Embed Size (px)

Citation preview

Smart GridsDick Kronman, ABB Oy, 21.3.2012

From Vision to Reality

Introducing ABB

© ABB Group April 4, 2012 | Slide 3

A global leader in power and automation technologiesLeading market positions in main businesses

135,000 employees in about 100 countries

$38 billion in revenue (2011)

Formed in 1988 merger of Swiss and Swedish engineering companies

Predecessors founded in 1883 and 1891

Publicly owned company with head office in Switzerland

Power systems

Discrete automation and motion

Europe

Asia

Americas

Middle East and Africa

Well-balanced business and geographic portfolioCapturing growth opportunities, wherever they arise

Share of employees2011

47%

Mature markets

Emerging markets

Power products

Process automation

Low voltage products

53%

25%

21%22%

12%

20%

Orders by division% of total orders 2011 (non-consolidated)

38%

30%

23%

9%

Orders by region% of total orders 2011

© ABB Group April 4, 2012 | Slide 5

Leading power system’s biggest-ever transformationSmarter, greener grid for more efficiency and reliability

Merging power and automation technologies makes electricity network more reliable, flexible, secure and efficient. Smart grid benefits include:

Lower power consumption

Greater use of renewable energy

ABB’s broad offering in both power and automation technologies positions it uniquely to support this evolution

Transformation of grid to take place over several decades

Transformation of the electricity supply

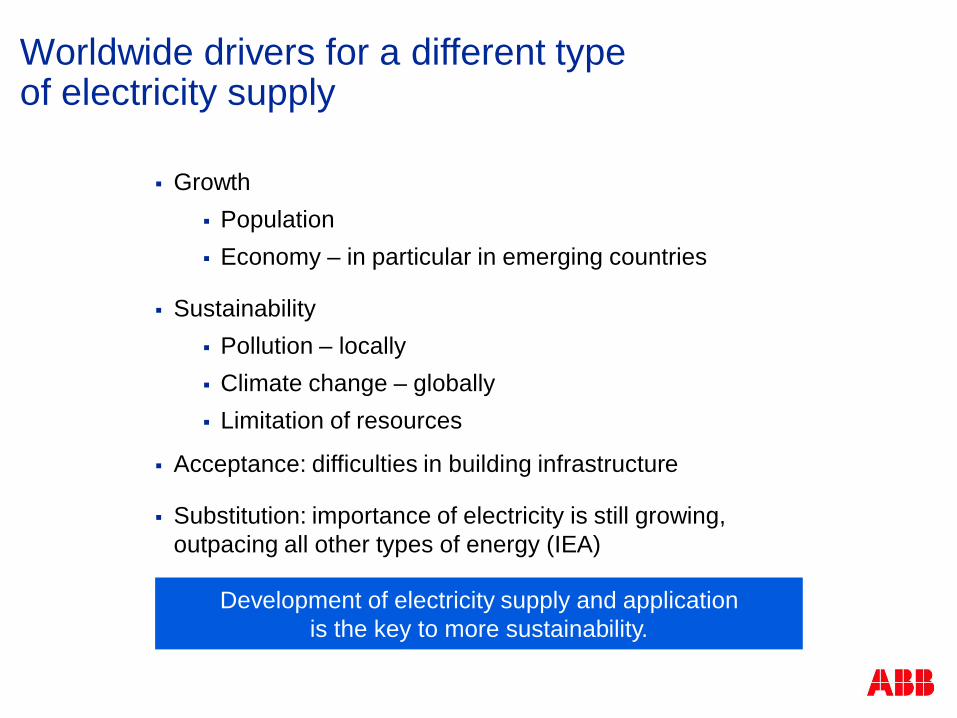

Worldwide drivers for a different typeof electricity supply

GrowthPopulationEconomy – in particular in emerging countries

SustainabilityPollution – locallyClimate change – globallyLimitation of resources

Acceptance: difficulties in building infrastructure

Substitution: importance of electricity is still growing, outpacing all other types of energy (IEA)

Development of electricity supply and applicationis the key to more sustainability.

© ABB Group April 4, 2012 | Slide 8

Today’s energy challengesCut link between growth, energy use and emissions

Meeting these challenges requires the world to:

Reduce the correlation between economic growth

and energy use

Reduce the correlation between energy use and

emissions

Energy

efficiency

Renewable sources

of energy

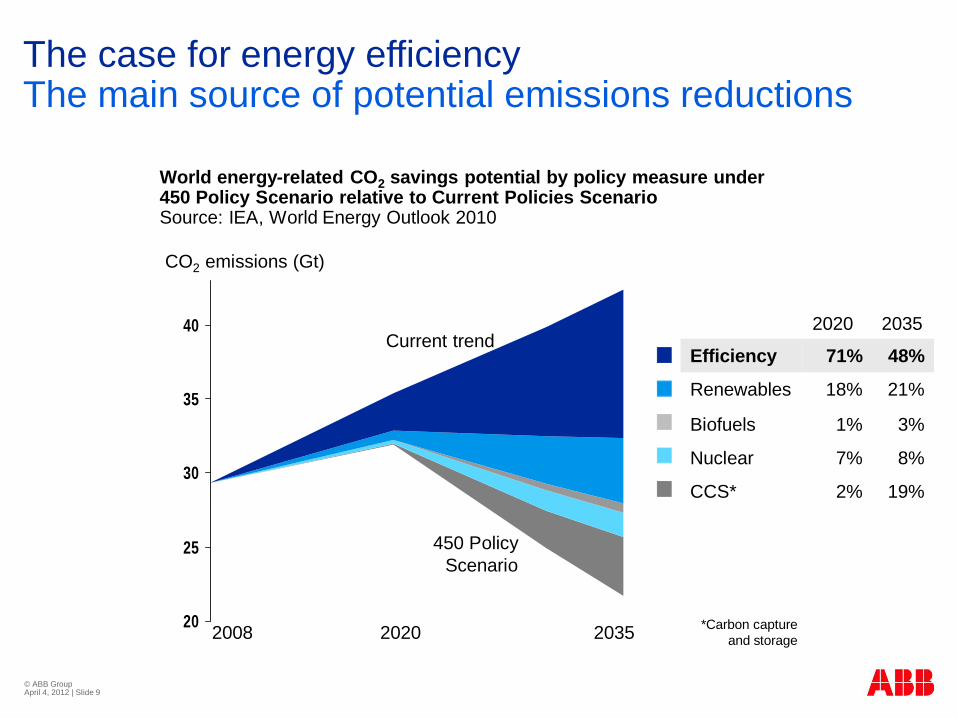

The case for energy efficiencyThe main source of potential emissions reductions

20

25

30

35

40

2008 20352020 *Carbon capture and storage

CO2 emissions (Gt)

World energy-related CO2 savings potential by policy measure under 450 Policy Scenario relative to Current Policies ScenarioSource: IEA, World Energy Outlook 2010

