Embed Size (px)

Citation preview

This research note is restricted to the personal use of Tom O'Connor

(tom.o'[email protected]).

Smart Grid Survey: What Utilities Want and

Where They Think They Can Get It 21 September 2010 | ID:G00206762

Zarko Sumic

We provide results of Gartner's utilities smart grid programs survey, which indicates

business and regulatory drivers, technology focus, sourcing concerns, and perceived

vendor capabilities.

Overview

The capital infusion in the smart grid space created the "smart grid gold rush"

phenomenon, attracting multiple product and service providers with widely disparate

capabilities — some with little or no domain expertise. This makes service provider

selection a complex issue in this market poised for rapid growth. This research offers an

overview of smart-grid-related activities and service providers, based on the results of a

survey conducted in 2Q10. Readers can use this research to benchmark themselves

against their peers and to create shortlists of service providers for different activities

related to smart grid program deployment.

Key Findings

� This survey indicates that utilities increasingly approach smart grid initiatives as an

enterprisewide program affecting multiple lines of business with a C-level

sponsorship.

� Meter data management (MDM) leads the chart as an IT business application, a

component of the advanced metering infrastructure (AMI), that utilities are

deploying (or considering). Advanced distribution management is ranked highest

among "engineering" IT applications.

� Although many service providers have their eyes on the smart grid area, not all of

them have relevant industry, geographic and technology experience in the right

combination, making sourcing of smart grid service skills a challenge.

� Large service providers — in particular those that offer management consulting

services — have succeeded initially to capture mind share in the smart-grid-related

service area. Niche service providers focused on the operational side of the business

— such as Kema and Black & Veatch — have attained presence and captured mind

share, especially for infrastructure-improvement-related initiatives.

Recommendations

� Utilities exploring smart grid initiatives should consider external service providers

when looking at how to augment skills and reduce costs with regard to smart-grid-

related solutions deployment and support.

� Utilities should always carefully validate claims of competency, because the

combination of ill-defined and emerging market needs, limited skilled resource

availability, specific needs in different geographies, and diverse skills required for

different phases of smart grid deployment makes smart grid service provision one of

the more complex evaluations they will conduct, and many providers' references are

limited.

� Utilities should consider small specialist firms in their smart grid sourcing decisions,

Page 1 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

particularly if they are considering a resource augmentation model, because these

firms usually have in-depth skills, although the skills are specific to a particular

activity.

Table of Contents

Analysis

1.0 Introduction

2.0 The Purpose of This Research

3.0 Survey Demographics

4.0 Smart Grid Project Governance

5.0 Technology Focus of Smart Grid Programs

6.0 Smart Grid Project Sourcing

6.1 Functional Breakdown of Smart-Grid-Related Activities

6.2 Smart Grid Service Providers

6.3 Smart Grid Business Management Consulting Services

6.4 Smart Grid Demonstration

6.5 Smart Grid Architecture Development

6.6 Smart-Grid-Related Technology Selection and Procurement

6.7 Smart-Grid-Related System Integration Activities

6.8 Smart-Grid-Related Application Development

7.0 Research Methodology

Recommended Reading

List of Figures

Figure 1. Energy Company Primary Focus Area

Figure 2. Did You Submit a Request for Financing a Smart Grid

Initiative Through Government Stimulus Programs?

Figure 3. Who Is Sponsoring the Smart Grid Initiative?

Figure 4. Which Group Is Responsible for Smart Grid Initiative?

Figure 5. Which IT Applications Are Included in Your Smart Grid

Programs?

Figure 6. Which OTs Are (Will Be) Included in Your Smart Grid

Program?

Figure 7. Which Consumer Technologies Are Included in Your Smart

Grid Program?

Figure 8. Which Smart Grid Management Consulting Activities Did You

Complete, Are Currently Involved With or Are Planning During

the Next 12 Months?

Figure 9. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Figure 10. Which Provider Have You Worked With or Plan to Work With

for Assessment of the Business Impact, Benefits and

Impediments?

Figure 11. Which Provider Have You Worked With or Plan to Work With

for Business Case Development?

Figure 12. Which Provider Have You Worked With or Plan to Work With

for Regulatory Treatment and Rate Case Support?

Figure 13. Which Provider Have You Worked With or Plan to Work With

for Funding and/or Grant Advisory Work?

Figure 14. Which Smart Grid Demonstration Activities Did You Complete,

Page 2 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Are Currently Involved in or Planning During the Next 12

Months?

Figure 15. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Figure 16. Which Provider Have You Worked With or Plan to Work With

for Program Management for Smart Grid Demonstration

Activities?

Figure 17. Which Provider Have You Worked With or Plan to Work With

for Development of a Smart Grid Demonstration Project?

Figure 18. Which Provider Have You Worked With or Plan to Work With

for Development of a Smart Grid Technology Lab?

Figure 19. Which Provider Have You Worked With or Plan to Work With

for Smart Grid Project Management?

Figure 20. Which Smart Grid Architecture Development Activities Did You

Complete, Are Currently Involved in or Are Planning During

the Next 12 Months?

Figure 21. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Figure 22. Which Provider Have You Worked With or Plan to Work With

for Developing a Common Requirement Vision Across the

Enterprise?

Figure 23. Which Provider Have You Worked With or Plan to Work With

for Developing a Smart Grid Architectural Framework?

Figure 24. Which Provider Have You Worked With or Plan to Work With

for Developing a Smart Grid Security Framework?

