%, of the total electricity consumption around the USA in 2018.

The commercial sector consists of institutional buildings, commercial areas, public roads, streets lights, consuming about 141 kWh of electricity for lighting and representing nearly half of all local energy charges.

Companies

Connected street lights and road lights, which would sense vehicles and pedestrians and therefore go on and off when needed, should be considered whenever a municipality is about to renovate its local infrastructure as it would lead to big savings on electricity consumption, payments and ultimately benefit the local environment.

Segmentation

4140 Smart Mobility in Israel

Segmentation

4342 Smart Mobility in Israel

Urban Smart Mobility

The Urban Smart Mobility segment integrates many separate ideas into a bigger vision of efficiency, flexibility and safety in the most environmentally friendly way possible, bringing it all into the urban environment.

The biggest challenge facing Urban Smart Mobility is that no two countries, cities or even roads are the same. London’s road infrastructures are different than Tel Aviv’s; New York’s public transportation needs are not like those of Jerusalem; and the regulation in Shanghai is different from the regulation in Sydney. While some mobility solutions like ride-hailing can be used in many different locations, many other solutions must be looked at on a regional level. Uber and its struggles in Israel compared to the global success of the company serves as a prime example for the topic.

The global urban mobility market experienced tremendous growth during the last year. According to PitchBook, the global urban mobility VC activity in 2018 summed up to an impressive $45B, with about 370 deals. There has been a 73% growth in funds from 2017 and a 750% increase overall dating from 2014, the first year during which investments in the sector surpassed the $1B mark.

The UN Sustainable Development Goals (SDG) for smart cities set similar targets for 2030, “to provide access to safe, affordable, accessible and sustainable transport systems for all, improving road safety, notably by expanding public transport, with special attention to the needs of those in vulnerable situations.”

Therefore, to implement the smart mobility concept we will have to look into creating an efficient, minimally disruptive service which is perfectly moulded to the specific needs of customers. It will be built around the best integration possible between the different transportation methods, from mass transportation to micromobility.

While many seem to find the cure for mass transportation as the most beneficial medicine to the ills of traditional mobility, others move in a completely different direction. Micro-mobility solutions, which are specifically tailored for the needs of each specific individual, seem the proper solution in a hyper customized world. However, despite the optimism, at this current time we believe that a holistic solution for the growth pains of society would be an integration of the various modes of mobility, starting with mass transportation and ending with micro-mobility models, creating a seamless mobility network.

*

The population of Amsterdam is estimated at 800,000. Over 10 years data regarding the residents was collected by 32 departments in the city. Later, this data was analyzed resulting in a inception of around 100 new bicycle related initiatives.

One of these initiatives tested the impact of changing garbage collection, shifting to a single truck to collect and sort both waste and recycling. The reduction in the number of trucks in Amsterdam’s narrow streets freed up immense amounts of space, reducing congestion on trash and recycling pick-up days and in turn benefitting residents.

The Jerusalem light rail. Photo by: Leinad, Wikimedia Commons

CompaniesWith operations in more than 100 cities and trust from more than 6,000 corporations around the globe, Gett is a leader of the Israeli mobility ecosystem. The company has raised close to $700M so far. It offers the passenger the option of paying through the app itself, check the driver’s rating and interests and reduces the ride cost compared to a regular taxi, mainly by sticking to metered pricing.

Another company which aims to make cities better is UMo Urban Mobility. The company developed UMo’s AI-Urban Brain which gathers data using mobile devices, city data and third parties. That data is later processed and turned into analytics and insights on a dedicated dashboard. UMo’s ‘brain’ also gives municipalities the option to communicate with citizens, as well as rewarding them for using sustainable modes of transportation like walking, cycling, carpooling, etc.

Spaceek, which has raised $1.97M, has patent-pending technology that utilizes smartphones and their sensors for parking. It guides drivers to available nearby parking spots and provides a parking management tool with insights and recommendations.

**

CyberAutonomous cars would carry interlinked computing systems, control panels, microprocessors – all controlled by lines of code and operated by critical functions. This raises the chance of hackers taking control of vehicles and using them in malicious ways with threats increasing as more features, processors and software augmented autonomous cars.

Threats come from both external – hackers and thieves – and internal sources - individuals working in the autonomous vehicle industry. Each part of the design and manufacturing processes is vulnerable to a multiplicity of cyber threats. Hackers might break into cars with the goal of access to intellectual property; to sabotage or degrade vehicular performance; or commit acts of terrorism, theft, burglary, mischief or simply to test their own hacking skills against software safeguards. Such threats can affect OEMs, distributors, dealers, mechanics, road infrastructure managers, drivers, passengers and a state economy as a whole, bringing transportation to a screeching halt with merely few lines of malicious code.