Current trend

450 Policy Scenario

© ABB Group April 4, 2012 | Slide 9

2020 2035

Efficiency 71% 48%

Renewables 18% 21%

Biofuels 1% 3%

Nuclear 7% 8%

CCS* 2% 19%

European SmartGrids Technology Platform

Evolution of grid designFrom traditional to future grids

Centralized power generation

One-directional power flow

Generation follows load

Operation based on historical experience

Limited grid accessibility for new producers

Centralized and distributed power generation

Intermittent renewable power generation

Consumers become also producers

Multi-directional power flow

Load adapted to production

Operation based more on real-time data

trad

ition

al g

rids

futu

re g

rids

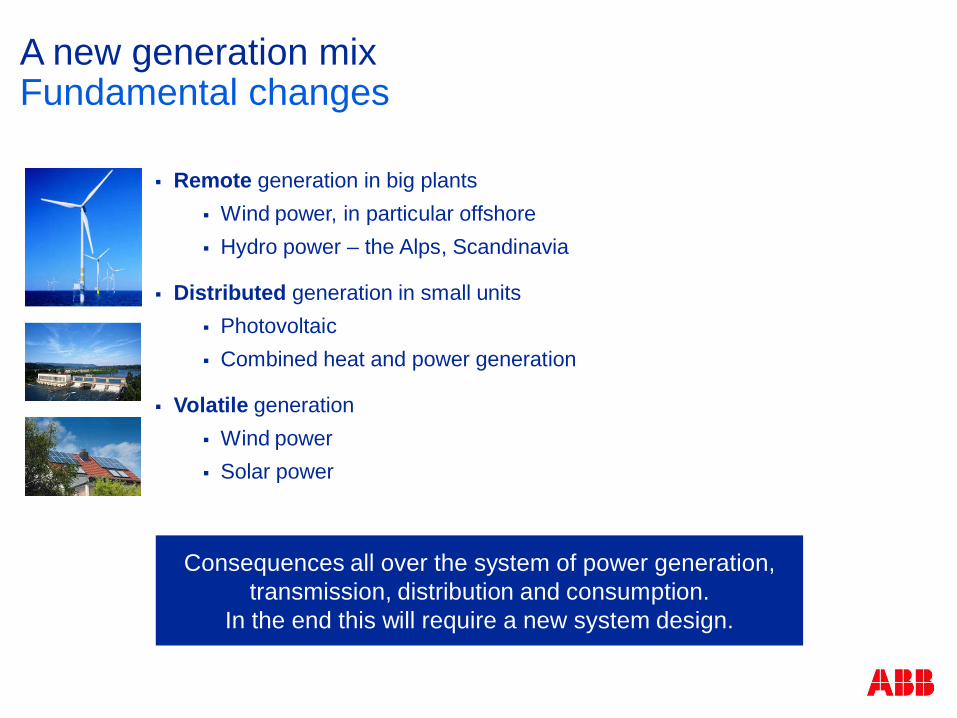

A new generation mixFundamental changes

Remote generation in big plantsWind power, in particular offshoreHydro power – the Alps, Scandinavia

Distributed generation in small unitsPhotovoltaicCombined heat and power generation

Volatile generationWind powerSolar power

Consequences all over the system of power generation, transmission, distribution and consumption.

In the end this will require a new system design.