Figure 25. Which Provider Have You Worked With or Plan to Work With

for Developing Smart Grid Architectural Principles?

Figure 26. Which Smart-Grid-Related Technology Procurement Activities

Did You Complete, Are Currently Involved in or Are Planning

to Complete During the Next 12 Months?

Figure 27. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Figure 28. Which Provider Have You Worked With or Plan to Work With

for Requirement Gathering for Smart Grid Technology

Selection?

Figure 29. Which Provider Have You Worked With or Plan to Work With

for RFI/RFP Development for Smart Grid Technology

Selection?

Figure 30. Which Provider Have You Worked With or Plan to Work With

for Technology Product or Service Provider Selection for

Smart Grid Technology Selection?

Figure 31. Which Provider Have You Worked With or Plan to Work With

for Technology Product or Service Provider Contract

Finalization for Smart Grid Technology or Service Selection?

Figure 32. Which Smart Grid System Integration Activities Did You

Complete, Are Currently Involved in or Are Planning to

Complete During the Next 12 Months?

Figure 33. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Figure 34. Which Provider Have You Worked With or Plan to Work With

for Smart-Grid-Related System/Application Interface

Development?

Figure 35. Which Provider Have You Worked With or Plan to Work With

for Smart-Grid-Related System Integration Project

Management?

Figure 36. Which Smart-Grid-Related Development System Activities Did

Page 3 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Analysis

1.0

Introduction

Continuing pressure from policymakers and consumers on energy utilities to address

energy sustainability concerns has resulted in an increasing focus on smart grid

development. A smart grid, or "intelligent grid," is a vision of the new energy delivery

infrastructure that leverages advancements in several technology domains, such as

communications technology, IT, operational technology, energy technology and consumer

technology, to improve system use and resilience while empowering consumers and

addressing environmental concerns (see "How to Make Your Grid Smarter: An Intelligent

Grid Primer").

Realistically, the smart grid concept encompasses nearly every technology involved with

the production, transmission, distribution, measurement and consumption of electricity.

The Gartner Hype Cycle for smart grid technology (see "Hype Cycle for Smart Grid

Technologies, 2010"), which depicts the maturity of technologies that contribute to smart

grid transformation, indicates that most of them are clustered around the Peak of Inflated

Expectations, implying relative immaturity, and consequently high risk.

The flood of stimulus funds in 2009 in the U.S. and other markets, such as Australia — and

the mandated spending pace — are forcing utilities in some cases to make premature

decisions. This could lead them to embark on smart grid initiatives without a clear

understanding of project ownership, expected deliverables, governance, security,

intellectual property considerations, technology maturity and vendor expertise. The

situation is further complicated by uneven treatment of the regulators for smart-grid-

related investment recovery, which adds even more business risk to smart grid

deployment.

Gartner has published research to help clients embark on intelligent grid initiatives while

taking into consideration the associated risks. Even though existing stimulus packages in

some markets make financing less of an issue, we recommend that companies follow the

structured approach outlined in "How to Make Your Grid Smarter: An Intelligent Grid

Primer." To understand the risks associated with smart-grid-related technology selection,

we have for several years published Hype Cycles for smart grid technologies depicting the

maturation and adoption of technologies in the smart grid domain, including IT, operating

technologies (OTs), communication technologies and consumer technologies.

We expect to see positive effects from the government capital infusion on smart grid

technology maturation in the long run. However, stimulus funds did not instantly change

the fact that many smart grid technologies and related service offerings are still immature.

Just as utilities need to be careful about technology selection — considering available

standards, component interoperability, security implications, performance, scalability and

future-proofing to meet upcoming needs — they must also be careful about selecting

vendors that can help them speed up deployment of the smart-grid-related solutions.

The capital infusion in the smart grid space during the economic crisis created a "tornado

alley" phenomenon for some smart-grid-related product vendors (such as those offering

You Complete, Are Currently Involved in or Are Planning to

Complete During the Next 12 Months?

Figure 37. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Figure 38. Which Provider Have You Worked With or Plan to Work With

for Requirement Gathering for Custom Development of a

Smart-Grid-Related Solution?

Figure 39. Which Provider Have You Worked With or Plan to Work With

for Custom Solution Development of a Smart-Grid-Related

Solution?

Figure 40. Which Provider Have You Worked With or Plan to Work With

for Modification of Existing Applications as a Result of Smart

Grid Initiatives?

Page 4 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

AMI and Phasor Measurement Unit [PMU]), as well as for service providers focused on

those products. While this is good for job creation in an ailing economy, it created a vendor

community with widely disparate capabilities — some with little or no domain expertise.

This conspired to make service provider selection even more of an issue in this market

poised for rapid growth. This research should assist our clients in smart grid service

provider selection.

2.0

The Purpose of This Research

In 2Q10, Gartner conducted a survey of energy companies aimed at identifying a level of

smart-grid-related activities, functional focus, selected technologies and governance

structure of the smart grid projects. The survey was sourced thorough LinkedIn. The

survey demographic consisted of 100 energy utility professionals that have declared

themselves "knowledgeable" to "extremely knowledgeable" about smart grid initiatives in

their organizations.

The survey had two goals:

� To assess the general level of smart grid activities, including past, present and

future focus of the energy companies in smart-grid-related programs. We also

wanted to see what type of governance structure utilities use when starting smart

grid programs, what kind of business benefits they are trying to achieve, and which

technologies they consider most important for investments.