CompaniesKaramba Security, which has raised $27M to date, offers Carwall, an autonomous cybersecurity solution for connected vehicles. Carwall integrates seamlessly into a vehicle's engine control unit (ECU) and provides multiple security layers to automatically insulate automotive software against cyberattacks. The company’s automated approach offers the automotive industry a tool to immediately detect and prevent cyberattacks that exploit software bugs in the code of connected cars. Thus, drivers can be confident they will

always be in complete control over their vehicles, and manufacturers will learn more about the frequency and nature of such attacks.

Pyramid is a hardware cyber solution for AV developed by Regulus Cyber, which has raised $6.3M to date. Implementing Pyramid in a system is purportedly easy due to it small measurements (14cm and 28.35 grams) and it enhances the operational robustness, makes the system fully secured, detects spoofing spots jamming incidents, and analyzes big data.

Upstream Security ($11M, $9M of which in a Series A) has come up with a solution that monitors communication between the connected vehicle and the IoT, then scans it for malware and indications of attempted attacks. All the collected data is presented on a dashboard which returns insights and fleet monitoring. Upstream’s solution is the first cloud-based cyber and analysis platform for the AV industry.

Vsentry is a system developed by SafeRide Technologies. It protects the computerized elements of the AV and blocks attacks on communication channels. The system also blocks code-breaking attempts and information theft possibilities.

C2A Security, which raised $6.5M in February of 2019 and $7.7M since its inception, develops a suite of end-to-end cyber solutions. The company developed it products after 36 months of R&D alongside leading vehicle manufacturers which led to fast integrated, low-cost and minimal in-vehicle footprint. The founder of the company is Michael Dick, a co-founder of NDS which was sold to Cisco in 2012.

Bootstrapped NeoPeach has developed a similar system that sends notifications and updates about available parking spaces in the vicinity of the driver. The system also provides directions for the driver to the parking lot.

A major part of the improvement of the urban space is making it safer for all users of mobility, be it drivers, riders or walkers. Safe Place has used its $1M in seed funding to develop a solution for reducing reckless driving and enhance violations enforcement. The platform detects a wide range of risky road behaviors and can operate in any weather conditions, at any time of the day. By using video and photos, the platform collects evidence that would help to improve ticket

There are 47M citizens in Spain, which is 0.006% of the world’s population. However, 20% of the bike-sharing services, which number around the globe is estimated to be 500, is located in Spain. Viu Bicing is the bike-sharing service which serves the 1.6M citizens of Barcelona, which has 6,000 bicycles, followed by Valencia and Sevilla (2,000 each). The cost for the using is as little as 47€ a year (if no fines for delays in return occur) and is operated by a simple membership plastic card. Viu’s claims to save €2.5M a year.

***

accuracy, traffic flow and overall safety.With a similar goal of maximizing safety and eliminating dangerous driving habits, Safe Lane has developed a voice-operated app that uses the phone’s camera and internet connection to record and send traffic violations. The recordings are sent to a dedicated center of the Israeli Road Safety Authority which analyses them and sends them to the police, which can use them later as evidence in case it is needed.

Segmentation

4544 Smart Mobility in Israel

4746 Smart Mobility in Israel

Exits

Cyber

The biggest exit thus far in the history Israel’s smart mobility industry belongs to Argus Cyber Security. The company provides end-to-end, multilayered solutions and services that protect connected vehicles from cyber attacks. It was acquired by the German corporation Continental for $450M. Continental is one of the biggest original equipment suppliers (OES) in the vehicle industry. By acquiring Argus, it consolidates its status as one of the leaders in the field of smart vehicle systems.

Another notable exit of a cybersecurity provider belongs to TowerSec, which raised less than $3M before it was acquired by Harman for an estimated $75M. Both of TowerSec’s products, ECUSHIELD (which detects real-time security breaches) and TCUSHIELD (which protects against harmful wireless communication), were integrated into Harman’s security systems.

NNG, the developer of the iGO navigation app that predates Waze and Google Maps, acquired Arilou Technologies for $10M. Arilou provides security agents with detection and prevention capabilities for the cyber protection of vehicles. Airlou’s goal is to be able to secure any vehicular system with it, regardless of its original vulnerability.

AV

SAIPS, which became famous for its self-driving machine learning and computer vision technology, was acquired by Ford Motors. After the deal, SAIPS was labeled a subsidiary and continues serving its preexisting clients from a variety of industries. SAIPS expertise in algorithm development over deep neural networks (DNN) will be instrumental in realizing Ford’s vision to produce a fully autonomous vehicle by 2021.

The only company to go public in this section of the report is Foresight Automotive. The ADAS developer went public on the Tel Aviv Stock Exchange under the ticker FRSX and subsequently raised $7M. The company’s platform provides low false alarm rates and cost-effective threat detection which reduces risk and the incidence of accidents.