Managing the challenge

European Electricity Grid Initiative

EEGI – Focus Areas

Source: Entso-e, Edso for SG 2010

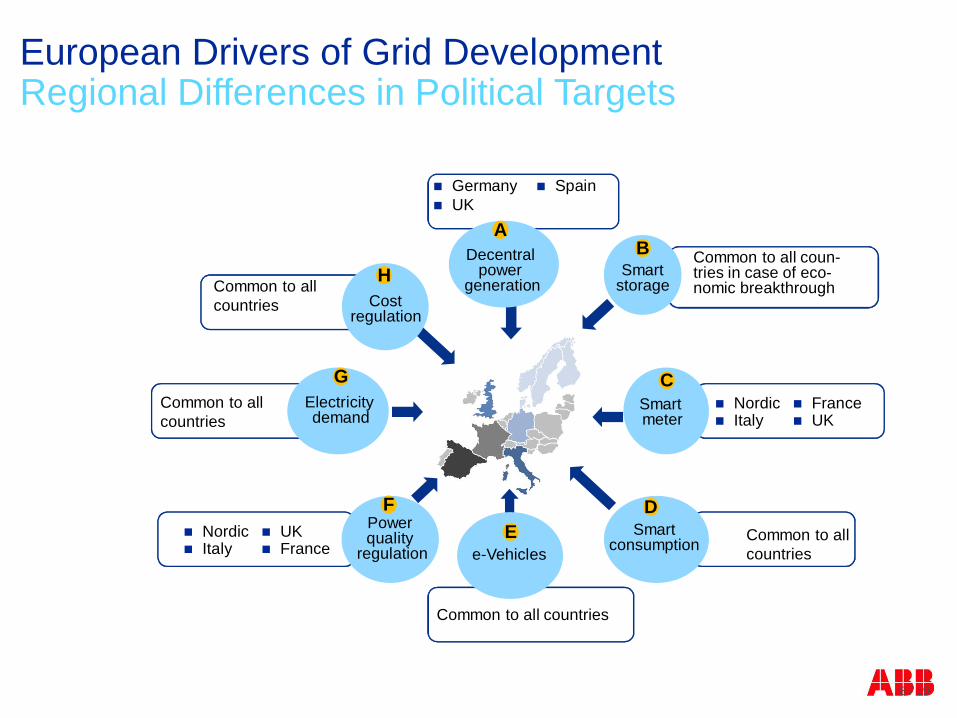

European Drivers of Grid DevelopmentRegional Differences in Political Targets

8 / 19

Common to all countries

Common to allcountries

Germany UK

Spain

Decentral power

generation

A

Smartstorage

B

Smart meter

C

Smart consumption

DPower quality

regulation

F

Electricity demand

G

Costregulation

H

NordicItaly

FranceUK

NordicItaly

UKFrance

Common to allcountries

Common to all coun-tries in case of eco-nomic breakthrough

e-VehiclesE

Common to all countries

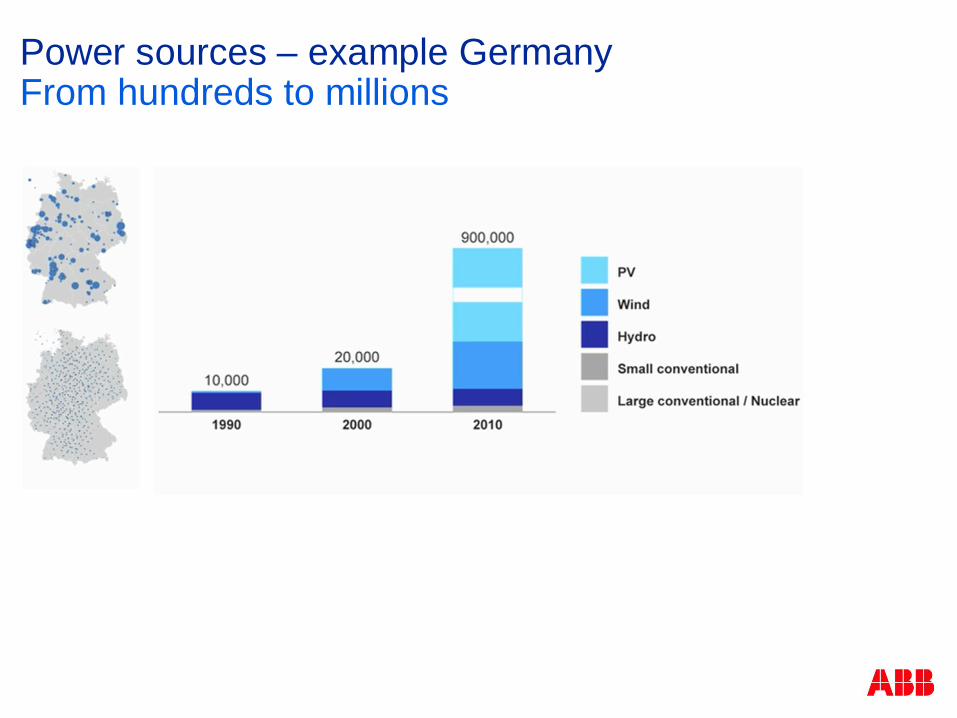

Power sources – example GermanyFrom hundreds to millions

MWWind production

Source :

Statnett

Integration of renewables also brings many challengesExample - balancing demand and supply in real-time

Unpredictable / intermittent

Need for balancing reserves

Legislation / incentives for renewables

Negative tariffs

The effect of heavy wind power feed-in on tariffs

Base: -35,57Peak 9,47Max(18) 42,59Min (7) -199,99

Source: EnBW, 2010

100

50

0

-50

-100

-150

-200

-250

€/MWh

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

hour

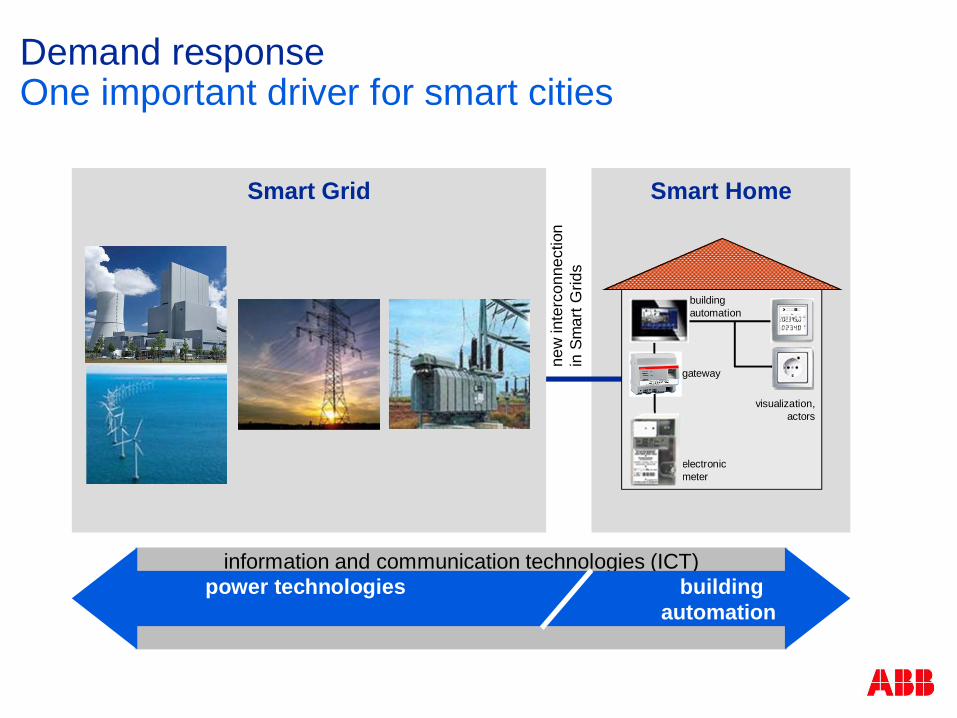

information and communication technologies (ICT)

Demand responseOne important driver for smart cities

Smart Home

power technologies buildingautomation

new

inte

rcon

nect

ion

in S

mar

t Grid

s

Smart Grid

building automation

electronic meter

visualization,actors

gateway

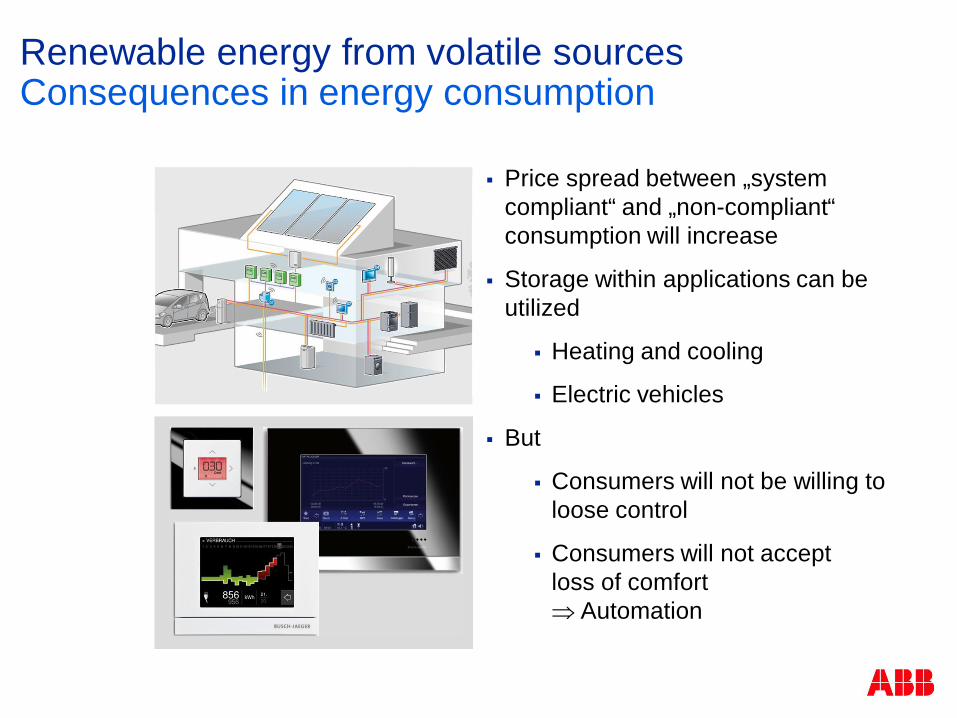

Renewable energy from volatile sourcesConsequences in energy consumption

Price spread between „system compliant“ and „non-compliant“ consumption will increase