This information can be used by energy utility clients to benchmark their programs

and priorities against their peers' initiatives. It can also be used to provide an overall

assessment of the potential sourcing issues that utility companies may face when

addressing certain areas — either because of the high demand for particular skills or

because of the lack of appropriate resources on the market.

� To assess the availability of resources that can help utility companies address

smart-grid-related service needs. We have broken the survey into a number of

distinct activities (from management consulting to legacy application modification)

to identify utilities' affinity toward external sourcing as well as "top-of-the-mind"

providers in different categories.

Given the criticality and growing role of service provider in smart grid programs, utility

companies would do well to understand the factors in choosing a partner with the

experience matched to their needs.

3.0

Survey Demographics

Of the utility professionals surveyed, 88% worked for North American energy utilities

(U.S., 85%, Canada, 3%) followed by 7% Australian and 5% Western European utilities.

The reason for this U.S. centricity is the fact that the sample universe was drawn from

professional social networking site LinkedIn members, which tends to be predominantly

U.S.-based. Consequently, the results of this study are representative of the respondent

base, but not necessarily of the global market as a whole.

Although this gives these results a U.S. flavor, utilities in other geographies can benefit

from findings in U.S. markets, because the level of government investment in the U.S. —

through the U.S. Department of Energy Smart Grid Investment Grant (SGIG) programs —

made the U.S. the most active "smart grid market" in 2009 and 2010.

Nearly half (48%) of those surveyed professionals worked in large organizations with more

than 10,000 employees. These were followed by 20% that worked for utilities with

between 2,500 and 5,000 employees. Companies in the range of 1,000 to 2,500 and 5,000

to 10,000 employees were equally represented (16%) in our survey. Figure 1 illustrates

the distribution of the sample based on the primary focus area of the represented

companies.

Figure 1. Energy Company Primary Focus Area

Page 5 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Of the surveyed utility professionals, 46% indicated that their companies have already

implemented projects related to smart grid initiatives, while 44% were planning to do so

during the next 12 months.

We also found out that less than one-quarter of smart grid initiatives were driven by

regulator-mandated programs. That relatively low percentage in an industry that is heavily

driven by regulatory mandates — particularly for large IT investment programs — indicates

that regulators are trailing with instigating and even approving smart grid programs.

To identify the impact of government capital infusion (stimulus programs) on smart grid

initiatives, we asked companies about their participation in smart-grid-related government

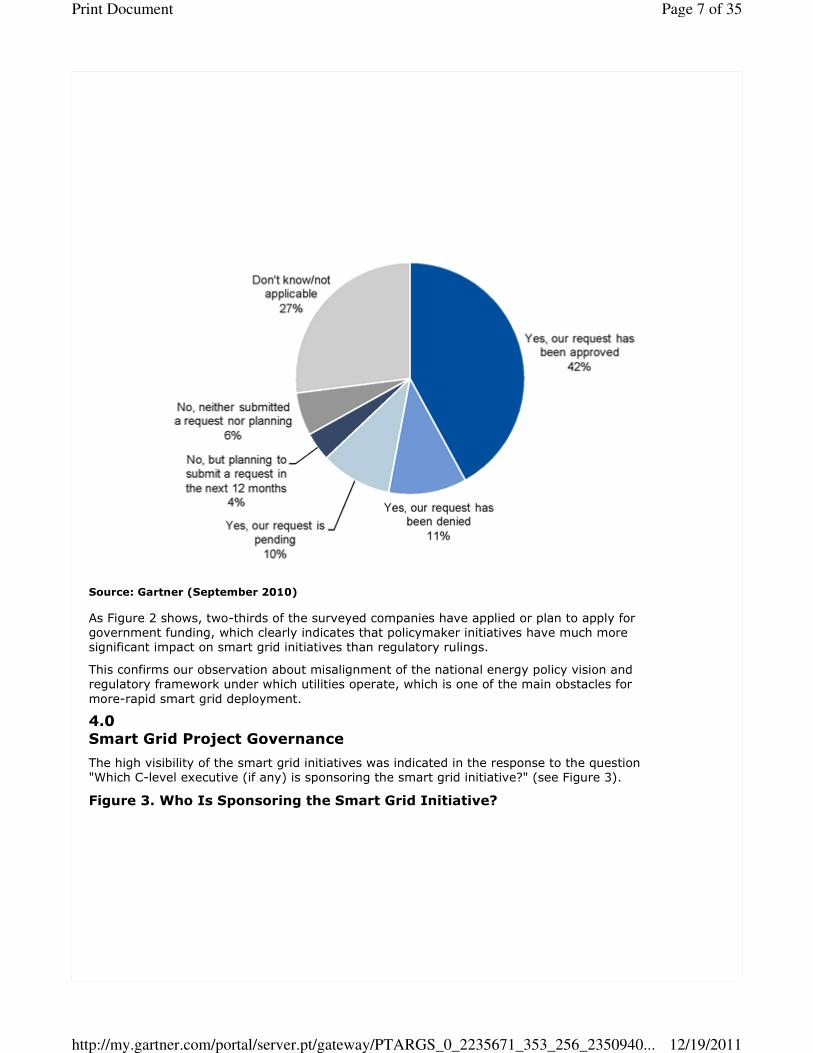

stimulus programs (see Figure 2).