Urban Smart Mobility

Juno Lab, which operated a ridesharing platform in New York City, was acquired by Gett for $200M. Juno was founded in 2015 and fought head-to-head with Uber, offering drivers a cut of approximately 65% from their commission payments. Gett wanted to use the company to penetrate the US market and to fight with Uber and similar apps over market share.

Parko was acquired by the Swedish company, EasyPark, after raising $1.1M in a seed round. Parko began as an app for locating parking spaces and connected drivers who left or were leaving parking spaces to drivers who were looking for parking themselves. After collecting enough data, the company developed three analytics tools: ParkoData, which estimates how many spots will be occupied at any given time; ParkoAnalytics, which can analyze different areas or neighborhoods and provide insights accordingly; and ParkoLastMile, which navigates drivers to newly available parking spaces. EasyPark’s philosophy is the transformation of city infrastructure into smart infrastructure, specializing in fleet management and parking management for large events.

Connectivity

Altair Semiconductor, which manufactures single-mode LTE telecom chipsets for smart cars among other things, was acquired by Sony for $212M. Since its foundation in 2004, Altair had raised approximately $124M and over 30 international manufacturers were using the company’s chips. Sony maintained the company’s offices in Israel and designated them the company’s local R&D center.

Red Bend was acquired by Harman for $200M. The company developed a technology for mobile operators to update firmware and software over the air. The company’s operations have continued uninterrupted by the acquisition, with Harman keeping the original team and management in place.

Exits

In the current early stage of smart mobility, the governments play an important role in the shaping of the future. They do so by implementing both pull and push factors; by both providing funds and infrastructure, and by enforcing regulation. The Israeli government, its agencies and offices are postioned to influence the future of smart mobility in Israel. The most important office in this context is undoubtedly the ministry of transportation. It has the exciting role of bringing the future into fruition, by preforming a balancing act of encoureging innovation while keeping the public interests in mind.

Regulation and Public Spending

HaShalom Interchange, Tel Aviv. Photo by: Jens Herrndorff

4948 Smart Mobility in Israel

Segmentation

5150 Smart Mobility in Israel

When looking at the regulation in Israel, we can identify several key players which determine the future of smart mobility development and implementation in Israel. Those players will determine the regulatory framework which will dictate the rules and terms on the streets, encourage specific startups and whole subfields with subsidies and tax reliefs, foster cooperation between the practitioners and the academia and grow international cooperation of the ecosystem.

The government’s role in the future of mobility will be divided into two main actions: promotion and regulation. On the one hand, the government will have to promote startups and entrepreneurs in the field by allocating funding, boosting legalization, encouraging research, and by cooperating with the global community in order to reserve the Israeli market’s position as a global leader.

Another field where the government should get involved is education. The Ministry of Transportation will have to implement initiatives and regulations, but for long ter success, the Ministry of Education will have to encourage future students to excel in STEM fields to bolster the smart mobility industry and the entire technology sector, as it were.

Furthermore, the government will have to set and enforce balanced regulation of new means of mobility, which will take into account public safety while not stifling innovation. Besides the human toll, as we

The Israeli Government

witnessed regarding the Uber fatality case in 2018, mobility-related casualties might do severe harm for the advancement of technology and mass adoption of strong solutions to acute problems, due to negative public perception of mobility innovation as a whole.

Behavioral economists like to point out that it is all about the right incentives. While the Israeli government attempts to showcase its enthusiasm for smart mobility solutions, some of the incentives that might encourage its own employees to adopt such solutions point at the exact opposite direction. For example, the government is currently actively promoting the use of private transportation methods by giving benefits to private car owning public sector employees. Obviously, the aforementioned shortcomings in the public transportation sphere and the lack of public trust in the network serve as a negative incentive and contribute to the higher-than-average private car ownership in the country.

In order to close those gaps, there is an acute need for a change both in the public and the private spheres. In order to address that gap, over 50% of recent governmental transport investment concentrated on public transportation due to a strategic decision of the government to shift the local mobility division away from private mobility, thus increasing the market share for public transportation by 60%, from the current 25% rate to 40% (it’s worth noting that the world average of public transportation use is currently close to 60%).

A high-speed rail link between Jerusalem and Tel Aviv has started its testing stage and should be fully operational sometime over the course of 2019. The government also aims to develop light rail systems in the country’s three main cities between by 2023 (Jerusalem’s has launched, but will be expanded). Additionally, the Infrastructure 2030 plan that was recently published by the Ministry of Transportation focuses on massive mobility projects such as high-speed railways, the new light rail under construction in the Tel Aviv metropolitan area, a fast train to the southern tourist city of Eilat among others. By investing in physical mobility, the government aims at reducing resource leakage, foreseeing that improving public transportation networks and transport infrastructure, especially to the periphery of the country outside the Tel Aviv metropolitan area, will go a long way to improve social mobility.