Storage within applications can be utilized

Heating and cooling

Electric vehicles

But

Consumers will not be willing to loose control

Consumers will not acceptloss of comfort

Automation

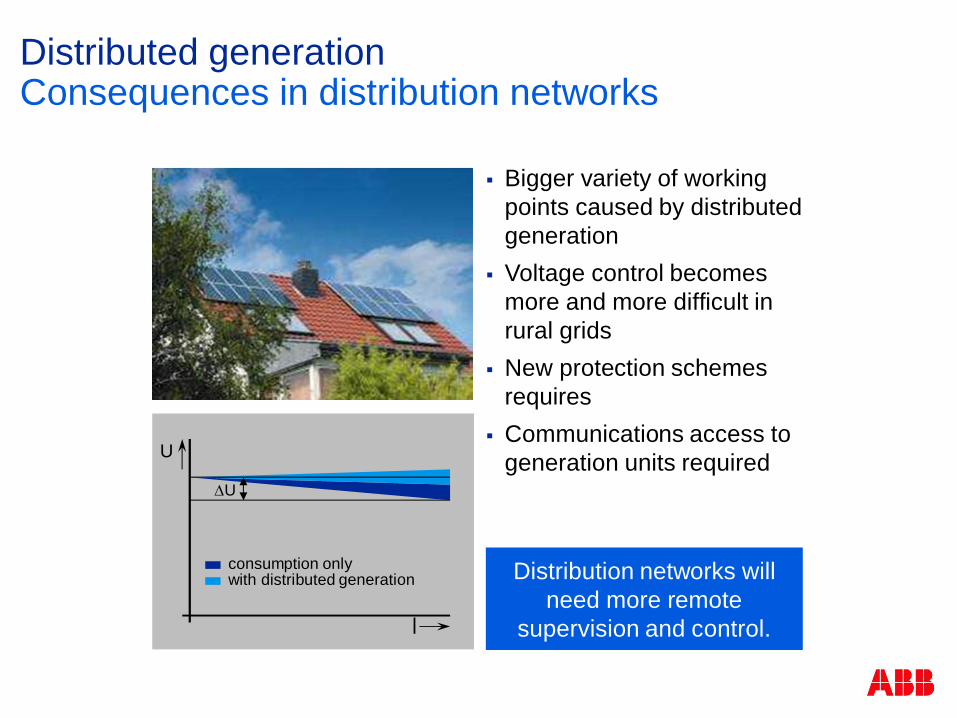

Distributed generationConsequences in distribution networks

Bigger variety of working points caused by distributed generationVoltage control becomes more and more difficult in rural gridsNew protection schemes requiresCommunications access to generation units requiredU

l

U

consumption onlywith distributed generation Distribution networks will

need more remote supervision and control.