Figure 2. Did You Submit a Request for Financing a Smart Grid Initiative

Through Government Stimulus Programs?

Page 6 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

As Figure 2 shows, two-thirds of the surveyed companies have applied or plan to apply for

government funding, which clearly indicates that policymaker initiatives have much more

significant impact on smart grid initiatives than regulatory rulings.

This confirms our observation about misalignment of the national energy policy vision and

regulatory framework under which utilities operate, which is one of the main obstacles for

more-rapid smart grid deployment.

4.0

Smart Grid Project Governance

The high visibility of the smart grid initiatives was indicated in the response to the question

"Which C-level executive (if any) is sponsoring the smart grid initiative?" (see Figure 3).

Figure 3. Who Is Sponsoring the Smart Grid Initiative?

Page 7 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 3 shows that in more than 80% of cases, a smart grid initiative has C-level

executive sponsorship; in half of those cases, sponsorship comes from the very top.

One indication that utilities have begun approaching smart grid initiatives more holistically

can be seen from the fact that 62% of the surveyed companies are approaching it as a

single, overarching smart grid project that encompasses and coordinates all activities,

compared to less than a fourth of that (24%), which look at it as a number of unrelated

projects.

The similar conclusion can be derived from answers to the question "Which group is (will

be) responsible for smart grid initiatives?" The answers to that question (see Figure 4)

clearly indicate that companies are approaching smart grid initiatives more and more as

enterprisewide transformational activities. Figure 4 also shows that an enterprisewide

steering committee is the dominant model for smart grid program leadership, while

examples of an individual line of business (LOB) — including IT — leading smart grid

initiatives are less common. Where individual LOBs do lead smart grid initiatives, there is

no single dominant LOB.

Figure 4. Which Group Is Responsible for Smart Grid Initiative?

Page 8 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

The enterprisewide approach to smart grid is visible through the fact that almost 80% of

the surveyed companies indicated that they expect smart grid initiatives to address

infrastructure-improvement-related needs as well as tighter customer integration in energy

markets; only 20% are focused on the single benefit (either one of those needs). This

represents the evolution in thinking among utilities. Traditionally, there had been two

distinct sets of programs — one focused on infrastructure improvement (dubbed

distribution automation) and a separate one (usually on the technology feasibility level)

focused on demand response and consumer-service-related benefits (see "Advanced

Metering Infrastructure, Part 1: Business, Regulatory and Technical Considerations").

5.0

Technology Focus of Smart Grid Programs

To gauge utility companies' interest in various smart-grid-related technologies, and to

identify the leading IT, OT and consumer technologies included in active and planned

smart grid programs, we asked three separate questions (see Figure 5, Figure 6 and Figure

7).

Figure 5. Which IT Applications Are Included in Your Smart Grid

Programs?

Page 9 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Not surprisingly, meter data management (MDM) leads the chart as an IT component of

the AMI composite technology. As the more mature component of the AMI (although still

offered in a relatively immature technology market), many companies tend to enter AMI

(smart metering) through an "MDM first" approach. Demand response as a means to

address commodity management concerns and better asset utilization (coupled with time

of use and real-time billing) comes in a close second. Advanced distribution management

(still an "ill-defined" IT application that should enable a majority of the infrastructure-

related benefits) is ranked highest among "engineering" IT applications. That also

corresponds with Gartner observations, based on interaction with our clients and volume of

market activities, which earned advanced distribution management systems (ADMSs) a

position at the Peak of Inflated Expectations in "Hype Cycle for Smart Grid Technologies,

2010."

Figure 6. Which OTs Are (Will Be) Included in Your Smart Grid Program?

Page 10 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

In OT areas, AMI (the two other non-IT components of AMI — meters and

communication), as the cornerstone of smart grid once again, is the expected winner,

mentioned 50% more times than any other competing OT. Intelligent electronic devices

(IEDs) for asset and energy flow monitoring, as well as advanced protection and

restoration devices that address the need for increased reliability through self-healing and

event avoidance in distribution networks, scored high. Synchrophasors (also known as

PMUs), which address similar issues in already somewhat "smart" transmission networks,

also scored high.

Figure 7. Which Consumer Technologies Are Included in Your Smart Grid

Program?

Source: Gartner (September 2010)

Page 11 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

In the consumer technology space, smart thermostats and in-home displays lead the

chart, followed by technologies that enable electric vehicle integration in utility networks,

as well as technologies that address the incorporation of consumer-owned energy

technologies (including microgrids).

6.0

Smart Grid Project Sourcing

To help our clients identify service provider capabilities in smart-grid-related areas (one of

the most frequent inquiries we are getting from our clients these days), we asked

respondents questions regarding which providers they have used or are considering for

different smart-grid-related activities. Their answers — although not comprehensive

enough for us to provide formal vendor positioning in the smart grid service provider

markets — can be used to indicate "top-of-the-mind" providers, as well as those that had

the largest number of engagements in particular smart-grid-related activities. Although the

number of engagements does not necessarily guarantee vendor capability, it can be used

as an indication of the "bench depth" and, potentially, domain expertise and focus.

However, we do advise clients to use this research as a starting point to indicate a list of

potential providers in a particular area, and then perform their own vendor capability

assessments before engaging them in smart-grid-related programs.

6.1

Functional Breakdown of Smart-Grid-Related Activities

According to Gartner research — and contrary to the popular belief or what some vendors

would like you to believe — smart grid is not a single product or a technology. Rather, it is

a collection of technology products and services addressing the need for energy

provisioning transformation offered in a variety of technology markets. Because this is still

an emerging area, most of those markets are immature, which creates increased risk when

procuring technology and vendor services, and creates concern on the user side, regarding

technology as well as vendor selection.

Although we advocate an enterprisewide approach to smart grid, smart-grid-related

activities can be broken into several distinct areas (specific initiatives). We have found

that, with the exception of a handful of leading system integrators (SIs) in the utility

space, most vendors tend to focus on just a few areas that best match their existing skill

sets. To provide a functional breakdown and consequent functional capability assessment

of service providers, Gartner has defined the six classes of services against which user

activities and vendors capabilities were evaluated in this smart grid survey:

� Smart grid business management consulting services

� Smart grid demonstration projects

� Smart grid architecture development

� Smart grid technology selection and procurement

� Smart grid system integration services

� Smart-grid-related development services

To address our clients' overwhelming focus on AMI deployment, companion research will

include results of the survey, which will provide deeper insights into AMI and MDM

initiatives.

6.2

Smart Grid Service Providers

The sample of service providers whose involvement in smart-grid-related activities we

assessed in this end-user survey was developed based on Gartner's smart grid vendor

survey performed in 1Q10, in which we prequalified vendors that offer services and

activities in smart grid areas, excluding vendors who offer smart-grid-related services as

an extension of their products. Although driven by the lure of the "smart grid gold rush," it

is hard these days to find a technology provider that does not offer (or wishes to offer)

smart-grid-related products or services, we have limited this list to 26 vendors that have

not only indicated, but demonstrated, capabilities at least in some of the smart-grid-

related service areas in one or more geographies.

Page 12 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

While there have been a number of mergers and acquisitions among service providers

(indicated with an *), we decided to keep acquired companies as distinct entities in this

survey. Most of the acquired entities still operate as separate units under their original

brands. The new owners have not done full product and service integration, and

harmonization, so they are known to users under the original names. The vendors are:

� Atos Origin

� Accenture

� Black & Veatch

� Brattle Group

� Bridge Energy Group

� Bridge Strategy Group

� Capgemini

� CSC

� Enspiria* (acquired by Black & Veatch)

� HP/EDS

� IBM

� Infosys

� Kema

� Lockheed Martin

� Logica

� Plexus Research* (Plexus Research/RW; acquired by R.W. Beck)

� PricewaterhouseCoopers (PwC)

� Quanta Technology

� R.W. Beck* (acquired by SAIC)

� SAIC

� Siemens IS

� Structure Group

� Tieto

� T-Systems

� Vertex

� Wipro Technologies (Wipro)

Note that we have intentionally excluded vendors that offer smart-grid-related services (in

particular system integration) associated with their products.

6.3

Smart Grid Business Management Consulting Services

Vendors claiming to provide smart grid products or solutions offer, at best, a component

technology that can help achieve some smart grid benefits (see "Hype Cycle for Smart Grid

Technologies, 2010" for a list of relevant technologies). We realize that many energy

utilities, rather than looking for a supplier of smart grid products or solutions, look instead

for a partner that can help them articulate the smart grid vision or eventually manage a

smart grid program. Consequently, vendors that offer management consulting and

technology strategy consulting services — with significant energy utility expertise — are

the ones we see most often engaged early on in smart grid initiatives.

The smart grid has ramifications for all four major business process life cycles in utilities

(commodity, asset, customer and revenue). Consequently, energy companies must

establish clear intelligent grid project governance, starting from top-level executive

sponsorship and involving stakeholders from different business units that can benefit or be

affected by the smart grid initiatives.

Joint ownership of the intelligent grid ensures that multiple aspects and implications across

the enterprise are considered, and it enables achieving a coherent vision. However,

reaching consensus in such a collaborative environment may impede the decision-making

Page 13 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

process. For that reason, many companies retain external vendors to help the enterprise

achieve the coherent "joint requirement vision" and define common strategy.

During our initial vendor survey, a number of service providers indicated their capabilities

to support utility companies in assessing business and regulatory aspects of smart grid

initiatives. This is also understandable, since management consulting activities tend to be

the most profitable, and are the types of engagement that help system integrators

establish good rapport with C-level executives, which, in turn, helps business development

and seeds subsequent smart-grid-related engagements. They are also the types of

activities that utility companies exercise first to help them gain better understanding of the

business benefits, regulatory repercussions and, financial implications, in particular in the

case of government funding programs.

Figure 8 indicates where the companies in the survey are in regard to management

consulting activities. Figure 9, Figure 10, Figure 11, Figure 12 and Figure 13 indicate which

management consulting activities they sourced (or plan to source) for external help, as

well as what companies they used, are using or plan to use to obtain a certain type of

management consulting services in a smart grid area.

Figure 8. Which Smart Grid Management Consulting Activities Did You

Complete, Are Currently Involved With or Are Planning During the Next

12 Months?

Source: Gartner (September 2010)

Figure 9. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Page 14 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 10. Which Provider Have You Worked With or Plan to Work With

for Assessment of the Business Impact, Benefits and Impediments?

Source: Gartner (September 2010)

Figure 11. Which Provider Have You Worked With or Plan to Work With

for Business Case Development?

Page 15 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 12. Which Provider Have You Worked With or Plan to Work With

for Regulatory Treatment and Rate Case Support?