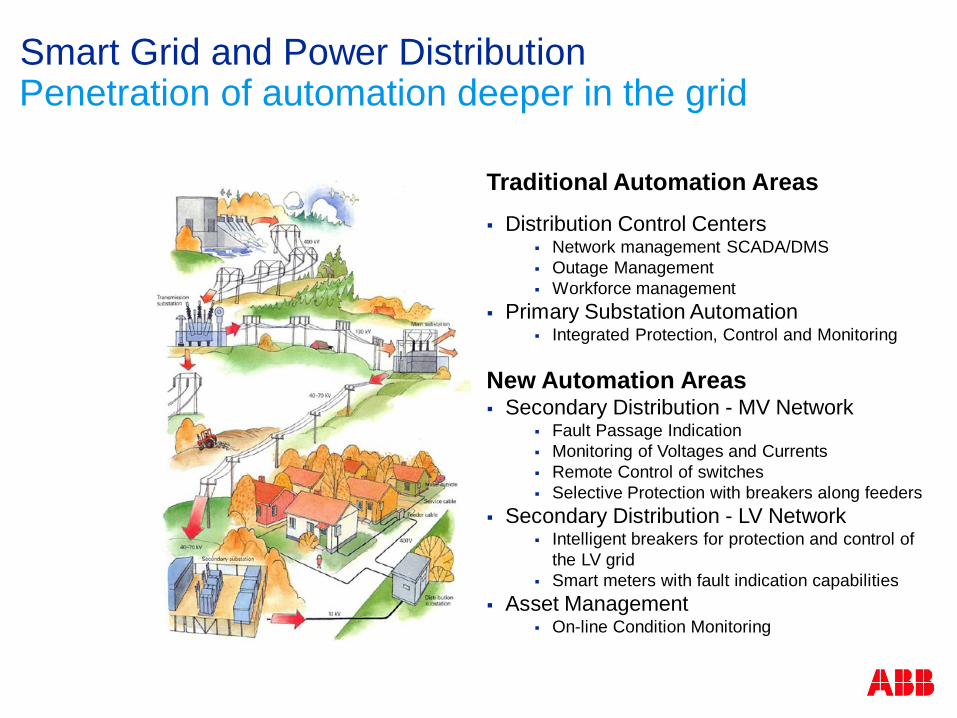

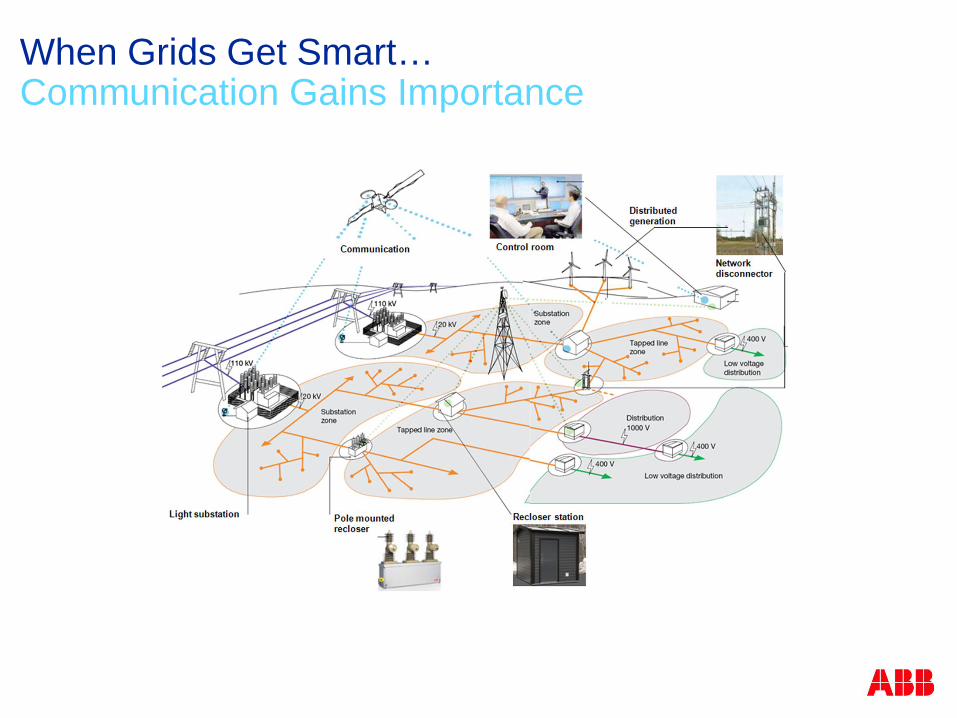

Smart Grid and Power Distribution

Traditional Automation AreasDistribution Control Centers

Network management SCADA/DMSOutage ManagementWorkforce management

Primary Substation AutomationIntegrated Protection, Control and Monitoring

New Automation Areas Secondary Distribution - MV Network

Fault Passage IndicationMonitoring of Voltages and CurrentsRemote Control of switchesSelective Protection with breakers along feeders

Secondary Distribution - LV NetworkIntelligent breakers for protection and control of the LV gridSmart meters with fault indication capabilities

Asset ManagementOn-line Condition Monitoring

Penetration of automation deeper in the grid

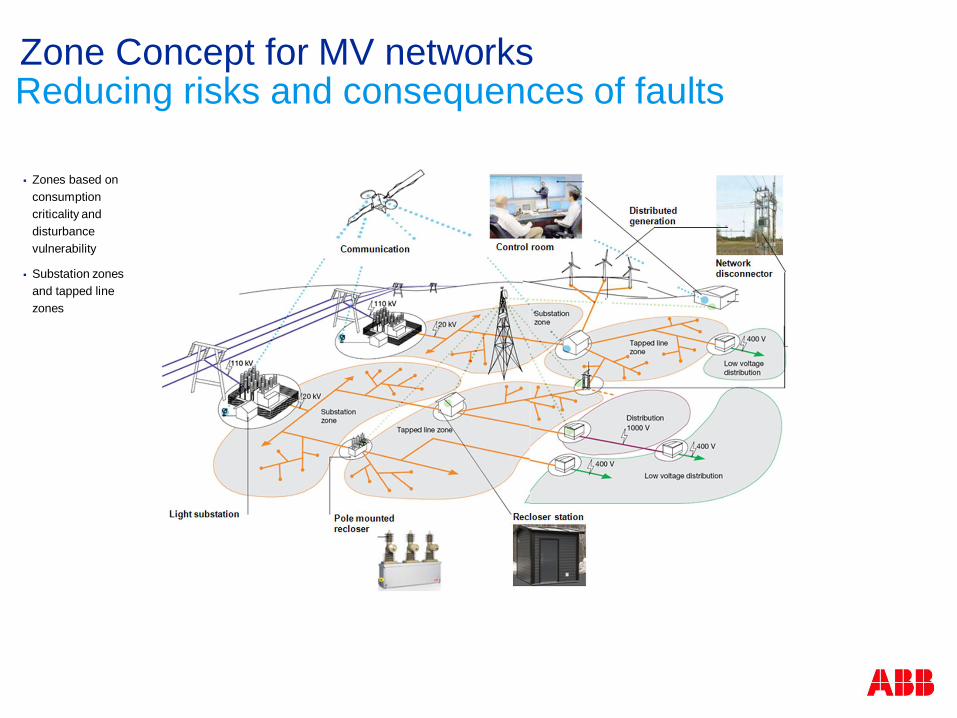

Zones based on consumption criticality and disturbance vulnerability

Substation zones and tapped line zones

Zone Concept for MV networks Reducing risks and consequences of faults

When Grids Get Smart…Communication Gains Importance

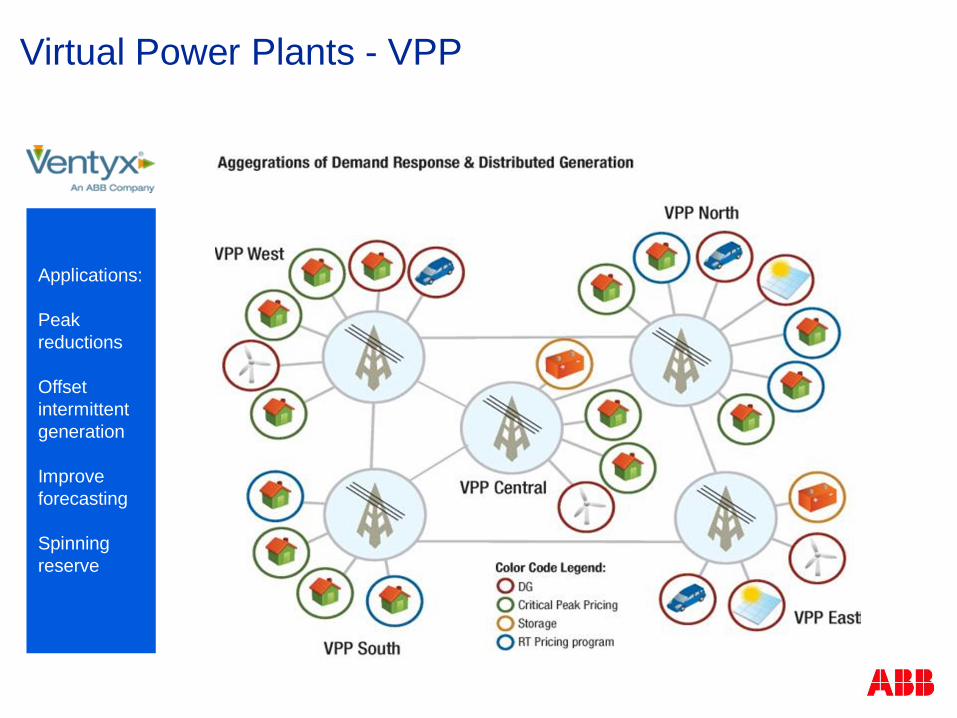

Virtual Power Plants - VPP

Applications:

Peak reductions

Offset intermittent generation

Improve forecasting

Spinning reserve

Smart Cities

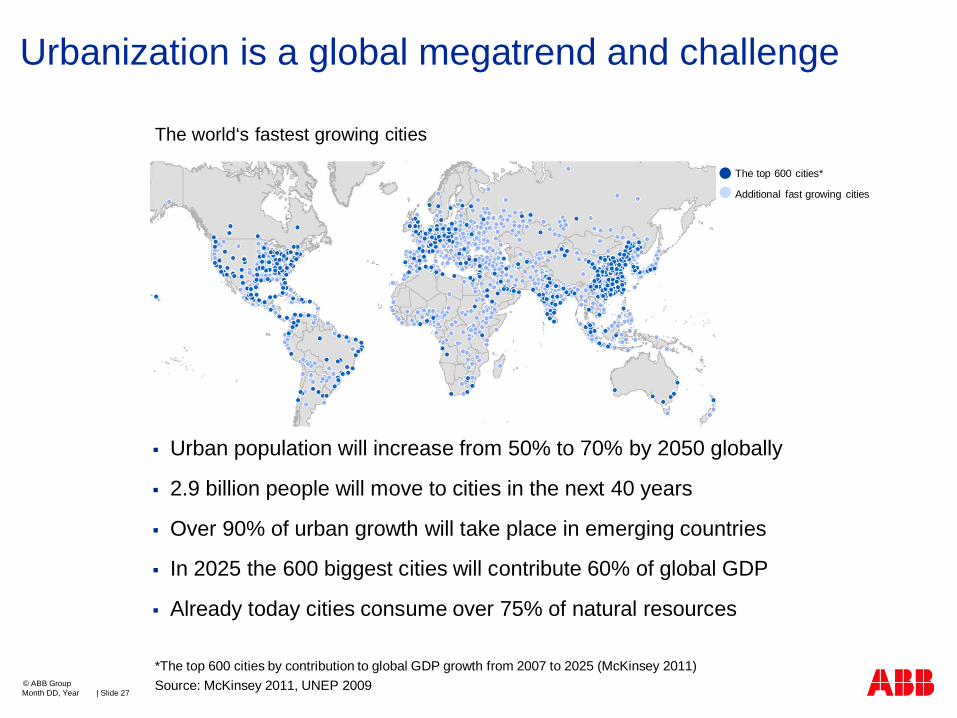

Urbanization is a global megatrend and challenge

Month DD, Year | Slide 27© ABB Group

The world‘s fastest growing cities

The top 600 cities*

Additional fast growing cities

Urban population will increase from 50% to 70% by 2050 globally

2.9 billion people will move to cities in the next 40 years

Over 90% of urban growth will take place in emerging countries

In 2025 the 600 biggest cities will contribute 60% of global GDP

Already today cities consume over 75% of natural resources

*The top 600 cities by contribution to global GDP growth from 2007 to 2025 (McKinsey 2011)Source: McKinsey 2011, UNEP 2009

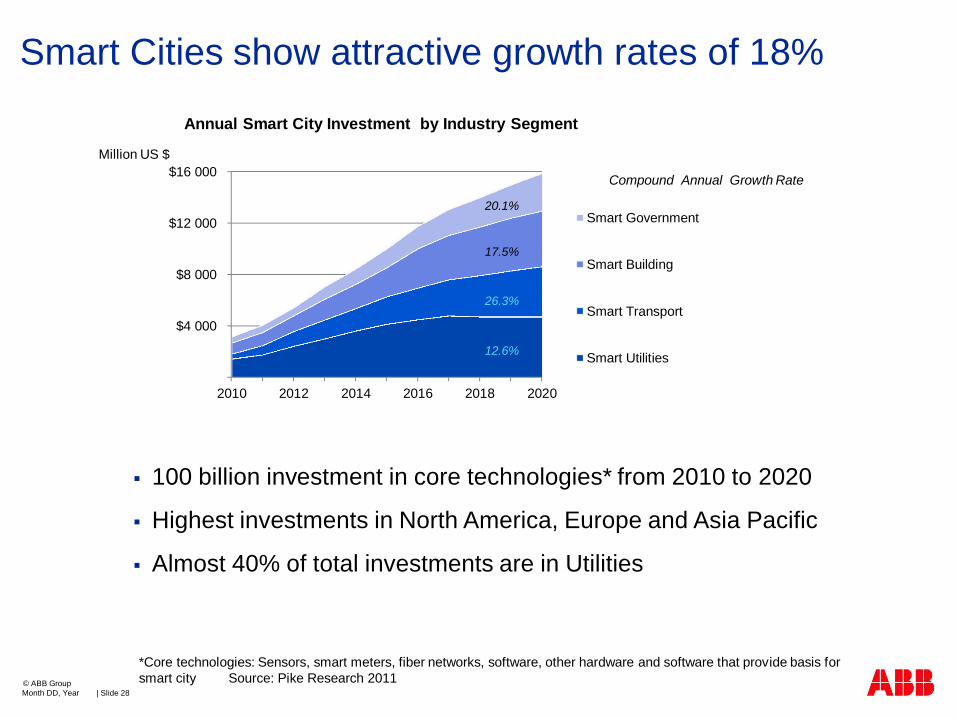

Smart Cities show attractive growth rates of 18%

100 billion investment in core technologies* from 2010 to 2020

Highest investments in North America, Europe and Asia Pacific

Almost 40% of total investments are in Utilities

Month DD, Year | Slide 28© ABB Group

$-

$4 000

$8 000

$12 000

$16 000

2010 2012 2014 2016 2018 2020

Smart Government

Smart Building

Smart Transport

Smart Utilities

Annual Smart City Investment by Industry Segment

12.6%

26.3%

17.5%

20.1%

Compound Annual Growth Rate

*Core technologies: Sensors, smart meters, fiber networks, software, other hardware and software that provide basis for smart city Source: Pike Research 2011

Million US $

ABB Smart City Projects

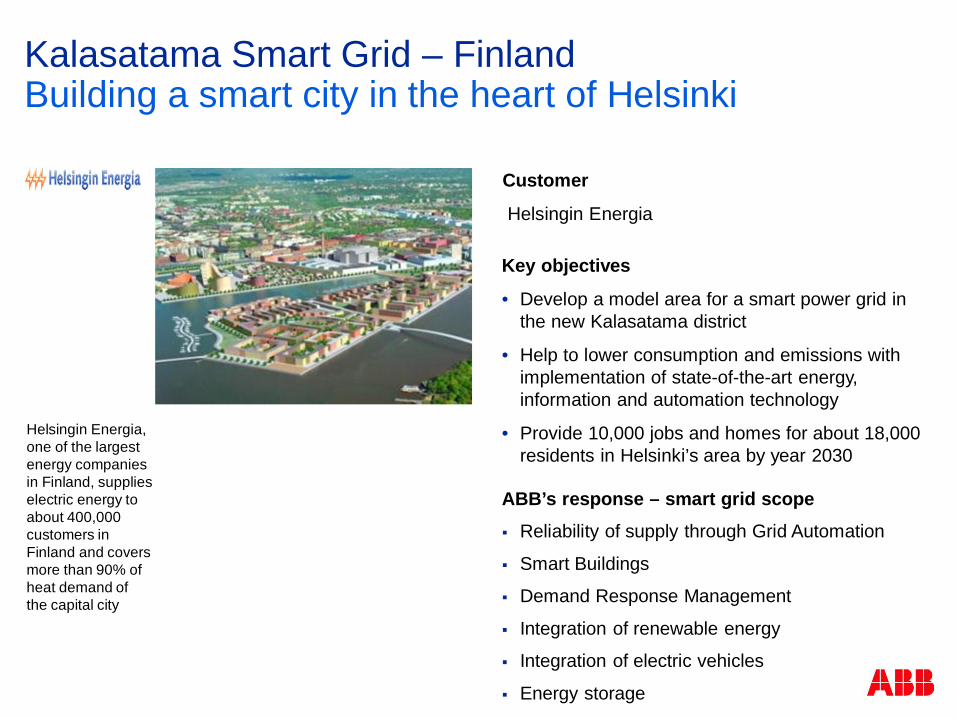

Kalasatama Smart Grid – FinlandBuilding a smart city in the heart of Helsinki

Key objectives

• Develop a model area for a smart power grid in the new Kalasatama district

• Help to lower consumption and emissions with implementation of state-of-the-art energy, information and automation technology

• Provide 10,000 jobs and homes for about 18,000 residents in Helsinki’s area by year 2030

ABB’s response – smart grid scopeReliability of supply through Grid Automation

Smart Buildings

Demand Response Management

Integration of renewable energy

Integration of electric vehicles

Energy storage

Customer

Helsingin Energia

Helsingin Energia, one of the largest energy companies in Finland, supplies electric energy to about 400,000 customers in Finland and covers more than 90% of heat demand ofthe capital city

Stockholm Royal Seaport project - Sweden An integrated approach for metropolitan areas…

Focus areas

• Efficient energy use• Environmentally efficient transports• Local ecocycles• Environmental life styles• Regulatory framework

Customers

• Fortum • Stockholm Municipality

Key objectives

• Develop a world class sustainable city district• Reduce CO2 emissions to a level below 1.5

tonnes per inhabitant by 2020 • Become fossil fuel free by 2030• Adapt to climate change

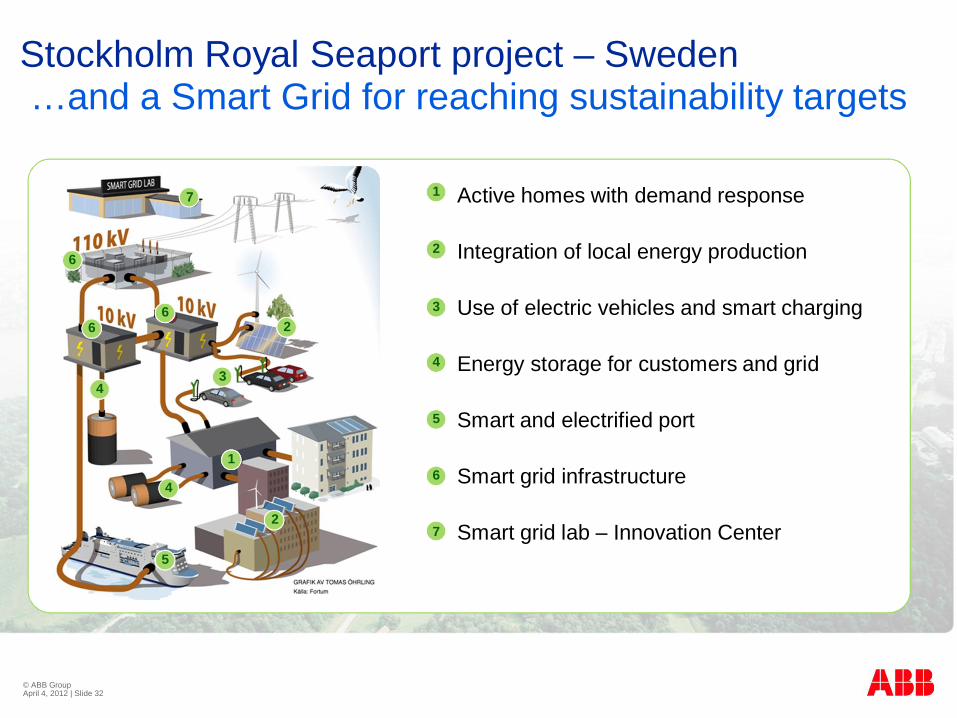

Stockholm Royal Seaport project – Sweden…and a Smart Grid for reaching sustainability targets

© ABB Group April 4, 2012 | Slide 32

Active homes with demand response

Integration of local energy production

Use of electric vehicles and smart charging

Energy storage for customers and grid

Smart and electrified port

Smart grid infrastructure

Smart grid lab – Innovation Center

7

6

66

4

4

3

2

2

1

5

1

2

3

4

5

6

7

ABB Smart Grids Projects

© ABBMonth DD, YYYY | Slide 33

Espoo, MäkkyläAdjutantti - a new consept of sustainable living

Own Solar electricity productionElectric vehicle chargingApartments for sustainable living

Measuring and visualization of water consumptionMeasuring and visualization of energy consumption

Possibility of consumption decreaseRoom-specific heating control and decreaseAt home / away controls

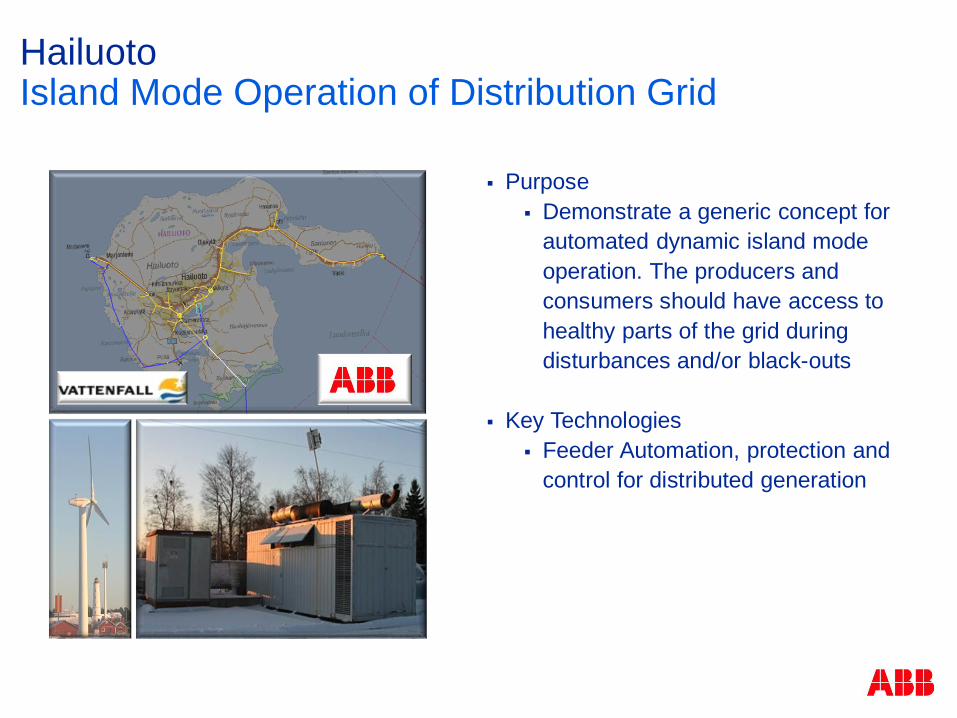

HailuotoIsland Mode Operation of Distribution Grid

PurposeDemonstrate a generic concept for automated dynamic island mode operation. The producers and consumers should have access to healthy parts of the grid during disturbances and/or black-outs