Source: Gartner (September 2010)

Figure 13. Which Provider Have You Worked With or Plan to Work With

for Funding and/or Grant Advisory Work?

Page 16 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

IBM, Accenture, Black & Veatch and Capgemini have consistently shown up as the top five

companies utilities use or plan to use in smart grid management consulting activities. IBM

in particular has been identified by surveyed utilities as the "top-of-mind company" in all

the smart grid management consulting activities.

6.4

Smart Grid Demonstration

As an initial step of smart grid deployments, many utility companies tend to start with

demonstration labs that help educate their own employees, customers and regulators

about smart grid concepts, implications and benefits. They start rolling smart grid

initiatives in a form of several smaller projects (quick hits) to quickly demonstrate smart

grid concepts within each organizational unit. With that approach, utilities can develop

momentum and buy-in internally for the smart grid concept and demonstrate tangible

investment opportunities. In addition, many utilities use such a facility as a laboratory to

test technology feasibility, interoperability, scalability, or customer adoption. Because

those facilities usually need special skills to develop demonstration programs, use cases,

and technology pilots, and those tend to be temporary assignments, utilities frequently

seek external help in developing and staffing smart grid demonstration projects.

Figure 14 depicts smart grid demonstration activities that companies completed, are

currently involved with or plan to get involved in during the next 12 months. Figures 15,

Figure 16, Figure 17, Figure 18 and Figure 19 indicate which smart grid demonstration

activities utilities have sourced (or are planning to source) external help, as well as what

companies they used, are using or planning to use most often to provide a certain type of

smart grid demonstration activities.

Figure 14. Which Smart Grid Demonstration Activities Did You Complete,

Are Currently Involved in or Planning During the Next 12 Months?

Page 17 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 15. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Source: Gartner (September 2010)

Figure 16. Which Provider Have You Worked With or Plan to Work With

for Program Management for Smart Grid Demonstration Activities?

Page 18 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 17. Which Provider Have You Worked With or Plan to Work With

for Development of a Smart Grid Demonstration Project?

Source: Gartner (September 2010)

Figure 18. Which Provider Have You Worked With or Plan to Work With

for Development of a Smart Grid Technology Lab?

Page 19 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 19. Which Provider Have You Worked With or Plan to Work With

for Smart Grid Project Management?

Source: Gartner (September 2010)

IBM and Black & Veatch are consistently listed in the top five vendors in this category, with

IBM winning in all the smart grid demonstration project categories.

6.5

Smart Grid Architecture Development

An intelligent grid initiative should be approached as an enterprise architecture exercise

that must result in achieving a coherent "common requirements vision" defining key

architectural principles (such as a common-based communication backbone or providing

Page 20 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

an Internet Protocol [IP] link into customer homes). In addition, a smart grid initiative

should provide a smart grid "master plan" and eventually create an implementation road

map.

The enterprise architecture approach (which IT should actively participate in, and perhaps

lead but not own) will guide clients on a journey to the end state through a number of

technology projects (steppingstones) that will address key business needs. These business

needs will address requirements resulting from increased consumer energy awareness, the

energy market transformation, and address energy sustainability and climate concerns.

At Gartner, we advise our clients to approach smart grid initiatives as enterprisewide

endeavors. As such, we advocate use of the enterprise architecture framework in

developing smart grid initiatives. In this section of surveys, we wanted to assess what type

of architectural activities utilities are currently involved in or plan to pursue (as depicted in

Figure 20). Figure 21, Figure 22, Figure 23, Figure 24 and Figure 25 indicate which smart

grid architecture development activities they sourced (or are planning to source) to

external help, as well as what companies they most often used, are currently using or

planning to use during the next 12 months to provide a certain type of smart grid

architecture development activities.

Figure 20. Which Smart Grid Architecture Development Activities Did You

Complete, Are Currently Involved in or Are Planning During the Next 12

Months?

Source: Gartner (September 2010)

Figure 21. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Page 21 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 22. Which Provider Have You Worked With or Plan to Work With

for Developing a Common Requirement Vision Across the Enterprise?

Source: Gartner (September 2010)

Figure 23. Which Provider Have You Worked With or Plan to Work With

for Developing a Smart Grid Architectural Framework?

Page 22 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 24. Which Provider Have You Worked With or Plan to Work With

for Developing a Smart Grid Security Framework?

Source: Gartner (September 2010)

Figure 25. Which Provider Have You Worked With or Plan to Work With

for Developing Smart Grid Architectural Principles?

Page 23 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

IBM and Accenture were most frequently quoted in the top five providers of choice in

addressing smart grid architectural needs, with IBM once again leading as the top-of-the-

mind provider of architectural service in the smart grid area.

6.6

Smart-Grid-Related Technology Selection and Procurement

Following Smart Grid Investment Grant (SGIG) program awards, many utilities in the U.S.

have made the decision to proceed with procuring some smart-grid-related technologies.

AMI and, in particular, MDM from the consumer-related side as well as DMS are technology

areas in which we have seen a lot of activity — particularly in the North American and

Australia/New Zealand markets. Consequently, some vendors have begun offering

specialized procurement services in those markets.

We have also seen some cases of large vendors sometimes preferring to stay out of the

procurement business to avoid conflict of interest with more-lucrative parts of their

businesses, such as management consulting services (which provide higher margins and

establish tighter relationships with C-level executives) or system integration services

(which tend to a employ lot of resources). That also creates opportunities for specialized

vendors — such as Enspiria (now owned by Black & Veatch) or Plexus research (now

owned by R.W. Beck/SAIC) — that have created specialized offerings such as AMI RFP

definition or AMI technology selection.

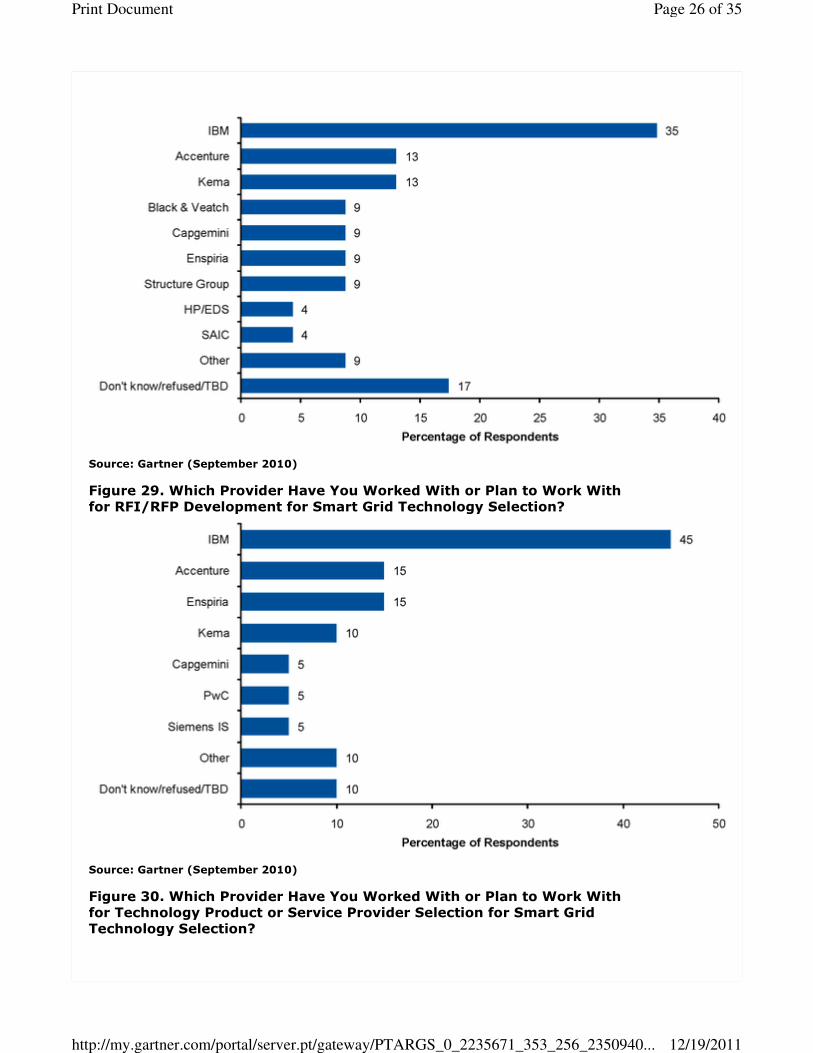

Figure 26 shows the procurement activities that utilities are involved with or plan to get

involved with. Figure 27, Figure 28, Figure 29, Figure 30 and Figure 31 indicate for which

smart grid procurement services utilities sourced (or plan to source) externally, as well as

which companies they used, are currently using or planning to use during the next 12

months to obtain certain types of smart-grid-related technology procurement activities.

Figure 26. Which Smart-Grid-Related Technology Procurement Activities

Did You Complete, Are Currently Involved in or Are Planning to Complete

During the Next 12 Months?

Page 24 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 27. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Source: Gartner (September 2010)

Figure 28. Which Provider Have You Worked With or Plan to Work With

for Requirement Gathering for Smart Grid Technology Selection?

Page 25 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 29. Which Provider Have You Worked With or Plan to Work With

for RFI/RFP Development for Smart Grid Technology Selection?

Source: Gartner (September 2010)

Figure 30. Which Provider Have You Worked With or Plan to Work With

for Technology Product or Service Provider Selection for Smart Grid

Technology Selection?

Page 26 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 31. Which Provider Have You Worked With or Plan to Work With

for Technology Product or Service Provider Contract Finalization for

Smart Grid Technology or Service Selection?

Source: Gartner (September 2010)

In the procurement services — in addition to the "usual suspects" such as IBM, Accenture,

Kema and Black & Veatch — we have also noticed Enspiria (now owned by Black & Veatch)

coming up third in RFI/RFP development services.

6.7

Smart-Grid-Related System Integration Activities

In the smart grid system integration area we have identified just two activities —

Page 27 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

system/application interface development and system integration project management.

Although in most cases, utilities tend to select one vendor to manage the project and

develop interfaces, in some instances, utilities tend to keep system integration project

management in-house, while interface development is sourced externally.

In this set of questions we asked utilities where they are with system integration activities,

which ones have they completed, are currently involved with or plan to complete during

the next 12 months. The answers are summarized in Figure 32, which indicates that most

utilities are currently focused on system integration activities. Figure 33 shows for which of

those activities utilities are using or plan to use external help, while Figure 34 and Figure

35 show which vendors they use (or plan to use) most commonly.

Figure 32. Which Smart Grid System Integration Activities Did You

Complete, Are Currently Involved in or Are Planning to Complete During

the Next 12 Months?