Key TechnologiesFeeder Automation, protection and control for distributed generation

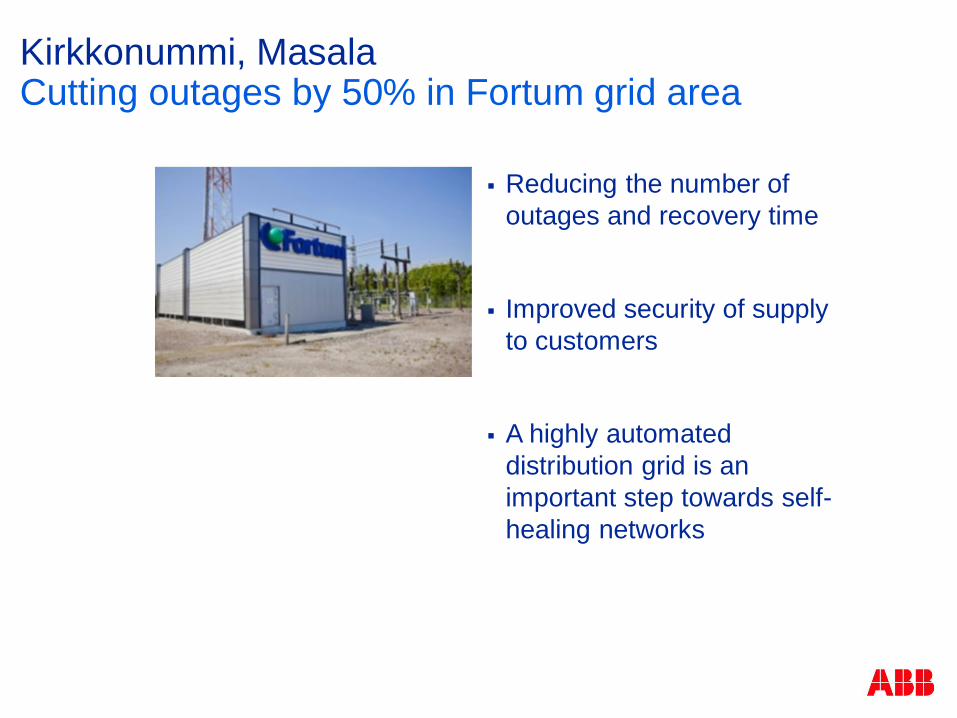

Kirkkonummi, MasalaCutting outages by 50% in Fortum grid area

Reducing the number of outages and recovery time

Improved security of supply to customers

A highly automated distribution grid is an important step towards self-healing networks

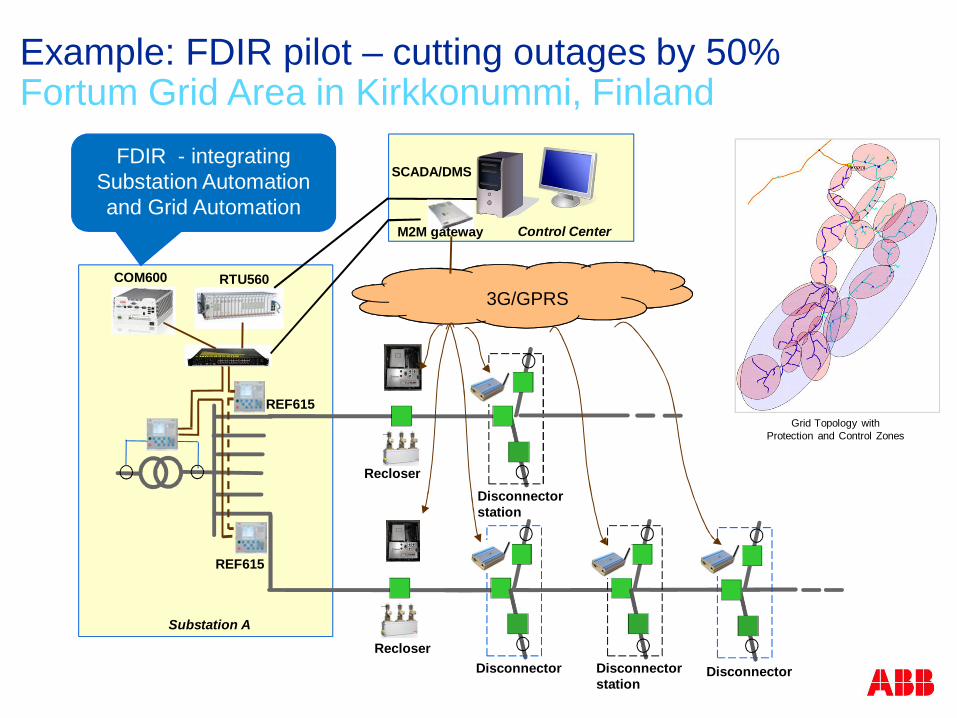

Example: FDIR pilot – cutting outages by 50%Fortum Grid Area in Kirkkonummi, Finland

3G/GPRS

Disconnector

SCADA/DMS

RTU560

Recloser

Substation A

Control Center

Disconnectorstation

Disconnectorstation

Disconnector

M2M gateway

COM600

REF615

REF615

Recloser

FDIR - integrating Substation Automation and Grid Automation

Grid Topology with Protection and Control Zones

ABB Finland

© ABBMonth DD, YYYY | Slide 38

Distribution Automation, products and systems – making the power distribution smartGenerators and Converters – generating electricity from windPV Inverters – connecting solar panels to the gridMotors – top class energy efficiencyHome Automation – making our living smart and sustainable

ABB Finland – A Leading Technology SupplierSmart Grids – Energy Efficiency – Renewables

November 08, 2011

| Slide 39

![[MICRO]GRIDS TODAY - marsdd.com€¦ · [MICRO]GRIDS TODAY Themes and Outcomes. JULY 2015. ONTARIO SMART GRID . FORUM](https://img.dokumen.tips/doc/110x75/5b37f9f87f8b9abd438cc430/microgrids-today-microgrids-today-themes-and-outcomes-july-2015-ontario.jpg)