Source: Gartner (September 2010)

Figure 33. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Page 28 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 34. Which Provider Have You Worked With or Plan to Work With

for Smart-Grid-Related System/Application Interface Development?

Source: Gartner (September 2010)

Figure 35. Which Provider Have You Worked With or Plan to Work With

for Smart-Grid-Related System Integration Project Management?

Page 29 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

6.8

Smart-Grid-Related Application Development

In addition to selecting off-the-shelf products, many of the smart-grid-related initiatives

require custom development of the new solutions for which vendors do not yet offer

products. In some cases, smart grid programs may require modification of an existing

application to accommodate new requirements resulting from smart grid initiatives, such

as introduction of the "time of use" billing into a customer information system (CIS)

product to enable rolling out economic demand response programs. Both of these will

require software development and may require utilities to outsource the entire activity to

an external vendor or use resources from the sourcing vendor in a resource augmentation

mode.

Figure 36 shows where utilities stand regarding smart-grid-related solution development

and legacy application modification at this point (have they done it, currently involved in it,

or plan to do it). Figure 37 indicates how likely they are to seek external help for those

activities. Figure 38, Figure 39 and Figure 40 indicates the vendors they currently use or

plan to use to offer those services.

Figure 36. Which Smart-Grid-Related Development System Activities Did

You Complete, Are Currently Involved in or Are Planning to Complete

During the Next 12 Months?

Page 30 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 37. For Which of Those Activities Are You Using or Planning to Use

External Help During the Next 12 Months?

Source: Gartner (September 2010)

Figure 38. Which Provider Have You Worked With or Plan to Work With

for Requirement Gathering for Custom Development of a Smart-Grid-

Related Solution?

Page 31 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Figure 39. Which Provider Have You Worked With or Plan to Work With

for Custom Solution Development of a Smart-Grid-Related Solution?

Source: Gartner (September 2010)

Figure 40. Which Provider Have You Worked With or Plan to Work With

for Modification of Existing Applications as a Result of Smart Grid

Initiatives?

Page 32 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Source: Gartner (September 2010)

Large system integrators with significant practices in the energy and utility sectors once

again dominate top of mind for utilities for development activities, although we hear of

concerns from our clients regarding higher fees charged by Tier 1 service providers with

deep domain expertise.

7.0

Research Methodology

In 2Q10, Gartner surveyed 100 energy companies regarding their current and planned

smart grid initiatives. The survey was conducted as on online interview methodology. The

sample universe was drawn from the global membership of professional social site

LinkedIn to find utility employees identified as knowledgeable, very knowledgeable and

extremely knowledgeable about the smart-grid-related activities of their organizations.

The respondent organizations have 1,000 or more employees and have currently

implemented or are planning to implement during the next 12 months projects related to

smart grid. The questionnaire was developed collaboratively by a team of Gartner analysts

who follow those markets, and was reviewed and tested by Gartner's Research Data and

Analytics (RDA) team. The results of this study are representative of the respondent base,

but not necessarily of the market as a whole.

Recommended Reading

"Hype Cycle for Smart Grid Technologies, 2010"

"AMI Is the Clear Winner of the U.S. Smart Grid Investment Grant Program Competition"

"How to Make Your Grid Smarter: An Intelligent Grid Primer"

"Advanced Metering Infrastructure, Part 1: Business, Regulatory and Technical

Considerations"

© 2010 Gartner, Inc. and/or its Affiliates. All Rights Reserved. Reproduction and distribution of this publication

in any form without prior written permission is forbidden. The information contained herein has been obtained

from sources believed to be reliable. Gartner disclaims all warranties as to the accuracy, completeness or

adequacy of such information. Although Gartner's research may discuss legal issues related to the information

technology business, Gartner does not provide legal advice or services and its research should not be

Page 33 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

construed or used as such. Gartner shall have no liability for errors, omissions or inadequacies in the

information contained herein or for interpretations thereof. The opinions expressed herein are subject to

change without notice.

Page 34 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

Page 35 of 35Print Document

12/19/2011http://my.gartner.com/portal/server.pt/gateway/PTARGS_0_2235671_353_256_2350940...

![[Smart Grid Market Research] Smart Grid Index: November 2012 - Zpryme Smart Grid Insights](https://img.dokumen.tips/doc/110x75/541402018d7f728a698b47a5/smart-grid-market-research-smart-grid-index-november-2012-zpryme-smart-grid-insights.jpg)

![Cyber security in the Smart Grid: Survey and …ecee.colorado.edu/~ekeller/classes/fall2014_advsec/...Grid design [12,13]. Since the research on cyber security for the Smart Grid is](https://img.dokumen.tips/doc/110x75/5f76f61bea3afc7c365913d5/cyber-security-in-the-smart-grid-survey-and-ecee-ekellerclassesfall2014advsec.jpg)

![[Smart Grid Research & Survey] The New Energy Consumer by Zpryme, Sponsored by Itron](https://img.dokumen.tips/doc/110x75/5500e2434a7959ac638b48c1/smart-grid-research-survey-the-new-energy-consumer-by-zpryme-sponsored-by-itron.jpg)

![[Smart Grid Market Research] The Optimized Grid - Zpryme Smart Grid Insights](https://img.dokumen.tips/doc/110x75/541402188d7f7294698b47d2/smart-grid-market-research-the-optimized-grid-zpryme-smart-grid-insights.jpg)